capital asset policies and procedures handbook. session objectives understand what data might be...

TRANSCRIPT

CAPITAL ASSET CAPITAL ASSET POLICIES POLICIES

AND PROCEDURES AND PROCEDURES HANDBOOKHANDBOOK

Session ObjectivesSession Objectives

Understand What Data Might Be Understand What Data Might Be Included in A Detailed Capital Asset Included in A Detailed Capital Asset Policies & Procedures HandbookPolicies & Procedures Handbook

Discuss in Detail Each of the Topics Discuss in Detail Each of the Topics Included in the Above DocumentIncluded in the Above Document

A Capital Asset Record SystemA Capital Asset Record System

Is It Integrated With The General Is It Integrated With The General Ledger System?Ledger System?

Can It Calculate Depreciation Expense By Can It Calculate Depreciation Expense By Function?Function?

Can It Provide A Report Of Disposed Can It Provide A Report Of Disposed Assets?Assets?

Can It Provide A Report Of Data By Can It Provide A Report Of Data By Function?Function?

A Capital Asset Record SystemA Capital Asset Record System

What It IsWhat It Is

How it WorksHow it Works

Who Does WhatWho Does What

How Much DetailHow Much Detail

The Property RecordThe Property Record

Property Identification NumberProperty Identification Number

Fund and AccountFund and Account

Major Asset ClassMajor Asset Class

Function and ActivityFunction and Activity

Acquisition Document NumberAcquisition Document Number

Acquisition DateAcquisition Date

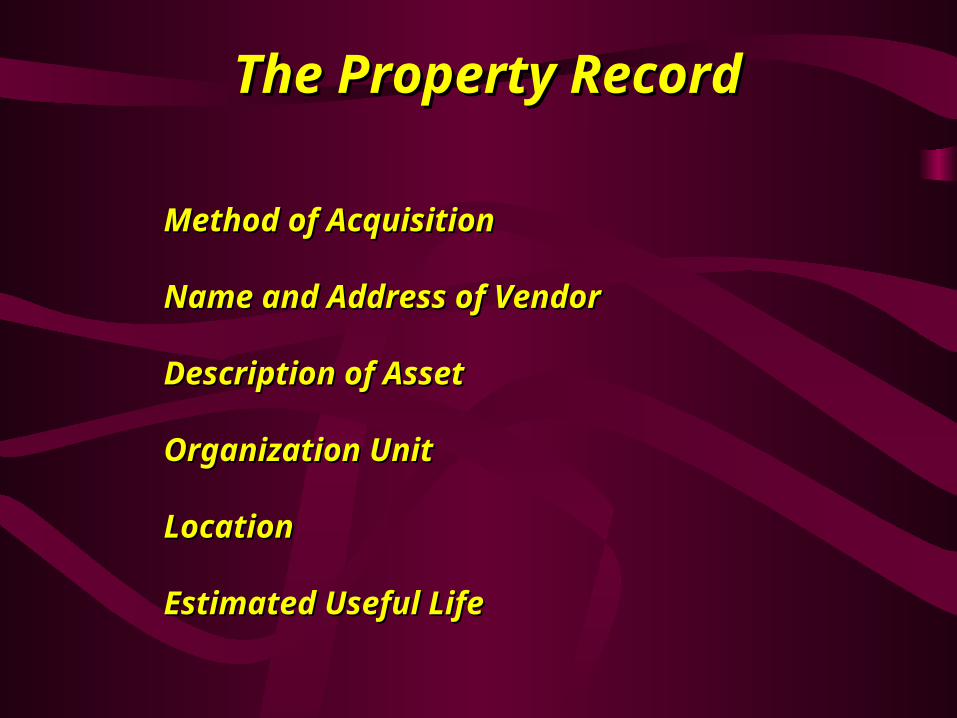

The Property RecordThe Property Record

Method of AcquisitionMethod of Acquisition

Name and Address of VendorName and Address of Vendor

Description of AssetDescription of Asset

Organization UnitOrganization Unit

LocationLocation

Estimated Useful LifeEstimated Useful Life

The Property RecordThe Property Record

Estimated Salvage ValueEstimated Salvage Value

Date, Method, and Authorization of DispositionDate, Method, and Authorization of Disposition

Identify Reporting RequirementsIdentify Reporting Requirements

Inventory Report by LocationInventory Report by Location

Inventory Report by StewardshipInventory Report by Stewardship

Inventory Report by ClassInventory Report by Class

Depreciation Expense ReportDepreciation Expense Report

Schedule of Capital Assets by ClassSchedule of Capital Assets by Class

Schedule of changes in Capital Assets by ClassSchedule of changes in Capital Assets by Class

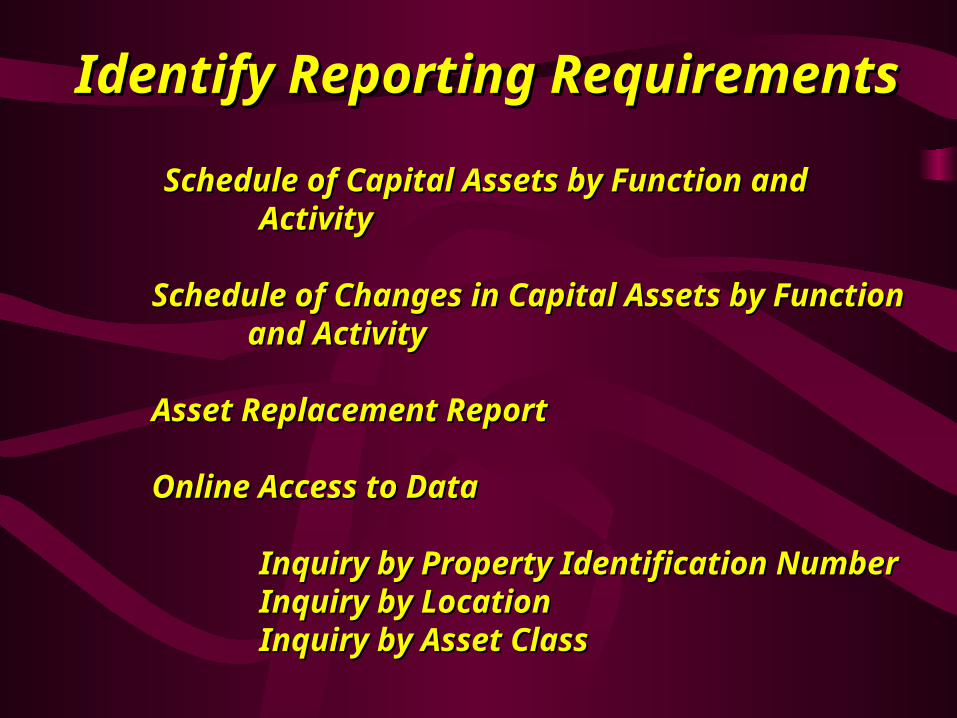

Identify Reporting RequirementsIdentify Reporting Requirements

Schedule of Capital Assets by Function and Schedule of Capital Assets by Function and ActivityActivity

Schedule of Changes in Capital Assets by Schedule of Changes in Capital Assets by Function Function and Activityand Activity

Asset Replacement ReportAsset Replacement Report

Online Access to DataOnline Access to Data

Inquiry by Property Identification NumberInquiry by Property Identification NumberInquiry by LocationInquiry by LocationInquiry by Asset ClassInquiry by Asset Class

Capital Asset ClassificationsCapital Asset Classifications

Specific ClassificationsSpecific Classifications

ThresholdsThresholds

Capital Asset ClassificationCapital Asset Classification

Capital Assets Includes:Capital Assets Includes:

-Land -Land -Land Improvements-Land Improvements-Buildings -Buildings -Building Improvements-Building Improvements-Vehicles-Vehicles-Machinery & Equipment-Machinery & Equipment-Works of Art & Historical Treasures-Works of Art & Historical Treasures-Infrastructure-Infrastructure-In-tangible Assets-In-tangible Assets

Capital Asset ThresholdsCapital Asset Thresholds

•Two Primary CriteriaTwo Primary Criteria

- Cost of the Asset- Cost of the Asset

- Useful Life- Useful Life

National GFOA Recommends a $5,000 National GFOA Recommends a $5,000 Threshold Per Unit Threshold Per Unit

•Threshold Needs To Cover 75% - 80% of Threshold Needs To Cover 75% - 80% of The CostsThe Costs

Capital Asset ThresholdsCapital Asset Thresholds

Spend Your Time Controlling Large Spend Your Time Controlling Large ItemsItems

LandLandBuildingsBuildingsVehiclesVehicles

Capital Asset ThresholdsCapital Asset Thresholds

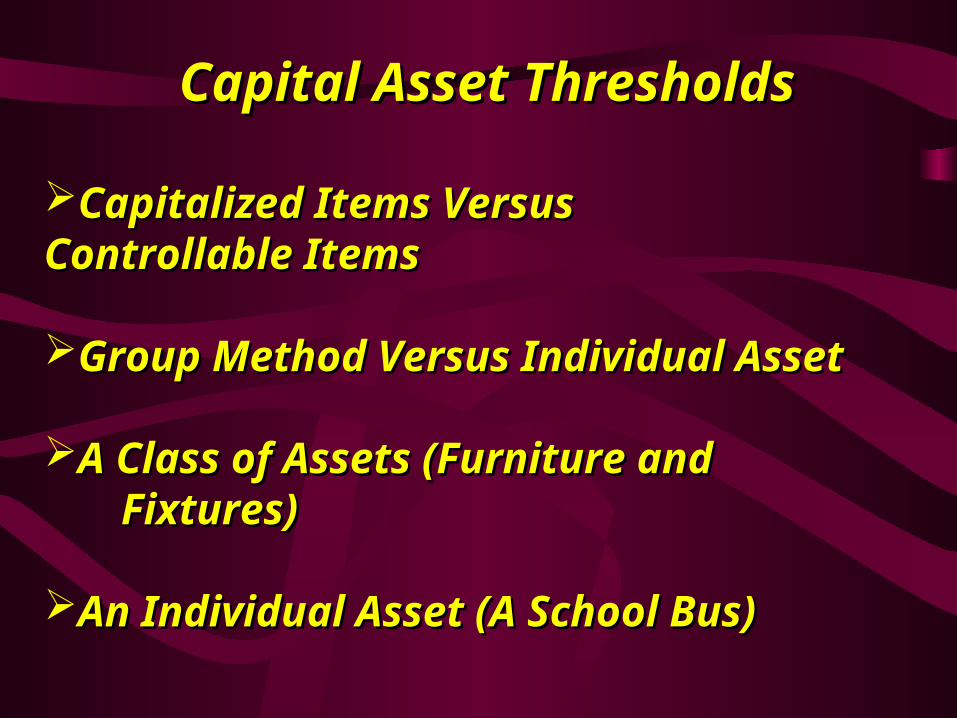

Capitalized Items Versus Capitalized Items Versus Controllable ItemsControllable Items

Group Method Versus Individual AssetGroup Method Versus Individual Asset

A Class of Assets (Furniture and A Class of Assets (Furniture and Fixtures)Fixtures)

An Individual Asset (A School Bus)An Individual Asset (A School Bus)

Capital Asset ClassificationCapital Asset Classification

Divide Between Major Class and Divide Between Major Class and SubclassSubclass

Major Class Usually equates to General Major Class Usually equates to General Ledger Asset Accounts For Ease in Ledger Asset Accounts For Ease in Financial ReportingFinancial Reporting

LandLand

Potential SubclassesPotential Subclasses

-- Vacant Parcel (Deed)Vacant Parcel (Deed)-- Land Under a Building (Deed)Land Under a Building (Deed)-- Land Under the RoadsLand Under the Roads

LandLand

Includes the Cost of Preparing Land for Includes the Cost of Preparing Land for UseUse

Separate Land Cost from Cost of Separate Land Cost from Cost of Buildings or Improvements if all Three Buildings or Improvements if all Three are Purchased Togetherare Purchased Together

Park LandsPark Lands

Land ImprovementsLand Improvements

Fencing Fencing

Paving (i.e., Parking Lots)Paving (i.e., Parking Lots)

LightingLighting

Plumbing (e.g., water facets)Plumbing (e.g., water facets)

Landscaping??Landscaping??

BuildingsBuildings

Components:Components:

Building ShellBuilding ShellRoofRoofElevatorElevatorElectrical SystemElectrical SystemPlumbing SystemPlumbing SystemHeating/Air Conditioning SystemHeating/Air Conditioning System

Buildings ImprovementsBuildings Improvements

Sometimes These Costs are Just Sometimes These Costs are Just Capitalized as BuildingsCapitalized as Buildings

Alarm SystemsAlarm Systems

CarpetingCarpeting

Shelving and CabinetsShelving and Cabinets

Clock SystemsClock Systems

Buildings ImprovementsBuildings Improvements

Public Address & Speaker Systems Public Address & Speaker Systems Where Wiring Is "Built-in".Where Wiring Is "Built-in".

CurtainsCurtains

VehiclesVehicles

Vehicle TagsVehicle Tags

All Rolling StockAll Rolling Stock

TrucksTrucks

AutomobilesAutomobiles

BusesBuses

Machinery and EquipmentMachinery and Equipment

Computer EquipmentComputer Equipment

Furniture and FixturesFurniture and Fixtures

WeaponsWeapons

Heavy EquipmentHeavy Equipment

Radios and Cell PhonesRadios and Cell Phones

Historical Treasures and Historical Treasures and Works of ArtWorks of Art

PaintingsPaintings

StatutesStatutes

Totem PolesTotem Poles

GASBS 34 RequirementsGASBS 34 Requirements

Governments Should Capitalize Governments Should Capitalize Works Works Of Art, Historical Treasures, And Of Art, Historical Treasures, And

Similar Assets At Their Historical Similar Assets At Their Historical Cost Cost Or Fair Value At Date Of Or Fair Value At Date Of Donation Donation (Estimated If Necessary) (Estimated If Necessary) Whether Whether They Are Held As Individual They Are Held As Individual Items Or Items Or In A CollectionIn A Collection.

GASBS 34 RequirementsGASBS 34 Requirements

Governments Are Encouraged, But Not Required, To Governments Are Encouraged, But Not Required, To Capitalize A Collection (And All Additions To That Capitalize A Collection (And All Additions To That Collection) Whether Donated Or Purchased That Meets Collection) Whether Donated Or Purchased That Meets All Of The Following Conditions. The Collection Is:All Of The Following Conditions. The Collection Is:

Held For Public Exhibition, Education, Or Held For Public Exhibition, Education, Or Research Research In Furtherance Of Public Service, Rather In Furtherance Of Public Service, Rather Than Than Financial GainFinancial Gain

Protected, Kept Unencumbered, Cared For, And Protected, Kept Unencumbered, Cared For, And PreservedPreserved

Subject To An Organizational Policy That Requires Subject To An Organizational Policy That Requires The Proceeds From Sales Of Collection Items To The Proceeds From Sales Of Collection Items To

Be Used To Acquire Other Items For Collections.Be Used To Acquire Other Items For Collections.

IntangiblesIntangibles

Software – Mainframe, Site Licenses, Software – Mainframe, Site Licenses, Upgrades, MaintenanceUpgrades, Maintenance

Radio Station LicenseRadio Station License

InfrastructureInfrastructure

Storm sewersStorm sewers

BridgesBridges

Parks (excluding land)Parks (excluding land)

RoadsRoads

TrailsTrails

IslandsIslands

Street lightsStreet lights

Traffic signalsTraffic signals

SignageSignage

BettermentsBetterments

What Are Betterments?What Are Betterments?

Extends The Estimated LifeExtends The Estimated Life

Exceeds A Certain CostExceeds A Certain Cost

A Big IssueA Big Issue

It Depends Upon The Property RecordIt Depends Upon The Property Record

GAAP ValuesGAAP Values

• Historical Cost

• Cost Of Capital Assets In Accordance With Costs

• Prevailing At Date Of Construction

• Installation

• Fair Market Value

• Estimated Amount At Which The Capital Asset Might Exchange Between Buyer And Seller Neither Under

Compulsion, Having Reasonable Knowledge Of All Relevant Facts – With Equity To Both

Inventorying Capital AssetInventorying Capital Asset

FrequencyFrequency

ProcessProcess

DiscrepanciesDiscrepancies

FrequencyFrequency

Original InventoryOriginal Inventory

Re-Inventory – At Least AnnuallyRe-Inventory – At Least Annually

ResponsibilityResponsibility

The Inventory ProcessThe Inventory Process

Project Planning MeetingProject Planning Meeting

InclusionsInclusionsExclusionsExclusionsTagging @ the Same Time?Tagging @ the Same Time?Utilizing Existing InventoriesUtilizing Existing Inventories

When To InventoryWhen To Inventory

• There Is No Correct TimeThere Is No Correct Time

• During The Normal WorkdayDuring The Normal Workday

• Nights Or WeekendsNights Or Weekends

Inventory - LandInventory - Land

– Listed By ParcelListed By Parcel

– Assessor's Parcel NumberAssessor's Parcel Number

– Lot, Block, TrackLot, Block, Track

– UseUse

– LocationLocation

Inventory - BuildingsInventory - Buildings

– Building TypeBuilding Type

– UseUse

– LocationLocation

Inventory - BuildingsInventory - Buildings

– Building TypeBuilding Type

– UseUse

– LocationLocation

Inventory – Machinery and Inventory – Machinery and EquipmentEquipment

– QuantityQuantity

– DescriptionDescription

– ManufacturerManufacturer

– Serial NumberSerial Number

– Year AcquiredYear Acquired

Inventory – Do’s and Don’tsInventory – Do’s and Don’ts

– Don't Start Inventories with Existing Inventory ListsDon't Start Inventories with Existing Inventory Lists

– Inventory by LocationInventory by Location

– Provide Advance NoticeProvide Advance Notice

– Avoid AbbreviationsAvoid Abbreviations

– Generic NameGeneric Name

– Write LegiblyWrite Legibly

Inventory – Do’s and Don’tsInventory – Do’s and Don’ts

• Organize Thoughts Before Making NotationsOrganize Thoughts Before Making Notations

• Review Field NotesReview Field Notes

• Use Available Resources ---- Ask QuestionsUse Available Resources ---- Ask Questions

• Maintain Contact with Those Responsible for the Maintain Contact with Those Responsible for the ProjectProject

• If You're Behind/Ahead of Schedule---Keep If You're Behind/Ahead of Schedule---Keep People AdvisedPeople Advised

Changes in Capital AssetsChanges in Capital Assets

• AdditionsAdditions

• DisposalsDisposals

• TransfersTransfers

• SurplusSurplus

AdditionsAdditions

• Purchased or ConstructedPurchased or Constructed

• LeasedLeased

• ContributedContributed

• Acquired Via TradesAcquired Via Trades

DisposalsDisposals

• Trade-insTrade-ins

• Sales – Sealed Bids - AuctionSales – Sealed Bids - Auction

• Cannibalization - BusesCannibalization - Buses

• Contributed to Other GovernmentsContributed to Other Governments

TransfersTransfers

• Between DepartmentsBetween Departments

• Between BuildingsBetween Buildings

• Any Budget Impact?Any Budget Impact?

SurplusSurplus

• Adding to SurplusAdding to Surplus

• Taking from SurplusTaking from Surplus

The Eight “W’s” to TaggingThe Eight “W’s” to Tagging

• Why Tag?Why Tag?

• Which Assets to Tag?Which Assets to Tag?

• What Types of Tags to Use?What Types of Tags to Use?

• Where to Purchase the Tags?Where to Purchase the Tags?

• What Should Appear on the Tag?What Should Appear on the Tag?

• When to Tag?When to Tag?

• Who Tags?Who Tags?

• Where is the Tag Placed?Where is the Tag Placed?

Tagging PurposeTagging Purpose

• Primary Purpose of a Tagging is toPrimary Purpose of a Tagging is to

Maintain a Positive Identification ofMaintain a Positive Identification of

Assets Owned by the GovernmentAssets Owned by the Government

Why Tag?Why Tag?

– Quick and Accurate Method of IdentifyingQuick and Accurate Method of Identifying

– Facilitate Re-inventoryFacilitate Re-inventory

– Controls the Location of AssetsControls the Location of Assets

– Assists in Maintaining AssetsAssists in Maintaining Assets

– Provides Common Ground for CommunicationProvides Common Ground for Communication

Which Assets Should Be Which Assets Should Be Tagged?Tagged?

• Influenced by Purpose of TaggingInfluenced by Purpose of Tagging

• Accounting IssuesAccounting Issues

• Property AccountabilityProperty Accountability

• Types of ActivitiesTypes of Activities

• Cost of TaggingCost of Tagging

What Type of Tags What Type of Tags Should We Use?Should We Use?

– MetalMetal

– Decal TypeDecal Type

– Bar CodedBar Coded

– Stencil/PaintedStencil/Painted

What Do We Purchase Tags?What Do We Purchase Tags?

• Office Equipment DealerOffice Equipment Dealer

• Yellow Pages of Telephone BookYellow Pages of Telephone Book

• The Type of Adhesive Must Be ConsideredThe Type of Adhesive Must Be Considered

• Prices VaryPrices Vary

What Should Be Imprinted on What Should Be Imprinted on the Tag?the Tag?

• Identifying MarkIdentifying Mark

• Numbering SystemNumbering System

– SequentialSequential

– ChronologicalChronological

When To Tag?When To Tag?

• Tag With Initial InventoryTag With Initial Inventory

• Normal Working Periods vs Nights and Normal Working Periods vs Nights and WeekendsWeekends

Who Should Tag?Who Should Tag?

• Accounting DepartmentAccounting Department

• Purchasing DepartmentPurchasing Department

• Receiving DepartmentReceiving Department

• Asset User (Police Department)Asset User (Police Department)

Where Should The Where Should The Tag Be Placed?Tag Be Placed?

• Placement Where Number Can Be Identified Placement Where Number Can Be Identified Without Disturbing The OperationWithout Disturbing The Operation

• Placement Allows For Easy Periodic Placement Allows For Easy Periodic Inventory TakingInventory Taking

• Placement Should Be ConsistentPlacement Should Be Consistent

Session 8Session 8

Depreciating Capital AssetsDepreciating Capital Assets

Depreciating Capital AssetsDepreciating Capital Assets

The MethodThe Method

The Estimated Useful LivesThe Estimated Useful Lives

Residual ValuesResidual Values

Fully Depreciated Capital AssetsFully Depreciated Capital Assets

Depreciating Capital AssetsDepreciating Capital Assets

When to Start Calculation DepreciationWhen to Start Calculation Depreciation

Charging to Applicable FunctionsCharging to Applicable Functions

Capital Assets For Resale –Capital Assets For Resale –Governmental FundsGovernmental Funds

Acquired Via Foreclosure and DonationsAcquired Via Foreclosure and Donations

Fund Balance Should Be ReservedFund Balance Should Be Reserved

Capital Assets Purchased Via Capital Assets Purchased Via Capital Lease –Capital Lease –

Governmental FundsGovernmental Funds

Debit - ExpendituresDebit - Expenditures

Credit – Other Financing Sources – Credit – Other Financing Sources – Inception of Capital LeaseInception of Capital Lease

Capital Assets Purchased By Capital Assets Purchased By Federal GovernmentFederal Government

Reversionary InterestReversionary Interest

Normally Reported As Governmental Normally Reported As Governmental AssetAsset

Capital Asset NoteCapital Asset NoteAdjusted

Balance Balance

7/1/02 Additions Deductions 6/30/03

Governmental activities:

Capital assets not being depreciated:

Land 11,612,251$ 434,038$ 30,000$ 12,016,289$

Construction in progress 186,870 5,254,702 29,673 5,411,899

Total capital assets not being depreciated 11,799,121 5,688,740 59,673 17,428,188

Depreciable capital assets:

Buildings 17,846,132 433,131 322,656 17,956,607

Improvements other than buildings 2,730,637 634,665 - 3,365,302

Machinery and equipment 4,875,353 499,778 - 5,375,131

Infrastructure 16,305,937 1,299,620 - 17,605,557

Total depreciable capital assets 41,758,059 2,867,194 322,656 44,302,597

Total capital assets 53,557,180 8,555,934 382,329 61,730,785

Accumulated depreciation:

Buildings 6,517,492 413,654 8,594 6,922,552

Improvements other than buildings 1,073,679 145,294 - 1,218,973

Machinery and equipment 2,721,992 451,734 - 3,173,726

Infrastructure 6,390,599 385,047 - 6,775,646

Total accumulated depreciation 16,703,762 1,395,729 8,594 18,090,897

Governmental activities capital assets, net 36,853,418$ 7,160,205$ 373,735$ 43,639,888$

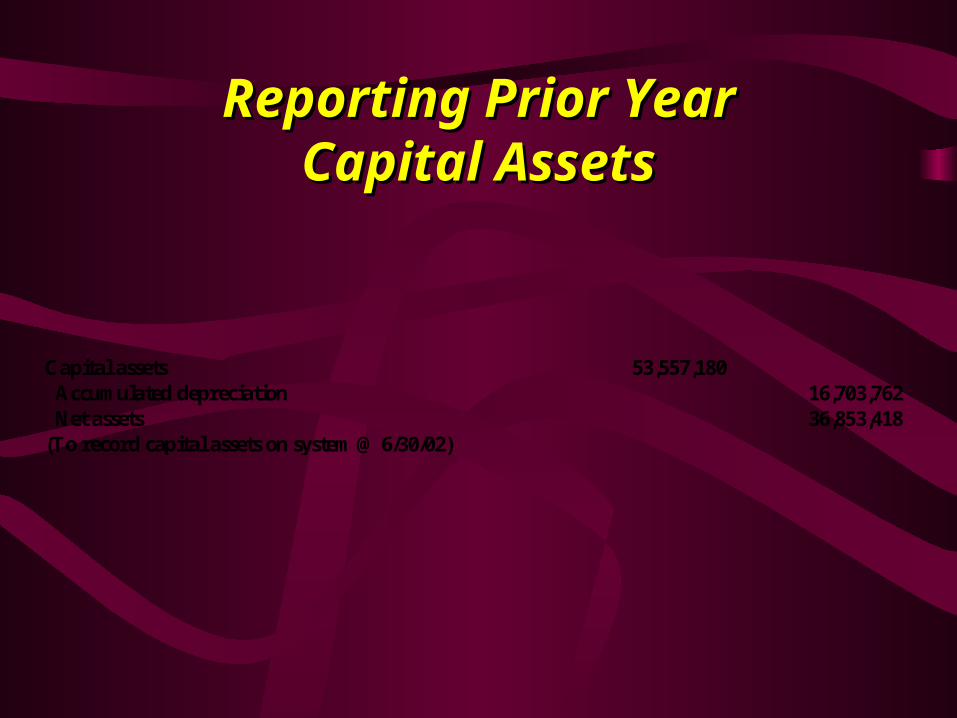

Reporting Prior YearReporting Prior YearCapital AssetsCapital Assets

Capital assets 53,557,180 Accumulated depreciation 16,703,762 Net assets 36,853,418 (To record capital assets on system @ 6/30/02)

Reporting Prior YearReporting Prior YearCapital AssetsCapital Assets

Depreciation - general government 102,585

Depreciation - public safety 252,904

Depreciation - public works 498,101

Depreciation - culture and recreation 132,650

Depreciation - housing and development 7,744

Depreciation - education 401,745

Accumulated depreciation 1,395,729 (To record fiscal year 2003 depreciation expense)

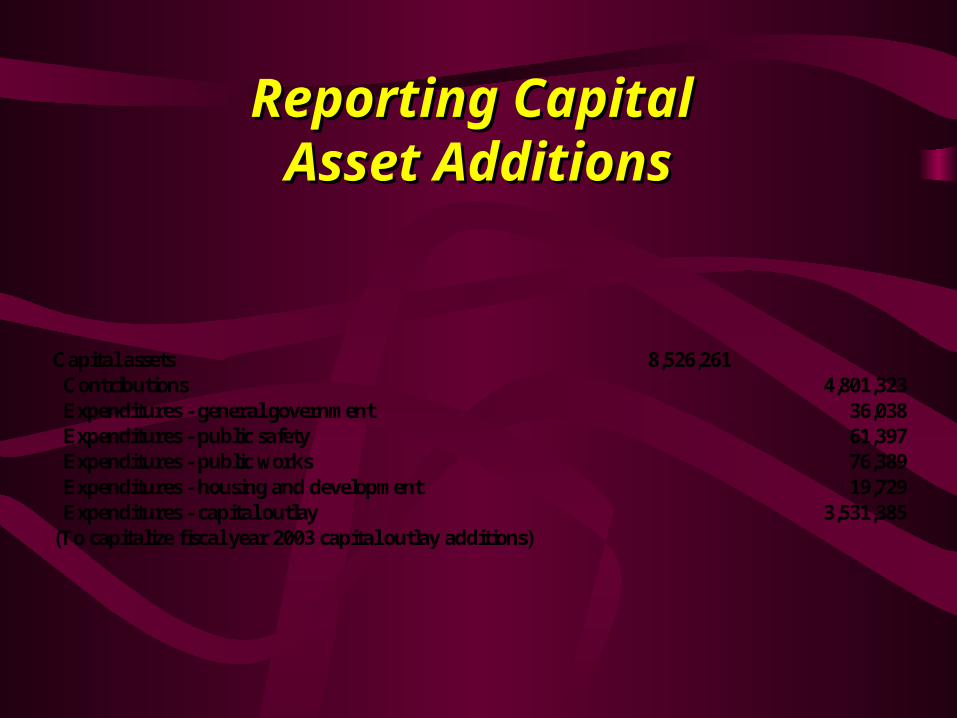

Reporting Capital Reporting Capital Asset AdditionsAsset Additions

Capital assets 8,526,261 Contributions 4,801,323 Expenditures - general government 36,038 Expenditures - public safety 61,397 Expenditures - public works 76,389 Expenditures - housing and development 19,729 Expenditures - capital outlay 3,531,385 (To capitalize fiscal year 2003 capital outlay additions)

Reporting Capital Reporting Capital Asset DeletionsAsset Deletions

Accumulated depeciation 8,594 Disposition of capital assets 344,062 Capital assets 352,656 (To record disposition of capital asset in fiscal year 2003)

WE ARE FINISHED!WE ARE FINISHED!

• ANY QUESTIONS, FEEL FREE TO ANY QUESTIONS, FEEL FREE TO EMAIL ME:EMAIL ME:

[email protected]@mindspring.com

• OR CALL ME @ 352/875-7449OR CALL ME @ 352/875-7449