cecl - cpa firms | accountant | financial accounting cost (cecl) asc 326-30 financial instruments-...

TRANSCRIPT

8/1/2016

1

CECLBreaking Down the Final Standard

Gordon Dobner, CPADirector

Trey Turnage, CPAPartner

July 27, 2016

8/1/2016

2

• Participate in entire webinar• Answer polls when they are provided• If you are viewing this webinar in a group

Complete group attendance form with• Title & date of live webinar• Your company name• Your printed name, signature & email address

All group attendance sheets must be submitted to [email protected] within 24 hours of live webinar Answer polls when they are provided

• If all eligibility requirements are met, each participant will be emailed their CPE certificates within 15 business days of live webinar

TO RECEIVE CPE CREDIT

NEW IMPAIRMENT GUIDANCE

Incurred/Probable Expected/Lifetime

8/1/2016

3

NEW IMPAIRMENT GUIDANCE

Topic Scope

ASC 450-20(FAS 5)

Contingencies- Loss Contingencies

ASC 310-30 Receivables- Loans & Debt Securities -Acquired with Deteriorated Credit Quality

ASC 310-10 Receivables- Overall

ASC 320-10 Investments- Debt Securities

• ASU 2016-13Topic Scope

ASC 326-20 Financial Instruments-Credit Losses-Amortized Cost (CECL)

ASC 326-30 Financial Instruments- Credit Losses-AFS Debt Securities

• Current Guidance

Effective Date (for Entities with Calendar Year-Ends)

ASU 2016-13 Impairment (CECL)

*

Type 2020 2021 2022

PBE – SEC filers

Interim & annual

PBE – small Interim & annual

All others Annual Interim

* Early adoption permitted for all entities for periods beginning after December 15, 2018

CECL IMPLEMENTATION DATES

8/1/2016

4

2018• ASU 2014-09 Revenue Recognition• ASU 2016-01 Classification & Measurement

2019• ASU 2016-02 Leases

2020• ASU 2016-13 CECL

OTHER MAJOR PROJECTS – EFFECTIVE DATES PUBLIC ENTITIES

• Included Financing receivables Held to maturity debt Loan commitments, guarantees,

standby L/C Lease receivables Reinsurance receivables Receivables on repurchase &

securities lending agreements

• Excluded Financial assets at fair value Available for sale debt (updated

model) Participant loans defined

contribution benefit plans Insurance policy loans NFP pledges receivable

CECL SCOPE

8/1/2016

5

Which of the following is NOT within the scope of ASU 2016-03? Reinsurance receivables Investments in equity securities Investments in debt securities measured at FV-OCI Loan commitments not measured at FV-NI I don’t know

POLLING QUESTION 1

Start –Begin with historical

losses

Adjust –Look forward for a

“reasonable” period

Revert –Revert to historical

averages

RANGE OF INFORMATION

Entities cannot rely solely on past events to estimate expected credit losses

Entities are not required to develop forecasts over asset’s or pool’s contractual term

8/1/2016

6

For a 30-year mortgage, does CECL require a 30-year forecast? Yes No Unsure

POLLING QUESTION 2

INDIVIDUAL VS. POOLED ?

Entities can develop credit loss estimates on a pooled basis if the assets share similar risk characteristics; if not, an individual evaluation is appropriate

8/1/2016

7

Does CECL get rid of individual loan impairment assessments? Yes No Unsure

POLLING QUESTION 3

Specific approach is not mandated

Banks can leverage existing credit risk management systems & processes, including

• Discounted cash flow• Loss rate method• Roll rate method• Probability of default• Aging schedules

METHODS

8/1/2016

8

• Fancy model – No, Excel spreadsheets ok!

• Additional data – Yes Banks will need to capture &

save additional loan level data – risk rating by individual loan, loan duration, individual loan balance, individual loan charge-offs & recoveries (partial & full), etc.

METHODS

• OTTI model eliminated• Allowance approach• Losses will be recognized sooner than under today’s guidance;

however, model allows for immediate gain recognition on recovery

AVAILABLE FOR SALE DEBT SECURITIES

8/1/2016

9

• Modifies definition of what were previously known as purchased credit-impaired (PCI)

• “Acquired financial asset or acquired groups of financial assets with similar risk characteristics that have experienced a more-than-insignificant deterioration in credit quality since origination, based on the buyer’s assessment”

PURCHASED ASSETS WITH CREDIT DETERIORATION

• Same approach as originated assets• Initial allowance for credit losses will be added to purchase price

rather than being recorded as a credit loss expense in income statement

• Subsequent changes in allowance for credit losses for PCD assets will be recorded as a credit loss expense in income statement

PURCHASED ASSETS WITH CREDIT DETERIORATION

8/1/2016

10

Bank ABC pays $750,000 for a bond with a par amount of $1,000,000. Bond is measured at amortized cost basis. At purchase, allowance for credit loss on unpaid principal balance is estimated at $175,000

Loan—par amount $ 1,000,000Loan—noncredit discount $ 75,000Allowance for credit losses $ 175,000Cash $ 750,000

$75,000 noncredit discount would be accreted into interest income over bond’s life

PURCHASED ASSETS WITH CREDIT DETERIORATION (PCD)

PCD TRANSITION RELIEF

• Assets previously accounted for PCI assets would be classified as PCD assets at adoption

• Allowance for expected credit losses for all PCD assets would be grossed up at adoption

• Interest income would continue to be based on asset yield as of adoption date

8/1/2016

11

For PCD financial assets, interest income would be based on contractual cash flows. True False I don’t know

POLLING QUESTION 4

• Many existing disclosure have been carried forward without change• Past due loans• Nonaccrual loans• TDRs

Judgment will be required in determining correct level of detail to satisfy financial statement users without aggregating too much data or including excess details

DISCLOSURES

8/1/2016

12

• How does management monitor credit quality of its financial assets & assess risks?

• Includes both quantitative & qualitative information, including • A description of credit quality indicator• Amortized cost basis, by credit quality indicator • For credit quality indicator, date or range of dates in which information

was last updated

NEW DISCLOSURES – CREDIT QUALITY

• Not required for entities that aren’t public business entities • For PBEs that are non-SEC filers, transitional relief will allow

banks to “build up” data over time to meet full disclosure requirements

NEW DISCLOSURES – CREDIT QUALITY VINTAGE

8/1/2016

13

CURRENT REGULATORY EXPECTATIONS

“ ”The agencies do not expect smaller and less complex institution will need to implement complex modeling techniques.

The ASU allows expected credit loss estimation approaches that build on existing credit risk management systems and processes, as well as existing methods (e.g. historical loss rate, roll-rate, discounted cash flows)

6/17/16 Joint Statement

8/1/2016

14

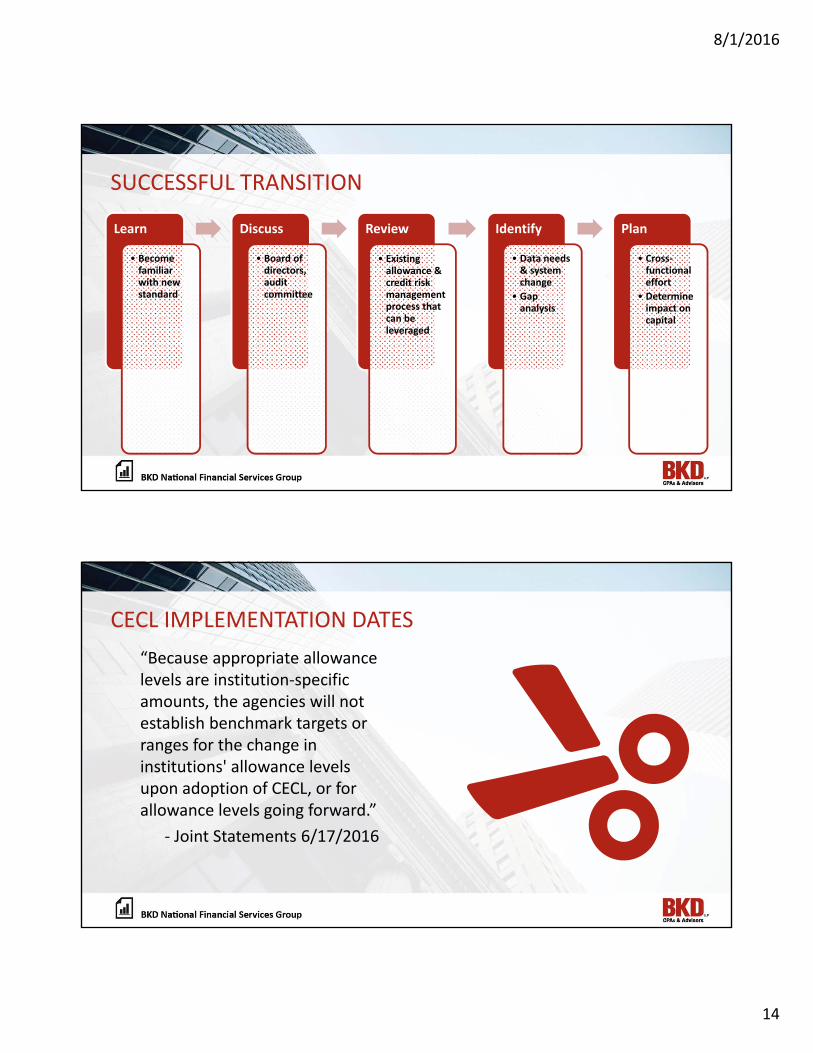

Learn

• Become familiar with new standard

Discuss

• Board of directors, audit committee

Review

• Existing allowance & credit risk management process that can be leveraged

Identify

• Data needs & system change

• Gap analysis

Plan

• Cross-functional effort

• Determine impact on capital

SUCCESSFUL TRANSITION

CECL IMPLEMENTATION DATES“Because appropriate allowance levels are institution-specific amounts, the agencies will not establish benchmark targets or ranges for the change in institutions' allowance levels upon adoption of CECL, or for allowance levels going forward.”

- Joint Statements 6/17/2016

8/1/2016

15

BKD.COM THOUGHTWARE®

8/1/2016

16

CONTINUING PROFESSIONAL EDUCATION (CPE) CREDITS

BKD, LLP is registered with the National Association of State Boards of Accountancy (NASBA) as a sponsor of continuing professional education on the National Registry of CPE Sponsors. State boards of accountancy have final authority on the acceptance of individual courses for CPE credit. Complaints regarding registered sponsors may be submitted to the National Registry of CPE Sponsors through its website: www.learningmarket.org.

The information in BKD webinars is presented by BKD professionals, but applying specific information to your situation requires careful consideration of facts & circumstances. Consult your BKD advisor before acting on any matters covered in these webinars.

• CPE credit may be awarded upon verification of participant attendance

• For questions, concerns or comments regarding CPE credit, please email the BKD Learning & Development Department at [email protected].

CPE CREDIT

8/1/2016

17

Trey Turnage | 601.948.6700 | [email protected]

Gordon Dobner | 713.499.4600 | [email protected]