capital structure and the changing role of off - balance ... · capital structure and the changing...

TRANSCRIPT

Capital Structure and the Changing Role of Off-

Balance-Sheet Lease Financing

LAUREL A. FRANZEN, KIMBERLY J. RODGERS,

and TIMOTHY T. SIMIN*

ABSTRACT

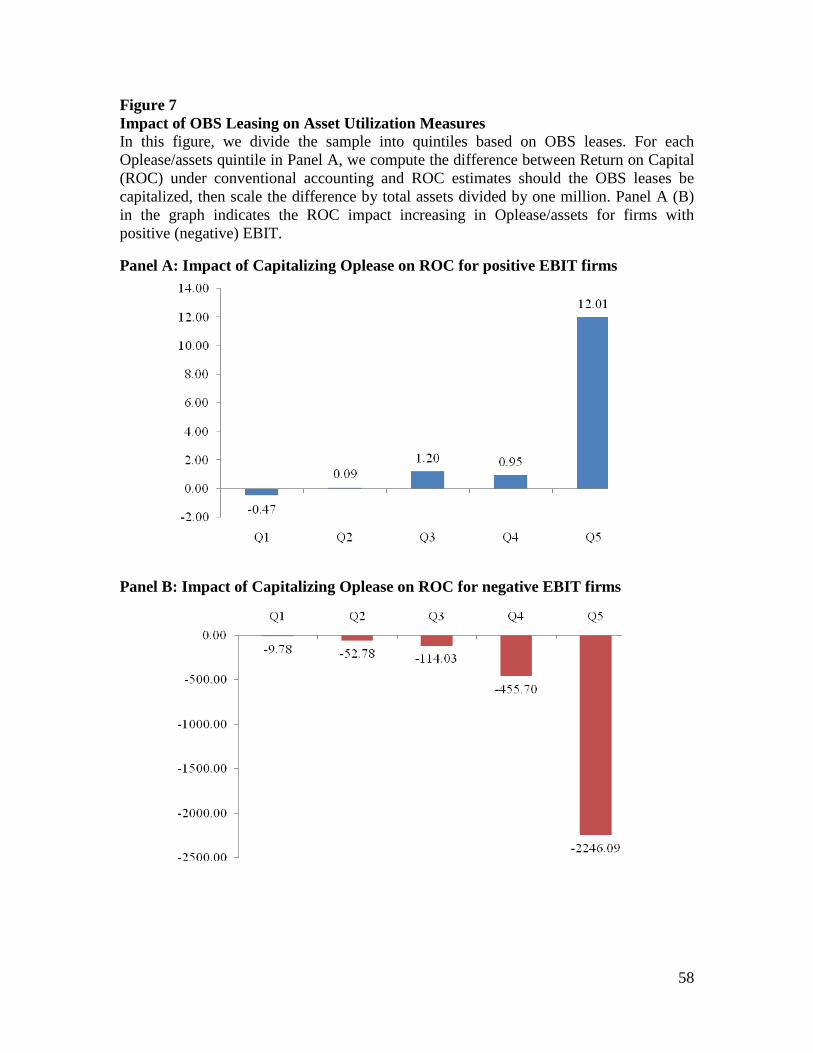

First Draft: April 2008 This Draft: August 2009

Using trend regression analysis, we demonstrate the remarkable increase in off-balance-sheet (OBS) lease financing and simultaneous decrease in capital (on-balance-sheet) leases over the last 27 years. This trend is consistent with the contentions of regulators and popular press that firms intentionally structure leases to qualify for OBS accounting treatment. Moreover, we find that firms rely heavily on this OBS financing in addition to, not merely in lieu of, conventional debt. We include a proxy for the benefits of the OBS accounting treatment as an additional explanatory variable in a traditional capital structure model and find a significantly negative relationship: as abnormal OBS lease activity increases, conventional debt ratios fall. Our results suggest common financial risk metrics underestimate the risk of such firms as the lower debt ratios may be associated with higher OBS debt financing. Our results should be of interest to a host of market participants as the US considers changes in accounting treatment of lease financing. JEL classification: G32, M41, M48 Keywords: Capital structure, Operating leases, Off-Balance-Sheet financing

*Franzen ([email protected]) is at Loyola Marymount University, Rodgers ([email protected]) is at American University, and Simin ([email protected]) is at the Pennsylvania State University. The authors are grateful to John Graham for estimated marginal tax rates, to Jerry Martin for insight and practical experience from a lessor’s perspective, and for comments and suggestions from Jess Cornaggia and seminar participants at the University of Texas.

1

In this study we document that from 1980–2007, Off-Balance-Sheet lease financing as a

percentage of total debt has increased a remarkable 745%. Since leases are non-

cancellable, fixed-term, fixed-income claims with bankruptcy priority, they are

essentially debt.1

Financial leasing theory and prior empirical evidence suggests that leasing

activity is explained by expected costs of bankruptcy, costs of contracting, tax status and

asset specificity.

If leased assets were brought onto the balance sheet over our 27 year

sample period, average debt-to-capital ratios would increase by 50-75%. It appears there

is significant benefit for managers to move these non-cancelable obligations off the

balance sheet.

2

The similarity to debt and ease of moving leases off the balance sheet under

current Generally Accepted Accounting Principles (GAAP) has caught the attention of

regulators and financial press. A 2007 Forbes article states, “…companies have been

working the system [lease accounting] to lower the amount of debt they show investors.”

We show that the benefits of Off-Balance-Sheet (hearater OBS)

accounting treatment of leases are themselves a determinant of leasing activity. Our

results suggest that lower conventional leverage ratios, common risk metrics such as

Adjusted O- and Z-Scores (both of which ignore OBS lease financing), and conventional

levered equity betas understate the financial risk of such firms.

3

1 Capital leases are included as debt in traditional leverage measurements as these leases essentially reflect secured debt. However, operating leases are expensed rather than treated as debt, even when the obligation is non-cancelable and long term. Qualification for OBS treatment is detailed in section II below. 2See McConnell and Schallheim (1983), Smith and Wakeman (1985), Krishnan and Moyer (1994), Sharpe and Nguyen (1995), and Graham, Lemmon and Schallheim (1998). 3 “Debt Hazards Ahead”, June 16, 2007, Forbes Magazine. See also “Hidden in Plain Sight”, August 2005, CFO Magazine.

Regulators have also expressed concern that the financial reporting may not reflect the

2

underlying economics of the transaction [See SEC (2005)]. As early as 2003, former SEC

chairman Arthur Levitt Jr asked:

“Should companies still be allowed to leave billions of off-balance sheet debt, such as lease financing, out of a company’s reported liabilities? Off-balance sheet debt persists, distorting the financial picture investors have been given in companies in many sectors. Markets will discipline themselves and their participants but only if they have accurate information.”4

Concerns of regulators notwithstanding, we note that in an efficient market the

OBS accounting treatment should have no economic impact. Non-cancellable future lease

payments under operating leases are not recognized on the balance sheet, but they do

appear in the disclosure notes to the financial statements. With effort, financial statement

users should be able to adjust for accounting differences across operating leases and

capital leases.

5

Prior leasing theory does not include potential benefits of keeping debt off the

balance sheet as a determinant of the lease versus buy decision. We employ an otherwise-

well-specified, state-of-the-literature model of lease financing to generate a proxy for the

Because this information may not be fully reflected in credit ratings or

other conventional risk metrics, it is an important empirical question as to whether these

trends are significant and if so, whether the benefits of OBS financing influence observed

corporate capital structures. We find they are and they do.

To further investigate the extent to which this trend reflects a substitution effect,

we first consider the types of firms increasing their OBS lease financing. We cannot

attribute the growth in OBS lease financing to financially distressed firms. Nor can we

attribute this trend to retail and transportation firms with general assets. Our trend

regression analysis suggests this phenomenon is pervasive across industries.

4 “The SEC’s Repair Job”, February 10, 2003, Wall Street Journal. 5 We discuss the different treatment of these obligations by Moody’s and S&P below.

3

unexplained benefits of OBS treatment. We refer to this proxy as abnormal or excess

OBS leasing and include it as an additional explanatory variable in a state-of-the

literature model of conventional capital structure. We find that as the benefits of OBS

debt increase, the conventional debt ratio falls.

We explore a host of non-competing explanations for the observed preference for

OBS lease financing. We find some evidence that firms less subject to scrutiny by

institutional investors, analysts and credit ratings rely more heavily on OBS financing.

These results hold after controlling for firm age and size. Because so few of our firms are

subject to this scrutiny, we cannot assume their existence deters firms in general.6

6 Our median firm has zero stock held by Qualified Institutional Investors and zero analyst coverage. Only 15.5% of our sample has a credit rating from S&P.

Finally, we model the ratio of OBS lease obligations to balance sheet debt. Our

results suggest that firms with higher growth options rely more heavily on OBS leasing.

This is consistent with a risk containment strategy. The leased asset has an inherent put

option and higher growth (higher risk) firms pay a premium for this option even if they

have access to conventional debt.

We expect that our findings will be of interest to regulators, information

intermediaries, academics, and practitioners as the Financial Accounting Standards Board

(FASB) and the International Accounting Standards Board (IASB) consider bringing all

material, long-term lease obligations onto the balance sheet.

The following section of the paper (II) details background information on the

financial reporting of leases. In Section III, we discuss prior literature, state our research

questions and formulate testable hypothesis. In Section IV, we describe our data and

methodology. We present empirical results in Section V and Section VI concludes.

4

II. Financial Reporting of Leases by the Lessee

Under current Generally Accepted Accounting Principles (GAAP), the lessee should

classify lease obligations as a capital (ON-balance-sheet) lease if the lease meets at least

one of the four criteria identified in Accounting for Leases, Financial Accounting

Standard No. 13.7

The exact specifications of FAS 13 create an accounting loophole that allows a

lease to be purposefully structured to achieve operating lease accounting and remain

OBS. For example, given the specific thresholds specified in the above classification

criteria (75% and 90%) lease arrangements that are 74% of the asset life or 89% of the

These criteria are as follows:

(1) the agreement specifies that ownership of the asset transfers to the lessee

(2) the agreement contains a bargain purchase option

(3) the lease term is equal to 75% or more of the expected economic life of the asset

(4) the present value of the minimum lease payments is equal to or greater than 90%

of the fair value of the asset.

At inception of a capital lease, a lease liability and a leased asset are recognized

on the balance sheet. The leased asset is depreciated over its useful life and periodic

interest accrual over time decreases the lease liability. The capital lease is a financing

vehicle for the purchase of an operational asset and is essentially secured debt. However,

if a lease arrangement does not meet any of the four criteria of a capital lease, it is

accounted for as an operating lease. Operating leases have no effect on the balance sheet;

periodic rent expense is recorded on the income statement.

7 FAS 13 is effective for lease transactions entered into on or after January 1, 1977.

5

fair value of the leased asset can qualify for operating lease treatment under GAAP.8

There is a large empirical literature examining the theoretical determinants of the

lease versus buy decision.

Similarly, “lease payments” can be minimized to circumvent criteria #4 by requiring

excessive maintenance payments. Anecdotal evidence suggests that opportunistic

structuring of leases has become a thriving industry since the passage of FAS 13.

Numerous websites advertise services and techniques for structuring operating leases.

Miller and Bahnson (2008) suggest that reputable accounting firms help clients

intentionally structure lease arrangements specifically to remain OBS. To the extent that

market frictions exist, firms have incentive to exploit these accounting rules to keep debt

off the balance sheet.

III. Literature Review and Hypothesis Development

A. The lease versus buy decision

9

Leasing theory predicts that financially distressed firms obtain more favorable

financing terms from lessors than from traditional creditors. This predicted relation

stems from the priority of lessors’ claims in bankruptcy proceedings and is likely to be

strongest for leases classified as operating leases that ostensibly never intend to transfer

However, given recent regulatory concern of increasing and

potentially dubious reliance on OBS lease financing, we investigate whether the

theoretical determinants continue to explain lease activity.

8 Under International Accounting Standards, IAS 17, whether a lease is a capital lease or an operating lease depends on the substance of the transaction rather than the legal form of the contract. That is, the criteria for capital lease treatment under IAS 17 differs from FAS 13 in not specifying specific cutoffs. 9 See McConnell and Schallheim (1983), Smith and Wakeman (1985), Krishnan and Moyer (1994), Sharpe and Nguyen (1995), and Graham, Lemmon and Schallheim (1998).

6

ownership. Weiss & Wruck (1998) document the court-sponsored asset stripping of

Eastern Airlines where the court allowed the debtor to sell secured creditors’ collateral

(including capital leases) to fund operating losses.10,11

The lease versus buy decision should be influenced by the nature of the asset.

Fixed assets of general usage (such as real estate, aircraft, trucks and automobiles,

electronics and computer equipment) are readily transferable and as a result have greater

availability on the leasing market. With few alternative uses, the economics of

The Eastern case may be a legal

anomaly, but it demonstrates rational incentive for creditors to maintain ownership of

their collateral going forward. Under an operating (OBS) lease, the lessor maintains

ownership of assets where capital leases indicate intended transfer of ownership just as in

a traditional purchase financed by conventional debt.

Krishnan and Moyer (1994) empirically investigate the relation between capital

(on-balance-sheet) leases and the costs of bankruptcy and find that capital leasing activity

is positively related to the costs of bankruptcy. Graham, Lemmon and Schallheim (1998)

find that this positive relationship extends to operating (OBS) leases.

Leasing theory also predicts that firms with higher costs of external funds reduce

investment costs by leasing assets. Finance theory and empirical evidence further suggest

that the cost of external funds is higher when information asymmetry, agency problems,

and underinvestment problems are more severe (Myers and Majluf (1984), Sharpe and

Nguyen (1995), Graham et. al (1998)).

10 Eastern Airlines filed Chapter 11 on March 9, 1989. After $1.4 billion in operating losses, Eastern ceased operations and auctioned remaining aircraft. The final reorganization plan was confirmed by the bankruptcy court on December 22, 1994. 11 In addition to the aircraft sold to fund losses, many recovered aircraft were recovered in poor condition. Weiss and Wruck note that because Eastern failed to maintain planes as dictated by the terms of its capital leases, lessors had to make major repairs on many recovered planes to return them to flying condition.

7

specialized assets suggest conventional debt (or equity) financing. Consistent with these

predictions, Graham et. al (1998) and Sharpe and Nguyen (1995) report a negative

relation between leasing and proxies for asset specificity.

Finally, because the operating lease transfers tax shields, leasing theory predicts

that the potential borrower (lessee) marginal tax rate is negatively related to the

propensity to lease assets. A profitable lessor can take advantage of the tax benefits of

interest payments and depreciation and pass savings along (at least in part) to the lessee

unable to fully utilize the tax benefits of ownership.12

Though the lease versus buy decision is well studied, there is relatively little focus

specifically on the role of OBS leases. This is surprising given the 2005 SEC report that

non-cancellable future payments required under OBS leases were an estimated $1.25

trillion. Prior literature provides mixed evidence on whether market participants

appropriately adjust for OBS lease obligations.

Graham et. al (1998) find operating

leases are indeed negatively related to the pre-financing marginal tax rate.

B. Off Balance Sheet Leases

13 Explanations for why they may not

include (1) limited attention and other potential systematic biases, (2) costly information

processing and (3) differences in the perceived reliability of information that is

recognized versus disclosed.14

12 To transfer tax shields, the lease must qualify as a “true lease” under IRS tax rules. For legal and tax purposes, when the lessor retains ownership of the leased asset, the lease is a “true lease” for the lessee, however this tax classification is not publicly available. Tax rules for leasing are similar on most dimensions to financial reporting rules. Graham et. al (1998) provide a detailed comparison of tax and financial accounting rules. 13 See Altamuro, et al. (2008), Ely (1995), Imhoff, Lipe and Wright (1993), Beattie, Edwards and Goodacre (1998) and Ge, Imhoff and Lee (2008). 14 See Ahmed, et. al (2009), Aboody (1996) Davis-Friday, et. al (1999), Hirshleifer and Teoh (2003), Barth et. al (2003) and Libby, et. al. (2005).

All of these explanations suggest that structuring leases

8

such that they are relegated to lengthy disclosure notes rather than prominently

recognized in the financial statements can lead to more favorable firm valuations.15

Traditional theories and models of corporate capital structure focus on the demand for

debt versus equity capital, either as a tradeoff of cost and benefit of debt or market

timing.

C. Research questions and testable hypotheses

Our first research question is motivated partially by the concerns of regulators that

firms increasingly (dubiously) structure leases to qualify for OBS accounting treatment.

As noted above, leases are contained in the disclosure notes of audited financial

statements filed with the SEC. In an efficient market, regulators, investors, and other

market participants should be able to adjust assessments of financial risk to account for

these obligations.

Q1: Has the role of OBS leases in corporate financing changed through time?

H1a: The mix of On- and Off-balance sheet lease financing appears stable over time.

H1b: OBS lease financing as a percentage of conventional debt is stable over time.

16

15 In financial reporting, the term “recognition” refers to incorporating an item into the primary financial statements. In contrast, the term “disclosure” refers to providing information about an item in the notes to the primary financial statements.

16 Demand-driven theory of optimal capital structure begins with Modigliani and Miller (1963). Extensions include DeAngelo and Masulis (1980), Kim (1982), Modigliani (1982), Myers (1984) and Bradley, Jarrell, and Kim (1984). Empirical tests of these models include Titman and Wessels (1988), MacKie-Mason (1990), Berger, Ofek, and Yermack (1997), Shyam-Sunder and Myers (1999), Hovakimian, Opler, and Titman (2001), Fama and French (2002), Mehrotra, Mikkelson, and Partch (2003), Dittmar (2004), Hovakimian, Hovakimian, and Tehranian (2004), and Frank and Goyal (2009). Baker and Wurgler (2002) propose a theory which suggests that a firm’s capital structure is the cumulative result of managerial attempts to time the equity market. Similarly, Graham and Harvey (2001) and Barry, Mann, Mihov, and Rodriguez (2008) note the importance of debt timing with respect to interest rates.

But the supply of capital is also determined by potential lender risk profiles.

9

Firms facing financial distress may find better terms from lessors who maintain

ownership of the asset.

Q2: Is the increase in OBS lease financing attributable to firms facing higher

probability of financial distress?

H2: Reliance on (and the increase in) OBS lease financing should be greatest among

firms with higher Z-scores (and adjusted O-scores).

A related consideration is the differential tax status of the lessee vis-à-vis the creditor or

lessor. If the potential lessee faces a lower marginal tax rate, this firm may prefer to

transfer the tax benefit of ownership to the lessor by structuring the lease as an operating

lease in order to lower the cost of lease financing.

Q3: Is the increase in OBS lease financing attributable to firms that cannot take full

advantage of debt tax shield?

H3: Reliance on (and the increase in) OBS lease financing should be greatest (least)

among firms with lowest (highest) marginal tax rates.

Financial theory suggests that liquid fixed assets of general usage are more appropriate

for lease financing. If there is a change in the industrial composition of firms using lease

financing, we can infer the role of the lease has changed. Specifically, evidence of

increased OBS lease financing among industrial firms would indicate greater propensity

to lease less liquid (firm-specific) assets that are less valuable to the lessor than to the

lessee. For firms without access to debt markets, specialized assets could be financed

with capital (rent to own) leases, but are unlikely structured as operating leases unless the

motivation is keeping debt off the balance sheet.

10

Q4a: Is there a change in the industrial composition of firms using lease financing? Is

there an increase in OBS lease financing among industrial firms?

Q4b: Is there an increase in OBS lease financing among firms with relatively high

investment in Research & Development?

H4a: Reliance on (and the increase in) OBS lease financing is attributable to firms

with general assets found in Retail and Transportation industries.

H4b: Reliance on (and the increase in) OBS lease financing is attributable to firms

with low R&D intensity.

To the extent that market frictions exist, the OBS treatment of operating leases may be an

overlooked benefit to be considered in the lease versus buy decision. Market participants

may not fully consider OBS leases and thus make inaccurate risk assessments. We

investigate whether benefits of OBS financing influence observed corporate capital

structures expecting that as the benefits of OBS debt increase, observed, on-balance-sheet

debt levels decrease.

Q5: Do benefits from OBS treatment of operating leases influence corporate capital

structures?

H5: Excess OBS lease financing is negatively related to conventional debt ratios.

Finally, we investigate whether the economics of the firm can explain the observed mix

of On- and Off-balance sheet debt. Given the latitude in accounting standards for

classifying leases and the concern of regulators that firms utilizing OBS financing are

“hiding debt”, this is an important empirical question. Empirical scrutiny of the

appropriateness of these financial reporting lease classifications is sparse and out of date

11

with the results of our study.17

Our initial sample contains all firms in the merged CRSP-Compustat database

from 1980 through 2007. We include only firms with common stock and exclude

regulated financial firms (SIC codes 6000-6799) and utilities (SIC codes 4800-4999).

Before matching Compustat and CRSP data we adjust for the Compustat convention that

companies with fiscal years ending between June of year t and May of year t+1 are coded

as year t. We assign firms with fiscal years ending in the first quarter of year t+1 to year

t+1 and assume a 6-month lag between the end of a firm's fiscal year end and when

If leases are funds of last resort for firms without access

to debt markets, we should expect to see firms utilizing capital leases (renting to own).

However, if the trend in lease financing is a reflection of a preference for OBS financing

to appear more conservatively financed, we expect to see firms utilizing operating leases

in lieu of capital leases. Moreover, if firms are indeed able to “hide debt” as regulators

suggest, they may utilize more total fixed-cost (debt) financing. That is, the increase in

OBS lease financing may well be in addition to, not merely in lieu of, balance sheet debt.

Q6: Do firms use operating leases to expand debt capacity? That is, do firms finance

assets with operating (OBS) leases in lieu of on-balance-sheet debt financing

(conventional debt or capital lease), or are OBS leases in addition to on-balance-

sheet debt?

H6: Capitalizing leased assets has no effect on debt-to-capital ratios.

IV. Data and Methodology

A. Sample Selection

17 Krishnan and Moyer (1994) investigate whether capital leases may be misclassified as operating leases for their sample in the years 1984-1986. They concluded that in these three years, very few firms had non-cancelable lease arrangements that were not reported as capital leases on the balance sheet.

12

financial statement information is publicly available. Firms with a less than $1 million in

total assets, negative sales, and no debt are then removed from the sample. After forming

the needed variables detailed in Appendix A, we winsorize each variable, except the

marginal tax rate data, at the upper and lower 0.05 percentiles.18

18 The simulated marginal tax rate data we use was kindly provided by John Graham and we also acknowledge the use of the 38 industry designations which come from Ken French’s web page.

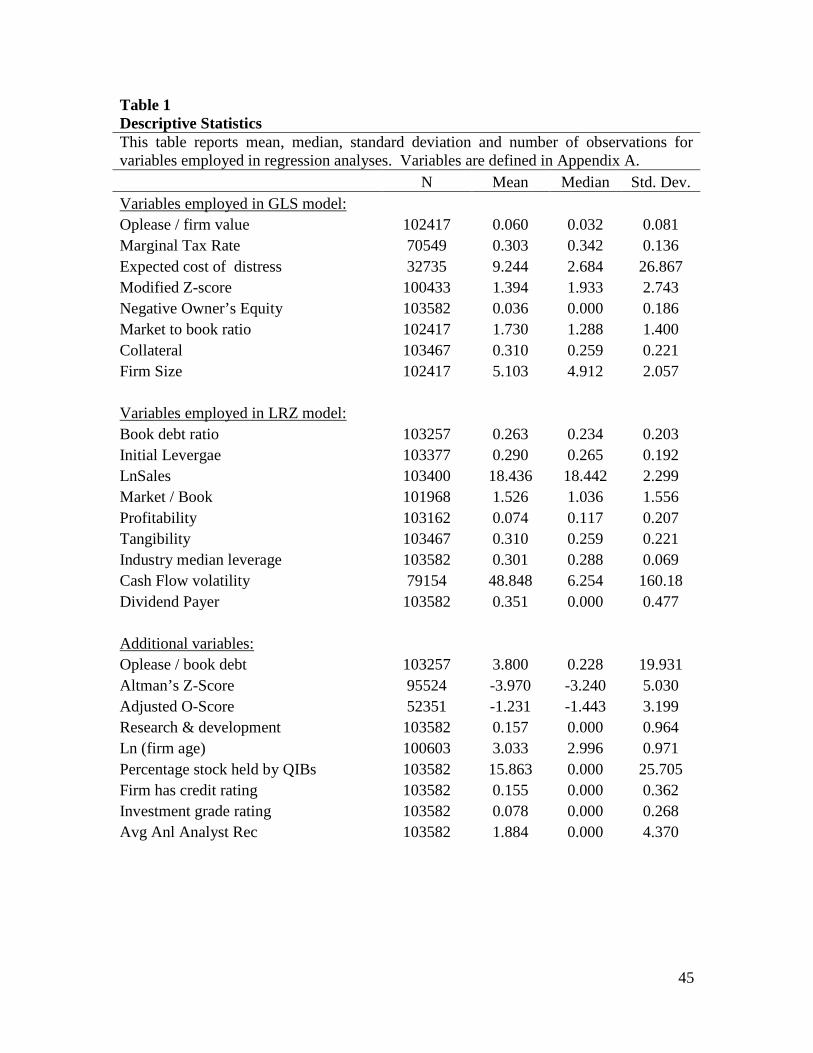

We use the maximum amount of data available in each of our tests below. The

number of firm years for each series ranges from a maximum of 103582 with simulated

marginal tax rates (MTR) and expected cost of financial distress (ecost) having the fewest

observations, 70549 and 32735 respectively. Theses series look similar to previous

samples. Most of the series are fat tailed with cash flow volatility (CFvol), ecost and

negative owners equity (oeneg) having a considerable amount of positive skew. We

report summary statistics in Table 1.

B. Unobserved Benefits of Off-Balance Sheet Leasing

In addition to testing for trends in univariate settings, we also test whether

‘abnormal’ operating lease levels (operating leases not explained by proxies for

theoretical determinants) help explain conventional debt ratios. To create a proxy for

‘abnormal’ operating lease levels we estimate the state-of-the-literature model of

theoretical determinants of lease financing by Graham Lemmon Schallheim (1998),

hereafter, GLS. In particular, we estimate the specification in equation (1) using a panel

regressions with fixed year effects.

OPlease/TVit = α1 + β1Mtr + β2Ecost + β3Zmod + β4Oeneg + β5Mtb + β6Coll (1) + β7Size + β8d2000 + β9d3000 + β10d4000 + β11d86 + β12d8792 + εit

13

We report traditional t-statistics and t-statistics based on an extension of cluster-

robust standard errors that allows for clustering along more than one dimension proposed

by Cameron et al. (2006) and Thompson (2006).19

We then estimate the state-of-the-literature conventional leverage model of

Lemmon Roberts Zender (2008), hereafter LRZ, both with and without AbOplease. This

allows us to test whether AbOplease is significantly related to the Conventional Leverage

dependant variable. Specifically, we estimate the following specification both with and

without AbOplease.

Since operating (OBS) leases as a

percentage of firm value is the dependent variable in this model, we use the error terms

from this estimation as the proxy for the abnormal operating lease levels (AbOplease).

20

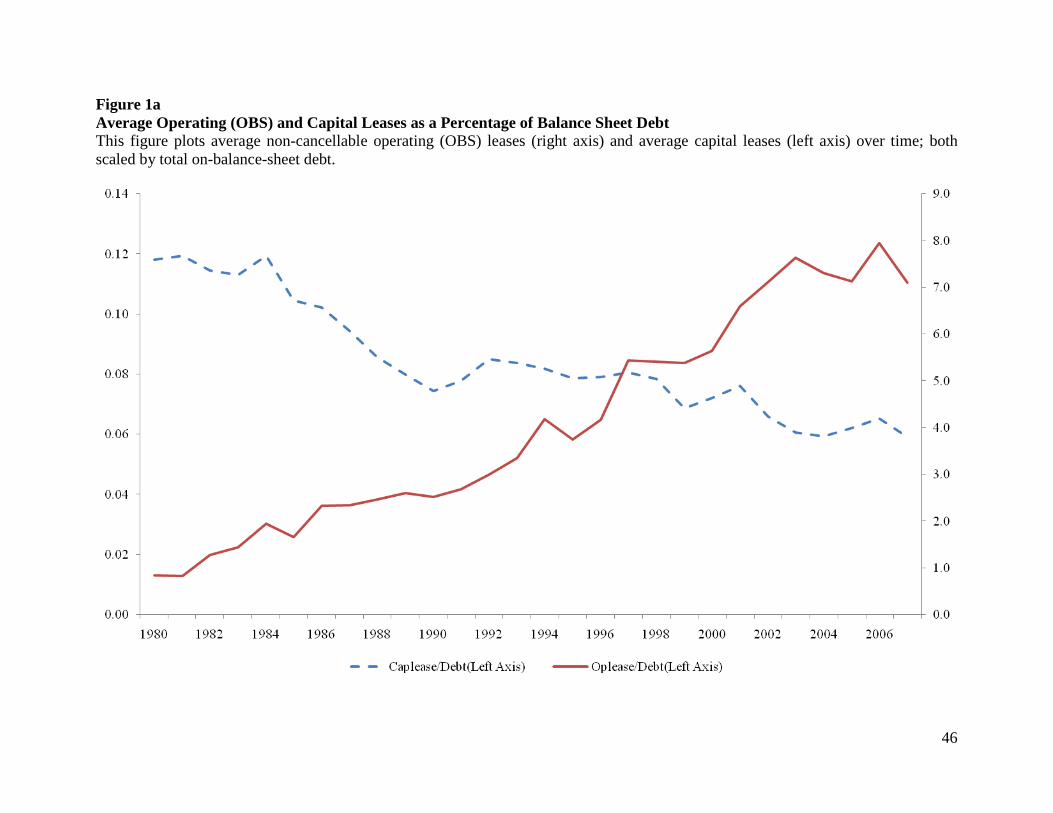

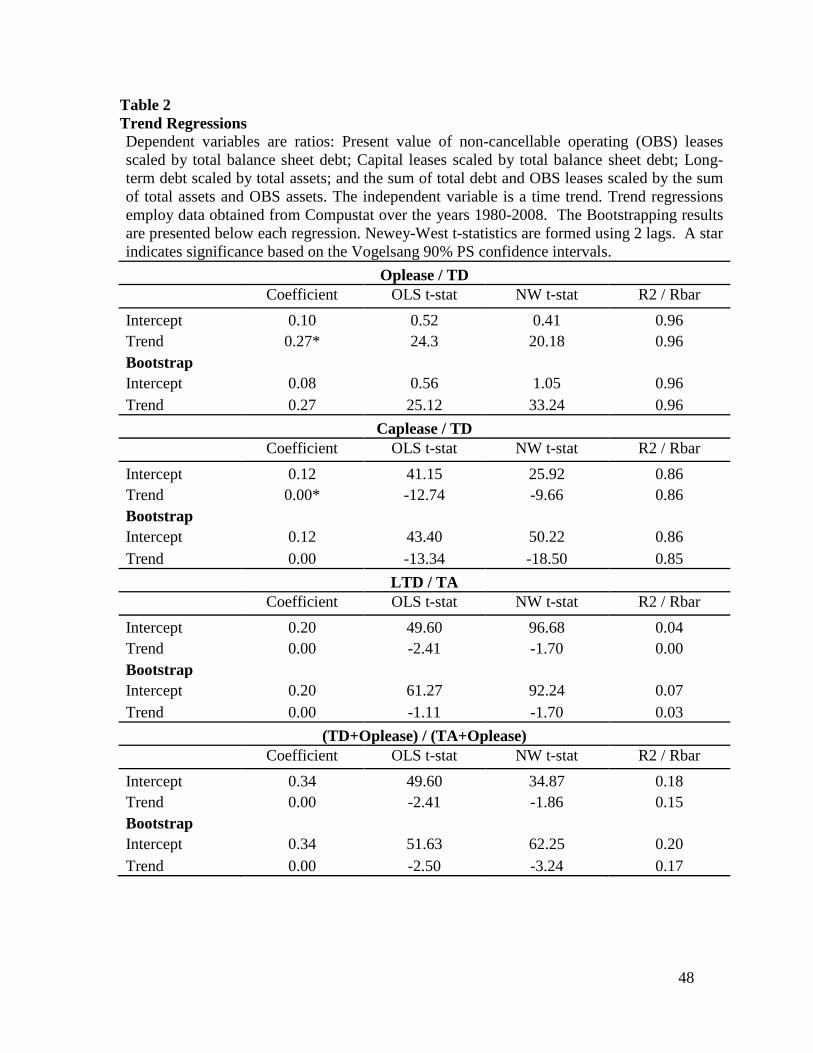

Figure 1a clearly demonstrates the magnitude of operating (OBS) lease liabilities

to total debt (Oplease/TD) has increased over time while the magnitude of capital (on-

balance-sheet) lease liabilities to total debt (Caplease/TD) has decreased.

BLit = α1 + β1Intlev + β2LnSale + β3Mtb + β4Profit + β5Tang + β6Indmedlev + (2) β7CFvol + β8SDivpay + β9 AbOplease + εit

V. Empirical Results

A. Leasing across time: univariate analysis

21

19 Two-way clustering corrects for both time-series and cross-sectional dependence. In our application we cluster by firm and year to capture time series dependence within firms and cross-sectional dependence within year. 20 Definitions of variables employed in the GLS and LRZ models are provided in Appendix A. 21 The trends occur while the number of firms in each annual cross-section first increase then falls to a third of the number in 1980, making it doubtful that the trends are due to some type of firm effect.

The mean

ratio of Caplease/TD was 0.118 in 1980 and by 2007 the ratio has declined to 0.059. On

14

average, capital leases make up a smaller portion of debt across time. In contrast, mean

Oplease/TD is large in magnitude and increasing across time. Specifically, mean

Oplease/TD is 0.84 in 1980 and by 2007 has risen to 7.116; a 745% increase in 27 years.

Clearly, OBS lease financing is an increasingly important source of corporate funding.22

In Table 2, we test whether these observed trends in Figure 1a are statistically

significant. We regress Oplease/TD on a time trend and Caplease/TD on a time trend.

Our sample spans the period 1980-2007, so our time trend variable represents values

from 1 to 28 where 1 corresponds to the year 1980 and 28 corresponds to the year 2007.

These results confirm that the observed time trends are statistically significant. When

Oplease/TD is the dependent variable, the coefficient on time trend is positive and

significant.

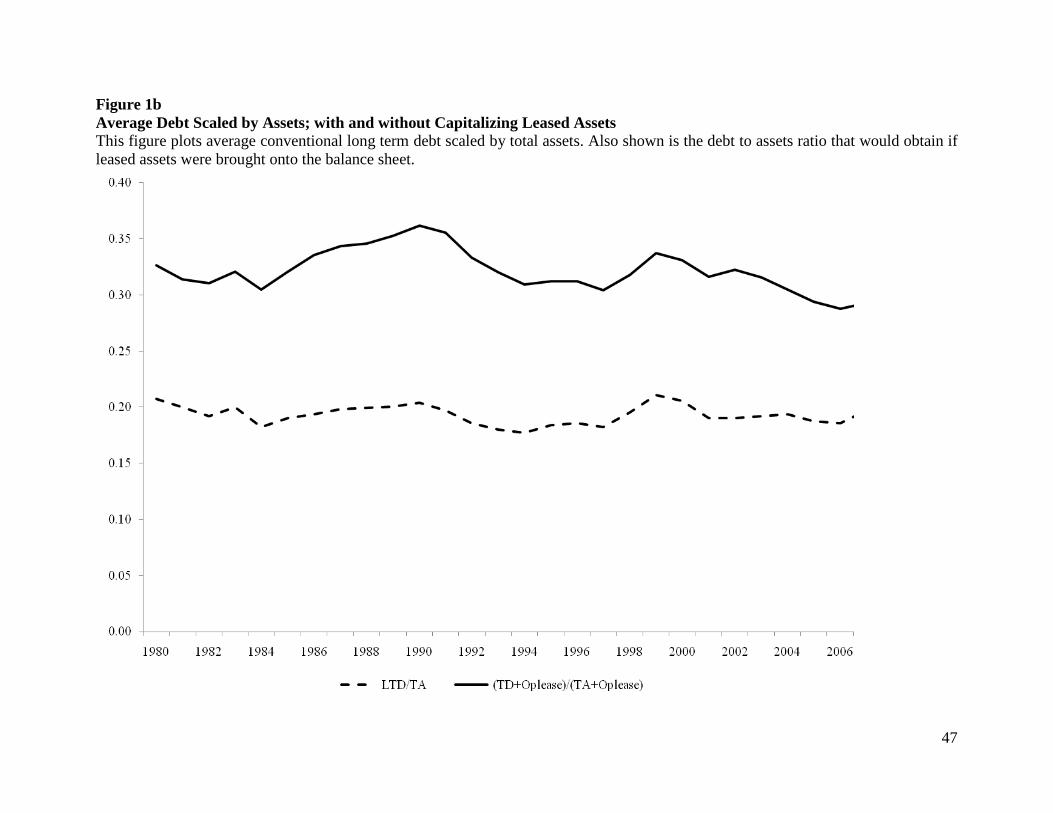

Figure 1b demonstrates no obvious trend in conventional long term debt-to-capital

ratios over the same time period. This suggests that the remarkable increase in OBS

obligations are in addition to, not merely in lieu of conventional debt financing. Figure

1b also plots the average debt-to-capital ratio that exists if the leased assets are brought

onto the balance sheet. The trend in Figure 1a is not obvious here because Oplease is

added to the numerator (debt) and denominator (assets). What is remarkable is the effect

on the debt-to-capital ratio. Conventional accounting results in a much more conservative

picture (approximately 20%) than the reality (30-35%).

23

22 This trend exists when we plot unscaled operating and capital leases or if we scale these variables by total financial claims including on-balance sheet debt and our estimate of OBS lease liabilities. The trend also exists in a constant sample of firms across time. 23 The trend is significant based t-statistics formed using Newey-West standard errors or based on the Vogelsang 90% PS confidence intervals.

In contrast, when Caplease/TD is the dependent variable, the coefficient on

time trend is negative and significant. We ensure that these results are not driven by the

15

small sample size via a bootstrapping procedure that resamples the original data 10,000

times. Our results are qualitatively similar under the bootstrapping procedure.

We find no statistical evidence of any trend in LTD/TA indicated by the OLS t-

statistics, Newey-West t-statistics, or the Vogelsang confidence intervals. While the

regression t-statistics for (TD+Oplease)/(TA+Oplease) seem to indicate a downward

trend, the Vogelsang confidence intervals do not support any trend.

We take this evidence from Figure 1 and Table 2 as a rejection of both H1a and

H1b. The magnitude of OBS leases is massive relative to capital leases, so we cannot

conclude that the increase merely reflects a shift from capital to operating leases.

Further, the increase in OBS leasing is not diminishing conventional debt. We reject H6.

We next investigate whether the trends in lease financing are explained by factors

previously demonstrated to influence the lease versus buy decision. We focus our

attention on operating (OBS) leases going forward given the much smaller magnitude of

the capital lease story.

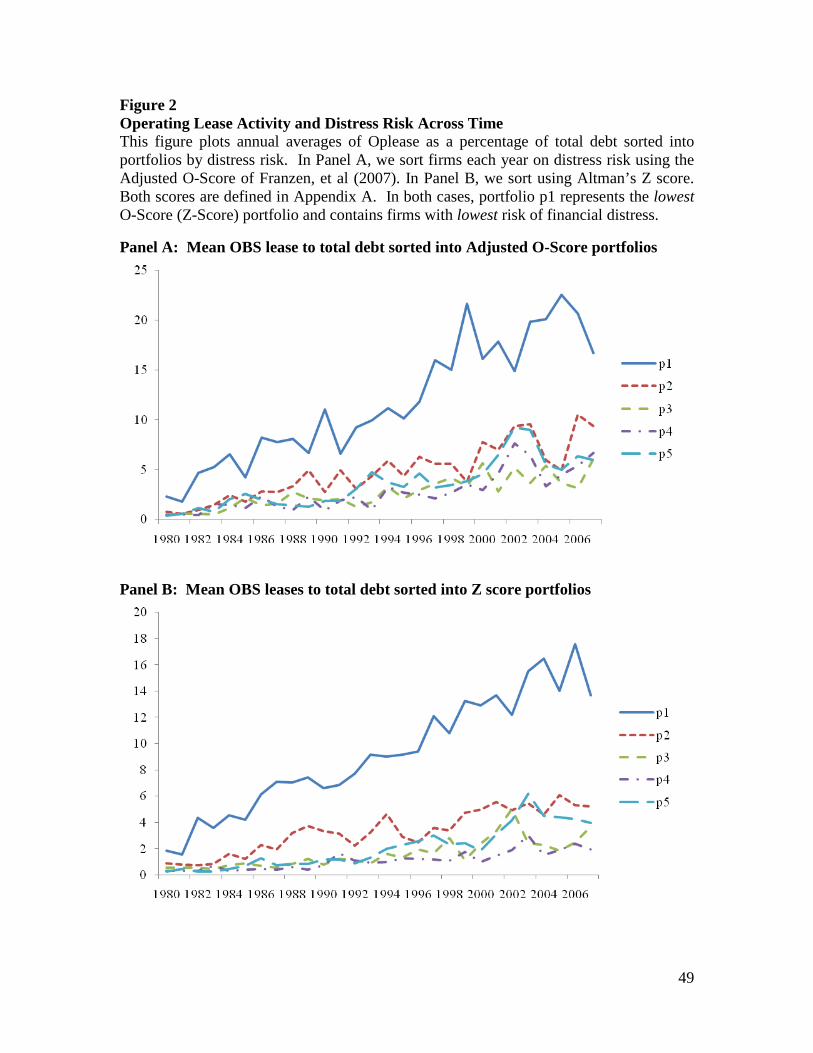

In Figure 2, we classify firms by year into five portfolios based on the likelihood

of bankruptcy, using the adjusted O-score of Franzen et al (2007) and Altman’s Z-score

in Panels A and B, respectively. Both scores increase in distress, thus portfolio 1 (5)

contains the least (most) distressed firms. For each portfolio, we plot the mean level of

Oplease/TD.24 These plots indicate that the mean level of OBS leases to total debt is

highest for firms with the lowest bankruptcy risk (p1) and increasingly so.25

24 Our data are winsorized at the upper and lower 0.05 percentiles; the means should not reflect outliers. 25 In untabulated analysis, we confirm that the upward trend in the mean level of Oplease/TD across time in the top and bottom O- and Z-score portfolios is statistically significant using the Vogelsang confidence intervals.

These

results run counter to the argument that lease financing is a source of last resort for

16

financially distressed firms and do not support H2. This result is at least partly

attributable to the fact that these distress risk proxies overlook the OBS obligations.

Adjusted O-score is purely a function of balance sheet and income statement ratios, i.e. it

does not incorporate OBS obligations. The Z-score contains a market data component,

but only reflects OBS obligations to the extent that market participants account for them

properly. Even the results employing the more market-based Z-Score reject H2.

It is important to note that this surprising result is not simply an issue of imperfect

proxies for financial distress.26

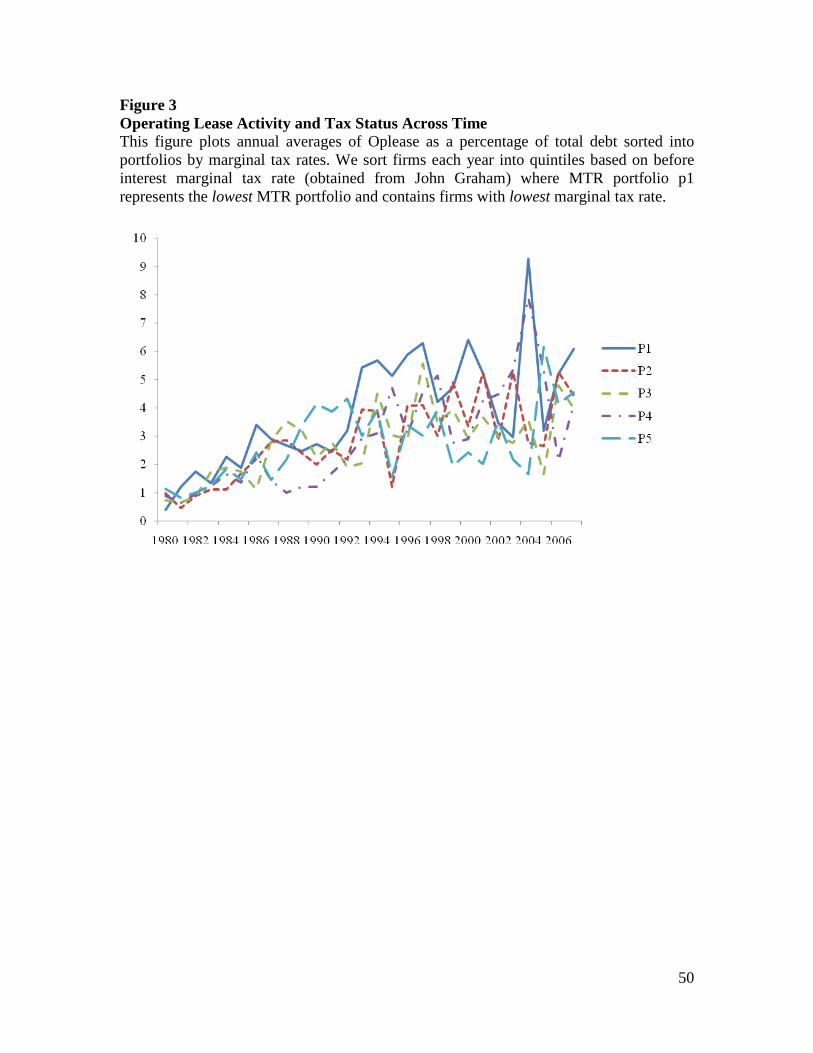

In Figure 3, we investigate the relation between tax status and OBS leasing

activity across time. Leasing theory predicts a negative relation between tax status and

leasing activity. We sort firms into quintiles based on the estimated before interest

marginal tax rate (MTR) and plot the mean Oplease/TD across time for each. We infer at

best weak support for H3.

The plots in Figure 2 are themselves an important

empirical result: commonly employed risk metrics overlook this increasingly important

source of debt financing. These imperfections notwithstanding, quintiles of Adjusted-O

and Z-scores continue to properly sort firms by bankruptcy incidence (See Franzen et al,

2007) and we thus cannot conclude that the increase in OBS lease financing is

attributable to those most likely to go bankrupt. To the contrary, the increase appears

attributable to firms not facing bankruptcy.

27

26 A host of empirical studies support Z-score as a reliable indicator of bankruptcy. Likewise, Frazen et al (2007) demonstrate the efficacy of the adjusted O-score.. 27 Similarly, untabulated trend regressions also fail to support H3.

While the lowest MTR portfolio has higher lease financing

on average, there are periods (including the 2005-2006 period) where highest MTR

portfolio overtakes the lowest MRT portfolio. Moreover, the upward trend is evident in

17

each quintile, not primarily p1. MTR may be a determinant of the lease versus buy

decision, but alone it cannot explain the trends documented in Figure 1a and Table 2.28

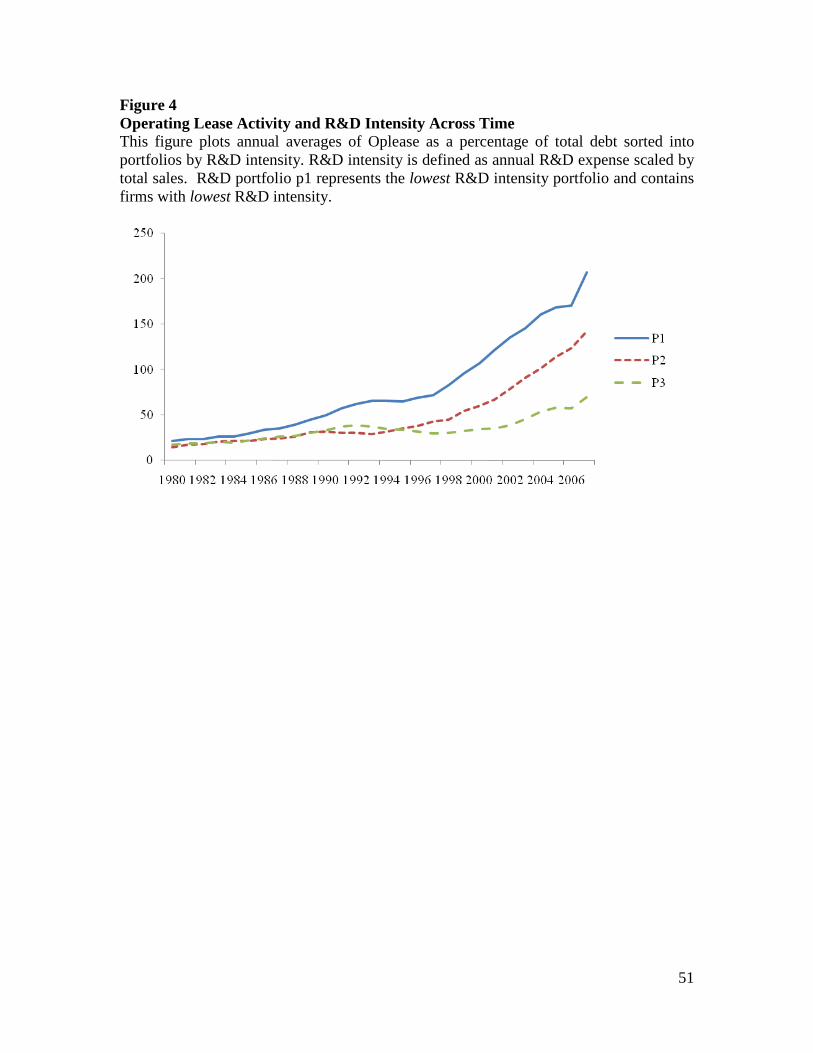

In Figure 4, we investigate the relation between OBS leasing activity and asset

specificity. We use R&D expense (scaled by total sales) as our measure of asset

specificity as R&D intensive firms are more likely to have specialized assets.

29

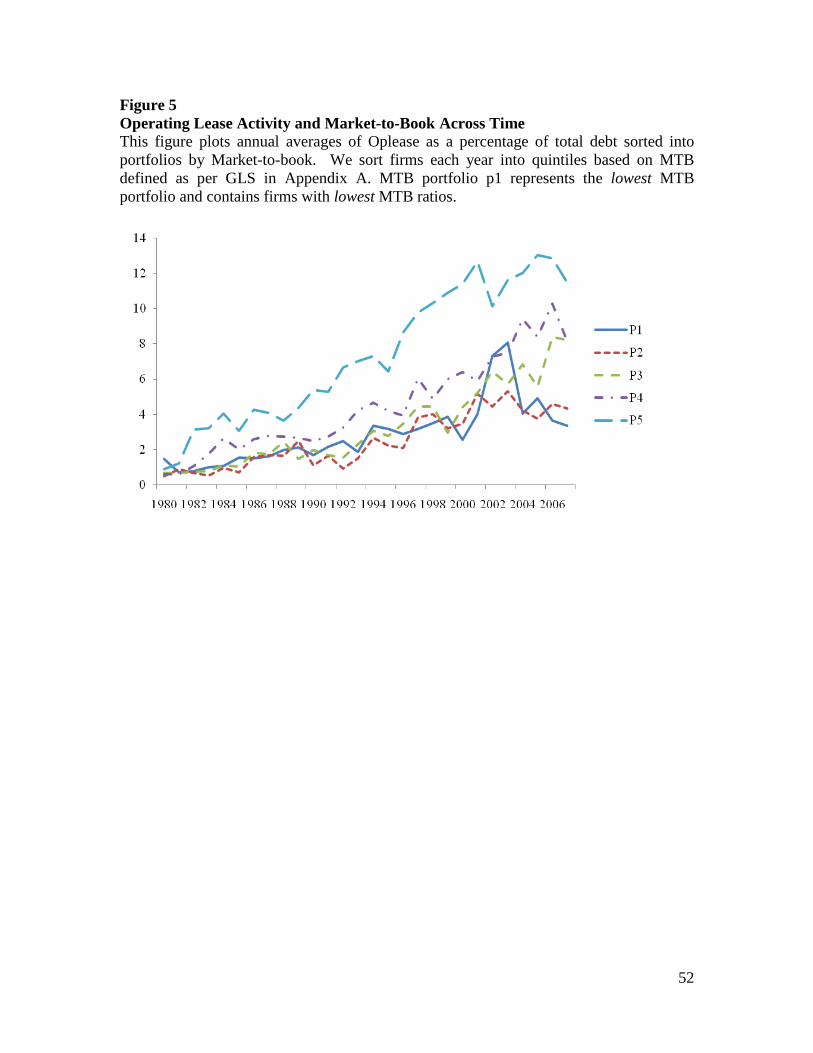

In Figure 5, we sort firms into quintiles based on market-to-book (defined as per

GLS in Appendix B) and then plot Oplease/TD across time for each. Drawing on the

underinvestment problem associated with fixed cost financing (see Myers, (1977)) GLS

suggest that firms with more growth options in their investment opportunity sets should

have a lower proportion of fixed claims in their capital structure. To the contrary, Figure

5 actually suggests that, in a univariate setting, firms with highest market-to-book ratios

We sort

firms by year into three R&D portfolios. Because the median level of R&D as a

percentage of assets is zero, the bottom portfolio (pl) contains firms without R&D

expenses. The highest portfolio (p3) contains firms with non-zero R&D and the middle

portfolio contains both zero and non-zero R&D firms. From 1996 to 2007, mean

operating lease activity decreases monotonically across R&D portfolios. This suggests

that asset specificity remains an important determinant of leasing activity across time but

provides little support for H4b. Untabulated trend coefficients are significantly positive

for all three operating lease portfolios.

28 During our sample period, there were two major changes in tax law that affected the tax depreciation of assets. The Economic Recovery Act of 1981 introduced the Accelerated Cost Recovery System (ACRS) for assets placed in service after 1980. Then, in 1986, the Tax Reform Act of 1986, introduced the Modified Accelerated Cost Recovery System (MACRS) for assets placed in service after 1986. To the extent that the determination of tax depreciation of assets has not changed significantly since 1986, tax considerations are unlikely to be an increasingly important determinant of OBS lease activity across time. 29 We find qualitatively identical patterns whether we define firm total value as book value, market value or as the implied market value described in the appendix.

18

employ OBS leases to a far greater extent than firms with lower market-to-book ratios.

We revisit this inconsistency in multivariate regressions later in the paper.

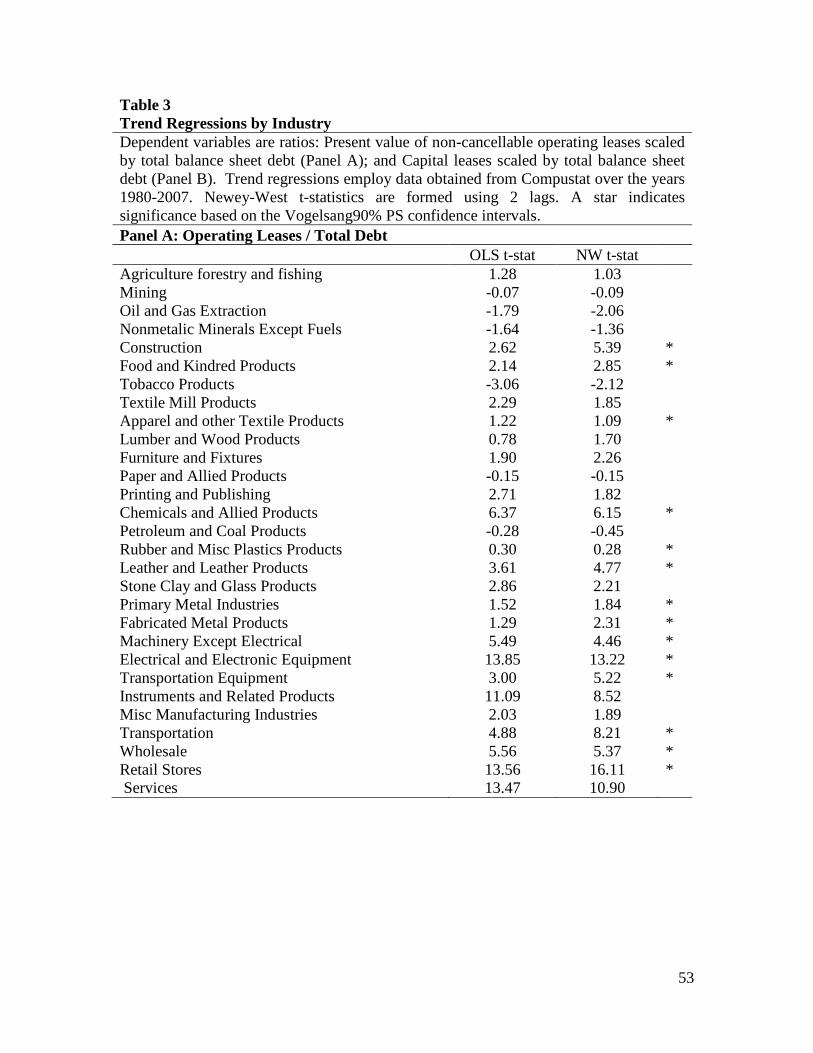

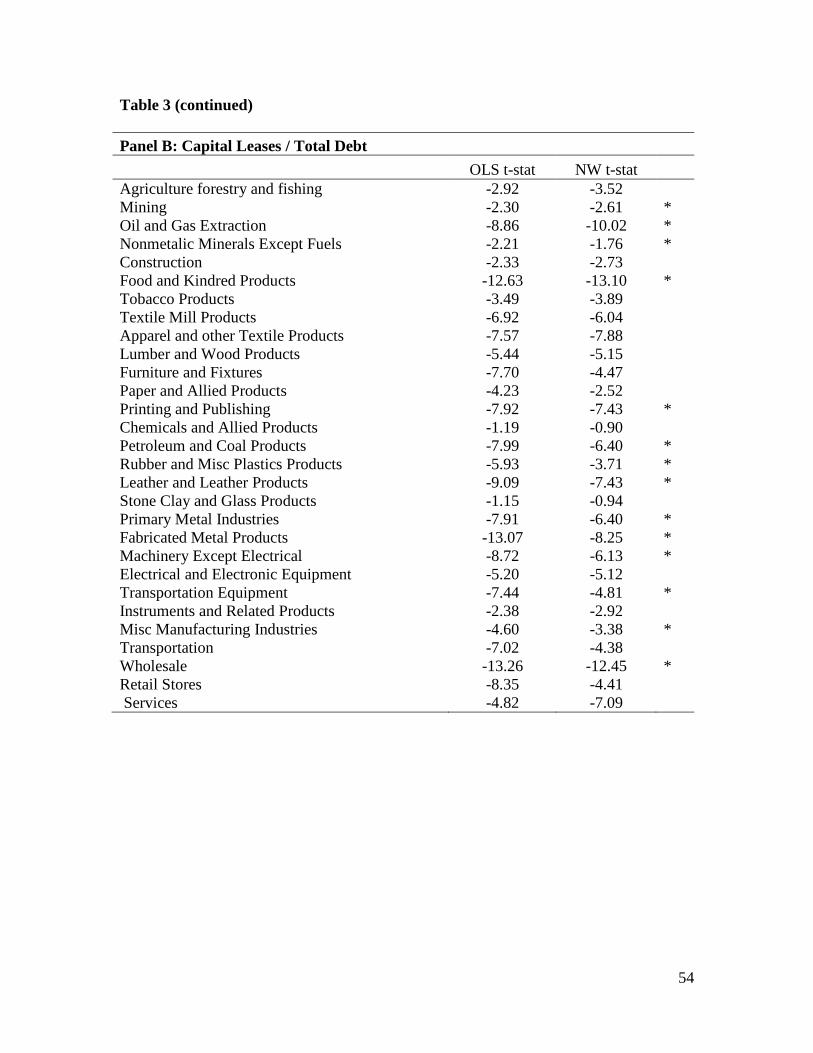

In Table 3, we estimate the trend regressions for equally weighted industry

portfolios. Financial theory suggests that liquid fixed assets of general usage are

appropriate for lease financing indicating that OBS lease financing should be found

primarily in industries such as retail and transportation. In Panel A we find that 14 of the

29 industries exhibit significant positive trends in operating lease as a percentage of total

debt. There is some evidence that Oil and Gas Extraction and Food and Kindred Products

had a significant decrease over this period. In Panel B all but two of the industries

portfolios had a significant negative trend in capital leases as a percentage of total debt

with fourteen of the trends falling within the 90% Vogelsang confidence intervals. This

evidence indicates that leases are structured off-balance sheet for more than liquid

general usage assets. Table 3 results lead us to reject H4a; the increase in OBS lease

financing is not driven by retail and transportation firms.

B. Leasing across time: multivariate analysis

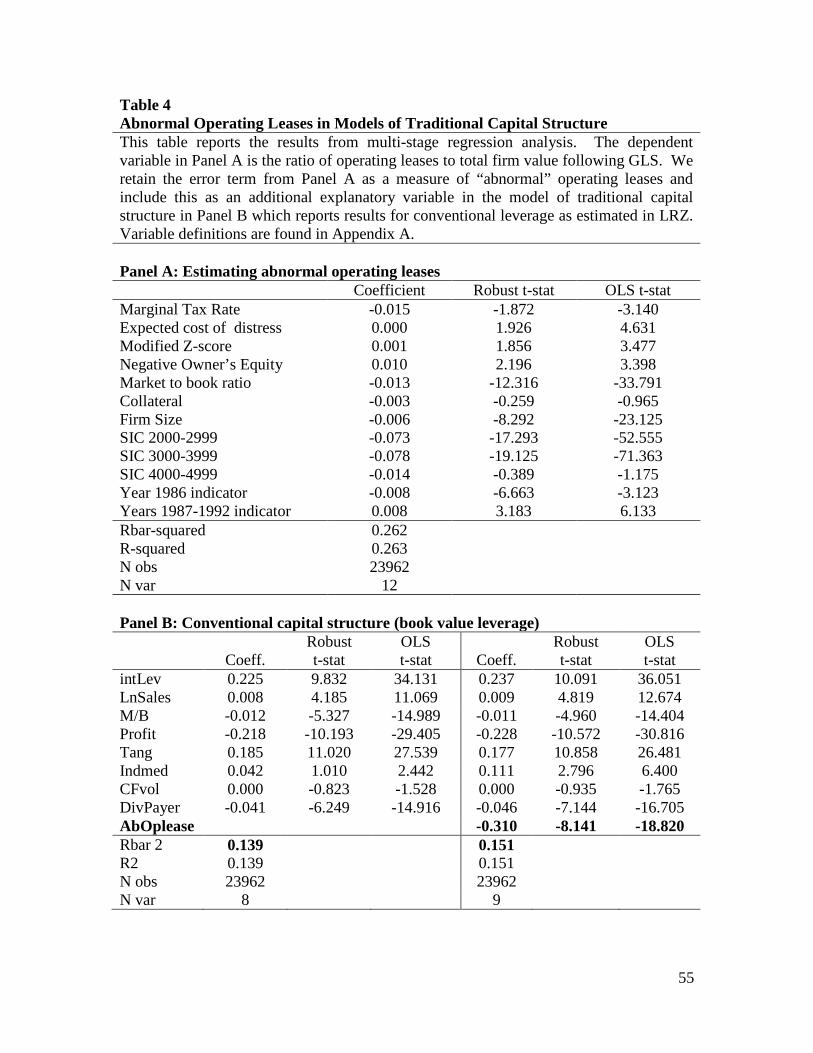

We next investigate whether these expected relationships between operating lease

activity and theoretical determinants of leasing hold in a multivariate leasing model. In

Table 4 Panel A, we specify the leasing model following Graham, Lemmon and

Schallheim (1998). As measured in GLS and defined in our Appendix A, independent

variables are before interest marginal tax rate, expected cost of distress, modified Z-

score, a dummy variable for whether owners’ equity is negative, market to book,

collateral, and firm size. We include industry dummy variables and time period indicators

19

as in GLS. With the exception of collateral, all of the signs on the coefficients on our

explanatory variables are significant in the expected direction. Specifically, we find that

marginal tax rate is negatively related and proxies for distress (expected costs of

bankruptcy, modified Z-score, negative owners’ equity) are positively related to

operating lease activity. We find an insignificant coefficient on collateral, but the

coefficients on market to book and size are significantly negative as expected. Overall,

we find that the GLS leasing model performs as well in our more recent sample period

(1980-2007) as it did in theirs (1981-1992). The explanatory power of the model across

our sample period is 26% compared to 25% in GLS.

Given that this leasing model remains well-specified, we use the error term from

the leasing regression as a proxy for the unspecified benefits from OBS financing not

explained by theoretical leasing determinants. We expect that these benefits are an

important determinant of observed debt levels. Specifically, we expect that observed on-

balance sheet debt ratios should decrease as the benefits from OBS financing increase.

We refer to this error term as ‘abnormal leasing’ (AbOplease) and employ it as an

additional explanatory variable in the capital structure model specified in Lemmon,

Roberts and Zender (2009) in Panel B.30

30 AbOplease remains significant in alternative models of capital structure, including models without the Initial Leverage variable.

We find support for our prediction. We find a

significant negative relation between conventional (book value) debt ratios and

AbOplease, our proxy for benefits from off-balance sheet financing. Consistent with H5,

increased unexplained leasing activity results in lower conventional debt levels.

C. Exploration of potential explanations

20

Given the significant trend in OBS lease financing, which is not confined to retail

and transportation firms and is not explained by financial distress or marginal tax rates,

an obvious question remains: Why are firms doing this? In particular, why should the

upward trend be greatest among firms least financially distressed? We searched for

potential explanations in popular financial press and posed these questions informally to

colleagues and to a handful of practitioners.31

Higher debt ratios are ubiquitously viewed as an indication of higher financial

risk. Simple levered beta calculations clearly suggest that firms with higher debt-to-

equity ratios face higher costs of capital. The first explanation we consider is that firms

intentionally structure leases to qualify for OBS treatment in order to appear more

conservatively financed. This supposes that many investors, resting on the work of

auditors, rely heavily on balance sheets and income statements as reported. Under

current GAAP, non-cancellable operating leases are not recognized in the financial

statements as a liability, however they must be reported in disclosure notes.

A host of potential (non-mutually-

exclusive) explanations strike us as plausible, though none appears sufficiently

compelling on its own. In this section, we consider these explanations for the excess

lease financing (that not explained by theoretical determinants) and attempt to provide

supportive evidence where possible.

(1) Hiding debt (risk) off the balance sheet?

32

31 We spoke informally an off the record to a bond trader, credit ratings analysts, and a Managing Director in private wealth management at a Bulge Bracket investment bank. 32 SFAS No. 13 requires disclosure of future minimum rental payments that are required as of the date of the latest balance sheet presented, in the aggregate and for each of the five succeeding fiscal years. This disclosure is required for all operating leases having noncancelable terms in excess of one year.

The

efficient markets hypothesis suggests that the manner in which information is

21

disseminated should have no effect on the valuation of the firm. However, empirical

research finds that information relegated to disclosure notes (such as OBS leases) is

weighted significantly less heavily than information recognized on balance sheets and

income statements.33

In order to demonstrate the potential impact of non-cancelable OBS lease

obligations on a ubiquitous measure of risk, we estimate levered equity betas that reflect

the full extent of non-cancellable OBS lease commitments and compare them to betas

that reflect only conventional accounting D/E ratios. We estimate (unlevered) asset betas

following the approach specified by Damodaran (2002).

This evidence suggests that the ability to structure leases and keep

disclosure off the balance sheet can lead to more favorable firm valuations.

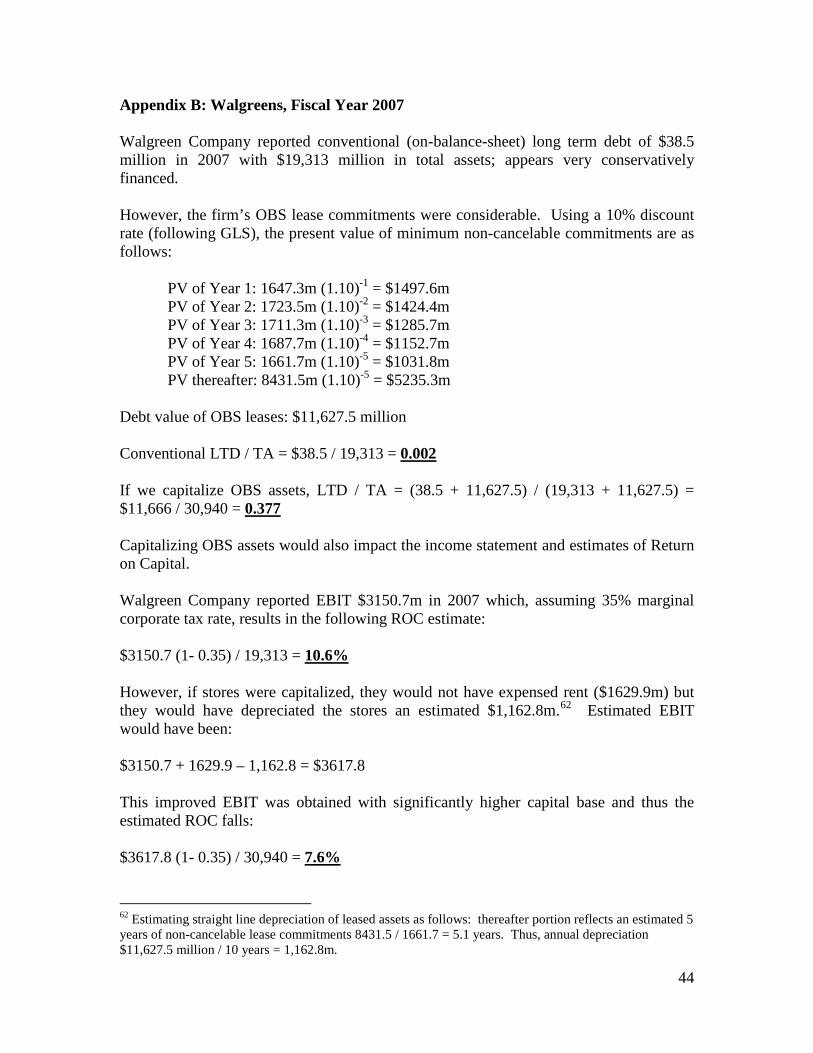

To demonstrate the potential magnitude of the OBS financing, we offer the

example of Walgreen Company in Appendix B. Walgreen’s reported conventional (on-

balance-sheet) long term debt of $38.5 million in 2007 with $19,313 million in total

assets; the firm appears very conservatively financed. However, the firm’s OBS lease

commitments are considerable. We estimate that bringing this debt onto their balance

sheet results in 18,750% increase in their LTD / TA ratio. Before dismissing this as

merely a real estate phenomenon, we refer back to Table 3; this trend in financing assets

off the books is across industries, not confined to retail firms.

34

33 See Ahmed, et. al (2009), Aboody (1996) and Davis-Friday, et. al (1999), Hirshleifer and Teoh (2003), Barth et. al (2003) and Libby, et. al. (2005).. 34 Damodaran (2002) details the process of building forward-looking betas by levering asset betas in “Investment Valuation” second edition, Chapter 8. The process of levering asset betas as opposed to employing regression betas is to overcome the problems of high standard errors and the backward looking aspect (given that firms alter not only their debt ratios but also their asset mixes over time).

Specifically, for firms with

adequate data, we regress monthly stock returns on market returns to attain betas that

22

reflect the equity risk of each firm in the prior five year period.35

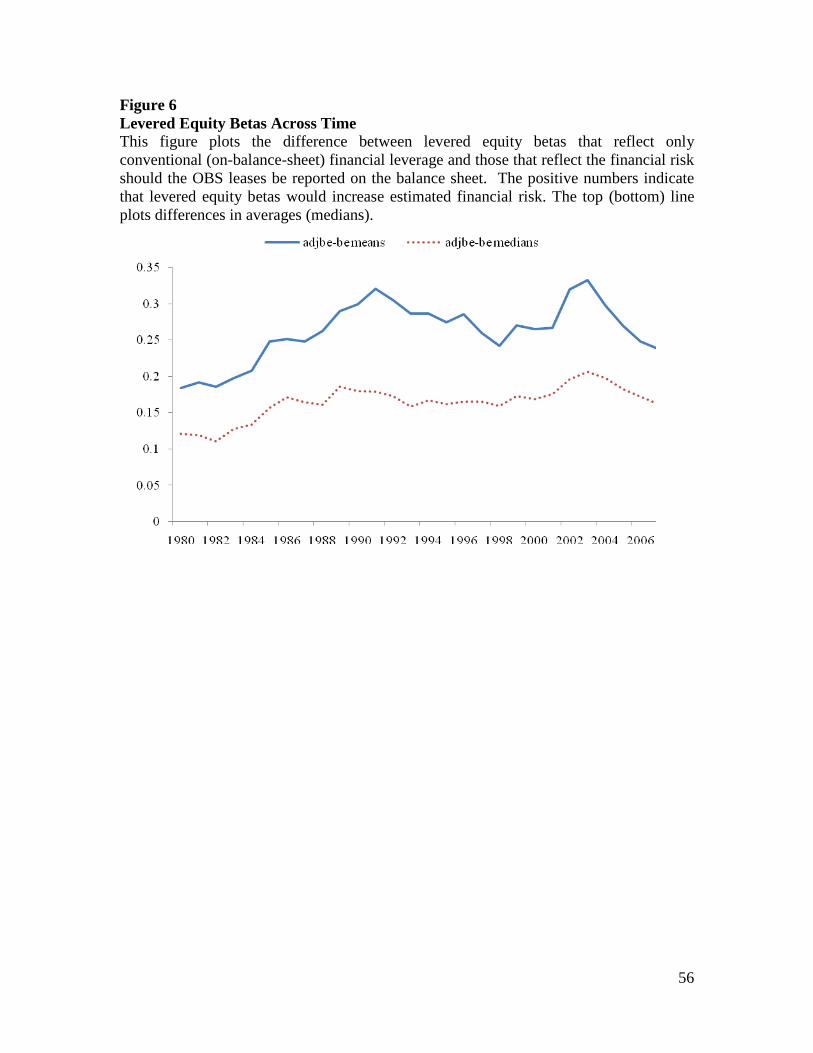

This exercise is not purely academic as FASB and IASB consider bringing all

material, long-term lease obligations onto the balance sheet. Figure 6 plots the difference

between these levered equity betas.

We then unlever each

beta according to its capital structure as follows:

βasset = βequity / (1+(D/E))

Next, we group firms into industries (as per table 2) and employ the average unlevered

beta as an estimate of asset risk typical of the industry. With this estimate of asset risk,

we lever beta for each firm, by industry, in two different ways. First, in accordance with

conventional accounting:

βequity = βasset (1+(D/E))

Thus far, we have estimated asset betas and levered them in accordance with

standard practice, as per Damodaran (2002). We also lever the asset betas using leverage

ratios attained by capitalizing the OBS lease obligations:

βequity = βasset {1+[(D+Oplease)/E]}

36

35 Requiring 60 months of CRSP stock returns reduces our sample size to 11,571 firms. We lose 3.4% of that sample by requiring a positive value of book equity in order to compute meaningful D/E ratios. 36 To the extent that these levered betas differ, and they clearly do, the argument can be made that the asset betas were estimated inaccurately. But our purpose here is not to offer an alternative methodology for computing a more precise forward-looking beta. Rather, our purpose is to demonstrate the impact of capitalizing OBS leases on the D/E ratio in a commonly used application.

The impact of OBS leases on the financial leverage

clearly results in a higher estimate of equity risk. Moreover, this impact increases over

time as the reliance on OBS leases increases (see Figures 6 and 1a). In 1980, the average

levered beta reflecting OBS lease obligations is 0.184 greater than the average levered

23

beta reflecting only conventional balance sheet debt. This difference grows to 0.333 in

2003 and 0.238 by 2007.37

It has been suggested that Qualified Institutional Investors (QIBs) should be more

sophisticated and better able to understand, value and adjust for these obligations.

38,39

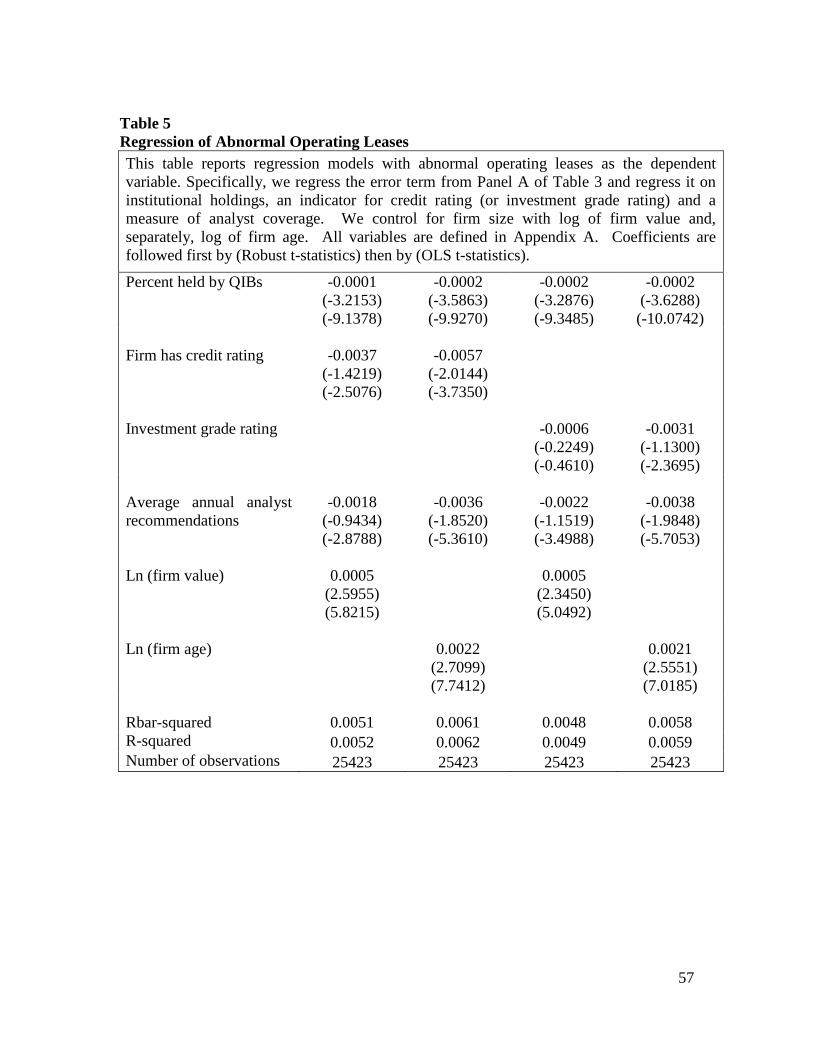

In Table 5, we regress the abnormal OBS lease financing (the error term from the

GLS-based specifications found in Table 4 Panel A) on institutional holdings, an

indicator for credit rating (or, separately, an investment grade rating) and a measure of

analyst coverage. We control for firm size (log of firm value) and, separately, firm age.

One might also expect that credit ratings agencies and analysts covering these firms

should properly adjust for the risk of these off-balance-sheet obligations. However, the

conflicts of interest inherent in credit ratings agencies paid by issuers (and the analysts

employed by issuers’ underwriters) have been well documented.

It is important to note that only 15.5% of our sample has a credit rating from

S&P; (see Table 1). Moreover, while the average firm has 15.8% of its stock held by

QIBs, the median firm has none. Similarly, while the average firm has 1.9 annual analyst

recommendations, the median firm has none. With data on institutional investor holdings,

analyst coverage, and credit ratings, we can examine the extent to which these potential

monitors curtail the practice. But with low representation in our sample, we cannot

conclude that the existence of analysts, credit ratings, and QIBs deter firms in general.

37 Differences in medians are 0.121 in 1980, peaking at 0.207 in 2003 and landing at 0.162 by 2007. 38 SEC Rule 144a establishes the QIBs which are viewed as sufficiently savvy to be exempt from certain SEC protection. For instance, in the “144a market” QIBs are exempt from the two-year holding requirement for privately-placed debt faced by the investing public. Entities investing $100 million or more in unaffiliated issuers qualify. 39 It is worth noting that this expectation was not universal among those we surveyed. A counter argument was made that a typical analyst may be responsible many firms and thus may take balance sheet at face value. It was further suggested that to the extent analysts incorporate the footnote disclosures of these obligations they may at best employ ad hoc adjustments (such as 8x rent expense).

24

These results suggest firms with less institutional ownership and less analyst coverage

use OBS lease financing to a greater extent. Furthermore, though the relationship is less

significant, it appears that the presence of credit ratings is also inversely related to the

extent of OBS lease financing. Because we have controlled for the size and age of the

firm, this result should not merely reflect a sample selection issue.

It is important to note that we cannot bifurcate the sample and claim that firms

with higher levels of institutional ownership do not intentionally structure leases to keep

the debt off the balance sheet, only that they do so to a lesser extent. This leads to our

second potential explanation, which is that institutional investors are not fooled, but

rather are complicit in this practice.

(2) Yield chasing by fund managers?

Many institutional investors (pension fund managers, insurance companies) are

subject to regulatory risk guidelines, yet compensated based on return.40,41 Yield chasing

on the part of regulated fund managers is thought to have contributed to the over-

exposure of such funds to structured finance products (RMBS and CDOs) backed by

subprime mortgages.42

40 Risk guidelines for pension funds are set by the Employee Retirement Income Savings Act (ERISA) and insurance companies face similar guidelines set by state regulators. 41 Mutual funds not subject to the regulatory constraints faced by pension funds and insurance companies are to a lesser extent bound by the risk parameters established by the fund. For example, Fidelity offers a Taxable Bond Fund reported to “invest primarily in higher quality debt securities from government, corporate, and mortgage-backed issuers” and a High Yield Bond Fund reported to “invest in securities from corporations with non-investment-grade credit ratings”. The Taxable Bond Fund manager is presumably not indifferent to returns. 42 See Coval, Jurek, and Stafford (2009) and Kleit and Rodgers (2009).

Without inflated credit ratings, these structured markets are

greatly inhibited given the constraints of regulated bond investors [see Kleit and Rodgers

(2009)]. To the extent that credit ratings agencies do not accurately adjust for the risk

25

inherent in the off balance sheet obligations, similar yield chasing may be at play in the

market for corporate bonds. Fund managers bound by regulation or fund guidelines to

buy only those bonds rated (and perhaps at some arbitrary level) by a Nationally

Recognized Statistical Rating Organization (NRSRO)43 seek to invest in firms with less

obvious risk in order to generate higher returns. Without the credit ratings at or above

some threshold, these regulated institutional investors could not have purchased or held

risky securities.44

43 NRSROs are credit rating agencies whose opinions are relevant for meeting regulatory requirements. Over our sample period Moody’s and S&P were the 800 lb gorillas in this market. 44 According to Michael Lewis, heavily regulated institutional investors were not the only ones relying heavily on the opinions of the NRSROs. The following quote is taken from Liar’s Poker (1989): “Money managers relied on the debt-rating agencies to tell them what was safe (or, rather, to sanction their investments so they did not appear imprudent.) But the rating services, like the commercial banks, relied almost exclusively on the past – corporate balance sheets and track records – in rendering their opinions. The outcome of the analysis as determined by the procedure rather than by the analyst. This was a poor way to evaluate any enterprise, be it new and small, or old, large and shaky.”

It is important, therefore to examine the treatment of operating leases

by the credit rating agencies.

We consider here the approaches employed by Moody’s Investors Service and by

Standard & Poors. Rather than discount actual non-cancellable lease commitments,

Moody’s advocates multiples of operating lease (rent) expense to estimate the value of

operating leases [Moody’s (1999)]. One problem with this approach is that only existing

signed commitments are non-cancellable and thus analogous to debt. The use of

multiples assumes leases are perpetually renewed. This may be the case in general, but

until obligations are signed, firms have the option should they face unexpected changes in

market conditions. Moody’s methodology, though easy to understand, simple to compute,

and likely accurate on average, is also likely to over-estimate the obligations of firms that

ultimately face distress.

26

Standard & Poor’s, on the other hand, does take care to value actual non-

cancellable lease commitments. However, S&P discounts future commitments at firm-

specific rates intended to reflect firm-specific cost of on-balance-sheet debt.45

Specifically, S&P compute a firm-specific discount rate as Interest Expense divided by

Average Conventional Debt, using data from the most recent annual report. Thus, firms

with high conventional debt ratios are perversely given the benefit of higher discount

rates. This approach systematically under-states the extent of off-balance-sheet leasing

for firms with higher conventional debt relative to firms with lower conventional debt.46

There may be an income statement motivation beyond any balance sheet

motivation. Firms generating income with assets they do not technically own may

improve asset utilization measures.

This disproportionately under-penalizes firms with both on-balance-sheet and off-balance

debt. In a cross-sectional regression, this induces a spurious negative relationship

between conventional debt and the propensity to lease (via the operating lease structure).

(3) Asset utilization?

47 Firms may not just be removing debt from the

balance sheet, but removing assets in order to improve their income as a percentage of

assets.48

45 Standard & Poor’s (2006). 46 Consider, for example, two firms with the same assets – both on and off the books. Assume Firm A employs 50% debt and 50% equity financing for their on-balance sheet assets while Firm B uses 100% equity financing. S&P will employ a much higher discount rate (leading to a lower valuation) when valuing the OBS debt in Firm A relative to Firm B which has signed the same lease contracts for the same OBS assets. 47 Operations management defines and measures asset utilization in terms of production output and total capacity; Ellis (1998). However, financial managers and analysts are likely more concerned with generating revenues and maximizing profitability than with fully utilizing capacity.

As the case of Walgreens (detailed in Appendix B) demonstrates, the affect on

27

ROC when assets are removed from the balance sheet can be material. Assuming straight

line depreciation over the term of the lease, Walgreens’ ROC would have fallen 7.6% in

fiscal 2007 if the leased assets had been capitalized.49

In Figure 7, we estimate the impact on ROC for our entire sample of firms and

demonstrate the impact separately for firms with positive and firms with negative

earnings in order to show a leverage effect. Specifically, we first divide the sample into

quintiles based on relative reliance on OBS leases. For each Oplease/assets quintile, we

compute the difference between Return on Capital (ROC) under conventional accounting

and ROC estimates after bringing OBS leases onto the balance sheet, then scale the

difference by total assets.

50 As demonstrated in the Walgreens anecdote, capitalizing

OBS leases impacts the income statement as well as the balance sheet. We follow the

EBIT and ROC estimation detailed in Appendix B.51

The estimated ROC improvement from moving assets off the balance sheet is

found among profitable firms. This evidence is interesting given earlier (Figure 2)

evidence that the upward trend in OBS leasing is not attributable to an upward trend in

48 While the effect OBS leasing on debt ratios is always the same directionally, the affect on income is somewhat ambiguous There are competing effects of operating leases on income: rent expense lowers income, but income is raised due to forgone interest payments and asset depreciation. While the net effect on income varies by depreciation schedule and such, ROC is likely increased as the denominator shrinks when assets are OBS. In fact, Ross, Westerfield, Jaffe, 1993, state on page 694 “We indicated that a firm desiring to project a strong balance sheet might select an operating lease. In addition, the firm’s ROA is generally higher with an operating lease than with either a capitalized lease or a purchase.”

49 It is important to note that this trend in OBS leasing is not confined to retail firms such as Walgreens leasing real estate or to transportation firms leasing trucking fleets or aircraft. Table 3 indicates that this trend is significant across industries. 50 Plots of unscaled differences in ROC appear the same but on a different scale.

51 Some caveats regarding these figures. First, we rely on the marginal tax rates (obtained from John Graham) that estimate taxes under conventional accounting. The evidence in GLS suggests a relationship between leasing and taxes that may result in higher marginal tax rates if OBS leases were capitalized. Second, our estimated straight line depreciation imperfectly reflects the Modified Accelerated Cost Recover System (MACRS) depreciation of these (unobservable) assets. If these OBS assets were on the balance sheet, depreciation would likely be higher in earlier years and decline over time. However, higher depreciation in early years would depress ROC even more than our estimate suggests.

28

financial distress, but rather is found among firms least likely to be bankrupt. Firms with

highest Oplease relative to on-balance-sheet assets appear to perform especially well in

terms of ROC when earnings are positive, but appear to perform poorly if earnings go

negative. It appears that moving assets off the balance sheet is a leverage tradeoff for this

common measure of asset utilization. By moving debt off the balance sheet, ROC is

higher in good times but this strategy is risky since in bad times this behavior inflates the

negative ROC.

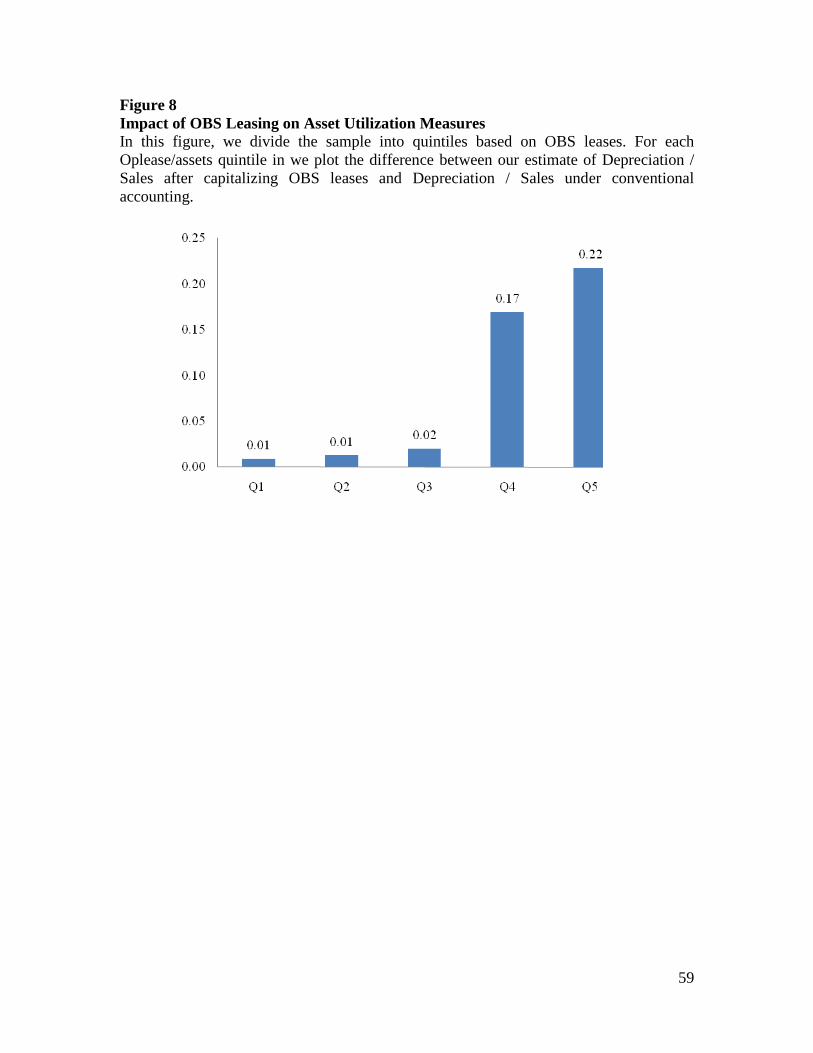

While ROC measures how effectively management utilizes its assets to create

income, analysts interested in ‘asset utilization’ also measure the percentage of sales

needed to cover wear and tear of assets (Depreciation / Sales). For each Oplease/assets

quintile in Figure 8, we plot the difference between our estimate of Depreciation / Sales

after capitalizing OBS leases and Depreciation / Sales under conventional accounting.

Clearly this ratio increases by moving assets off the balance sheet. The average change

in this ratio is 9% for the entire sample, but average difference among the quintile of

firms with greatest relative OBS leases is over 20%.

(4) Risk management?

Consider the risk management arguments for the use of project finance. Project

finance is often preferable to corporate finance in cases such as the B.P. Amoco

investment in the Azerbaijan oil fields.52

52 Esty and Kane (2003a and 2003b) explain this case in greater detail.

Faced with the risk of expropriation by host

governments, entrepreneurial host country criminals, financial distress by foreign

partners (Lokoil), and uncertainty regarding pipelines, firms such as B.P. are willing to

pay higher interest rates to borrow money from host country banks whose only recourse

29

is the assets in the host country.53

Heretofore, we have discussed the lease versus buy decision (and the choice to

structure leases to qualify for OBS financing) as a choice made by borrowing firms.

However, the driving motivation may belong instead to the suppliers of capital. Lenders

may prefer to retain ownership of the asset for multiple reasons including the tax benefit

of depreciation and less risk of loss in the case of bankruptcy. In this case, lenders

(lessors) may offer more attractive operating lease terms than capital lease terms (or

traditional debt financing). We include in our regression models the marginal tax rate of

the borrowing firm, but the (unobservable) marginal tax rate of the lender (lessor) is also

important. Moreover, while the case of Eastern Airlines may not signal a regime shift in

Title 11 interpretation, it clearly demonstrates an incentive for creditors to retain control

of their collateral.

This risk containment rationale may extend to

investments in markets (product or geographic) that are unknown to a particular firm.

Should such investment underperform expectations, leased assets have an embedded put

option that can be exercised without risking the balance sheet assets. Because the lessor

can only repossess the leased asset in the case of default, one motivation for lease

financing may be akin to project finance motives: risk isolation.

(5) A supply story, not a demand story?

54

53 The quasi-governmental lenders such as IFC and World Bank also play an important role in such international investments. But the risk containment to the project may be compelling even in high risk domestic investments. 54 See Weiss and Wruck (1998).

To the extent that maintaining ownership of the asset (through

operating leases) mitigates this risk, the preference for keeping assets off the borrowing

firms’ balance sheets may stem from the financier.

30

Finally, with respect to suppliers of capital, we note that Wall Street was seeking

new sources of marginal financing over this period. Consider, for example, the explosion

in structured finance markets that maps well to our latter sample period market by the

increase in OBS leasing. Our trend in lease financing may be supply-side innovation

more than concern by borrowers about their balance sheets. This is consistent with our

results suggesting that the increase in operating leases is in addition to (not merely in lieu

of) on-balance-sheet debt financing.

The following quote explains the OBS innovation in response to a regulatory

constraint faced by a particular sector.

The Mortgage trading desk evolved from corner shop to supermarket. By increasing the number of products, they increased the number of shoppers. The biggest shoppers, the thrifts, often had a very particular need. They wanted to grow beyond the limits imposed by the Federal Home Loan Bank Board in Washington. It was a constant struggle to stay one step ahead of thrift regulators in Washington. Many “new products” invented by Salomon Brothers were outside the rules of the regulatory game; they were not required to be listed on thrift balance sheets and therefore offered a way for thrifts to grow. In some cases, the sole virtue of a new product was in its classification as “off-balance sheet”.55

Leases financing has long been offered by commercial banks and equipment

manufacturers interested in increasing revenues from marginal customers who may

This motivation cannot cleanly be extrapolated to industrials, but demonstrates the

industry- and perhaps firm-specific benefits to OBS lease financing captured in the error

term in Table 4 Panel A.

D. Who are the lessors?

55 Quote taken form “Liar’s Poker” by Michael Lewis (1989), page 138-9.

31

otherwise lack the requisite capital for a traditional (debt- or equity-financed) purchase.

It appears that much of the increase in OBS leasing is attributable to growth in third-party

lessors. Firms like AerCap Holding N.V. (AER) and Aircastle Ltd (AYR) both of which

lease (but do not manufacture) aircraft to U.S airlines have seen remarkable growth over

the latter part of our sample period.56,57

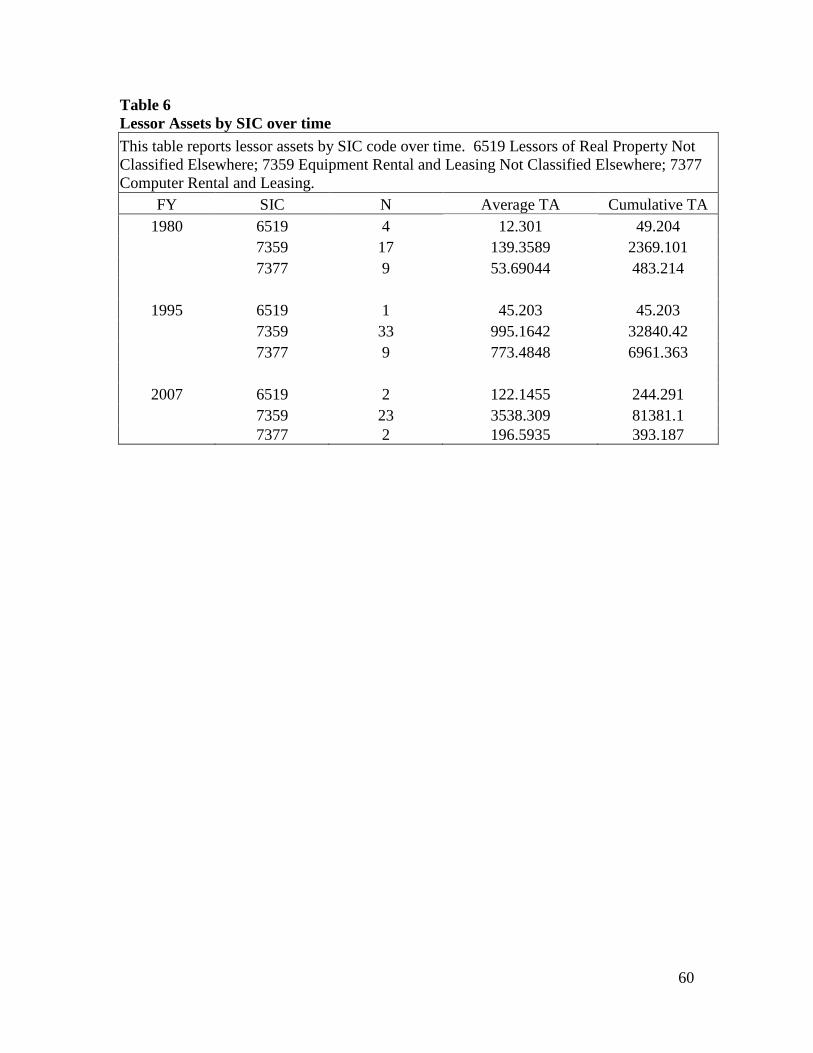

In order to demonstrate growth in the leasing industry from the lessor perspective,

we report in Table 6 lessors by SIC along with their total assets at three points in time:

fiscal years 1980, 1995, 2007.

Indeed, the largest aircraft lessor, International

Lease Finance Corp (ILFC), is a third-party lessor rather than a manufacturer.

58

This is the first of two caveats regarding these data. Because the largest lessors

are either subsidiaries of larger firms in broader industries (including GE Capital

Tejon Ranch Compnay (NYSE: TRC), which leases

farmland and oil fields, is represented in SIC 6519 in all three years reported. Total

assets for Tejon are $29,826,000 in 1980, $45,203,000 in 1995 and $175,503,000 in

2007. Cumulative (average) total assets in SIC 7359, which contains AerCap Holding

(AER) and Aircastle Ltd (AYR) mentioned above, increased from $2,369,101,000

($139,358,900) in 1980 to $81,381,100,000 ($3,538,309,000) in 2007. Growth in SIC

7377 appears to have peaked in the 1990s and waned since. However, negative growth in

SIC 7377 (computer rentals and leasing) may be misleading as this SIC does not include

the largest computer lessors, such as IBM.

56 AerCap Holding fleet includes models from Airbus, Boeing, and McDonnell-Douglas. Aircastle's aircraft portfolio consists of 130 passenger and freighter aircraft leased to 58 lessees located in 32 countries. 57 Market capitalization (from CRSP) for AER increased from $15,415,000 to $255,961,000 over the period January 1980 through December 2008. AYR was not listed on CRSP until late 2006 with December 2008 market cap $375,813,200. 58 Additional SIC codes pertaining to leasing are found at OSHA.gov. Those tabulated are those containing firms covered by Compustat. We discarded SIC 6794 “Patent Owners and Lessors” which are firms leasing franchises such as Choice Hotels and Dunkin Donuts.

32

Aviation Services, Textron, Deere, IBM, etc.) or are not publicly traded (International

Lease Finance Corp) the data reported in Table 6 severely underestimate the magnitude

of the leasing industry. Additionally, some firms represented in these data are likely

leasing on a smaller scale to consumers rather than corporations.59

The models of GLS examine the lease versus buy decision with separate models

of operating leases, capital leases, and conventional debt, each scaled by total firm value.

Here, we are especially interested in the mix of off- and on-balance sheet debt and thus

construct models of OBS leases scaled by balance sheet debt. These regression models

are reported in Table 7. Independent variables include lessee marginal tax rate, an

estimate of collateral value (of on-balance-sheet assets), Z-Score, market-to-book (proxy

for growth opportunities), investment in R&D (proxies for intangible assets and growth),

firm size (or firm age), indicator variables for retail and transportation firms, and a

dummy variable for the period 1996-2007 (motivated by Figure1a). As expected, lessee

marginal tax rate is negatively related to the propensity to lease assets. Lessees unable to

Thus, we cannot

make strong claims based on these data, but the growth seen here is consistent with

growth in third-party leasing companies such as AER, AYR and ILFC.

E. Modeling the mix of On- and Off-balance sheet debt

Figure 1 and Table 2 suggest that OBS lease financing appears not only to replace

capital leases (as firms intentionally structure contracts to meet GAAP requirements) but

also reflects a significant increase in debt. In this subsection, we consider the choice to

finance assets off the balance sheet.

59 For example, SIC code 7359 contains Rent-A-Center as well as AT&T Capital, AER and AYR.

33

fully utilize interest and depreciation tax shields transfer them to lessors facing higher

marginal tax rates, who can in turn offer a lower cost of financing.

Fixed assets of general usage lend themselves better to lease financing than more

specialized assets with fewer alternative uses. For firms without access to capital markets,

specialized assets may be financed with capital (rent to own) leases on the balance sheet,

but unlikely structured as operating leases since the assets have less marketable value to

the lessor (unless the motivation is keeping debt off the balance sheet). So, the negative

relationship between our estimate of collateral value (of on-balance-sheet assets) and the

use of OBS leases is unexpected. Our measure of asset tangibility (employed in two

models) is also significantly negative. We note that the observed collateral value

(tangibility) of ON-balance-sheet assets at best imperfectly indicates the (unobserved)

collateral value of OBS assets. However, we cannot conclude that OBS lease financing is

contained to firms marked by more general assets. Firms with more specialized assets are

clearly using OBS leases. This interpretation is supported further by the significant

positive coefficient on R&D (intangible off-balance-sheet assets).

Theory predicts a positive relationship between financial distress and OBS leasing

activity. The “lender of last resort” argument stems from the priority of lessors’ claims in

bankruptcy proceedings and this relation is thus likely to be strongest for leases classified

as operating leases that ostensibly never intend to transfer ownership. This is consistent

with the positive relationship between OBS lease financing and Z-Score.

Drawing on the underinvestment problem associated with fixed-cost financing

(see Myers, (1977)) GLS suggest that firms with more growth options in their investment

opportunity sets should have a lower proportion of fixed claims in their capital structure.

34

Consistent with this, GLS report significantly negative coefficients on MTB in

regressions of debt-to-value, capital leases-to-value, and operating leases-to-value.

However, Stulz and Johnson (1985) suggest that the ability to finance new investment

with higher priority claims (including leases) can alleviate this underinvestment problem.

That is, while OBS leases are indeed fixed claims, their higher priority claim changes

their impact on investment.

Motivated in part by Stulz and Johnson and in part by the “risk management”

rationale advanced in the section above, we posit that leasing assets off the balance sheet

offers an attractive compromise between conventional debt and equity for firms with

higher growth options. Growth options are riskier than assets in place. The ability to

contain risk by leasing assets may allow funding marginal projects. So, while GLS

document negative relationships between growth options and the lease-to-value ratio

(which reflects a fixed costs as a percentage of firm value) we expect to find a positive

relation between growth options and the ratio of OBS leases to on-balance sheet debt

(which reflects fixed costs off- and on- balance sheet). In Table 7 we document a

significantly positive relationship between OBS financing and conventional proxies for

growth opportunities, R&D (scaled by total sales) and the Market-to-Book ratio (defined

as per GLS in Appendix A). These results are consistent with those reported in Figure 5.

Our control for firm size is negatively related to the proportion of debt moved off

the balance sheet (significant in most models). This may be mechanical: observable firm

size is greater when assets are kept on the balance sheet.60

60 This negative relationship holds when firm size is gauged with market values as well as book values. The extent to which the market incorporates these assets is unclear; see sections V.C.1 and V.C.2 above.

However, models employing

35

firm age rather than firm size also find that more mature firms have a smaller proportion

of debt off their balance sheets.

Finally, we obtain the positive coefficients expected in two indicator variables.

Retail firms have a significantly higher proportion of debt kept off the balance sheet

(reflecting the lease financing of their real estate). However, transportation firms (which

also have highly generalized assets) are not significantly different. As the results in

Figure 1a and Table 2 suggest, the dummy variable for the period 1996-2007 indicates a

significantly greater propensity to lease OBS in this latter part of the sample.

VI. Conclusion

Given the imperfect and inconsistent treatment of operating (OBS) lease financing

by credit rating agencies, perhaps it is not surprising that regulators and popular financial

press contend that firms intentionally structure leases to qualify for OBS accounting

treatment in order to hide non-cancellable commitments.

We document remarkable trends: mean OBS leases (as a percentage of total debt)

increases 745% from 1980 to 2007, while capital leases to total debt decreases 49.8%.

We also find that the benefit of the OBS accounting treatment of lease financing is a

significant determinant of corporate capital structure: as excess OBS leasing increases,

conventional debt ratios fall. This substitution notwithstanding, we find that the increase

in OBS leases is largely in addition to, not in lieu of, on-balance-sheet debt. This

marginal source of financing has increased financial risk across time. If leased assets

were brought onto the balance sheet average debt-to-capital ratios would move from 20%

ballpark to 30-35% over our 1980-2007 sample.

36

This evidence from our trend analysis is time series. However, our potential

explanations are largely cross-sectional. We cannot identify any one fully explanatory

catalyst to this change in corporate behavior, but the fact remains that the trend is

material and consequential. Because OBS leases are long-term, non-cancelable

obligations (i.e., debt), risk metrics such as conventional debt and coverage ratios,

conventional levered equity betas, and Adjusted O- and Z-Scores (which ignore OBS

obligations) no longer fully capture financial risk.

Our results should be of interest to a host of market participants as the US

considers changes in the OBS accounting treatment of lease financing. Our results

suggest that benefits from the OBS treatment influence corporate decision-making and

provides some support for these proposed changes. However, to the extent that theoretical

determinants of leasing maintain explanatory power, a rule that requires capitalizing all

operating leases may not be appropriate. We offer a similar caution to information

intermediaries that apply “one-size-fits-all” adjustments for operating leases.

37

References

Aboody, D., 1996, Recognition versus disclosure in the oil and gas industry. Journal of Accounting Research 34 (supplement) 21-32.

Ahmed, Anwer S., Emre Kilic and Gerald J. Lobo, 2009, Does recognition versus

disclosure matter? Evidence from value-relevance of banks’ recognized and disclosed derivative financial instruments, The Accounting Review (forthcoming)

Altamuro, Jennifer, Rick Johnston, Shail Pandit, and Haiwen Zhang. 2008. Operating

leases and credit assessments. The Ohio State University, working paper. Baker, M., and J. Wurgler, 2002, Market timing and capital structure, Journal of Finance

57, 1-32. Barry, C.B., S.C. Mann, V.T Mihov, and M. Rodriguez, “Corporate Debt Issuance and

the Historical Level of Interest Rates” Financial Management 37, 413-430. Barth, Mary, G. J. Clinch, and T. Shibano. 2003. Market effects of recognition and

disclosure. Journal of Accounting Research 41 (September) 581-609. Beattie, V., K. Edwards, A. Goodacre. 1998. The impact of constructive operating lease

capitalization on key accounting ratios. Accounting and Business Research (Autumn): 233-254.