c o n s u m e r & c o m m u n i t y b a n k i n g · c o n s u m e r & c o m m u n i t y b...

TRANSCRIPT

C O N S U M E R & C O M M U N I T Y B A N K I N G

Gordon Smith, Chief Executive Officer Consumer & Community Banking

February 28, 2017

Page

Agenda

CO

NS

UM

ER

&

C

OM

MU

NIT

Y

BA

NK

IN

G

Consumer & Community Banking 1

Payments 13

Mortgage Banking 24

Banking 37

Appendix 57

We remain focused on a consistent set of strategic priorities

CO

NS

UM

ER

&

C

OM

MU

NIT

Y

BA

NK

IN

G

Deepen relationships with our customers, simplify and improve customer experience

Increase digital engagement by delivering differentiated experiences

Continue in our unwavering commitment to build and maintain an effective and efficient control

environment

Lead payments innovation by delivering solutions that address merchant and consumer needs

Execute structural expense management strategies while continuing to invest for the future

Protect the Firm, its clients/customers, investors, and employees from cyber attacks, as well as

protecting the privacy of their data and transactions

Attract, train, develop, and retain the best, diverse talent

1

Performance targets

2015 2016

Medium-term

guidance (+/-)

2016 Investor Day

Medium-term

guidance (+/-)

Business

Banking Net charge-off rate 0.66% 0.61% 0.60% 0.70%

Mortgage

Banking Net charge-off rate1 0.18% 0.10% 0.10% 0.15%

Card Services Net charge-off rate 2.51% 2.63% 3-3.25% 2.50%

Net revenue rate 12.33% 11.29% 11.25% 11.25%

Auto Finance Net charge-off rate 0.38% 0.45% 0.50% 0.45%

Total CCB ROE 18% 18% 20% 20%

Consumer & Community Banking targets

CCB 2016 ($B) % of JPMC

Net revenue $44.9 45%

Net income $9.7 39%

1 Excludes the impact of purchased credit-impaired (PCI) loans

CO

NS

UM

ER

&

C

OM

MU

NIT

Y

BA

NK

IN

G

2

We have continued strong momentum across key business drivers, driven by

consistent investment strategy

CO

NS

UM

ER

&

C

OM

MU

NIT

Y

BA

NK

IN

G

Key business drivers ($B, except ratios and where otherwise noted)

2016 YoY ∆

Consumer &

Community Banking

Households1 (mm) 60.0 4%

Active mobile customers (mm) 26.5 16%

Consumer Banking Average deposits $461 11%

Client investment assets (end of period) $235 7%

Business Banking

Average deposits $110 9%

Average loans2 $22 7%

Loan originations $7 8%

Net charge-off rate 0.61% (5) bps

Mortgage Banking

Total mortgage origination volume $104 (3%)

Foreclosure units (K, end of period) 47 (36%)

Average loans $232 14%

Net charge-off rate3 0.10% (8) bps

Credit Card

New accounts opened4 (mm) 10.4 20%

Sales volume4 $545 10%

Average loans $131 4%

Net charge-off rate 2.63% 12 bps

Commerce Solutions Merchant processing volume $1,063 12%

Auto Finance

Loan and lease originations $35 9%

Average loan and leased assets $75 16%

Net charge-off rate 0.45% 7 bps 1 Reflects data as of November 2016 2 Includes predominantly Business Banking loans as well as deposit overdrafts 3 Excludes the impact of PCI loans 4 Excludes Commercial Card

3

Consumer & Community Banking avg. loans1 ($B)

We continue to see strong growth in deposits and core loans

CO

NS

UM

ER

&

C

OM

MU

NIT

Y

BA

NK

IN

G

Consumer & Community Banking avg. deposits ($B)

$414 $453

$487 $531

$587

2012 2013 2014 2015 2016

$109 $110 $114 $118 $125

$53 $57 $69

$108

$151 $48 $51

$53

$56

$63

$15 $16 $18

$20

$22

$184 $159 $137

$115

$96

2012 2013 2014 2015 2016

Card Mortgage Banking

Auto Business Banking/Other

Non-core loans (all LOBs)

$409 $393 $391

2012 – 2016

CAGR

Non-core

loans:

(15%)

Core

loans:

+13%

Total:

+3%

2

Total: +10%

Core: +20%

3

$417

$457

CAGR

+9%

Note: Numbers may not sum due to rounding 1 Includes held-for-sale loans 2 Non-core loans include runoff portfolios, discontinued portfolios and portfolios the Firm has an intent to exit 3 Other includes securities-based lending of $1.5B in 2016, $1.4B in 2015, $0.8B in 2014, and $0.2B in 2013

4

Business drivers have supported revenue growth, with offsets in Card

investments and deposit margin compression

CO

NS

UM

ER

&

C

OM

MU

NIT

Y

BA

NK

IN

G

CCB revenue ($B)

Note: Numbers may not sum due to rounding; chart not to scale 1 Excludes Auto lease income, new Card origination costs, and Card co-brand renewals 2 Reflects new account origination costs and Sapphire Reserve travel credits

5

$43.8

$44.9

$1.8 $0.6

$0.6

($0.9)

($0.7) ($0.4)

2015Revenue

NII (excl. depositmargin compression)

NIR¹ Auto leaseincome

New Cardorigination costs²

Card co-brandrenewals

Deposit margincompression

2016Revenue

We have invested heavily in technology and marketing – and we are seeing

strong returns

Select investments Results

~$550mm pre-tax benefit in current annual run-rate

~4.3mm new accounts

~$44.4B annual spend

~$8.2B average outstandings

Credit Card

new account marketing1

Consumer Banking

new account marketing

~670K new households

~$5.2B in average deposits

Branch operating model

Digital

Chase Pay

Control and infrastructure

~$200mm pre-tax benefit in current annual run-rate

Digital engagement leads to higher retention – attrition improvement

since 2014 equal to 100K customers, or production of 211 branches

Significant future benefits expected

Continue to uplift standards – cybersecurity, KYC, and data

Cumulative spend

(2015 and 2016)

~$1.0B

~$1.7B1

Select investments Results (steady state)3 Incremental spend

over 2 years2

1 Credit Card new account marketing reflects spend before the reduction for new account origination costs, which are amortized against revenue 2 Incremental spend over 2 years calculated as the 2015 incremental versus 2014 plus the 2016 incremental versus 2014 3 Steady state reflects year 3 performance for Card and year 1 for Consumer Banking

Technology investments

Marketing investments1

CO

NS

UM

ER

&

C

OM

MU

NIT

Y

BA

NK

IN

G

6

4Q12 4Q16 All other households Digitally-engagedhouseholds

Our growing digitally-engaged customer base delivers strong performance metrics

CO

NS

UM

ER

&

C

OM

MU

NIT

Y

BA

NK

IN

G

Consumer Bank households – impact of digitally-engaged households1

% of households who are digitally-engaged Attrition2

Digitally-engaged population is growing Retention rates are higher (FY16)

+18ppt (11ppt)

Spending is higher (FY16)3

All other households Digitally-engagedhouseholds

Credit + debit card spend per household

+91%

Teller QuickDeposit

Cost of digital transactions is lower (FY16)

Cost per check deposit by channel

(96%)

Note: For footnoted information, refer to appendix

7

CCB has experienced strong growth across key business drivers, outpacing

operational volumes, while unit costs significantly decreased

CO

NS

UM

ER

&

C

OM

MU

NIT

Y

BA

NK

IN

G

Strong momentum across key business drivers1…

Average deposit

growth

9%

Average core

loan growth

16%

Card

new accounts2

13%

Card

sales volumes2

9%

Merchant

processing volume

12%

…while continuing to improve unit costs

Operations Volume CAGR1 Unit cost CAGR1

Customer service (inbound calls) 2% (3%)

Collections (2%) (9%)

Merchant processing transactions3 11% 0%

1 Reflects CAGR from 2013 – 2016 2 Excludes Commercial Card 3 Excludes network licensing fees for ChaseNet

8

We have substantially reduced expense, while continuing to prudently invest

CO

NS

UM

ER

&

C

OM

MU

NIT

Y

BA

NK

IN

G

CCB expense ($B)

Overhead 58% 55%4

Headcount3 148.2K 141.0K

~$2.4B

CCB structural expense5

~225 bps

CCB overhead ratio6

~7K

CCB headcount3

$25.6 $25.0

($2.4)

$1.0 $0.7

2014 Structuralexpense

Auto leasegrowth

Incrementalinvestments and

growth¹

2016exit²

Overall progress since 2014

Note: For footnoted information, refer to appendix

9

Our structural expense reduction initiatives are substantially complete, but work

to eliminate waste will always continue

CO

NS

UM

ER

&

C

OM

MU

NIT

Y

BA

NK

IN

G

Structural expense initiatives overview

Select initiatives Structural savings

(2016 exit vs. 2014) Accomplishments since 2014

Mortgage transformation1 ~$1.2B

Process streamlining

Overall delinquency rate2 approaching lowest level in a decade

Product simplification (e.g., sale of USDA business)

Branch transformation ~$0.5B

Reduced teller transactions by ~130mm

Decreased transactional staff by ~15%

Continued rolling out next generation of ATMs

Technology efficiencies ~$0.2B Rationalized technology spend

Reduced consumables

Digital adoption and

paperless ~$0.1B

Grew active digital customers by ~20%3

Reduced number of paper statements by 24%

Various initiatives4 ~$0.5B

Vendor rationalization

Real estate/location strategy

Marketing efficiencies

Total structural

expense reduction ~$2.4B

Note: Numbers may not sum due to rounding; 2016 exit reflects 4Q16 annualized 1 Includes mortgage operating losses, in large part foreclosure-related 2 Based on total mortgage and home equity loans serviced, as reported to Inside Mortgage Finance (IMF) as of December 2016 3 Users of all web and/or mobile platforms who have logged in within the past 90 days 4 Includes non-core items

10

We are focused on executing the next wave of expense reduction strategies

CO

NS

UM

ER

&

C

OM

MU

NIT

Y

BA

NK

IN

G

Focus areas Planned strategies

Operations integration ■ Increase data sharing with partners to reduce fraud

■ Reduce the cost of metal and plastic cards

Branch transformation

■ Modernize teller staffing tools

■ Data driven sales leads

■ Digital account opening and digital wealth management

Technology efficiencies ■ Agile development and cloud-based technology

■ Consolidate internal applications

Support customers’

transition to digital

channels

■ Digital mortgage pilot

■ E-letters and bill pay merchant directory

■ Increase paperless new checking accounts

Expense reduction strategies

11

We expect to achieve a ~50% overhead ratio in the medium-term

CO

NS

UM

ER

&

C

OM

MU

NIT

Y

BA

NK

IN

G

CCB overhead ratio

1 Excludes incremental auto lease income 2 Includes marketing, investments in payments and digital innovation and technology, and business growth

12

55%

~50%

(~5%)

~1%

~2.5%

(~2.5%) (~1%)

2016overhead ratio

Revenue growth(excl. interestrate impact)¹

Growth inauto leasebusiness

Incrementalinvestmentsand growth²

Efficiencies Interest rateimpact

Targetoverhead ratio

Page

Agenda

CO

NS

UM

ER

&

C

OM

MU

NIT

Y

BA

NK

IN

G

Payments 13

Consumer & Community Banking 1

Mortgage Banking 24

Banking 37

Appendix 57

Key business drivers ($B, except ratios and where otherwise noted)

2015 2016 YoY ∆

Payments

Card average loans $126 $131 4%

Card end of period loans $131 $142 8%

Credit card sales volume1 $496 $545 10%

Debit & credit card sales volume1 $754 $818 9%

Merchant processing volume $949 $1,063 12%

Card new accounts opened (mm)1 8.7 10.4 20%

Card Services net revenue rate 12.33% 11.29% (104) bps

Card net charge-off rate 2.51% 2.63% 12 bps

Payments has seen strong metric growth driven by investments in the business

4Q16 sales1 growth showed significant improvement of 14% year-over-year

1 Credit card data excludes Commercial Card

PA

YM

EN

TS

13

Our strong business performance has resulted in leading market positions

PA

YM

EN

TS

07/20/11

General purpose credit card sales market share1

General purpose credit card EOP outstandings

market share1

Source: Company filings; internal JPMorgan Chase estimates

Note: Numbers may not sum due to rounding 1 Based on 4Q16 sales volume and loans outstanding disclosures by peers and internal JPMorgan Chase estimates. Sales volume excludes private label and Commercial

Card. Outstandings exclude private label, AXP Charge Card, and Citi Retail Cards 2 AXP reflects the U.S. Consumer segment and internal JPMorgan Chase estimates for AXP’s U.S. small business sales

20.9% 21.7%

7.8% 11.5%

24.3% 19.9%

9.4% 8.9%

5.1% 4.7%

11.0% 11.0%

21.6% 22.3%

4Q15 4Q16

Chase C AXP BAC DFS COF Other

▲80 bps

▼77 bps

▼47 bps

▼32 bps

▲ 6 bps

▲69 bps

YoY ∆

2

16.4% 16.7%

8.4% 10.1%

8.3% 6.9%

11.2% 10.9%

7.2% 7.2%

9.7% 10.1%

38.8% 38.2%

4Q15 4Q16

Chase C AXP BAC DFS COF Other

YoY ∆

2

▼33 bps

▲ 1 bp

▲39 bps

▼ 61 bps

▲28 bps

▲ 27 bps

14

Payments strategy

Integrated Merchant

Experience

Core acquiring and

processing services

ChaseNet closed loop

system

Integrated merchant loyalty

Consumer to

Business

Deliver superior consumer

value by launching new and

enhanced products

Lead payments innovation

with unique solutions

Our overall card and payments strategy balances a focus on core business growth

with future investment

Person-to-Person

Build simplified, real-time

person-to-person (P2P)

payment solution

Ensure Chase cards can be used everywhere our customers shop

PA

YM

EN

TS

15

2012 2016

New product launches and a broad investment in marketing have generated

strong customer engagement and return on our investment

PA

YM

EN

TS

2012 2016

2012 2016

2012 2016

Acquisition vintage in-year performance Total portfolio performance

~2x +7% CAGR

>2x +7ppt

Vintage in-year sales

Vintage in-year outstandings

Average sales per account

Average % of accounts with sales activity

Note: Data excludes Commercial Card and certain terminated partner portfolios

16

The new Sapphire Reserve customers we are acquiring have attractive

characteristics

PA

YM

EN

TS

Early adopter profile of Sapphire Reserve customers as of December 2016

Average FICO score >785

Lift in On Chase spend2 >50%

Average Deposit & Investment wallet >$800K

1 Reflects self-reported income at time of application 2 Compares July 2016 and December 2016 credit card spend (Pre-Reserve vs. Post-Reserve acquisition for existing Chase card customers only). Excludes December

acquisitions

Average income1 >$180K

17

Chase Card has modest exposure to FICO <660, and is lowest in the 640 – 720 range

28% 29% 30% 31% 34%

38%

Chase AXP DFS C COF BAC

Chase vs. competitors – FICO <660 portfolio mix1

Chase vs. competitors FICO (640 – 720) portfolio

mix2

15% 15%

34% 36%

25% 25%

17% 18%

16% 15%

14% 14%

1Q15 2Q15 3Q15 4Q15 1Q16 2Q16 3Q160%

6%

12%

18%

24%

30%

36%

Chase COF WFC DFS C BAC

1 Source: “U.S. Cards Subprime Plateau,” Autonomous sell-side research report, 11/3/2016. Leveraged peers’ Form10-Q/K disclosures and incorporates their own internal

estimates. Credit card loans without a FICO score included in FICO <660 category 2 Based on Lightspeed Behavioral Tracking Panel data for sample of existing portfolios’ customers polled during 3Q16. Data represents FICO scores from 640 – 719

PA

YM

EN

TS

18

Digital 77%

Branch 13%

Direct mail 8%

Other 2%

Increased efficiencies within our acquisition channels

PA

YM

EN

TS

Acquisitions are moving to lower cost channels

2016 new credit card accounts by channel1

Increased mobile acquisitions

1 Data excludes Commercial Card and certain terminated partner portfolios 2 Represents applications from smartphone and tablet visitors in Chase-hosted digital channels; excludes applications hosted on partner sites

2012 2016

% of total digital credit card applications sourced

from mobile devices2

19

+28ppt

Our investments in Payments extend into P2P, an important emerging segment, and

we continue to enhance and grow our P2P offering with Chase QuickPay

We are well positioned to succeed in P2P

Active mobile CBB households1

$28B 2016 Chase

QuickPay volume

94mm 2016 Chase

QuickPay

transactions

15mm 90 day active as of

4Q16

4mm 90 day active as of

4Q16

PA

YM

EN

TS

Chase QuickPay user households2

P2P volume and growth3 Annual P2P transactions3

1 CBB households with a user of all mobile platforms who has logged in within the past 90 days 2 Represents figures for CBB households only who have agreed to the Chase QuickPay legal agreements and sent a payment via Chase QuickPay during the selected time

frame (as of December 2016) 3 Includes Chase QuickPay transactions from CBB households

+38% YoY growth

20

Chase Pay, our proprietary digital solution, expands the capabilities of our

successful core business with an innovative product

PA

YM

EN

TS

Track purchases

Pay securely

Easy digital checkout Keep cards updated

Order/pay ahead1

Automatic savings

Key

Features

Key

Partners LevelUp

1 Order/pay ahead is not available at Starbucks locations within the Chase Pay app

21

$655

$1,063

2012 2016

PA

YM

EN

TS

Commerce Solutions surpassed $1 trillion in processing volume

Commerce Solutions total processing volume ($B)

+13% CAGR

New company relationships by referral source1

Internal >55%

External <45%

Deal closure rate by relationship1

Prospects Existing JPMclients

+20ppt

1 Data represents full-year 2016. Sales lead classification based on internal JPMorgan Chase data

22

#1 position in both credit card sales and

outstandings market share1

Surpassed $1T in merchant processing volume

Successfully launched new partner and branded

products

Renewed 80% of co-brand sales volume in the

last two years

Launched Chase Pay with Starbucks and Best

Buy

What we’ve accomplished Where we’re headed

Lead payments innovation and transform the

payment experience

Provide superior customer value

Deliver overall financial returns

1

2

3

Create lifelong, engaged relationships by serving all spending and borrowing needs of our

targeted customer segments

We made significant progress in 2016, and our go-forward strategy remains consistent

PA

YM

EN

TS

1 Based on 4Q16 sales volume and loans outstanding disclosures by peers (C, BAC, COF, AXP, DFS) and internal JPMorgan Chase estimates. Sales volume excludes private

label and Commercial Card. AXP reflects the U.S. Consumer segment and internal JPMorgan Chase estimates for AXP’s U.S. small business sales. Outstandings exclude

private label, AXP Charge Card, and Citi Retail Cards

23

Page

Agenda

CO

NS

UM

ER

&

C

OM

MU

NIT

Y

BA

NK

IN

G

Mortgage Banking 24

Payments 13

Consumer & Community Banking 1

Banking 37

Appendix 57

We continue to execute against our strategy of building a higher quality and less

volatile mortgage business

MO

RT

GA

GE

B

AN

KIN

G

Maximize our share of

high quality

originations

Improve quality of

servicing portfolio

and de-risk the

business

Deliver a great

customer experience

Progress

Improved J.D. Power originations and servicing rankings

Expanded affordable lending programs

Increased our share of jumbo originations

Attractive returns and outstanding quality

Overall delinquency rate1 approaching lowest level in a decade

Sale of USDA business

1 Based on total mortgage and home equity loans serviced, as reported to IMF as of December 2016

24

The underlying performance of the business is strong

Key business drivers ($B, except ratios and where otherwise noted)

2015 2016 YoY Δ

Mortgage

Production

Total mortgage origination volume $106 $104 (3%)

Consumer origination volume $36 $44 23%

Correspondent origination volume $70 $59 (16%)

Home equity origination volume $5 $7 40%

Mortgage

Servicing

Total loans serviced (end of period) $910 $847 (7%)

Third-party mortgage loans serviced (end of period) $674 $592 (12%)

Foreclosure units (K, end of period) 73 47 (36%)

Loan balances and

credit performance

Mortgage Banking loans (average) $204 $232 14%

Mortgage Banking net charge-off rate1 0.18% 0.10% (8) bps

Note: Numbers may not sum due to rounding 1 Excludes the impact of PCI loans

MO

RT

GA

GE

B

AN

KIN

G

25

We have seen improvement in internal and external measurements of customer

satisfaction

J.D. Power Mortgage surveys2 Annual Net Promoter Score1

2012 2013 2014 2015 2016

Chase rank

2015

2016

’15 – ’16

change

Originations Servicing

7 10

5 6

+2 +4

2010 12 13

1 Net Promoter Score = % promoters minus % detractors. Survey started in August 2012. Survey methodology changed in 3Q14 2 Source: "U.S. Primary Mortgage Origination and Servicer Satisfaction Studies,” J.D. Power, 2010, 2015, and 2016

MO

RT

GA

GE

B

AN

KIN

G

26

We are focused on high-quality originations…

1 Source: IMF. Firmwide mortgage originations for top 5 ranked banks. Includes Conventional, Government, Jumbo, and excludes Home Equity 2 Source: IMF and JPMorgan Chase internal data. Mortgage Banking only originations. Excludes Private Bank and Home Equity 3 Data as of 12/31/2016. Based on unpaid principal balance of loans serviced. Includes foreclosures and excludes real estate owned (“REO”) inventory 4 Excludes PCI loans and private label securities

Mortgage companies and small banks have gained

share from large banks

The largest share gain for mortgage companies and

small banks has been in government lending

Chase originations market share by product type2

We have shifted our origination mix toward high

quality jumbo, consistent with our strategy of building

a less volatile mortgage business

The 30+ delinquency rate3 for jumbo is 1.05%4,

compared to 13.15% for government products

54%

25%

46%

75%

2011 2016

Top 5 banks by originations All Other1

Total originations market share

MO

RT

GA

GE

B

AN

KIN

G

9%

3% 2%

12%

Government Jumbo

2011 2016

27

…and continue to see strong core loan growth

$51 $53 $57 $69

$108

$151

$174 $152

$132 $114

$96

$81

$225

$205

$189 $183

$204

$232

2011 2012 2013 2014 2015 2016

2011 – 2016

CAGR

Non-core:

(14%)

Core: +24%

Total: +1%

Mortgage Banking average loan balances ($B)

% of

originations

retained3

3% 4% 11% 33% 66% 49%

Non-core1

Core2

1 Non-core loans include runoff portfolios, which are predominantly discontinued products no longer originated and PCI loans 2 Core loans primarily include loans held in Real Estate Portfolios, as well as loans residing in Mortgage Production and Mortgage Servicing, which are predominantly prime

mortgage loans repurchased from Government National Mortgage Association (“Ginnie Mae”) pools, which are insured by U.S. government agencies 3 Excludes Home Equity and Private Bank loans

MO

RT

GA

GE

B

AN

KIN

G

28

2.37%

0.85%

0.37%

0.18% 0.10%

FY12 FY13 FY14 FY15 FY16

Mortgage Banking net charge-off rate2 trend

We continue to maintain strong credit performance

(227) bps

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

4Q12 4Q13 4Q14 4Q15 4Q16

Mortgage Banking1 30+ delinquency rate (%)

3

1 Excludes PCI loans and mortgage loans insured by U.S. government agencies that are 30 or more days past due. These amounts have been excluded based upon the

government guarantee 2 Excludes the impact of PCI loans 3 Includes the effect of incremental net charge-offs based on regulatory guidance

MO

RT

GA

GE

B

AN

KIN

G

29

We are actively managing our servicing book by bringing in high-quality new

originations while reducing our volume of low-quality units

2014 – 2016 Chase servicing book activity

Units 30+ delinquency rate

New originations ~790K 0.02%

Acquired servicing ~235K 0.10%

Total “in flows” ~1,025K 0.04%

Units 30+ delinquency rate

Run-off ~1,850K 7.65%

Sales ~350K 29.94%

Total “out flows” ~2,200K 11.19%

“Coming In” Dec 2014 through Dec 2016

“Going Out” Dec 2014 through Dec 2016

30+ delinquency rate1 for Chase servicing book

6.23%

4.70%

December 2014 December 2016

Units in

servicing

book

6.5mm 5.4mm

1 Based on number of loans serviced. Includes foreclosures and second liens and excludes REO inventory

MO

RT

GA

GE

B

AN

KIN

G

30

Our default inventory continues to decline, driving lower overall servicing expense

Non-Performing Performing

Servicing cost per unit1

Note: Numbers may not sum due to rounding 1 2015 Chase data as defined by the Mortgage Bankers Association (MBA) in the Stratmor survey 2 Credit costs excluded from all time periods 3 FY12 includes ~$1B of additional expense for foreclosure-related matters

(25 – 30x)

Servicing expense2 ($B)

$4.7

$3.0

$2.3 $2.0

$1.7

FY12 FY13 FY14 FY15 FY163

Foreclosure inventory (K)

312

167

93 73 47

FY12 FY13 FY14 FY15 FY16

(85%)

>$3.0

MO

RT

GA

GE

B

AN

KIN

G

31

We are through a significant portion of home equity interest-only recast risk for

the legacy Chase book, with performance in line with expectations

Note: Excludes PCI portfolio. Data as of December 2016 1 Based on carrying value; excludes home equity balloon loans that maintain an interest only payment after the draw period ends 2 Includes modifications which no longer exhibit recast risk based on modified terms 3 Current estimated combined LTV for junior lien home equity loans considers all available lien positions, as well as unused lines, related to the property

MO

RT

GA

GE

B

AN

KIN

G

HELOC portfolio1 balance ($B)

$13.1

$15.0

$0.6 $0.2

Past recast Future recast

HELOC balance 30+ day delinquent balance

2

Loans with CLTV3 > 80%

27%

12%

Past recast Future recast

703

743

600

650

700

750

800

Past recast Future recast

Average FICO

32

We anticipate a smaller, purchase-driven market, with tightening primary and

secondary spreads

1 Source: IMF 2014 through 2016; 2017F reflects average of forecasts from Fannie Mae (1/10/17), Freddie Mac (1/30/17), and MBA (1/19/17) 2 Source: Freddie Mac Primary Mortgage Market Survey (PMMS). Represents 30-yr fixed rate 3 Source: JPMorgan Chase Securitized Products Group (SPG) Research. Represents Fannie Mae 30-yr current coupon rate 4 Source: JPMorgan Chase SPG Research

Mortgage origination market1 ($B) Primary2 and secondary3 mortgage rates

4.17%

3.85% 3.65%

4.25%

3.19%

2.84% 2.59%

3.28%

0.98% 1.01% 1.06% 0.97%

2014 2015 2016 2017F

Primary Secondary Spread

MO

RT

GA

GE

B

AN

KIN

G

$783 $924

$1,060 $1,077

$517

$811

$1,005

$468 $1,300

$1,735

$2,065

$1,545

2014 2015 2016 2017F

Purchase Refinance

4

33

We are piloting a digital mortgage experience to address the needs of an

increasingly tech-centric customer base

Transparent – customers always know where they stand in the process

Convenient – customers can securely upload documents to the platform

Connected – customers can e-sign documents

Customers empowered with real-time information and transparency

Efficiency gains for Chase through automation of manual handoffs

Ongoing enhancements to the platform

…resulting in benefits for customers and Chase

Our mobile-enabled customer portal will be…

MO

RT

GA

GE

B

AN

KIN

G

34

We have a tremendous growth opportunity within our own Chase customer base – our

performance with CPC1 customers shows the power of a differentiated experience

CCB household distribution by homeownership

~5mm2,4

Chase mortgage

% of Chase customers originating a mortgage with

Chase by relationship type, FY2016 ($ basis)

~30mm3

With mortgage

60mm2

CCB households

Card Checking CPC

>4x

MO

RT

GA

GE

B

AN

KIN

G

1 Chase Private Client

2 Reflects data as of November 2016

3 JPMorgan Chase internal analysis 4 JPMorgan Chase internal data

35

We remain focused on executing against our strategy

MO

RT

GA

GE

B

AN

KIN

G

Improved the customer experience

Enhanced the quality of the servicing

portfolio and de-risked the business

Substantially reduced expenses

Grown our balance sheet with high quality

originations

What we’ve accomplished

Positions us well to execute our strategy and drive future growth with our existing Chase

customer base

Where we’re headed

Enrich digital experience for increasingly tech-

centric customer base

Transform Chase customer experience by

leveraging internal and external data

Accelerate focus on deepening Chase

relationships

1

2

3

36

Page

Agenda

CO

NS

UM

ER

&

C

OM

MU

NIT

Y

BA

NK

IN

G

Banking 37

Payments 13

Mortgage Banking 24

Consumer & Community Banking 1

Appendix 57

Consumer & Business Banking strategic priorities and progress

BA

NK

IN

G

Acquire and deepen

relationships

Increase digital

engagement

Drive down

expenses

Progress

Grew Consumer & Business Banking deposits & investments by ~$250B – a

10% CAGR since 2012

Acquired ~2.7mm net new consumer checking households and ~235K net new

business households since year-end 2012

Primary bank for more than 70% of our consumer households and nearly 50%

of our business households1

More than doubled Consumer & Business Banking households using mobile

since year-end 20122

Released next generation of ATM hardware and software with enhanced ATM

functionality

Reduced structural expenses by ~$600mm3 since year-end 2014 while

reinvesting a meaningful portion of the savings in marketing and digital

Reduced teller transactions by ~130mm since year-end 2014

Decreased transactional staff by 15% since year-end 2014

1 Primary relationship based on internal JPMorgan Chase definition

2 Users defined as consumer or business households that had at least one mobile log-in in a given quarter 3 Savings from 2014 based on 2016 exit (4Q16 annualized)

37

2015 2016 YoY Δ

Relationships (mm) Consumer households 23.3 23.9 3%

Business households1 2.4 2.5 4%

Financial metrics ($B)

CBB revenue $18.0 $18.7 4%

CBB non-interest expense $11.9 $11.8 (1%)

CBB overhead ratio 66% 63% (3 ppt)

Balances ($B)

Average deposits2 $515 $571 11%

Deposit margin2 1.90% 1.81%

Client investment assets (end of period) $219 $235 7%

% managed assets 41% 40%

Average Business Banking loans3 $20.5 $21.9 7%

Distribution channels

Branches 5,413 5,258 (3%)

ATMs 17,777 18,493 4%

Average deposits/branch employee ($mm)2 $11.4 $12.5 10%

Consumer & Business Banking business drivers

Consumer & Business Banking business drivers

BA

NK

IN

G

1 Includes only Business Banking households that have either a business checking, savings, CD product or credit product on the Business Banking P&L

2 Includes Consumer & Business Banking deposits 3 Includes predominantly Business Banking loans as well as deposit overdrafts

38

9.8%

6.3%

2.7% 2.8%

Chase NationalBanks

SuperRegional

Other

Change in deposits vs. industry (2012 – 2016 CAGR)1

Industry avg.

growth = 4.0%

We continue to lead the industry in deposit balance growth

BA

NK

IN

G

Note: For footnoted information, refer to appendix

39

We have established our physical presence in faster growing markets

BA

NK

IN

G

Chase performance in top 10 Chase markets (2012 – 2016)1

Chase top 10

markets by

deposit

balances (2016)

Chase $

deposit

growth

rank

Chase

deposit

share

(2016)

Chase share

of $ deposit

growth

Chase

growth rate

vs. industry

ex-Chase

1 New York, NY 1 21% 35% 2.3x

2 Los Angeles, CA 1 17% 29% 2.2x

3 Chicago, IL 1 19% 53% 5.7x

4 Houston, TX 1 21% 27% 1.5x

5 Dallas-Fort Worth, TX 1 19% 28% 1.8x

6 San Francisco, CA 3 13% 19% 1.8x

7 Miami, FL 2 12% 23% 2.7x

8 Phoenix, AZ 1 26% 29% 1.2x

9 Detroit, MI 1 20% 35% 2.5x

10 San Diego, CA 1 19% 29% 2.0x

Note: For footnoted information, refer to appendix

4.6%

3.0%

Chase markets Non-Chase markets

Industry deposit growth (2012 – 2016

CAGR)1

Industry avg.

growth = 4.0%

40

Three-quarters of our growth has come from customers who use our branches

BA

NK

IN

G

Chase Consumer Bank deposit growth attribution

by channel usage segment (2012 – 2016)1

Digitally-centric 18%

Multi-channel

60%

Branch-centric

16%

Other 6%

Households across generations continue to use the

branch2

57%

64%

70%

71%

Millennials

Gen X

BabyBoomers

SilentGeneration

% of households using

the branch (4Q16)

Avg. visits/quarter3

3

4

5

5

Note: For footnoted information, refer to appendix

41

Digital engagement embeds us in our customers’ daily lives – on average, mobile

banking users have 5 mobile log-ins per week

BA

NK

IN

G

Chase leadership positions

#1 rated mobile banking app and #1 in active mobile users among large bank peers1

#1 most visited banking portal in the U.S.2

#1 ATM network in the U.S.3

CBB Chase QuickDeposit

usage CBB Chase QuickPay usage

+19% households using

QuickDeposit vs. 2015

+30% households using

QuickPay vs. 2015

Key engagement metrics4

CBB mobile usage

+12% households using

mobile vs. 2015

74mm transactions in 2016

94mm transactions in 2016

5 log-ins per week in 2016

1 Source: “2016 Mobile Banking Financial Institution Scorecard,” Javelin Strategy & Research, May 2016. Ranking is among large banks. Active mobile users based on

disclosures by peers in 4Q16 2 Source: SimilarWeb.com as of December 2016 (formerly compete.com) 3 Based on competitor filings 4 Households using mobile defined as households that have at least one log-in through the Chase Mobile app or via mobile browser in 4Q16. Households using QuickDeposit or

QuickPay are defined as households that complete at least one of the specified transactions in 4Q16

42

2012 2013 2014 2015 2016All other households Digitally-engagedhouseholds

Digital engagement is a contributing factor to our record low attrition

BA

NK

IN

G

4Q12 4Q16

Digitally-engaged households All other households

Digitally-engaged households are growing rapidly…1

HH growth

(2012 – 2016

CAGR)

11%

(7%)

Consumer Bank household attrition rates3

(4ppt)

1 Digitally-engaged households include digitally-centric and multi-channel households. All other households include branch-centric and other households 2 Net Promoter Score = % promoters minus % detractors. Based on Net Promoter Score data collected from January – November 2016 3 Attrition rates are based on Consumer Bank households with deposit products and include households that closed all of their deposit products with Chase. Attrition rate

calculated by taking an average of the annualized monthly rates for the 12 months of each year

…and exhibit higher Net Promoter Scores1,2

~+20%

43

2014 2016

2014 2016

While delivering this winning experience, we have also reduced structural

expenses

BA

NK

IN

G

Annual teller transactions (mm)

(~130mm)

Annual self-service/digital transactions (mm)2

Online

Mobile

ATM

% change

+118%

+1%

(39%)

~+180mm

Today, ~80% of transactions are completed through self-service channels; going forward, we

will continue to drive transaction migration

Example: branch transformation

Branch

transformation

~55%

1 2016 represents 2016 exit (4Q16 annualized) 2 Excludes mobile and online log-ins

Branch and ATM

consolidation

~20%

Paperless ~15%

Business Banking ~10%

Distribution of structural expense reductions

CBB structural expense reduction (2014 – 2016)1

Branch

transformation

~50% Branch and ATM

consolidation / other

~25%

44

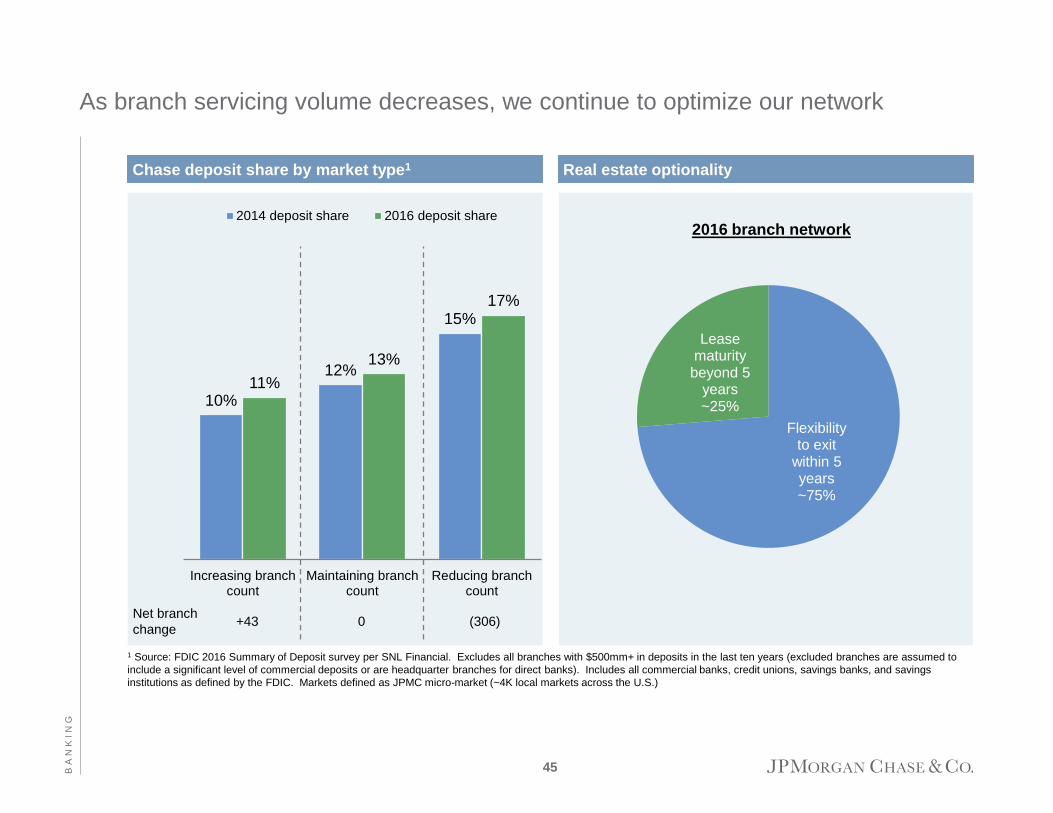

Flexibility to exit

within 5 years ~75%

Lease maturity beyond 5

years ~25%

2016 branch network

As branch servicing volume decreases, we continue to optimize our network

BA

NK

IN

G

Real estate optionality

10%

12%

15%

11%

13%

17%

Increasing branchcount

Maintaining branchcount

Reducing branchcount

2014 deposit share 2016 deposit share

Chase deposit share by market type1

Net branch

change +43 0 (306)

1 Source: FDIC 2016 Summary of Deposit survey per SNL Financial. Excludes all branches with $500mm+ in deposits in the last ten years (excluded branches are assumed to

include a significant level of commercial deposits or are headquarter branches for direct banks). Includes all commercial banks, credit unions, savings banks, and savings

institutions as defined by the FDIC. Markets defined as JPMC micro-market (~4K local markets across the U.S.)

45

We have a clear, focused strategy

BA

NK

IN

G

Primary bank for more than 70% of our consumer

households1

Leading brand perception in trust and advice

Leading physical presence and digital capabilities

Strong positioning with Millennials

Success in promoting self-service options for

everyday transactions

What we’ve accomplished Where we’re headed

Promote operational excellence across our

organization

Continue to evolve our leading multi-channel

experience

Develop lifelong relationships with our clients by delivering a powerful

combination of a trusted brand, leading multi-channel access, advice and financial

solutions to meet their evolving needs

Enhance financial solutions and advice

1

2

3

1 Primary relationship based on internal JPMorgan Chase definition

46

Chase has built a powerful small business franchise

BA

NK

IN

G

Chase for Business assets

Business card #2 small business credit card issuer by purchase volume4

Merchant services #2 merchant acquirer5

Deposits #3 primary bank market share3

Mobile offering

Branches

#1 rated mobile app for a large bank2

~5,250 branches and 10K+ specially-trained bankers

Online experience #1 most visited banking portal in the U.S.1

1 Source: SimilarWeb.com as of December 2016 (formerly compete.com) 2 Source: “2016 Mobile Banking Financial Institution Scorecard,” Javelin Strategy & Research, May 2016. Ranking is among large banks 3 Source: Barlow Research Associates, Primary Bank Market Share Database as of 4Q16. Rolling eight quarter average of small businesses with revenues of $100K – <$25mm 4 Source: The Nilson Report, Issue 1089, June 2016. Data as of 2015 and AXP quarterly financial reports and presentations 5 Source: The Nilson Report, Issue 1082, March 2016. Data as of 2015. Chase is the #1 wholly-owned merchant acquirer in the U.S. When volume from JVs and revenue share

arrangements are included in First Data’s volume, First Data holds #1 share position in the U.S. 6 Source: "U.S. Small Business Satisfaction Study,” J.D. Power, 2016

We rank among the top 3 providers across all regions according to J.D. Power6

47

The JPMC platform offers a unique value proposition to small businesses

~75% of customers have a

Consumer Banking account1

~30% of customers use Chase

Card Services1

15% of Relationship Managed

customers use Commerce

Solutions products1

200+ customers grew into

Commercial Banking clients in

2016, migrating ~$1B in

deposits

Business Banking customers

use multiple Treasury

Services products

Business Banking customers leverage product offerings across the firm

Business Banking

Consumer Banking

Card Services

Commerce Solutions

Commercial Banking

Treasury Services

1 As of December 2016. U.S. customers only

BA

NK

IN

G

48

4Q14 4Q16

Omni-channel capabilities enable Chase to meet the needs of small businesses

BA

NK

IN

G

Small businesses increasingly interact digitally, leading to a decrease in teller transactions

Small businesses continue to rely upon the branch network, particularly for complex interactions

55%

29% 16%

Branch Majority online Entirely online

Branch active Non-branch active

# of teller transactions

(19%)

Total branch activity in 4Q16 Industry-wide channel preference for account opening3

2

~70% of

businesses

transact at a

branch at least

once per quarter

# of mobile log-ins per business1

4Q14 4Q16

Blue +31%

1 Channel usage per customer active in channel 2 Branch active defined by at least one branch transaction per quarter 3 Source: “Digital Account Opening Study: New Customer Experience,” Barlow Research Associates, October 2016. Small businesses with revenues of $100K – <$25mm. New

checking accounts only

49

2014 2016

Core markets Expansion markets

We have had strong performance since 2014 led by our expansion markets

BA

NK

IN

G

2014 2016

Core markets Expansion markets

Deposits average daily balance Loan average daily balance

2014 – 2016

CAGR

▲ 18%

▲ 8%

2014 – 2016

CAGR

▲ 21%

▲ 2%

+10% CAGR 6% CAGR

50

The small business market is fragmented, creating an opportunity for Chase to

consolidate primary bank share and deepen product penetration

Small business primary bank market share1 Small business product usage

81%

48% 43%

10%

Businesscard

Merchantservices

Deposit +Card +

Merchantservices

All three -Relationship

Managed

28mm3 small businesses contribute ~$120B4 to financial services revenue in the U.S.

3% 6%

9%

9%

10% 64%

US Bank Credit Unions

Chase Bank of America

Wells Fargo Other

Industry2 Chase

Business

Banking

10% of Relationship Managed customers

have all three products with Chase

Opportunity

1 Source: Barlow Research Associates, Primary Bank Market Share Database as of 3Q16. Rolling eight quarter average of small businesses with revenues of $100K – <$25mm.

Numbers may not sum due to rounding 2 Source: “Oliver Wyman Survey of Small Business Owners,” Oliver Wyman, 2Q14. Based on surveys of small businesses with checking accounts and revenues of $100K+. Card

includes either credit or charge card 3 Source: “Small Business Profiles for the States and Territories,” U.S. Small Business Administration, 2014 4 Source: “Digital Models for a Digital Age: Transition and Opportunity in Small Business Banking,” McKinsey & Co., 2013. Based on 2011 data of small businesses with

revenues of <$20mm BA

NK

IN

G

51

Deepening engagement with Relationship Managed customers through multi-

product relationships leads to stronger deposit and revenue growth

Impact of small businesses choosing Chase for multiple products

Business Banking +

Chase Card1

21% higher

deposit balances

43% higher

deposit balances

Business Banking +

Chase Card +

Merchant services1

Higher revenue2 Lower attrition3

Note: “Relationship Managed” includes customers assigned to Business Banking Relationship Manager portfolios. They typically have larger balances, more complex products, and

larger credit relationships. “Business Banking” includes Business deposits and Business loans/lines 1 Deposits as of December 2016 2 Revenue annualized from December 2016 3 Attrition based on P&L aligned bookends for December 2015 and December 2016 and Relationship Managed customers that closed all business accounts in the time period

BA

NK

IN

G

BusinessBanking Only

Deposit, Card,and Merchant

services

BusinessBanking Only

Deposit, Card,and Merchant

services

(4ppt) 2.3x

52

We continue to invest for further growth

BA

NK

IN

G

Deposits and

business loans

Business card

Merchant services

Chase Business Quick Capital (OnDeck)

Next-day funding and product simplification

Expanded product set and improved credit decision time

Investment initiatives

Digital platform New Chase Business Online integrating Deposit, Payments,

and Lending

Customer onboarding Common application and underwriting

53

Fintech collaboration can accelerate our growth

BA

NK

IN

G

Chase Business Quick Capital

2012 2016

1.6

9.6

+57% CAGR

Small business online lending

in the U.S. ($B)1

1 Loan originations derived from internal JPMorgan Chase estimates using select financial reporting of online marketplace lenders and “Global Marketplace Lending: Disruptive

Innovation in Financials,” Morgan Stanley, May 2015

54

9.5%

8.8%

9.6% 9.7%

6.2%

8.5%

4%

8%

12%

2012 2013 2014 2015 2016

Bank of America Wells Fargo Chase

Our Net Promoter Score and primary bank market share show the momentum we

have to build upon

Primary bank market share of top 3 banks2

We have grown primary bank market share from ~6% to ~9% over the past four years

Net Promoter Score1

29

34 36

36

40

25

35

45

2012 2013 2014 2015 2016

1 Net Promoter Score = % promoters minus % detractors. Survey transitioned from phone to email in September 2015. Survey design changed in 3Q16 2 Source: Barlow Research Associates, Primary Bank Market Share Database as of 4Q16. Rolling eight quarter average of small businesses with revenues of $100K – <$25mm

BA

NK

IN

G

55

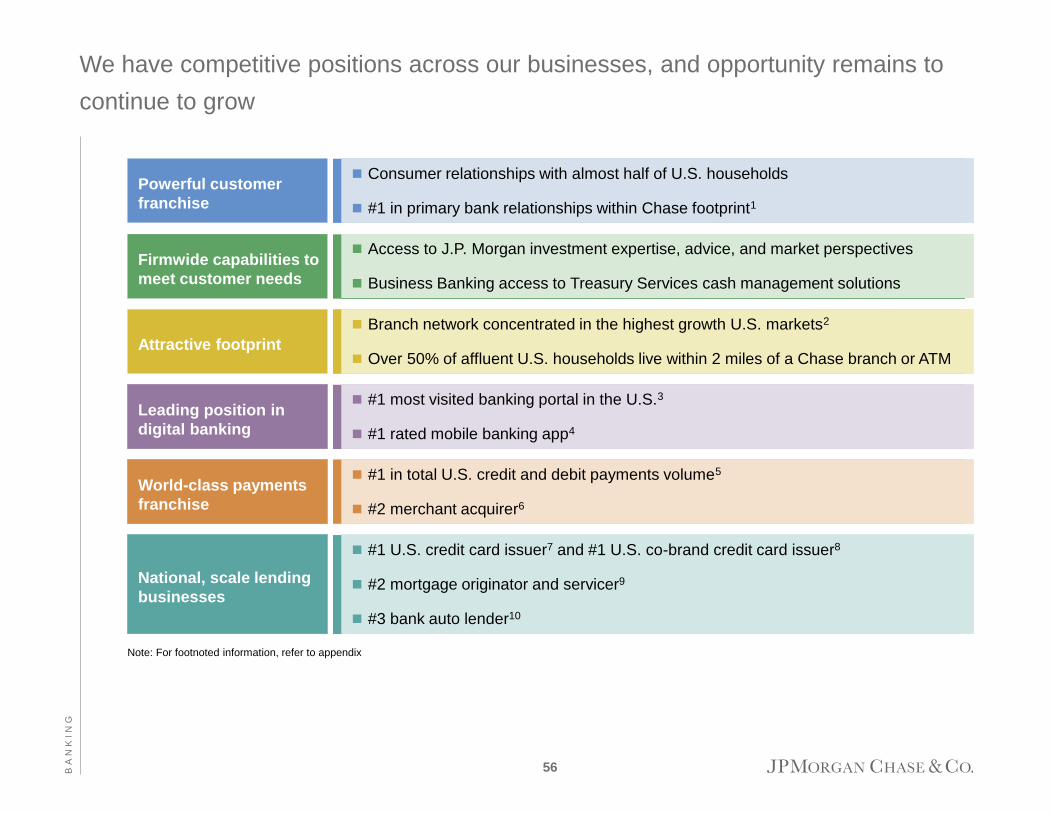

We have competitive positions across our businesses, and opportunity remains to

continue to grow

Consumer relationships with almost half of U.S. households

#1 in primary bank relationships within Chase footprint1

Powerful customer

franchise

Access to J.P. Morgan investment expertise, advice, and market perspectives

Business Banking access to Treasury Services cash management solutions

Firmwide capabilities to

meet customer needs

Branch network concentrated in the highest growth U.S. markets2

Over 50% of affluent U.S. households live within 2 miles of a Chase branch or ATM Attractive footprint

#1 most visited banking portal in the U.S.3

#1 rated mobile banking app4

Leading position in

digital banking

#1 in total U.S. credit and debit payments volume5

#2 merchant acquirer6

World-class payments

franchise

#1 U.S. credit card issuer7 and #1 U.S. co-brand credit card issuer8

#2 mortgage originator and servicer9

#3 bank auto lender10

National, scale lending

businesses

BA

NK

IN

G

Note: For footnoted information, refer to appendix

56

Page

Agenda

CO

NS

UM

ER

&

C

OM

MU

NIT

Y

BA

NK

IN

G

Appendix 57

Payments 13

Mortgage Banking 24

Banking 37

Consumer & Community Banking 1

1. Consumer Bank household channel segments are defined based on the tenure of the household as of the respective time period. For

households with tenure of greater than 12 months, we use the following thresholds calculated over a year: Digitally-centric – <=4 branch

visits and 12+ digital transactions or 100+ digital log-ins or 24+ external ACH transactions per year; Multi-channel – >4 branch visits and 12+

digital transactions or 100+ digital log-ins or 24+ external ACH transactions per year; Branch-centric – >4 branch visits and <12 digital

transactions and <100 digital log-ins and <24 external ACH transactions per year; Other – <=4 branch visits and <12 digital transactions and

<100 digital log-ins and <24 external ACH transactions per year. For households that are less than 12 months on books, we reduce the

thresholds by 75% and track the household activity over a 3 month time period. Digitally-engaged households includes Digitally-centric

households and Multi-channel households. All other households includes Branch-centric households and Other households

2. Attrition rates are based on Consumer Bank households with deposit products and includes households that closed all of their deposit

products with Chase. Attrition rate for each Consumer Bank household channel segment is calculated by reclassifying households into

segments each month based on their channel activity and by taking an average of the annualized monthly rates for the 12 months of 2016

3. Includes households that had at least one credit transaction and one debit transaction in 2016. Normalized for number of customers per

household

Notes on slide 7 – Our growing digitally-engaged customer base delivers strong

performance metrics

AP

PE

ND

IX

57

Notes on slide 9 – We have substantially reduced expense, while continuing to

prudently invest

AP

PE

ND

IX

Note: Numbers may not sum due to rounding; 2016 exit reflects 4Q16 annualized

1. Includes marketing, investments in select payments and digital projects, and select business growth and technology investments

2. Excludes non-core items, FDIC surcharge, and normalized legal expense at 2014 levels given the legal benefit in 2016

3. Includes employees and contractors

4. Reflects full-year 2016

5. Reflects 2016 exit vs. 2014

6. Reflects full-year 2016 vs. 2014

58

1. FDIC 2016 Summary of Deposits survey per SNL Financial. Excludes all branches with $500mm+ in deposits in any of the last ten

years (excluded branches are assumed to include a significant level of commercial deposits or are headquarter branches for direct banks).

Includes all commercial banks, credit unions, savings banks, and savings institutions as defined by the FDIC. National banks include Wells

Fargo, Bank of America, Citi, and U.S. Bancorp. Super regional banks include all other top 50 banks by retail deposits (excluding deposits

from branches with over $500mm in any of the last ten years)

Notes on slide 39 – We continue to lead the industry in deposit balance growth

AP

PE

ND

IX

59

1. FDIC 2016 Summary of Deposits survey per SNL Financial. Excludes all branches with $500mm+ in deposits in any of the last ten

years (excluded branches are assumed to include a significant level of commercial deposits or are headquarter branches for direct banks).

Includes all commercial banks, credit unions, savings banks, and savings institutions as defined by the FDIC. National banks include Wells

Fargo, Bank of America, Citi, and U.S. Bancorp. Super regional banks include all other top 50 banks by retail deposits (excluding deposits

from branches with over $500mm in any of the last ten years). Chase markets are defined as core based statistical areas (CBSAs) with a

Chase branch. Non-Chase markets are defined as CBSAs without a Chase branch. Chase top 10 markets defined as top ten markets by

deposit balances in 2016. Chase $ deposit growth rank based on total dollar increase in deposits from 2012-2016. Chase share of $

deposit growth represents 2012-2016 increase in Chase deposits as a percentage of 2012-2016 total increase in deposits in each specified

market. Chase growth rate versus the industry ex-Chase represents Chase annual growth rate from 2012-2016 in the specified market

divided by the specified market ex-Chase annual growth rate from 2012-2016

Notes on slide 40 – We have established our physical presence in faster growing

markets

AP

PE

ND

IX

60

1. Represents growth from 4Q12 to 4Q16. Consumer Bank household channel segments are defined based on the tenure of the household as

of the respective time period. For households with tenure of greater than 12 months, we use the following thresholds calculated over a year:

Digitally-centric – <=4 branch visits and 12+ digital transactions or 100+ digital log-ins or 24+ external ACH transactions per year. Multi-

channel – >4 branch visits and 12+ digital transactions or 100+ digital log-ins or 24+ external ACH transactions per year. Branch-centric –

>4 branch visits and <12 digital transactions and <100 digital log-ins and <24 external ACH transactions per year. Other – <=4 branch visits

and <12 digital transactions and <100 digital log-ins and <24 external ACH transactions per year. For households with fewer than 12

months on books, we reduce the thresholds by 75% and track the household activity over a 3 month time period

2. Generations defined by head of household birth years: Millennials – born 1981 – 1997. Gen X – born 1965 – 1980. Baby Boomers – born

1946 – 1964. Silent Generation – born 1928 – 1945

3. Average visits per quarter for those who used the branch in 4Q16

Notes on slide 41 – Three-quarters of our growth has come from customers who

use our branches

AP

PE

ND

IX

61

Notes on slide 56 – We have competitive positions across our businesses, and

opportunity remains to continue to grow

AP

PE

ND

IX

1. Kantar TNS 4Q16 Retail Banking Monitor. Data is based on total U.S. (5K surveys per quarter) and Chase footprint (~2.8K surveys per

quarter); Calculations derived from the following questions: "With which banks do you currently do business?" and "Which do you consider to

be your main or primary bank?“

2. Highest growth U.S. markets refers to top 30 core based statistical areas by deposit balance growth from 2012 to 2016, per SNL Financial

3. SimilarWeb.com as of December 2016 (formerly compete.com)

4. “2016 Mobile Banking Financial Institution Scorecard,” Javelin Strategy & Research, May 2016. Ranking is among large banks

5. The Nilson Report, Issue 1086, May 2016. Data as of 2015

6. The Nilson Report, Issue 1082, March 2016. Data as of 2015. Chase is the #1 wholly-owned merchant acquirer in the U.S. When volume

from JVs and revenue share arrangements are included in First Data’s volume, First Data holds #1 share position in the U.S.

7. Based on 4Q16 sales volume and loans outstanding disclosures by peers (C, BAC, COF, AXP, DFS) and internal JPMorgan Chase

estimates. Sales volume excludes private label and Commercial Card. AXP reflects the U.S. Consumer segment and internal JPMorgan

Chase estimates for AXP’s U.S. small business sales. Outstandings exclude private label, AXP Charge Card, and Citi Retail Cards

8. “Credit Card Monitor 2016: Cobrand Market Shares by Issuer,” Phoenix, for 12-month period ending October 2016. Based on card accounts,

revolving balance dollars and spending dollars

9. Inside Mortgage Finance as of 4Q16 for Servicer and Originator rankings

10. Experian AutoCount data for full-year 2016; bank auto lenders are non-captive auto lenders

62

Forward-looking statements

AP

PE

ND

IX

This presentation contains forward-looking statements within the meaning of the Private Securities

Litigation Reform Act of 1995. These statements are based on the current beliefs and expectations

of JPMorgan Chase & Co.’s management and are subject to significant risks and uncertainties.

Actual results may differ from those set forth in the forward-looking statements. Factors that could

cause JPMorgan Chase & Co.’s actual results to differ materially from those described in the

forward-looking statements can be found in JPMorgan Chase & Co.’s Annual Report on Form 10-K

for the year ended December 31, 2016, filed with the Securities and Exchange Commission and

available on JPMorgan Chase & Co.’s website https://www.jpmorganchase.com/corporate/investor-

relations/investor-relations and on the Securities and Exchange Commission’s website

(www.sec.gov). JPMorgan Chase & Co. does not undertake to update the forward-looking

statements to reflect the impact of circumstances or events that may arise after the date of the

forward-looking statements.

63