cash flow statement mf h

TRANSCRIPT

STATEMENT OF CASH FLOWS

January 18, 2015 1DMH

Mahfuzul Hoque PhD

Professor

Department of Accounting & Information Systems

Faculty of Business Studies

University of Dhaka

1. Indicate the usefulness of the statement of cash flows.

2. Distinguish among operating, investing, & financing

activities.

3. Explain the impact of the product life cycle on a

company’s cash flows.

4. Prepare a statement of cash flows using the indirect

method.

5. Use the statement of cash flows to evaluate a company.

Study Objectives

January 18, 2015 2DMH

Usefulness

Classifications

Significant noncash

activities

Format

Corporate life cycle

Preparation

Indirect & direct

methods

Step 1: Operating

activities

Step 2: Investing &

financing activities

Step 3: Net change in

cash

Free cash flow

Assessing liquidity &

solvency

The Statement of

Cash Flows:

Usefulness &

Format

Preparing the

Statement of Cash

Flows—Indirect

Method

Using Cash Flows to

Evaluate a

Company

Statement of Cash Flows

January 18, 2015 3DMH

Provides information to help assess:

1. Entity’s ability to generate future cash flows.

2. Entity’s ability to pay dividends & obligations.

3. Reasons for difference between net income & net cash

provided (used) by operating activities.

4. Cash investing & financing transactions during the

period.

Usefulness & Format

Usefulness of the Statement of Cash Flows

January 18, 2015 4DMH

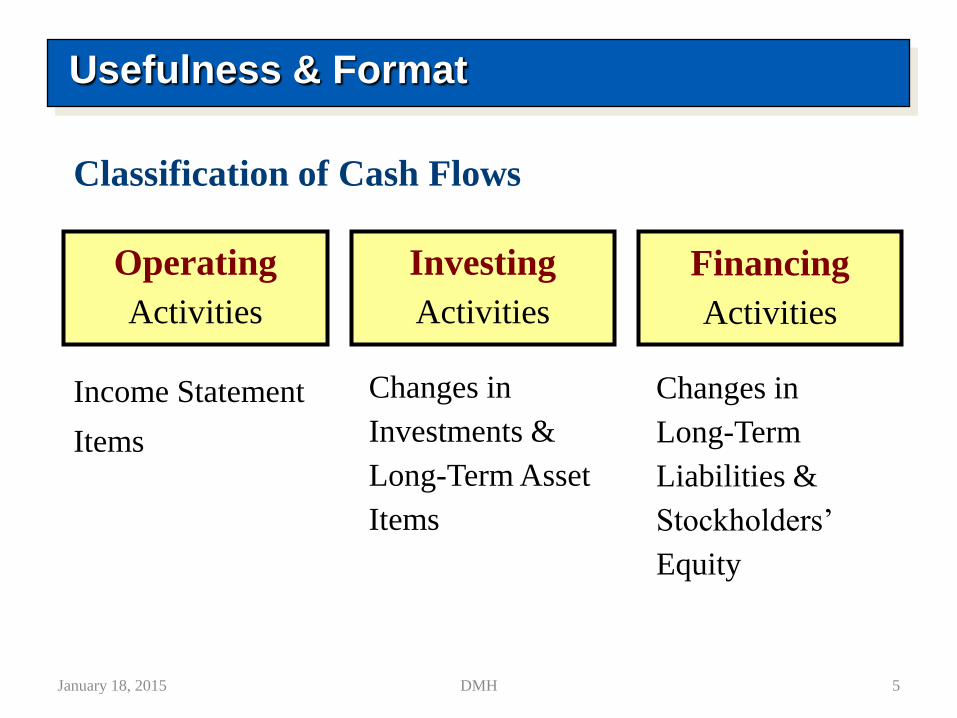

Classification of Cash Flows

Usefulness & Format

Income Statement

Items

Operating

Activities

Changes in

Investments &

Long-Term Asset

Items

Investing

Activities

Changes in

Long-Term

Liabilities &

Stockholders’

Equity

Financing

Activities

January 18, 2015 5DMH

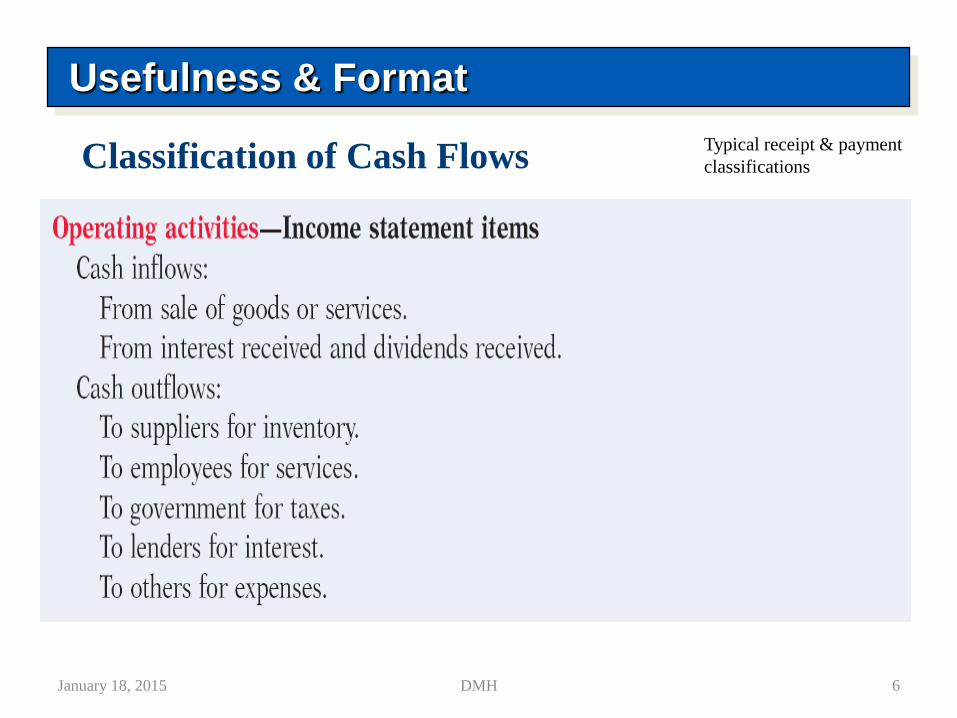

Usefulness & Format

Typical receipt & payment

classificationsClassification of Cash Flows

January 18, 2015 6DMH

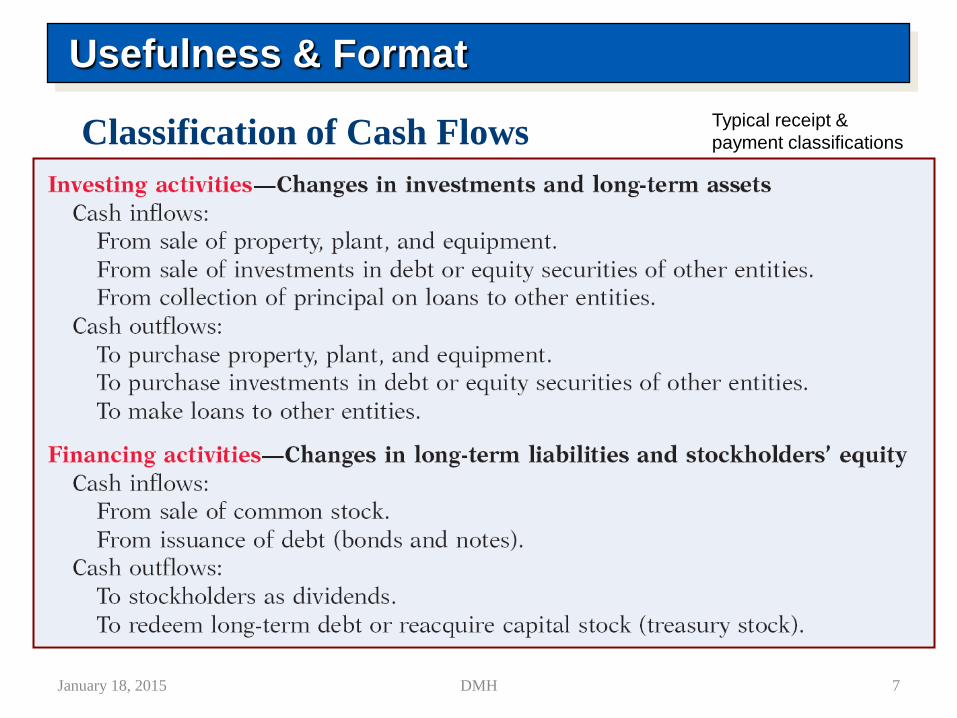

Usefulness & Format

Typical receipt &

payment classificationsClassification of Cash Flows

January 18, 2015 7DMH

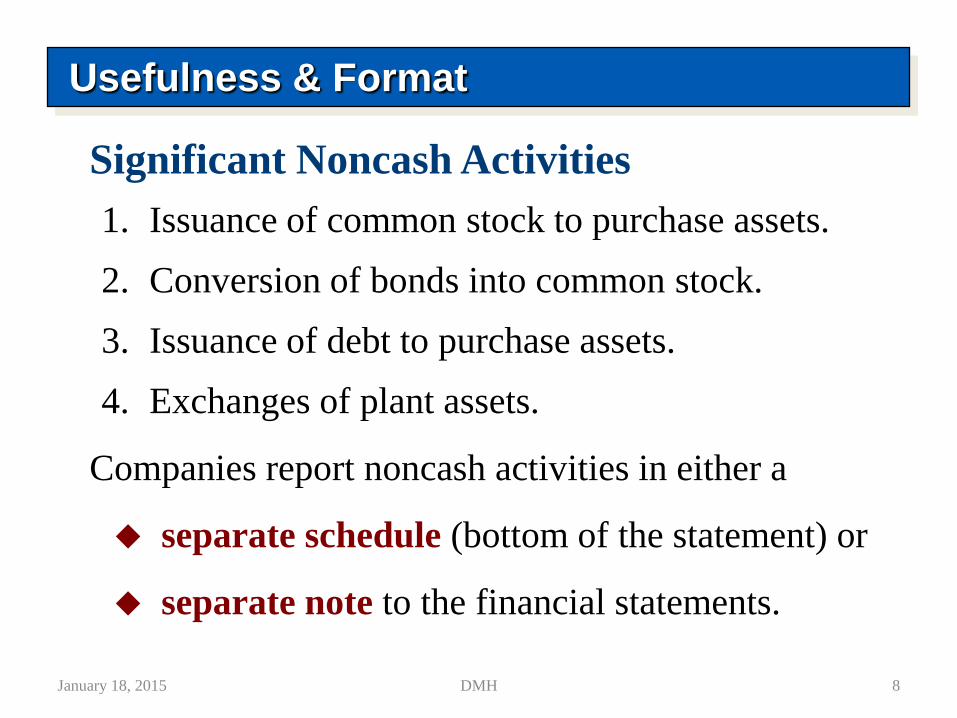

1. Issuance of common stock to purchase assets.

2. Conversion of bonds into common stock.

3. Issuance of debt to purchase assets.

4. Exchanges of plant assets.

Companies report noncash activities in either a

separate schedule (bottom of the statement) or

separate note to the financial statements.

Usefulness & Format

Significant Noncash Activities

January 18, 2015 8DMH

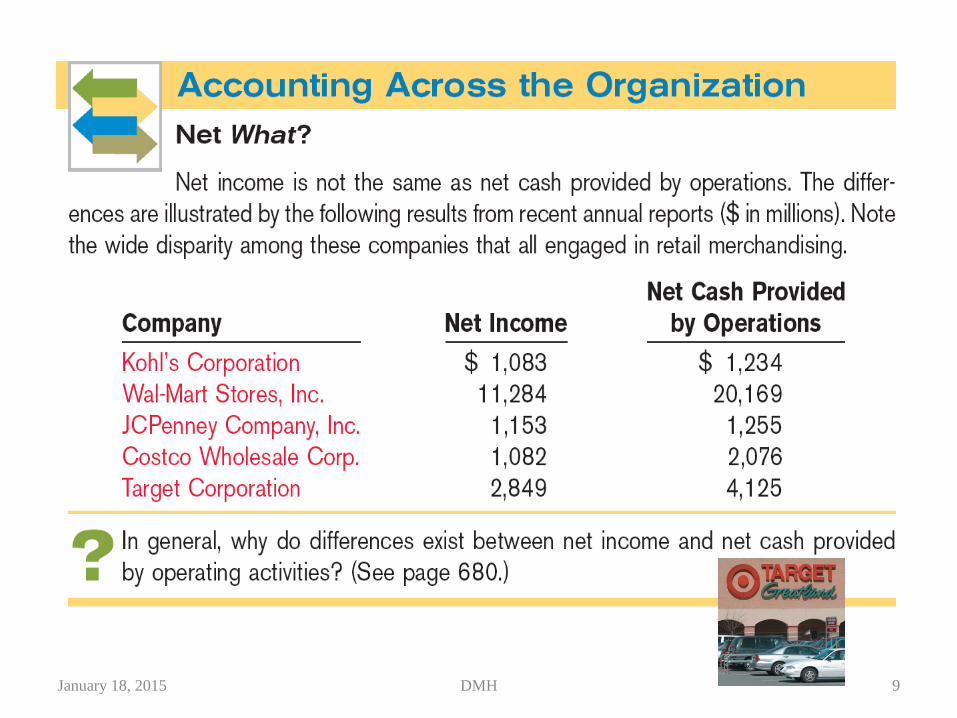

January 18, 2015 9DMH

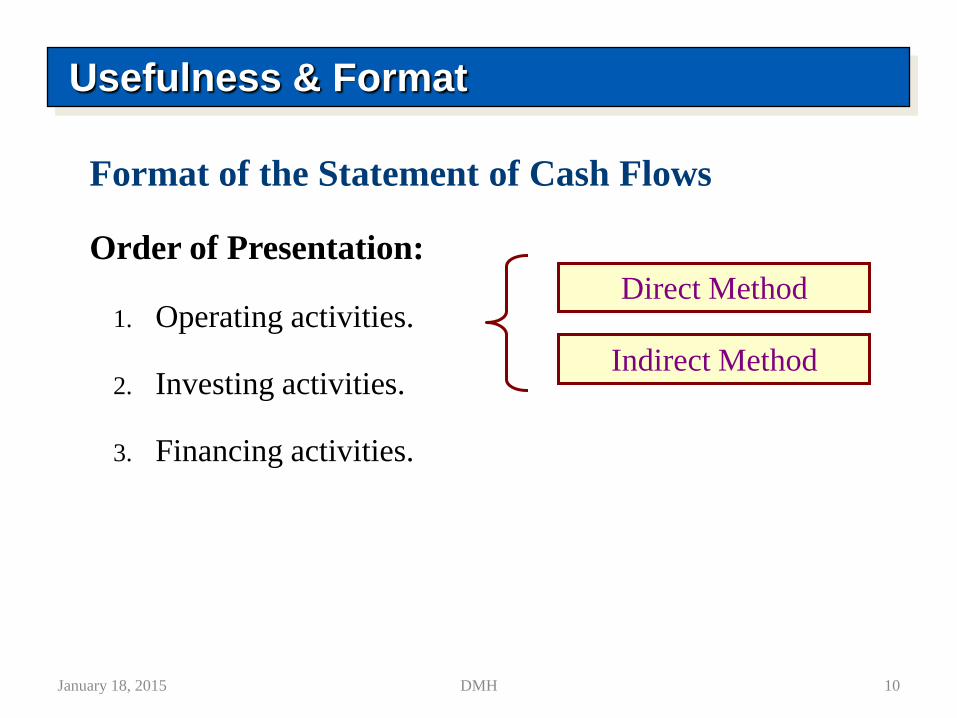

Order of Presentation:

1. Operating activities.

2. Investing activities.

3. Financing activities.

Direct Method

Indirect Method

Usefulness & Format

Format of the Statement of Cash Flows

January 18, 2015 10DMH

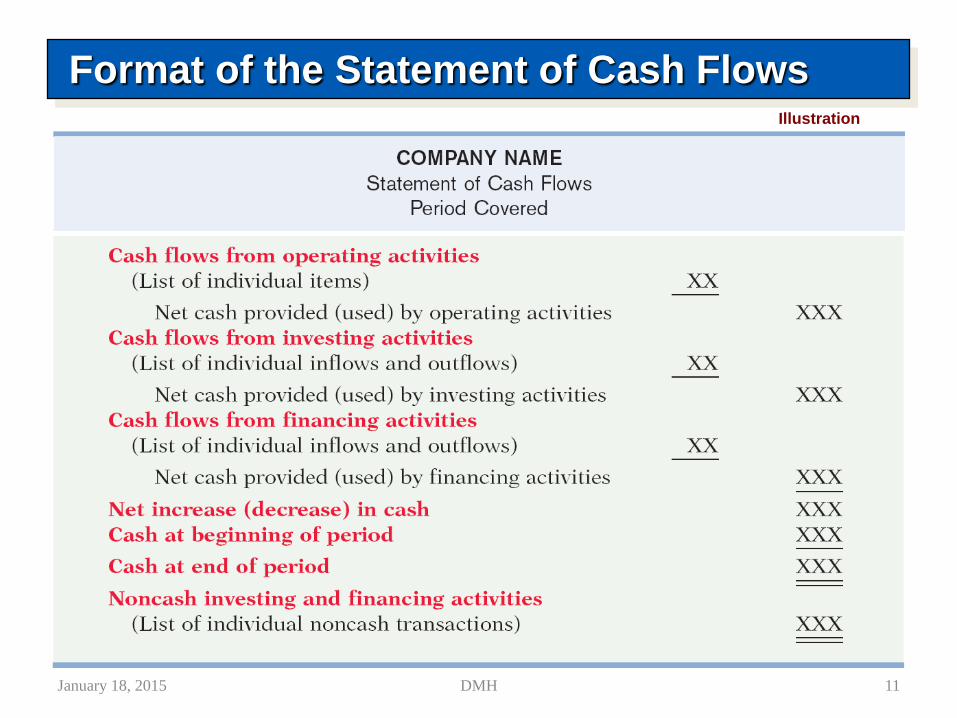

Illustration

Format of the Statement of Cash Flows

January 18, 2015 11DMH

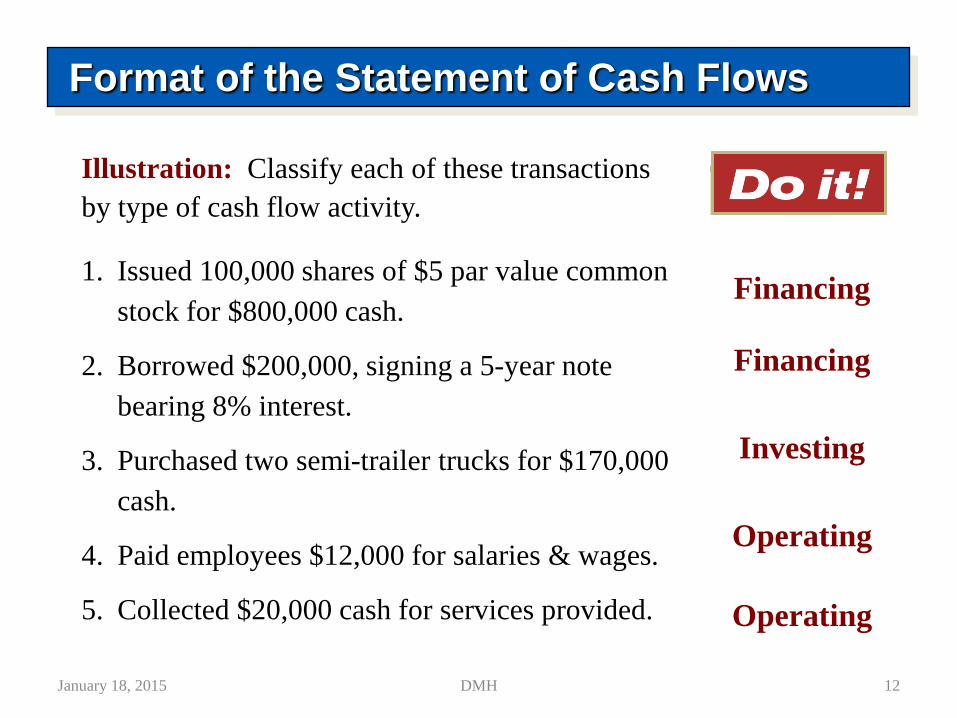

Illustration: Classify each of these transactions

by type of cash flow activity.

Format of the Statement of Cash Flows

1. Issued 100,000 shares of $5 par value common

stock for $800,000 cash.

2. Borrowed $200,000, signing a 5-year note

bearing 8% interest.

3. Purchased two semi-trailer trucks for $170,000

cash.

4. Paid employees $12,000 for salaries & wages.

5. Collected $20,000 cash for services provided.

Financing

Financing

Investing

Operating

Operating

January 18, 2015 12DMH

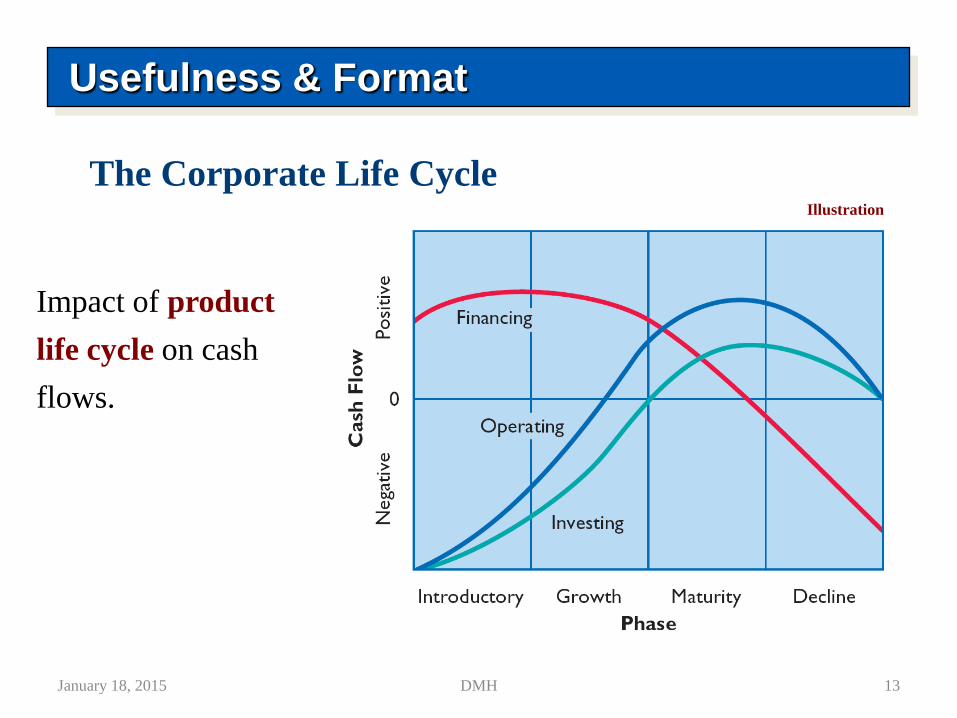

Usefulness & Format

Impact of product

life cycle on cash

flows.

Illustration

The Corporate Life Cycle

January 18, 2015 13DMH

January 18, 2015 14DMH

Three Sources of Information:

1. Comparative balance sheets

2. Current income statement

3. Additional information

Usefulness & Format

Preparing the Statement of Cash Flows

January 18, 2015 15DMH

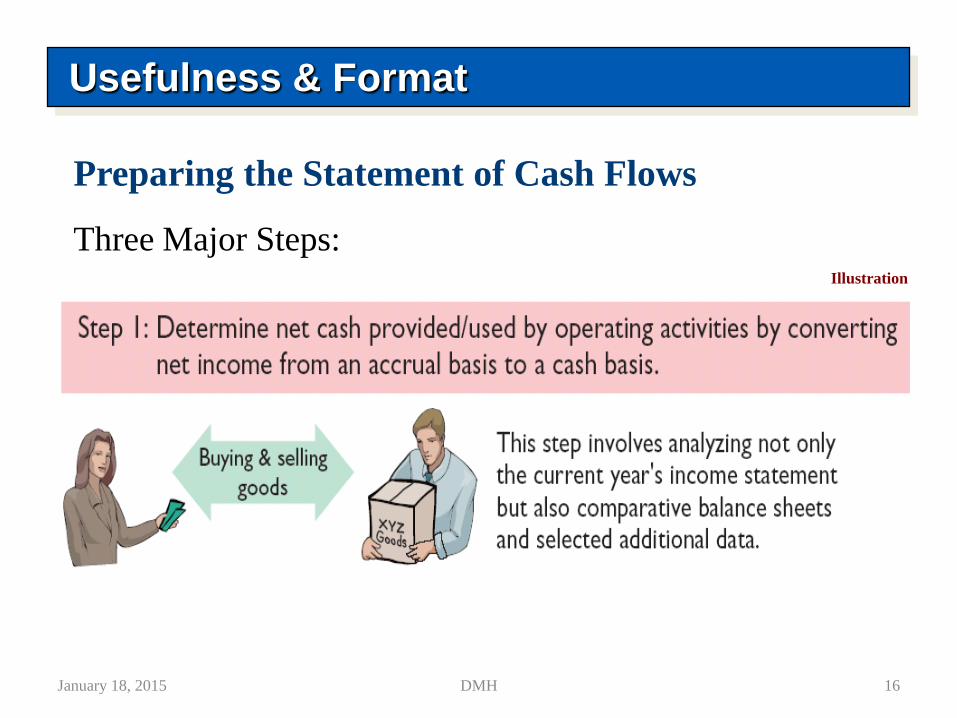

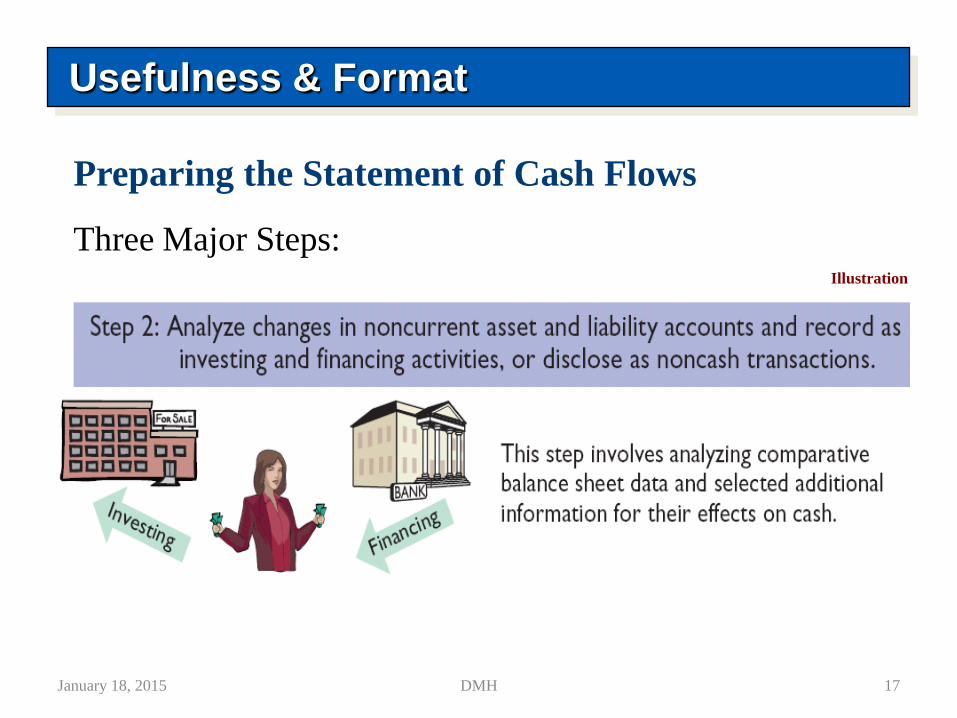

Usefulness & Format

Three Major Steps:Illustration

Preparing the Statement of Cash Flows

January 18, 2015 16DMH

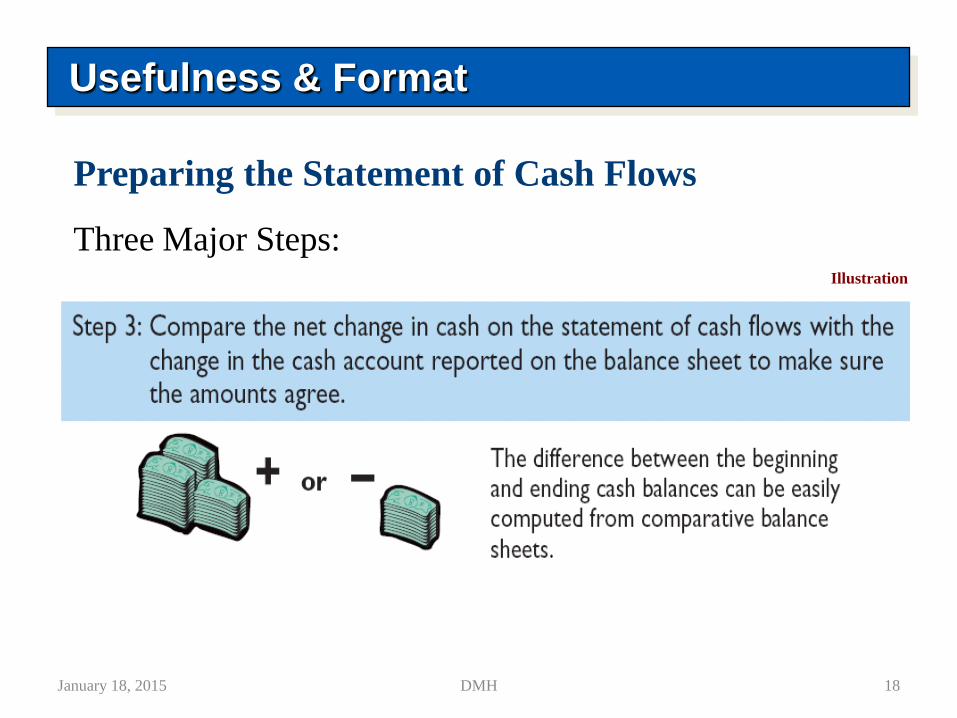

Usefulness & Format

Three Major Steps:Illustration

Preparing the Statement of Cash Flows

January 18, 2015 17DMH

Usefulness & Format

Three Major Steps:Illustration

Preparing the Statement of Cash Flows

January 18, 2015 18DMH

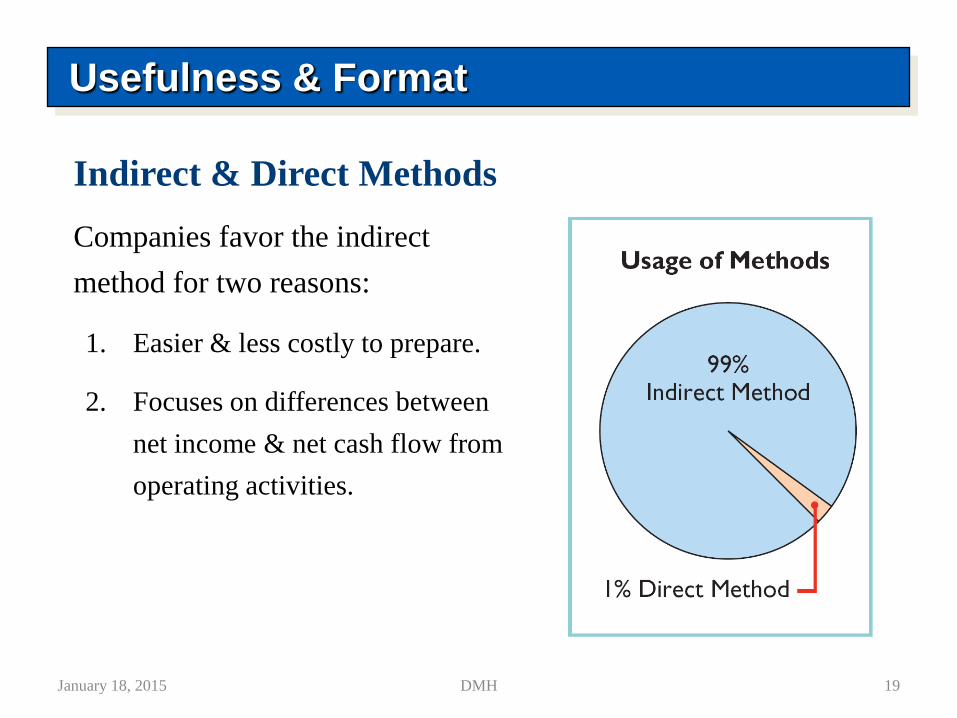

Companies favor the indirect

method for two reasons:

1. Easier & less costly to prepare.

2. Focuses on differences between

net income & net cash flow from

operating activities.

Usefulness & Format

Indirect & Direct Methods

January 18, 2015 19DMH

January 18, 2015 20DMH

Statement of Cash Flows

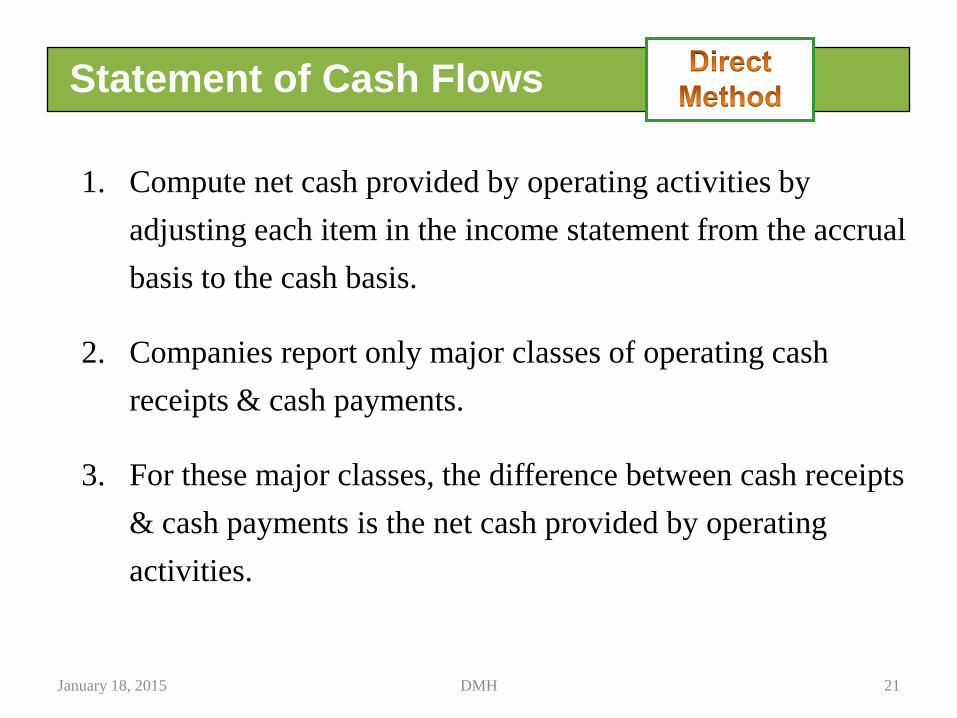

1. Compute net cash provided by operating activities by

adjusting each item in the income statement from the accrual

basis to the cash basis.

2. Companies report only major classes of operating cash

receipts & cash payments.

3. For these major classes, the difference between cash receipts

& cash payments is the net cash provided by operating

activities.

January 18, 2015 21DMH

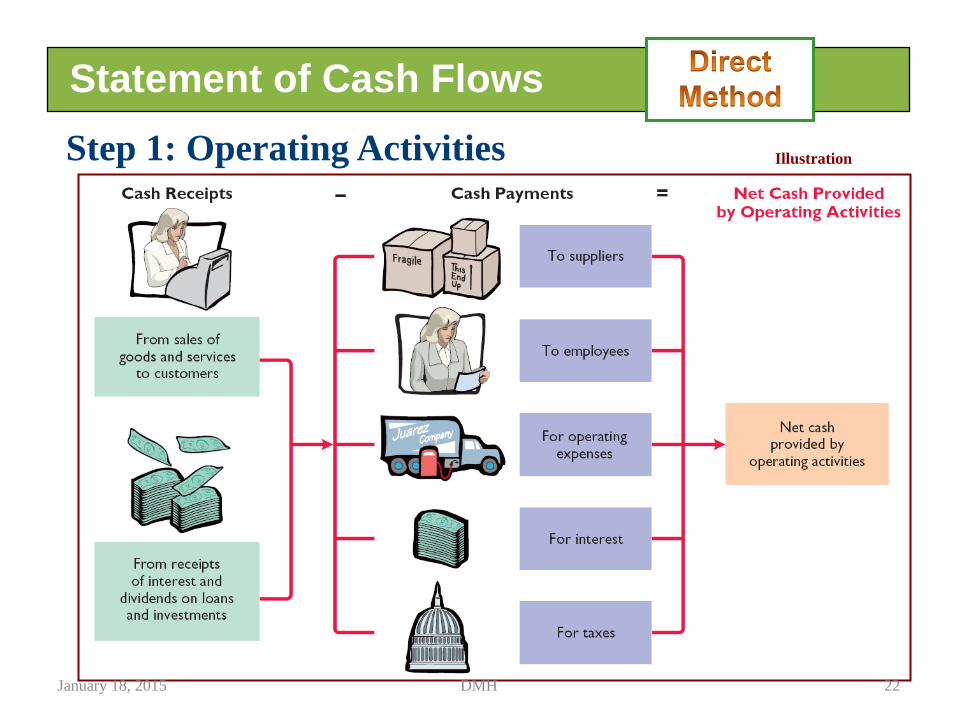

IllustrationStep 1: Operating Activities

Statement of Cash Flows

January 18, 2015 22DMH

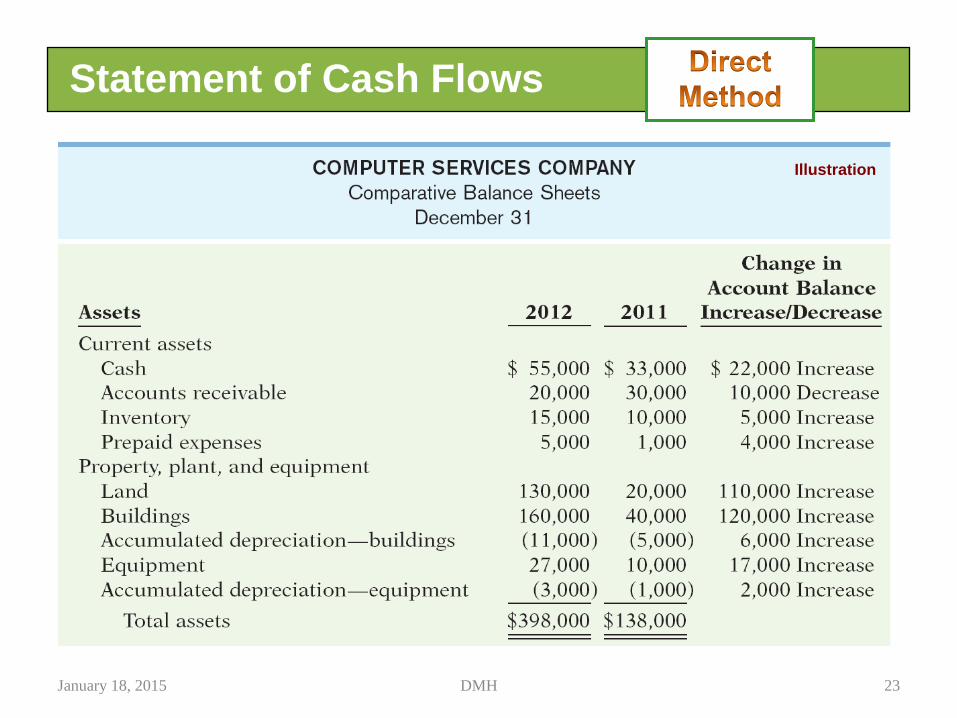

Illustration

Statement of Cash Flows

January 18, 2015 23DMH

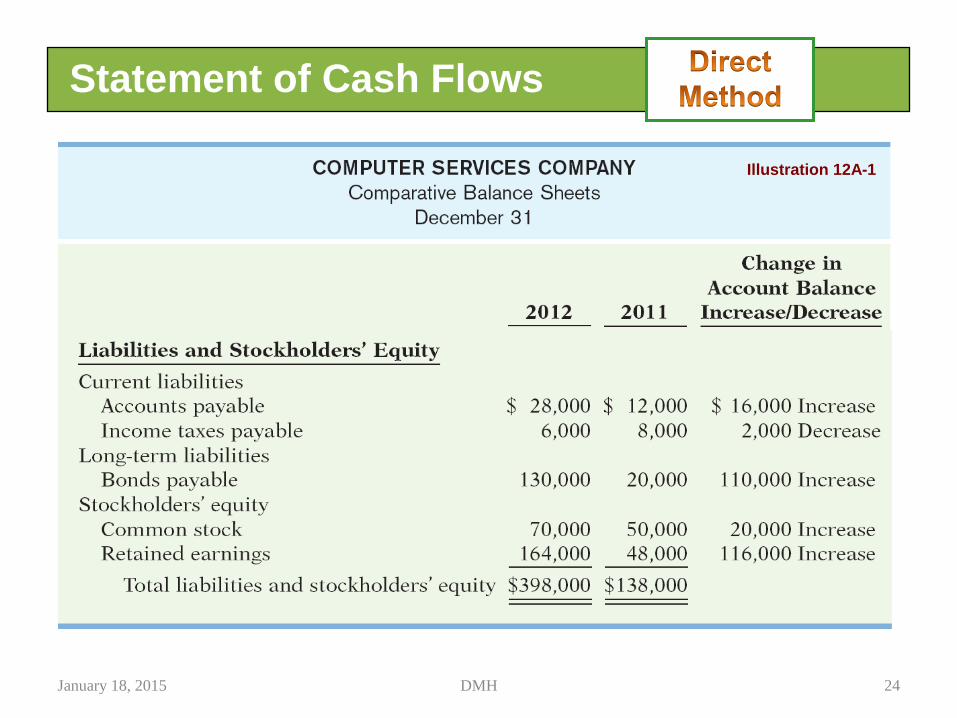

Illustration 12A-1

Statement of Cash Flows

January 18, 2015 24DMH

Illustration 12A-1

January 18, 2015 25DMH

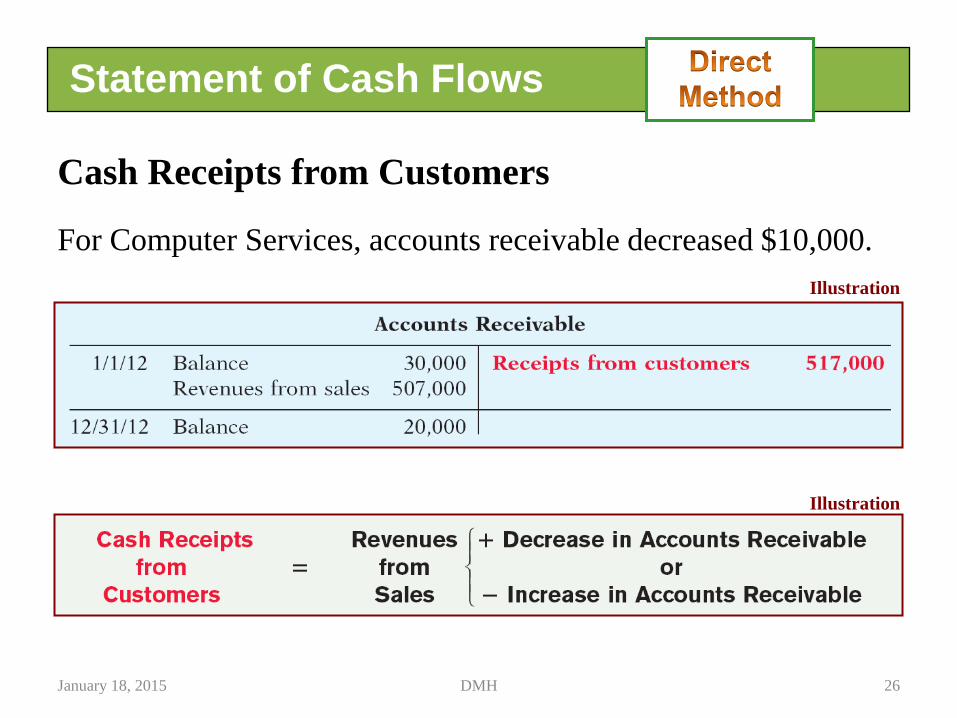

Illustration

Cash Receipts from Customers

For Computer Services, accounts receivable decreased $10,000.

Illustration

Statement of Cash Flows

January 18, 2015 26DMH

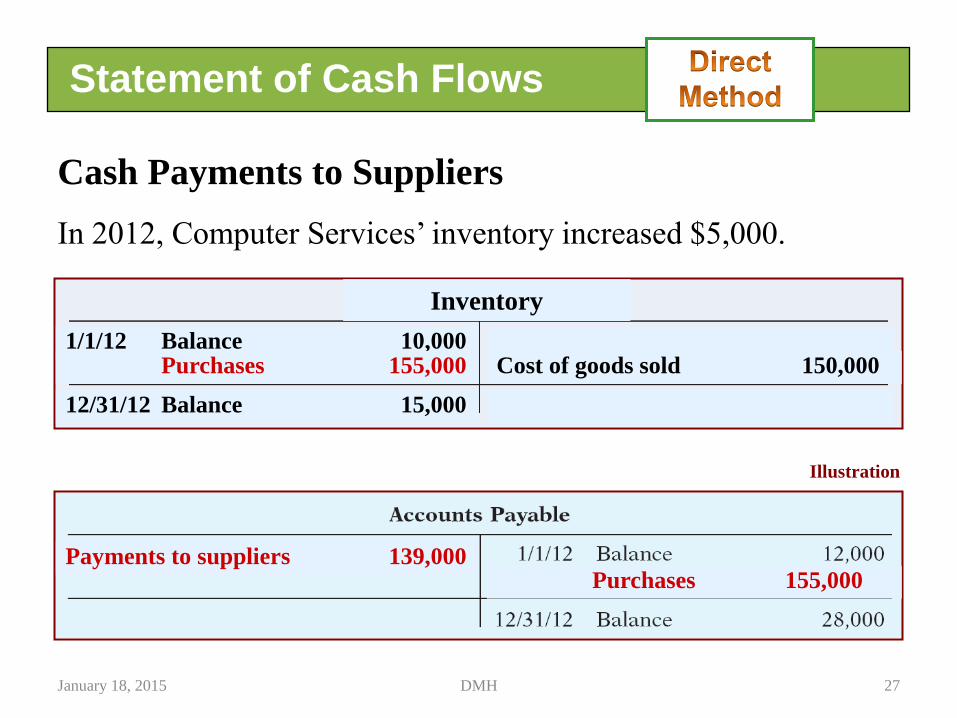

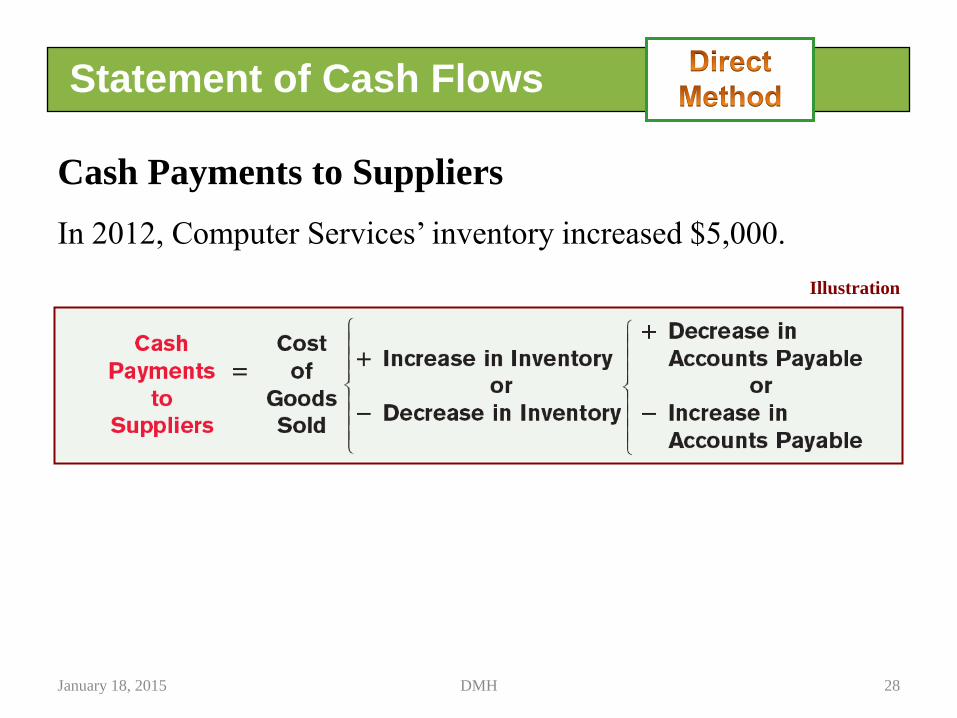

Cash Payments to Suppliers

In 2012, Computer Services’ inventory increased $5,000.

Illustration

Inventory

1/1/12 Balance 10,000

12/31/12 Balance 15,000

Purchases 155,000 Cost of goods sold 150,000

Purchases 155,000Payments to suppliers 139,000

Statement of Cash Flows

January 18, 2015 27DMH

Illustration

Cash Payments to Suppliers

In 2012, Computer Services’ inventory increased $5,000.

Statement of Cash Flows

January 18, 2015 28DMH

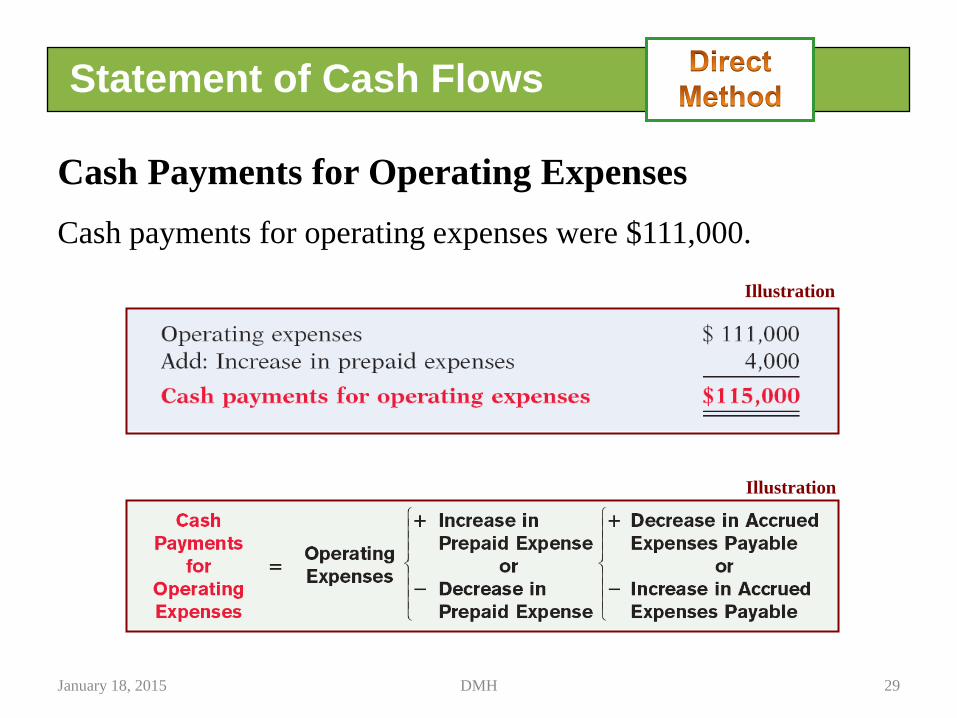

Illustration

Cash Payments for Operating Expenses

Cash payments for operating expenses were $111,000.

Illustration

Statement of Cash Flows

January 18, 2015 29DMH

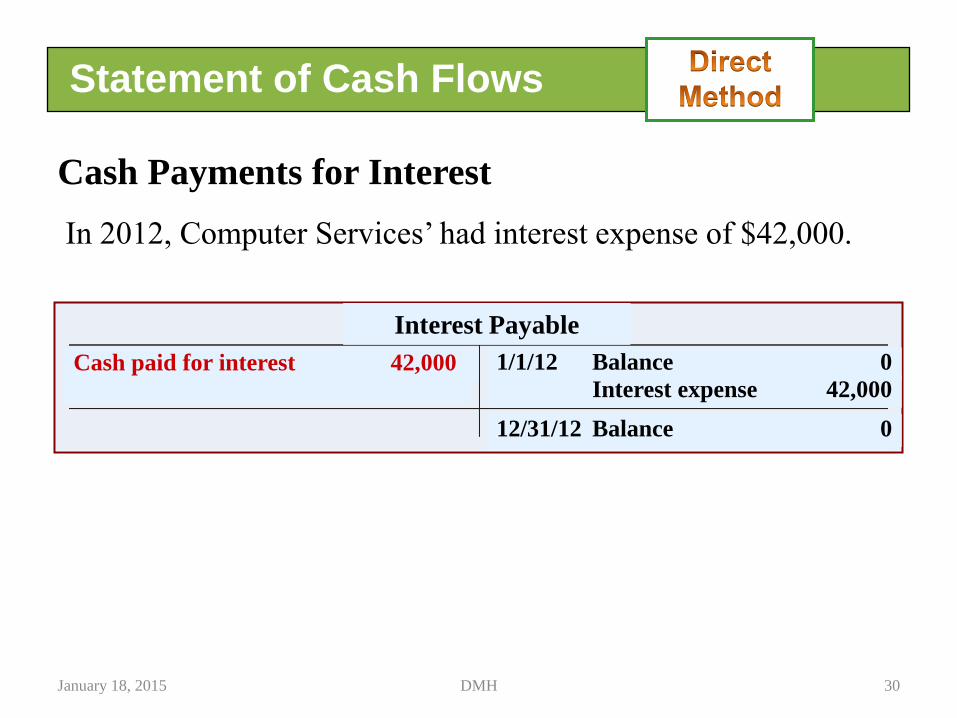

Cash Payments for Interest

In 2012, Computer Services’ had interest expense of $42,000.

Interest Payable

1/1/12 Balance 0

12/31/12 Balance 0

Interest expense 42,000

Cash paid for interest 42,000

Statement of Cash Flows

January 18, 2015 30DMH

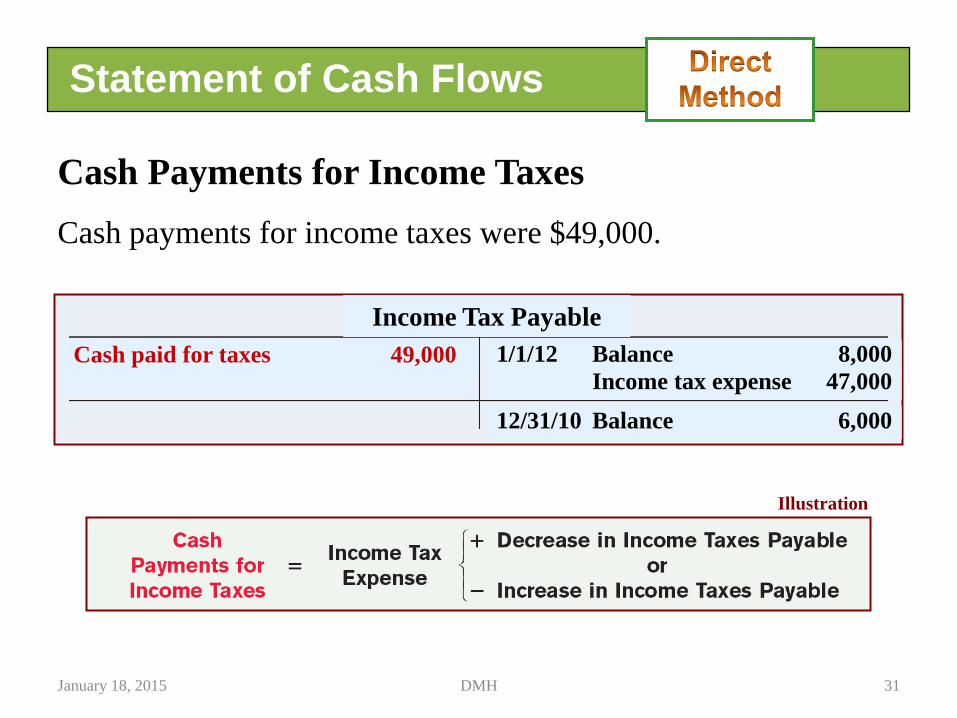

Cash Payments for Income Taxes

Cash payments for income taxes were $49,000.

Illustration

Income Tax Payable

1/1/12 Balance 8,000

12/31/10 Balance 6,000

Income tax expense 47,000

Cash paid for taxes 49,000

Statement of Cash Flows

January 18, 2015 31DMH

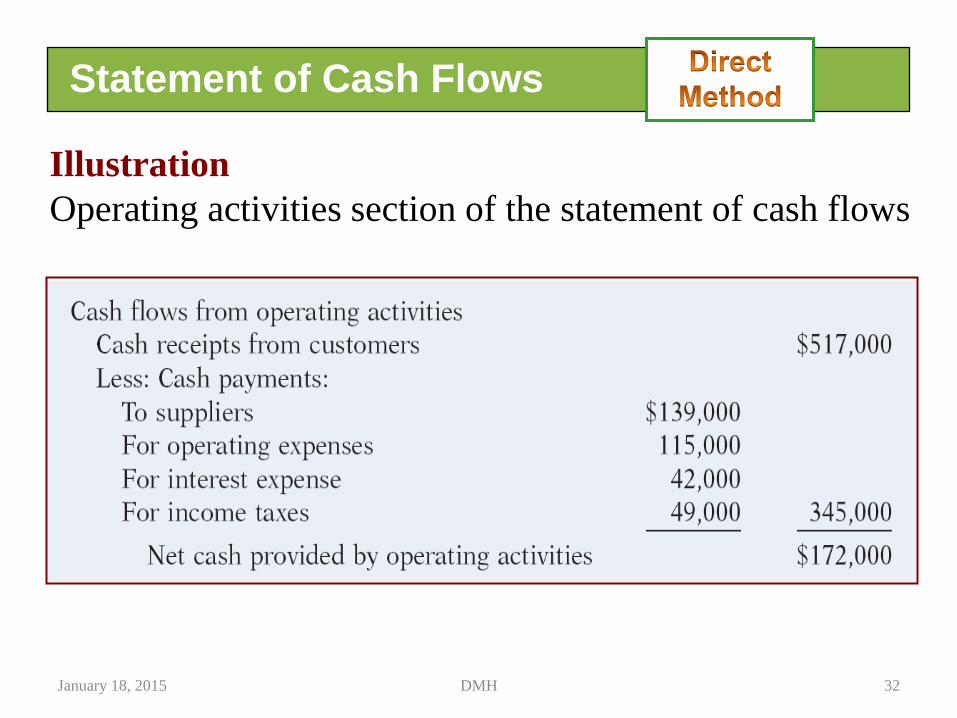

Illustration

Operating activities section of the statement of cash flows

Statement of Cash Flows

January 18, 2015 32DMH

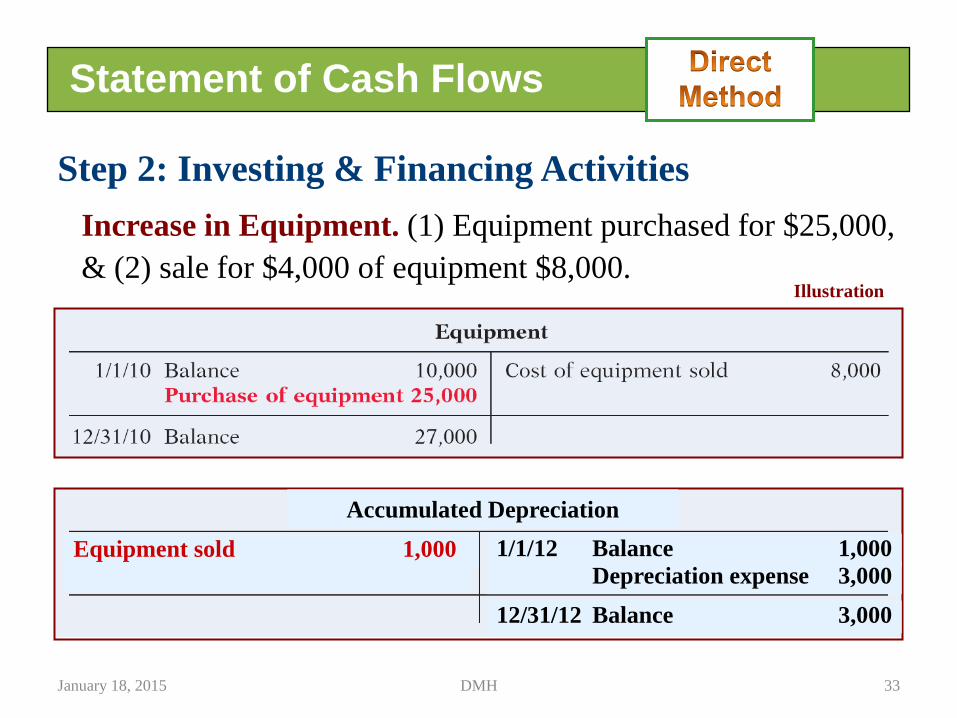

Increase in Equipment. (1) Equipment purchased for $25,000,

& (2) sale for $4,000 of equipment $8,000.

Step 2: Investing & Financing Activities

Accumulated Depreciation

1/1/12 Balance 1,000

12/31/12 Balance 3,000

Depreciation expense 3,000

Equipment sold 1,000

Illustration

Statement of Cash Flows

January 18, 2015 33DMH

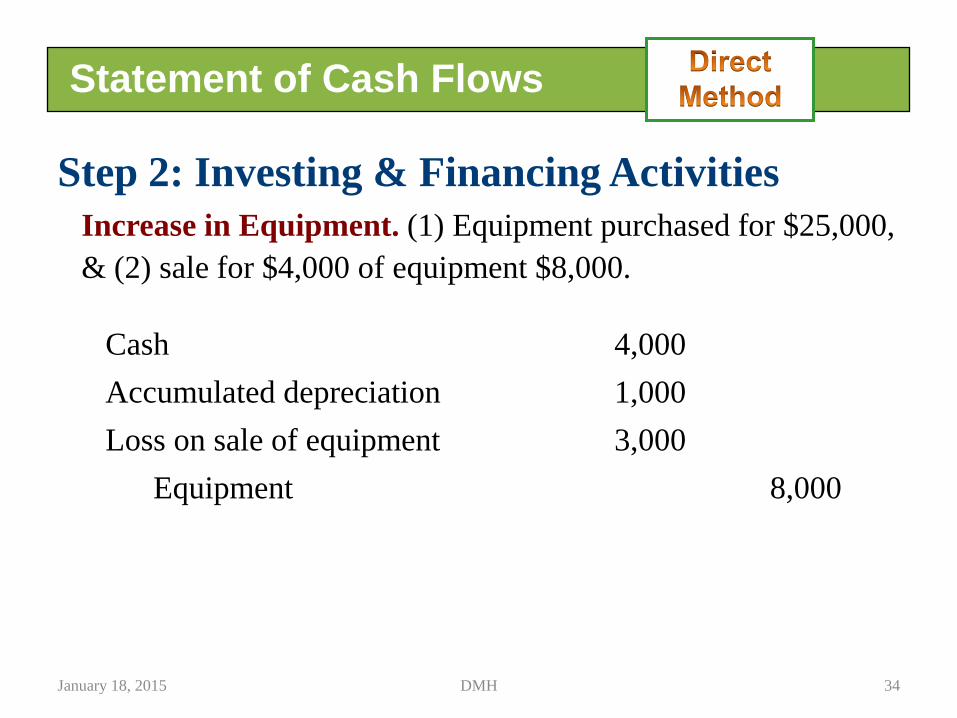

Increase in Equipment. (1) Equipment purchased for $25,000,

& (2) sale for $4,000 of equipment $8,000.

Step 2: Investing & Financing Activities

Cash 4,000

Accumulated depreciation 1,000

Loss on sale of equipment 3,000

Equipment 8,000

Statement of Cash Flows

January 18, 2015 34DMH

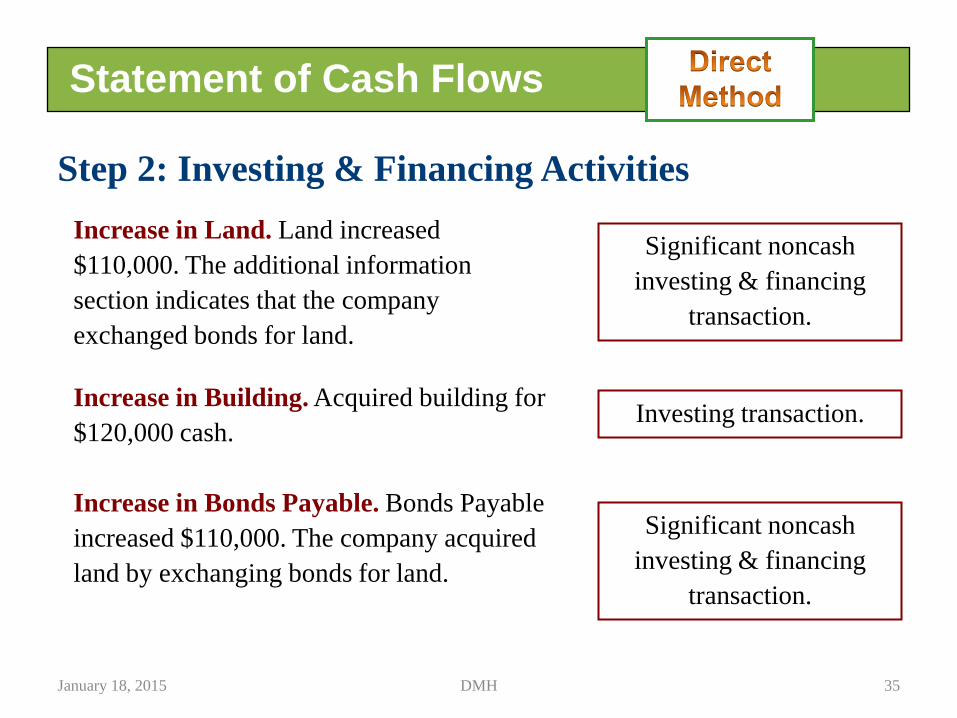

Increase in Land. Land increased

$110,000. The additional information

section indicates that the company

exchanged bonds for land.

Step 2: Investing & Financing Activities

Significant noncash

investing & financing

transaction.

Increase in Bonds Payable. Bonds Payable

increased $110,000. The company acquired

land by exchanging bonds for land.

Significant noncash

investing & financing

transaction.

Increase in Building. Acquired building for

$120,000 cash.Investing transaction.

Statement of Cash Flows

January 18, 2015 35DMH

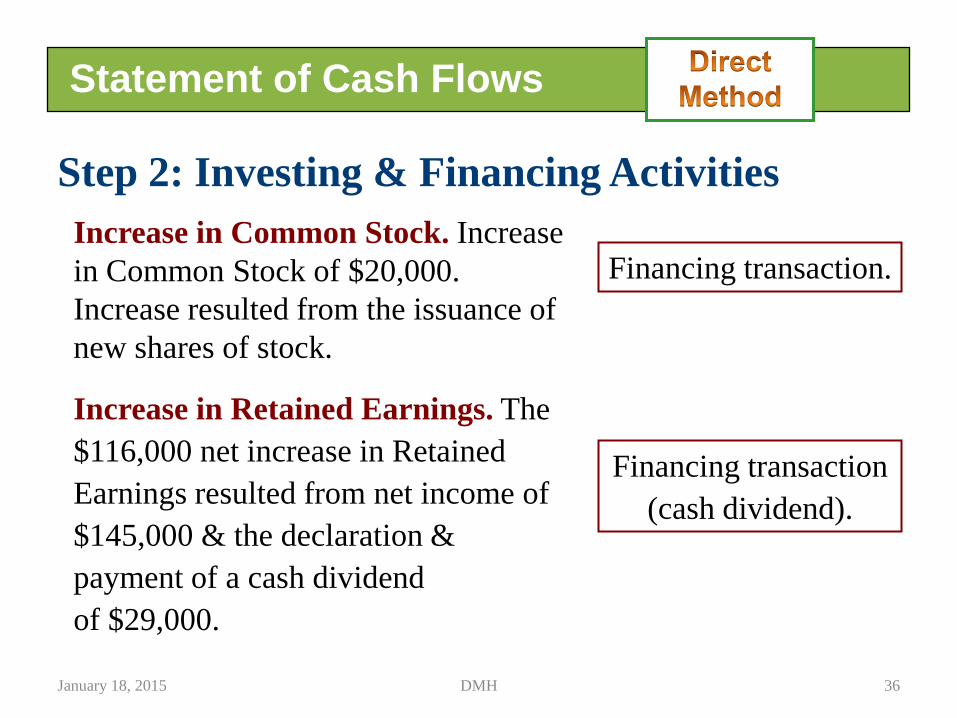

Increase in Common Stock. Increase

in Common Stock of $20,000.

Increase resulted from the issuance of

new shares of stock.

Step 2: Investing & Financing Activities

Increase in Retained Earnings. The

$116,000 net increase in Retained

Earnings resulted from net income of

$145,000 & the declaration &

payment of a cash dividend

of $29,000.

Financing transaction

(cash dividend).

Financing transaction.

Statement of Cash Flows

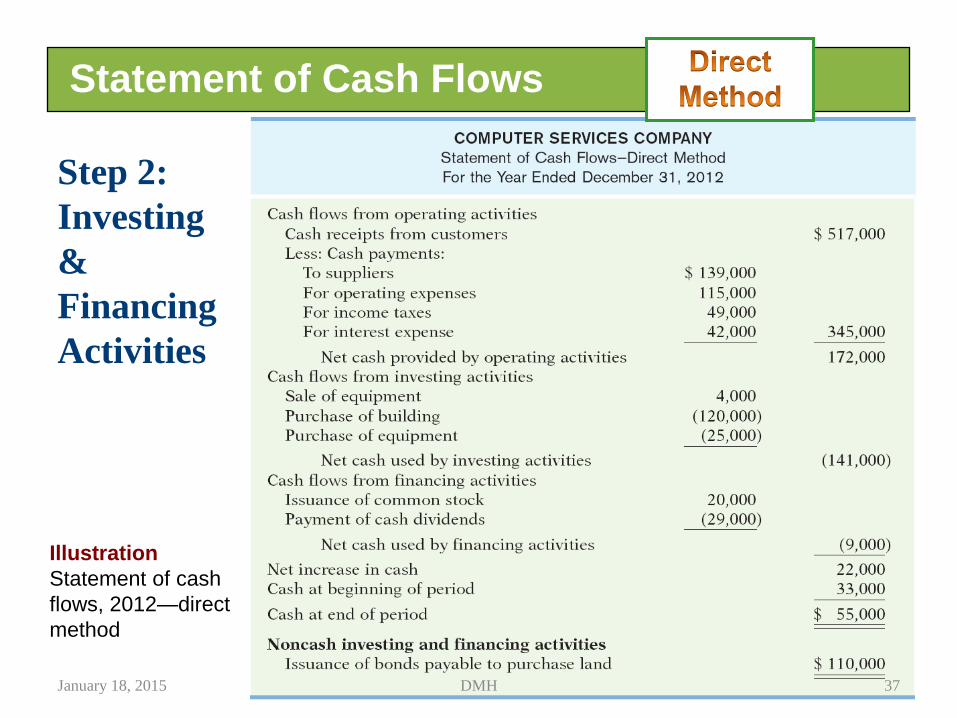

January 18, 2015 36DMH

Step 2:

Investing

&

Financing

Activities

Illustration

Statement of cash

flows, 2012—direct

method

Statement of Cash Flows

January 18, 2015 37DMH

Compare the net change in cash on the Statement of Cash Flows

with the change in the cash account reported on the Balance

Sheet to make sure the amounts agree.

Statement of Cash Flows

January 18, 2015 38DMH

Preparing the

Statement of Cash Flows

Indirect Method

January 18, 2015 39DMH

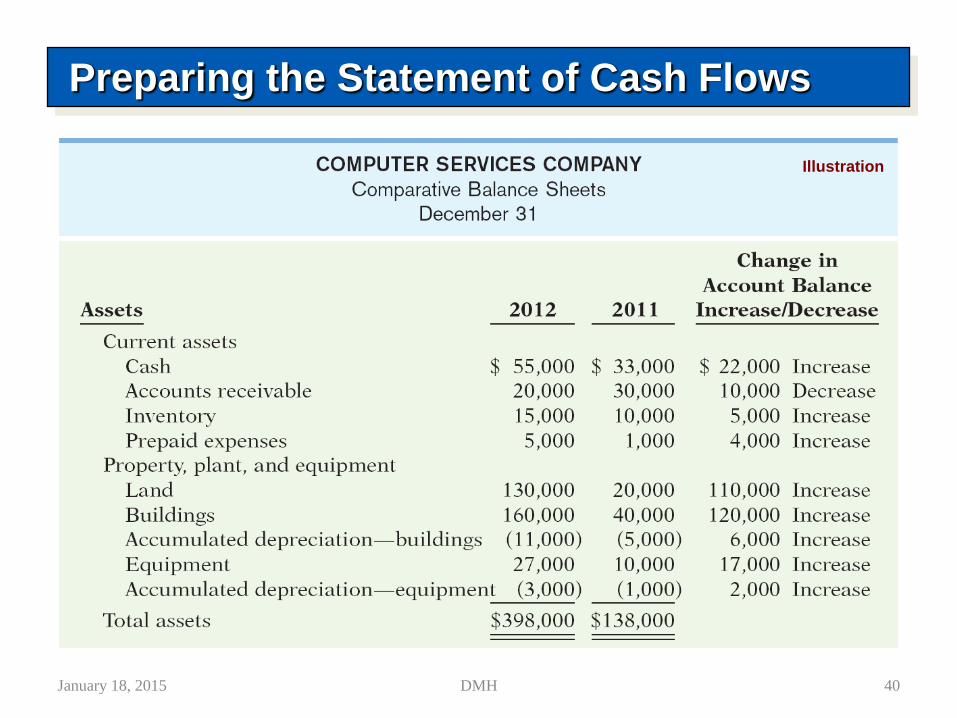

Preparing the Statement of Cash Flows

Illustration

January 18, 2015 40DMH

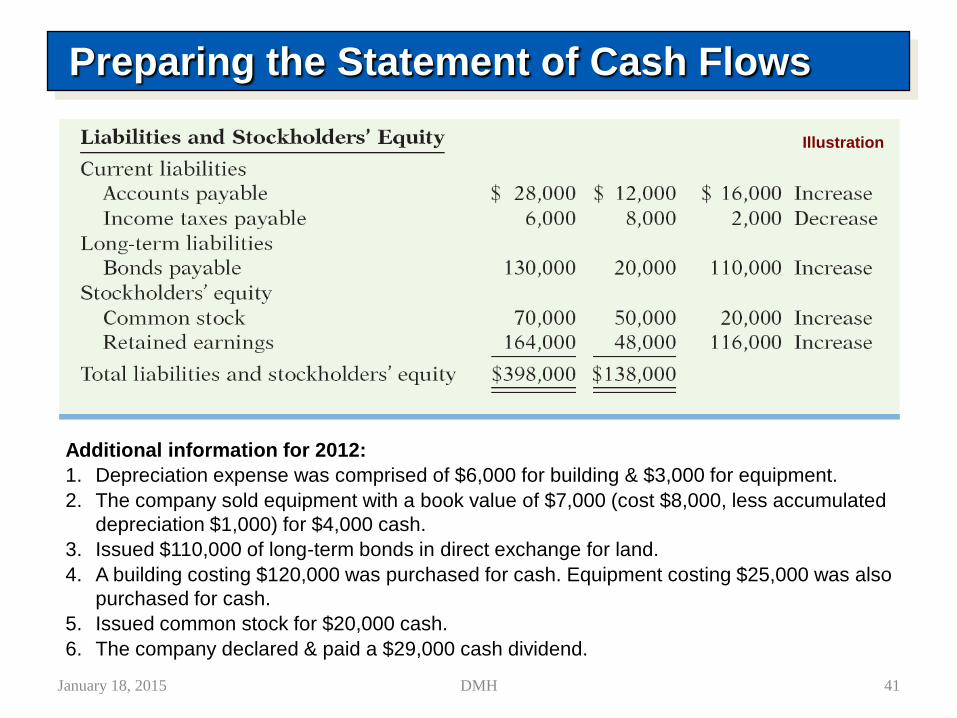

Preparing the Statement of Cash Flows

Illustration

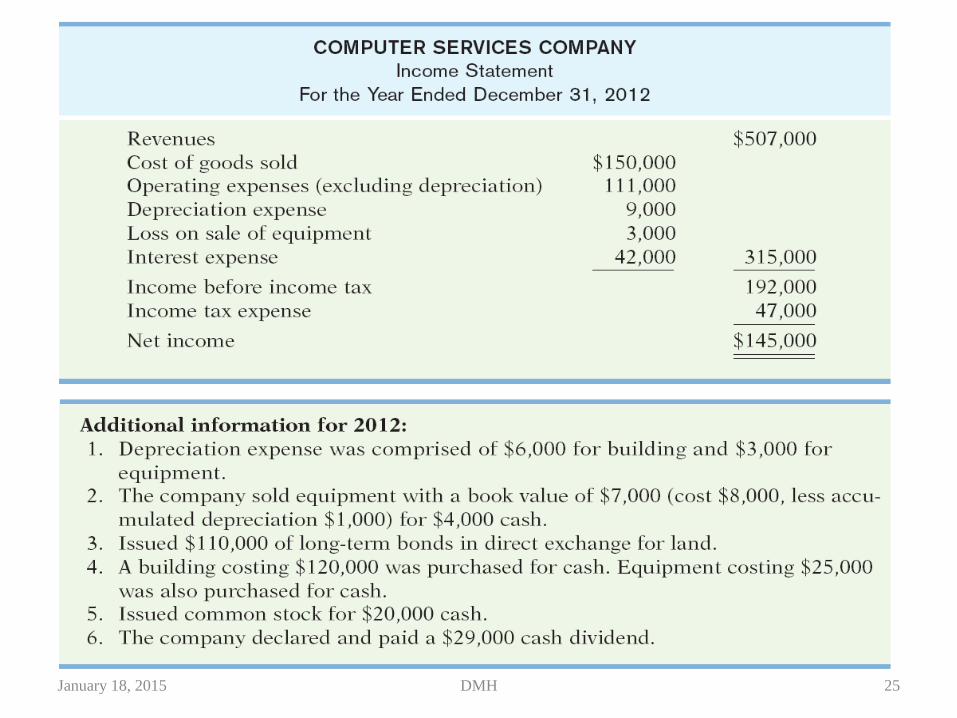

Additional information for 2012:

1. Depreciation expense was comprised of $6,000 for building & $3,000 for equipment.

2. The company sold equipment with a book value of $7,000 (cost $8,000, less accumulated

depreciation $1,000) for $4,000 cash.

3. Issued $110,000 of long-term bonds in direct exchange for land.

4. A building costing $120,000 was purchased for cash. Equipment costing $25,000 was also

purchased for cash.

5. Issued common stock for $20,000 cash.

6. The company declared & paid a $29,000 cash dividend.

January 18, 2015 41DMH

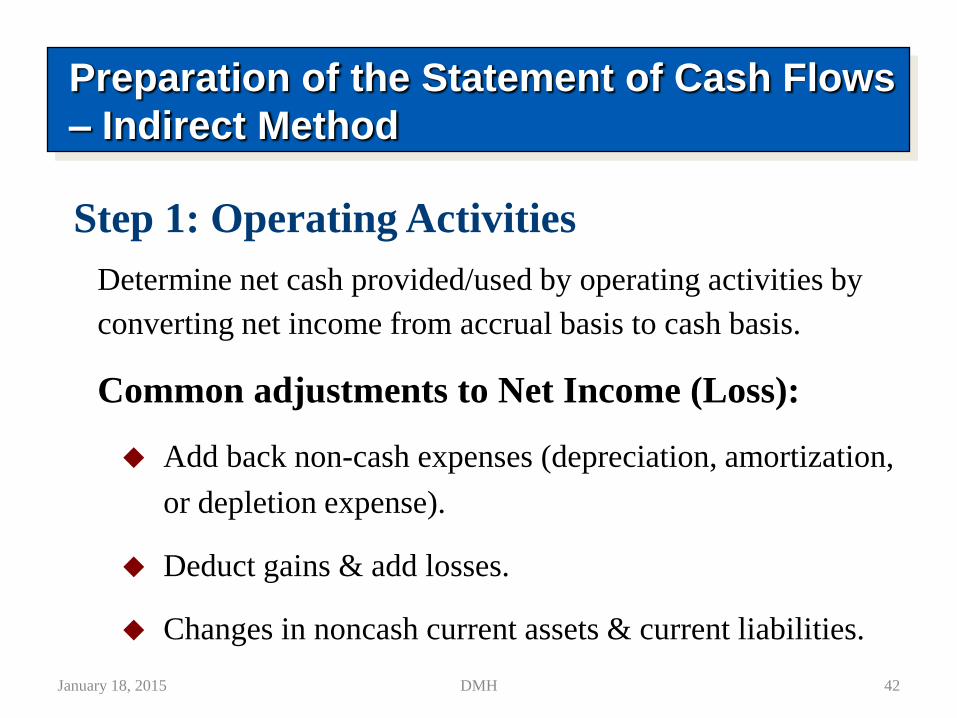

Step 1: Operating Activities

Determine net cash provided/used by operating activities by

converting net income from accrual basis to cash basis.

Preparation of the Statement of Cash Flows

– Indirect Method

Common adjustments to Net Income (Loss):

Add back non-cash expenses (depreciation, amortization,

or depletion expense).

Deduct gains & add losses.

Changes in noncash current assets & current liabilities.

January 18, 2015 42DMH

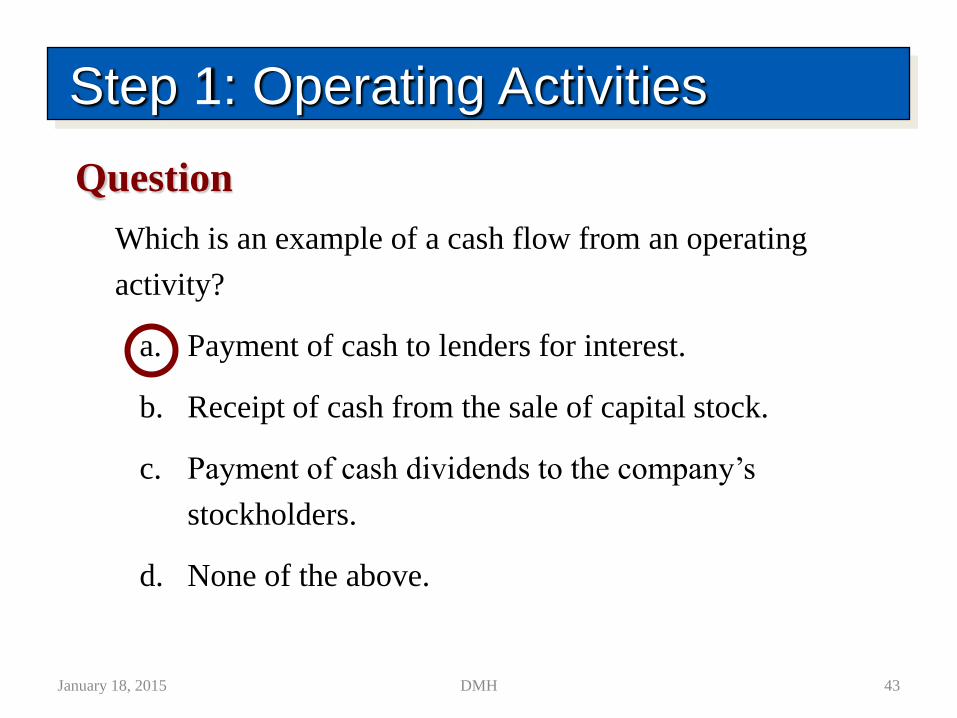

Which is an example of a cash flow from an operating

activity?

a. Payment of cash to lenders for interest.

b. Receipt of cash from the sale of capital stock.

c. Payment of cash dividends to the company’s

stockholders.

d. None of the above.

Question

Step 1: Operating Activities

January 18, 2015 43DMH

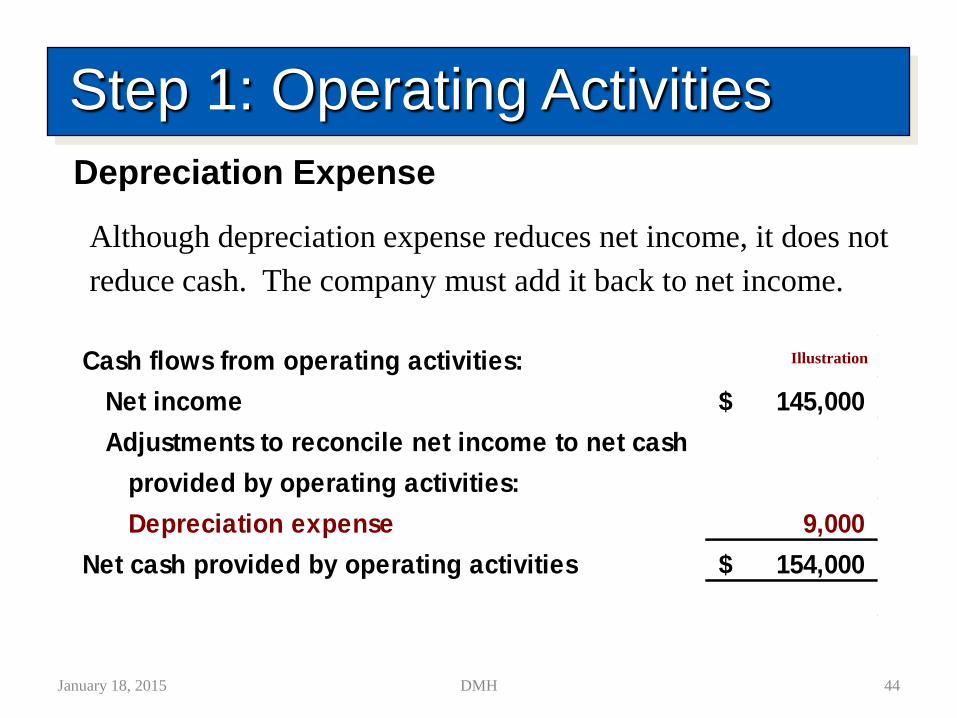

Depreciation Expense

Although depreciation expense reduces net income, it does not

reduce cash. The company must add it back to net income.

Cash flows from operating activities:

Net income 145,000$

Adjustments to reconcile net income to net cash

provided by operating activities:

Depreciation expense 9,000

Net cash provided by operating activities 154,000$

Illustration

Step 1: Operating Activities

January 18, 2015 44DMH

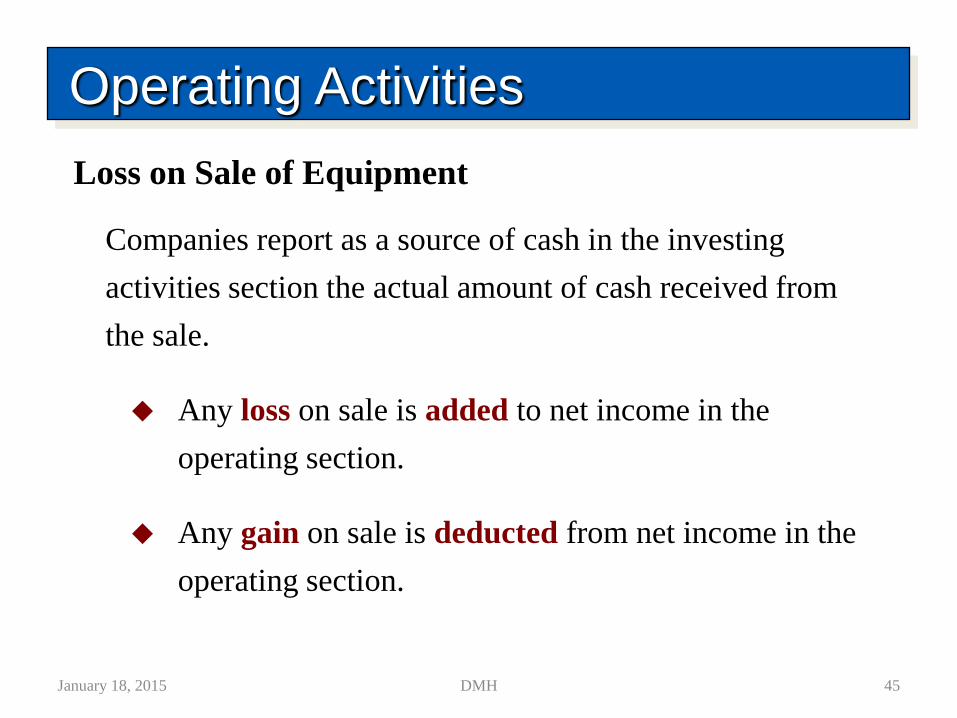

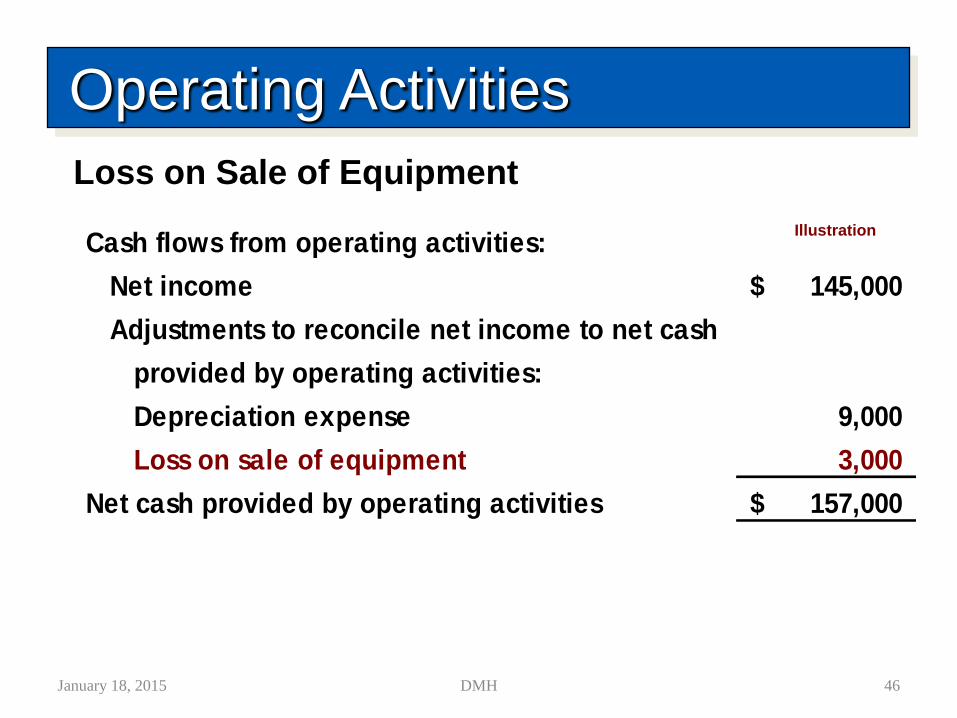

Loss on Sale of Equipment

Companies report as a source of cash in the investing

activities section the actual amount of cash received from

the sale.

Any loss on sale is added to net income in the

operating section.

Any gain on sale is deducted from net income in the

operating section.

Operating Activities

January 18, 2015 45DMH

Operating Activities

Cash flows from operating activities:

Net income 145,000$

Adjustments to reconcile net income to net cash

provided by operating activities:

Depreciation expense 9,000

Loss on sale of equipment 3,000

Net cash provided by operating activities 157,000$

Illustration

Loss on Sale of Equipment

January 18, 2015 46DMH

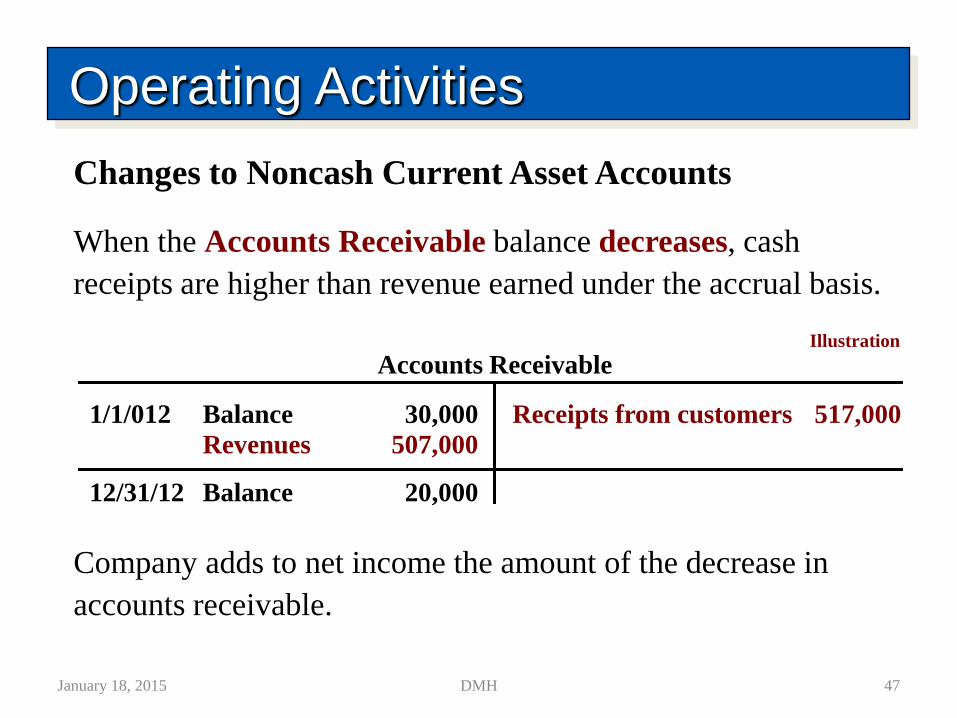

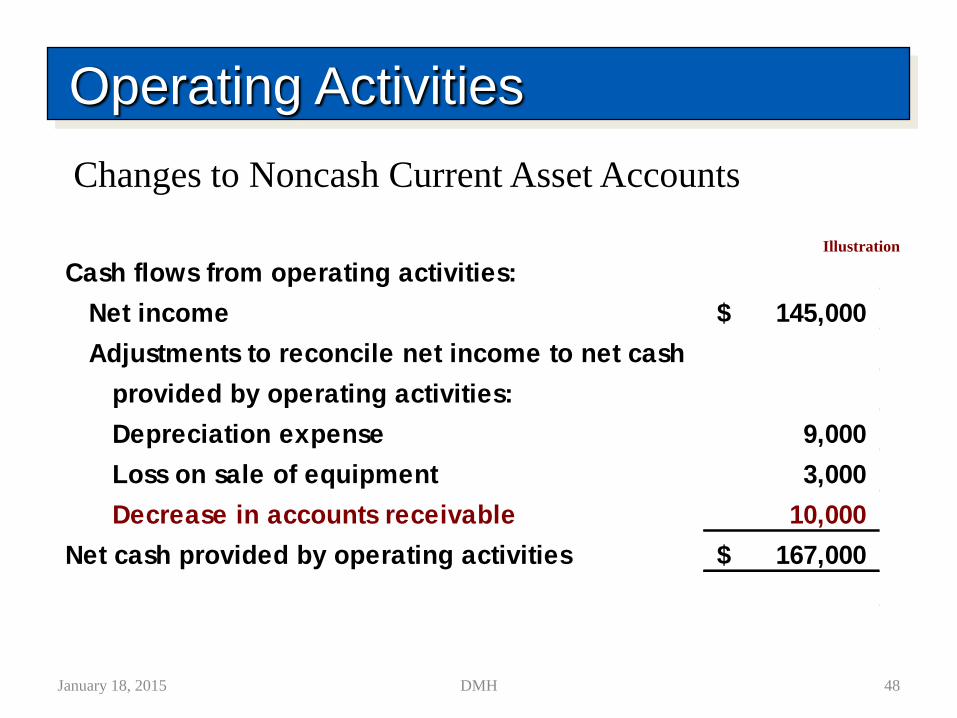

Changes to Noncash Current Asset Accounts

When the Accounts Receivable balance decreases, cash

receipts are higher than revenue earned under the accrual basis.

Operating Activities

Company adds to net income the amount of the decrease in

accounts receivable.

Accounts Receivable

1/1/012 Balance 30,000

Revenues 507,000

Receipts from customers 517,000

12/31/12 Balance 20,000

Illustration

January 18, 2015 47DMH

Operating Activities

Cash flows from operating activities:

Net income 145,000$

Adjustments to reconcile net income to net cash

provided by operating activities:

Depreciation expense 9,000

Loss on sale of equipment 3,000

Decrease in accounts receivable 10,000

Net cash provided by operating activities 167,000$

Illustration

Changes to Noncash Current Asset Accounts

January 18, 2015 48DMH

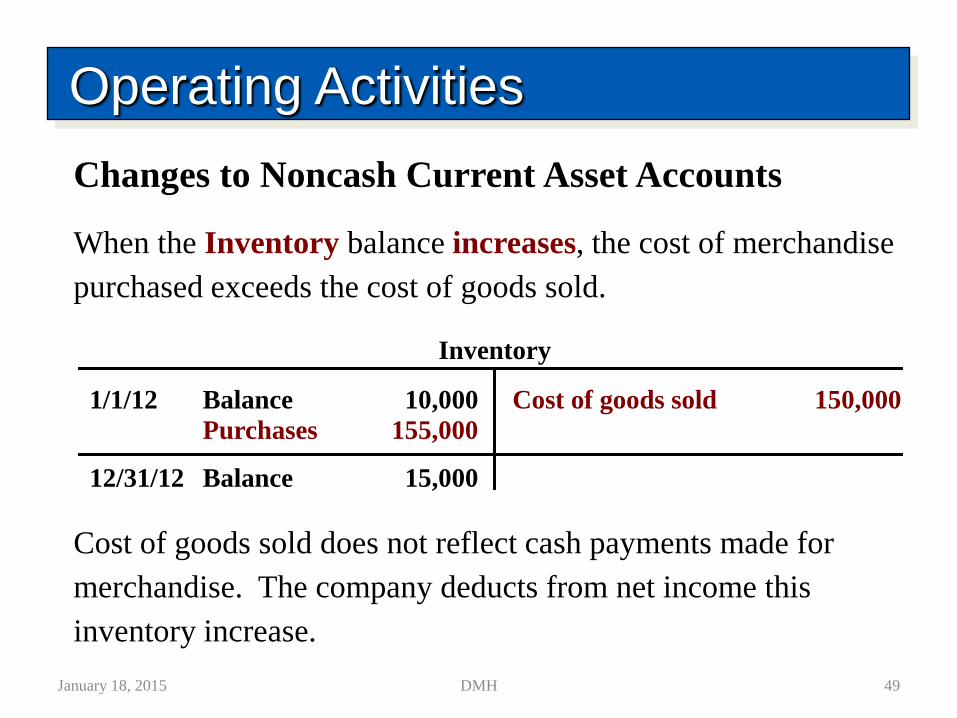

When the Inventory balance increases, the cost of merchandise

purchased exceeds the cost of goods sold.

Operating Activities

Changes to Noncash Current Asset Accounts

Inventory

1/1/12 Balance 10,000

Purchases 155,000

Cost of goods sold 150,000

12/31/12 Balance 15,000

Cost of goods sold does not reflect cash payments made for

merchandise. The company deducts from net income this

inventory increase.

January 18, 2015 49DMH

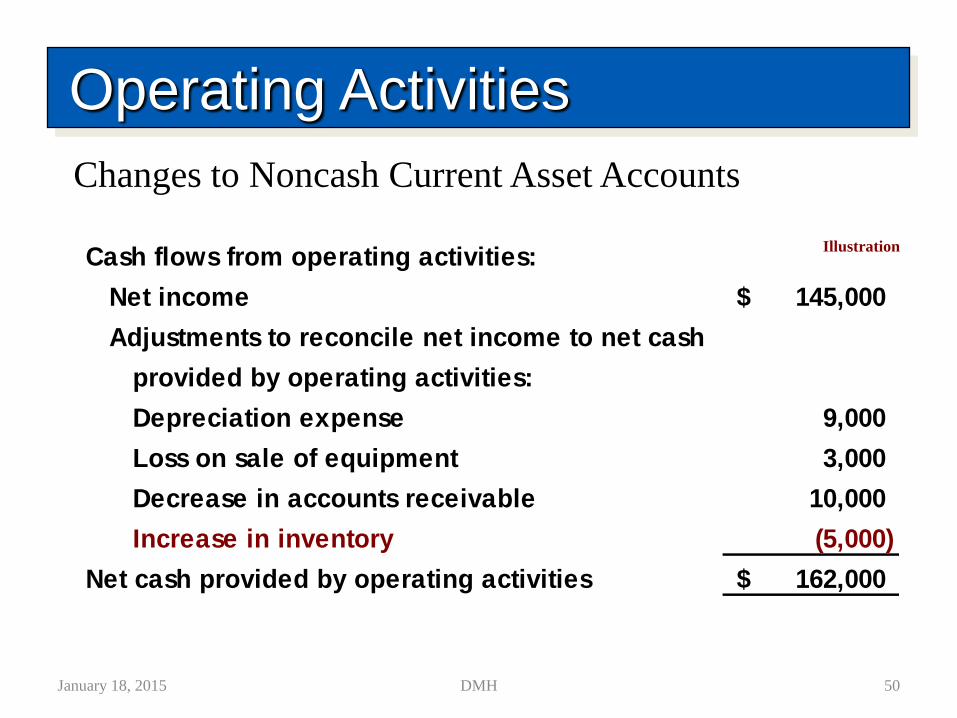

Operating Activities

Cash flows from operating activities:

Net income 145,000$

Adjustments to reconcile net income to net cash

provided by operating activities:

Depreciation expense 9,000

Loss on sale of equipment 3,000

Decrease in accounts receivable 10,000

Increase in inventory (5,000)

Net cash provided by operating activities 162,000$

Changes to Noncash Current Asset Accounts

Illustration

January 18, 2015 50DMH

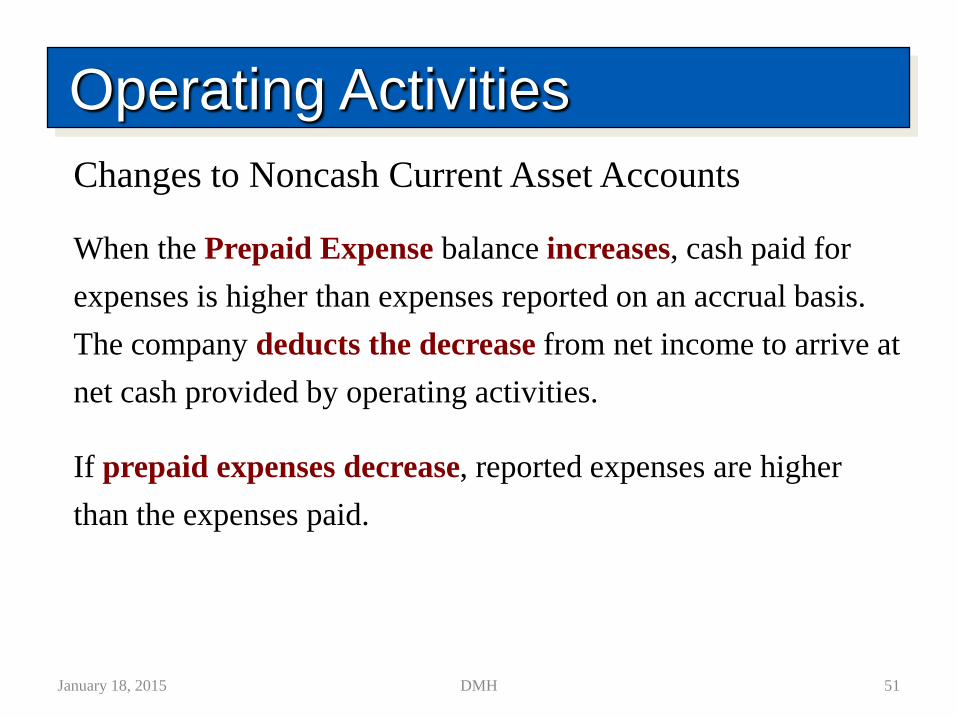

When the Prepaid Expense balance increases, cash paid for

expenses is higher than expenses reported on an accrual basis.

The company deducts the decrease from net income to arrive at

net cash provided by operating activities.

If prepaid expenses decrease, reported expenses are higher

than the expenses paid.

Operating Activities

Changes to Noncash Current Asset Accounts

January 18, 2015 51DMH

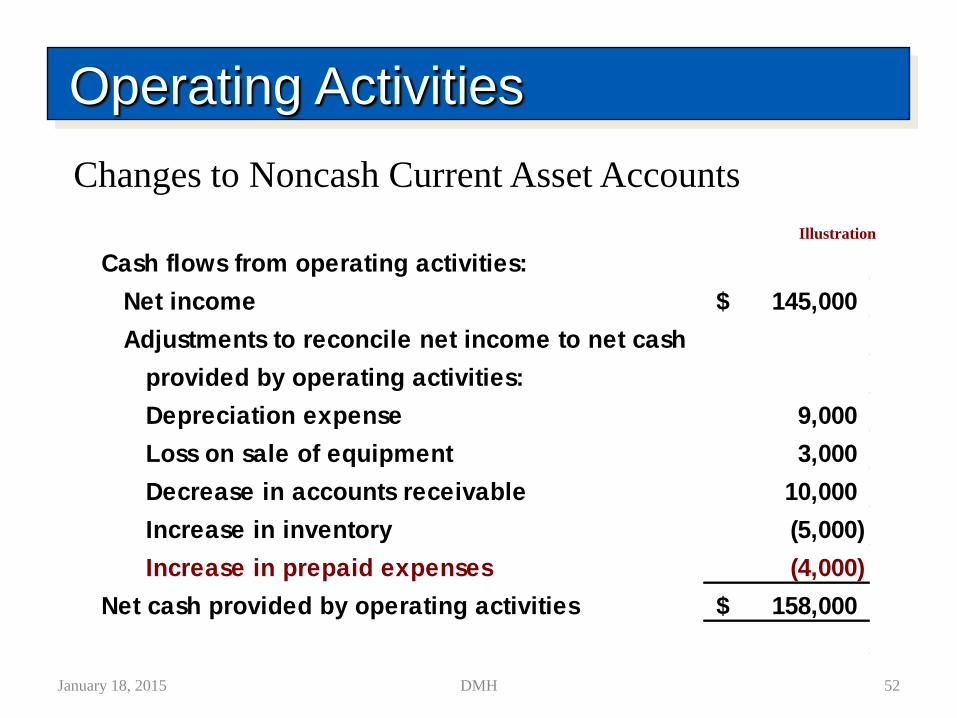

Operating Activities

Cash flows from operating activities:

Net income 145,000$

Adjustments to reconcile net income to net cash

provided by operating activities:

Depreciation expense 9,000

Loss on sale of equipment 3,000

Decrease in accounts receivable 10,000

Increase in inventory (5,000)

Increase in prepaid expenses (4,000)

Net cash provided by operating activities 158,000$

Changes to Noncash Current Asset Accounts

Illustration

January 18, 2015 52DMH

Changes to Noncash Current Liability Accounts

When Accounts Payable increases, the company received

more in goods than it actually paid for. The increase is added

to net income to determine net cash provided by operating

activities.

When Income Tax Payable decreases, the income tax expense

reported on the income statement was less than the amount of

taxes paid during the period. The decrease is subtracted from

net income to determine net cash provided by operating

activities.

Operating Activities

January 18, 2015 53DMH

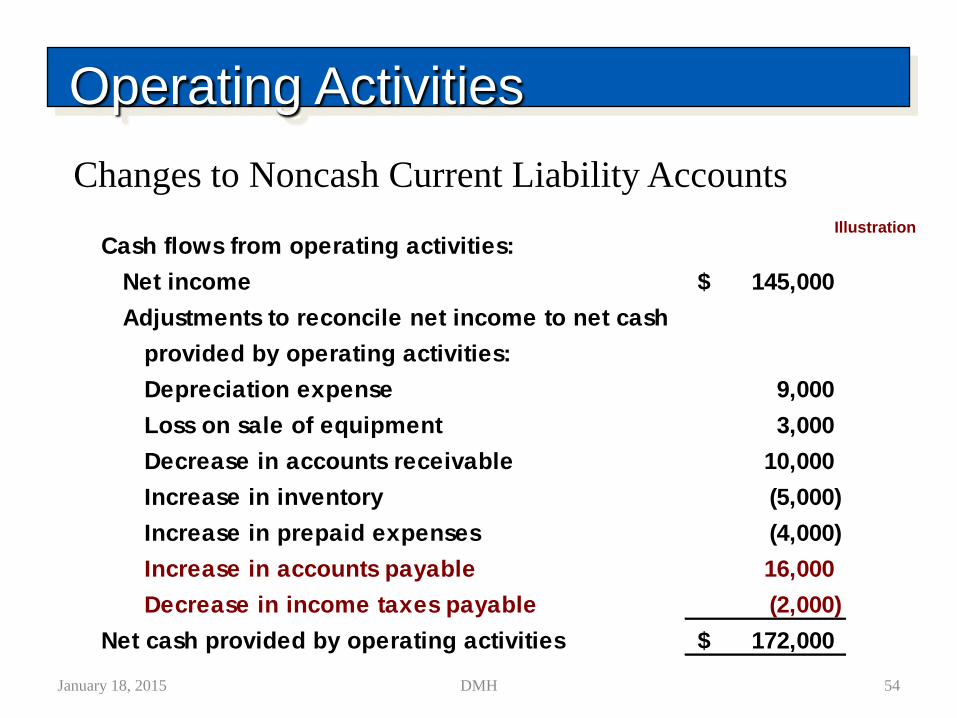

Operating Activities

Cash flows from operating activities:

Net income 145,000$

Adjustments to reconcile net income to net cash

provided by operating activities:

Depreciation expense 9,000

Loss on sale of equipment 3,000

Decrease in accounts receivable 10,000

Increase in inventory (5,000)

Increase in prepaid expenses (4,000)

Increase in accounts payable 16,000

Decrease in income taxes payable (2,000)

Net cash provided by operating activities 172,000$

Illustration

Changes to Noncash Current Liability Accounts

January 18, 2015 54DMH

Operating Activities

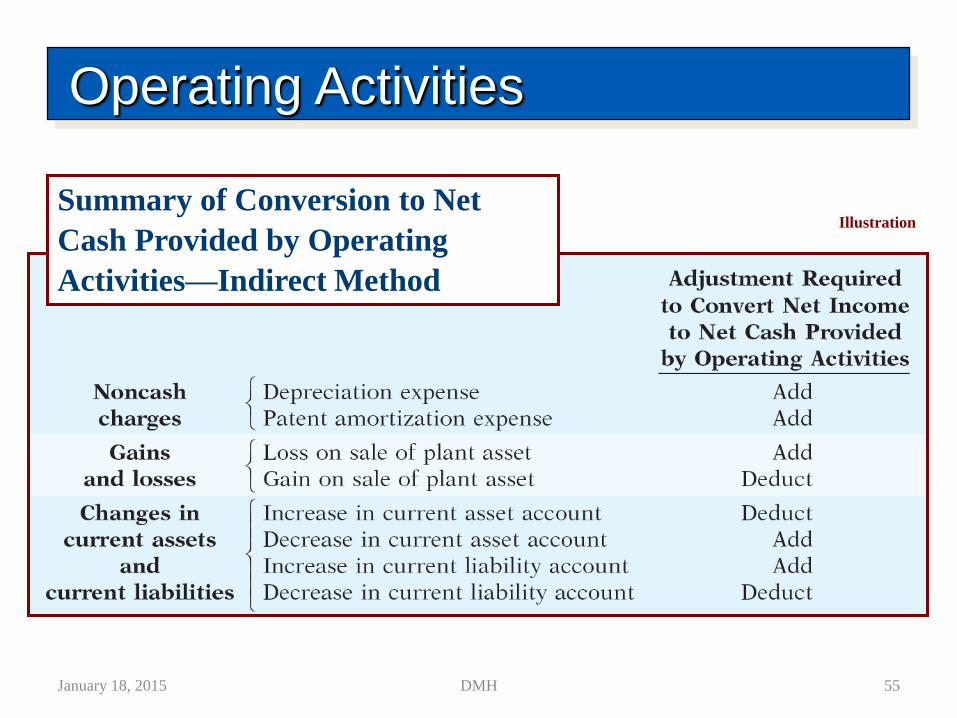

IllustrationSummary of Conversion to Net

Cash Provided by Operating

Activities—Indirect Method

January 18, 2015 55DMH

January 18, 2015 56DMH

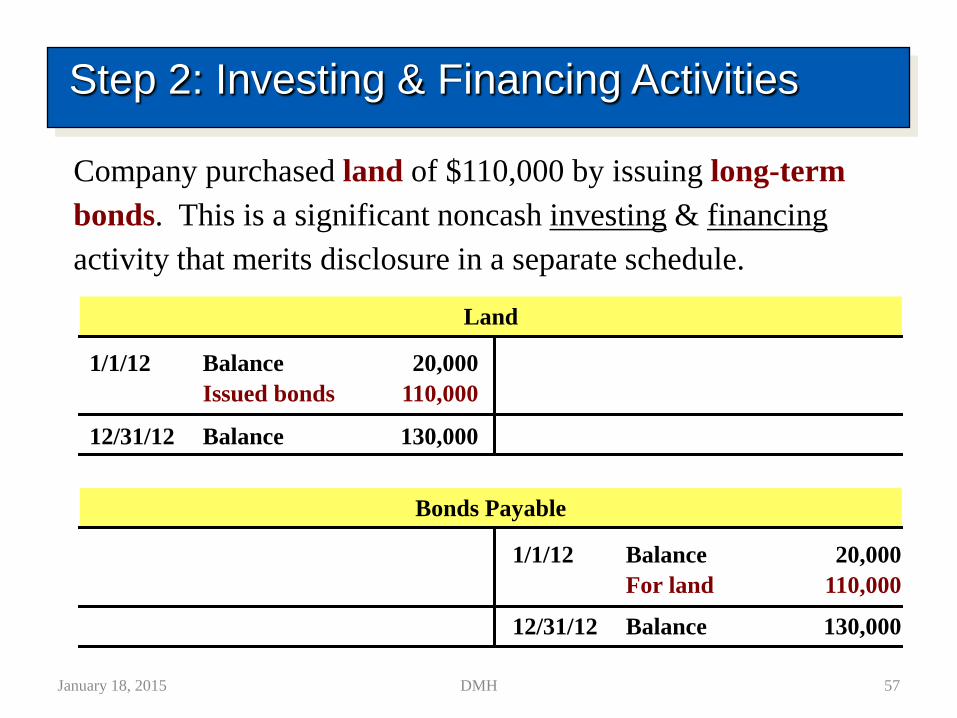

Company purchased land of $110,000 by issuing long-term

bonds. This is a significant noncash investing & financing

activity that merits disclosure in a separate schedule.

Step 2: Investing & Financing Activities

Land

1/1/12 Balance 20,000

Issued bonds 110,000

12/31/12 Balance 130,000

Bonds Payable

1/1/12 Balance 20,000

For land 110,000

12/31/12 Balance 130,000

January 18, 2015 57DMH

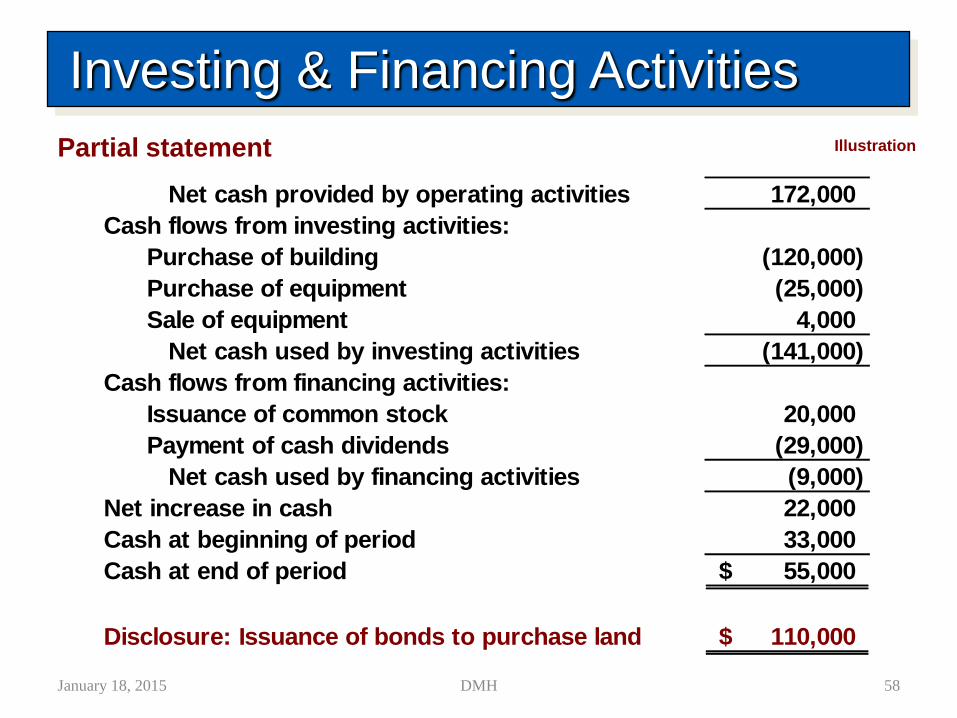

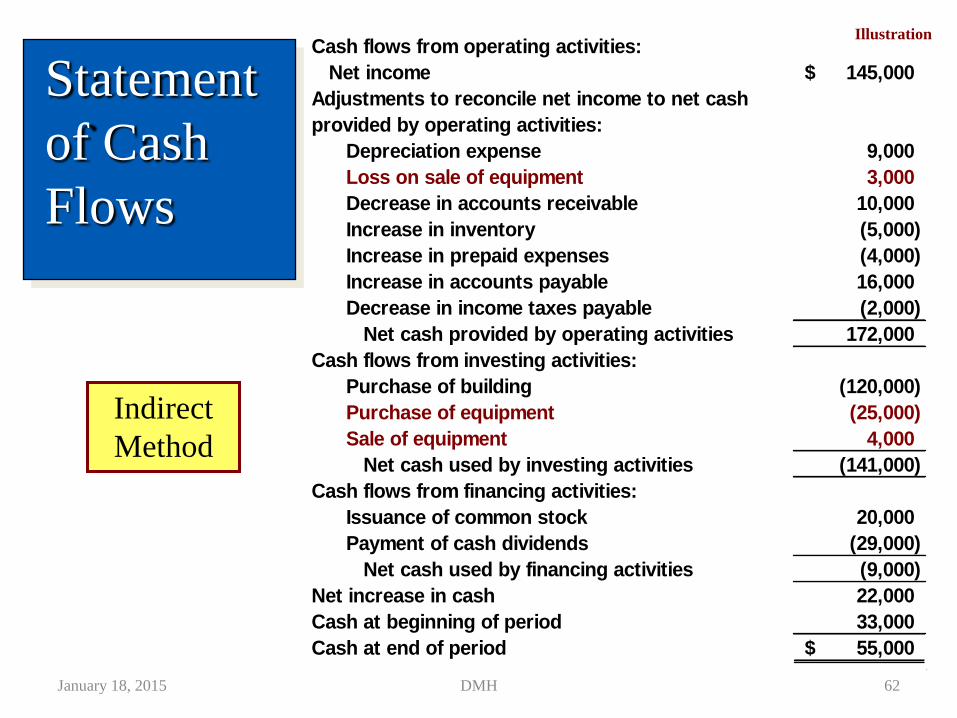

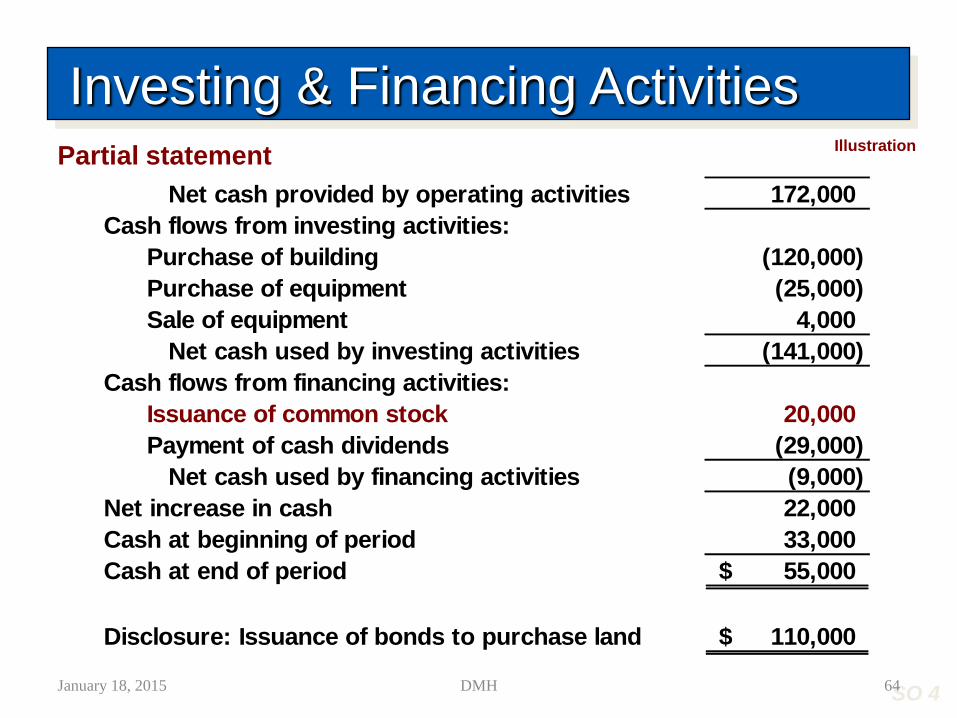

Net cash provided by operating activities 172,000

Cash flows from investing activities:

Purchase of building (120,000)

Purchase of equipment (25,000)

Sale of equipment 4,000

Net cash used by investing activities (141,000)

Cash flows from financing activities:

Issuance of common stock 20,000

Payment of cash dividends (29,000)

Net cash used by financing activities (9,000)

Net increase in cash 22,000

Cash at beginning of period 33,000

Cash at end of period 55,000$

Disclosure: Issuance of bonds to purchase land 110,000$

Investing & Financing Activities

Illustration Partial statement

January 18, 2015 58DMH

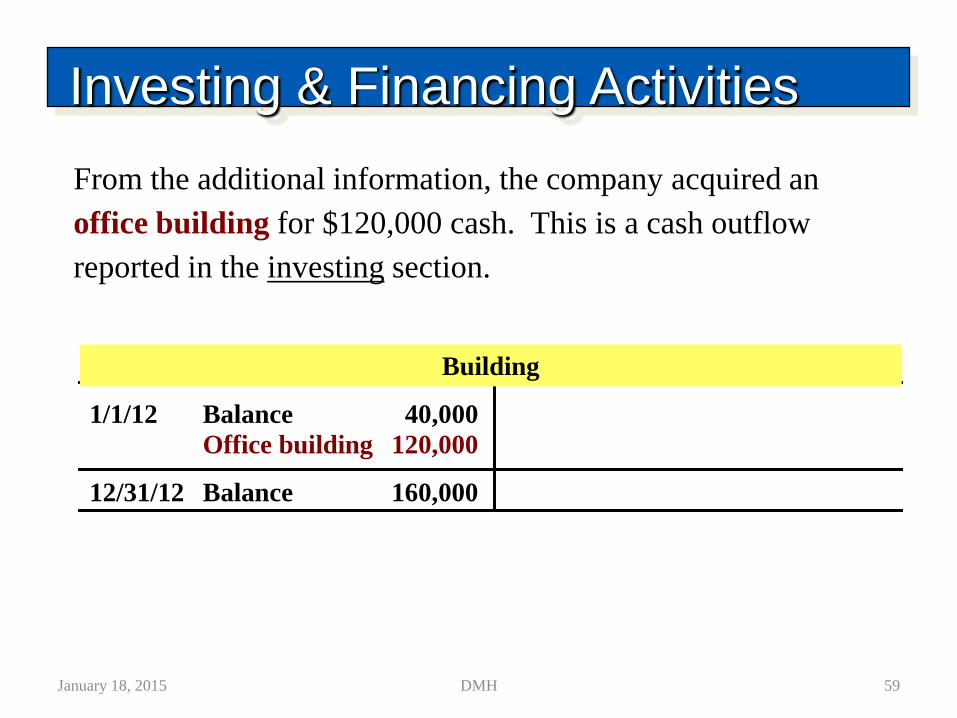

From the additional information, the company acquired an

office building for $120,000 cash. This is a cash outflow

reported in the investing section.

Investing & Financing Activities

1/1/12 Balance 40,000

Office building 120,000

12/31/12 Balance 160,000

Building

January 18, 2015 59DMH

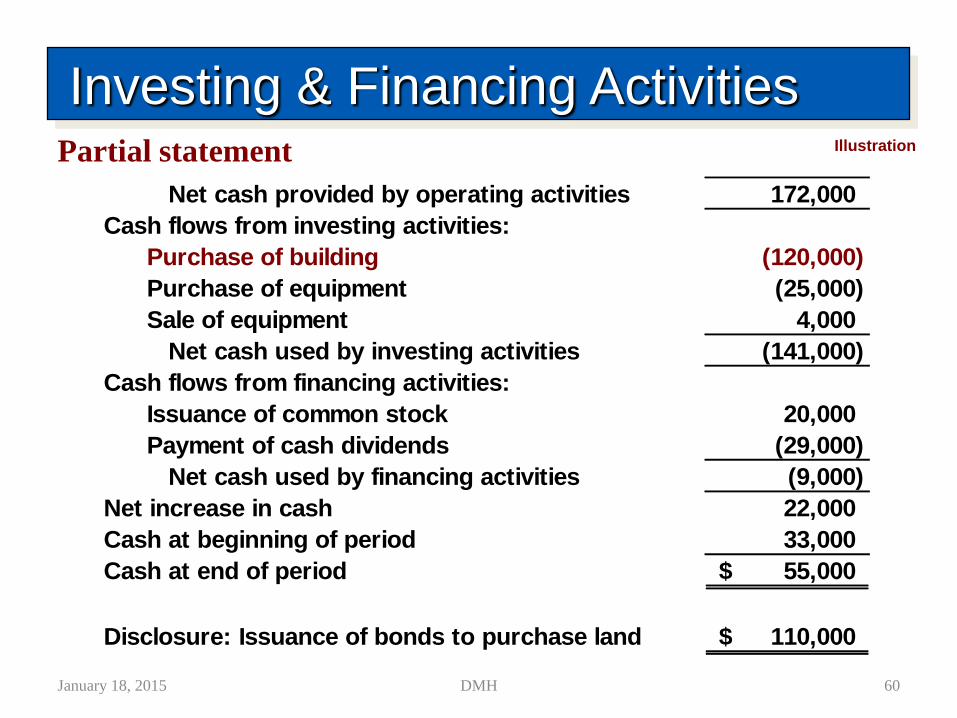

Net cash provided by operating activities 172,000

Cash flows from investing activities:

Purchase of building (120,000)

Purchase of equipment (25,000)

Sale of equipment 4,000

Net cash used by investing activities (141,000)

Cash flows from financing activities:

Issuance of common stock 20,000

Payment of cash dividends (29,000)

Net cash used by financing activities (9,000)

Net increase in cash 22,000

Cash at beginning of period 33,000

Cash at end of period 55,000$

Disclosure: Issuance of bonds to purchase land 110,000$

Investing & Financing ActivitiesIllustration Partial statement

January 18, 2015 60DMH

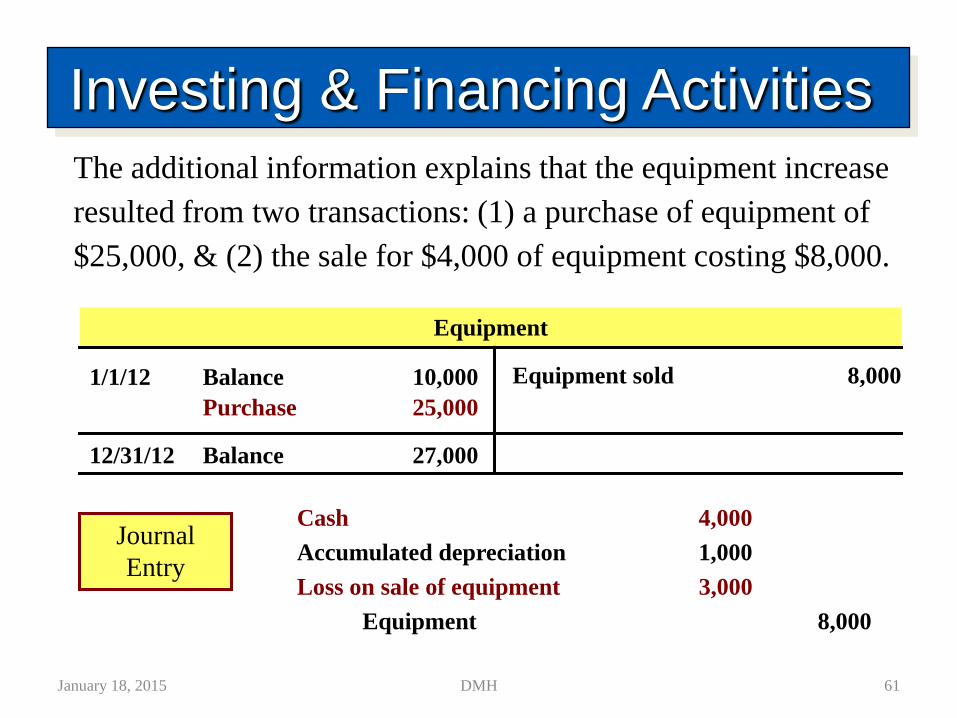

The additional information explains that the equipment increase

resulted from two transactions: (1) a purchase of equipment of

$25,000, & (2) the sale for $4,000 of equipment costing $8,000.

Investing & Financing Activities

1/1/12 Balance 10,000

Purchase 25,000

12/31/12 Balance 27,000

Equipment sold 8,000

Cash 4,000

Accumulated depreciation 1,000

Loss on sale of equipment 3,000

Equipment 8,000

Journal

Entry

Equipment

January 18, 2015 61DMH

Statement

of Cash

Flows

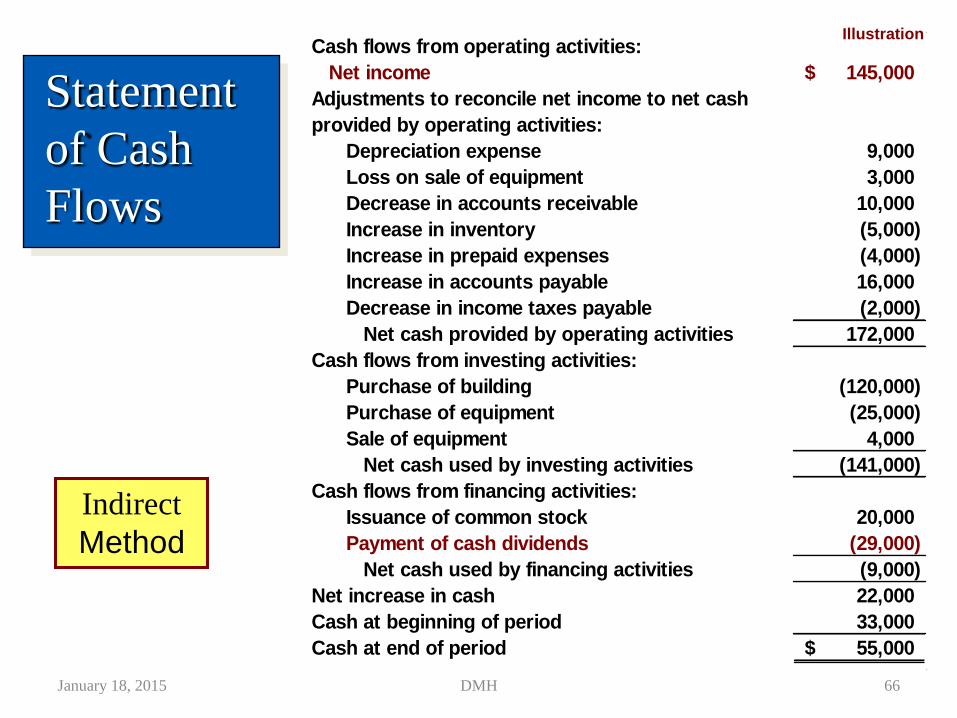

Cash flows from operating activities:

Net income 145,000$

Adjustments to reconcile net income to net cash

provided by operating activities:

Depreciation expense 9,000

Loss on sale of equipment 3,000

Decrease in accounts receivable 10,000

Increase in inventory (5,000)

Increase in prepaid expenses (4,000)

Increase in accounts payable 16,000

Decrease in income taxes payable (2,000)

Net cash provided by operating activities 172,000

Cash flows from investing activities:

Purchase of building (120,000)

Purchase of equipment (25,000)

Sale of equipment 4,000

Net cash used by investing activities (141,000)

Cash flows from financing activities:

Issuance of common stock 20,000

Payment of cash dividends (29,000)

Net cash used by financing activities (9,000)

Net increase in cash 22,000

Cash at beginning of period 33,000

Cash at end of period 55,000$

Illustration

Indirect

Method

January 18, 2015 62DMH

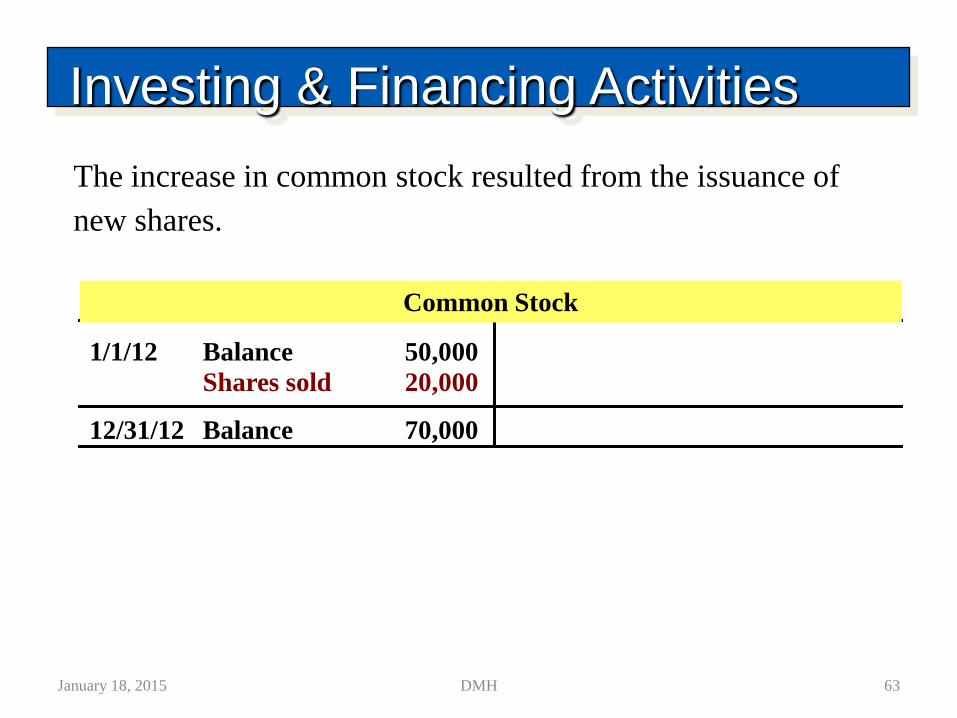

The increase in common stock resulted from the issuance of

new shares.

Investing & Financing Activities

1/1/12 Balance 50,000

Shares sold 20,000

12/31/12 Balance 70,000

Common Stock

January 18, 2015 63DMH

Net cash provided by operating activities 172,000

Cash flows from investing activities:

Purchase of building (120,000)

Purchase of equipment (25,000)

Sale of equipment 4,000

Net cash used by investing activities (141,000)

Cash flows from financing activities:

Issuance of common stock 20,000

Payment of cash dividends (29,000)

Net cash used by financing activities (9,000)

Net increase in cash 22,000

Cash at beginning of period 33,000

Cash at end of period 55,000$

Disclosure: Issuance of bonds to purchase land 110,000$

Investing & Financing ActivitiesIllustration

Partial statement

SO 4January 18, 2015 64DMH

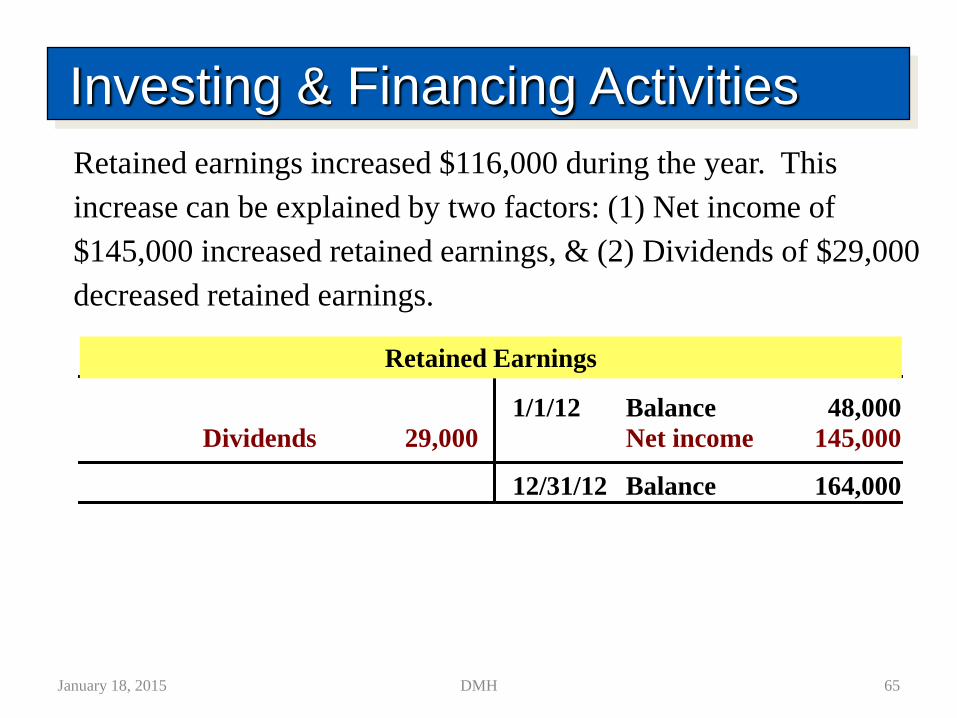

Retained earnings increased $116,000 during the year. This

increase can be explained by two factors: (1) Net income of

$145,000 increased retained earnings, & (2) Dividends of $29,000

decreased retained earnings.

Investing & Financing Activities

1/1/12 Balance 48,000

Net income 145,000

12/31/12 Balance 164,000

Dividends 29,000

Retained Earnings

January 18, 2015 65DMH

Statement

of Cash

Flows

Cash flows from operating activities:

Net income 145,000$

Adjustments to reconcile net income to net cash

provided by operating activities:

Depreciation expense 9,000

Loss on sale of equipment 3,000

Decrease in accounts receivable 10,000

Increase in inventory (5,000)

Increase in prepaid expenses (4,000)

Increase in accounts payable 16,000

Decrease in income taxes payable (2,000)

Net cash provided by operating activities 172,000

Cash flows from investing activities:

Purchase of building (120,000)

Purchase of equipment (25,000)

Sale of equipment 4,000

Net cash used by investing activities (141,000)

Cash flows from financing activities:

Issuance of common stock 20,000

Payment of cash dividends (29,000)

Net cash used by financing activities (9,000)

Net increase in cash 22,000

Cash at beginning of period 33,000

Cash at end of period 55,000$

Illustration

Indirect

Method

January 18, 2015 66DMH

Compare the net change in cash on the Statement of

Cash Flows with the change in the cash account

reported on the Balance Sheet to make sure the

amounts agree.

Step 3: Net Change in Cash

January 18, 2015 67DMH

Which is an example of a cash flow from an investing activity?

a. Receipt of cash from the issuance of bonds payable.

b. Payment of cash to repurchase outstanding capital stock.

c. Receipt of cash from the sale of equipment.

d. Payment of cash to suppliers for inventory.

Review Question

Investing & Financing Activities

January 18, 2015 68DMH

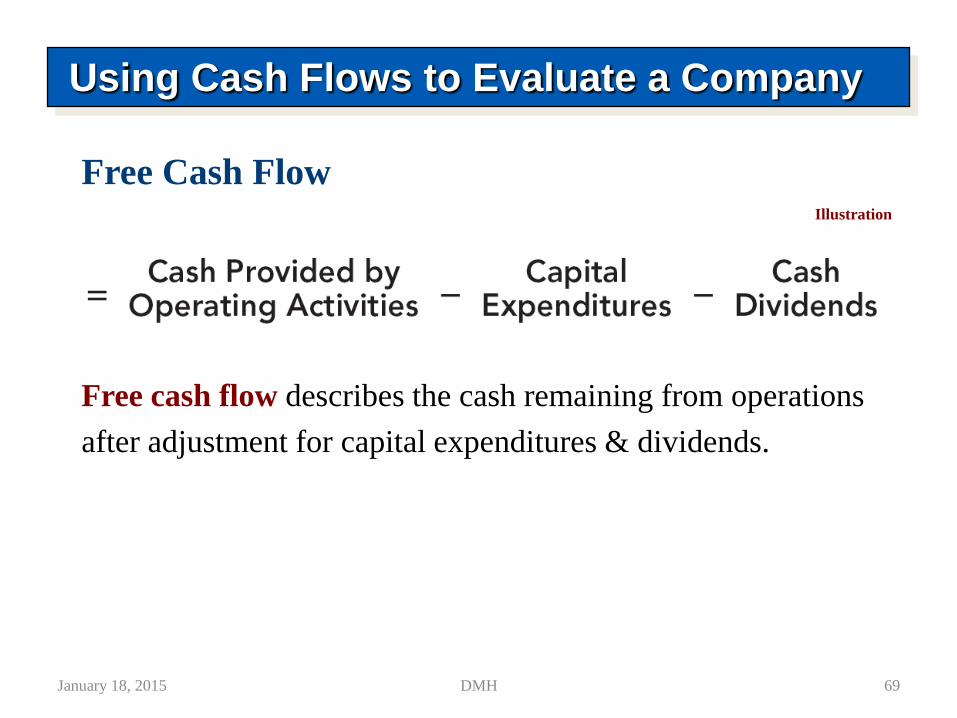

Free Cash Flow

Free cash flow describes the cash remaining from operations

after adjustment for capital expenditures & dividends.

Using Cash Flows to Evaluate a Company

Illustration

January 18, 2015 69DMH

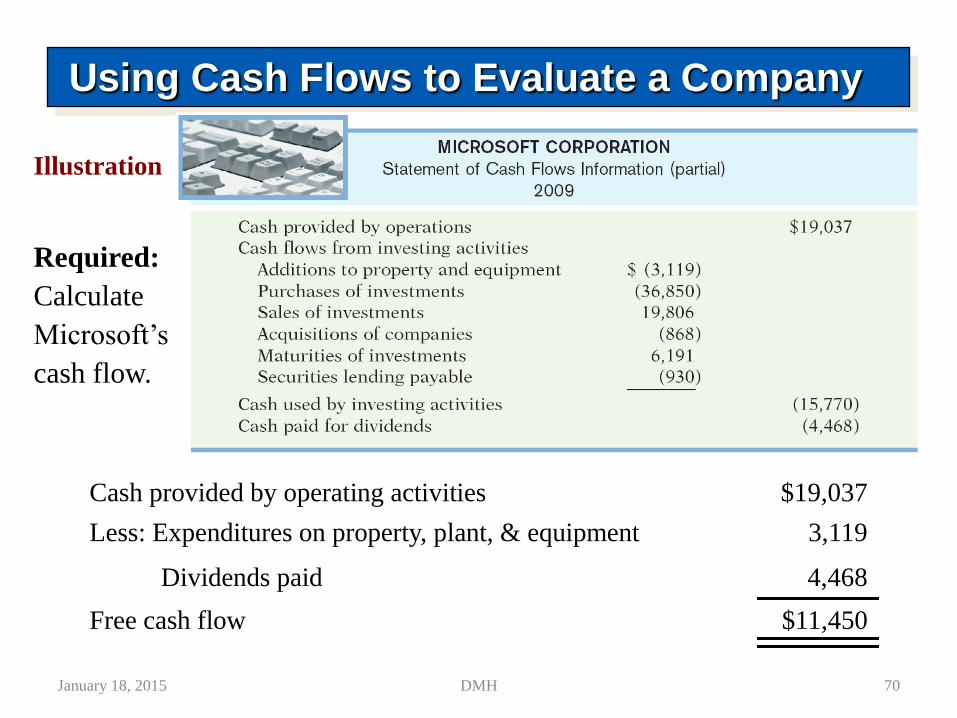

Cash provided by operating activities $19,037

Using Cash Flows to Evaluate a Company

Less: Expenditures on property, plant, & equipment 3,119

Dividends paid 4,468

Free cash flow $11,450

Illustration

Required:

Calculate

Microsoft’s free

cash flow.

January 18, 2015 70DMH

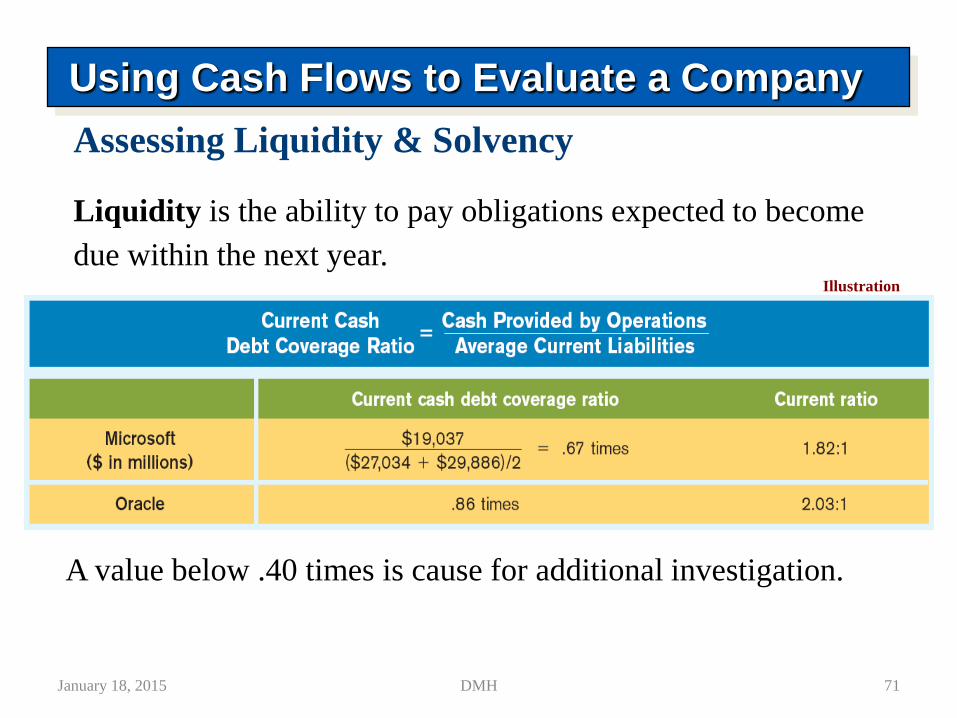

Assessing Liquidity & Solvency

Liquidity is the ability to pay obligations expected to become

due within the next year.

Using Cash Flows to Evaluate a Company

Illustration

A value below .40 times is cause for additional investigation.

January 18, 2015 71DMH

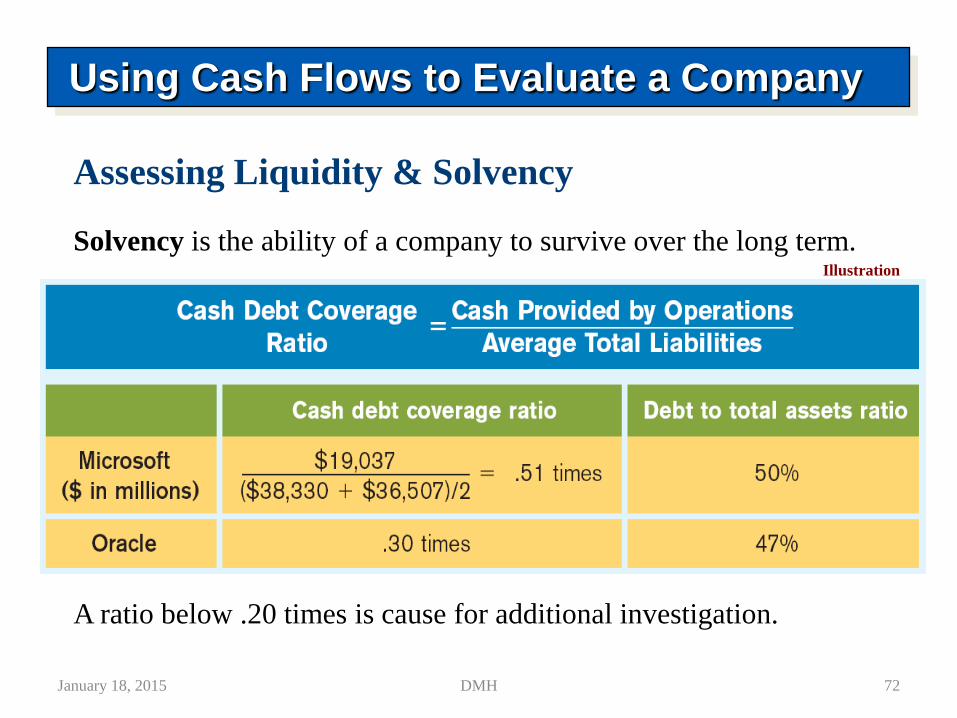

Assessing Liquidity & Solvency

Solvency is the ability of a company to survive over the long term.Illustration

A ratio below .20 times is cause for additional investigation.

Using Cash Flows to Evaluate a Company

January 18, 2015 72DMH

Companies preparing financial statements under IFRS must

prepare a statement of cash flows as an integral part of the

financial statements.

Both IFRS & GAAP require that the statement of cash flows

should have three major sections—operating, investing, &

financing—along with changes in cash & cash equivalents.

Similar to GAAP, the cash flow statement can be prepared

using either the indirect or direct method under IFRS. In both

U.S. & international settings, companies choose for the most

part to use the indirect method for reporting net cash flows

from operating activities.

Key Points

January 18, 2015 73DMH

Key Points

The definition of cash equivalents used in IFRS is similar to

that used in GAAP. A major difference is that in certain

situations, bank overdrafts are considered part of cash & cash

equivalents under IFRS (which is not the case in GAAP).

Under GAAP, bank overdrafts are classified as financing

activities in the statement of cash flows & are reported as

liabilities on the balance sheet.

January 18, 2015 74DMH

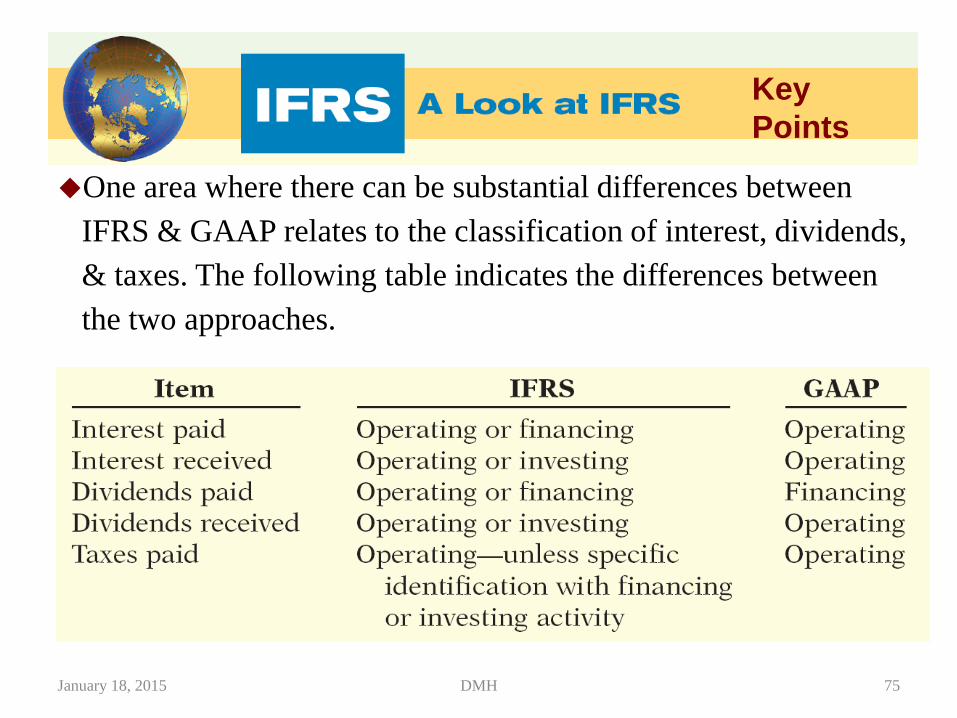

One area where there can be substantial differences between

IFRS & GAAP relates to the classification of interest, dividends,

& taxes. The following table indicates the differences between

the two approaches.

Key

Points

January 18, 2015 75DMH

Under IFRS, some companies present the operating section

in a single line item, with a full reconciliation provided in

the notes to the financial statements. This presentation is not

seen under GAAP.

Similar to GAAP, under IFRS companies must disclose the

amount of taxes & interest paid. Under GAAP, companies

disclose this in the notes to the financial statements. Under

IFRS, some companies disclose this information in the

notes, but others provide individual line items on the face of

the statement.

Key Points

January 18, 2015 76DMH

FASB & the IASB are involved in a joint project on the

presentation & organization of information in the financial

statements. One possible approach is that the income statement &

balance sheet would adopt headings similar to those of the

statement of cash flows. That is, the income statement & balance

sheet would be broken into operating, investing, & financing

sections. In addition, the FASB favors presentation of operating

cash flows using the direct method only. However, the majority

of IASB members express a preference for not requiring use of

the direct method of reporting operating cash flows. The two

Boards will have to resolve their differences in this area in order

to issue a converged standard for the statement of cash flows.

Looking into the Future

January 18, 2015 77DMH

Under IFRS, interest paid can be reported as:

a) only a financing element.

b) a financing element or an investing element.

c) a financing element or an operating element.

d) only an operating element.

January 18, 2015 78DMH

IFRS requires that noncash items:

a) be reported in the section to which they relate, that is, a

noncash investing activity would be reported in the

investing section.

b) be disclosed in the notes to the financial statements.

c) do not need to be reported.

d) be treated in a fashion similar to cash equivalents.

January 18, 2015 79DMH

In the future, it appears likely that:

a) the income statement & balance sheet will have headings

of operating, investing, & financing, much like the

statement of cash flows.

b) cash & cash equivalents will be combined in a single line

item.

c) the IASB will not allow companies to use the direct

approach to the statement of cash flows.

d) None of the above.

January 18, 2015 80DMH