cashflowmvit 13117382206982-phpapp01-110726230250-phpapp01

TRANSCRIPT

11

ESTIMATION OF CASH FLOWSESTIMATION OF CASH FLOWS

By CA N.VenkatakrishnanBy CA N.Venkatakrishnan

@@

MVITMVIT

1212THTH MAY 2011 MAY 2011

22

ESTIMATION OF CASH FLOWSESTIMATION OF CASH FLOWS

OVERVIEW OF CAPITAL OVERVIEW OF CAPITAL BUDGETING AND BUDGETING AND EXPENDITUREEXPENDITURE;;

What is Capital Budgeting;What is Capital Budgeting;

The process of identifying, evaluating The process of identifying, evaluating and selecting investments whose and selecting investments whose returns (cash flows) are expected to returns (cash flows) are expected to extend beyond one year ie Long term extend beyond one year ie Long term Investments Investments

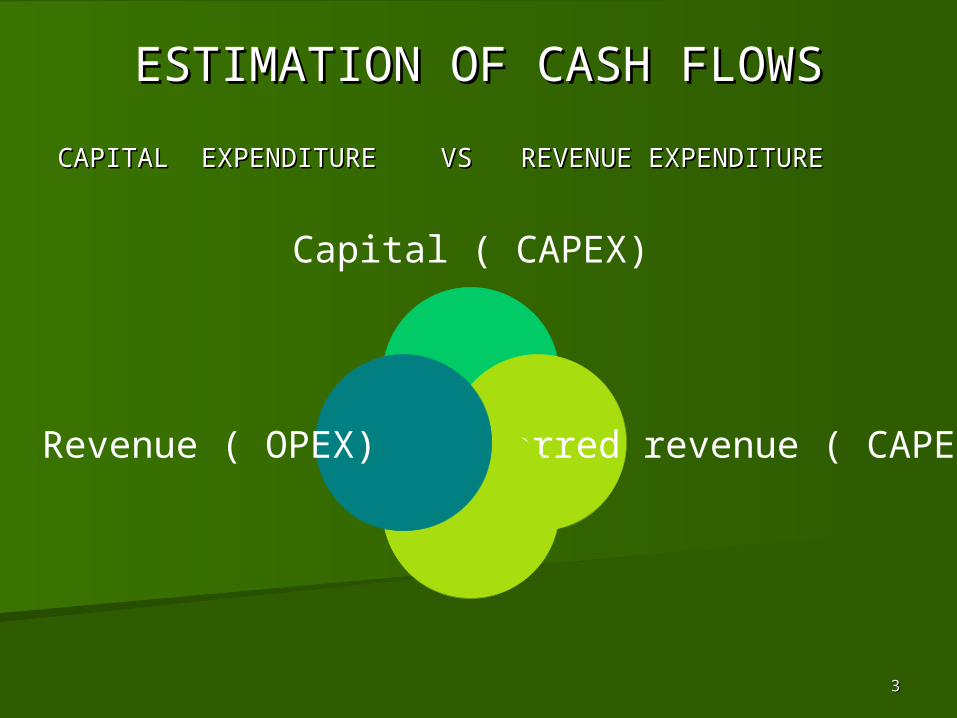

33

ESTIMATION OF CASH FLOWSESTIMATION OF CASH FLOWS

CAPITAL EXPENDITURE VS REVENUE EXPENDITURECAPITAL EXPENDITURE VS REVENUE EXPENDITURE

Capital ( CAPEX)

Deferred revenue ( CAPEX) Revenue ( OPEX)

44

ESTIMATION OF CASH FLOWSESTIMATION OF CASH FLOWS

CAPITAL EXPENDITURECAPITAL EXPENDITURE;;

Purchase of capital equipmentPurchase of capital equipmentFurniture and FixturesFurniture and FixturesComputersComputersCommunication EquipmentCommunication EquipmentLand and BuildingsLand and BuildingsElectrical InstallationElectrical InstallationOffice EquipmentOffice EquipmentMajor repairs to any Asset which would enhance the life of Major repairs to any Asset which would enhance the life of that particular Asset.that particular Asset.

55

ESTIMATION OF CASH FLOWSESTIMATION OF CASH FLOWS

REVENUE EXPENDITUREREVENUE EXPENDITURE;;

Manufacturing costsManufacturing costsSalary, Bonus Gratuity etc-Employee costsSalary, Bonus Gratuity etc-Employee costsRentRentElectricityElectricityInterest Interest Communication ExpensesCommunication ExpensesAdvertisementAdvertisementMarketing ExpensesMarketing Expenses

66

ESTIMATION OF CASH FLOWSESTIMATION OF CASH FLOWS

IMPORTANCE OF CASH FLOWS /CAPITAL IMPORTANCE OF CASH FLOWS /CAPITAL BUDEGETING DECISIONS;BUDEGETING DECISIONS;

1)Affect the profitability of the company –Earning Assets of the 1)Affect the profitability of the company –Earning Assets of the company.company.

2)Will have a long term effect over the company2)Will have a long term effect over the company

3)Not easily reversible without much Financial loss.3)Not easily reversible without much Financial loss.

4)Involves huge costs and scarce resources4)Involves huge costs and scarce resources

DIFFICULTIES IN CAPITAL EXPENDITURE DECISIONS;DIFFICULTIES IN CAPITAL EXPENDITURE DECISIONS;

1)Relate to uncertain future Period involving various risk 1)Relate to uncertain future Period involving various risk factors.factors.

2)Costs and revenue accrue at different time periods.2)Costs and revenue accrue at different time periods.

77

ESTIMATION OF CASH FLOWSESTIMATION OF CASH FLOWS

CLASSIFICATION OF INVESTMENT PROJECT CLASSIFICATION OF INVESTMENT PROJECT PROPOSALS;PROPOSALS;

11. New products or expansion. New products or expansion of existing products of existing products

2. Replacement2. Replacement of existing equipment or buildings of existing equipment or buildings

3. Infrastructure Projects3. Infrastructure Projects

4. Research and development4. Research and development

5. Exploration5. Exploration

6. Mandatory Requirements (e.g., safety or pollution related)6. Mandatory Requirements (e.g., safety or pollution related)

7. Others-welfare related like Townships etc.7. Others-welfare related like Townships etc.

All these could be Independent or Mutually Exclusive.All these could be Independent or Mutually Exclusive.

88

ESTIMATION OF CASH FLOWSESTIMATION OF CASH FLOWS

EXECUTIVES/PROFESSIONALS INVOLVED IN CAPITAL EXECUTIVES/PROFESSIONALS INVOLVED IN CAPITAL BUDEGETINGBUDEGETING;;

1. Engineering Teams-for outlays1. Engineering Teams-for outlays

2.2. Plant Managers- for giving their inputsPlant Managers- for giving their inputs

3. Production Team of Engineers-for operational costs3. Production Team of Engineers-for operational costs

4.4. Marketing Team.– for estimationMarketing Team.– for estimation

5.5. Finance Team- For working out the Financial dataFinance Team- For working out the Financial data

6 Capital Expenditures Committee6 Capital Expenditures Committee

7. President7. President

8. Board of Directors8. Board of Directors

99

ESTIMATION OF CASH FLOWSESTIMATION OF CASH FLOWS

CAPITAL BUDGETING AND ESTIMATING CASH FLOWSCAPITAL BUDGETING AND ESTIMATING CASH FLOWS;;

THE CAPITAL BUDGETING PROCESS;THE CAPITAL BUDGETING PROCESS;

Generate investment proposals consistent with the firm’s Generate investment proposals consistent with the firm’s strategic objectives.strategic objectives.Estimate after-tax incremental operating cash flows for the Estimate after-tax incremental operating cash flows for the investment projects.investment projects.Evaluate project incremental cash flowsEvaluate project incremental cash flowsSelect projects based on a value-maximizing acceptance Select projects based on a value-maximizing acceptance criterion.criterion.Reevaluate implemented investment projects continually and Reevaluate implemented investment projects continually and perform post audits for completed projectsperform post audits for completed projects

1010

ESTIMATION OF CASH FLOWSESTIMATION OF CASH FLOWSDIFFICULTIES IN ESTIMATION;DIFFICULTIES IN ESTIMATION;

Inaccurate data can distort the cash flow Inaccurate data can distort the cash flow projections and eventually the conclusions may projections and eventually the conclusions may prove wrong.prove wrong.

Future cannot be predicted with certainty.Future cannot be predicted with certainty. The company has to rely on a lot of external Data The company has to rely on a lot of external Data

especially for new projects.especially for new projects. Accurate projections are important because the Accurate projections are important because the

company may accept an unviable proposal or reject company may accept an unviable proposal or reject a good proposal.a good proposal.

1111

ESTIMATION OF CASH FLOWSESTIMATION OF CASH FLOWS

PRINCIPLES OF CASH FLOWPRINCIPLES OF CASH FLOW;;To arrange proper Financing for a project, it is imperative to To arrange proper Financing for a project, it is imperative to

ascertain the correct profitability of the Project. The project cash ascertain the correct profitability of the Project. The project cash

flows consider almost every kind of inflows of cashflows consider almost every kind of inflows of cash . .1)Consistency principle1)Consistency principle; ; cash flows should be consistent as to the discount rates and cash flows should be consistent as to the discount rates and

estimating the cash flows. If distorted, then the purpose will be estimating the cash flows. If distorted, then the purpose will be defeated.defeated.

Investors’ and Inflation factors have to be factored in the cash Investors’ and Inflation factors have to be factored in the cash flowflow

2)Post Tax principle2)Post Tax principle; ; Cash flows have to factor in the taxes applicable. Whether it is the Cash flows have to factor in the taxes applicable. Whether it is the

company’s average tax or the projects marginal tax would depend company’s average tax or the projects marginal tax would depend on the situation of the company. eg Previous existing Losses. on the situation of the company. eg Previous existing Losses.

Non cash charges do affect cash flows.Non cash charges do affect cash flows.

1212

ESTIMATION OF CASH FLOWSESTIMATION OF CASH FLOWSPRINCIPLES OF CASH FLOW;PRINCIPLES OF CASH FLOW;3)Incremental principle; 3)Incremental principle; According to this principle, only differences due to the According to this principle, only differences due to the

decision needs to be considered. Other factors may be decision needs to be considered. Other factors may be important but not to the decision at hand.important but not to the decision at hand.

Incidental Effects: Any kind of project taken by a company Incidental Effects: Any kind of project taken by a company remains related to the other activities of the firm. Because of remains related to the other activities of the firm. Because of this, a particular project influences all the other activities this, a particular project influences all the other activities carried out, either negatively or positively. It can increase the carried out, either negatively or positively. It can increase the profits for the firm or it may cause losses.profits for the firm or it may cause losses.

4)Separation principle; 4)Separation principle; This principle recognizes the fact that any This principle recognizes the fact that any project cash flow estimation has two sides viz Investment and project cash flow estimation has two sides viz Investment and Financing.Financing.

1313

ESTIMATION OF CASH FLOWSESTIMATION OF CASH FLOWSDATA REQUIRED-IDENTIFYING RELEVANT CASH FLOWSDATA REQUIRED-IDENTIFYING RELEVANT CASH FLOWS

1)CASH FLOW VS ACCOUNTING PROFIT1)CASH FLOW VS ACCOUNTING PROFIT;;

Cash Flow method is a better method of measuring Economic Cash Flow method is a better method of measuring Economic Viability;Viability;

Accounting Profits/losses include Non Cash Expenses and will not Accounting Profits/losses include Non Cash Expenses and will not give an accurate picture of the EV of the Investment proposal. Cash give an accurate picture of the EV of the Investment proposal. Cash Flows will describe the Cash Transactions the company will Flows will describe the Cash Transactions the company will experience once the Project is accepted.experience once the Project is accepted.

There are Accounting ambiguities in determining net profits under There are Accounting ambiguities in determining net profits under Accounting profits eg Valuation of Inventories, ,allocation of costs, Accounting profits eg Valuation of Inventories, ,allocation of costs, methods of depreciation, provisions etc. Cash Flow method provides methods of depreciation, provisions etc. Cash Flow method provides a near perfect picture of the EV of the Investment proposal.a near perfect picture of the EV of the Investment proposal.

Cash Flow method recognizes the Time value of money where as Cash Flow method recognizes the Time value of money where as Accounting profits are more historical and on accrual basis.Accounting profits are more historical and on accrual basis.

..

1414

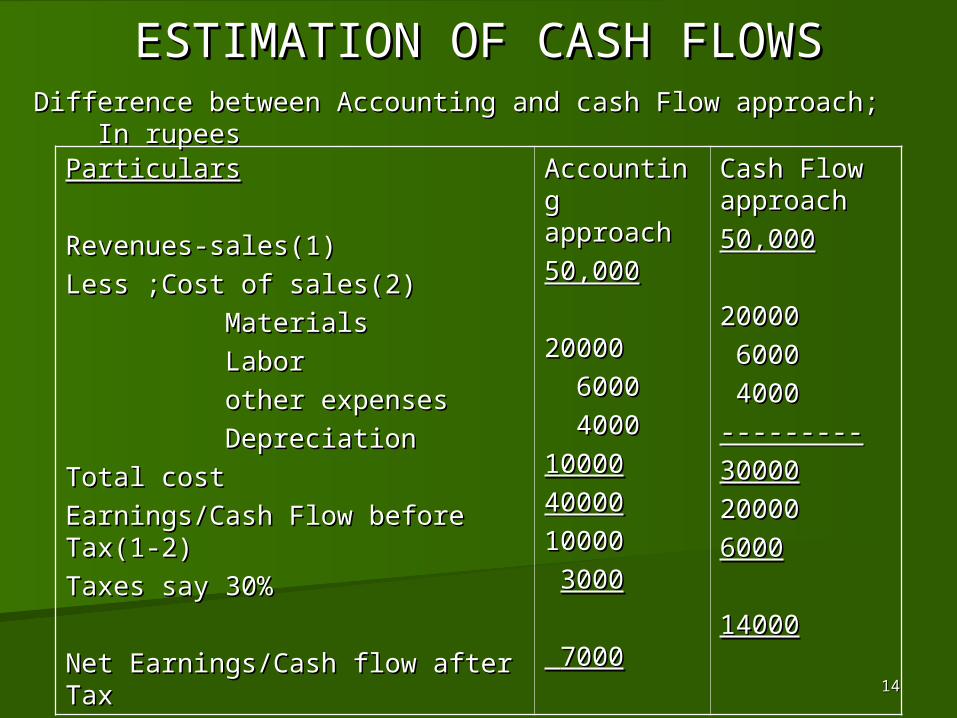

ESTIMATION OF CASH FLOWSESTIMATION OF CASH FLOWSDifference between Accounting and cash Flow approach; In Difference between Accounting and cash Flow approach; In rupeesrupees

ParticularsParticulars

Revenues-sales(1)Revenues-sales(1)

Less ;Cost of sales(2)Less ;Cost of sales(2)

MaterialsMaterials

LaborLabor

other expensesother expenses

DepreciationDepreciation

Total costTotal cost

Earnings/Cash Flow before Tax(1-Earnings/Cash Flow before Tax(1-2)2)

Taxes say 30%Taxes say 30%

Net Earnings/Cash flow after TaxNet Earnings/Cash flow after Tax

Accounting Accounting approach approach

50,00050,000

2000020000

60006000

40004000

1000010000

4000040000

1000010000

30003000

70007000

Cash Flow Cash Flow approachapproach

50,00050,000

2000020000

60006000

40004000

------------------

3000030000

2000020000

60006000

1400014000

1515

ESTIMATION OF CASH FLOWSESTIMATION OF CASH FLOWS2)INCREMENTAL CASH FLOWS;2)INCREMENTAL CASH FLOWS; These are cash flows These are cash flows WITHWITH the Proposed Project MINUS the the Proposed Project MINUS the

company’s cash flow company’s cash flow WITHOUTWITHOUT the Project. the Project. Cash Flows (and only those cash flows) which are directly Cash Flows (and only those cash flows) which are directly

attributable to the Investment are considered.attributable to the Investment are considered. Eg Fixed Overhead costs which remain the same whether the Eg Fixed Overhead costs which remain the same whether the

proposal is accepted or rejected are not considered.proposal is accepted or rejected are not considered. If there is an increase in the FO costs due to the new proposal If there is an increase in the FO costs due to the new proposal

they may be considered.they may be considered.

1616

ESTIMATION OF CASH FLOWSESTIMATION OF CASH FLOWS

Relevant and Irrelevant cash outflows;Relevant and Irrelevant cash outflows;

Relevant for cash outflows;Relevant for cash outflows;

Cost of the InvestmentCost of the InvestmentVariable costs-Material and LaborVariable costs-Material and LaborAdditional Fixed overheadsAdditional Fixed overheadsTaxesTaxesEffects of InflationEffects of InflationOpportunity costsOpportunity costs

Irrelevant for cash outflowsIrrelevant for cash outflows

Fixed OverheadsFixed OverheadsSunk costs.Sunk costs.

1717

ESTIMATION OF CASH FLOWSESTIMATION OF CASH FLOWSINGREDIENTS OF CASH FLOW STREAMS;INGREDIENTS OF CASH FLOW STREAMS;Tax effect-Tax effect-

>Cash flows are to be considered net of taxes. >Cash flows are to be considered net of taxes.

> If the company is loss making any profit earned can be set > If the company is loss making any profit earned can be set off against the losses incurred earlier.off against the losses incurred earlier.

Effect on Other ProjectsEffect on Other Projects; ;

>May have an effect on the proposed project. eg, an existing >May have an effect on the proposed project. eg, an existing product may suffer due to the new project. This has to be product may suffer due to the new project. This has to be factored. The new project evaluation cannot be isolated and factored. The new project evaluation cannot be isolated and taken as it is. taken as it is.

>Any reduction in cash flow of other projects will have a >Any reduction in cash flow of other projects will have a bearing on the Incremental cash flow of the proposed project.bearing on the Incremental cash flow of the proposed project.

Effect of Indirect ExpensesEffect of Indirect Expenses;;

>depends on whether the amount of overheads will change as >depends on whether the amount of overheads will change as a result of the of the decision. If yes, then it should be factored. a result of the of the decision. If yes, then it should be factored. If there is going to no change, then they are not relevant.If there is going to no change, then they are not relevant.

1818

ESTIMATION OF CASH FLOWSESTIMATION OF CASH FLOWSEffect of Depreciation;Effect of Depreciation; Is a non cash expenditure which does not have a cash outflow Is a non cash expenditure which does not have a cash outflow

but has to deducted while working out the tax on the net cash but has to deducted while working out the tax on the net cash flows and evaluation there after.flows and evaluation there after.

Companies Act prescribes various depreciation ratesCompanies Act prescribes various depreciation rates Normally two methods are used-Straight line method or WDV Normally two methods are used-Straight line method or WDV

method.method. Income tax Act provides rates which are also followed by many Income tax Act provides rates which are also followed by many

companies in their books.companies in their books.

Effect of working capital;Effect of working capital; Constitutes another important ingredient which directly affects Constitutes another important ingredient which directly affects

the proposal. It is a cash out flow in the year there is an the proposal. It is a cash out flow in the year there is an increase in the net WC requirement. It could be from t0 to tn.increase in the net WC requirement. It could be from t0 to tn.

1919

ESTIMATION OF CASH FLOWSESTIMATION OF CASH FLOWSCOMPONENTS OF CASH FLOW;COMPONENTS OF CASH FLOW;

1)INITIAL INVESTMENT OR OUTLAY/OUTFLOW-1)INITIAL INVESTMENT OR OUTLAY/OUTFLOW-a)a) Purchase price of “new” assetsPurchase price of “new” assets

b) +Capitalized expenditure-Freight , Insurance, Transportation, b) +Capitalized expenditure-Freight , Insurance, Transportation, Training of Manpower to use the machine,CD etcTraining of Manpower to use the machine,CD etc

c)c) Opportunity costs incurred.. eg own land/house used for the Opportunity costs incurred.. eg own land/house used for the project.project.

d)+ (-)Increase (decrease) =Net Working Capital.d)+ (-)Increase (decrease) =Net Working Capital.

e)-e)- Net proceeds from sale of “old” Assets ,if replacement Net proceeds from sale of “old” Assets ,if replacement

f) f) + (-)+ (-) Taxes (savings) due to the sale of ‘old Taxes (savings) due to the sale of ‘old ‘machines/assets‘machines/assets

f) f) == Initial cash Initial cash outflowoutflow

2020

ESTIMATION OF CASH FLOWSESTIMATION OF CASH FLOWS

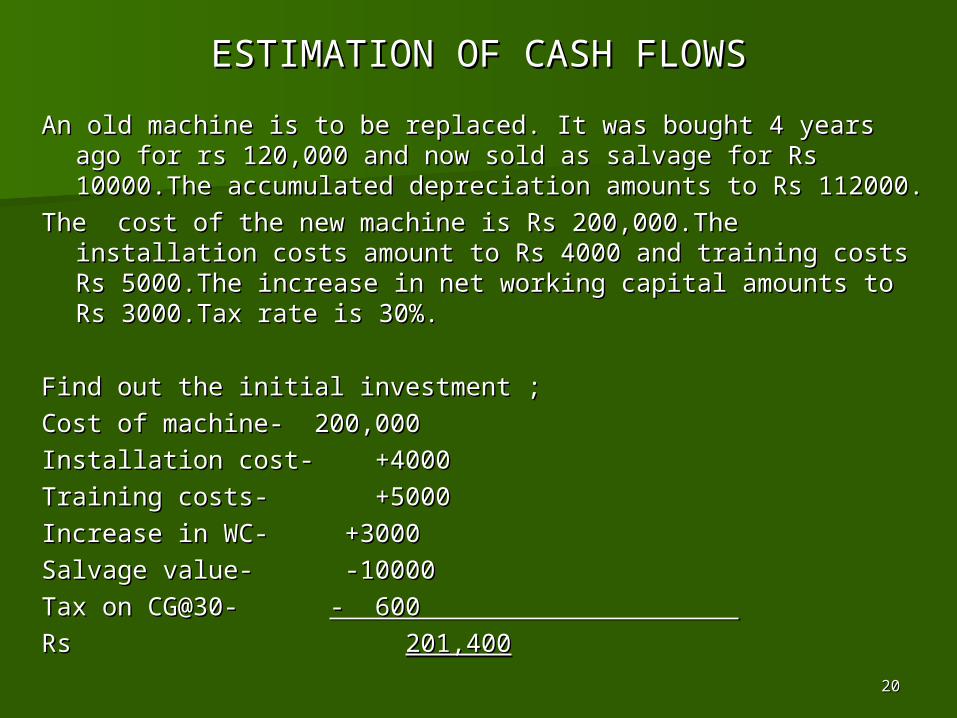

An old machine is to be replaced. It was bought 4 years ago for rs An old machine is to be replaced. It was bought 4 years ago for rs 120,000 and now sold as salvage for Rs 10000.The 120,000 and now sold as salvage for Rs 10000.The accumulated depreciation amounts to Rs 112000.accumulated depreciation amounts to Rs 112000.

The cost of the new machine is Rs 200,000.The installation costs The cost of the new machine is Rs 200,000.The installation costs amount to Rs 4000 and training costs Rs 5000.The increase in amount to Rs 4000 and training costs Rs 5000.The increase in net working capital amounts to Rs 3000.Tax rate is 30%.net working capital amounts to Rs 3000.Tax rate is 30%.

Find out the initial investment ;Find out the initial investment ;

Cost of machine- 200,000Cost of machine- 200,000

Installation cost- +4000Installation cost- +4000

Training costs- +5000Training costs- +5000

Increase in WC- +3000Increase in WC- +3000

Salvage value- -10000Salvage value- -10000

Tax on CG@30- Tax on CG@30- - 600 - 600

Rs Rs 201,400201,400

2121

ESTIMATION OF CASH FLOWSESTIMATION OF CASH FLOWS

2) 2) OPERATING CASH FLOWS/NET ANNUAL CASH OPERATING CASH FLOWS/NET ANNUAL CASH FLOWSFLOWS;;

Represents cash inflows on account of sales/revenue Represents cash inflows on account of sales/revenue generation minus cash out flow on account of expenses.generation minus cash out flow on account of expenses.

Every Investment is expected to generate future benefits in Every Investment is expected to generate future benefits in the form of cash flows from operations.the form of cash flows from operations.

Represents annual cash flows generated from the investments.Represents annual cash flows generated from the investments.

Represent net flows before depreciation and after taxes.Represent net flows before depreciation and after taxes.

2222

ESTIMATION OF CASH FLOWSESTIMATION OF CASH FLOWS

3)TERMINAL CASH FLOWS3)TERMINAL CASH FLOWS; ; The cash inflow to the company during the terminal The cash inflow to the company during the terminal year (last year) is called Terminal cash flow.year (last year) is called Terminal cash flow.Represents some value in the asset when the asset is Represents some value in the asset when the asset is terminated/project is completed.terminated/project is completed.When Replacement decision is taken to replace old When Replacement decision is taken to replace old asset with new asset, the sale value of the old asset is asset with new asset, the sale value of the old asset is the terminal cash flow of the asset replaced. (eg True the terminal cash flow of the asset replaced. (eg True value exchange of Maruthi car).value exchange of Maruthi car).Due to termination of the Asset, there may be release Due to termination of the Asset, there may be release of some Net working capital tied up in the initial year of some Net working capital tied up in the initial year which should also be added to the salvage of the asset which should also be added to the salvage of the asset in the terminal cash flows.in the terminal cash flows.

2323

ESTIMATION OF CASH FLOWSESTIMATION OF CASH FLOWS

Determination of InflowsDetermination of Inflows

ParticularsParticulars

SalesSales

Less Operating costsLess Operating costs

Cash Inflows before Taxes Cash Inflows before Taxes (CFBT)(CFBT)

Less DepnLess Depn

Taxable IncomeTaxable Income

Less TaxLess Tax

Earnings after TaxEarnings after Tax

Plus DepreciationPlus Depreciation

Cash inflows after Taxes Cash inflows after Taxes ( CFAT)( CFAT)

PLUS salvage value (yn)PLUS salvage value (yn)

PLUS Recovery of working PLUS Recovery of working capitalcapital

Y1 Y1 y2y2 y3y3 y4y4 ynyn

2424

ESTIMATION OF CASH FLOWSESTIMATION OF CASH FLOWSInvestments, costs and Revenues( in rs 000)Investments, costs and Revenues( in rs 000)

RevenuesRevenues

Costs -Costs -300300

Undiscounted cash flow -Undiscounted cash flow -300300

Cum cash flow -Cum cash flow -300300

NPV=400NPV=400

Pay back period=2.78 Pay back period=2.78 yearsyears

Y1Y1

100100

2020

8080

-220-220

Y2Y2

100100

2020

8080

-140-140

Y3Y3

200200

2020

180180

4040

Y4Y4

200200

2020

180180

220220

Y5Y5

200200

2020

180180

400400

2525

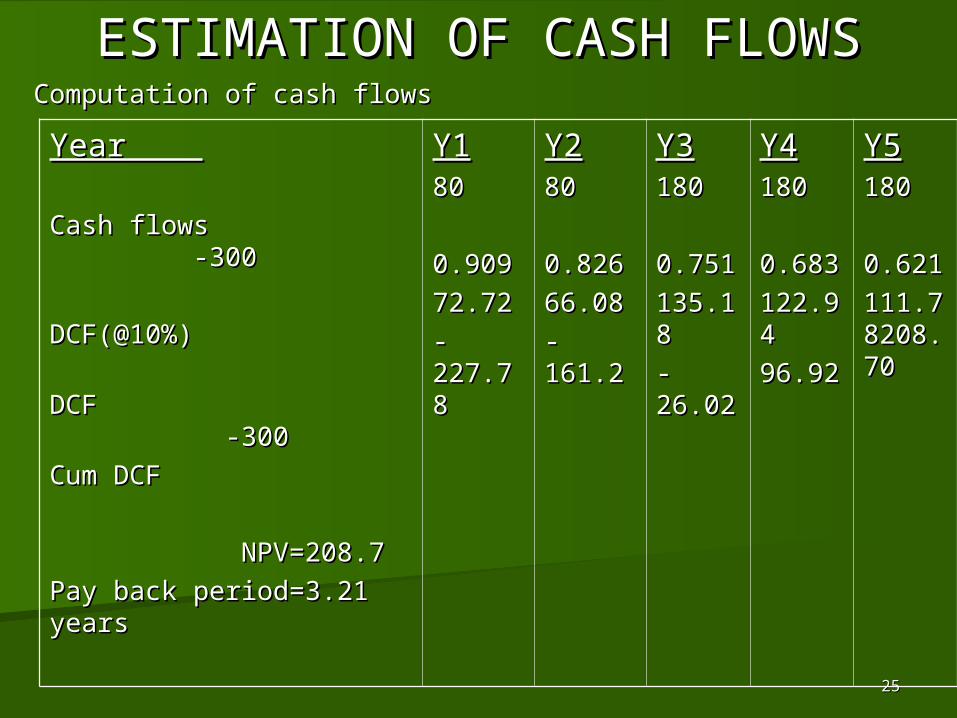

ESTIMATION OF CASH FLOWSESTIMATION OF CASH FLOWSComputation of cash flowsComputation of cash flows

Year Year Cash flows -Cash flows -300300

DCF(@10%) DCF(@10%)

DCF -DCF -300300

Cum DCFCum DCF

NPV=208.7NPV=208.7

Pay back period=3.21 Pay back period=3.21 yearsyears

Y1Y18080

0.9090.909

72.7272.72

--227.7227.788

Y2Y28080

0.8260.826

66.0866.08

-161.2-161.2

Y3Y3180180

0.7510.751

135.1135.188

--26.0226.02

Y4Y4180180

0.6830.683

122.9122.944

96.9296.92

Y5Y5180180

0.6210.621

111.7111.78208.8208.7070

2626

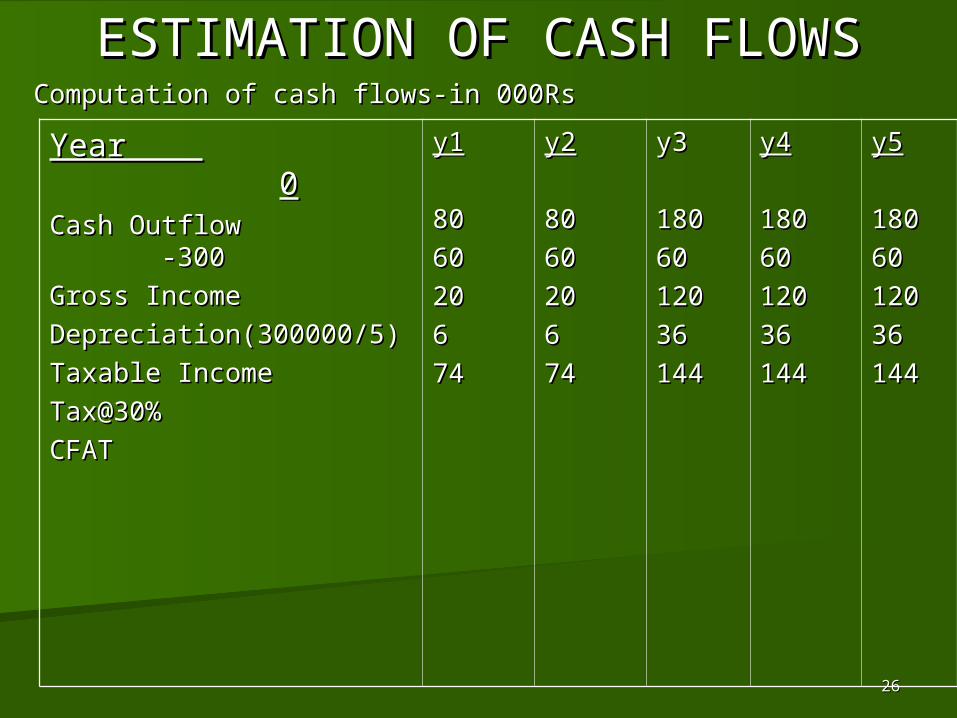

ESTIMATION OF CASH FLOWSESTIMATION OF CASH FLOWSComputation of cash flows-in 000RsComputation of cash flows-in 000Rs

Year Year 00Cash Outflow -Cash Outflow -300300

Gross IncomeGross Income

Depreciation(300000/5)Depreciation(300000/5)

Taxable IncomeTaxable Income

Tax@30%Tax@30%

CFATCFAT

y1y1

8080

6060

2020

66

7474

y2y2

8080

6060

2020

66

7474

y3y3

180180

6060

120120

3636

144144

y4y4

180180

6060

120120

3636

144144

y5y5

180180

6060

120120

3636

144144

2727

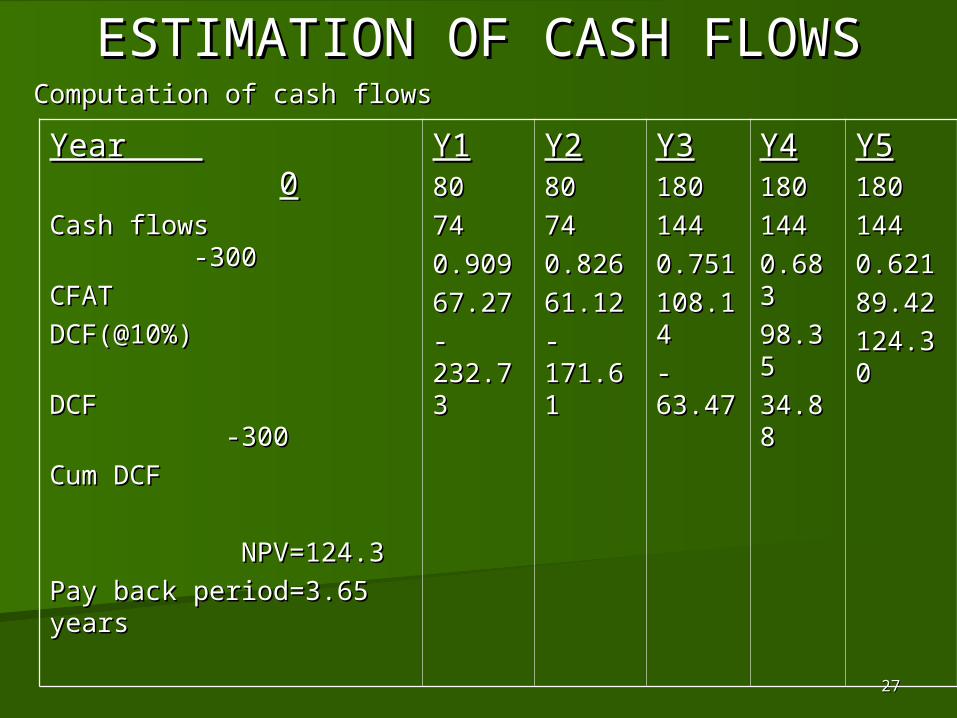

ESTIMATION OF CASH FLOWSESTIMATION OF CASH FLOWSComputation of cash flowsComputation of cash flows

Year Year 00Cash flows -Cash flows -300300

CFATCFAT

DCF(@10%) DCF(@10%)

DCF -DCF -300300

Cum DCFCum DCF

NPV=124.3NPV=124.3

Pay back period=3.65 Pay back period=3.65 yearsyears

Y1Y18080

7474

0.9090.909

67.2767.27

--232.7232.733

Y2Y28080

7474

0.8260.826

61.1261.12

--171.6171.611

Y3Y3180180

144144

0.7510.751

108.1108.144

--63.4763.47

Y4Y4180180

144144

0.6830.683

98.3598.35

34.8834.88

Y5Y5180180

144144

0.6210.621

89.4289.42

124.3124.300

2828

ESTIMATION OF CASH FLOWSESTIMATION OF CASH FLOWS

BEFORE TAX AFTER BEFORE TAX AFTER TAXTAXNPV (Rs NPV (Rs 000)000)

400400

208.7208.7

85.585.5

2.22.2

PAY BACK PAY BACK PERIODPERIOD

2.782.78

3.213.21

3.853.85

4.954.95

Rate(%)Rate(%)

00

1010

2020

3030

PAY BACK PAY BACK PERIODPERIOD

3.063.06

3.653.65

4.64.6

>5>5

NPV( Rs NPV( Rs 000)000)

280280

124.31124.31

23,6723,67

-44.63-44.63

2929

ESTIMATION OF CASH FLOWSESTIMATION OF CASH FLOWS

IMPACT OF IMPROPER CASH FLOW ESTIMATION;IMPACT OF IMPROPER CASH FLOW ESTIMATION;

Reasons;Reasons;Improper assessment of the project.Improper assessment of the project.Inadequate Data.Inadequate Data.

Results;Results;

Affects investment evaluation leading to wrong decision Affects investment evaluation leading to wrong decision making.making.Affects the profitability of the project and the company.Affects the profitability of the project and the company.Affects the financial position of the company leading to cash Affects the financial position of the company leading to cash crunch situationscrunch situationsAffects the existing business lines as the “new” project starts Affects the existing business lines as the “new” project starts eating into the resources of the existing business.eating into the resources of the existing business.Affects the reputation of the company.Affects the reputation of the company.

3030

ESTIMATION OF CASH FLOWSESTIMATION OF CASH FLOWSCase study;Case study;““A” company is into retail business for the last 10 years with an A” company is into retail business for the last 10 years with an average turnover of Rs 50 crores and an average net profit of average turnover of Rs 50 crores and an average net profit of Rs 2.5 crores during the last 5 years. As the margins are low in Rs 2.5 crores during the last 5 years. As the margins are low in retail business due to severe competition, the average net retail business due to severe competition, the average net profits of the retail Industry is around 5% and A company was profits of the retail Industry is around 5% and A company was within the Industry standards vis a vis the average net profit.within the Industry standards vis a vis the average net profit.The Management wanted to expand and it took on lease a The Management wanted to expand and it took on lease a property in the CBD area and modified it into an ultra modern property in the CBD area and modified it into an ultra modern show room .The cost of the expansion was Rs 50 crores and it show room .The cost of the expansion was Rs 50 crores and it had to borrow the entire amount as term loan from the bank had to borrow the entire amount as term loan from the bank at an interest rate of 12 %per annum repayable in 10 years. at an interest rate of 12 %per annum repayable in 10 years. Annual property lease cost is Rs 2 crores.Annual property lease cost is Rs 2 crores.The new showroom would generate an average turnover of Rs The new showroom would generate an average turnover of Rs 30 crores per annum in the first 5 years with an average net 30 crores per annum in the first 5 years with an average net profit of 1.5 crores @5percent. The gross profit is 30 percentprofit of 1.5 crores @5percent. The gross profit is 30 percentHas “A “company taken a good decision? Make suitable Has “A “company taken a good decision? Make suitable assumptions and advise “A “company the position ,pointing out assumptions and advise “A “company the position ,pointing out where and in which areas of cash flow estimation they have where and in which areas of cash flow estimation they have gone wrong.gone wrong.

3131

ESTIMATION OF CASH FLOWSESTIMATION OF CASH FLOWS

Thank youThank you