central banking and the money supply

TRANSCRIPT

Central Banking and the Money Supply

Marshall Urias

Marshall Urias Central Banking and the Money Supply 1 / 34

Roadmap

We saw that with banks, inside money (demand deposits) replacedoutside money (fiat currency) so that financial intermediationmobilized all the savings of the economy for investment in capital.

Central bank has two additional tools

reserve requirementsbank loans

First step toward explaining coexistence of fiat money and deposits

Marshall Urias Central Banking and the Money Supply 2 / 34

Legal restrictions on financial intermediation

What if people prefer inside money to fiat money?

Prices would have to be expressed in a different unit of account, andthe government would be unable to raise any revenue from seigniorage

Central bank can use reserve requirement to have both inside andoutside money valued in equilibrium

Marshall Urias Central Banking and the Money Supply 3 / 34

Reserve requirements

Reserves are held in the form of vault cash or deposits within FederalReserve banks

No required reserves on the first $14.5 million of deposits, 3% onreservable deposits less than $103.6 million, and 10% on depositsexceeding $103.6 million

Reserve requirements on Canadian chartered banks were phased outin 1994

Reserve requirements in China are now 14.5% for large banks and12.5% for small banks

Marshall Urias Central Banking and the Money Supply 4 / 34

Environment

Continue environment of people with three-period lives and illiquidcapital

Capital pays return X > (n/z)2 two periods after its creation

Let Mt = zMt−1 with z ≥ 1

Initial middle-aged begin with stock of money

The net worth of a bank is what is owed to shareholders

Assume net worth is zero (liabilities completely take the form ofdeposits)

Marshall Urias Central Banking and the Money Supply 5 / 34

The bank’s balance sheet

Assets Liabilities

Reserves γH Deposits HInterest-bearing assets (1− γ)H Net worth 0Total assets H Total liabilities H

Table: Balance sheet. Deposits H are subject to reserve requirement γ, so thatthe bank must hold at least γH. Given that capital offers a higher return, thebank just satisfies the reserve requirements, purchasing (1− γ)H ofinterest-bearing assets.

Marshall Urias Central Banking and the Money Supply 6 / 34

Prices

The price level pt : the value of a good in terms of fiat money

Let ht be the goods deposited in banks by an individual

Supply and demand for fiat money (individuals do not hold currency)

νtMt = γNtht

Hence, the price level satisfies

pt =Mt

γNtht

Consider zero reserve requrement policy in Canda: γ = 0

Implies pt =∞ (no demand for fiat money)

There must be other sources of demand for fiat money (currency,bank demand other than through reserve requirement)

Marshall Urias Central Banking and the Money Supply 7 / 34

Seigniorage

Let St denote seigniorage revenue at date t

St = νt(Mt −Mt−1)

= νtMt

(1− 1

z

)= γNtht

(1− 1

z

)Seigniorage rises with an increase in the reserve requirement γ, anincrease in the real stock of bank deposits Ntht , and an increase inthe rate of fiat money creation z

Marshall Urias Central Banking and the Money Supply 8 / 34

Capital and output

Output is the sum of

labor endowmentcapital invested directly ktcapital invested directly in intermediaries: (1− γ)ht

Output Yt satisfies

Yt = Nty + Nt−2Xkt−2 + Nt−2X (1− γ)ht−2

Marshall Urias Central Banking and the Money Supply 9 / 34

Effect on output of reducing reserve requirements

An increase in γ reduces output by reducing bank intermediation

How large is this effect?

At the end of 2008, total net private capital stock in the UnitedStates was $34, 261 billion

Required reserves by U.S. commerical banks was $53 billion

Replacing all reserves with new capital stock would raise capital stockby under 0.16%

Marshall Urias Central Banking and the Money Supply 10 / 34

Deposits

So far, we assumed deposits Ntht were fixed in examining effects onprices, seigniorage, and output

Willigness to make deposits depends on rate of return (depends onsubstitution and income effects) held by banks

Marshall Urias Central Banking and the Money Supply 11 / 34

Gross real rate of return on deposits

One-period return on capital is x = X 1/2

Competitive banking induces banks to offer depositors the rate ofreturn they earn on assets

Rate of return is weighted average of return on money and capital:

r = γ(nz

)+ (1− γ)x

= x − γ[x −

(nz

)]

Increase in reserve requirement lowers rate of return on deposits

Increase in z lowers rate of return on deposits

Marshall Urias Central Banking and the Money Supply 12 / 34

Welfare

What are the effects of reserve requirements on individual welfare?

From νt = (γNtht)/Mt , an increase in reserve requirements raisesvalue of money and benefits the initial middle-aged (money holders)

Increase in γ lowers r and hence reduces c2 even if seignioragerevenue is returned to future generations

Welfare on future generations is lower because of lower return

Marshall Urias Central Banking and the Money Supply 13 / 34

Central bank definitions of money

In general, in economies with outside and inside money, there aredistinctions about the various ‘moneyness’ associated with differenttypes

Central banks define monetary aggregates

Definition of money varies across countries because deposit contractsand other assets differ

Marshall Urias Central Banking and the Money Supply 14 / 34

Famous quotes on moneyness

’I have always found it useful to explain to the student that ithas been rather a misfortune that we describe money by a noun,and that it would be more helpful for the explanation of monetaryphenomenon if ‘money’ were an adjective describing a propertywhich different things could possess to varying degrees’

(Friedrich Hayek, Denationalization of Money: the Argument Refined)

Marshall Urias Central Banking and the Money Supply 15 / 34

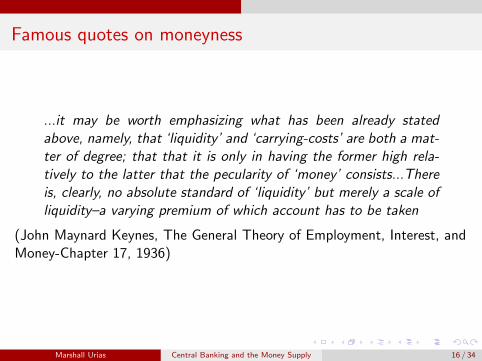

Famous quotes on moneyness

...it may be worth emphasizing what has been already statedabove, namely, that ‘liquidity’ and ‘carrying-costs’ are both a mat-ter of degree; that that it is only in having the former high rela-tively to the latter that the pecularity of ‘money’ consists...Thereis, clearly, no absolute standard of ‘liquidity’ but merely a scale ofliquidity–a varying premium of which account has to be taken

(John Maynard Keynes, The General Theory of Employment, Interest, andMoney-Chapter 17, 1936)

Marshall Urias Central Banking and the Money Supply 16 / 34

Famous quotes on moneyness

In brief, the general approach consists of regarding each asset as ajoint product having different degrees of ‘moneyness,’ and definingthe quantity of money as the weighted sum of the aggregated valueof all assets...

(Friedman and Schwartz, A Monetary History of the United States, 1970)

Marshall Urias Central Banking and the Money Supply 17 / 34

Monetary aggregates

Marshall Urias Central Banking and the Money Supply 18 / 34

The total money supply in the model

Define M1t as the total nominal stock deposits at period t

Deposits are the only form of money in this economy

Stock of fiat money in a reserve-requirement economy is referred toas the monetary base

M1t =Mt

γ

1/γ is called the money multiplier

Marshall Urias Central Banking and the Money Supply 19 / 34

Relationship between M1 and other variables

pt =Mt

γNtht=

M1tNtht

Quantity theory holds if Ntht does not depend on rate of return

If demand for deposits, Ntht is affected by the rate of return ondeposits, then the change in the price level depends on the tool usedto change M1

Typology

One-time increase in monetary base does not affect rPermanent increase in monetary base reduces rLower γ increase M1t and raises r

Marshall Urias Central Banking and the Money Supply 20 / 34

Central bank lending

Banks must demonstrate that they meet the level of reserves requiredfor deposits

If they fall short, they are faced with one of three options

sell interest-bearing assets for fiat moneyborrow from other banks (federal funds market)borrow from central bank (discount window)

Point of central bank lending is to permit banks to meet reserverequirements without precipitously selling off interest-bearing assets

Marshall Urias Central Banking and the Money Supply 21 / 34

Limited central bank lending

Let δ be the fraction of a bank’s reserves financed by loans from acentral bank

Let ΓBt represent the total nominal amount of borrowed reserves

Mt is the stock of fiat money not borrowed from reserves

δ =ΓBt

ΓBt + Mt

Marshall Urias Central Banking and the Money Supply 22 / 34

Bank balance sheet with central bank loans

Marshall Urias Central Banking and the Money Supply 23 / 34

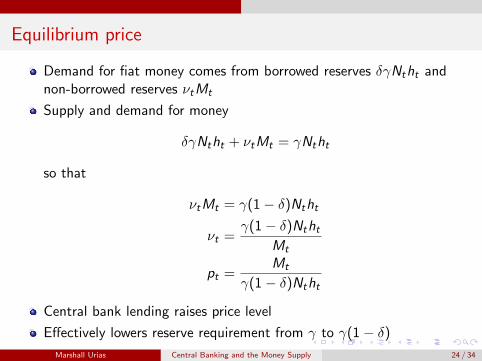

Equilibrium price

Demand for fiat money comes from borrowed reserves δγNtht andnon-borrowed reserves νtMt

Supply and demand for money

δγNtht + νtMt = γNtht

so that

νtMt = γ(1− δ)Ntht

νt =γ(1− δ)Ntht

Mt

pt =Mt

γ(1− δ)Ntht

Central bank lending raises price level

Effectively lowers reserve requirement from γ to γ(1− δ)

Marshall Urias Central Banking and the Money Supply 24 / 34

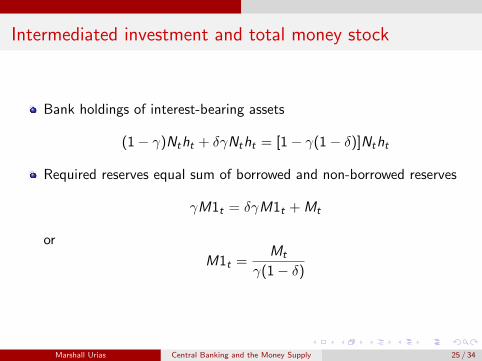

Intermediated investment and total money stock

Bank holdings of interest-bearing assets

(1− γ)Ntht + δγNtht = [1− γ(1− δ)]Ntht

Required reserves equal sum of borrowed and non-borrowed reserves

γM1t = δγM1t + Mt

or

M1t =Mt

γ(1− δ)

Marshall Urias Central Banking and the Money Supply 25 / 34

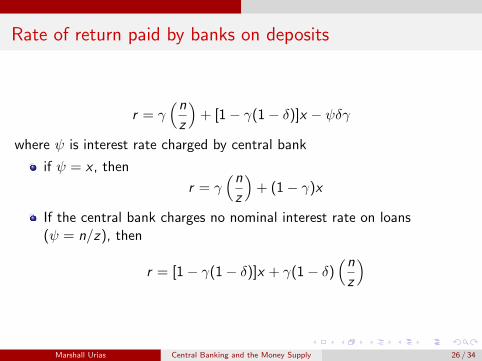

Rate of return paid by banks on deposits

r = γ(nz

)+ [1− γ(1− δ)]x − ψδγ

where ψ is interest rate charged by central bank

if ψ = x , then

r = γ(nz

)+ (1− γ)x

If the central bank charges no nominal interest rate on loans(ψ = n/z), then

r = [1− γ(1− δ)]x + γ(1− δ)(nz

)

Marshall Urias Central Banking and the Money Supply 26 / 34

Unlimited central bank lending

Suppose central bank just sets the interest it will charge, ψ, andpermits banks to borrow as much as they desire

A fixed return to capital x leads to indeterminacy

if ψ > x , then no bank borrows

if ψ < x , then the bank borrows unlimited amounts

if ψ = x , then any borrowed reserves is possible, and the price level isindeterminate

Marshall Urias Central Banking and the Money Supply 27 / 34

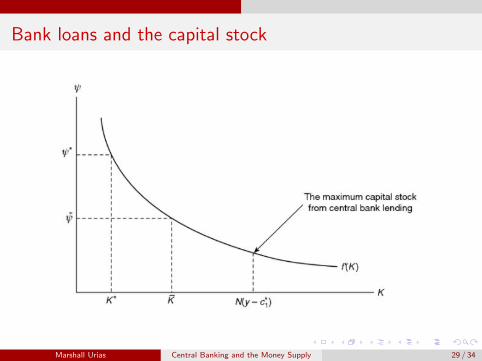

Breaking the indeterminacy

A diminishing marginal product of capital restores determinacy

Assume return f (k), where f (0) = 0, f ′(0) =∞, and f ′′(k) < 0

Banks borrow until f ′(k) = ψ

Marshall Urias Central Banking and the Money Supply 28 / 34

Bank loans and the capital stock

Marshall Urias Central Banking and the Money Supply 29 / 34

Limits of central bank lending

Expanding lending raises the price level, which hurts current holdersof fiat money

Real effect on capital of lowering the rate charged by the central bankis bounded above by γNtht

Marshall Urias Central Banking and the Money Supply 30 / 34

Central bank lending in the United States and Canada

From 1980-1995, the Bank of Canada followed a floating penalty rate:the bank rate was equal to the 91-day Treasury bill rate plus onequarter of 1%

The United States sets a rate and changes it infrequently(administered rate)

Since 1995, the Bank of Canada has also followed an administeredrate

Marshall Urias Central Banking and the Money Supply 31 / 34

Central bank lending rates

Figure: Source: the Bank rate is from various issues of the Bank of CanadaReview. The discount rate is from the Federal Reserve Bulletin. Both series aremonthly.

Marshall Urias Central Banking and the Money Supply 32 / 34

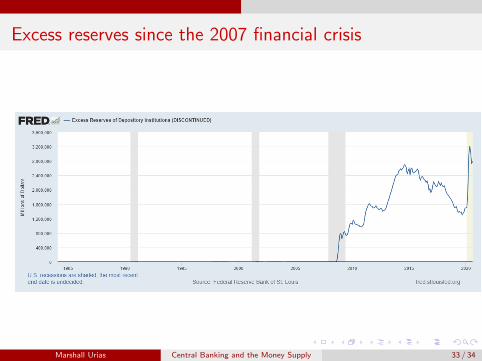

Excess reserves since the 2007 financial crisis

Marshall Urias Central Banking and the Money Supply 33 / 34

Summary

Reserve requirements give rise to a money multiplier whereby thetotal money supply is a multiple of the monetary base

Reserve requirements increase the demand for fiat money (andseigniorage) but reduce intermediation (and output)

Higher reserve requirements make future generations worse off bylowering the rate of return that banks can pay on deposits

Central bank lending is equivalent to a decrease in the reserverequirement

Marshall Urias Central Banking and the Money Supply 34 / 34