can hedge-fund returns be replicated?: the...

TRANSCRIPT

JOIMwww.joim.com

JOURNAL OF INVESTMENT MANAGEMENT, Vol. 5, No. 2, (2007), pp. 5–45

© JOIM 2007

CAN HEDGE-FUND RETURNS BE REPLICATED?: THE LINEAR CASE�

Jasmina Hasanhodzica and Andrew W. Lob,∗

In contrast to traditional investments such as stocks and bonds, hedge-fund returns havemore complex risk exposures that yield additional and complementary sources of risk premia.This raises the possibility of creating passive replicating portfolios or “clones” using liquidexchange-traded instruments that provide similar risk exposures at lower cost and withgreater transparency. By using monthly returns data for 1610 hedge funds in the TASSdatabase from 1986 to 2005, we estimate linear factor models for individual hedge fundsusing six common factors, and measure the proportion of the funds’ expected returns andvolatility that are attributable to such factors. For certain hedge-fund style categories, wefind that a significant fraction of both can be captured by common factors corresponding toliquid exchange-traded instruments. While the performance of linear clones is often inferiorto their hedge-fund counterparts, they perform well enough to warrant serious considerationas passive, transparent, scalable, and lower-cost alternatives to hedge funds.

�The views and opinions expressed in this paper are those ofthe authors only, and do not necessarily represent the viewsand opinions of AlphaSimplex Group, MIT, or any of theiraffiliates and employees. The authors make no representationsor warranty, either expressed or implied, as to the accuracy orcompleteness of the information contained in this paper, norare they recommending that this paper can serve as the basisfor any investment decision—this paper is for informationpurposes only.aDepartment of Electrical Engineering and Computer Sci-ence; Laboratory for Financial Engineering, MIT, Cambridge,MA, USAbSloan School of Management; Laboratory for Financial Engi-neering, MIT, Cambridge, MA, USA and AlphaSimplexGroup, LLC

1 Introduction

As institutional investors take a more active inter-est in alternative investments, a significant gap hasemerged between the culture and expectations ofthose investors and hedge-fund managers. Pensionplan sponsors typically require transparency fromtheir managers and impose a number of restrictionsin their investment mandates because of regula-tory requirements such as ERISA rules; hedge-fundmanagers rarely provide position-level transparency

∗Corresponding author. MIT Sloan School, 50 Memo-rial Derive, E52–454, Cambridge 02142–1347, MA, USA.E-mail: [email protected]

SECOND QUARTER 2007 5

6 JASMINA HASANHODZIC AND ANDREW W. LO

and bristle at any restrictions on their investmentprocess because restrictions often hurt performance.Plan sponsors require a certain degree of liquidityin their assets to meet their pension obligations,and also desire significant capacity because of theirlimited resources in managing large pools of assets;hedge-fund managers routinely impose lock-ups of1–3 years, and the most successful managers havethe least capacity to offer, in many cases return-ing investors’ capital once they make their personalfortunes. And as fiduciaries, plan sponsors arehypersensitive to the outsize fees that hedge fundscharge, and are concerned about misaligned incen-tives induced by performance fees; hedge-fundmanagers argue that their fees are fair compensa-tion for their unique investment acumen, and atleast for now, the market seems to agree.

This cultural gap raises the natural question ofwhether it is possible to obtain hedge-fund-likereturns without investing in hedge funds. In short,can hedge-fund returns be “cloned”?

In this paper, we provide one answer to thischallenge by constructing “linear clones” of indi-vidual hedge funds in the TASS Hedge FundDatabase. These are passive portfolios of com-mon risk factors like the S&P 500 and theUS Dollar Indexes, with portfolio weights esti-mated by regressing individual hedge-fund returnson the risk factors. If a hedge fund generates partof its expected return and risk profile from certaincommon risk factors, then it may be possible todesign a low-cost passive portfolio—not an activedynamic trading strategy—that captures some ofthat fund’s risk/reward characteristics by taking onjust those risk exposures. For example, if a particularlong/short equity hedge fund is 40% long growthstocks, it may be possible to create a passive port-folio that has similar characteristics, for example,a long-only position in a passive growth portfoliocoupled with a 60% short position in stock-indexfutures.

The magnitude of hedge-fund alpha that can becaptured by a linear clone depends, of course, onhow much of a fund’s expected return is drivenby common risk factors versus manager-specificalpha. This can be measured empirically. Whileportable alpha strategies have become fashionablelately among institutions, our research suggeststhat for certain classes of hedge-fund strategies,portable beta may be an even more importantsource of untapped expected returns and diversifi-cation. In particular, in contrast to previous studiesemploying more complex factor-based models ofhedge-fund returns, we use six factors that corre-spond to basic sources of risk and, consequently,expected return: the stock market, the bond mar-ket, currencies, commodities, credit, and volatility.These factors are also chosen because, with theexception of volatility, each of them is tradable vialiquid exchange-traded securities such as futures orforward contracts.

Using standard regression analysis we decomposethe expected returns of a sample of 1610 indi-vidual hedge funds from the TASS Hedge FundLive Database into factor-based risk premia andmanager-specific alpha, and we find that for certainhedge-fund style categories, a significant fraction ofthe funds’ expected returns is due to risk premia.For example, in the category of Convertible Arbi-trage funds, the average percentage contribution ofthe US Dollar Index risk premium, averaged acrossall funds in this category, is 67%. While estimatesof manager-specific alpha are also quite significantin most cases, these results suggest that at least aportion of a hedge fund’s expected return can beobtained by bearing factor risks.

To explore this possibility, we construct linear clonesusing five of the six factors (we omit volatilitybecause the market for volatility swaps and futuresis still developing), and compare their performanceto the original funds. For certain categories such asEquity Market Neutral, Global Macro, Long/Short

JOURNAL OF INVESTMENT MANAGEMENT SECOND QUARTER 2007

REPLICATING HEDGE-FUND RETURNS 7

Equity Hedge, Managed Futures, Multi-Strategy,and Fund of Funds, linear clones have comparableperformance to their fund counterparts, but forother categories such as Event Driven and Emerg-ing Markets, clones do not perform nearly as well.However, in all cases, linear clones are more liquid(as measured by their serial correlation coefficients),more transparent and scalable (by construction),and with correlations to a broad array of marketindexes that are similar to those of the hedge fundson which they are based. For these reasons, weconclude that hedge-fund replication, at least forcertain types of funds, is both possible and, in somecases, worthy of serious consideration.

We begin in Section 2 with a brief review of theliterature on hedge-fund replication, and providetwo examples that motivate this endeavor. In Sec-tion 3, we present a linear regression analysis ofhedge-fund returns from the TASS Hedge FundLive Database, with which we decompose the funds’expected returns into risk premia and manager-specific alpha. These results suggest that for certainhedge-fund styles, linear clones may yield reason-ably compelling investment performance, and weexplore this possibility directly in Section 4. Weconclude in Section 5.

2 Motivation

In a series of recent papers, Kat and Palaro(2005, 2006a,b) argued that sophisticated dynamictrading strategies involving liquid futures con-tracts can replicate many of the statistical prop-erties of hedge-fund returns. More generally,Bertsimas et al. (2001) have shown that securi-ties with very general payoff functions (like hedgefunds, or complex derivatives) can be syntheti-cally replicated to an arbitrary degree of accuracyby dynamic trading strategies—called “epsilon-arbitrage” strategies—involving more liquid instru-ments. While these results are encouraging for the

hedge-fund replication problem, the replicatingstrategies are quite involved and not easily imple-mented by the typical institutional investor. Indeed,some of the derivatives-based replication strategiesmay be more complex than the hedge-fund strate-gies they intend to replicate, defeating the verypurpose of replication.1

The motivation for our study comes, instead, fromSharpe’s (1992) asset-class factor models in which heproposes to decompose a mutual fund’s return intotwo distinct components: asset-class factors such aslarge-cap stocks, growth stocks, and intermediategovernment bonds, which he interprets as “style,”and an uncorrelated residual that he interprets as“selection.” This approach was applied by Fung andHsieh (1997a) to hedge funds, but there the factorswere derived statistically from a principal compo-nents analysis of the covariance matrix of theirsample of 409 hedge funds and CTAs. While suchfactors may yield high in-sample R2s, they sufferfrom significant over-fitting bias and also lack eco-nomic interpretation, which is one of the primarymotivations for Sharpe’s (1992) decomposition.Several authors have estimated factor models forhedge funds using more easily interpretable factorssuch as fund characteristics and indexes (Schneeweisand Spurgin, 1998; Liang, 1999; Edwards andCaglayan, 2001; Capocci and Hubner, 2004; Hill,et al., 2004), and the returns to certain options-based strategies and other basic portfolios (Fungand Hsieh, 2001, 2004; Agarwal and Naik 2000a,b,2004).

However, the most direct application of Sharpe’s(1992) analysis to hedge funds is found in Ennis andSebastian (2003). They provide a thorough styleanalysis of the HFR Fund of Funds index, and con-clude that funds of funds are not market neutraland although they do exhibit some market-timingabilities, “…, the performance of hedge funds hasnot been good enough to warrant their inclusionin balanced portfolios. The high cost of investing

SECOND QUARTER 2007 JOURNAL OF INVESTMENT MANAGEMENT

8 JASMINA HASANHODZIC AND ANDREW W. LO

in funds of funds contributes to this result” (Ennisand Sebastian, 2003, p. 111). This conclusion is thestarting point for our study of linear clones.

Before turning to our empirical analysis of individ-ual hedge-fund returns, we provide two concreteexamples that span the extremes of the hedge-fundreplication problem. For one hedge-fund strategy,we show that replication can be accomplished eas-ily, and for another strategy, we find replication tobe almost impossible using linear models.

2.1 Capital Decimation Partners

The first example is a hypothetical strategy proposedby Lo (2001) called “Capital Decimation Partners”(CDP), which yields an enviable track record thatmany investors would associate with a successfulhedge fund: a 43.1% annualized mean return and20% annualized volatility, implying a Sharpe ratioof 2.15,2 and with only 6 negative months over the96-month simulation period from January 1992 toDecember 1999 (see Table 1). A closer inspection ofthis strategy’s monthly returns in Table 2 yields few

Table 1 Performance summary of simulatedshort-put-option strategy consisting of short-selling out-of-the-money S&P 500 put optionswith strikes approximately 7% out of the moneyand with maturities less than or equal to 3months, from January 1992 to December 1999.

Statistic S&P500 CDP

Monthly mean 1.4% 3.6%Monthly SD 3.6% 5.8%Minimum month −8.9% −18.3%Maximum month 14.0% 27.0%Annual Sharpe ratio 1.39 2.15# Negative months 36 6Correlation to S&P 500 100% 61%Return Since Inception 367% 2560%

surprises for the seasoned hedge-fund investor—themost challenging period for CDP was the summerof 1998 during the LTCM crisis, when the strategysuffered losses of −18.3% and −16.2% in Augustand September, respectively. But those investorscourageous enough to have maintained their CDPinvestment during this period were rewarded withreturns of 27.0% in October and 22.8% in Novem-ber. Overall, 1998 was the second-best year forCDP, with an annual return of 87.3%.

So what is CDP’s secret? The investment strategysummarized inTables 1 and 2 involves shorting out-of-the-money S&P 500 (SPX) put options on eachmonthly expiration date for maturities less thanor equal to 3 months, and with strikes approx-imately 7% out of the money. According to Lo(2001), the number of contracts sold each monthis determined by the combination of: (1) CBOEmargin requirements3; (2) an assumption that weare required to post 66% of the margin as collateral4;and (3) $10M of initial risk capital. The essenceof this strategy is the provision of insurance. CDPinvestors receive option premia for each option con-tract sold short, and as long as the option contractsexpire out of the money, no payments are necessary.Therefore, the only time CDP experiences lossesis when its put options are in the money, that is,when the S&P 500 declines by more than 7% dur-ing the life of a given option. From this perspective,the handsome returns to CDP investors seem morejustifiable—in exchange for providing downsideprotection, CDP investors are paid a risk premiumin the same way that insurance companies receiveregular payments for providing earthquake or hur-ricane insurance. Given the relatively infrequentnature of 7% losses, CDP’s risk/reward profile canseem very attractive in comparison to more tradi-tional investments, but there is nothing unusualor unique about CDP. Investors willing to takeon “tail risk”—the risk of rare but severe events—will be paid well for this service (consider howmuch individuals are willing to pay each month for

JOURNAL OF INVESTMENT MANAGEMENT SECOND QUARTER 2007

REPLICATING HEDGE-FUND RETURNS 9

Tab

le2

Mon

thly

retu

rns

ofsi

mul

ated

shor

t-pu

t-op

tion

stra

tegy

cons

isti

ngof

shor

tsel

ling

out-

of-t

he-m

oney

S&P

500

put

opti

ons

wit

hst

rike

sapp

roxi

mat

ely

7%ou

toft

hem

oney

and

wit

hm

atur

itie

sles

stha

nor

equa

lto

3m

onth

s,fr

omJa

nuar

y19

92to

Dec

embe

r19

99.

1992

1993

1994

1995

1996

1997

1998

1999

Mon

thSP

XC

DP

SPX

CD

PSP

XC

DP

SPX

CD

PSP

XC

DP

SPX

CD

PSP

XC

DP

SPX

CD

P

Jan

8.2

8.1

−1.2

1.8

1.8

2.3

1.3

3.7

−0.7

1.0

3.6

4.4

1.6

15.3

5.5

10.1

Feb

−1.8

4.8

−0.4

1.0

−1.5

0.7

3.9

0.7

5.9

1.2

3.3

6.0

7.6

11.7

−0.3

16.6

Mar

0.0

2.3

3.7

3.6

0.7

2.2

2.7

1.9

−1.0

0.6

−2.2

3.0

6.3

6.7

4.8

10.0

Apr

1.2

3.4

−0.3

1.6

−5.3

−0.1

2.6

2.4

0.6

3.0

−2.3

2.8

2.1

3.5

1.5

7.2

May

−1.4

1.4

−0.7

1.3

2.0

5.5

2.1

1.6

3.7

4.0

8.3

5.7

−1.2

5.8

0.9

7.2

Jun

−1.6

0.6

−0.5

1.7

0.8

1.5

5.0

1.8

−0.3

2.0

8.3

4.9

−0.7

3.9

0.9

8.6

Jul

3.0

2.0

0.5

1.9

−0.9

0.4

1.5

1.6

−4.2

0.3

1.8

5.5

7.8

7.5

5.7

6.1

Aug

−0.2

1.8

2.3

1.4

2.1

2.9

1.0

1.2

4.1

3.2

−1.6

2.6

−8.9

−18.

3−5

.8−3

.1Se

p1.

92.

10.

60.

81.

60.

84.

31.

33.

33.

45.

511

.5−5

.7−1

6.2

−0.1

8.3

Oct

−2.6

−3.0

2.3

3.0

−1.3

0.9

0.3

1.1

3.5

2.2

−0.7

5.6

3.6

27.0

−6.6

−10.

7N

ov3.

68.

5−1

.50.

6−0

.72.

72.

61.

43.

83.

02.

04.

610

.122

.814

.014

.5D

ec3.

41.

30.

82.

9−0

.610

.02.

71.

51.

52.

0−1

.76.

71.

34.

3−0

.12.

4

Year

14.0

38.2

5.7

23.7

−1.6

33.6

34.3

22.1

21.5

28.9

26.4

84.8

24.5

87.3

20.6

105.

7

SECOND QUARTER 2007 JOURNAL OF INVESTMENT MANAGEMENT

10 JASMINA HASANHODZIC AND ANDREW W. LO

their homeowner’s, auto, health, and life insurancepolicies). CDP involves few proprietary elements,and can be implemented by most investors, hencethis is one example of a hedge-fund-like strategythat can easily be cloned.

2.2 Capital Multiplication Partners

Consider now the case of “Capital MultiplicationPartners” (CMP), a hypothetical fund based on adynamic asset-allocation strategy between the S&P500 and 1-month US Treasury Bills, where thefund manager can correctly forecast which of thetwo assets will do better in each month and investsthe fund’s assets in the higher-yielding asset at thestart of the month.5 Therefore, the monthly returnof this perfect market-timing strategy is simply thelarger of the monthly return of the S&P 500 andT-Bills. The source of this strategy’s alpha is clear:Merton (1981) observes that perfect market-timingis equivalent to a long-only investment in the S&P500 plus a put option on the S&P 500 with a strikeprice equal to the T-Bill return. Therefore, the eco-nomic value of perfect market-timing is equal to thesum of monthly put-option premia over the life ofthe strategy. And there is little doubt that such astrategy contains significant alpha: a $1 investmentin CMP in January 1926 grows to $23,143,205,448

Table 3 Performance summary of simulated monthly perfect market-timingstrategy between the S&P 500 and 1-month US Treasury bills, and a passivelinear clone, from January 1926 to December 2004.

Statistic S&P 500 T-Bills CMP Clone

Monthly mean 1.0% 0.3% 2.6% 0.7%Monthly SD 5.5% 0.3% 3.6% 3.0%Minimum month −29.7% −0.1% −0.1% −16.3%Maximum month 42.6% 1.4% 42.6% 23.4%Annual Sharpe ratio 0.63 4.12 2.50 0.79# Negative months 360 12 10 340Correlation to S&P 500 100% −2% 84% 100%Growth of $1 since inception $3,098 $18 $2.3 × 1010 $429

by December 2004! Table 3 provides a more detailedperformance summary of CMP which confirmsits remarkable characteristics—CMP’s Sharpe ratioof 2.50 exceeds that of Warren Buffett’s BerkshireHathaway, arguably the most successful pooledinvestment vehicle of all time!6

It should be obvious to even the most naive investorthat CMP is a fantasy because no one can time themarket perfectly. Therefore, attempting to replicatesuch a strategy with exchange-traded instrumentsseems hopeless. But suppose we try to replicateit anyway—how close can we come? In particu-lar, suppose we attempt to relate CMP’s monthlyreturns to the monthly returns of the S&P 500by fitting a simple linear regression (see Figure 1).The option-like nature of CMP’s perfect market-timing strategy is apparent in Figure 1’s scatterof points, and visually, it is obvious that the lin-ear regression does not capture the essence of thisinherently nonlinear strategy. However, the formalmeasure of how well the linear regression fits the

data, the “R2,” is 70.3% in this case, which suggests

a very strong linear relationship indeed. But whenthe estimated linear regression is used to constructa fixed portfolio of the S&P 500 and 1-monthT-Bills, the results are not nearly as attractive asCMP’s returns, as Table 3 shows.

JOURNAL OF INVESTMENT MANAGEMENT SECOND QUARTER 2007

REPLICATING HEDGE-FUND RETURNS 11

Regression of CMP Returns on S&P 500 ReturnsJanuary 1926 to December 2004

y = 0.5476x + 0.0206

R2 = 0.7027

-20%

-10%

0%

10%

20%

30%

40%

50%

-40% -30% -20% -10% 0% 10% 20% 30% 40% 50%

S&P 500 Return

CM

P R

etu

rn

CMP vs. S&P 500 Returns Linear (CMP vs. S&P 500 Returns)

Figure 1 Scatter plot of simulated monthly returns of a perfect market-timing strategy between the S&P500 and 1-month US Treasury bills, against monthly returns of the S&P 500, from January 1926 toDecember 2004.

This example underscores the difficulty in replicat-ing certain strategies with genuine alpha using linear

clones, and cautions against using the R2

as the only

metric of success. Despite the high R2

achieved bythe linear regression of CMP’s returns on the mar-ket index, the actual performance of the linear clonefalls far short of the strategy because a linear modelwill never be able to capture the option-like payoffstructure of the perfect market-timer.

3 Linear regression analysis

To explore the full range of possibilities for repli-cating hedge-fund returns illustrated by the twoextremes of CDP and CMP, we investigated thecharacteristics of a sample of individual hedge fundsdrawn from the TASS Hedge Fund Database. The

database is divided into two parts: “Live” and“Graveyard” funds. Hedge funds that are in the“Live” database are considered to be active as of theend of our sample period, September 2005.7 Weconfine our attention to funds in the Live databasesince we wish to focus on the most current set ofrisk exposures in the hedge-fund industry, and weacknowledge that the Live database suffers fromsurvivorship bias.8

However, the importance of such a bias for ourapplication is tempered by two considerations.First, many successful funds leave the sample as wellas the poor performers, reducing the upward biasin expected returns. In particular, Fung and Hsieh(2000) estimated the magnitude of survivorshipbias to be 3.00% per year, and Liang’s (2000)estimate is 2.24% per year. Second, the focus of

SECOND QUARTER 2007 JOURNAL OF INVESTMENT MANAGEMENT

12 JASMINA HASANHODZIC AND ANDREW W. LO

our study is on the relative performance of hedgefunds versus relatively passive portfolios of liquidsecurities, and as long as our cloning process is notselectively applied to a peculiar subset of funds inthe TASS database, any survivorship bias shouldimpact both funds and clones identically, leavingtheir relative performance unaffected.

Of course, other biases plague the TASS databasesuch as backfill bias (including funds with returnhistories that start before the date of inclusion),9

selection bias (inclusion in the database is volun-tary, hence only funds seeking new investors areincluded),10 and other potential biases imparted bythe process by which TASS decides which funds toinclude and which to omit (part of this process isqualitative). As with survivorship bias, the hope isthat the impact of these additional biases will besimilar for clones and funds, leaving relative com-parisons unaffected. Unfortunately, there is little tobe done about such biases other than to acknowl-edge their existence, and to interpret the outcomeof our empirical analysis with an extra measure ofcaution.

Although theTASS Hedge Fund Live database startsin February 1977, we limit our analysis to the sam-ple period from February 1986 to September 2005because this is the timespan for which we havecomplete data for all of our risk factors. Of thesefunds, we drop those that: (i) do not report net-of-fee returns11; (ii) report returns in currenciesother than the US dollar; (iii) report returns lessfrequently than monthly; (iv) do not provide assetsunder management or only provide estimates; and(v) have fewer than 36 monthly returns. These filtersyield a final sample of 1610 funds.

3.1 Summary statistics

TASS classifies funds into one of the 11 differentinvestment styles, listed in Table 4 and described

in Appendix A, of which 10 correspond exactly tothe CSFB/Tremont sub-index definitions.12 Table 4also reports the number of funds in each categoryfor our sample, as well as summary statistics forthe individual funds and for the equal-weightedportfolio of funds in each of the categories. Thecategory counts show that the funds are not evenlydistributed across investment styles, but are con-centrated among five categories: Long/Short EquityHedge (520), Fund of Funds (355), Event Driven(169), Managed Futures (114), and Emerging Mar-kets (102). Together, these five categories accountfor 78% of the 1610 funds in our sample. Theperformance summary statistics in Table 4 under-score the reason for the growing interest in hedgefunds in recent years—double-digit cross-sectionalaverage returns for most categories with aver-age volatility lower than that of the S&P 500,implying average annualized Sharpe ratios rang-ing from a low of 0.25 for Dedicated Short Biasfunds to a high of 2.70 for Convertible Arbitragefunds.

Another feature of the data highlighted by Table 4is the large positive average return-autocorrelationsfor funds in Convertible Arbitrage (42.2%), Emerg-ing Markets (18.0%), Event Driven (22.2%),Fixed Income Arbitrage (22.1%), Multi-Strategy(21.0%), and Fund of Funds (23.2%) categories.Lo (2001) and Getmansky et al. (2004) haveshown that such high serial correlation in hedge-fund returns is likely to be an indication ofilliquidity exposure. There is, of course, nothinginappropriate about hedge funds taking on liq-uidity risk—indeed, this is a legitimate and oftenlucrative source of expected return—as long asinvestors are aware of such risks, and not mis-led by the siren call of attractive Sharpe ratios.13

But illiquidity exposure is typically accompaniedby capacity limits, and we shall return to thisissue when we compare the properties of hedgefunds to more liquid alternatives such as linearclones.

JOURNAL OF INVESTMENT MANAGEMENT SECOND QUARTER 2007

REPLICATING HEDGE-FUND RETURNS 13

Tab

le4

Sum

mar

yst

atis

tics

forT

ASS

Live

hedg

efu

nds

incl

uded

inou

rsa

mpl

efr

omFe

brua

ry19

86to

Sept

embe

r20

05.

Ann

ualiz

edpe

rfor

man

ceA

nnua

lized

Ann

ualiz

edSD

Ann

ualiz

edLj

ung-

Box

ofeq

ual-

wei

ghte

dm

ean

(%)

(%)

Shar

pera

tio

ρ1

(%)

p-va

lue

(%)

port

folio

offu

nds

Sam

ple

Cat

egor

ysi

zeM

ean

SDM

ean

SDM

ean

SDM

ean

SDM

ean

SDM

ean

(%)

SD(%

)Sh

arpe

Con

vert

ible

arbi

trag

e82

8.41

5.11

6.20

5.28

2.70

5.84

42.2

17.3

11.0

22.2

11.0

75.

362.

07D

edic

ated

shor

tbia

s10

5.98

4.77

28.2

710

.05

0.25

0.24

5.5

12.6

24.2

20.3

6.40

23.2

30.

28E

mer

ging

mar

kets

102

20.4

113

.01

22.9

215

.16

1.42

2.11

18.0

12.4

36.3

30.2

22.3

417

.71

1.26

Equ

ity

mar

ketn

eutr

al83

8.09

4.77

7.78

5.84

1.44

1.20

9.1

23.0

32.6

29.7

12.8

36.

232.

06Ev

entd

rive

n16

913

.03

8.65

8.40

8.09

1.99

1.37

22.2

17.6

27.0

29.3

13.4

74.

373.

08Fi

xed

inco

me

arbi

trag

e62

9.50

4.54

6.56

4.41

2.05

1.48

22.1

17.6

35.9

35.2

10.4

83.

582.

93G

loba

lmac

ro54

11.3

86.

1611

.93

6.10

1.07

0.58

5.8

12.2

43.1

32.5

14.9

18.

641.

73Lo

ng/S

hort

equi

tyhe

dge

520

14.5

98.

1415

.96

9.06

1.06

0.58

12.8

14.9

36.0

30.5

16.3

511

.84

1.38

Man

aged

futu

res

114

13.6

49.

3521

.46

12.0

70.

670.

392.

510

.240

.131

.515

.96

19.2

40.

83M

ulti

-str

ateg

y59

10.7

95.

228.

729.

701.

861.

0321

.020

.128

.230

.114

.59

5.78

2.52

Fund

offu

nds

355

8.25

3.73

6.36

4.47

1.66

0.86

23.2

15.0

27.1

26.3

11.9

37.

481.

59

SECOND QUARTER 2007 JOURNAL OF INVESTMENT MANAGEMENT

14 JASMINA HASANHODZIC AND ANDREW W. LO

3.2 Factor model specification

To determine the explanatory power of com-mon risk factors for hedge funds, we performa time-series regression for each of the 1610hedge funds in our sample, regressing the hedgefund’s monthly returns on the following six factors:(1) USD: the US Dollar Index return; (2) BOND:the return on the Lehman Corporate AA Inter-mediate Bond Index; (3) CREDIT: the spreadbetween the Lehman BAA Corporate Bond Indexand the Lehman Treasury Index; (4) SP500: theS&P 500 total return; (5) CMDTY: the GoldmanSachs Commodity Index (GSCI) total return; and(6) DVIX: the first-difference of the end-of-monthvalue of the CBOE Volatility Index (VIX).These sixfactors are selected for two reasons: They providea reasonably broad cross-section of risk exposuresfor the typical hedge fund (stocks, bonds, curren-cies, commodities, credit, and volatility), and eachof the factor returns can be realized through rel-atively liquid instruments so that the returns oflinear clones may be achievable in practice. In par-ticular, there are forward contracts for each of thecomponent currencies of the US Dollar index, andfutures contracts for the stock and bond indexesand for the components of the commodity index.Futures contracts on the VIX index were intro-duced by the CBOE in March 2004 and are notas liquid as the other index futures, but the OTCmarket for variance and volatility swaps is growingrapidly.

The linear regression model provides a simple butuseful decomposition of a hedge fund’s return Ritinto several components:

Rit = αi + βi1RiskFactor1t + · · ·+ βiK RiskFactorKt + εit (1)

From this decomposition, we have the followingcharacterization of the fund’s expected return and

variance:

E[Rit ] = αi + βi1E[RiskFactor1t ] + · · ·+ βiK E[RiskFactorKt ] (2)

Var[Rit ] = β2i1Var[RiskFactor1t ] + · · ·

+ β2iK Var[RiskFactorKt ]

+ Covariances + Var[εit ] (3)

where “Covariances” is the sum of all pairwisecovariances between RiskFactorpt and RiskFactorqtweighted by the product of their respective betacoefficients βipβiq .

This characterization implies that there are two dis-tinct sources of a hedge fund’s expected return: betaexposures βik multiplied by the risk premia asso-ciated with those exposures E[RiskFactorkt ], andmanager-specific alpha αi . By “manager-specific,”we do not mean to imply that a hedge fund’sunique source of alpha is without risk—we are sim-ply distinguishing this source of expected returnfrom those that have clearly identifiable risk fac-tors associated with them. In particular, it may wellbe the case that αi arises from risk factors otherthan the six we have proposed, and a more refinedversion of Eq. (1)—one that reflects the particu-lar investment style of the manager—may yield abetter-performing linear clone.

From Eq. (3), we see that a hedge fund’s vari-ance has three distinct sources: the variances of therisk factors multiplied by the squared beta coef-ficients, the variance of the residual εit (whichmay be related to the specific economic sources ofαi), and the weighted covariances among the fac-tors. This decomposition highlights the fact that ahedge fund can have several sources of risk, eachof which should yield some risk premium, that is,risk-based alpha, otherwise investors would not bewilling to bear such risk. By taking on exposureto multiple risk factors, a hedge fund can generate

JOURNAL OF INVESTMENT MANAGEMENT SECOND QUARTER 2007

REPLICATING HEDGE-FUND RETURNS 15

attractive expected returns from the investor’s per-spective (see, e.g. Capital Decimation Partners inSection 2.1).14

3.3 Factor exposures

Table 5 presents summary statistics for the beta coef-ficients or factor exposures in Eq. (1) estimatedfor each of the 1610 hedge funds by ordinaryleast squares and grouped by category. In partic-ular, for each category we report the minimum,median, mean, and maximum beta coefficient foreach of the six factors and the intercept, acrossall regressions in that category. For example, theupper left block of entries with the title “Inter-cept” presents summary statistics for the interceptsfrom the individual hedge-fund regressions withineach category, and the “Mean” column shows thatthe average manager-specific alpha is positive forall categories, ranging from 0.42% per monthfor Managed Futures funds to 1.41% per monthfor Emerging Markets funds. This suggests thatmanagers in our sample are, on average, indeed con-tributing value above and beyond the risk premiaassociated with the six factors we have chosen inEq. (1). We shall return to this important issue inSection 3.4.

The panel in Table 5 with the heading Rsp500 pro-vides summary statistics for the beta coefficientscorresponding to the S&P 500 return factor, and theentries in the “Mean” column are broadly consistentwith each of the category definitions. For example,funds in the Dedicated Short Bias category have anaverage S&P 500 beta of −0.88, which is consistentwith their shortselling mandate. On the other hand,Equity Market Neutral funds have an average S&P500 beta of 0.05, confirming their market neutralstatus. And Long/Short Equity Hedge funds, whichare mandated to provide partially hedged equity-market exposure, have an average S&P 500 betaof 0.38.

The remaining panels in Table 5 show that riskexposures do vary considerably across categories.This is more easily seen in Figure 2 which plots themean beta coefficients for all six factors, categoryby category. From Figure 2, we see that ConvertibleArbitrage funds have three main exposures (longcredit, long bonds, and long volatility), whereasEmerging Markets funds have four somewhat dif-ferent exposures (long stocks, short USD, longcredit, and long commodities). The category withthe smallest overall risk exposures is Equity MarketNeutral, and not surprisingly, this category exhibitsthe second lowest average mean return, 8.09%.

The lower right panel of Table 5 contains a sum-mary of the explanatory power of (1) as measured by

the R2

statistic of the regression (1). The mean R2s

range from a low of 10.4% for Equity Market Neu-tral (as expected, given this category’s small averagefactor exposures to all six factors) to a high of 40.4%for Dedicated Short Bias (which is also expectedgiven this category’s large negative exposure to theS&P 500).

To provide further intuition for the relation between

R2

and fund characteristics, we regress R2

on several

fund characteristics, and find that lower R2

fundsare those with higher Sharpe ratios, higher manage-ment fees, and higher incentive fees. This accordswell with the intuition that funds providing greater

diversification benefits, that is, lower R2’s, com-

mand higher fees in equilibrium. See Hasanhodzicand Lo (2006b) for further details.

3.4 Expected-return decomposition

Using the parameter estimates of (1) for the indi-vidual hedge funds in our sample, we can nowreformulate the question of whether or not a hedge-fund strategy can be cloned as a question abouthow much of a hedge fund’s expected return is due

SECOND QUARTER 2007 JOURNAL OF INVESTMENT MANAGEMENT

16 JASMINA HASANHODZIC AND ANDREW W. LO

Tab

le5

Sum

mar

yst

atis

tics

for

mul

tiva

riat

elin

ear

regr

essi

ons

ofm

onth

lyre

turn

sof

hedg

efu

nds

inth

eT

ASS

Live

data

base

from

Febr

uary

1986

toSe

ptem

ber

2005

onsi

xfa

ctor

s:th

eS&

P50

0to

talr

etur

n,th

eLe

hman

Cor

pora

teA

AIn

term

edia

teB

ond

Inde

xre

turn

,the

US

Dol

lar

Inde

xre

turn

,the

spre

adbe

twee

nth

eLe

hman

US

Agg

rega

teLo

ngC

redi

tB

AA

Bon

dIn

dex

and

the

Lehm

anTr

easu

ryLo

ngIn

dex,

the

first

-diff

eren

ceof

the

CB

OE

Vol

atili

tyIn

dex

(VIX

),an

dth

eG

oldm

anSa

chs

Com

mod

ity

Inde

x(G

SCI)

tota

lret

urn.

Inte

rcep

tR

sp50

0R

lbR

usd

Sam

ple

Cat

egor

ysi

zeSt

atis

tic

Min

Med

Mea

nM

axSD

Min

Med

Mea

nM

axSD

Min

Med

Mea

nM

axSD

Min

Med

Mea

nM

axSD

Con

vert

ible

arbi

trag

e82

beta

−0.5

20.

410.

431.

570.

37−0

.63

−0.0

1−0

.02

0.45

0.15

−0.0

80.

260.

301.

730.

29−0

.98

0.01

−0.0

20.

680.

28t-

stat

−1.5

62.

124.

5583

.10

11.3

5−2

.58

−0.1

40.

067.

651.

53−0

.52

1.60

1.60

4.50

1.12

−2.2

30.

150.

122.

911.

22D

edic

ated

shor

tbia

s10

beta

−0.0

40.

770.

671.

130.

38−1

.78

−1.0

1−0

.88

−0.1

10.

50−0

.60

0.18

0.25

0.96

0.48

−0.0

80.

730.

671.

250.

51t-

stat

−0.1

20.

730.

911.

830.

66−1

0.95

−3.2

9−3

.88

−0.4

82.

72−1

.37

0.24

0.17

1.05

0.70

−0.1

91.

261.

071.

990.

77E

mer

ging

mar

kets

102

beta

−0.7

51.

191.

416.

501.

08−0

.41

0.31

0.43

3.30

0.52

−4.5

30.

020.

012.

330.

77−4

.66

−0.3

9−0

.42

2.18

0.79

t-st

at−1

.03

1.83

2.74

44.6

74.

57−1

.77

1.69

1.65

5.46

1.61

−2.1

70.

090.

223.

711.

09−3

.74

−1.0

3−0

.97

2.53

1.20

Equ

ity

mar

ketn

eutr

al83

beta

−0.6

10.

590.

592.

420.

41−1

.22

0.05

0.05

0.90

0.27

−1.1

60.

050.

020.

820.

33−2

.83

0.02

−0.0

41.

240.

44t-

stat

−1.4

02.

022.

8813

.89

3.00

−4.8

60.

750.

654.

161.

98−3

.74

0.30

0.27

2.67

1.09

−4.1

70.

080.

163.

651.

39Ev

entd

rive

n16

9be

ta−0

.12

0.78

0.93

6.18

0.78

−0.3

50.

080.

131.

170.

22−4

.23

0.08

0.04

1.31

0.46

−6.3

8−0

.05

−0.1

31.

460.

60t-

stat

−0.6

93.

383.

8821

.54

2.89

−2.8

01.

261.

3410

.87

1.88

−2.3

10.

400.

423.

211.

08−2

.86

−0.3

1−0

.14

3.40

1.35

Fixe

din

com

ear

bitr

age

62be

ta0.

000.

520.

582.

030.

42−0

.39

0.03

0.02

0.23

0.10

−0.5

50.

200.

271.

860.

40−0

.66

0.05

0.07

0.77

0.35

t-st

at0.

002.

853.

8524

.30

3.91

−2.4

20.

550.

443.

231.

25−2

.63

1.00

1.26

11.0

21.

99−3

.48

0.38

0.66

4.62

1.68

Glo

balm

acro

54be

ta−0

.79

0.63

0.59

1.75

0.54

−0.4

90.

010.

101.

140.

30−0

.74

0.21

0.34

2.03

0.56

−2.0

0−0

.23

−0.2

31.

350.

67t-

stat

−1.5

61.

531.

717.

661.

62−2

.97

0.19

0.59

6.16

1.84

−1.9

30.

710.

926.

051.

51−6

.51

−0.8

3−0

.73

4.52

1.95

Long

/Sho

rteq

uity

hedg

e52

0be

ta−1

.53

0.84

0.89

7.60

0.75

−1.3

70.

330.

383.

130.

44−3

.04

−0.0

10.

033.

490.

59−2

.57

−0.0

3−0

.09

2.45

0.60

t-st

at−1

.80

1.84

1.86

10.4

71.

38−3

.72

2.06

2.27

20.0

72.

50−3

.47

−0.0

10.

063.

331.

06−4

.60

−0.1

0−0

.19

3.41

1.18

Man

aged

futu

res

114

beta

−1.8

40.

480.

423.

690.

73−0

.81

−0.0

10.

032.

300.

37−0

.44

0.88

0.89

2.62

0.67

−2.6

5−0

.37

−0.3

91.

140.

63t-

stat

−2.3

60.

720.

654.

981.

08−2

.94

−0.0

50.

207.

881.

43−1

.70

1.46

1.60

4.34

1.22

−4.2

5−0

.83

−0.7

21.

990.

98M

ulti

-str

ateg

y59

beta

−0.4

10.

710.

712.

680.

47−0

.31

0.07

0.15

1.34

0.26

−1.8

10.

100.

122.

400.

51−1

.84

0.07

0.01

0.78

0.41

t-st

at−0

.43

3.22

3.41

10.5

12.

41−2

.22

1.27

1.37

5.98

1.68

−1.4

90.

580.

573.

491.

13−2

.78

0.36

0.39

3.19

1.34

Fund

offu

nds

355

beta

−0.7

70.

420.

431.

880.

34−0

.80

0.09

0.12

0.85

0.15

−0.5

00.

120.

182.

250.

29−1

.12

−0.0

7−0

.10

0.62

0.24

t-st

at−3

.55

2.34

2.67

10.5

12.

14−2

.65

1.56

1.84

9.44

1.80

−1.5

90.

830.

954.

841.

17−3

.63

−0.5

3−0

.42

3.32

1.28

JOURNAL OF INVESTMENT MANAGEMENT SECOND QUARTER 2007

REPLICATING HEDGE-FUND RETURNS 17

Tab

le5

(Con

tinue

d)

Rcs

�V

IXR

gsci

Sign

ifica

nce

(%)

Sam

ple

Cat

egor

ysi

zeSt

atis

tic

Min

Med

Mea

nM

axSD

Min

Med

Mea

nM

axSD

Min

Med

Mea

nM

axSD

Stat

isti

cM

inM

edM

ean

Max

SD

Con

vert

ible

arbi

trag

e82

beta

0.00

0.39

0.52

2.87

0.57

−0.2

50.

050.

050.

320.

08−0

.07

0.01

0.02

0.16

0.03

Adj

.R2

−11.

016

.017

.366

.215

.4

t-st

at0.

193.

062.

957.

721.

58−1

.41

0.50

0.66

3.56

0.98

−1.1

50.

520.

512.

170.

69p(

F)0.

01.

011

.897

.123

.6

Ded

icat

edsh

ortb

ias

10be

ta−0

.98

−0.2

6−0

.19

0.93

0.67

−0.2

60.

050.

040.

440.

23−0

.38

−0.1

1−0

.12

0.06

0.13

Adj

.R2

−3.5

39.7

40.4

79.5

25.4

t-st

at−2

.67

−0.6

8−0

.44

2.54

1.64

−1.1

10.

240.

232.

561.

10−2

.19

−0.8

6−0

.95

0.54

0.92

p(F)

0.0

0.0

8.3

83.0

26.2

Em

ergi

ngm

arke

ts10

2be

ta−0

.56

0.46

0.59

2.89

0.67

−1.4

1−0

.05

0.01

3.91

0.50

−0.3

40.

050.

060.

340.

09A

dj.R

2−4

.717

.419

.454

.714

.3

t-st

at−1

.97

1.32

1.33

4.82

1.36

−3.9

5−0

.35

−0.2

83.

881.

17−1

.46

0.68

0.60

2.40

0.79

p(F)

0.0

0.2

8.4

78.8

17.7

Equ

ity

mar

ketn

eutr

al83

beta

−1.7

8−0

.03

−0.0

60.

720.

31−1

.19

0.02

0.03

0.80

0.23

−0.1

20.

010.

020.

380.

07A

dj.R

2−8

.17.

210

.463

.213

.7

t-st

at−3

.83

−0.2

7−0

.35

3.34

1.44

−3.1

00.

220.

253.

951.

23−2

.05

0.48

0.43

2.80

1.11

p(F)

0.0

7.4

19.9

94.1

24.6

Even

tdri

ven

169

beta

−1.9

60.

250.

332.

010.

45−1

.81

0.02

0.05

1.19

0.26

−0.2

70.

010.

010.

270.

06A

dj.R

2−7

.515

.519

.568

.516

.4

t-st

at−1

.66

1.51

1.81

8.31

1.99

−2.7

60.

420.

364.

581.

17−2

.27

0.50

0.60

4.06

1.15

p(F)

0.0

0.3

11.1

88.6

20.0

Fixe

din

com

ear

bitr

age

62be

ta−0

.70

0.10

0.19

1.54

0.46

−0.7

10.

050.

070.

500.

18−0

.06

0.01

0.02

0.15

0.05

Adj

.R2

−8.9

12.8

14.9

78.9

15.9

t-st

at−3

.29

0.80

1.25

11.7

42.

56−3

.16

0.85

1.16

5.62

1.93

−1.7

60.

570.

522.

521.

10p(

F)0.

02.

117

.794

.626

.3

Glo

balm

acro

54be

ta−0

.61

0.13

0.18

1.73

0.42

−0.3

60.

030.

070.

550.

19−0

.09

0.02

0.04

0.27

0.08

Adj

.R2

−12.

68.

914

.874

.017

.3

t-st

at−1

.60

0.44

0.60

3.96

1.25

−3.0

80.

330.

343.

611.

11−1

.22

0.37

0.60

3.92

1.20

p(F)

0.0

4.9

16.8

97.0

24.3

Long

/Sho

rteq

uity

hedg

e52

0be

ta−1

.37

0.17

0.28

4.55

0.59

−1.6

70.

070.

072.

760.

33−0

.33

0.04

0.06

0.88

0.11

Adj

.R2

−13.

818

.821

.690

.219

.0

t-st

at−5

.28

0.58

0.69

4.94

1.36

−4.7

00.

460.

383.

671.

28−3

.31

0.74

0.77

5.91

1.13

p(F)

0.0

0.4

11.8

97.7

22.9

Man

aged

futu

res

114

beta

−5.9

8−0

.33

−0.3

53.

200.

82−0

.75

0.14

0.15

1.29

0.32

−0.3

10.

110.

130.

800.

15A

dj.R

2−6

.013

.315

.370

.013

.3

t-st

at−2

.85

−0.9

2−0

.73

2.56

1.04

−2.8

10.

730.

744.

361.

28−2

.15

1.32

1.36

5.25

1.22

p(F)

0.0

0.6

8.2

88.5

17.0

Mul

ti-s

trat

egy

59be

ta−0

.48

0.07

0.17

1.64

0.41

−0.3

80.

040.

090.

950.

19−0

.05

0.03

0.04

0.75

0.11

Adj

.R2

−13.

58.

912

.951

.715

.7

t-st

at−2

.20

0.72

1.21

6.34

2.12

−1.5

90.

680.

873.

721.

31−1

.34

0.87

0.81

2.90

0.97

p(F)

0.0

6.7

21.7

97.5

28.9

Fund

offu

nds

355

beta

−0.7

80.

170.

171.

410.

22−0

.32

0.06

0.07

0.48

0.09

−0.2

30.

030.

050.

350.

05A

dj.R

2−7

.220

.422

.372

.314

.9

t-st

at−3

.62

1.38

1.53

6.35

1.55

−2.7

40.

980.

984.

691.

12−3

.16

1.38

1.39

4.28

1.01

p(F)

0.0

0.2

5.7

84.0

14.3

SECOND QUARTER 2007 JOURNAL OF INVESTMENT MANAGEMENT

18 JASMINA HASANHODZIC AND ANDREW W. LO

-1.00

-0.50

0.00

0.50

1.00

1.50

2.00

ConvertibleArbitrage

DedicatedShort Bias

EmergingMarkets

Equity MarketNeutral

Event Driven Fixed IncomeArbitrage

Global Macro Long/ShortEquity

ManagedFutures

Multi-Strategy Fund ofFunds

Ave

rag

e R

egre

ssio

n C

oef

fici

ent

Manager-Specific Alpha S&P 500 BondsUSD Credit Spread DVIXCommodities

Figure 2 Average regression coefficients for multivariate linear regressions of monthly returns of hedgefunds in the TASS Live database from February 1986 to September 2005 on six factors: the S&P 500total return, the Lehman Corporate AA Intermediate Bond Index return, the US Dollar Index return, thespread between the Lehman US Aggregate Long Credit BAA Bond Index and the Lehman Treasury LongIndex, the first-difference of the CBOE Volatility Index (VIX), and the Goldman Sachs Commodity Index(GSCI) total return.

to risk premia from identifiable factors. If it is asignificant portion and the relationship is primar-ily linear, then a passive portfolio with just thoserisk exposures—created by means of liquid instru-ments such as index futures, forwards, and othermarketable securities—may be a reasonable alter-native to a less liquid and opaque investment inthe fund.

Table 6 summarizes the results of the expected-return decomposition (2) for our sample of 1610funds, grouped according to their style categoriesand for all funds. Each row of Table 6 containsthe average total mean return of funds in a given

category and averages of the percent contributionsof each of the six factors and the manager-specificalpha to that average total mean return.15 Notethat the average percentage contributions add upto 100% when summed across all six factors andthe manager-specific alpha because this decompo-sition sums to 100% for each fund, and when thisdecomposition is averaged across all funds, the sumis preserved.

The first row’s entries indicate that the most signifi-cant contributors to the average total mean return of8.4% for Convertible Arbitrage funds are CREDIT(27.1%), USD (67.1%), BOND (34.9%), and

JOURNAL OF INVESTMENT MANAGEMENT SECOND QUARTER 2007

REPLICATING HEDGE-FUND RETURNS 19

Table 6 Decomposition of total mean returns of hedge funds in the TASS Live database according topercentage contributions from six factors and manager-specific alpha, for 1610 hedge funds from February1986 to September 2005.

Average of percentage contribution of factors tototal expected return (%)

Category Sampledescription size Avg. E [R] CREDIT USD SP500 BOND DVIX CMDTY ALPHA

Convertible arbitrage 82 8.4 27.1 67.1 −19.3 34.9 −8.4 31.8 −33.3Dedicated short bias 10 6.0 12.2 19.4 −108.2 7.0 8.9 −64.9 225.6Emerging markets 102 20.4 −0.3 −3.2 19.3 0.1 −0.4 6.2 78.3Equity market neutral 83 8.1 0.2 3.6 4.0 3.9 1.3 6.3 80.8Event driven 169 13.0 2.1 3.0 4.3 9.4 −0.7 3.1 79.0Fixed income arbitrage 62 9.5 −1.4 3.3 2.7 18.5 −0.5 4.4 73.1Global macro 54 11.4 2.0 8.1 9.7 25.0 −3.3 10.0 48.6Long/Short equity hedge 520 14.6 1.1 1.9 17.8 2.1 −1.8 8.4 70.5Managed futures 114 13.6 1.9 23.4 −3.4 53.8 −1.5 53.2 −27.5Multi-strategy 59 10.8 0.5 3.5 5.7 10.1 −1.9 3.2 78.9Fund of funds 355 8.3 0.5 5.4 9.7 8.8 −2.8 7.3 71.1All Funds 1,610 11.3 2.3 7.8 8.5 11.3 −1.9 10.9 61.0

CMDTY (31.8%), and the average contributionof manager-specific alpha is −33.3%. This impliesthat on average, Convertible Arbitrage funds earnmore than all of their mean returns from the riskpremia associated with the six factor exposures, andthat the average contribution of other sources ofalpha is negative! Of course, this does not meanthat convertible-arbitrage managers are not addingvalue—Table 6’s results are averages across all fundsin our sample, hence the positive manager-specificalphas of successful managers will be dampenedand, in some cases, outweighed by the negativemanager-specific alphas of the unsuccessful ones.

In contrast to the Convertible Arbitrage funds,for the 10 funds in the Dedicated Short Bias cat-egory, the manager-specific alpha accounts for225.6% of the funds’ total mean return on average,and the contribution of the SP500 factor is neg-ative. This result is not as anomalous as it seems.The bull market of the 1990s implies a perfor-mance drag for any fund with negative exposureto the S&P 500, therefore, Dedicated Short Biasmanagers that have generated positive performance

during this period must have done so through othermeans. A concrete illustration of this intuition isgiven by the return decomposition of the annual-ized average return of the two most successful fundsin the Dedicated Short Bias category, funds 33735and 33736. These two funds posted annualized net-of-fee returns of 15.56% and 10.02%, respectively,but the contribution of the SP500 factor to theseannualized returns was negative in both cases (bothfunds had negative SP500 beta exposures, as theyshould, and the S&P 500 yielded positive returnsover the funds’ lifetimes).16

Between the two extremes of Convertible Arbi-trage and Dedicated Short Bias funds, Table 6shows considerable variation in the importanceof manager-specific alpha for the other categories.Over 80% of the average total return of EquityMarket Neutral funds is due to manager-specificalpha, but for Managed Futures, the manager-specific alpha accounts for −27.5%. For the entiresample of 1610 funds, 61% of the average totalreturn is attributable to manager-specific alpha,implying that on average, the remaining 39% is

SECOND QUARTER 2007 JOURNAL OF INVESTMENT MANAGEMENT

20 JASMINA HASANHODZIC AND ANDREW W. LO

due to the risk premia from our six factors. Theseresults suggest that for certain types of hedge-fundstrategies, a multi-factor portfolio may yield someof the same benefits but in a transparent, scalable,and lower-cost vehicle.

4 Linear clones

The multivariate regression results in Section 3 sug-gest that linear clones may be able to replicate someof the risk exposures of hedge funds, and in thissection we investigate this possibility directly byconsidering two types of clones. The first type con-sists of “fixed-weight” portfolios, where we use theentire sample of a given fund’s returns to estimatea set of portfolio weights for the instruments corre-sponding to the factors used in the linear regression.These portfolio weights are fixed through time foreach fund, hence the term “fixed-weight.”17 Butbecause this approach involves a certain degree of“look-ahead” bias—we use the entire history of afund’s returns to construct the portfolio weights thatare applied each period to compute the clone port-folio return—we also construct a second type oflinear clone based on rolling-window regressions.

4.1 Fixed-weight vs. rolling-window clones

To construct a fixed-weight linear clone for fund i,we begin by regressing the fund’s returns {Rit } onfive of the six factors we considered in Section 3(we drop the DVIX factor because its returns arenot as easily realized with liquid instruments),where we omit the intercept and constrain the betacoefficients to sum to one:

Rit = βi1SP500t + βi2BONDt

+ βi3USDt + βi4CREDITt

+ βi5CMDTYt + εit ,

t = 1, . . . , T (4a)

subject to 1 = βi1 + · · · + βi5 (4b)

This is the same technique proposed by Sharpe(1992) for conducting “style analysis,” however, ourmotivation is quite different. We omit the inter-cept because our objective is to estimate a weightedaverage of the factors that best replicates the fund’sreturns, and omitting the constant term forces theleast-squares algorithm to use the factor means tofit the mean of the fund, an important feature ofreplicating hedge-fund expected returns with factorrisk premia. And we constrain the beta coefficientsto sum to one to yield a portfolio interpretationfor the weights. Note that we do not constrain theregression coefficients to be non-negative as Sharpe(1992) does because unlike Sharpe’s original appli-cation to long-only mutual funds, in our context allfive factors correspond to instruments that can beshortsold, and we do expect to be shortselling eachof these instruments on occasion to achieve the kindof risk exposures hedge funds typically exhibit. Forexample, clones of Dedicated Short Bias funds willundoubtedly require shorting the SP500 factor.

The estimated regression coefficients {β∗ik} are then

used as portfolio weights for the five factors, hencethe portfolio returns are equivalent to the fittedvalues R∗

it of the regression equation. However,we implement an additional renormalization sothat the resulting portfolio return R̂it has the samesample volatility as the original fund’s return series:

R∗it ≡ β∗

i1SP500t + β∗i2BONDt + β∗

i3USDt

+ β∗i4CREDITt + β∗

i5CMDTYt (5)

R̂it ≡ γi R∗it , γi ≡

√∑Tt=1 (Rit − Ri)2/(T −1)√∑Tt=1 (R∗

it − R∗i )2/(T −1)

(6)

Ri ≡ 1

T

T∑t=1

Rit , R∗i ≡ 1

T

T∑t=1

R∗it (7)

The motivation for this renormalization is to createa fair comparison between the clone portfolio and

JOURNAL OF INVESTMENT MANAGEMENT SECOND QUARTER 2007

REPLICATING HEDGE-FUND RETURNS 21

the fund by equalizing their volatilities. Renormal-izing (5) is equivalent to changing the leverage ofthe clone portfolio, since the sum of the renormal-ized betas γi

∑k β∗

ik will equal the renormalizationfactor γi , not one. If γi exceeds one, then pos-itive leverage is required, and if less than one,the portfolio is not fully invested in the five fac-tors. A more complete expression of the portfolioweights of clone i may be obtained by introducingan additional asset that represents leverage, that is,borrowing and lending, in which case the portfolioweights of the five factors and this additional assetmust sum to one:

1 = γi(β∗i1 + · · · + β∗

i5) + δi (8)

The clone return is then given by:

R̂it = γi(β∗i1 SP500t + · · ·

+ β∗i5 CMDTYt ) + δi Rl (9)

where Rl is the borrowing/lending rate. Since thisrate depends on many factors such as the credit qual-ity of the respective counterparties, the riskiness ofthe instruments and portfolio strategy, the size ofthe transaction, and general market conditions, wedo not attempt to assume a particular value for Rlbut simply point out its existence.18

As discussed above, fixed-weight linear clones areaffected by look-ahead bias because the entire histo-ries of fund and factor returns are used to constructthe clones’ portfolio weights and renormalizationfactors. To address this issue, we present an alter-nate method of constructing linear clones using arolling window for estimating the regression coeffi-cients and renormalization factors. Rolling-windowestimators can also address the ubiquitous issueof nonstationarity that affects most financial time-series studies; time-varying means, volatilities, andgeneral market conditions can be captured to somedegree by using rolling windows.

To construct a “rolling-window” linear clone, foreach month t , we use a 24-month rolling window

from months t −24 to t −1 to estimate the sameregression (4) as before19:

Rit−k = βit1SP500t−k + βit2BONDt−k

+ βit3USDt−k + βit4CREDITt−k

+ βit5CMDTYt−k + εit−k ,

k = 1, . . . , 24 (10a)

subject to 1 = βit1 + · · · + βit5 (10b)

but now the coefficients are indexed by both i andt since we repeat this process each month for everyfund i. The parameter estimates are then used in thesame manner as in the fixed-weight case to constructclone returns R̂it :

R∗it ≡ β∗

it1SP500t + β∗it2BONDt + β∗

it3USDt

+ β∗it4CREDITt + β∗

it5CMDTYt (11)

R̂it ≡ γit R∗it , γit ≡

√∑24k=1 (Rit−k − Rit )2/23√∑24k=1 (R∗

it−k − R∗it )2/23

(12)

Rit ≡ 1

24

24∑k=1

Rit−k , R∗it ≡ 1

24

24∑k=1

R∗it−k (13)

where the renormalization factors γit are nowindexed by time t to reflect the fact that they arealso computed within the rolling window. Thisimplies that for any given clone i, the volatilityof its returns over the entire history will no longerbe identical to the volatility of its matching fundbecause the renormalization process is applied onlyto rolling windows, not to the entire history ofreturns. However, as long as volatilities do not shiftdramatically over time, the rolling-window renor-malization process should yield clones with similarvolatilities.

Although rolling-window clones may seem morepractically relevant because they avoid the mostobvious forms of look-ahead bias, they have

SECOND QUARTER 2007 JOURNAL OF INVESTMENT MANAGEMENT

22 JASMINA HASANHODZIC AND ANDREW W. LO

drawbacks as well. For example, the rolling-window estimation procedure generates more fre-quent rebalancing needs for the clone portfolio,which is counter to the passive spirit of the cloningendeavor. Moreover, rolling-window estimators aretypically subject to greater estimation error becauseof the smaller sample size. This implies that at leastpart of the rebalancing of rolling-window clonesis unnecessary. The amount of rebalancing can,of course, be controlled by adjusting the lengthof the rolling window—a longer window impliesmore stable weights, but stability implies less flex-ibility in capturing potential nonstationarities inthe data.

Ultimately, the choice between fixed-weight androlling-window clones depends on the nature ofthe application, the time-series properties of thestrategies being cloned, and the specific goals andconstraints of the investor. A passive investor withlittle expertise in trading and risk management maywell prefer the fixed-weight clone, whereas a moreactive investor with trading capabilities and a desireto implement dynamic asset-allocation policies willprefer the rolling-window clone. For these rea-sons, we present results for both types of clonesin Sections 4.2–4.5.

4.2 Performance results

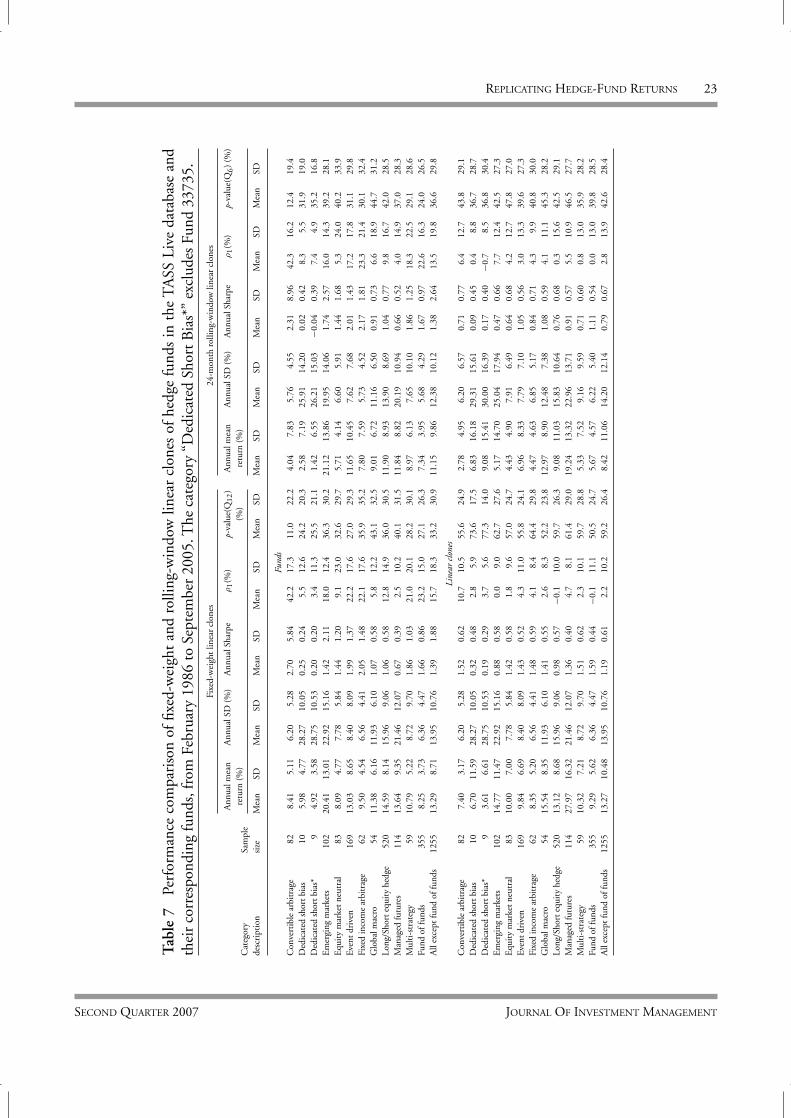

Table 7 contains a comparison between the perfor-mance of fixed-weight and rolling-window linearclones and the original funds from which the clonesare derived.20 The results are striking—for severalcategories, the average mean return of the clones isonly slightly lower than that of their fund counter-parts, and in some categories, the clones do better.For example, the average mean return of the Con-vertible Arbitrage fixed-weight clones is 7.40%, andthe corresponding figure for the funds is 8.41%.For Long/Short Equity Hedge funds, the aver-age mean return for fixed-weight clones and funds

is 13.12% and 14.59%, respectively. And in theMulti-Strategy category, the average mean returnfor fixed-weight clones and funds is 10.32% and10.79%, respectively.

In five cases, the average mean return of thefixed-weight clones is higher than that of thefunds: Dedicated Short Bias (6.70% vs. 5.98%),Equity Market Neutral (10.00% vs. 8.09%), GlobalMacro (15.54% vs. 11.38%), Managed Futures(27.97% vs. 13.64%), and Fund of Funds (9.29%vs. 8.25%). However, these differences are notnecessarily statistically significant because of thevariability in mean returns of funds and cloneswithin their own categories. Even in the case ofManaged Futures, the difference in average meanreturn between fixed-weight clones and funds—almost 15 percentage points—is not significantbecause of the large fluctuations in average meanreturns of the Managed Futures fixed-weight clonesand their corresponding funds (e.g. one standarddeviation of the average mean of the ManagedFutures fixed-weight clones is 16.32% and onestandard deviation of the average mean of the cor-responding sample of funds is 9.35%, accordingto Table 7). Nevertheless, these results suggest thatfor certain categories, the performance of fixed-weight clones may be comparable to that of theircorresponding funds.

On the other hand, at 9.84%, the average perfor-mance of the Event-Driven fixed-weight clones isconsiderably lower than the 13.03% average forthe funds. While also not statistically significant,this gap is understandable given the idiosyncraticand opportunistic nature of most event-drivenstrategies. Moreover, a significant source of the prof-itability of event-driven strategies is the illiquiditypremium that managers earn by providing capitalin times of distress. This illiquidity premium willclearly be missing from a clone portfolio of liquidsecurities, hence we should expect a sizable perfor-mance gap in this case. The same can be said for the

JOURNAL OF INVESTMENT MANAGEMENT SECOND QUARTER 2007

REPLICATING HEDGE-FUND RETURNS 23

Tab

le7

Perf

orm

ance

com

pari

son

offix

ed-w

eigh

tan

dro

lling

-win

dow

linea

rcl

ones

ofhe

dge

fund

sin

the

TA

SSLi

veda

taba

sean

dth

eir

corr

espo

ndin

gfu

nds,

from

Febr

uary

1986

toSe

ptem

ber

2005

.The

cate

gory

“Ded

icat

edSh

ortB

ias*

”ex

clud

esFu

nd33

735.

Fixe

d-w

eigh

tlin

ear

clon

es24

-mon

thro

lling

-win

dow

linea

rcl

ones

Ann

ualm

ean

Ann

ualS

D(%

)A

nnua

lSha

rpe

ρ1(%

)p-

valu

e(Q

12)

Ann

ualm

ean

Ann

ualS

D(%

)A

nnua

lSha

rpe

ρ1(%

)p-

valu

e(Q

6)

(%)

retu

rn(%

)(%

)re

turn

(%)

Cat

egor

ySa

mpl

ede

scri

ptio

nsi

zeM

ean

SDM

ean

SDM

ean

SDM

ean

SDM

ean

SDM

ean

SDM

ean

SDM

ean

SDM

ean

SDM

ean

SD

Fund

sC

onve

rtib

lear

bitr

age

828.

415.

116.

205.

282.

705.

8442

.217

.311

.022

.24.

047.

835.

764.

552.

318.

9642

.316

.212

.419

.4D

edic

ated

shor

tbia

s10

5.98

4.77

28.2

710

.05

0.25

0.24

5.5

12.6

24.2

20.3

2.58

7.19

25.9

114

.20

0.02

0.42

8.3

5.5

31.9

19.0

Ded

icat

edsh

ortb

ias*

94.

923.

5828

.75

10.5

30.

200.

203.

411

.325

.521

.11.

426.

5526

.21

15.0

3−0

.04

0.39

7.4

4.9

35.2

16.8

Em

ergi

ngm

arke

ts10

220

.41

13.0

122

.92

15.1

61.

422.

1118

.012

.436

.330

.221

.12

13.8

619

.95

14.0

61.

742.

5716

.014

.339

.228

.1E

quit

ym

arke

tneu

tral

838.

094.

777.

785.

841.

441.

209.

123

.032

.629

.75.

714.

146.

605.

911.

441.

685.

324

.040

.233

.9Ev

entd

rive

n16

913

.03

8.65

8.40

8.09

1.99

1.37

22.2

17.6

27.0

29.3

11.6

510

.45

7.62

7.68

2.01

1.43

17.2

17.8

31.1

29.8

Fixe

din

com

ear

bitr

age

629.

504.

546.

564.

412.

051.

4822

.117

.635

.935

.27.

807.

595.

734.

522.

171.

8123

.321

.430

.132

.4G

loba

lmac

ro54

11.3

86.

1611

.93

6.10

1.07

0.58

5.8

12.2

43.1

32.5

9.01

6.72

11.1

66.

500.

910.

736.

618

.944

.731

.2Lo

ng/S

hort

equi

tyhe

dge

520

14.5

98.

1415

.96

9.06

1.06

0.58

12.8

14.9

36.0

30.5

11.9

08.

9313

.90

8.69

1.04

0.77

9.8

16.7

42.0

28.5

Man

aged

futu

res

114

13.6

49.

3521

.46

12.0

70.

670.

392.

510

.240

.131

.511

.84

8.82

20.1

910

.94

0.66

0.52

4.0

14.9

37.0

28.3

Mul

ti-s

trat

egy

5910

.79

5.22

8.72

9.70

1.86

1.03

21.0

20.1

28.2

30.1

8.97

6.13

7.65

10.1

01.

861.

2518

.322

.529

.128

.6Fu

ndof

fund

s35

58.

253.

736.

364.

471.

660.

8623

.215

.027

.126

.37.

343.

955.

684.

291.

670.

9722

.616

.324

.026

.5A

llex

cept

fund

offu

nds

1255

13.2

98.

7113

.95

10.7

61.

391.

8815

.718

.333

.230

.911

.15

9.86

12.3

810

.12

1.38

2.64

13.5

19.8

36.6

29.8

Line

arcl

ones

Con

vert

ible

arbi

trag

e82

7.40

3.17

6.20

5.28

1.52

0.62

10.7

10.5

55.6

24.9

2.78

4.95

6.20

6.57

0.71

0.77

6.4

12.7

43.8

29.1

Ded

icat

edsh

ortb

ias

106.

7011

.59

28.2

710

.05

0.32

0.48

2.8

5.9

73.6

17.5

6.83

16.1

829

.31

15.6

10.

090.

450.

48.

836

.728

.7D

edic

ated

shor

tbia

s*9

3.61

6.61

28.7

510

.53

0.19

0.29

3.7

5.6

77.3

14.0

9.08

15.4

130

.00

16.3

90.

170.

40−0

.78.

536

.830

.4E

mer

ging

mar

kets

102

14.7

711

.47

22.9

215

.16

0.88

0.58

0.0

9.0

62.7

27.6

5.17

14.7

025

.04

17.9

40.

470.

667.

712

.442

.527

.3E

quit

ym

arke

tneu

tral

8310

.00

7.00

7.78

5.84

1.42

0.58

1.8

9.6

57.0

24.7

4.43

4.90

7.91

6.49

0.64

0.68

4.2

12.7

47.8

27.0

Even

tdri

ven

169

9.84

6.69

8.40

8.09

1.43

0.52

4.3

11.0

55.8

24.1

6.96

8.33

7.79

7.10

1.05

0.56

3.0

13.3

39.6

27.3

Fixe

din

com

ear

bitr

age

628.

355.

206.

564.

411.

480.

594.

18.

464

.429

.84.

474.

636.

855.

170.

840.

714.

39.

940

.830

.0G

loba

lmac

ro54

15.5

48.

3511

.93

6.10

1.41

0.55

2.6

8.3

52.2

23.8

12.9

78.

9012

.48

7.38

1.08

0.59

4.1

11.1

45.3

28.2

Long

/Sho

rteq

uity

hedg

e52

013

.12

8.68

15.9

69.

060.

980.

57−0

.110

.059

.726

.39.

0811

.03

15.8

310

.64

0.76

0.68

0.3

15.6

42.5

29.1

Man

aged

futu

res

114

27.9

716

.32

21.4

612

.07

1.36

0.40

4.7

8.1

61.4

29.0

19.2

413

.32

22.9

613

.71

0.91

0.57

5.5

10.9

46.5

27.7

Mul

ti-s

trat

egy

5910

.32

7.21

8.72

9.70

1.51

0.62

2.3