canada 1 january 2002 think canada thinkaerospace industry thinkinvestment think bottom line

TRANSCRIPT

Canada 1

January 2002

Think Canada

Think Aerospace Industry

Think Investment

Think Bottom Line

Canada 2

Aerospace - an Established Platform

Why Canada?

The Aerospace Edge

Summary

Canada 3

Canadian Aerospace and Defence… Performance Proven

• Approximately 700 firms with 93,000 employees

• Gross Sales of $20.5 Billion in 2000

• Invested approximately $900 Million in R&D (2000)

• Globally competitive with exports of 76% of output

• Extensively integrated in the global aerospace and defence industries

Source: Statistics Canada, Canadian Aerospace and Defence Sector Survey 2000/2001, December 2001.

Canada 4

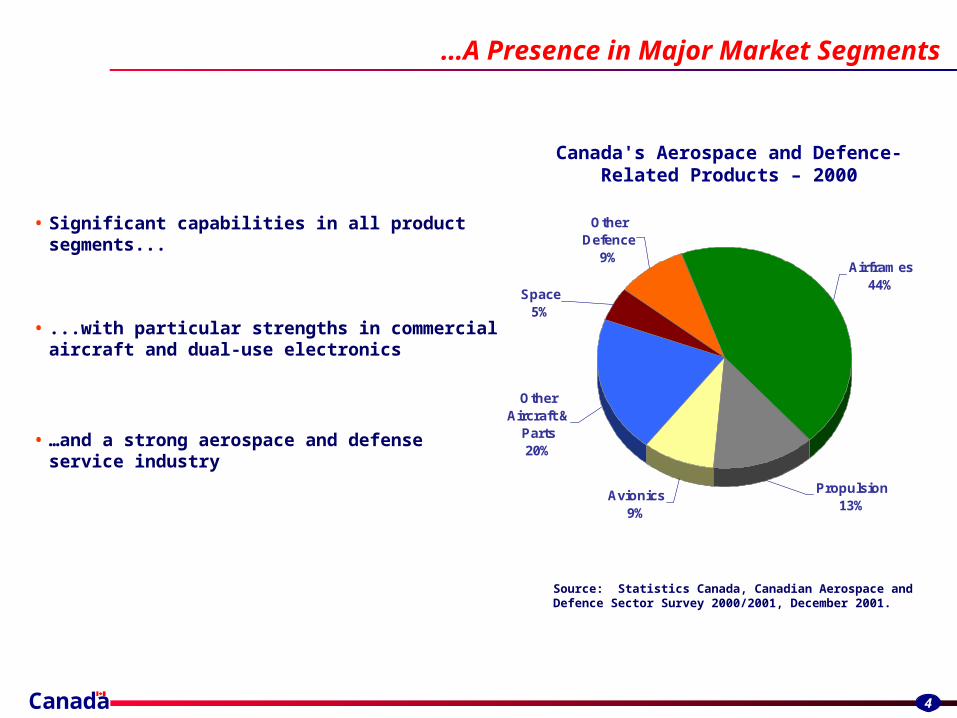

…A Presence in Major Market Segments

• Significant capabilities in all product segments...

• ...with particular strengths in commercial aircraft and dual-use electronics

• …and a strong aerospace and defense service industry

Canada's Aerospace and Defence-Related Products – 2000

Airframes44%

Other Defence

9%

Space5%

Other Aircraft &

Parts20%

Avionics9%

Propulsion13%

Source: Statistics Canada, Canadian Aerospace and Defence Sector Survey 2000/2001, December 2001.

Canada 5

A Continuously Strong Record of Performance...

• In 2000, aerospace sales by the G-7 totaled $189 billion $ U.S.

• Continued strong growth in past three years

• From 1976 to 1998, Canada’s share of world production more than tripled

• Canada was sixth in sales in 1999

Aerospace Output, 19997 Largest Western Aerospace Nations

(Based on Constant 1997 Prices and 1999 ECU’s)

Source: The European Association of Aerospace Industries (AECMA)

0

1

2

3

4

5

6

1993 1994 1995 1996 1997 1998 1999

Canada’s Share of Global Aerospace Sales(Based on Constant 1999 Prices and 1999 ECU’s)

2.43%

5.54%

6.37%

6.37%

11.63%

11.32%

56.34%

Italy

Canada

Japan

Germany

France

U.S.

U.K.

Source: The European Association of Aerospace Industries (AECMA)

0

5

10

15

20

25

30

1998 1999 2000 2001f 2002f

Exports Total Sales

AerospaceExports vs Total Sales

$ Billions

Source: Statistics Canada, Canadian Aerospace and Defence Sector Survey 2000/2001, December 2001.

Canada 6

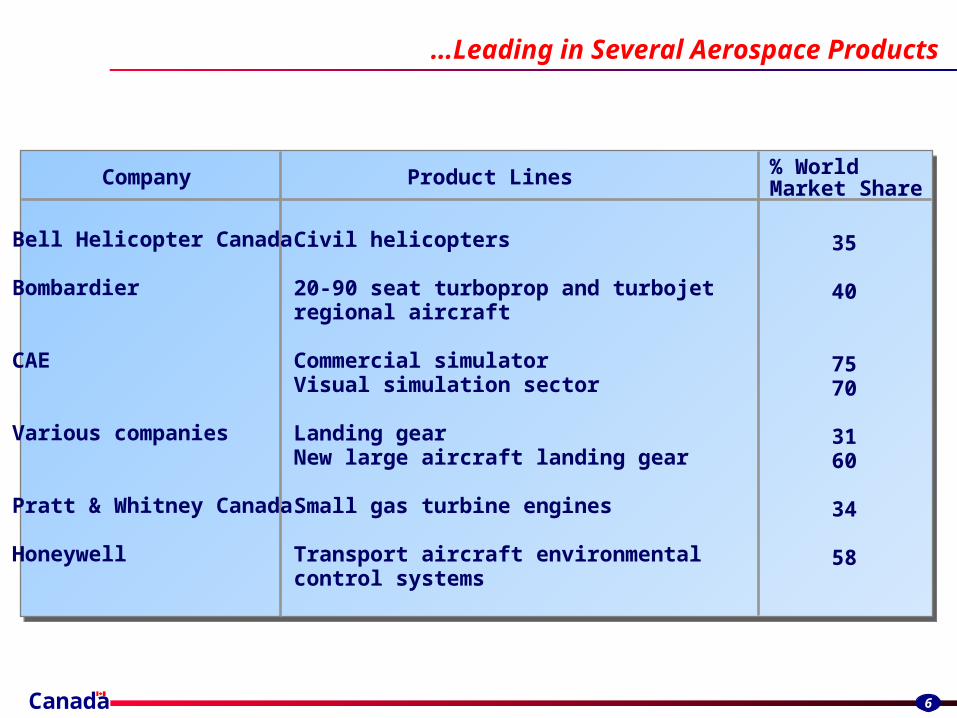

…Leading in Several Aerospace Products

Product LinesCompany % WorldMarket Share

35

40

7570

3160

34

58

Bell Helicopter Canada

Bombardier

CAE

Various companies

Pratt & Whitney Canada

Honeywell

Civil helicopters

20-90 seat turboprop and turbojet regional aircraft

Commercial simulatorVisual simulation sector

Landing gearNew large aircraft landing gear

Small gas turbine engines

Transport aircraft environmental control systems

Canada 7

...and Leading Edge Space Companies

• Strategic International Partnerships- USA (NASA) partner for over 3 decades - from Alouette to RADARSAT

- special relationship with the European Space Agency for over 2 decades

- only non-European country with quasi-associate status

- extensive bilateral cooperation with other European and Asian countries

• World - leading capabilities- space robotics and moveable spacecraft antennas (EMS and MD Robotics)

- many space microwave subsystems (COM DEV)

- turn-key earth observation data receiving, processing, archiving and distribution (MDA)

- Satellite communications systems consulting (Telesat)

- Synthetic Aperture Radar (MDA)

• Larger export proportion than other spacefaring nations

Canada 8

Aerospace - an Established Platform

Why Canada?

The Aerospace Edge

Summary

Canada 9

Canada: a Dynamic, Competitive Economy— Open for Global Business

Canada's economic fundamentals andrelative cost advantages provide afirst-rate business environment. Canada provides:

Excellent economic fundamentals

Report Card

Overall government budget in surplus.

Low inflation and low interest rates.

Easy access to marketsGeography and NAFTA provide easyaccess to the world's most prosperousmarket.

A cost-competitive businessenvironment

Large stock of skilled workers; low start-up costs; competitive tax system(particularly for R&D); strong technologicalenvironment; positive business climate.

An excellent place to live

Superb overall quality of life.

Canada 10

C

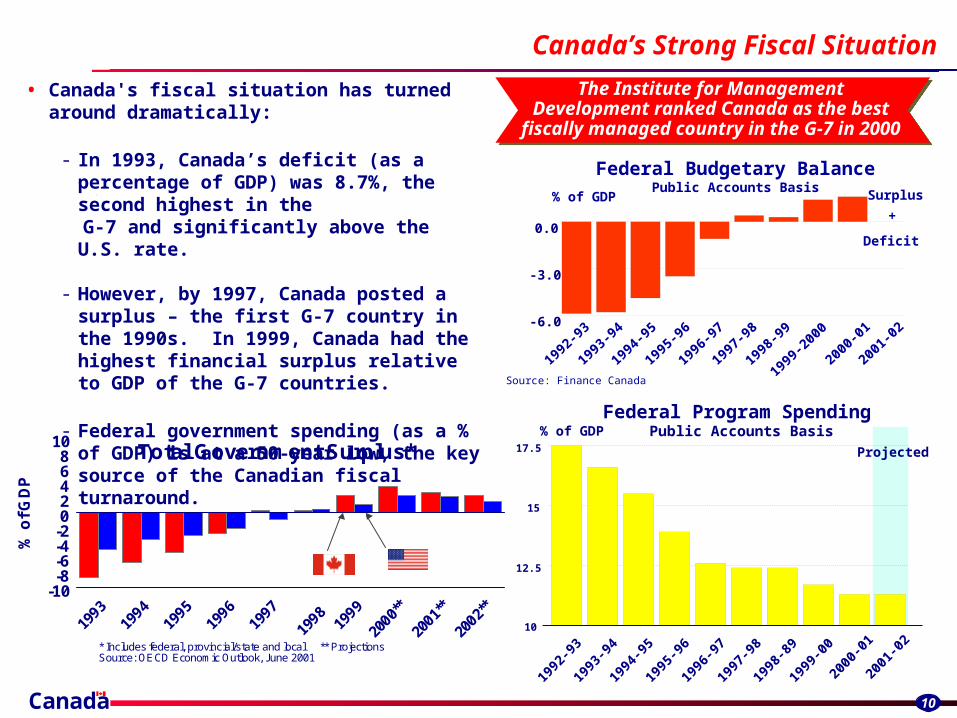

• Canada's fiscal situation has turned around dramatically:

- In 1993, Canada’s deficit (as a percentage of GDP) was 8.7%, the second highest in the

G-7 and significantly above the U.S. rate.

- However, by 1997, Canada posted a surplus – the first G-7 country in the 1990s. In 1999, Canada had the highest financial surplus relative to GDP of the G-7 countries.

- Federal government spending (as a % of GDP) is at a 50-year low, the key source of the Canadian fiscal turnaround.

Canada’s Strong Fiscal Situation

CC

The Institute for Management Development ranked Canada as the best fiscally managed country in the G-7 in 2000

Federal Budgetary BalancePublic Accounts Basis

Source: Finance Canada

0.0

-3.0

-6.0

% of GDP

1992

-93

1993

-94

1994

-95

1995

-96

1996

-97

1997

-98

1998

-99

1999

-200

0

2000

-01

2001

-02

Surplus

Deficit

+

Federal Program SpendingPublic Accounts Basis

1992

-93

1993

-94

1994

-95

1995

-96

1996

-97

1997

-98

1998

-89

1999

-00

2000

-01

2001

-02

10

12.5

15

17.5

% of GDP

Projected10

* Includes federal, provincial/state and local ** ProjectionsSource: OECD Economic Outlook, June 2001

Total Government Surplus*

1993

1994

1995

1996

1997

1998

1999

2000*

*

2001*

*

2002*

*

02468

-2-4-6-8

-10

% o

f G

DP

Canada 11

• The federal government and the Bank of Canada have an inflation target that locks the inflation rate in the 1% to 3% range.

- Over the past five years, Canadian inflation averaged 1.7% — 30% lower than the U.S. rate.

• Canada's excellent fiscal situation and low inflation are reflected In low domestic interest rates.

Low Inflation and Low Interest Rates

Sources: Statistics Canada and the Federal Reserve Bank of St. Louis

Source: Bank of Canada, Government long-term bond, last Wednesday in the month

Last data point plotted: October 31, 2001

Long-Term Interest Rates

1993 1994 1995 1996 1997 1998 1999 2000 20013

5

8

10

%

Inflation

93 94 95 96 97 98 9920

00 0

1

2

3

4

Yea

r-O

ver-

Yea

r %

Ch

an

ge

Canada 12

Streamlined Border Flows ...

• Since the enactment of the North American Free Trade Agreement (NAFTA) in 1994, Canada provides long-term assured access to the North American market — nearly 400 million people with a combined GDP of over $9.4 trillion ($U.S.).

• In addition to eliminating tariffs, NAFTA provides procedures for:

- border facilitation;- movement of personnel;- investment and intellectual property

protection; and- product certification.

• The North American market is serviced through a well integrated transportation system which is among world’s best.

- Automated permit ports, transponder identification systems and joint processing centres are being tested and deployed.

Source: Statistics Canada

Annual Transborder Crossings -Total Number of Trucks and Canada-US Air Passengers Entering Canada

Truck

Air

80 82 84 86 88 90 92 94 96 98 20000

5

10

15

20

Brian McGill, Director of TransportationPratt & Whitney Canada Inc.

"Pratt & Whitney has a worldwide distribution network. Customs operations have been streamlined to the point that the

Canada-US border plays no role in our distribution system."

Mil

lio

ns

of

Cro

ss

ing

s

Canada 13

...and Short Distances to Markets

• Almost half of the U.S. population lives within a 10 hour drive of Toronto, and over 60 percent within a two hour flight.

• Business travel between Canada and the U.S. has increased considerably since the inception of the “Open Skies*” Agreement (February, 1995)

• Direct air service between major cities in Canada and the U.S. has nearly doubled in 6 years.*Under “Open Skies” Canadian Air Carriers gained unlimited rights to establish routes from any point in Canada to any point in the United States. Similarly, U.S. carriers also gained unlimited access to the Canadian market (with a phase in period for up to three years)

Calgary Regina

Halifax

Los Angeles

Denver

New York

Boston

Philadelphia

Washington

BaltimoreDetroitChicagoCleveland

St. Louis Pittsburgh

Milwaukee

Houston

Atlanta

Vancouver

Toronto

Montréal

Seattle

Miami

Mexico City

San Francisco

Winnipeg

300 mi

600 mi Charlottetown

St. John's

Edmonton

VictoriaOttawa

Windsor

QuébecFredericton

Increase in TransborderRoutes Since Open Skies

89

165

Feb. 1995 Feb.2001

Source: Transport Canada

Direct Scheduled flights only.

Canada 14

• The overall skill level of Canada's workforce ranks high among competing countries.

• According to the Word Competitiveness Yearbook, Canada has the highest percentage of individuals achieving at least college or university education.

Superior Quality Workforce

“ High-tech companies are pursuing skilled peoplewherever they are available, and Canada has emerged asone of the top sources.”

Alan McMillian, CEO at PlanetIntra

* Percentage of the population that has attained at least tertiary education among 36 countries considered in the World Competitiveness Yearbook, 2001.

Canad

a

Japan U.S

.

France U.K

.

Germ

any

Italy

In

dex

1st 2nd

3rd

9th15th

20th

30th

Higher Education Achievement* World Rank

Canada 15

• According to the U.S. Bureau of Labor Statistics, labour costs in Canadian manufacturing (wage and non-wage) are the lowest in the G-7.

• Occupational wages are also lower in Canada for knowledge workers.

Low Labour Costs

* Figures are for 1999. Source: U.S. Bureau of Labor Statistics, September 2000

Cost of Labour — Manufacturing*

140

109100 94 86 86 81

Germany Japan U.S. France Italy U.K. Canada

$U.S

. p

er h

ou

r

U.S.=100

Occupational Wages — Knowledge Workers, 1999

* Canadian data have been converted to full-year assuming a 52-week work year.** Purchasing power parity for 1999*** date for computer programmers based on average for 1997, 1998, 1999Source: IC calculations based on Statistics Canada Labour Force Survey and U.S. Bureau of LabourStatistics Occupational Employment and Wage Estimates

Life Science Professionals

Physical Science Professionals

Computer Programmers***

Electrical and Electronic Engineers

Chief Executives

$49,469

$52,423

$54,960

$62,309

$101,240

Full-time, full-year wages* ($U.S. PPP**)

$42,097

$46,348

$36,467

$48,945

$59,608

Canada 16

• Canadian locations compare well internationally in terms of statutory corporate income tax rates.

The federal government and some provinces have announced sharp cuts in corporate taxes, to take effect over a five-year period.

The Economic Statement and Budget Update accelerated the pace of this tax relief.

• By 2005, firms in Canada will have a 5.1% corporate income tax rate advantage over U.S. firms (including capital tax).

Competitive Corporate Taxes

Source: Finance Canada

44.9%

41.5%

38.6%

35.6% 34.9%

40.0%

46.6%

Corporate Income Tax Rates including capital tax equivalents

2000 2001 2002 2003 2004 2005

Canada 17

Programs for Investing in Technology Development

In 2000, these government mechanisms contributed to R&D expenditures totaling $740 Million in the Canadian aerospace

sector, and accounted for 12% of total R&D expenditures

Canada’s aerospace and defence industries benefit from a list of programs including:

• Technology Partnerships Canada – risk-sharing partner in technology development

• National Research Council •Institute for Aerospace Research – aerospace R&D and testing •Industrial Research Assistance Program – support for small and medium-sized Canadian firms•The Aerospace Manufacturing Technology Centre (AMTC) – facilitate next generation

manufacturing, particularly among SMEs.

• Export Development Corporation (EDC) – export financing and insurance services

• Industrial and Regional Benefits (IRB) – industrial participation in major Crown procurements

• Defence Industry Research Program – financial and scientific support for industry-initiated research

• Granting councils – support university and project research through partnerships of universities with industry

• University Chairs – increase number of environmental university chairs in eco-efficiency areas (engineering, environmental science and business) in order to produce more graduates, enhance university research and strengthen research networks

• Canadian Commercial Corporation – guarantees contract performance for Canadian exporters, especially for sales to governments

Canada 18

• Canada's technological infrastructure is second only to the U.S. among the G-7 — we rank above or very close to the U.S. in terms of:

- internet users and internet hosts, - computers per capita, and- computer instructions per second.

• Building a universal, competitive, leading edge "Information Highway" is a government priority.

First-Class Technological Infrastructure

“Canadians are well known and respected around the world for developing advanced technology and also

for having good business and trade practices.”

Chris Piché, Chairman and CEO of West Vancouver-based Eyeball.com Network Inc. –

July 7, 2000

* Standing among 49 countries. Index based on 12 characteristics including investment in telecommunications, computers in use, computer power, internet connections, number of telephone lines, cost of telephone calls and use of robotics. Source: World Competitiveness Yearbook, 2001

I nd

ex

Technological Infrastructure*World Rank1st

6th

14th

19th15th

30th

23rd

CanadaU.S. U.K. JapanGermany ItalyFrance

Canada 19

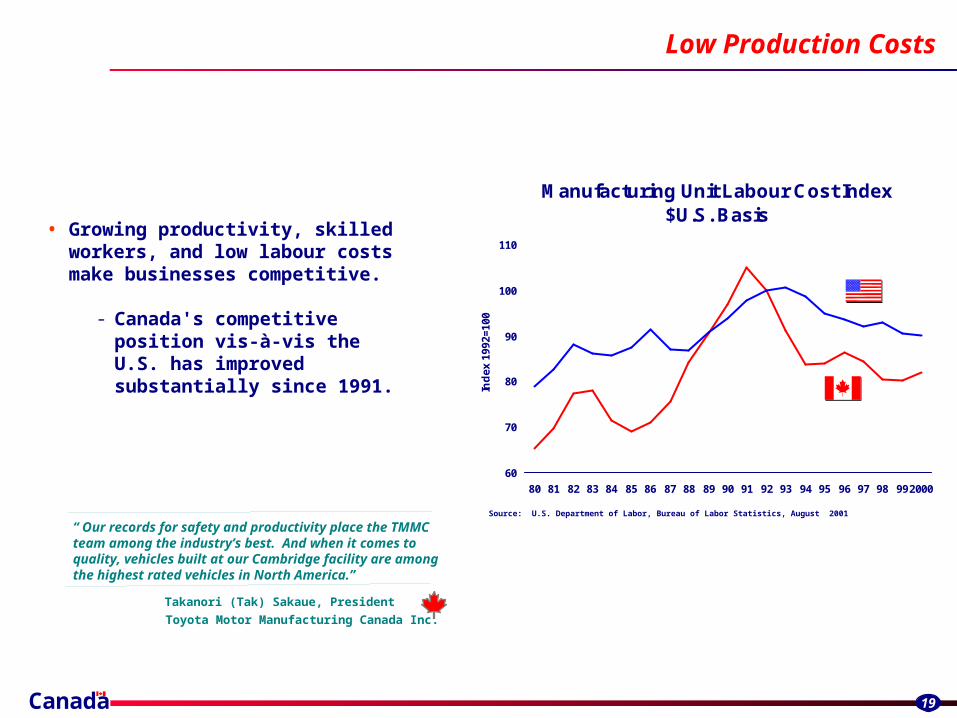

Low Production Costs

• Growing productivity, skilled workers, and low labour costs make businesses competitive.

- Canada's competitive position vis-à-vis the U.S. has improved substantially since 1991.

“ Our records for safety and productivity place the TMMCteam among the industry’s best. And when it comes to quality, vehicles built at our Cambridge facility are amongthe highest rated vehicles in North America.”

Toyota Motor Manufacturing Canada Inc.

Takanori (Tak) Sakaue, President

Manufacturing Unit Labour Cost Index $U.S. Basis

60

70

80

90

100

110

80 81 82 83 84 85 86 87 88 89 90 91 92 93 94 95 96 97 98 992000In

dex

199

2=10

0

Source: U.S. Department of Labor, Bureau of Labor Statistics, August 2001

Canada 20

Reasonable Cost of Living

• Canada has the lowest cost of living among the G-7.

• In particular, the cost of living in most large Canadian cities is better than or comparable to that in similar U.S. cities.

- And, Canadian cities rank better than U.S. cities in terms of the level of crime, pollution, environment and leisure facilities.

Cost of Living — World Rank*, 2001

Japan U.K

.

France Ita

ly

Germ

any

U.S.

Canad

a

Ind

ex:

New

Yo

rk C

ity

= 1

00

48th

42nd 35th 31st 27th 25th 20th

* Rank among 49 countries considered in the World Competitiveness Yearbook 2001Source: IMD

75100125150175

Canada 21

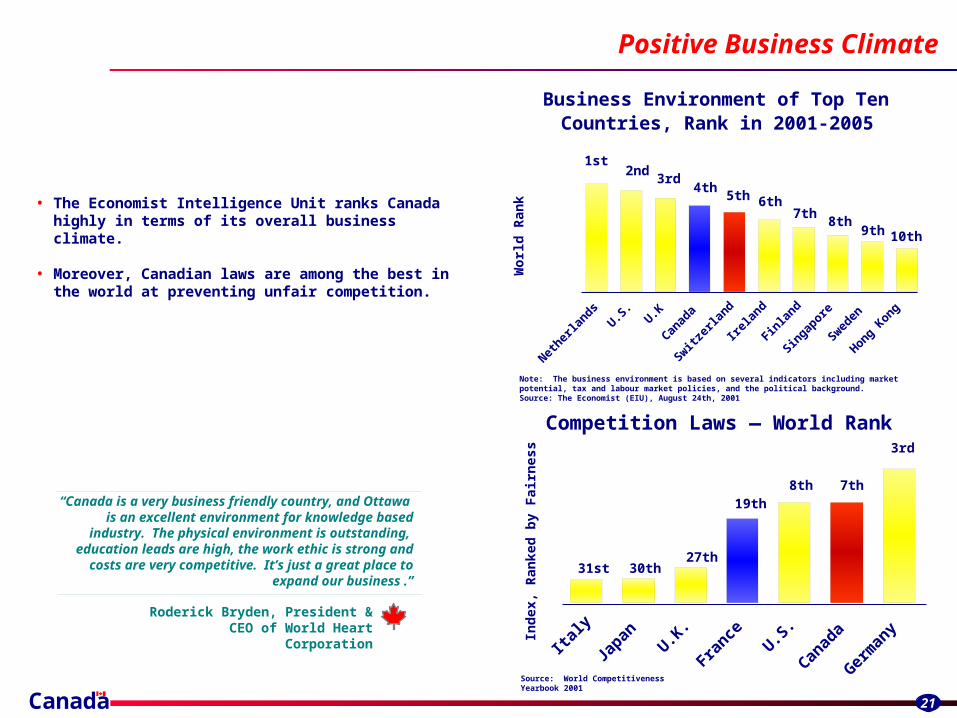

Positive Business Climate

• The Economist Intelligence Unit ranks Canada highly in terms of its overall business climate.

• Moreover, Canadian laws are among the best in the world at preventing unfair competition.

Note: The business environment is based on several indicators including market potential, tax and labour market policies, and the political background.Source: The Economist (EIU), August 24th, 2001

Business Environment of Top TenCountries, Rank in 2001-2005

Nether

lands

U.S.

U.K

Canad

a

Switzer

land

Irela

nd

Finla

nd

Singap

ore

Sweden

Hong Kong

Wo

rld

Ran

k

1st 2nd

3rd 4th

5th 6th 7th

10th9th8th

Competition Laws — World Rank

Italy

Japan U.K

.

France U.S

.

Canad

a

Germ

any

Ind

ex, R

anke

d b

y F

airn

ess

31st 30th27th

19th8th 7th

3rd

Source: World Competitiveness Yearbook 2001

“Canada is a very business friendly country, and Ottawa is an excellent environment for knowledge based

industry. The physical environment is outstanding, education leads are high, the work ethic is strong and

costs are very competitive. It’s just a great place toexpand our business .”

Roderick Bryden, President & CEO of World Heart Corporation

Canada 22

• The economic policies of the government of Canada are focused on making Canada a world leader in the global knowledge-based economy of the 21st century. Commitments include:

- Making Canada the most connected Government to its citizens by 2004.

- Making high-speed broadband access available to Canadians in all communities by 2004.

- Becoming one of the top five countries for research and development by 2010.

- Shaping a “National System of Innovation”; and

- Providing marketplace frameworks/services benchmarked against the best in the world.

Government as a Partner for the Knowledge Economy

“A knowledge-based workforce, a competitive R&D tax structure, government support programs such as

Technology Partnerships Canada, and well-established infrastructure in Canada: these attributes make Canada

the top choice for Pratt and Whitney in considering future R&D investments in the ever-competitive world of aerospace.”

Gilles P. Ouimet, PresidentPratt & Whitney Canada Inc.

Canada 23

Aerospace - an Established Platform

Why Canada?

The Aerospace Edge

Summary

Canada 24

Aerospace is a Proven Investment Platform...

Canadian-based companies offer investors unique opportunities

• Team with Canadian-based multinationals, including:

- Bombardier Aerospace – third largest commercial airliner manufacturer

- Pratt & Whitney Canada – small gas turbine power for the world

- CAE – corners the commercial flight simulator market

- Bell Helicopter Canada – one of the world’s leading commercial helicopter manufacturer

• Access capabilities of companies that supply the OEMs, e.g.:

- Avcorp – Winner of a Gold Award for entrepreneurial achievement at the Canadian Productivity Awards

- Haley Industries – one of the world’s most technologically advanced foundries

- NMF Canada – world leader in processing large, machined wing panels

- Spar Aviation Services – one of only 11 Lockheed-approved C-130 Maintenance and Modification Centres.

- Composites Atlantic – advanced composite components for commercial aircraft, space structures, rocket motor cases, etc.

Canada 25

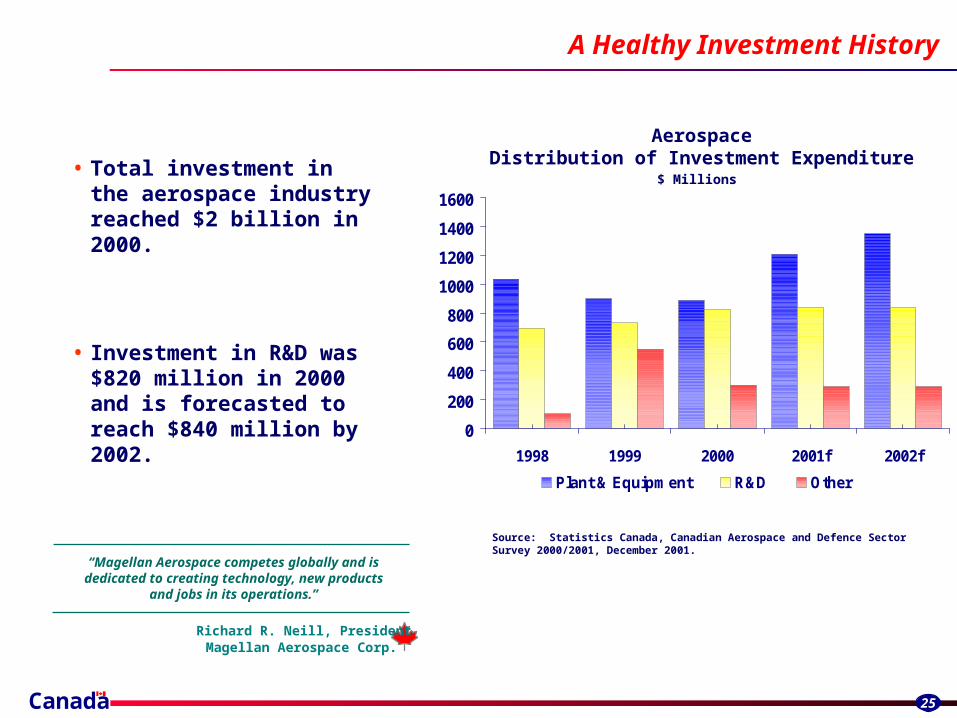

AerospaceDistribution of Investment Expenditure

$ Millions

0

200

400

600

800

1000

1200

1400

1600

1998 1999 2000 2001f 2002f

Plant & Equipment R&D Other

A Healthy Investment History

• Total investment in the aerospace industry reached $2 billion in 2000.

• Investment in R&D was $820 million in 2000 and is forecasted to reach $840 million by 2002.

“Magellan Aerospace competes globally and is dedicated to creating technology, new products

and jobs in its operations.”

Richard R. Neill, PresidentMagellan Aerospace Corp.

Source: Statistics Canada, Canadian Aerospace and Defence Sector Survey 2000/2001, December 2001.

Canada 26

Unique Access to the U.S. Market

• The U.S.A. consumes 50% of G-7 aerospace production with a strong domestic industry.

• Canada has a special relationship to access this market- For U.S. military purchases, Canada is considered part of the North American

Defence Industrial Base- Special trade agreements can facilitate participation in US military projects

Defence Production Sharing Agreement Defence Development Sharing Agreement

• The U.S. market accounts for the majority of Canadian aerospace and defence exports – on average $5B annually. Boeing alone purchases in excess of $800M from Canadian companies.

• 60% of the Canadian aerospace and defence industry output is attributed to subsidiaries of US firms operating in Canada – a high level of cross-border integration.

Canada 27

Some Investors Who Have Chosen Canada

Canada 28

Aerospace - an Established Platform

Why Canada?

The Aerospace Edge

Summary

Canada 29

• Canada's economic fundamentals are excellent — government policies are geared toward competitiveness.

• Canada provides assured access to the world's richest economy, in addition to having a large and growing domestic market of its own.

• Canada provides a cost-competitive and future-oriented environment for business:

- quality, productive workers;- a competitive tax system;- prime locations for R&D activities;- abundant energy at low prices; and- an excellent infrastructure.

• Canada is an outstanding place to live, invest and do business.

Canada Offers Much

David O'Blenis, President,Honeywell Canada

"Aerospace is truly a global business and these wins [move of Power Management and Generating systems to Toronto, expansion of plants in Montreal and Summerside, and

investment of more than $50 million in a new headquarters, engineering and

manufacturing facility] for Canada were made possible by the excellent business

climate here: sound fiscal management in the public sector, attractive R&D tax

incentives, and unique opportunities to partner with Governments to achieve growth.

It is clear to me that the decisions taken at the Corporate level of our global business to

focus our growth here show great confidence in Canada."

Canada 30

For more information:

Contact:

Aerospace and Automotive BranchIndustry Canada235 Queen StreetOttawa, Ontario K1A 0H5

Ron Watkins Nathalie CoutureDirector General Industry Development Officer(613) 954-3343 (613) [email protected] [email protected]

For more information, visit Strategis, Industry Canada’s award-winning Web site:

http://strategis.ic.gc.ca/aerodef_e

Canada 31

For more information (continued):

R&D Tax Credit:John JonesScience Policy CoordinatorScientific Research Section of Revenue CanadaTel.: (613) 941-1130Fax: (613) 957-3622e-mail: [email protected]

Technology Partnerships Canada (TPC):Jeffrey ParkerDeputy Executive Director and DirectorAerospace and DefenceIndustry CanadaTel.: (613) 941-6747Fax: (613) 954-9117e-mail: [email protected]