can a wider look on reporting enable greater trust in ...file/ey... · can a wider look on...

TRANSCRIPT

The better the question. The better the answer �.The better the world works.

Can a wider look on reportingenable greater trust in business?

4th Annual Financial Reporting Insights

Athens, 13 December 2017

Page 2 Financial Reporting Insights – December 2017

1 Wider Corporate Reporting

Regulatory Update

Governance: Audit Committee role; Auditorrole: key audit matters

Revenue Recognition – practical considerations

Break-out Sessions:q IFRS Technical Updateq US GAAP Technical Update

Agenda

23

4

5

Morning break

Lunch break

Page 3

Wider Corporate Reporting

Financial Reporting Insights – December 2017

Page 4 Financial Reporting Insights – December 2017

Trust in business, financial institutions and society as a whole is at an all-time low ... brings together diverse stakeholders to create a framework which is a consistent model forhow companies can measure and report the long-term value they create.”

Mark Weinberger, EY Global Chairman and CEO

Wider Corporate Reporting

Page 5

Wider Corporate Reporting

► What is currently going on in the world of corporate reporting?

► What is the future of corporate reporting?

► How do we improve: Long Term Value

► Call for coordination and greater standardization

► Integrated reporting

Financial Reporting Insights – December 2017

Page 6

Wider Corporate Reporting

Financial Reporting Insights – December 2017

Short-termvalue

Long termvalue

Page 7 Financial Reporting Insights – December 2017

Investors perspective

ESG factors can significantly impact a company’s long term value. Onlythrough successful integration of ESGfactors can investors mitigate both theirinvestment and their reputational risk, whilepotentially improving their risk-adjusted returns.

Allianz Global Investors

We aim to be a responsible corporate citizenand to take into account environmental, social andgovernance issues that have real and quantifiable financial

impacts over the long-term for our firm and the firms inwhich we invest.

Blackrock

Page 8 Financial Reporting Insights – December 2017

Corporates’ perspective

Long-term investment and sustainablegrowth models go hand in hand. Businesses mustoperate with purpose embedded in their strategy, serving their shareholdersand wider society. The ability to articulate this in a standardized, meaningfulway has long been needed so markets can properly measure this broaderapproach to value creation.

Paul Polman, CEO of Unilever

Business must do more than simply turn aprofit. We must also be guided by a deepsense of purpose. This means measuring our success not onlyquarter to quarter, but also year to year and decade to decade. It meanscreating value for shareholders as well as society. Companies that embracethis mindset will be the ones to thrive long-term.

Indra Nooyi, Chairman and CEO of PepsiCo

Page 9

Accounting and reporting of long term value

Financial Reporting Insights – December 2017

The issues

1. Accounting profit and shareholderreturns are disconnected

2. We often report the wrong things

3. Diminishing trust in organizations

4. Over-burdensome regulation andincreased demands for informationresulting in reduced reportingclarity

The answers

1. Develop reporting systems providinginsight into how organizations createvalue over the long term;

2. Communicate the value of strategicassets;

3. Provide multi-stakeholder reportswith wider set of information relevantto stakeholders to rebuild trust;

4. Simplify reporting

Page 10

Integrated Reporting

Financial Reporting Insights – December 2017

Page 11

“Half the benefit of integratedreporting is integrated thinking.”

Richard Howitt, CEO of the International Integrated Reporting Council (IIRC)

Financial Reporting Insights – December 2017

Page 12

► There is a growing gap between market capitalization and book value.► Investors know there is a “hidden value” not fully recognized in financial statements, that is,

to a great extent, attributable to intangible assets.

17%32%

68%80% 84%

83%68%

32%20% 16%

0%

20%

40%

60%

80%

100%

1975 1985 1995 2005 2015

Tangible Assets

Intangible Assets

Source: OceanTOMO LLCJanuary 1, 2015

Organisational value creation is no longer fully captured bythe financial statements

Financial Reporting Insights – December 2017

Page 13 Financial Reporting Insights – December 2017

Page 14

Integrated Reporting

Financial Reporting Insights – December 2017

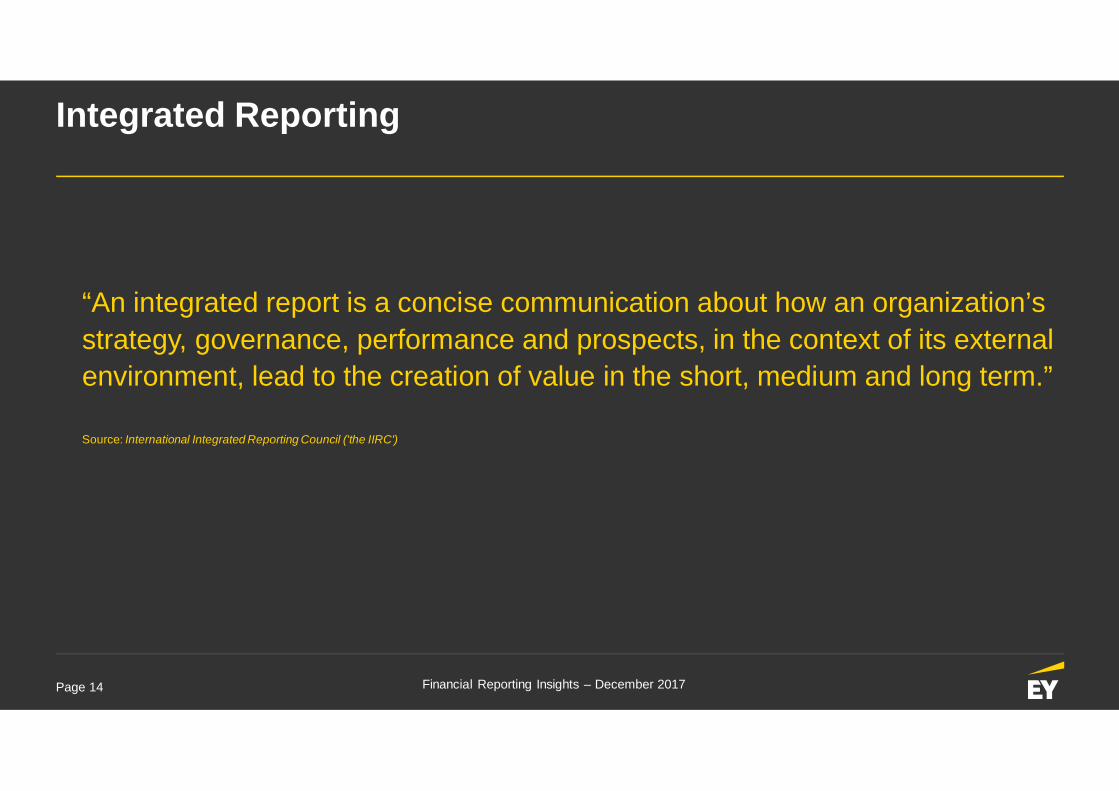

“An integrated report is a concise communication about how an organization’sstrategy, governance, performance and prospects, in the context of its externalenvironment, lead to the creation of value in the short, medium and long term.”

Source: International Integrated Reporting Council ('the IIRC')

Page 15

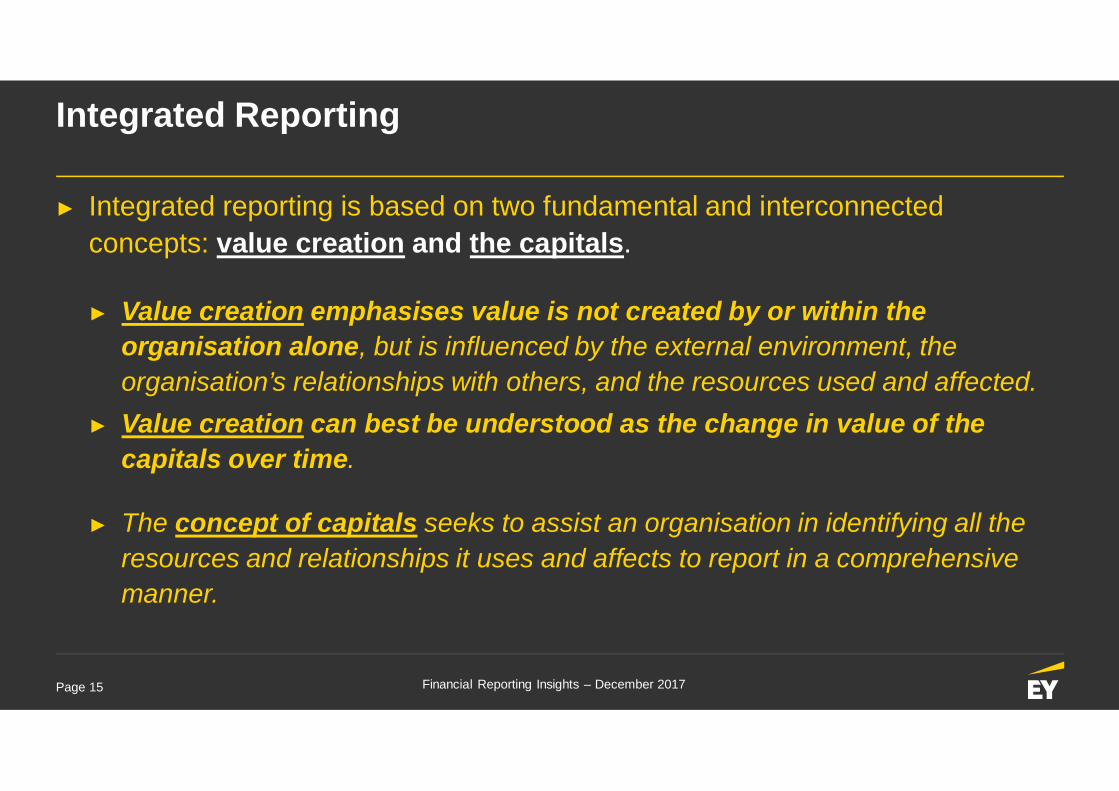

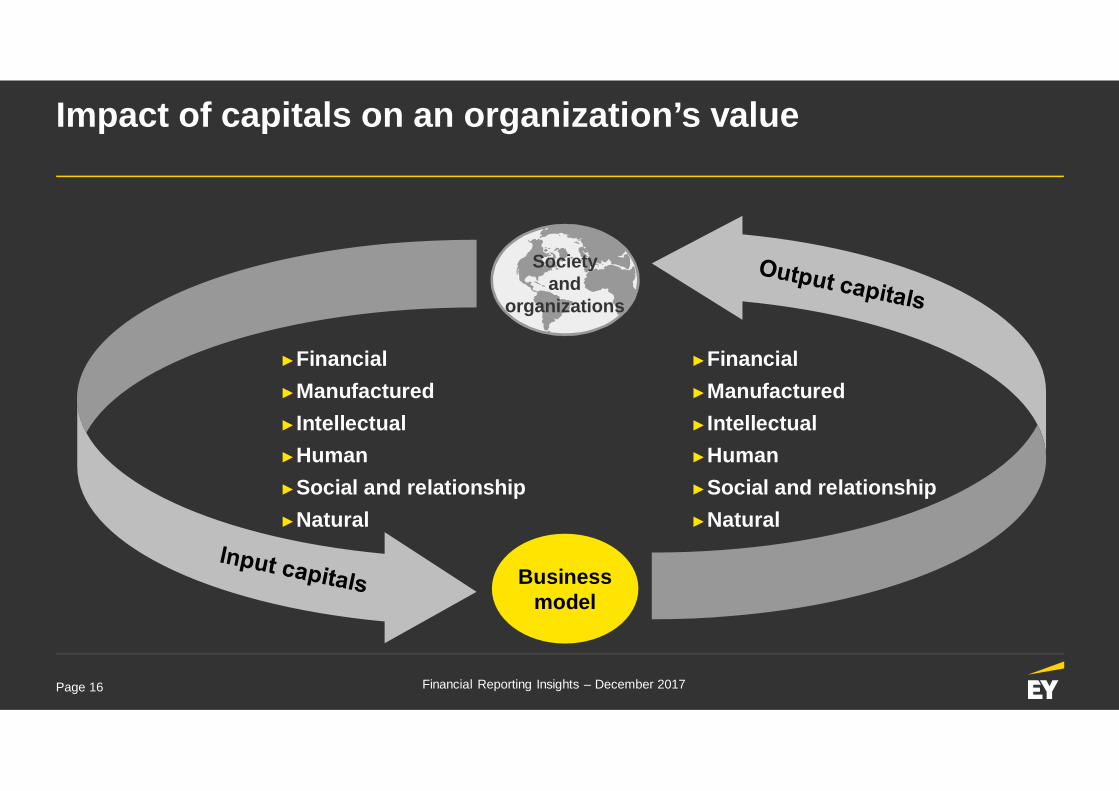

► Integrated reporting is based on two fundamental and interconnectedconcepts: value creation and the capitals.

► Value creation emphasises value is not created by or within theorganisation alone, but is influenced by the external environment, theorganisation’s relationships with others, and the resources used and affected.

► Value creation can best be understood as the change in value of thecapitals over time.

► The concept of capitals seeks to assist an organisation in identifying all theresources and relationships it uses and affects to report in a comprehensivemanner.

Integrated Reporting

Financial Reporting Insights – December 2017

Page 16

Impact of capitals on an organization’s value

►Financial►Manufactured►Intellectual►Human►Social and relationship►Natural

►Financial►Manufactured►Intellectual►Human►Social and relationship►Natural

Businessmodel

Societyand

organizations

Financial Reporting Insights – December 2017

Page 17

The goalis not to provide more information,but better information.

Financial Reporting Insights – December 2017

Page 18

Need to disclose information on:

► environmental matters,► social and employee-related aspects,► respect for human rights,► anti-corruption and bribery issues, and► supply chain.

New EU Directive on non-financial reporting (Law 4403/2016)

Comply or Explain

Financial Reporting Insights – December 2017

Regarding their:

► Business model► Policies and due diligence► Outcomes► Principal risks and their management► KPIs

Page 19 Financial Reporting Insights – December 2017

Law 4403/2016: “heavy” non-financial reporting

According to the provisions of Law 2190/20, as amended by the provisions ofLaw 4403/2016:

Mandatory Mandatory Mandatory Mandatory

Report with non-financial

information(incorporated in

Directors’ Report)

Public InterestEntities>500

employees

FinancialInstitutions >

500employees

Insurance andRe-insurance

companies >500employees

Subsidiaries ofcompanies that are

characterized asPublic InterestEntities in the

country of origin

Page 20 Financial Reporting Insights – December 2017

Law 4403/2016: “light” non-financial reporting

According to the provisions of Law 2190/20, as amended by the provisions ofLaw 4403/2016:

Mandatory Mandatory Mandatory

Directors’ report Large entities and largegroups

Medium entities andmedium groups

Small entities andsmall groups

Total Assets > 20.000.000 4.000.000 - 19.999.999 350.000 - 3.999.999

Net Turnover > 40.000.000 8.000.000 - 39.999.999 700.000 - 7.999.999

Average number ofemployees > 250 50 - 249 10 - 49

Page 21

► Actual and potential impacts of the entity on theenvironment

► Disclosure of procedures applied by the entity forthe prevention and control of pollution andenvironmental impacts of factors such as: energyuse, direct and indirect use of air pollutants,protection of biodiversity and water resources,waste management, environmental impacts fromtransport or use and disposal of products andservices

► Reference to the development of green productsand services, if they exist.

► Diversity and equal opportunities policy(irrespective of gender, religion, disability or otheraspects)

► Respect for employees’ rights and their rights toparticipate in trade unions

► Health and safety at work, training systems,promotion policy.

Environmental issues Labor issues

Law 4403/2016: “light” non-financial reporting

Page 22 Financial Reporting Insights – December 2017

Page 23

The Embankment Project for Inclusive Capitalism

► Marked withering of public trust in business

► A significant debate has begun about how toimprove capitalism so that it creates long-term value that sustains human endeavorwithout harming the stakeholders andbroader environment

► There is now solid academic research toshow that companies that follow inclusiveand sustainable standards perform better fortheir shareholders than those that do not.

► It is not just about Corporate SocialResponsibility

► It is about encouraging businesses to makechanges and expand their investment andmanagement practices to regain public trust.

The problem The actions

Financial Reporting Insights – December 2017

Page 24

The Embankment Project for Inclusive Capitalism

The contribution

Financial Reporting Insights – December 2017

► The proposed framework would become atool for asset owners and asset managersbut also other stakeholders to understand,measure and compare the investmentsmade by asset creators in their purpose,brand, intellectual property, products,employees, environment and communities.

► EY has developed a proof-of-conceptframework that will be tested and furtherdeveloped by some of the world’s largestasset owners, asset managers, and assetcreators (corporations).

► Aetna, DuPont, Johnson & Johnson, Nestlé,PepsiCo, Unilever.

Page 25

Regulatory Update

Financial Reporting Insights – December 2017

Page 26 Financial Reporting Insights – December 2017

ESMA1 SEC2

New standards adoption and disclosures (revenue, leases, financial instruments) ü ü

Acquisitions and business combinations ü ü

Reporting non-financial information ü ü

Entity-specific disclosures ü ü

Fair value measurements and disclosures ü ü

Alternative Performance Measures (APMs) / Non-GAAP measures ü ü

Specific issues of IAS 7 Statement of Cash Flows. ü

Brexit: Assessment and disclosure of the associated risks and expected impacts on businessstrategy and activities

ü

Segment reporting ü

Income taxes ü

Commitments and contingencies ü

1 Source: European common enforcement priorities for 2017 IFRS financial statements2 Source: Comment letter topics for SEC FYE 30 June 2016

Common enforcement priorities

Page 27 Financial Reporting Insights – December 2017

1 Source: ESMA, https://www.esma.europa.eu/sites/default/files/library/esma32-63-340_esma_european_common_enforcement_priorities_2017.pdf

Common enforcement prioritiesNew standards adoption and disclosures

Expecteddisclosures1 Accounting policy choices including those relating to transition approach

and use of practical expedients

Amount and nature of the expected impacts compared to previouslyrecognized amounts.

Concise entity-specific quantitative and qualitative description of thechanges introduced by the new standards

Issuers should not merely repeat the requirements of the standards andavoid the risk of overloading financial statements with boilerplatedisclosures that do not fulfil the objective.

Page 28 Financial Reporting Insights – December 2017

Source:

Disclosure effectiveness

Page 29 Financial Reporting Insights – December 2017

Disclosure effectiveness

Key benefits,reactions andchallenges“Our focus whenpreparing thefinancials is to ensurethat our disclosuresare linked to ourbusiness strategy andwe have givenrelevant informationpresented and writtenin a way that all ourstakeholders caneasily understand.”ITV plc

The process

“The journeytowards improvingcommunication ofinformation in thefinancial statementsstarts fromidentifying easywins. Taking thatfirst step is the mostimportant activity inthis process.”Pandora A/S

Triggers of change

“Our directors feltthat time thefinancial reportingprocess wascompliance-drivenand burdensome. Itwas time werefocused theattention oncommunicating ourstory.”Wesfarmers Limited

Areas of successand lessons learnt“The mostchallenging bit ofthe process wasactually gettingstarted. Once thatwas done, havingseniormanagement’ssupport and theright people in theroom were then keyingredients forsuccess.”Fonterra Co-operative GroupLimited

A change towardsgreatertransparency

“We hope toachieve greatertransparencythrough linking theaccounting to theway we do businessin real life.”Orange SA

1 Source: IFRS Foundation Disclosure Initiative—Case Studies (http://www.ifrs.org/news-and-events/2017/10/ifrs-foundation-publishes-a-case-study-report-on-better-communication/)

Page 30

New role of the Audit Committee

Financial Reporting Insights – December 2017

Page 31

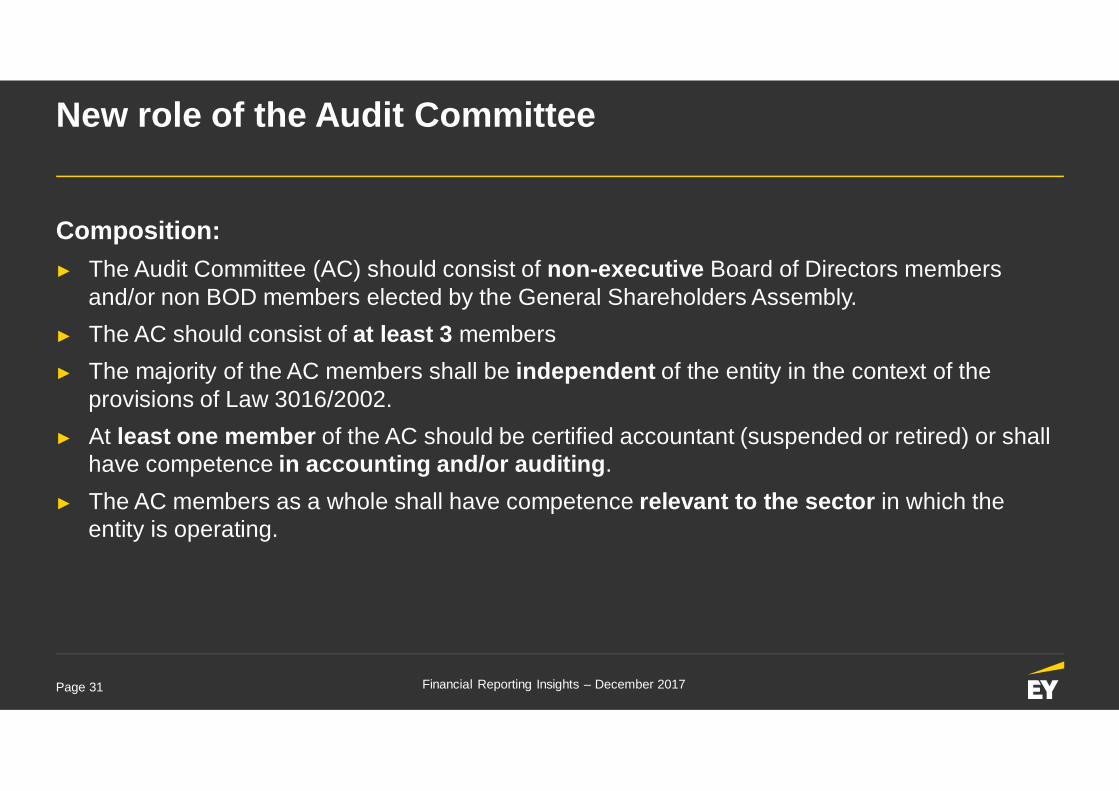

New role of the Audit Committee

Composition:► The Audit Committee (AC) should consist of non-executive Board of Directors members

and/or non BOD members elected by the General Shareholders Assembly.► The AC should consist of at least 3 members► The majority of the AC members shall be independent of the entity in the context of the

provisions of Law 3016/2002.► At least one member of the AC should be certified accountant (suspended or retired) or shall

have competence in accounting and/or auditing.► The AC members as a whole shall have competence relevant to the sector in which the

entity is operating.

Financial Reporting Insights – December 2017

Page 32

New role of the Audit Committee

Financial Reporting Insights – December 2017

Supervision:► The Hellenic Capital Markets Commission (HCMC) supervises the AC compliance as set out

in paragraph 4 of Law 4449/2017. In case of infringements detected the HCMC may imposeto the audit committee members the penalties provided for in Article 10 of law 3016/2002.

► HCMC has made recommendations/interpretations regarding the actions expected to becarried out by the audit committees (No. 1302/28/04/2017). HCMC requests companies to actimmediately on the following:

► Reassess the composition of existing ACs and alter in order to comply with Regulation► Reassess the responsibilities of ACs taking into consideration Art 44 of Law 4449/2017► Develop an AC Charter, that includes description of composition, roles, responsibilities and assessment of

effectiveness of AC► Ensure that ACs have direct and full access to information needed in order to execute their role and has

adequate resources► Maintenance of records, including minutes of meetings, that reflect the actions and results► Update BoD on AC matters and conclusions► AC Chair to update shareholders during annual AGM

Page 33

Responsibilities of the Audit Committee

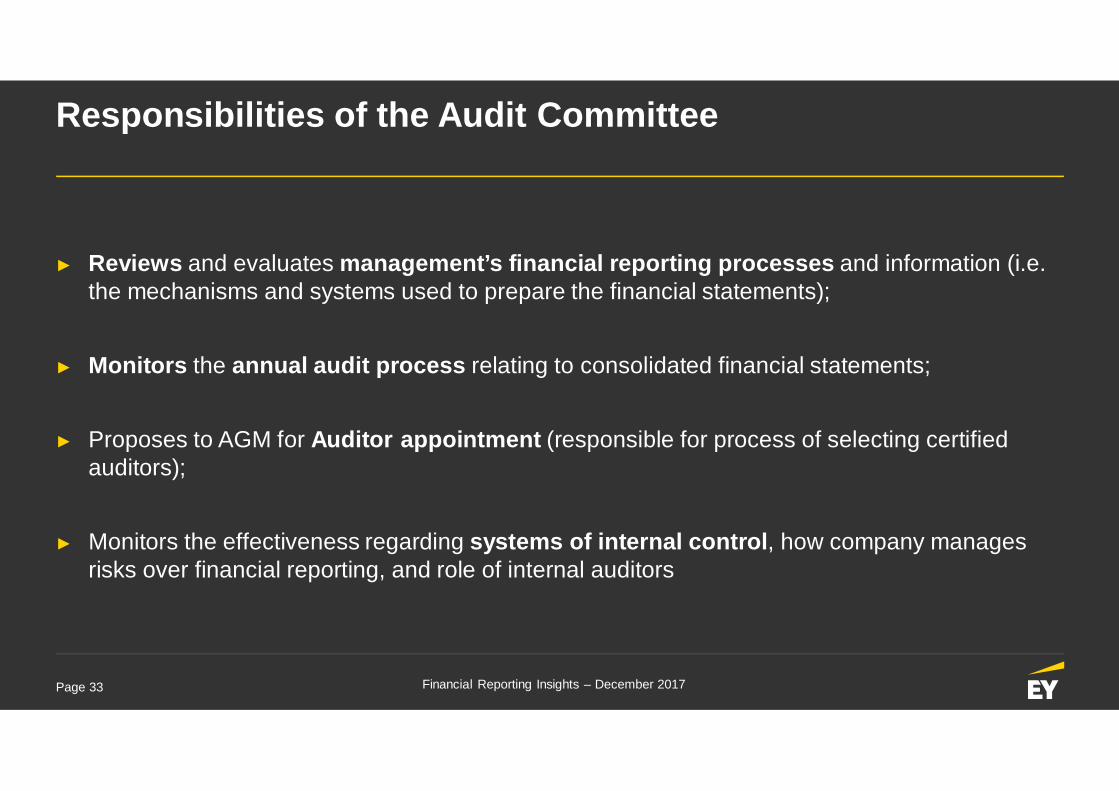

► Reviews and evaluates management’s financial reporting processes and information (i.e.the mechanisms and systems used to prepare the financial statements);

► Monitors the annual audit process relating to consolidated financial statements;

► Proposes to AGM for Auditor appointment (responsible for process of selecting certifiedauditors);

► Monitors the effectiveness regarding systems of internal control, how company managesrisks over financial reporting, and role of internal auditors

Financial Reporting Insights – December 2017

Page 34

Additional Report to the Audit Committee

The Auditors of Public Interest Entities submit an additional report to the Audit Committee, thelatest by the audit report date. This report among others should state:

► Extent, timing, methodology and materiality levels used in audit process► Accounts on which the Auditor performed test of controls► The audit materiality level► Events and conditions that indicate the existence of a material uncertainty about the going

concern assumption of the company► Possible inadequacies in the internal control systems of the company► Significant errors and/or omissions and other significant audit matters Accounts on which the

Auditor executed substantive audit procedures► Independence confirmation and identification of key audit partners

Financial Reporting Insights – December 2017

Page 35

Key Audit Matters – the Game Changer

Financial Reporting Insights – December 2017

Page 36

“GreaterTransparency intothe FinancialStatement Audit.”

Drivers for change in auditor reporting

Global financial crisisprompted desire for moreinformation

Essential to the continuedrelevance of the audit

Change is occurringglobally

► “Pass/fail” opinion valued, but auditor’s report could bemore informative according to investors and otherstakeholders

► It is time for a new foundation in auditor reporting

► UK auditor’s reports – 2013► NL auditor’s reports – 2014► International Standards on Auditing – 2016 (some countries

2017+)► EU Audit regulation – 2017► US PCAOB – New standards in 2017

Financial Reporting Insights – December 2017

Page 37

KAM: Decision-making framework

KAM:Mattersof most

significancein the audit

Matters communicatedwith TCWG

Matters requiringsignificant auditor

attention

Always consider:► Higher assessed risks and

significant risks► Areas of significant management

judgment and estimationuncertainty

► Significant transactions or events

Description of each KAM in theauditor’s report required to include:► Why the matter was considered to

be one of most significance in theaudit

► How the matter was addressed inthe audit

► Reference to the relateddisclosure(s)

Financial Reporting Insights – December 2017

Page 38

The revised auditor’s report

INDEPENDENT AUDITOR’S REPORT

Report on the Audit of the Financial Statements

Opinion

Basis for Opinion

Key Audit MattersKey audit matters are those matters that, in our professional judgment, were of most significance in the audit of the financial statements ofthe current period. These matters were addressed in the context of the audit of the financial statements as a whole, and in forming theauditor’s opinion thereon, and we do not provide a separate opinion on these matters. For each matter below, our description of howour audit addressed the matter is provided in that context.

Financial Reporting Insights – December 2017

Page 39

The revised auditor’s report

Goodwill[Why a matter was determined to be a KAM]Under IFRS the Group is required to annually test the amount of goodwill for impairment. This annual impairment test was significant to ouraudit because the balance of XX as of 31 December 20X6 is material to the financial statements. In addition, management’s assessmentprocess is complex and highly judgmental and is based on assumptions, specifically [describe certain assumptions], which are affected byexpected future market or economic conditions, particularly those in [name of country or geographic area].

[How a KAM was addressed in the audit]Our audit procedures included, among others, using a valuation expert to assist us in evaluating the assumptions and methodologies used bythe Group, in particular those relating to the forecasted revenue growth and profit margins for [name of business line]. We also focused on theadequacy of the Group’s disclosures about those assumptions to which the outcome of the impairment test is most sensitive, that is, thosethat have the most significant effect on the determination of the recoverable amount of goodwill.

[Refer to the related disclosures]The Company’s disclosures about goodwill are included in Note X, which specifically explains that small changes in the key assumptionsused could give rise to an impairment of the goodwill balance in the future.

Financial Reporting Insights – December 2017

Page 40

The revised auditor’s report

Revenue Recognition[Why a matter was determined to be a KAM]The amount of revenue and profit recognized in the year on the sale of [name of product] and aftermarket services is dependent on theappropriate assessment of whether or not each long-term aftermarket contract for services is linked to or separate from the contract for saleof [name of product]. As the commercial arrangements can be complex, significant judgment is applied in selecting the accounting basis ineach case. In our view, revenue recognition is significant to our audit as the Group might inappropriately account for sales of [name ofproduct] and long-term service agreements as a single arrangement for accounting purposes and this would usually lead to revenue andprofit being recognized too early because the margin in the long-term service agreement is usually higher than the margin in the [name ofproduct] sale agreement.

[How a KAM was addressed in the audit]Our audit procedures to address the risk of material misstatement relating to revenue recognition, which was considered to be a significantrisk, included:► Testing of controls, assisted by our own IT specialists, including, among others, those over: input of individual advertising campaigns’

terms and pricing; comparison of those terms and pricing data against the related overarching contracts with advertising agencies; andlinkage to viewer data; and

► Detailed analysis of revenue and the timing of its recognition based on expectations derived from our industry knowledge and externalmarket data, following up variances from our expectations.

[Refer to the related disclosures]The Company’s disclosures on revenue recognition are included in Note X.

Financial Reporting Insights – December 2017

Page 41

The revised auditor’s report

Other information included in The Company’s 20X6 Annual ReportOther information consists of the information included in the Annual Report, other than the financial statements and our auditor’s reportthereon. Management is responsible for the other information. Our opinion on the financial statements does not cover the other informationand we do not express any form of assurance conclusion thereon. In connection with our audit of the financial statements, our responsibility isto read the other information and, in doing so, consider whether the other information is materially inconsistent with the financial statements orour knowledge obtained in the audit or otherwise appears to be materially misstated. If, based on the work we have performed, we concludethat there is a material misstatement of this other information, we are required to report that fact. We have nothing to report in this regard.

Responsibilities of Management and Directors for the Financial Statements

Auditor’s Responsibilities for the Audit of the Financial Statements

Report on other legal and regulatory requirements

Financial Reporting Insights – December 2017

Page 42

The UK experiences - Which KAM are reported?

Financial Reporting Insights – December 2017

Page 43

Benefits- Challenges of the new auditor’s report

q Enhanced valueq Overall improvement of key deliverable of auditq Greater transparency of the audit and its resultsq Including information about areas of auditor

focus in the auditor’s report expected to:q Increase audit quality due to increased auditor

focus on matters to be reportedq Enhance financial statement disclosures due to

increased focus by management and TCWG onmatters to be reported

q Enhance communications between the auditorand TCWG

Financial Reporting Insights – December 2017

ChallengesBenefits

q Additional time required from senior audit teammembers, management and TCWG (determiningand drafting key audit matters)

q Drafting the auditor’s report needs to happenearlier in the process to allow adequate time forreview

q Considering these changes in discussionsbetween auditors, management and thosecharged with governance

q Determining scope, timing and extent ofprocedures around other information

Coffee break!

4th Annual Financial Reporting Insights

Page 45

Revenue recognition – practical considerations

Financial Reporting Insights – December 2017

Page 46 Financial Reporting Insights – December 2017

Revenue from contracts with customersFive step model

Step 02Identify the performance

obligations in the contract

Step 01Identify the contract(s) with the customer

Core principle:Recognise revenue to depict the transfer of promised goods or services to customers in an amount thatreflects the consideration to which the entity expects to be entitled in exchange for those goods orservices.

Step 05Recognise revenue when (or as)each performance obligation issatisfied

Step 04Allocate the transaction price

to the performance obligations

Step 03Determine the transaction price

Page 47

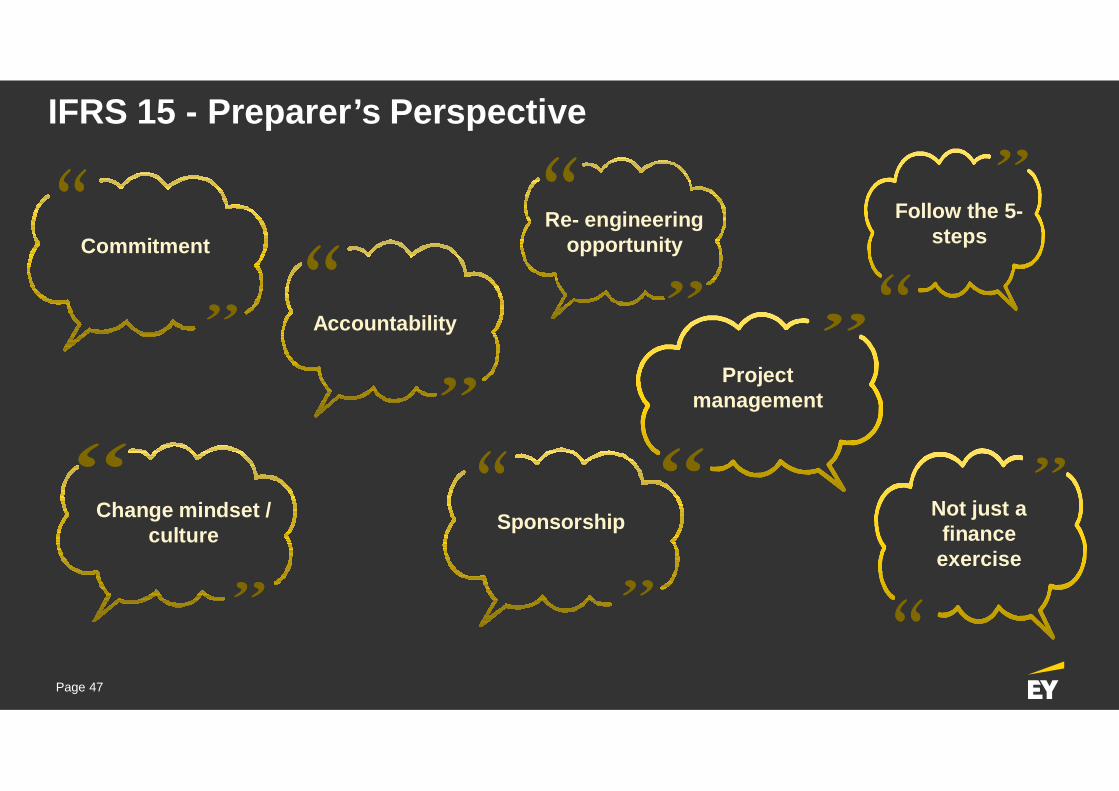

Change mindset /culture

Not just afinanceexercise

Commitment

Accountability

Sponsorship

Follow the 5-steps

Projectmanagement

Re- engineeringopportunity

IFRS 15 - Preparer’s Perspective

>> 0 >> 1 >> 2 >> 3 >> 4 >>

…18 days before theeffective date

IFRS 15 / ASC 606…what to do now?

Page 49

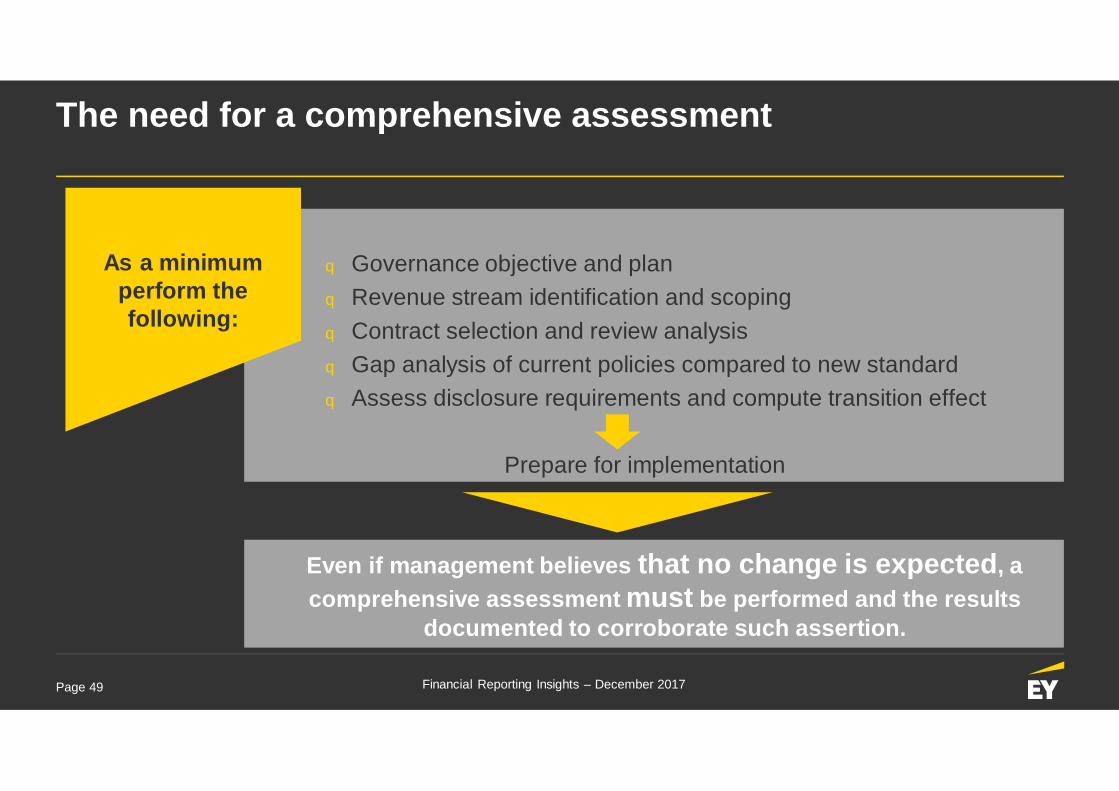

q Governance objective and planq Revenue stream identification and scopingq Contract selection and review analysisq Gap analysis of current policies compared to new standardq Assess disclosure requirements and compute transition effect

Prepare for implementation

The need for a comprehensive assessment

Financial Reporting Insights – December 2017

As a minimumperform thefollowing:

Even if management believes that no change is expected, acomprehensive assessment must be performed and the results

documented to corroborate such assertion.

Page 50

Comprehensive assessment1. Governance objective and plan

Financial Reporting Insights – December 2017

Purpose

Key Management tasks

Output

q Project sponsor is competent and has theproper decision making authority

q Project team is diversifiedq Familiarize project team with the 5-step

approach

Set up project team, aroadmap andchange managementstrategy

Defined project plan:qProject work streamsqKey stakeholdersqTimeline and key

milestonesqAnticipated work

products

Lessons learned:q Formulate your project team including all appropriate stakeholders across the organizationq Involve the right people and departments to better understand revenue streams and contract terms

Page 51

Comprehensive assessment2. Revenue stream identification and scoping

Financial Reporting Insights – December 2017

Purpose

Key Management tasks

Output

qDevelop process for verifying thecompleteness of all revenue contractsqDevelop an approach to identify significant

revenue streamsqDevelop an approach to identify specific

contracts to analyze within each revenuestream

Lessons learned:q One-size fits all approach is not effective. Tailor in entity’s specific facts and circumstancesq Successful scoping when the auditor participates in the brainstormingq Re-evaluate scoping based on knowledge acquired from contract review analysis step

Verify the population ofcontracts is complete;Stratify the population intogroups expected to havesame or similar accountingbased on terms.

Memo to include:qSignificant revenue

streamsqSampling approachqHigh level accounting

issues for each stream

Page 52

Comprehensive assessment3. Contract selection and review analysis

Financial Reporting Insights – December 2017

Purpose

Key Management tasks

Output

Evaluate terms of therepresentative contractsvs the five-step model

qDetermine the impact of the standard onrevenue for a contract or the revenue streamrepresented by that contractqDetermine the assumptions, judgements and

estimates requiredqValidate the assumptions made within the

revenue stream scoping step and updatepreliminary decisions

Contract analysismemo:Will form the outlineof the accountingposition papers

Lessons learned:q Need for a robust documentation to support initial assessmentsq Detailed documentation as evidence of management's review process and conclusionsq Clear documentation on areas of the standard not applicable to the contract

Page 53

Comprehensive assessmentContract selection and review analysis-Practice tool: Contract analysis enabler

Financial Reporting Insights – December 2017

Page 54

Comprehensive assessment4. Gap analysis of current policies compared to new standard

Financial Reporting Insights – December 2017

Purpose

Key Management tasks

Output

q Develop expectations of changes incurrent accounting policies and practices.

q Evaluate the degree of changes andaddress the differences between currentand future states

q Identify accounting areas requiring furtherinvestigation

Gap analysis report:q Preliminary impact from

contract analysis andsummary of expecteddifferences

q Heat map of the mostsignificant issuesanticipated to impact

Lessons learned:q Gap analysis should not be limited to financial-related topics.q For areas without a significant change, management should document its conclusions.

Identify the mostsignificant areasexpected to change bykey revenue stream

Page 55

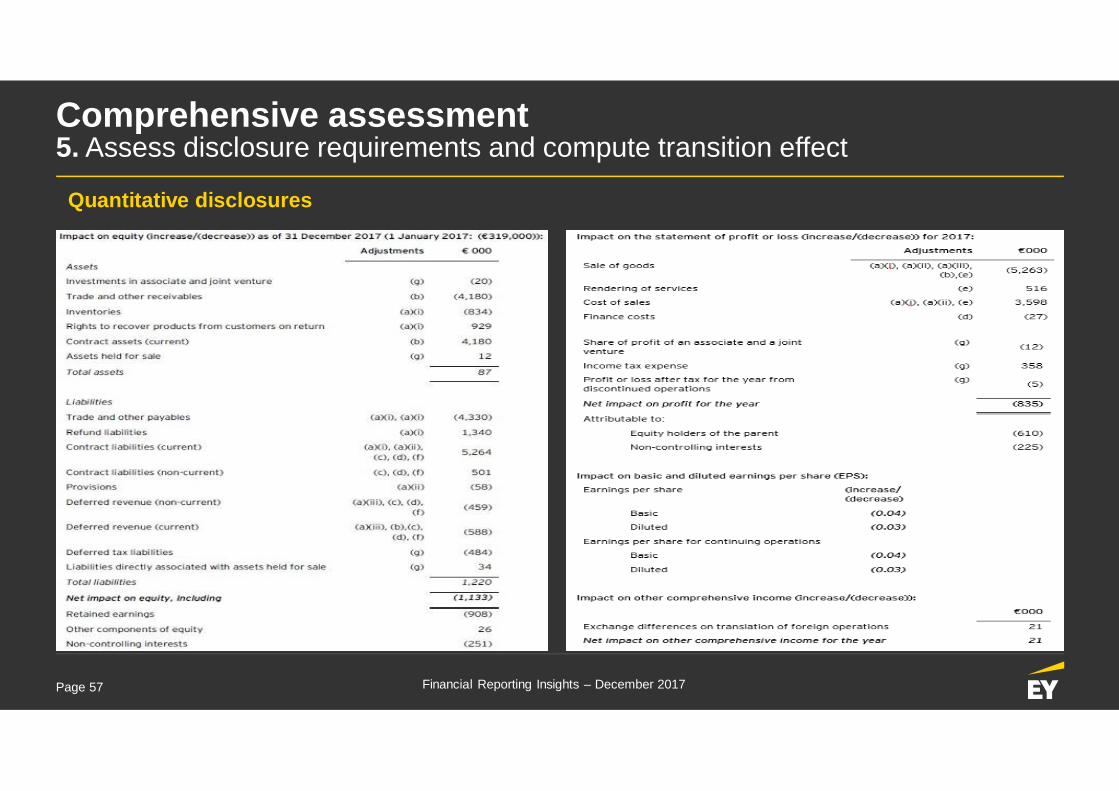

Comprehensive assessment5. Assess disclosure requirements and compute transition effect (cont’d)

Financial Reporting Insights – December 2017

Purpose

Key Management tasks

Output

Form preliminary viewon how disclosures willchangeAssess level of effortneeded for transitiondisclosures in 2017 FS

q Compute transition effect – decision orworking assumption

q Understand disclosure requirements underthe new standard and how they differ fromcurrent requirements

Disclosures:q Transition Disclosures

in 2017 FSq Additional disclosure

requirements for the2018 FS

Lessons learned:q Companies draft a footnote (disclosure checklist) to assist in understanding the qualitative and

quantitative disclosures required and identifying applicable sources of infoq New disclosure requirements have been underestimated. All companies will need to provide additional

disclosures

Page 56

Comprehensive assessment5. Assess disclosure requirements and compute transition effect (cont’d)

Financial Reporting Insights – December 2017

Qualitative disclosuresGood Group suggests considerations analysis per significant revenue stream

q Description of the performance obligationsq Description of significant judgements and estimatesq Areas expected to be impacted by the new standard vs

current accounting treatmentsq Presentation and disclosure requirementsq Other adjustments

Page 57

Comprehensive assessment5. Assess disclosure requirements and compute transition effect

Financial Reporting Insights – December 2017

Quantitative disclosures

Page 58

Example disclosures

Financial Reporting Insights – December 2017

Page 59

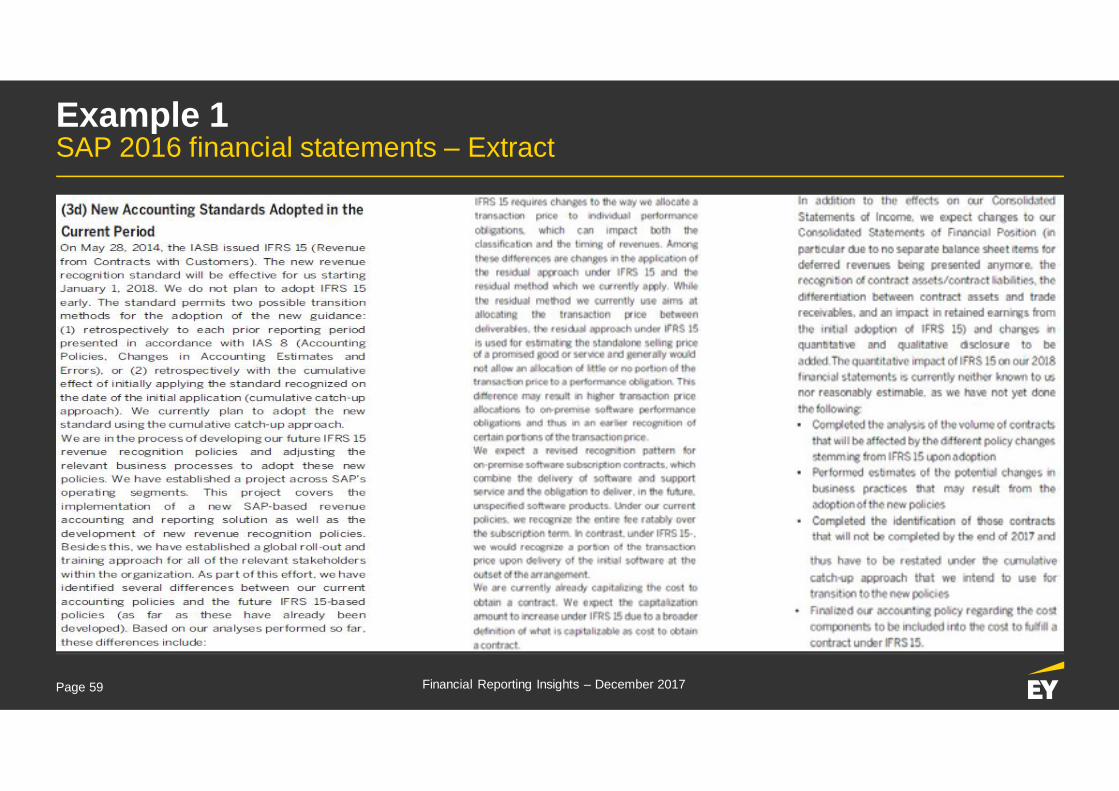

Example 1SAP 2016 financial statements – Extract

(…)

Financial Reporting Insights – December 2017

Page 60

Example 2Royal Philips 2016 financial statements – Extract

Financial Reporting Insights – December 2017

Page 61

Example 3Rolls-Royce 2016 financial statements – Extract

Financial Reporting Insights – December 2017

Page 62

Example 3Rolls-Royce 2016 financial statements – Extract (cont.)

Financial Reporting Insights – December 2017

Page 63

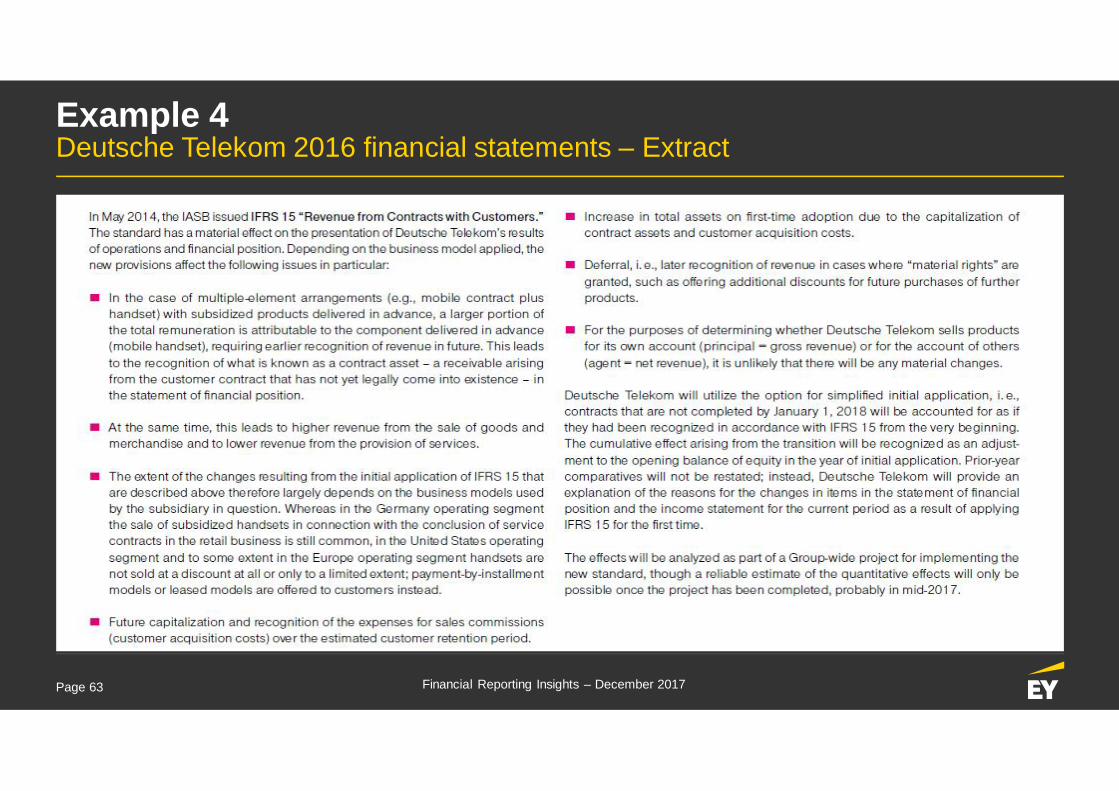

Example 4Deutsche Telekom 2016 financial statements – Extract

Financial Reporting Insights – December 2017

Page 64

Example 5 and 6BMW and Nestlé 2016 financial statements – Extracts

Financial Reporting Insights – December 2017

Page 65 Financial Reporting Insights – December 2017

High complexity

Low Volume

High complexity

High Volume

Low complexity

Low Volume

Low complexity

High Volume

A B

DC

Revenue from contracts with customersWhich category describes you best?

Page 66

A comment on the new standard projects generally

Financial Reporting Insights – December 2017

Expectation

q Accounting issues can be solved quickly

q Nothing can move until accounting isresolved

q It can all be done in finance head office

q No need to read contracts

q No issues in the business

q Need an accountant to run the project

Reality

q They can take time, so get the auditors onboard asap

q Often the IT / manual solution can be flexed

q Must involve other departments (e.g. business)

q Must read contracts

q Unexpected issues can arise in the business

q PM skills are equally important

Questions?

Lunch break!

4th Annual Financial Reporting Insights

EY | Assurance | Tax | Transactions | Advisory

About EYEY is a global leader in assurance, tax, transaction and advisory services.The insights and quality services we deliver help build trust and confidencein the capital markets and in economies the world over. We developoutstanding leaders who team to deliver on our promises to all of ourstakeholders. In so doing, we play a critical role in building a better workingworld for our people, for our clients and for our communities.

EY refers to the global organization, and may refer to one or more, of themember firms of Ernst & Young Global Limited, each of which is a separatelegal entity. Ernst & Young Global Limited, a UK company limited byguarantee, does not provide services to clients. For more information aboutour organization, please visit ey.com.

About EY’s Assurance ServicesOur assurance services help our clients meet their reporting requirements byproviding an objective and independent examination of the financialstatements that are provided to investors and other stakeholders.Throughout the audit process, our teams provide a timely and constructivechallenge to management on accounting and reporting matters and a robustand clear perspective to audit committees charged with oversight. Thequality of our audits starts with our 60,000 assurance professionals, whohave the breadth of experience and ongoing professional development thatcome from auditing many of the world’s leading companies. For every client,we assemble the right multidisciplinary team with the sector knowledge andsubject matter knowledge to address your specific issues. All teams use ourGlobal Audit Methodology and latest audit tools to deliver consistent auditsworldwide.

© 2015 EYAll Rights Reserved.