cair issue no. 67 - january 2009

DESCRIPTION

InterVISTAS report on aviation industry.TRANSCRIPT

CANADIAN AVIATION INTELLIGENCE REPORT

In this issue…

Features Columns: Regular Reports: • CEO Update (p.1) • Crude Oil Update (p.2) • WestJet Seat Capacity (p.3). • 2008 Airline Market Caps (p.4) • The Environmental Report (p.12) • The Caribbean Report (p.13) • The Asia Report (p.14) • The European Report (p.15) • The Ottawa Report (p.16) • Impacts of New U.S. Administration on

Canada (p.18) • The Washington Report (p.19)

• Airline Data - Canada (p.5) • Airline Data – U.S. (p. 6) • Selected Canadian Airport Data

(p.7) • News (p.8) • InterVISTAS News (p.20)

InterVISTAS’ Canadian Aviation Intelligence Report January 2009 Copyright ©2009 InterVISTAS Consulting Inc., all rights reserved. Page 1

Gerry Bruno President & CEO

CEO UPDATE January 2009

Welcome to InterVISTAS Consulting Inc.’s first edition of the Canadian Aviation Intelligence Report (CAIR) for 2009.

Recapping 2008 The year 2008 certainly gave us a rollercoaster ride. We started off the year well: IATA industry traffic figures showed growth in Revenue Passenger Kilometres (RPKs) in each of the first eight months and in Freight Tonne Kilometres (FTKs) in each of the first five months. Since then, however, there has been a decline in global RPKs and FTKs in every month. The declines were widespread – though the Middle East continued to do well for a while longer, by year end, its monthly cargo numbers were negative and its passenger numbers had softened. In December, industry RPKs were down 4.6%, and FTKs down a stunning 22.6%. Overall, global RPKs finished ahead of 2007 by only 1.6%, and FTKs dropped 4% below 2007 levels.

As we start the new year, it looks like we are in store for continued turbulence for the next while. Our industry, however, is a resilient one, and we remain confident that we will weather this storm as we have so many others. So fasten your seatbelts securely, and prepare for an interesting 2009!

InterVISTAS Projects Update The InterVISTAS Group is currently working on a large number of consulting assignments for a broad range of clients throughout the world. A recent project continues our strong work on cross-border issues:

• Cross-Border Flow Analysis – Value Stream Mapping InterVISTAS Consulting has been retained by Industry Canada to conduct case studies that identify and quantify logistics, security and compliance costs for each of seven Canadian businesses with significant cross-border operations. Underlying causes of border challenges are to be identified, and solutions proposed. Value Stream Mapping will be employed to identify and address weak links and unnecessary delays.

The January CAIR Line-Up Although the global economic downturn continues to be a major focus, there have been a couple of political developments that also will have a significant impact. The Ottawa Report covers the recent federal budget, and a related column discusses the impact of the new U.S. Administration on Canada. In addition to these columns, and the regularly reported airline data, airport data and news stories, the January edition also includes the following updates:

▪ Environment Report ▪ Caribbean Report ▪ Asia Report

▪ European Report ▪ Washington Report

I hope you enjoy this month’s publication and that you have a successful new year!

InterVISTAS’ Canadian Aviation Intelligence Report January 2009 Copyright ©2009 InterVISTAS Consulting Inc., all rights reserved. Page 2

Doris Mak Director

Special Projects

CRUDE OIL UPDATE January 2009

Crude oil prices drop to $41 per barrel, despite OPEC’s December cut Crude oil prices for near term delivery are currently hovering at around $41 per barrel. Over the past month, fuel prices have dropped by nearly $10 per barrel, despite the decision made by the Organization of the Petroleum Exporting Countries (OPEC) in December 2008 to further reduce fuel supply by 2.2 million barrels per day. OPEC had already reduced fuel production by 500,000 barrels per day in September 2008, which was followed by another cut of 1.5 million barrels per day in October 2008. The primary objective of OPEC is to stabilize oil prices between $70 and $90 per barrel, as indicated by OPEC President Chakib Kheli. However, according to oil trader and analyst, Stephen Schork, “After a strong start to 2009… prices… have since collapsed,” and the fluctuations are expected to continue in the short term.

The downward pressure of crude oil prices is primarily caused by the over-supply from crude oil producers, accompanied with weakened consumer demand resulting from a negative global economic outlook. Other factors contributing to crude oil price fluctuations include the uncertainty of the global financial markets, a strengthening U.S. Dollar, a global economic slowdown, and turbulence in the financial and housing sectors.

…with futures prices at $67 by 2012 and $74 by 2016 Currently, a futures contract for delivery of crude oil in December 2012 costs $67 per barrel (65% higher than current spot price), while a futures contract with a December 2016 delivery date costs $74 per barrel (82% higher than current spot price).

Futures prices in January 2009 remain lower than futures prices established in December 2008, as shown in the figure below. A futures contract in January 2009 for delivery of crude oil in December 2012 is currently priced at $67. The price of the same contract would have been 16% higher if purchased in December 2008, or 103% higher if purchased in the peak period in May 2008.

Crude Oil Futures Prices

$0

$20

$40

$60

$80

$100

$120

$140

$160

Jan-

03

Jul-0

3

Jan-

04

Jul-0

4

Jan-

05

Jul-0

5

Jan-

06

Jul-0

6

Jan-

07

Jul-0

7

Jan-

08

Jul-0

8

Jan-

09

Jul-0

9

Jan-

10

Jul-1

0

Jan-

11

Jul-1

1

Jan-

12

Jul-1

2

Jan-

13

Jul-1

3

Jan-

14

Jul-1

4

Jan-

15

Jul-1

5

Jan-

16

Jul-1

6

Month of Delivery

US

$ pe

r Bar

rel

Mar 2008

Crude Oil Spot Prices

Crude OilFutures Prices

May 2008

Sep 2008

Jan 2009

Dec 2008

InterVISTAS’ Canadian Aviation Intelligence Report January 2009 Copyright ©2009 InterVISTAS Consulting Inc., all rights reserved. Page 3

Sean Broadbent Project Analyst

Share of Transborder Seat Capacity (YVR, YYC, YYZ)

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

2004 2005 2006 2007 2008

YVR YYC YYZ

Source: OAG December 2008 disc

CHANGE IN WESTJET SEAT CAPACITY (2004-2008) January 2009

Since its 1996 inception, WestJet has continually expanded its route network, adding domestic, transborder, and international seat capacity. This column evaluates WestJet’s historical seat capacity, specifically growth in its transborder capacity.

Transborder Service Expansion Since 2004, transborder seat capacity increased over 1,100%, growing from 2% of total WestJet seats in 2004 to 12% in 2008. U.S. destinations have expanded from 7 in 2004 (Fort Lauderdale, Los Angeles, New York, Orlando, Phoenix, San Francisco, Tampa) to 13 in 2008 with the addition of Fort Myers, Honolulu, Kahului, Kona, Las Vegas, Newark, Palm Springs, and West Palm Beach (and the elimination of New York and San Francisco). During the same period (2004-2008), WestJet experienced absolute growth of 63% in overall seat capacity.

Moreover, between 2004 and 2008, the number of Canadian points receiving transborder service has increased. Originally offered at Vancouver, Calgary, and Toronto, a total of 13 airports, including Calgary, Edmonton, Halifax, Montréal, Ottawa, Toronto, Vancouver, Winnipeg, Kelowna, Regina, Saskatoon, Victoria, and Hamilton now receive service.

Transborder Capacity grows at YVR, YYZ and YYC Looking exclusively at departing flights from the three original points; Vancouver, Toronto, and Calgary, reveals that much of the capacity growth in transborder services has occurred at these three airports. WestJet dramatically expanded transborder services at all three focus airports, especially Vancouver which experienced a 125-fold increase in its departing transborder seat capacity from 0.1% of total capacity in 2004 to 10.9% of total WestJet seat capacity at the airport in 2008. WestJet transborder seat capacity from Calgary increased 9-fold during the 5-year period ending 2008 to account for 7% of total departing seat capacity, while transborder seat capacity at Toronto increased 6-fold, representing nearly 12% of overall WestJet departing seat capacity at the airport in 2008.

Seat Capacity 2004 - 2008

-

2

4

6

8

10

12

14

16

18

20

2004 2005 2006 2007 2008

Sea

t Cap

acity

(in

mill

ions

)

International

Transborder

Domestic98% 93% 93% 90% 87%

1%

7%7% 9%

12%

2%

Source: OAG December 2008 disc

InterVISTAS’ Canadian Aviation Intelligence Report January 2009 Copyright ©2009 InterVISTAS Consulting Inc., all rights reserved. Page 4

Connie Chang Senior Analyst

2008 AIRLINE MARKET CAPS January 2009

In Canada, the major air carriers have experienced significant declines in their market capitalisation levels over the past year. The nation’s largest airline, Air Canada, saw a decline in its market cap by 80% to CAD$244 million in December 2008 over the same month last year. Comparatively, Westjet saw a less severe, yet significant, decrease in its market cap by 42% declining from CAD$2.9 billion in December 2007 to CAD$1.7 billion in December 2008.

On the other hand, the United States airline industry encountered mixed results. Among the U.S. full service carriers, American and Continental saw increases in its market caps of 28% and 34% respectively, while Delta* and United experienced declining market caps of 33% and 66% respectively, in December 2008 over December 2007. Over the same period, U.S. low cost carriers also encountered varying results. JetBlue more than doubled its market cap to US$1.9 billion, while AirTran and Southwest experienced decreases in market capitalizations by 17% and 34% respectively.

For international airlines, changes in market capitalisation levels were also mixed. In China, China Eastern saw it market cap decline by 84% to US$745 million. Brazilian carrier, GOL Linhas Aereas, had a similar drop of 82% to US$849 million; however, Chilean carrier, LAN Chile SA’s market capitalization more than doubled to US$2.7 billion.

Figure 1: Airline Market Capitalisation by Carrier (US$ billions)

0.00

2.00

4.00

6.00

8.00

10.00

12.00

Air

Can

ada

Wes

tJet

Am

eric

an

Con

tinen

tal

Del

ta*

Uni

ted

AirT

ran

JetB

lue

Sout

hwes

t

US

Airw

ays

Ala

ska

Air

Chi

na E

aste

rn

GO

L Li

nhas

Aer

eas

LAN

Chi

le S

A

Mar

ket C

apita

lisat

ion

($U

S bi

llion

s)

2007 2008

Canada US – Full Service US – Low-Cost US – Misc. International

34%

-66%

-17%

106%

-34%

-27% 53%

-84%

-80%

28%

-33%

-42%

-82%

219%

0.00

2.00

4.00

6.00

8.00

10.00

12.00

Air

Can

ada

Wes

tJet

Am

eric

an

Con

tinen

tal

Del

ta*

Uni

ted

AirT

ran

JetB

lue

Sout

hwes

t

US

Airw

ays

Ala

ska

Air

Chi

na E

aste

rn

GO

L Li

nhas

Aer

eas

LAN

Chi

le S

A

Mar

ket C

apita

lisat

ion

($U

S bi

llion

s)

2007 2008

Canada US – Full Service US – Low-Cost US – Misc. International

34%

-66%

-17%

106%

-34%

-27% 53%

-84%

-80%

28%

-33%

-42%

-82%

219%

Source: Canadian carriers: Air Canada and WestJet 2006 and 2007 Annual Reports and Toronto Stock Exchange. U.S. and International carriers: Aviation Daily, Aviation Industry Stock Performance, December 2007 and December 2008. Notes: Prices are in US dollars, except for Air Canada and WestJet which are presented in Canadian dollars. *Northwest merged with Delta on 31 October 2008; therefore, 2008 year-end market caps represent Delta’s market cap after its acquisition. For comparison purposes, market caps are combined for Northwest and Delta in 2007.

InterVISTAS’ Canadian Aviation Intelligence Report January 2009 Copyright ©2009 InterVISTAS Consulting Inc., all rights reserved. Page 5

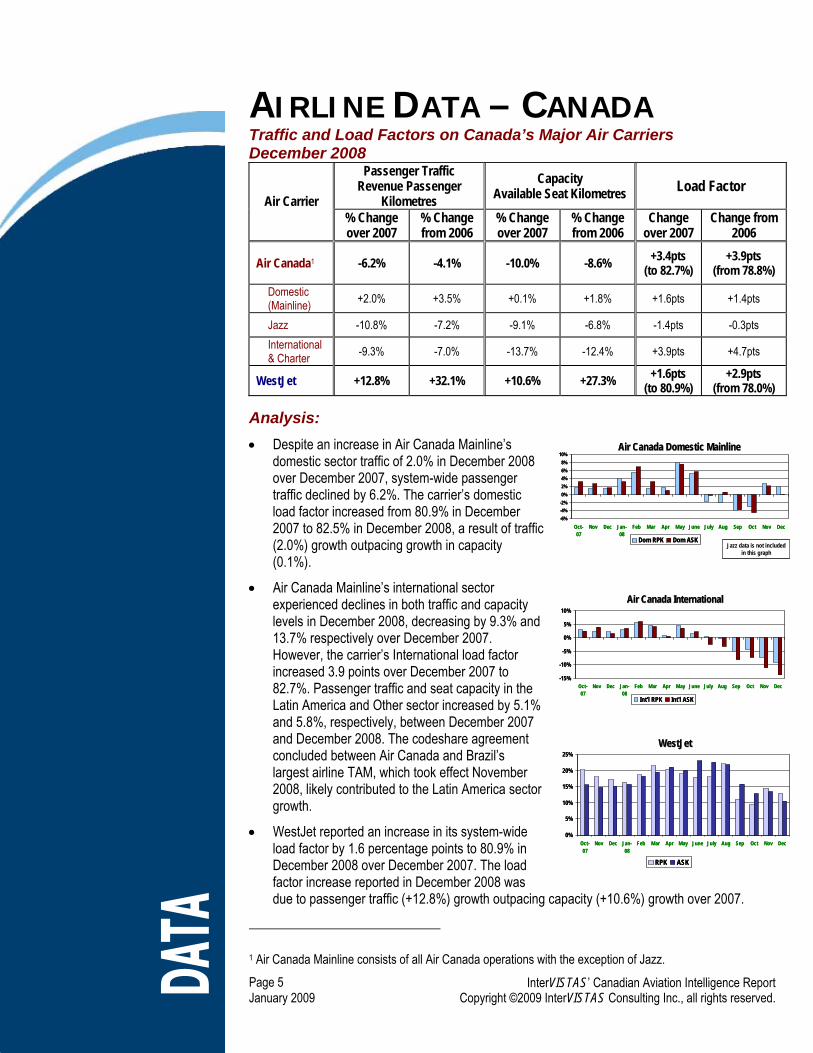

AIRLINE DATA – CANADA Traffic and Load Factors on Canada’s Major Air Carriers December 2008

Passenger Traffic Revenue Passenger

Kilometres Capacity

Available Seat Kilometres Load Factor Air Carrier

% Change over 2007

% Change from 2006

% Change over 2007

% Change from 2006

Change over 2007

Change from 2006

Air Canada1 -6.2% -4.1% -10.0% -8.6% +3.4pts (to 82.7%)

+3.9pts (from 78.8%)

Domestic (Mainline) +2.0% +3.5% +0.1% +1.8% +1.6pts +1.4pts

Jazz -10.8% -7.2% -9.1% -6.8% -1.4pts -0.3pts International & Charter -9.3% -7.0% -13.7% -12.4% +3.9pts +4.7pts

WestJet +12.8% +32.1% +10.6% +27.3% +1.6pts (to 80.9%)

+2.9pts (from 78.0%)

Analysis: • Despite an increase in Air Canada Mainline’s

domestic sector traffic of 2.0% in December 2008 over December 2007, system-wide passenger traffic declined by 6.2%. The carrier’s domestic load factor increased from 80.9% in December 2007 to 82.5% in December 2008, a result of traffic (2.0%) growth outpacing growth in capacity (0.1%).

• Air Canada Mainline’s international sector experienced declines in both traffic and capacity levels in December 2008, decreasing by 9.3% and 13.7% respectively over December 2007. However, the carrier’s International load factor increased 3.9 points over December 2007 to 82.7%. Passenger traffic and seat capacity in the Latin America and Other sector increased by 5.1% and 5.8%, respectively, between December 2007 and December 2008. The codeshare agreement concluded between Air Canada and Brazil’s largest airline TAM, which took effect November 2008, likely contributed to the Latin America sector growth.

• WestJet reported an increase in its system-wide load factor by 1.6 percentage points to 80.9% in December 2008 over December 2007. The load factor increase reported in December 2008 was due to passenger traffic (+12.8%) growth outpacing capacity (+10.6%) growth over 2007.

1 Air Canada Mainline consists of all Air Canada operations with the exception of Jazz.

-6%-4%-2%0%2%4%6%8%

10%

Oct-07

Nov Dec Jan-08

Feb Mar Apr May June July Aug Sep Oct Nov Dec

Dom RPK Dom ASK

Air Canada Domestic Mainline Air Canada Domestic Mainline

Jazz data is not included in this graph

-6%-4%-2%0%2%4%6%8%

10%

Oct-07

Nov Dec Jan-08

Feb Mar Apr May June July Aug Sep Oct Nov Dec

Dom RPK Dom ASK

Air Canada Domestic Mainline Air Canada Domestic Mainline

Jazz data is not included in this graph

-15%

-10%

-5%

0%

5%

10%

Oct-07

Nov Dec Jan-08

Feb Mar Apr May June July Aug Sep Oct Nov Dec

Int'l RPK Int'l ASK

Air Canada InternationalAir Canada International

-15%

-10%

-5%

0%

5%

10%

Oct-07

Nov Dec Jan-08

Feb Mar Apr May June July Aug Sep Oct Nov Dec

Int'l RPK Int'l ASK

Air Canada InternationalAir Canada International

0%

5%

10%

15%

20%

25%

Oct-07

Nov Dec Jan-08

Feb Mar Apr May June July Aug Sep Oct Nov Dec

RPK ASK

WestJetWestJet

0%

5%

10%

15%

20%

25%

Oct-07

Nov Dec Jan-08

Feb Mar Apr May June July Aug Sep Oct Nov Dec

RPK ASK

WestJetWestJet

InterVISTAS’ Canadian Aviation Intelligence Report January 2009 Copyright ©2009 InterVISTAS Consulting Inc., all rights reserved. Page 6

AIRLINE DATA – U.S. U.S. Airlines Release December 2008 Traffic Figures

Airline Traffic (RPMs – millions)

Capacity (ASMs – millions) Load Factor

2,122 ↓1.8%

2,671 ↓5.1%

79.4% ↑2.6 pts

588

↓12.4% 837

↓13.5% 70.2% ↑0.9 pts

5,794 ↑1.1%

8,318 ↓1.0%

69.7% ↑1.5pts

1 7,111 ↓6.7%

8,901 ↓8.9%

79.9% ↑1.2 pts

2 8,204 ↓11.5%

10,263 ↓12.7%

79.9% ↑1.1 pts

10,320 ↓8.2%

13,030 ↓8.6%

79.2% ↑0.4 pts

9,779 ↑0.7%

12,204 ↓2.4%

80.1% ↑2.4 pts

6,041 ↓3.6%

7,376 ↓4.5%

81.9% ↑0.7 pts

2 4,655 ↓1.1%

5,800 ↓6.4%

80.3% ↑4.4 pts

1,456 ↑2.3%

1,825 ↓6.9%

79.8% ↑7.1 pts

721

↓9.7% 907

↓17.5% 79.5% ↑6.9 pts

Notes: 1. Mainline operations only. 2. Load factor includes scheduled service only. Sources: Carrier traffic reports.

InterVISTAS’ Canadian Aviation Intelligence Report January 2009 Copyright ©2009 InterVISTAS Consulting Inc., all rights reserved.

Page 7

Summary of Total Year-Over-Year Passenger Traffic Performance at Selected Canadian Airports

Source: Transport Canada and individual airports’ traffic reports. N/A: not available at press time. Note: Subject to revision.

Toronto Vancouver Montréal-Trudeau Calgary Edmonton Ottawa Winnipeg Halifax Victoria Kelowna Saskatoon Regina St.

John’s November +5.0% +8.5% +6.1% +8.8% +15.6% +11.0% +4.7% +5.7% +10.8% +4.2% +8.4% +9.1% +0.8% December +2.8% +4.4% +8.1% +3.7% +8.2% +9.2% +3.8% +4.2% +8.1% +3.7% +7.5% +3.7% -5.5% 4th Quarter +3.8% +5.2% +7.3% +7.1% +12.4% +9.5% +4.0% +4.8% +8.9% +5.0% +7.7% +6.0% +0.7%

2007

Full Year +1.7% +3.3% +8.7% +8.5% +16.3% +7.4% +5.5% +2.7% +6.6% +11.3% +8.6% +10.2% -0.2% January +4.8% +9.2% +4.3% +4.9% +7.6% +6.4% +4.4% +2.2% +6.1% +4.5% +9.2% -0.3% -2.2% February +7.7% +12.8% +9.8% +7.4% +10.2% +8.3% +7.4% +8.6% +7.9% +10.3% +9.1% +8.3% +4.3%

March +6.2% +8.0% +2.2% +8.0% +8.2% +6.8% +4.7% +20.4% +2.5% +0.7% +19.0% +15.8% +5.8% 1st Quarter +6.2% +9.9% +5.3% +6.8% +8.6% +7.2% +5.5% +11.2% +5.4% +5.0% +12.2% +7.6% +2.7%

April +5.5% +6.2% +3.1% +3.6% +5.3% +10.0% +4.6% +9.2% +3.2% +0.1% +1.9% +3.4% +2.5% May +5.1% +6.7% +1.4% +3.1% +5.9% +7.6% -2.1% +12.1% +3.3% +1.0% +3.5% +5.3% +5.2% June +6.4% +5.1% -2.7% +2.4% +5.2% +8.5% -1.4% +6.6% +7.6% +0.5% +6.1% +2.2% +6.4%

2nd Quarter +5.7% +6.0% +0.5% +3.0% +5.5% +8.7% +0.2% +9.3% +4.7% +0.5% +3.9% +3.6% +4.8% July +3.0% +0.7% -2.1% +1.9% +7.2% +9.1% -1.4% -3.9% +5.6% +2.7% +8.8% -1.5% +0.3%

August +3.0% +0.3% -0.9% +1.0% +4.1% +9.9% -4.8% +2.0% +6.7% +4.8% +8.1% +6.9% +3.0% September -1.6% -6.0% -5.1% -5.7% +4.9% +6.9% -2.4% -4.1% +3.5% +2.0% +14.9% +4.7% +2.5% 3rd Quarter +1.6% -1.4% -2.6% -0.7% +5.4% +8.6% -2.9% -1.8% +5.4% +3.2% +10.5% +3.2% +1.9%

October N/A -3.2% -3.9% -3.4% +6.1% +1.0% -3.7% -1.0% +3.5% +2.4% +12.3% +10.3% +2.7%

2008

November -3.2% N/A N/A -0.1% +2.7% -5.6% -1.3% -8.5% +3.2% -1.1% +7.4% +0.6% +4.3%

InterVISTAS’ Canadian Aviation Intelligence Report January 2009 Copyright ©2009 InterVISTAS Consulting Inc., all rights reserved. Page 8

NEWS AIR CANADA UPDATE NEW SERVICE AC reintroduced weekly non-stop service between Montréal and Fort-de-France, Martinique on 10 December 2008. The initial weekly service will be offered on Saturdays throughout the summer from 4 July 2009 to 29 August 2009 and return to year-round service on 5 December 2009. On 15 December 2008, Air Canada announced the reintroduction of seasonal non-stop service between Montréal and Rome. The daily service, scheduled to begin 20 June 2009, will offer connecting flights via Rome to Bari, Milan, Palermo, and Venice through partner carrier Air One. Air Canada also commenced a new direct, weekly A319 service from Montreal to St. Lucia at the beginning of the 2009 winter season.

ESCAPE PASS INTRODUCED AC launched its new Escape Pass on 8 January 2008, a new incentive directed at both Canadian and American leisure travellers within North America for travel on AC and Jazz between 15 January and 3 May, 2009. The pass is packaged in four or eight one-way trips valid for either three days (Tuesday, Saturday, Sunday) or seven days a week, and sold according to four main regional zones in Canada (Atlantic, Central, Prairies, West/North) and three main zones in the US (Eastern, Western, all North America). Each of the four Canadian zones offers four variations (Domestic, Domestic Plus, Transborder, and Transborder Plus) of the pass that permit travellers to fly to neighbouring zones, across Canada, and to the United States. Purchasers of the Escape Pass may also buy a bonus pass for travel to select international destinations, such as London, Paris, Sao Paulo, Bogota, Lima, or Hong Kong, valid between 14 April and 15 June, 2009.

AIR NEW ZEALAND PROPOSAL REJECTED BY ACCC

On 28 January 2009, The Australian Competition and Consumer Commission (ACCC) rejected a proposal to allow Air New Zealand to enter an

agreement with Air Canada, stating a reduction in competitiveness if the co-operation were accepted. The proposal outlined an agreement that, had it been accepted, would have granted both airlines permission to promote and sell direct flights between Sydney and Vancouver, operated by Air Canada, and Auckland and Vancouver, operated by Air New Zealand. Following the ACCC rejection, AC warned of a potential cut back in its Australian operations, while a disappointed Air New Zealand commented that it would consider an appeal to the Commission’s decision.

WESTJET UPDATE WINNIPEG-ORLANDO SERVICE INTRODUCED

WestJet announced the launch of a new

seasonal service between Winnipeg and Orlando on 12 January 2009. Beginning 4 February 2009, the non-stop service will be offered on a weekly basis until 12 March 2009, increasing to twice weekly service between 13 March 2009 and 3 April 2009.

TORONTO-LA ROMANA AND CALGARY-KAMLOOPS SERVICES LAUNCHED WestJet launched two non-stop services between Toronto-La Romana, Dominican Republic and Calgary-Kamloops on 15 December 2008. Seasonal non-stop service between La Romana-Toronto will operate once a week on Mondays, while new non-stop service between Calgary-Kamloops will operate on a daily basis.

InterVISTAS’ Canadian Aviation Intelligence Report January 2009 Copyright ©2009 InterVISTAS Consulting Inc., all rights reserved. Page 9

NEWS – CON’T WESTJET UPDATE – CON’T WESTJET ADDS NEW NON-STOP SERVICES TO SUMMER SCHEDULE WestJet announced the addition of several new non-stop services to its summer schedule on 18 December 2008. On 3 May 2009, new seasonal non-stop service between Vancouver-Saskatoon, Vancouver-Regina, Vancouver-Fort McMurray, and Fort McMurray-Toronto will commence operation on a daily basis, and Edmonton-Yellowknife service will begin daily operation 4 May 2009. Three-times weekly service between Toronto-Sydney, N.S. will begin 5 May 2009 and daily service between Vancouver-London, Ont., and London, Ont.-Halifax is scheduled to start 11 May 2009. Additional routes added to the summer schedule include three-times weekly service between Calgary-San Diego and Calgary-San Francisco on 1 June 2009 and 2 June 2009, respectively.

WESTJET AND SOUTHWEST CODESHARE AGREEMENT EXECUTED

On 24 December 2008, WestJet and Southwest Airlines officially executed

the agreement to deliver codesharding capabilities in late 2009 between the two airlines. An announcement of both carriers’ intention to enter a formal agreement was made back in July 2008. Over a week earlier on 16 December 2008, WestJet enabled Southwest customers to book flights to Canada on WestJet via a link from southwest.com to WestJet’s booking portal. The move marked a first step in the codeshare relationship between both carriers.

OTHER CANADIAN AIRLINES SUNWING LAUNCHES NEW SEPT ÎLES-PUERTO PLATA SERVICE

Sunwing announced the launch of new

seasonal service from Sept Îles, Quebec to Puerto Plata, Dominican Republic on 25

November 2008. The weekly service will be offered every Wednesday from 11 February 2009 to 8 April 2009.

GO TRAVEL DIRECT INTRODUCES EUROPEAN CAPACITY

Canadian tour operator, GO Travel Direct, announced non-stop service from Montréal to Paris and service

from Toronto, Winnipeg, Halifax, and St. John’s to London on 14 January 2009. Paris service will operate aboard Finnair, following the recently signed bilateral agreement between Canada and the European Union. Paris and London flights will begin service June 2009 and conclude October 2009.

U.S. AIRLINES UNITED AIRLINES AND EGPYPTAIR ENTER CODESHARE AGREEMENT

Star Alliance members United Airlines and EGYPTAIR signed an agreement on 11 December 2008 to offer flights on a

codeshare basis. The partnership will allow United to use its code on EGYPTAIR flights linking New York JFK and London Heathrow with Cairo, while EGYPTAIR will use its code on United flights linking New York JFK with Los Angeles and San Francisco, as well as London Heathrow with Chicago, Los Angeles, San Francisco, and Washington Dulles. The scheduled start date of the codeshare agreement is summer 2009.

InterVISTAS’ Canadian Aviation Intelligence Report January 2009 Copyright ©2009 InterVISTAS Consulting Inc., all rights reserved. Page 10

NEWS – CON’T U.S. AIRLINES – CON’T DELTA OFFERS IN-FLIGHT INTERNET

On 15 December 2008 Delta announced its

intention to equip its aircraft with Aircell’s Gogo in-flight Internet Service. At the outset, Delta will offer Gogo service on 5 Boeing MD-88s that operate between New York LaGuardia, Boston Logan, and Washington National, and a Boeing 757 that operates in its domestic route network. The carrier anticipates equipping 10 aircraft with the in-flight Internet service by the end of 2009 and will initiate Gogo installations on the domestic fleet of its subsidiary Northwest Airlines. Internet access rates of $9.95 for flights less than 3 hours and $12.95 for flights longer than 3 hours will be competitive with domestic airlines that already offer the service.

CARGO LUFTHANSA CARGO DECREASES CAPACITY

Lufthansa Cargo revealed plans to decrease freighter capacity on 22

December 2008 due to declining demand resulting from increasingly difficult economic conditions. The cargo carrier will trim capacity by approximately 10% beginning 1 January 2009 and reduce its cooperation efforts with World Airways, which operated two MD-11F and a Boeing 747-400F. Despite the capacity adjustments, Lufthansa also announced plans to expand cooperation with German-Chinese airfreight carrier Jade Cargo International through a harmonized capacity portfolio, centralized and decentralized frequencies, and bundling of the two organizations’ marketing skills.

PEOPLE IN THE NEWS VAA APPOINTS NEW BOARD

The Victoria Airport Authority (VAA) announced its 2009 Board of Directors on 6 January 2009, naming Christine Stoneman as Board Chair. Stoneman, who served on the VAA Board and Committees

since 2004 and also serves on the Board of Canadian Tourism Human Resource Council, replaced former Board Chair Gordon Denford. Other 2009 VAA Board appointees include Peter Bray, Mel Couvelier, Peter Dolezal, and R. Chad Rintoul.

NEW FAA HEAD APPOINTED With a little over a week remaining in his second term, President George Bush appointed Lynne Osmus as Acting Administrator of the Federal Aviation

Administration (FAA). Current Acting Administrator Bobby Sturgell named Osmus, a former Assistant Administrator for Security and Hazardous Material, following his announced resignation effective 16 January 2009. Osmus is expected to serve in the position until a replacement is made by President Obama and confirmed by the Senate, a typically time-consuming process.

InterVISTAS’ Canadian Aviation Intelligence Report January 2009 Copyright ©2009 InterVISTAS Consulting Inc., all rights reserved. Page 11

NEWS – CON’T AIRPORTS UPDATE NEW RUNWAY AND TERMINAL APPROVED AT HEATHROW

Following six years of

public debate, the construction of a third runway and sixth terminal at London’s Heathrow airport was approved 15 January 2009. As part of the approval process, the UK government imposed environmental restrictions on the additional infrastructure, limiting initial use on the third runway so that the increase in flights does not exceed 125,000 movements per year and allocating green slots that would favour capacity for cleaner and quieter aircraft. High-speed rail service between London and Scotland was also approved by government officials, creating easier access to the airport via an international interchange station at Heathrow.

OTHER IATA PREDICTS TURBULENT 2009

On 9 December 2008 the International Air Transportation Association (IATA)

released its industry forecast for 2009, predicting an industry loss of US$2.5 billion. Some key forecast highlights include a decline in industry revenues of US$501 billion, a decline in yields of 3%, a reduction in passenger traffic of 3%, and a 5% decrease in cargo traffic. Geographically, IATA anticipates North America to be the only region where carriers post a profit in 2009, as Asia-Pacific and European carriers are expected to post losses of US$1.1 billion and US$1 billion, respectively, in 2009. On a positive note, IATA commends the efforts of airlines in restructuring operations since 2001 and cited a 13% decline in non-fuel unit costs and 19% improvement in fuel efficiency.

CANADA AND EU CONCLUDE BLUE SKY AGREEMENT

On 9 December 2008 Canada and the European Union (EU) concluded a comprehensive air transport

agreement consistent with Canada’s Blue Sky policy. The agreement, which will be unrolled in 4 phases over an unspecified timeline, enables enhanced city pairs, new direct markets for Canada’s gateway airports and an introduction to the European market for mid-size airports. Phase I provides direct point-to-point service between any location to/from between any Canadian and EU airport. Phase II permits cargo airlines to operate to/from a third country on routes including Canada or the EU (i.e., 7th freedom rights) and will begin when Canada increases foreign ownership levels to 49%. Phase III of the agreement permits a party to setup and control a new airline in the other’s market (i.e., Right of Establishment). This would be the first time Canada would allow complete foreign ownership of a domestic airline. Furthermore, Phase III permits airlines to fly to the other and beyond to a third country, thus enabling EU carriers to operate U.S. services via Canadian airports, carrying transborder traffic (i.e., 5th freedom rights). Finally, Phase IV grants cabotage rights, which also represents a first for Canada. Phase IV would be contingent upon completion of enabling legislation to allow full ownership and control of carriers by the others’ nationals. The agreement replaces the existing 19 bilateral agreements and opens access to all 27 Member States in the EU, including the eight Member States (Cyprus, Estonia, Latvia, Lithuania, Luxembourg, Malta, Slovakia and Slovenia) with which Canada had no prior air agreements.

12th Hamburg Aviation Conference

Change Course:New Challenges for Financial Viabilityand Economic Sustainability in Aviation

11–13 February 2009InterContinental Hamburg, Germany

Preliminary Conference Programme

In association with

University of British ColumbiaCentre for Transportation Studies

Deutsche Gesellschaftfür Luft- und Raumfahrt

Contact:

For further information please contact:

c/o Michael Vagedes GmbH

Tel.: +49 (0)40 30 30 03 36 (Hotline)

Fax: +49 (0)40 30 30 03 33

E-mail: [email protected]

www.hamburg-aviation-conference.de

Conference venue:

InterContinental Hamburg

Fontenay 10

20354 Hamburg

Germany

Tel.: +49 (0)40 4142 0

Fax: +49 (0)40 4142 2298

Please visit our website:www.hamburg-aviation-conference.de

InterVISTAS’ Canadian Aviation Intelligence Report January 2009 Copyright ©2009 InterVISTAS Consulting Inc., all rights reserved. Page 12

Joe Kelly Director

Environmental Services

THE ENVIRONMENT REPORT January 2009

Oregon Mandates GHG Emissions Reporting The State of Oregon announced a new reporting rule 13 November 2008 that mandates facilities with air discharge permits to measure and submit greenhouse gas (GHG) emissions to the state’s Department of Environmental Quality. The phased reporting program is scheduled to begin 1 January 2009 for businesses with an air discharge permit whose annual GHG emissions exceed 2,500 MT of carbon dioxide-equivalent (CO2e) and will expand to include solid waste, wastewater, electric generation, and electricity/natural gas distribution systems for those businesses not required to have an air quality permit but release over 2,500 MTCO2e. The program was initiated in order for Oregon to participate in the Western Climate Initiative, a partnership between states and provinces to establish a regional GHG trading program of which British Columbia, Manitoba, Ontario, and Quebec are members.

Washington State Introduces Cap-and-Trade Legislation Washington State proposed legislation on 12 December 2008 for a cap-and-trade program to meet regional and statewide greenhouse gas (GHG) emissions reduction goals, consistent with other members of the Western Climate Initiative. Beginning in 2012, the proposed legislation would cap emissions from electric utility-providers and industrial facilities that emit over 25,000 MT of GHGs annually. The allowances required to offset these emissions will be provided by free allocations and auctions, where 10% of total emissions would be distributed via auction. The second phase of the cap-and-trade program, set to begin in January 2015, proposes the inclusion of both transportation and non-transportation fuel use. Although not explicitly stated in the legislation, the point of compliance for regulating fuel usage will most likely occur at the distributor level, not the consumer level. Fuels used for aircraft, trains and marine vessels will be excluded from regulation. Washington State’s announcement of a cap-and-trade system follows a similar announcement made by California, whose proposed legislation will auction 100% of allowances.

SFO to Offer In-Terminal Carbon Offset Kiosks The San Francisco International Airport (SFO) unveiled plans on 24 December 2008 to offer its passengers certified carbon offsets at airport terminal kiosks. Similar to self-service check-in stations already located in airport terminals, carbon kiosks would permit travelers to input their destination and calculate the corresponding carbon footprint and cost associated with offsetting the impact of their flight, which the user can then pay via credit card. SFO and its partner, 3Degrees – a renewable energy and carbon-reduction investment firm – will select offset projects certified by the city’s Environment Department that may include renewable energy ventures in developing nations, methane capture from coal mines, organic and agriculture waste capture, and sustainable forestry, as well as local projects such as energy efficiency programs, solar panel installations, and waste oils to biofuel conversion efforts. The program is scheduled to begin in Spring of 2009.

Browner Appointed “Climate Czar” Carol M. Browner, former Environmental Protection Agency Administrator under President Clinton, was recently appointed White House Coordinator of Energy and Climate Policy by the Obama Administration. The newly created position, referred to as the “Climate Czar”, signals Obama’s commitment to address climate change, environmental regulation, and energy conservation. Browner has a strong resume in environmental protection, law and management consulting and has publicly condemned George W. Bush’s White House as “the worst environmental administration ever.”

InterVISTAS’ Canadian Aviation Intelligence Report January 2009 Copyright ©2009 InterVISTAS Consulting Inc., all rights reserved. Page 13

Jacqueline Clarke Manager,

Strategic Development

THE CARIBBEAN REPORT January 2009

Jamaica Signs Expanded Open Skies Agreement with U.S. The U.S. and Jamaica signed an amendment expanding the countries’ 2002 Open Skies Agreement. The amendment allows U.S. and Jamaican air carriers to make decisions on routes, capacity, and pricing, and fully liberalizes conditions for charters and other aviation activities including unrestricted code-sharing rights. Furthermore, the new agreement permits Air Jamaica, as well as other Jamaican carriers, to expand from hub service between the Eastern Caribbean and the U.S. to direct service, a move that could assist the government’s so far unsuccessful efforts to secure a divestment partner for Air Jamaica. A 2006 InterVISTAS-ga² economic impact study on Open Skies found that traffic growth between newly-liberalized countries averaged between 12 to 35 percent.

JetBlue boosts capacity to the Caribbean in 2009 JetBlue Airways will up gauge to an A320 on its Bermuda-New York route that will result in a seat capacity increase of 50 per cent for the first quarter of 2009. Subject to government approval, the carrier also announced plans to add flights from Fort Lauderdale to Santo Domingo (operated by A320), and to Cancun in May (operated by E90). Also in May, JetBlue will add daily nonstop service to San Juan, Puerto Rico, a previously winter-only route.

Virgin Atlantic adds Caribbean services The UK carrier announced it will increase to twice weekly services from Manchester to Barbados beginning in May and add an additional service between Gatwick and Montego Bay in November. The airline will also commence weekly service to Puerto Rico in November. Eighty percent of the aircraft’s seats will be assigned for passengers joining cruises out of San Juan. The weekly service is expected to generate $30 million annually in tourism revenue for the island of Puerto Rico.

Spirit expands in the D.R. Spirit Airlines will launch service between Fort Lauderdale and Santiago, Dominican Republic, on June 18, with four weekly flights.

CTO Objects to Proposed Levy Increases The Chairman of the Caribbean Tourism Organization (CTO), Harold Lovell, signaled the organization’s intention to lobby against the planned increase in the UK’s Air Passenger Duty. The CTO anticipates that the increase (almost +90%) for economy passengers over a two-year period, from GBP40 to GBP75, could have a significant impact on the region’s attractiveness to UK holidaymakers.

Start-up launches Dominica service Sisserou Airways, a new airline based at Melville Hall Airport on Dominica, has launched service between Dominica and St. Maarten, St. Thomas and Barbados. The carrier will be offering three flights per week between Dominica and each of the three Caribbean destinations with 19-seat Jetstream aircraft.

InterVISTAS’ Canadian Aviation Intelligence Report January 2009 Copyright ©2009 InterVISTAS Consulting Inc., all rights reserved. Page 14

Doris Mak Director,

Special Projects

THE ASIA REPORT January 2009

Singapore Concludes Open Skies with Romania and Czech Republic Singapore has concluded two separate Open Skies Agreements (OSAs) with Romania and the Czech Republic. The signing of the Singapore-Romania agreement took place at the International Civil Aviation Organisation (ICAO) Air Services Negotiation Conference held in Dubai, United Arab Emirates, in early December 2008. The pact allows carriers from both countries to operate any number of flights between Singapore and Romania. On 19 January 2009, Singapore also signed an OSA with the Czech Republic. This agreement allows carriers of both nations to operate an unlimited number of flights between Singapore and the Czech Republic and beyond (with the permission of the third country). Singapore now has OSAs with 16 nations of the European Union.

Singapore Establishes Open Skies with Its First African Country Singapore also established its first OSA with an African country, with the signing of an agreement with Zambia. Also signed at ICAO’s Air Services Negotiation Conference, the pact allows both passenger and cargo carriers of Singapore and Zambia to operate an unlimited number of flights between the countries and beyond. To date, Singapore has concluded OSAs with more than 30 countries.

China’s Government Provides Financial Aid to Major Carriers The Chinese Government has increased the size of their financial aid package to China Eastern Airlines to 7 billion yuan (equivalent to US$1 billion), more than double the amount originally secured by the carrier in a Hong Kong stock exchange filing in early December 2008, worth 3 billion yuan (or US$437 million). The cash injection to China Eastern Airlines will be made through a share issue to its parent company, CEA Holding, and to CEA Holding’s overseas arm, CES Global. China Eastern is currently in the weakest financial position among major Chinese carriers.

The Government of China had also agreed to a 3 billion yuan (approximately US$437 million) financial aid package to China Southern in early December 2008, but there has not been any indication of an increase in the carrier’s financial aid package similar to that of China Eastern. This was followed by an announcement made by Hainan Airlines, China’s fourth largest carrier, on securing a government aid package.

A Change in China’s Tax Regime May Hurt Carriers The Government of China introduced changes to their tax regime in mid-December 2008 that is aimed to raise revenues from foreign businesses. Effective 1 January 2009, the change includes a 5% tax on revenues generated by foreign companies leasing aircraft to Chinese carriers. According to an article from the Wall Street Journal, the new tax may have a negative impact on China’s airlines, as it would likely be passed on as a price increase to the Chinese carriers. The new tax is expected to cost the airlines somewhere in the range of US$54 million to US$90 million.

Australian Government Approves Essendon Airport’s Master Plan The Australian Government has recently approved Melbourne’s Essendon Airport master plan for the general aviation facilities over the next 20 years, assuring that it has “no current plans” to close the airport or relax its existing curfew. Although the airport operating company has a 50-year lease to operate the airport, with an additional 49 year option, Essendon Airport has been facing opposition of the Victoria state premier, John Brumby, and the “Close Essendon Airport Campaign”, which raises concerns on noise, environmental issues and safety and calls for the airport’s operations to be transferred to other airports in Melbourne, such as Avalon and Melboune Tullamarine. In response to these concerns, the Australian Government has ordered the airport operator to develop strategies on dealing with these externalities and to report back by April 2009.

InterVISTAS’ Canadian Aviation Intelligence Report January 2009 Copyright ©2009 InterVISTAS Consulting Inc., all rights reserved. Page 15

Ian Kincaid Director,

Economic Analysis InterVISTAS - EU

UK Office

THE EUROPEAN REPORT January 2009

Air France KLM Purchases 25% Stake in Alitalia Air France (AF) KLM became a minority partner in the reorganized Alitalia on 13 January 2009, after purchasing a 25% stake in the restructured carrier. Alitalia filed for bankruptcy protection in August 2008 and has entertained offers from potential buyers including Lufthansa and British Airways since the filing. AF KLM represented the best fit due to its membership in SkyTeam, its existing antitrust immunity with Alitalia on transatlantic routes, and its joint venture with Alitalia on routes between France and Italy since 2002. AF KLM expects the new partnership to include a multi-hub strategy featuring Paris Charles de Gaulle, Amsterdam Schiphol, Rome Fiumicino and Milan Malpensa.

Airbus reports 777 net aircraft orders in 2008 Airbus announced its 2008 results at an annual press conference on 15 January 2009, and acknowledged the challenging environment in the global aviation industry over the next 12 months. The aircraft manufacturer received 900 gross orders in 2008, but after experiencing over 120 cancellations, finished the year with a total of 777 net orders (compared to 1,341 net orders in 2007). Over half of the cancellations were due to the collapse of Skybus, a U.S.-based low-cost carrier, which had 65 A320s on order. Despite the cancellations, total net orders at Airbus represented 54% of the market share for commercial aircraft with passenger capacity above 100 seats, ranking it ahead of the 662 orders reported by Boeing. Airbus deliveries totalled 483 for 2008, surpassing 2007 shipments by 30 aircraft, and included its target of 12 A380 aircraft. Sales of the A380 declined in 2008 over 2007, decreasing 14 units from 23 in 2007 to 9 in 2008, and are expected to be slow in 2009 with 10 new orders. Airbus estimates 2009 to be a soft year for all aircraft sales and estimates between 300-400 gross orders for the year.

European Airlines Must Compensate for Cancelled Flights On 24 December 2008, the European Commission welcomed a decision by the European Court of Justice that established legal precedence for airlines to compensate passengers for flights cancelled for technical reasons. The decision follows the case of Friederike Wallentin-Hermann v Alitalia, which resulted from the cancellation of an Alitalia flight from Vienna to Brindisi via Rome on 28 June 2005 due to a complex engine defect in the turbine. Alitalia considered the mechanical problem an extraordinary circumstance, which under European Union rules would not require any monetary compensation from the air carrier due to the problem being beyond its control. However, according to the latest European Court of Justice ruling technical issues identified during aircraft maintenance, such as a defective engine turbine, do not constitute an extraordinary circumstance that would permit airlines to avoid compensating passengers for cancelling the flight. Opponents of the decision, including the European Regions Airline Association, criticized the Court for putting passenger rights ahead of passenger safety.

Vueling and Clickair Receive Merger Authorisation The European Commission’s Directorate General for Competition issued authorisation for Vueling and Clickair to continue merger proceedings on 14 January 2009. The merger will double Vueling’s size, making it the leading airline in its Barcelona and Seville hubs. If the integration continues as planned, customers could see a combined Vueling/Clickair offering as early as summer 2009.

InterVISTAS’ Canadian Aviation Intelligence Report January 2009 Copyright ©2009 InterVISTAS Consulting Inc., all rights reserved. Page 16

Fred Gaspar Regional Vice President

InterVISTAS Ottawa Office

THE OTTAWA REPORT January 2009

Federal Budget The most anticipated federal budget in recent memory was tabled in the House of Commons on 27 January 2009. The budget was crafted in direct response to rapidly-developing economic and political crises that began to dominate public discourse in Ottawa, following the Government’s poorly-received fall economic update.

In response to opposition demands for more aggressive action on the emerging economic crisis, the government’s budget contained an assertive set of deficit-spending priorities to stimulate the economy away from recession:

Immediate Action to Build Infrastructure

o Almost $12 billion in new infrastructure stimulus funding for roads, bridges, broadband internet access, electronic health records, laboratories and border crossings across the country.

Action to Reduce Taxes and Freeze Employment Insurance Rates

o $20 billion in personal income tax relief.

Action to Stimulate Housing Construction

o $7.8 billion to build housing, stimulate construction, and enhance energy efficiency. Measures include a renovation tax credit of up to $1,350, funding for energy retrofits, investments for social housing to support low-income Canadians, seniors, persons with disabilities and Aboriginal Canadians, and low-cost loans to municipalities.

Action to Improve Access to Financing and Strengthen Canada’s Financial System

o $200 billion through the Extraordinary Financing Framework to improve access to financing for consumers and allow businesses to obtain the financing they need to invest, grow and create new jobs.

Additional Direct Supports

o $8.3 billion for the Canada Skills and Transition Strategy, which includes enhancements to Employment Insurance and funding for skills & training.

Action to Support Businesses and Communities

o $7.5 billion in targeted support for the auto, forestry and manufacturing sectors, as well as funding for clean energy.

InterVISTAS’ Canadian Aviation Intelligence Report January 2009 Copyright ©2009 InterVISTAS Consulting Inc., all rights reserved. Page 17

THE OTTAWA REPORT – CON’T January 2009

The bottom lines of this budget are dramatic:

Budget deficits for the next 5 years:

o $1.1 billion in 2008–09;

o $15.7 billion in 2009–10;

o $14.3 billion in 2010–11;

o $8.3 billion in 2011–12;

o $2.3 billion in 2012–13; and,

o A surplus of $5.5 billion in 2013–14.

Boost to real GDP of 2.5 per cent by the end of 2010.

Creation or maintenance of about 265,000 jobs by the end of 2010.

Opposition Coalition In response to the dramatic reversal of course by the Government, the new leader of the opposition Liberal Party, Michael Ignatieff, signaled his intent to support the budget on condition that the government agree to a regular reporting schedule to Parliament on progress, relative to expectations; terms which the Conservatives quickly accepted. With this development, speculation over a change in government or an imminent election has fallen by the wayside in Ottawa.

InterVISTAS’ Canadian Aviation Intelligence Report January 2009 Copyright ©2009 InterVISTAS Consulting Inc., all rights reserved. Page 18

Fred Gaspar Regional Vice President

InterVISTAS Ottawa Office

IMPACT OF NEW U.S. ADMINISTRATION ON CANADA January 2009

The incoming U.S. administration has already signalled a number of dramatic and immediate policy reversals from the previous administration. From a Canadian public policy perspective, changes in the United States have the potential to significantly impact many of Canada’s own priorities.

The two earliest indicators of potentially contentious areas between the two countries involve trade policy and security. With respect to the former, Canadian government officials and stakeholders will focus early on the new administration’s mandate the extent to which a discernable shift towards trade protectionism takes hold in an attempt to bolster U.S. domestic production.

On the issue of security, Canada will likely face increased pressure to extend its military commitment to Afghanistan, in response to President Obama’s own stated commitment in that area.

Incoming Director of the U.S. Department of Homeland Security, former Arizona Governor Janet Napolitano, brings extensive experience to her role. As a border governor with six ports of entry in her state, Napolitano has fought to curb illegal immigration, but has been skeptical of simplistic, ideologically-driven proposals to confront immigration challenges, having once remarked; "You build a 50-foot wall, somebody will find a 51-foot ladder." She was the first governor to call for National Guard troops to secure the U.S.-Mexico border.

Last year, her state passed a law that requires all Arizona businesses to use the federal online database, E-Verify, to confirm that new hires have valid Social Security numbers and are eligible for employment. This has been a cornerstone of the Bush administration's immigration policy.

Overall, Napolitano’s approach to border management during her tenure in Arizona can best be characterized as zealous pragmatism. She has demonstrated a clear resolve to take decisive measures to address border concerns, while resisting simplistic but politically popular measures.

Napolitano is not new to Canada and its issues, having previously participated in a joint climate change pact with other western premiers and governors, as well as having been instrumental in promoting the CANAMEX trade corridor running from Western Canada south to Mexico. Moreover, during her tenure as Arizona Governor, she has been a leader in developing WHTI-compliant driver’s licenses.

Ms. Napolitano travelled to Ottawa last year for talks with the Prime Minister on border security and trade -- a first-ever visit for an Arizona governor -- that highlighted her interest in expanding the $3-billion in bilateral trade between her state and Canada.

Notwithstanding her pre-existing understanding of Canadian issues and interests, Napolitano will be confronted with ongoing operational and political concerns within the department and on Capitol Hill regarding the perceived porous nature of the northern border.

It is imperative that Canadian stakeholders engage her early and directly with an education campaign aimed at demonstrating a clear and working-level commitment to facilitating the department’s security goals on the northern border. The degree to which Canadian airports, in particular, can demonstrate and communicate the value of passenger processing improvements in the context of delivering an enhanced level of security for the United States, will help frame the Secretary’s perspective on DHS investments in Canada (i.e. preclearance).

InterVISTAS’ Canadian Aviation Intelligence Report January 2009 Copyright ©2009 InterVISTAS Consulting Inc., all rights reserved. Page 19

Jon Ash President,

InterVISTAS – ga2 Consulting Inc. Washington, D.C.

THE WASHINGTON REPORT January 2009

Update on U.S.-EU Open Skies The U.S. and the European Union (EU) are expecting to meet for another round of second stage open skies negotiations, likely to take place in Spring 2009. The first round of second-stage negotiations was held in May 2008 in Slovenia and the second stage in September 2008 in Washington DC. According to John Byerly, the U.S. State Department Deputy Assistant Secretary for Transportation Affairs, there are many U.S. proposals on the agenda for the third round, including full seventh freedom cargo rights for U.S. carriers to match those enjoyed by the EU under the first-stage open skies negotiations, stronger reassurance that the EU will implement a “balanced approach” to airport noise management endorsed by the International Civil Aviation Organization (ICAO), and discussion of issues around cross-border investment in airlines. The EU, on the other hand, is hoping for an Open Aviation Area between the two countries, which would allow unlimited cabotage, unlimited rights for each country to own and control airlines in the other country, and extensive regulatory convergence. However, according to John Byerly, this “is not going to happen in the near term”, as these changes would require statutory amendment and consensus among labour, airlines, airports, and the incoming Administration and Congress.

DOT Announce Changes to Passenger Rights The U.S. Department of Transportation (DOT) recently adopted several legislative changes involving passenger rights. The minimum limit on lost baggage liability was increased from the previous US$3,000 per passenger to US$3,300 per passenger. As well, the maximum civil penalty for most violations of aviation economic regulations and statutes was also raised, including an increase from $25,000 to $27,500 for failing to make required payments. The DOT also recently proposed a rule requiring airlines to develop contingency plans for tarmac flight delays, which is to be included in the contract for carriage. This will allow passengers to sue a carrier in state court for mistreatment during tarmac delays.

FAA Inaugurates Washington Airspace Restrictions The Federal Aviation Administration (FAA) recently announced a final rule making permanent the airspace restrictions and procedures implemented around Washington, D.C. The airspace restrictions were initially implemented as a result of the 9/11 terrorist attacks to enhance safety and security. The secure airspace is made up of two concentric rings. The interior ring, the Flight Restricted Zone (FRZ), is a 15-nautical mile radius around the Ronald Reagan Washington National Airport and is restricted to flights authorized by the FAA and the Transportation Security Administration (TSA). The outer ring, the Special Flight Rules Area (SFRA), is a 30-nautical mile radius around the Airport and it requires pilots to file flight plans, communicate with air traffic control using a two-way radio and operate the aircraft transponder on the transponder code assigned by air traffic control. This rule will allow air traffic controllers and security agencies to monitor air traffic and ensure that all aircraft in the Washington airspace comply with instructions from air traffic controllers.

FAA Reduces Israel’s Aviation Safety Rating to Category 2 After assessing Israel’s civil aviation authority in July 2008, the FAA downgraded the country’s safety standard rating to Category 2, from the Category 1 rating that it has maintained since November 1995. Under Category 2, Israeli air carriers will not be allowed to begin new services to the U.S. The Civil Aviation Authority of Israel is responding to this downgrade by working with the FAA on an aggressive action plan to ensure that their safety oversight systems adhere to safety standards established by the ICAO.

InterVISTAS’ Canadian Aviation Intelligence Report January 2009 Copyright ©2009 InterVISTAS Consulting Inc., all rights reserved. Page 20

InterVISTAS’ Canadian Aviation Intelligence Report is a collection of information gathered from public sources, such as press releases, media articles, etc., information from confidential sources, and items heard on the street. Thus, some of the information is speculative and may not materialise.

To inquire about advertising opportunities or to provide comments/feedback on the InterVISTAS’ Canadian Aviation Intelligence Report, please contact Robert Andriulaitis at [email protected] or 1-604-717-1807.

To subscribe, please send an email to [email protected]

To unsubscribe, please send an email to [email protected]

INTERVISTAS NEWS InterVISTAS Upcoming Speaking Engagements Dr. Mike Tretheway, Executive Vice President, Chief Economist • BC Premier’s Economic Summit: Vancouver, BC – 3-4 February 2009.

Dr. Tretheway will be speaking on the Tourism Panel at the Economic Summit.

• Canadian Airports Council Conference: Ottawa, ON – 30 April 2009. Dr. Tretheway will chair a session titled “The Future of the International Airline Sector”.

Robert Andriulaitis, Vice President, Transportation & Logistics Studies • BC Tourism Industry Conference: Vancouver, BC – 11-12 February 2009.

Mr. Andriulaitis has been invited to participate in a panel discussing “Trends in Air Transportation You Need to Know”.