bvmf presentation - july 2011

TRANSCRIPT

7/30/2019 BVMF Presentation - July 2011

http://slidepdf.com/reader/full/bvmf-presentation-july-2011 1/51

July 2011

7/30/2019 BVMF Presentation - July 2011

http://slidepdf.com/reader/full/bvmf-presentation-july-2011 2/51

Forward Looking Statements

This presentation may contain certain statements that express the management’s expectations, beliefs and assumptions

about future events or results. Such statements are not historical fact, being based on currently available competitive,

financial and economic data, and on current projections about the industries BM&FBovespa works in.

The verbs “anticipate,” “believe,” “estimate,” “expect,” “forecast,” “plan,” “predict,” “project,” “target” and other similarverbs are intended to identify these forward-looking statements, which involve risks and uncertainties that could cause

actual results to differ materially from those projected in this presentation and do not guarantee any future BM&FBovespa

performance.

The factors that might affect performance include, but are not limited to: ( i) market acceptance of BM&FBOVESPA services;

(ii) volatility related to (a) the Brazilian economy and securities markets and (b) the highly-competitive industries

BM&FBovespa operates in; (iii) changes in (a) domestic and foreign legislation and taxation and (b) government policies

related to the financial and securities markets; (iv) increasing competition from new entrants to the Brazilian markets; (v)ability to keep up with rapid changes in technological environment, including the implementation of enhanced functionality

demanded by BM&FBovespa customers; (vi) ability to maintain an ongoing process for introducing competitive new

products and services, while maintaining the competitiveness of existing ones; (vii) ability to attract new customers in

domestic and foreign jurisdictions; (viii) ability to expand the offer of BM&FBovespa products in foreign jurisdictions.

All forward-looking statements in this presentation are based on information and data available as of the date they were

made, and BM&FBovespa undertakes no obligation to update them in light of new information or future development.

This presentation does not constitute an offer to sell or the solicitation of an offer to buy any securities, nor shall there be

any sale of securities where such offer or sale would be unlawful prior to registration or qualification under the securities

law. No offering shall be made except by means of a prospectus meeting the requirements of the Brazilian Securities

Commission CVM Instruction 400 of 2003, as amended.

2

7/30/2019 BVMF Presentation - July 2011

http://slidepdf.com/reader/full/bvmf-presentation-july-2011 3/51

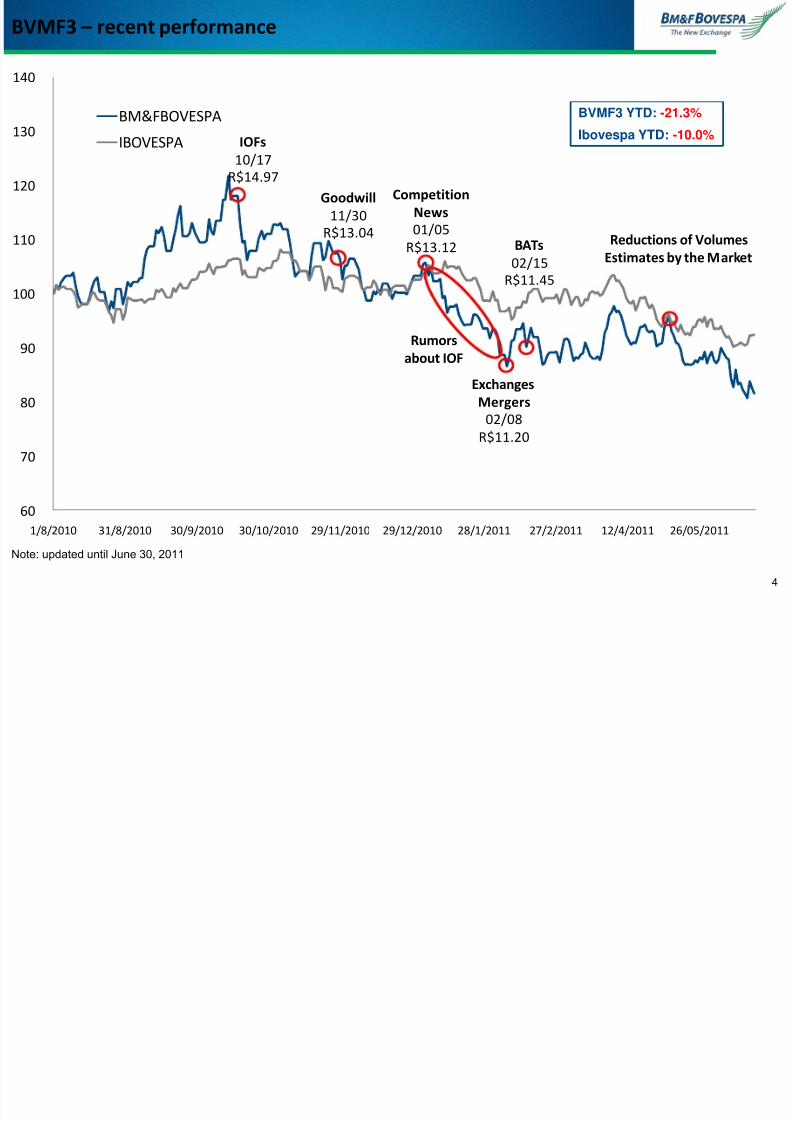

BVMF STOCK PRICE Recent Performance

3

7/30/2019 BVMF Presentation - July 2011

http://slidepdf.com/reader/full/bvmf-presentation-july-2011 4/51

IOFs10/17

R$14.97

Goodwill

11/30R$13.04

Competition

News

01/05

R$13.12

Rumors

about IOF

Exchanges

Mergers

02/08R$11.20

BATs

02/15

R$11.45

Reductions of Volumes

Estimates by the Market

60

70

80

90

100

110

120

130

140

1/8/2010 31/8/2010 30/9/2010 30/10/2010 29/11/2010 29/12/2010 28/1/2011 27/2/2011 12/4/2011 26/05/2011

BM&FBOVESPA

IBOVESPA

BVMF3 – recent performance

Note: updated until June 30, 2011

BVMF3 YTD: -21.3%

Ibovespa YTD: -10.0%

4

7/30/2019 BVMF Presentation - July 2011

http://slidepdf.com/reader/full/bvmf-presentation-july-2011 5/51

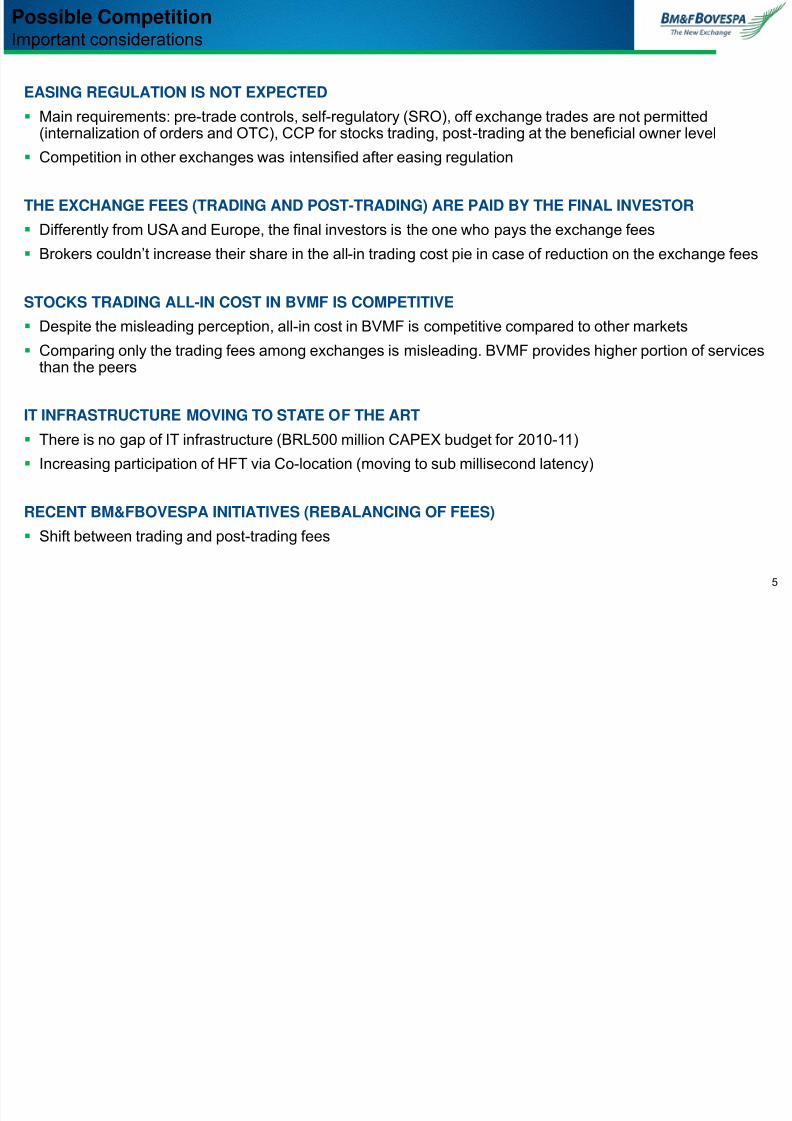

Possible CompetitionImportant considerations

EASING REGULATION IS NOT EXPECTED

Main requirements: pre-trade controls, self-regulatory (SRO), off exchange trades are not permitted

(internalization of orders and OTC), CCP for stocks trading, post-trading at the beneficial owner level Competition in other exchanges was intensified after easing regulation

THE EXCHANGE FEES (TRADING AND POST-TRADING) ARE PAID BY THE FINAL INVESTOR

Differently from USA and Europe, the final investors is the one who pays the exchange fees

Brokers couldn’t increase their share in the all-in trading cost pie in case of reduction on the exchange fees

STOCKS TRADING ALL-IN COST IN BVMF IS COMPETITIVE

Despite the misleading perception, all-in cost in BVMF is competitive compared to other markets

Comparing only the trading fees among exchanges is misleading. BVMF provides higher portion of servicesthan the peers

IT INFRASTRUCTURE MOVING TO STATE OF THE ART There is no gap of IT infrastructure (BRL500 million CAPEX budget for 2010-11)

Increasing participation of HFT via Co-location (moving to sub millisecond latency)

RECENT BM&FBOVESPA INITIATIVES (REBALANCING OF FEES)

Shift between trading and post-trading fees

5

7/30/2019 BVMF Presentation - July 2011

http://slidepdf.com/reader/full/bvmf-presentation-july-2011 6/51

BRAZILIAN MARKET OPPORTUNITIES

6

7/30/2019 BVMF Presentation - July 2011

http://slidepdf.com/reader/full/bvmf-presentation-july-2011 7/51

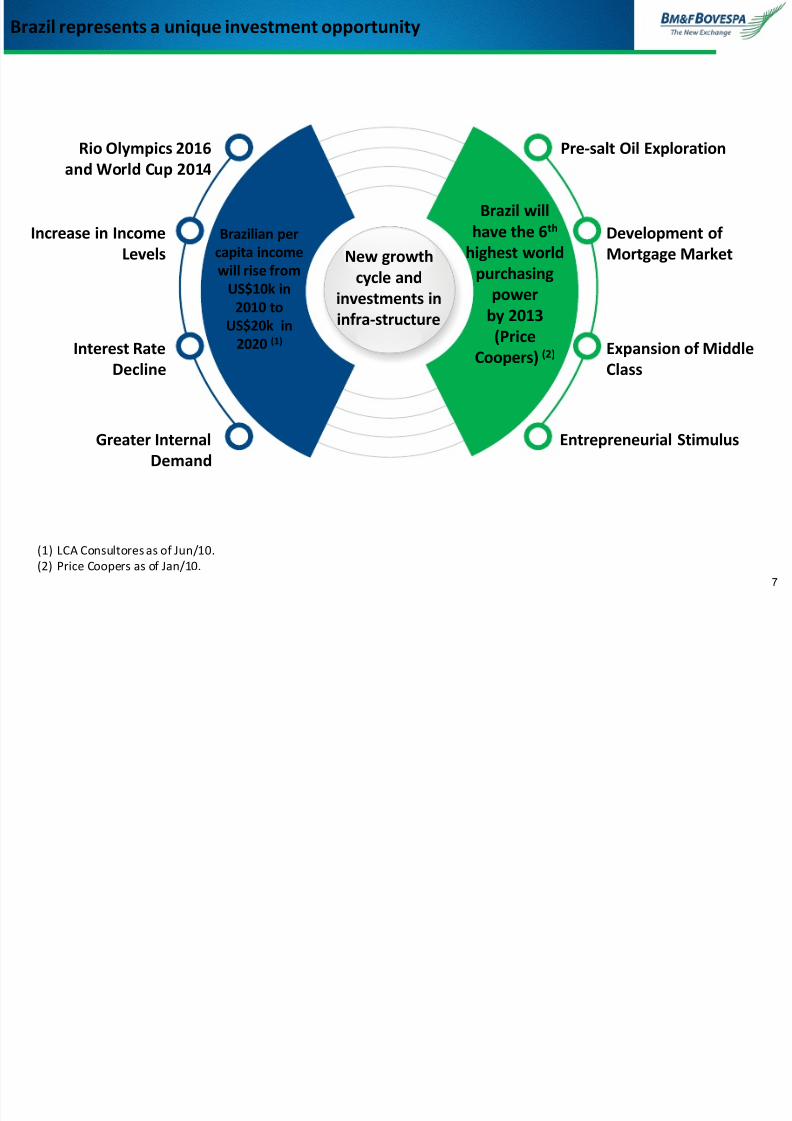

Brazil represents a unique investment opportunity

New growth

cycle andinvestments in

infra-structure

Pre-salt Oil Exploration

Development of

Mortgage Market

Expansion of Middle

Class

Entrepreneurial StimulusGreater Internal

Demand

Rio Olympics 2016

and World Cup 2014

Increase in Income

Levels

Interest Rate

Decline

Brazil will

have the 6th

highest world

purchasingpower

by 2013

(Price

Coopers) (2)

Brazilian per

capita income

will rise fromUS$10k in

2010 to

US$20k in

2020 (1)

(1) LCA Consultores as of Jun/10.(2) Price Coopers as of Jan/10.

7

7/30/2019 BVMF Presentation - July 2011

http://slidepdf.com/reader/full/bvmf-presentation-july-2011 8/51

J a n - 0 5

J u l - 0 5

J a n - 0 6

J u l - 0 6

J a n - 0 7

J u l - 0 7

J a n - 0 8

J u l - 0 8

J a n - 0 9

J u l - 0 9

J a n - 1 0

J u l - 1 0

J a n - 1 1

Source: ABRAPP, WFE and BM&FBOVESPA8

Equity Market (BOVESPA Segment)Low penetration in the Brazilian market

Clients base: huge potential in retail and pension funds segments

Number of custody accounts (thousands)

128.6

Jun’11

632.4

Pension funds portfolioLow penetration of equity and

derivatives in the main investors’portfolios

Stable and “low” interest rateenvironment encourage more

exposure in equities

Recent growth in the number of retail investors, but still low

compared to other markets

Listed Companies

Low number of listed companies compared to othercountries

Lack of important economic sectors in the exchange,for instance: oil & gas, infrastructure, retail, IT andpharmaceutical,

Investment cycle may bring new companies andsectors to the exchange

Currently, SMEs are not able to raise money throughequity easily

Dec’10 Listed Companies (27th in the World)

6,586

5,095

3,741 3,566 3,476 3,3452,966

1,999 1,798

379

India USA Canada Japan China / HK Spain London Australia Korea Brazil

27.7%

30.9%72.3%

69.1%

2002 2010

% in Securities Fixed Income and Others

BRL168.5 billion

BRL501.5 billion

7/30/2019 BVMF Presentation - July 2011

http://slidepdf.com/reader/full/bvmf-presentation-july-2011 9/519

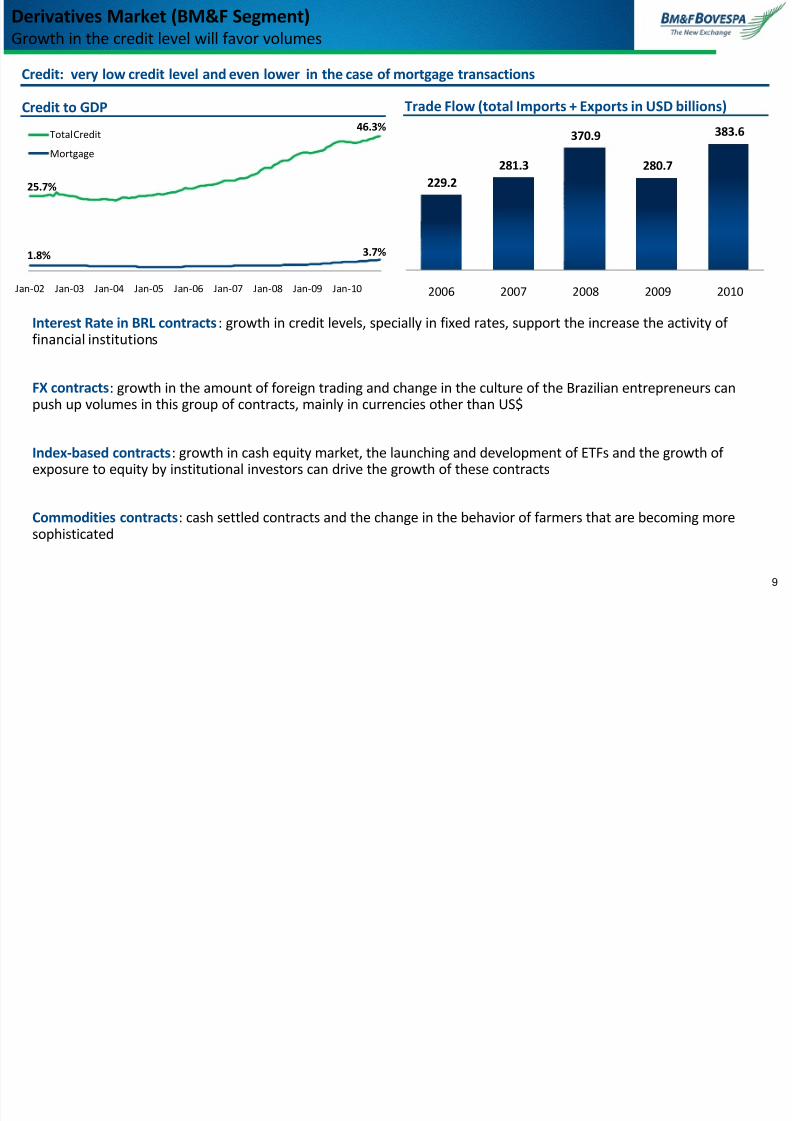

Derivatives Market (BM&F Segment)Growth in the credit level will favor volumes

Credit: very low credit level and even lower in the case of mortgage transactions

Credit to GDP

Interest Rate in BRL contracts: growth in credit levels, specially in fixed rates, support the increase the activity of financial institutions

FX contracts: growth in the amount of foreign trading and change in the culture of the Brazilian entrepreneurs canpush up volumes in this group of contracts, mainly in currencies other than US$

Index-based contracts: growth in cash equity market, the launching and development of ETFs and the growth of exposure to equity by institutional investors can drive the growth of these contracts

Commodities contracts: cash settled contracts and the change in the behavior of farmers that are becoming moresophisticated

Trade Flow (total Imports + Exports in USD billions)

25.7%

46.3%

1.8% 3.7%

Jan-02 Jan-03 Jan-04 Jan-05 Jan-06 Jan-07 Jan-08 Jan-09 Jan-10

Total CreditMortgage

229.2

281.3

370.9

280.7

383.6

2006 2007 2008 2009 2010

7/30/2019 BVMF Presentation - July 2011

http://slidepdf.com/reader/full/bvmf-presentation-july-2011 10/51

MAIN INITIATIVES

10

h f d

7/30/2019 BVMF Presentation - July 2011

http://slidepdf.com/reader/full/bvmf-presentation-july-2011 11/51

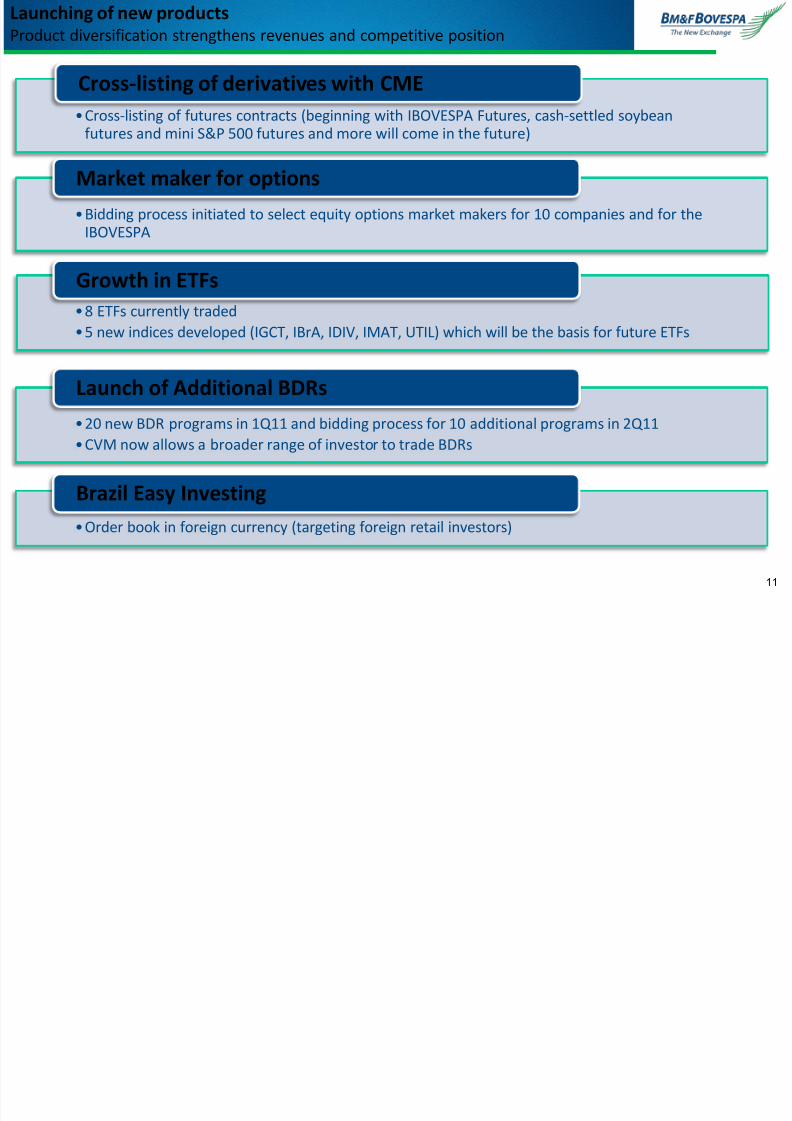

Launching of new productsProduct diversification strengthens revenues and competitive position

•8 ETFs currently traded

•5 new indices developed (IGCT, IBrA, IDIV, IMAT, UTIL) which will be the basis for future ETFs

Growth in ETFs

•Bidding process initiated to select equity options market makers for 10 companies and for theIBOVESPA

Market maker for options

•Cross-listing of futures contracts (beginning with IBOVESPA Futures, cash-settled soybean

futures and mini S&P 500 futures and more will come in the future)

Cross-listing of derivatives with CME

•20 new BDR programs in 1Q11 and bidding process for 10 additional programs in 2Q11

•CVM now allows a broader range of investor to trade BDRs

Launch of Additional BDRs

•Order book in foreign currency (targeting foreign retail investors)

Brazil Easy Investing

11

7/30/2019 BVMF Presentation - July 2011

http://slidepdf.com/reader/full/bvmf-presentation-july-2011 12/51

Retail Investors: less than 0.5% of the population invest

in stocks Marketing campaign that will be released in mass

medias (wanna be a shareholder?) and educationalprograms

HFT: unexplored market by these group of investors

IT developments, pricing policy and sales force

Foreign Investors: a high number of investors are not inBrazil yet

Strengthening the sales force, quotes in other

currencies and DMA

12

Institutional key drivers to attract new investors to the market

New Participants:

Listed Companies: around 400 companies not properly reflect the diversity of BrazilianEconomy

Developing a listing segment for SMEs and educational initiatives for entrepreneurs

7/30/2019 BVMF Presentation - July 2011

http://slidepdf.com/reader/full/bvmf-presentation-july-2011 13/51

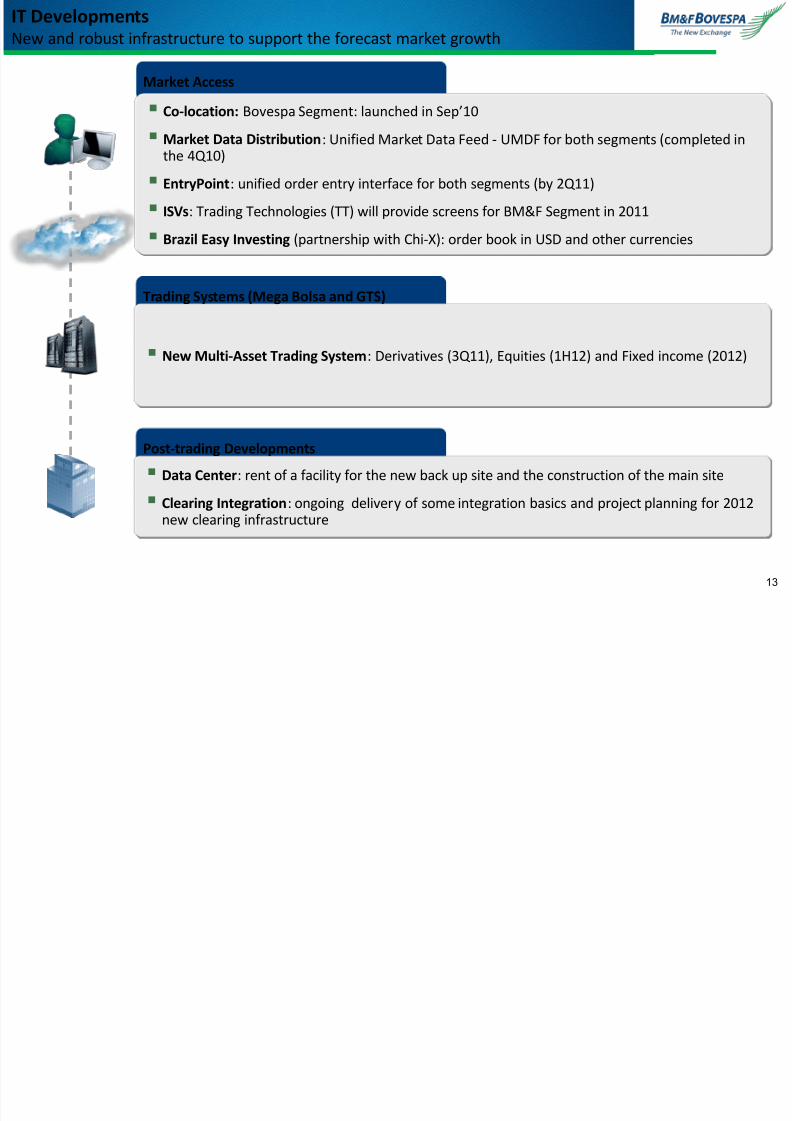

Excellence in IT Solutions and Post-Trading Services

13

Market Access

Co-location: Bovespa Segment: launched in Sep’10

Market Data Distribution: Unified Market Data Feed - UMDF for both segments (completed inthe 4Q10)

EntryPoint: unified order entry interface for both segments (by 2Q11)

ISVs: Trading Technologies (TT) will provide screens for BM&F Segment in 2011

Brazil Easy Investing (partnership with Chi-X): order book in USD and other currencies

Trading Systems (Mega Bolsa and GTS)

New Multi-Asset Trading System: Derivatives (3Q11), Equities (1H12) and Fixed income (2012)

Post-trading Developments

Data Center: rent of a facility for the new back up site and the construction of the main site

Clearing Integration: ongoing delivery of some integration basics and project planning for 2012new clearing infrastructure

IT DevelopmentsNew and robust infrastructure to support the forecast market growth

7/30/2019 BVMF Presentation - July 2011

http://slidepdf.com/reader/full/bvmf-presentation-july-2011 14/51

Strengthening the sales force in other countries

- Offices in New York, London and Shanghai

Partnerships with international exchanges

- Strategic partnership with CME Group

- Asia: MoU and discussions with HKEx andShanghai Exchanges

- Latam: MoU with Chile exchange anddiscussions with Peru and Colombia

International ProjectsCreating a global market

14

7/30/2019 BVMF Presentation - July 2011

http://slidepdf.com/reader/full/bvmf-presentation-july-2011 15/51

BUSINESS MODEL AND REGULATORY

FRAMEWORK

15

i k l il d i h

7/30/2019 BVMF Presentation - July 2011

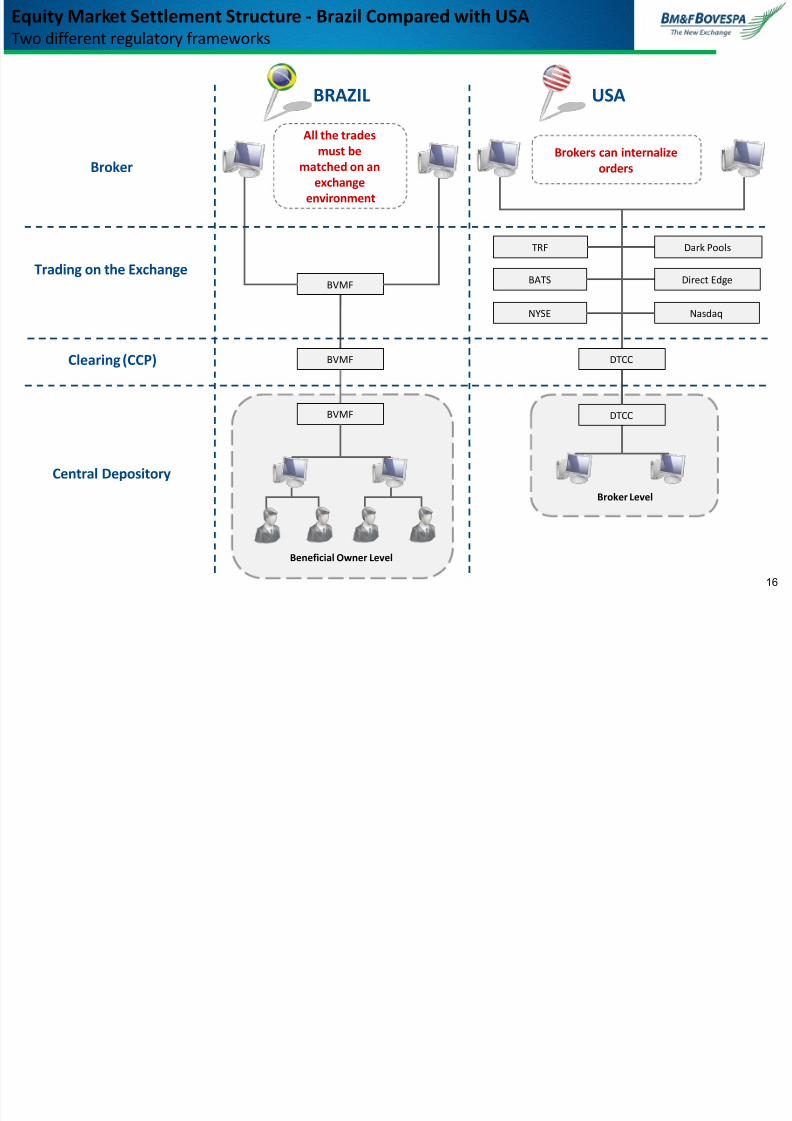

http://slidepdf.com/reader/full/bvmf-presentation-july-2011 16/51

BRAZIL USA

BVMF

BVMF

BVMF

DTCC

DTCC

NYSE Nasdaq

BATS Direct Edge

TRF Dark Pools

Beneficial Owner Level

Broker Level

All the tradesmust be

matched on an

exchange

environment

Brokers can internalize

orders

Central Depository

Clearing (CCP)

Trading on the Exchange

Broker

Equity Market Settlement Structure - Brazil Compared with USATwo different regulatory frameworks

16

7/30/2019 BVMF Presentation - July 2011

http://slidepdf.com/reader/full/bvmf-presentation-july-2011 17/51

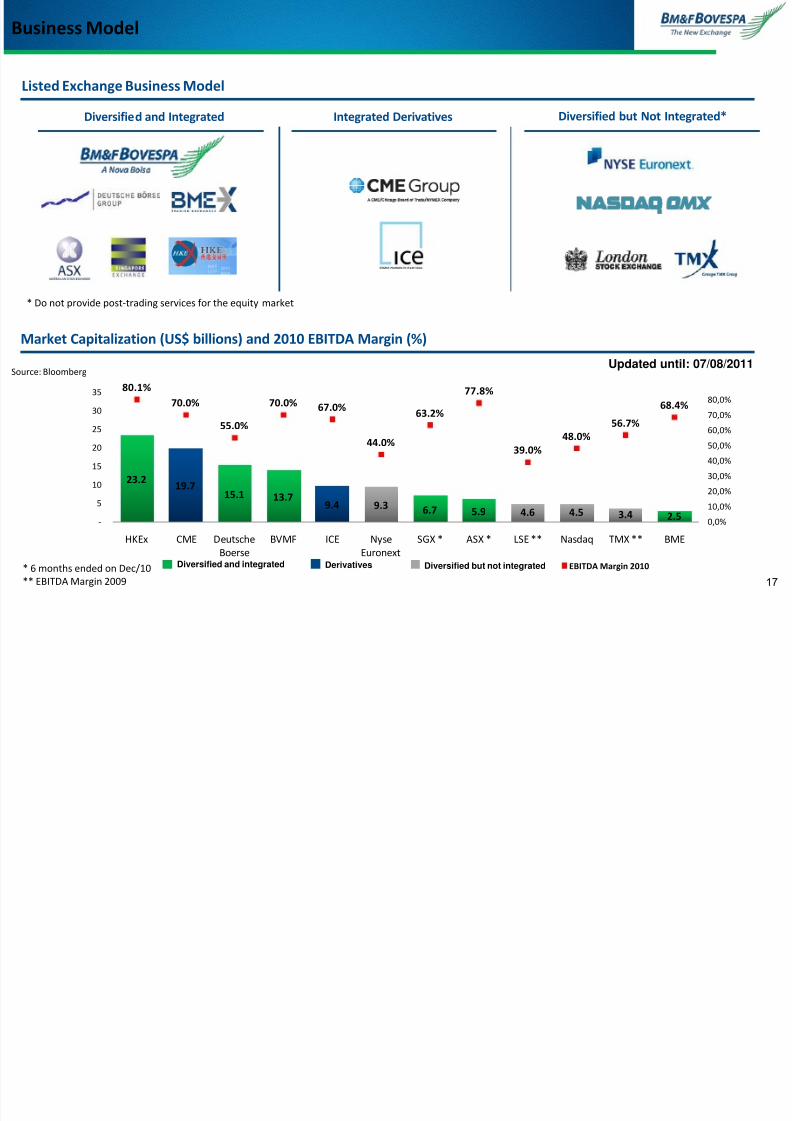

Updated until: 07/08/2011

Market Capitalization (US$ billions) and 2010 EBITDA Margin (%)

Listed Exchange Business Model

Diversified and Integrated Integrated Derivatives Diversified but Not Integrated*

* Do not provide post-trading services for the equity market

Diversified and integrated Derivatives Diversified but not integrated

Business Model

17

Source: Bloomberg

* 6 months ended on Dec/10

** EBITDA Margin 2009

23.219.7

15.1 13.79.4 9.3 6.7 5.9 4.6 4.5 3.4 2.5

80.1%

70.0%

55.0%

70.0% 67.0%

44.0%

63.2%

77.8%

39.0%

48.0%

56.7%

68.4%

0,0%

10,0%

20,0%

30,0%

40,0%

50,0%

60,0%70,0%

80,0%

-

5

10

15

20

25

30

35

HKEx CME Deutsche

Boerse

BVMF ICE Nyse

Euronext

SGX * ASX * LSE ** Nasdaq TMX ** BME

EBITDA Margin 2010

B ili M k t R l t F k

7/30/2019 BVMF Presentation - July 2011

http://slidepdf.com/reader/full/bvmf-presentation-july-2011 18/51

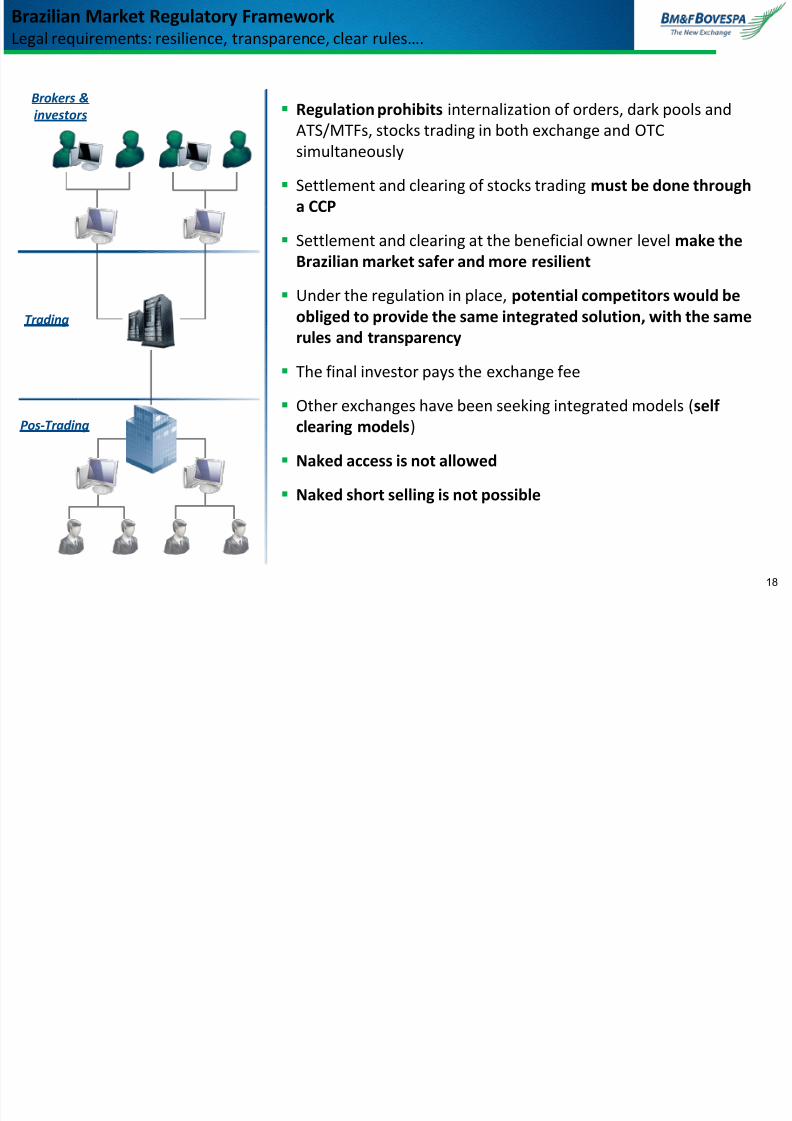

Brokers &

investors

Trading

Pos-Trading

Regulation prohibits internalization of orders, dark pools and

ATS/MTFs, stocks trading in both exchange and OTC

simultaneously

Settlement and clearing of stocks trading must be done through

a CCP

Settlement and clearing at the beneficial owner level make the

Brazilian market safer and more resilient

Under the regulation in place, potential competitors would be

obliged to provide the same integrated solution, with the same

rules and transparency

The final investor pays the exchange fee

Other exchanges have been seeking integrated models (self

clearing models)

Naked access is not allowed

Naked short selling is not possible

18

Brazilian Market Regulatory FrameworkLegal requirements: resilience, transparence, clear rules….

BM&FBOVESPA C titi St th

7/30/2019 BVMF Presentation - July 2011

http://slidepdf.com/reader/full/bvmf-presentation-july-2011 19/5119

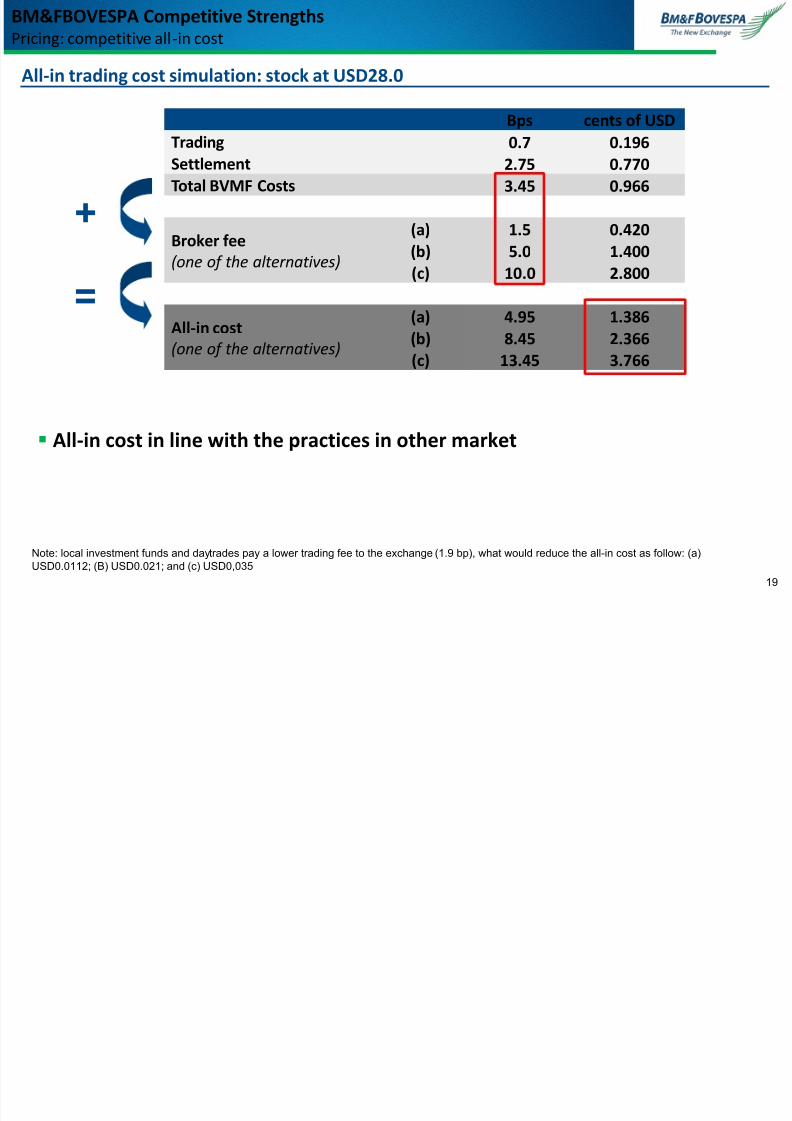

BM&FBOVESPA Competitive StrengthsPricing: competitive all-in cost

Bps cents of USD

Trading 0.7 0.196Settlement 2.75 0.770

Total BVMF Costs 3.45 0.966

Broker fee

(one of the alternatives)

(a) 1.5 0.420

(b) 5.0 1.400

(c) 10.0 2.800

All-in cost

(one of the alternatives)

(a) 4.95 1.386

(b) 8.45 2.366

(c) 13.45 3.766

All-in trading cost simulation: stock at USD28.0

All-in cost in line with the practices in other market

Note: local investment funds and daytrades pay a lower trading fee to the exchange (1.9 bp), what would reduce the all-in cost as follow: (a)USD0.0112; (B) USD0.021; and (c) USD0,035

+

=

7/30/2019 BVMF Presentation - July 2011

http://slidepdf.com/reader/full/bvmf-presentation-july-2011 20/51

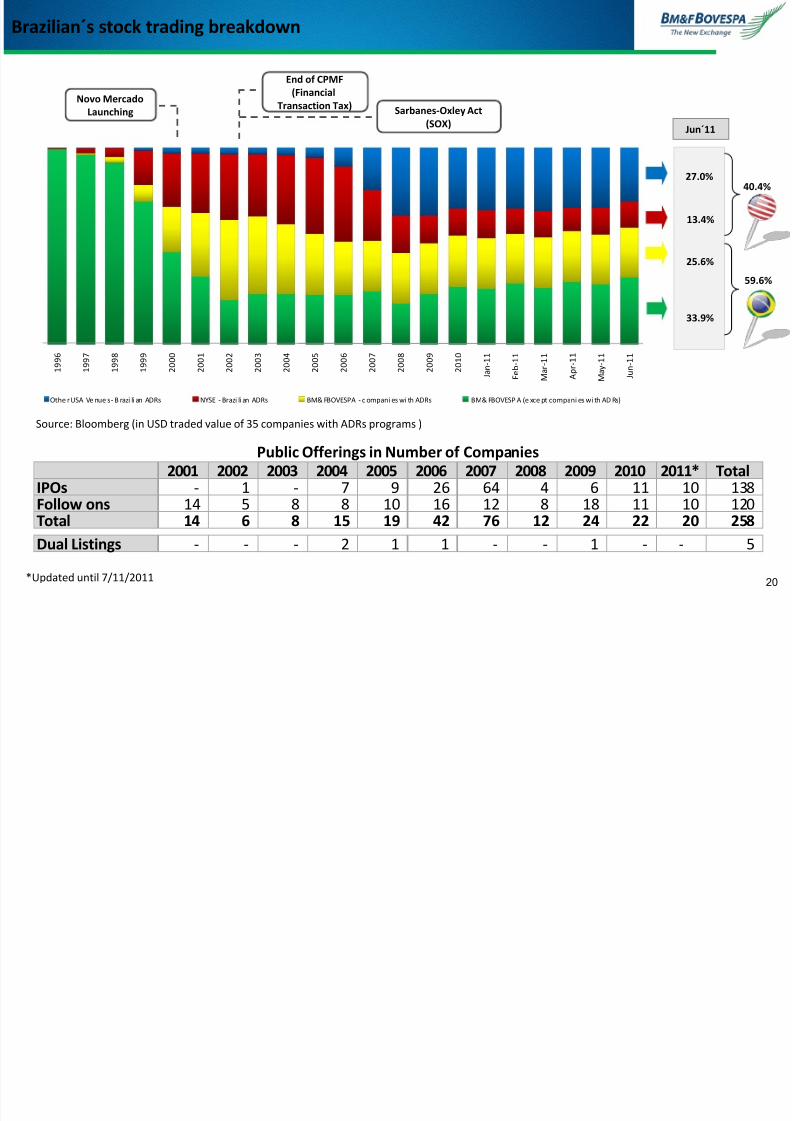

33.9%

25.6%

13.4%

27.0%

Jun´11

Source: Bloomberg (in USD traded value of 35 companies with ADRs programs )

End of CPMF

(Financial

Transaction Tax) Sarbanes-Oxley Act

(SOX)

*Updated until 7/11/2011

40.4%

59.6%

Novo Mercado

Launching

20

Brazilian´s stock trading breakdown

1 9 9 6

1 9 9 7

1 9 9 8

1 9 9 9

2 0 0 0

2 0 0 1

2 0 0 2

2 0 0 3

2 0 0 4

2 0 0 5

2 0 0 6

2 0 0 7

2 0 0 8

2 0 0 9

2 0 1 0

J a n - 1 1

F e b - 1 1

M a r - 1 1

A p r - 1 1

M a y - 1 1

J u n - 1 1

Othe r USA Ve nue s - B razi li an ADRs NYSE - Brazi li an ADRs BM& FBOVESPA - c ompani es wi th ADRs BM& FBOVESP A (e xce pt compani es wi th AD Rs)

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011* TotalIPOs - 1 - 7 9 26 64 4 6 11 10 138 Follow ons 14 5 8 8 10 16 12 8 18 11 10 120 Total 14 6 8 15 19 42 76 12 24 22 20 258

Dual Listings - - - 2 1 1 - - 1 - - 5

Public Offerings in Number of Companies

7/30/2019 BVMF Presentation - July 2011

http://slidepdf.com/reader/full/bvmf-presentation-july-2011 21/51

OPERATIONAL HIGHLIGHTS

21

7/30/2019 BVMF Presentation - July 2011

http://slidepdf.com/reader/full/bvmf-presentation-july-2011 22/51

1.21.6

2.4

4.9

5.5 5.3

6.5 6.46.5

7.3

6.5

6.7

6.1 5.95.5

2004 2005 2006 2007 2008 2009 2010 2011* Jan-11 Feb-11 Mar-11 Apr-11 May-11 Jun-11 Jul-11*

**Relation of the trading value in the cash market and the market cap of the exchange

Updated until: Jun 30, 2011

22

BOVESPA Segment: operational highlights

Average Daily Traded Value – ADTV (BRL billions)

Number of Custody Accounts (Thousands) Turnover Velocity ** (12 months average)

CAGR (2004-10)32.1%

559576

640

581580

661640 632629626625637

632

2008 2009 20 10 1Q1 0 2Q10 3Q10 4Q1 0 Jan-1 1Feb-11Mar-11Apr-11May-11Jun-11

30.8% 29.4%36.8% 37.6% 38.7%

42.3%

56.4%

63.2%66.6% 63.8%

60,8%

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

* Updated until: July 15th, 2011

7/30/2019 BVMF Presentation - July 2011

http://slidepdf.com/reader/full/bvmf-presentation-july-2011 23/51

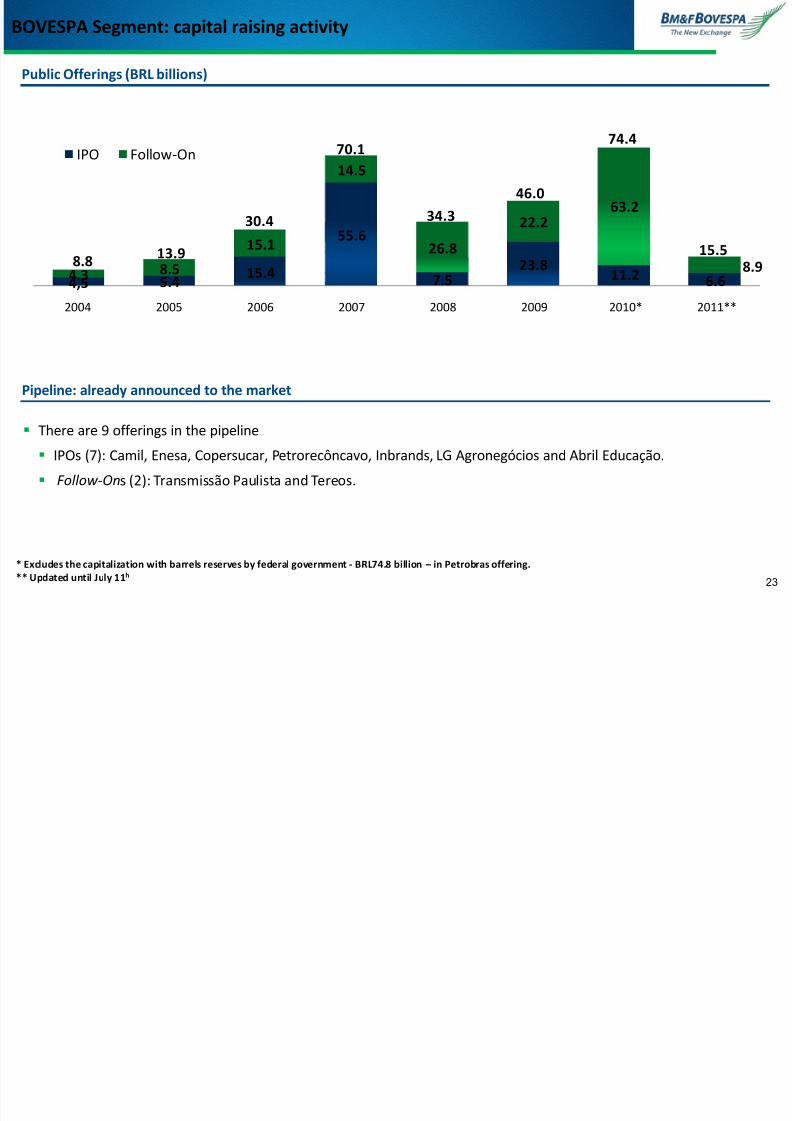

BOVESPA Segment: capital raising activity

There are 9 offerings in the pipeline

IPOs (7): Camil, Enesa, Copersucar, Petrorecôncavo, Inbrands, LG Agronegócios and Abril Educação.

Follow-Ons (2): Transmissão Paulista and Tereos.

23

* Excludes the capitalization with barrels reserves by federal government - BRL74.8 billion – in Petrobras offering.

** Updated until July 11h

Public Offerings (BRL billions)

Pipeline: already announced to the market

4,5 5.4 15.4

55.6

7.5

23.8

11.2 6.64.38.5

15.1

14.5

26.8

22.263.2

8.9

2004 2005 2006 2007 2008 2009 2010* 2011**

IPO Follow-On

8.813.9

30.4

70.1

34.3

46.0

74.4

15.5

BOVESPA Segment

7/30/2019 BVMF Presentation - July 2011

http://slidepdf.com/reader/full/bvmf-presentation-july-2011 24/51

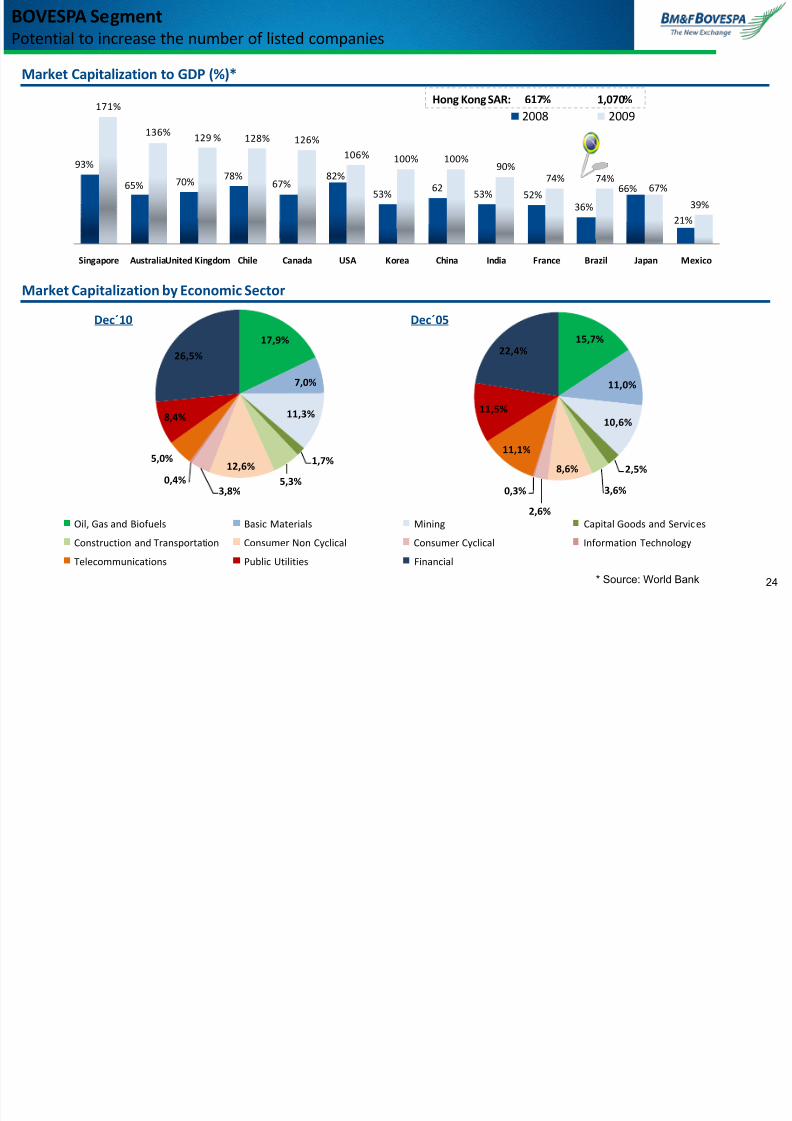

17,9%

7,0%

11,3%

1,7%

5,3%

12,6%

3,8%0,4%

5,0%

8,4%

26,5%

Oil, Gas and Biofuels Basic Materials Mining Capital Goods and Services

Construction and Transportation Consumer Non Cyclical Consumer Cyclical Information Technology

Telecommunications Public Utilities Financial

15,7%

11,0%

10,6%

2,5%

3,6%

8,6%

2,6%

0,3%

11,1%

11,5%

22,4%

Dec´10 Dec´05

Market Capitalization to GDP (%)*

Market Capitalization by Economic Sector

BOVESPA SegmentPotential to increase the number of listed companies

93%

65% 70%78%

67%82%

53%62

53% 52%36%

66%

21%

171%

136%

129 % 128% 126%106% 100% 100%

90%74% 74%

67%

39%

Singapore AustraliaUnited Kingdom Chile Canada USA Korea China India France Brazil Japan Mexico

2008 2009

Hong Kong SAR: 617% 1,070%

* Source: World Bank 24

7/30/2019 BVMF Presentation - July 2011

http://slidepdf.com/reader/full/bvmf-presentation-july-2011 25/51

422 501 711 988 789 843

1,684 1,884 1,937 2,0682,364 2,552

1,2171,493 1,458

110 168

266

473535 447

541478 438 391

437522

574531 419

86 7468

112 88 80

89 95 62117

84108

84114 99

187 109124

167 162 150

191269 218

248221

300

323292 283

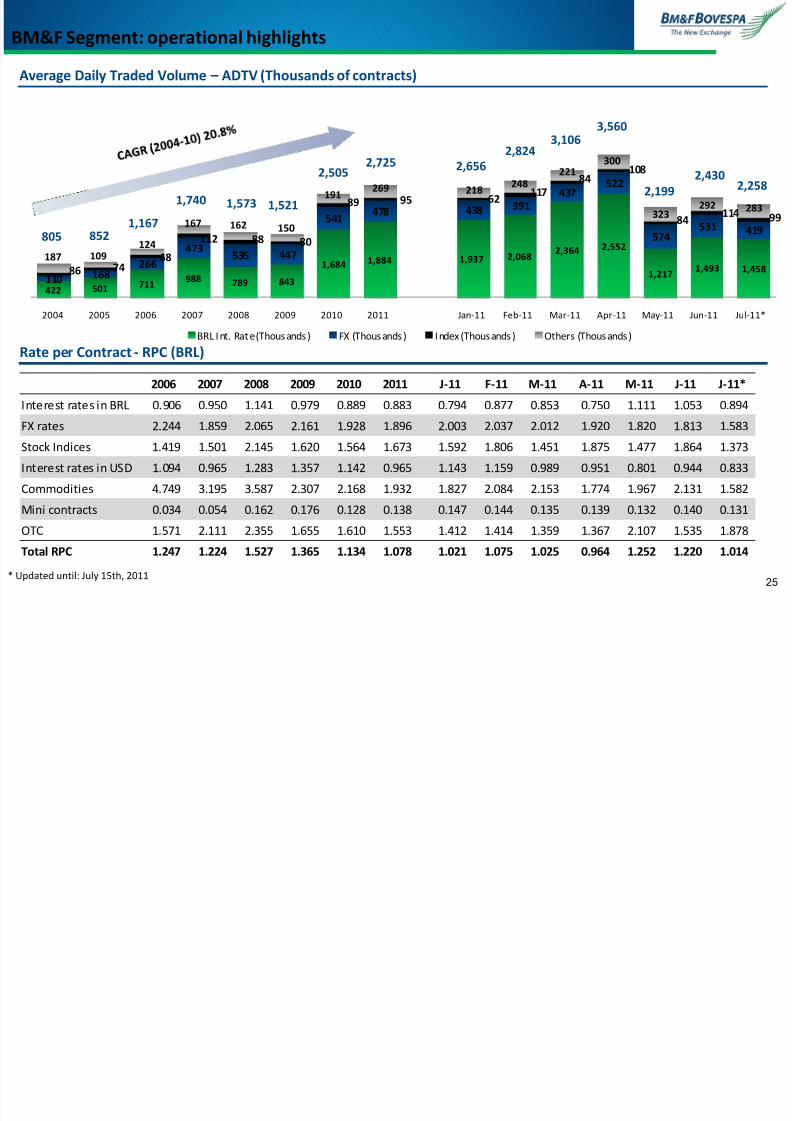

2004 2005 2006 2007 2008 2009 2010 2011 Jan-11 Feb-11 Mar-11 Apr-11 May-11 Jun-11 Jul-11*

BRL Int. Rate (Thousands) FX (Thousands) Index (Thousands) Others (Thousands)

* Updated until: July 15th, 201125

BM&F Segment: operational highlights

805 8521,167

1,740 1,573 1,521

2,5052,725

Average Daily Traded Volume – ADTV (Thousands of contracts)

Rate per Contract - RPC (BRL)

2,6562,824 3,106

3,560

2,199

2,4302,258

2006 2007 2008 2009 2010 2011 J-11 F-11 M-11 A-11 M-11 J-11 J-11*

Interest rates in BRL 0.906 0.950 1.141 0.979 0.889 0.883 0.794 0.877 0.853 0.750 1.111 1.053 0.894

FX rates 2.244 1.859 2.065 2.161 1.928 1.896 2.003 2.037 2.012 1.920 1.820 1.813 1.583

Stock Indices 1.419 1.501 2.145 1.620 1.564 1.673 1.592 1.806 1.451 1.875 1.477 1.864 1.373

Interest rates in USD 1.094 0.965 1.283 1.357 1.142 0.965 1.143 1.159 0.989 0.951 0.801 0.944 0.833

Commodities 4.749 3.195 3.587 2.307 2.168 1.932 1.827 2.084 2.153 1.774 1.967 2.131 1.582

Mini contracts 0.034 0.054 0.162 0.176 0.128 0.138 0.147 0.144 0.135 0.139 0.132 0.140 0.131

OTC 1.571 2.111 2.355 1.655 1.610 1.553 1.412 1.414 1.359 1.367 2.107 1.535 1.878

Total RPC 1.247 1.224 1.527 1.365 1.134 1.078 1.021 1.075 1.025 0.964 1.252 1.220 1.014

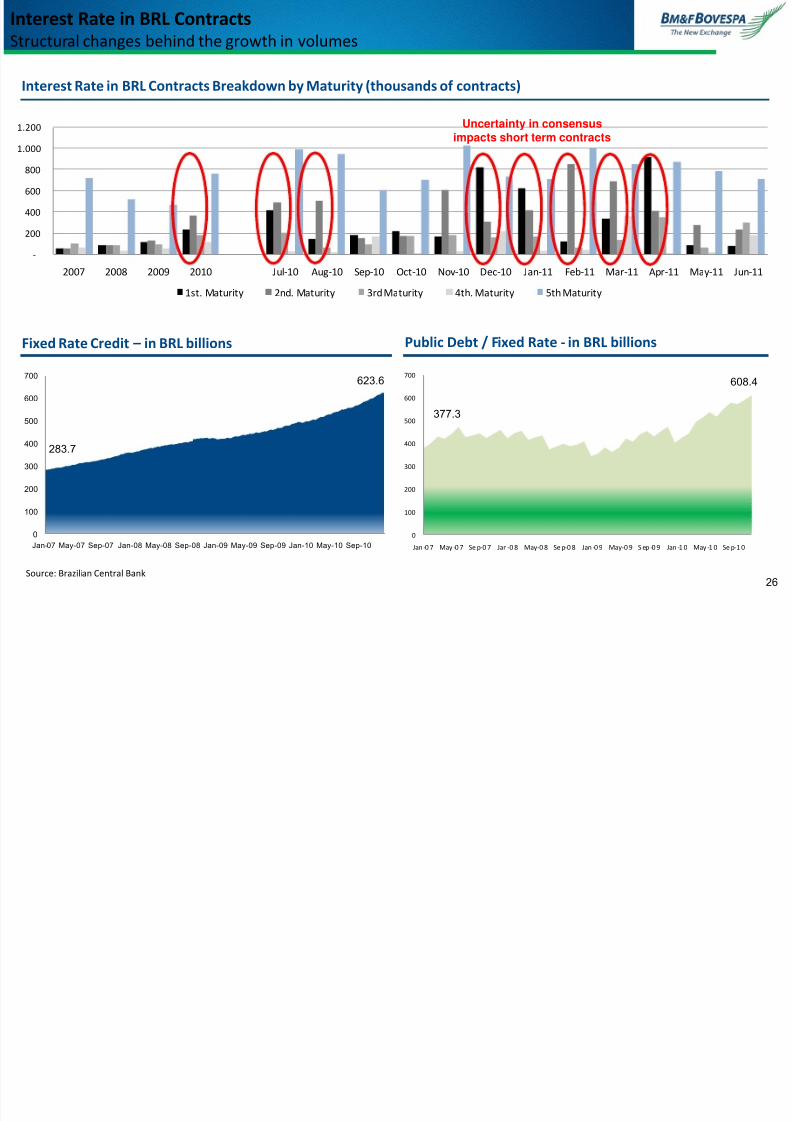

Interest Rate in BRL Contracts

7/30/2019 BVMF Presentation - July 2011

http://slidepdf.com/reader/full/bvmf-presentation-july-2011 26/51

-

200

400

600

800

1.000

1.200

2007 2008 2009 2010 Jul-10 Aug-10 Sep-10 Oct-10 Nov-10 Dec-10 Jan-11 Feb-11 Mar-11 Apr-11 May-11 Jun-11

1st. Maturity 2nd. Maturity 3rd Maturity 4th. Maturity 5th Maturity

26

Interest Rate in BRL ContractsStructural changes behind the growth in volumes

Interest Rate in BRL Contracts Breakdown by Maturity (thousands of contracts)

Uncertainty in consensus

impacts short term contracts

Fixed Rate Credit – in BRL billions Public Debt / Fixed Rate - in BRL billions

Source: Brazilian Central Bank

0

100

200

300

400

500

600

700

Jan-07 May-07 Sep-07 Jan-08 May-08 Sep-08 Jan-09 May-09 Sep-09 Jan-10 May-10 Sep-10

0

100

200

300

400

500

600

700

Jan -0 7 May -0 7 Se p-0 7 Jan-0 8 May-0 8 Se p-0 8 Jan -0 9 May-0 9 S ep -0 9 Jan -1 0 May -1 0 Se p-1 0

283.7

623.6

377.3

608.4

High Frequency Trading (HFT)

7/30/2019 BVMF Presentation - July 2011

http://slidepdf.com/reader/full/bvmf-presentation-july-2011 27/51

27

High Frequency Trading (HFT)HFT will play an important role in both cash and derivatives markets

HFT – BM&F Segment(ADTV in thousands of contracts and mkt. share)

HFT – Bovespa Segment(ADTV in BRL billions and mkt. share)

Co-location

BM&F Segment (thousands of contracts) Bovespa Segment (thousands of BRL)

* Updated until: June 30, 2011

22,128 18,397

39,280

71,952

125,620

211,097

256,817

217,518 217,883

247,923

S ept/10 O ct/10 Nov/10 Dec/10 Jan/11 Feb/11 Ma/11 A pr/11 May /11 Jun/11*

4 20 41 50 69

155

74 77 66101

65 65 67 82118 101

5

1844

41

50

43 38 43

45

2951 48

49

4542

47

22

53

77

93

9093

82

95

68

90 8890

10292

42

17

10

17

16 1818

8

4

0.3%1.0%

2.8%

4.8%

3.8%

6.0%

4.4%

4.8%

3.7% 5.0%3.5%

4.2% 3.9% 3.6%6.7%

5.4%

1Q09 2Q09 3Q09 4Q09 1Q10 2Q10 3Q10 4Q10 1Q11 2Q11 Jan-11 Feb-11 Mar-11 Apr -11 May-11 jun/11

FX Equiti es Mini contr acts Interest Rates i n BRL % in Overall Volume

8 32

81

151

188

301

207 208

251

179

222 222239

274

239

0 1 3 7 12 15 13 17 20 25

84

164 162151156162

203

161

125112

162173

186

246 232

3.2%

1.4%

3.3% 3.2%2.6%

4.1%

4.8%

2.9%

2.1%2.1%

2.9%2.8%

2.7%

5.6%4.8%

0.56 0.500.73

0.960.75 0.78

1.00 0.90

4.5%4.0%

5.7%

6.6%

5.9%5.9%

8.7% 7.6%

0,0%

1,0%

2,0%

3,0%

4,0%

5,0%

6,0%

7,0%

8,0%9,0%

10,0

-

0,20

0,40

0,60

0,80

1,00

1,20

Nov-10 Dec-10 Jan-11 Feb-11 Mar-11 Apr-11 May-11 Jun-11

ADTV -Day Trade (in BRL billions) % of overall market

7/30/2019 BVMF Presentation - July 2011

http://slidepdf.com/reader/full/bvmf-presentation-july-2011 28/51

28

Appendix

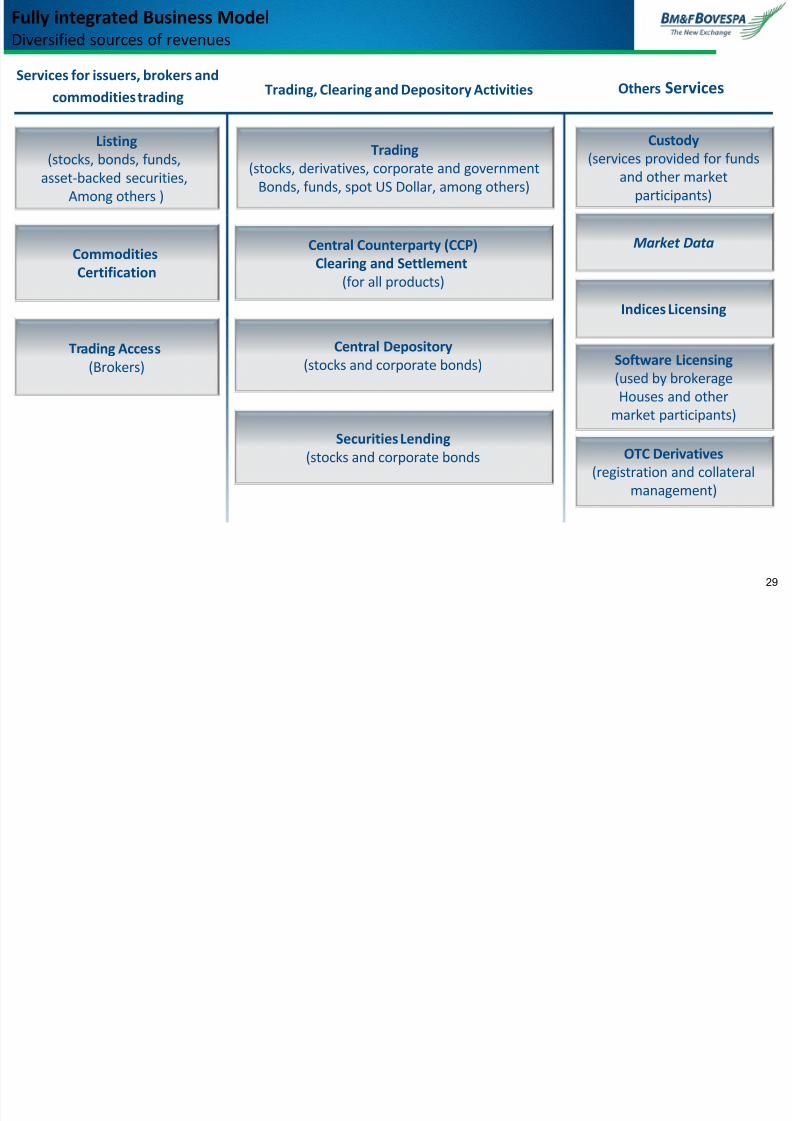

Fully integrated Business Model

7/30/2019 BVMF Presentation - July 2011

http://slidepdf.com/reader/full/bvmf-presentation-july-2011 29/51

Listing(stocks, bonds, funds,

asset-backed securities,

Among others )

Commodities

Certification

Trading

(stocks, derivatives, corporate and government

Bonds, funds, spot US Dollar, among others)

Central Counterparty (CCP)

Clearing and Settlement

(for all products)

Central Depository

(stocks and corporate bonds)

Securities Lending

(stocks and corporate bonds

Custody(services provided for funds

and other market

participants)

Market Data

Indices Licensing

Software Licensing

(used by brokerage

Houses and other

market participants)

OTC Derivatives

(registration and collateral

management)

Fully integrated Business ModelDiversified sources of revenues

Services for issuers, brokers and

commodities tradingTrading, Clearing and Depository Activities Others Services

29

Trading Access

(Brokers)

ll i l i d di i

7/30/2019 BVMF Presentation - July 2011

http://slidepdf.com/reader/full/bvmf-presentation-july-2011 30/51

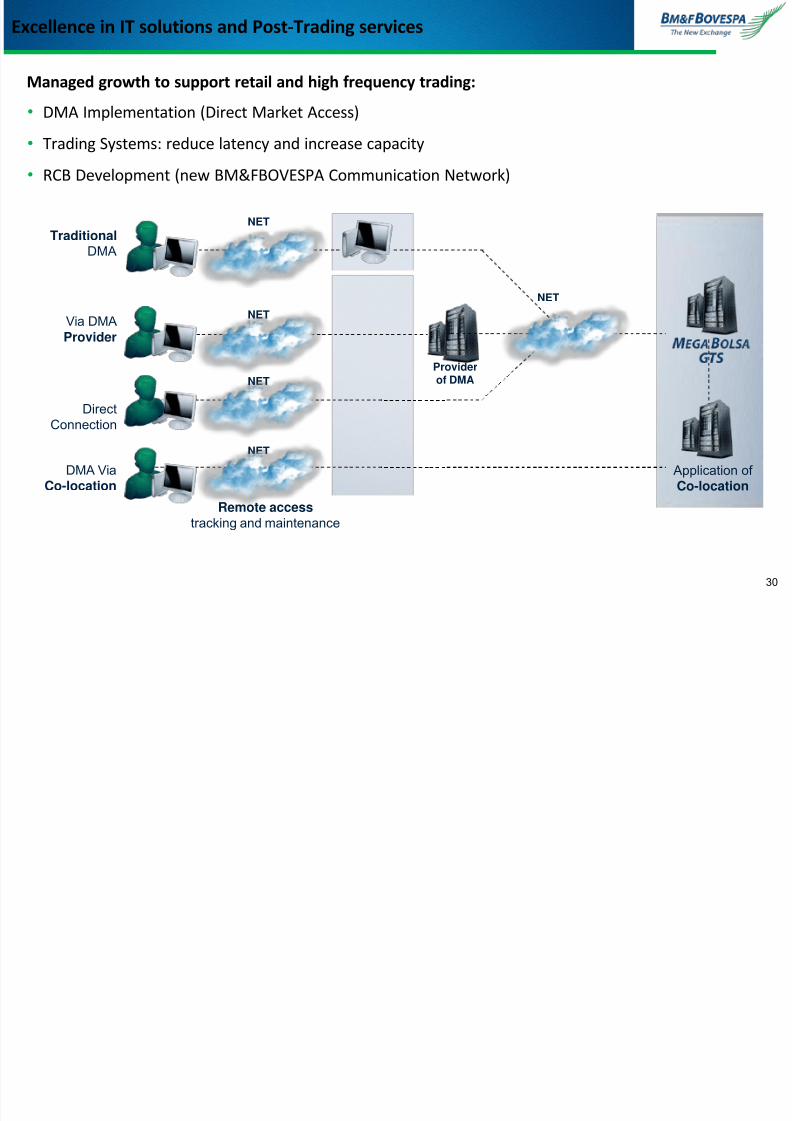

Managed growth to support retail and high frequency trading:

• DMA Implementation (Direct Market Access)

• Trading Systems: reduce latency and increase capacity

• RCB Development (new BM&FBOVESPA Communication Network)

DMA ViaCo-location

TraditionalDMA

Via DMAProvider

DirectConnection

NET

NET

NET

NET

Remote accesstracking and maintenance

Application of Co-location

NET

Providerof DMA

Excellence in IT solutions and Post-Trading services

30

BM&FBOVESPA Costs

7/30/2019 BVMF Presentation - July 2011

http://slidepdf.com/reader/full/bvmf-presentation-july-2011 31/51

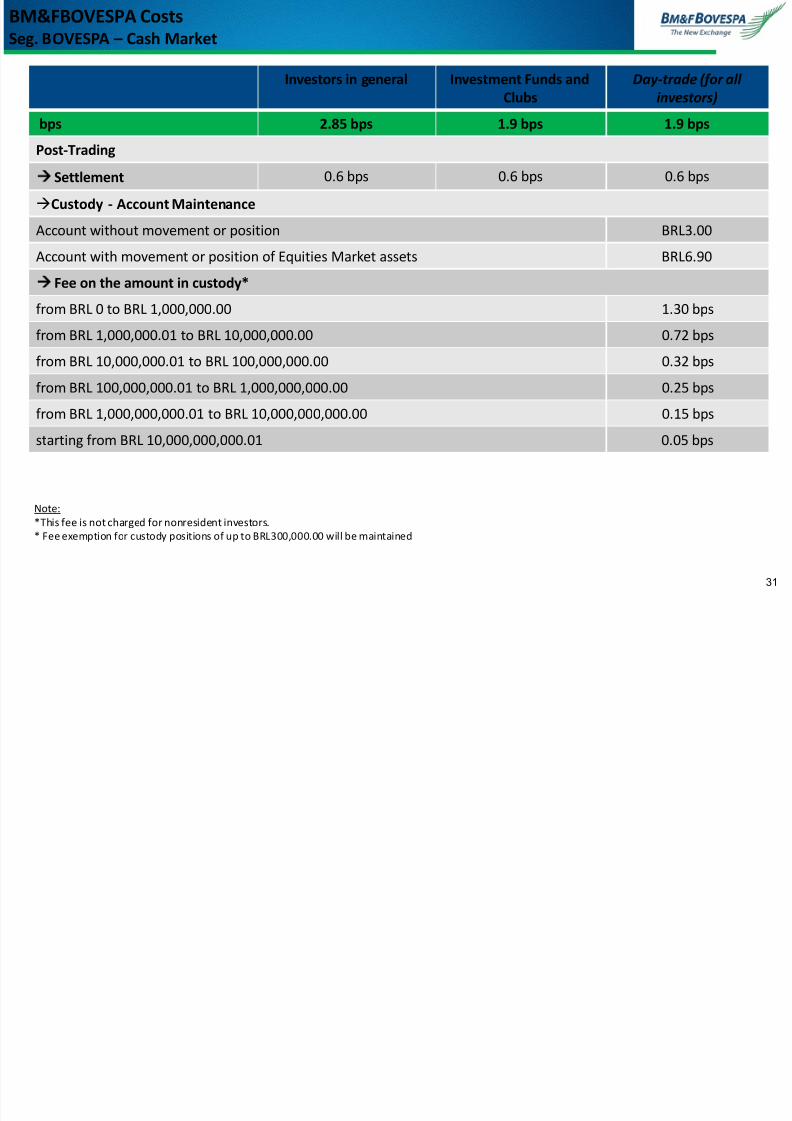

BM&FBOVESPA CostsSeg. BOVESPA – Cash Market

Investors in general Investment Funds and

Clubs

Day-trade (for all

investors)

bps 2.85 bps 1.9 bps 1.9 bps

Post-Trading

Settlement 0.6 bps 0.6 bps 0.6 bps

Custody - Account Maintenance

Account without movement or position BRL3.00

Account with movement or position of Equities Market assets BRL6.90

Fee on the amount in custody*

from BRL 0 to BRL 1,000,000.00 1.30 bps

from BRL 1,000,000.01 to BRL 10,000,000.00 0.72 bps

from BRL 10,000,000.01 to BRL 100,000,000.00 0.32 bps

from BRL 100,000,000.01 to BRL 1,000,000,000.00 0.25 bps

from BRL 1,000,000,000.01 to BRL 10,000,000,000.00 0.15 bpsstarting from BRL 10,000,000,000.01 0.05 bps

Note:

*This fee is not charged for nonresident investors.

* Fee exemption for custody positions of up to BRL300,000.00 will be maintained

31

N P d Pi li

High Frequency Trading - HFT

7/30/2019 BVMF Presentation - July 2011

http://slidepdf.com/reader/full/bvmf-presentation-july-2011 32/51

New Products Pipeline

32

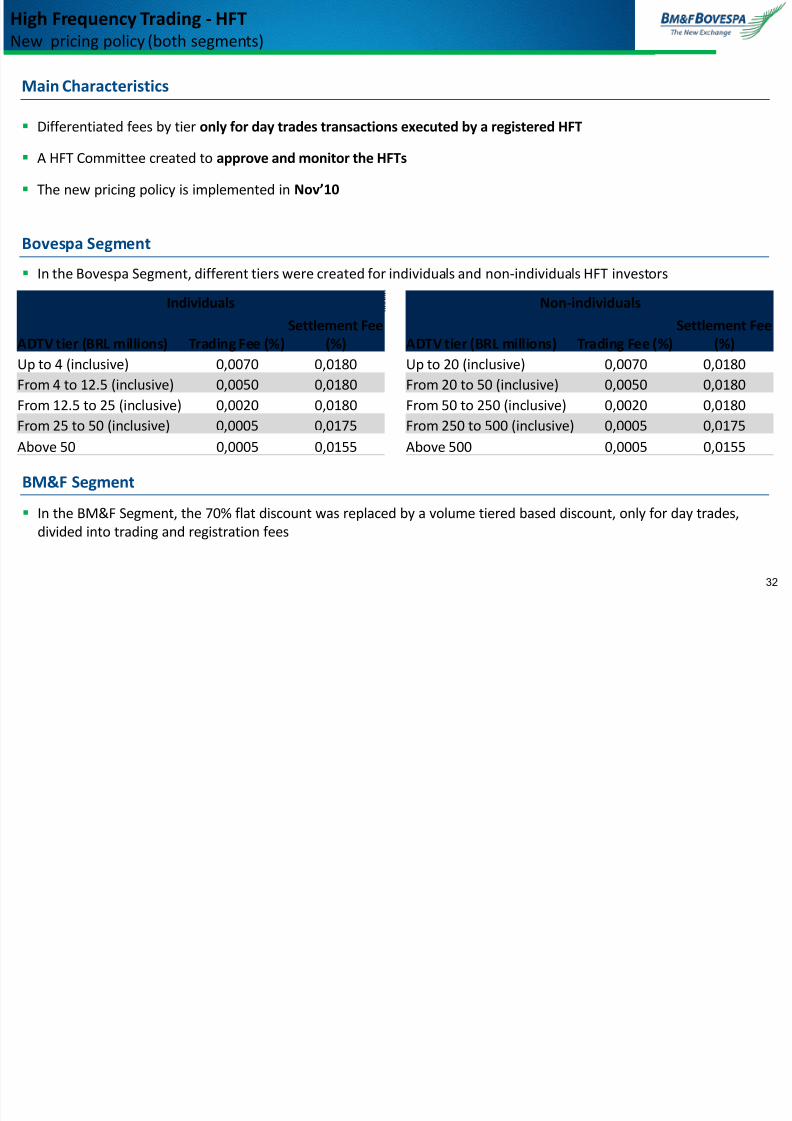

High Frequency Trading HFTNew pricing policy (both segments)

Main Characteristics

Differentiated fees by tier only for day trades transactions executed by a registered HFT

A HFT Committee created to approve and monitor the HFTs

The new pricing policy is implemented in Nov’10

Bovespa Segment

In the Bovespa Segment, different tiers were created for individuals and non-individuals HFT investors

BM&F Segment

In the BM&F Segment, the 70% flat discount was replaced by a volume tiered based discount, only for day trades,

divided into trading and registration fees

Individuals

ADTV tier (BRL millions) Trading Fee (%)

Settlement Fee

(%)

Up to 4 (inclusive) 0,0070 0,0180

From 4 to 12.5 (inclusive) 0,0050 0,0180

From 12.5 to 25 (inclusive) 0,0020 0,0180

From 25 to 50 (inclusive) 0,0005 0,0175

Above 50 0,0005 0,0155

Non-individuals

ADTV tier (BRL millions) Trading Fee (%)

Settlement Fee

(%)

Up to 20 (inclusive) 0,0070 0,0180

From 20 to 50 (inclusive) 0,0050 0,0180

From 50 to 250 (inclusive) 0,0020 0,0180

From 250 to 500 (inclusive) 0,0005 0,0175

Above 500 0,0005 0,0155

7/30/2019 BVMF Presentation - July 2011

http://slidepdf.com/reader/full/bvmf-presentation-july-2011 33/51

*Includes regular trades and public offering; updated until June 30th, 2011.

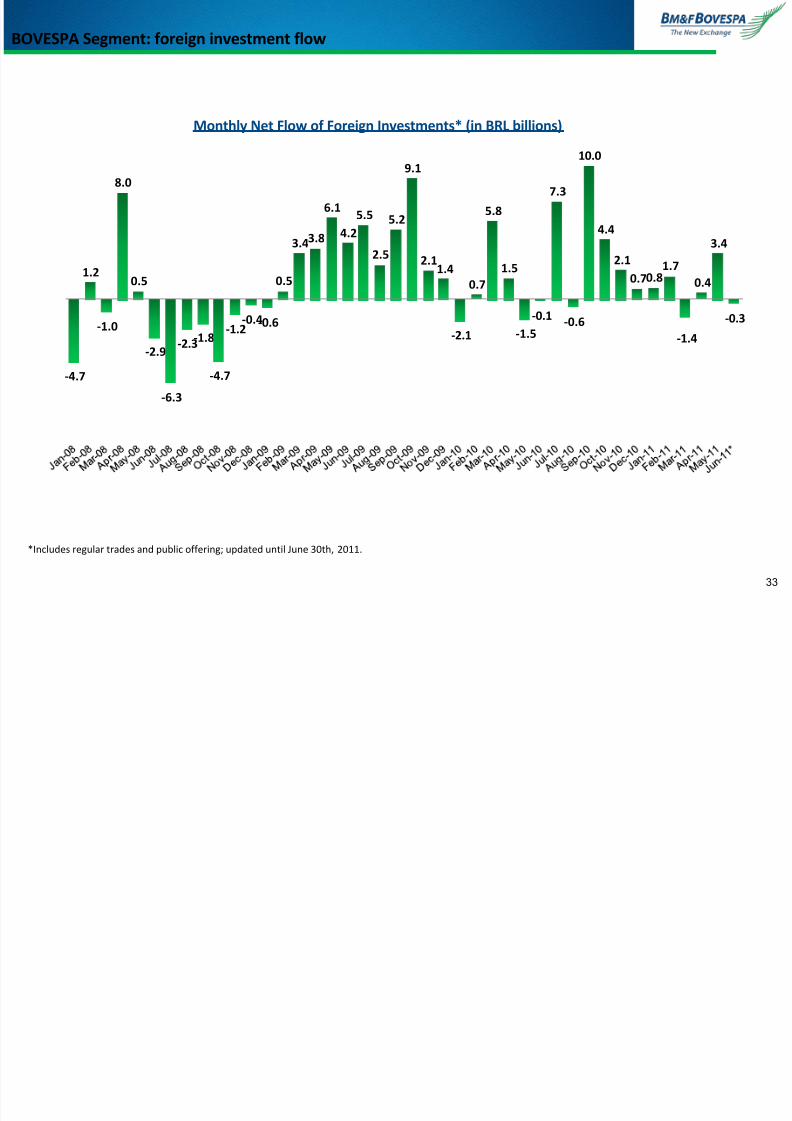

Monthly Net Flow of Foreign Investments* (in BRL billions)

BOVESPA Segment: foreign investment flow

33

-4.7

1.2

-1.0

8.0

0.5

-2.9

-6.3

-2.3-1.8

-4.7

-1.2-0.4-0.6

0.5

3.43.8

6.1

4.2

5.5

2.5

5.2

9.1

2.11.4

-2.1

0.7

5.8

1.5

-1.5

-0.1

7.3

-0.6

10.0

4.4

2.1

0.70.8

1.7

-1.4

0.4

3.4

-0.3

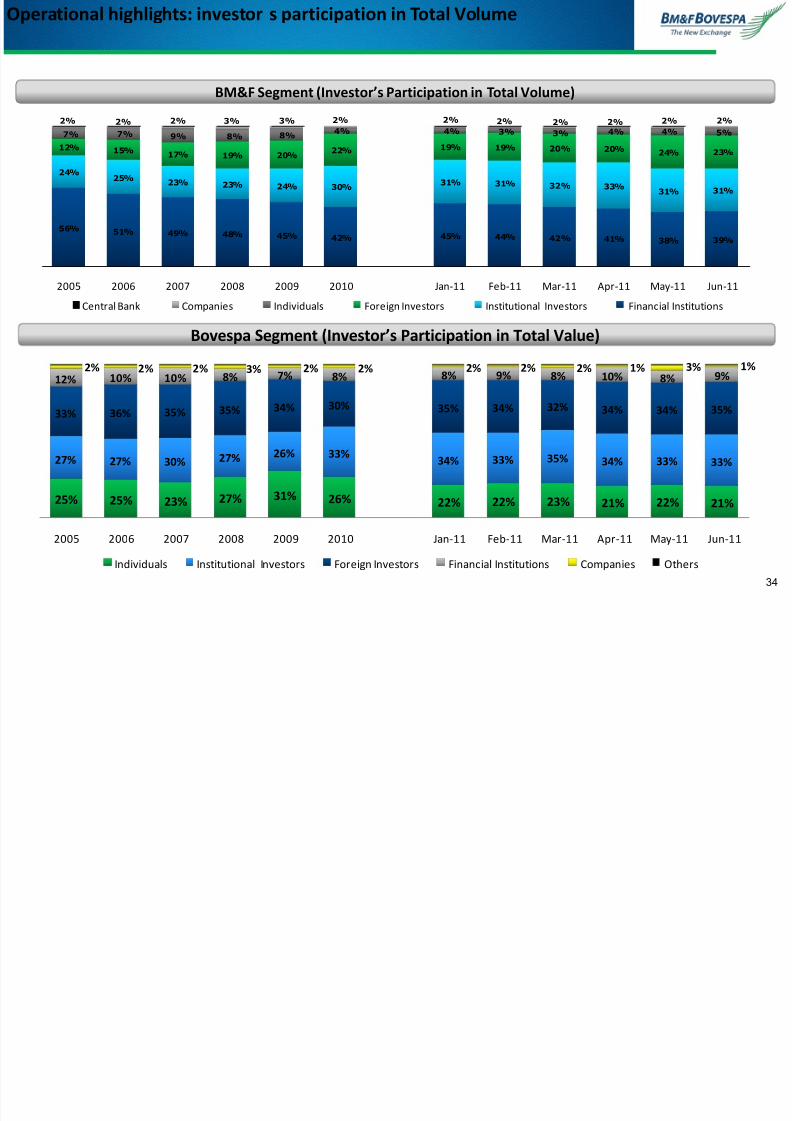

Operational highlights: investor s participation in Total Volume

7/30/2019 BVMF Presentation - July 2011

http://slidepdf.com/reader/full/bvmf-presentation-july-2011 34/51

BM&F Segment (Investor’s Participation in Total Volume)

Bovespa Segment (Investor’s Participation in Total Value)

p g g p p

34

56%51% 49% 48% 45% 42% 45% 44% 42% 41% 38% 39%

24%25%

23% 23% 24% 30%31% 31% 32% 33%

31% 31%

12% 15%17% 19% 20%

22%19% 19% 20% 20%

24% 23%

7% 7% 9% 8% 8%4% 4% 3% 3% 4% 4% 5%

2% 2% 2% 3% 3% 2% 2% 2% 2% 2% 2% 2%

2005 2006 2007 2008 2009 2010 Jan-11 Feb-11 Mar-11 Apr-11 May-11 Jun-11

Central Bank Companies Individuals Foreign Investors Institutional Investors Financial Institutions

25% 25% 23% 27% 31% 26% 22% 22% 23% 21% 22% 21%

27% 27% 30% 27% 26% 33%34% 33% 35% 34% 33% 33%

33%36% 35% 35% 34% 30% 35% 34% 32% 34% 34% 35%

12% 10% 10% 8% 7% 8% 8% 9% 8% 10% 8% 9%2% 2% 2% 3% 2% 2% 2% 2% 2% 1% 3% 1%

2005 2006 2007 2008 2009 2010 Jan-11 Feb-11 Mar-11 Apr-11 May-11 Jun-11

Individuals Institutional Investors Foreign Investors Financial Institutions Companies Others

7/30/2019 BVMF Presentation - July 2011

http://slidepdf.com/reader/full/bvmf-presentation-july-2011 35/51

SUSTAINABILITY

35

BM&FBOVESPA Sustainability Mission

7/30/2019 BVMF Presentation - July 2011

http://slidepdf.com/reader/full/bvmf-presentation-july-2011 36/51

BM&FBOVESPA’s Sustainability Mission“Support, promote and practice the concepts and actions towards economic,

social and environmental responsibility with the purpose of contributing to

sustainable development”

36

BM&FBOVESPA Sustainability Mission

Novo Valor BM&FBOVESPA

Program created in 2010 to guide sustainability actions of

BVMF.Goal

Induce and promote the sustainable development of theBM&FBOVESPA and the capital market, involving all audiences,including investors, companies and brokerages.

BM&FBOVESPA Sustainability Program

7/30/2019 BVMF Presentation - July 2011

http://slidepdf.com/reader/full/bvmf-presentation-july-2011 37/51

1. Natural Resources Mgt

• GHG Inventory

• Materials recycling program

• Ecoefficiency

• Green IT

• Member of Carbon Disclosure Project South America

• Board of Empresas pelo Clima, FGV

2. Governance

• Novo Mercado

• Advisory Boards

• Sustainability Committee

• Sustainability Comission

3. Products and Services

• Indexes: ISE, ICO2 and IGC/IGCT

• Carbon Market

• Em Boa Companhia ( program with companies)

4. Stakeholder Engagement

• Instituto BM&FBOVESPA

• Stakeholders

• Global Compact Signatory (1st exchange)

• PRI Signatory (Principles for Responsible Investment)

• Organization Stakeholder GRI (Global ReportingInitiative) ; Member of Board for GRI Brazil

y gWorking in four dimensions

37

7/30/2019 BVMF Presentation - July 2011

http://slidepdf.com/reader/full/bvmf-presentation-july-2011 38/51

1Q11 EARNINGS

38

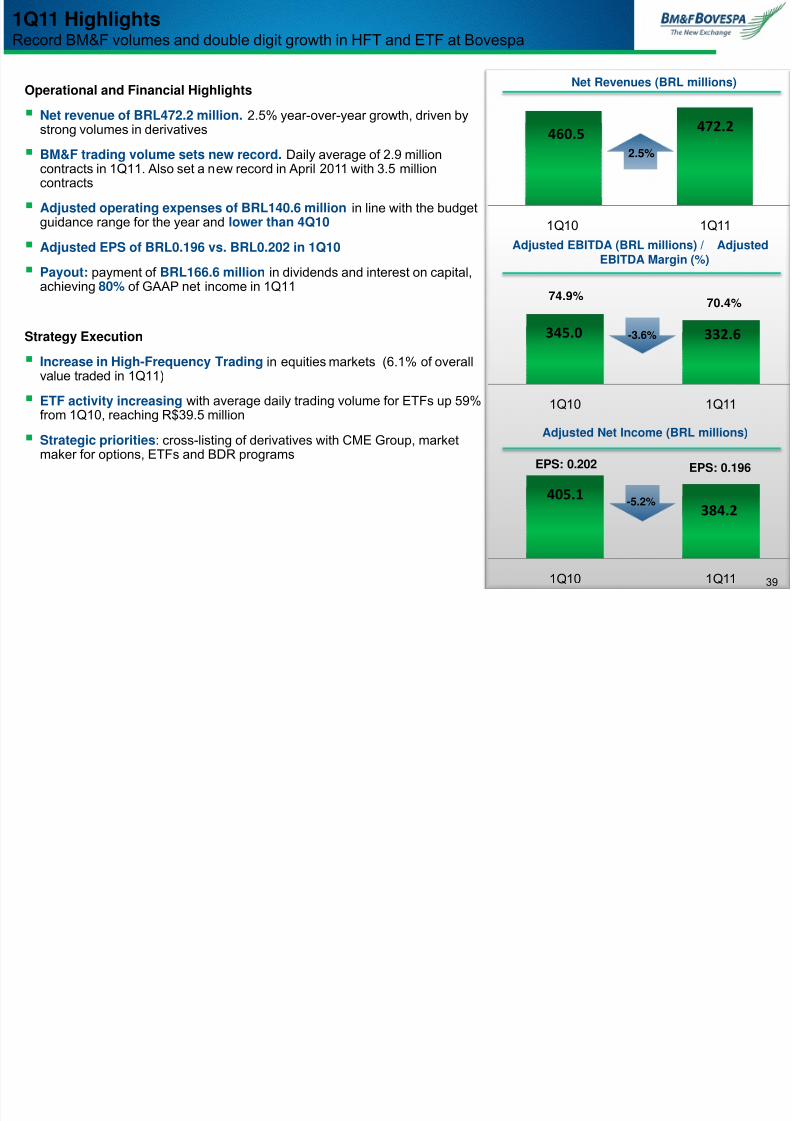

1Q11 Highlights

7/30/2019 BVMF Presentation - July 2011

http://slidepdf.com/reader/full/bvmf-presentation-july-2011 39/51

Operational and Financial Highlights

Net revenue of BRL472.2 million. 2.5% year-over-year growth, driven bystrong volumes in derivatives

BM&F trading volume sets new record. Daily average of 2.9 millioncontracts in 1Q11. Also set a new record in April 2011 with 3.5 millioncontracts

Adjusted operating expenses of BRL140.6 million in line with the budgetguidance range for the year and lower than 4Q10

Adjusted EPS of BRL0.196 vs. BRL0.202 in 1Q10

Payout: payment of BRL166.6 million in dividends and interest on capital,achieving 80% of GAAP net income in 1Q11

Strategy Execution

Increase in High-Frequency Trading in equities markets (6.1% of overallvalue traded in 1Q11)

ETF activity increasing with average daily trading volume for ETFs up 59%

from 1Q10, reaching R$39.5 million Strategic priorities: cross-listing of derivatives with CME Group, market

maker for options, ETFs and BDR programs

460.5472.2

1Q10 1Q11

345.0 332.6

1Q10 1Q11

405.1384.2

1Q10 1Q11

Net Revenues (BRL millions)

Adjusted EBITDA (BRL millions) / AdjustedEBITDA Margin (%)

Q g gRecord BM&F volumes and double digit growth in HFT and ETF at Bovespa

Adjusted Net Income (BRL millions)

-3.6%

2.5%

EPS: 0.202 EPS: 0.196

-5.2%

74.9%70.4%

39

Revenues – 1Q11 vs. 1Q10

7/30/2019 BVMF Presentation - July 2011

http://slidepdf.com/reader/full/bvmf-presentation-july-2011 40/51

Revenues in BM&F segment grew 10% year-over-year

In BRL thousands 1Q11 1Q10% Change

1Q11 x 1Q10

Gross operating revenues 525,477 512,049 2.6%BOVESPA Trd. / Sttmnt. 251,716 256,494 -1.9%

BM&F Trd. / Sttmnt. 186,662 170,213 9.7%

Other operating revenues 87,099 85,342 2.1%

Depositary and custody 22,105 20,890 5.8%

Vendors 16,224 19,628 -17.3%

Securities Lending 15,405 10,520 46.4%Trading access (Brokers) 12,470 12,446 0.2%

Listing 11,276 11,511 -2.0%

Bank 4,711 3,288 43.3%

Other 2,489 5,945 -58.1%

Bolsa Brasileira de Mercadorias 2,419 1,114 117.1%

48%

35%

17%

Bovespa Trd. / Sttmnt

BM&F Trd. / Sttmnt

Other operational revenuesOperating performance 1Q11 1Q10% Change

1Q11 x 1Q10

BOVESPAADTV - in BRL millions 6,735.4 6,599.6 2.1%

Margin - in bps 6.017 6.361 -0.34bp

BM&F ADTV - in thousands 2,865.8 2,453.6 16.8%

RPC - in BRL 1.040 1.126 -7.6%

40

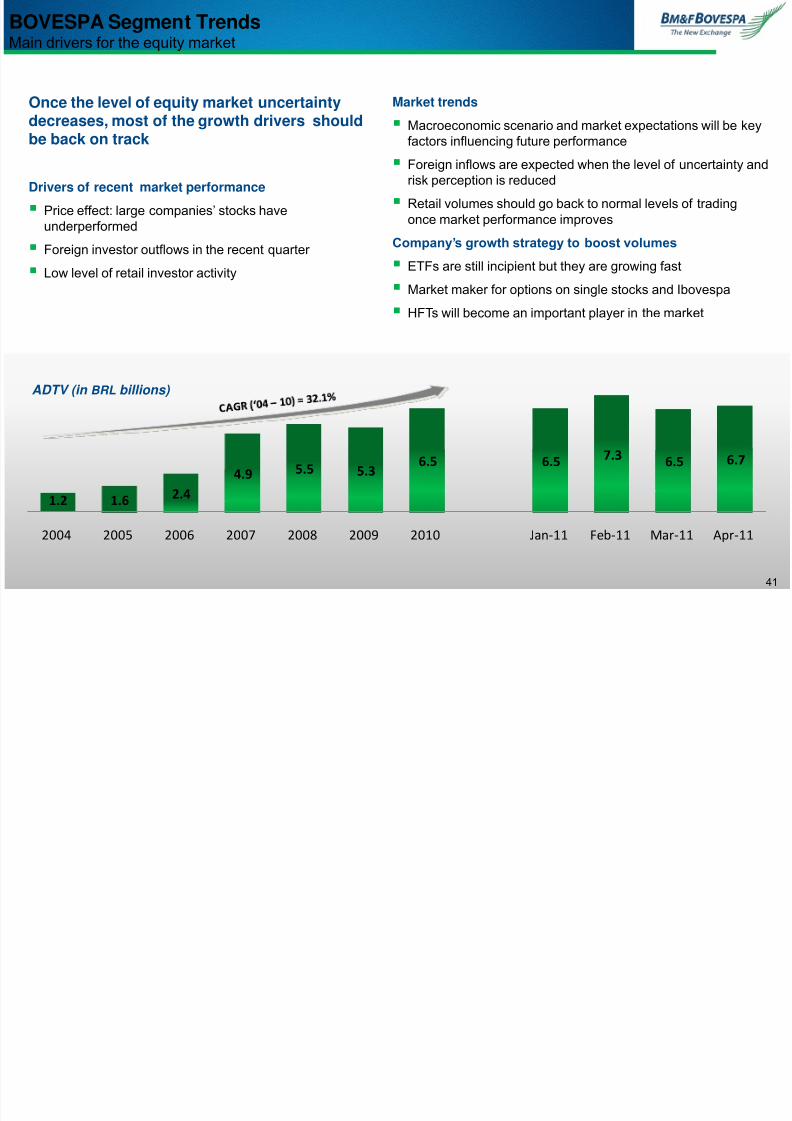

BOVESPA Segment Trends

7/30/2019 BVMF Presentation - July 2011

http://slidepdf.com/reader/full/bvmf-presentation-july-2011 41/51

Once the level of equity market uncertaintydecreases, most of the growth drivers should

be back on track

Drivers of recent market performance

Price effect: large companies’ stocks have

underperformed

Foreign investor outflows in the recent quarter

Low level of retail investor activity

1.2 1.6 2.4

4.9 5.5 5.36.5 6.5 7.3 6.5 6.7

2004 2005 2006 2007 2008 2009 2010 Jan-11 Feb-11 Mar-11 Apr-11

BOVESPA Segment TrendsMain drivers for the equity market

Market trends

Macroeconomic scenario and market expectations will be key

factors influencing future performance Foreign inflows are expected when the level of uncertainty and

risk perception is reduced

Retail volumes should go back to normal levels of tradingonce market performance improves

Company’s growth strategy to boost volumes

ETFs are still incipient but they are growing fast

Market maker for options on single stocks and Ibovespa

HFTs will become an important player in the market

ADTV (in BRL billions)

41

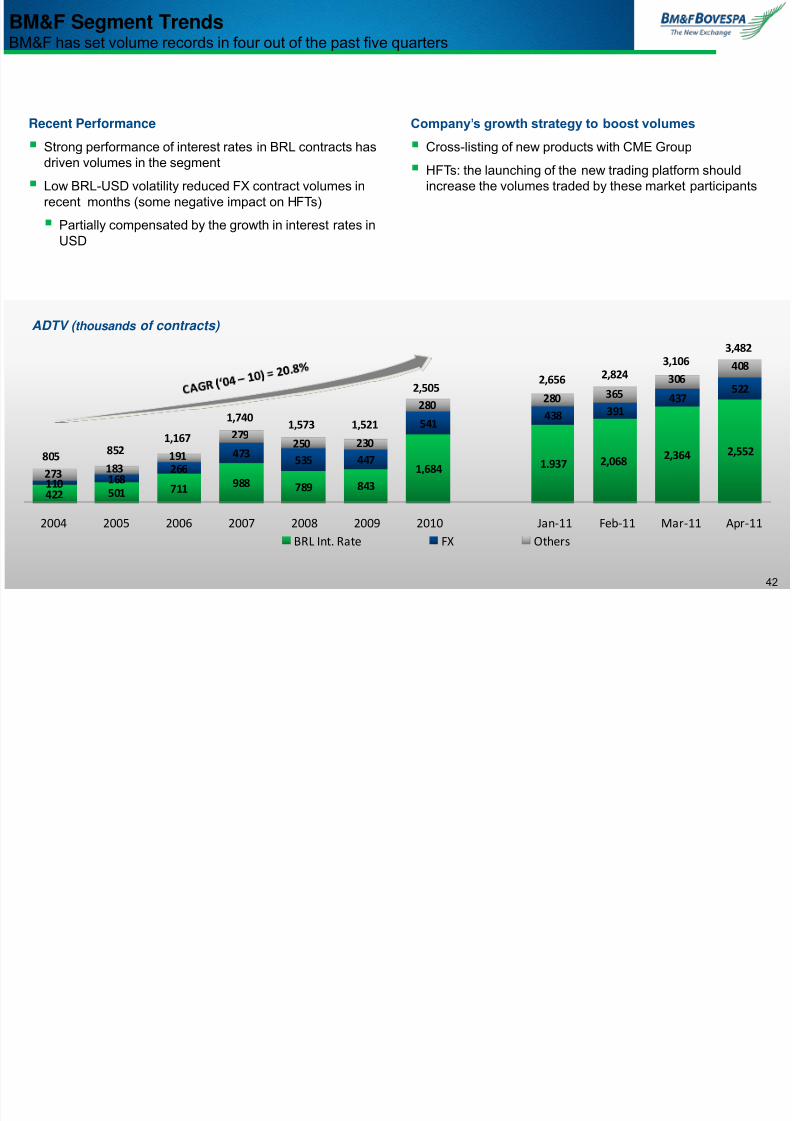

BM&F Segment Trends

7/30/2019 BVMF Presentation - July 2011

http://slidepdf.com/reader/full/bvmf-presentation-july-2011 42/51

Recent Performance

Strong performance of interest rates in BRL contracts hasdriven volumes in the segment

Low BRL-USD volatility reduced FX contract volumes inrecent months (some negative impact on HFTs)

Partially compensated by the growth in interest rates inUSD

Company’s growth strategy to boost volumes

Cross-listing of new products with CME Group

HFTs: the launching of the new trading platform shouldincrease the volumes traded by these market participants

& Seg e t e dsBM&F has set volume records in four out of the past five quarters

ADTV ( thousands of contracts)

422 501 711988 789 843

1,684 1.937 2,0682,364 2,552

110 168266

473535 447

541 438

391437

522

273 183191

279250 230

280280 365

306408

2004 2005 2006 2007 2008 2009 2010 Jan-11 Feb-11 Mar-11 Apr-11

BRL Int. Rate FX Others

3,4823,106

2,8242,6562,505

1,5211,5731,7401,167

852805

42

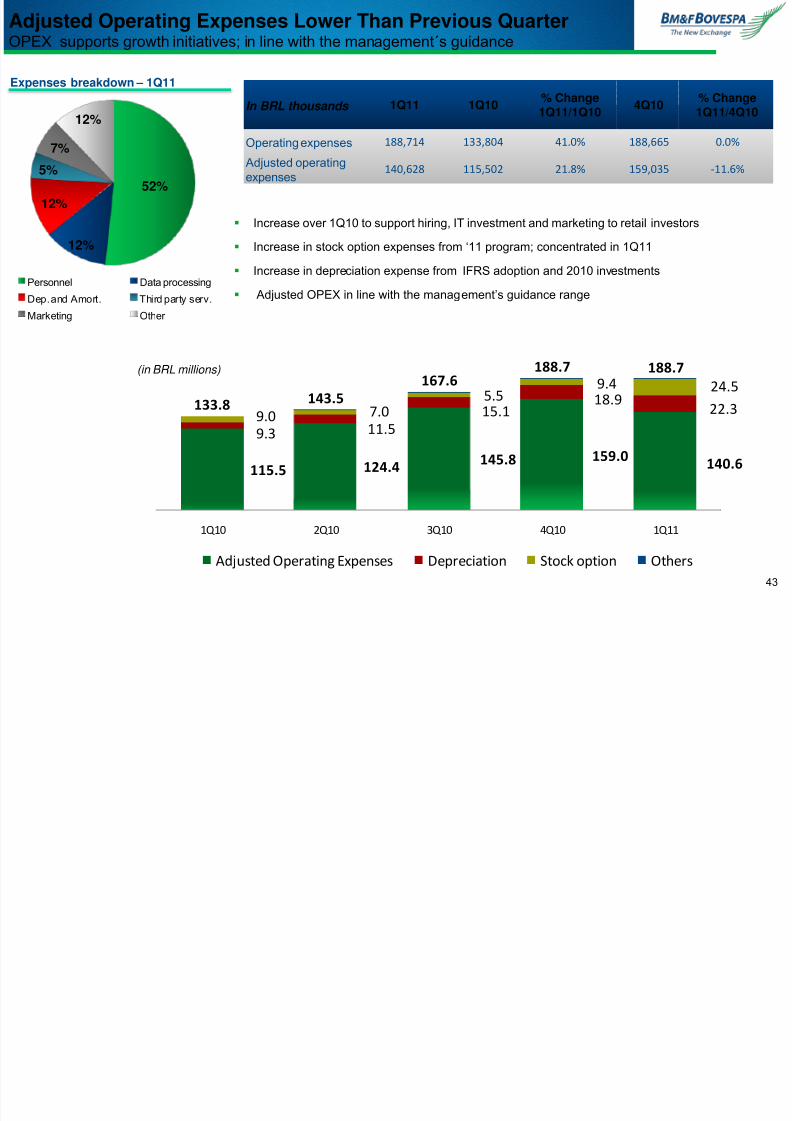

Adjusted Operating Expenses Lower Than Previous Quarter

7/30/2019 BVMF Presentation - July 2011

http://slidepdf.com/reader/full/bvmf-presentation-july-2011 43/51

j p g pOPEX supports growth initiatives; in line with the management´s guidance

Expenses breakdown – 1Q11

52%

12%

12%

5%

7%

12%

Personnel Data processingDep. and Amort. Third party serv.

Marketing Other

Increase over 1Q10 to support hiring, IT investment and marketing to retail investors

Increase in stock option expenses from ‘11 program; concentrated in 1Q11

Increase in depreciation expense from IFRS adoption and 2010 investments

Adjusted OPEX in line with the management’s guidance range

(in BRL millions)

In BRL thousands 1Q11 1Q10% Change1Q11/1Q10

4Q10% Change1Q11/4Q10

Operating expenses 188,714 133,804 41.0% 188,665 0.0% Adjusted operatingexpenses

140,628 115,502 21.8% 159,035 -11.6%

115.5 124.4145.8 159.0

140.6

9.3 11.515.1

18.922.3

9.07.0

5.59.4 24.5

1Q10 2Q10 3Q10 4Q10 1Q11

Adjusted Operating Expenses Depreciation Stock option Others

133.8 143.5

167.6188.7 188.7

43

Strategic investments to enhance growthI i h d d k i h

7/30/2019 BVMF Presentation - July 2011

http://slidepdf.com/reader/full/bvmf-presentation-july-2011 44/51

54.7 57.4 66.280.9 72.9

9.0 7.05.5

9.4 24.5

1Q10 2Q10 3Q10 4Q10 1Q11

Adj. PersonnelStock Options

5.39.9

15.811.4 13.4

1Q10 2Q10 3Q10 4Q10 1Q11

Average: BRL13.6

Increase of 28.3% in the average headcount (particularly in IT and business development areas), in line with our growth strategy to strength the core business areas of the Company

Due to the recognition of the expenses of a new stock option program granted in 2011, the amount of stock option

expenses recognized in the 1Q11 rose to BRL24.5 million (most of this additional expense is concentrated in the1Q11). In 2010 there was no new program granted

Collective bargaining agreement: 6% annual salary increase (Aug. 2010)

Increases in headcount and marketing to support growth strategy

33.2%

151.3%

Programs to attract more retailinvestors to the market

Intensification of marketingactivities and strengthening of Financial Education campaigns

38.9%

AdjustedPersonnel

(1Q11 x 1Q10)

Marketing

(1Q11 x 1Q10)

Marketing and Promotion Expenses – R$ millions

Personnel Expenses (R$ millions)

9.9%

The 4Q10 was impacted byprofit-sharing distribution toemployees.

AdjustedPersonnel

(1Q11 x 4Q10)

59,6

30,9

2009 2010

Stock Option Expenses(R$ millions)

44

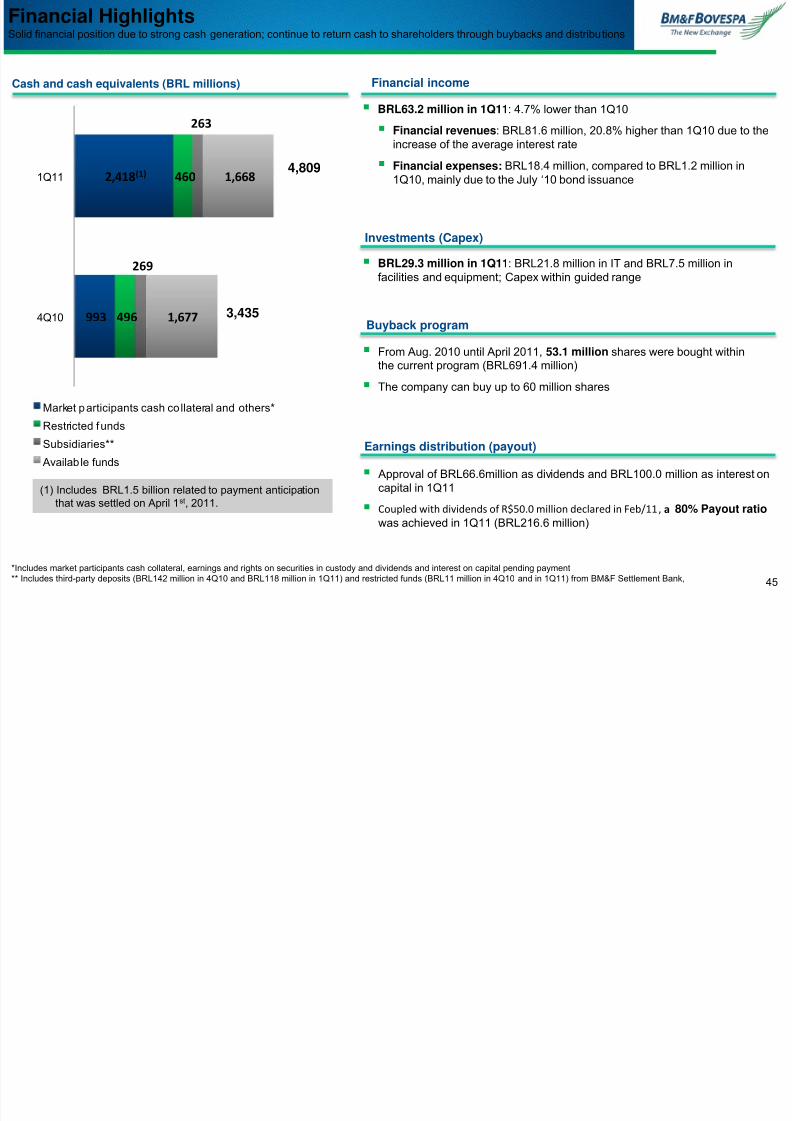

Financial HighlightsS lid fi i l iti d t t h ti ti t t h t h h ld th h b b k d di t ib ti

7/30/2019 BVMF Presentation - July 2011

http://slidepdf.com/reader/full/bvmf-presentation-july-2011 45/51

BRL29.3 million in 1Q11: BRL21.8 million in IT and BRL7.5 million in

facilities and equipment; Capex within guided range

3,435

4,809

*Includes market participants cash collateral, earnings and rights on securities in custody and dividends and interest on capital pending payment** Includes third-party deposits (BRL142 million in 4Q10 and BRL118 million in 1Q11) and restricted funds (BRL11 million in 4Q10 and in 1Q11) from BM&F Settlement Bank,

Solid financial position due to strong cash generation; continue to return cash to shareholders through buybacks and distributions

BRL63.2 million in 1Q11: 4.7% lower than 1Q10

Financial revenues: BRL81.6 million, 20.8% higher than 1Q10 due to the

increase of the average interest rate

Financial expenses: BRL18.4 million, compared to BRL1.2 million in1Q10, mainly due to the July ‘10 bond issuance

Investments (Capex)

From Aug. 2010 until April 2011, 53.1 million shares were bought withinthe current program (BRL691.4 million)

The company can buy up to 60 million shares

Buyback program

Approval of BRL66.6million as dividends and BRL100.0 million as interest oncapital in 1Q11

Coupled with dividends of R$50.0 million declared in Feb/11, a 80% Payout ratiowas achieved in 1Q11 (BRL216.6 million)

Earnings distribution (payout)

Cash and cash equivalents (BRL millions) Financial income

(1) Includes BRL1.5 billion related to payment anticipationthat was settled on April 1st, 2011.

993

2,418(1)

496

460

269

263

1,677

1,668

4Q10

1Q11

Market participants cash collateral and others*

Restricted funds

Subsidiaries**

Available funds

45

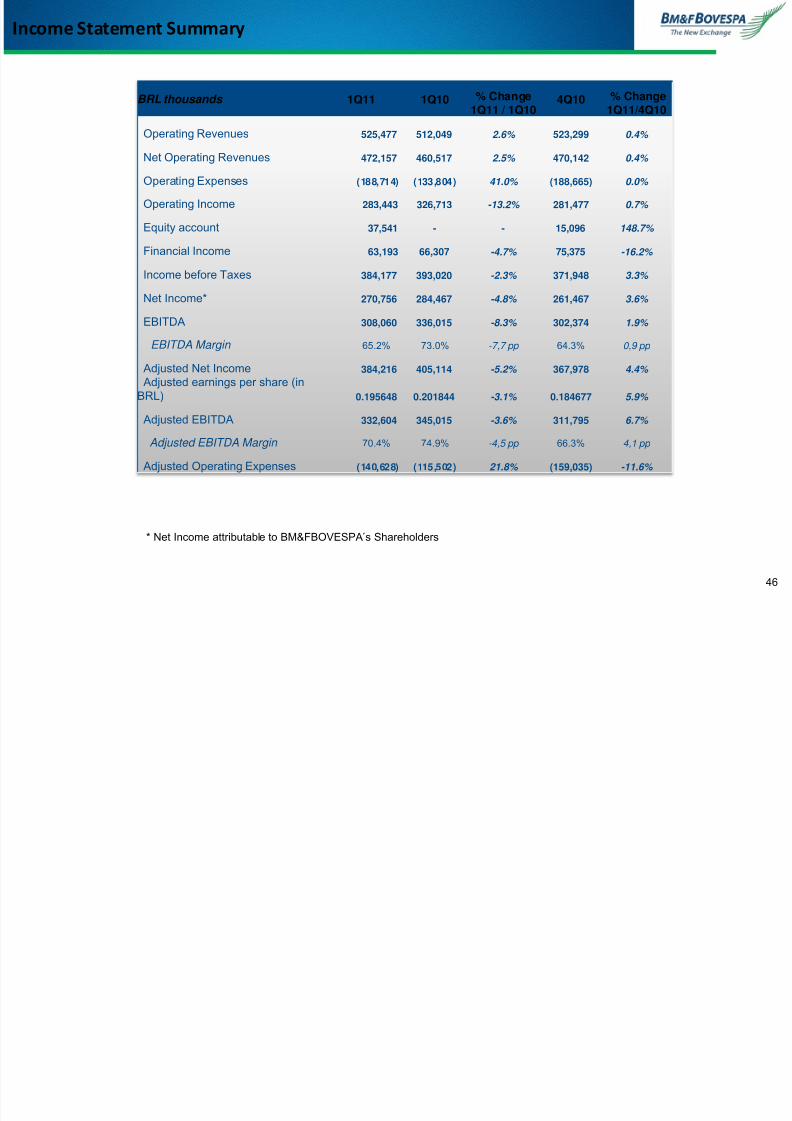

Income Statement Summary

7/30/2019 BVMF Presentation - July 2011

http://slidepdf.com/reader/full/bvmf-presentation-july-2011 46/51

Income Statement Summary

BRL thousands 1Q11 1Q10 % Change1Q11 / 1Q10

4Q10 % Change1Q11/4Q10

Operating Revenues 525,477 512,049 2.6% 523,299 0.4%

Net Operating Revenues 472,157 460,517 2.5% 470,142 0.4%

Operating Expenses (188,714) (133,804) 41.0% (188,665) 0.0%

Operating Income 283,443 326,713 -13.2% 281,477 0.7%

Equity account 37,541 - - 15,096 148.7%

Financial Income 63,193 66,307 -4.7% 75,375 -16.2%

Income before Taxes 384,177 393,020 -2.3% 371,948 3.3%

Net Income* 270,756 284,467 -4.8% 261,467 3.6%

EBITDA 308,060 336,015 -8.3% 302,374 1.9%

EBITDA Margin 65.2% 73.0% -7,7 pp 64.3% 0,9 pp

Adjusted Net Income 384,216 405,114 -5.2% 367,978 4.4%

Adjusted earnings per share (inBRL) 0.195648 0.201844 -3.1% 0.184677 5.9%

Adjusted EBITDA 332,604 345,015 -3.6% 311,795 6.7%

Adjusted EBITDA Margin 70.4% 74.9% -4,5 pp 66.3% 4,1 pp

Adjusted Operating Expenses (140,628) (115,502) 21.8% (159,035) -11.6%

* Net Income attributable to BM&FBOVESPA´s Shareholders

46

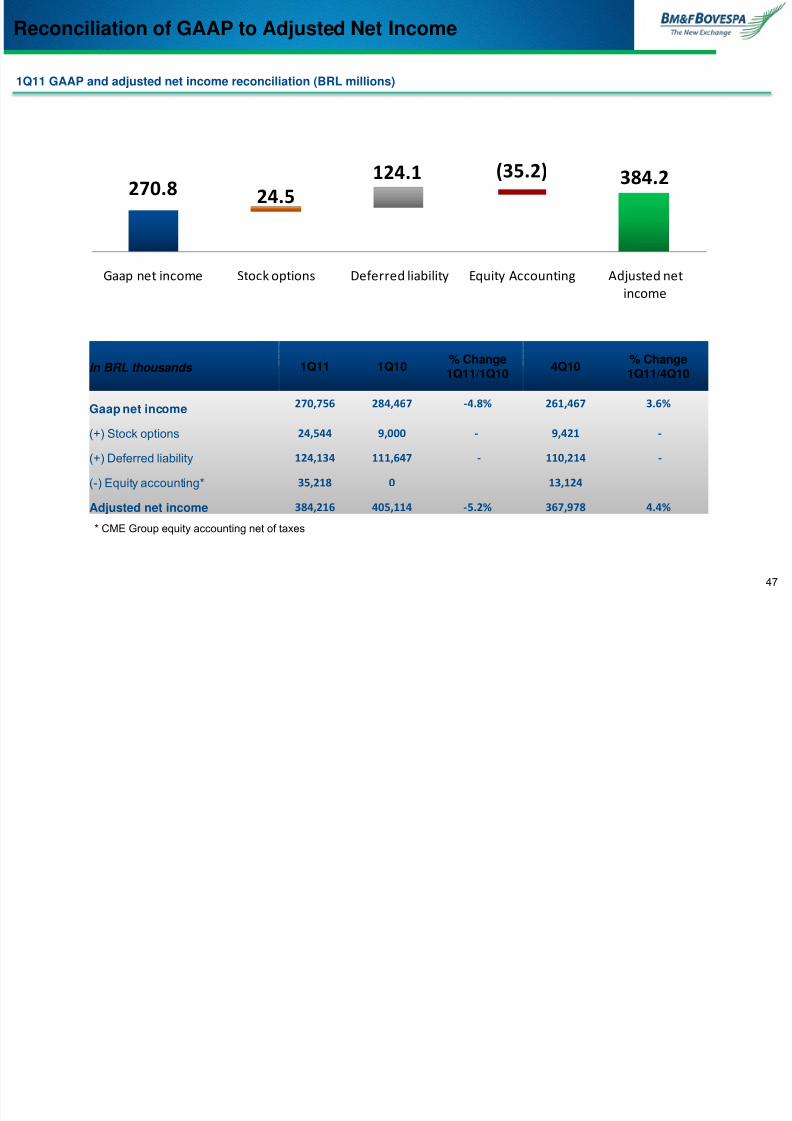

Reconciliation of GAAP to Adjusted Net Income

7/30/2019 BVMF Presentation - July 2011

http://slidepdf.com/reader/full/bvmf-presentation-july-2011 47/51

Reconciliation of GAAP to Adjusted Net Income

In BRL thousands 1Q11 1Q10% Change1Q11/1Q10

4Q10% Change1Q11/4Q10

Gaap net income 270,756 284,467 -4.8% 261,467 3.6%

(+) Stock options 24,544 9,000 - 9,421 -

(+) Deferred liability 124,134 111,647 - 110,214 -

(-) Equity accounting* 35,218 0 13,124

Adjusted net income 384,216 405,114 -5.2% 367,978 4.4%

1Q11 GAAP and adjusted net income reconciliation (BRL millions)

* CME Group equity accounting net of taxes

270.8(35.2) 384.2

24.5

124.1

Gaap net income Stock options Deferred liability Equity Accounting Adjusted net

income

47

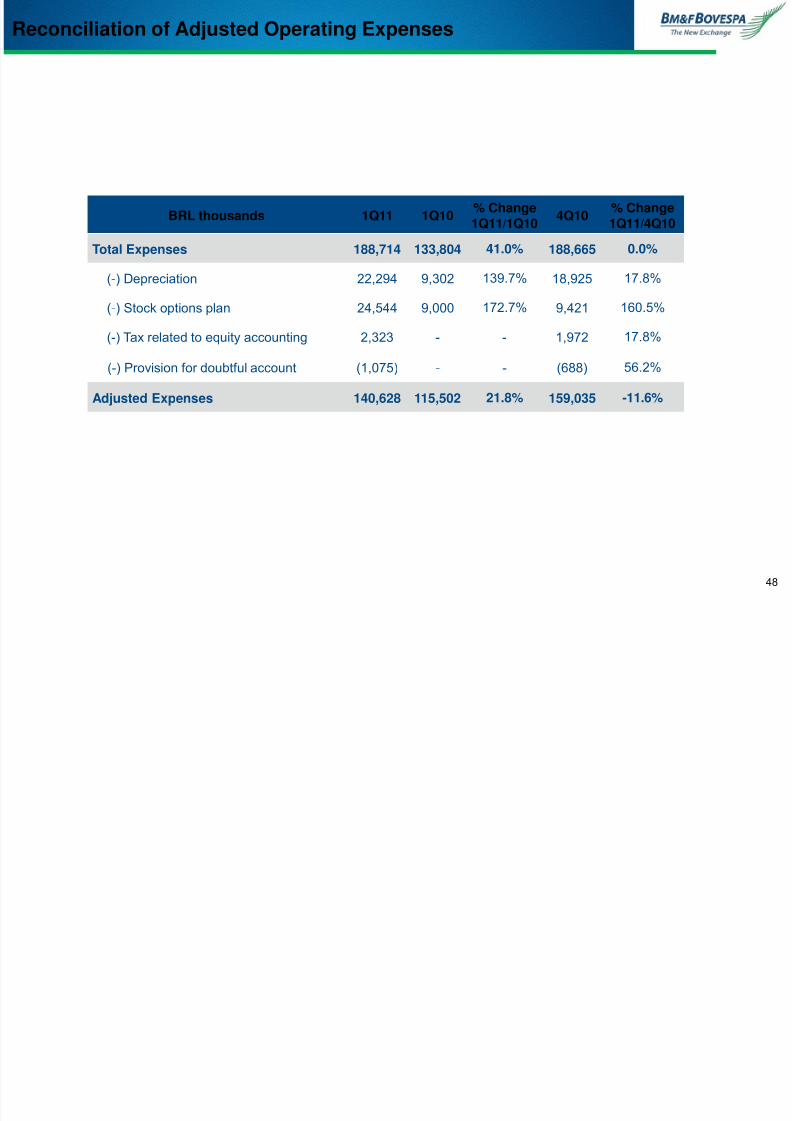

Reconciliation of Adjusted Operating Expenses

7/30/2019 BVMF Presentation - July 2011

http://slidepdf.com/reader/full/bvmf-presentation-july-2011 48/51

BRL thousands 1Q11 1Q10% Change1Q11/1Q10

4Q10% Change1Q11/4Q10

Total Expenses 188,714 133,804 41.0% 188,665 0.0%

(-) Depreciation 22,294 9,302 139.7% 18,925 17.8%

(-) Stock options plan 24,544 9,000 172.7% 9,421 160.5%

(-) Tax related to equity accounting 2,323 - - 1,972 17.8%

(-) Provision for doubtful account (1,075) - - (688) 56.2%

Adjusted Expenses 140,628 115,502 21.8% 159,035 -11.6%

Reconciliation of Adjusted Operating Expenses

48

Balance Sheet

7/30/2019 BVMF Presentation - July 2011

http://slidepdf.com/reader/full/bvmf-presentation-july-2011 49/51

ASSETS 03/31/2011 12/31/2010LIABILITIES AND SHAREHOLDERS'

EQUITY03/31/2011 12/31/2010

Current assets 3,779,796 2,547,589 Current liabilities 2,751,091 1,416,204

Cash and cash equivalents1,542,301 104,017

Collateral for transactions2,373,947 954,605

Financial investments2,031,429 2,264,408

Others377,144 461,599

Others206,066,00 179,164

Non-current liabilities1,906,389 1,798,723

Non-current assets20,252,482 20,086,386

Financing986,830 1,010,059

Long-term receivables1,396,972 1,216,812

Deferred Inc. Tax and Social Contrib.858,129 732,074

Financial investments1,235,124 1,066,920

Others61,430 56,590

Others 161,848 149,892

Investments 2,265,098 2,286,537Shareholders' equity

19,374,798 19,419,048

Property and equipment361,071 367,134

Capital2,540,239 2,540,239

Capital reserve16,677,595 16,523,181

Intangible assets16,229,341 16,215,903

Others140,144 200,046

Minority interest in subsidiaries16,820 16,283

TOTAL ASSETS 24,032,278 22,633,975TOTAL LIAB. AND SHAREHOLDERS'

EQUITY24,032,278 22,633,975

(In BRL thousands )

49

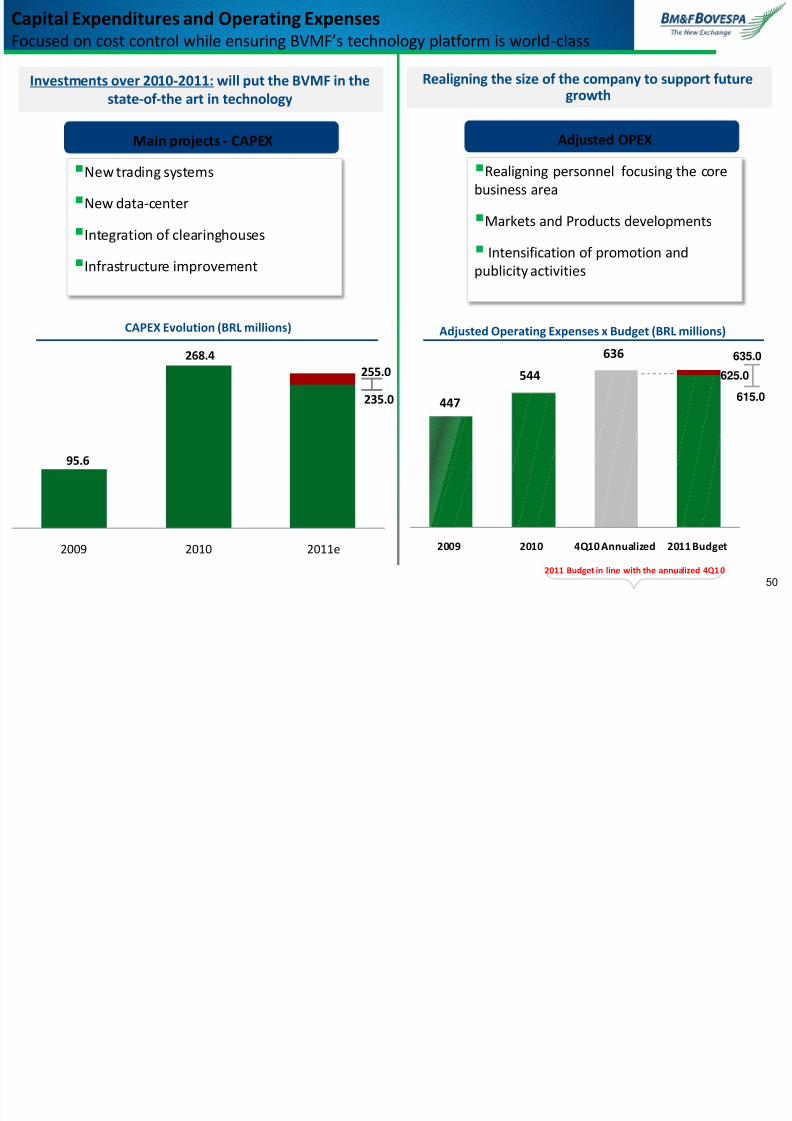

Capital Expenditures and Operating Expensesd l h l ’ h l l f ld l

7/30/2019 BVMF Presentation - July 2011

http://slidepdf.com/reader/full/bvmf-presentation-july-2011 50/51

447

544

636

2009 2010 4Q10 Annualized 2011 Budget

635.0

615.0

625.0

2011 Budget in line with the annualized 4Q10

95.6

268.4

2009 2010 2011e

235.0

255.0

Adjusted Operating Expenses x Budget (BRL millions)

Focused on cost control while ensuring BVMF’s technology platform is world-class

CAPEX Evolution (BRL millions)

Investments over 2010-2011: will put the BVMF in the

state-of-the art in technology

New trading systems

New data-center

Integration of clearinghouses

Infrastructure improvement

Main projects - CAPEX

Realigning the size of the company to support futuregrowth

Adjusted OPEX

Realigning personnel focusing the core

business area

Markets and Products developments

Intensification of promotion and

publicity activities

50

7/30/2019 BVMF Presentation - July 2011

http://slidepdf.com/reader/full/bvmf-presentation-july-2011 51/51