cambrian group - pomonaeconomics-files.pomona.edu/jlikens/seniorseminars/cambrian/final... · to...

TRANSCRIPT

CAMBRIAN GROUP

strategic report

CAMBRIAN GROUP

General Motors

CAMBRIAN GROUP

TEAM MEMBERS

Cailee Moberg, Lead

Zachary Mattler

Richard Creedon

CAMBRIAN GROUP

COPYRIGHT NOTICE © 2011 Cambrian Consulting, LLC. All rights reserved. This material may not be reproduced, displayed, modified or distributed without the express prior written permission of the copyright holder and the Client.

CONSULTANT�’S DISCLAIMER Cambrian Consulting, LLC (�“Cambrian�”) has prepared this report (�“report�”) at the request of the Client and for the sole use of the Client. This report may not be relied upon by any other party without the express written agreement of Cambrian. The use of this report by unauthorized third parties without written authorization from Cambrian shall be at their own risk, and Cambrian accepts no duty of care to any such third party.

Cambrian has exercised due and customary care in conducting this report but has not, except as specifically stated, independently verified information provided by others, including the Client. Cambrian makes no representations or warranty as to the accuracy, completeness or correctness of the information and statistical data contained herein.

No other warranty, express or implied is made in relation to the conduct of this report of the contents of this report. Therefore, Cambrian assumes no

liability for any loss resulting from errors, omissions, or misrepresentations made by others.

Any recommendations, opinions, or findings reflect the judgment of Cambrian at the date of publication and are subject to change at any time without notice. Any recommendations, opinions, or findings stated in this report are based on circumstances and facts as they existed at the time Cambrian performed the work. Any changes in such circumstances and facts upon which this report is based may adversely affect any recommendations, opinions, or findings contained in this report.

CAMBRIAN GROUP

TABLE OF CONTENTS EXECUTIVE SUMMARY�…�…�…�…�…�…�…�…�…...............................�…�….�…�…�…�…�…�…�…�…..�….1

PART I: INTRODUCTION COMPANY OVERVIEW�…�…�…�…�…�…�…�….�…�…�….�…�…�…�…�…�…�…�…�…�….�…�…�…�…�…..�…..�…..4 Company Overview and History�….........�….�…�…�….�…�…�…�…�…�…�…�…�…�…�…�….�…�…4

Business Model.....�…�…�…�…�…�…�…�…�…�….�…�…�…�….�…�…�…�…�…�…�…�…�…�…�…�…�…...8

PART II: ANALYSIS COMPETITIVE ANALYSIS�…�…�…�…�…�….�…�…�…�…�…�…�…�….�…�…�…�….�…�…�…�…�…�…�…�…�…�…11

Internal Rivalry......�…..�…�…�…�…�…�…�…�…�…�…�…�…�…�…�…�…�…�…�…�…�…�…�…�…�…...11

Supplier Power�…�…�…..�…..�…�…�…�…�…�…�…�….�…�…�…�…�…�…�…�…�…�…�…�…�…�…�…...12

Buyer Power..................�…..�…�…�…�…�…�…�…�….�…�…�…�…�…�…�…�…�…�…�…�…�…�…�…..14

Entry & Exit..........�…�…�…�…�….�…�…�…�…�…�….�….�…�…�…�…�…�…�…�…�…�…�…�…�…�…...15

Substitutes & Complements�…�…�…...�…�…�…�…�….�…�…�…�…�…�…�…�…�…�…�…�…�…�….16

FINANCIAL ANALYSIS....�…�…�…�…�…�…�…..�…�…�…�…�…�…�…�…�…�…�…�…�…�…�…�…�…�…�…�…..�….17 Overview & Stock Performance.....�…..�…�…�…�…�…�…�…�…�…�…�…�…�…�…�…�…�…..�…..17

Profitability............�…..�…�…�…�…�…�…�…�…�…�…�…�…�…�…�…�…�…�…�…�…�…�…�…�…..�…..19

Industry Comparable Analysis..�…�…�…�…�…�…�…�…�…�…�…�…�…�…�…�…�…�…�…�…�…�…20

Financial Health & Liquidity......�…..�…�…�…�…�…�…�…�…�…�…�…�…�…�…�…�…�…�…�…�…21

Regional Analysis..�…..�…�…�…�…�…�…�…�…�…�…�…�…�…�…�…�…�…�…�…�…�…�…�…�…�…�…22

SWOT ANALYSIS�…�…�…�…�…�…........�…�…�…�…�…�…�…�…�…�…�…�…�…�…�…�…�…�…�…�…�…�…�…�…..24 Strengths�…�…�…�…�…�…�…�…�…�…�…..�…�…�….�…�…�…�…�…�…�…�…�…�…�…�…�…�…�…�…...24

Weaknesses�…�…�…�…�…�…�…�…�…�…�…�…�….�…�…�…�…�…�…�…�…�…�…�….......................26

Opportunities�…�…�…..�…�…�…�…�…�…�…�…�….�…�…�…�….�…�…�…�…�…�…�…�…�…�…�…......26

Threats�…�…�…�…�…�…�…�…�…�…�…�…�…�…�….�…�…�…�…�…�…�…�…�…�…�….......................27

PART III: RECOMMENDATIONS STRATEGIC RECOMMENDATIONS�…�…�…�…�…�…�…�…�…�…�…�….�…�…�…�…�…�…�…�…�…�…�…�….10

Global Positioning..................�…�…�…�…�…�…..�…�…�…�…�…�…�…�…�…�…�…�…�…�…�…�….30

Fleet Sales�…�…�…..�…�…�…�…�…�…�…�…�…�….�…�…�…�…�…�…�…�…�…�…�….......................35

CAMBRIAN GROUP

U.S. Pricing�…�…�…�…�…�…�…�…�…�…�…�…�….�…�…�…�…�…�…�…�…�…�…�….......................36

Product Development & Production�….�…�…�…....�…�…�…�…�…�…�…�….......................37

GM Financial....................................�…�…�…....�…�…�…�…�…�…�…�…�…�…�…�…�…�…�…...38

Brand Positioning.............................�…�…�…�….�…�…�…�…�…�…�…�…�…�…�…�…�…..�…....38

Product Positioning..........................�…�…�…�….�…�…�…�…�…�…�…�…�…�…�…�…�….....�….31

APPENDICES.�…�…�…�…�…�…�…�…�…�…�…�…�…..............................�…�…�…�…�…�…�…�….�…�…�…...43

CITATIONS...�…�…�…�…�…�…�…�…�…�…�…�…�…..............................�…�…�…�…�…�…�…�…�….�…�…�….47

CAMBRIAN GROUP

EXECUTIVE SUMMARY Over the last century General Motors (GM) has become the largest automobile manufacturer in the United States and second largest worldwide through constant evolution of geographic, product, brand, pricing, vertical integration, and technology strategy. Currently GM develops, manufactures, and markets automobiles under the Buick, Cadillac, Chevrolet, GMC, and other international brands; manufactures and sells auto parts; and provides auto financing and leasing options.

Rising fuel prices at the start of the 21st century followed by the economic recession has led to a rough decade in the auto industry. GM faced increasing financial difficulty during this period as a result of slowing vehicle sales, excess production capacity, and labor union liabilities culminating in bankruptcy in 2009. A new GM has emerged from bankruptcy free of prior bad assets and focused on core businesses and key brands, increasing its profitability.

In addition to constantly shifting consumer demand and pressure from labor unions, GM continues to face fierce competition on price, technology, fuel efficiency, and product quality. The company is aided by its established presence in emerging markets and strong brand recognition.

To maximize growth and profitability in the short term and position for optimal performance in the long term, we recommend that General Motors implement the following strategies:

�• Increase focus on Asian and South American markets �• Refresh European product portfolio and cut production capacity �• Improve fleet sales vehicle quality �• Reduce U.S. price discounts �• Standardize and consolidate production and product development

through a company-wide modular system �• Offer short term loans to suppliers through GM Financial

CAMBRIAN GROUP

�• Pursue a cohesively exhaustive and mutually exclusive brand positioning strategy

�• Focus on smart technology integration and fuel efficiency in product development

To achieve the first objective of growth in Asia GM should pursue the following regional strategies. The company should increase small affordable vehicle offerings in Chinese and Indian cities, increase availability of trucks and vans to more rural customers in China and India, bring the South American mini trucks and mini vans line to Asian markets, sell auto parts to Chinese auto manufacturers, and consider forming a JV with an Indian auto company. In South Korea, the company should increase competitiveness of GM Korea by bringing the Cadillac brand to compete in the luxury market with Hyundai. GM should continue to enter new emerging markets as demand grows enough to make entry profitable, such as the current example of Thailand, and utilize strength in nearby markets to do so.

CAMBRIAN GROUP

PART I INTRODUCTION

CAMBRIAN GROUP

COMPANY OVERVIEW Overview and History

General Motors (GM) is the largest auto manufacturer in the United States, with 18.8% market share, and the second largest worldwide, with a market share of 11.4%. Current brands marketed in North America include: Buick, Cadillac, Chevrolet, and GMC. Outside the US, GM additionally manufactures and markets automobiles under the brands: Daewoo, Holden, Isuzu, Jiefang, Opel, Vauxhall, Wuling, and FAW. The company produces automobiles in over 31 different countries and sells vehicles in over 120. The U.S., Europe, Asia and Latin America are the largest marketsi. The General Motors Company of today was formed through a long history of repositioning through acquisition, international expansion, technological innovation, changing industry trends, brand development, and corporate restructuring.

General Motors was first founded as a holding company for the Buick Motor Company in 1908. By 1910, GM had acquired Oldsmobile, Cadillac, the Rapid Motor Vehicle Company (GMC) and half of Oakland Motor Car Co. (Pontiac). In1912, Cadillac released the first electric self-starter. Over the next twenty years General Motors grew in size, geographic scope, and technological innovation due to soaring demand for automobiles, financing options created by General Motors Acceptance Corp. (GMAC), and the leadership of President Alfred Sloan who introduced the company�’s new philosophy of �“a car for every purse and purpose�”. By 1930, GM had produced the first sixteen cylinder engine, acquired Chevrolet Motor Co., U.K. Vauxhall Motors Ltd., a majority stake in Fisher Body Co., Adam Opel AG in Germany, Holden�’s Ltd in Australia, and set up operations in Canada, Denmark, Argentina, France, Brazil, India, and China. It was the world�’s largest automaker.

Due to worker strikes in 1937 GM recognized the United Auto Worker union, beginning a long tumultuous relationship. At the start of World War II, GM converted 100% of production to the war effortii. Afterwards, the company reentered civilian auto production stronger than ever, releasing

CAMBRIAN GROUP

the industry�’s first V8 engines and air conditioning, rising to 54% domestic market shareiii.Continuing GM�’s commitment to the reputation of offering options for customers of all income levels, Chevy made a name for itself by releasing the first low priced car with automatic transmission in 19502.

Although GM continued to lead the auto industry in revenue, the 1960�’s and 1970�’s were marked by many unsuccessful product launches and image changes for all of GM�’s brands. Driven by European competition, rising fuel prices, and environmental concerns, the 1960�’s began the trend of smaller more fuel efficient vehicles. However, GM�’s Chevrolet and Pontiac models were less popular than their Ford competitors. Many of the new models released during this period were plagued by product defects. Although GM corrected problems as soon as possible, it wasn�’t in time to save the reputation of the models or their brands; their market share suffered. GM also began releasing higher performance Chevrolets and Pontiacs, blurring the lines between their low end brands and high end brands such as Buick and Oldsmobileiv.

The late 1970�’s and early 1980�’s brought the Arab oil embargo and economic recession, which led to sales decline across the auto industry. GM�’s sales were composed of a greater share of large vehicles and faced less flexible labor costs than encroaching Japanese competitors, resulting in market share decline. Roger Smith became CEO in 1980 and made significant changes throughout the next decade in response to recent problems. Under Smith�’s leadership the company invested in automated manufacturing, downsized the product line and consolidated operations between different brands3. GM received criticism for this consolidation and their reputation suffered from controversies regarding the interchange of parts between brands4. Despite this criticism, profits rose throughout the late eighties, reaching $4.6 billion in 1988.

GM continued to expand through acquisitions and joint ventures. Recognizing the globalization trend early on, much of their expansion was international. Throughout the 1980�’s GM formed a joint venture with Toyota aimed at learning manufacturing best practices and enhancing innovation, acquired 34% of Isuzu Motors, and purchased Saab Automobile AB of Sweden. In 1990, the company released its first electric car, the

CAMBRIAN GROUP

Impact, and began mass producing vehicles under the new brand Saturn to compete in the small cars market with growing Japanese competitors.

GM again suffered declining sales during the recession in the early 1990�’s, losing an industry record $4.45 billion in 1991. Increased demand and success of their SUV and light truck sales in the second half of the twentieth century helped restore sales and increased market share. During this time GM began splitting off the peripheral businesses, decreasing vertical integration, while continuing to expand within the automobile industry. Electronic Data Systems and Delphi Automotive Systems were spun off as separate companies3. GM acquired the rights to the HUMMER brand and released the OnStar safety and security system for Cadillac. One of the most important moves was starting a joint venture with Shanghai Automotive Industry Corporation. This allowed them to enter China, the market that would come to compose the company�’s highest percentage of sales a decade later2.

After the September 11, 2001 attacks, GM released its �“Keep America Rolling�” campaign which boosted SUV and truck sales. The company proceeded to focus production and resources on SUVs and trucks during the following several years. This decision exacerbated their growing problems in the late twenty first century, as increasing gas prices caused a major decline in truck and SUV sales. In order to mitigate problems from overinvestment in truck and SUV production GM announced the closing of four major truck and SUV factories. Additional repositioning during this time included the sale of their defense unit, halting the production of Oldsmobiles, and entering the auto repair business through opening the Goodwrench Autobody Center Program.

GM made progress towards improved fuel efficiency and international expansion during this period. In 2000 they opened the new assembly plant in Brazil, began production at Opel�’s new facility in Germany, and acquired a majority stake in bankrupt South Korean Daewoo Auto & Technology. Major advancements were made in the development of automobile fuel cell technology and the use of alternative fuels such as bioethanol. GM also began offering hybrid options for its most popular models including trucks and SUVs3.

CAMBRIAN GROUP

Despite international and technological expansion, falling large vehicle sales were not GM�’s only problems. They reported increasing losses between 2005 and 2008 as the stock market crash of 2007 brought into question their ability to cover their pension fund liabilities. Additionally, the worldwide recession and resulting tightening of credit, declining household income, and increasing unemployment caused industry wide demand reduction for automobiles. GM was especially hard hit due to their high percentage of U.S. sales and growing speculation of impending bankruptcy.

In an effort to generate much needed cash flow in 2006, GM sold 51% of GMAC to a consortium of investors led by Cerberus Capital Management, the private equity company that in 2007 acquired Chrysler Corporation. Despite contracts between GM and Cerberus ensuring GMAC�’s continued GM vehicle financing in the near term, GM�’s lack of a controlling stake in a financing company put them at risk for being subject to the limited offering of bank financing. This vulnerability caused GM sales to be hurt more than competitors by the contraction of credit that accompanied the recession starting in 2007, during which the number of people with subprime credit grew and GM�’s ability to serve them decreased 4.

After years of surmounting problems, GM filed for Chapter 11 bankruptcy in June 2009. The company was pulled off the NYSE and began a government-endorsed reorganization plan. A new entity, NGMCO Inc., which later changed its name to General Motors Company, was created to purchase the desirable operations and trademarks from GM. This new company was comprised of a 60.8% stake by the United States Government, 11.7% stake by the Canadian Government, 17.5% by the United Auto Workersv. The remaining undesirable assets were left with General Motors Corporation which changed its name to Motors Liquidation Company, existing solely for the purpose of liquidating remaining assets.

The new General Motors Company made the decision to halt the production of Hummer, Saturn, and Pontiac brands and sell Saab. These brands are no longer a part of GM. The company retained overseas operations under Daewoo, Holden, Isuzu, Jiefang, Opel, Vauxhall, Wuling, and FAW but narrowed domestic brand focus to Cadillac, Buick, Chevrolet, and GMC. General Motors Company also implemented a new branding

CAMBRIAN GROUP

strategy that places emphasis on individual brands under a shared invisible corporate structure rather than the old model in which GM was at the heart of each of their brandsvi. Further restructuring included increased vertical integration through the purchase of a stake in the new Delphi Corporation, GM�’s main auto parts supplier, also recently emerged from bankruptcy.

In October 2010, GM acquired AmeriCredit Corp. for $3.5 billion, once again providing it with a captive finance unit for the first time since the sale of GMAC in 2006, and increasing competitiveness in auto financing and leasing options. Before the acquisition, GM had a lower percentage of subprime customers than its major competitors and AmeriCredit had a history of lending to subprime auto customers. GM and AmeriCredit had already been running a non-prime credit program together since September 2009 which eased the transition since AmeriCredit had previously done business with many GM dealersvii. The name was changed to General Motors Financial Company. Through GM Financial the company is now able to provide increased automotive financing to potential customers who get turned away from more traditional financing institutions.

General Motors Company held an IPO in November 2010 on the NYSE. The company sold 478 million common shares at $33 each and $4.35 million in preferred shares raising a total of $20.1 billion and diluting the U.S. and Canadian governments�’ stakesviii.

Business Model

GM develops produces, and markets cars, trucks, and parts under several different brands. Production and assembly facilities in the U.S. and many others around the world are owned and operated solely by GM. Additionally, GM operates through several international joint ventures including: GM DaeWoo in South Korea, Shanghai General Motors Co., SCIAC-GM-Wuling Automobile, and FAW-GM Light Duty Commercial Vehicle Co. in P.R. China.

In North America the cars and trucks are distributed and marketed through franchised and independent retail dealers. Outside of North America they are mainly sold through distributors and dealers, many of which are

CAMBRIAN GROUP

independent. In addition to consumer sales through retail dealers, GM also sells to fleet customers including: business fleets, rental and leasing companies, and the government. These are marketed through third party dealers or direct contract sales.

GM also offers financing services for automotive purchases through GM Financial. The subsidiary purchases finance contracts for new and used vehicles from franchised and independent dealerships. Most of these contracts are for consumers who are unable to obtain outside financing due to credit historyix.

CAMBRIAN GROUP

PART II ANALYSIS

CAMBRIAN GROUP

COMPETITIVE ANALYSIS Force Strategic Significance

Internal Rivalry High Supplier Power Medium Buyer Power Low to Medium Entry and Exit Low to Medium Substitutes and Complements Medium

Internal Rivalry

General Motors competes in the automotive industry, with the vast majority of its revenues coming from the production and sale of passenger cars and trucks. The company is divided into four segments: GM North America, GM Europe, GM International Operations, and GM South America. The four segments, operating in such different markets, face unique challenges and serve very different customer bases, but they all have one thing in common. Each segment faces the fierce internal rivalry that is characteristic of the automotive industry. Other major players include Toyota, Volkswagen, Ford, Honda, Chrysler, Nissan, and Hyundai/Kia, which each compete in all of GM�’s major markets.

Given the costs structure of automobile production, firms benefit hugely from economies of scale, resulting in an industry dominated by a small number of large firms. In the United States, for example, seven automakers provided over 85% of the market share in 2010, with GM leading at 18.8%9. Given this high level of consolidation, firms face great pressure to generate return customers, sell to new customers, and to take customers from away from other firms. The two main methods of appealing to customers are price competitiveness and product differentiation. To stay competitive in the fierce internal rivalry of the automobile industry, a firm must constantly balance the benefits of economies of scale from standardizing production practices and consolidating product offerings across different markets,

CAMBRIAN GROUP

thereby being able to offer lower prices, with customizing vehicles to adapt to the preferences of different markets and different customer segments within each market.

Different consumers have different deal-breakers that determine which car they will purchase. Some of the most important considerations include: price, quality, availability, style, safety, reliability, fuel economy and functionality. As a result, consumers create demand for a wide variety of vehicles. Not wanting to cede certain customer groups to competitors, automotive firms must provide widely differentiated products. Increasing the number of models of cars and trucks adds tremendously to the R&D costs of automakers, driving down profitability.

Similarly, because cars represent a very large purchase for most consumers, price becomes a very important consideration. With a small number of firms, usually offering one or two competing products designed to fit a specific niche, automakers are also forced to compete on price. As a result, firms resort to numerous promotional offers, discounts, and other deals, which impose further costs, while at the same time eroding profit margins.

Finally, because there are so few major players in each market, image, branding, and advertising become extremely important. After developing the diverse product line, and providing a competitive price, firms still have to show consumers their products, and convince them that they are better than the competition�’s. As a result, automakers incur further costs advertising their latest models, current promotions, and developing the image and brand name they hope will maintain sales for years to come.

Supplier Power

General Motors has historically been a vertically integrated firm. However, the sale of subsidiaries to generate emergency cash flow during the years leading up to bankruptcy and the sale of non-core businesses as part of the restructuring has left GM less vertically integrated with respect to automobile parts than ever before. Additionally, GM and their parts suppliers depend on a large number of suppliers throughout the world for raw materials, energy, freight and transportation. Of these supplies, raw materials pose the greatest risk. General Motors depends greatly on

CAMBRIAN GROUP

supplies of steel, aluminum, resins, copper, lead, and platinum group metals, of which they do not hold substantial inventory. The supplier risk is lessened because GM does not rely heavily on any single supplier of any one input. In fact, for many parts and raw materials suppliers, GM represents a large percentage of business. Therefore, suppliers have relatively little power over GM, and in many cases, GM has strong bargaining power over suppliers.

However, GM is subject to some of the risk that these suppliers face themselves. If an economic, political, or environmental condition prevents a supplies industry or several key suppliers from providing GM with raw materials or parts, a significant delay in the production of automobiles could result and GM would be forced to scramble to get new parts for continuing production schedules, representing higher costs. We have seen an example of this with the disruption of deliveries from Japanese parts manufacturers. Supplier delay is particularly problematic in the automotive industry, given the cyclical nature of new car purchases that depends greatly on the time of the year, gas prices, etc. If a delay occurred shortly before an upswing in demand, GM would face the possibility of missing the opportunity entirely.

The largest supplier power GM faces is from unionized labor in its North American operations. GM employs 202,000 workers around the world. This is a reduction from the 215,000 in 2009 and 242,000 in 2008. Of the current workforce, 135,000 (67%) are hourly employees and 67,000 (33%) are salaried. Supplier power of the International Union, United Automobile, Aerospace and Agriculture Implement Workers of America (UAW) and Canadian Auto Workers Union (CAW) have forced concessions from GM throughout its history. GM�’s inability to cover its pension liabilities after the stock market crash was a critical factor leading to bankruptcy. Through bankruptcy, GM was able to shed some of its labor liabilities. At the end of 2010, 49,000 of GM�’s U.S. employees (64%) were represented by unions. 48,000 were represented by the UAW. Many employees outside the U.S. are also represented by various other unions. Additionally, GM is liable for pension plans of 400,000 U.S. hourly and 120,000 U.S. salaried retirees, surviving spouses and deferred vested participants9.

CAMBRIAN GROUP

The UAW�’s power over GM and political weight were demonstrated in the outcome of negotiations during bankruptcy. The GM, UAW, and government trilateral agreement did not fund salaried non-union workers�’ pensions but maintained pension plans for UAW workersx. Many analysts argue that the union also received preferential treatment over other investors during the bankruptcy. A UAW trust fund established to cover health care for retired union workers received 17.5% of the �“new GM�” stock while bond holders were offered a deal of 10% up front and possible additional 15% later. Many investors in the old GM, including all stockholders, received nothing after bankruptcy. Additionally, the Union was the first to recover money owed to them by the �“old GM�” through the sale of their shares during the IPO in November 2010. Unions rarely get such preferential treatment during bankruptcy. This is likely to reduce investment in the new GM in the future.

Since emerging from bankruptcy, GM has slowly made efforts to move away from unionized workforce. The new lithium battery plant that opened in February 2010 is the first U.S. entirely non-union plant GM has opened in 30 yearsxi. Additionally, GM is hoping to use recent profitability to convince the UAW in upcoming contract negotiations to agree to profit sharing bonus checks rather than flat line obligationsxii. Despite this progress, labor unions still pose a serious threat to GM, especially in the U.S. It is possible that labor negotiations could take a turn for the worse, eating into GM�’s profitability, or causing delays in production, missed contracts, etc. which would be costly, and damaging to GM�’s image.

Buyer Power

Given the importance of price competition between firms, it would appear that there is significant risk of buyer power in the automotive industry. However, the price competition is almost entirely directed towards the demand function for automobiles, and not toward the individual consumer during purchasing negotiations. General Motors, like most automakers, utilizes the dealership model. It sells large numbers of cars to dealers distributed across its target markets, and allows the dealers to negotiate with consumers. Indeed, from GM�’s direct perspective, the individual consumer has almost no say in the price.

CAMBRIAN GROUP

However, General Motors does also do a substantial portion of its business through rental and fleet sales. Rental firms buy a large number of cars at one time to be able to provide their own customers with the newest models. Additionally, firms and organizations buy enough vehicles for their fleets to be considerable parts of the GM business model. Indeed, just over 28% of 2010 sales were rental or fleet sales9. These customers, unlike individuals, have appreciable bargaining power, because they buy hundreds or thousands of vehicles at once. Buying cars in such bulk makes these consumers very price-oriented, and they have the ability to easily negotiate prices with other automakers. As a result, GM will often be forced to reduce prices very low in order to make the sale. Often, fleet customers are less concerned with the quality of their vehicles and more concerned about the price. This leads to the purchase of basic models with no additional features or quality options.

Entry & Exit

The threat of entry and exit of new firms in the automotive industry is low due to strong existing competition and high barriers to entry but varies depending on the market. In North America and Western Europe, the threat is almost nonexistent. The costs for a new firm to try and enter these markets would be astronomical. A new entrant would have to open production facilities, design at least one model, and begin production without any economies of scale in regions where the cost of labor is high. In order to see any return on investment, the new entrant would also have to spend significant amounts of money developing a brand name and convincing customers of their product�’s worth in a market where internal rivalry is already fierce among developed major players fighting for stagnant markets. The only way for a new firm to really enter these developed markets would be to buy a small local automaker, and then utilize its existing brand name to try to expand. As a result, GM faces almost no new competition for its 18.2% of the North American market, or its 8.8% of the European market9.

On the other hand, developing countries�’ automobile markets are growing. As countries develop, building infrastructure and generating higher incomes, both the demand for and the practicality of individual car ownership increases. The fastest growing automobile market is China, and

CAMBRIAN GROUP

generally Southeast Asia. In these countries, a new firm would not face such astronomical start-up costs. Labor and materials would be cheaper than in developed markets, production facilities would be less costly, and the marketing and branding would be less behind existing firms than in developed markets. Most importantly (especially with China), local firms would probably be able to benefit from government involvement and support, aiding in the development of these new entrants. This poses an advantage for local entrants and makes it more difficult for foreign firms wanting to enter a new market. Although entry is easier in developing markets, it still represents relatively low risk because the fierce internal rivalry of international companies in emerging markets still poses strong disincentives for potential new entrants.

In entering new emerging markets, GM may have to negotiate tricky government regulations in order to begin production, and will still face substantial marketing, advertising and branding costs. One particular advantage that GM has over its other main competitors is that it already has significant exposure in the developing world, especially China where they had a 12.8% market share in 20109. Startup costs for entering new emerging markets near countries in which GM already has brand strength will be lower due to the likelihood of brand recognition prior to entry.

Substitutes & Compliments

There are very few direct substitutes for passenger cars and trucks. Passenger cars and trucks provide a relatively affordable means of primarily short-distance transportation, but most other forms of transportation are indirect substitutes at best. Planes and trains are generally long-distance, to the point where there is rarely interchangeability between the two. Moreover, the consumer decision on whether to drive, fly, or take the train depends more on the price of gasoline or tickets for the alternative. These long distance trips do not affect whether or not consumers chose to buy cars. Similarly, walking and bicycling are usually too short-distance and weather-exposed to be valid substitutes. The closest methods of transportation would be public transportation (subways, buses, etc.), motorcycles, or private transportation (taxi, rental, etc.). Of these, motorcycles generally appeal to a very different customer demographic, and taxis and rental cars are far too expensive and unavailable in many areas to

CAMBRIAN GROUP

truly be substitutes for cars except in a small number of cities (New York City, San Francisco, Hong Kong, etc.). The biggest concern for General Motors from the substitute standpoint would be consumers becoming less willing to buy cars, and opting for public transportation instead. However, public transportation has remained unpopular in most cities over time, and is not likely to change significantly in the near future considering the continuing government plans for investment in road infrastructure in major auto markets such as the U.S., China, Russia, and India.

Gasoline is the obvious complement to automobiles. When gas prices increase, demand for cars clearly shifts from large inefficient models to smaller, better-designed ones. Additionally, as GM has experienced multiple times throughout its history, total demand for cars decreases if gas prices rise. For this reason, General Motors is tied very closely to the complementary price of gas, although it is working to improve its fuel efficiency, fuel switching capabilities, and hybrid, electric, and fuel cell technology in order to compete in the world of decreasing gasoline dependency. There are some other complementary goods to automobiles, such as the cost of parking and the cost of driving (tolls, etc.), but these costs are generally fixed, or increase slowly and predictably.

FINANCIAL ANALYSIS Overview & Stock Performance

General Motors emerged from its Chapter 11 reorganization in July 2009 with increased financial stability after shedding bad assets and non-core businesses. The company had its initial public offering in November 2010, and since then its share price has remained relatively constant, staying within 15% of the original IPO price. Figure 1 displays the changes in the Company�’s stock price since its IPO. Investor confidence in GM reached a high point after the 2010 annual report showed a revenue increase of 29% over 2009 and Net Income of $4.7 billion. However, this confidence has deteriorated over the past several months as analysts and investors realize GM may not actually be as strong as originally thought. Additionally, lingering concerns from GM�’s bankruptcy less than two years ago continue to create doubt. During 2011, GM�’s stock has underperformed its major

CAMBRIAN GROUP

competitors, none of which declared bankruptcy, especially with respect to foreign competitors15. Figure 2 displays GM stock performance relative to competitors.

Figure 1: GM stock price from 11/18/2010 �– 4/15/2011

Source: Yahoo! Finance

CAMBRIAN GROUP

Figure 2: GM, Toyota, Ford, and VW stock prices 2011 YTD

Source: Yahoo! Finance

Profitability

The new GM�’s profitability has clearly improved, recording their first profit in 2010 since 2004, not including the income attributable to bankruptcy in 2009. In 2010, the Company�’s revenue increased by $30 billion, a 28.7% increase from the previous year. The main drivers of this revenue growth were increased wholesale volumes due to an improving economy and successful launches of new vehicles including the Chevrolet Equinox and the Buick LaCrosse, and increased revenues from OnStar, among other factors. GM�’s FY 2010 profit was $4.67 billion, as compared to its $4.23 billion loss in the period between 7/10/2009 and 12/31/2009. Additionally, this marks a 115% increase from its $30.94 billion loss in FY 2008. This difference is mainly attributable to increased operating income, which was $5.1 billion in FY2010 compared to a loss of $21.0 billion in FY2009. Restructuring efforts have drastically improved the gross margin of automotive sales, bringing it to 11.5% in FY2010 after years of being negative9.

CAMBRIAN GROUP

The company�’s revenue has continued improve in early 2011. Total U.S. sales rose 49% in February 2011. The Company�’s Chevy brand accounted for the most sales volume in February 2011, with total sales of 142,919 vehicles. GMC, Cadillac, and Buick followed behind. Don Johnson, Vice President of U.S. Sales Operations cites the following reasons for the company�’s recent success: �“Having the right vehicles in inventory, combined with aggressive advertising and targeted consumer marketing has been the key to our success in the first two months this year�”xiii.

As a result of these sales figures, the company�’s market share has increased in 2011. In March GM had captured a 21.3% share, up from 19.4% for the comparable two months of 2010. Analysts suggest that GM increased its market share through price discount programs. During the two-month period, the average discount on a Chevrolet Impala was nearly $7,500, and the average discount on a Cadillac CTS was $7,700. GM claims that these discount programs match its production with consumer demands. Analysts are more wary of this tacticxiv. The company has a history of such discounts, and chasing unprofitable market share was part of what led to their bankruptcy in 2009.

Industry Comparable Analysis

Within the automotive industry, GM competes primarily with Ford, Toyota, Volkswagen, and Chrysler. However, analysts usually compare GM to Ford, Toyota, and VW because Chrysler is privately held. Presently, GM lags behind its publically traded competitors in both total earnings and behind Toyota and Ford in gross margin. This is likely due to the heavy discounts GM is offering on vehicles (much greater than competitors) to regain market share and reputation after bankruptcy. An operating margin in between its competitors shows the success of cost cutting objectives during reorganization, before which GM had lower operating margins than all three competitors.

Largely as a result of lingering investor precaution after GM�’s bankruptcy, the company�’s current market capitalization and price to sales ratio is the lowest among the four and their price-to-earnings ratio takes the second to lowest rank. A fair amount of investor uncertainty remains surrounding

CAMBRIAN GROUP

GM�’s ability to maintain profitability in the long term. Table 1 contains relevant information about GM�’s financial performance relative to its peers�’.

Table 1: Industry Comparable Analysis 5/15/2011

GM F TM VOW.DE

Market Cap 47.20B 55.64B 121.73B 243.06B Employees 202,000 164,000 317,734 399,381 Revenue (ttm) 135.59B 128.95B 236.41B 183.10B Gross Margin (ttm) 12.79% 16.11% 13.03% 6.95% EBITDA (ttm) 12.42B 14.48B 21.26B 18.32B Operating Margin (ttm) 4.28% 6.90% 2.64% 6.02% Net Income (ttm) 4.67B 6.56B 5.96B 9.86B EPS (ttm) 2.89 1.66 3.8 4.38 P/E (ttm) 10.46 8.84 20.42 23.83 P/S (ttm) 0.35 0.43 0.52 1.33 Source: Yahoo! Finance

Financial Health & Liquidity

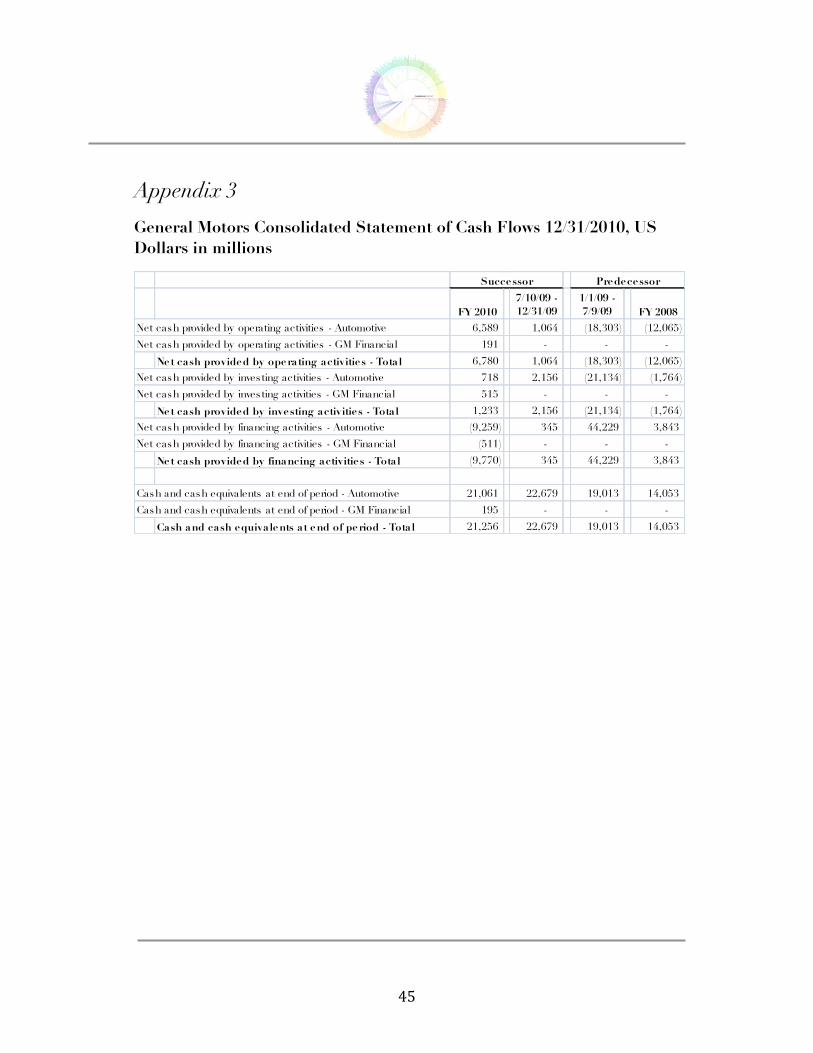

GM�’s operating activities generated $6.78 billion during 2010. This represents a change from 2008 and 2009 during which operating activities instead required cash. Investing activities provided another $1.2 billion, 41.8% from GM Financial and 58.2% from Automotive. The November IPO provided an additional $4.9 billion from issuance of stock. GM made debt payments of $10.5 billion9.

Table 2: Relevant Financial Health Ratios

2010 2009 ROA 0.03 0.77 ROE 0.21 4.77 Debt/Equity 0.12 0.72 Debt/Assets 0.03 0.12 Quick Ratio 0.75 0.58 Current Ratio 1.13 1.13 Leverage 3.74x 6.21x Source: General Motors 2010 10-K Balance Sheet

CAMBRIAN GROUP

The ratios in Table 2 clearly illustrate the financial effects of GM�’s Chapter 11 reorganization in July 2009. After emerging from the reorganization, the company�’s return on assets (ROA) and return on equity (ROE) plummeted. This is primarily due to the 95.5% decline in the Company�’s earnings from FY2009 to FY2010, which is attributable to nonrecurring gains from the Chapter 11 filing that �“old GM�” earned for the period between 1/1/2009 and 7/9/2009 (please reference the income statement in the appendix to see this effect)9. The 2010 ROA is in line with the industry average and the ROE is among the highest in the industry.

Through the bankruptcy restructuring elimination of debt and sale of bad assets GM reduced its debt-to-equity ratio from 0.72 to 0.12, its debt-to-assets ratio from 0.12 to 0.03, and decreased its leverage multiple by 39.8%. This was mainly due to the 84% decrease in short term debt and 46% decrease in long term debt. These indicators suggest that its new capital structure is less prone to bankruptcy risk. These figures are very low relative to GM�’s major publically held competitors, none of which have recently filed for bankruptcy. The quick ratio decreased due to the simultaneous increase in cash and cash equivalents and decrease in short term debt. The current ratio is in line with industry averages and quick ratio is lowxv.

Regional Analysis

GM has seen consistent slight market share declines in North America and Europe, constant market share in South America, and growing market share in International Operations. North America and Europe also have the lowest overall industry growth. In 2010, 81% of EBIT came from North America, 32% from International Operations, and 12% from South America. European Operations lost 20% of total automotive EBIT. Table 3 shows GM�’s vehicle sales, market share, and EBIT from 2008 to 2010. Between 2009 and 2010 GM lost market share in the US to Ford, Chrysler, Nissan, and Hyundai/Kia. The US market overall saw 11% increase. A majority of GM sales growth was in midsize cars, SUVs, and pickup trucks. Through the sale of excess capacity during the bankruptcy reorganization capacity utilization of the GMNA division has improved from 61.5% in 2009 to 89.6% in 2010. However, this is still represents a lower return on assets than is ideal. The European market is stagnant at only 0.9% growth and GM

CAMBRIAN GROUP

continues to lose money in this region, representing a loss of $1.7 billion in 20109. As Figure 3 shows, GM�’s South American and International Operations are increasingly making up a greater portion of sales.

Table 3: Regional Sales

FY 2010 - GM FY 2009 - Combined GM FY 2008 - Old GM

Values in

mill ions

Vehicle Sales

(Units)

Market Share

EBIT ($USD)

Vehicle Sales

(Units)

Market Share

EBIT ($USD)

Vehicle Sales

(Units)

Market Share

EBIT ($USD)

GMNA 2,625 18.2% 5,748 2,484 18.9% (15,912) 3,565 21.5% (12,203)

GME 1,662 8.8% (1,764) 1,668 8.9% (3,629) 2,043 9.3% (2,625)

GMIO 3,077 8.8% 2,262 2,453 8.7% 303 1,832 7.4% (555)

GMSA 1,026 19.9% 818 872 20.0% (37) 920 20.7% 1,076

Worldwide 8,390 11.4% 7,064 7,477 11.6% (19,275) 8,359 12.3% (14,307)

Source: General Motors 2010 10-K

Figure 3: GM Vehicle Sales

Source: General Motors 2010 10-K

3,565 2,484 2,625

2,043 1,668 1,662

1,832 2,453 3,077

920 872

1,026

2008 2009 2010

GM Vehicle Sales (Units in Millions)

GMNA GME GMIO GMSA

CAMBRIAN GROUP

The strongest market growth for the auto industry is in Asia Pacific and South America. The largest percentage market growth in Asia Pacific was in India, at 33.6%. GM saw Indian market share increase but still represents a small percentage of the market, only 3.7%. The Chinese market grew by 33.5% but GM sales did not quite keep up at only 28.8% growth. GM has been able to maintain consistent market share in South America, growing sales at 18%. The Brazilian market grew by 11.9%. The strongest growth in South America for the industry overall, and where GM saw market share increase, has been in Argentina, Colombia, and smaller countries9. Please reference the Regional Market Growth in the appendix.

SWOT ANALYSIS Strengths Weaknesses

Leadership in Emerging Markets High Labor Costs & Union Issues Competitive Technology SUV and Truck Exposure Strong Brand Recognition Bankruptcy Reputation Damage Financial Benefits of Bankruptcy & Gov.

Exposure to Supplier Risk

Diversified Sales Vertical Integration through GM Financial

Opportunities Threats New Emerging Markets Competitors in Asian Emerging

Markets Developing niche SUV/Truck Market

Rising Gasoline Prices

Parts for New Market Entrants China�’s Vehicle Restrictions OnStar Technology Domestic Price War

Strengths

Leadership in Emerging Markets �• Second largest market share (8.8%) for combined Asia-Pacific, Africa,

and the Middle East Market

CAMBRIAN GROUP

�• Growth in Asian market share since 2008 �• Market leader in China (12.8%) through JVs �• Second largest market share (19.9%) in South America �• No domestic Brazilian manufacturers �• Growing market share in India since 2008

Competitive Technology

�• Successful recent launch of new fuel efficient models �• OnStar is the market leader in security, support, and recently launched

internet smart integration �• More clean tech patent registrations in the U.S. during 2010 than any

other organization

Strong Brand Recognition

�• Second largest worldwide market share �• Largest US market share and iconic American brand image �• Recent streamlining of domestic brand focus: Cadillac, Chevrolet,

GMC, Buick

Financial Benefits from Bankruptcy and Government Stake

�• Old GM (Motors Liquidation Co.) continues to be saddled with liabilities such as environmental cleanup of GM�’s previous operations

�• Tax Breaks granted for previous losses despite bankruptcy declaration �• Government support in employee relations and non-union worker

benefit cuts

Diversified Sales

�• Product portfolio includes options for high, medium, and low income customers through different brands which helps cushion total sales from a change in spending habits of any one customer segment

�• In 2010, 73.6% of sales were outside the US and 43.0% came from emerging markets including: China, Brazil, and India. Geographic diversification of sales limits the exposure to one failing economy or government regulation

Vertical Integration through GM Financial

�• Increases the number of consumers able to purchase GM vehicles

CAMBRIAN GROUP

�• May push lower income consumers with unestablished credit to choose a GM vehicle over a competitor

�• Provides an additional revenue stream

Weaknesses

High Labor Costs and Obligations �• Higher percentage of Union labor than international competitors �• Continuing obligations to existing and retired UAW employees.

Although restructuring shifted many healthcare liabilities to Union operated trust, GM is still responsible for union pension plans

�• High sales and production percentage in U.S. where labor costs are higher and union power is stronger

SUV and Truck Exposure �• Increased correlation of revenue and stock price with gasoline price

volatility �• High financial and reputation exposure to growing fuel efficiency

regulation

Poor Financial Reputation �• Bankruptcy filing continues to make investors wary �• Preferential treatment given to UAW over investors during bankruptcy

will deter some potential new investors �• Will need several years of positive profit to erase memory of losses

since 2004

Exposure to Supplier Risk �• Centralized purchasing reduces supplier diversification �• Minimal holding of input stocks increases risk of input volatility

disrupting operations or increasing costs

Opportunities

Growth of New Emerging Markets �• Knowledge of successful entry best practices through learning �• Strength in China and Brazil can be used as base for expansion into

surrounding emerging markets

CAMBRIAN GROUP

�• Products are well suited to emerging markets �– small vehicles under Baojun and Chevrolet brands for emerging crowded cities and Trucks, Vans, and SUVs for developing areas

Increasingly Niche SUV and Truck Market �• Cash Cow market future �– High market share with low overall market

growth �• Strong GMC and Chevy brand recognition and reputation �• GMC and Chevy have the best EPA fuel estimates among domestic

trucks �• Risk of gasoline exposure is causing slow exit by competitors and

preventing entrants �• Demand will persist, especially in emerging markets where

development requires heavy duty vehicles

New Entrants in Emerging Markets Create Market for Auto Parts �• Vertically integrated into upstream parts production �• Alternative revenue stream in emerging markets �• Will allow income from GM�’s auto parts technology that would

eventually be copied by domestic competitors

Maximize Revenues Driven by OnStar �• Provides product differentiation �• Leadership in this technology builds reputation and brand recognition �• Internet and smart technology integration is forecasted to be one of the

major future auto trends

Threats

Competitors in Asian Emerging Markets �• Recent gains by Chinese auto manufacturers in the domestic market �• Chinese government provides support for Chinese manufacturers �• Growth of Hyundai/Kia market share in Asia Pacific and in U.S. market

Rising Gas Prices �• Poses threat to auto industry overall and increases likelihood

consumers will switch to substitutes

CAMBRIAN GROUP

�• Especially dangerous for GM due to high profitability of SUV and Truck sales

Government Regulation

�• China is considering limiting the number of vehicle registrations allowed in major cities which would decrease demand in GM�’s largest market and intensify internal competition

Price War

�• History of domestic price wars between GM, Ford, and Chrysler eroding profits

�• GM heavily discounted vehicle prices in the US in early 2011 �• Doubts about how much longer Ford will tolerate GM�’s discounting

without reacting �• Loss of Ford market share in early 2011

CAMBRIAN GROUP

PART III RECOMMENDATIONS

CAMBRIAN GROUP

STRATEGIC RECOMMENDATIONS Global Positioning: Emphasis on South America and Asia

The European market has stagnated and the North American market is growing slowly. In contrast, South American and Asian markets are growing rapidly. Luckily for GM, these are also the markets where it has seen strongest maintenance of its market share. Additionally, GM�’s historical competitive advantage, reputational strength, and leading fuel efficiency in trucks and SUVs are well aligned with the demand that will emerge in these markets as the more rural areas develop. GM is especially well positioned in South America where fuel is cheap, no local competitors exist, foreign competitor penetration is currently low, and unlike the shift

towards small cars throughout the rest of the world, consumers like to drive bigger vehicles. Additionally, production in Asia and South America is accompanied by far less union pressures. Increasing the percentage of GM production in these regions will decrease company labor costs and liabilities. To capitalize on this potential for growth and cost reduction, we

recommend that GM shift its emphasis away from Europe and focus on these key emerging markets.

China - Increase Small Vehicle Offerings in Cities

As the current market leader in China through three major JVs, GM is in a strong position to gain from the projected growth of the Chinese automobile market. In 2010, GM and its JVs generated a net income of $2.8 trillion9. Market growth will likely slow due to eliminated tax incentives and

new restrictions on the number of license plates allowed in Beijing, but will continue in low double digitsxvi. The number of Chinese driving age consumer with enough disposable income to afford a car is supposed to grow from the current 700 million to more than 1.1 billion by 2020xvii. As competitors increasingly fight for this reduced new growth, it is important

for GM to pursue an aggressive strategy in the short term to maintain market share while simultaneously product positioning for maximum success in the long term.

Despite growth in GM China sales over the past three years, market share has declined; the industry is growing faster than GM9. Emerging Chinese

CAMBRIAN GROUP

domestic auto manufacturers comprise a majority of this higher growth. There are two things domestic manufacturers are doing differently than GM: they sell a higher percentage of small vehicles and offer lower pricesxviii. GM is not effectively capturing the most rapidly expanding customer segment in China, first time low cost auto consumers. Much of the new demand for 2011 is predicted to come from motorcycle drivers upgrading to small vehicles which they are able to afford for the first time17. In the short term, GM must increase their offering of small vehicles in major cities, especially the second tier cities, and increase price competitiveness to maintain their share of this market where growth is largely driven by first time low cost buyers.

The newly developed Baojun brand of affordable passenger cars and Wuling�’s first mini car (Lechi) will hopefully help fill this void18. GM is already committed to refreshing their European portfolio with new models of small vehicles. Relevant aspects of this product development should also be put to use in China through the new global product development strategy (see below). GM should continue to keep a finger on the pulse of consumer demand in China through their JV partner�’s domestic experience.

Additionally, GM should consider which of their existing Chevrolet models would appeal to this customer. During 2010, Chevrolet was their highest selling brand9. GM should consider reducing prices on select Chevrolet models they believe would meet significant demand from the higher end of this very price elastic consumer segment. This will allow the popularity of the brand to be used to drive sales in this currently underserved segment. However, GM must also maintain the image and quality of the Chevrolet brand, rather than marketing it as a budget vehicle, in order to appeal to the growing middle class in China in the long term. After the short term push for maintaining competitiveness, as the Chinese market matures and Chinese consumer purchasing power grows, GM will be able to increase prices and restore its margins. Additionally, GM can use their established company popularity in the country to push Cadillac and Buick sales to appeal to the emerging wealthy consumers, the most valuable consumer segment in the long term.

CAMBRIAN GROUP

China - Increase Pickup Truck and Van Availability to Developing Rural Areas

The large Chinese cities are in the midst of their auto market development. Eventually these markets will mature and this growing demand for city vehicles will slow. The next phase of growth will come from the development of more rural areas in China, driving increased demand for pickup trucks and vans, which are used in construction, moving materials long distances (between cities and rural areas), and agriculture. This is good news for GM whose competitive strength has historically been in its trucks and SUVs. GM should begin positioning itself for this type of growth in the long term.

The Wuling brand of vans already has strong recognition and developed operations in China. This brand can help fill the projected growth in demand for vans. The strength of the Chevrolet brand can also be used

through introduction of Chevrolet trucks into China. Additionally, GM should introduce the line of Chevrolet mini trucks and vans that are currently sold in South America into the Chinese market to help fill this void. These condensed low cost vehicles are perfectly in line with the long term demand prediction in dense and growing China.

China - Sell Parts to Local Auto Makers

Much of the recent decline in GM�’s market share is due to the entrance and growth of domestic Chinese competitors. The Chinese government is openly committed to supporting the success of these domestic companies. GM is currently shedding non-core businesses and recently sold their steering parts manufacturing unit in China to Chinese Pacific Century Motors. PCM and other auto and auto parts manufacturers in China have

expressed interest in acquiring more of GM�’s parts manufacturing unitsxix. GM should be cautious in selling due to the increased supplier power they will face as a result. To counter the mounting supplier power of increasingly vertically integrated domestic competitors, GM should retain its profitable parts manufacturing units in China and begin negotiations for selling these parts to domestic auto manufacturers. This would increase the degree to which they can benefit from Chinese auto market growth, diversify their revenue streams in China to reduce exposure the fluctuations

CAMBRIAN GROUP

in consumer taste and potential future governmental regulation, and control the some of the upstream channels of their competitors.

The Chinese auto parts manufacturing industry is relatively new and is still technologically behind international parts manufacturers in many respects19. However, it is likely that emerging Chinese manufacturers will explore and emulate best practice technologies in the industry, as Chinese industry is known to do. This is another important reason to sell parts to local competitors. If GM can lock in long term parts sales contracts, the company will be able to increase revenue from parts�’ technology and delay Chinese companies�’ copying of it.

India - Increase Vehicle Offering and Explore JV with Domestic Company

GM has sustained year over year market share growth since 2008 in the rapidly expanding Indian market despite relatively low corporate emphasis placed on this region compared to other emerging markets. In 2010, India comprised 7.5% of total automobile industry sales in Asia, Africa, and South America but only 2.7% of GM�’s sales in these regions9. Currently, the streets of India are filled with motorbikes and low cost Indian manufacturer, Tata Motors, dominates both the motorbike and automobile markets.

However, GM�’s natural growth indicates the potential for GM to expand in India. The growing average income of consumers and commitment of the government to building road infrastructure predicts that this market will continue to grow. By 2020, the number of driving age consumers able to afford a low cost vehicle is projected to reach 500 million, compared to the current 165 million17.

Currently, GM is increasing focus on developing smaller low cost vehicles for introduction in Europe, U.S.9, and as we recommended above, China. These new vehicles should also be introduced in Indian cities, where new auto consumers are likely upgrading from motorbikes and the highest demand growth is likely to be in low cost vehicles as increasing numbers of people are able to afford cars for the first time. If the new Baojun brand is successful in China, we recommend also bringing this budget brand focused on small vehicles to India, where major cities are seeing similar development a few years later.

CAMBRIAN GROUP

Additionally, as in the Chinese market, India will see demand increase for trucks and vans in the long term as the more rural areas develop. This growth will be fueled by the Indian government�’s commitment to expanding the road network to rural parts of the country. The Chevrolet mini trucks and vans currently sold in South America are a good fit for this demand growth. This development is several years behind China, but GM should be aware of this opportunity in the long term.

The simultaneous marketing push for GM vehicles and forging JV�’s proved a successful model for becoming a major player in China, an emerging market where, like India, domestic players already existed. GM should evaluate the potential to partner with a domestic producer as an avenue for expansion in India.

South Korea - Build up GM Korea to Compete with Hyundai/Kia

Over the past several years Hyundai/Kia has increased market share in Asia and the U.S., which are both critical for GM. In order to effectively compete with this growing industry player, GM should build up GM Korea, GM�’s JV in South Korea formerly Daewoo Auto & Technology Co. GM Korea has already announced it will abandon the Daewoo brand and focus on selling Chevrolet. Hyundai�’s market share growth is attributable to their continued low cost small vehicle offerings through the Kia brand and recent entry into the luxury market through new Hyundai brand modelsxx. In addition to focusing on Chevrolet, GM must compete with Hyundai in the luxury market in South Korea and offer Cadillac models that can compete with the increasing technological competitiveness of Hyundai and appeal to the growing wealthy class in South Korea.

New Markets (e.g. Thailand) - Enter Utilizing Position in Nearby Markets

GM�’s strong reputation, brand recognition, and production capacity in key emerging markets such as China, Brazil, and Mexico can be utilized to help enter or expand sales in nearby markets as they grow. This must be viewed as a long term strategy as many emerging markets are still far from providing demand high enough for profitable entry. Thailand, the third fastest growing auto market in Asia, with no major domestic manufacturers, is ripe for GM�’s entry. GM�’s strong reputation, brand recognition, and capacity in China will undoubtedly facilitate entry into this market.

CAMBRIAN GROUP

Europe - Refresh Product Portfolio and Cut Capacity

The European division continues to operate at a loss. There are two major reasons for this. First, GM�’s product portfolio is poorly aligned with European demand, damaging sales. Secondly, GM is overinvested in capacity in Europe and faces a difficult cost structure while Europe�’s market growth is stagnant. GME has already announced that they plan to refresh 80% of their European brand (Opel and Vauxhall) models by 2012 and reduce capacity by 20%9.

Due to stagnant demand and poor growth outlook, GM should be cautious about investing more capital into the European market. GM should consider abandoning its most outdated models all together, focusing on smaller and more fuel-efficient models. In determining where capacity reduction should come from, GME should consider the efficiency of each production facility and the cost of changing the facilities to abandon outdated models and produce the new models.

Fleet Sales: Improve Vehicle Quality to Rental Companies

In 2010, fleet sales represented 21.4% of worldwide vehicle sales and 28.2% of U.S. vehicle sales. Of the fleet sales in the U.S. 68.8% were daily rental sales. The vehicles sold to short-term rental companies are often standard stripped down models without additional technology or luxury options. Due to GM�’s high share of U.S. rental fleet sales, renting a car is undoubtedly many consumers�’ first experience with a GM vehicle. Therefore, low quality vehicle sales to rental companies are hurting GM�’s consumer sales. Instead, GM should view sales to rental companies as an advertising opportunity, a chance to steal future market share away from competitors. If a car consumer rents a GM vehicle while on vacation or a business trip and is impressed by the technology, fuel efficiency, or quality, they are much more likely to consider and seek out GM models the next time they purchase a car. Therefore, we recommend that GM pursue higher quality vehicle sales to short-term rental fleet customers.

CAMBRIAN GROUP

U.S. Pricing: Reduce Discounts to Limit Competition

During the first part of 2011, GM sold at strong discounts in the U.S.14. This initial push to regain market share after emerging from bankruptcy is understandable. However, we recommend that GM reduce discounts and exercise caution in the future before severely slashing prices. There are two reasons for this. First, the company should avoid chasing unprofitable market share as they did in the years preceding bankruptcy. In addition to lost profits as a result of selling at a discount, the additional customers at the margin who are convinced to buy GM vehicles as a result of the lower price are more likely to need financing from GM Financial and more likely to default on the received loans. GM's former addiction to providing easy credit and cut-rate financing contributed to surmounting problems that led to bankruptcy. Instead, GM should focus on selling to customers who can afford the vehiclesxxi. Additionally, these customers represent a lower future profit stream as they are less likely to purchase a second vehicle or to upgrade their vehicle in the future.

Secondly, discounting vehicle prices opens the door for intensified price competition in the U.S. market with competitors Ford and Chrysler. Although Ford has openly committed to not engaging in a price war, many analysts suggest that if GM continues the sell at such high discounts they risk increasing the already strong internal competition that will undoubtedly erode profits in the industry and may even lead to a domestic price war14. This pressure has been intensified by Ford�’s market share decline in early 2011, presumably resulting from the strong GM and Toyota discountsxxii.

Additionally, despite lower sales in 2009, there was evidence that customers in the U.S. were increasingly willing to pay more for good cars. At the country�’s biggest auto dealership, AutoNation (AN), revenue per car increased $800 even though new-car unit sales fell 25%xxiii. By offering large discounts, GM is failing to capture this increased consumer willingness to pay. Instead, GM should reduce discounts and commit to a �“pull�” strategy, in which the automobile industry only produces the number of vehicles demanded but remains profitable, rather than a �“push�” strategy, in which the industry sells at strong discounts to increase demand. To optimize profitability while implementing this strategy and show domestic

CAMBRIAN GROUP

competitors that GM is committed to preventing price war, we recommend that GM consider further cutting capacity in Europe, above the current strategy of cutting 20%, and in the US, where utilization is still only 89.6%11.

Product Development & Production: Transition to a Modular Shared Global Platform

GM�’s current product development strategy is focused on consolidating and standardizing. The company hopes to increase the number of vehicles produced which are one of ten global product archetypes including: mini, small, compact, midsize, midsize crossover, midsize truck, small SUV, compact SUV, small rear wheel drive, and large rear wheel drive. Management�’s goal is to increase the percentage of archetype vehicle sales from 17% in 2010 to over 50% by 20159. This is a great strategy that will help GM benefit from economies of scale in both design and production. However, it is not aggressive enough. GM should begin the transition to a global modular product development and production system that maximizes the potential for sharing of parts and expertise across brands, models, and markets. The modular strategy is excellently employed by Volkswagen Group and GM should use their innovative approach as a guide.

It will be important to balance these benefits with adjusting for the different demands of GM�’s various markets and maintaining separate brand images. To accomplish this, GM should pursue a strategy of customized uniformity. Under this strategy there will be two sets of product development teams. The first set will consist of ten teams that each specialize in one of the ten global archetypes listed above. This product development will focus on improving the underlying structure and systems of their designated product archetype. Additionally, these ten teams should work together to maximize the potential for sharing of parts and expertise across different archetypes.

The second set of product development teams will each specialize in regional demand and will customize all archetype designs sold in their market of expertise to meet the demands of the different customers within their region. It will be the responsibility of these teams to adapt the designs and product offerings for each brand across all archetypes offered in the

CAMBRIAN GROUP

region to ensure that each brand effectively appeals to its target regional market. In new emerging markets or countries in which GM�’s existing design teams are less familiar with the market, JV�’s have proven to be a successful way of incorporating local demands into standardized models. This method of customized uniformity in product development and production will allow the economies of scale benefits and synergies of increased standardization while maintaining the ability to adapt to each market and customer segment. The teams specializing in each archetype will be able to use and develop their knowledge across markets and brands and the regional specialist teams will be able to use their knowledge across different products in their region of expertise, customizing each archetype to fit local demand through different brand images.

GM Financial: Offer Short Term Loans to Suppliers

The reliability of GM�’s suppliers is important to their business. In recent years, financial difficulty experienced by suppliers has led to disrupted operations and increased costs for GM9. The purchasing power and bulk discounts GM acquires through centralized procurement is accompanied by increased consequences if their suppliers fail. As the company continues to shed non-core businesses and decreases vertical integration, including the recently announced sale of the Class A Membership Interest in Delphi Automotive, exposure to supplier failure risk increasesxxiv.

Currently, GM Financial offers vehicle financing for consumers. We recommend that GM Financial enter the small business loan market in order to offer loans for key GM suppliers that run into short term financial difficulty or liquidity problems. This will help minimize GM�’s supplier related operation disruptions and related cost increases. GM Financial should not take on bad loans in order to save suppliers but rather use this business expansion as an additional revenue stream.

Brand Positioning: Cohesively Exhaustive and Mutually Exclusive

As a part of the post bankruptcy reorganization, GM has streamlined its domestic brands through shedding Pontiac, Hummer, Saturn, and Oldsmobile to focus on Chevrolet, Buick, Cadillac, and GMC9. This was a

CAMBRIAN GROUP

good move considering the overlap of many of the brands in the former portfolio. Selling more vehicles from fewer brands increases economies of scale in every stage of production. Moreover, advertising and sales expenses are wasted if they end up simply stealing the sale from another GM brand. Therefore, it is important for GM to differentiate their vehicles not only from competitors but also from their other brands. Moving forward, we recommend that GM pursue a cohesively exhaustive but mutually exclusive branding strategy in product development, advertising, and pricing in order to maximize market share and profits. In other words, GM should use these four brands to offer vehicle options that appeal to all customer segments without overlapping segments.

Cadillac is obviously the luxury and performance brand, purely appealing to the wealthy customer segment concerned with the driving experience and image. Buick is a midrange brand offering larger cars that will appeal to customers looking for family or driver vehicles. Chevrolet has always been GM�’s affordable brand. After the introduction of the Volt, it has also created an image as young, trendy, and ecologically responsible. GM is historically known for their trucks and SUVs, especially the GMC brand. With increasing fuel costs and fuel efficiency regulation, demand for SUVs and trucks are stagnating. As a result we see many competitors moving away from the production of these vehicles and no new entrants. However,

CAMBRIAN GROUP

demand is likely to continue even if it is not growing, largely as result of new demand in emerging markets replacing declining demand in established markets. This emerging cash cow market provides a unique opportunity for GMC to become the niche provider for trucks and SUVs in the long term.

The different brands will help GM price discriminate between different consumers�’ willingness to pay for a vehicle, and also between consumers�’ willingness to pay for technology and fuel efficiency. For example, the technology options could be offered at a lower price in Chevrolet vehicles than the same options in Cadillac. Table 4 offers insight into the customer segments for each brand.

Figure 4: GM�’s Customer Segments by Brand

Brand Customer Income

Key Demographic

Fuel Efficiency

Attraction

Importance of

Technology Cadilac High Professional Image High Buick Medium Family or

Driver $ Gas Savings Low

Chevrolet Low Young $ Gas Savings Medium** GMC Medium SUV

customers $ Gas

Savings* Low

*GMC customers may choose GMC over competitors�’ SUV brands if fuel efficiency is better. The draw for them would likely be the potential gas savings. However, their price elasticity for this feature would be high as fuel efficiency is likely not a major concern for customers who are already choosing to purchase an SUV or truck.

**Technological integration will be important to this younger demographic. However, they will tend to have high price elasticity.

GM Daewoo Auto & Technology Co., GM�’s joint venture in South Korea, has announced that it will change its name to GM Korea and will focus on selling the Chevrolet Brand, replacing the currently sold Daewoo brand9. Considering the increasingly global reach of advertising and brand loyalty

CAMBRIAN GROUP

benefits, we recommend that GM streamline brands globally in the long term. However, due to differences in local market demand and existing brand equity GM should only replace international brands with one of the core four if the existing brand is underperforming, as Daewoo was. Currently, it is not advisable for GM to replace any existing brands abroad.

SAIC-GM-Wuling Automobile Co., one of GM�’s two joint ventures in P.R. China has recently begun marketing under the newly developed Baojun brand of affordable passenger cars as a part of their multi brand approach to China18. Chevrolet is currently GM�’s fastest growing brand in China and it will be important to ensure that Baojun is kept distinct from Chevrolet, as super low budget, to ensure that the new brand doesn�’t cannibalize Chevrolet sales in this key market.

Product Positioning: Technology Integration and Fuel Efficiency

Major global trends of improving technology and increasing fuel prices will continue to shape every industry around the world, and automobiles are no exception. As existing markets evolve and new markets emerge, the future of the automobile industry will see movement towards greater demand for computerization and technological integration, increased fuel efficiency, and price reductionxxv. In order to stay competitive, GM must pursue an integrated approach towards advancing all three. It is imperative that GM remain technologically competitive and innovative. The company is currently well positioned to do this. In 2010, GM received more clean energy patents for new technologies than any other organization. Also in 2010, their OnStar division launched the most advanced internet integration system for automobiles on the market9.

Leveraging the OnStar technology and brand, continuing strong investments in R&D, and maintaining the newly created venture capital arm, General Motors Ventures, will be important in coming yearsxxvi. Key focus areas should include electric vehicles and integration with smart devices and information technology. These features are becoming increasingly standard and should be available as options in all models in developed markets to help consumers self select. GM should consider partnering with technology companies, such as Apple, to develop vehicle

CAMBRIAN GROUP

technology integration. Infrastructure complements, such as electric vehicle charging stations, will be crucial to the success of GM�’s electric vehicles. We recommend GM also consider partnering with electric utilities to develop this infrastructure.

CAMBRIAN GROUP

APPENDICES Appendix 1

General Motors Income Statement 12/31/2010, US Dollars in millions

FY 2010 7/10/09 - 12/31/09 1/1/09 - 7/9/09 FY 2008

Net Sale s and revenue

Automotive Sales 134,142 57,329 46,787 147,732

GM Financial and other revenue 281 - - -

Other automotive revenue 169 145 328 1,247

Total net sales and revenue 134,592 57,474 47,115 148,979

Cos ts and expens es

Automotive cost of sales 118,792 56,381 55,814 149,257

Automotive Gross Margin 11.55% 1.90% -18.46% -0.19%

GM Financial operating expenses and other 152 - - -

Automotive selling, general and adminstrative expenses 11,446 6,006 6,161 14,253

Other automotive expenses , net 118 15 1,235 6,699

Total costs and expenses 130,508 62,402 63,210 170,209

Operating income (loss ) 5,084 (4,928) (16,095) (21,230)

Equity in income (loss ) of and dispos ition of interes t in Ally Financial - - 1,380 (6,183)

Automotive interes t expense (1,098) (694) (5,428) (2,525)

Interes t income and other non-operating income, net 1,555 440 852 424

Gain (loss ) on extinguishment of debt 196 (101) (1,088) 43

Reorganization gains , net - - 128,155 -

Income (loss ) before income taxes and equity income 5,737 (5,283) 107,776 (29,471)