canada leads the global cannabis paradigm shiftfishn.ca/invest/58341.pdf · resources to invest in...

TRANSCRIPT

May 2018

This report was prepared by an analyst(s) employed by BMO Nesbitt Burns Inc., and who is (are) not registered as a research analyst(s) under FINRA rules. For disclosure statements, including Analyst’s Certification, please refer to pages 50 to 53. 16:00 ET~

This report is intended for Canadian & EU distribution only. Unauthorized reproduction, transmission orpublication without the prior written consent of BMO Capital Markets is strictly prohibited.

Tamy Chen, CFACannabis Analyst BMO Nesbitt Burns Inc.(416) [email protected]

Peter Sklar, CPA, CARetailing/Consumer Analyst BMO Nesbitt Burns Inc.(416) [email protected]

Initiating Aphria and Canopy at Outperform

Canada Leads the Global Cannabis Paradigm Shift

Table of Contents

Initiating BMO Cannabis Coverage ................................................................................................................... 2

Executive Summary .......................................................................................................................................... 4

Legal Environment Favours Canadian LPs ........................................................................................................ 6

Initial Recreational Market Outlook ................................................................................................................. 7

Current Medical Market in Canada: Opaque .................................................................................................. 13

Near-Term International Medical Opportunity: Germany ............................................................................. 15

Long-Term Industry Outlook ........................................................................................................................... 16

Company Snapshot: Our Current Coverage Universe ..................................................................................... 24

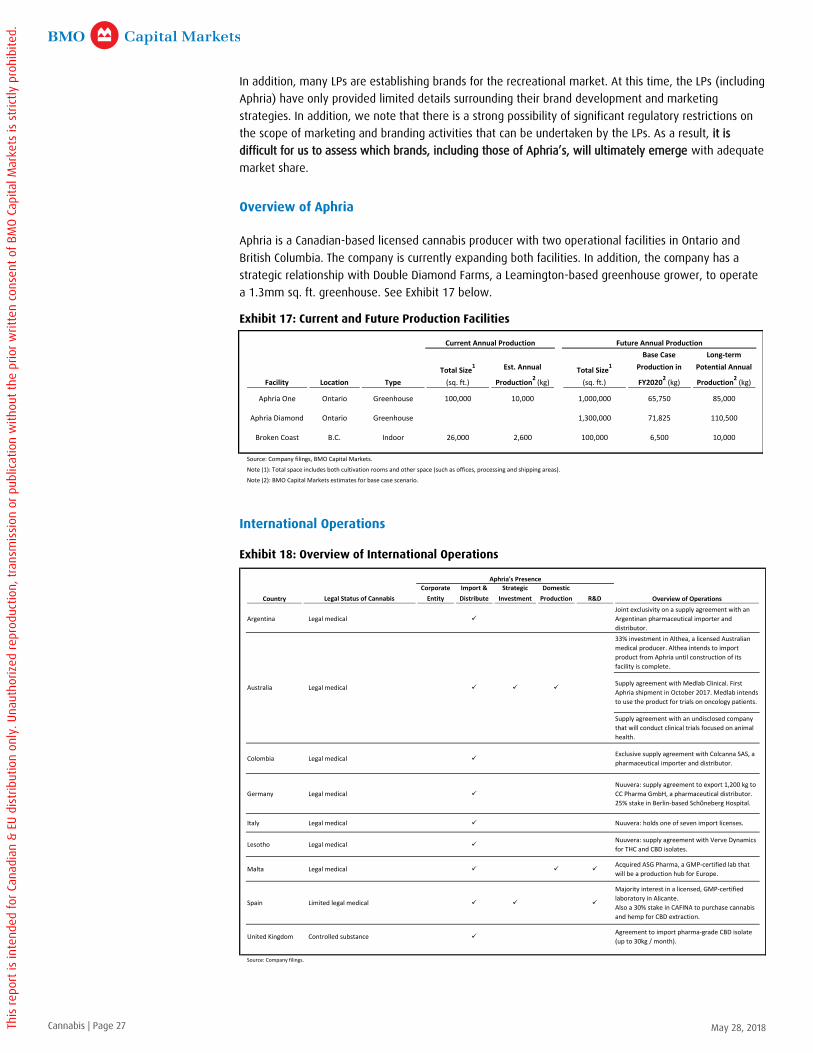

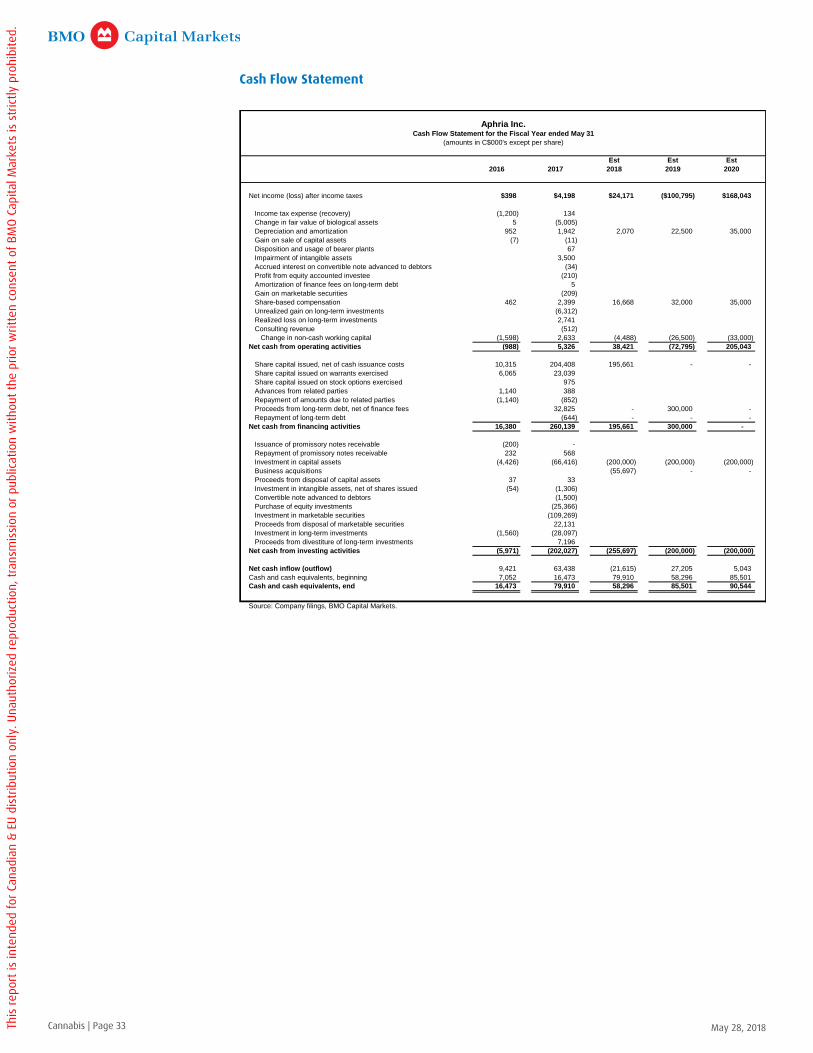

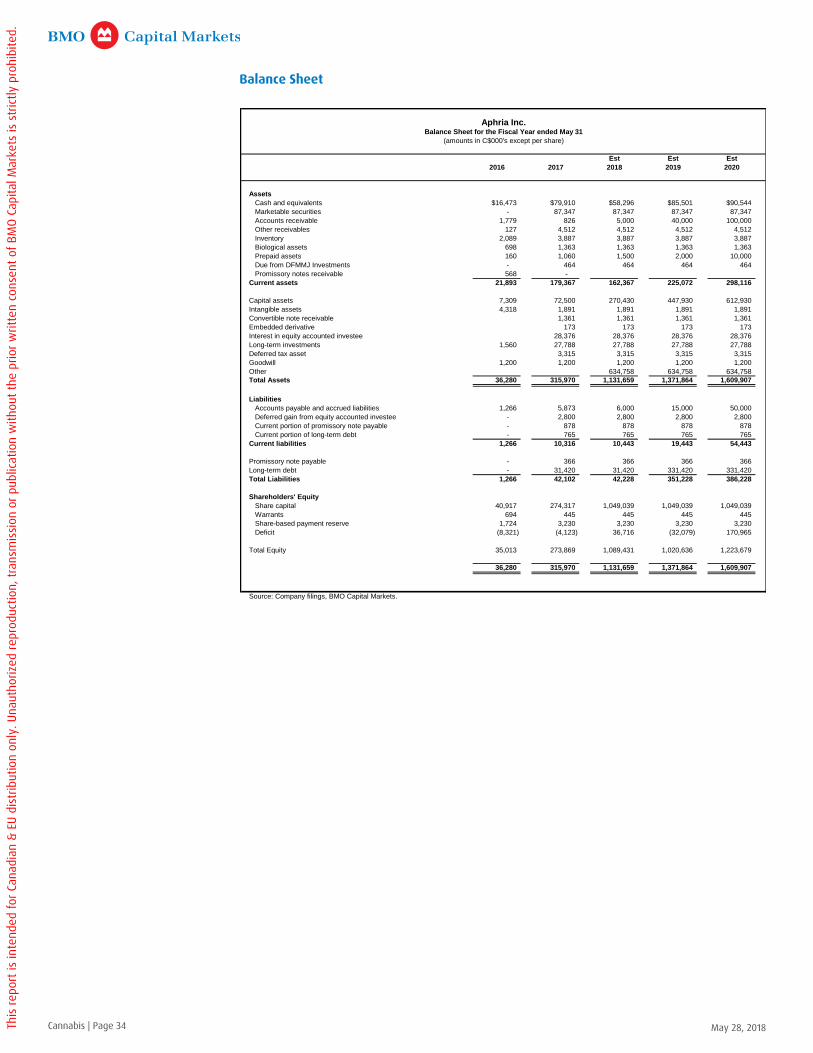

Company Coverage: Aphria ............................................................................................................................ 25

Company Coverage: Canopy ........................................................................................................................... 35

Comparable Companies - Cannabis ................................................................................................................ 46

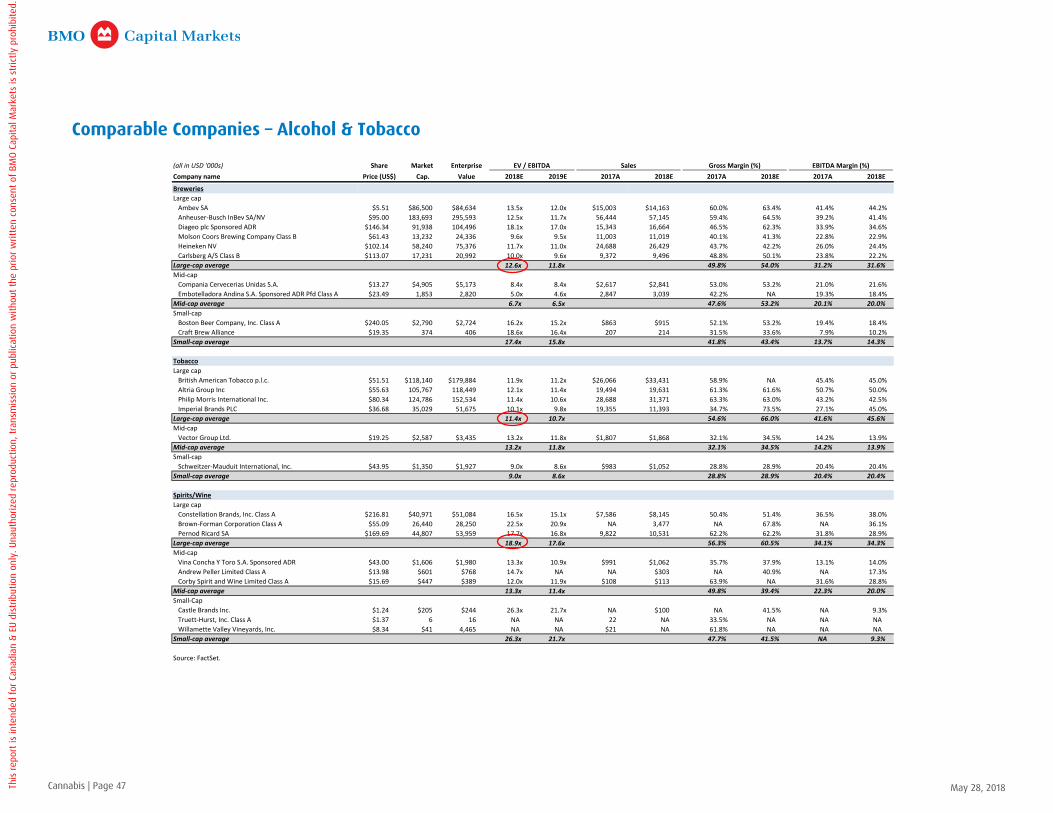

Comparable Companies – Alcohol & Tobacco ................................................................................................ 47

Glossary ........................................................................................................................................................... 48

Cannabis | Page 1 May 28, 2018This

repo

rt is

inte

nded

for C

anad

ian

& EU

dis

tribu

tion

only

. Una

utho

rized

repr

oduc

tion,

tran

smis

sion

or p

ublic

atio

n w

ithou

t the

prio

r writ

ten

cons

ent o

f BM

O Ca

pita

l Mar

kets

is s

trict

ly p

rohi

bite

d.

Initiating BMO Cannabis Coverage

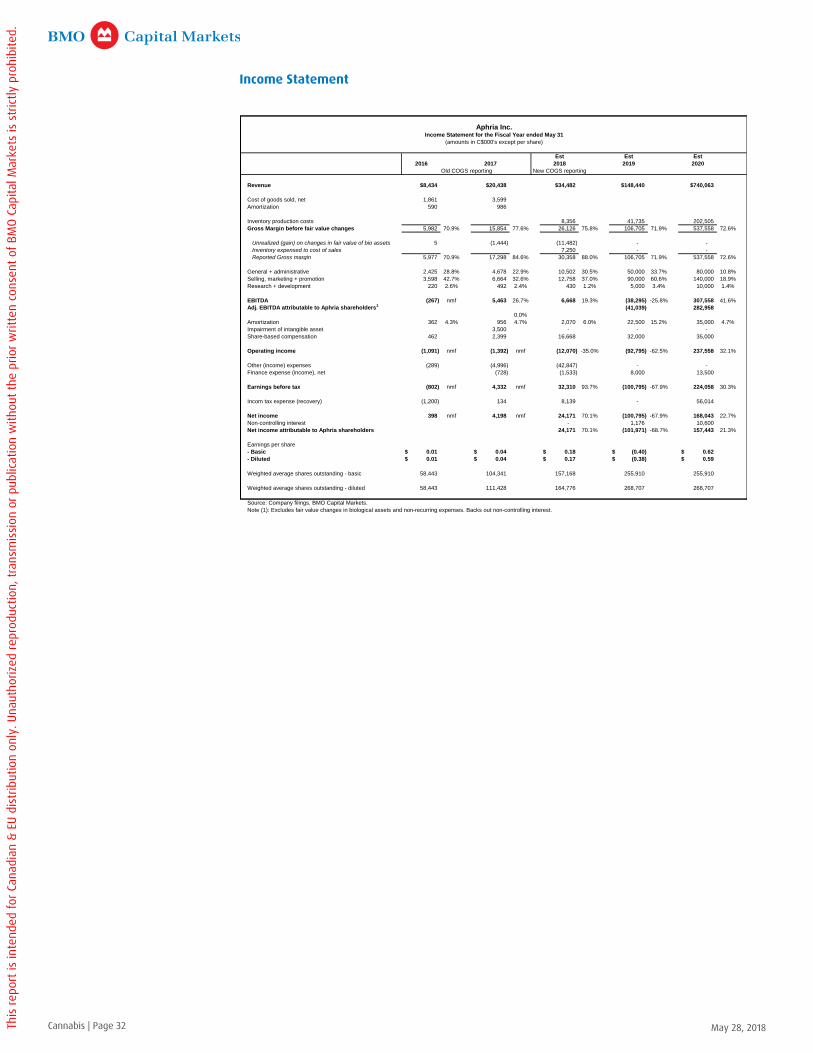

Aphria: We are initiating coverage of Aphria (APH-TSX) with an Outperform rating.

First Mover Advantage: We believe Aphria will be one of the few licensed producers (LPs) with sufficient

product to supply the initial recreational demand and we believe such a “first mover” advantage should

enable the company to quickly capture significant share and generate attractive unit economics in an

undersupplied market.

Leading Low-Cost Producer: We believe Aphria could emerge as a leading low-cost cannabis producer

given the significant commercial-scale greenhouse cultivation expertise held by the management team,

and the infrastructure and greenhouse culture that is inherent in the Leamington, Ontario community.

Scale Is Critical to Long-Term Growth: We believe Aphria’s scale will facilitate meaningful investment in

long-term growth opportunities such as brand development, value-add format manufacturing, the

gradual legalization of international medical markets, and advanced pharmaceutical applications.

Valuation: Our target price of $17 is based on a projected enterprise value that is about 17x our Base

Case fiscal 2020 EBITDA estimate. We note that our Base Case fiscal 2020 EBITDA estimate assumes that

Aphria’s facility expansions are only at 65% of full ramp potential versus management’s expectation

that the facilities will be close to 100% ramp by that time. If these facilities were to reach full ramp by

fiscal 2020 and Aphria experiences firmer selling prices, our implied target multiple would be in the

high-single-digit range. See Aphria company section for details.

Canopy: We are initiating coverage of Canopy (WEED-TSX) with an Outperform rating.

First Mover Advantage: We believe Canopy will be one of the few LPs with sufficient product to supply

the initial recreational demand and we believe such a “first mover” advantage should enable the

company to quickly capture significant share and generate attractive unit economics in an undersupplied

market.

Head Start in International: We consider the company’s current international operations to be more

advanced versus most other players, and Canopy appears to be laying the groundwork in markets where

medical is not yet legalized, but may soon be. The approach to develop cultivation in “hub” regions like

Denmark for export to Germany and eventually Australia for export to the Asia-Pacific region provides

the company longer-term access to these markets.

Long-Term Global Branded Leader: Canopy could emerge as a leader over the long term given that the

company’s scale will facilitate meaningful investment in long-term growth opportunities such as brand

development, value-add format manufacturing, the gradual legalization of international medical

markets, and advanced pharmaceutical applications. We believe Canopy’s strategic alliance with

Constellation Brands (STZ-NYSE; US$216.81; Outperform rated by Amit Sharma, BMO Capital Markets

Corp.) could prove to be a significant advantage as the industry evolves into value-add formats, and

particularly, into cannabis-infused beverages.

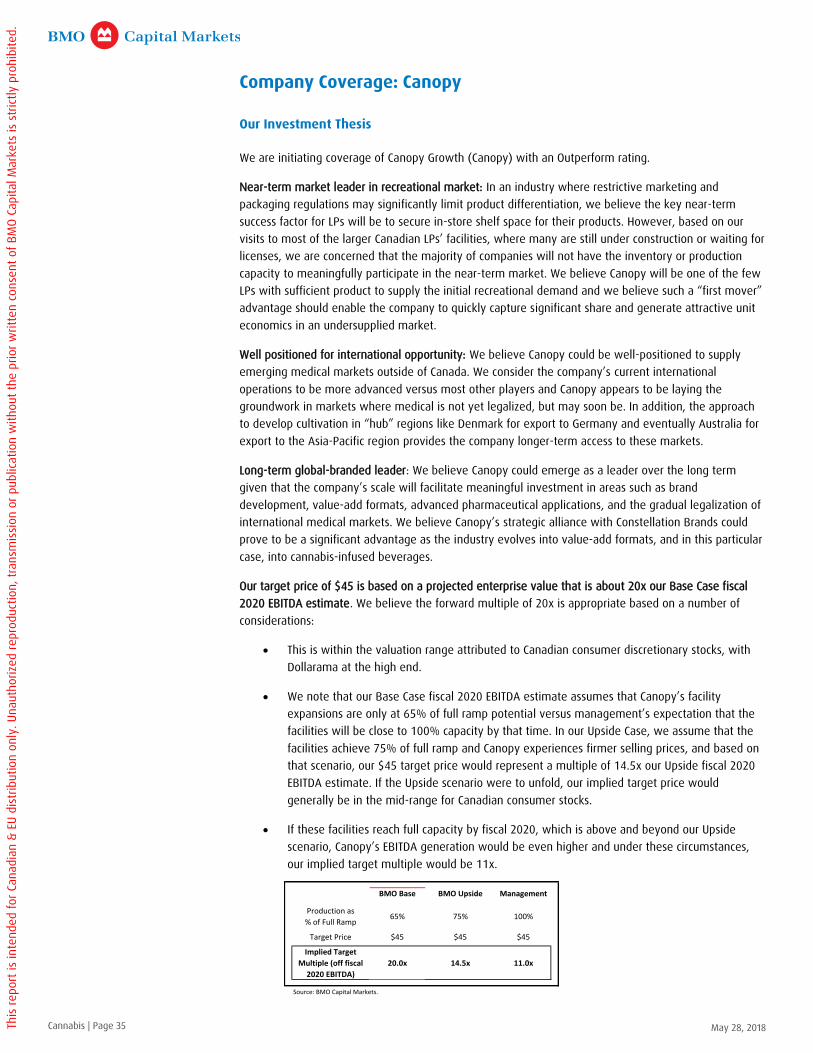

Valuation: Our target price of $45 is based on a projected enterprise value that is about 20x our Base

Case fiscal 2020 EBITDA estimate. Our target multiple reflects our view that Canopy has a relative head

start in brand development and international expansion, and could emerge as a leading global-branded

company in the long term. We note that our Base Case fiscal 2020 EBITDA estimate assumes that

Canopy’s facility expansions are only at 65% of full ramp potential versus management’s expectation

that the facilities will be close to 100% ramp by that time. If these facilities were to reach full ramp by

fiscal 2020 and Canopy experiences firmer selling prices, our implied target multiple would be 11x. See

Canopy company section for details.

Cannabis | Page 2 May 28, 2018This

repo

rt is

inte

nded

for C

anad

ian

& EU

dis

tribu

tion

only

. Una

utho

rized

repr

oduc

tion,

tran

smis

sion

or p

ublic

atio

n w

ithou

t the

prio

r writ

ten

cons

ent o

f BM

O Ca

pita

l Mar

kets

is s

trict

ly p

rohi

bite

d.

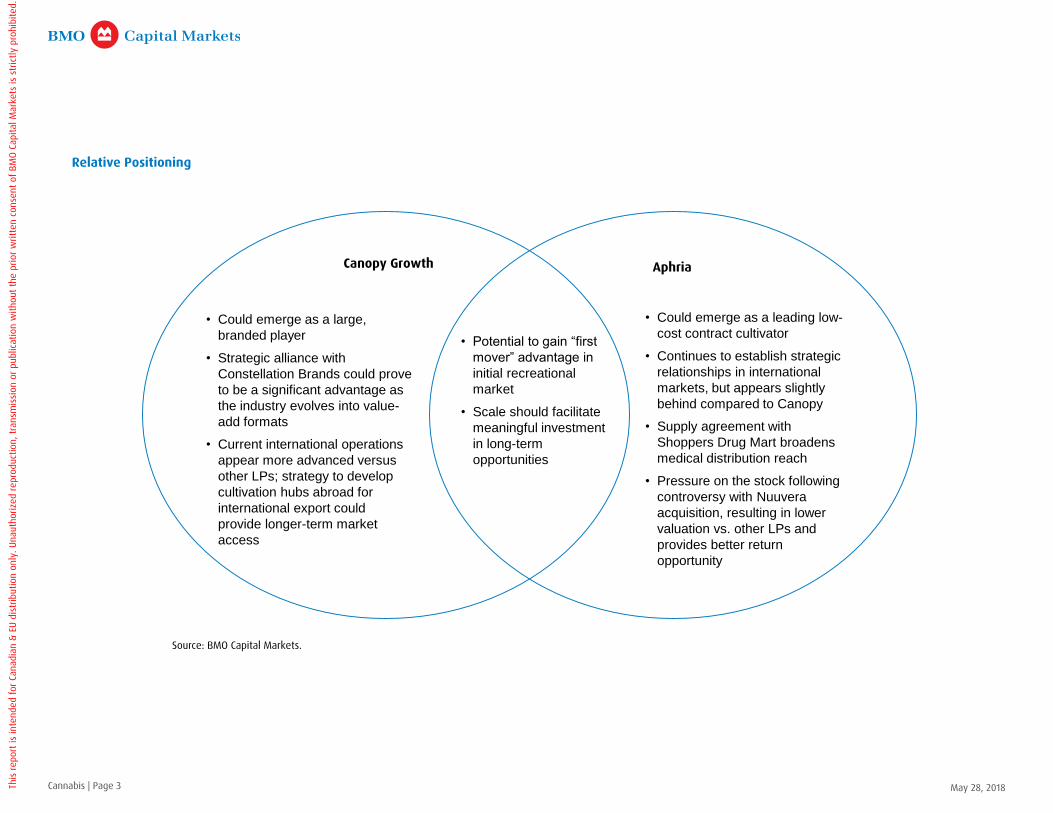

Relative Positioning

• Potential to gain “first

mover” advantage in

initial recreational

market

• Scale should facilitate

meaningful investment

in long-term

opportunities

• Could emerge as a large,

branded player

• Strategic alliance with

Constellation Brands could prove

to be a significant advantage as

the industry evolves into value-

add formats

• Current international operations

appear more advanced versus

other LPs; strategy to develop

cultivation hubs abroad for

international export could

provide longer-term market

access

• Could emerge as a leading low-

cost contract cultivator

• Continues to establish strategic

relationships in international

markets, but appears slightly

behind compared to Canopy

• Supply agreement with

Shoppers Drug Mart broadens

medical distribution reach

• Pressure on the stock following

controversy with Nuuvera

acquisition, resulting in lower

valuation vs. other LPs and

provides better return

opportunity

Source: BMO Capital Markets.

Canopy Growth Aphria

Cannabis | Page 3 May 28, 2018This

repo

rt is

inte

nded

for C

anad

ian

& EU

dis

tribu

tion

only

. Una

utho

rized

repr

oduc

tion,

tran

smis

sion

or p

ublic

atio

n w

ithou

t the

prio

r writ

ten

cons

ent o

f BM

O Ca

pita

l Mar

kets

is s

trict

ly p

rohi

bite

d.

Executive Summary

Near-Term Outlook

First Mover Advantage for Larger LPs: Initially, demand/supply dynamics will favour the larger

LPs. Anticipated demand from the initial recreational market in Canada is expected to

considerably exceed industry production as only a handful of the larger LPs will have sufficient

cannabis output at that time to meaningfully fill the distribution channels. As a result, this “first

mover” advantage should enable the larger LPs to benefit from the favourable pricing

dynamics expected in an initially undersupplied market. See Exhibit 3.

In addition, this “first mover” advantage should enable the larger LPs to initially dominate

retail shelf space in the recreational market, which would provide a head start for brand

development.

Value-Add Formats Will Mitigate Dried Flower Price Compression: We anticipate in year two of

our forecast that supply will begin to catch up to demand, which will result in some pricing

pressure on dried flower. However, our Base Case projections anticipate that in year two,

federal regulators will begin legalizing value-add product formats, which should carry much

higher pricing on a grams-equivalent basis and mitigate the pricing pressure that arises in

dried flower (see Exhibits 3 and 4).

Our Base Case forecast assumes that the industry growth rate for medical patient acquisition

slows when the recreational market is legalized. Some existing medical patients, and potential

future patients, could prefer the recreational market when legalized. However, this may be

more than offset if more employers begin to include medicinal cannabis under insurance

coverage plans.

Near-Term International Opportunity Favours Larger LPs: For the international export

opportunity, we expect that only a handful of the larger LPs will be able to secure the licensing

and certification requirements, and develop the necessary distribution infrastructure in those

regions.

Longer-Term Outlook

Supply Catches Up in Year Two of Recreational Legalization: We project that dried flower supply

will begin to catch up with demand in year two, and potentially exceed demand in the third or

fourth year following recreational legalization in Canada.

It is not clear if this projected supply/demand imbalance will weigh on the cannabis prices

realized by the LPs as there will be the opportunity to export increasing volumes of medical

cannabis to international markets, and the introduction of additional value-add product formats

should provide higher pricing to compensate for price compression in dried flower.

Evolution Into Either Branded Players or Low-Cost Cultivators: As dried flower prices continue to

settle, we believe the Canadian market will rationalize into a handful of larger, branded

players and a handful of low-cost contract cultivators. Beyond the branded companies and low-

cost contract growers, it is not clear to us how the many other LPs, outside of niche brands,

will survive under this pricing environment.

Cannabis | Page 4 May 28, 2018This

repo

rt is

inte

nded

for C

anad

ian

& EU

dis

tribu

tion

only

. Una

utho

rized

repr

oduc

tion,

tran

smis

sion

or p

ublic

atio

n w

ithou

t the

prio

r writ

ten

cons

ent o

f BM

O Ca

pita

l Mar

kets

is s

trict

ly p

rohi

bite

d.

Near-Term International Export Opportunity Is Temporary: We believe the current international

opportunity for Canadian LPs, which is the ability to export products into other markets at

favourable economics, will prove to be transitory. As a result, we believe the long-term global

opportunity for Canadian LPs is developing intellectual property and brands.

Long-Term Medical Market Opportunity in Pharmaceutical Applications: We believe the

distribution model for medical cannabis in Canada will eventually expand beyond the current

channel of direct-to-patient. In addition, we consider that Canadian LPs could eventually be in

a position to make efficacy claims that are supported by clinical trials. At that point, medical

cannabis could qualify for a Drug Identification Number, which we believe would be a

significant catalyst to accelerate growth of the medical market.

Scale Is Critical to Long-Term Growth: Over the long term, we anticipate that only a handful of

LPs will be attributed a premium valuation. These long-term industry leaders will be those that

capture sizable shares of the near-term recreational market, and possess the scale and

resources to invest in the long-term opportunities such as brand development, value-add

format manufacturing, the gradual legalization of international medical markets, and advanced

pharmaceutical applications.

It is also possible that these LPs could ultimately be acquired by large CPG players in the

beverage and tobacco industries or pharmaceutical companies given the potential disruption

cannabis-infused products could present.

The Blue Sky Scenario Beyond Our Forecasts: An additional long-term upside would be if other

jurisdictions consider recreational legalization, and we understand that Malta is currently

drafting legislation to legalize recreational use. If Malta establishes and implements a

framework legalizing the recreational market, we believe this could set a precedent that

encourages potential recreational legalization in other European countries. Under such a

scenario, Canadian LPs would have to establish cultivation in those markets in order to

participate as UN treaties prevent international trade of cannabis for non-medical purposes.

Cannabis | Page 5 May 28, 2018This

repo

rt is

inte

nded

for C

anad

ian

& EU

dis

tribu

tion

only

. Una

utho

rized

repr

oduc

tion,

tran

smis

sion

or p

ublic

atio

n w

ithou

t the

prio

r writ

ten

cons

ent o

f BM

O Ca

pita

l Mar

kets

is s

trict

ly p

rohi

bite

d.

Legal Environment Favours Canadian LPs

In Canada, medical cannabis was legalized in 2001, following court decisions, with the Marihuana

Medical Access Regulations (MMAR). Under this framework, approved individuals could grow cannabis or

appoint a designated person to grow for them. The MMAR framework was replaced by the Marihuana

for Medical Purposes Regulation (MMPR), which only permitted Health Canada approved commercial

licensed producers (LPs) to grow cannabis. Following a court ruling in 2016, the MMPR was replaced by

the Access to Cannabis for Medical Purposes Regulation (ACMPR), which is the current regulation

governing Canada’s medical market. The ACMPR framework allows patients to either purchase medical

cannabis from LPs or grow a limited amount on their own.

Following the election of the Trudeau government in 2015 and the report of the McLellan Task Force on

Legalization in December 2016, Bill C-45 was drafted as the proposed regulatory framework to legalize

recreational cannabis. On June 7, 2018, the Senate is scheduled to hold a final vote on Bill C-45.

However, there are a number of issues that could delay legalization. Provincial governments will receive

a period of eight to twelve weeks following the effective date of Bill C-45 in order to secure supply and

establish retail locations. In addition, some members of the Senate are recommending the federal

government delay Bill C-45 for up to a year to address concerns related to Indigenous communities,

although Prime Minister Trudeau has indicated that there will be no delay. We believe it is unlikely that

the recreational market will be legalized before the fall.

In the U.S., cannabis is considered by the federal government as a Schedule 1 narcotic, although several

states have legalized medical and recreational use. This federal-state conflict exists, in part, as a result

of the Ogden and Cole memoranda issued by the U.S. Department of Justice during the Obama

administration that deprioritized enforcement of the U.S. federal cannabis prohibition in certain

instances. These memoranda were rescinded pursuant to a memorandum issued by Attorney General

Jeff Sessions on January 4, 2018. As a result of the federal status of cannabis, U.S. cannabis companies in

legalized states are unable to supply international markets.

The international flow of cannabis, which is considered a controlled substance, is governed by three

United Nations treaties, and only permitted for medical purposes by countries with a legal federal

framework. Several countries have legalized medical cannabis, including Germany, Denmark,

Netherlands, Italy, and Australia, and more countries are expected to progress towards medical

legalization over the next several years. However, we note that Canada is the only developed country

with a comprehensive regulatory framework, permitting both medical consumption and domestic

cultivation. The lack of domestic production in many countries with legalized medical use has created

the opportunity for Canadian LPs to supply international markets.

Sizing Up the Industry in Canada

No. of Licenses1 104

Industry production in 20171 81k kg

Industry revenue in 20171 $239 mm

Prices in medical market4 $8 to $9 / g

Prices in illicit market4 $7 to $9 / g

Avg. annual yield for indoor3 100 to 300 g / sq. ft. / yr.

Avg. annual yield for greenhouse3 60 to 120 g / sq. ft. / yr.

Cost of production5 $1 to $2 / g

Note (1): Statistics Canada.

Note (2): Deloitte.

Note (3): BMO Capital Markets.

Note (4): Statistics Canada, company filings.

Note (5): Company filings. Excludes shipping & packaging.

Cannabis | Page 6 May 28, 2018This

repo

rt is

inte

nded

for C

anad

ian

& EU

dis

tribu

tion

only

. Una

utho

rized

repr

oduc

tion,

tran

smis

sion

or p

ublic

atio

n w

ithou

t the

prio

r writ

ten

cons

ent o

f BM

O Ca

pita

l Mar

kets

is s

trict

ly p

rohi

bite

d.

Exhibit 1: Top 10 Publicly Traded Companies (by Market Capitalization)

Note: BMO Capital Markets is restricted on Aurora Cannabis

Initial Recreational Market Outlook

We believe initial demand in the legal recreational market will likely be below many industry estimates.

This is based on our view that several factors will initially temper the level of illicit market displacement

(see Exhibit 2 below). For example, several provinces are only establishing a modest number of retail

stores in the first year of legalization, and it is not clear to us how prevalent e-commerce sales will be

initially. In addition, we are concerned that many of these stores will be situated in locations that are

too far from convenient urban centres (i.e., Ontario’s first four sites). Finally, we note that initial

recreational legalization will only permit three product formats: dried flower, oils, and gel capsules,

which is relatively limited compared to the breadth of categories available in the illicit market.

We believe meaningful displacement of the illicit market will take several years, but over the long term,

we expect consumers will participate in the recreational market due to the legality, safety, and

convenience of product formats that will be offered.

Exhibit 2: Key Factors Influencing Illicit Market Conversion

Source: BMO Capital Markets.

Company Ticker

Market Cap.

C$ mm Overview

Canopy Growth WEED $8,697 Facilities across Canada and a portfolio of medical and recreational targeted brands.

Aurora Cannabis ACB $4,793Constructing three hybrid facilities in Alberta and Northern Europe.

Announced acquisition of MedReleaf.

Aphria APH $3,198 Operating greenhouses in Leamington, focused on becoming a leading low cost producer.

MedReleaf LEAF $2,809 A premium-branded medical supplier. Announced it will be acquired by Aurora.

Cronos CRON $1,673 Indoor facilities in Ontario, recently established facility in Israel.

Hydropothecary THCX $1,179 Quebec-based, signed 5-yr Quebec supply agreement.

The Green Organic Dutchman TGOD $1,040Early-stage. Developing first facility to grow organic cannabis.

Signed uptake agreement with Aurora.

CannTrust TRST $877 Licensed producer. A leading player in the medical market.

Organigram OGI $788 NB-based, has a partnership with Colorado-based The Green Solution.

Cannabis Wheaton CBW $716Cannabis investment company.

Provides LPs with resources in exchange for financial or product uptake.

Source: BMO Capital Markets, company filings, FactSet.

The uptake in demand from existing illicit market users could be lower than expected if:

-There is an insufficient number of stores initially

-Stores are in inconvenient locations (such as the first four sites in Ontario)

-Other formats in the illicit market (edibles, concentrates) will not be permitted initially

-If retail prices are not competitive with the illicit market

Slower illicit market displacement could be countered by:

-New users who did not want to participate in the illicit market

-The migration of some medical patients whose underlying use was recreational

Cannabis | Page 7 May 28, 2018This

repo

rt is

inte

nded

for C

anad

ian

& EU

dis

tribu

tion

only

. Una

utho

rized

repr

oduc

tion,

tran

smis

sion

or p

ublic

atio

n w

ithou

t the

prio

r writ

ten

cons

ent o

f BM

O Ca

pita

l Mar

kets

is s

trict

ly p

rohi

bite

d.

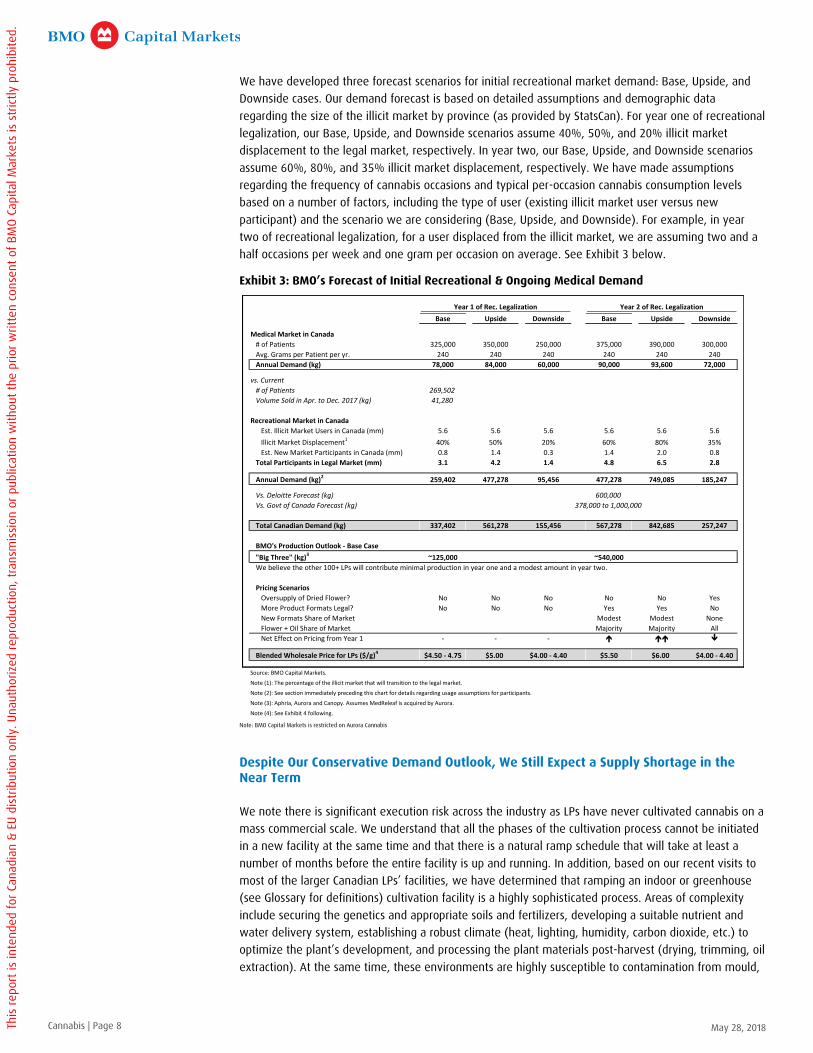

We have developed three forecast scenarios for initial recreational market demand: Base, Upside, and

Downside cases. Our demand forecast is based on detailed assumptions and demographic data

regarding the size of the illicit market by province (as provided by StatsCan). For year one of recreational

legalization, our Base, Upside, and Downside scenarios assume 40%, 50%, and 20% illicit market

displacement to the legal market, respectively. In year two, our Base, Upside, and Downside scenarios

assume 60%, 80%, and 35% illicit market displacement, respectively. We have made assumptions

regarding the frequency of cannabis occasions and typical per-occasion cannabis consumption levels

based on a number of factors, including the type of user (existing illicit market user versus new

participant) and the scenario we are considering (Base, Upside, and Downside). For example, in year

two of recreational legalization, for a user displaced from the illicit market, we are assuming two and a

half occasions per week and one gram per occasion on average. See Exhibit 3 below.

Exhibit 3: BMO’s Forecast of Initial Recreational & Ongoing Medical Demand

Note: BMO Capital Markets is restricted on Aurora Cannabis

Despite Our Conservative Demand Outlook, We Still Expect a Supply Shortage in the Near Term

We note there is significant execution risk across the industry as LPs have never cultivated cannabis on a

mass commercial scale. We understand that all the phases of the cultivation process cannot be initiated

in a new facility at the same time and that there is a natural ramp schedule that will take at least a

number of months before the entire facility is up and running. In addition, based on our recent visits to

most of the larger Canadian LPs’ facilities, we have determined that ramping an indoor or greenhouse

(see Glossary for definitions) cultivation facility is a highly sophisticated process. Areas of complexity

include securing the genetics and appropriate soils and fertilizers, developing a suitable nutrient and

water delivery system, establishing a robust climate (heat, lighting, humidity, carbon dioxide, etc.) to

optimize the plant’s development, and processing the plant materials post-harvest (drying, trimming, oil

extraction). At the same time, these environments are highly susceptible to contamination from mould,

Year 1 of Rec. Legalization Year 2 of Rec. Legalization

Base Upside Downside Base Upside Downside

Medical Market in Canada

# of Patients 325,000 350,000 250,000 375,000 390,000 300,000

Avg. Grams per Patient per yr. 240 240 240 240 240 240

Annual Demand (kg) 78,000 84,000 60,000 90,000 93,600 72,000

vs. Current

# of Patients 269,502

Volume Sold in Apr. to Dec. 2017 (kg) 41,280

Recreational Market in Canada

Est. Illicit Market Users in Canada (mm) 5.6 5.6 5.6 5.6 5.6 5.6

Illicit Market Displacement140% 50% 20% 60% 80% 35%

Est. New Market Participants in Canada (mm) 0.8 1.4 0.3 1.4 2.0 0.8

Total Participants in Legal Market (mm) 3.1 4.2 1.4 4.8 6.5 2.8

Annual Demand (kg)2259,402 477,278 95,456 477,278 749,085 185,247

Vs. Deloitte Forecast (kg) 600,000

Vs. Govt of Canada Forecast (kg) 378,000 to 1,000,000

Total Canadian Demand (kg) 337,402 561,278 155,456 567,278 842,685 257,247

BMO's Production Outlook - Base Case

"Big Three" (kg)3~125,000 ~540,000

We believe the other 100+ LPs will contribute minimal production in year one and a modest amount in year two.

Pricing Scenarios

Oversupply of Dried Flower? No No No No No Yes

More Product Formats Legal? No No No Yes Yes No

New Formats Share of Market Modest Modest None

Flower + Oil Share of Market Majority Majority All

Net Effect on Pricing from Year 1 - - -

Blended Wholesale Price for LPs ($/g)4$4.50 - 4.75 $5.00 $4.00 - 4.40 $5.50 $6.00 $4.00 - 4.40

Source: BMO Capital Markets.

Note (1): The percentage of the illicit market that will transition to the legal market.

Note (2): See section immediately preceding this chart for details regarding usage assumptions for participants.

Note (3): Aphria, Aurora and Canopy. Assumes MedReleaf is acquired by Aurora.

Note (4): See Exhibit 4 following.

Cannabis | Page 8 May 28, 2018This

repo

rt is

inte

nded

for C

anad

ian

& EU

dis

tribu

tion

only

. Una

utho

rized

repr

oduc

tion,

tran

smis

sion

or p

ublic

atio

n w

ithou

t the

prio

r writ

ten

cons

ent o

f BM

O Ca

pita

l Mar

kets

is s

trict

ly p

rohi

bite

d.

mildew, and bugs. As a result, we believe the majority of LPs, many of which are still developing their

facilities or waiting for licenses, will not have the inventory or production capacity to meaningfully

supply the initial recreational market.

Notwithstanding that our projection for demand is lower than other industry expectations, we would

expect that provincial governments will seek to fill the retail channel with a meaningful inventory level,

and on balance, we believe the initial recreational market will experience a supply shortage. We are

also concerned that some LPs that have been awarded supply contracts could experience difficulties

meeting their supply obligations in the near term. As a result, our view anticipates that the select few

LPs with sufficient inventory will be able to sell all that they can produce in the near term.

After the initial fulfillment of the provincial retail channels, our industry supply and demand outlook for

both medical and recreational markets indicate that total domestic demand will still exceed industry

supply in the second year post recreational legalization. As a result, we believe the LPs should be able to

continue to sell all that they can produce and pricing should be firm. We anticipate in year two of our

forecast that industry supply will begin to catch up to demand, which will result in some pricing pressure

on dried flower. However, our Base Case projections anticipate that federal regulators will begin to

legalize expanded product formats, such as vape pens, edibles, and beverages, which should carry much

higher pricing on a grams-equivalent basis. As a result, our Base Case scenario projects that blended

pricing per gram for the LPs will improve modestly in the second year of our forecast period (see Exhibit

4 below).

Exhibit 4: Product Mix on Blended Pricing

Provincial & Territorial Supply Contracts Are Critical to Participate in the Recreational Market

Overseeing the distribution of recreational cannabis will be the responsibility of the provincial/territorial

governments. Most provincial/territorial governments will purchase cannabis from LPs on a wholesale

basis to distribute into the retail channel, which includes both e-commerce and physical stores. As a

result of this regulated supply chain, securing provincial/territorial supply contracts will be critical for LPs

to access recreational markets.

We understand that there will be two typical avenues for LPs to access the provinces/territories: either

with a direct supply agreement with the province/territory, or by wholesaling to another LP that has a

provincial/territorial supply contract. We would assume that wholesaling to another LP generates lower

economics relative to a direct supply agreement, but we believe the majority of LPs will ultimately need

to wholesale to other LPs in order to participate in the provinces’/territories’ recreational markets. This

is based on our view that in the near term, provincial/territorial governments are primarily focused on

securing sufficient inventory and scope of product offerings to meet initial demand, a criterion that

should favour the larger LPs. We also believe the contractual wholesale price in these

provincial/territorial supply agreements could vary among the signed LPs as we understand that pricing

is determined through a negotiated process.

Dried

Flower

Oil & Gel

Capsules

Other Value-add

Formats Blended

Year 1 of Rec. Legalization

% of Market 90% 10% Not Legal 100%

Est. Wholesale Price (per gram) $4.50 $6.00 Not Legal $4.65

BMO Base Case from Exhibit 3 $4.50 - 4.75

Year 2 of Rec. Legalization

% of Market 70% 20% 10% 100%

Est. Wholesale Price (per gram) $4.00 $6.00 $15.00 $5.50

BMO Base Case from Exhibit 3 $5.50

Source: BMO Capital Markets.

Cannabis | Page 9 May 28, 2018This

repo

rt is

inte

nded

for C

anad

ian

& EU

dis

tribu

tion

only

. Una

utho

rized

repr

oduc

tion,

tran

smis

sion

or p

ublic

atio

n w

ithou

t the

prio

r writ

ten

cons

ent o

f BM

O Ca

pita

l Mar

kets

is s

trict

ly p

rohi

bite

d.

Certain regional LPs could also be well positioned to secure direct supply agreements in their home

province/territory as a result of the economic development created from their operations. However,

these regional LPs may be challenged to secure direct supply contracts in other provinces/territories,

which would limit their ability to grow on a national scale. The announced LP suppliers for Quebec,

Newfoundland & Labrador, New Brunswick, Prince Edward Island (PEI), and Yukon appear to support our

view that the LPs best positioned to secure direct supply agreements with the remaining

provinces/territories are likely to be the ones that can demonstrate an ability to supply a significant

amount of volume and/or are contributing to economic development in that province/territory. See

Exhibit 5 following.

The largest recreational markets should be Ontario and Quebec given the significant population in these

two provinces. However, we believe the opportunity to access the Quebec market through a direct

supply contract is now unavailable over the next few years for LPs other than the six that have entered

into agreements with the province: Aphria, Aurora (Restricted), Canopy, Hydropothecary, MedReleaf,

and Tilray. Only Hydropothecary has disclosed additional details of its supply agreement (see Exhibit 6

following). We also note that only Hydropothecary has a five-year contractual term to supply the

province, with an optional sixth year renewal at the government’s discretion.

Exhibit 5: Hydropothecary’s Expected Economics in Quebec

Unlike other provinces, the Ontario Cannabis Store (OCS) will secure supply through periodic product

calls, whereby the OCS will select LPs to purchase SKUs under contractual terms. On April 11, the OCS

announced the commencement of its first product call process. Selected LPs will be eligible to

participate in the OCS’s product calls over a contractual two-year term, but the OCS will not make any

volume commitments. Pricing will be set at a predetermined amount for the term.

Term 5-year

Frequency of purchases 4 orders / year

Product Offering Full range1

SKUs 63 initially

Expected Product Mix - initial 80% flower

Expected Product Mix - Later 30% flower

Per Gram Economics

Wholesale price2 $5.40

Less excise tax (1.00)

Revenue to Hydropothecary $4.40

All-in Cost - now $2.60 Margin

Est. EBITDA - now $1.80 41%

All-in-Cost - mgmt's outlook $2.00

Est. EBITDA - mgmt's outlook $2.40 55%

Source: Company press release.

Note (1): Dried flower, oils, Elixir spray product, capsules.

Note (2): Weighted average by product mix. Pricing could

change in later years depending on demand.

Cannabis | Page 10 May 28, 2018This

repo

rt is

inte

nded

for C

anad

ian

& EU

dis

tribu

tion

only

. Una

utho

rized

repr

oduc

tion,

tran

smis

sion

or p

ublic

atio

n w

ithou

t the

prio

r writ

ten

cons

ent o

f BM

O Ca

pita

l Mar

kets

is s

trict

ly p

rohi

bite

d.

Exhibit 6: Supply Chain for Recreational Market by Province/Territory

Source: Government websites. Note: BMO Capital Markets is restricted on Aurora Cannabis

Distribution

Announced Suppliers

Retail

Online

Stores

New Brunswick Nova Scotia PEI Yukon North West Nunavut

Govt (NB Liquor) Govt (NSLC) Govt (PEI LCC) Govt. Govt. Only NWTLC. No info yet.

Aphria, Canopy,

Hydropothecary,

Organigram (NB-based),

Zenabis (NB-based)

None announced

Canada's Island Garden

(PEI-based), Canopy,

Organigram

Canopy, Tilray None announced None announced

Govt. Govt. Govt. Govt. Govt. Will have online platform.

Govt. All 20 initial

locations have been

announced.

Govt. Allow co-location

with alcohol. 9 sites in

urban hubs announced.

More stores possible in

future.

Govt. 4 sites only.

At least 1 govt-run

location. May allow

private.

Govt. Initially inside

existing liquor stores.

Stand-alone stores are

possible in the future.

Govt and private. No

physical stores expected

in 2018.

British Columbia Alberta Manitoba Saskatchewan Ontario Quebec Newfoundland

Distribution Govt (BC LDB) Govt (AGLC) Govt (LGA)Private. Regulated by

govt (SLGA).

Govt (OCS) via product

calls.Govt (SAQ)

Private. LPs will sell

directly to stores.

Announced Suppliers None announced None announced None announced None announcedFirst product call

process under way

Aphria, Aurora, Canopy,

Hydropothecary (QC-

based), MedReleaf,

Tilray

Canopy

Retail

Online Govt. Govt. Private. Private.Govt. Partnered with

Shopify.Govt. Govt.

Stores

Govt and private.

Unlimited private

licenses.

Private. 250 licenses

expected in the first

year.

Private.

Private. Licenses issued

lottery-style. Only 51

licenses in 32

municipalities, which can

opt-out (5 have).

Govt. 150 stores by

2020. 40 openings in

2018, 40 in 2019.

Announced first 4

locations.

Govt. Initially 15 stores.Private. Announced 41

licenses.

Cannabis | Page 11 May 28, 2018This

repo

rt is

inte

nded

for C

anad

ian

& EU

dis

tribu

tion

only

. Una

utho

rized

repr

oduc

tion,

tran

smis

sion

or p

ublic

atio

n w

ithou

t the

prio

r writ

ten

cons

ent o

f BM

O Ca

pita

l Mar

kets

is s

trict

ly p

rohi

bite

d.

Read-Throughs From Quebec and Ontario Supply Arrangements

In the near term, we believe the retail price (pre-HST) for dried flower will generally range

between $7 and $9 per gram and the wholesale price to LPs will range between $4 and $5 per

gram.

We believe the provinces will need to make several significant adjustments over the near term

in the quantity and type of products they purchase as they develop a better understanding of

consumer preferences as a result of actual point-of-sale purchases. This presents a risk to LPs if

demand for their product SKUs is materially lower than anticipated.

Who Will Win in the Near Term? Will Branding Help?

Heading into the recreational market, we note that the strategy being adopted by most LPs is to

establish brands through “lifestyle” associations to experiences such as the outdoors, health and

wellness, music, art, or to specific celebrities. There is a view among LPs that branding, particularly if

communicated to consumers before legalization, will create brand recognition and encourage in-store

purchase when the market is legal.

However, we believe federal regulations will restrict the marketing reach of products intended for the

recreational market. For example, we note that MedReleaf cancelled the Quebec launch of its San Rafael

’71 brand in April 2018 following concerns from the provincial government that the brand’s lifestyle

positioning may be in violation of proposed Bill C-45 regulations. In addition, recent proposals from

Health Canada, if enforced, would materially impair the LPs’ ability to convey their brand in-store via

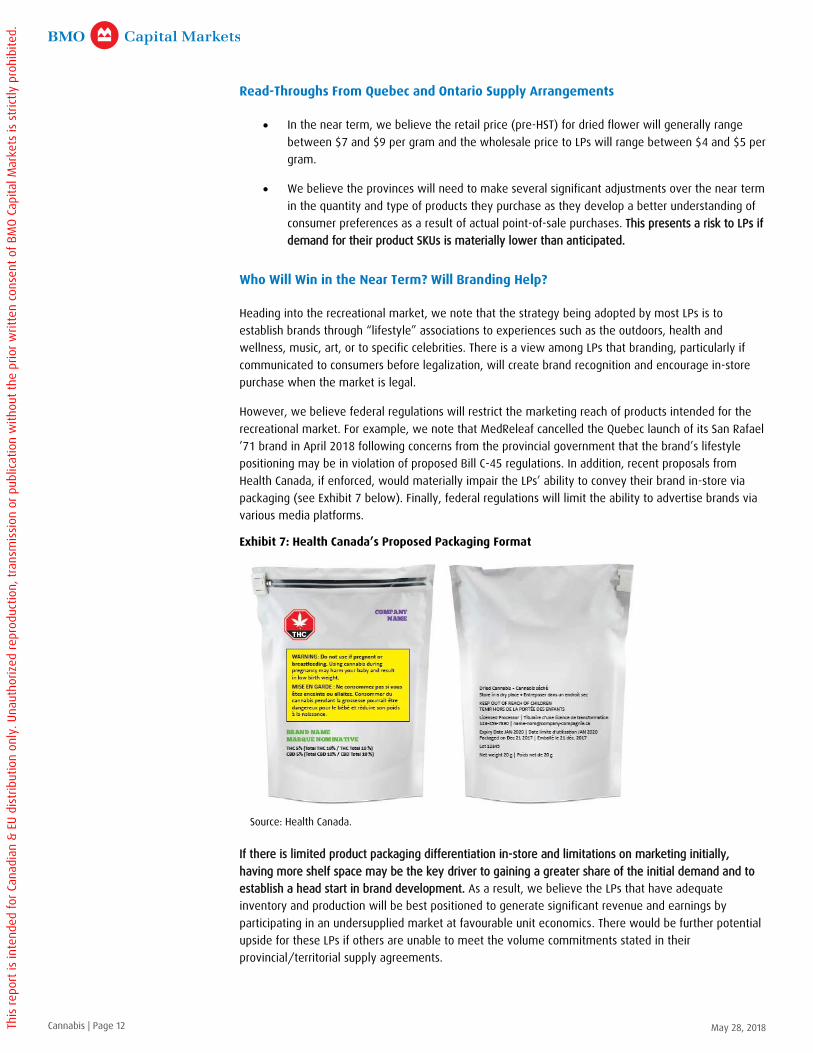

packaging (see Exhibit 7 below). Finally, federal regulations will limit the ability to advertise brands via

various media platforms.

Exhibit 7: Health Canada’s Proposed Packaging Format

If there is limited product packaging differentiation in-store and limitations on marketing initially,

having more shelf space may be the key driver to gaining a greater share of the initial demand and to

establish a head start in brand development. As a result, we believe the LPs that have adequate

inventory and production will be best positioned to generate significant revenue and earnings by

participating in an undersupplied market at favourable unit economics. There would be further potential

upside for these LPs if others are unable to meet the volume commitments stated in their

provincial/territorial supply agreements.

Source: Health Canada.

Cannabis | Page 12 May 28, 2018This

repo

rt is

inte

nded

for C

anad

ian

& EU

dis

tribu

tion

only

. Una

utho

rized

repr

oduc

tion,

tran

smis

sion

or p

ublic

atio

n w

ithou

t the

prio

r writ

ten

cons

ent o

f BM

O Ca

pita

l Mar

kets

is s

trict

ly p

rohi

bite

d.

It is also likely that restrictions on marketing and packaging could cause a large portion of consumers to

simply seek the highest-potency strains (i.e., high in THC and/or CBD). In this scenario, LPs with more

product offerings in high-potency strains could be better positioned to capture more demand. If

Canadian consumers focus on specific strains, the recreational market will be comparable to Colorado,

where dried flower branding is at the strain level and differentiation is based on qualities of that strain,

including efficacy, potency, and consistency. We note that popular strains in those states are able to

command premium pricing. If differentiation in the Canadian recreational market is based on strains, it

could undermine the branding strategies of many LPs.

On the other hand, there is a view that strain-level branding is unique to Colorado due to the state’s

fragmented landscape of regional producers specializing in specific strains and regulations that facilitate

a “deli-style” retail environment. Dried flower is not pre-packaged and instead, is placed in containers

for customers to purchase, much like a deli counter. In Washington, where dried flower is pre-packaged,

there are company-level brands, similar to ones being developed by Canadian LPs. As well, we believe

strain-level branding will become less relevant as value-add products with cannabis extracts, such as

vape pens and consumables, are introduced.

Branding Power May Be Limited In-Store; Can Budtenders Bridge the Gap?

While brands could develop consumer awareness and influence in-store purchasing, we believe

branding power may be limited if it is not communicated or promoted by the in-store sales staff (also

known as budtenders). When we visited cannabis dispensaries in Denver and LA, we found that

budtenders play a crucial role in consumer education and product recommendations, which are based on

personal experiences and third-party user feedback.

Specific to Canada, where packaging designs could be limited and consumers may be focused on specific

strains, it would be the budtender’s role to differentiate the products, and in particular, highlight the

variances of otherwise genetically similar strains grown by different LPs. We note that several LPs could

be cultivating the same strain for the recreational market and while the strain’s core genetic profile is

the same, qualities such as potency, efficacy, and consistency may differ as a result of the particularly

environment it is grown in (also known as the plant’s phenotype).

We are concerned that initially, budtenders may not have sufficient knowledge to effectively

communicate the differences between products and segment them based on perceived quality. In

addition, we believe there is a risk that provinces/territories could limit the channels in which LPs can

establish partnerships with the sales staff. For example, we understand that Ontario’s regulations will

prohibit budtenders from making brand recommendations, although they will be permitted to provide

factual information about the product such as the terpene profile and potency level. As a result of the

restrictive regulations on marketing, branding, and budtenders, we believe the initial successful LPs will

be companies with sufficient products to fill the retail channel and maximize shelf space.

Current Medical Market in Canada: Opaque

According to Statistics Canada, there are currently 269,500 registered medical cannabis patients in the

country. A widely disclosed metric by LPs is the number of patients they have onboarded as there is a

perception that the number of patients registered with an LP is indicative of the company’s share of the

Canadian medical market. However, we believe this metric alone is a misleading measure for market

share as patients can register with more than one LP, a patient may be registered with the LP but not

actively ordering products, or a LP could have fewer registered patients but higher average consumption

per patient. In addition, we believe there is currently no standardized definition of an “active” patient.

Cannabis | Page 13 May 28, 2018This

repo

rt is

inte

nded

for C

anad

ian

& EU

dis

tribu

tion

only

. Una

utho

rized

repr

oduc

tion,

tran

smis

sion

or p

ublic

atio

n w

ithou

t the

prio

r writ

ten

cons

ent o

f BM

O Ca

pita

l Mar

kets

is s

trict

ly p

rohi

bite

d.

As a result, we believe it is important to consider the volume sold, reported revenues, number of

registered patients, and implied average consumption per patient (see Exhibit 8 below).

Exhibit 8: Key Publicly Traded Players in the Canadian Medical Cannabis Market

Note: BMO Capital Markets is restricted on Aurora Cannabis

We find the current Canadian medical market to be opaque with respect to patient acquisition and

churn. Physicians can either directly prescribe their patients for medical cannabis or refer them to a

cannabis clinic. In the former, the physician will prescribe a specific dosage, and can also provide product

recommendations. Alternatively, the physician can refer the patient to a cannabis clinic where the

patient can access further information about which products would be most suitable for their needs.

We understand that both prescribing physicians and cannabis clinics are typically receiving “education

fees” from LPs. This may prove to be an inappropriate payment that will eventually be addressed by

medical regulators. The challenge in assessing the prevalence of this fee is the lack of disclosure,

including the amount typically charged by clinics and physicians. Our view is that since cannabis is closer

to an alternative natural health product than a pharmaceutical drug and has no clinical trials, the primary

channel for LPs to acquire patients is to encourage physicians through strategic partnerships and

cannabis clinics. As a result, we believe these education fees likely represent significant patient

acquisition costs for LPs and we have heard anecdotally that they can represent about 15% of the LP’s

selling price.

We also consider churn to be a key metric in assessing the competitive dynamics of the medical market.

However, there is a lack of disclosure by LPs on this measure and any approximation is challenged by

the continued growth in the overall Canadian medical market. Based on our understanding of the

industry, we believe churn could be quite high as cannabis products have a wide range of efficacy

depending on the individual, and it is likely that patients are trialing numerous LPs’ products to

determine the best one(s) for their needs.

Supply & Demand in the Medical Market When Recreational Is Legal

We believe there could be some material changes in both the level of supply and demand in the

medical market when the recreational market is legalized. Some existing patients, and potential future

patients, could prefer the recreational market given that the latter provides relatively easier access to

cannabis than the medical prescription process. However, this may be more than offset if more

employers begin to include medicinal cannabis under insurance coverage plans. In addition, medical

expenses are tax deductible above a certain threshold. Overall, our Base Case forecast assumes that the

industry growth rate for medical patient acquisition slows when the recreational market is legalized. On

the supply side, we believe there will likely be a tighter market for medical cannabis in the near term as

we expect that most LPs will prioritize their inventory to gain a share of the recreational market.

Last Quarter Last Quarter

Volume Sold

(kg)

Share of

Volume # Patients

Share of

Patients

Grams per

patient

Avg. Selling

Price ($ / g)

Canada 15,616 269,502 58

Canopy 2,330 15% 69,919 26% 33 $8.30

Aurora 1,353 9% 45,776 17% 30 $7.99

MedReleaf 1,263 8% n.a. n.a. $8.64

Aphria1~1,000 6% ~40,000 15% 25 $8.30

CannTrust 982 6% 40,000 15% 25 $7.63

Source: Company filings.

Note (1): Excludes wholesale to other LPs.

Cannabis | Page 14 May 28, 2018This

repo

rt is

inte

nded

for C

anad

ian

& EU

dis

tribu

tion

only

. Una

utho

rized

repr

oduc

tion,

tran

smis

sion

or p

ublic

atio

n w

ithou

t the

prio

r writ

ten

cons

ent o

f BM

O Ca

pita

l Mar

kets

is s

trict

ly p

rohi

bite

d.

Near-Term International Medical Opportunity: Germany

There is considerable focus on the international opportunity for Canadian LPs as the country’s tenured

federal medical framework, expected national legalization of the recreational market, large number of

LPs with cultivation experience, and access to capital markets puts Canada at the forefront of the global

cannabis opportunity.

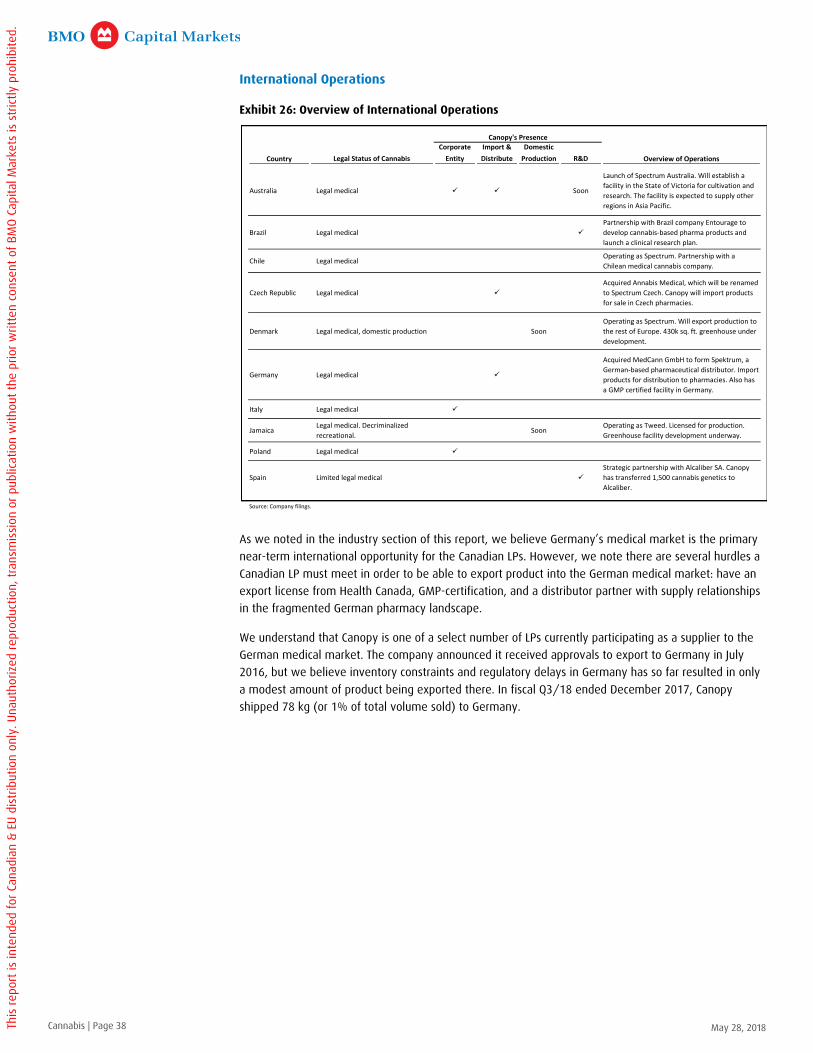

In the near term, we believe Germany’s medical market is the primary international opportunity for the

Canadian LPs due to its medical legalization, size of population, and a favourable insurance coverage

outlook. In a recent report by Prohibition Partners, a cannabis-focused market intelligence firm, the

long-term German medical cannabis market opportunity was estimated at €10 billion.

We understand that prior to medical legalization there were only about 1,000 German citizens with

permission to use cannabis for serious medical conditions. Since medical legalization in 2017, the

country’s three large insurance companies disclosed that there have been 20,000 medical cannabis

claims, of which 13,000 were approved for reimbursement. In addition to these claims, there are also

private cannabis prescriptions where the patient covers the expense. We understand that German law

requires health insurance coverage for medical cannabis, although we have heard that the associated

paperwork is onerous and often a grounds for a patient to not qualify for coverage.

Germany’s current medical cannabis framework does not permit domestic cultivation. As a result, the

country relies on imports to meet demand. Initially, Germany imported exclusively from a Dutch

producer called Bedrocan, but a few Canadian LPs are now focusing on the country. Canadian LPs must

wholesale their exports to the pharmacy distributors as only pharmacies are permitted to dispense

medical cannabis prescriptions. Currently, retail and wholesale prices (the price shared by distributors

and Canadian LPs) in Germany can be as high as $25 and $15 per gram, respectively, due to the supply

shortage from a lack of domestic cultivation and prior administrative issues that delayed international

companies from being able to import into the country. As a result, Canadian LPs exporting into Germany

are receiving much higher wholesale prices than they are receiving in the Canadian medical market. See

Exhibit 9 below for LPs that have secured the licenses, Good Manufacturing Process (GMP) certification

and distribution partners, and are either already or will begin exporting into Germany.

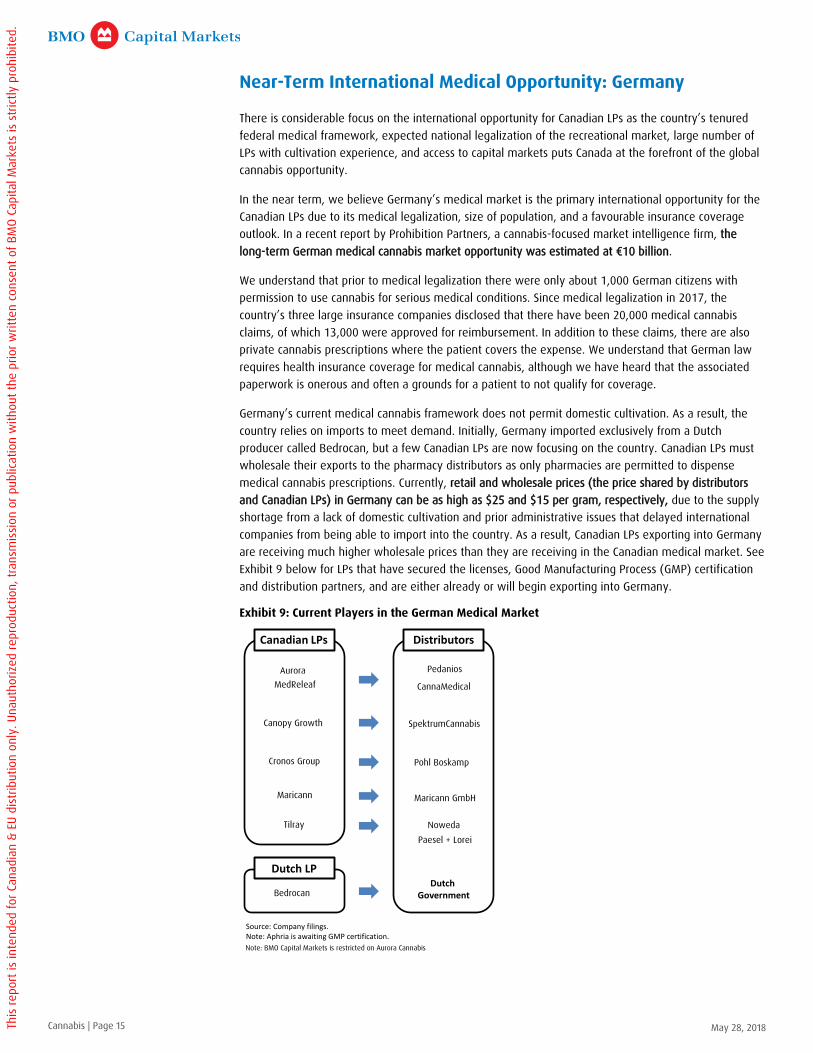

Exhibit 9: Current Players in the German Medical Market

Note: BMO Capital Markets is restricted on Aurora Cannabis

Canadian LPs

Dutch LP

Distributors

Dutch Government

GmbH

Source: Company filings. Note: Aphria is awaiting GMP certification.

Paesel + Lorei

Aurora

Tilray

CannaMedical

Pedanios

MedReleaf

Maricann

SpektrumCannabisCanopy Growth

Cronos Group Pohl Boskamp

Maricann GmbH

Noweda

Bedrocan

Cannabis | Page 15 May 28, 2018This

repo

rt is

inte

nded

for C

anad

ian

& EU

dis

tribu

tion

only

. Una

utho

rized

repr

oduc

tion,

tran

smis

sion

or p

ublic

atio

n w

ithou

t the

prio

r writ

ten

cons

ent o

f BM

O Ca

pita

l Mar

kets

is s

trict

ly p

rohi

bite

d.

Asterisks Behind the German Opportunity

Notwithstanding these favourable dynamics, we believe the German market opportunity for Canadian

LPs should be evaluated carefully. We expect only a handful of the larger LPs will be able to secure the

licensing and certifications requirements, and develop the necessary distribution infrastructure in the

country. Canadian LPs need an export license from Health Canada, be GMP-certified, and have a

distributor partner to supply the fragmented German pharmacy landscape.

We note that achieving GMP certification is a significant undertaking for an LP. In addition, there are

varying forms of the GMP standards, some of which may not be recognized in certain jurisdictions. We

believe the challenges associated with GMP certification represent a significant hurdle in terms of capital

and other investments for the smaller LPs to meet.

We also understand that unlike the Canadian medical market, cannabis producers and distributors are

not permitted to communicate directly with patients and education fees are prohibited. In Germany, the

prescribing doctor has sole discretion in selecting the LP for the patient, and pharmacies cannot

substitute for another producer’s product when dispensing the prescription. As a result, we consider the

focus by some Canadian LPs on the number of German pharmacies their distributor partner has

relationships with is somewhat misleading as these distributors can supply to any German pharmacy,

and it is the doctor who ultimately determines which LP’s product will be prescribed. We believe

establishing relationships with doctors is critical in order to become a meaningful player in the German

medical market, and such an investment presents another hurdle for the smaller LPs. We understand

that there are about 100,000 doctors and 27,000 pharmacies in Germany.

Finally, it appears that favourable economics from German sales have yet to materially contribute to

earnings for the participating Canadian LPs. Current exports into the German medical market only

represent a modest portion of sales for the handful of Canadian LPs that are able to sell products there.

Long-Term Industry Outlook

Oversupply Expected in the Long Term but Impact on Pricing for LPs Is Uncertain

Based on our outlook for industry demand in Exhibit 3 and our forecast for production output by the Big

Three LPs, which we believe will represent the majority of industry supply, we project that supply will

catch up with demand in year two and potentially begin to significantly exceed demand likely in the

third or fourth year following recreational legalization. It is not clear if this projected supply/demand

imbalance will weigh on the cannabis prices realized by the LPs as by then there will be the opportunity

to export increasing volumes to international markets, such as Germany, and the introduction of

additional product formats (such as vape pens, edibles, and beverages) should provide higher pricing

and margins per gram equivalent to compensate for price compression in dried flower.

The analysis in Exhibit 10 following outlines our view that in the long term, the Canadian market will

shift from a supply shortage to significant oversupply of dried flower as Canadian LPs complete their

facility build-outs. Exhibit 10 highlights that just the production capacity currently being developed by

the Big Three LPs will account for eight million of the estimated 11 million square feet of production

space required to satisfy total Canadian demand. We note that the eight million square feet does not

consider the facility expansions of the other LPs, many of which we understand are also undertaking

significant facility developments.

Cannabis | Page 16 May 28, 2018This

repo

rt is

inte

nded

for C

anad

ian

& EU

dis

tribu

tion

only

. Una

utho

rized

repr

oduc

tion,

tran

smis

sion

or p

ublic

atio

n w

ithou

t the

prio

r writ

ten

cons

ent o

f BM

O Ca

pita

l Mar

kets

is s

trict

ly p

rohi

bite

d.

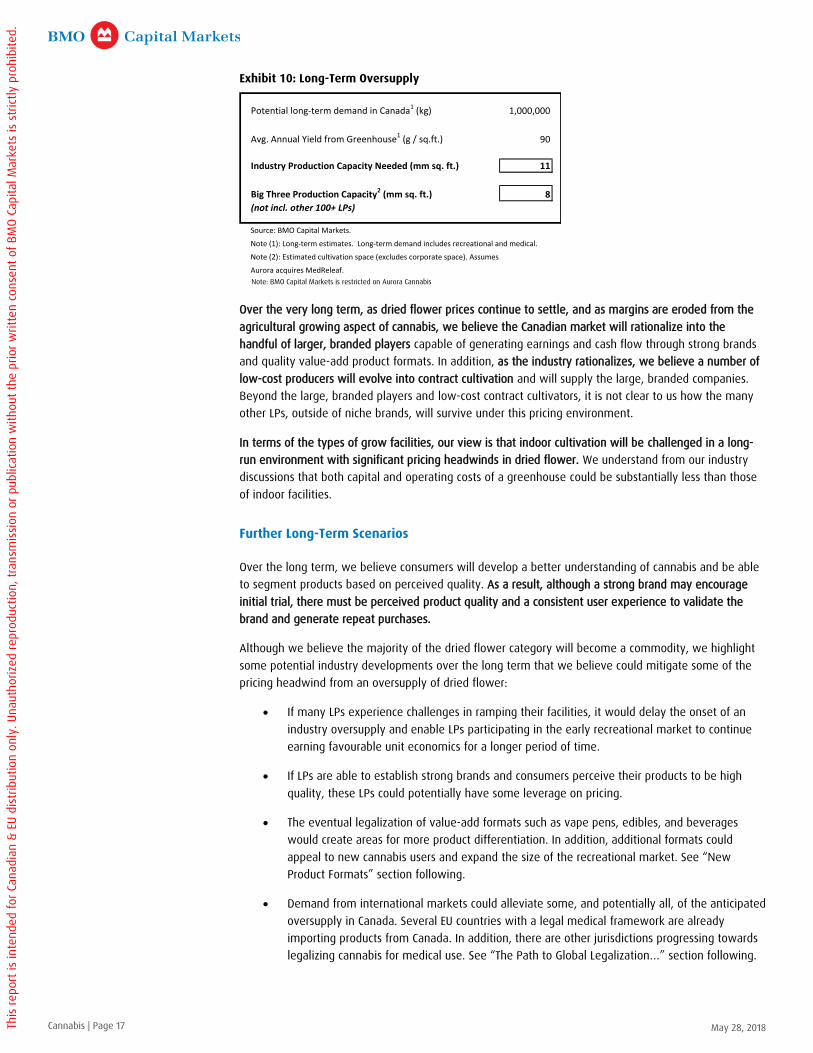

Exhibit 10: Long-Term Oversupply

Note: BMO Capital Markets is restricted on Aurora Cannabis

Over the very long term, as dried flower prices continue to settle, and as margins are eroded from the

agricultural growing aspect of cannabis, we believe the Canadian market will rationalize into the

handful of larger, branded players capable of generating earnings and cash flow through strong brands

and quality value-add product formats. In addition, as the industry rationalizes, we believe a number of

low-cost producers will evolve into contract cultivation and will supply the large, branded companies.

Beyond the large, branded players and low-cost contract cultivators, it is not clear to us how the many

other LPs, outside of niche brands, will survive under this pricing environment.

In terms of the types of grow facilities, our view is that indoor cultivation will be challenged in a long-

run environment with significant pricing headwinds in dried flower. We understand from our industry

discussions that both capital and operating costs of a greenhouse could be substantially less than those

of indoor facilities.

Further Long-Term Scenarios

Over the long term, we believe consumers will develop a better understanding of cannabis and be able

to segment products based on perceived quality. As a result, although a strong brand may encourage

initial trial, there must be perceived product quality and a consistent user experience to validate the

brand and generate repeat purchases.

Although we believe the majority of the dried flower category will become a commodity, we highlight

some potential industry developments over the long term that we believe could mitigate some of the

pricing headwind from an oversupply of dried flower:

If many LPs experience challenges in ramping their facilities, it would delay the onset of an

industry oversupply and enable LPs participating in the early recreational market to continue

earning favourable unit economics for a longer period of time.

If LPs are able to establish strong brands and consumers perceive their products to be high

quality, these LPs could potentially have some leverage on pricing.

The eventual legalization of value-add formats such as vape pens, edibles, and beverages

would create areas for more product differentiation. In addition, additional formats could

appeal to new cannabis users and expand the size of the recreational market. See “New

Product Formats” section following.

Demand from international markets could alleviate some, and potentially all, of the anticipated

oversupply in Canada. Several EU countries with a legal medical framework are already

importing products from Canada. In addition, there are other jurisdictions progressing towards

legalizing cannabis for medical use. See “The Path to Global Legalization…” section following.

Potential long-term demand in Canada1 (kg) 1,000,000

Avg. Annual Yield from Greenhouse1 (g / sq.ft.) 90

Industry Production Capacity Needed (mm sq. ft.) 11

Big Three Production Capacity2 (mm sq. ft.) 8

(not incl. other 100+ LPs)

Source: BMO Capital Markets.

Note (1): Long-term estimates. Long-term demand includes recreational and medical.

Note (2): Estimated cultivation space (excludes corporate space). Assumes

Aurora acquires MedReleaf.

Cannabis | Page 17 May 28, 2018This

repo

rt is

inte

nded

for C

anad

ian

& EU

dis

tribu

tion

only

. Una

utho

rized

repr

oduc

tion,

tran

smis

sion

or p

ublic

atio

n w

ithou

t the

prio

r writ

ten

cons

ent o

f BM

O Ca

pita

l Mar

kets

is s

trict

ly p

rohi

bite

d.

New Product Formats

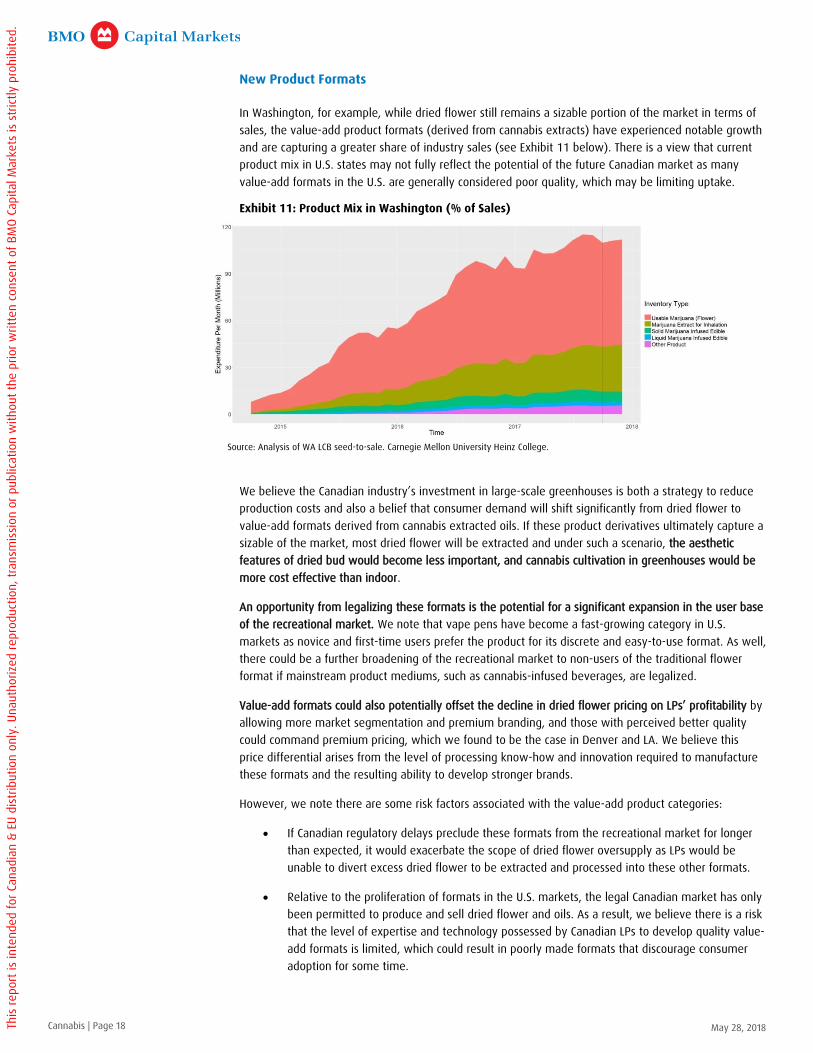

In Washington, for example, while dried flower still remains a sizable portion of the market in terms of

sales, the value-add product formats (derived from cannabis extracts) have experienced notable growth

and are capturing a greater share of industry sales (see Exhibit 11 below). There is a view that current

product mix in U.S. states may not fully reflect the potential of the future Canadian market as many

value-add formats in the U.S. are generally considered poor quality, which may be limiting uptake.

Exhibit 11: Product Mix in Washington (% of Sales)

We believe the Canadian industry’s investment in large-scale greenhouses is both a strategy to reduce

production costs and also a belief that consumer demand will shift significantly from dried flower to

value-add formats derived from cannabis extracted oils. If these product derivatives ultimately capture a

sizable of the market, most dried flower will be extracted and under such a scenario, the aesthetic

features of dried bud would become less important, and cannabis cultivation in greenhouses would be

more cost effective than indoor.

An opportunity from legalizing these formats is the potential for a significant expansion in the user base

of the recreational market. We note that vape pens have become a fast-growing category in U.S.

markets as novice and first-time users prefer the product for its discrete and easy-to-use format. As well,

there could be a further broadening of the recreational market to non-users of the traditional flower

format if mainstream product mediums, such as cannabis-infused beverages, are legalized.

Value-add formats could also potentially offset the decline in dried flower pricing on LPs’ profitability by

allowing more market segmentation and premium branding, and those with perceived better quality

could command premium pricing, which we found to be the case in Denver and LA. We believe this

price differential arises from the level of processing know-how and innovation required to manufacture

these formats and the resulting ability to develop stronger brands.

However, we note there are some risk factors associated with the value-add product categories:

If Canadian regulatory delays preclude these formats from the recreational market for longer

than expected, it would exacerbate the scope of dried flower oversupply as LPs would be

unable to divert excess dried flower to be extracted and processed into these other formats.

Relative to the proliferation of formats in the U.S. markets, the legal Canadian market has only

been permitted to produce and sell dried flower and oils. As a result, we believe there is a risk

that the level of expertise and technology possessed by Canadian LPs to develop quality value-

add formats is limited, which could result in poorly made formats that discourage consumer

adoption for some time.

Source: Analysis of WA LCB seed-to-sale. Carnegie Mellon University Heinz College.

Cannabis | Page 18 May 28, 2018This

repo

rt is

inte

nded

for C

anad

ian

& EU

dis

tribu

tion

only

. Una

utho

rized

repr

oduc

tion,

tran

smis

sion

or p

ublic

atio

n w

ithou

t the

prio

r writ

ten

cons

ent o

f BM

O Ca

pita

l Mar

kets

is s

trict

ly p

rohi

bite

d.

We observed in Denver and LA that packaging was a key branding tool for companies to

differentiate their value-add product formats. We believe Health Canada’s proposals, if

enforced, would materially impair Canadian LPs’ ability to communicate their branding and

their products’ features to consumers.

The Path to Global Legalization and Potential Impact for Canada

Currently, the international flow of controlled substances is governed by three United Nations treaties:

the Single Convention on Narcotic Drugs, the Convention on Psychotropic Substances, and the

Convention against Illicit Traffic in Narcotic Drugs and Psychotropic Substances. As a result of these

treaties, international trade of cannabis is only permitted for medical purposes and countries must have

a legal federal framework in order to participate. Countries that legalize recreational use must satisfy

demand with domestic production.

Although the pace for global legalization is unclear, there is a view that medical legalization will

continue to take place across various jurisdictions, particularly in the European Union. Some industry

forecasts have sized the global cannabis market opportunity at about $55 billion by 2025. We

understand that in addition to Germany, other European countries with a legalized medical framework

implemented are Denmark, Italy, the Netherlands, and Poland. However, only a few European countries

such as Denmark and the Netherlands have permitted domestic production and exporting under certain

circumstances. Outside of Europe, we note that Israel has a significant history in cannabis research and

cultivation, but the Israeli government has not yet permitted exports from the country.

We believe the current international opportunity for Canadian LPs, which is the ability to export products

into other markets at favourable economics, will prove to be transitory. Over the medium term,

countries where Canadian LPs are currently exporting to could establish domestic cultivation. We note

that Germany recently undertook a tender process to issue cultivation licenses and we understand that a

number of Canadian LPs were involved in the process. However, on March 28, a German court

temporarily halted the process. In the interim, Canadian LPs can continue to export products into the

German medical market without the potential for displacement from domestic production. However, a

negative read-through from the German court ruling is that a new tender process could favour German

companies over Canadian LPs. If a new tender process results in most or all of the licenses being

awarded to German LPs, we believe there could still be an opportunity for Canadian LPs as strategic

partners given that German companies would have limited experience in cannabis cultivation and

processing. This partnership approach may become the avenue in which Canadian LPs participate in the

growth of domestic production in international markets given their significant expertise in cultivation,

processing, etc.

Over the long term, we believe there will be countries with favourable climates and lower wage rates

(such as Colombia, Jamaica, and Israel) that emerge as the low-cost growers of dried flower for medical

export. The potential for Israel to become a competitor to Canada in the international export market

could be a near-term risk if the Israeli government permits exports from the country. As a result, we

believe the long-term global opportunity for Canadian LPs is developing intellectual property in areas

such as the development of new strains through genetic modification, cannabinoid isolation and

formulation for advanced medical applications, and new technological innovations for value-add

formats. As well, the current environment is providing Canadian LPs with the unique opportunity to

develop the first global brands.

Although there are several state-level medical and recreational markets, the classification of cannabis as

a Schedule 1 drug by the U.S. federal government confines the operations of U.S. cannabis companies

within their state. As a result, U.S. cannabis companies lack scale and are restricted from participating in

international markets, all of which have created a favourable competitive environment for Canadian LPs.

We believe there would be significant disruption to Canadian LPs if the U.S. legalizes cannabis on a

Cannabis | Page 19 May 28, 2018This

repo

rt is

inte

nded

for C

anad

ian

& EU

dis

tribu

tion

only

. Una

utho

rized

repr

oduc

tion,

tran

smis

sion

or p

ublic

atio

n w

ithou

t the

prio

r writ

ten

cons

ent o

f BM

O Ca

pita

l Mar

kets

is s

trict

ly p

rohi

bite

d.

federal level. Such a scenario would see increased competition to supply international markets. In

addition, we believe this scenario would exacerbate Canada’s domestic oversupply issue and LP margins

would erode further if Canada was to permit imports of dried flower from the U.S., where wholesale

prices are as low as $2 per gram.

Finally, we note that our discussion only considers the global medical market. The additional long-term

upside would be if other jurisdictions consider recreational legalization and we understand that Malta is

currently drafting legislation to legalize recreational use. If Malta establishes and implements a

framework legalizing the recreational market, we believe this could set a precedent that encourages

potential recreational legalization in other European countries. Should other countries legalize

recreational cannabis, Canadian LPs must establish cultivation in those markets in order to participate as

suppliers as the UN treaties prevent international trade of cannabis for non-medical purposes.

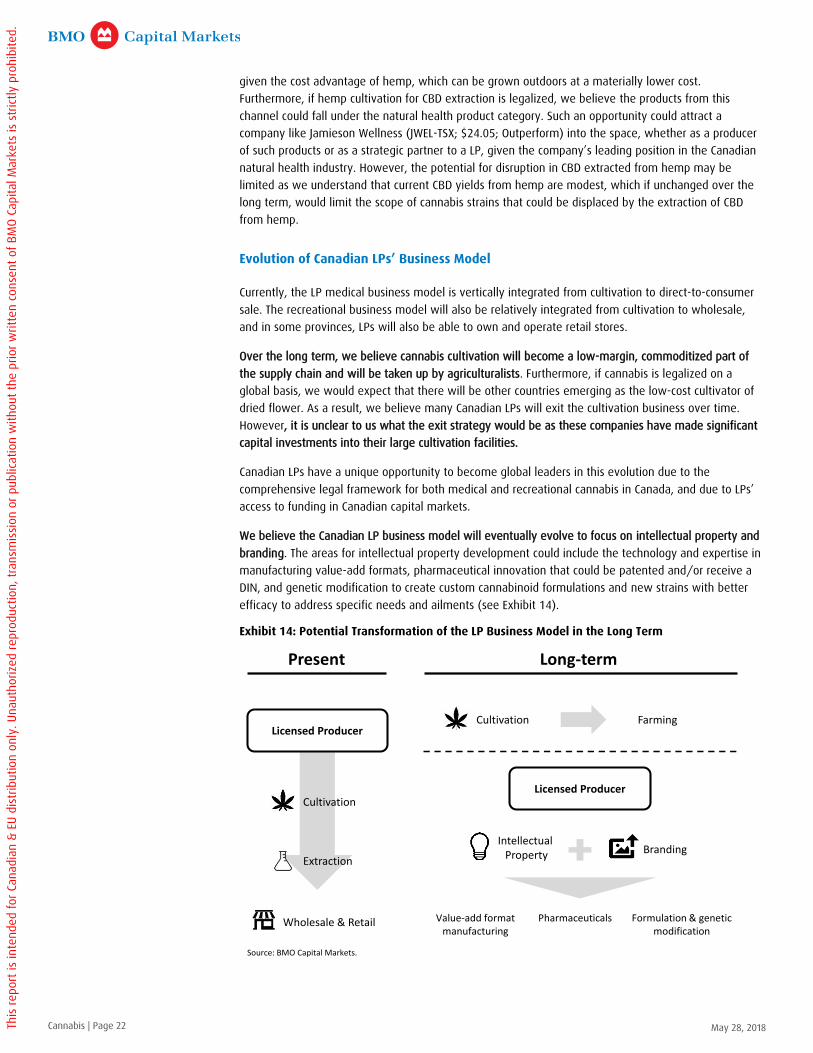

Evolution of the Canadian Medical Market

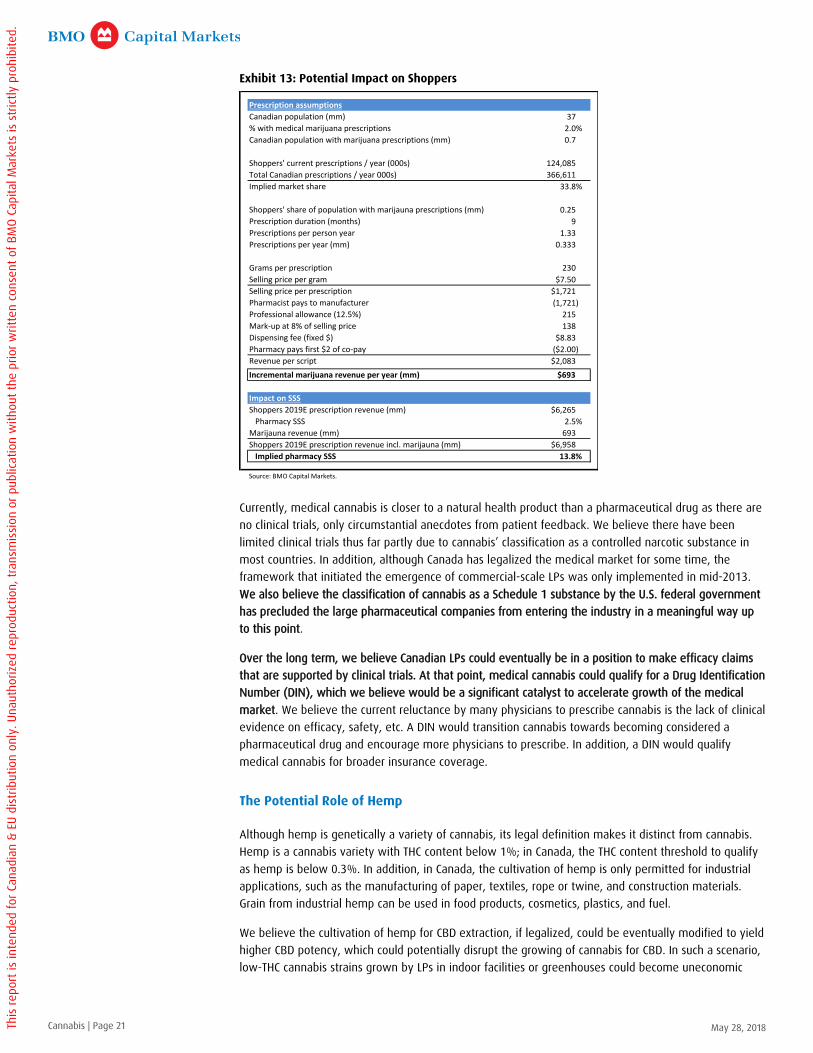

Over the long term, we believe the Canadian distribution model for medical cannabis will expand

beyond the current channel where LPs ship product directly to the patient. We note the industry

generally expects that regulations will eventually permit pharmacies to dispense medical prescriptions.

Pharmacy chains including Shoppers Drug Mart and Pharmasave have already signed supply agreements

with several LPs (see Exhibit 12 below).

Exhibit 12: Notable LP Supply Agreements With Pharmacies

Shoppers Drug Mart Pharmasave

Aphria

Aurora

MedReleaf

Tilray

CanniMed

Delta 9 Cannabis

Tilray

Zenabis

Source: Company Press Releases

Note: BMO Capital Markets is restricted on Aurora Cannabis

If pharmacies are permitted to dispense prescriptions, we believe the potential uplift to Shoppers’

same-store sales (SSS) could be significant as a result of higher pricing for medical cannabis relative to

other prescriptions. For medical cannabis, average retail pricing is around $7.50 per gram for dried

flower with average daily consumption of just under a gram, compared to generic drug prescriptions

where prices per day can be as low as the pennies range. We believe there is also potential upside for

Shoppers’ front-of-store sales as a result of increased traffic from medical cannabis patients. The

following Exhibit 13 illustrates our scenario on the potential impact to Shoppers.

However, we believe the same pricing headwind that will ultimately pressure the recreational market

due to anticipated oversupply will also impact the medical market. Based on this consideration, our

analysis of the financial impact to Shoppers may be overstated if prices decline by the time regulations

allow pharmacies to dispense prescriptions.

Cannabis | Page 20 May 28, 2018This

repo

rt is

inte

nded

for C

anad

ian

& EU

dis

tribu

tion

only

. Una

utho

rized

repr

oduc

tion,

tran

smis

sion

or p

ublic

atio

n w

ithou

t the

prio

r writ

ten

cons

ent o

f BM

O Ca

pita

l Mar

kets

is s

trict

ly p

rohi

bite

d.

Exhibit 13: Potential Impact on Shoppers

Currently, medical cannabis is closer to a natural health product than a pharmaceutical drug as there are

no clinical trials, only circumstantial anecdotes from patient feedback. We believe there have been

limited clinical trials thus far partly due to cannabis’ classification as a controlled narcotic substance in

most countries. In addition, although Canada has legalized the medical market for some time, the

framework that initiated the emergence of commercial-scale LPs was only implemented in mid-2013.

We also believe the classification of cannabis as a Schedule 1 substance by the U.S. federal government

has precluded the large pharmaceutical companies from entering the industry in a meaningful way up

to this point.

Over the long term, we believe Canadian LPs could eventually be in a position to make efficacy claims

that are supported by clinical trials. At that point, medical cannabis could qualify for a Drug Identification

Number (DIN), which we believe would be a significant catalyst to accelerate growth of the medical

market. We believe the current reluctance by many physicians to prescribe cannabis is the lack of clinical

evidence on efficacy, safety, etc. A DIN would transition cannabis towards becoming considered a

pharmaceutical drug and encourage more physicians to prescribe. In addition, a DIN would qualify

medical cannabis for broader insurance coverage.

The Potential Role of Hemp