capital link shipping weekly markets reportvaluation through their positioning in the investment...

TRANSCRIPT

Monday, April 2, 2012 (Week 14)

IN THE NEWS→ Capital Link’s 6th Annual Invest in Shipping Forum is a Great Success, Sets New Record in Attendance → Latest Company News→ Select Dividend Paying Shipping Stocks

CAPITAL MARKETS DATA→ Currencies, Commodities & Indices→ Shipping Equities - Weekly Review→ Weekly Trading Statistics, by Knight Capital→ Shipping Bonds - Weekly Review, by Knight Capital

SHIPPING MARKETS→ Dry Bulk Market - Weekly Highlights, by Intermodal Shipbrokers → Weekly Tanker Market Opinion, by Poten & Partners→ The Week In Review, by Golden Destiny → Tanker Market - Weekly Highlights, by Charles R. Weber Company → Weekly Freight Rate & Asset Trends, by Intermodal Shipbrokers→ Container Market - Weekly Highlights, by Braemar Seascope→ S&P Secondhand, Newbuilding & Demolition Markets, by Golden Destiny

TERMS OF USE & DISCLAIMER

CONTENT CONTRIBUTORS

Capital Link Shipping Weekly Markets Report

New York - 230 Park Avenue, Suite 1536, New York, NY, 10169 Tel.: +1 212 661 7566 Fax: +1 212 661 7526London - Longcroft House,2-8 Victoria Avenue, London, EC2M 4NS, U.K Tel. +44(0) 203 206 1320 Fax. +44(0) 203 206 1321Athens - 40, Agiou Konstantinou Str, Suite A 5, 151-24 Athens, Greece Tel. +30 210 6109 800 Fax +30 210 6109 801

Capital Link - New York - London - Athenswww.capitallink.comwww.capitallinkforum.com

www.CapitalLinkShipping.comA web based resource that provides information on the major shipping and stock market

Investor Relations & Financial Advisory

indices, as well as on all shipping stocks. It also features an earnings and conference call calendar, industry reports from major industry participants and interviews with CEOs, analysts and other market participants.

www.CapitalLinkWebinars.comSector Forums & Webinars: Regularly, we organize panel discussions among CEOs, analysts, bankers and shipping industry participants on the developments in the various shipping sectors (containers, dry bulk, tankers) and on other topics of interest (such as Raising Equity in Shipping Today, Scrapping, etc).

Capital Link Investor Shipping ForumsIn New York, Athens and London bringing together investors, bankers, financial advisors, listed companies CEOs, analysts, and shipping industry participants.

www.MaritimeIndices.comCapital Link Maritime Indices: Capital Link developed and maintains a series of stock market maritime indices which track the performance of U.S. listed shipping stocks (CL maritime Index, CL Dry Bulk Index, CL Tanker Index, CL Container Index, CL LNG/LPG Index, CL Mixed Fleet Index, CL Shipping MLP Index – Bloomberg page: CPLI. The Indices are also distributed through the Reuters Newswires and are available on Factset.

Capital Link Shipping Weekly Markets ReportWeekly distribution to an extensive audience in the US & European shipping, financial and investment communities with updates on the shipping markets, the stock market and listed company news.

Operating more like a boutique investment bank rather than a traditional Investor Relations firm, our objective is to assist our clients enhance long term shareholder value and achieve proper valuation through their positioning in the investment community. We assist them to determine their objectives, establish the proper investor outreach strategies, generate a recurring information flow, identify the proper investor and analyst target groups and gather investor and analyst feedback and related market intelligence information while keeping track of their peer group. Also, to enhance their profile in the financial and trade media.

Capital Link is a New York-based Advisory, Investor Relations and Financial Communications firm. Capitalizing on our in-depth knowledge of the shipping industry and capital markets, Capital Link has made a strategic commitment to the shipping industry becoming the largest provider of Investor Relations and Financial Communications services to international shipping companies listed on the US and European Exchanges. Capital Link's headquarters are in New York with a presence in London and Athens.

In our effort to enhance the information flow to the investment community and contribute to improving investor knowledge of shipping, Capital Link has undertaken a series of initiatives beyond the traditional scope of its investor relations activity, such as:

...Linking Shipping and Investors Across the GlobeCapital Link Shipping

CAPITAL LINK’S 6TH ANNUAL INVEST IN SHIPPING FORUM IS A GREAT SUCCESS, SETS NEW RECORD IN ATTENDANCE

PRESS RELEASE

CONFERENCE MATERIALS AND EXECUTIVE VIDEO INTERVIEWS AVAILABLE AT www.CapitalLinkShipping.com.

NEW YORK, NY, MARCH 26, 2012—Capital Link’s 6th Annual Invest in International Shipping Forum took place on Monday, March 19, 2012, in New York City with great success and with an attendance of 927, setting a new record.

18 Shipping Companies, analysts, financiers, and market Eeperts participated in various panels and presentations.

The forum provided a comprehensive review and outlook on the various markets—the container, dry bulk, and tanker sectors in addition to offshore drilling—made more relevant by the timely release of companies’ annual performance results. The event also examined critical issues affecting the shipping industry, such as bank financing, access to the capital markets, alternative financing, restructuring, bankruptcy, ship recycling, and investment opportunities in shipping.

CONFERENCE MATERIAL

There is an archive of all presentations and panel discussions, including slides and audio files.Please click on the following link or copy and paste it into your browser: www.CapitalLinkShipping.com.

EXECUTIVE VIDEO INTERVIEWS

The 6th Annual Invest in International Shipping Conference took place at the Metropolitan Club in New York City.

Tradewinds TV interviewed several of the participating executives at the Capital Link Shipping Forum. In addition, Barry Parker also conducted several interviews for Capital Link Shipping.

An archive of all these executive interviews can be found by clicking on the following link or copying and pasting it into your browser: www.CapitalLinkShipping.com.

PARTICIPATING SHIPPING COMPANIES

• Danaos Corporation (NYSE: DAC) • DryShips Inc. (NASDAQ: DRYS) • Euroseas Ltd. (NASDAQ: ESEA) • Excel Maritime Carriers Ltd (NYSE: EXM) • General Maritime Corporation (OTC.BB: GMRRQ.OB) • Maersk Broker K/S • Navios Maritime Acquisition (NYSE: NNA) • Navios Maritime Holdings Inc. (NYSE: NM) • Ocean Rig (NASDAQ: ORIG) • Odfjell Drilling (Oslo: ODF.OL) • Prospector Offshore Drilling S.A. (Oslo: PROS.OL) • Safe Bulkers, Inc. (NYSE: SB) • Scorpio Tankers Inc. (NYSE: STNG) • Seadrill / North Atlantic Drilling (NYSE: SDRL) • Seanergy Maritime Holdings Corp. (NASDAQ: SHIP)

• Star Bulk Carriers Corp. (NASDAQ: SBLK) • Synergy Marine • Tsakos Energy Navigation Ltd (NYSE: TNP)

PARTICIPATING ANALYSTS

• Clarkson Capital Markets • Knight Capital Americas • Jefferies & Co. • Morgan Stanley • RS Platou Markets • Wells Fargo Securities, LLC

PARTICIPATING BANKS, AUDITING AND LAW FIRMS & OTHER ORGANIZATIONS

• ABN AMRO • AMA Capital Partners • Bank of America Merrill Lynch • Bracewell & Giuliani LLP • Clarkson Capital Markets • DVB Group • Ernst & Young • Fried, Frank, Harris, Shriver & Jacobson LLP • Gibson, Dunn & Crutcher LLP

• Global Marketing System (GMS) • Jefferies & Co. • Knight Capital Group • Morgan, Lewis & Bockius LLP • Morgan Stanley • Nordea Bank Norge ASA • PwC • RS Platou Markets • Seward & Kissel LLP • Watson, Farley & Williams LLP • Wells Fargo Securities, LLC

SPONSORS, SUPPORTING ORGANIZATIONS & MEDIA PARTNERS

In Cooperation With: NYSE, NASDAQ OMX

Global Lead Sponsors: ABN AMRO, Tsakos Energy Navigation Ltd

Global Gold Sponsors: Knight Capital Group, DVB Bank

Global Silver Sponsors: Clarksons, Ernst & Young, PwC, International Registries, Inc.

Global Corporate Sponsors: AMA Capital Partners, Bank of America Merrill Lynch, Fried, Frank, Harris, Shriver & Jacobson LLP, Global Marketing System (GMS), Jefferies & Co., Morgan Stanley, RS Platou Markets, Watson, Farley & Williams LLP, Wells Fargo Securities, LLC

Event Sponsors & Presenters: Bracewell & Giuliani, Danaos Corporation, DryShips Inc., Euroseas Ltd., Excel Maritime Carriers Ltd, Gibson, Dunn & Crutcher LLP, Morgan, Lewis & Bockius, Navios Maritime Holdings Inc., Navios Maritime Acquisition, Nordea Bank Norge ASA, Ocean Rig, Safe Bulkers, Inc., Seanergy Maritime Holdings, Star Bulk Carriers Corp.

“Alternative Sources of Ship Finance Panel” from left ot right: Erik Helberg (RS Platou Markets), Peter Sorkin (Knight Capital Group), Hamish Norton (Jefferies & Co.), and Sofia Kalomenidis (Ernst & Young).

Nick Kounis (ABN AMRO) delivers the current state of the global economy and world trade.

Anil Sharma (Global Marketing Systems) presents on “Ship Recycling - Headline ‘Risk’ or Opportunity?”

COMPANY PRESENTATIONS

Evangelos Chatzis, CFO, Danaos Corporation

Aristides J. Pittas, CEO, Euroseas Ltd

Pavlos Kanellopoulos, CFO, Excel Maritime Carriers Ltd

Loukas Barmparis, President & Director, Safe Bulkers Inc.

Dale Ploughman, CEO, Seanergy Maritime Holdings Corp.

Spyros Capralos, CEO, Star Bulk Carriers Corp.

George Saroglou, COO, Tsakos Energy Navigation, Ltd

SECTOR PANEL DISCUSSIONS

“Container Sector Panel” from left to right: Kevin Kennedy (The Synergy Group), Claes Devantier (Maersk Broker), Aristides J. Pittas (Euroseas Ltd), John Coustas (Danaos Corporation), and Michael Webber (Wells Fargo Securities, LLC).

“Dry Bulk Sector Panel” from left to right: Spyros Capralos (Star Bulk Carriers Corp.), Dale Ploughman (Seanergy Maritime Holdings Corp.), Loukas Barmparis (Safe Bulkers Inc.), Ismini Panayotides (Excel Maritime Carriers Ltd), and Ben Nolan (Knight Capital Group).

“Tanker Sector Panel” from left to right: Robert Bugbee (Scorpio Tankers), Ted Petrone (Navios Maritime Acquisition), George Saroglou (Tsakos Energy Navigation), and Douglas J. Mavrinac (Jefferies & Co.).

“Offshore Panel” from left to right: Tor Olav Trøim, (Seadrill / North Atlantic Drilling Ltd), Bill Rose (Prospector Offshore Drilling), Simen Lieungh (Odfjell Drilling), George Economou (Ocean Rig), and Anders Bergland (RS Platou Markets).

Supporting Organizations & Media Partners: Barron’s, IMASMA, Lloyd’s List, The Maritime Executive, NAMEPA, New York Maritime, Inc. (NYMAR), Ship2Shore, TradeWinds, WISTA USA, Worldoils

ABOUT THE ORGANIZER – CAPITAL LINK, INC.

Capital Link is a New York-based Investor Relations and Financial Communications firm. Capitalizing on its in-depth knowledge of the shipping industry and capital markets, Capital Link has made a strategic commitment to the industry, becoming the largest provider of Investor Relations and Financial Communications services to international shipping companies listed on the US and European Exchanges. Capital Link’s

PANEL DISCUSSIONS & PRESENTATIONS

A networking cocktail reception took place after the forum.

headquarters are in New York with a presence in London and Athens. Capital Link is a member of the Baltic Exchange.

Magnus Fyhr (Clarkson Capital Markets) delivers a presentation on “Investment Opportunities in Shipping Today.”

Members of the “Analyst Panel” Investor Attitudes in Shipping & Shipping Markets Outlook” from left to right: Douglas Mayvrinac (Jefferies & Co.), Michael S. Pak (Clarkson Capital Markets), and Daniel Rodgers (Watson, Farley & Williams LLP.

“Chapter 11: Safe Haven or Bermuda Triangle?” from left to right: Steve Strom (Jefferies & Co.), John Asmead (Seward & Kissel LLP), and Robert G. Burns (Bracewell & Giuliani LLP.

“Shipping & Bank Financing” from left to right: Ronny Bjørnådal (Nordea Bank), Evan Cohen (DVB Group), Gust Biesbroeck (ABN AMRO), and Emil Yiannopoulos (PwC Greece).

Capital Link, Inc.230 Park Avenue, Suite 1536New York, NY 10169T: (212) 661-7566 | F: (212) 661-7526www.capitallinkshipping.com | forums.capitallink.com

Monday, April 2, 2012 (Week 14)Capital Link Shipping Weekly Markets Report

Page 7

IN THE NEWS

Monday, March 26, 2012

Scorpio Tankers Inc. Announces Agreement to Construct One Newbuilding

Scorpio Tankers Inc. (NYSE: STNG) announced that it has signed a contract with Hyundai Mipo Dockyard Co., Ltd. of South Korea (“HMD”) to construct a 52,000 DWT MR product tanker for $36.0 million, which is the Company’s eighth 52,000 DWT MR product tanker newbuilding with HMD. The eighth newbuilding is scheduled to be delivered to the Company in May 2013.

Tuesday, March 27, 2012

Hercules Offshore Prices Private Placement of Senior Secured Notes and Senior Notes

Hercules Offshore, Inc. (Nasdaq: HERO) announced that it has priced a private placement of $300,000,000 aggregate principal amount of senior secured notes due 2017 (the “secured notes”), which will bear an interest rate of 7.125% per annum. The Company also announced that it has priced a private placement of $200,000,000 aggregate principal amount of senior notes due 2019 (the “unsecured notes” and, together with the secured notes, the “notes”), which will bear an interest rate of 10.25% per annum. The notes are being sold at par. Hercules Offshore expects to use the net proceeds from the notes offering to repay all of the indebtedness outstanding under our existing secured term loan. As a result of the repayment of our term loan, our outstanding 10.5% Senior Secured Notes will become unsecured. The Company expects to use the remaining net proceeds for general corporate purposes, including to fund a portion of the purchase price for the previously announced acquisition of the drilling rig Ocean Columbia as well as the costs associated with the repair, upgrade and mobilization of the Ocean Columbia.

Wednesday, March 28, 2012

Euroseas Ltd. Announces New Acquisition for Its Joint Venture Euromar LLC

Euroseas Ltd., (NASDAQ: ESEA) announced that its joint venture, Euromar LLC (“Euromar”), signed a memorandum of agreement to purchase the M/V Cap Norte, a gearless containership of 41,850 dwt and 3,091 teu built in 2007 in Poland. M/V Cap Norte comes with a 3-year time charter at about $17,500 per day to a first class charterer. M/V Cap Norte, to be renamed EM Kea, is expected to be delivered not later than June 16, 2012.

Thursday, March 29, 2012

Diana Shipping Inc. Signs Shipbuilding Contracts for the Purchase of Two Ice Class Panamax Dry Bulk Carriers

Diana Shipping Inc. (NYSE:DSX) announced that it has signed, through separate wholly-owned subsidiaries, two shipbuilding contracts with China Shipbuilding Trading Company, Limited and Jiangnan Shipyard (Group) Co., Ltd, for the construction of two Ice Class Panamax dry bulk carriers of approximately 76,000 dwt

each for a contract price of US$29 million per vessel. The Company expects to take delivery of the vessels during the fourth quarter of 2013. Excluding the two vessels described above and the previously announced Newcastlemax new-building dry bulk carrier that is expected to be delivered during the second quarter of 2012, Diana Shipping Inc.’s fleet currently consists of 26 dry bulk carriers (16 Panamax, 1 Post-Panamax, 8 Capesize and 1 Newcastlemax) with a weighted average age of 6 years.

Friday, March 30, 2012

Vantage Drilling Announces Proposed Offering by Its Subsidiary Offshore Group Investment Limited of Additional 11 1/2% Senior Secured First Lien Notes Due 2015

Vantage Drilling Company (AMEX: VTG) announced that its wholly-owned subsidiary Offshore Group Investment Limited (the “Issuer”) intends to offer, subject to market and other conditions, $775.0 million in aggregate principal amount of 11 1/2% Senior Secured First Lien Notes due 2015 (the “Notes”). The Notes will be offered as additional notes under an existing indenture pursuant to which the Issuer previously issued $1.0 billion aggregate principal amount of 11 1/2% Senior Secured First Lien Notes due 2015 in July 2010 and an additional $225.0 million aggregate principal amount of 11 1/2% Senior Secured First Lien Notes due 2015 in June 2011. The Notes will be guaranteed by Vantage and each of the Issuer’s existing and future subsidiaries and by certain of Vantage’s other subsidiaries and will be senior secured obligations of the Issuer and the guarantors.

Navios Maritime Holdings Inc. Announces Delivery of One Newbuild Kamsarmax Vessel

Navios Maritime Holdings Inc. (“Navios Holdings”) (NYSE: NM ) announced that the Navios Centaurus, a new building Kamsarmax vessel of 81,472 dwt, was delivered today from a South Korean shipyard to Navios Holdings’ owned fleet. The vessel is chartered-out for 2 years at a net rate of $12,825 per day. It is anticipated that the Navios Centaurus will generate annual EBITDA of $3.0 million and aggregate EBITDA of $6.0 million over the life of the charter contract.

Diana Shipping Inc. Announces the Acquisition of a Panamax Dry Bulk Carrier

Diana Shipping Inc. (NYSE:DSX) announced that it has signed, through a separate wholly-owned subsidiary, a Memorandum of Agreement to purchase from an unaffiliated third party the m/v “Mining Star”, a 2005 built Panamax dry bulk carrier of 76,225 dwt, for a price of US$20.65 million. The vessel, to be renamed “Melia”, is expected to be delivered to the Company by the sellers in mid-April 2012. Excluding the aforementioned vessel our fleet currently consists of 26 dry bulk carriers (16 Panamax vessels, 8 Capesize vessels, 1 Post-Panamax vessel and 1 Newcastlemax vessel), as well as 1 new building Newcastlemax vessel expected to be delivered to the Company during the second quarter of 2012 and 2 new building Ice Class Panamax vessels expected to be delivered to the Company during the fourth quarter of 2013. As of today, the combined carrying capacity of our current fleet, excluding the

Latest Company News

Monday, April 2, 2012 (Week 14)Capital Link Shipping Weekly Markets Report

Page 8

IN THE NEWS

four vessels not yet delivered, is 2.9 million dwt with a weighted average age of 6 years. A table describing the current Diana Shipping Inc. fleet can be found on the Company’s website, www.dianashippinginc.com. Information contained on the Company’s website does not constitute a part of this press release.

Monday, April 02, 2012

Ocean Rig UDW Inc. Announces Acceptance by Petrobras of the Ocean Rig Mykonos

Ocean Rig UDW Inc. (NASDAQ: ORIG) announced that on March 22, 2012, the Ocean Rig Mykonos completed the general testing of equipment as required by Petroleo Brazilieiro S.A., and has commenced revenue-generating drilling operations in Brazil.

Navios Maritime Holdings Inc. Announces Acquisition of One Handysize Vessel and Favorable Financing of Acquired and Existing Vessels

Navios Maritime Holdings Inc. (NYSE: NM) announced that it has acquired the Navios Serenity, a 2011-built Handysize vessel of 34,718 DWT, for $26.0 million. The vessel was previously part of Navios Holdings’ long-term chartered-in fleet. The improvement to cash flow, as a result of the replacement of the charter-in cost, is estimated at approximately $2.4 million on an annualized basis. The acquisition of Navios Serenity is financed by a new credit facility of up to $42.0 million with a syndicate of commercial banks. The new facility will also refinance the existing debt of Navios Astra due for repayment in 2013, thus eliminating refinancing risk for 2013. The new facility has a term of 8 years and is divided in two tranches having amortization profile of 18 and 14 years and margin of 2.85% and 3.6% respectively.

The leading specialist in international transport finance

www.dvbbank.com

Frankfurt/Main · Hamburg · London · Cardiff · Rotterdam · BergenOslo · Piraeus · Zurich · Singapore · Tokyo · New York · Curaçao

0611_DVB-Anz_half-page_quer.indd 1 07.06.11 13:25

Monday, April 2, 2012 (Week 14)Capital Link Shipping Weekly Markets Report

Page 9

IN THE NEWS

Select Dividend Paying Shipping Stocks

Get your message across to

36,000 weekly recipients around the globeJoin a select group of shipping & financial industry’s advertisers by promoting your brand with

Capital Link’s Shipping Weekly Markets Report.

For additional advertising information and a media kit, please contact/email:

Nicolas Bornozis at +1 212 661-7566, [email protected]

Company Name Ticker Quarterly Dividend

Annualized Dividend

Last Closing Price (MAR-30, 2012)

Annualized Dividend Yield

Containers Costamare Inc CMRE $0.27 * $1.08 $13.77 7.84% Dry Bulk Globus Maritime Limited GLBS $0.16 $0.64 $5.08 12.60% Navios Maritime Holdings Inc NM $0.06 $0.24 $4.20 5.71% Navios Maritime Partners NMM $0.44 $1.76 $16.67 10.56% Safe Bulkers Inc SB $0.15 $0.60 $6.68 8.98% Star Bulk Carriers Corp SBLK $0.015 $0.06 $0.90 6.67% Tankers Capital Product Partners Lp CPLP $0.2325 $0.93 $8.11 11.47% Navios Maritime Acquisition Corp NNA $0.05 $0.20 $3.26 6.13% Tsakos Energy Navigation Ltd TNP $0.15 $0.60 $8.68 6.91% Mixed Fleet Euroseas Ltd ESEA $0.05 $0.20 $2.28 8.77%

London Listed Companies (Great British Pence) Ticker

2011 Total Dividend

Last Closing Price (MAR-30, 2012)

Annualized Dividend Yield

Goldenport Holdings GPRT 6.00 81.75 7.34%

*Board approved an eight percent (8%) dividend increase, beginning with the third quarter 2011 dividend, raising the quarterly dividend from $0.25 to $0.27 per common share.

Monday, April 2, 2012 (Week 14)Capital Link Shipping Weekly Markets Report

Page 11

CAPITAL MARKETS DATA

Currencies, Commodities & IndicesWeek ending Friday, March 30, 2012

KEY CURRENCY RATES

Rate Current Price Price Last Week % Change YTD %Chg 52 Week High 52 Wk Low 3-Month LIBOR 0.4682 0.4732 -1.07% -19.63% 0.5393 0.2844 10-Yr US Treas. Yield 2.2124 2.2317 -0.86% 13.61% 3.3190 2.3833 USD/EUR 0.7494 0.7537 -0.57% -2.19% 0.7920 0.6694 USD/GBP 0.6250 0.6301 -0.81% -2.18% 0.6563 0.5972 USD/JPY 82.0800 82.6300 -0.67% 7.07% 85.5300 75.3800 USD/CNY 6.2962 6.3001 -0.06% 0.00% 6.5480 6.2870

PRECIOUS METALS

Current Price Price Last Week % Change YTD %Chg 52 Week High 52 Wk Low Gold 1,663.65 1,651.25 0.75% 3.89% 1,921.15 1,428.15 Silver 32.42 31.72 2.20% 10.30% 49.79 26.07 Platinum 1,646.25 1,623.75 1.39% 15.61% 1,916.75 1,344.25 Copper 382.65 380.80 0.49% 8.45% 452.60 305.00 Palladium 653.40 658.75 -0.81% -1.52% 773.60 583.25

KEY AGRICULTURAL & CONSUMER COMMODITIES

Current Price Price Last Week % Change YTD %Chg 52 Week High 52 Wk Low Corn 644.00 646.50 -0.39% -2.20% 793.00 584.50 Soybeans 1,403.00 1,365.75 2.73% 14.30% 1,468.50 1,115.50 Wheat 660.75 654.25 0.99% 0.57% 975.00 597.50 Cocoa 2,219.00 2,307.00 -3.81% 4.92% 3,367.00 2,005.00 Coffee 182.45 178.75 2.07% -19.70% 311.55 174.45

Cotton 93.52 89.63 4.34% -2.38% 125.37 84.23 Sugar #11 24.71 25.63 -3.59% 0.82% 27.03 21.00

KEY FUTURES

Commodities Current Price Price Last Week % Change YTD %Chg 52 Week High 52 Wk Low Gas Oil 1,012.00 1,026.25 -1.39% 6.89% 1,045.75 810.75 WTI Crude 103.06 106.80 -3.50% 0.10% 113.40 76.53 Natural Gas 2.12 2.27 -6.70% -29.23% 4.98 2.07

Heating Oil 316.84 320.77 -1.23% 4.29% 331.27 258.00

Gasoline RBOB 338.99 338.64 0.10% 23.33% 341.18 247.07

Monday, April 2, 2012 (Week 14)Capital Link Shipping Weekly Markets Report

Page 12

CAPITAL MARKETS DATA

Currencies, Commodities & IndicesMAJOR INDICES

Index Symbol Close Last Week % Change YTD % Change 4-Jan-12

Dow Jones INDU 13,212.04 13,080.73 1.00% 6.57% 12,720.48

Dow Jones Transp. TRAN 5,253.16 5,217.82 0.68% 3.70% 5,280.75

NASDAQ CCMP 3,091.57 3,067.92 0.77% 16.72% 2,786.70

NASDAQ Transp. CTRN 2,424.47 2,403.42 0.88% 10.80% 2,297.32

S&P 500 SPX 1,408.47 1,397.11 0.81% 10.29% 1,315.38

Russell 2000 Index RTY 830.30 830.03 0.03% 10.37% 784.62

Amex Oil Index XOI 1,267.37 1,283.12 -1.23% 0.52% 1,273.79

FTSE 100 Index UKX 5,768.45 5,854.89 -1.48% 1.20% 5,728.55

CAPITAL LINK MARITIME INDICES

Index Symbol 30-March-12 23-March-12 % Change 4-Jan-12 YTD % Change

Capital Link Maritime Index CLMI 2,196.69 2,185.23 0.52% 2,185.20 0.53% Tanker Index CLTI 2,196.56 2,150.13 2.16% 1,888.57 16.31% Drybulk Index CLDBI 717.67 708.33 1.32% 661.81 8.44% Container Index CLCI 1,216.36 1,222.87 -0.53% 1,112.58 9.33% LNG/LPG Index CLLG 3,775.44 3,774.34 0.03% 3,810.14 -0.91% Mixed Fleet Index CLMFI 1,401.64 1,376.82 1.80% 1,030.58 36.00% MLP Index CLMLP 3,126.23 3,137.23 -0.35% 2,755.12 13.47%

BALTIC INDICES

Index Symbol 30-March-12 23-March-12 % Change 4-Jan-12 YTD % Change Baltic Dry Index BDIY 934 908 2.86% 1,624 -42.49% Baltic Capesize Index BCIY 1,412 1,369 3.14% 2,955 -52.22% Baltic Panamax Index BPIY 1,051 1,036 1.45% 1,619 -35.08%

Baltic Supramax Index BSI 1,030 1,035 -0.48% 1,158 -11.05% Baltic Handysize Index BHSI 565 551 86.93% 570 80.70%

Baltic Dirty Tanker Index BDTI 818 809 1.11% 783 4.47% Baltic Clean Tanker Index BCTI 642 650 -1.23% 762 -15.75%

Monday, April 2, 2012 (Week 14)Capital Link Shipping Weekly Markets Report

Page 13

CAPITAL MARKETS DATA

Shipping Equities: The Week in Review

MARITIME INDEX DAILY COMPARISON CHARTS (52 WEEK)*

CAPITAL LINK TANKER INDEX DAILY COMPARISON CHARTS

CAPITAL LINK DRY BULK INDEX DAILY COMPARISON CHARTS

*SOURCE: BLOOMBERG

0.700.750.800.850.900.951.001.051.101.15

Capital Link Maritime Index S&P 500 Russell 2000

0.350.500.650.800.951.101.251.401.55

Capital Link Drybulk Index Baltic Dry Index

0.500.700.901.101.301.501.701.90

Capital Link Tanker Index Baltic Clean Tanker Index Baltic Dirty Tanker Index

SHIPPING EQUITIES UNDERPERFORM THE BROADER MARKETTANKERS THE BEST PERFORMER

During last week, shipping equities underperformed the broader market, with the Capital Link Maritime Index (CLMI), a composite index of all US listed shipping stocks inching up 0.52%, compared to the S&P 500 rising 0.81%, and the Dow Jones Industrial Average (DJII) up 1.00%. U.S. stock markets closed out their best first quarter since this century, largely on the back of improving domestic economic data.

Tanker equities performed the best during last week, with the Index up 2.16%, followed by Mixed Fleet Index increasing 1.80%. Container equities were the worst performer again last week, with Capital Link Container Index sliding 0.53%. The biggest winners in Shipping Equities last week were Teekay Tankers (TNK), Overseas Shipholdings (OSG) and Tsakos Energy Navigation (TNP), up 15.84%, 13.35% and 11.83%, respectively.

Dry Bulk shipping stocks underperformed the physical market, with the Capital Link Dry Bulk Index up 1.32%, compared to the Baltic Dry Index (BDI) increasing 2.86%. Year-to-date, the BDI is now down 42.49% compared to the Capital Link Dry Bulk Index gaining 8.44%.

Tanker stocks outperformed the physical market, with Capital Link Tanker Index soaring 2.16% last week, compared to Baltic Dirty Tanker Index (BDTI) rising 1.11%, with the demand from China pushing VLCC rates higher, and Baltic Clean Tanker Index (BCTI) losing 1.23%. Year-to-date, the BDTI is up 4.47% while the BCTI is down 15.75%, and the Capital Link Tanker Index stays positive with a gain of 16.31%.

The Trading Statistics supplied by Knight Capital provide details of the trading performance of each shipping stock and analyze the market’s trading momentum and trends for the week and year-to-date.

The objective of the Capital Link Maritime Indices is to enable investors, as well as all shipping market participants, to better track the performance of listed shipping stocks individually, by sector or as an industry. Performance can be compared to other individual shipping stocks, to their sector, to the broader market, as well as to the physical underlying shipping markets or other commodities. The Indices currently focus only on companies listed on US Exchanges providing a homogeneous universe. They are calculated daily and are based on the market capitalization weighting of the stocks in each index. In terms of historical data, the indices go back to January 1, 2005, thereby providing investors with significant historical performance.

There are seven indices in total; the Capital Link Maritime Index comprised of all 44 listed shipping stocks, and six Sector Indices, the CL Dry Bulk Index, the CL Tanker Index, the CL Container Index, the CL LNG / LPG Index, the CL Mixed Fleet Index and the CL Maritime MLP Index.

The Index values are updated daily after the market close and can be accessed at www.CapitalLinkShipping.com or at or www.MaritimeIndices.com. They can also be found through the Bloomberg page “CPLI” and Reuters.

FROM DEEP SEA TO DEEP KNOWLEDGE

In a volatile world market, a bank with global presence and staying power is rare. ABN AMRO has been fi nancing this sector since 1720. Many clients

have been with us for decades because our support goes beyond dollars. A stable team of sector specialists with the experience to advise you on

funding diversifi cation and strategic capital management, we offer a complete product range and the industry know-how to develop creative solutions.

Add fast decision-making, fl awless execution, and integrated risk and portfolio management, and you can see why companies tend to stay with us for

the long haul. For more on how our Transportation team could support your business, visit abnamro.com/ect

ABN ECT_Adv_1-1_Transport 210x280_WT.indd 1 07-02-12 11:41

Monday, April 2, 2012 (Week 14)Capital Link Shipping Weekly Markets Report

Page 15

CAPITAL MARKETS DATA

Weekly Trading Statistics

Custom Statistics Prepared Weekly for Capital Link Shipping

BROAD MARKET Percent Change of Major Indexes for the Week Ending Friday, March 30, 2012 Name Symbol Close Net Gain Percent Gain Dow Jones Industrial Average Index INDU 13212.04 131.31 1.00% Nasdaq-100 Index NDX 2755.27 26.72 0.98% Nasdasq Transportation Index TRANX 2424.47 21.05 0.88% S&P 500 Index SPX 1408.47 11.36 0.81% Russell 1000 Index RUI 778.91 5.98 0.77% Nasdaq Composite Index COMPX 3091.57 23.65 0.77% Russell 3000 Index RUA 834.08 5.94 0.72% Dow Jones Transportation Index TRAN 5253.16 35.34 0.68% Phlx Semiconductor Sector Index SOX 438.62 2.94 0.67% Russell 2000 Index RUT 830.39 0.36 0.04%

Index Data: INDU (Dow Jones Industrial Average Index. The INDU closed today at 13,212.04 for a weekly gain of 131.31 pts (+1.0038%). The high of the week was 13,298.96 while the low was 12,993.84 (close = 71.51% of high/low range). The INDU closed 0.90% from its 52 week high (13,331.77) and 27.50% from its 52 week low (10,362.26).

INDU Important Moving Averages

50 Day: 12,941.46 100 Day: 12,505.06 200 Day: 12,092.72

SHIPPING INDUSTRY DATA (50 Companies) Moving Averages

48.84% closed > 10D Moving Average. 72.09% closed > 50D Moving Average. 76.74% closed > 100D Moving Average. 69.77% closed > 200D Moving Average.

Top Upside Momentum (Issues with the greatest 100 day upside momentum*)

Top Downside Momentum (Issues with the greatest 100 day downward momentum*)

Symbol Close Weekly % Change

50-Day % Change

NEWL 1.77 41.60% 185.48% FREE 1.08 -16.28% 151.16% GSL 3.46 2.06% 81.15% FRO 7.1 -7.19% 57.43% GASS 6.14 4.07% 47.60% EGLE 1.8 2.27% 66.67% TNP 7.8 4.98% 48.01% SFL 15.05 -3.90% 50.50% TK 33.13 1.56% 29.57% DRYS 3.38 -7.14% 51.57%

*Momentum: (100D % change) + 1.5*(50D % change) + 2.0*(10D % change) for each stock then sort group in descending order and report the top 10.

Symbol Close Weekly % Change

50-Day % Change

TRMD 0.64 0.00% -8.57% ESEA 2.28 -2.56% -17.99% GNK 6.34 -1.86% -12.07% SBLK 0.9 -4.26% -3.23% DHT 0.96 -6.80% 26.32% BALT 4.16 4.52% -3.48% CMRE 13.77 -2.27% -6.33% VLCCF 14.38 0.28% 0.14% OSG 12.65 13.35% -4.53% EXM 2.00 4.71% 27.39%

*Momentum: (100D % change) + 1.5*(50D % change) + 2.0*(10D % change) for each stock - sort names that have a negative value in ascending order - report the top 10.

Monday, April 2, 2012 (Week 14)Capital Link Shipping Weekly Markets Report

Page 16

CAPITAL MARKETS DATA

Weekly Trading StatisticsTop Consecutive Higher Closes Top Consecutive Lower Closes

Symbol Close Up Streak NAT 15.88 6 SSW 17.34 4 FRO 7.7 4 NMM 16.67 3 ANW 6.93 3 DAC 3.94 3 EXM 2 2 DRYS 3.48 2 SB 6.68 2 VLCCF 14.38 2

Symbol Close Down Streak SFL 15.31 -2 SHIP 3.32 -2 STNG 7.08 -2 TEU 8.64 -4 TGP 39.08 -4

Top Largest Weekly Trading Gains Top Largest Weekly Trading Losses

Symbol Close One Week Ago

Friday Close

Net Change

% Change

TNK 5.24 6.07 0.83 15.84% OSG 11.16 12.65 1.49 13.35% TNP 7.78 8.7 0.92 11.83% DAC 3.56 3.94 0.38 10.67% FRO 7.14 7.7 0.56 7.84% EGLE 1.8 1.94 0.14 7.78% TOPS 2.17 2.33 0.16 7.37% NAT 14.79 15.88 1.09 7.37% TK 33.1 34.75 1.65 4.98% EXM 1.91 2 0.09 4.71%

Symbol Close One Week Ago

Friday Close

Net Change % Change

NEWL 1.77 1.4 -0.37 -20.90% DHT 1.03 0.96 -0.07 -6.80% SHIP 3.55 3.32 -0.23 -6.48% SBLK 0.94 0.9 -0.04 -4.26% NNA 3.4 3.26 -0.14 -4.12% GASS 6.14 5.9 -0.24 -3.91% TEU 8.9 8.64 -0.26 -2.92% FREE 1.08 1.05 -0.03 -2.78% ESEA 2.34 2.28 -0.06 -2.56% PRGN 0.84 0.82 -0.02 -2.38%

Top Largest Monthly Trading Gains (A month has been standardized to 20 trading days)

Top Largest Monthly Trading*Losses (A month has been standardized to 20 trading days)

Symbol Prior Close

Friday Close

Net Change % Change

NEWL 0.85 1.4 0.55 64.71% OSG 8.59 12.65 4.06 47.26% GSL 2.4 3.5 1.10 45.83% FRO 5.44 7.7 2.26 41.54% TNK 4.41 6.07 1.66 37.64% TNP 6.46 8.7 2.24 34.67% EGLE 1.5 1.94 0.44 29.33% TK 28.93 34.75 5.82 20.12% GASS 5.02 5.9 0.88 17.53% SFL 13.05 15.31 2.26 17.32%

Symbol Prior Close

Friday Close Net Change %

Change FREE 1.25 1.05 -0.20 -16.00% SSW 19.48 17.34 -2.14 -10.99% ESEA 2.55 2.28 -0.27 -10.59% GLNG 42.46 38.05 -4.41 -10.39% NNA 3.61 3.26 -0.35 -9.70% SB 7.32 6.68 -0.64 -8.74% DHT 1.05 0.96 -0.09 -8.57% GLBS 5.43 5.08 -0.35 -6.45% DAC 4.21 3.94 -0.27 -6.41% DCIX 6.45 6.04 -0.41 -6.36%

Stocks Nearest to 52-Week Highs Stocks Nearest To 52-Week Lows Symbol 52W High % Away TGP 40.44 -3.36% TOO 30.14 -3.98% TK 36.29 -4.24% GMLP 39.05 -4.94% ALEX 54.01 -10.26% SSW 20.24 -14.31% NMM 19.48 -14.45% TNP 10.22 -14.89% NNA 3.93 -16.98% GASS 7.20 -18.06%

Symbol 52W Low % Away SBLK 0.85 5.85% ESEA 2.11 7.92% VLCCF 13.04 10.24% BALT 3.46 20.26% TRMD 0.52 23.08% CMRE 10.51 31.07% SB 5.06 31.92% NNA 2.42 34.69% DSX 6.59 35.81% TOO 21.24 36.23%

Monday, April 2, 2012 (Week 14)Capital Link Shipping Weekly Markets Report

Page 17

CAPITAL MARKETS DATA

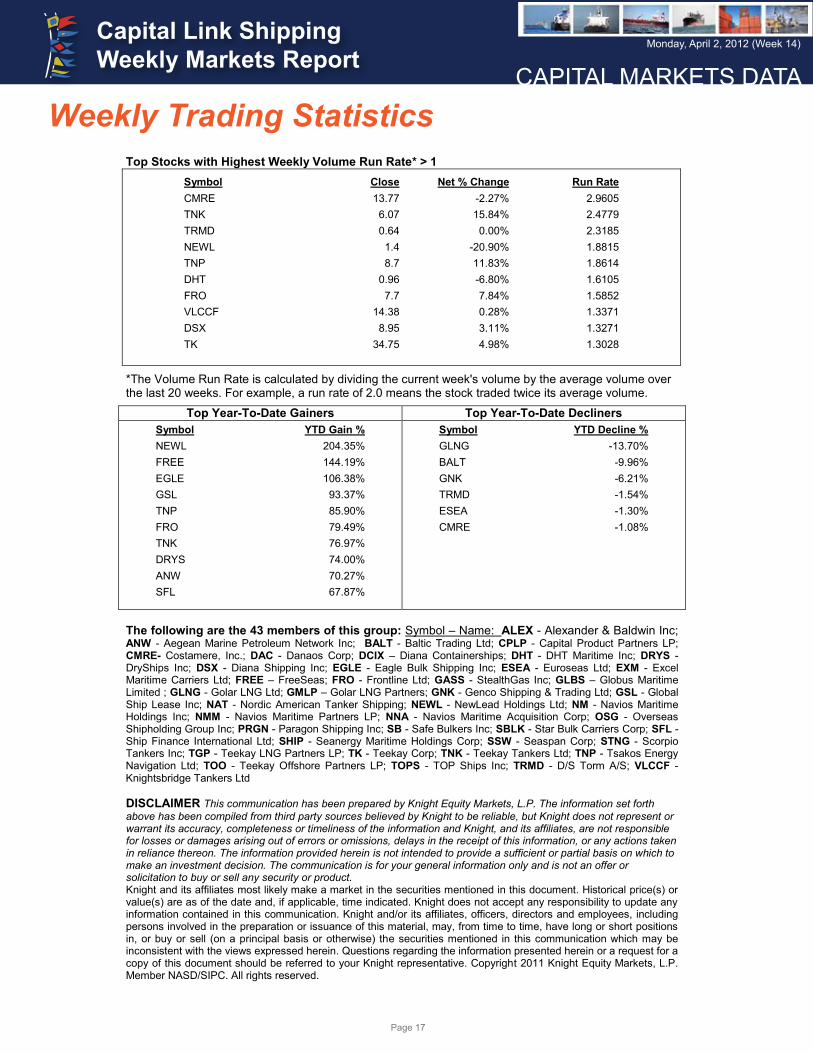

Weekly Trading StatisticsTop Stocks with Highest Weekly Volume Run Rate* > 1

Symbol Close Net % Change Run Rate CMRE 13.77 -2.27% 2.9605 TNK 6.07 15.84% 2.4779 TRMD 0.64 0.00% 2.3185 NEWL 1.4 -20.90% 1.8815 TNP 8.7 11.83% 1.8614 DHT 0.96 -6.80% 1.6105 FRO 7.7 7.84% 1.5852 VLCCF 14.38 0.28% 1.3371 DSX 8.95 3.11% 1.3271 TK 34.75 4.98% 1.3028

*The Volume Run Rate is calculated by dividing the current week's volume by the average volume over the last 20 weeks. For example, a run rate of 2.0 means the stock traded twice its average volume.

Top Year-To-Date Gainers Top Year-To-Date Decliners Symbol YTD Gain % NEWL 204.35% FREE 144.19% EGLE 106.38% GSL 93.37% TNP 85.90% FRO 79.49% TNK 76.97% DRYS 74.00% ANW 70.27% SFL 67.87%

Symbol YTD Decline % GLNG -13.70% BALT -9.96% GNK -6.21% TRMD -1.54% ESEA -1.30% CMRE -1.08%

The following are the 43 members of this group: Symbol – Name: ALEX - Alexander & Baldwin Inc; ANW - Aegean Marine Petroleum Network Inc; BALT - Baltic Trading Ltd; CPLP - Capital Product Partners LP; CMRE- Costamere, Inc.; DAC - Danaos Corp; DCIX – Diana Containerships; DHT - DHT Maritime Inc; DRYS - DryShips Inc; DSX - Diana Shipping Inc; EGLE - Eagle Bulk Shipping Inc; ESEA - Euroseas Ltd; EXM - Excel Maritime Carriers Ltd; FREE – FreeSeas; FRO - Frontline Ltd; GASS - StealthGas Inc; GLBS – Globus Maritime Limited ; GLNG - Golar LNG Ltd; GMLP – Golar LNG Partners; GNK - Genco Shipping & Trading Ltd; GSL - Global Ship Lease Inc; NAT - Nordic American Tanker Shipping; NEWL - NewLead Holdings Ltd; NM - Navios Maritime Holdings Inc; NMM - Navios Maritime Partners LP; NNA - Navios Maritime Acquisition Corp; OSG - Overseas Shipholding Group Inc; PRGN - Paragon Shipping Inc; SB - Safe Bulkers Inc; SBLK - Star Bulk Carriers Corp; SFL - Ship Finance International Ltd; SHIP - Seanergy Maritime Holdings Corp; SSW - Seaspan Corp; STNG - Scorpio Tankers Inc; TGP - Teekay LNG Partners LP; TK - Teekay Corp; TNK - Teekay Tankers Ltd; TNP - Tsakos Energy Navigation Ltd; TOO - Teekay Offshore Partners LP; TOPS - TOP Ships Inc; TRMD - D/S Torm A/S; VLCCF - Knightsbridge Tankers Ltd DISCLAIMER This communication has been prepared by Knight Equity Markets, L.P. The information set forth above has been compiled from third party sources believed by Knight to be reliable, but Knight does not represent or warrant its accuracy, completeness or timeliness of the information and Knight, and its affiliates, are not responsible for losses or damages arising out of errors or omissions, delays in the receipt of this information, or any actions taken in reliance thereon. The information provided herein is not intended to provide a sufficient or partial basis on which to make an investment decision. The communication is for your general information only and is not an offer or solicitation to buy or sell any security or product. Knight and its affiliates most likely make a market in the securities mentioned in this document. Historical price(s) or value(s) are as of the date and, if applicable, time indicated. Knight does not accept any responsibility to update any information contained in this communication. Knight and/or its affiliates, officers, directors and employees, including persons involved in the preparation or issuance of this material, may, from time to time, have long or short positions in, or buy or sell (on a principal basis or otherwise) the securities mentioned in this communication which may be inconsistent with the views expressed herein. Questions regarding the information presented herein or a request for a copy of this document should be referred to your Knight representative. Copyright 2011 Knight Equity Markets, L.P. Member NASD/SIPC. All rights reserved.

Monday, April 2, 2012 (Week 14)Capital Link Shipping Weekly Markets Report

Page 18

CAPITAL MARKETS DATA

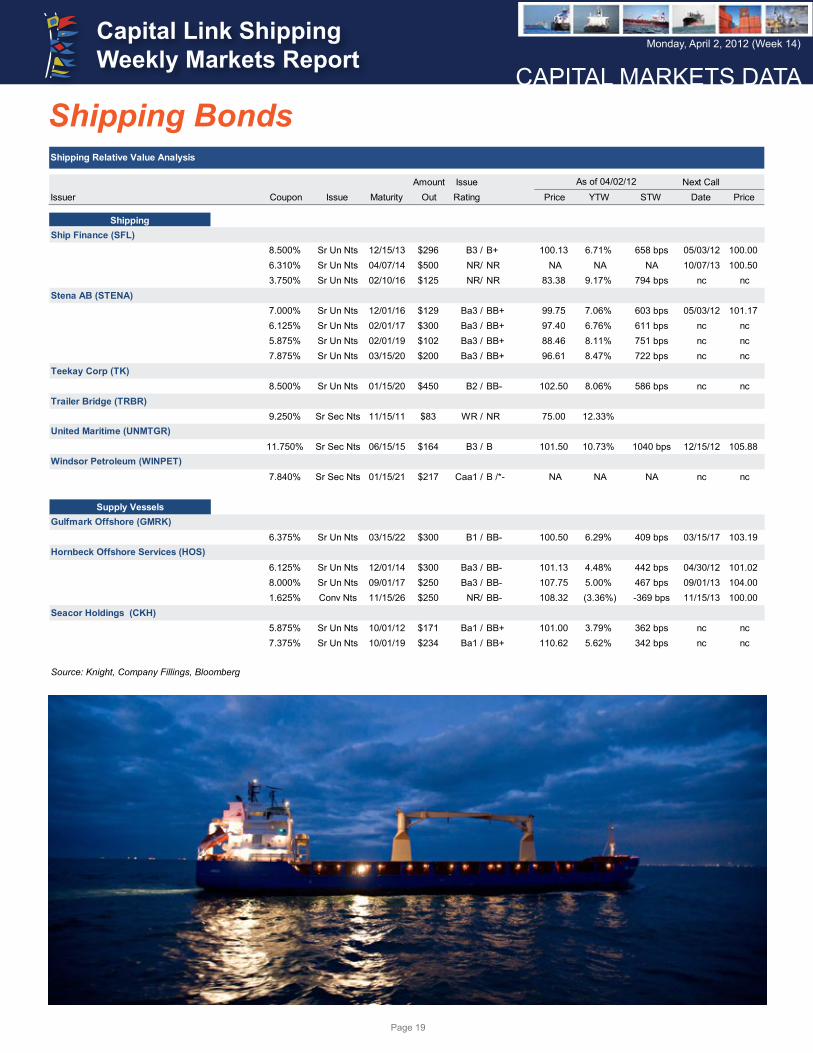

Shipping Bonds Contributed by

Shipping Relative Value Analysis

Amount Issue Next CallIssuer Coupon Issue Maturity Out Rating Price YTW STW Date Price

Shipping

12.500% Sr Sec Nts 07/15/17 $200 B2 / BB- 112.75 6.67% 634 bps 07/15/13 106.25

10.250% Sr Sec Nts 05/01/15 $258 B1 / B+ 105.00 7.59% 726 bps 05/03/12 105.13

7.500% Sr Un Nts 05/15/14 $400 NR/ CCC- 29.13 83.63% 8329 bps 05/15/12 103.7512.000% Sr Un Nts 02/10/15 $125 NR/ NR 25.07 268.32% 26799 bps nc nc

CMA CGM (CMACG)8.500% Sr Un Nts 04/15/17 $396 Caa2 / CCC /*- 62.50 20.90% 1987 bps 04/15/14 104.258.875% Sr Un Nts 04/15/19 $286 Caa2 / CCC /*- 62.13 18.80% 1915 bps 04/15/15 104.44

General Maritime (GMR)12.000% Sr Un Nts 11/15/17 $300 WR / CCC- 2.50 379.09% 37806 bps 11/15/13 106.00

8.040% Sr Sec Nts 02/01/19 $96 B2 / BB- /*- 86.50 10.89% 1114 bps nc nc

7.375% Sr Un Nts 02/01/19 $250 B3 / B 102.88 6.66% 563 bps 02/01/15 103.69DryShips (DRYS)

5.000% Conv Nts 12/01/14 $700 NR/ NR 84.20 12.13% 1180 bps nc ncExcel Maritime (EXM)

1.875% Conv Nts 10/15/27 $150 NR/ NR 47.46 34.77% 3443 bps 10/22/14 100.00Horizon Lines (HRZ)

11.000% Sr Sec Nts 10/15/16 $225 NR/ NR 101.50 9.43% 909 bps 10/15/12 101.506.000% Conv Nts 04/15/17 $179 NR/ NR 58.20 19.38% 1834 bps nc nc

10.875% Sr Sec Nts 01/15/17 $250 B3 / B- 105.50 9.11% 808 bps 01/15/13 108.16

8.625% Sr Sec Nts 11/01/17 $505 B2 / B 90.50 10.94% 991 bps 11/01/13 104.31Navios Maritime (NM)

8.875% Sr Sec Nts 11/01/17 $400 Ba3 / BB- 102.50 8.05% 756 bps 11/01/13 104.448.125% Sr Un Nts 02/15/19 $350 B3 / B+ 86.00 11.09% 889 bps 02/15/15 104.069.250% Sr Un Nts 04/15/19 $9 B3 / B+ 85.00 12.52% 1032 bps 04/15/14 106.94

8.750% Sr Un Nts 12/01/13 $64 Caa1 / B- 95.06 12.11% 1178 bps nc nc8.125% Sr Un Nts 03/30/18 $300 Caa1 / B- 64.00 18.26% 1722 bps nc nc7.500% Sr Un Nts 02/15/24 $146 Caa1 / B- 65.25 13.43% 1123 bps nc nc

Royal Caribbean (RCL)7.000% Sr Un Nts 06/15/13 $550 Ba1 / BB 104.50 3.13% 279 bps nc nc6.875% Sr Un Nts 12/01/13 $350 Ba1 / BB 106.50 2.83% 249 bps nc nc5.625% Sr Un Nts 01/27/14 $1,000 Ba1 / BB 101.25 4.88% 470 bps nc nc

11.875% Sr Un Nts 07/15/15 $300 Ba1 / BB 121.76 4.64% 414 bps nc nc7.250% Sr Un Nts 06/15/16 $350 Ba1 / BB 109.50 4.72% 369 bps nc nc7.250% Sr Un Nts 03/15/18 $150 Ba1 / BB 107.75 5.69% 466 bps nc nc7.500% Sr Un Nts 10/15/27 $300 Ba1 / BB 101.50 7.34% 401 bps nc nc

Ship Finance (SFL)8.500% Sr Un Nts 12/15/13 $296 B3 / B+ 100.13 6.71% 658 bps 05/03/12 100.006.310% Sr Un Nts 04/07/14 $500 NR/ NR NA NA NA 10/07/13 100.503.750% Sr Un Nts 02/10/16 $125 NR/ NR 83.38 9.17% 794 bps nc nc

Stena AB (STENA)7.000% Sr Un Nts 12/01/16 $129 Ba3 / BB+ 99.75 7.06% 603 bps 05/03/12 101.176.125% Sr Un Nts 02/01/17 $300 Ba3 / BB+ 97.40 6.76% 611 bps nc nc5.875% Sr Un Nts 02/01/19 $102 Ba3 / BB+ 88.46 8.11% 751 bps nc nc7.875% Sr Un Nts 03/15/20 $200 Ba3 / BB+ 96.61 8.47% 722 bps nc nc

Teekay Corp (TK)8.500% Sr Un Nts 01/15/20 $450 B2 / BB- 102.50 8.06% 586 bps nc nc

Trailer Bridge (TRBR)9.250% Sr Sec Nts 11/15/11 $83 WR / NR 75.00 12.33%

11.750% Sr Sec Nts 06/15/15 $164 B3 / B 101.50 10.73% 1040 bps 12/15/12 105.88

7.840% Sr Sec Nts 01/15/21 $217 Caa1 / B /*- NA NA NA nc nc

Supply Vessels

6.375% Sr Un Nts 03/15/22 $300 B1 / BB- 100.50 6.29% 409 bps 03/15/17 103.19

6.125% Sr Un Nts 12/01/14 $300 Ba3 / BB- 101.13 4.48% 442 bps 04/30/12 101.028.000% Sr Un Nts 09/01/17 $250 Ba3 / BB- 107.75 5.00% 467 bps 09/01/13 104.001.625% Conv Nts 11/15/26 $250 NR/ BB- 108.32 (3.36%) -369 bps 11/15/13 100.00

Seacor Holdings (CKH)5.875% Sr Un Nts 10/01/12 $171 Ba1 / BB+ 101.00 3.79% 362 bps nc nc7.375% Sr Un Nts 10/01/19 $234 Ba1 / BB+ 110.62 5.62% 342 bps nc nc

Source: Knight, Company Fillings, Bloomberg

Hornbeck Offshore Services (HOS)

Gulfmark Offshore (GMRK)

Windsor Petroleum (WINPET)

American Commercial (ACLI)

As of 04/02/12

Navios Maritime Acquisition (NNA)

Marquette Transportation (MARTRA)

Overseas Shipholding (OSG)

United Maritime (UNMTGR)

Great Lakes Dredge & Dock (GLDD)

Golden State Petro (GOLDEN)

Berlian Laju Tanker (BLTAIJ)

American Petroleum Tankers (AMPETR)

The current year to date high yield deal volume is $92.400 billion in 183 deals, compared to last year’s $88.942 billion in 207 deals. Of the 183 deals year to date, 136 of them were by U.S. Issuers and 170 of them were dollar denominated. The month to date high yield deal volume is $28.993 billion in 63 deals, compared to last year’s $31.009 billion in 72 deals for the same period. The default rate by number of issuers is 0.61% for March, versus 0.62% in February. The shadow default rate is 1.53%. On the high yield calendar there are $7.24 billion and €300 million deals being marketed. Data from EPFR Global reported an inflow to HY funds of $176 million for the week.

Horizon Lines, Inc has entered into restructuring agreements with holders. Under these agreements, the company’s remaining convertible senior secured notes will be converted into 90% of the company’s stock, or warrants for non-U.S. citizens.

Monday, April 2, 2012 (Week 14)Capital Link Shipping Weekly Markets Report

Page 19

CAPITAL MARKETS DATA

Shipping BondsShipping Relative Value Analysis

Amount Issue Next CallIssuer Coupon Issue Maturity Out Rating Price YTW STW Date Price

Shipping

12.500% Sr Sec Nts 07/15/17 $200 B2 / BB- 112.75 6.67% 634 bps 07/15/13 106.25

10.250% Sr Sec Nts 05/01/15 $258 B1 / B+ 105.00 7.59% 726 bps 05/03/12 105.13

7.500% Sr Un Nts 05/15/14 $400 NR/ CCC- 29.13 83.63% 8329 bps 05/15/12 103.7512.000% Sr Un Nts 02/10/15 $125 NR/ NR 25.07 268.32% 26799 bps nc nc

CMA CGM (CMACG)8.500% Sr Un Nts 04/15/17 $396 Caa2 / CCC /*- 62.50 20.90% 1987 bps 04/15/14 104.258.875% Sr Un Nts 04/15/19 $286 Caa2 / CCC /*- 62.13 18.80% 1915 bps 04/15/15 104.44

General Maritime (GMR)12.000% Sr Un Nts 11/15/17 $300 WR / CCC- 2.50 379.09% 37806 bps 11/15/13 106.00

8.040% Sr Sec Nts 02/01/19 $96 B2 / BB- /*- 86.50 10.89% 1114 bps nc nc

7.375% Sr Un Nts 02/01/19 $250 B3 / B 102.88 6.66% 563 bps 02/01/15 103.69DryShips (DRYS)

5.000% Conv Nts 12/01/14 $700 NR/ NR 84.20 12.13% 1180 bps nc ncExcel Maritime (EXM)

1.875% Conv Nts 10/15/27 $150 NR/ NR 47.46 34.77% 3443 bps 10/22/14 100.00Horizon Lines (HRZ)

11.000% Sr Sec Nts 10/15/16 $225 NR/ NR 101.50 9.43% 909 bps 10/15/12 101.506.000% Conv Nts 04/15/17 $179 NR/ NR 58.20 19.38% 1834 bps nc nc

10.875% Sr Sec Nts 01/15/17 $250 B3 / B- 105.50 9.11% 808 bps 01/15/13 108.16

8.625% Sr Sec Nts 11/01/17 $505 B2 / B 90.50 10.94% 991 bps 11/01/13 104.31Navios Maritime (NM)

8.875% Sr Sec Nts 11/01/17 $400 Ba3 / BB- 102.50 8.05% 756 bps 11/01/13 104.448.125% Sr Un Nts 02/15/19 $350 B3 / B+ 86.00 11.09% 889 bps 02/15/15 104.069.250% Sr Un Nts 04/15/19 $9 B3 / B+ 85.00 12.52% 1032 bps 04/15/14 106.94

8.750% Sr Un Nts 12/01/13 $64 Caa1 / B- 95.06 12.11% 1178 bps nc nc8.125% Sr Un Nts 03/30/18 $300 Caa1 / B- 64.00 18.26% 1722 bps nc nc7.500% Sr Un Nts 02/15/24 $146 Caa1 / B- 65.25 13.43% 1123 bps nc nc

Royal Caribbean (RCL)7.000% Sr Un Nts 06/15/13 $550 Ba1 / BB 104.50 3.13% 279 bps nc nc6.875% Sr Un Nts 12/01/13 $350 Ba1 / BB 106.50 2.83% 249 bps nc nc5.625% Sr Un Nts 01/27/14 $1,000 Ba1 / BB 101.25 4.88% 470 bps nc nc

11.875% Sr Un Nts 07/15/15 $300 Ba1 / BB 121.76 4.64% 414 bps nc nc7.250% Sr Un Nts 06/15/16 $350 Ba1 / BB 109.50 4.72% 369 bps nc nc7.250% Sr Un Nts 03/15/18 $150 Ba1 / BB 107.75 5.69% 466 bps nc nc7.500% Sr Un Nts 10/15/27 $300 Ba1 / BB 101.50 7.34% 401 bps nc nc

Ship Finance (SFL)8.500% Sr Un Nts 12/15/13 $296 B3 / B+ 100.13 6.71% 658 bps 05/03/12 100.006.310% Sr Un Nts 04/07/14 $500 NR/ NR NA NA NA 10/07/13 100.503.750% Sr Un Nts 02/10/16 $125 NR/ NR 83.38 9.17% 794 bps nc nc

Stena AB (STENA)7.000% Sr Un Nts 12/01/16 $129 Ba3 / BB+ 99.75 7.06% 603 bps 05/03/12 101.176.125% Sr Un Nts 02/01/17 $300 Ba3 / BB+ 97.40 6.76% 611 bps nc nc5.875% Sr Un Nts 02/01/19 $102 Ba3 / BB+ 88.46 8.11% 751 bps nc nc7.875% Sr Un Nts 03/15/20 $200 Ba3 / BB+ 96.61 8.47% 722 bps nc nc

Teekay Corp (TK)8.500% Sr Un Nts 01/15/20 $450 B2 / BB- 102.50 8.06% 586 bps nc nc

Trailer Bridge (TRBR)9.250% Sr Sec Nts 11/15/11 $83 WR / NR 75.00 12.33%

11.750% Sr Sec Nts 06/15/15 $164 B3 / B 101.50 10.73% 1040 bps 12/15/12 105.88

7.840% Sr Sec Nts 01/15/21 $217 Caa1 / B /*- NA NA NA nc nc

Supply Vessels

6.375% Sr Un Nts 03/15/22 $300 B1 / BB- 100.50 6.29% 409 bps 03/15/17 103.19

6.125% Sr Un Nts 12/01/14 $300 Ba3 / BB- 101.13 4.48% 442 bps 04/30/12 101.028.000% Sr Un Nts 09/01/17 $250 Ba3 / BB- 107.75 5.00% 467 bps 09/01/13 104.001.625% Conv Nts 11/15/26 $250 NR/ BB- 108.32 (3.36%) -369 bps 11/15/13 100.00

Seacor Holdings (CKH)5.875% Sr Un Nts 10/01/12 $171 Ba1 / BB+ 101.00 3.79% 362 bps nc nc7.375% Sr Un Nts 10/01/19 $234 Ba1 / BB+ 110.62 5.62% 342 bps nc nc

Source: Knight, Company Fillings, Bloomberg

Hornbeck Offshore Services (HOS)

Gulfmark Offshore (GMRK)

Windsor Petroleum (WINPET)

American Commercial (ACLI)

As of 04/02/12

Navios Maritime Acquisition (NNA)

Marquette Transportation (MARTRA)

Overseas Shipholding (OSG)

United Maritime (UNMTGR)

Great Lakes Dredge & Dock (GLDD)

Golden State Petro (GOLDEN)

Berlian Laju Tanker (BLTAIJ)

American Petroleum Tankers (AMPETR)

Shipping Relative Value Analysis

Amount Issue Next CallIssuer Coupon Issue Maturity Out Rating Price YTW STW Date Price

Shipping

12.500% Sr Sec Nts 07/15/17 $200 B2 / BB- 112.75 6.67% 634 bps 07/15/13 106.25

10.250% Sr Sec Nts 05/01/15 $258 B1 / B+ 105.00 7.59% 726 bps 05/03/12 105.13

7.500% Sr Un Nts 05/15/14 $400 NR/ CCC- 29.13 83.63% 8329 bps 05/15/12 103.7512.000% Sr Un Nts 02/10/15 $125 NR/ NR 25.07 268.32% 26799 bps nc nc

CMA CGM (CMACG)8.500% Sr Un Nts 04/15/17 $396 Caa2 / CCC /*- 62.50 20.90% 1987 bps 04/15/14 104.258.875% Sr Un Nts 04/15/19 $286 Caa2 / CCC /*- 62.13 18.80% 1915 bps 04/15/15 104.44

General Maritime (GMR)12.000% Sr Un Nts 11/15/17 $300 WR / CCC- 2.50 379.09% 37806 bps 11/15/13 106.00

8.040% Sr Sec Nts 02/01/19 $96 B2 / BB- /*- 86.50 10.89% 1114 bps nc nc

7.375% Sr Un Nts 02/01/19 $250 B3 / B 102.88 6.66% 563 bps 02/01/15 103.69DryShips (DRYS)

5.000% Conv Nts 12/01/14 $700 NR/ NR 84.20 12.13% 1180 bps nc ncExcel Maritime (EXM)

1.875% Conv Nts 10/15/27 $150 NR/ NR 47.46 34.77% 3443 bps 10/22/14 100.00Horizon Lines (HRZ)

11.000% Sr Sec Nts 10/15/16 $225 NR/ NR 101.50 9.43% 909 bps 10/15/12 101.506.000% Conv Nts 04/15/17 $179 NR/ NR 58.20 19.38% 1834 bps nc nc

10.875% Sr Sec Nts 01/15/17 $250 B3 / B- 105.50 9.11% 808 bps 01/15/13 108.16

8.625% Sr Sec Nts 11/01/17 $505 B2 / B 90.50 10.94% 991 bps 11/01/13 104.31Navios Maritime (NM)

8.875% Sr Sec Nts 11/01/17 $400 Ba3 / BB- 102.50 8.05% 756 bps 11/01/13 104.448.125% Sr Un Nts 02/15/19 $350 B3 / B+ 86.00 11.09% 889 bps 02/15/15 104.069.250% Sr Un Nts 04/15/19 $9 B3 / B+ 85.00 12.52% 1032 bps 04/15/14 106.94

8.750% Sr Un Nts 12/01/13 $64 Caa1 / B- 95.06 12.11% 1178 bps nc nc8.125% Sr Un Nts 03/30/18 $300 Caa1 / B- 64.00 18.26% 1722 bps nc nc7.500% Sr Un Nts 02/15/24 $146 Caa1 / B- 65.25 13.43% 1123 bps nc nc

Royal Caribbean (RCL)7.000% Sr Un Nts 06/15/13 $550 Ba1 / BB 104.50 3.13% 279 bps nc nc6.875% Sr Un Nts 12/01/13 $350 Ba1 / BB 106.50 2.83% 249 bps nc nc5.625% Sr Un Nts 01/27/14 $1,000 Ba1 / BB 101.25 4.88% 470 bps nc nc

11.875% Sr Un Nts 07/15/15 $300 Ba1 / BB 121.76 4.64% 414 bps nc nc7.250% Sr Un Nts 06/15/16 $350 Ba1 / BB 109.50 4.72% 369 bps nc nc7.250% Sr Un Nts 03/15/18 $150 Ba1 / BB 107.75 5.69% 466 bps nc nc7.500% Sr Un Nts 10/15/27 $300 Ba1 / BB 101.50 7.34% 401 bps nc nc

Ship Finance (SFL)8.500% Sr Un Nts 12/15/13 $296 B3 / B+ 100.13 6.71% 658 bps 05/03/12 100.006.310% Sr Un Nts 04/07/14 $500 NR/ NR NA NA NA 10/07/13 100.503.750% Sr Un Nts 02/10/16 $125 NR/ NR 83.38 9.17% 794 bps nc nc

Stena AB (STENA)7.000% Sr Un Nts 12/01/16 $129 Ba3 / BB+ 99.75 7.06% 603 bps 05/03/12 101.176.125% Sr Un Nts 02/01/17 $300 Ba3 / BB+ 97.40 6.76% 611 bps nc nc5.875% Sr Un Nts 02/01/19 $102 Ba3 / BB+ 88.46 8.11% 751 bps nc nc7.875% Sr Un Nts 03/15/20 $200 Ba3 / BB+ 96.61 8.47% 722 bps nc nc

Teekay Corp (TK)8.500% Sr Un Nts 01/15/20 $450 B2 / BB- 102.50 8.06% 586 bps nc nc

Trailer Bridge (TRBR)9.250% Sr Sec Nts 11/15/11 $83 WR / NR 75.00 12.33%

11.750% Sr Sec Nts 06/15/15 $164 B3 / B 101.50 10.73% 1040 bps 12/15/12 105.88

7.840% Sr Sec Nts 01/15/21 $217 Caa1 / B /*- NA NA NA nc nc

Supply Vessels

6.375% Sr Un Nts 03/15/22 $300 B1 / BB- 100.50 6.29% 409 bps 03/15/17 103.19

6.125% Sr Un Nts 12/01/14 $300 Ba3 / BB- 101.13 4.48% 442 bps 04/30/12 101.028.000% Sr Un Nts 09/01/17 $250 Ba3 / BB- 107.75 5.00% 467 bps 09/01/13 104.001.625% Conv Nts 11/15/26 $250 NR/ BB- 108.32 (3.36%) -369 bps 11/15/13 100.00

Seacor Holdings (CKH)5.875% Sr Un Nts 10/01/12 $171 Ba1 / BB+ 101.00 3.79% 362 bps nc nc7.375% Sr Un Nts 10/01/19 $234 Ba1 / BB+ 110.62 5.62% 342 bps nc nc

Source: Knight, Company Fillings, Bloomberg

Hornbeck Offshore Services (HOS)

Gulfmark Offshore (GMRK)

Windsor Petroleum (WINPET)

American Commercial (ACLI)

As of 04/02/12

Navios Maritime Acquisition (NNA)

Marquette Transportation (MARTRA)

Overseas Shipholding (OSG)

United Maritime (UNMTGR)

Great Lakes Dredge & Dock (GLDD)

Golden State Petro (GOLDEN)

Berlian Laju Tanker (BLTAIJ)

American Petroleum Tankers (AMPETR)

© September 2010 Knight Capital Group, Inc. All rights reserved.Knight Equity Markets, L.P. and Knight Capital Markets LLC are o�-exchange liquidity providers and members of FINRA and SIPC. To learn about Knight Capital Group, Inc. (NYSE Euronext: KCG) go to knight.com.

Knight Corporate Access is an unbiased service for issuers to

connect with institutional investors. Through a combination of

strategic investor introductions, thought leadership initiatives

and market insight, Knight can help strengthen and diversify a

company’s investor base.

Knight is the leading source of o�-exchange liquidity in U.S.

equities and has a greater share volume than any U.S. exchange.

For additional information,please contact:

Sandy Reddin

phone 212-455-9255email [email protected]

Monday, April 2, 2012 (Week 14)Capital Link Shipping Weekly Markets Report

Page 21

SHIPPING MARKETS

Dry Bulk Market - Weekly HighlightsContributed by

IntermodalIntermodal Shipbrokers Co.17th km Ethniki Odos Athens-Lamia & 3 Agrambelis Street,145 64 N. Kifisia,Athens - Greece

Phone: +30 210 6293300Website: www.intermodal.gr

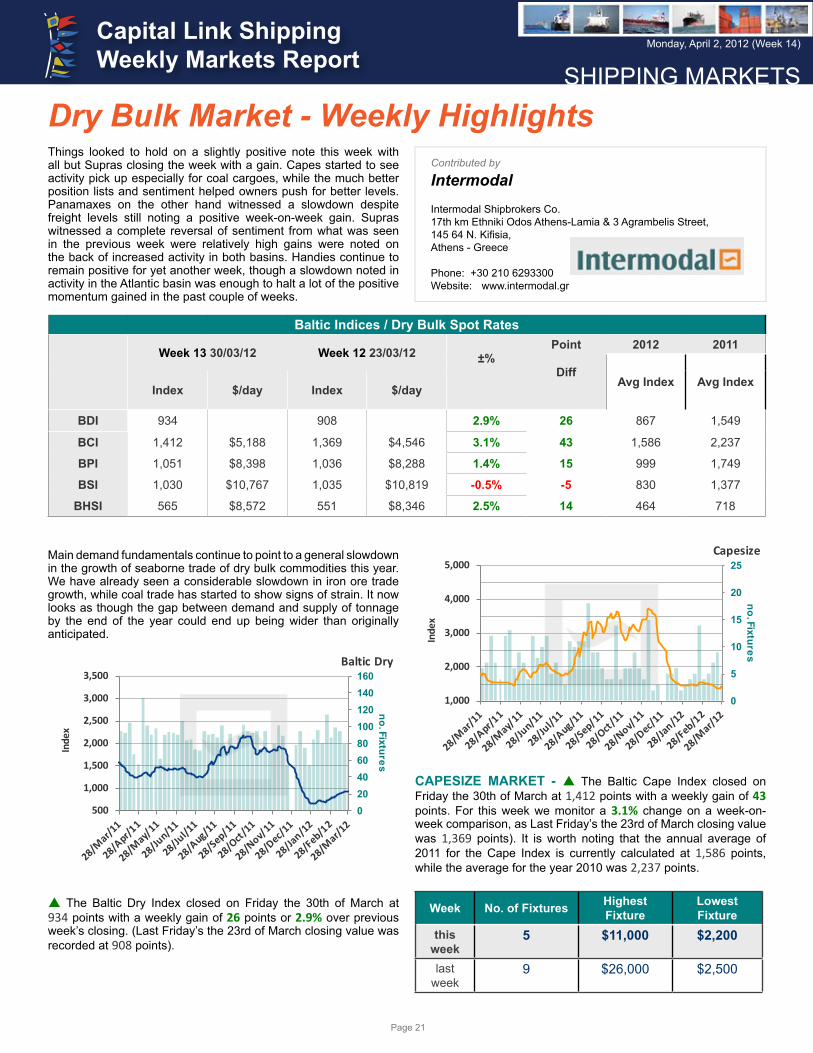

Things looked to hold on a slightly positive note this week with all but Supras closing the week with a gain. Capes started to see activity pick up especially for coal cargoes, while the much better position lists and sentiment helped owners push for better levels. Panamaxes on the other hand witnessed a slowdown despite freight levels still noting a positive week-on-week gain. Supras witnessed a complete reversal of sentiment from what was seen in the previous week were relatively high gains were noted on the back of increased activity in both basins. Handies continue to remain positive for yet another week, though a slowdown noted in activity in the Atlantic basin was enough to halt a lot of the positive momentum gained in the past couple of weeks.

Baltic Indices / Dry Bulk Spot Rates

Week 13 30/03/12 Week 12 23/03/12 ±%

Point

Diff

2012 2011

Avg Index Avg IndexIndex $/day Index $/day

BDI 934 908 2.9% 26 867 1,549

BCI 1,412 $5,188 1,369 $4,546 3.1% 43 1,586 2,237

BPI 1,051 $8,398 1,036 $8,288 1.4% 15 999 1,749

BSI 1,030 $10,767 1,035 $10,819 -0.5% -5 830 1,377

BHSI 565 $8,572 551 $8,346 2.5% 14 464 718

Main demand fundamentals continue to point to a general slowdown in the growth of seaborne trade of dry bulk commodities this year. We have already seen a considerable slowdown in iron ore trade growth, while coal trade has started to show signs of strain. It now looks as though the gap between demand and supply of tonnage by the end of the year could end up being wider than originally anticipated.

020406080100120140160

500

1,000

1,500

2,000

2,500

3,000

3,500

no. Fixtures

Inde

x

Baltic Dry

p The Baltic Dry Index closed on Friday the 30th of March at 934 points with a weekly gain of 26 points or 2.9% over previous week’s closing. (Last Friday’s the 23rd of March closing value was recorded at 908 points).

0

5

10

15

20

25

1,000

2,000

3,000

4,000

5,000

no. Fixtures

Inde

x

Capesize

CAPESIZE MARKET - p The Baltic Cape Index closed on Friday the 30th of March at 1,412 points with a weekly gain of 43 points. For this week we monitor a 3.1% change on a week-on-week comparison, as Last Friday’s the 23rd of March closing value was 1,369 points). It is worth noting that the annual average of 2011 for the Cape Index is currently calculated at 1,586 points, while the average for the year 2010 was 2,237 points.

Week No. of Fixtures Highest Fixture

Lowest Fixture

this week

5 $11,000 $2,200

last week

9 $26,000 $2,500

Monday, April 2, 2012 (Week 14)Capital Link Shipping Weekly Markets Report

Page 22

SHIPPING MARKETS

Dry Bulk Market - Weekly HighlightsWeek Period Charter Trip Charter

this week $11,000 $5,150last week $0 $11,278

For Week 13 we have recorded a total of 5 timecharter fixtures in the Capesize sector, 1 for period charter averaging $11,000 per day, while 4 trip charters were reported this week with a daily average of $5,150 per day.

This week’s fixture that received the lowest daily hire was the M/V ‘’E.R. BORNEO’’, 178000 dwt, built 2010, dely Amsterdam spot , redely Skaw-Cape Passero, $2200, Swiss Marine, for a transatlantic round -300$ reduced from last week, and the fixture with the highest daily hire was the M/V ‘’SUCCESSOR’’, 174000 dwt, built 2007, dely China 10/20 Apr , redely worldwide, $11000, Classic Maritime, for a 8/12 months trading -15000$ reduced from last week.

The BCI is showing a 3.1% rise on a weekly comparison, a -7.8% decrease on a 1 month basis, a -58.5% decrease on a 3 month basis, a -57.7% decrease on a 6 month basis and a -21.2% decrease on a 12 month basis.

0102030405060708090100

500

1,500

2,500

3,500

no. Fixtures

Inde

x

Panamax

PANAMAX MARKET - p The Baltic Panamax Index closed on Friday the 30th of March with a gain at 1,051 points having gained 15 points on a weekly comparison. It is worth noting that last Friday’s the 23rd of March saw the Panamax index close at 1,036 points. The week-on-week change for the Panamax index is calculated to be 1.4%, while the yearly average for the Baltic Panamax Index for this running year is calculated at 999 points while the average for 2010 was 1,749 points.

Week No. of Fixtures Highest Fixture

Lowest Fixture

this week

44 $17,500 $6,000

last week

36 $20,500 $6,500

Week Period Charter Trip Charterthis week $10,050 $10,471last week $9,880 $11,792

For Week 13 we have recorded a total of 44 timecharter fixtures in the Panamax sector, 3 for period charter averaging $10,050 per day, while 41 trip charters were reported this week with a daily average of $10,471 per day.

The daily earnings differential for the Panamaxes, that we calculate from all this week’s reported fixtures, i.e. the difference between the lowest and highest reported fixture for this week was reduced, and this week’s fixture that received the lowest daily hire was the M/V ‘’THEMIS P’’, 70165 dwt, built 1994, dely Chiwan 30/31Mar, redely India, $6000, PCL, for a trip via Indonesia -500$ reduced from last week, and the fixture with the highest daily hire was the M/V ‘’TORM PACIFIC’’, 77171 dwt, built 2009, dely Jorf Lasfar 31 Mar/4 Apr , redely Singapore-Japan, $17500, Cargill, for a trip via EC South America -3000$ reduced from last week.

The BPI is showing a 1.4% rise on a weekly comparison, a 26.3% rise on a 1 month basis, a -37.3% decrease on a 3 month basis, a -36.0% decrease on a 6 month basis and a -45.4% decrease on a 12 month basis.

05101520253035404550

500

1,000

1,500

2,000

2,500

no Fixtures

Inde

x

Supramax

SUPRAMAX & HANDYMAX MARKET - q The Baltic Supramax Index closed on Friday the 30th of March at 1,030 points down with a weekly loss of -5 points or -0.5% . The Baltic Supramax index on a weekly comparison is with a downward trend as last Friday’s the 23rd of March closing value was 1,035 points. The annual average of the BSI is recorded at 830 points while the average for 2010 was 1,377 points.

Week No. of Fixtures Highest Fixture

Lowest Fixture

this week

26 $19,000 $11,000

last week

28 $22,750 $5,500

Monday, April 2, 2012 (Week 14)Capital Link Shipping Weekly Markets Report

Page 23

SHIPPING MARKETS

Dry Bulk Market - Weekly HighlightsWeek Period Charter Trip Charter

this week $11,750 $13,874last week $12,288 $15,100

For Week 13 we have recorded a total of 26 timecharter fixtures in the Supramax & Handymax sector, 3 for period charter averaging $11,750 per day, while 23 trip charters were reported this week with a daily average of $13,874 per day.

The minimum vs maximum daily rate differential as analyzed from our fixtures database was overall reduced and from the reported fixtures we see that this week’s fixture that received the lowest daily hire was the M/V ‘’AMAMI K’’, 58613 dwt, built 2012, dely Karachi 6/10 April , redely China intention iron ore, $11000, KEC, for a trip 5500$ improved from last week, and the fixture with the highest daily hire was the M/V ‘’TOXOTIS’’, 56713 dwt, built 2010, dely dop Surabaya spot , redely India approx, $19000, Ultrabulk, for a trip via Indonesia -3750$ reduced from last week.

The BSI is showing a -0.5% decrease on a weekly comparison, a 44.7% rise on a 1 month basis, a -12.9% decrease on a 3 month basis, a -30.4% decrease on a 6 month basis and a -31.8% decrease on a 12 month basis.

024681012141618

250

500

750

1,000

no. Fixtures

Inde

x

Handysize

HANDYSIZE MARKET - p The Baltic Handysize Index closed on Friday the 30th of March with an upward trend at 565 points with a weekly gain of 14 points and a percentage change of 2.5%. It is noted that last Friday’s the 23rd of March closing value was 551 points and the average for 2011 is calculated at 464 points while the average for 2010 was 718 points.

Week No. of Fixtures Highest Fixture

Lowest Fixture

this week

6 $20,100 $9,000

last week

6 $12,700 $5,500

Week Period Charter Trip Charterthis week $0 $12,392last week $9,800 $10,220

For Week 13 we have recorded a total of 6 timecharter fixtures in the Handysize sector, 0 for period charter averaging $0 per day, while 8 trip charters were reported this week with a daily average of $12,392 per day.

The minimum vs maximum daily rate differential as analyzed from our fixtures database was overall improved and this week’s fixture that received the lowest daily hire was the M/V ‘’LAST TYCOON’’, 34500 dwt, built 2011, dely CJK 30 Mar/5 Apr, redely SEAsia, $9000, Asan Merchant Marine, for a trip via SKorea -800$ reduced from last week and the fixture with the highest daily hire was the M/V ‘’MARINA R’’, 37785 dwt, built 2010, dely Recalada 3/6 Apr , redely WC South America, $20100, Clipper, for a trip 7400$ improved from last week.

The BHI is showing a 2.5% change on a weekly comparison, a 36.1% rise on a 1 month basis, a -2.2% decrease on a 3 month basis, a -17.8% decrease on a 6 month basis and a -28.1% decrease on a 12 month basis.

All Baltic Dry Indices, 1 day, 1week , 1 month, 3 months, 6 months and 12 months % changes based on last Friday’s closing figures.

INDEX 1 DAY 1 WEEK 1 MONTH 3 MONTHS 6 MONTHS 1 YEAR

BDI 0.4% 2.9% 24.5% -47.7% -51.4% -38.6%

BCI 1.9% 3.1% -7.8% -58.5% -57.7% -21.2%

BPI 0.7% 1.4% 26.3% -37.3% -36.0% -45.4%

BSI -1.2% -0.5% 44.7% -12.9% -30.4% -31.8%

BHI -0.2% 2.5% 36.1% -2.2% -17.8% -28.1%

Monday, April 2, 2012 (Week 14)Capital Link Shipping Weekly Markets Report

Page 24

SHIPPING MARKETS

The Week In ReviewContributed by

Golden Destiny S.A. Golden Destiny S.A.57 Akti Miaouli, Piraeus, 18536,Greece

Phone: +30 210 4295000Website: www.goldendestiny.gr

Week Ending: 30th March 2012(Given in good faith but without guarantee)

This Week’s News: A snapshot on the economic and shipping environment

ECONOMIC ENVIRONMENT

The rising fuel price, one of the major threats of the worldwide economy, pushed US, UK and France, some of the world’s biggest oil buyers, to consider a release of strategic oil stocks in a bid to calm oil market. France’s energy minister, Eric Besson, confirmed that his country is in talks with US, UK and Japan to release billion of barrels of oil in the market. He also said that the countries are waiting conclusions from the International Energy Agency, which coordinates emergency stock releases in case of severe oil supply.

Saudi Oil Minister Ali al-Naimi blasted “irrationally” high oil prices by stating in the Financial Times that Saudi Arabia would like to see a lower price and Riyadh would do all it could do to bring prices down. He also said that supply is not the problem and there is no rational reason why oil prices remain at these high levels. Oil is trading near $124/barrel in part due to concerns about Iran’s exports amid tightening sanctions. The influential Saudi oil minister identified $100 per barrel as an ideal price for producers and consumers earlier this year. The bottom line is that Saudi Arabia would like to see a lower fair and reasonable price that does not hurt the global economic recovery.

The International Energy Agency said that if crude prices do not fall, oil consumer nations will pay a record $2 trillion this year. The IEA’s chief economist Fatih Birol, said in Reuters, that US crude oil imports would cost 3.4% of GDP, up from 3.1% in 2011 at a record of $426 billion this year, up from $380 in 2011. Furthermore, European Union, at the current price levels, would have to pay $500 billion in 2012, up from $470 billion last year; while China’s imported oil bill would reach $250 billion this year, up by $50 billion from 2011. “If China’s economy slows down as a result of high oil prices then it will have an impact not only on China but also the rest of the world” said Birol, noting that the world’s second biggest oil consumer had helped to pull the world out of the 2008 recession.

In the eurozone, market confidence is still fragile, even policy making decisions to avoid the contagion of the sovereign debt crisis. The organization for Economic Cooperation and Development said that the eurozone’s public debt crisis is not over despite calmer financial markets with a warning that the bloc’s banks remain weak, debt levels are still rising and fiscal targets are far from assured. The ECB has provided eurozone banks with more than €1tn loans, in a period of three years, as a means to strengthen the euro zone’s financial system. However, ECB figures showed that the flow of bank credit to the real economy contracted in February, although at a slower rate than at the end of last year. Loans to the private sector fell by €11bn compared with the previous month, while the annual growth rate fell from 1.1 per cent in January to 0.7 per cent, the lowest since June 2010, when the eurozone was recovering from the recession that followed the collapse of Lehman Brothers investment bank.

The Paris-based Organization for Economic Cooperation and Development points a robust growth in the United States and Canada for the first half of 2012, but much weaker activity in Europe, where the outlook remains fragile. In an interim forecast, the OECD projected U.S. gross domestic product to grow at an annualized rate of 2.9% in the current quarter and 2.8% in the second. The euro-zone’s three largest economies, Germany, France and Italy, are set to shrink by 0.4% on average in the first quarter, followed by growth of 0.9% in the second. Japan is predicted to expand by an annualized 3.4% in the first quarter and 1.4% in the second.

In the U.S. economy, the rapid rise in gross domestic income at an annualized rate of 4.4% in the fourth quarter of 2011, with lower estimates for the growth in gross domestic product at 3%, suggests that the world’s largest economy may be healthier than previously thought. The strength of the gross domestic income may be explained by a gap between the recent strength of the labor market and a rise in consumer spending of 2.1%. As per data from U.S. Labor Department, U.S. jobless claims fell by 5,000 last week to a total of 359,000, as per data from. However, Chairman Ben Bernanke said that the U.S. job market remains weak despite three months of strong hiring. The number of people working and the total hours worked are still significantly below pre-crisis peaks. Recent job gains have lifted hopes for the economy and consumer spending. Employers added an average of 245,000 jobs per month from December through February with unemployment rate falling to 8.3%, roughly a percentage point down since summer.

In China, GDP growth for the full year is likely to reach 8.5 percent, above the government’s target of 7.5 percent, despite a “combination of shrinking short-term demand and falling long-term potential productivity”, said Yu Bin, director-general of the Department of Macroeconomic Research Center of the State Council. Major threat on the Chinese economy is the slack of export growth with China exports showing a decline of 0.5% over the year in January, the first fall in more than two years. The export figures in the past two months were far less than the previous year and they set a pessimistic tone for the whole year, Mr Zhong Shan, China’s Deputy Commerce Minister, said. China posted its largest trade deficit in almost ten years in February. Furthermore, Chinese manufacturing activity declined in March, falling to 48.1 points from 49.6 points in February, according to the HSBC Purchasing Manager’s Index (PMI). This suggests that China’s manufacturing sector is in recession, mainly due to weaker demand for Chinese goods in the eurozone.

SHIPPING MARKET

Overall confidence levels in the shipping industry increased slightly

Monday, April 2, 2012 (Week 14)Capital Link Shipping Weekly Markets Report

Page 25

SHIPPING MARKETS

The Week In Reviewin the three months ended February 2012, to reach their highest level since May 2011, according to the latest Shipping Confidence Survey from international accountant and shipping adviser Moore Stephens. This is the third successive quarter in which there has been a small uptick in confidence. Rates are expected to increase over the coming year in the three main tonnage sectors covered by the survey. But the number of respondents expecting to make a major new investment over the next twelve months fell to its lowest figure for three years. In February 2012, the average confidence level expressed by respondents in the markets in which they operate was 5.5 on a scale of 1 (low) to 10 (high). This is marginally up on the figure of 5.4 recorded in the previous survey in November 2011. In February 2011, the average confidence level was at 5.8 and 5.9 in February 2010. The survey was launched in May 2008 with a confidence rating of 6.8.

In the dry market, the capesize pressure remains with panamax and supramax vessels experiencing better returns and the BDI standing one step behind of breaking the 1,000 points mark. Strong South American grain demand and an increase in coal exports from U.S. and Europe provide a firm support in the panamax market with earnings almost 40% more than capesize vessels.

In the iron ore market, comforting sign is the fall of Chinese iron ore inventories for a second consecutive week to 98,4 million tons, 1mt (1%) less than a weak ago. Brazil’s Vale is optimistic about the outlook of iron ore in China, like its Australian rivals BHP and Rio Tinto, believing in a moderate growth that is still significant for iron ore demand given the large steel production capacity of China. Vale forecasts that steel output in China will grow 5% this year after expanding more than 10% a year ago. One more positive sign is that Chinese February iron ore imports improved, after a weak January, totalled 65.0mt, up 10% m-o-m and 33% y-o-y. In addition, China’s daily crude steel output rose 1.1% in the second ten days of March from previous period. According to the China Iron & Steel Association, daily crude steel output stood at 1,919 million tons during March 11-20, up from 1,898 million tons in the previous ten years. Hu Zhengwu, an analyst with industry consultancy Custeel.com expects China’s daily crude steel output to reach 1.95 million tons in March, compared with a daily steel production of 1.917 million tons a year earlier.

In the coal market, heavy rains in Eastern Australia led to a temporary operating suspension at several coal mines resulting in slower Australian coal fixture volumes that may have an impact on the vessel earnings of smaller vessel sizes, panamax and supramax.

The index closed today at 934 points, down by 2.4% from last week’s closing and down by 39% from a similar week closing in 2011 when it was 1,520 points. The highest rate increase has been in the capesize segment, BCI up 3.1% w-o-w, BPI up 1.4% w-o-w, BSI down 0.4% w-o-w, BHSI up 2.5% w-o-w.

Capesize average time charter earnings are up by 14% w-o-w, panamax up 1.3% w-o-w, supramax down by 0.4% w-o-w and handysize down by 2.7%. Capesizes are currently earning $5,188/day, $3,384/day less than handysizes, showing an increase of $642/day from a week ago, while panamaxes are earning $8,398/day, an increase of $110/day. At similar week in 2011, capesizes were

earning $10,554/day, while panamaxes were earning $15,463/day. Supramaxes are trading at $10,767/day, down by $52/day from last week’s closing, 108% higher than capesize and 28% than panamax earnings. At similar week in 2011, supramaxes were getting $15,795/day, up by 46% from the current levels and 50% higher levels than capesizes. Handysize vessels are trading at $ 8,572day; a decline by $226/day from last week, when at similar week in 2011 handysize units were earning $11,774/day.

In the wet market, the freight market remains volatile with crude spot rates being under pressure from decline of fixture activity of Middle East, West Africa and Mediterranean. However, Dahlman Rose is predicting a firmer performance of the market during spring from political Iran turmoil, the world’s third largest crude exporter. The risk of losing more Iranian crude output is “threatening logistical patterns and disrupting supply” this spring, Dahlman’s Rose Analyst Omar Nokta said. That will keep spot shipping rates higher than they would otherwise be in a time when industry fundamentals are generally weak, he said. Nokta raised his forecast of shipping rates for very large crude oil tankers to $25,000 per day during 2012 and to $30,000 per day during 2013. That’s up from his previous estimate of $17,000 per day in 2012 and $24,000 per day in 2013.

The supply of super tankers competing to load cargoes of Persian Gulf crude fell to a nine- month low, according to Marex Spectron Group with daily returns on the industry’s benchmark Saudi Arabia-Japan route jumping to a 13 month high, according to Baltic Exchange. The risk of Iranian oil output coming off line supports higher freight rates disrupting supply with demand. However, the crude tanker freight market remains in downward momentum with investors seem to have more faith in the U.S. product demand.

Scorpio Tankers president Robert Bugbee said in the Capital Link Shipping Forum said that the product tanker market offers a much better investment opportunity than crude tankers. Although the product tanker market has experienced tremendous supply growth, Mr. Bugbee believes that the market is about to rise as more western refineries are shutting down and more cargoes will be shipped over longer distances, leading in an increase of ton mile demand. Scorpio Tankers has confirmed an order for one MR 52,000 dwt product tanker with delivery in 2013, increasing the tally of its orderbook to eight product tankers for delivery between July 2012 and May 2013. The order is estimated to bring the global orderbook in the range of 10,000-60,000 dwt to 171 vessels, 13% of the global fleet.

In the gas market, the LNG vessel segment has emerged as the most profitable investment business from soaring LNG spot rates, since last year, with LNG being shipped all over the world as a cheaper source of energy. Before three years, the LNG was out of the spotlight with around 30% of the LNG capacity being idle. The surprising and unexpected rise in US LNG production, from the discovery of significant shale of gas reserves had a negative impact on the prosperity of the segment with Asian demand not being able to offer a remedy. The nuclear catastrophe of Japan spurred high LNG imports that reversed the sentiment, with shipowners experiencing significant gains and targeting in their expansion of their fleet through the placement for the construction of LNG units in South Korean yards.

Monday, April 2, 2012 (Week 14)Capital Link Shipping Weekly Markets Report

Page 26

SHIPPING MARKETS

The Week In ReviewIn the container market, the Shanghai Container Freight Index is on rise for a fifth consecutive week by closing on Friday March 23rd at 1230 points, 7 points more than previous week and up by 30% from February 17th, when it was at 949 points. Asia-USWC and Asia-USEC showed for a second week higher rates, but with a softer rise of 1% and 2% respectively compared with last week’s outstanding increase of 14% on the Asia-USWC route and 8% on the Asia-USEC.

Asia-Europe and Asia-Mediterranean are sliding for a third week by posting soft declines with their rates being still above $1,000/TEU. On a weekly basis, Asia-Europe and Asia-Mediterranean routes have fallen by 1% and standing at $1371/TEU and $1376/TEU respectively. The general rate increases applied by liner operators keep a stronger sentiment on the two major routes, where post panamax units of more than 10,000 TEU are deployed. Rates on the Asia-Europe route are 90% higher than February 10th, when they were at $721/TEU, while rates on Asia-Mediterranean are up by 81% from $758/TEU. CMA CGM, one of the major players on Asia-Europe trade, is optimistic about the rate increases and expects to see further rate increases for this year peak’s season. CMA CGM is focusing on rate restoration rather than capacity increases and has actually cut back some capacity to Northern Europe and Mediterranean. Transpacific rates, Asia-USWC and Asia-USEC, along with Asia-East West Africa outperformed among other routes.Rates on the Asia-USWC route rose to $2021/FEU and $3204/FEU in Asia-USEC, up by $268/FEU and $290/FEU respectively from March 9th, when rates were $1753/FEU and $2914/FEU respectively.