cccc- the industry leader with attractive valuation jp...

TRANSCRIPT

June, 2013

JP Morgan Investors Forum, Beijing

CCCC- The Industry Leader With Attractive Valuation

Agenda

1

Company Overview

Financial Highlights and Stock Performance

Focus of Business Strategy

Industry Opportunity and Company Outlook

2

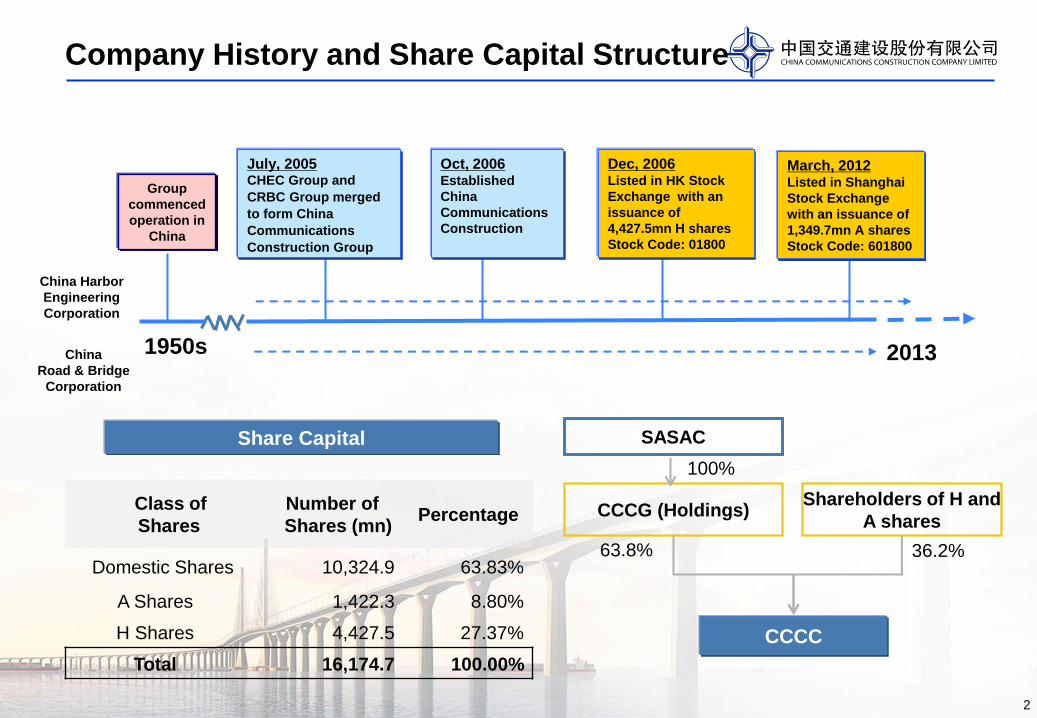

Company History and Share Capital Structure

2013 1950s

Class of

Shares

Number of

Shares (mn) Percentage

Domestic Shares 10,324.9 63.83%

A Shares 1,422.3 8.80%

H Shares 4,427.5 27.37%

Total 16,174.7 100.00%

Share Capital SASAC

63.8%

Shareholders of H and

A shares

36.2%

100%

CCCG (Holdings)

Oct, 2006 Established

China

Communications

Construction

July, 2005 CHEC Group and

CRBC Group merged

to form China

Communications

Construction Group

Dec, 2006 Listed in HK Stock

Exchange with an

issuance of

4,427.5mn H shares

Stock Code: 01800

Group

commenced

operation in

China

China Harbor

Engineering

Corporation

China

Road & Bridge

Corporation

March, 2012 Listed in Shanghai

Stock Exchange

with an issuance of

1,349.7mn A shares

Stock Code: 601800

CCCC

3

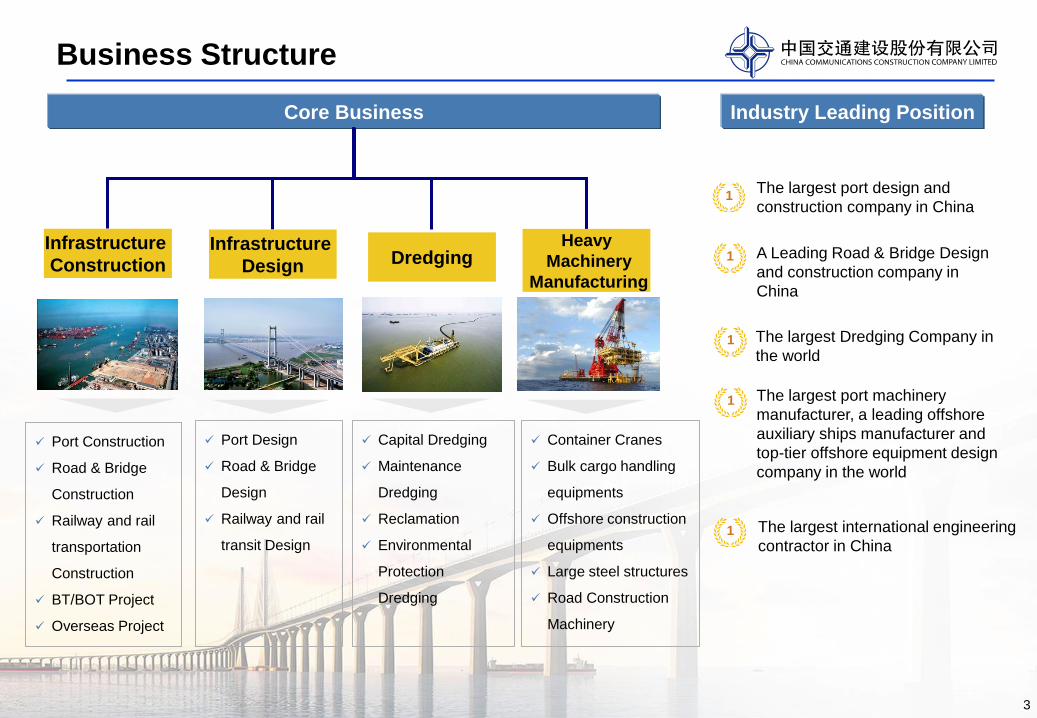

Business Structure

Core Business

Infrastructure

Construction

Port Construction

Road & Bridge

Construction

Railway and rail

transportation

Construction

BT/BOT Project

Overseas Project

Port Design

Road & Bridge

Design

Railway and rail

transit Design

Capital Dredging

Maintenance

Dredging

Reclamation

Environmental

Protection

Dredging

Container Cranes

Bulk cargo handling

equipments

Offshore construction

equipments

Large steel structures

Road Construction

Machinery

Infrastructure

Design Dredging Heavy

Machinery

Manufacturing

Industry Leading Position

1

1

1

1

1

The largest port design and

construction company in China

A Leading Road & Bridge Design

and construction company in

China

The largest Dredging Company in

the world

The largest port machinery

manufacturer, a leading offshore

auxiliary ships manufacturer and

top-tier offshore equipment design

company in the world

The largest international engineering

contractor in China

Agenda

4

Company Overview

Financial Highlights and Stock Performance

Focus of Business Strategy

Industry Opportunity and Company Outlook

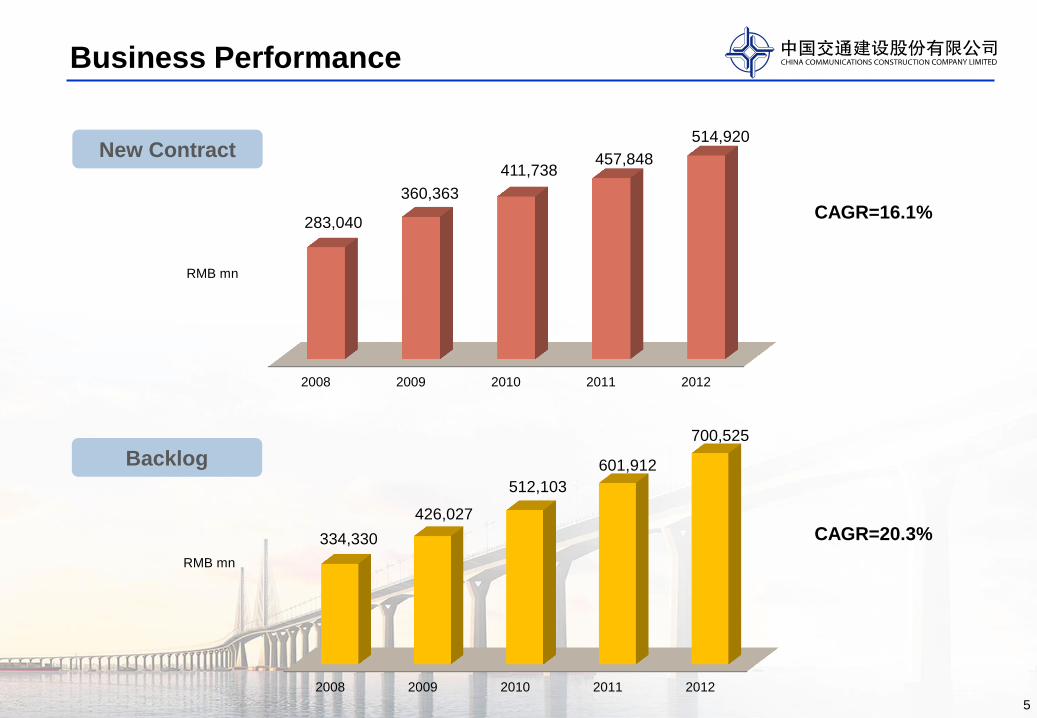

Business Performance

5

New Contract

Backlog

CAGR=16.1%

2008 2009 2010 2011 2012

283,040

360,363

411,738 457,848

514,920

2008 2009 2010 2011 2012

334,330

426,027

512,103

601,912

700,525

CAGR=20.3%

RMB mn

RMB mn

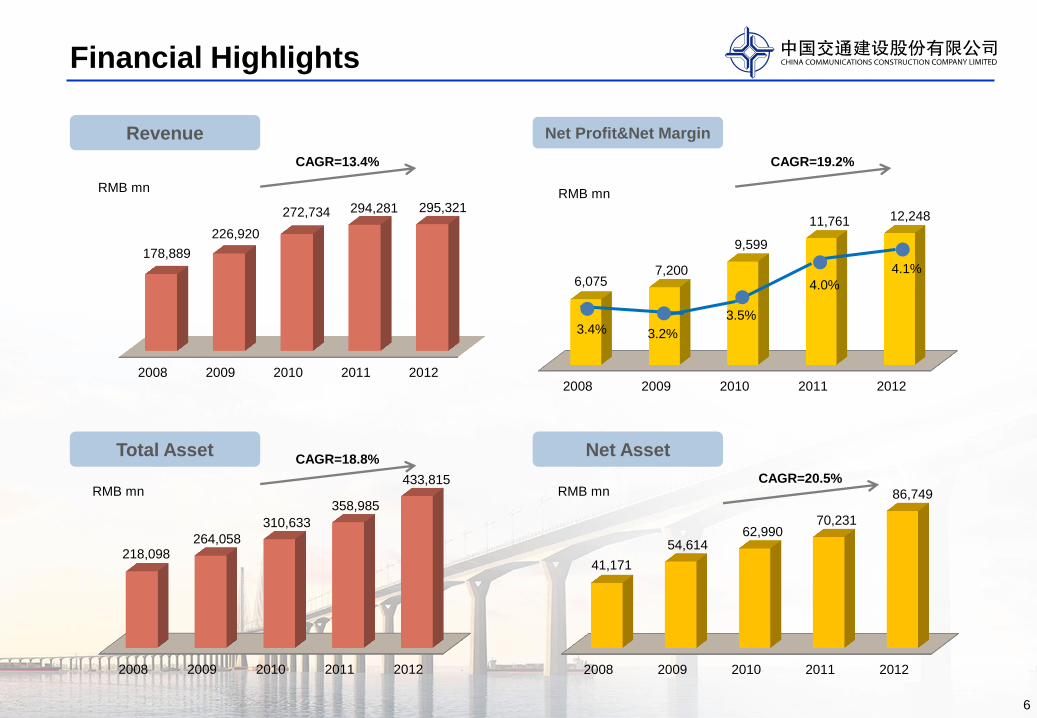

2008 2009 2010 2011 2012

218,098 264,058

310,633

358,985

433,815

CAGR=18.8%

2008 2009 2010 2011 2012

6,075 7,200

9,599

11,761 12,248

3.4% 3.2%

3.5%

4.0%

4.1%

2008 2009 2010 2011 2012

41,171

54,614 62,990

70,231

86,749

Financial Highlights

6

Net Profit&Net Margin

2008 2009 2010 2011 2012

178,889

226,920

272,734 294,281 295,321

Revenue

Total Asset Net Asset

CAGR=13.4% CAGR=19.2%

CAGR=20.5%

RMB mn

RMB mn RMB mn

RMB mn

Stock Performance Since Listing

7

0

2000

4000

6000

8000

10000

12000

14000

-100%

-50%

0%

50%

100%

150%

200%

250%

300%

350%

06-12 07-06 07-12 08-06 08-12 09-06 09-12 10-06 10-12 11-06 11-12 12-06 12-12

成交金额 CCCC HSI HSCEI

CCCC’s H-share price outperformed HSI and HSCEI for much of the time since listing,

which has demonstrated market confidence in the company. It reached its historical high

price at HKD24.6 in Nov 2007.

Resulted from gloomy market expectations influenced by economic downturn and

tightening policy by the Chinese government, CCCC’s share price had been sluggish for

the year around 2010, but for the year 2012 it started to pick up and outperform again.

Volume

Agenda

8

Company Overview

Financial Highlights and Stock Performance

Focus of Business Strategy

Industry Opportunity and Company Outlook

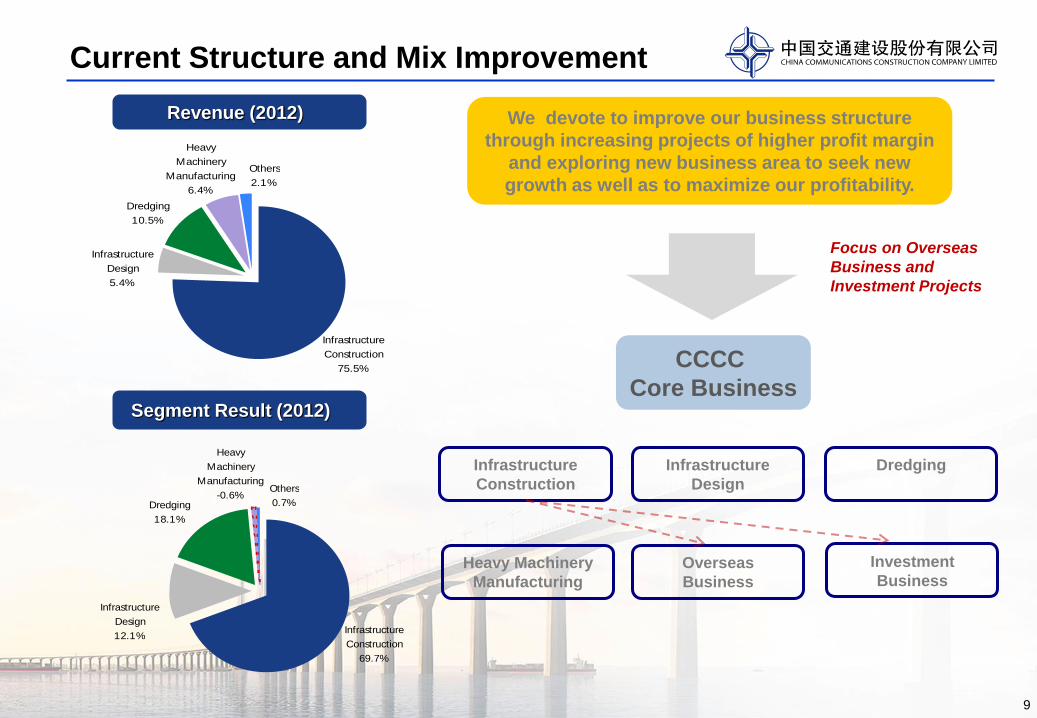

Infrastructure

Construction

75.5%

Infrastructure

Design

5.4%

Dredging

10.5%

Heavy

Machinery

Manufacturing

6.4%

Others

2.1%

Segment Result (2012)

Infrastructure

Construction

69.7%

Infrastructure

Design

12.1%

Dredging

18.1%

Heavy

Machinery

Manufacturing

-0.6%Others

0.7%

Revenue (2012) We devote to improve our business structure

through increasing projects of higher profit margin

and exploring new business area to seek new

growth as well as to maximize our profitability.

Focus on Overseas

Business and

Investment Projects

CCCC

Core Business

Infrastructure

Construction

Heavy Machinery

Manufacturing

Infrastructure

Design

Investment

Business Overseas

Business

Dredging

Current Structure and Mix Improvement

9

We have established global

presence in over 120 countries and

regions, e.g. Africa, South East

Asia and Middle East.

Latin America is one area of new

focus.

2008 2009 2010 2011 2012

60,800 62,720 62,323

80,828 75,417

14,700

21,958 27,151

32,151 38,950

New order

Revenue

RMB million

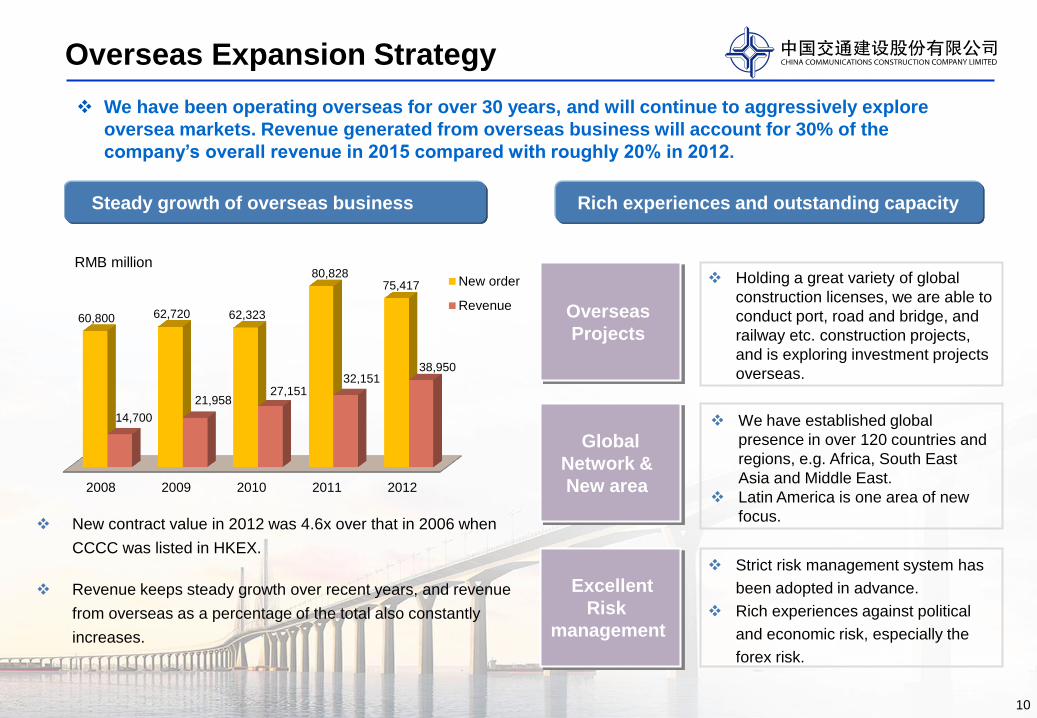

10

Overseas Expansion Strategy

We have been operating overseas for over 30 years, and will continue to aggressively explore

oversea markets. Revenue generated from overseas business will account for 30% of the

company’s overall revenue in 2015 compared with roughly 20% in 2012.

Rich experiences and outstanding capacity Steady growth of overseas business

Holding a great variety of global

construction licenses, we are able to

conduct port, road and bridge, and

railway etc. construction projects,

and is exploring investment projects

overseas.

Overseas

Projects

Global

Network &

New area

Excellent

Risk

management

Strict risk management system has

been adopted in advance.

Rich experiences against political

and economic risk, especially the

forex risk.

New contract value in 2012 was 4.6x over that in 2006 when

CCCC was listed in HKEX.

Revenue keeps steady growth over recent years, and revenue

from overseas as a percentage of the total also constantly

increases.

11

Further Development of Investment Business

The idea of developing investment business (mainly BT/BOT project) is to transform CCCC from a

contractor to a contractor + operator with assets that are able to generate stable returns in the long-term.

Xianning to Tongshan

Expressway in Hubei Province,

BOT+EPC Project

Guiyang to Duyun Expressway

in Guizhou Province,

BOT+EPC Project

Guangming Expressway,

Guangzhou,

BOT Project

Setting as the focus of business

transition as the company

strategic plan

Projects mainly include: Expressway, land development, real estate,

integrated urban development, etc.

Strict risk control: “Five Don’ts” – not undertaking projects which:

fall outside of our core business, require un-

secured loans, have no guarantees, deliver below

standard rates of return, and exceed our capability

Chongqing Chaotianmen

Yangtze River Bridge,

BT Project

At the end of 2012

Number of investment projects: 103

Total investment (contract value): RMB274.5bn

Revenue from investment projects as a

percentage of total: 10.3%

Target value of overall BOT asset

by end of 2015: RMB100bn

12

Unique Business Model

Diversified products create a balanced business and help minimise risks.

Comprehensive solutions are available to customers as a result of integrated business chain.

Combinative

business of

land and

water

One-stop

solutions

Ports, navigation

channels, roads,

bridges, tunnels,

railways, urban

rails, airport

Planning

Design and Build

Investment

Operation

HongKong-Macao-

Zhuhai Bridge under

construction :

Master plan, reclamation

of artificial islands, steel

structure manufacturing,

construction of islands

and tunnels by CCCC

Zhuhai Hengqin Island

under construction:

Integrated development of

the new city area, including

infrastruture construction and

reclamation of artificial

islands by CCCC

Agenda

13

Company Overview

Financial Highlights and Stock Performance

Focus of Business Strategy

Industry Opportunity and Company Outlook

14

11th Five-Year Plan 12th Five-Year Plan %change

Total Transportation Network (thousand km) 4,320 4,900 13.4%

Railway mileage (thousand km) 91 120 31.9%

Expressway mileage (thousand km) 58 83 43.1%

Urban rail mileage (km) 1,400 3,000 114.3%

Number of deep-water berths 1,774 2,214 24.8%

Number of airport for civil use 175 230 31.4%

Industry Opportunity

The 12th Five-Year Plan for Comprehensive Development of Transportation (MOT, July 2012)

MOT General Policy on

Transportation Infrastructure

Development:

Moderately In Advance

-Out of the MOT plan, there are

increasing demand of urban

development as a result of

urbanization

-Investment as a major impetus

for Chinese economic growth

- More credit flowing into real

economy

Market

Opportunity

for CCCC

15

Outlook

Leading global contractor that provides one-stop

services in infrastructure construction

Global investor in infrastructure

Developer and Operator in comprehensive

civil engineering and development

Global top-tier company with standardized corporate

governance structure, scientific management, flexible

operational system, state-of-the-art expertise, high

employee satisfactions and strong social recognition.

Overall Target

Becoming a top-tier

conglomerate worldwide

Maximizing shareholder’s

interests

16

Thank You

Investor Relations Team

YU Jingjing, TAN Lu, ZHAO Yang, LI Yilin

Tel: +86-10-8201 6562

Fax: +86-10-8201 6524

Email: [email protected]