cdfi certification: a building block of community finance

TRANSCRIPT

Community Development with a Purpose

CDFI Certification: A Building Block of Community Finance

CDFI Fund

• CDFI Fund established by Congress in 1994 through the efforts of Federation and others in community finance

• Certification given by the U.S. Department of Treasury

• Broad bi-partisan support; appropriations stable or increasing

Mission of CDFI Fund Expand the capacity of financial institutions to provide credit, capital, and financial services to underserved populations and economically distressed communities in the United States

CDFI Target Markets

• Places (Geographic) CDFI Investment Area (Census Tracts) Low Income High Poverty High Unemployment

384 Persistent Poverty Counties Poverty rate above 20% as of 1990, 2000 and 2010

• People (Demographic) Low Income Targeted Populations Other Targeted Populations

Credit Unions & CDFI Fund

• CUs Initially slow to embrace CDFI certification

• New momentum since 2010 Doubling in number of NCUA Low Income Designated CUs

Increased visibility of CDFI success stories

2014 NCUA CDFI Certification Challenge

Federation CDFI Certification Challenge

Positive research findings on performance & impact of CDFI CUs

The CDFI Industry

• More than just credit unions…

Type of CDFI December 2013 October 2015

Percentage Increase

Number Percent Number Percent

Unregulated CDFIs

Loan Funds 492 61% 514 53% +4%

Venture Capital Funds 13 2% 14 1% +8%

Regulated CDFIs

Credit Unions 173 22% 265 27% +53%

Banks and Thrifts 76 9% 112 12% +47%

Depository Holding Companies 50 6% 61 6% +22%

Total 804 100% 966 100%

Top Ten States for CDFI Credit Unions

Rank State # CDFIs Credit Unions Loan Funds

Banks & Depository

Holding Companies

Venture Capital Funds

CU % of State CDFIs

1 Missouri 33 27 4 2 0 82%

2 Louisiana 51 21 8 21 1 41%

3 New York 73 17 49 6 1 23%

4 Texas 34 15 18 1 0 44%

5 Florida 33 14 19 0 0 42%

6 Michigan 24 13 10 1 0 54%

7 California 79 11 50 17 1 14%

8 Mississippi 63 11 3 49 0 17%

9 Illinois 34 10 8 15 1 29%

10 Washington 25 9 16 0 0 36%

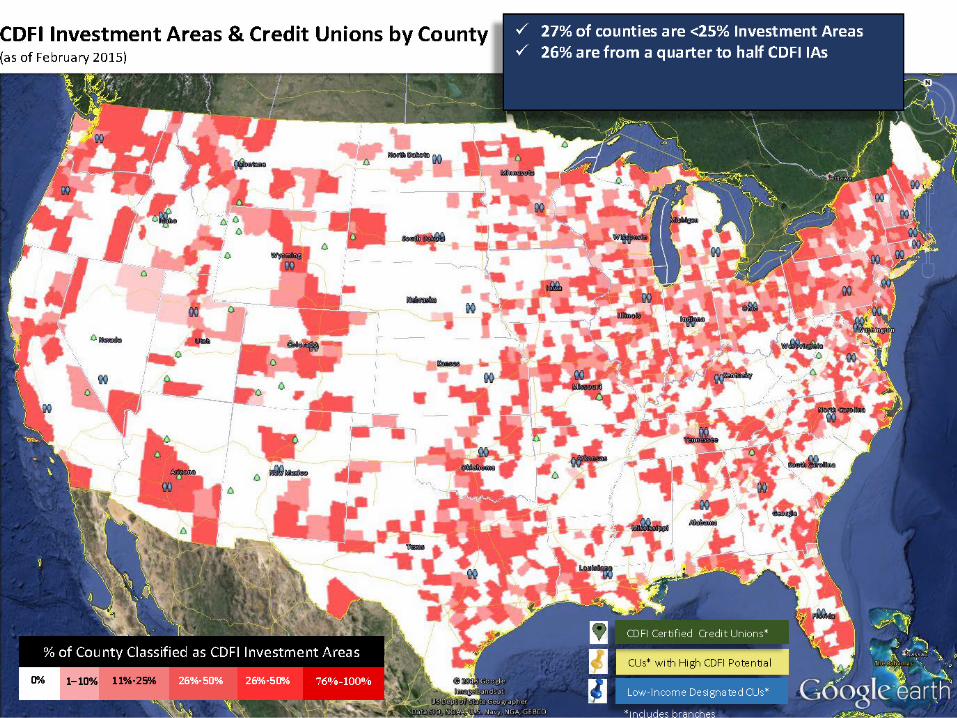

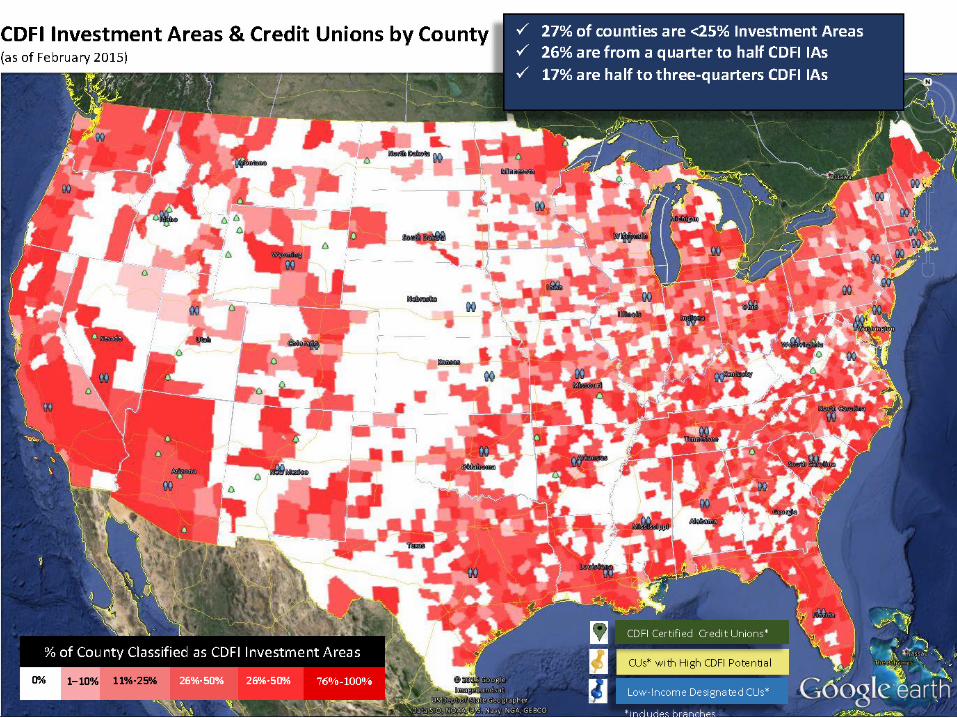

CDFI Certifications as of 10/31/2015

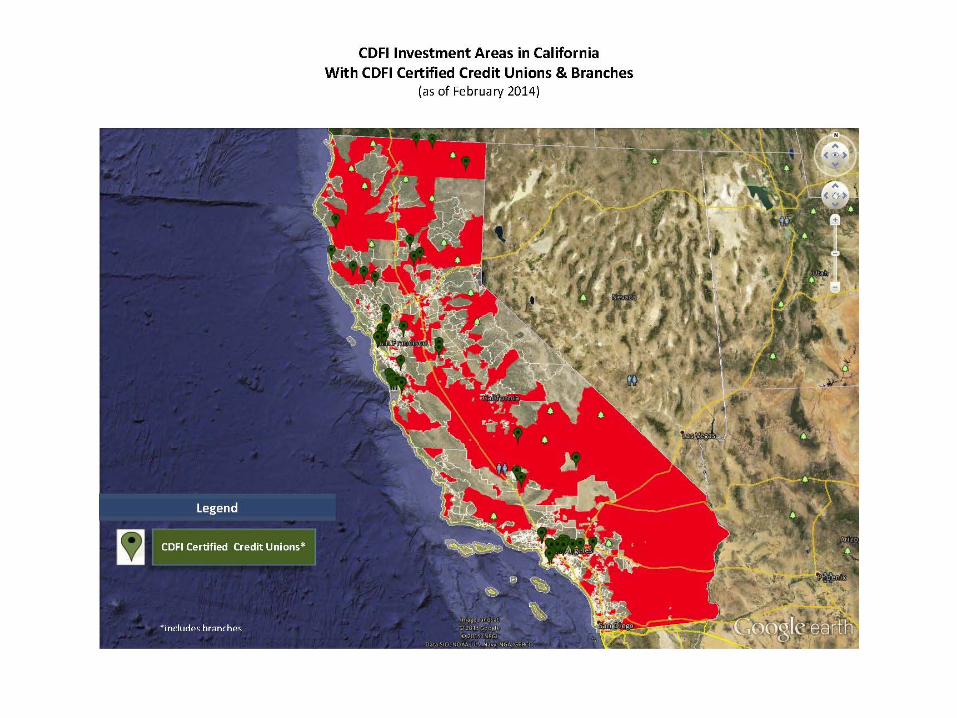

California in CDFI Terms

• 46% of census tracts in state classified as “Investment Areas” by CDFI Fund Indicators of economic distress include low median family income, high rates of

poverty, unemployment

• Nearly 17 million Californians live in CDFI Investment Areas

• 11 California credit unions are CDFI certified

• 34 credit unions show strong potential for certification More than 67% of branches located in CDFI Investment Areas

Strong financial and operational capacity

Profile of community development products and services comparable to CDFI credit unions

By the numbers

Type of Credit Unions

# of CUs

# of Branches

Total Members

Total Assets

CDFI Certified 11 56 328,603 $ 4,061,370,839

High Potential CDFIs 34 63 215,298 $ 1,896,659,823

Totals 45 119 543,901 $ 5,958,030,662

California CDFI Credit Unions CDFI certifications as of 10/31/2015; Financial data as of 12/31/2014

CDFI CUs by Congressional District

• All 53 Congressional Districts include census tracts that qualify as CDFI Investment Areas minimum 11 tracts in CA 45th

maximum 176 tracts in CA 11th

• CDFI certified credit unions are located in 21 Districts From 1 to 8 branches, depending on District

• 32 Districts have no CDFI certified credit unions at this time

• 43 potential CDFI credit unions have branches in

13 Districts that currently have at least one CDFI credit union

25 Districts that currently have zero

What the Research Says

2011

2012 2014

2015

Positive Impact of CDFI Credit Unions

• CDFIs promote economic revitalization among underserved communities and populations

• Financial services are a critical path to financial inclusion

• CDFI credit unions leverage more private capital than any other type of CDFI

Median Loan Fund leverage: $1.10 Median CDFI Credit Union leverage: $9.91

• From 2009-2013, 61 credit unions that received $102.7 million in CDFI grants increased

Total Assets by $2.4 billion Total Loans by $1.5 Billion Leverage rate of more than 23:1

Positive Performance of CDFI Credit Unions

• Despite serving low-income, underserved markets, when compared with mainstream peers, CDFI credit unions – Deliver comparable financial results (ROI) Show no greater institutional risks Rate equal or better in operational efficiency

• CDFI CUs outperform their mainstream peers in – Member service technologies Complex loan products Community development loan products Community development services Capacity building services

What Makes a CDFI?

• CDFI Fund has 7 requirements for certification – 1. Legal entity

2. Primary mission of community development

3. Financing entity

4. Target market (more than 60% of activities)

5. Accountability to target market

6. Development services to build capacity of members

7. Non-governmental entity.

What Really Makes a CDFI?

• A matter of intent – What they do, not where they live

• CDFI credit unions far more likely than peers to offer Community Development Loan Products credit builder, shared secured credit cards, micro business & consumer,

pay da, refund anticipation anti-predatory STS loans

Community Development Savings & Account Services check-cashing, international remittances, money orders, business share

accounts

Capacity-Building Services financial counseling, financial education, first-time home-buyers

programs, bilingual services, free tax preparation services.

CDFI Certification

Requirements & Process

7 Tests for CDFI Certification

1. Legal Entity

2. Primary Mission

3. Financing Entity

4. Target Market

5. Accountability

6. Development Services

7. Non-Government Entity

Documents Automatic

Documents Automatic

Documents Automatic

Documents Automatic (LICUs)

Documents Automatic

What’s left?

1. Legal Entity

2. Primary Mission

3. Financing Entity

4. Target Market

5. Accountability

6. Development Services

7. Non-Government Entity

Test # 4: Target Market

• Single most critical test for credit unions • At least 60% of financing activities must be targeted to eligible

Target Market • CDFI Target Markets: CDFI Investment Areas Low-Income Targeted Populations Other Targeted Populations

• May use one or more TMs to qualify

Investment Areas (IA)

• A geographic unit (county, census tract, block group, Indian/Native areas), or contiguous geographic units in the US that meets distress benchmarks for:

Low median family income; High rate of poverty; and/or High rate of unemployment.

• Most CDCUs qualify simply on IA criteria

• Easiest Target Market to document Random sample of member addresses CDFI Fund mapping program Qualified Investment Area must consist of contiguous tracts

Geocode member addresses to tell % that live in Investment Areas Cross check with updated ACS data

Low Income Targeted Pop (LITP)

• Population for a geographic unit is comprised of individuals whose family income is not more than 80% of the MFI.

• Requires more extensive analysis: Federation has developed a Random sample

of borrowers addresses and income CDFI Fund mapping program Geocode member addresses to tell % that live in

Investment Areas Identify area median income benchmark for each

borrower Compare actual borrower income to low-income

benchmark

Other Targeted Populations

• African Americans, Alaska Natives residing in Alaska, Hispanics, Native Americans, Native Hawaiians residing in Hawaii, Other ethnicities.

• OTP data not typically collected systematically by credit unions

• Must provide basis for estimating % of total activities directed towards OTP

• OTP credit unions can generally also qualify on basis of Investment Areas or Low-Income Targeted Populations

Test #5: Accountability

• Based on analysis of governing and advisory board members • Automatic for or credit unions with Target Market defined as Low

Income Targeted Population (LITP) or Investment Areas (if accounts for more than 50% activities)

OTP (if accounts for more than 50% of activities)

• CU boards are democratically elected by the people they serve (no other types of CDFIs have such direct accountability to their TMs)

• Federation continues to advocate with CDFI Fund that credit unions are automatically accountable to all TMS in proportion to membership CDFIs must ensure that Boards understand and support CDFI

certification

#6. Development Services

• Non transactional activities Builds capacity to manage personal finances Linked to financial products e.g., financial education, credit counseling, VITA/EITC

• Complete Development Services Table

• Provide one-page narrative Briefly describe each Development Service Clearly describe link to CU financial products

• If a partner organization provides your Dev Services: Describe relationship Attach a copy of the services contract/agreement

CDFI Certification Assistance

• Federation approach is based on preliminary analysis of a CU’s borrowers sampling

• Helps determine eligibility • 100% success rate for eligible

certification applicants • Sampling can be used for

Certification, Recertification, Monitoring and CDCI Compliance

Questions?