callable bonds & swaptions - dnatrainingconsulting.net - printout.pdf · callable bonds &...

TRANSCRIPT

Callable Bonds & Swaptions

Callable Bonds & Swaptions

www.dnatrainingconsulting.net © DNA Training & Consulting1

Outline

PART ONE

! Chapter 1: callable debt securities generally; intuitive approach to pricing embedded call

! Chapter 2: payer and receiver swaptions; intuitive pricing approach

www.dnatrainingconsulting.net © DNA Training & Consulting2

Outline

PART TWO

! Chapter 3: standard pricing model for European swaptions

! Chapter 4: standard pricing model for European and Bermudan callable bonds

www.dnatrainingconsulting.net © DNA Training & Consulting3

Outline

PART THREE

! Chapter 5: applications involving swaptions and callable bonds; combining swaptions with callable bonds to provide cost-efficient financing

! Chapter 6: Quiz

www.dnatrainingconsulting.net © DNA Training & Consulting4

Chapter 1

! Introduce callable debt securities

! Intuitive approach to pricing embedded call

www.dnatrainingconsulting.net © DNA Training & Consulting5

! Simplest form of callable bond is one that contains single option to prepay instrument on one specific future date prior to maturity

! Example:

" ABC is able today to issue 5-year debt at par, paying 6% s.a.

" ABC anticipates that rates will decline significantly in next couple of years, and would like to refinance fixed-rate debt at lower cost when this occurs

" ABC proposes to investor 25 bps yield pick-up, to 6.25%, in return for allowing ABC, on bond’s second anniversary, to prepay it in whole at par

Callable bonds: introduction

www.dnatrainingconsulting.net © DNA Training & Consulting6

! If issuer view is right, issuer will be able in 2 years’ time to issue

3-year debt at substantially lower rate than those prevailing on day

one

! Issuer would prepay outstanding bond and reissue for remaining 3years at lower rate

! Brings aggregate cost for entire 5-year period potentially lower than 6% originally available on 5-year straight debt

Callable bond: issuer benefits

www.dnatrainingconsulting.net © DNA Training & Consulting7

Callable bond: sample term sheet

6.25%, paid semi-annuallyCoupon

The bond may be prepaid on its second anniversary at par (plus accrued and unpaid interest)

Prepayment

Senior unsecuredStatus

5 yearsTenor

$100Issue price

$100Face Value

Company ABCIssuer

Term Sheet

www.dnatrainingconsulting.net © DNA Training & Consulting8

! On second anniversary, assume ABC can issue 3-year non-callable debt at 5% s.a.

! ABC would call original debt at par

! ABC would refinance it for 3 years at 5%

! ABC’s all-in cost over entire 5-year period would fall between 6.25% and 5%

Scenario analysis

www.dnatrainingconsulting.net © DNA Training & Consulting9

Principal 100 -100.000Coupon yrs 1-2 6.25% 3.125Coupon yrs 3-5 5.00% 3.125

3.1253.1252.5002.5002.5002.5002.500

102.500

Semi-annual IRR 2.77%

Annualized IRR 5.54%

Calculating All-in Cost Over 5 Years

www.dnatrainingconsulting.net © DNA Training & Consulting10

Scenario analysis

RefinanceRefinanceLeave original

bond outstandingOutcome

AIC < 6%6% < AIC < 6.25%AIC = 6.25%All-in-cost

3

Rate < 5.81%

2

6.25% > Rate > 5.81%

1

Rate > 6.25%Scenario

3-year rate on second anniversary

►By issuing callable, issuer is implicitly assuming that 3-yr rates have reasonable probability, on second anniversary, to have fallen below 5.81% from current level

►Not sufficient for rates generally to decline for issuer to save money►They must decline enough so issuer savings in years 3-5 > coupon premium incurred in years 1-2 on PV basis

www.dnatrainingconsulting. net© DNA Training & Consulting

11

! Often call right is not “European”, but “Bermudan”; so rather than arising only on a specific anniversary, right arises on any coupon payment date on or after that specific anniversary

! Call price may not be exactly par: common to set call price > par if bond is called early, then have call price decline gradually towards par the later the call date

Call provision: alternative styles

www.dnatrainingconsulting.net © DNA Training & Consulting12

“Bermudan” callable bond

Term Sheet

Issuer Company ABC

Face Value $100

Issue price $100

Tenor 5 years

Status Senior unsecured

Coupon 6.35%, paid semi-annually

Prepayment The bond may not be prepaid until the second anniversary. On or after the second anniversary, the bond may be prepaid as follows:

"If called on the second anniversary, call price is 101.60

"If called on the third anniversary, call price is 100.80; and

"If called on the fourth anniversary, call price is 100 (par)

www.dnatrainingconsulting.net © DNA Training & Consulting13

! Call price premium compensates investor for early call, since investor undertook process of obtaining internal approvals and reviewing documentation, and incurred significant legal expenses

! Also investor may have to reinvest returned principal at unattractive levels, given decline in interest rates, impacting portfolio performance

! This is classic reinvestment risk

! Note 0.10% additional coupon under Bermudan alternative, and step-down in call price from 101.80 to 100 over time

! Both features are consistent with greater issuer flexibility allowed by Bermudan call relative to European

Bermudan callable – investor perspective

www.dnatrainingconsulting.net © DNA Training & Consulting14

-100.000 Principal 100

3.1753.1753.175

3.175 Coupon Call Price

3.175 Years 1-3 6.35% 100.803.975 Years 4-5 5.50%

2.7502.7502.750

102.750

Semi-annual IRR 3.10%

Annualized IRR 6.20%

Calculating Breakeven for Call on Third Anniversary

www.dnatrainingconsulting.net © DNA Training & Consulting15

Breakevens for Bermudan callable

5.14%

Second

Anniversary

Breakeven rate on call date for

remaining tenor

4.96%

Third

Anniversary

4.37%

Fourth

Anniversary

Breakeven Rate

Called on

!The later issuer exercises call and refinances, the more rates

for remaining maturity must decline to achieve breakeven

www.dnatrainingconsulting.net © DNA Training & Consulting16

! If interest rates change rapidly, and by large amounts, value to

issuer of bond prepayment privilege > than if rates stable

! Chances that rates will fall below breakeven level are greater in

more volatile markets.

! Manifests itself in larger upward adjustment for callable bond

coupon versus non-callable alternative than in markets with stable

rates

! Restatement of principle that options on high volatility assets are

more valuable than options on low volatility assets

Volatility: intuitive impact on call price

www.dnatrainingconsulting.net © DNA Training & Consulting17

! Intuitively would expect that flat curve implies higher chance of

declining rates than steep curve, so prepayment option should be

more expensive for issuer when curve is flat

! But offsetting this is fact that when curve is steep, shorter rates are

lower than longer rates, so even absent any drop in rates it may

make sense to refinance, just to take advantage of the curve

“rolldown” effect

Effect of curve shape

www.dnatrainingconsulting.net © DNA Training & Consulting18

! Assume flat curve at 6%, and 5-year bond callable only on first

anniversary. Pricing model has led you to 6.25% coupon for

callable alternative

! In one year, 4-year rate, currently at 6%, needs to have fallen or

remained same, or have risen no higher than 6.25%, i.e. by no

more than 25 bps, for bond to be worth refinancing

Effect of curve shape

www.dnatrainingconsulting.net © DNA Training & Consulting19

! Now assume a positive curve, whose 5-year point is still at 6%, but

whose 4-year point is presumably lower, at 5.50% say. Again we

suppose bond callable on first anniversary comes with 6.25%

coupon

! True, curve shape implies generally higher probability of rate

increase, which appears to diminish value of prepayment option;

but offsetting this is fact that refinancing still makes economic

sense if, in one year, 4-year rate has risen no more than 75 bps,

versus only 25 bps with flat curve

! In fact option with flat curve still turns out generally more valuable

than with steep curve, but simple intuition is not sufficient to lead to

correct result

Effect of curve shape

www.dnatrainingconsulting.net © DNA Training & Consulting20

Chapter 2

! Introduce payer and receiver swaptions

! Intuitive approach to pricing

www.dnatrainingconsulting.net © DNA Training & Consulting21

! Borrower has 5-year debt at L + 75 bps, and is worried that rates may increase

! Borrower could simply swap from floating to fixed; if 5-year swap rate is 6%, all-in cost would come to 6.75%

! Borrower is contemplating currently divestiture of a division, expected to close in one year, which if implemented would enablehim to prepay loan and eliminate interest rate worries

! Should divestiture not close, borrower would like to switch intofixed

Swaptions: introduction

www.dnatrainingconsulting.net © DNA Training & Consulting22

Rather than enter immediately into 5-year swap, borrower pays upfront premium of 80 bps for right to enter 4-year swap at 6% (against Libor) inone year’s time, where borrower pays fixed

Swaption as flexible hedge

! Debt prepaid

! Exercise swaption

! Assign swap to bank (unwind) and collect FMV

! Exercise the swaption and fix debt at 6%

! Debt prepaid

! Swaption is worthless so no exercise

! No exercise:

! Either retain floating debt at L+75bps, or

! Swap at prevailing market rate

Divestiture

4-yearswap > 6%

4-yearswap < 6%

SuccessFailure

www.dnatrainingconsulting.net © DNA Training & Consulting23

Swaption term sheet

6m LiborSwap floating rate

30/360Fixed rate convention

BankParty paying floating

Act/360Floating rate convention

Term Sheet

6%, payable semi-annuallySwap fixed rate

BorrowerParty paying fixed

4 yearsUnderlying swap tenor

1 yearSwaption tenor

0.80%, payable upfrontPremium

$100 millionNotional

www.dnatrainingconsulting. net© DNA Training & Consulting

24

Borrower has purchased a payer swaption; in reference to fact that he is party acquiring option, and option gives him right to pay

fixed rate of 6% under underlying swap

We always link position to swap’s fixed leg

Bank is described as having sold a payer swaption

Note very importantly: verb “purchase” which applied to borrower becomes “sell” from bank’s perspective; but underlying swap is still a “payer” and does not become a “receiver”

Swaption terminology

www.dnatrainingconsulting.net © DNA Training & Consulting25

Now assume investor owns FRN paying Libor flat, and is worried that rates may diminish, so is considering entering a receive-fixed swap to create a synthetic fixed-rate investment

Investor however is still uncertain about direction of rates near-term, so rather than enter into swap immediately, he pays 80 bpsupfront to bank, in return for right, in one year’s time, to receive

fixed at 6% and pay Libor for another 4 years

We say in this case investor has bought receiver swaption, and that bank has sold receiver swaption

Swaption terminology

www.dnatrainingconsulting.net © DNA Training & Consulting26

We refer to swaption with which we began chapter as a 1 x 4

First figure (“1”) indicates tenor in years until option expiration, and second figure (“4”) indicates tenor of underlying swap from date of option expiration, i.e. from when swap comes alive

Swaption notation

www.dnatrainingconsulting.net © DNA Training & Consulting27

Swaption risk factors

PayerReceiver

ShortLongShortLong

Vol Down +–+

–+–+Vol Up

–

–++–Curve Up

+––+Curve Down

www.dnatrainingconsulting.net © DNA Training & Consulting28

Short vol swaption trade

What should trader do if she has no strong directional view on curve shifts, but believes vols are unsustainably high and very likely to decline?

Trader sells swaption “straddle”, i.e. sells both receiver and payer with same strike, and earns two upfront premiums

Assuming rates do not move too much (in either direction), she enjoys large gain from diminution in vols

Any loss on either position from curve movement, if it is not too large, will be offset to some degree by gain on other position, but probably not of same magnitude

www.dnatrainingconsulting.net © DNA Training & Consulting29

Swaptions may be European or Bermudan or even American

Bermudan version may be exercised on more than one single date, but is still limited to specific dates only

American swaption may be exercised on any date prior to expiration

Swaption variations

www.dnatrainingconsulting.net © DNA Training & Consulting30

Additional issue (relevant to Bermudan and American alternativesonly):

! is tenor of underlying swap fixed upfront (“constant maturity swaption”), or

! does it depend on date of exercise, diminishing in tenor the later the exercise date (“remaining maturity swaption”)

Most common version of “remaining maturity swaption” fixes maturity date of underlying swap irrespective of option exercisedate.

So if a 5x5 Bermudan is exercised after 3 years, underlying swapwould have 7-year tenor; but if exercise happens one year later, underlying swap’s tenor would be 6 years

Swaption variations

www.dnatrainingconsulting.net © DNA Training & Consulting31

Constant v. remaining maturity

6%, s.a. (30/360)6%, s.a. (30/360)Swap strike

Bank BankParty paying floating (6-mo. Libor, A/360)

BorrowerBorrower Party paying fixed

,where n is number of years elapsed since trade date

4 yearsUnderlying swap tenor

Option may be exercised on any of 1st, 2nd, 3rd, or 4th anniversary after trade date

Option may be exercised on any of 1st, 2nd, 3rd or 4th

anniversary after trade date

Swaption tenor

0.90%, payable upfront1.00%, payable upfrontPremium

$100 million$100 millionNotional

Alternative 2 (“remaining

maturity swap”)

Alternative 1 (“constant

maturity swap”)

(5-n) years

www.dnatrainingconsulting. net© DNA Training & Consulting

32

Under Alternative 1, underlying swap tenor is always 4 years, irrespective of exercise date

Under Alternative 2, tenor diminishes the later the exercise date and always equals remaining number of years since inception, assuming a total of 5 years

Constant v. remaining maturity

www.dnatrainingconsulting.net © DNA Training & Consulting33

Both versions are usually more expensive than European alternative, since they provide more flexibility to owner regarding exercise privilege

Alternative 1 is more expensive than Alternative 2, since it carries same number of exercise rights as Alternative 2, but involves underlying whose duration (price volatility) is higher than Alternative 2’s for all but first exercise date

Constant v. remaining maturity

www.dnatrainingconsulting.net © DNA Training & Consulting34

Buyer has right, but not obligation, on (or sometimes before) option expiration date, to enter cross-currency swap at pre-determined notionals, coupons and tenor

International borrower issues 7-year USD debt, but purchases option to swap last 5 years of debt’s coupons, as well as principal repayment, into EUR if he sees risk of USD appreciating against EUR

Swaption alternative: cross-currency swaption

www.dnatrainingconsulting.net © DNA Training & Consulting35

Cross-currency swaption

1) At inception

2) At swaption expiration, if swaption exercised

3) Periodic payments under CCS

4) At CCS maturity

► Index can be floating or fixed with different frequencies and day-counts

SwaptionBuyer

Bank

Notional in CCY1

Notional in CCY2

Notional in CCY2

Notional in CCY1

Notional CCY2 x index 2

Notional CCY1 x index 1

Premium

www.dnatrainingconsulting. net © DNA Training & Consulting

36

International borrower has substantial cash flows in both EUR and USD, so indifferent whether to issue in one currency or the other

Borrower can subsidize his funding cost by borrowing in EUR but granting to lender option to convert principal and coupons into USD at pre-determined rates and on pre-determined dates

Effectively embedding a cross-currency swaption into loan, whose premium may be paid upfront or, more typically, embedded in interest rate under loan facility

Swaption alternative: cross-currency swaption

www.dnatrainingconsulting.net © DNA Training & Consulting37

Option to enter basis swap on defined date in future and for defined term and notional amount

Example: bank pays counterparty upfront premium, in return for right to enter 5-year swap in 2 years’ time on $100 notional, under which bank pays 3m Libor and receives 6m Libor minus 25 bps, or pays 3m Libor and receives Fed Funds plus 50 bps

Swaption alternative: basis swaption

www.dnatrainingconsulting.net © DNA Training & Consulting38

Basis swaption

1) At inception

2) At swaption expiration, if swaption is exercised

3) Exchange of periodic payments

SwaptionBuyer

BankNotional x (Index2 + Spr2)

Basis Swaption

Premium

Notional x (Index1 + Spr1)

www.dnatrainingconsulting.net © DNA Training & Consulting39

Callable Bonds & Swaptions

(Part II)

Callable Bonds & Swaptions

(Part II)

www.dnatrainingconsulting.net © DNA Training & Consulting40

Outline

PART TWO

! Chapter 3: standard pricing model for swaptions

! Chapter 4: standard pricing model for callable bonds

www.dnatrainingconsulting.net © DNA Training & Consulting41

Chapter 3

! Standard pricing model for European swaptions

www.dnatrainingconsulting.net © DNA Training & Consulting42

Strike 6.00%Fwd Vol 30%Option Expiration 2Swap Tenor 5

Forward Swap 6.0000%Payer Swaption 3.8197%Receiver Swaption 3.8197%

Period FRA/Spot DFs Fixed PaymentsPV of Fixed

Payments

Floating

Payments

PV of

Floating

Payments

Principal

at Begin

1 6.00% 0.97 3.00 2.91 3.00 2.91 100

2 6.00% 0.94 3.00 2.83 3.00 2.83 100

3 6.00% 0.92 3.00 2.75 3.00 2.75 100

8 6.00% 0.79 3.00 2.37 3.00 2.37 100

9 6.00% 0.77 3.00 2.30 3.00 2.30 100

10 6.00% 0.74 3.00 2.23 3.00 2.23 100

11 6.00% 0.72 3.00 2.17 3.00 2.17 100

18 6.00% 0.59 3.00 1.76 3.00 1.76 100

19 6.00% 0.57 3.00 1.71 3.00 1.71 10020 6.00% 0.55 3.00 1.66 3.00 1.66 100

Pricing Swaption in Flat Curve Environment

www.dnatrainingconsulting.net © DNA Training & Consulting43

Strike 6.00% Forward Swap 7.0520%

Fwd Vol 30% Payer Swaption 6.4005%Option

Expiration 2 Receiver Swaption 2.4385%

Swap Tenor 5

PeriodFRA/

SpotDFs Fixed Payments

PV of Fixed

Payments

Floating

Payments

PV of

Floating

Payments

Principal

at Begin

1 5.00% 0.9756 3.0000 2.9268 2.5000 2.4390 100

2 5.25% 0.9507 3.0000 2.8520 2.6250 2.4955 100

3 5.50% 0.9252 3.0000 2.7756 2.7500 2.5443 100

8 6.75% 0.7933 3.0000 2.3798 3.3750 2.6773 100

9 7.00% 0.7665 3.0000 2.2994 3.5000 2.6826 100

10 7.25% 0.7396 3.0000 2.2189 3.6250 2.6812 100

11 7.50% 0.7129 3.0000 2.1387 3.7500 2.6734 10018 9.25% 0.5327 3.0000 1.5982 4.6250 2.4639 10019 9.50% 0.5086 3.0000 1.5257 4.7500 2.4157 10020 9.75% 0.4849 3.0000 1.4548 4.8750 2.3640 100

Pricing Swaption in Steep Curve Environment

www.dnatrainingconsulting.net © DNA Training & Consulting44

! Illustration of potential arbitrage if ATMF 2x5 payer is worth 4% while

ATMF 2x5 receiver is worth 3.75%.

Arbitrage strategy if payer/receiver parity does not apply

If swap rate in 2 years < strike

If swap rate in 2 years > strike

Bank 2Bank 1

Bank 3

Arbitrageur:Sell 2x5 payer

Upfrontpremium of 4%

Libor

fixed @ strike fixed @ strike

Libor

fixed @ strike

Buy 2x5 receiver

Upfront premium of

3.75%

Libor

2X5 forward-start swap

net profit of 25bps annuity

www.dnatrainingconsulting.net © DNA Training & Consulting45

Arbitrage strategies: payer/receiver parity

Outcome:

Receiver premium –

Payer premium

Payer premium –

Receiver premiumProfit

00Risk

Receive fixedPay fixedForward-start swap

ShortLongReceiver

LongShortPayer

Strategy:

ATMF Payer <

ATMF Receiver

ATMF Payer >

ATMF Receiver

www.dnatrainingconsulting.net © DNA Training & Consulting46

! Closed-form solution (available for pricing European swaption) not

applicable to Bermudan alternative, nor American one

! True of both constant-maturity swaption and remaining maturity

swaption

! Numerical solutions are required, typically involving binomial or

trinomial trees, similar to ones used in FX Options module

! Will illustrate binomial technique in next chapter, on callable bond

pricing

Bermudian swaption: pricing

www.dnatrainingconsulting.net © DNA Training & Consulting47

Chapter 4

! Pricing model for European and Bermudan callable bonds using binomial trees

www.dnatrainingconsulting.net © DNA Training & Consulting48

Period 0 1 2 3 Vol 10%

3.5000% 5.4289% 7.0053% 9.1986%4.4448% 5.7354% 7.5312%

4.6958% 6.1660%5.0483%

2-Year 4.2% Bond

Coupon 4.20

100.000 103.034 104.200103.966 104.200

104.200

3-Year 4.7% Bond

Coupon 4.70

100.000 102.523 102.546 104.700104.477 103.721 104.700

104.704 104.700104.700

Callable Bond Pricing (Low vol)

www.dnatrainingconsulting.net © DNA Training & Consulting49

4-Year 5.2% Bond

Coupon 5.20

100.000 101.961 100.789 101.538 105.200105.039 103.238 103.032 105.200

105.316 104.290 105.200105.344 105.200

105.200

4-Year 6.5% Bond

Coupon 6.50

104.643 106.730 104.425 104.029 106.500109.881 106.918 105.541 106.500

109.034 106.815 106.500107.882 106.500

106.500

4-Year 6.5% Bond Callable Every year at Par

Coupon 6.50Call Price 100

102.899 106.500 104.425 104.029 106.500106.500 106.500 105.541 106.500

106.500 106.500 106.500106.500 106.500

106.500

www.dnatrainingconsulting.net © DNA Training & Consulting50

4-Year 6.5% Bond Callable at 102 in Year 1, 101 in Year 2, and 100 in Year 3

Coupon 6.50Call Price EOY 1 102Call Price EOY 2 101Call Price EOY 3 100

103.942 106.660 104.425 104.029 106.500108.500 106.770 105.541 106.500

107.500 106.500 106.500106.500 106.500

106.500

4-Year Step-Up Note, Coupons 5.50% Years 1-2, 9.5% Years 3-4, Callable Every Year at Par

Coupon Yrs 1-2 5.50Coupon Yrs 3-4 9.50Call Price 100

102.453 105.567 105.500 109.500 109.500106.510 105.500 109.500 109.500

105.500 109.500 109.500109.500 109.500

109.500

www.dnatrainingconsulting.net © DNA Training & Consulting51

! Real tree would have many more time steps of substantially

shorter duration

! Precision of model increases as we increase number of time steps

Binomial tree: time steps

www.dnatrainingconsulting.net © DNA Training & Consulting52

! Investor has granted issuer option to prepay on any anniversary,

but coupon has not risen to compensate for this privilege

! So value of callable must be less than 104.643, price of non-

callable

Callable bond: pricing

www.dnatrainingconsulting.net © DNA Training & Consulting53

! Call option can be European, Bermudan or American

! Callable bond = Non-callable bond – call option

! Value of call option being positive in all case, callable bond is

worth < non-callable version, in all cases

Deconstruction of callable bond

Callablebond

Non-callablebond

Call option

–

www.dnatrainingconsulting.net © DNA Training & Consulting54

! Puttable bond = Non-puttable bond + put option

Deconstruction of puttable bond

Puttablebond

Non-puttablebond

Put option

+

www.dnatrainingconsulting.net © DNA Training & Consulting55

! Principal new feature in tree starting on Row 54, which reflects

issuer’s right to call at par, is stipulation that if price in that cell

obtained under normal formula exceeds call price plus accrued

interest – which would give issuer immediate arbitrage since he

could call the bond by paying 106.5 and then sell it for this higher

price – market would preempt this arbitrage by refusing to price

this instrument above 106.50

! Stated differently, no rational investor would agree to pay > 106.5

for this instrument on any call date, no matter what formula says,

since investor would face then immediate loss when bond is called

away at 106.5 exactly

Amending the tree

www.dnatrainingconsulting.net © DNA Training & Consulting56

! We know that

Callable Bond = Non-callable Bond – Call Option

! Also value of call option increases when vol rises

! Therefore increase in vol will reduce bond value further, pulling it

closer to 100

Amending the tree

www.dnatrainingconsulting.net © DNA Training & Consulting57

Period 0 1 2 3 Vol 20%

3.5000% 5.9194% 8.3440% 12.0003%3.9679% 5.5931% 8.0441%

3.7492% 5.3921%3.6144%

2-Year 4.2% Bond

Coupon 4.20

100.000 102.577 104.200104.423 104.200

104.200

3-Year 4.7% Bond

Coupon 4.70

100.000 101.562 101.337 104.700105.438 103.854 104.700

105.616 104.700104.700

Callable Bond Pricing (High vol)

www.dnatrainingconsulting.net © DNA Training & Consulting58

4-Year 5.2% Bond

Coupon 5.20

100.000 100.450 98.281 99.128 105.200106.550 103.495 102.568 105.200

107.248 105.018 105.200106.730 105.200

105.200

4-Year 6.5% Bond

Coupon 6.50

104.643 105.185 101.872 101.589 106.500111.427 107.180 105.071 106.500

111.000 107.551 106.500109.285 106.500

106.500

4-Year 6.5% Bond Callable Every year at Par

Coupon 6.50Call Price 100

102.108 104.864 101.872 101.589 106.500106.500 106.500 105.071 106.500

106.500 106.500 106.500106.500 106.500

106.500

www.dnatrainingconsulting.net © DNA Training & Consulting59

4-Year 6.5% Bond Callable at 102 in Year 1, 101 in Year 2, and 100 in Year 3

Coupon 6.50Call Price EOY 1 102Call Price EOY 2 101Call Price EOY 3 100

103.116 104.950 101.872 101.589 106.500108.500 106.682 105.071 106.500

107.500 106.500 106.500106.500 106.500

106.500

4-Year Step-Up Note, Coupons 5.50% Years 1-2, 9.5% Years 3-4, Callable Every Year at Par

Coupon Yrs 1-2 5.50Coupon Yrs 3-4 9.5Call Price 100

102.453 105.104 105.500 107.268 109.500106.974 105.500 109.500 109.500

105.500 109.500 109.500109.500 109.500

109.500

www.dnatrainingconsulting.net © DNA Training & Consulting60

! Remind you that this feature is common, to discourage early

redemption – or at least compensate investor if it does happen for

previous efforts – by paying her extra amount for her troubles

! Increase in call strike for first two exercise dates diminishes call

value

! So given equation

Callable Bond = Non-callable Bond – Call Option

! Anticipate increase in price of this bond versus previous version

Raising the strike

www.dnatrainingconsulting.net © DNA Training & Consulting61

! Trade-off between this bond and 6.5% bond callable at par on

each anniversary, priced at 102.899

! Earn 1% less under this version in Years 1-2, then potentially 3%

more in Years 3-4 if bond survives long enough

! Not enough to compare PV of 3%s to PV of foregone 1%s and

deduce this instrument (under this simple PV analysis) offers

better value

Comparison

www.dnatrainingconsulting.net © DNA Training & Consulting62

! Likelihood of actually receiving high coupon in Years 3-4 is

diminished by substantial probability bond will have been called by

then

! Involves probability-weighted comparison; tree enables this

comparison by solving for entire investment’s fair value, revealing

spot price of 102.453, so pointing to slight decline in value from

fixed-coupon alternative

! Quiz question will ask you to price puttable bond

Comparison

www.dnatrainingconsulting.net © DNA Training & Consulting63

Callable Bonds &Swaptions(Part III)

Callable Bonds &Swaptions(Part III)

www.dnatrainingconsulting.net © DNA Training & Consulting64

Outline

PART THREE

! Chapter 5: applications of swaptions and callable bonds

! Chapter 6: Quiz

www.dnatrainingconsulting.net © DNA Training & Consulting65

Chapter 5

! Applications of swaptions and callable bonds

! Combining swaptions and callable bonds to provide cost-efficient financing for issuers

www.dnatrainingconsulting.net © DNA Training & Consulting66

Extendible interest rate swap

! Gives owner right at specific time in future to extend swap

tenor for pre-determined period

! Example:

" Swap curve is flat at 6%

" Borrower contracted 7-year loan at L + 75 bps

" Borrower may prepay loan in two years from proceeds of

asset disposal; otherwise, loan will remain outstanding for

all 7 years

! Should borrower hedge debt with 2-year IRS, 7-year IRS, or something else?

www.dnatrainingconsulting.net © DNA Training & Consulting67

Extendible interest rate swap

! Either 2-year or 7-year IRS brings all-in-

cost to 6.75% fixed

! Could we construct 2-year IRS, extendible

at borrower’s option into 7-year IRS (to be

available if Borrower doesn’t prepay loan)

! What would be fixed rate under this instrument?

! Swap curve flat at 6%

! 7-year loan at L + 75

! May be prepaid in 2

years, otherwise

remains outstanding

for 7 years

www.dnatrainingconsulting.net © DNA Training & Consulting68

Extendible swap deconstruction

2-yr pay-fixed IRS extendible into 7-yr IRS at borrower’s option

=

Normal 2-yr pay-fixed IRS @ K%

+

2 x 5 bought payer swaption

! So borrower has fixed his cost for Years 1-2 at K%, and can extend

protection again at K% if he does not prepay loan and if K% rate is

still competitive under current market conditions

www.dnatrainingconsulting.net © DNA Training & Consulting69

Strike (K%) 6.00% Forward Swap 6.0000%

Fwd Vol 30% Payer Swaption 3.8197%

Option Expiration 2 Receiver Swaption 3.8197%

Swap Tenor 5

Spot 2-year swap 6.0000%

PV of K% swap 0.0000%

Extendible Swap 3.8197%

PeriodFRA/

SpotDFs Fixed Payments

PV of Fixed

Payments

Floating

Payments

PV of

Floating

Payments

Principal

at Begin

1 6.00% 0.971 3.000 2.913 3.000 2.913 100

2 6.00% 0.943 3.000 2.828 3.000 2.828 100

3 6.00% 0.915 3.000 2.745 3.000 2.745 100

10 6.00% 0.744 3.000 2.232 3.000 2.232 100

11 6.00% 0.722 3.000 2.167 3.000 2.167 100

12 6.00% 0.701 3.000 2.104 3.000 2.104 100

13 6.00% 0.681 3.000 2.043 3.000 2.043 100

14 6.00% 0.661 3.000 1.983 3.000 1.983 100

Extendible Swap Pricing

www.dnatrainingconsulting.net © DNA Training & Consulting70

Extendible swap valuation – achieving zero NPV

PV = 0

Off-market 2-yr pay-fixed IRS, fixed leg at

K%+

2x5 payer swaption on K%

swap

PV = – ve

2-yr pay-fixed IRS, extendible

into 7-yr IRS=

PV = + ve

Solve for fixed rate K% that achieves zero upfront NPV as per equation

below (which shows borrower perspective):

www.dnatrainingconsulting.net © DNA Training & Consulting71

Monetizing underlying option in callable bond

Swaptions can be used in connection with callable bonds to

generate cost savings for high-grade borrowers, such as FNMA and

other US agencies before credit crisis

Example:

! Assume AAA-rated FNMA can borrow for any maturity on fixed-

rate basis at swap rate flat

! Swap curve is perfectly flat at 6% and vols in swaption market

are 30% for any combination of maturity and strike

! Retail bond market investors buy callable bonds at small

coupon premium over non-callable bonds, say 50 bps,

irrespective of other specifics

www.dnatrainingconsulting.net © DNA Training & Consulting72

Monetizing underlying option in callable bond

FNMA could issue either 7-year straight debt at 6%, or 7-year debt

callable in 2 years (at par) at 6.50%

FNMA CFO has expressed strong preference for 7-year fixed-rate

funding, so is leaning away from callable instrument

However CFO recognizes that 50 bps annual coupon premium

appears modest relative to potential savings of refinancing at

potentially much lower 5-year rate in 2 years

www.dnatrainingconsulting.net © DNA Training & Consulting73

Monetizing underlying option in callable bond

Investors

At issuance:

FNMA issues 6.50% callable bond at par

FNMA sells 2x5 receiver for 88 bps annuity

FNMA BankCallable

Bond

88bps

Receiverswaption

www.dnatrainingconsulting.net © DNA Training & Consulting74

Residual risks for FNMA

Investors FNMA Bank6.50%

coupons

0.88%annuity

Scenario 1:

On second anniversary

If 5-yr IRS # 6.50%

Swaption lapses

! FNMA still pays 5.62% net

www.dnatrainingconsulting.net © DNA Training & Consulting75

Residual risks for FNMAScenario 2

OldInvestors

FNMABank

Par

FRN at

Libor

88bps

6.50%

Libor

NewInvestors

Par

Old bond

On second anniversary

If 5-yr IRS < 6.50%:

Swaption is exercised, FNMA pays 6.50% fixed and receives Libor

FNMA calls back old bonds

FNMA issues FRN at Libor

! FNMA pays 5.62% net

www.dnatrainingconsulting.net © DNA Training & Consulting76

FNMA is assured to pay fixed, directly or synthetically, for entire 7

years under either scenario

But FNMA received on Day 1 a premium whose annualized value

was 88 bps, bringing down effective all-in cost for 7 years to only

5.62% and saving it 38 bps net per annum

Conclusion

www.dnatrainingconsulting.net © DNA Training & Consulting77

Is example realistic? To what do we attribute significant value

generated for issuer?

Borrower has taken advantage of serious mis-pricing of interest

rate optionality in retail bond market that purchases FNMA paper

We demonstrated that 7-year callable bond issued by FNMA can

be decomposed into 7-year straight bond plus 2x5 receiver

swaption, priced in interbank swaption market at 88 bps per annum

Less sophisticated retail market, attracted to FNMA principally on

account of triple-A rating, considers 50 bps annually under callable

almost free money!

Monetizing underlying option in callable bond

www.dnatrainingconsulting.net © DNA Training & Consulting78

FNMA in effect is buying this option cheap in retail market, then

reselling it in market which appreciates its value fully and is

prepared to pay fair price

Savings of this size are unrealistic in US market, but still occur in

less liquid markets

Illustration is excellent example of arbitrage funding strategies

Monetizing underlying option in callable bond

www.dnatrainingconsulting.net © DNA Training & Consulting79

Infinite variety of structured investment products, relating to numerous

asset classes, from interest rates and FX to credit and commodities

Structured investment products

Consider investor who expects USD Libor to decline so asks to be shown

variety of inverse floaters:

1. You show her first simple vanilla alternative paying (10% – Libor) when curve

lies at 5%

2. Then you show her leveraged version paying 20% – (3 x L)

3. Then you improve this to 22% – (3 x L) but place a cap on her coupon at 13%

4. Next you make instrument callable on its first anniversary only, which enables

you to lift coupon to 23% – (3 x L)

5. Finally you make call Bermudan, and increase coupon to 24% – (3 x L)

www.dnatrainingconsulting.net © DNA Training & Consulting80

Process is one in which different features are added gradually to

structure, each introducing its own risks but enabling you to offer

“headline” coupon, in return for asking investor to accept additional

risks that may not trouble her

Last two steps involved inclusion of call feature to enhance yield,

initially European and then more expensive Bermudan version

Numbers in this example were not confirmed via pricing model

Structured investment products

www.dnatrainingconsulting.net © DNA Training & Consulting81

Chapter 6

! Quiz

www.dnatrainingconsulting.net © DNA Training & Consulting82

Question 1

! Using a Libor curve that lies completely flat at 6%, calculate first the rate on the fixed leg of a 7-year, semi-annual spot-starting swap.

! Then assuming the same vol input of 30% we used for swaptions throughout the module, combine a 7-year off-market rate spot-starting swap with a 2x5 receiver swaption to engineer a 7-year IRS cancelable on its second anniversary at the option of the fixed-rate payer, so that the NPV of the aggregate package is zero.

! What is the strike of this cancelable swap, accurate to two decimal places?

a) 6.83%b) 7.03%c) 7.23%d) 7.43%

www.dnatrainingconsulting.net © DNA Training & Consulting83

! Libor curve being flat at 6% means that all swap rates, whether spot-starting or forward-starting, lie at 6%

Solution to Question 1

www.dnatrainingconsulting.net © DNA Training & Consulting84

Strike (K%) 6.00% Forward Swap 6.0000%

Fwd Vol 30% Payer Swaption 3.8197%

Option Expiration 2 Receiver Swaption 3.8197%

Swap Tenor 5

Spot 2-year swap 6.0000%

PV of K% swap 0.0000%

Extendible Swap 3.8197%

PeriodFRA/

SpotDFs Fixed Payments

PV of Fixed

Payments

Floating

Payments

PV of

Floating

Payments

Principal

at Begin

1 6.00% 0.971 3.000 2.913 3.000 2.913 100

2 6.00% 0.943 3.000 2.828 3.000 2.828 100

3 6.00% 0.915 3.000 2.745 3.000 2.745 100

10 6.00% 0.744 3.000 2.232 3.000 2.232 100

11 6.00% 0.722 3.000 2.167 3.000 2.167 100

12 6.00% 0.701 3.000 2.104 3.000 2.104 100

13 6.00% 0.681 3.000 2.043 3.000 2.043 100

14 6.00% 0.661 3.000 1.983 3.000 1.983 100

Solution to Question 1

www.dnatrainingconsulting.net © DNA Training & Consulting85

Solution to Question 1

Initialposition:pay fixed under 7-yr swap

If holder exercisesswaption

+

1y 2y 3y 4y 5y 6y 7y

Receives L L L L L L L

Pays 7.23% 7.23% 7.23% 7.23% 7.23% 7.23% 7.23%

3y 4y 5y 6y 7y

Pays L L L L L

Receives 7.23% 7.23% 7.23% 7.23% 7.23%

=

1y 2y

ReceivesL L

Pays 7.23% 7.23%

www.dnatrainingconsulting.net © DNA Training & Consulting86

Solution to Question 1

Initialposition:pay fixed under 7-yr swap

Do nothingIf holder does not exercise

=

+

1y 2y 3y 4y 5y 6y 7y

Receives L L L L L L L

Pays 7.23% 7.23% 7.23% 7.23% 7.23% 7.23% 7.23%

1y 2y 3y 4y 5y 6y 7y

Receives L L L L L L L

Pays 7.23% 7.23% 7.23% 7.23% 7.23% 7.23% 7.23%

www.dnatrainingconsulting.net © DNA Training & Consulting87

! Put-call parity brings about this result

! More generally, swap with a maturity M years, extendible at one party’s option for N years at same fixed rate, is exactly equivalent in cash flows terms to swap with maturity (M+N) years (with same fixed rate as before), but cancelable inthat party’s option after M years

! Shape of the curve does not affect this outcome, which is true whether curve is flat, positive, inverted or humped

! Correct answer is (c)

Solution to Question 1

www.dnatrainingconsulting.net © DNA Training & Consulting88

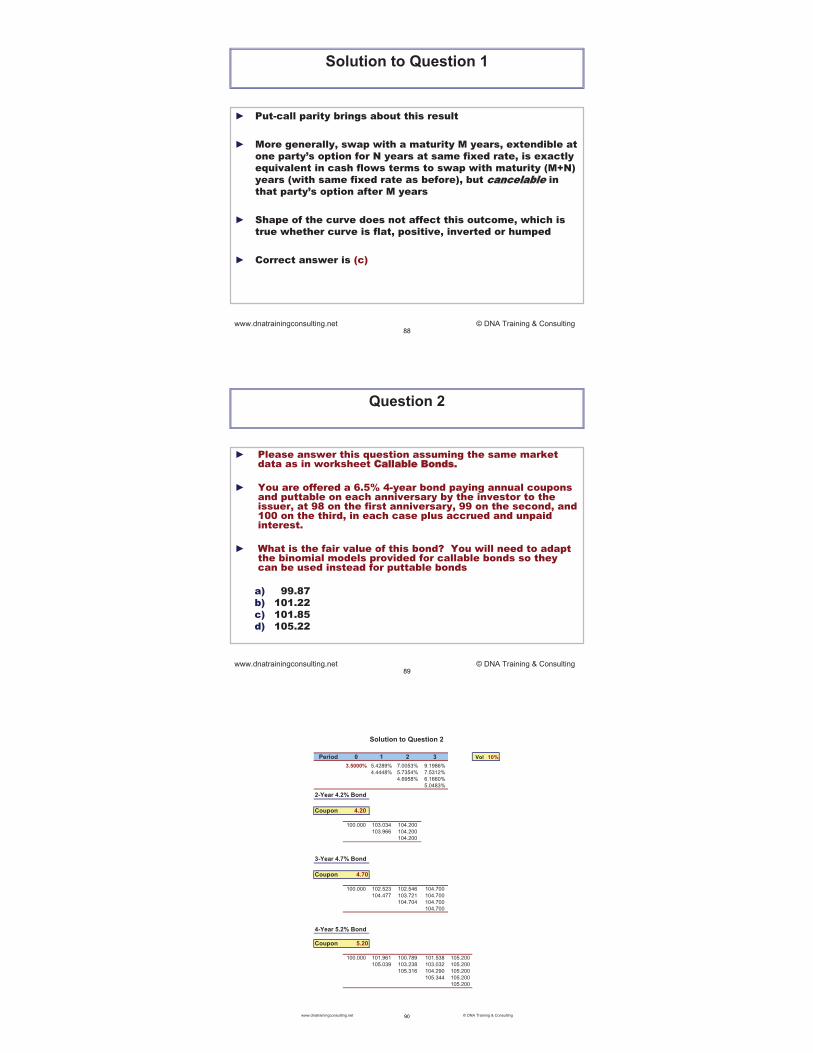

Question 2

! Please answer this question assuming the same market data as in worksheet Callable Bonds.

! You are offered a 6.5% 4-year bond paying annual coupons and puttable on each anniversary by the investor to the issuer, at 98 on the first anniversary, 99 on the second, and 100 on the third, in each case plus accrued and unpaid interest.

! What is the fair value of this bond? You will need to adapt the binomial models provided for callable bonds so they can be used instead for puttable bonds

a) 99.87b) 101.22c) 101.85d) 105.22

www.dnatrainingconsulting.net © DNA Training & Consulting89

Period 0 1 2 3 Vol 10%

3.5000% 5.4289% 7.0053% 9.1986%4.4448% 5.7354% 7.5312%

4.6958% 6.1660%5.0483%

2-Year 4.2% Bond

Coupon 4.20

100.000 103.034 104.200103.966 104.200

104.200

3-Year 4.7% Bond

Coupon 4.70

100.000 102.523 102.546 104.700104.477 103.721 104.700

104.704 104.700104.700

4-Year 5.2% Bond

Coupon 5.20

100.000 101.961 100.789 101.538 105.200105.039 103.238 103.032 105.200

105.316 104.290 105.200105.344 105.200

105.200

Solution to Question 2

www.dnatrainingconsulting.net © DNA Training & Consulting90

4-Year 6.5% Bond Puttable at 98 in Year 1, 99 in Year 2, and 100 in Year 3

Coupon 6.50Put Price EOY 1 98Put Price EOY 2 99Put Price EOY 3 100

105.219 107.706 106.028 106.500 106.500110.098 107.372 106.500 106.500

109.034 106.815 106.500107.882 106.500

106.500

www.dnatrainingconsulting.net © DNA Training & Consulting91

Question 3

! The 5-year swap rate is 5% while the 10-year swap rate is 5.50%. A borrower with floating rate debt enters into a 5-year swap with HSBC, but which can be extended, in HSBC’s sole discretion, for 5 additional years at the same fixed rate as for the first 5 years.

! Which of the following is true? You may not use any spreadsheets to answer this question

a) The rate the borrower will pay on the fixed leg of the swap will be below 5%

b) The rate the borrower will pay on the fixed leg of the swap will be below 5.50% but not necessarily below 5%

c) The rate the borrower will pay on the fixed leg of the swap will be below 5.50% but above 5%

d) The rate the borrower will pay on the fixed leg of the swap will be above 5.50%

www.dnatrainingconsulting.net © DNA Training & Consulting92

! Problem leaves significant majority of people confused

! Many are inclined to assume that positive shape of yield curve pushes fixed leg of extendible swap above 5% level of spot-starting 5-year swap

! Simple observation dispels this illusion: extendible is sum of spot-start swap plus (or minus) swaption

! Here borrower has entered spot-starting 5-year swap at K%, but has also sold to bank 5x5 European receiver swaption, with strike K% as well

Solution to Question 3

www.dnatrainingconsulting.net © DNA Training & Consulting93

Solution to Question 3

PV = 0

Off-market 5-yr receive-fixed IRS,

fixed leg at K%+

5x5 receiver swaption on K%

swap

PV = – ve

5-yr receive-fixed IRS, extendible at bank’s option into

10-yr IRS

=

PV = + ve

!Fixed rate K% must achieve zero upfront PV as per equation below (which shows bank’s perspective)

!Thus the correct answer is (a)

www.dnatrainingconsulting.net © DNA Training & Consulting94

Question 4

! Using a Libor curve that is completely flat at 5% and a 30% vol for all interest rates, determine the rate on the fixed leg of a 5-year, semi-annual, interest rate swap for a borrower who wishes to pay fixed, and is eager to earn a subsidy by granting to the bank the right to double the swap’s notional amount on its first anniversary for its remaining life:

a) 4.58%

b) 4.66%

c) 4.88%

d) 4.98%

www.dnatrainingconsulting.net © DNA Training & Consulting95

! Structure – referred to sometimes as expandableswap – was not discussed in module

! Can intuit that bank’s right to double notional is long position in 1x4 swaption struck at same fixed rate as original swap

! If bank exercises option, swap notional for remaining life doubles, since swap underlying swaption and original swap have identical terms from that point until maturity

Solution to Question 4

www.dnatrainingconsulting.net © DNA Training & Consulting96

Solution to Question 4

PV = 0

Off-market 5-yr $100 receive-fixed IRS,

fixed leg at K%+

1x4 $100 receiver swaption on K%

swap

PV = – ve

5-yr $100 receive-fixed IRS,

expandable to $200 at bank’s option on first anniversary

=

PV = + ve

! Solve for fixed rate K% that achieves zero upfront NPV as per equation below (which shows bank perspective)

www.dnatrainingconsulting.net © DNA Training & Consulting97

Strike (K%) 5.00% Forward Swap 5.0000%

Fwd Vol 30% Payer Swaption 2.0343%

Option Expiration 1 Receiver Swaption 2.0343%

Swap Tenor 4

Spot 2-year swap 5.0000%

PV of K% swap 0.0000%

Extendible Swap -2.0343%

PeriodFRA/

SpotDFs Fixed Payments

PV of Fixed

Payments

Floating

Payments

PV of

Floating

Payments

Principal

at Begin

1 5.00% 0.976 2.500 2.439 2.500 2.439 100

2 5.00% 0.952 2.500 2.380 2.500 2.380 100

3 5.00% 0.929 2.500 2.321 2.500 2.321 100

10 5.00% 0.781 2.500 1.953 2.500 1.953 100

11 5.00% 0.762 2.500 1.905 2.500 1.905 100

12 5.00% 0.744 2.500 1.859 2.500 1.859 100

13 5.00% 0.725 2.500 1.814 2.500 1.814 100

14 5.00% 0.708 2.500 1.769 2.500 1.769 100

Solution to Question 4

www.dnatrainingconsulting.net © DNA Training & Consulting98

! Correct answer is (b)

! Expandable version of IRS appeals to borrowers who have no strong view on what maximum percentage of floating-rate debt should be swapped into fixed

! Consider for example borrower with $1BN of debt in aggregate, all of it currently floating, determined to swap at least $300MM but prepared to reach $600MM if right incentive is available

Solution to Question 4

www.dnatrainingconsulting.net © DNA Training & Consulting99

! Borrower could find very appealing immediate 34 bps of savings under first $300MM swap he initiates

! Downside is only that if rates have declined by first anniversary, notional of this swap doubles, but only at same fixed rate as original one

! Of course by that time 4.66% may not be that attractive relative to market rates for 4-year swaps

Solution to Question 4

www.dnatrainingconsulting.net © DNA Training & Consulting100

Question 5

! Assume a completely flat Libor curve at 4% (s.a.), and an annualized volatility for interest rates of 40%

! Assume also, as we did in Chapter 5, that FNMA is rated triple-A and can issue non-callable debt for any maturity at the swap rate flat or Libor flat

! Assume finally that FNMA debt containing a European call option of any tenor requires a 30 bps coupon premium for successful placement

www.dnatrainingconsulting.net © DNA Training & Consulting101

Question 5 (continued)

! How much would the issuer save, in basis points annually, if it issued a 5-year bond, paying coupons semi-annually and callable on its first anniversary, and immediately sold an appropriate swaption to lock in guaranteed 5-year fixed-rate funding under any interest rate scenario?

! You are encouraged to use the same approach we used in Chapter 5 to answer this question.

a) 12b) 23c) 32d) 41

www.dnatrainingconsulting.net © DNA Training & Consulting102

Strike 4.30% Forward Swap 4.0000%

Fwd Vol 40% Payer Swaption 1.8251%Option

Expiration 1 Receiver Swaption 2.8813%

Swap Tenor 4 Annualized 0.6415%receiver premium

Period FRA/Spot DFs Fixed Payments

PV of

Fixed

Payments

Floating

Payments

PV of

Floating

Payments

Principal

at Begin

1 4.00% 0.980 2.150 2.108 2.000 1.961 100

2 4.00% 0.961 2.150 2.067 2.000 1.922 100

3 4.00% 0.942 2.150 2.026 2.000 1.885 100

10 4.00% 0.820 2.150 1.764 2.000 1.641 100

11 4.00% 0.804 2.150 1.729 2.000 1.609 100

12 4.00% 0.788 2.150 1.695 2.000 1.577 100

13 4.00% 0.773 2.150 1.662 2.000 1.546 100

14 4.00% 0.758 2.150 1.629 2.000 1.516 10015 4.00% 0.743 2.150 1.597 2.000 1.486 100

16 4.00% 0.728 2.150 1.566 2.000 1.457 10017 4.00% 0.714 2.150 1.535 2.000 1.428 10018 4.00% 0.700 2.150 1.505 2.000 1.400 10019 4.00% 0.686 2.150 1.476 2.000 1.373 10020 4.00% 0.673 2.150 1.447 2.000 1.346 100

Solution to Question 5

www.dnatrainingconsulting.net © DNA Training & Consulting103

Solution to Question 5

Investors FNMA Bank4.30%

coupons

64bps

! If 4-yr IRS ! 4.30% on first anniversary

! Swaption lapses

! FNMA still pays 3.66% net

www.dnatrainingconsulting.net © DNA Training & Consulting104

Solution to Question 5

Old

Investors

FNMA BankPar

FRN at

Libor

64bps

4.30%

Libor

New

Investors

Par

Old bond

! If 4-yr IRS < 4.30% on first anniversary

! Swaption is exercised, FNMA pays 4.30% fixed and receives Libor

! FNMA calls back old bonds

! FNMA issues FRN at Libor

! FNMA pays 3.66% net

! So correct answer is (c)

www.dnatrainingconsulting.net © DNA Training & Consulting105

Question 6

! Turkey can borrow at 5% for 5 years in either Euros or US dollars. Spot and forward FX rates for EUR/USD are 1.50 for all maturities.

! Since the country has significant remittances in both of these currencies from a combination of exports (mostly in US dollars) and worker remittances (mostly in Euros), Deutsche Bank proposes to Turkey that it borrow EUR 100 MM for 5 years at 3%, provided that on the loan’s first anniversary Deutsche can, in its sole discretion, convert half the loan into a 4-year USD 75MM loan at 3%, and on the second anniversary Deutsche can, in its sole discretion, convert the second half of the loan into a 3-year USD 75MM loan at 3%.

www.dnatrainingconsulting.net © DNA Training & Consulting106

Question 6 (continued)

! How might you deconstruct the loan described above:

a) Turkey has borrowed EUR 100MM at market rates and has also bought one or more European cross-currency swaptions

b) Turkey has borrowed EUR 100MM at market rates and has also bought one or more Bermudan cross-currency swaptions

c) Turkey has borrowed EUR 100MM at market rates and has also sold one or more European cross-currency swaptions

d) Turkey has borrowed EUR 100MM at market rates and has also sold one or more Bermudan cross-currency swaptions

www.dnatrainingconsulting.net © DNA Training & Consulting107

! To achieve 2% subsidy over normal 5-year rates Turkey must have sold optionality to Deutsche, not bought it

! And since each right to convert portion of loan into USD can be exercised on one specific date only,these are European options, not Bermudan

Solution to Question 6

www.dnatrainingconsulting.net © DNA Training & Consulting108

! In addition to borrowing EUR 100MM for 5 years, Turkey has sold to Deutsche

i. 1x4 cross-currency swaption enabling Deutsche on loan’s first anniversary to initiate cross-currency swap with Deutsche under which Deutsche will deliver EUR and receive USD, with notionals of EUR 50 and USD 75MM, and

ii. 2x3 cross-currency swaption enabling Deutsche on loan’s second anniversary to initiate a cross-currency swap with Deutsche under which Deutsche will deliver EUR and receive USD, with notionals of EUR 50 and USD 75MM

Solution to Question 6

www.dnatrainingconsulting.net © DNA Training & Consulting109

! Premium earned from selling these two cross-currency swaptions is built into loan and reduces interest rate to 3% in either currency

! Therefore correct answer is (c)

Solution to Question 6

www.dnatrainingconsulting.net © DNA Training & Consulting110