capital watch june 2014

TRANSCRIPT

WORLD IN PERSPECTIVE PG 2

POTENTIAL RISKS PG 2

US UPDATE PG 3

IN T

HIS

ISSU

E

In our May issue, we highlighted our continued optimism on the global market for the long term while expecting a mild correction in the short term. Our opinion remains unchanged. Most major markets are trading at their respective resistance levels. In particular, Asian markets are range bound. Any major pullback should present a good opportunity for investors to increase their allocation to equities. Many economies are still facing various challenges. Thailand is in political turmoil. Russia is still at loggerhead with US and EU. Why are we still optimistic? The reality is that crisis breeds opportunity and investors are always on a lookout to take advantage of oversold markets to capture returns. In the long term, one’s investment decision should be based on some fundamentals such as valuation, cost of money (interest rate policy), easy access to money (liquidity), opportunity cost, productivity and the law of supply and demand. Let us touch on a few of these factors. The return on deposits is unlikely to outpace inflation for many years to come. In a low interest rate environment, investors will have to deploy their money into investments to keep up with inflation. This push factor will provide a strong support for the equity, bond and property markets. However, where the money eventually flows to depends on where investors see value and potential. For example, Japan was one of the

best performing market last year because investors saw a change in government policy to boost growth through money printing and inflationary policies. Another strong factor that will increase demand is the world population growth. Every month, the world population increases by approximately 6 million people. Imagine the impact on consumption from this factor alone!

In general, when demand is greater than supply, prices go up. Therefore, in the long run, money must be invested. The stock market should appreciate over an extended period of time. Across the U.S., Europe and Japan (Developed Markets), economic conditions continue to improve. Emerging Markets currently offer good value. Their respective governments have embarked on fundamental economic reforms, but these measures will take time to gain traction and for investors to be convinced. Historically, emerging market gains have outstripped those in developed markets. Asian markets offer the best value globally. GDP growth forecasts are positive, unemployment is low and inflation is healthy. The famed U.S investor Warren Buffett once exhorted fellow investors to “Always invest for the long term. In this spirit, I would like to encourage you to do the same by focusing on the fundamentals and retaining a long-term view of your investments.

UK & EUROPE UPDATE PG 4

ASIA AND EMERGING MARKETS UPDATE PG 5

ISSUE 66 | JUN 2014

Albert LamInvestment DirectorIPP Financial Advisers Pte Ltd

Important Notice: This publication is for information, without any regard to your specific investment objectives, financial situation or particular needs. You should read the prospectuses, annual reports and factsheets that are available from respective product providers or its distributors, before deciding whether to subscribe or purchase units of the Fund. The value of units in the Fund and the income accruing to the units, if any, may fall or rise dramatically. Past performance of the Fund and any economic or market predictions, projections or forecasts are not necessarily indicative of future or likely performance. Any opinion or view presented here is subject to change without notice. IPP Financial Advisers shall not be liable for any losses or damages of any kind howsoever arising from you acting on any information herein. You may wish to seek advice from a financial adviser before making a commitment to purchase the Fund. In the event that you choose not to seek advice from a financial adviser, you should consider whether the Fund is suitable for you. This publication is the property of IPP Financial Advisers, and no reproduction and / or circulation of this publication, whether in parts of in its entirety is allowed.

Since the annexation of Ukraine in the first quarter of the year, Russian president Vladimir Putin has sent conflicting signals about his intentions.

On 19 May, he ordered Russian troops near the Ukrainian bases to return to their bases. In addition, he also expressed support for increased dialogue between Kiev and the separatists in the Eastern regions. While Putin seems to have mellowed in recent days, it is too early to tell if his passive stance is of a permanent nature. Investors should continue to pay attention to news flow emanating from the region.

POTENTIAL RISKS

JUN 20142

WORLD IN PERSPECTIVE

IS RUSSIA STEPPING BACK?

MERS: THE NEXT PANDEMIC CRISIS?

A new virus strain from Saudi Arabia baptised Mers, or the Middle East Respiratory Virus, looks set to pose a new challenge to healthcare systems worldwide. In the U.S, a third potential case of the virus was uncovered in mid-May. To date, the virus has infected more than 500 individuals in Saudi Arabia alone, and signs that the virus is spreading to other countries highlight the potential for the situation to develop into a global pandemic. The World Health Organisation has convened an emergency meeting to discuss the matter.

IPPFA'S OUTLOOK.

• The Fed currently repurchases $45 billion worth of se-curities each month and expects to reduce the figure to zero by the end of the year. In an earlier policy address, Fed chairperson Janet Yellen said that the U.S economy was “on track” but sounded a cautious note on the state of the housing market. U.S Non-Farm payrolls data in May came in at 192K, below the consensus estimate of 200K. The unemployment rate came in at 6.7%, slightly higher than the estimated rate of 6.6% but unchanged relative to the previous month. While the reduction in the scale of Quantitative Easing has been priced into the market to some degree, investors need to remain vigi-lant about a rate hike occurring earlier than expected.

• On 13 May, the S&P 500 index attained a historic high of 1,900 even as major European indices reached six-year highs. The German DAX traded at the 9,700 level while the U.K FTSE reached a 14-year high to trade at 6,873.08. The VIX, a major volatility index, floated near its one-year low and was quoted at 12.13 at the close on 13 May. The VIX measures implied volatility in S&P index options and a lower value indicates that investors do not expect significant near term volatil-ity. As the VIX is currently trading below its histori-cal average of 19, we see significant downside risks for investors currently long developed market equities.

• The month of May saw Vietnam and regional power-house China clash over competing claims in the South China sea. Since 3 May, Vietnamese ships have repeat-edly clashed with their Chinese counterparts. Each side has accused the other of using water cannons, low level aircraft and even ramming tactics to intimi-date its respective vessels. Both China and Vietnam claim the Paracel islands and various swaths of the South China Sea. On 11 May, violent protests broke out in parts of the country in which many factories run by Chinese, Taiwanese and Singaporean compa-nies were attacked. The Vietnamese government has since moved swiftly to quell the protests by announc-ing that protesters would be prosecuted. The govern-ment has also increased the level of security around the Chinese embassy. Even though there is now some semblance of calm, it is possible that further action by China to reassert its claims would worsen the conflict.

• An inconspicuous development in small-cap equities may give some clues about the future of global equities. From 13 May to 15 May, the Russell 2000 index lost 3.3% of its value. On 16 May, the same index briefly fell be-low 10% from a March high. Coupled with the recent sell down of overvalued technology counters, it is pos-sible that the lack of strength in small-cap equities may portend future near-term weakness in global equities.

In the past month, apart from the ferry disaster in South Korea and the Vietnamese riots, the month of May was largely uneventful. There was a mild sell down of small caps in the US but the major markets moved up 1-4%. The Dow rose 1.4% while NASDAQ rebounded up 4%. In major Asian markets, Hang Seng was the best performer, rising 4.3%. STI rose 1.1%.

Looking ahead, we will be transitioning to the summer season and we are confronted with the old saying of ‘sell in May and go away’. While the stock market has yet to show any sign of weakness, in the short term, we want to take risk off the table. We are unclear of the direction of the market in the next month as upward pressure of positive economic news are somewhat negated by short time overbought sentiments. We are in the opinion that the market needs to take a breather before continuing its long term upward movement. We will reassess the direction of the market at end June.

JUN 20143

U.S Non-Farm Payrolls: 288K versus the 210K esti-mate U.S unemployment rate de-clines from 6.7% to 6.3%

MAY 2014

• U.S Non-Farm payrolls came in ahead of expectations. The key metric was reported at 288K, versus the consensus estimate of 210K and well ahead of the previous reading of 203K.

• The U.S ISM Manufacturing PMI index came in at 54.9 versus the expected reading of 54.3. A reading above 50 indicates that the economy is in expansion.

• The unemployment rate for the world's largest economy came in at 6.3%, compared to the expected rate of 6.6% In the previous month, unemployment was tagged at 6.7%.

US ISM Manufacturing PMI (Apr) 54.9 54.3

US Nonfarm Payrolls (Apr) 288K 210K

US Unemployment Rate (Apr) 6.3% 6.6%

US Consumer Price Index (MoM) (Apr) 0.3% 0.3%

US Consumer Price Index (YoY) (Apr) 2.0% 2.0%

US Consumer Price Index Ex Food & Energy (MoM) (Apr) 0.2% 0.1%

US Consumer Price Index Ex Food & Energy (YoY) (Apr) 1.8% 1.7%

US Personal Spending (Mar) 0.9% 0.6%

US Markit Manufacturing PMI (Apr) 55.4 55.8

US Average Hourly Earnings (MoM) (Apr) 0.0% 0.2%

Our opinion on the US: In the long term, we are neutral on this market as the huge run-up has surpressed the possibility of supernormal gains going forward

Data source: FXStreet Economic Calendar

USECONOMICSNAPSHOT

May YTD

S&P 500 1.61% 4.20%

Dow Jones 0.78% 1.36%

NASDAQ 2.54% 1.69%

KEY ECONOMIC DATA POINTS ACTUAL EXPECTED

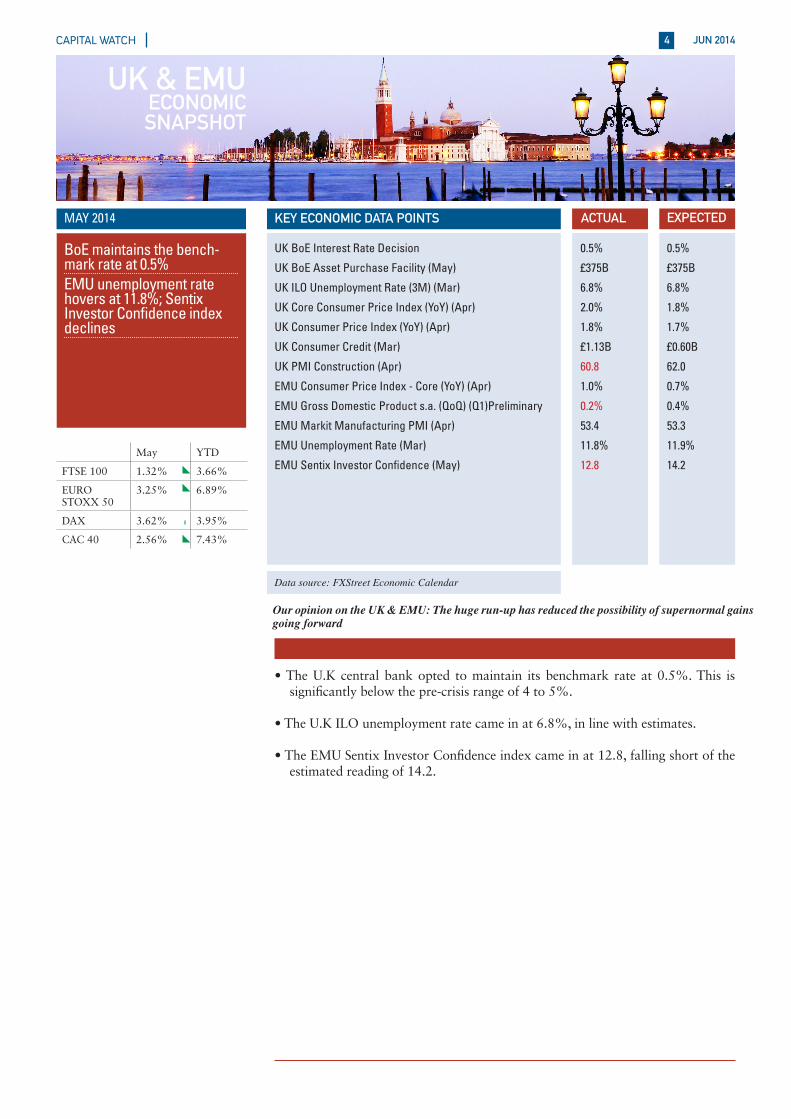

BoE maintains the bench-mark rate at 0.5% EMU unemployment rate hovers at 11.8%; Sentix Investor Confidence index declines

MAY 2014

• The U.K central bank opted to maintain its benchmark rate at 0.5%. This is significantly below the pre-crisis range of 4 to 5%.

• The U.K ILO unemployment rate came in at 6.8%, in line with estimates.

• The EMU Sentix Investor Confidence index came in at 12.8, falling short of the estimated reading of 14.2.

UK BoE Interest Rate Decision 0.5% 0.5%

UK BoE Asset Purchase Facility (May) £375B £375B

UK ILO Unemployment Rate (3M) (Mar) 6.8% 6.8%

UK Core Consumer Price Index (YoY) (Apr) 2.0% 1.8%

UK Consumer Price Index (YoY) (Apr) 1.8% 1.7%

UK Consumer Credit (Mar) £1.13B £0.60B

UK PMI Construction (Apr) 60.8 62.0

EMU Consumer Price Index - Core (YoY) (Apr) 1.0% 0.7%

EMU Gross Domestic Product s.a. (QoQ) (Q1)Preliminary 0.2% 0.4%

EMU Markit Manufacturing PMI (Apr) 53.4 53.3

EMU Unemployment Rate (Mar) 11.8% 11.9%

EMU Sentix Investor Confidence (May) 12.8 14.2

Our opinion on the UK & EMU: The huge run-up has reduced the possibility of supernormal gains going forward

Data source: FXStreet Economic Calendar

UK & EMUECONOMICSNAPSHOT

JUN 20144

May YTD

FTSE 100 1.32% 3.66%

EURO STOXX 50

3.25% 6.89%

DAX 3.62% 3.95%

CAC 40 2.56% 7.43%

KEY ECONOMIC DATA POINTS ACTUAL EXPECTED

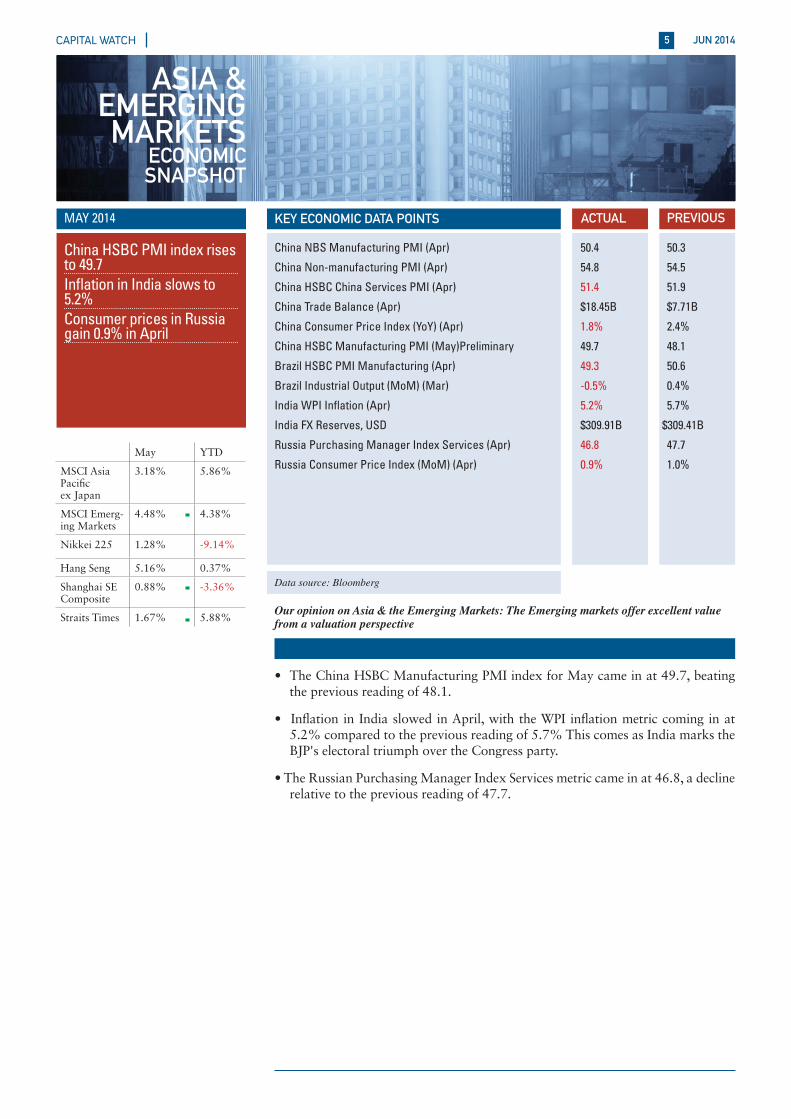

China HSBC PMI index rises to 49.7Inflation in India slows to 5.2%Consumer prices in Russia gain 0.9% in April

MAY 2014

• The China HSBC Manufacturing PMI index for May came in at 49.7, beating the previous reading of 48.1.

• Inflation in India slowed in April, with the WPI inflation metric coming in at 5.2% compared to the previous reading of 5.7% This comes as India marks the BJP's electoral triumph over the Congress party.

• The Russian Purchasing Manager Index Services metric came in at 46.8, a decline relative to the previous reading of 47.7.

China NBS Manufacturing PMI (Apr) 50.4 50.3

China Non-manufacturing PMI (Apr) 54.8 54.5

China HSBC China Services PMI (Apr) 51.4 51.9

China Trade Balance (Apr) $18.45B $7.71B

China Consumer Price Index (YoY) (Apr) 1.8% 2.4%

China HSBC Manufacturing PMI (May)Preliminary 49.7 48.1

Brazil HSBC PMI Manufacturing (Apr) 49.3 50.6

Brazil Industrial Output (MoM) (Mar) -0.5% 0.4%

India WPI Inflation (Apr) 5.2% 5.7%

India FX Reserves, USD $309.91B $309.41B

Russia Purchasing Manager Index Services (Apr) 46.8 47.7

Russia Consumer Price Index (MoM) (Apr) 0.9% 1.0%

Our opinion on Asia & the Emerging Markets: The Emerging markets offer excellent value from a valuation perspective

Data source: Bloomberg

ASIA & EMERGING MARKETS

ECONOMICSNAPSHOT

JUN 20145

May YTD

MSCI Asia Pacificex Japan

3.18% 5.86%

MSCI Emerg-ing Markets

4.48% 4.38%

Nikkei 225 1.28% -9.14%

Hang Seng 5.16% 0.37%

Shanghai SE Composite

0.88% -3.36%

Straits Times 1.67% 5.88%

KEY ECONOMIC DATA POINTS ACTUAL PREVIOUS