cdp 2014 investor - air products & chemicals/media/files/pdf/company/cdp-2014-response.pdf2...

TRANSCRIPT

CDP 2014 Investor CDP 2014 Information Request

2

Module: Introduction

CC0.1 Introduction

Please give a general description and introduction to your organization Air Products (NYSE:APD) serves customers in technology, energy, healthcare and industrial markets worldwide with a unique portfolio of products, services and solutions, providing atmospheric, process and specialty gases; performance materials; and equipment and services. For over 70 years, the company has enabled customers to become more productive, energy efficient and sustainable. With fiscal 2013 annual revenues of $10 billion, operations in more than 50 countries, and 21,600 employees, we strive to build lasting relationships with our customers and communities based on understanding, integrity and passion.

Air Products ranks 276th in sales among FORTUNE magazine's 2014 list of the 500 largest corporations in the United States. Corporate headquarters are located in eastern Pennsylvania's Lehigh Valley, near Allentown; European headquarters are at Hersham, near London; and Asian headquarters are in Singapore and Shanghai.

This is Air Products’ 12th consecutive response to the Carbon Disclosure Project information request. Our emissions reporting period is January 1, 2013 to December 31, 2013.

We maintain an open dialogue regarding our environmental performance, as detailed in our Corporate Sustainability (GRI) and Annual Reports [2013 Sustainability Report and 2013 Annual Report attached].

From our earliest days as a gases company with atmospheric gas separation at our core, we’ve delivered technologies and solutions that have contributed to cleaner air, energy efficiency improvements, and safer products for our customers and the communities where we live and operate. In bringing this unique capability and real answers to market problems, our commitment to protect the environment has never wavered. Over 70 years later, with the hurdles we all face in protecting the global environment from climate change, we believe the challenge of mitigating greenhouse gases (GHG) must be addressed through a diverse mix of technology solutions.

Our strategy for responding to climate change is straight forward – identify opportunities where our core technology and product strengths bring cost-effective solutions to enable our customers to reduce their overall supply-chain environmental impact, and seek to minimize GHG emissions and the potential cost impact of a carbon-constrained energy supply on our operations through continued technology innovation and energy efficiency. As a subset of Air Products’ Sustainability Council, our Greenhouse Gas (GHG) Strategy Team serves as our company-wide center of excellence on climate change and leads the company’s efforts to explore new markets and technologies. Research and development efforts include partnering with appropriate government agencies and industry consortiums around the world to advance new technologies for energy efficiency and carbon capture. With our core strengths as a leading industrial gases and materials company and a culture of product innovation, Air Products is a leading developer of technologies for capturing CO2 from fossil fuel conversion before it reaches the atmosphere, a key to Carbon Capture and Sequestration (CCS) for GHG mitigation.

We carefully follow pending climate change regulatory developments around the world and engage with governmental and non-governmental stakeholders to support a balance between economic and environmental objectives.

CC0.2 Reporting Year

Please state the start and end date of the year for which you are reporting data.

The current reporting year is the latest/most recent 12-month period for which data is reported. Enter the dates of this year first.

We request data for more than one reporting period for some emission accounting questions. Please provide data for the three years prior to the current reporting year if you have not provided this information before, or if this is the first time you have answered a CDP information request. (This does not apply if you have been offered and selected the option of answering the shorter questionnaire). If you are going to provide additional years of data, please give the dates of those reporting periods here. Work backwards from the most recent reporting year.

Please enter dates in following format: day(DD)/month(MM)/year(YYYY) (i.e. 31/01/2001).

Enter Periods that will be disclosed Tue 01 Jan 2013 - Tue 31 Dec 2013

3

CC0.3 Country List of Configuration

Please select the countries for which you will be supplying data. This selection will be carried forward to assist you in completing your response.

Argentina Netherlands

Belgium Norway

Brazil Peru

Canada Philippines Chile Poland

China Portugal

Colombia Qatar

Czech Republic Russia

Ecuador Singapore

Egypt Slovakia

France South Africa

Germany South Korea

Guatemala Spain

India Switzerland

Indonesia Taiwan

Ireland Thailand

Israel United Arab Emirates

Italy United Kingdom

Japan United States of America

Malaysia Zambia

CC0. 4 Currency selection

Please select the currency in which you would like to submit your response. All financial information contained in the response should be in this currency.

USD($)

CC0. 6 Modules

As part of the request for information on behalf of investors, electric utilities, companies with electric utility activities or assets, companies in the automobile or auto component manufacture sectors, companies in the oil and gas industry, companies in the information technology and telecommunications sectors and companies in the food, beverage and tobacco sectors should complete supplementary questions in addition to the main questionnaire.

If you are in these sectors (according to the Global Industry Classification Standard (GICS)), the corresponding sector modules will not appear below but will automatically appear in the navigation bar when you save this page. If you want to query your classification, please email [email protected].

If you have not been presented with a sector module that you consider would be appropriate for your company to answer, please select the module below. If you wish to view the questions first, please see https://www.cdp.net/en-US/Programmes/Pages/More-questionnaires.aspx.

Further Information

Attachments https://www.cdp.net/sites/2014/35/435/Investor CDP 2014/Shared Documents/Attachments/InvestorCDP2014/CC0.Introduction/2013 Annual Report.pdf https://www.cdp.net/sites/2014/35/435/Investor CDP 2014/Shared Documents/Attachments/InvestorCDP2014/CC0.Introduction/2013 Sustainability Report.pdf

4

Module: Management

CC1 Governance

CC1.1 Where is the highest level of direct responsibility for climate change within your organization?

Individual/Sub-set of the Board or other committee appointed by the Board

CC1.1a Please identify the position of the individual or name of the committee with this responsibility

At the highest level, the Board of Directors’ Environmental, Safety and Public Policy Committee, has formal oversight for environmental performance, including climate change programs, risks and opportunities.

Mr. Guillermo Novo is Sustainability Council Executive Champion and Senior Vice President and General Manager Electronics, Performance Materials, Strategy and Technology. Mr. Novo reports directly to the Chairman, President and CEO, and has direct responsibility for climate change programs within Air Products. He is a member of Air Products’ Corporate Executive Committee (CEC), which includes the seven most senior executives of the company. CEC members conduct regular reviews of climate change risks and opportunities.

Mr. Novo leads Air Products’ Sustainability Council, which is comprised of senior executives and functional experts who define policies, programs and performance indicators for sustainability initiatives, including climate change. The Sustainability Council was chartered by and reports to the Chairman, President and CEO. Mr. Joseph Pietrantonio, Vice President, Environment, Health, Safety & Quality and Corporate Chief Engineer, has direct operating responsibility for climate change policy and GHG inventory programs. He reports to CEC member Patricia Mattimore, Senior Vice President, Supply Chain.

In addition, Air Products’ Greenhouse Gases Strategy Team (comprised of cross-functional representation from each division and functional group) serves as the focal point for the corporation on climate change and GHG matters. The GHG Strategy Team supports Air Products’ Sustainability Council.

CC1.2 Do you provide incentives for the management of climate change issues, including the attainment of targets?

Yes

CC1.2a Please complete the table

Please provide further details on the incentives provided for the management of climate change issues.

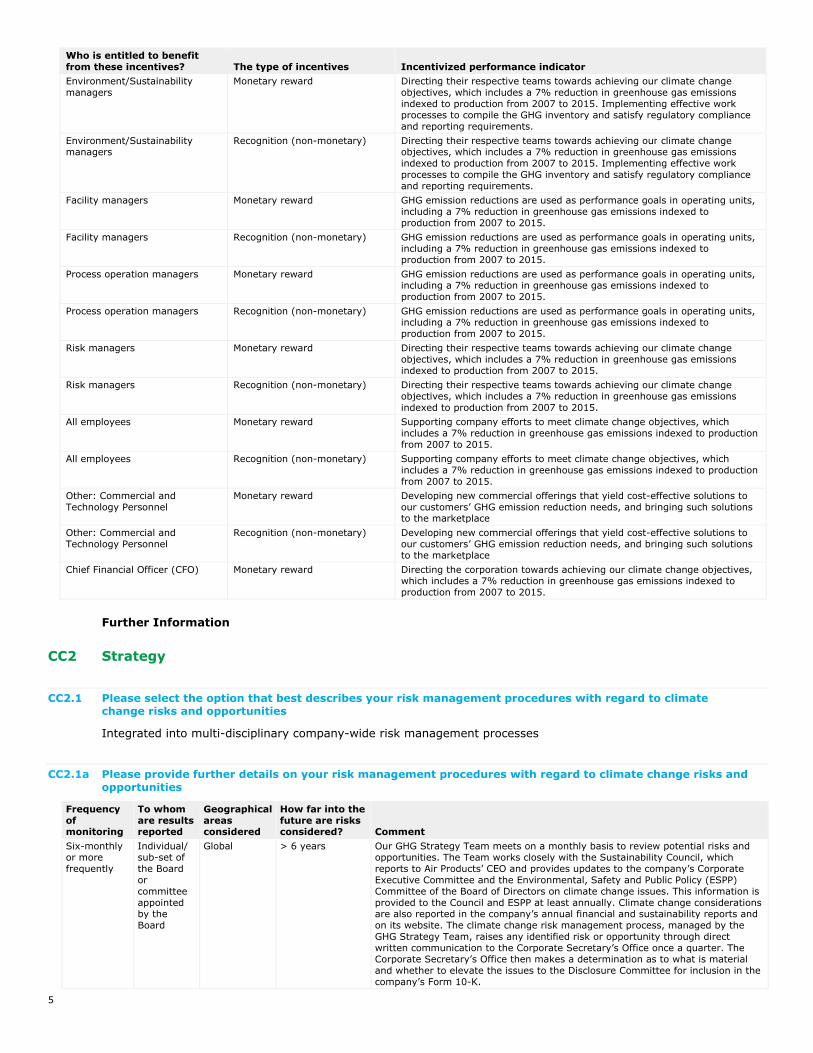

Who is entitled to benefit from these incentives? The type of incentives Incentivized performance indicator Corporate executive team Monetary reward Directing the corporation towards achieving our climate change objectives,

which includes a 7% reduction in greenhouse gas emissions indexed to production from 2007 to 2015.

Chief Executive Officer (CEO) Monetary reward Directing the corporation towards achieving our climate change objectives, which includes a 7% reduction in greenhouse gas emissions indexed to production from 2007 to 2015.

Executive officer Monetary reward Directing the corporation towards achieving our climate change objectives, which includes a 7% reduction in greenhouse gas emissions indexed to production from 2007 to 2015.

Management group Monetary reward Directing the corporation towards achieving our climate change objectives, which includes a 7% reduction in greenhouse gas emissions indexed to production from 2007 to 2015.

Management group Recognition (non-monetary) Directing the corporation towards achieving our climate change objectives, which includes a 7% reduction in greenhouse gas emissions indexed to production from 2007 to 2015.

Business unit managers Monetary reward Directing the corporation towards achieving our climate change objectives, which includes a 7% reduction in greenhouse gas emissions indexed to production from 2007 to 2015.

Business unit managers Recognition (non-monetary) Directing the corporation towards achieving our climate change objectives, which includes a 7% reduction in greenhouse gas emissions indexed to production from 2007 to 2015.

Energy managers Monetary reward Directing the corporation towards achieving our climate change objectives, which includes a 7% reduction in greenhouse gas emissions indexed to production from 2007 to 2015.

Energy managers Recognition (non-monetary) Directing the corporation towards achieving our climate change objectives, which includes a 7% reduction in greenhouse gas emissions indexed to production from 2007 to 2015.

5

Who is entitled to benefit from these incentives? The type of incentives Incentivized performance indicator Environment/Sustainability managers

Monetary reward Directing their respective teams towards achieving our climate change objectives, which includes a 7% reduction in greenhouse gas emissions indexed to production from 2007 to 2015. Implementing effective work processes to compile the GHG inventory and satisfy regulatory compliance and reporting requirements.

Environment/Sustainability managers

Recognition (non-monetary) Directing their respective teams towards achieving our climate change objectives, which includes a 7% reduction in greenhouse gas emissions indexed to production from 2007 to 2015. Implementing effective work processes to compile the GHG inventory and satisfy regulatory compliance and reporting requirements.

Facility managers Monetary reward GHG emission reductions are used as performance goals in operating units, including a 7% reduction in greenhouse gas emissions indexed to production from 2007 to 2015.

Facility managers Recognition (non-monetary) GHG emission reductions are used as performance goals in operating units, including a 7% reduction in greenhouse gas emissions indexed to production from 2007 to 2015.

Process operation managers Monetary reward GHG emission reductions are used as performance goals in operating units, including a 7% reduction in greenhouse gas emissions indexed to production from 2007 to 2015.

Process operation managers Recognition (non-monetary) GHG emission reductions are used as performance goals in operating units, including a 7% reduction in greenhouse gas emissions indexed to production from 2007 to 2015.

Risk managers Monetary reward Directing their respective teams towards achieving our climate change objectives, which includes a 7% reduction in greenhouse gas emissions indexed to production from 2007 to 2015.

Risk managers Recognition (non-monetary) Directing their respective teams towards achieving our climate change objectives, which includes a 7% reduction in greenhouse gas emissions indexed to production from 2007 to 2015.

All employees Monetary reward Supporting company efforts to meet climate change objectives, which includes a 7% reduction in greenhouse gas emissions indexed to production from 2007 to 2015.

All employees Recognition (non-monetary) Supporting company efforts to meet climate change objectives, which includes a 7% reduction in greenhouse gas emissions indexed to production from 2007 to 2015.

Other: Commercial and Technology Personnel

Monetary reward Developing new commercial offerings that yield cost-effective solutions to our customers’ GHG emission reduction needs, and bringing such solutions to the marketplace

Other: Commercial and Technology Personnel

Recognition (non-monetary) Developing new commercial offerings that yield cost-effective solutions to our customers’ GHG emission reduction needs, and bringing such solutions to the marketplace

Chief Financial Officer (CFO) Monetary reward Directing the corporation towards achieving our climate change objectives, which includes a 7% reduction in greenhouse gas emissions indexed to production from 2007 to 2015.

Further Information

CC2 Strategy

CC2.1 Please select the option that best describes your risk management procedures with regard to climate change risks and opportunities

Integrated into multi-disciplinary company-wide risk management processes

CC2.1a Please provide further details on your risk management procedures with regard to climate change risks and opportunities

Frequency of monitoring

To whom are results reported

Geographical areas considered

How far into the future are risks considered? Comment

Six-monthly or more frequently

Individual/ sub-set of the Board or committee appointed by the Board

Global > 6 years Our GHG Strategy Team meets on a monthly basis to review potential risks and opportunities. The Team works closely with the Sustainability Council, which reports to Air Products’ CEO and provides updates to the company’s Corporate Executive Committee and the Environmental, Safety and Public Policy (ESPP) Committee of the Board of Directors on climate change issues. This information is provided to the Council and ESPP at least annually. Climate change considerations are also reported in the company’s annual financial and sustainability reports and on its website. The climate change risk management process, managed by the GHG Strategy Team, raises any identified risk or opportunity through direct written communication to the Corporate Secretary’s Office once a quarter. The Corporate Secretary’s Office then makes a determination as to what is material and whether to elevate the issues to the Disclosure Committee for inclusion in the company’s Form 10-K.

6

CC2.1b Please describe how your risk and opportunity identification processes are applied at both company and asset level

Air Products has a process for identifying risks and opportunities associated with climate change. The GHG Strategy Team manages the process, providing preliminary assessments of the potential financial and operating impacts climate change considerations may have on our businesses and operations. This team, with cross-functional and global representation, works directly with potentially impacted businesses to support analysis of the risks and opportunities, including scenario planning, and serves as a resource for our global businesses to shape strategies and opportunities for growth.

Company level assessments Managed at the enterprise level by its GHG Strategy Team, Air Products has a formalized climate change risk management process that is integrated into its long standing, multi-disciplinary, company-wide risk management process. The GHG Strategy Team has cross-functional representation from each division and functional group, and each of its members are responsible for monitoring GHG developments related to his or her functional area of expertise or business unit and identifying potential climate change related risks and opportunities. During monthly meetings, the GHG Team discusses and analyzes any new or changing risk or opportunity for impacts on specific divisions and on the company as a whole.

Asset level assessments Capital expenditures, engineering and Continuous Improvement (CI) projects may be managed at the asset level, depending on scope. Project teams complete these assessments using documented procedures and criteria.

Air Products has a formal Business Continuity Planning process through which each business area evaluates its operational assets and develops Business Continuity Plans in the event of an impairment of the asset. These plans are used in concert with our Crisis Management Process.

The Corporate Risk Department maintains an evaluation of physical risk from extreme weather in order to ensure our capital assets are suitably protected.

CC2.1c How do you prioritize the risks and opportunities identified?

Air Products’ GHG Strategy Team identifies climate change risks and opportunities and serves as our global company-wide center of excellence for matters on internal policy development, regulations, legislation, and regularly updates management and the Board. The Team prioritizes climate change risks and opportunities based on potential financial and operating impacts on the company. Examples of risks and opportunities examined include those driven by changes in regulation, such as cap and trade schemes; those driven by changes in physical parameters, including droughts; and those from other developments, such as mixed market signals.

From a corporate perspective, on an annual basis, risk elements proposed for review are discussed by risk experts in the Corporate Risk Office, and risk owners from the businesses and functional areas. The Corporate Compliance & Risk Committee reviews and approves elements to be included. Each risk element is mapped for materiality vs. probability and velocity, and shown to the accountable Board oversight committee. In addition, detailed country risk assessments that consider GHG/Climate Change (among other) risks are conducted for new geographies for expansion. Once risks are identified, the business unit or function must create plans to mitigate the risks. The risk of business interruption due to natural disaster, supply chain disruption, pandemic, etc. is assessed and planned for in the Business Continuity Plan (BCP). Each business must complete a Business Impact Analysis (BIA) and a Business Recovery Plan (BRP) on a regular basis.

CC2.1d Please explain why you do not have a process in place for assessing and managing risks and opportunities from climate change, and whether you plan to introduce such a process in future

Main reason for not having a process Do you plan to introduce a process? Comment

CC2.2 Is climate change integrated into your business strategy?

Yes

CC2.2a Please describe the process of how climate change is integrated into your business strategy and any outcomes of this process

i. Influence on business strategy As a solutions provider, Air Products’ strategy for responding to climate change is straight forward – identify

opportunities where our core technology and product strengths bring cost-effective solutions that enable our

7

customers to reduce their overall supply-chain environmental impact, while using innovation and efficiency improvements to reduce GHG emissions and the potential cost impacts of a carbon-constrained energy supply on our operations. These opportunities can drive top-line growth, particularly as the company applies its growth strategy of serving energy, environmental and emerging markets. Examples include:

• Oxygen for oxyfuel combustion that reduces fuel consumption and GHG emissions; for de-bottlenecking catalytic cracking units and sulfur recovery units; for facilitating CO2 capture and sequestration; for use in Integrated Gasification Combined Cycle power facilities; for use in waste gasification; and in biomass combustion/gasification for renewable power and biofuels.

• Hydrogen for use as an emission-free transportation fuel; in the production of biodiesel from renewable feedstocks; and to enable refiners to meet fuels emissions standards while increasing the amount of fuel that can be produced from oil.

• Nitrogen for unconventional natural gas production and increased demand for energy-integrated Liquefied Natural Gas.

• The design, construction and start-up of a state-of-the-art system to capture CO2 from Air Products’ SMRs in the Valero Port Arthur Texas refinery

• High purity process gases and cleaning agents and services that support the drive for renewable energy sources.

• Gases for high efficiency lighting and insulation of windows to reduce energy losses from buildings. • Catalysts and surfactants for polyurethane foam that provides superior insulation. • Curing agents for epoxy resins used in high strength-to-weight composites that enable weight reduction in

transportation vehicles and wind turbines. ii. Climate change aspects influencing the strategy Climate change represents a significant potential for business growth, and managing the potential opportunities and

risks from climate change has influenced the company’s strategy. Managed at the enterprise level by its GHG Strategy Team, Air Products has a formalized climate change risk management process that is integrated into its long standing, multi-disciplinary, company-wide risk management process. Risk management has prompted the quantification and review of the company’s GHG emissions and energy use. Since the company must continually improve its energy efficiency as a supplier, it has set global, company-wide goals for energy efficiency and GHG reduction. The specific goal for energy is to reduce consumption by 7% indexed against production by 2015 for ASUs and HYCO from a 2007 baseline. Likewise the goal for greenhouse gases is to reduce emissions by 7% indexed against production by 2015 from a 2007 baseline. Progress against these goals is enabled through several work processes, including annual budgeting and strategy reviews, annual reporting, and ongoing consideration of environmental issues for new products, processes, mergers and acquisitions, and sourcing.

iii. Short term strategy components Developed and managed by its GHG Strategy Team, Air Products employs a long term strategy for climate change.

Shorter term activities (e.g., 1-5 years) that have been influenced by climate change include efforts to integrate GHG considerations through several work processes, including annual budgeting and strategy reviews, annual reporting, and ongoing consideration of environmental issues for products, processes, mergers and acquisitions, and sourcing.

iv. Long term strategy components From a long term (e.g., 6-10 years) perspective, the company is investing significantly in research and

development of offerings that enable its customers to reduce their environmental footprint and energy consumption. More than 50 percent of the company's R&D spending (~$133.7 million in fiscal 2013) is related to environmental and energy efficiency offerings.

v. How gaining strategic advantage Air Products’ competitive advantage lies in its understanding of environmental and energy issues combined with its

applications expertise to address customer needs. The company is a leader in climate innovation, as exemplified by: • Efficiency-optimized steam methane reforming technology for hydrogen production • Novel CO2 capture technology, including the design, construction and start-up of a state-of-the-art system to

capture CO2 from Air Products’ steam methane reformers (SMRs) in the Valero Port Arthur Texas refinery • Ceramic ion transport membrane technology in development for more energy-efficient oxygen production • World-leading natural gas liquefaction equipment, including recently announced supply of proprietary liquefied

natural gas (LNG) process technology and equipment to Technip for a mid-scale LNG project in the Yangling Demonstration Area, ShaanXi Province, China to help meet the growing demand for clean energy.

• High-purity process gases and cleaning agents for the latest generation photovoltaic solar cell production • Hydrogen fueling capabilities, including more than 160 fueling stations in 20 countries for commercial and

governmental use, as well as fuel cells for material handling such as forklifts vi. Substantial business decisions In 2013, Air Products executed several projects focused on clean energy technologies that demonstrate the

company’s innovative technologies for greenhouse gases, including:

8

• The design, construction and start-up of a state-of-the-art system to capture CO2 from Air Products’ SMRs in the Valero Port Arthur Texas refinery; designed to capture one million tons of CO2 annually to be recovered and purified by Air Products, and transported via pipeline for injection into an enhanced oil recovery project in Texas

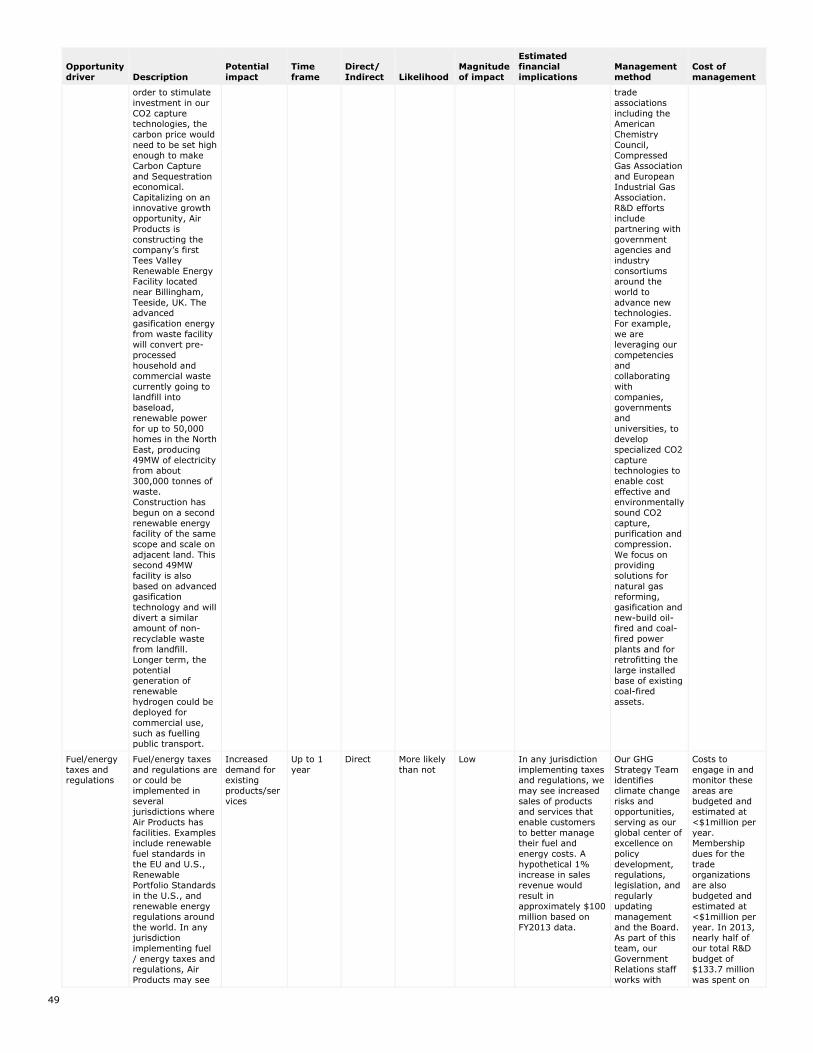

• Ongoing construction of the company’s Tees Valley Renewable Energy Facility located near Billingham, Teesside, UK. The advanced gasification energy from waste scheme will convert pre-processed household and commercial waste currently going to landfill into baseload, renewable power for up to 50,000 homes in the North East, producing 49MW of electricity from about 300,000 tonnes of waste. Construction has begun on a second renewable energy facility of the same scope and scale on adjacent land. This second 49MW facility is also based on advanced gasification technology and will divert a similar amount of non-recyclable waste from landfill.

CC2.2b Please explain why climate change is not integrated into your business strategy

CC2.3 Do you engage in activities that could either directly or indirectly influence public policy on climate change through any of the following? (tick all that apply)

Direct engagement with policy makers Trade associations Funding research organizations Other

CC2.3a On what issues have you been engaging directly with policy makers?

Focus of legislation

Corporate Position Details of engagement Proposed legislative solution

Clean energy generation

Support As part of the normal legislative process, Air Products directly engages policy makers through consultation and direct meetings to ensure that developing energy and related policies take appropriate account of the specific characteristics of the renewable energy technology that forms the basis of our investment intentions. As an example of those efforts, Air Products has engaged with the UK government on matters concerning the Renewables Obligation Scheme, and the rollout of the Energy Market Reform policy and attendant regulations.

Air Products supports the development and use of renewable, clean energy, and has helped educate policy makers on the benefits. The company is a member of the UK Renewable Energy Association which takes a strong, public position in support of renewable energy.

Mandatory carbon reporting

Support with minor exceptions

Air Products engages with various agencies on mandatory carbon reporting, particularly the US EPA Greenhouse Gas Reporting Rules (Greenhouse Gas Reporting Rule 40CFR Part 98) and California's Regulation for the Mandatory Reporting of Greenhouse Gas Emissions. The company periodically meets directly with regulatory staff, participates in public regulatory workshops and provides key input to comments submitted by various trade associations to which the Company belongs.

Air Products seeks to ensure reporting methodologies define reasonable measurement requirements, accuracy expectations and alternatives to address missing data points.

Cap and trade Support with minor exceptions

Working through the California Large Energy Consumers Association, we have provided data to the California Public Utility Commission supporting designation of atmospheric gases production as an Energy Intensive/Trade Exposed industry sector worthy of rebates against the electricity cost increase attributed to the California greenhouse gas cap and trade program. Through the vehicles of the European Industrial Gas Association (EIGA) and selected European national industrial gases associations, Air Products has responded to consultations and met directly with EU policy-makers to ensure that the role of our industry in achieving the aims of EU environmental policies can more easily and more cost-effectively be achieved. Examples include policies relating to emissions trading and fluorinated refrigerants.

Air Products seeks comparable treatment under the regulations (e.g., consistent basis for allocation of free allowances) to all producers, regardless of ownership structure, so as to not unduly disadvantage the over-the-fence supply model.

CC2.3b Are you on the Board of any trade associations or provide funding beyond membership?

Yes

9

CC2.3c Please enter the details of those trade associations that are likely to take a position on climate change legislation

Trade association

Is your position on climate change consistent with theirs? Please explain the trade association's position

How have you, or are you attempting to, influence the position?

American Chemistry Council (ACC)

Mixed The ACC does not have a formal position on climate change. ACC has noted that chemistry plays a central role in climate mitigation both in terms of cost efficient reductions in energy consumption as well as providing technologies to decarbonise energy production, thus further reducing GHG emissions. The Association has also engaged with the U.S. Congress to shape climate change policy while promoting the efficient use of resources to promote economic recovery and deliver the most cost-effective reduction in emissions. ACC has challenged certain aspects of legislation and regulations related to climate change in an effort to prevent market distortions that could impact its member companies.

Our business benefits from participation in trade associations that bring together organizations for best practice sharing and working on common issues The members of ACC, like most large trade associations, have a wide range of views, and we do not always agree with all the positions ACC chooses to support. In all cases, any Air Products public position on a matter of public policy is the prevailing company position, irrespective of any trade association position to the contrary.

European Industrial Gas Association (EIGA)

Consistent EIGA does not have a formal position on climatechange. The Association engages on behalf of its members with Member States on a variety of issues related to climate change.

Air Products supports EIGA's efforts to appropriately engage with Member States on climate change issues and to ensure that the industrial gases sector is placed on an equal footing with other industrial sectors with regard to treatment of direct and indirect emissions.

National Association of Manufacturers (NAM)

Mixed "NAM member companies are committed to advancing sustainability efforts that positively impact manufacturing and industry’s contributions to environmental protection, economic performance and the social well-being of the employees, communities, customers and consumers they serve. NAM members recognize these challenges and will respond by encouraging the adoption of sustainable best practices and application of life cycle analysis practices in the manufacturing sector. NAM members will work proactively with relevant stakeholders to ensure that the voice of manufacturing is heard and is contributing its positive story" (Taken from NAM Website)

Our management believes that our business, and thus our shareholders, benefit from our participation in an organization that represents U.S. manufacturing in Washington. The members of NAM, like most large trade associations, have a wide range of views, and we do not always agree with all the positions NAM chooses to support. In all cases, any Air Products public position on a matter of public policy is the prevailing company position, irrespective of any trade association position to the contrary.

CC2.3d Do you publically disclose a list of all the research organizations that you fund?

No

CC2.3e Do you fund any research organizations to produce or disseminate public work on climate change?

Yes

CC2.3f Please describe the work and how it aligns with your own strategy on climate change

Description of the work In 1998, Air Products was a founding member of the Business Environmental Leadership Council (BELC) of the Center for Climate and Energy Solutions (C2ES), formerly the Pew Center on Global Climate Change. C2ES believes “that ensuring safe, reliable, affordable energy for all – while protecting the global climate – is a paramount challenge of the 21st century.” The organization is focused on providing reliable, timely and impartial information and analysis on the various dimensions of climate and energy by bringing together businesses and other stakeholders to develop consensus solutions and pragmatic policies. C2ES’s BELC believes business engagement is critical for developing efficient, effective solutions to the climate problem.

Alignment with company strategy on climate change Air Products’ strategy on climate change is aligned with BELC’s guiding principles:

We accept the scientific consensus that climate change is occurring and that the impacts are already being felt. Delaying action will increase both the risks and the costs.

Businesses can and should incorporate responses to climate change into their core corporate strategies by taking concrete steps in the U.S. and abroad to establish and meet greenhouse gas (GHG) emission reduction targets, and/or invest in low and zero GHG products, practices and technologies.

The United States should significantly reduce its GHG emissions through economy-wide, mandatory approaches, which may vary by economic sector and include a flexible, market-based program. Complementary policies may

10

also be necessary for sectors such as buildings, electricity generation, forestry, agriculture, and transportation that will help drive innovation and ease the transition to a low-carbon economy.

Climate change is a global challenge that ultimately requires a global solution. An international climate framework must establish fair, effective, and binding commitments for all developed and major developing economies.

CC2.3g Please provide details of the other engagement activities that you undertake

Air Products is engaged with several other organizations related to climate change including:

Climate Leadership Program

Method of engagement – Engaging as individual company

Topic of engagement – Support for GHG emissions reduction goal

Nature of engagement - In 2011, Air Products successfully transferred its comprehensive, carbon-intensity metric and 7% GHG emissions reduction goal (by 2015) that covers 100% of our Scope 1 and Scope 2 emissions from the U.S. EPA Climate Leaders program to the successor Climate Leadership Program, jointly sponsored by the U.S. EPA, the Climate Registry, the Center for Climate and Energy Solutions, and the Association of Climate Change Officers.

Actions advocated – Transfer of GHG emissions reduction goal (as noted above).

Global Environmental Leadership (IGEL)

Method of engagement – Engaging through a group

Topic of engagement – Knowledge around sustainability issues, including climate change

Nature of engagement - Based at Wharton at the University of Pennsylvania, IGEL promotes knowledge for business sustainability through world-class research, transformative teaching and constructive dialogue between top alumni, academic, corporate, government, and non-government organizations. The organization provides opportunities for business leaders with high-level environmental responsibilities, including climate change, to consult together and with academic leaders from Wharton and Penn and selected experts.

Actions advocated – Sharing of best practices for addressing sustainability issues, including climate change, and promoting use of these practices

Conference Board Sustainability Council II

Method of engagement – Engaging through a group

Topic of engagement - Knowledge around sustainability issues, including climate change

Nature of engagement - Members share information on product development processes that enable customers and downstream users to reduce their impact on the environment, including GHG reduction.

Actions advocated – Increasing consideration of sustainability issues, including energy savings and GHG emissions reduction, in new product development

CC2.3h What processes do you have in place to ensure that all of your direct and indirect activities that influence policy are consistent with your overall climate change strategy?

Air Products’ GHG Strategy Team identifies climate change risks and opportunities and serves as our global company-wide center of excellence for matters on internal policy development, regulations, legislation, and regularly updates management and the Board. Direct engagement is lead by professionals in our Corporate Government Relations Team who are also members of the GHG Strategy Team. Likewise the Team provides a forum for broad review of indirect activities the company is undertaking in the climate change arena.

CC2.3i Please explain why you do not engage with policy makers

Further Information

11

CC3 Targets and Initiatives

CC3.1 Did you have an emissions reduction target that was active (ongoing or reached completion) in the reporting year? Intensity target

CC3.1a Please provide details of your absolute target

ID Scope % of emissions in scope

% reduction from base year

Base year

Base year emissions (metric tonnes CO2e)

Target year Comment

CC3.1b Please provide details of your intensity target

ID Scope

% of emissions in scope

% reduction from base year Metric

Base year

Normalized base year emissions

Target year Comment

Int1 Scope 1+2

100% 7% Other: Indexed value from Base Year (e.g. Base Year Index = 1.0), where Index values is based on production metrics in the general form of “metric tonnes CO2-e per unit of production."

2007 1 2015 Our intensity goal is configured as the ratio of reporting year (2013) emissions to reporting year production compared to the same emission to production ratio in our Base Yea (2007). Using a ratio allows the intensity value to be dimensionless and protects confidential process efficiency data. For 2013, our GHG intensity figure relative to the base year is 0.877, representing a 12.3% reduction from the Base Year. This metric is the basis for our voluntary GHG Reduction goal, approved by US EPA Climate Leaders Program in 2010.

CC3.1c Please also indicate what change in absolute emissions this intensity target reflects

ID

Direction of change anticipated in absolute Scope 1+2 emissions at target completion?

% change anticipated in absolute Scope 1+2 emissions

Direction of change anticipated in absolute Scope 3 emissions at target completion?

% change anticipated in absolute Scope 3 emissions Comment

Int1 Increase 39

Absolute emissions will increase as production increases, but the rate of the increase will be reduced through efficiency improvement, emission reduction and CO2 capture programs.

CC3.1d For all of your targets, please provide details on the progress made in the reporting year

ID % complete (time)

% complete (emissions) Comment

Int1 75% 100% Scope 1 emission reductions from our HYCO and Electronic Specialty Materials business contributed to a reduction in the composite production Scope 1 intensity metric (and a minimal increase on an absolute basis). ESM reductions resulted from process loss reductions which also increase product yield. Implementation of a large CO2 capture project from two hydrogen plants helped offset emissions increases from new facilities. . Scope 2 emissions increased at pace with production increases. The net result is a combined Scope 1 and Scope 2 Intensity Index reduction of 12.3% that exceeds our 2015 goal of a 7% reduction. Air Products recognizes there are production increases in future years that will continue to challenge our 2015 goal attainment, so will continue to track performance with our combined Scope 1 and Scope 2 Intensity Metric.

CC3.1e Please explain (i) why you do not have a target; and (ii) forecast how your emissions will change over the next five years

12

CC3.2 Does the use of your goods and/or services directly enable GHG emissions to be avoided by a third party?

Yes

CC3.2a Please provide details of how the use of your goods and/or services directly enable GHG emissions to be avoided by a third party

Oxygen (O2) for Combustion: O2 is required for any combustion process. Replacing air with O2 or adding pure O2 (O2 enrichment) improves the overall combustion process. Likewise the use of O2 enables enhanced alternative fuel substitution, reducing the need for fossil fuels.

Fuel efficiency gains of 5-65% are achieved depending on process requirements and capabilities. These gains result in the reduction of direct emissions of CO and CO2 through reduced fossil fuel consumption.

Our oxy-fuel applications technology saves customers 1.6 million MT CO2e every year excluding O2 production, or 1 million MT/yr including O2 production. Over the past few years Air Products has installed O2 systems on several cement kilns to enable increased alternative fuel substitution that has decreased fuel rates (coal and petcoke) by 10% to ~60% on these kilns (avg. reduction of 29%). This represents 99,900 tons/yr of CO2e saved via alternative fuels substitution during operation.

Analyses compare energy consumption using O2 vs. air. The emission factors used were 2.418 kg CO2/kg coal and 3.18 kg CO2/kg coke. The emission factors for the non-renewable alternate fuel in relation to coal were estimated using an equation that considered the LHV of coal (26.3 MJ/kg) and the composition of the alternative fuel (water, ash and carbon content). For the alternative fuels example, analyses are based on field testing. The amount of CO2e saved at these facilities has been calculated as the sum of the change in fossil fuel rate multiplied by the CO2 credit for the alternative fuel (0.9 for Refuse Derived Fuel, and 2.5 for biomass) for each facility. Air Products completed an LCA for oxygen use in cement kilns with alternative fuels that confirmed the CO2e savings from substitution of coal.

No plans to generate CERs/ERUs

Hydrogen (H2) as alternative transportation fuel: Air Products’ H2 fuel stations support the use of fuel cell zero emission vehicles. Our hydrogen stations supporting light-duty fuel cell electric vehicles (FCEV’S) in California (CA) has avoided 271 MT CO2e. Replacing gasoline and diesel internal combustion engine vehicles with H2 powered fuel-cell vehicles allows for reduction in GHG emissions and opens up non-traditional and renewable energy resources for the transportation sector.

Overall fossil fuel consumption and GHG emissions are reduced over the life cycle of fuel by shifting light-duty vehicle fuel combustion from internal combustion engines to more efficient fuel cell light-duty vehicles, using less carbon intensive natural gas as a fuel source and enabling the supply and procurement of renewable biogas that supplies two hydrogen fuel stations.

Through supply of less GHG intensive H2 fuel for fuel cell vehicles, consumers reduced their driving well-to-wheels greenhouse emissions by 65% relative to the CA Low Carbon Fuel Cell (LCFS) 2012 baseline for gasoline vehicle, resulting in 244 g CO2e saved for each mile driven. During 2013, our H2 fuelling stations serving light-duty vehicles substituted 42,561 gallons of gasoline, thus avoiding 271 MT CO2e. Air Products has been awarded projects to construct an additional 10 stations by the end of 2014 as part of a CA Energy Commission Roadmap supported by the Governor’s Executive Order establishing specific milestones on a path toward reaching 1.5 million zero-emission vehicles in California by 2025. This roadmap contains plans to build upwards of 100 hydrogen fueling stations, commensurate with the OEM forecast vehicle deployment of FCEV’s, resulting in significant reductions in GHGs in the CA market.

An LCA was completed to estimate the CO2e avoided. The analysis estimated the lifecycle emission of H2 energy supply considering 33.3% of H2 from eligible renewable on a full well-to-wheels basis; applied an Energy Efficiency Ratio of 2.3 for FCEV’s established under CA LCFS; and estimated emissions performance of traditional gasoline cars based on LCFS 2013 gasoline baseline (422 g CO2e/mile). Emission factors varied from 12.3 to 27 g CO2/g H2 depending on the hydrogen source.

No plans to generate CERs/ERUs

CC3.3 Did you have emissions reduction initiatives that were active within the reporting year (this can include those in the planning and implementation phases)

Yes

13

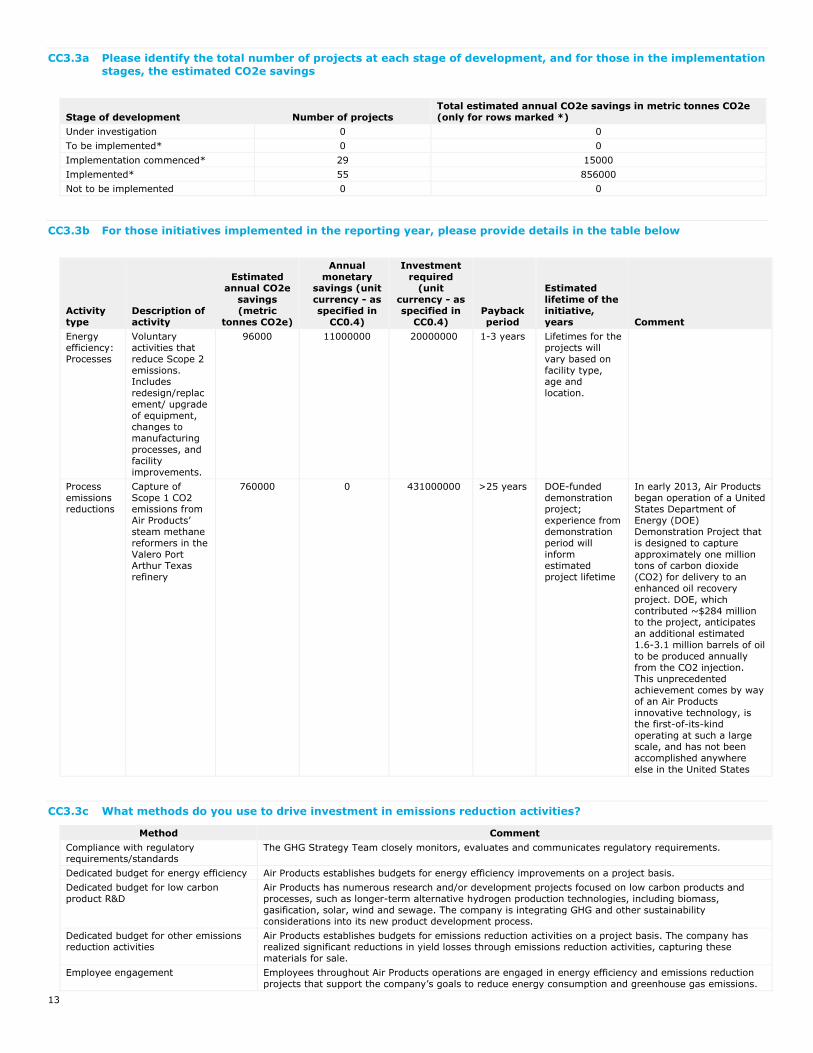

CC3.3a Please identify the total number of projects at each stage of development, and for those in the implementation stages, the estimated CO2e savings

Stage of development Number of projects Total estimated annual CO2e savings in metric tonnes CO2e (only for rows marked *)

Under investigation 0 0 To be implemented* 0 0 Implementation commenced* 29 15000 Implemented* 55 856000 Not to be implemented 0 0

CC3.3b For those initiatives implemented in the reporting year, please provide details in the table below

Activity type

Description of activity

Estimated annual CO2e

savings (metric

tonnes CO2e)

Annual monetary

savings (unit currency - as specified in

CC0.4)

Investment required

(unit currency - as specified in

CC0.4) Payback period

Estimated lifetime of the initiative, years

Comment

Energy efficiency: Processes

Voluntary activities that reduce Scope 2 emissions. Includes redesign/replacement/ upgrade of equipment, changes to manufacturing processes, and facility improvements.

96000 11000000 20000000 1-3 years Lifetimes for the projects will vary based on facility type, age and location.

Process emissions reductions

Capture of Scope 1 CO2 emissions from Air Products’ steam methane reformers in the Valero Port Arthur Texas refinery

760000 0 431000000 >25 years DOE-funded demonstration project; experience from demonstration period will inform estimated project lifetime

In early 2013, Air Products began operation of a United States Department of Energy (DOE) Demonstration Project that is designed to capture approximately one million tons of carbon dioxide (CO2) for delivery to an enhanced oil recovery project. DOE, which contributed ~$284 million to the project, anticipates an additional estimated 1.6-3.1 million barrels of oil to be produced annually from the CO2 injection. This unprecedented achievement comes by way of an Air Products innovative technology, is the first-of-its-kind operating at such a large scale, and has not been accomplished anywhere else in the United States

CC3.3c What methods do you use to drive investment in emissions reduction activities?

Method CommentCompliance with regulatory requirements/standards

The GHG Strategy Team closely monitors, evaluates and communicates regulatory requirements.

Dedicated budget for energy efficiency Air Products establishes budgets for energy efficiency improvements on a project basis.Dedicated budget for low carbon product R&D

Air Products has numerous research and/or development projects focused on low carbon products and processes, such as longer-term alternative hydrogen production technologies, including biomass, gasification, solar, wind and sewage. The company is integrating GHG and other sustainability considerations into its new product development process.

Dedicated budget for other emissions reduction activities

Air Products establishes budgets for emissions reduction activities on a project basis. The company has realized significant reductions in yield losses through emissions reduction activities, capturing these materials for sale.

Employee engagement Employees throughout Air Products operations are engaged in energy efficiency and emissions reduction projects that support the company’s goals to reduce energy consumption and greenhouse gas emissions.

14

Method CommentInternal incentives/recognition programs

Employees are recognized for progress against achieving our climate change objectives, developing new commercial offerings that yield cost-effective solutions to our customers’ GHG emission reduction needs and bringing such solutions to the marketplace, and implementing effective work processes to compile the GHG inventory and satisfy regulatory compliance and reporting requirements. Efforts are recognized through existing compensation and awards programs.

Internal finance mechanisms Air Products has integrated GHG considerations into its global expenditure authorization process, which is used to prepare requests for capital expenditures, marketing and procurement and investment transactions.

Partnering with governments on technology development

Air Products seeks opportunities to collaborate with governments on technology developments. For example, the company is has employed novel CO2 capture technology for some of the largest carbon capture and storage demonstration projects in the world, including pre-combustion capture with the US Department of Energy (DOE) in Texas.

Employee engagement Productivity improvements - Air Products has a robust productivity improvement process. Employee recommendations to improve productivity frequently focus on conservation and emissions reduction projects. These ideas are tracked in a global, central database that includes quantified costs and benefits. Data from this system was used to respond to the above questions (3.3a and 3.3b).

CC3.3d If you do not have any emissions reduction initiatives, please explain why not

Further Information

For question 3.3a: The system the company uses for tracking projects does not distinguish between projects under investigation and to be implemented.

CC4 Communication

CC4.1 Have you published information about your organization’s response to climate change and GHG emissions performance for this reporting year in places other than in your CDP response? If so, please attach the publication(s)

Publication Page/Section reference Attach the document

In mainstream financial reports (complete)

10, 37 https://www.cdp.net/sites/2014/35/435/Investor CDP 2014/Shared Documents/Attachments/CC4.1/2013 Annual Report.pdf

In voluntary communications (complete)

Information provided throughout the report (pages 4, 8, 11, 12, 15, 20, 27, 30, 55, 57, 63, 64, 66, 70). See pages 30 and 70 for performance data.

https://www.cdp.net/sites/2014/35/435/Investor CDP 2014/Shared Documents/Attachments/CC4.1/2013 Sustainability Report.pdf

Module: Risks and Opportunities

CC5. Climate Change Risks

CC5.1 Have you identified any climate change risks that have the potential to generate a substantive change in your business operations, revenue or expenditure? Tick all that apply

Risks driven by changes in regulation Risks driven by changes in physical climate parameters Risks driven by changes in other climate-related developments

CC5.1a Please describe your risks driven by changes in regulation

Please describe your risks driven by changes in regulation

Risk driver Description Potential impact

Time frame

Direct/Indirect Likelihood

Magnitude of impact

Estimated financial implications Mgmt. method Cost of Mgmt.

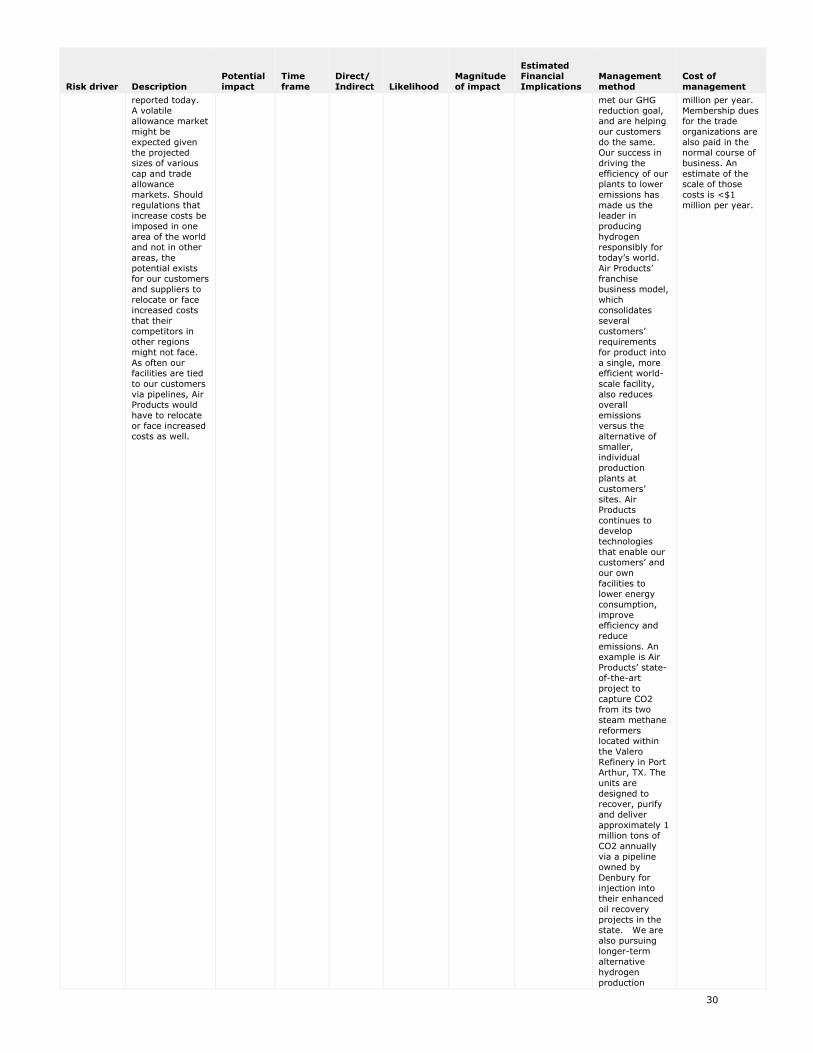

International agreements

The high degree of uncertainty in the timing and content of any binding international agreement

Increased operational cost

Unknown Direct Unknown Unknown The high degree of uncertainty in the timing and content of an international agreement prevents accurate prediction of the potential risk impact to Air

Our GHG Strategy Team identifies climate change risks and opportunities, serving as our global center of excellence on

The company has not incurred additional costs to actively engage in and monitor these areas as the

15

Risk driver Description Potential impact

Time frame

Direct/Indirect Likelihood

Magnitude of impact

Estimated financial implications Mgmt. method Cost of Mgmt.

prevents accurate prediction of the potential risk impact to Air Products. However any binding agreement that limits or taxes GHG emissions from Air Products’ facilities could impact our value chain and growth by increasing operating costs, both directly and through suppliers.

Products. Given our market capitalization of $23.6 billion as of 31 Dec 2013, a hypothetical impact (from increased operating costs or reduced demand for certain products) that would result in a decreased stock-price of 1% would yield a reduced market value of ~$200 million.

policy development, regulations, legislation, and regularly updating management and the Board. As part of this team, our Government Relations staff works with agencies and NGOs in regions of the world where we have significant business interests to develop strategy, understand business environments, and protect/position our businesses to respond to climate change risks and opportunities. These efforts are augmented through membership in executive leadership forums, including the Business Environmental Leadership Council of the Center for Climate and Energy Solutions that provides insights into the local and international stage. We are involved with trade associations including the American Chemistry Council, Compressed Gas Association and European Industrial Gas Association. We continue to develop technologies that enable our customers and our facilities to lower energy consumption, improve efficiency and reduce emissions. In 2013, nearly half of our total R&D budget of $133.7 million was spent on developing products that reduce GHGs and address other sustainability issues. Our business planning processes focus on energy reduction targets that translate into GHG impact. We have also integrated GHG considerations into other business

efforts of our GHG Strategy and other teams, as well as costs associated with reduction commitments and customer engagement for cost recovery through contracts, are budgeted in the normal course of business. An estimate of the scale of those costs is <$1million/yr. Membership dues for trade organizations are paid in the normal course of business. An estimate of these costs is <$1million.

16

Risk driver Description Potential impact

Time frame

Direct/Indirect Likelihood

Magnitude of impact

Estimated financial implications Mgmt. method Cost of Mgmt.

processes. The company believes it will be able to mitigate some of these potential costs through contractual terms.

International agreements

The high degree of uncertainty in the timing and content of any binding international agreement prevents accurate prediction of the potential risk impact to Air Products. However any binding agreement that limits or taxes GHG emissions from Air Products’ facilities could impact our value chain and growth by reducing demand for certain products.

Reduced demand for goods/services

Unknown Direct Unknown Unknown The high degree of uncertainty in the timing and content of an international agreement prevents accurate prediction of the potential risk impact to Air Products. Given our market capitalization of $23.6 billion as of 31 Dec 2013, a hypothetical impact (from increased operating costs or reduced demand for certain products) that would result in a decreased stock-price of 1% would yield a reduced market value of ~$200 million.

Our GHG Strategy Team identifies climate change risks and opportunities, serving as our global center of excellence on policy development, regulations, legislation, and regularly updating management and the Board. As part of this team, our Government Relations staff works with agencies and NGOs in regions of the world where we have significant business interests to develop strategy, understand business environments, and protect/position our businesses to respond to climate change risks and opportunities. These efforts are augmented through membership in executive leadership forums, including the Business Environmental Leadership Council of the Center for Climate and Energy Solutions that provides insights into the local and international stage. We are involved with trade associations including the American Chemistry Council, Compressed Gas Association and European Industrial Gas Association. We continue to develop technologies that enable our customers and our facilities to lower energy consumption, improve efficiency and reduce emissions. In 2013, nearly half of our total R&D budget of $133.7 million was spent on developing

The company has not incurred additional costs to actively engage in and monitor these areas as the efforts of our GHG Strategy and other teams, as well as costs associated with reduction commitments and customer engagement for cost recovery through contracts, are budgeted in the normal course of business. An estimate of the scale of those costs is <$1million/yr. Membership dues for trade organizations are paid in the normal course of business. An estimate of these costs is <$1million.

17

Risk driver Description Potential impact

Time frame

Direct/Indirect Likelihood

Magnitude of impact

Estimated financial implications Mgmt. method Cost of Mgmt.

products that reduce GHGs and address other sustainability issues. Our business planning processes focus on energy reduction targets that translate into GHG impact. We have also integrated GHG considerations into other business processes. The company believes it will be able to mitigate some of these potential costs through contractual terms.

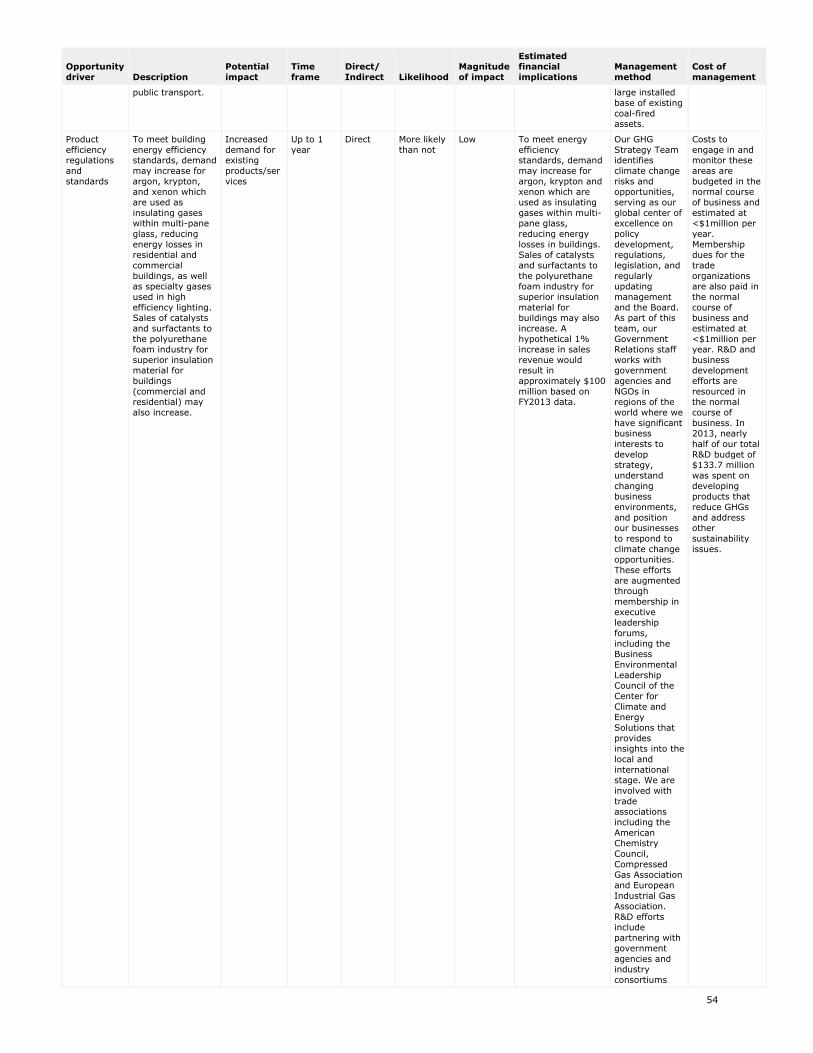

Air pollution limits

The US Federal EPA requires that new major sources and major modifications to existing sources consider Best Available Control Technology (BACT) in addressing the prevention of significant deterioration (PSD) and title V permitting requirements for GHGs. These requirements are expected to result in increased capital costs to enable monitoring and emission reductions at our hydrogen facilities, although these investments appear modest.

Increased capital cost

Up to 1 year

Direct Virtually certain

Low US EPA requires that new major sources and major modifications to existing sources consider Best Available Control Technology to address the prevention of significant deterioration and title V permitting requirements for GHGs. Air Products permits facilities that are subject to this rule, possibly resulting in increased capital costs, although these investments appear modest. Cost and time for large hydrogen plant environmental permit approval could increase ($200,000 per permit per site).

Our business planning processes focus on energy reduction targets that translate into GHG impact. We formally integrated GHG considerations into our global capital expenditure authorization process, marketing and procurement and investment transactions and continue to more fully integrate considerations into other processes, including product and process design, M&A, and sourcing. We offer our customers products from efficiently designed facilities employing Best Available Control Technologies and work to continually improve the design of those facilities. In 2013, nearly half of our total R&D budget of $133.7 million was spent on developing products that reduce GHGs and address other sustainability issues. The company also believes it will be able to mitigate some of these potential costs through its contractual terms.

The company has not incurred additional costs to actively engage in and monitor these areas as the efforts of our GHG Strategy and other teams, as well as costs associated with reduction commitments and customer engagement for cost recovery through contracts, are budgeted in the normal course of business. An estimate of the scale of those costs is <$1million/yr.

Carbon taxes The UK Climate Change Levy (CCL) is a tax on energy usage that has been in place since 2001. As a

Increased operational cost

Up to 1 year

Direct Virtually certain

Low A carbon tax example is the UK Climate Change Levy (CCL) on energy usage. If we had not been able to secure a renewed energy efficiency agreement, the financial impact

In 2012, Air Products recommitted to and signed a voluntary Climate Change Agreement, committing to an energy efficiency

The company has not incurred additional costs to actively engage in and monitor these areas as the efforts of our

18

Risk driver Description Potential impact

Time frame

Direct/Indirect Likelihood

Magnitude of impact

Estimated financial implications Mgmt. method Cost of Mgmt.

company with energy-intensive processes, such a tax could impact our value chain and growth by increasing operating costs, both directly and through suppliers. However, Air Products recommitted to and signed a voluntary Climate Change Agreement, committing to an energy efficiency target, and received a reduction in the CCL.

of this tax would have been in the range of $2-5 million.

target, and received a reduction in the CCL. We were able to commit to an energy efficiency target as we work to continually improve the design of those facilities to lower energy consumption, improve efficiency and reduce emissions. Consistent with our 7% intensity-based energy reduction goals, we continue to invest in efficiency improvements at our facilities. In 2013, nearly half of our total R&D budget of $133.7 million was spent on developing products that reduce GHGs and address other sustainability issues. Our business planning processes focus on energy reduction targets that translate into GHG impact. We formally integrated GHG considerations into our global capital expenditure authorization process, marketing and procurement and investment transactions and continue to more fully integrate considerations into other processes, including product and process design, M&A, and sourcing. The company also believes it will be able to mitigate some of these potential costs through its contractual terms.

GHG Strategy and other teams, as well as costs associated with reduction commitments and customer engagement for cost recovery through contracts, are budgeted in the normal course of business. An estimate of the scale of those costs is <$1million/yr.

Carbon taxes Carbon taxes are possible in other jurisdictions that could impact the Company. For example, China has discussed the potential for a carbon tax. Carbon taxes in the U.S. are exceptionally unlikely given the environment in Congress. Any regulation that limits or taxes GHG

Increased operational cost

Unknown Direct Unknown Unknown The high degree of uncertainty in the timing and content of future carbon taxes prevents accurate prediction of the potential risk impact to Air Products. Given our market capitalization of $23.6 billion as of 31 Dec 2013, a hypothetical impact (from increased operating costs or reduced demand for certain products) that would result in a decreased stock-price of 1% would yield a reduced market value of

Our GHG Strategy Team identifies climate change risks and opportunities, serving as our global center of excellence on policy development, regulations, legislation, and regularly updating management and the Board. As part of this team, our Government Relations staff works with agencies and

The company has not incurred additional costs to actively engage in and monitor these areas as the efforts of our GHG Strategy and other teams, as well as costs associated with reduction commitments and customer engagement for cost recovery through contracts, are budgeted in the

19

Risk driver Description Potential impact

Time frame

Direct/Indirect Likelihood

Magnitude of impact

Estimated financial implications Mgmt. method Cost of Mgmt.

emissions from company facilities could impact our value chain and growth by increasing operating costs, both directly and through suppliers. The company believes it will be able to mitigate some of these potential costs through its contractual terms, but the lack of definitive regulations prevents accurate prediction of the long-term impact.

~$200 million. NGOs in regions of the world where we have significant business interests to develop strategy, understand business environments, and protect/position our businesses to respond to climate change risks and opportunities. These efforts are augmented through membership in executive leadership forums, including the Business Environmental Leadership Council of the Center for Climate and Energy Solutions that provides insights into the local and international stage. We are involved with trade associations including the American Chemistry Council, Compressed Gas Association and European Industrial Gas Association. We continue to develop technologies that enable our customers and our facilities to lower energy consumption, improve efficiency and reduce emissions. In 2013, nearly half of our total R&D budget of $133.7 million was spent on developing products that reduce GHGs and address other sustainability issues. Our business planning processes focus on energy reduction targets that translate into GHG impact. We have also integrated GHG considerations into other business processes. The company believes it will be able to mitigate some of these potential costs through contractual terms.

normal course of business. An estimate of the scale of those costs is <$1million/yr. Membership dues for trade organizations are paid in the normal course of business. An estimate of these costs is <$1million.

Cap and trade schemes

Phase 3 (2013-2020) EU Emission Trading Scheme (ETS)

Reduced demand for goods/services

1 to 3 years

Direct About as likely as not

Low The company believes it will be able to mitigate some of these potential costs

Our GHG Strategy Team identifies climate change risks and opportunities,

The company has not incurred additional costs to actively

20

Risk driver Description Potential impact

Time frame

Direct/Indirect Likelihood

Magnitude of impact

Estimated financial implications Mgmt. method Cost of Mgmt.

is in force and associated legislative measures continue active consideration. Therefore, it is possible a provision could result in different treatments between our plants and our customers’ alternative in-house supply options. This issue is long-recognized and has been addressed as a “non-distortion principle” in Recital 23 of the relevant EU Directive. To date, that principle has been upheld in all the subsequent rulemaking. Likewise, as part of the implementation of CA AB32, the California Air Resource Board (CARB) has implemented a cap and trade scheme that started January 2013 and active reconsideration is ongoing. In South Korea, an ETS is scheduled to be implemented in 2015 and details are emerging. In China, seven regions (Beijing, Tianjin, Shanghai, Chongqing, and Shenzhen, Guangdong and Hubei) were chosen to start official, state-sanctioned ETS pilots in 2013. Pilots began in Beijing, Tianjin, Shanghai, Shenzhen, and Guangdong over the year. In any jurisdiction were details are still emerging or where active reconsideration is ongoing, any provision that results in difference in treatment could result in

through its contractual terms, but the lack of definitive regulations prevents accurate prediction of the long-term impact. Given our market capitalization of $23.6 billion as of 31 Dec 2013, a hypothetical impact (from increased operating costs or reduced demand for certain products) that would result in a decreased stock-price of 1% would yield a reduced market value of ~$200 million.

serving as our global center of excellence on internal policy development, regulations, legislation, and regularly updating management and the Board. As part of this team, our Government Relations staff works with government agencies and NGOs in regions of the world where we have significant business interests to develop strategy, understand changing business environments, and protect and position our businesses to respond to climate change risks and opportunities. These efforts are augmented through membership in executive leadership forums, including the Business Environmental Leadership Council of the Center for Climate and Energy Solutions that provides insights into the local and international stage. We are involved with trade associations including the American Chemistry Council, Compressed Gas Association and European Industrial Gas Association (EIGA).Through EIGA we supported the quantification of potential market distortions due to EU ETS and how such distortions could harm the EU industrial gas industry and result in increased emissions. Our efforts have been successful; four years ago this issue was addressed as a non-distortion principle in Recital 23 of the relevant EU ETS Directive, and that principle has been upheld in subsequent rulemaking.

engage in and monitor these areas as the efforts of our GHG Strategy and other teams, as well as costs associated with reduction commitments and customer engagement for cost recovery through contracts, are budgeted in the normal course of business. An estimate of the scale of those costs is <$1million/yr. Membership dues for trade organizations are paid in the normal course of business. An estimate of these costs is <$1million.

21

Risk driver Description Potential impact

Time frame

Direct/Indirect Likelihood

Magnitude of impact

Estimated financial implications Mgmt. method Cost of Mgmt.

pricing disadvantages for our products and services. Such distortions could lead some customers to produce products themselves instead of purchasing from Air Products (e.g., refineries making their own hydrogen for cleaner burning transportation fuels).

Through these efforts, the likelihood and magnitude of the risk over the entire EU ETS Phase 3 program from 2013-2020 was significantly decreased.

Cap and trade schemes

Phase 3 (2013-2020) EU Emission Trading Scheme (ETS) is in force and associated legislative measures continue active consideration. Therefore, it is possible a provision could result in different treatments between our plants and our customers’ alternative in-house supply options. This issue is long-recognized and has been addressed as a “non-distortion principle” in Recital 23 of the relevant EU Directive. To date, that principle has been upheld in all the subsequent rulemaking. Likewise, as part of the implementation of CA AB32, the California Air Resource Board (CARB) has implemented a cap and trade scheme that started January 2013 and active reconsideration is ongoing. In South Korea, an ETS is scheduled to be implemented in 2015 and details are emerging. In China, seven regions (Beijing, Tianjin, Shanghai, Chongqing, and Shenzhen,

Increased operational cost

1 to 3 years

Direct About as likely as not

Low The company believes it will be able to mitigate some of these potential costs through its contractual terms, but the lack of definitive regulations prevents accurate prediction of the long-term impact. Given our market capitalization of $23.6 billion as of 31 Dec 2013, a hypothetical impact (from increased operating costs or reduced demand for certain products) that would result in a decreased stock-price of 1% would yield a reduced market value of ~$200 million.

Our GHG Strategy Team identifies climate change risks and opportunities, serving as our global center of excellence on internal policy development, regulations, legislation, and regularly updating management and the Board. As part of this team, our Government Relations staff works with government agencies and NGOs in regions of the world where we have significant business interests to develop strategy, understand changing business environments, and protect and position our businesses to respond to climate change risks and opportunities. These efforts are augmented through membership in executive leadership forums, including the Business Environmental Leadership Council of the Center for Climate and Energy Solutions that provides insights into the local and international stage. We are involved with trade associations including the American Chemistry Council, Compressed Gas Association and European Industrial Gas Association

The company has not incurred additional costs to actively engage in and monitor these areas as the efforts of our GHG Strategy and other teams, as well as costs associated with reduction commitments and customer engagement for cost recovery through contracts, are budgeted in the normal course of business. An estimate of the scale of those costs is <$1million/yr. Membership dues for trade organizations are paid in the normal course of business. An estimate of these costs is <$1million.

22

Risk driver Description Potential impact

Time frame

Direct/Indirect Likelihood

Magnitude of impact

Estimated financial implications Mgmt. method Cost of Mgmt.

Guangdong and Hubei) were chosen to start official, state-sanctioned ETS pilots in 2013. Pilots began in Beijing, Tianjin, Shanghai, Shenzhen, and Guangdong over the year. In any jurisdiction were details are still emerging or where active reconsideration is ongoing, any provision that results in difference in treatment could result in pricing disadvantages for our products and services. Such distortions could lead some customers to produce products themselves instead of purchasing from Air Products (e.g., refineries making their own hydrogen for cleaner burning transportation fuels).

(EIGA).Through EIGA we supported the quantification of potential market distortions due to EU ETS and how such distortions could harm the EU industrial gas industry and result in increased emissions. Our efforts have been successful; four years ago this issue was addressed as a non-distortion principle in Recital 23 of the relevant EU ETS Directive, and that principle has been upheld in subsequent rulemaking. Through these efforts, the likelihood and magnitude of the risk over the entire EU ETS Phase 3 program from 2013-2020 was significantly decreased.

Cap and trade schemes

A cap and trade scheme could also be implemented in several jurisdictions where Air Products has facilities. It would be reasonable to assume emissions from Air Products’ facilities could be included. Cap and trade piloting has been announced in seven areas in China. Additionally, South Korea has passed a law for a cap and trade scheme with a 2015 start. However, a Federal cap and trade scheme in the U.S. is exceptionally unlikely given the current environment in the U.S. Congress. Any regulation that limits or

Reduced demand for goods/services

1 to 3 years

Direct About as likely as not

Low The company believes it will be able to mitigate some of these potential costs through its contractual terms, but the lack of definitive regulations prevents accurate prediction of the long-term impact. Given our market capitalization of $23.6 billion as of 31 Dec 2013, a hypothetical impact (from increased operating costs or reduced demand for certain products) that would result in a decreased stock-price of 1% would yield a reduced market value of ~$200 million.

Our GHG Strategy Team identifies climate change risks and opportunities, serving as our global center of excellence on internal policy development, regulations, legislation, and regularly updating management and the Board. As part of this team, our Government Relations staff works with government agencies and NGOs in regions of the world where we have significant business interests to develop strategy, understand changing business environments, and protect and position our businesses to respond to climate change risks and opportunities. These efforts are augmented

The company has not incurred additional costs to actively engage in and monitor these areas as the efforts of our GHG Strategy and other teams, as well as costs associated with reduction commitments and customer engagement for cost recovery through contracts, are budgeted in the normal course of business. An estimate of the scale of those costs is <$1million/yr. Membership dues for trade organizations are paid in the normal course of business. An estimate of these costs is <$1million.

23

Risk driver Description Potential impact

Time frame

Direct/Indirect Likelihood

Magnitude of impact

Estimated financial implications Mgmt. method Cost of Mgmt.