business transformation at tnt henk van dalen, cfo 12 december 2007

TRANSCRIPT

Business transformation at TNTHenk van Dalen, CFO12 December 2007

2

Business transformation at TNT

TNT today & history ‘’Focus on Networks’’ strategy TNT 2005 - 2007 What is a network Towards a differentiating strategy

o Phase 1o Phase 2

Finance function Return to stakeholders

3

express74,590 Employees (69,482 FTE)

200 Countries of operation

2,431 Depots/hubs

217 million consignments*3

4,7 million tonnes carried*3

44 Aircraft

84,739 Employees (41,496 FTE)

8 Countries of operation

476 Mail depots (inc 11 sorting centres)*3

Mail NL Addressed Volume 4,918 million*3

Addressed items delivered outside NL (EMN) 894 million*3

TNT today

*1. Including intercompany of € 16 million*2. Including non-allocated costs of € 65 million and €7 million other depreciation*3. As per 31 December 2006

Revenue 2006: € 10,060 million*1

EBITDA 2006: € 1,594 million*2

EBIT 2006: € 1,276 million*2

-- Mail: € 4,065 million

-- Express: € 6,011 million

-- Mail: € 896 million

-- Express: € 756 million

-- Mail: € 761 million

-- Express: € 580 million

post

4

TNT, a history of transformation

Risk Management & Internal controlDisposal Logistics & Freight ManagementPortfolio growth Express and MailCapital structure / Share Buy BackDutch State sells final stake

2006/2007

1998-2005

KPN listing on Amsterdam Stock ExchangeKPN acquires TNTTPG separate listing AEX

199419961998

Dutch State PostThomas Nationwide Transport (TNT) in Australia

17521946

Build Contract LogisticsGrow and Build ExpressOptimise Mail NLBuild Mail in Europe

Public Company

TNT Brand

2008-2012 • Grow and Build Value

Focuson Networks

5

‘’Focus on Networks’’

Slides as announced on 6 December 2005

6

TNT has conducted a thorough strategic review of its business and performance

Best Postal operator; fast growing

European Mail Networks (EMN)

Express leader in Europe, on track

for 10% operating margin

Excellent growth opportunities

in Asia/China

Good track record of acquisitions

in Mail and Express

Logistics non-network based

Consolidation in industry continues

Evaluation of TNT

Slide of6 Dec. 2005

7

Network-based business is intrinsically attractive0 EBIT margin trend

Median for sector, 4 years average

Logistics

Express

Same trendfor ROIC

10%

8%

9%

7%

6%

5%

4%

3%

2%

1%

0%

Same trendFor ROIC

Slide of6 Dec. 2005

8

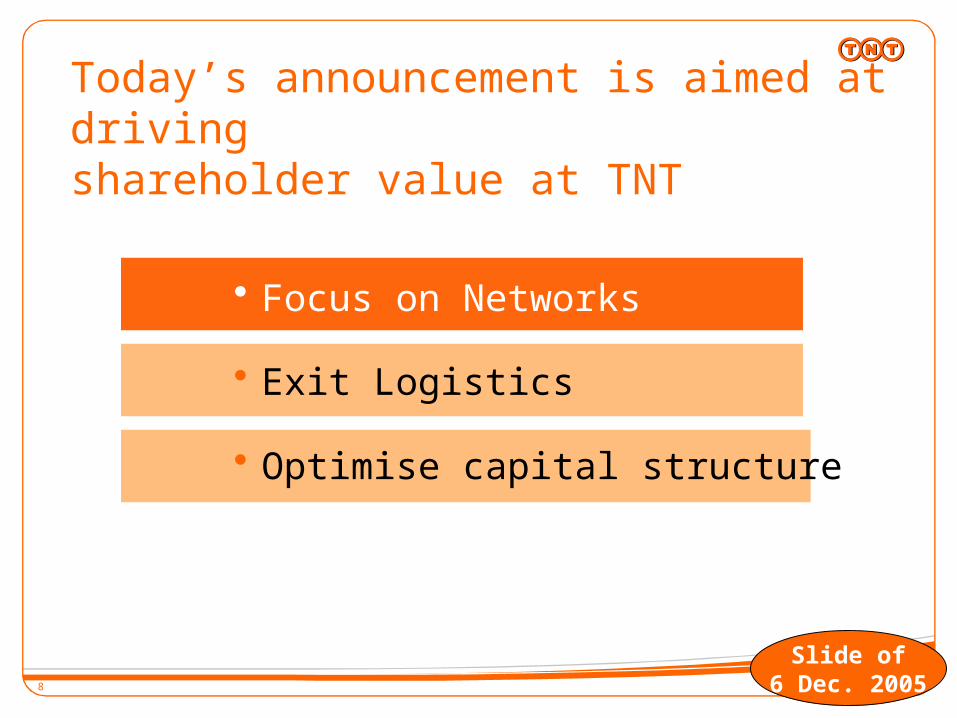

Today’s announcement is aimed at driving shareholder value at TNT

Exit Logistics

Optimise capital structure

Focus on Networks

Slide of6 Dec. 2005

9

What is a Network? Dataflow management is

essential – people and IT systems & processes

Infrastructure for collection, transport, sortation and handling, warehousing and delivery

Ability to process large numbers of transactions to achieve operational leverage

Express Road Network

Mail collection and delivery network

SC

SC

SC

SCSC

SC

SC

DepotDepotDepotDepotDepotDepot

DepotDepotDepotDepotDepotDepot

DepotDepotDepotDepotDepotDepot

Collection

Delivery= sorting

centre

LTLT

FIFISESE RURUNONO

EEEELVLV

DKDK

ICIC

TRTR

ATAT

PLPL

CHCH

BGBG

ROROHUHU

SISI

CZCZSKSK

HRHR

ALALMKMKGRGR

YUYU

UAUA

BYBY

BABA

MDMD

ITITESESPTPT

FRFR

GBGBIEIE

MARMAR

DEDENLNL

LULUBEBE

MADMAD

NXHNXH

GNQGNQ DNGDNGDFTDFT

MILMIL

VIEVIE

BZQBZQ HNJHNJ

HLBHLB

TKUTKU

QARQAR

LGGLGG

CASCAS

10

Quality, predictable volume growth

Increased drop density andmore itemsper drop

Improved transit

times and lower costs

Higheroverall margin

by improving mix

Networks intrinsic economics

Volume / Drop density

More volume leads to lower costs per unit

Combination of networks leads to further cost reduction per unit

More items

per drop

International network

Domestic network

Pick-up anddelivery costs/shipment

11

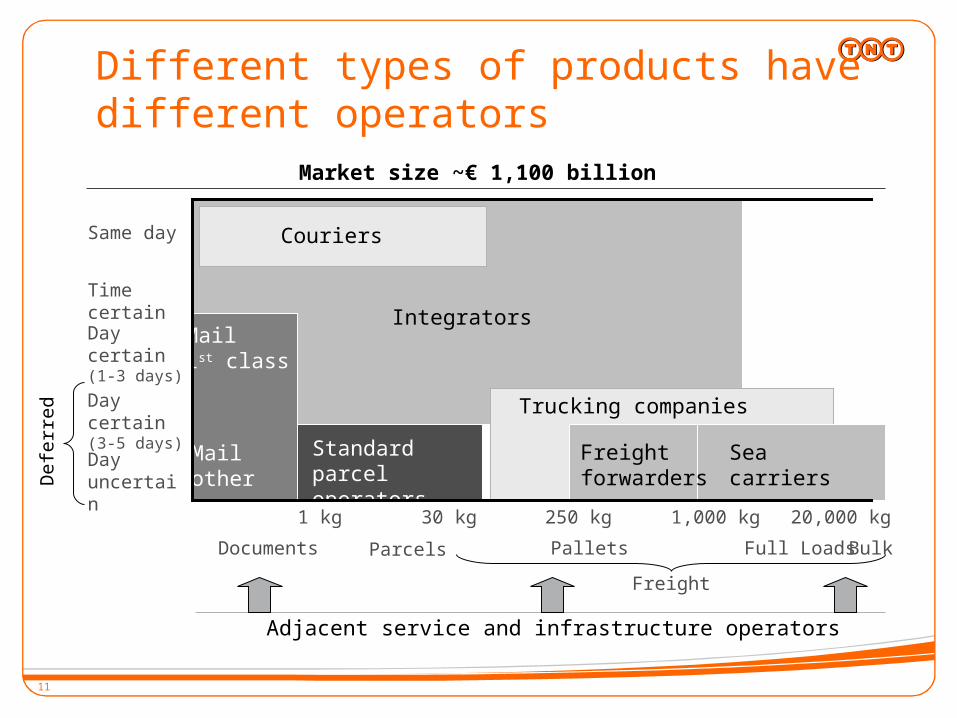

Different types of products have different operators

Documents Parcels Full Loads

1 kg 30 kg 1,000 kg

Same day

Time certain

Day certain (1-3 days)

Day certain (3-5 days)

Day uncertain

250 kg

Bulk

20,000 kg

Pallets

IntegratorsMail1st class

Standardparcel operators

Market size ~€ 1,100 billion

Couriers

Mailother

Freightforwarders

Seacarriers

Trucking companies

Def

err

ed

Adjacent service and infrastructure operators

Freight

12

Complementary Mail and Express networks

Network• Depots• Linehaul

• IT

• Back-

office

• F&A

• HRM

Marketing & Sales

Last mile delivery

Shared support

functions

Express offers Mail platform for

international growth

Mail offers Express B2C delivery capabilities

EMN shares infrastructure with domestic

express

European express

road network

European airnetwork

B2C/C2C B2B

Mail customers Express customers

13

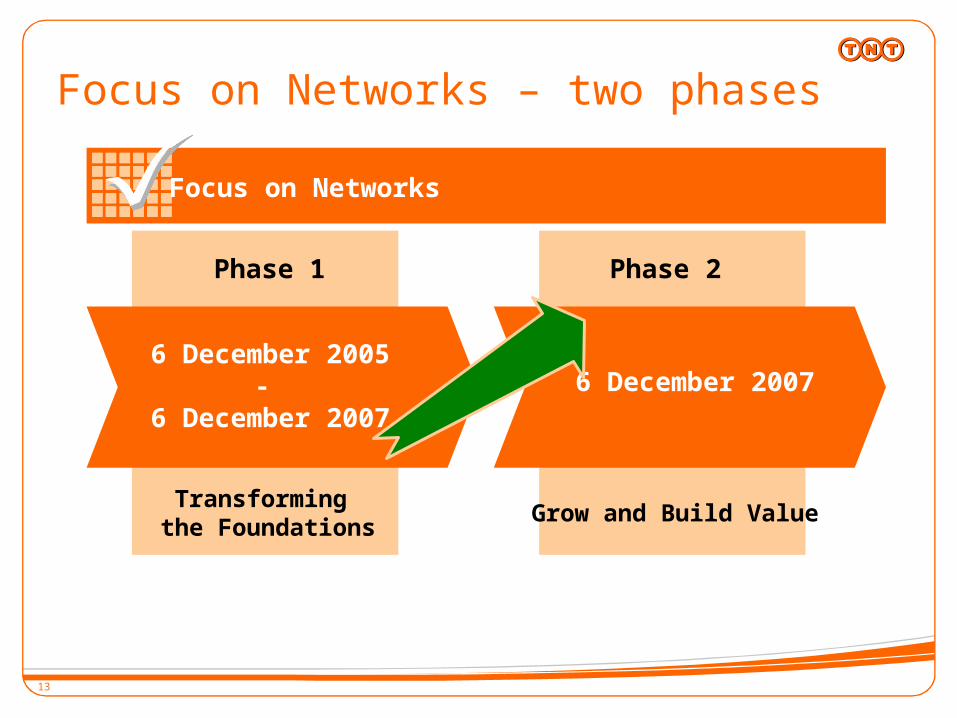

Focus on Networks – two phases

6 December 2005-

6 December 20076 December 2007

Focus on Networks

Phase 2Phase 1

Transforming the Foundations

Grow and Build Value

14

Focus 2005 /2007; ‘’transforming the foundations’’ Businesso Carve outo Clean up and complyo Grow the coreo Develop new growth platforms

Financialo Risk management, internal control, Integrity and

complianceo Carve out & Deal makingo Value processeso Sustainably optimise FLAT structure

15

Exit Logistics & FM

Optimisecapital structure

Focus on Networks

• Significant Cash returned to shareholders via buybacks and dividends

• Successful sale of non-core businesses

TNT’s strategy has delivered!

Target 6 Dec 2005

CAGR*

Express growth

10-15% 13%

Mail growth ~3% 3%EMN growth

18% 30%

* Period defined as Q4 2006-Q3 2007 compared with Full Year 2005

16

Delivered against strategic priorities

Int’lExpressEurope

AsiaPacific

Strategic Focus

GrowInvest

BuildFast

Explore& Build

ActivelyMaintain

Dom. ExpressEurope

SpecialServices

EMN Parcels

ExpressEurope

White spots

Rest ofWorld

FinancialFocus

CashGeneratio

n

Growth & Cash

ValueCreation

Value Creation Growing to WACC

VSP next week

delivery

Hoau (Chin

a)

747s

Asia Road

Network

Various expansio

ns

Strong growth EMNTG+

(Spain)

Expansion

European

network

Speedage (India)

Mail NL & other

New Master plan

initiatives

2011 EU liberalisati

on

Sale Logistics and FM

Mercúrio

Middle East Road

Network

17

• Drive business performance

• Maintain financial flexibility• Support growth;

Capex and M&A

• Keep balance sheet efficient• Target credit

rating around BBB+

• Effective Risk Management, Internal Control and Compliance

• Aligned legal, funding and tax structure

• Shareholder returns

SOx compliant over 2006

EBITDA up 13% EBIT up 13% Revenue up 14% Effective tax rate

down 17% EPS from

continuing operations up 34%

> € 3 billion of dividends and SBB from 6 December 2005

Financial strategy Key components Results Q4-05 – Q3-07*

*Period defined as Q4 2006-Q3 2007 compared with Q4 2004-Q3 2005, from continuing

operations

Performance “Transforming the Foundations”

18

Phase 2 Focus on Networks “Grow and Build Value”

2008 – 2012

Grow and Build Value

• Strengthen the core

• Grow profitable emerging platforms

• Maintain focus on shareholder value

19

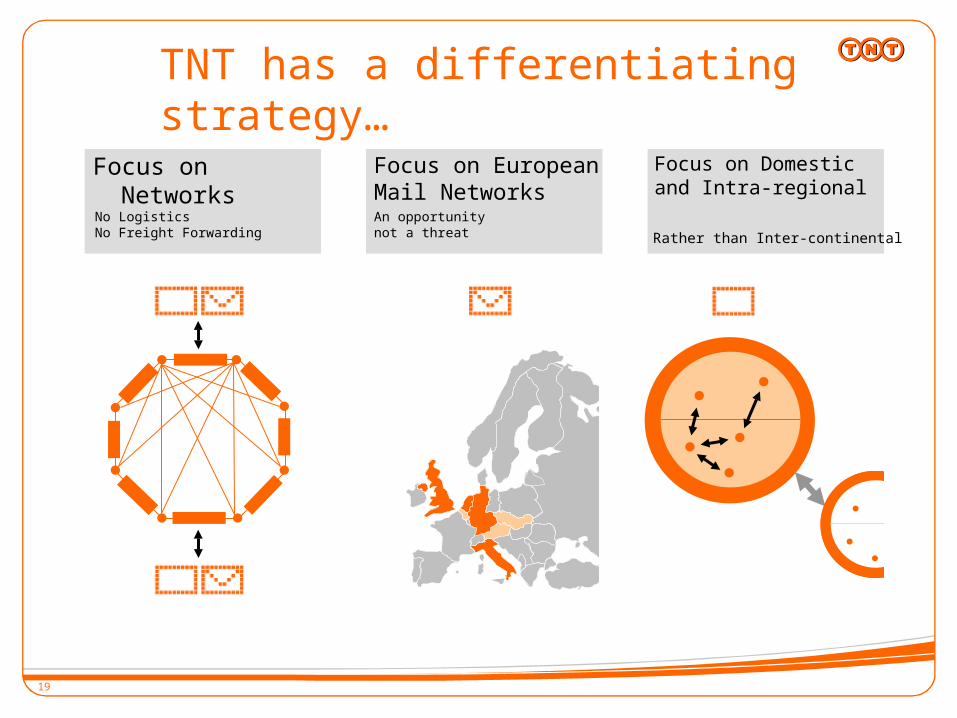

TNT has a differentiating strategy…

Focus on Networks Focus on European Mail Networks

Focus on Domestic and Intra-regional

Rather than Inter-continentalNo LogisticsNo Freight Forwarding

An opportunitynot a threat

20

Market size: ~€ 1,100 billion

1 kg 30 kg 1.000 kg250 kg 20.000 kg

Network dynamics shifting

Same day

Time certain

Day certain (1-3 days)

Day certain (3-5 days)

Day uncertain

Def

err

ed

Documents Parcels Full Loads BulkPallets

Freight

Adjacent service and infrastructure operators

Express Operators

Postal and ParcelOperators

Freight transportation companies

21

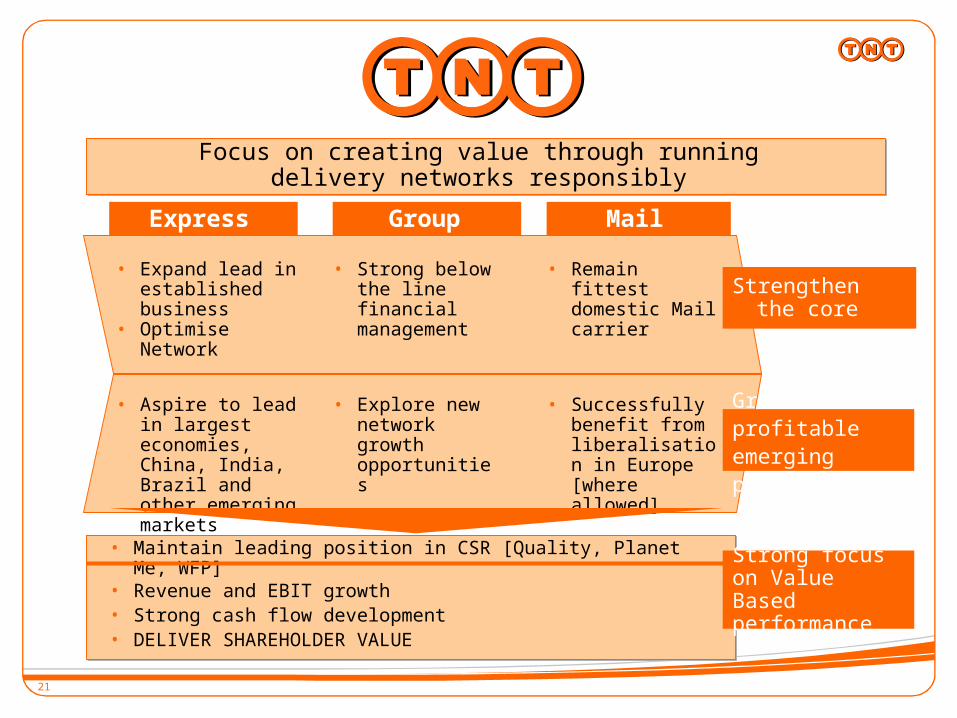

Focus on creating value through running

delivery networks responsibly

Express MailGroup

• Expand lead in established business

• Optimise Network

• Strong below the line financial management

• Remain fittest domestic Mail carrier

Strengthen the core

• Aspire to lead in largest economies, China, India, Brazil and other emerging markets

• Explore new network growth opportunities

• Successfully benefit from liberalisation in Europe [where allowed]

Grow profitable emerging platforms

• Revenue and EBIT growth• Strong cash flow development• DELIVER SHAREHOLDER VALUE

• Maintain leading position in CSR [Quality, Planet Me, WFP]Strong focus on Value Based performance

22

Phase 2 Focus on Networks TNT Express

Next wave of Express integrated networks optimisation

Strengthening the Europe- Asia Connectivity

Sharpened objectives

Grow and Build Value

Transformation of new domestic platforms

23

Domestic

Intra-regionalIntercontinen

tal

Customers

Emerging platforms

• In Europe, our platforms are fully integrated• Outside of Europe, we have built seamless connectivity

to our European distribution networks • In key emerging markets, we are building new domestic

platforms

…using a differentiating growth model for TNT Express

24

Pick-Up DeliveryAir or Road Linehaul

30,000 vehicles 836 depots

30,000 vehicles 836 depots

45 aircraft connect 25 countries3,900 trucks / week connect 34

countriesLatest collection Earliest deliveryFastest Transit

Most Reliable Service

Facilities& fleet

Objective

Technology

State of art information technology

Global track & trace systems

Cost Effective Service

Afternoon Overnight Morning

… Facilities, road and air linehaul connections, PUD …

The Next Wave of Express Networks Optimisation targets…

25

NetworksHub

infrastructureCountry / Depotinfrastructure

Integrated Network & Infrastructure Approach

PUD

Operations Infrastructure Planning & Optimisation

TNT - Global Optimisation (GO) ProgrammeDesign, Development and Implementation

2007 2017

Our new wave network optimisation is based on TNT Express strategy and continuity planning

26

Project Planning

1. Closure IMC

2. Rationalisation education

3. Rationalisation ICT

4. Repositioning SU Transport

5. Remodeling Delivery

6. Remodeling Collection

7. Remodeling of security mail

8. Optimalisation network structure

9. Marketing & Sales rationalisation

10. Retail rationalisation

Mail NL new Master plan overview cost measures of € 300 million

OperationsCompensation

& Benefits

Optimise sorting, transport, delivery and overheads

Steps towards market conformity of labour conditions

Marketing & Sales Overhead

Marketing & Sales rationalisation

Business Service change

Retail rationalisation

HR, F&A and ICT chain optimisation

Examples of projects of total of 60

27

Frequency/Speed

Daily 24h and 48hTwice a weekOnce a week

next week

Strategic proposition in addressed Dutch mail market

Other providers

Budget

Economy

‘A’-brand

The same week

Priceper piece

Mail NL: Introduction of economy product and budget mail

28

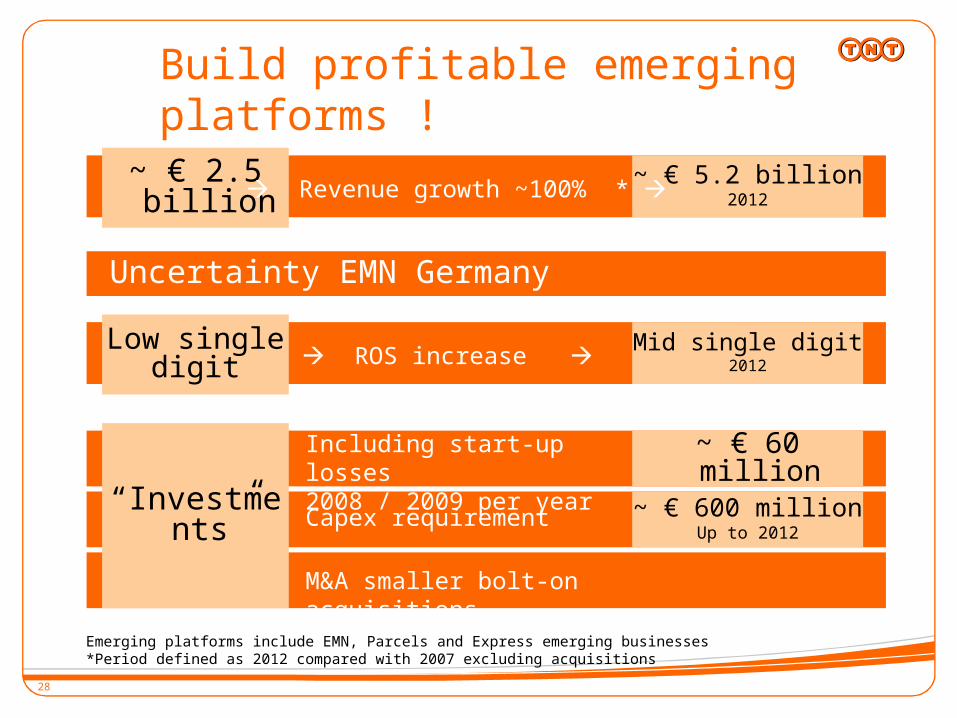

Build profitable emerging platforms !

~ € 2.5 billion

~ € 5.2 billion2012

Revenue growth ~100% *

Uncertainty EMN Germany

Low single digit

Mid single digit2012 ROS increase

~ € 60 million

~ € 600 millionUp to 2012

Including start-up losses 2008 / 2009 per year

Capex requirement

M&A smaller bolt-on acquisitions

“Investments”

Emerging platforms include EMN, Parcels and Express emerging businesses*Period defined as 2012 compared with 2007 excluding acquisitions

29

Integration overriding issues: Networks linking Systems interfacing Product offering restructuring

Estimated main sources of synergies: Revenues enhancement Sub-contracting efficiency and cost savings

Growing via transforming these companies into schedulednetworks

AcquiredTNT

All TNT Express acquisitions so far are providing a complementary network to the international set-up

30

Total revenues€ 1.7 – 2.0

billion

Addressed revenues

€ 1.3 – 1.5 billion

Operating margin 10% - 8%

0

500

1,000

1,500

2,000

2004 2005 2006 2007 2008 2009 2010 2011 2012

Revenues€ million

Unaddressed

Addressed mail +related services

Target 2012

Excluding parcels UK, Italy & Belgium

EMN ambition adjusted: on track for 2012

CAGR 16%-22%

31

Present Position and Expansion Routes in Parcels

B2C parcels

GreenfieldDominant postal operators

Large Mail Order Deliverer

ExpressLeverage infrastructure

B2B Parcels

Small local B2B players

Large European B2B players

Autonomous

Country by country

European Entry

Easy European entry not available

A focused country by country approach is required

€ 400 million

Focused growth

per country

Broker model forinternational flows

ItUKBNL

Domestic

Cross Border

Opportunistic growth strategy in two

dimensions

European positionfor

B2B/B2C parcels

32

Stand alone niche markets, with a network feeder component

32

Total pharmacy market in The Netherlands is € 4.5 billion and grows 6% annually

The submarket of repeat prescriptions has a value of € 3.5 billion

Dutch internet pharmacy market (for repeat prescriptions) is expected to grow substantially*

Initiative TNT Post : Nationale-Apotheek.nl focuses on repeat prescriptions via internet

TNT Post leverages its brand and excellent operational skills

- TNT Post is trusted

- Delivery with Track & Trace

2008 20102015*

*

Dutch internet pharmacy market

€10m€100

m€750

m

Market share TNT Post initiative

60% 50% 40%* Germany: Internet pharmacy Doc Morris has built up €100m revenue in three years; USA: Mail order pharmacy has already a 19% share of total pharmacy market** The Netherlands: Internet pharmacy is expected to have an 11% share in 2015

Market

33

Growth e-billing

Direct marketing services

Transaction mail

services

Market size (€ million) 759 162

Market share (%) 14% 19%

3,000

4,000

5,000

2006 2007 2008 2009 2010 2011 2012

Off line

On lineEmergence of on line direct marketing

0%

50%

100%

2005 2006 2007

TNT has a 14% market share in the off line marketing services market (printing, database management, call centres)

TNT also has a 19% market share in the transaction mail services market

TNT Post traditional portfolio can be leveraged to capture e-opportunities

Growth on line media spendTraditional portfolio

Post

Post + on line

On line

Emergence of e-billing

Stand alone niche markets, based on customer demand and channel optimisation

34

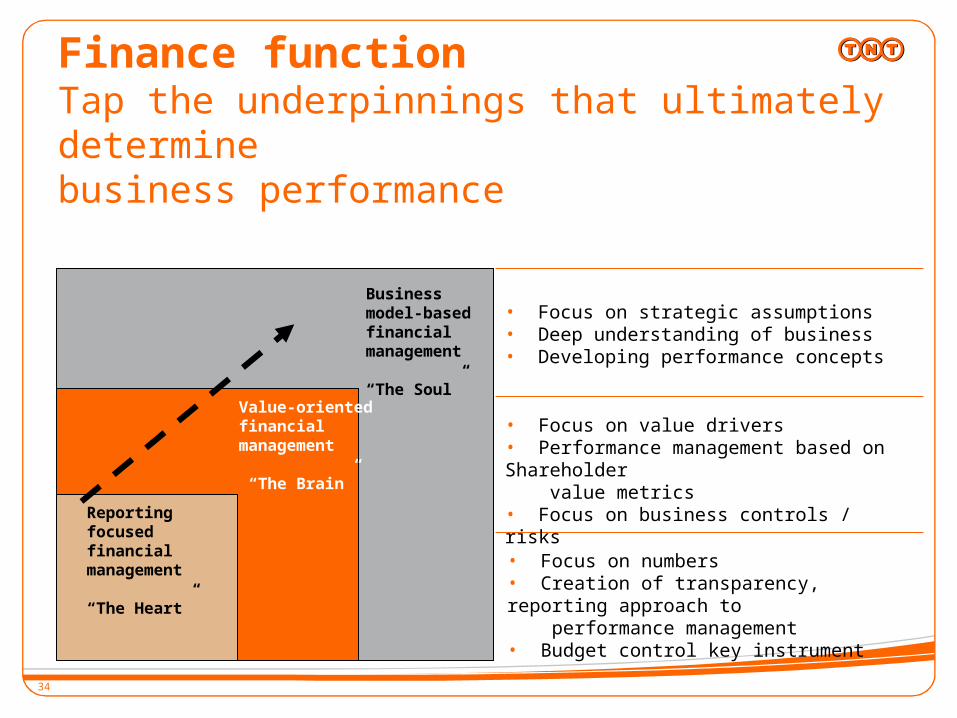

Finance function Tap the underpinnings that ultimately determine business performance

Business model-based financial management

“The Soul”

• Focus on numbers• Creation of transparency, reporting approach to performance management• Budget control key instrument

• Focus on value drivers• Performance management based on Shareholder value metrics• Focus on business controls / risks

• Focus on strategic assumptions• Deep understanding of business• Developing performance concepts

Value-oriented financial management

“The Brain”

Reporting focused financial management

“The Heart”

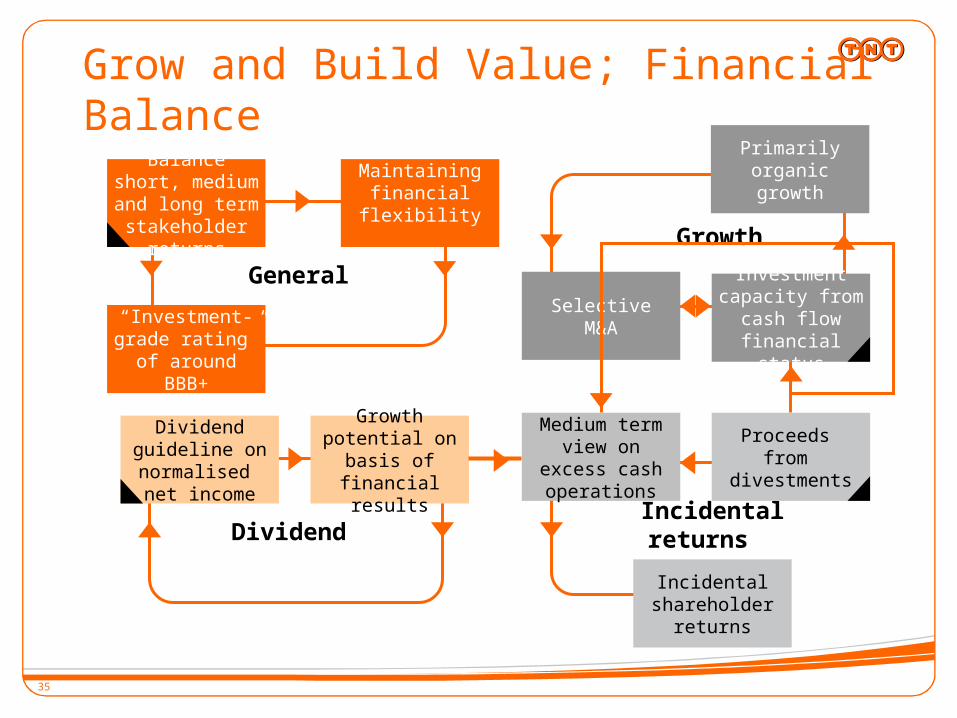

35

Incidental returns

General

Medium term view on excess cash operations

“Investment-grade rating” of around BBB+

Balance short, medium and

long term stakeholder

returns

Maintaining financial flexibility

Grow and Build Value; Financial Balance

Dividend

Growth potential on

basis of financial results

Dividend guideline on normalised net income

Growth

Primarily organic growth

SelectiveM&A

Proceeds from

divestments

Incidental shareholder

returns

Investment capacity from

cash flow financial status

36

Finance agenda 2008-2012

1. Strategy, budgeting, profit and growth drivers and

performance killers

2. Optimize sustainable ‘’FLAT’’ structure

3. Enhanced focus on Cash

4. Quality and standardization of processes

5. Alignment in control, integrity and risk management

6. HR in Finance

37

Structure Risk management, internal control, integrity, compliance Optimise financial standing around BBB+ investment grade Further ETR decrease to a level of around 25-26% by 2010 Dividend (per share) up, barring unforeseen circumstances Further external business transparency

Operational Capex as % of revenues 4-6%, including smaller acquisitions Specific business objectives on Revenue and ROS Restructuring charge in Mail € 125-175 million in phases up

to 2009 Grow Free Cash Flow of the Group

Medium term view on Free Cash Flow allocation

1. Strategic profitable growth steps and dividends2. Incidental return to shareholders

Focused Financial Strategy 2008 – 2012

38

M&A appraisal

s

Explicit and detailed evaluation of stand alone and synergy value

Post merger “100 day” and “1 year” reviews

Pay for performan

ce

Management incentive system explicitly linked to EP

Investment /

appraisals

Separate review of growth and replacement investments

Focus on capacity utilisation, asset light alternatives, fast cash payback

Post investment reviews

Budgetingand

Performance

Business unit budgets assessed based on year-on-year EP growth

Value drivers Focus on cash optimisation

Strategy Strategic options reviewed on the basis of EP, next to top and bottom line growth

Economic Profit (EP)

Economic Profit to measure and drive performance

EBIT

+ Add back interest operating leases

Adjusted pre-tax EBIT

- Tax charge- Capital charge for net

working capital- Capital charge for

fixed assets- Capital charge

operating leases

Economic Profit

EP definition at TNT Application of EP at BU level

39

SUN project: “driving value below the line”Significant unrecognised tax losses High effective tax rate

Loans in tax loss countries

Emerging markets balancesCash balancesInternal chargesGroup legal structure

Cash flow focus / Trade working capital

Legal

Accounting

Fiscal

Treasury

BusinessValue

4040

Regionalteams

Corporate legal structure

SUN key initiatives

Continuous country scan

Financingcompany

Emerging countries

41

Key performance indicators 2007 – 2012Outlook 2007 regrouped

RevenuesOrganic revenue

growthReturn on Sales

2007E 2007ECAGR ’08-’12

2007E2012

Target

Express segment

International & Domestic ~5,450 ~7% 8-10% ~11% 12-13%

Emerging platforms(Apac, India, China, LAM, MEA, Russia, Turkey)

~1,100 ~12% 15-20%Around break-even

Mid single digit

Mail segment

Mail total ~4,200 3-4% 4-6% ~17.5%Mid

teens

Emerging Mail + Parcels ~1,350 ~25% 12-15%Mid

single digit

High single digit

Emerging Mail + Parcels (excluding EMN Germany)

~1,100 ~23% 9-11%Mid

single digit

High single digit

Other Networks

Non allocated

Group total~11,00

0~6% ~10% ~12% ~12%

All figures 2007 are rounded and regrouped for indication purposes only based on the outlook as confirmed excluding the effect of any provisions related to the new Master plan initiatives

€ million

42

Stakeholder returns since 2005

43

We focus on delivering the best Customer Experience in creating a customer focused organisation

43

• Customer Experience is a newly created role focusing on making all customer touch points outstanding

44

Which resulted in our Clients rating our customerservice above our competitors´…Theme Attribute

TNT Expres

sDHL FedEx UPS

Customer Service

Ease of contacting required person (02) 3.48 3.33 3.28 3.24Ability of CS staff to answer all questions (27) 3.53 3.43 3.36 3.35Level of personalised service offered (26) 3.52 3.35 3.35 3.36Ability of sales rep to understand your business (31)

3.54 3.38 3.33 3.40

Adequacy of information provided (phone, e-mail etc) (36)

3.57 3.41 3.40 3.49

Problem handling

Timely notification of delivery problems (18) 3.36 3.15 3.28 3.29Availability of suitable solutions to problems (21) 3.33 3.26 3.31 3.22Speed of complaint resolution (38) 3.24 3.19 3.20 3.15

Driver Assistance

Ability of drivers to offer assistance (33) 3.71 3.56 3.62 3.68

Ease of use of Internet services

Ease of use of Internet services (12) 3.51 3.49 3.52 3.61

Operations

On time delivery of shipments sent (16) 3.62 3.57 3.61 3.66Ability to fulfill its commitments (37) 3.60 3.53 3.50 3.57Suitability of transportation services (4/5/6) 3.60 3.48 3.46 3.60Capability to handle all your shipments (07) 3.68 3.51 3.51 3.55Suitability of shipment collection times (10) 3.67 3.65 3.58 3.68

Source: RI customer research 2007 and CMI analysisCountries participated: Germany, UK, Italy, France, Netherlands, Belgium, Australia, Switzerland, Romania, Brazil

45

Since Dec 2005, TNT has outperformedmost of its competitors…

Share price development since December 2005

192123252729313335

1-Dec 1-Feb 1-Apr 1-Jun 1-Aug 1-Oct 1-Dec 1-Feb 1-Apr 1-Jun 1-Aug 1-Oct 1-Dec

TNT AEX DPWN FDX UPS OP

192123252729313335

1-Dec 1-Feb 1-Apr 1-Jun 1-Aug 1-Oct 1-Dec 1-Feb 1-Apr 1-Jun 1-Aug 1-Oct 1-Dec

TNT AEX DPWN FDX UPS OP

192123252729313335

1-Dec 1-Feb 1-Apr 1-Jun 1-Aug 1-Oct 1-Dec 1-Feb 1-Apr 1-Jun 1-Aug 1-Oct 1-Dec

TNT AEX DPWN FDX UPS OP

192123252729313335

1-Dec 1-Feb 1-Apr 1-Jun 1-Aug 1-Oct 1-Dec 1-Feb 1-Apr 1-Jun 1-Aug 1-Oct 1-Dec

TNT AEX DPWN FDX UPS OP

TNT AEX DPWN FDX UPS OP

46

Significant cash shareholder returns

> € 3 billion of Dividends and SBB from 6 December 2005 to 6 December 2007

Dividend in cash Cash Returns to Shareholders

237268

282298

5763

73

20 2226

30 30

0

50

100

150

200

250

300

350

2004 2005 2006 2007 YTD

0

10

20

30

40

50

60

70

80

Dividend paid in the year (€ million)

Dividend per share over the year (€ cent)

Interim dividend per share in the year (€ cent)

CAGR dividend per share 14%

New € 500 million SBB programme Current tranche € 200 million implemented

47

Convincing development shareholder value parameters

Earnings per share* (€ cents)

0

50

100

150

200

250

CAGR EPS 17%

FY-05 H2-05 /H1-06

Q4-05 /Q3-06

FY-06 H2-06 /H1-07

Q4-06 /Q3-07

0%

10%

20%

30%

40%

50%

60%

70%

FY-05 H2-05 /H1-06

Q4-05 /Q3-06

FY-06 H2-06 /H1-07

Q4-06 /Q3-07

CAGR RoE 36%

Return on Equity*

* From continuing operations

48

Highest score in Dow Jones Sustainability Index 2007

11 Highest score in all 3 dimensions

- Economic (94%)

- Environmental (95%)

- Social (90%) SAM Research: “TNT has

consistently improved not only its sustainability reporting, but also its sustainability performance”

12 Akzo Nobel3 Australia &

New Zealand Banks Group

4 Novo Nordisk5 Philips

91%88%87%

83%82%

49

Dividend pay out to 40% of normalised net income by

2010

Additional € 100 million tranche of € 500 million SBB

“Regular” incidental SBB from excess cash

49

Focus on Shareholder returns short term

50

Return to stakeholders since December 2005 Three years in a row Dow Jones Sustainability Index leader

Strong increase Earnings and Dividend per share

Incidental return to shareholders through > 3 bn share repurchases

Customer focus recognized and awarded

Investors in People (IiP) fully implemented

Top rated financial and business reporting

Solid Governance model

51

Warning about forward looking statements

Some statements in this presentation are “forward-looking statements”. By their nature, forward-looking statements involve risk and uncertainty because they relate to events that depend on circumstances that will occur in the future. These forward-looking statements are based on current expectations, estimates, forecasts, analyses and projections about the industries in which we operate and management’s beliefs and assumptions about future events. You are cautioned not to put undue reliance on these forward-looking statements, which only speak as of the date of this presentation and are neither predictions nor guarantees of future events or circumstances. We do not undertake any obligation to release publicly any revisions to these forward-looking statements to reflect events or circumstances after the date of this presentation or to reflect the occurrence of unanticipated events, except as may be required under applicable securities laws.

52

Focus On Networks

52