carolina banker win1718 - amazon web services

TRANSCRIPT

WIN

TER 2

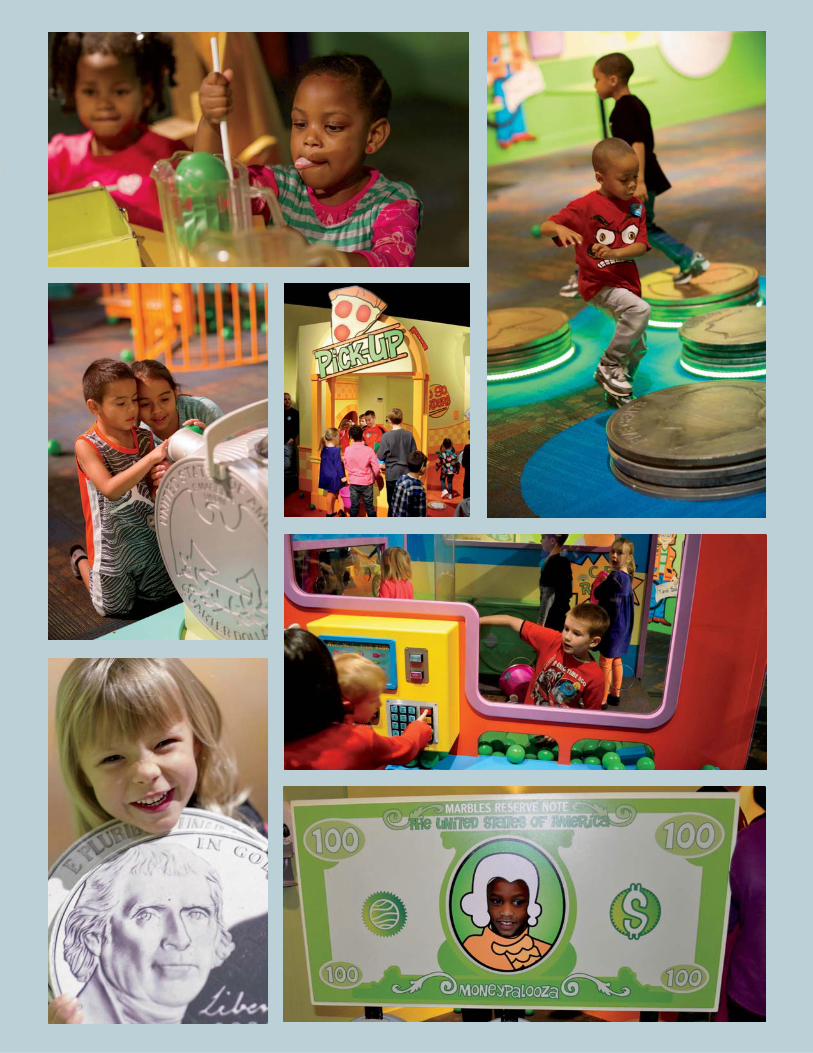

MoneypaloozaPlay-Based Financial Literacy Education

Carolina Banker | Winter 2017 3

Financial institutions of all sizes rely on Harland Clarke for best-in-class services and high-performing solutions that deliver exceptional ROI. Whether you’re looking for integrated payment, marketing or security solutions, we have more than a century of experience helping clients reach their goals. When it comes to results, it takes more than a lucky streak to determine success.

harlandclarke.com

When your results exceed expectations,

it’s not luck. It’s Harland Clarke.

CarCarCaCaCCC olioliolioliolina nana aa BanBanBanBankkerer | | WWWinWinWinttetetertertertereettee 220202 177717 33333

FiFinancial l innsts itutions off aall sis zes rer ly oon Harlandd ClClarke fforo bbese t-in-class sseervices anand high-p-pererforming solulutitioons thatt ddeeliver exceptit onal ROI. WhW ether you’u ree llookking for integrated payment, marketing or security soluutitions, wee hahave more than a century off eexxperience heelplping clientnts s reach theirr gogoals. When it comes to results, itit ttakes more than a lucky streak to determine success.

harlandclarke.com

When your resultsexceed expectations,

it’s not luck. It’s Harland Clarke.

1.800.351.3843 [email protected] Marketing Services • Payment Solutions • Operational Support © 2016 Harland Clarke Corp. All rights reserved.

4 Carolina Banker | Winter 2017

Community Investment Corporation of the Carolinas (CICCAR) StaffDavid Bennett, Executive Vice PresidentJohn Bocciardi, VP/Asset and Compliance ManagerCindy Wiggins-Tiede, Senior UnderwriterShellie Lempert, Servicing and Closing ManagerVikki Conley Ikard, Portfolio Analyst

ConsultantsRobert A. Singer, Greensboro Corporate CounselDr. Harry M. Davis, Boone NCBA Economist and Dean of the NCBA’s North Carolina School of Banking at UNC-Chapel Hill

Contents

Officers & DirectorsMark Holmes, Wilson ChairmanDavid Stevens, DurhamVice ChairmanRick Callicutt, High Point Immediate Past ChairmanPeter Gwaltney, Raleigh President & CEOWendell Begley, Black MountainCharles Canaday, BurlingtonDerek Cohen, WilmingtonPhil Collins, Morehead CityBruce Elder, RaleighSteve Fisher, Granite QuarryRichard Jefferson, JacksonvilleBob Johnson, Winston-SalemGrey Morgan, Mount OliveRoger Plemens, FranklinRick Redden, CharlotteJim Sills, Durham

North Carolina Bankers Association StaffPeter Gwaltney, President & CEONathan Batts, Senior Vice President & CounselGrace Sampson, Srenior Vice President & Secretary & PAC TreasurerMeghan Best, Vice President & Chief Financial OfficerBlair Jernigan, Vice President of Event ManagementVickie Bowers, Director of Human ResourcesScott Brownlow, Creative DirectorBrianna Reeder, Director of Professional DevelopmentMichelle Sutton, Executive AssistantBlaine Wiles, Director of Community Outreach & Member Engagement Frank Youngblood, Operations Coordinator

Community Bank Services (CBS) StaffKim Hutchens, Executive Vice PresidentLauren Perry, Vice PresidentJanice Royster, Director of Endorsed Vendor Programs

12 28

46

50

6

8

10

12

16

22

24

26

28

32

34

36

38

42

46

50

54

58

62

63

64

From The President’s DeskPeter Gwaltney, NCBA

NC Bank PAC

2018 Events Calendar

Legislative Update Nathan Batts, NCBA

News From CICCARDavid Bennett, CICCAR

Financial LiteracyBlaine Wiles, NCBA

CBS UpdateKim Hutchens, CBS

Health Benefit TrustLauren Perry, CBS

Grassroot EffortsPeter Gwaltney, NCBA

NC Young Bankers Conference

Management Team Conference

Women in Banking Leadership Symposium

Making Things HappenRob Nichols, ABA

Collaboration & Competition Between Banks & FintechErin Illman & Nate Viebrock, Bradley

The Top Fintech Trends Driving the Next DecadeRob Morgan, ABA

Smart Money PlayTaylor Rankin, Marbles Kids Museun

Ready and WaitingJim Reber, ICBA Securities

Faces in the News

Around the State

NC M&A Updates

Banks Backing Their Communities

NCBA NEWS & UPDATES

Carolina BankerThe award-winning quarterly magazine

published by Community Bank Services

(CBS), a wholly-owned subsidiary of

the NCBA, as a continuation of The Tarheel Banker since July of 1922.

Editor: Scott Brownlow

Circulation: 4,500-5,000

Subscription Fee: $12 Annual

Phone: 919-781-7979

Email: [email protected]

In This Issue...

Winter 2017

FEATURED TOPICS

FROM THE BANKERS

Financial literacy is one of the

NCBA’s core values, and with

bankers’ help we are seeing it on

the rise. In addition to the Bankers in

Schools programs covered by Blaine

Wiles, the good folks at Marbles

Kids Museum have organized the

Moneypalooza exhibit, a play-based

financial education experience. Find

this and more inside!

FROM THE PRESIDENT’S DESK

New Approach: I’m often asked about the mergers

of 2017 and the impact they will have on the NCBA.

The candid answer is that our consolidating membership

has reduced our revenue, which has required us to

conduct a head to toe evaluation of our programming

and member services. Our senior leadership team and

I have spent a great deal of time together examining

everything we do and how we do it, and I’m excited

about the plans we’ve developed and presented to the

NCBA Board of Directors. I’m blessed to work with

a talented and dedicated leadership team and an

equally capable and spirited staff. In the coming year,

we will be focused on listening to our members and

engaging bankers in everything we do.

New Year’s Resolution: As a membership organization,

it is important for our members to gather from time

to time to hear reports about the work of the Association,

network with peers, learn about developments in

legislation and regulation, and hear new and fresh

ideas across all aspects of banking. Our pledge to our

members is that our conferences and seminars will

feature the highest quality speakers, the newest ideas

and comfortable settings that inspire thinking and

networking. Please resolve to participate in one or

more of the NCBA programs.

New Fusion Forum: In 2018, one of the changes our

members will see is the combination of four annual

conferences—our Management Team Conference,

CFO Symposium, Credit Conference and Security

Summit. Since we’ve “fused” these conferences together,

we’re calling our new annual conference Fusion Forum

2018. Management teams will be invited to attend

and participate in the tracks appropriate for each

individual’s area of responsibility – senior management,

CFOs, credit officers, and security officers. General

sessions will be scheduled during the conference to

give participants opportunities to hear the kind of

speakers we cannot feature at smaller conferences.

Take a look at the Calendar of Events for more!

New Team: In the spirit of engaging our members

more deeply in the work of the Association, we are

creating a new Grassroots Team. The purpose of the

NCBA Grassroots Team is to foster deeper relationships

and enhanced communication with our elected officials

in Congress and the General Assembly. We are asking

every NCBA member bank to designate an individual

to serve on the Grassroots Team. I’m grateful to my

friend Jonathan Hand, President of the Specialized

Lending Group at North State Bank, for serving as

our Grassroots Team Leader. Please read the article

about this new initiative on page 28!

New Partner: Lastly, the New Year will bring a new

partner in the work of the Association, the Independent

Community Bankers of America. Earlier this year,

the NCBA Board of Directors responded to requests

of our many of our members and voted to affiliate

with the ICBA. Our affiliations with the ICBA and

the American Bankers Association will enhance our

legislative and regulatory efforts in Washington D.C.

and expand the portfolio of products and services we

offer our members. The ICBA, ABA, Financial

Services Roundtable and other f inancial trade

associations in Washington D.C. are working more

closely than ever on regulatory reform, tax reform

and a host of other issues. A unified and coordinated

effort between the banking industry’s national

associations and their state affiliates, like the NCBA,

will be critical to our success in the future.

All the best,

As much as I love Christmas, I love the beginning of a new year. I try to start each new year with a rested body and

mind, a clean desk and a store of enthusiasm for the work ahead. I’m particularly excited about 2018. At the NCBA, we

will be doing new things, going to new places, working with new partners and meeting new people in the new year.

In closing, I want to thank all of our bank members, affiliate and attorney members, the NCBA Board of

Directors, and our NCBA staff for your support and encouragement throughout the year. I truly love what I

do, and I love the people and organizations I’m blessed to serve. Here’s wishing all of you a very Merry Christmas

and a Happy New Year!

WHAT’S NEW?BIG CHANGES IN THE NEW YEAR

6 Carolina Banker | Winter 2017

Carolina Banker | Winter 2017 7

This conference is a fusion of our traditional CFO Symposium, Management Team Conference, Credit Conference and Security Summit... You will have the opportunity to hear from experts in your individual field as well as general financial industry updates. Registration will be offered for your role-specific track in addition to a full forum registration for those who wish to choose their own path. Exhibit and sponsorship opportunities will be available! Look out for more information at our website, newsletter, and social media.

Join the North Carolina Bankers Association next year at the first annual Fusion Forum.

8 Carolina Banker | Winter 2017

NC BANK PAC

NCBANKPACPolitical Action Committee for the NC Banking Industry

Your Voice in North Carolina & National Politics

NC Bank PAC supports the election campaigns of individuals who share banking’s legislative goals. It supports those who are willing to listen to and address our community’s biggest concerns.

% CLUBBlack Mountain Savings Bank, Black MountainCoastal Bank & Trust, JacksonvilleCornerstone Bank, WilsonNorth Carolina Bankers Association, RaleighNorth State Bank, RaleighOld North State Trust, GreensboroProvidence Bank, Rocky Mount

% CLUBAmerican National Bank, BurlingtonAquesta Bank, CorneliusBB&T, Winston-SalemCarolina Alliance Bank, AshevilleEntegra Bank, FranklinF&M Bank, SalisburyFifth Third Bank, CharlotteFirst Carolina Bank, Rocky MountFirst Federal Savings Bank, LincolntonFirst South Bank, WashingtonHomeTrust Bank, AshevilleJackson Savings Bank, SylvaKS Bank, SmithfieldLifestore Bank, West JeffersonLumbee Guaranty Bank, PembrokeParagon Bank, Raleigh Peoples Bank, NewtonPiedmont Federal Savings Bank, Winston-SalemRoxboro Savings Bank, RoxboroSelect Bank, DunnSound Bank, Morehead CitySouthern Bank, Mount OliveSunTrust Bank, DurhamTaylorsville Savings Bank, TaylorsvilleUnion Bank, Greenville

$125,000

PAC GOALT H A N K YO U F O R YO U R S U P P O R T !

$81,575

Carolina Banker | Winter 2017 9

COMMUNITY BANK SERVICES

CBS Endorsed Vendors

Provide NCBA Members

Savings, Service & Quality

Look for the Seal, Trust the Product

For more information on the CBS Endorsed Vendor Program, please contact

Janice Royster at (800) 662-7044 or [email protected]

SECURITIESICBA Securities

Jim Reber, (800) 422-6442

BANK OWNED LIFE INSURANCEPentegra Retirement Services

Fabrizio D’Uva, (914) 607-6855

PAYROLLCBIZ Flex-Pay

Sherry Burrick, (336) 462-7838

MERCHANT PROCESSING TSYS

Donna Burns, (731) 772-1425

CRA CREDIT RETAIL BUSINESS DEVELOPMENT

CRA PartnersSue Shaffer, (901) 529-4787

FLOOD DETERMINATIONS FZDS

Teri Sizemore, (419) 660-8589

FINANCIAL DATA & INTELLIGENCES&P Global Market Intelligence

Colin Wyatt, (434) 817-5475

COURTHOUSE RETRIEVAL SYSTEM & COMPREHENSIVE PROPERTY TAX DATA

CRS DataAlwyn Staley, (800) 374-7488 x 150

RETIREMENT PLANSPentegra Retirement ServicesWade Connor, (704) 608-4563

ELECTRONIC LIEN AND TITLE (ELT)Decision Dynamics, Inc.

Amanda Jensen, (803) 808-4929

FUNDING SOLUTIONS ANOVA Financial Corporation

Derek Blair, (888) 266-8293

BANK CYBER SECURITY CONSULTINGSBS CyberSecurity

Alexis Gamewell, (615) 669-5056

TAX EXEMPT LOANS FOR MANUFACTURING

Manufacturing Economic Development Financing Associates (MEDFAS)

Sam Macrina (610) 763-2310

BANK BONDS, D&O AND P&C PRODUCTS

Financial PSIBrian Mobley, (615) 244-5100

COMPANY STORES, COMMERCIAL PRINTING, PROMOTIONAL

PRODUCTS, CORPORATE APPAREL & MARKETING SERVICES

Regency360Chris Hickman (919) 582-9685

SMALL BUSINESS INVESTMENT COMPANIES FUND (SBIC)

Farragut Capital PartnersPhilip A. McNeill (301) 913-5293

OFFICE PRODUCTS, COFFEE & BREAKROOM SERVICES, PRINTER SERVICESRegency Business Solutions

Chris Hickman (919) 582-9685

CAPTIVE INSURANCEOxford Risk Management GroupDavid DiMayo, (410) 472-6490

ONLINE BANK ASSET FOR SALE

Danny Capitel, (866) 766-6426

DISCOUNT SHIPPINGUPS

Call CBS to Sign Up, (800) 662-7044

CHECK PRINTING Harland Clarke

Carroll Lynn Ritchie, (704) 649-3124

10 Carolina Banker | Winter 2017

2018 Events CalendarNCBA Events

January

April

June

February

March

May

5-6

20-22

21-22

27

3-6

7

16

3

17-18

10-12

25-26

3/304/2

Economic Forecast Forum Sheraton Imperial in DurhamThe Economic Forecast Forum is a gathering of our state’s most powerful and influential leaders, and is sure to, once again, attract a sold-out crowd.

BSA Seminar (Patti Blenden)Midtown Hilton in RaleighThis program is designed to enhance the skills of your BSA and AML support staff, your independent audit team, and any personnel responsible for managing and maintaining a strong BSA and AML program.

Commercial Lending School North Carolina Bankers AssociationThe School has been designed to prepare bankers to serve effectively and profitably as commercial loan officers by developing a better comprehension of the economy and how it affects lending decisions.

Spring Compliance Update (Patti Blenden)TBDThis will be a two-day comprehensive update on all current compliance issues in the banking industry.

American Mortgage Conference Pinehurst ResortThis conference connects the leading experts in the financial services industry, policy makers, investors and mortgage practitioners of every kind to discuss important issues in the mortgage field.

Attorney ForumTBDThis forum will gather attorneys from all across the state to discuss current trends and issues in the industry.

Technology Seminar (KPN Consulting)The Rural Center in RaleighThis seminar will be presented by KPN Consulting and will share with registrants how to understand and incorporate technology into their bank to make their institution more profitable and efficient.

Bank Directors AssemblyRaleigh Crabtree MarriottBring your entire bank board to this conference to keep your Directors up-to-date with industry trends so that they can better perform their jobs and contribute to the success of the bank.

Washington Bank CaucusThe Hay-Adams in Washington, D.C.Informative meetings with members of Congress, leaders of the bank regulatory agencies, and other important officials who impact our industry.

CBS Benefits Day & HR ConferenceGreensboro-High Point Airport MarriottThis program is a great opportunity for NCBA members to learn more about options available to their employees through our association and to focus on HR management with their peers. We encourage attendees to take advantage of the full program at the discounted rate.

Call Report SeminarParagon Bank in RaleighThis seminar is designed to explain the whys, wheres and hows of Call Report preparation, and is perfect for both the beginner and the experienced Call Report preparer.

122nd Annual ConventionThe Cloister in Sea Island, GADon’t miss this annual tradition to be held at the only resort in the world to receive the Forbes 5 star designation nine years in a row!

Delegate: $100 / $115

Patron Sponsor: $1,250 / $1,350

Delegate: $375 / $425

Delegate: $250 / $300

Delegate: $450 / $550

Exhibitor: $1,000 / $1,200

Delegate: $400

Spouse: $200

Both: $175 / $225

CBS: $50 / $75

HR: $125 / $175

Delegate: $250 / $300

Delegate: $325 / $375

Delegate: $825 / $875

Delegate: $375 / $425

Delegate: $525 / $625

Exhibitor: $1,100 / $1,250

Delegate: $675 / $775

Exhibitor: $1,200 / $1,300

July

On the Web

October

August

November

September

5-6

11-12

13

TBD

TBD

TBD

TBD

21-23

17-18 7/29 8/3

Certified Banking Security Manager Training (SBS)North Carolina Bankers AssociationAfter completing this program, attendees will understand how to successfully implement and manage each component of the information security program, and their knowledge of layered security programs will be boosted.

82nd Annual School of BankingUniversity of North Carolina at Chapel HillThe NC School of Banking is a four year management development program dedicated to expanding the skills and capabilities of middle level management and prospective managers.

TBDThis will be a two-day comprehensive update on all current compliance issues in the banking industry.

IRA Essentials Training & Advanced IRAs TrainingNorth Carolina Bankers AssociationThese one-day programs can be registered for separately, together, or attached to the HSA Frontline Fundamentals courses.

Health Savings Account TrainingTBDThis is a half-day program that can be registered for separately, or can be attached to the IRA Essentials and/or Advanced IRA Training courses.

Fusion Forum 2018TBDThis conference is a fusion of our CFO Symposium, Management Team Conference, Credit Conference and Security Summit. Registration for your role specific track will be offered as well as a full forum registration which will allow you to choose your path.

TBDThis program will bring you information to broaden your awareness and knowledge of key industry issues, inspire and empower you with stories of success and experience, and provide plenty of time to network with your peers from across the Carolinas.

Regulatory Compliance SchoolTBDThis event is designed to help financial institutions meet compliance challenges by providing intensive training on the various regulatory requirements. Attendees can choose to attend either the Deposits Module, the Lending Module, or the entire program.

Alumni UpdateTBDThis event will be spent reviewing the updated manual and discussing recent developments and common problems.

Young Banker’s ConferenceBlockade Runner in Wrightsville BeachThis annual conference will help to foster the professional development of the emerging leaders in our industry!

Delegate: $1,295 / $1,345

Student: $1,700

Delegate: $375 / $425

TBD

TBD

Full Program: $525 / $625

Tracked Option: $400 / $500

Exhibitor: $1,200 / $1,400

TBD

Deposits: $450 / $500

Lending: $1,050 / $1,100

Both: $1,325 / $1375

Delegate: $350/$400

Delegate: $525 / $600

As you begin to plan your budget and calendar for the upcoming year, the NCBA thought that it may be helpful to provide a guide with the estimated costs and dates of our 2018 professional development opportunities and conferences. To learn more about specific events or available sponsorship opportunities, contact Blair Jernigan at [email protected] or Brianna Reeder at [email protected].

The NCBA has partnered with affiliate members and Total Training Solutions to provide an ongoing series of webinars for our members that feature a wide array of topics. You can find the listings online by visiting www.ncbankers.org.

The NCBA welcomes the opportunity to partner with affiliate members on these convenient presentations. If you are an affiliate member and interested in this opportunity, please reach out to Brianna Reeder at [email protected].

Fall Compliance Seminar (Patti Blenden)

Women In Banking Leadership Symposium

*Please note that fees, dates and locations are subject to change prior to registration.

12 Carolina Banker | Winter 2017

Accessing the Law on POAsFirst, let’s start with how to retrieve

both laws. One of the things our General

Assembly is great about is providing full

content of these laws at www.ncleg.net.

Chapter 32A: “Powers of Attorney” can

be found using the “Shortcuts” tab in

the right column on that homepage and

then clicking below the “General

Statutes” heading the “Table of

Contents” link. At a later time, the

chapter list will be updated to also

include new Chapter 32C, but for now,

the law can be accessed using the “Find

a Bill” option in the menu at top right

on the General Assembly homepage and

typing in S 569. This will load Senate

Bill 569, which became Session Law

2017-153: “An Act to Adopt the Uniform

Power of Attorney Act in this State.”

Durable POAsThe new law is divided into a series of

statutes. After updated definitions, a

major change begins with General

Statute (GS) 32C-1-104. It says: “A

power of attorney created pursuant to

this Chapter is durable unless the

instrument expressly provides that it is

terminated by the incapacity of the

principal.” Terms like durable, incapacity,

and principal are defined in the law.

The important thing about this

statute is that it changes the presumption

in North Carolina. Previously, a POA

needed to include specif ic wording

mentioning that the POA was durable

or not affected by the principal ’s

subsequent incapacity or incompetence

in order for the POA to continue to be

usable after such a circumstance arose.

Plus, to use the POA after incapacity

LEGISLATIVE UPDATE

Nathan BattsSenior Vice President and

Counsel, NCBA

In 2017, the North Carolina General Assembly passed a bill substantially revising the

state’s laws on Powers of Attorney (POAs). Remember that a POA is simply a legal

document that allows a person to name another person or persons to act on his or her

behalf. The new law on POAs becomes effective January 1, 2018. It replaces a number

of Articles within Chapter 32A with a new Chapter 32C. In this article, I will

summarize the notable changes for banks.

THE NEW FRAMEWORK FOR POWERS OF ATTORNEY

Carolina Banker | Winter 2017 13

or incompetence arose, a person needed

to make sure that the POA was recorded

with the county Register of Deeds.

With the new law, those requirements

generally disappear.

Going forward beginning January

1, all POAs – those created when the

old law was in effect and those created

under the new law – are deemed to be

durable unless otherwise stated in the

POA. Gone too, with a notable

exception, is the requirement to take a

POA to a Register of Deeds off ice and

have it recorded. A person can still

choose to record a POA, but it is no

longer required unless a transfer of real

estate under authority granted in the

POA is anticipated, then the POA

needs to be recorded so that it can show

up in a title search.

Also of note, the def inition of

incapacity now also addresses a principal

being incarcerated in prison. We have

gotten questions over the years on this and

the new law helps to clear up the matter.

The Role of the Agent One of the things I also like is the

replacement of the term attorney-in-fact

with the word agent. This is a lot easier

to understand and makes it clearer that

I as the principal can name someone as

my agent to act for me with such powers,

and subject to such limitations, as I set

out in a POA that is signed by me and

acknowledged before a notary public or

similar official.

Choice of LawAnother thing to note about the new

law is GS 32C-1-107 that provides the

meaning and effect of a POA is

determined by the law of the jurisdiction

indicated in the POA, and in the absence

of an indication of jurisdiction, by the

law where the POA was executed. This

means that the POA can expressly say,

for example, it is construed under the

laws of the State of X, or it could be

signed in that state. If either of those

occur, then the POA is interpreted using

that state’s laws.

If you read that and have a moment

of fear thinking that a bank in North

Carolina cannot readily know the laws

of another state, the new law already

anticipated that scenario. GS 32C-1-119

dealing with acceptance and reliance on

a POA includes paragraphs (d)(2) and

(d)(3) to address situations like these.

Paragraph (d)(3) provides that a person

asked to accept a POA may make a

written request for an opinion from an

attorney as to any matter of law

concerning the POA. If the request is

made within seven business days after

the POA is presented for acceptance,

the opinion must be provided at the

principal ’s expense.

If terms aren’t defined in a POA and

it refers instead back to the other state’s

laws, or you aren’t sure what the other

state’s laws say about the role of witnesses

(NC requires acknowledgement, which

is usually done before a notary public

who then signs and applies his or her

seal, but other states may require

additional witnesses), then it is an

important tool to request an opinion.

The other subsection gives you the

ability to request an English translation

if the POA is in another language

besides English.

Remember that if a principal or agent

balks at providing such information

when reasonably and timely requested

to do so, you have grounds to decline to

honor the POA. If it is about the expense

of providing such a document, a potential

avenue for resolution could be for the

principal to simply provide you with a

new POA signed using North Carolina

law. There is nothing to prevent the

principal from having multiple POAs.

This is part of the balancing act in

trying to make sure that POAs are

honored and can be ported over from

other states, while making it more

realistic because no one can be an

expert on every law, particularly ones

where your bank does not operate and

has no experience.

Judicial ReliefAnother thing of note is GS 32C-1-116,

which provides increased clarity about

the role of the clerk of superior court in

helping to determine an agent’s authority

and powers. Sometimes POAs are

ambiguous or confusingly worded. The

new statute sets out how a clerk of superior

court can help to reconcile such matters.

14 Carolina Banker | Winter 2017

Reliance on a POA and Remedies for Unreasonable Refusal to Accept a POALooking at GS 32C-1-119 and 32C-1-120, you will see a lot

of familiar concepts in the standards that protect banks and

other parties who reasonably rely upon a POA and in the

criteria that must be established before there is liability for

failure to honor a POA. The phrasing is different, but the

general message is the same. If you don’t have an established

customer relationship with the principal, you are not required

to do business with an agent who presents a POA, provided,

of course, that you are in no way discriminating. It follows

from this that opening new accounts or agreeing to extend a

loan are treated like new customer relationships.

If you do have an existing customer relationship, and

you are presented with a new POA, take the time to review

it. Just like under the old law, it is not considered to be

unreasonable refusal solely on the basis of failure to accept

the POA within seven business days. Act with promptness

where you can, but remember that you are on the front line

protecting your customers. We have seen too often where

agents demand a quick response and as the facts are gathered

it begins to emerge that the agent may be attempting to

commit f inancial exploitation of an older or disabled

customer, which the bank must report as required by separate

state and federal law.

Expanded Definitions

Article 2 is where the definitions really get detailed. One

of the most useful statutes will be GS 32C-2-208, which,

unless other def initions are given in the POA, explains

what authority in a POA with respect to banking

transactions really means.

Under the old law, it was a common frustration among

bankers that the default definitions in the statutes didn’t

address such matters as opening and closing accounts.

Instead, the list of powers was focused on such matters as

cashing checks. Agents frequently sought to open or close

accounts, so bankers were left hunting within the POA for

other provisions that might allow for such a thing. For

example, the POA might have referenced personal property

transactions as well and been broadly written enough there

to also cover opening or closing accounts, or the POA might

have catch-all language saying the agent could do anything

the principal could do. The new law squarely addresses these

matters, which is a major improvement.

Another area where the old law was messy was with regard

to gift giving, including the granting of rights of survivorship

in accounts. Under the old law, when we wanted to see if an

agent could name himself or herself as a payable-on-death

beneficiary, we had to look for banking powers in the POA

and look for authorization for the agent to give a gift to

himself or herself. The new law provides updated statutes

addressing these matters.

Short Form POA

One of the things that will be familiar and different at

the same time is the template in the statutes for POAs.

GS 32C-3-3-301 provides a sample POA that can be used.

Although the format is similar to the old version, many

of the concepts like gift giving and rights of survivorship

are set out expressly. The template starts with the general

powers that the principal can initial beside if granting

them, then it progresses to the specif ic powers like gift

giving, rights of survivorship, and changing beneficiaries

which also need initials if granted. This is followed by

information about the effective date, a new optional

provision for naming a guardian, and the standard signature

lines for the principal and notary. The POA in the statutes

is, of course, a template, and people are free to create their

own documents or modify this version.

Agent’s CertificationYou will see also a certif ication form like the one many

banks obtain from agents. This is found in GS 32C-3-302

and is used as a way to help confirm that a POA is still

valid. Sometimes in asking for an agent to sign a

certif ication, the agent will reveal that the principal has

just passed away (in which case the POA is terminated) or

will reveal other facts or circumstances that call into

question the validity.

Limited POA for Real PropertyThere are situations where a principal simply needs someone

to help convey real estate. Now we have a template in GS

32C-3-303 for these types of transactions. This could become

a great benefit in standardizing such documents.

LEGISLATIVE UPDATE

Carolina Banker | Winter 2017 15

Effect on Existing Powers of AttorneyWhen the law goes into effect on January 1, one issue banks

will have to face is differentiating POAs that were written

under the old law from ones written under the new law. GS

32C-4-403 seeks to help answer these questions.

Remember this general rule of thumb: the new law in

Chapter 32C applies to POAs created before, on, or after

January 1, 2018, unless there is clear indication of a contrary

intent in the terms of the POA or unless application of a

particular provision of the law would substantially impair

rights of a party. Importantly, the statute goes on to state

that references to prior statutes and POAs, whether executed

on or after the adoption of the new law shall be deemed to

refer to the corresponding provisions of Chapter 32C, again

unless doing so would impair substantial rights of a party.

Also noteworthy is another subsection of GS 32C-4-

403 which says “Notwithstanding the provisions of this

Chapter, the powers conferred by former G.S. 32A-2

shall apply to a Statutory Short Form Power of Attorney

that was created in accordance with former G.S. 32A-1

prior to January 1, 2018.” GS 32A-1 provided the old

template and GS 32A-2 was the definitions statute that

explained what certain words in the template, or short

form POA, meant. I take this subsection to mean that

if you have an old short form POA under the prior law,

you need to interpret its meaning under the old definitions.

This becomes important when dealing with opening and

closing accounts, gift giving, adding rights of survivorship

or payable on death beneficiaries as I previously discussed

earlier in this article.

ConclusionThere will be an adjustment period as customers, agents, and bankers adapt to the new laws on POAs. I encourage you to

familiarize yourself with the new law because POAs are one of the most frequently encountered documents by bankers.

2018 Commercial Lending School

The NCBA has partnered with KPN Consulting and DHG Credit Risk Management to bring

our members the new and improved Commercial Lending School! The School has been

designed to prepare bankers to serve effectively and profitably as commercial loan officers

by developing a better comprehension of the economy and how it affects lending decisions.

Insight will be offered into how a business is structured and how it competes. Attendees

will develop an understanding of the role of the company’s management and how to

analyze and evaluate that management. Registrants will also be provided an opportunity to

apply analytical techniques in a lending situation and to carry them forward in the pricing

and structuring of a loan.

For information on specific courses and more, visit www.ncbankers.org.

Save the date!

April 10-12, 2018

16 Carolina Banker | Winter 2017

The underwriting package for a CICCAR loan is very similar to that of any commercial real estate loan,

including information such as a project description, appraisal, an operating proforma, a Phase I

environmental study and borrower financials. However, there is one item that may be less familiar to

our member banks: the LIHTC market study. This report offers important insight into the demand for

– and future viability of – a proposed LIHTC multifamily property. As such, it is an essential component

of our loan underwriting process, and a complement to the other information we review.

The market study is required by each state housing finance agency as part of the low income housing

tax credit (LIHTC) application process. While these reports are often engaged by the borrower, the

state tax credit allocating agency generally provides a list of approved market study firms that may be

used, along with the critical components that must be included in the report to make it acceptable for

the application. There is also a national industry group, the National Council of Housing Market

Analysts, which develops and maintains report standards to ensure consistency and reliability among

its members. This article will provide a brief overview of the content and purpose of the LIHTC market

study, and how to interpret its results.

CICCAR

David BennettExecutive VP, CICCAR

Analyzing the Proposed LocationIn many ways, a market study resembles an

appraisal. Much of the preliminary information

provided in a market study is designed to identify

and describe the project location, the proposed

project, the broader geographic region, nearby

recreational and cultural facilities, and access to

retail and commercial amenities. There will be

a discussion of comparable properties in the area,

and the analyst will document his or her site visit

observations with the same types of maps,

photographs and architectural renderings as one

would expect to see in an appraisal report.

The market study also includes a review of

historical crime statistics, to determine whether

the proposed project location is considered “high

risk” or less desirable as compared to local, state

and national crime statistics. Finally, the report

includes a review of economic, social and

demographic trends, to assess the long-term

prospects for the proposed project area, including

major employers, job concentrations, and past

and future employment trends relative to the

state and nation.

Defining the Market AreaPerhaps the most important component of the

market study is how the analyst defines the “market

area” for the project. The market area is the

geographic area from which the proposed property

is expected to attract its residents. The size of the

market area can vary significantly depending upon

where the project will be located. In a heavily

populated urban or suburban area, the market area

may be defined as a relatively small number of

contiguous census tracts. However, in a more rural

Carolina Banker | Winter 2017 17

area, the market area may include an entire county,

or even several adjacent counties. The idea is to

define the area where the target population of

residents resides, how far they may be expected to

relocate to the proposed property, and how appealing

the proposed property will be relative to other living

options and employment opportunities.

Within the defined market area, the analyst will

discuss household trends based upon available

demographic data. Is the total number of households

growing or shrinking? What is the average

household size, and the mix of income levels? What

is the current and projected mix of owners versus

renters? If the proposed project is aimed at seniors

aged 55 and older, the analyst will pay particular

attention to current and future population trends

that focus on this age group.

A market area that is too large or too small

may skew the analyst’s conclusions. If the defined

market area is too large, it may suggest the

existence of too many potential renters for the

property, and overstate demand for the units. If

it is too small, it could suggest that a much-needed

property is not viable because not all potential

residents were considered. However, assuming the

market area is properly delineated, the analyst

then focuses on the target population and resulting

demand for the proposed units.

Target Population & “Capture Rate”Finally, the analyst will break down the population

by income levels, household type and projected

trends. For the properties that CICCAR finances,

the objective is to determine how many low- to

moderate-income (LMI) households are living in

the market area, and analyze the number of “rent

burdened” households in the market. A household

is considered “rent burdened” if it is paying more

than 30% of gross income on housing expenses

(def ined as rent or mortgage plus utilities). For

proposed LIHTC projects, the higher the

percentage of rent-burdened households in a

market, the more likely that there will be strong

demand for affordable housing units.

The estimated demand for units is detailed in

what is called the “capture rate.” Looking at income

levels, current and projected population trends, and

currently available vs. proposed new units, the

analyst calculates a projected demand for the

proposed units. The “capture rate” is simply the

percentage calculation of the proposed units over

the estimated net demand. So, if a market study

estimated a net demand for 350 affordable units in

a market area, and a proposed project would supply

75 units, the overall capture rate would be

approximately 21%. The analyst will also look at

the potential demand for each proposed unit type

18 Carolina Banker | Winter 2017

CICCAR

(1BR, 2BR, etc.), to calculate capture rates for

each option. This is helpful because it can reveal

whether or not the proposed unit mix is

appropriate for a particular market. For example,

a rural market with a high senior population is

not able to absorb as many three-bedroom units

as a suburban market with a greater percentage

of families with children.

ConclusionAs a general rule, a calculated capture rate of 30% or less is considered acceptable. When evaluating

the capture rate, context is key. For senior properties, it is not uncommon to see capture rates in a

range of 20-30%, because the project is designed for a targeted sub-set of the broader population

(namely, LMI senior households). In rapidly growing markets such as Raleigh or Charlotte, we

regularly see capture rates as low as 1-2%, indicating that the proposed units are barely scratching

the surface in meeting the demand for affordable units. The lower the capture rate, the more confident

one can be that a multifamily property will lease up quickly and perform well over its lifespan.

The American Mortgage Conference connects the leading experts in the financial services industry, policy makers, investors, and mortgage practitioners of every kind to discuss important issues in the mortgage field.

• E-Mortgages • Digital Lending • Updates from Policymakers • Fair Lending & Access to Credit • HMDA • Affordable Housing

THE P INEHURST RESORT • APRIL 30 - MAY 2, 2018

FORGING CONNECTIONS

AAAmerican AAAAAAmmmmmmeeeerrrriiiiiicccccaaaaaannnnnMortgage MMMMMMMooorrrtttgggaaagggeeee

CCCConferenceCCCCCCoooooonnnnnfffffffeeeeeeerrrrreeeennnncccceee

Carolina Banker | Winter 2017 19

Oxford Crossing Apartments, Claremont, NCWeaver-Kirkland Housing and Zimmerman Properties were the developers/sponsors of Oxford Crossing Apart-

ments. The development provides 88 units affordable to families earning 30%/60% or less of the area median

income. This development received city funds for $300,000, a state tax credit loan for $930,448, and $6,736,607

in proceeds from the sale of federal tax credits.

Crescent Villas Apartments, Florence, SCDavid Douglas of Douglas Development is the managing member of Crescent Villas Apartments. The development

provides 48 units affordable to seniors earning 50%/60% or less of the area median income. This development received

HOME funds for $421,844, and approximately $5,748,776 in proceeds from the sale of federal tax credits.

RECENT LOAN CLOSINGSLoan 377340: Hampton’s Crossing Apartments, Lexington, SC . . . . . . . . . . . . . . . . . . . . . .

Loan 360341: Oxford Crossing Apartments, Claremont, NC . . . . . . . . . . . . . . . . . . . . . . . .

Loan 376362: Crescent Villas Apartments, Florence, SC . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Loan 379343: The Pointe Apartments, Blythewood, SC . . . . . . . . . . . . . . . . . . . . . . . . . .

closed on 10/18/17 for $1,440,000

closed on 10/19/17 for $1,895,600

closed on 10/31/2017 for $830,408

closed on 11/14/2017 for $1,415,000

The Pointe Apartments

Oxford Crossing Apartments

Crescent Villas Apartments

Hampton Crossing Apartments

NEWS FROM CICCAR

20 Carolina Banker | Winter 2017

CELEBRATING TWENTY-FIVE YEARS OF LENDING 1990-2015

Community Investment Corporation of the CarolinasP.O. Box 19999, Raleigh, NC 27619

Toll free: (800) 662-7044 Local: (919) 781-7979www.ncbankers.org/CICCAR

@CICCarolinas

Community Investment Corporation of the Carolinas is a lending consortium of more than

100 southeastern financial institutions, working together to provide permanent financing that

supports the development of high-quality affordable multifamily housing in the Carolinas,

Georgia, Tennessee, Virginia and West Virginia.

Since 1990, CICCAR members have funded more

than $275 million in loans, creating 17,000 units

in over 300 properties. In return, they receive

the benefits of loan growth, CRA credit and the

satisfaction of creating “home” for nearly 50,000

people.

Call today to learn more about the ways that

membership in CICCAR can benefit your bank and

the communities you serve.

It’s Home.

It’s Not Just a Building...

Carolina Banker | Winter 2017 21

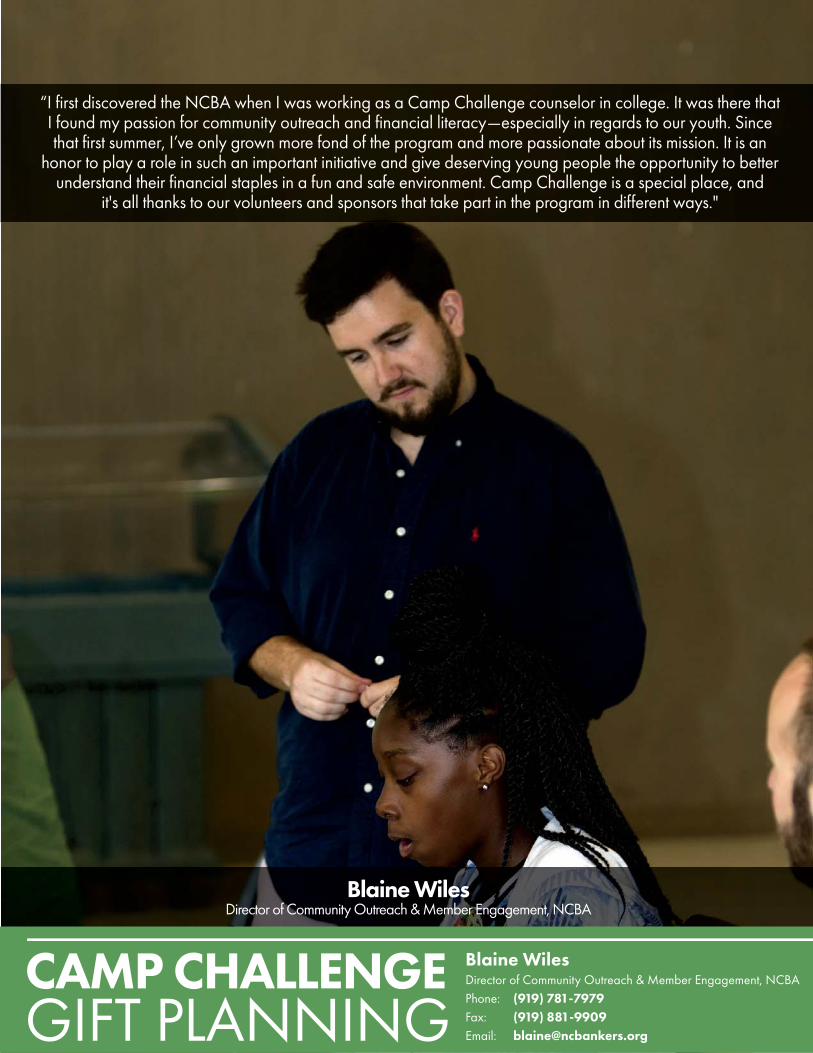

“I first discovered the NCBA when I was working as a Camp Challenge counselor in college. It was there that I found my passion for community outreach and financial literacy—especially in regards to our youth. Since that first summer, I’ve only grown more fond of the program and more passionate about its mission. It is an

honor to play a role in such an important initiative and give deserving young people the opportunity to better understand their financial staples in a fun and safe environment. Camp Challenge is a special place, and

it's all thanks to our volunteers and sponsors that take part in the program in different ways."

Blaine WilesDirector of Community Outreach & Member Engagement, NCBA

Blaine Wiles Director of Community Outreach & Member Engagement, NCBAPhone: (919) 781-7979Fax: (919) 881-9909 Email: [email protected]

22 Carolina Banker | Winter 2017

FINANCIAL LITERACY

Blaine WilesDirector of Community

Outreach & Member Engagement, NCBA

THIRD TIME’S THE CHARMThis past November, the North Carolina Young Bankers (NCYB) held the third installment of

its Bankers in Schools program, and it was a tremendous success and their best showing yet!

The Bankers in Schools program, originally launched in November of 2016, is an educational

outreach initiative led by a host of Young Bankers from across the state in an effort to expand

and strengthen financial literacy in North Carolina high schools. Twice a year, the Bankers in

Schools program offers high schools from across the state the opportunity to request members

of the NCYB to visit with their classes and teach a 45-minute lesson on budgeting.

Carolina Banker | Winter 2017 23

The goal of the program is not only to teach students basic components

of financial education, but to also initiate and foster a relationship between

bankers and those in their local communities at a young age. “This is a

great way to help provide the necessary information to students to help

them develop patterns of saving and helping them develop a banking

relationship at an early age,” says recurring volunteer Alan Stapleton,

Carolina Premier Bank, on why he is so passionate about the program.

Throughout the week of

November 13 – 17, with help from

over 20 volunteers, the NCYB was

able to visit 25 classrooms in 15

different schools from across the

state, reaching approximately 800

students! That number is almost

identical to the total number of

students that the NCYB had

already reached in the two previ-

ous sessions of Bankers in Schools

combined! To see such growth and

gained momentum for the pro-

gram is truly remarkable, and we

are incredibly grateful to all the

members of the NCYB who have

dedicated their time to this ini-

tiative thus far. As Bankers in

Schools continues to expand, we

hope that both the number of

schools and volunteers throughout

the state will increasingly grow

alongside it as well.

The importance of both

increasing financial literacy and

building meaningful relationships

with our youth is paramount to

the future of banking in North

Carolina. It is important for us to

be proactive in this endeavor, and

fully adopt an “all hands on deck”

approach. Understandably, most

young professionals don’t have the

time or resources to locate schools

in their communities, reach out to

them, build a curriculum, and

execute all of the minute details

that are involved with volunteering

with their local youth. That is

exactly why the Bankers in Schools

program is so essential to those

who live a busy lifestyle but have

a desire to give back to their

communities – it takes all of the

hard work out of the process.

As we prepare for another busy

and exciting year in 2018, we ask

you to please consider getting

involved in the mission of financial

literacy in whatever capacity you

can. We are continuously looking

for more schools from around the

state that we can partner with, as

well as volunteers with a little bit

of extra time to fill those spots. If

you can help put us in touch with

schools in your community, or

would like for your organization

to participate as volunteers, we

would love to have you on board!

24 Carolina Banker | Winter 2017

CBS UPDATE

Kim HutchensExecutive VP, CBS

Community Bank Services (CBS), a wholly owned subsidiary of the North Carolina Bankers Association,

is proud to announce a new emerging relationship with Will Greene and Palmetto Benefit Solutions for

voluntary benefits. Through this partnership, all NCBA members will have access to exclusive plan designs,

preferred underwriting and superior service.

We welcome Palmetto Benefit Solutions and Will Greene back into the CBS family. Our relationship with Will Greene goes

back several years, and we are very excited to be working with him on this opportunity for our members to enroll in a very strong

voluntary benefit package. He has a tremendous work ethic, deep knowledge of the insurance business and moreover, an existing

relationship with many of our banks. It’s really a pleasure to work with Will. I look forward to the relationship.

PALMETTO BENEFIT SOLUTIONSCBS HIGHLIGHTS ENDORSEMENT WITH

Voluntary benef its are a great way to enhance your

benefits package in order to help attract and retain employees,

at no cost to the employer. With deductibles and health care

costs continuing to rise, voluntary benefits are more attractive

than ever before. The Palmetto Benefits team can help your

employees protect their assets by selecting the appropriate

coverage for themselves and their families. At no direct cost

to the employer, Palmetto can provide:

• Voluntary benefits to supplement benefit offerings: (Critical

Illness, Cancer, Accident, Short Term Disability, Whole Life).

• Preferred underwriting on various Colonial Life products

which enable employees who need coverage to have a better

opportunity to qualify.

• One-on-one counseling sessions to help your employees

understand all of their benefits.

• End-to-end enrollment services with core enrollment and

communications.

• Integrated enrollment options.

• Wellness/health screening benefits paid yearly to employees.

• Guaranteed issue – Employees can elect coverage even with

pre-existing conditions.

Additional BenefitsFor valued NCBA members, Palmetto Benefits will provide

WellCards to each employee for discounts at participating

pharmacies and providers. Palmetto will also provide access

to MDLIVE, which gives 24/7 access to board-certif ied

doctors for a virtual consult to diagnose non-emergency

medical issues over the phone or through secure video on

your computer or mobile app. Doctors can send an

e-prescription straight to your local pharmacy, all at no

cost to the company or the employee.

What to Expect• Single access to coverage-very limited health questions

and some benefits offered with no health questions of

employees. Family coverage options are also available to

employees enrolled in the program.

• A customized, needs-based counseling session from

professional benefits advisors.

• Integrated online enrollment solutions.

• Assistance in the processs of transitioning coverage from

other carriers.

• Superior customer service.

Carolina Banker | Winter 2017 25

Options Available• Short Term Disability Insurance (STB): Replaces up to

60% of your income to help make ends meet if you become

disabled from a covered accident or covered sickness;

pregnancy/childbirth benefits included. 3-12 months

benefit periods available.

• Accident Insurance: On and off job coverage available.

This helps offset the unexpected expenses that can result

from a fracture, dislocation or other covered minor or

major accidental injury—you can use the money for bills,

food, rent or to cover medical deductibles. Policy also

includes life insurance benefit for accidental death.

Employers can choose wellness benefit for annual wellness

exam of $0, $25, $50, $100. No underwriting is required.

• Cancer Insurance: This insurance helps with out-of-pocket

medical costs and indirect, non-medical expenses related

to cancer treatment including travel, lost wages, and lost

spousal wages, deductibles, copays, and more. Includes

$50 wellness benefit for annual wellness exam but

employers may choose an alternative wellness benefit.

Employers can choose from 4 plan designs.

• Critical Illness Insurance: Recovery rates are higher than

ever and so is the cost of recovery. This insurance provides

a lump-sum benefit you can use to pay direct and indirect

costs related to a covered critical illness; heart attack,

stroke, end state renal failure, major organ failure,

permanent paralysis due to a covered accident, and more.

Includes subsequent diagnosis benefit for reoccurring

critical illnesses. Employees can elect a policy value from

$1,000 to $100,000 and no underwriting is required for

amounts under $30,000.

• Life Insurance: Whole life insurance provides a lump-sum

benefit of $5,000 -$100,000 while building additional

cash value and provides lifetime permanent protection.

Benefits amounts under $50,000 are guaranteed issue and

do not require medical underwriting.

Will Greene, Director of Sales at Palemetto Benefits palmettobenefits.net • 843-384-3549 (C) • 843-501-7373 (O)

Will Greene, Sales Director with Palmetto, is a seven year

insurance veteran. A native of Hilton Head Island, he

received his International Finance degree from Winthrop

University. In regards to the announcement, Greene said,

“I am excited to be working with Community Bank Services

once again. The CBS team is an awesome team to work

with and are willing to go to work for their members.

Worksite benefits are gaining traction amongst the banking

community and this partnership will allow members to get

the most value and greatest ROI available in the marketplace.

It is perfect timing for this partnership to happen!”

All Benefits Pay Cash Directly To The EmployeePolicies are portable and can be carried with the employee for a lifetime.

26 Carolina Banker | Winter 2017

HEALTH BENEFIT TRUST

This has sure been one eventful year in the world of healthcare! A lot has changed over the past twelve months, but Community Bank Services is here to provide you with all of the knowledge that you will need to navigate the ever-evolving, and often confusing, legislative and compliance atmosphere today. Below you will f ind some of the most signif icant highlights from 2017, and we will take a look at the key changes for individuals and employers in the coming year.

The Latest ACA Repeal Bill Has Been Withdrawn

• The Graham-Cassidy bill, the most

recent Republican effort to repeal and

replace the Affordable Care Act (ACA)

was withdrawn from a vote on

September 26th due to the lack of

Senate support.

• Due to opposition to the bill from

inf luential health organizations and

lawmakers on both sides of the aisle,

the proposed bill will require a variety

of amendments, which means the

ACA will likely remain unopposed

until 2018.

• The IRS conf irmed recently that

employers should continue to comply

with any ACA mandates, including

the individual mandate and employer

shared responsibility rules.

Employer “Pay or Play” Enforcement GuidelinesHave Been Officially Released by the IRS

• The ACA’s employer shared responsibility rules require applicable large employers

(ALEs) to offer “affordable, minimum value” health coverage to their full-time

employees or pay a penalty. These rules, known as the “employer mandate” or

“pay or play” rules took effect for most ALEs beginning on January 1, 2015.

• Prior to 2017, the IRS has been unable to identify the employers potentially

subject to an employer shared responsibility penalty or to access any penalties.

The IRS previously indicated that it expected to begin sending letters in early

2017 informing ALEs of their potential liability for a penalty; however, at this

time, no letters have been sent to any ALEs.

Some ACA Subsidies Will End In The Near Future

• On October 12, 2017, the White House announced that it will no longer

reimburse insurers for cost-sharing reductions made available to low-income

individuals through the Exchanges under the ACA, effective immediately.

Because Congress did not pass an appropriation for this expense, the Trump

administration has taken the position that it cannot lawfully make the cost-

sharing reduction payments.

• Cost-sharing reductions, which lower out-of-pocket costs such as deductibles

and coinsurance at the time of service, are available to individuals who have

incomes of up to 250 percent of the federal poverty level and are also eligible for

the premium tax credit.

• While the immediate impact of this change is unclear, it will have significant

impact on those who enroll through the Exchange during the 2018 open enrollment

period. Furthermore, insurers who offer plans through the Exchange will likely

not have enough time to make significant changes for 2018, causing confusion

and uncertainty in the Exchanges.

• Premium tax credits, which are the other type of federal subsidy available

through the Exchange, will continue to be available.

Lauren PerryVice President, CBS

Carolina Banker | Winter 2017 27

The IRS Has Reversed Policy on Certifying Individual Mandate Compliance

• On October 13, 2017, the IRS reversed a recent policy change in how

it monitors compliance with the Affordable Care Act’s (ACA) individual

mandate. For the upcoming 2018 filing season (2017 returns):

» The IRS will not accept electronically f iled tax returns

where the taxpayer does not certify whether the individual

had health insurance for the year.

» Paper returns that do not certify compliance with the

individual mandate may be suspended pending receipt of

additional information, and any refunds due may be delayed.

IRS Announces Employee Benefit Plan Limits for 2018

• Many employee benefits are subject to annual

dollar limits that are periodically increased for

inf lation. The IRS recently announced the cost-

of-living adjustments to the annual dollar limits

for various welfare and retirement plan limits for

2018.

• Health Flexible Spending Accounts (FSAs): The FSA dollar limit will increase to $2,650 for

taxable years beginning in 2018. Employers should

ensure that their health FSA will not allow

employees to make pre-tax contributions in excess

of $2,650 for 2018.

• Dependent Care FSA: Dependent care FSA

limits will remain $5,000 ($2,500 if married and

filing taxes separately).

• Health Savings Accounts (HSAs): The HSA

contribution limit has increased to $3,450 for self-

only high deductible health plan (HDHP) coverage

and $6,900 for family HDHP coverage. The

catch-up contribution for individuals over 55 will

remain $1,000.

• Qualified Small Employer HR A (QSEHR A):Payments and reimbursement limits for employee-

only coverage will increase to $5,050 in 2018 and

family coverage will increase to $10,250.

• 401(k) Contributions: Employee elective

deferrals will increase to $18,500 in 2018. Catch-up

contributions will remain $6,000.

The NCBA is introducing a new effort for 2018 to increase banker involvement in NCBA government

relations. Your NCBA government relations team is in regular contact with our elected officials, makes

frequent trips to Washington D.C., and is a constant presence at the Legislative Building in Raleigh,

but there is no substitute for direct contact between bankers and elected officials when an important

issue is being considered.

Our new NCBA Grassroots Team will consist of a representative of each NCBA member bank.

Grassroots Team members can be a bank CEO or another key officer or employee who has a special

interest in advocacy, with the CEO’s support and encouragement to participate. Team members will be

responsible for receiving NCBA Government Relations Updates and distributing communications to bank staff as appropriate,

coordinating and encouraging responses by bank personnel to NCBA Action Alerts, encouraging participation in NC

BankPAC, and working with NCBA staff to schedule bank visits with members of Congress and the General Assembly.

We have enlisted the help of Jonathan Hand of North State Bank to lead our Grassroots Team. Jonathan is a regular

participant in the NCBA Washington Bank Caucus, is a member of NC BankPAC, serves as the North Carolina representative

GRASSROOT EFFORTS

on the ABA Grassroots and Advocacy Committee, President's Club and is an effective advocate for banking in meetings

with elected officials. I sat down with Jonathan recently to discuss banking, regulatory reform and a host of other issues. I

want to share a portion of our conversation to give our readers an opportunity to get acquainted with Jonathan and gain an

understanding of what we are seeking to accomplish through the NCBA Grassroots Team.

PG: What is your role at North State Bank?

JH: Currently serve as the President of the Specialized Lending Group. SLG provides

comprehensive banking services to the homebuilding industry from land development to the

homebuyer’s permanent mortgage and everything in between.

PG: What do you enjoy most about your work?

JH: Working with a bank whose culture is first and foremost centered on improving the

lives of those we serve.

PG: How and when were you introduced to advocacy?

JH: I am fortunate to work with a CEO, Larry Barbour, who strongly encourages and provides

a platform for personal growth and development. Five years ago, Larry invited me to join him

on the NCBA Washington trip and has allowed me to accompany him each year since.

PG: How has your involvement in advocacy been worthwhile to you?

JH: My involvement with advocacy has given me a broader understanding of how government

functions and sometimes dysfunctions. Additionally, it has given me the opportunity to meet

and learn from other people and organizations throughout the country and share experiences

and learn best practices that can beneficial in better serving my customers and community.

PG: Why is it important for bankers to be involved in advocacy?

JH: Bankers, especially customer-facing bankers, bring everyday stories of impact to our legislators that they ordinarily

would not get from association staff, paid lobbyist and the like. Bankers understand the needs of our customers and can see

first- hand how well-intended legislation may actually do more harm than good in serving the banking needs of those in

their community. The Association staff does a great job educating elected officials and coordinating the banking industry’s

advocacy efforts, but we need customer-facing bankers to share the stories of impact.

Jonathan HandSenior Vice President & President of Specialized Lending at North State Bank and a key member of the new NCBA Grassroots Team.

Peter GwaltneyPresident & CEO, NCBA

28 Carolina Banker | Winter 2017

PG: What is your vision for the new NCBA Grassroots Team?

JH: My vision for grassroots is simple: Establish a network of bankers from each

of the NCBA member banks who will serve as the information gatekeeper for their

respective organization regarding communication to and from Washington. Team

members will be asked to host their local representatives in town hall style meetings

to discuss how bank legislation impacts their community. And finally, team members

will be encouraged to join the NCBA delegation on its annual trip to DC to meet

with the NC congressional delegation and regulatory agencies to share their stories

on issues that are impacting their bank, customers and the community.

PG: Will participation on the Grassroots Team be time consuming?

JH: No, we just need participants to monitor and distribute communications from

the NCBA and be responsive when feedback is needed. A little bit of time from each

designee will collectively enable NC Bankers across our state to have a strong voice

in Washington.

I want to thank Jonathan for his willingness to serve and his leadership in this important

endeavor. Please contact Grace Sampson in the NCBA office with any questions about

the NCBA Grassroots Team at [email protected].

Bank Directors must be well-informed and up-to-date with industry trends in order to adequately perform their jobs and contribute to the success of the bank. In order to become and remain an expert in the financial industry, bank directors absolutely must participate incomprehensive training. Luckily, the NC Bankers Association is here to help. Mark your calendars for this year’s Bank Directors Assembly.

Find more information at www.ncbankers.org.

March 5-6, 2018Raleigh Crabtree Valley Marriott

Carolina Banker | Winter 2017 29

30 Carolina Banker | Winter 2017

© Copyright 2016. CBIZ, Inc. NYSE Listed: CBZ. All rights reserved.

An affordable payroll solution with unmatched customer attention.CBIZ Flex-Pay

Getting the AnswersYou Need From Your

Current Payroll Provider?

Find superior customer service at CBIZ Flex-Pay. We’ll workto improve your payroll services and eliminate frustrations.

Call us today to see how we can save you time and money.

800.457.2143 | 336.245.2261 | www.cbizfl ex-pay.comSherry Burick, Area Sales Director | sherry.burick@cbizfl ex-pay.com

Carolina Banker | Winter 2017 31

32 Carolina Banker | Winter 20173232 CarCar lolina na BanBankerkere | | WinW terter 202 17

NC YOUNG BANKERS CONFERENCE

The second annual NC Young Bankers

Conference is officially in the books! The

conference was held September 24-26 at

the Crowne Plaza Resort in Asheville.

Asheville provided a perfect backdrop for

this year’s festivities. We held our first-ever

cornhole tournament—congratulations to

Michael Daly (Pinnacle Financial

Partners) and Darren Smith (ATM USA)

on taking home the trophy for the win!

The young leaders who attended the

conference left equipped to tackle the

challenges and obstacles the ever-

evolving banking industry presents. As

Kristen Brabble (First Carolina Bank)

eloquently states, “After walking out of

the Young Bankers conference, I feel as

if I can conquer mountains (figuratively

– I’m not Jennifer Pharr-Davis)! The

speakers were motivating and taught us

how to follow our goals. We may not be

the President & CEO by 25, but we

certainly now know how to get there.

The networking opportunities, leadership

speakers, and CEO’s have opened new

ways of thinking for me. I am already

looking forward to the NCYB

Conference in 2018!”

1

2 3

4

CROWN PLAZA RESORT ASHEVILLE, NC

1. JENNIFER PHARR DAVIS ON THE PURSUIT OF ENDURANCEJennifer Pharr Davis - hiker, author, speaker and National Geographic Adventurer of the Year - kicked off the conference with a her inspiring stories of endurance and perseverance throughout her many hikes. Over her adventures, she learned that hard work will only get you so far if you are moving in the wrong direction. She reminded her audience of the value found in being direct and authentic.

2. NETWORKING IS KEYOne of the major themes at the second annual NC Young Bankers Conference was the importance of building and maintaining a strong network. Daniel Williams and Charles Marcom got to know each other a little bit better during a round of speed-networking, where attendees moved around the room to share ideas on banking issues, community engagement and more!

3. BOOTS AND BREW BASHThe first day ended with some less official networking. After a break to explore Asheville, attendees gathered for the Boots and Brew Bash! Live music from North Carolina's own Red Herring Band accompanied an evening of dinner and drinks where Young Bankers had the chance to socialize and make connections in a less formal setting.

4. OFFICIAL CORNHOLE TOURNAMENTIn addition to the warm meals and cold beverages, the night concluded with the NCYB's first official cornhole tournament! Last year's blacklight bowling event was a tough act to follow, but playing cornhole outdoors in the refreshing mountain air was an excellent way to wind down after a long day, and the friendly competition made it a lively event.

Carolina Banker | Winter 2017 33CarCarCaroliolina na na BanBankerker || WinWinnnnnterterterterrterterterterrerrterrtterteteere 2022020200011717777777717171771717777717 333333333333333333333333333

8

5 6

7

5. MEREDITH ELLIOTT POWELL ON NETWORKING AND COMPETITIONIn the early hours of day two, business growth speaker Meredith Elliott Powell got our Young Bankers up and moving in an interactive session on the power of professional relationships, and she returned at the end of the evening to give tips on how to succeed no matter what the economy does. What was her advice? Follow three steps: Vision, Strategy and Execution.

6. PETER GWALTNEY ON WHAT'S HAPPENING IN D.C.NCBA President & CEO Peter Gwaltney delivered an impactful presentation on government relations and how our Young Bankers can get involved. There is a lot going on in D.C., and Peter discussed the effect this has on the banking industry. Several Young Bankers reported that they brought these tips back to their own institutions and were inspired to take part in grassroots initiatives!

7. THE CEO PANELNCBA President & CEO Peter Gwaltney also presided over a discussion between two of our state's most successful bankers: the CEO Panel featuring Asheville Savings Bank's Suzanne DeFerie and Carolina Alliance Bank's John Kimberly. The dialogue taught attendees important lessons on leadership and how to reach for it.

8. THE NCYB ADVISORY BOARDThank you to the members of the NCYB Advisory Board in attendance (L to R): Jason Rapuano, Paragon Bank; Kristen Brabble, First Carolina Bank; David Saul, Southern Bank & Trust; Michael Cortes, TD Bank; Jed Orman, Fidelity Bank; Katheryn Willard, BB&T; Meredith Begley, Black Mountain Savings Bank; David Beaver, Uwharrie Bank; Katrina Blumetti, Morganton Savings Bank; Blair Jernigan, NCBA; John Parker, KS Bank; and Hope Moore, Union Bank.

34 Carolina Banker | Winter 201734344 CarCaroliolinana BanBaB nkerkerkeer | || WinWinWinterter 202001717

MANAGEMENT TEAM CONFERENCE

The NCBA hosted our annual Management Team Conference

October 23-24 at the Grandover Resort. Over 80 attendees came

together for this event to network and learn. Attendees learned

about the future of the bank branch, heard an economic update,

how to apply lean six sigma to the industry, the effect and expectations that Amazon has set on your customer interactions,

heard from our State Treasurer and learned more about fintech and the impact on the industry.

1. ANTHONY BURNETT ON THE FUTURE OF THE BRANCHThe branch isn't dead - it's merely evolving to serve a new purpose. That was the conclusion that Anthony Burnett, Customer Experience Director at LEVEL5, has come to in his presentation on community banking and how to respond to new consumer demands.

2. CATCHING UP ON READING MATERIALWhat's that Jeff Smith of New Republic Savings Bank is perusing through during one of the breaks? That's this fall's Carolina Banker! 3. CRAIG DISMUKE AND THE ECONOMIC OUTLOOKCraig Dismuke, EVP and Chief Economist at Vining Sparks, used powerful visuals to explain the economic developments we have seen in 2017 and discussed what to expect moving forward.

4. DALE FOLWELL ON THE PRICE OF PROMISES"As State Treasurer, issues aren't political or emotional - they are mathematical." Those were the words of Treasurer Folwell as he discussed the challenges that accompany his task of balancing the state's budget. As Keeper of the Public Purse, the promises that were made touch 1 out of every 10 adult North Carolinians, and Treasurer Folwell discussed just how to keep these promises.

5. RECEPTION IN THE MARKETPLACEAt the end of the first day, friends from all over had the chance to come together, to discuss the presentations they had just witnessed and to simply catch up. Gathered here are Robert Ladd (Providence Bank), Charles Canaday (American National Bank), and past NCBA Chairmen Jerry Ocheltree (Carolina Trust Bank) and Bob Hatley (Paragon Bank).

1

4

2

3

5

THANKS TO OUR SPONSORS:

6 & 7. “HOW MANY OF YOU HAVE USED MOBILE PAYMENT APPS?”That question was posed by Dave DeFazio, Partner at StrategyCorps, during his presentation on the changing ways that Americans are making purchases and how banks can compete. “When building your mobile banking app,” he said, “you aren’t just competing with other mobile banking platforms. You are competing with every app and the expectations they set.”

8. AUDIENCE ENJOYMENTBob Washburn, President & CEO of LifeStore bank, and the rest of the crowded room laugh at one of the many amusing anecdotes that presenters use to get their point across. While this is certainly a serious conference, there’s no reason it shouldn’t entertain!

9. GROUP DINNER AT THE HOTELAfter a busy day full of learning and discussing, everybody had worked up an appetite. The Grand Ballroom at the Grandover Resort was the setting for this meal filled with good food and good conversation. It was an opportunity to network, converse, and, of course, to eat.

10. NCBA FOUNDATION GOLF TOURNAMENTAfter the Management Team Conference had ended, many stayed to take part in the first annual NCBA Foundation Golf Tournament. NCBA President & CEO Peter Gwaltney left the competitors with some parting words before they hit the green. Proceeds from the event went to the financial literacy efforts of the NCBA Foundation.

6 7

8

109

36 Carolina Banker | Winter 2017363 Carolina Banker | Winter 2017

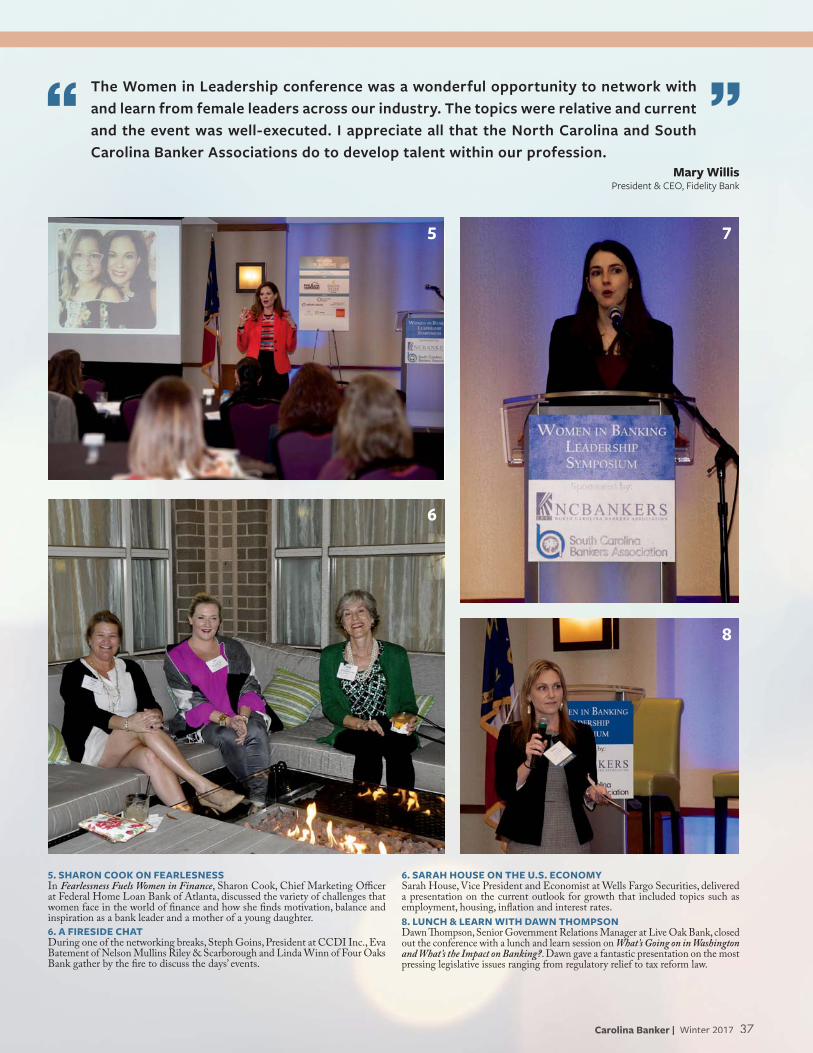

WOMEN IN BANKING LEADERSHIP SYMPOSIUM

The NCBA and SCBA hosted 70 women at the 4th Annual Women in

Banking Leadership Symposium November 6-7 at the Renaissance

Charlotte SouthPark Hotel. The conference was the perfect opportunity

to network and learn with other female leaders in the industry. Attendees

left with the necessary skills to become more effective leaders and bankers

thanks to the strong lineup of accomplished businesswomen.