canadian sales/use tax april 2009. overview definitions: sales tax – gst/hst/pst/rst/social...

TRANSCRIPT

Canadian Sales/Use Tax

April 2009

Overview

•Definitions: Sales Tax – GST/HST/PST/RST/Social Services Tax

•Examples: RST in Ontario & PST in British Columbia

•Contract Language

•Canadian Accounting

•Jobscope – Setting up Canadian Customers

•Sales Tax Accrual for Canadian Jobs

•Regulation 102 Waivers

•Regulation 105 Waivers

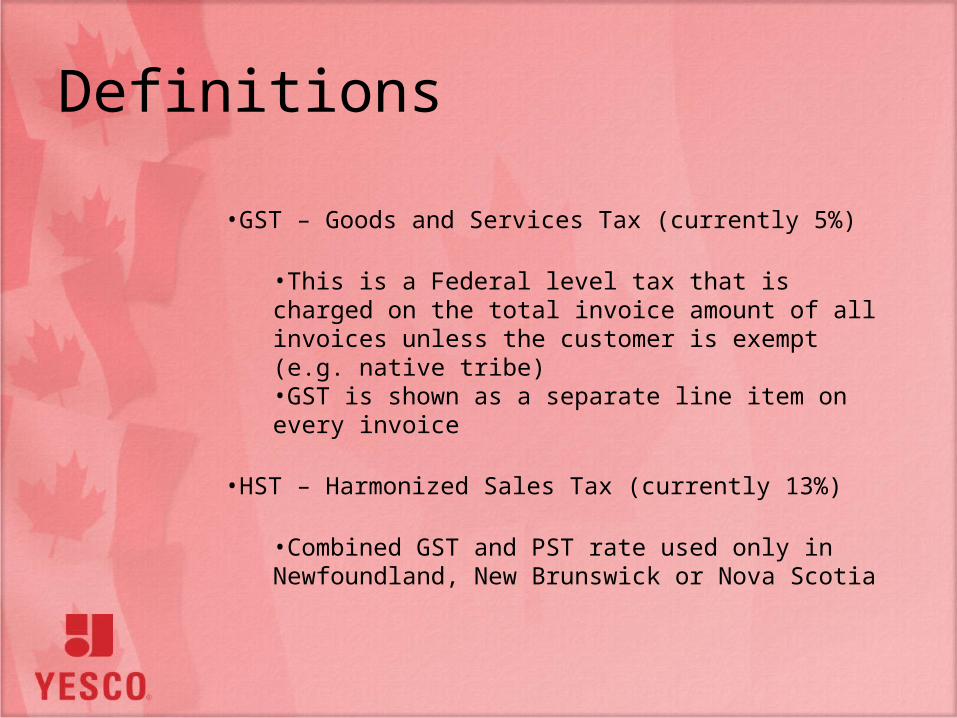

Definitions

•GST – Goods and Services Tax (currently 5%)

•This is a Federal level tax that is charged on the total invoice amount of all invoices unless the customer is exempt (e.g. native tribe)•GST is shown as a separate line item on every invoice

•HST – Harmonized Sales Tax (currently 13%)

•Combined GST and PST rate used only in Newfoundland, New Brunswick or Nova Scotia

Definitions (cont’d)

•PST – Provincial Sales Tax (varies by Province)•YESCO cannot charge this to the customer•Generally based on the material cost• YESCO recovers this cost by building the additional cost into estimate

•RST – Retail Sales Tax (varies by Province)•Only in Manitoba and Ontario•Treated the same as PST

•Social Service Tax (only in British Columbia)•Treated same as PST•YESCO vocabulary refers to this as “PST”

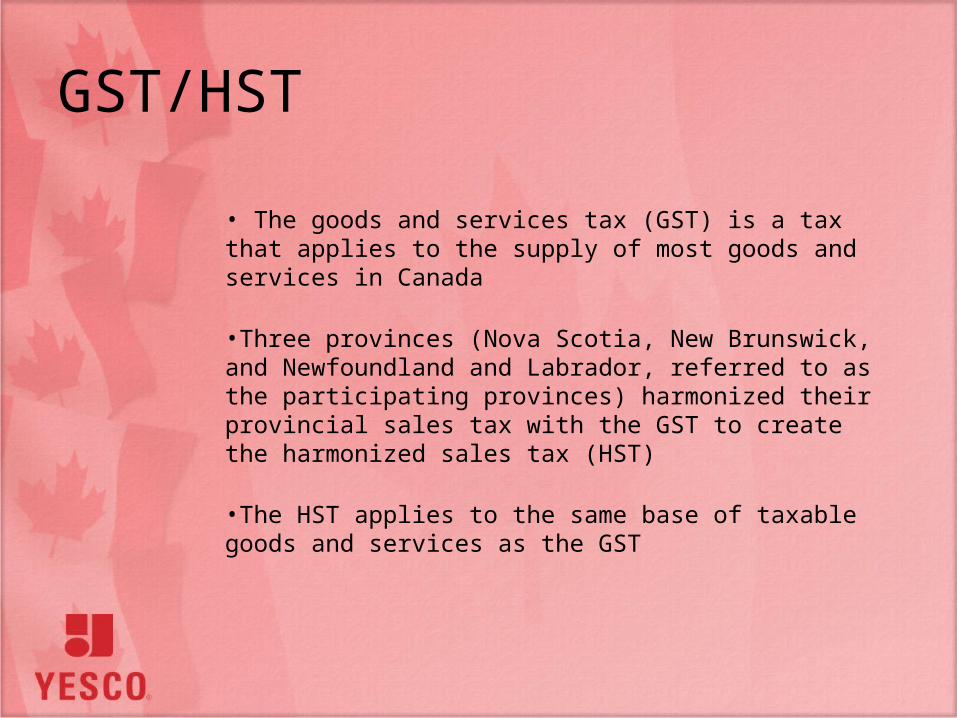

GST/HST

• The goods and services tax (GST) is a tax that applies to the supply of most goods and services in Canada

•Three provinces (Nova Scotia, New Brunswick, and Newfoundland and Labrador, referred to as the participating provinces) harmonized their provincial sales tax with the GST to create the harmonized sales tax (HST)

•The HST applies to the same base of taxable goods and services as the GST

GST/HST (cont’d)

• Although the consumer pays the tax, businesses are generally responsible for collecting and remitting it to the government

•Businesses that have a GST/HST registration number collect the GST/HST on most of their sales and pay the GST/HST on most purchases they make to operate their business

•They can claim a credit, called an input tax credit (ITC), to recover the GST/HST they paid or owe on the purchases they use in their commercial activities

HST

•Three provinces - Nova Scotia, New Brunswick, and Newfoundland and Labrador - harmonized their provincial sales tax with GST to create HST

•The HST is composed of the GST and the 8% provincial tax and applies to the same base of goods and services that are taxable under GST.

•GST/HST registrants continue to collect GST on taxable supplies of goods and services

•On supplies made in the participating provinces, they collect HST

RST in Ontario

•Ontario has separate rules for non-residents

•The Ontario Ministry gives YESCO a special number for every project

•To obtain this YESCO must complete a contract guarantee for each project and post a deposit or post a bond with the government for 4% of the contract amount

•This bond is obtained through our insurance broker Moreton and is more economical than posting a deposit for significant amounts

RST in Ontario (cont’d)

•Once the guarantee has been posted the Ministry provides YESCO with copies of a letter of compliance, which YESCO gives to the customer

•Once the job is completed YESCO files a non-resident form with the Ministry and gets a refund of the posted guarantee (or they cancel the bond) as the posted 4% of the total contract is typically larger than 8% RST charged on the cost of materials

•YESCO completes a Form 105 waiver for each project so the customer will not withhold 15% of the contract price for taxes on foreign companies

RST in Ontario (cont’d)

•Ontario has a standard way of dealing with contracts regardless of whether they are Time & Material or Lump Sum/Fixed Cost, all are treated as supply and install jobs

•YESCO cannot charge customers for the RST, however, the standard YESCO language includes a clause that allows us to collect and additional amount from the customer that is equal in amount to the RST.

•There is no RST charged on installation labor.

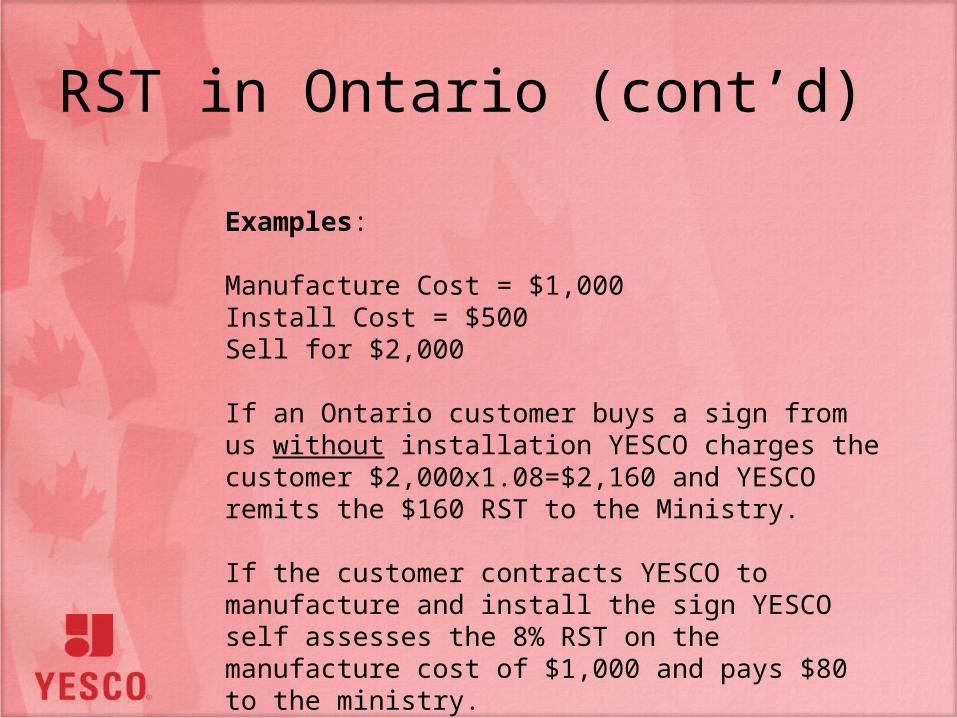

RST in Ontario (cont’d)

Examples: Manufacture Cost = $1,000Install Cost = $500Sell for $2,000

If an Ontario customer buys a sign from us without installation YESCO charges the customer $2,000x1.08=$2,160 and YESCO remits the $160 RST to the Ministry. If the customer contracts YESCO to manufacture and install the sign YESCO self assesses the 8% RST on the manufacture cost of $1,000 and pays $80 to the ministry.

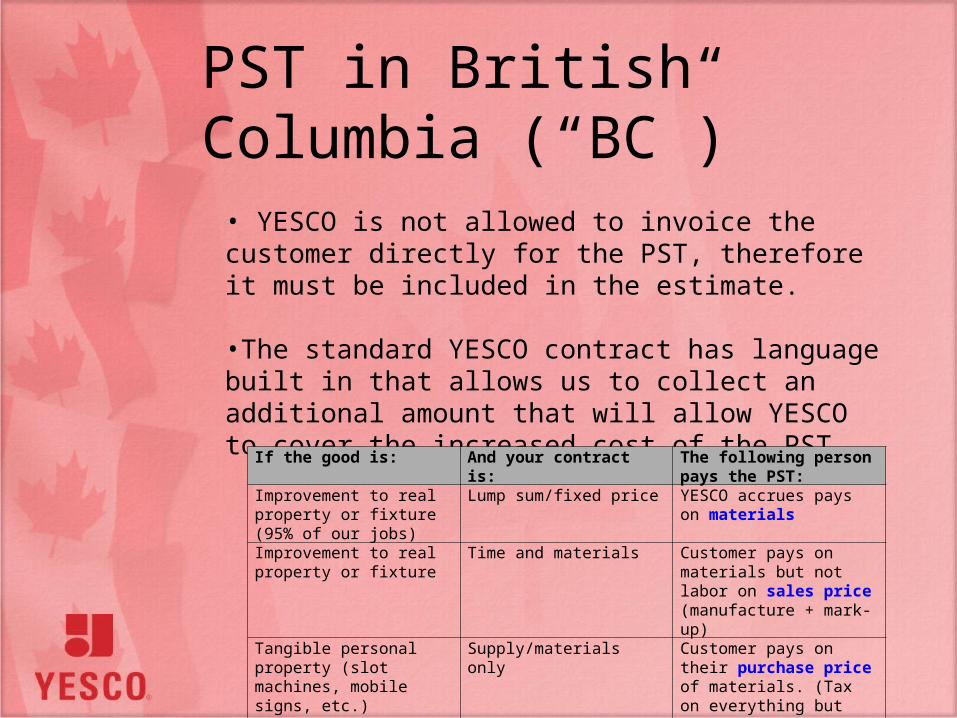

PST in British Columbia (“BC”)

• YESCO is not allowed to invoice the customer directly for the PST, therefore it must be included in the estimate.

•The standard YESCO contract has language built in that allows us to collect an additional amount that will allow YESCO to cover the increased cost of the PST.

If the good is: And your contract is: The following person pays the PST:

Improvement to real property or fixture (95% of our jobs)

Lump sum/fixed price YESCO accrues pays on materials

Improvement to real property or fixture

Time and materials Customer pays on materials but not labor on sales price (manufacture + mark-up)

Tangible personal property (slot machines, mobile signs, etc.)

Supply/materials only Customer pays on their purchase price of materials. (Tax on everything but installation labor).

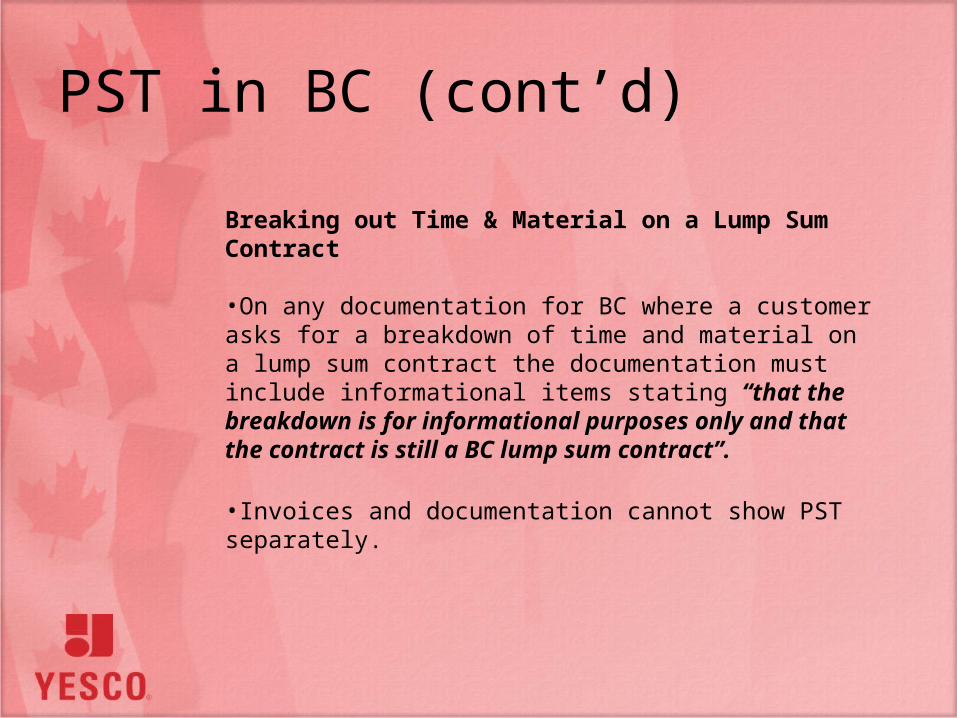

PST in BC (cont’d)

Breaking out Time & Material on a Lump Sum Contract •On any documentation for BC where a customer asks for a breakdown of time and material on a lump sum contract the documentation must include informational items stating “that the breakdown is for informational purposes only and that the contract is still a BC lump sum contract”.

•Invoices and documentation cannot show PST separately.

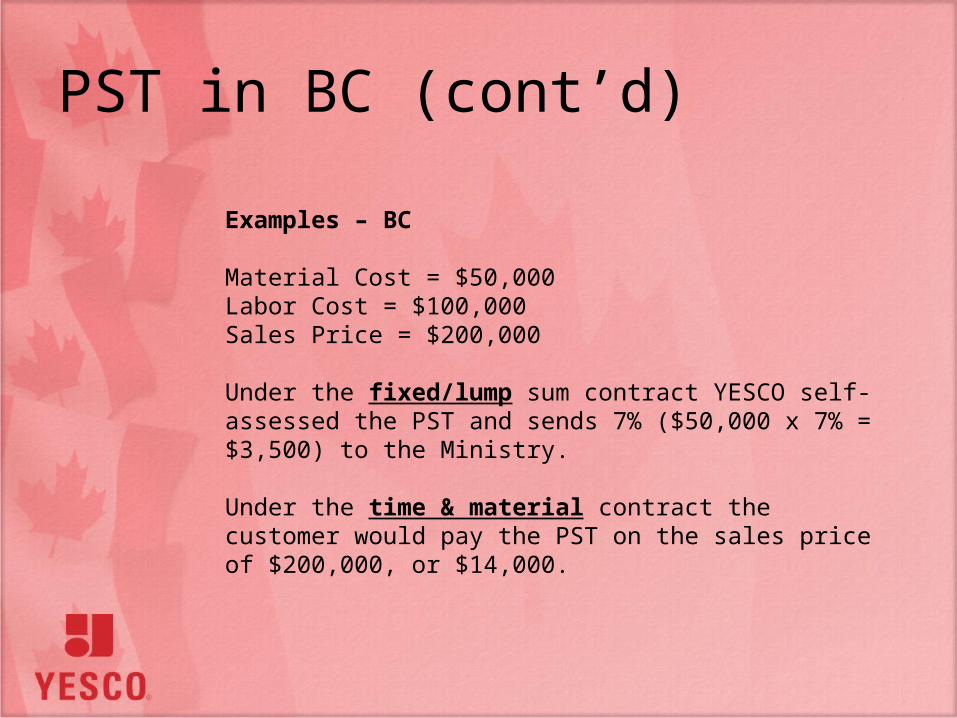

PST in BC (cont’d)

Examples – BC Material Cost = $50,000Labor Cost = $100,000Sales Price = $200,000 Under the fixed/lump sum contract YESCO self-assessed the PST and sends 7% ($50,000 x 7% = $3,500) to the Ministry. Under the time & material contract the customer would pay the PST on the sales price of $200,000, or $14,000.

Contract Language – PST/RST

Adjustments to Canadian Contract Language: “Price will be adjusted in the amount of any provincial taxes assessed.” (Collect amount equal to assessment) Applies only if taxes are assessed. OR “Consideration for this contract will be increased in the amount of any provincial taxes as self-assessed by Young Electric Sign Company and that are incurred as a cost of this contract.”

Contract Language (cont’d)Adjustments to Canadian Contract Language: •Note: You do not need this language if you have already added the provincial tax (PST/RST) to the price of materials in the contract.

•By law YESCO is not allowed to charge the tax on our contract, but we are allowed to increase the consideration for the contract by the amount of any provincial tax incurred by YESCO.

•YESCO will have to pay the provincial tax, so we will take a loss by the amount of the tax if we don’t increase the contract price or make the statement that the contract price will be increased (and invoice for the increased amount later).

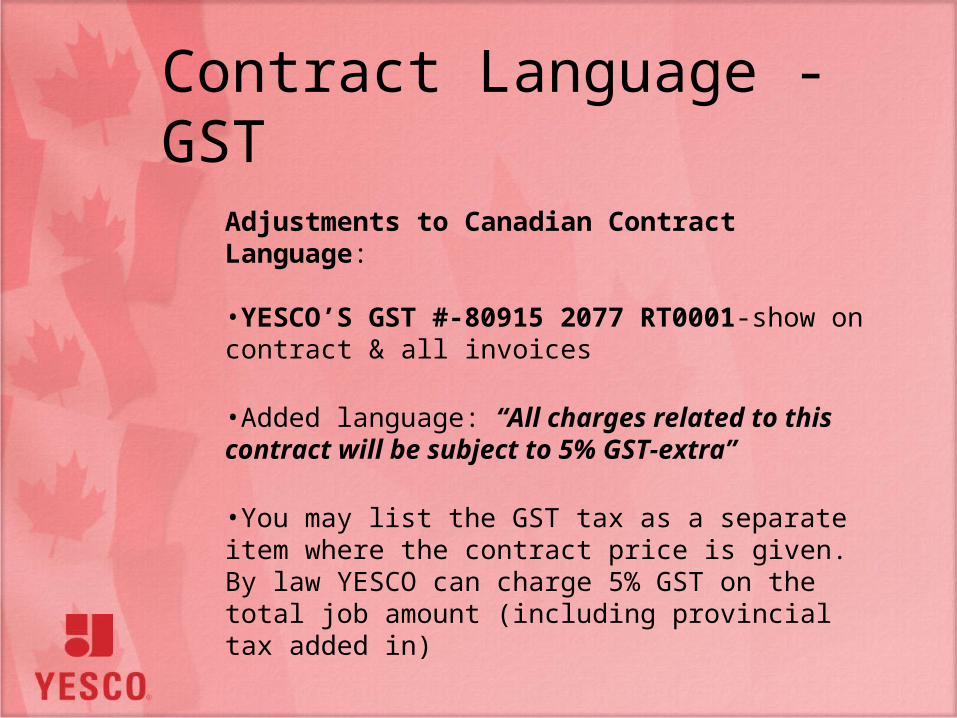

Contract Language - GST

Adjustments to Canadian Contract Language: •YESCO’S GST #-80915 2077 RT0001-show on contract & all invoices

•Added language: “All charges related to this contract will be subject to 5% GST-extra”

•You may list the GST tax as a separate item where the contract price is given. By law YESCO can charge 5% GST on the total job amount (including provincial tax added in)

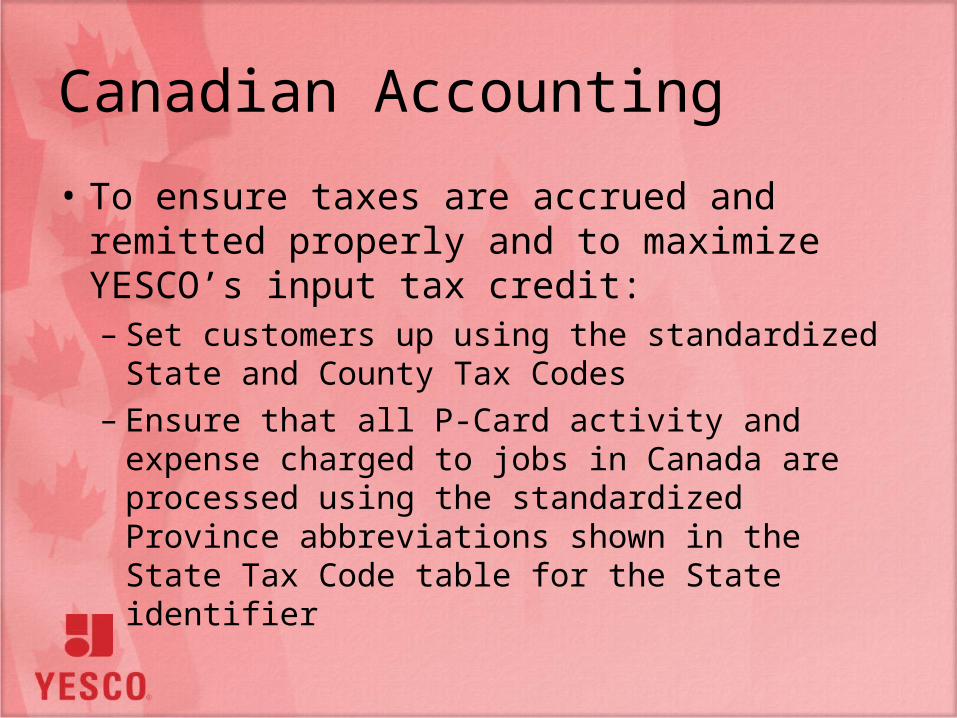

Canadian Accounting

• To ensure taxes are accrued and remitted properly and to maximize YESCO’s input tax credit:– Set customers up using the standardized State

and County Tax Codes– Ensure that all P-Card activity and expense

charged to jobs in Canada are processed using the standardized Province abbreviations shown in the State Tax Code table for the State identifier

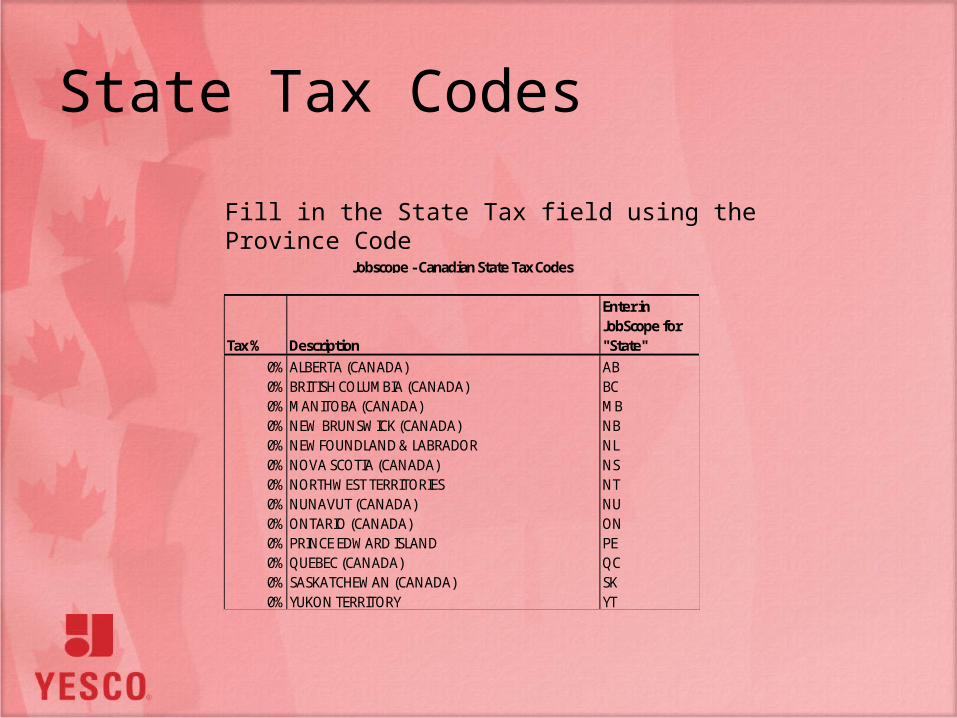

State Tax Codes

Tax % Description

Enter in JobScope for "State"

0% ALBERTA (CANADA) AB0% BRITISH COLUMBIA (CANADA) BC0% MANITOBA (CANADA) MB0% NEW BRUNSWICK (CANADA) NB0% NEWFOUNDLAND & LABRADOR NL0% NOVA SCOTIA (CANADA) NS0% NORTHWEST TERRITORIES NT0% NUNAVUT (CANADA) NU0% ONTARIO (CANADA) ON0% PRINCE EDWARD ISLAND PE0% QUEBEC (CANADA) QC0% SASKATCHEWAN (CANADA) SK0% YUKON TERRITORY YT

Jobscope - Canadian State Tax Codes

Fill in the State Tax field using the Province Code

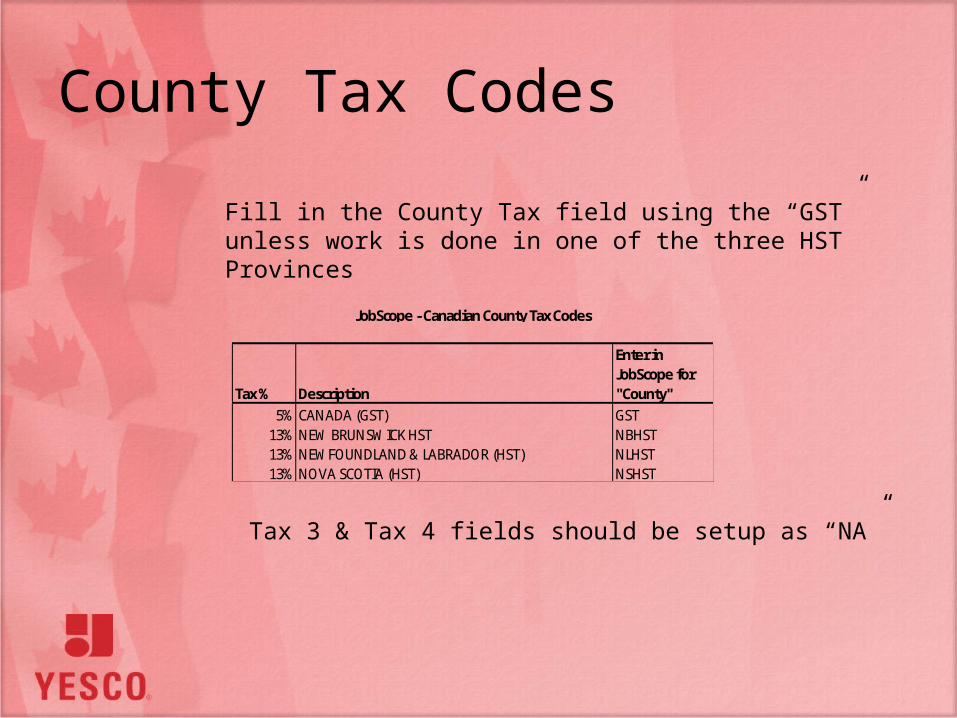

County Tax Codes

Tax % Description

Enter in JobScope for "County"

5% CANADA (GST) GST13% NEW BRUNSWICK HST NBHST13% NEWFOUNDLAND & LABRADOR (HST) NLHST13% NOVA SCOTIA (HST) NSHST

JobScope - Canadian County Tax Codes

Tax 3 & Tax 4 fields should be setup as “NA”

Fill in the County Tax field using the “GST” unless work is done in one of the three HST Provinces

Jobscope – Example

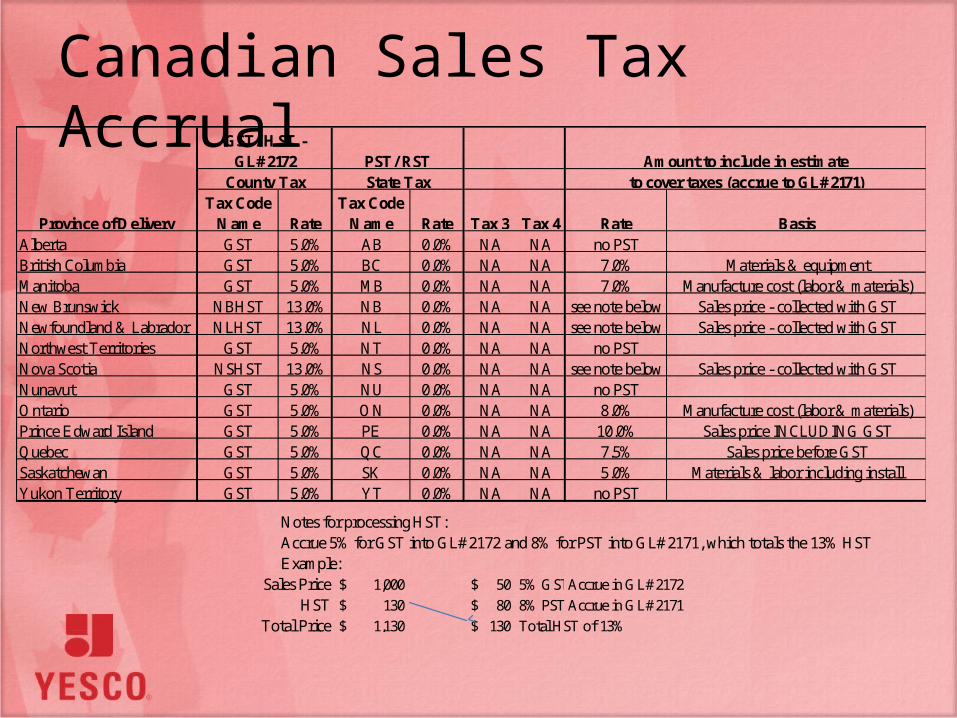

Canadian Sales Tax Accrual

Province of DeliveryTax Code

Name RateTax Code

Name Rate Tax 3 Tax 4 Rate BasisAlberta GST 5.0% AB 0.0% NA NA no PSTBritish Columbia GST 5.0% BC 0.0% NA NA 7.0% Materials & equipmentManitoba GST 5.0% MB 0.0% NA NA 7.0% Manufacture cost (labor & materials)New Brunswick NBHST 13.0% NB 0.0% NA NA see note below Sales price - collected with GSTNewfoundland & Labrador NLHST 13.0% NL 0.0% NA NA see note below Sales price - collected with GSTNorthwest Territories GST 5.0% NT 0.0% NA NA no PSTNova Scotia NSHST 13.0% NS 0.0% NA NA see note below Sales price - collected with GSTNunavut GST 5.0% NU 0.0% NA NA no PSTOntario GST 5.0% ON 0.0% NA NA 8.0% Manufacture cost (labor & materials)Prince Edward Island GST 5.0% PE 0.0% NA NA 10.0% Sales price INCLUDING GSTQuebec GST 5.0% QC 0.0% NA NA 7.5% Sales price before GSTSaskatchewan GST 5.0% SK 0.0% NA NA 5.0% Materials & labor including installYukon Territory GST 5.0% YT 0.0% NA NA no PST

Notes for processing HST:Accrue 5% for GST into GL#2172 and 8% for PST into GL#2171, which totals the 13% HSTExample:

Sales Price 1,000$ 50$ 5% GSTAccrue in GL#2172HST 130$ 80$ 8% PSTAccrue in GL#2171

Total Price 1,130$ 130$ Total HST of 13%

County Tax State Tax to cover taxes (accrue to GL#2171)

GST/ HST - GL#2172 PST/ RST Amount to include in estimate

Regulation 102 Waiver

•Regulation 102 Waiver must be filed with the Canada Customs and Revenue Agency (“CCRA”) prior to work being commenced within Canada

•The Regulation 102 Waiver exempts YESCO employees from being subject to withholdings (which can include income tax, as well Canada Pension Plan (“CPP”) contributions and Employment Insurance (“EI”) premiums

•Failure to file and obtain the 102 waiver will result in YESCO employees being subject to CPP and EI in Canada

Regulation 105 Waiver•YESCO files for a Regulation 105 Waiver for each job and change order performed in Canada

•This waiver reduces the amount of withholding tax on services provided in Canada

•In order to ensure consideration of a treaty-based waiver application, it should be submitted at least 30 days prior to the commencement of the services in Canada or 30 days prior to the initial payment for the related services

•Failure to file and obtain the 105 waiver will result in the customer withholding 15% of the contract price, which cannot be recovered until after the end of the calendar year and possible loss of exempt status for income tax purposes under a treaty-based waiver