business risks facing the issues monitor mining industry€¦ · these risks and kpmg’s mining...

TRANSCRIPT

KPMG INTERNATIONAL

Issues MonitorSharing Knowledge on topical issues in the

Automotive Industry

October 2010, Volume Seven

kpmg.com

Business risks facing the

Mining IndustryDecember 2011

kpmg.ca

2 | Business risks facing the Mining Industry

IntroductionIt’s a perplexing time to be in the mining industry. After a severe global financial crisis dashed commodities prices and swept aside a six-year boom, a promising two-year recovery gave the industry reason to hope. But the global economy has relapsed into another less severe downturn in 2011, staunching global demand and forcing down commodities prices once again.

This turn of events has the industry focusing on risk all over again. Many industry leaders believe that this downturn is a crisis of confidence more than a crisis of fundamentals. Economics and commodity prices may be beyond the control of the industry, but a lot can be accomplished through good management as we have witnessed since the first economic crisis.

The question is, what are the major risks that management is likely to face in 2012? To find out, KPMG surveyed mining industry executives at our Annual Mining Executive Forum and asked them to prioritize the three biggest risks they would be facing in 2012:

Based on the responses this year, the five risks most often identified by industry executives are:

Business Risk% who ranked it as a major risk for 2012

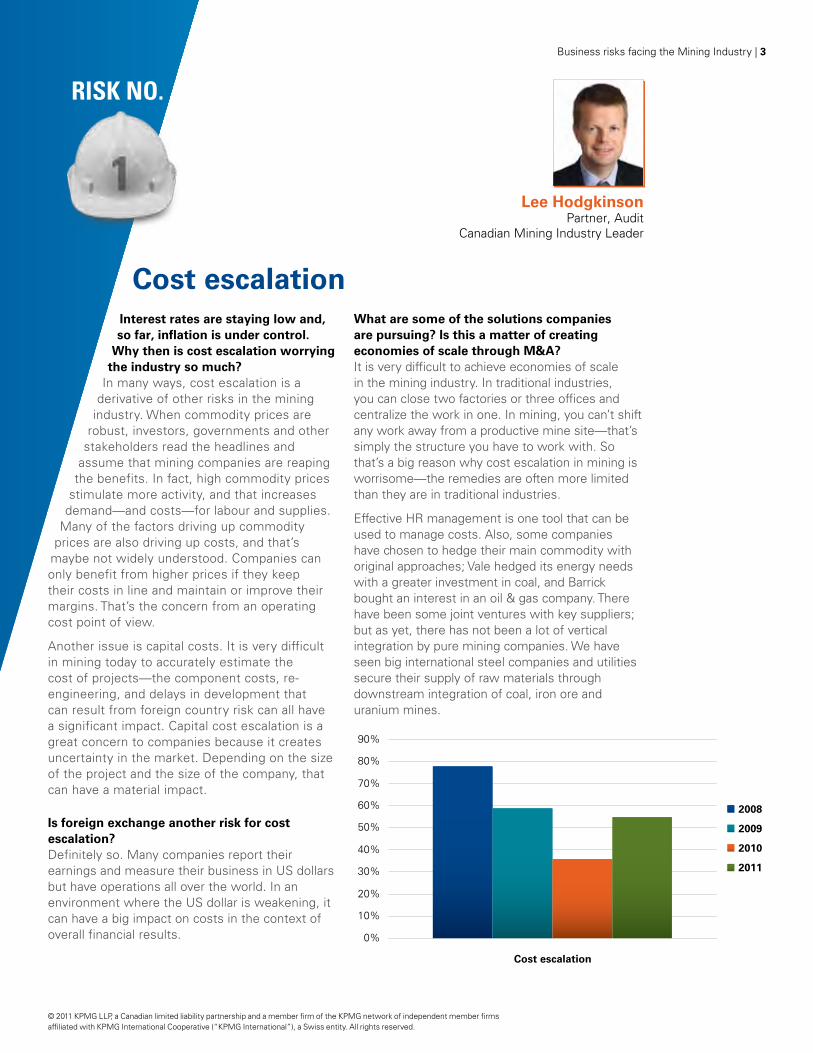

Cost escalation 55

Government involvement in the industry 40

Access to new projects 38

Ability to raise capital 35

Labour shortages 34

In the next few pages, we will show you the four-year survey trends for each of these risks and KPMG’s mining professionals will share their insights for each category, and discuss some solutions that are being pursued across the industry.

Wayne Jansen Partner & Global Head of Mining

© 2011 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Interest rates are staying low and, so far, inflation is under control.

Why then is cost escalation worrying the industry so much?

In many ways, cost escalation is a derivative of other risks in the mining

industry. When commodity prices are robust, investors, governments and other

stakeholders read the headlines and assume that mining companies are reaping

the benefits. In fact, high commodity prices stimulate more activity, and that increases

demand—and costs—for labour and supplies. Many of the factors driving up commodity

prices are also driving up costs, and that’s maybe not widely understood. Companies can only benefit from higher prices if they keep their costs in line and maintain or improve their margins. That’s the concern from an operating cost point of view.

Another issue is capital costs. It is very difficult in mining today to accurately estimate the cost of projects—the component costs, re-engineering, and delays in development that can result from foreign country risk can all have a significant impact. Capital cost escalation is a great concern to companies because it creates uncertainty in the market. Depending on the size of the project and the size of the company, that can have a material impact.

Is foreign exchange another risk for cost escalation?Definitely so. Many companies report their earnings and measure their business in US dollars but have operations all over the world. In an environment where the US dollar is weakening, it can have a big impact on costs in the context of overall financial results.

What are some of the solutions companies are pursuing? Is this a matter of creating economies of scale through M&A?It is very difficult to achieve economies of scale in the mining industry. In traditional industries, you can close two factories or three offices and centralize the work in one. In mining, you can’t shift any work away from a productive mine site—that’s simply the structure you have to work with. So that’s a big reason why cost escalation in mining is worrisome—the remedies are often more limited than they are in traditional industries.

Effective HR management is one tool that can be used to manage costs. Also, some companies have chosen to hedge their main commodity with original approaches; Vale hedged its energy needs with a greater investment in coal, and Barrick bought an interest in an oil & gas company. There have been some joint ventures with key suppliers; but as yet, there has not been a lot of vertical integration by pure mining companies. We have seen big international steel companies and utilities secure their supply of raw materials through downstream integration of coal, iron ore and uranium mines.

Cost escalation

Lee HodgkinsonPartner, Audit

Canadian Mining Industry Leader

Business risks facing the Mining Industry | 3

0%

10%

20%

30%

40%

50%

90%

80%

70%

60% 2008

2009

2010

2011

Cost escalation

Risk No.

© 2011 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

4 | Business risks facing the Mining Industry

Many governments around the world are facing tough challenges as a result of the current economic environment. With all the problems they are dealing with, are you surprised to see the level of government interference directed at the mining industry? In many ways, it’s not a surprising reaction at all for governments to engage with the mining industry in times of economic crisis. On one hand, ballooning deficits create strong incentive for governments to raise tax revenues by increasing or introducing new royalties and income taxes. With the current high metals prices and the large cash balances accumulated by some mining companies today, it’s easy to see why the government believes the mining industry has extra money it can part with. On the other hand, high unemployment means they also want to encourage mine development because of the jobs and economic growth that mining creates.

The research patterns from the Mining Executive Forum show a correlation between economic uncertainty and concern about government

involvement. In 2008, 2009 and 2011, years that involved economic uncertainty, executives ranked this a higher risk. In 2010, when the global economy seemed to be back on track after almost two years of economic recovery, this issue shrank to its lowest level.

You also need to consider that governments are always looking to get re-elected. There are many non-economic factors that play into government policy, such as environmental protection, public health and safety, energy and water consumption, rights of indigenous peoples, exploitation of developing countries, and so on. Because of the risks and hazards inherent in the mining industry, it is an easy target for government regulation that can restrict economic growth. There’s also the fact that mining brings up feelings of nationalism everywhere, and people don’t like to feel they’re giving their country’s resources away to foreigners. A good example of this is the Canadian government’s rejection of the BHP bid for Potash Corp.

Government involvement in the industry

Scott Jeffery Partner, Tax

Canadian Mining Industry Group

0%

10%

20%

30%

40%

50%

60%

Government involvement in industry

2008

2009

2010

2011

Risk No.

© 2011 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Business risks facing the Mining Industry | 5

Another negative kind of government interference can be found in some developing countries in the form of bribes and corruption, inconsistent permitting and mineral property expropriation, and unpredictable application of the law, among other things.

Does government involvement always take the form of unwanted interference?Not always – it can sometimes be very beneficial. Tax incentives and other government programs encourage investment and sustainable job creation over the long-term. Government-led programs designed to organize and store geological data can lead to more efficient and effective exploration programs. Investment by government in remote areas can also help build the transportation and energy infrastructure that mining needs. Unfortunately, these types of incentives and programs are more common in jurisdictions with mature mining industries typically associated with developed countries. We have yet to see a lot of developing countries invest in the mining industry to the same extent, but we hope it’s just a matter of time before they realize the potential long-term benefits.

An increasing form of government involvement in mining is sovereign capital. Is anyone worried about that as a risk?Without a doubt, investment backed by sovereign capital causes concern to some stakeholders, especially as the size and influence of sovereign wealth funds (SWFs) continues to grow. Some of these concerns are valid.

For one thing, there is the concern that sovereign capital introduces an artificial element to the market. Before sovereign capital, decisions and actions of mining companies were based

largely on market demand and other business criteria that focused on maximizing shareholder value. Now there is a perceived risk that other agendas can factor into decisions made by mining companies backed by sovereign capital, influenced more by politics than by market principles. This concern is further compounded by the lack of transparency with some SWFs, particularly those in non-democratic countries.

However, sovereign capital is not all bad. The emergence of sovereign capital over the past decade has increased the level of competition for resources and raw materials, which should lead to more efficient and effective pricing. Recent prices in M&A deals and commodity prices in general have been higher than ever before, but I don’t think you can isolate the political influences of sovereign capital as the reason why. Competition is generally stiffer because there aren’t as many good projects available and there more market participants. Sovereign capital also means a new source of financing for the mining industry, which is absolutely critical at a time of escalating capital costs and apprehensive capital markets.

As I see it, there are two main risks to the mining industry stemming from sovereign capital. The first is that existing mining industry participants don’t adapt to the new reality. Sovereign capital is driving a lot of investment in the mining industry today and mining companies need to compete – they can’t afford to sit on the sidelines. The second is government overreaction. The easy government response to a perceived sovereign capital threat is to establish protectionist measures to protect strategically important assets. Over the long term, such measures will hurt the mining industry and should only be exercised in the most extreme circumstances.

© 2011 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

6 | Business risks facing the Mining Industry

Why is access to new projects restricted?Access to a new project is not necessarily difficult, but access to the “right” new project is certainly more challenging. These projects are considered “best in class.” There are fewer of them, and competition for them is becoming more intense.

What is limiting the number of these desirable projects?The new projects in resource-rich areas of the world are more remote than ever before. There are many unknowns associated with the legal, regulatory and cultural environments. Companies aren’t going to spend the dollars it takes to develop a remote project with energy, transportation, labour training, and so on, unless it’s a high quality long-life asset. The money it takes to develop a project is exponentially higher than it was even a few decades ago, and the ability to accurately estimate the costs and timing associated with the project is difficult at best.

What approaches are companies taking to compete for new projects?Companies are spending more time, money and effort on exploration and on due diligence for the exploration projects of juniors. If larger companies believe they have found a property with potential, they will propose a joint venture with the junior or otherwise move on it. Companies are less inclined to take a wait-and-see attitude with a project they like, even if it’s an earlier stage project. With commodity prices high, riskier projects are being pursued and developed at a much faster pace.

Senior mining companies are doing some grassroots exploration, but they have a significant reliance on junior exploration and development companies. It’s a very different competitive environment. Where we used to have juniors teaming up with juniors, we now have majors wading in. There is increased competition for high quality projects coming on stream, and the right price will get you the deal.

Sheri Pearce Partner, Audit

US Mining Industry Group

Access to new projects

0%

10%

20%

30%

40%

50%

60%

Access to new projects

2008

2009

2010

2011

Risk No.

© 2011 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Business risks facing the Mining Industry | 7

Isn’t it in the industry’s best interests for long-term commodity prices to control the development of the supply side?It’s not that easy. Higher commodity prices do not always equate with higher share prices for mining companies. Share price value comes from future mining development and potential. In fact, when commodity prices are higher, investors expect more. Investors see companies generating significant cash flow and they want to know, “What are you going to do with it? What comes next?”

Are there any regions of the world, or particular metals or minerals, where access to projects is particularly competitive?Projects can be sought after anywhere in the world, but there are some categories that are particularly competitive. One category is rare earth minerals. They are a group of the most abundant minerals on earth, but they have to be found in high concentrations to be economically mineable, so there are very few projects. China has the largest number of economical projects, but exports are being restricted due to the high demand for these resources within China.

Precious metal and base metal projects are highly sought after, again, because of the high commodity prices right now. The higher prices are enabling companies to pursue projects in more remote areas of the world, as they are willing to assume the additional risks and costs associated with these mines.

© 2011 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

8 | Business risks facing the Mining Industry

We’ve been hearing a lot lately about strong balance sheets in the mining industry. Should mining executives still be worried about their ability to raise capital?The research from the Mining Executive Forum shows a steady recovery in the confidence to finance, from a fairly shaky level in 2008, as could be expected, to a much lower level of concern in 2011. However, financing conditions in most markets have continued to deteriorate since the latest survey was done early this fall. Markets have not shut down, but they are more challenging than they have been. If conditions don’t improve, I would expect that the ability to raise capital will rise to be among the very top risks of 2012.

Is this an across-the-board problem that affects juniors and seniors alike?Absolutely not. The reports of strong balance sheets are coming from the major producing companies, many of which have significant cash available to pay dividends, repurchase shares and invest in growth. They don’t need additional equity

capital, because they have excellent cash flow from operations. They are also well positioned to issue bonds or borrow from the banks, though credit markets have tightened.

Juniors are a different story. The juniors rarely have access to debt capital, even in stronger markets. Their stocks are down, and it is uncertain whether their projects will be interesting to senior companies that could help them out financially. Issuing shares right now is not a viable or attractive option. What many are doing right now is slowing things down—conserving cash while trying to maintain some progress on their projects.

Is there any role for private equity in the current situation?Yes, but a small role. Private equity usually takes the form of venture capital when it comes to mining, because the risk profile of this industry is not ideal for leverage financing. Private funds may be one place to turn for a select group of juniors with quality projects.

Brian ImriePartner, Corporate Finance Global Head, Mining M&A

Ability to raise capital

0%

10%

20%

30%

40%

50%

60%

Ability to raise capital

2008

2009

2010

2011

Risk No.

© 2011 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Business risks facing the Mining Industry | 9

What about sovereign capital? Is that being considered as an option, or are there concerns about foreign ownership?From a corporate point of view, concerns about foreign control are limited, particularly if a company has a narrow range of alternatives to obtain capital. Many state-owned enterprises (SOE) are currently in acquisition mode, like the Chinese SOEs. Government agencies like China Investment Corp (CIC) and Kores are active, and the export development banks of consuming countries represent an important source of project financing.

Does the current situation have any implications for the M&A market?We have seen levels of activity start to slow down in Canada, particularly in the third quarter. Big decisions are difficult right now, because it is uncertain in the short term whether we’re headed into another major global recession, or back toward recovery. We do have majors with the cash to make acquisitions and/or strategic investments. At the same time we have a challenging environment for the juniors. This dynamic should encourage a rebound in M&A activity when the overall economic picture becomes clearer. In the meantime, we are already seeing a resurgence in unsolicited or hostile bid activity, indicating a disconnect between the expectations of buyers and sellers.

© 2011 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

10 | Business risks facing the Mining Industry

Why is labour so hard to find at a time of high unemployment?

While that is generally true, you might say that the mining industry has had the opposite experience. Demand for mined resources has been spiking as Asia develops its infrastructure. Although it seems like an odd dynamic in our current economy, mining companies around the world have been wrestling with replenishing an aging workforce since commodity prices initially started to rise. Mining employees need quite a bit of training at all levels, in just about every job type. It’s not as easy as just pulling people off the street and putting them to work as electricians, safety specialists, or haul truck drivers, just to name a few positions.

What is the root of the problem?

Mining used to replenish its workforce from within, and it was not uncommon to find generation upon generation that worked in the industry. In the ‘80s and ‘90s, mining literally skipped over a whole generation in some places as mines became

more efficient and only maintained rather than increased production. As a result, the link between generations was broken, so now a new generation needs to be convinced that mining is a terrific industry with good career opportunities.

Does the shortage affect all categories of labour, from mine workers to managers and professionals?

Yes it does, and all for different reasons. Sometimes it’s the inability to find and or train local residents as mine workers in developing countries. Sometimes it’s the remote nature of today’s mining projects, and the unwillingness of people to be away from their families for months at a time.

Sometimes it’s the scarcity of education programs for mining professionals at universities and colleges. For example, Australia may not be able to complete half of the mining development projects it has started because the country does not have enough qualified, trained mine workers.

Roy HinkamperPartner, Advisory

US Mining Industry Leader

Labour shortages

0%

10%

20%

30%

40%

50%

60%

70%

80%

Labour shortages

2008

2009

2010

2011

Risk No.

© 2011 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Business risks facing the Mining Industry | 11

Some industries and professions have benefited from an influx of women. What about mining?

Mining still has a mostly male workforce. Every mining company I know has a diversity program that is trying to broaden the demographics of the employee base, from executives and office personnel through to the mine sites. At several companies, women hold C-level positions at head offices or sit on the board. Women often work in the offices at mine sites, but it’s not as common for them to be part of the mine operations. Women do drive heavy equipment at open pit mines, or work as geologists, environmental engineers, or in other mining roles, but the percentage of women is very low when compared to the workforce as a whole. I’ve spoken with many mine general managers who have said they’d love to have more people working at the mine regardless of gender. If they can help get ore or mineral out of the ground, they’d hire them.

What are the solutions to this problem?

Mining has had a good run for a decade or so. With growth comes opportunity, and with opportunity comes interest. That’s part of it.

The industry is also starting to generate awareness and create some excitement around mining as a job option. Mining has to fight off an old reputation as a very tough, dangerous, low-tech industry. We’ve got to keep engaging post-secondary institutions with partnerships, and specialized mining education programs. The world has had mining for a long time, and will continue to need it. Mining is an essential industry that provides the building blocks for every industry, including computers, solar energy, and many others. There’s a lot of innovation that depends on mining, and a lot of innovation is going on in the mining industry. We’ve got to keep getting the word out.

© 2011 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Contact us

Wayne Jansen Global Head of Mining KPMG in South Africa T: +27 11 647 7201 E: [email protected]

Helen Cook KPMG in Australia T: +61 8 9263 7342 E: [email protected]

Andre Castello Branco KPMG in Brazil T: +55 21 3515 9468 E: [email protected]

Lee Hodgkinson KPMG in Canada T: +1 416 777 3414 E: [email protected]

Brian Imrie KPMG in Canada T: +1 416 777 3992 E: [email protected]

Scott Jeffery KPMG in Canada T: +1 604 646 6340 E: [email protected]

Benedicto Vasquez KPMG in Chile T: +1 56 2798 1206 E: [email protected]

Melvin Guen KPMG in China T: +86 10 8508 7019 E: [email protected]

Hiranyava Bhadra KPMG in India T: +91 22 3983 6000 E: [email protected]

Lydia Petrashova KPMG in Russia T: +7 495 937 2975 E: [email protected]

Ian Kramer KPMG in South Africa T: +27 11 647 6646 E: [email protected]

Richard Sharman KPMG in the UK T: +44 20 7311 8228 E: [email protected]

Roy Hinkamper KPMG in the US T: +1 314 244 4061 E: [email protected]

Sheri Pearce KPMG in the US T: +1 303 295 8835 E: [email protected]

kpmg.ca

The information contained herein is of a general nature and is not intended to address the circumstances of any particular individual or entity. Although we endeavor to provide accurate and timely information, there can be no guarantee that such information is accurate as of the date it is received or that it will continue to be accurate in the future. No one should act on such information without appropriate professional advice after a thorough examination of the particular situation.

© 2011 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. 6104

The KPMG name, logo and “cutting through complexity” are registered trademarks or trademarks of KPMG International.