central florida expressway authority · central florida expressway authority presentation agenda 1....

TRANSCRIPT

CENTRAL FLORIDA EXPRESSWAY AUTHORITY

Rating Agency Presentation

May 2015 1

CENTRAL FLORIDA EXPRESSWAY AUTHORITY

PRESENTATION AGENDA

1. Organizational Background

2. Central Florida Expressway Authority Service Area

3. Operating and Financial Results

4. Traffic & Revenue

5. Five-Year Work Plan

6. Wekiva Parkway Update

7. Debt Management

8. Plan of Finance

9. Conclusion

2

CENTRAL FLORIDA EXPRESSWAY AUTHORITY

CENTRAL FLORIDA EXPRESSWAY

AUTHORITY ATTRIBUTES

• Strong economic base with increased tourism and theme park expansions; service area continues to diversify with growth in healthcare and education

• Excellent condition of the System; competitive toll rates with limited competition

• Positive revenue growth and financial flexibility with fixed rate debt at 80.4% and variable rate debt at 19.6% of total

• Forward looking toll structure indexed to the FL Consumer Price Index (CPI) with an annual 3 percent floor beginning on July 1, 2012 and every five years thereafter

• Proactive management efforts to contain costs and reduce variable rate debt & counterparty risk

• Conservative approach towards defining work program, future debt needs, and financial projections

• Strong debt service coverage and liquidity position provides significant bondholder protections

• Healthy reserve levels

• Low cost of toll collections

3

CENTRAL FLORIDA EXPRESSWAY AUTHORITY

0

50

100

150

200

250

300

350

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Mill

ion

s

Toll System Revenues Less E-PASS Discount

Toll Revenues

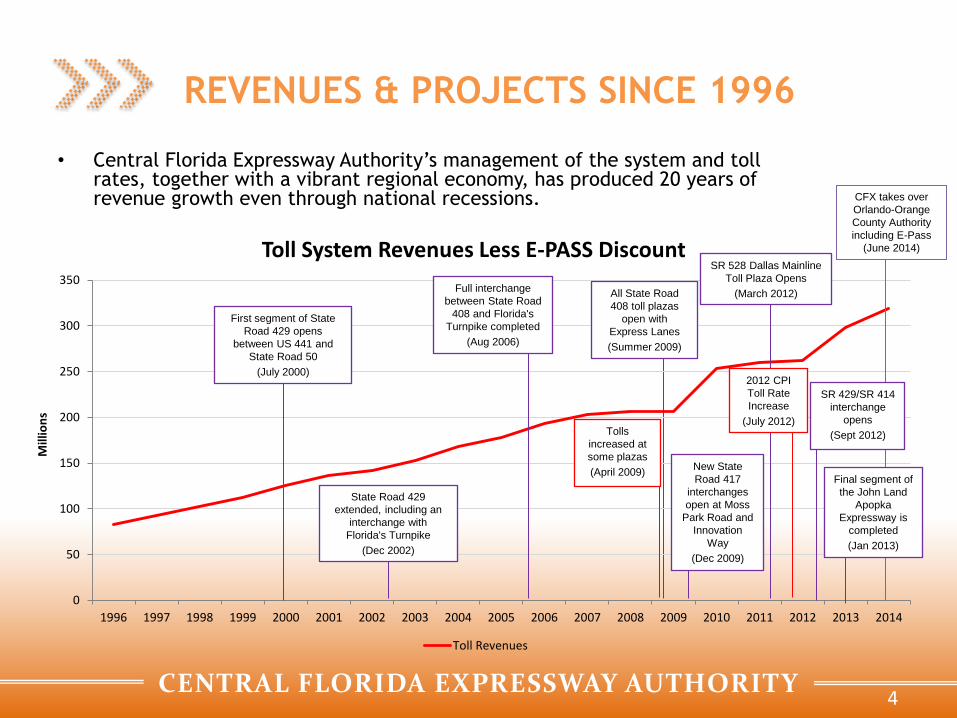

REVENUES & PROJECTS SINCE 1996

• Central Florida Expressway Authority’s management of the system and toll rates, together with a vibrant regional economy, has produced 20 years of revenue growth even through national recessions.

First segment of State

Road 429 opens

between US 441 and

State Road 50

(July 2000)

State Road 429

extended, including an

interchange with

Florida's Turnpike

(Dec 2002)

Full interchange

between State Road

408 and Florida's

Turnpike completed

(Aug 2006)

Tolls

increased at

some plazas

(April 2009)

SR 528 Dallas Mainline

Toll Plaza Opens

(March 2012)

SR 429/SR 414

interchange

opens

(Sept 2012)

Final segment of

the John Land

Apopka

Expressway is

completed

(Jan 2013)

2012 CPI

Toll Rate

Increase

(July 2012)

New State

Road 417

interchanges

open at Moss

Park Road and

Innovation

Way

(Dec 2009)

All State Road

408 toll plazas

open with

Express Lanes

(Summer 2009)

CFX takes over

Orlando-Orange

County Authority

including E-Pass

(June 2014)

4

CENTRAL FLORIDA EXPRESSWAY AUTHORITY

FISCAL YEAR TO DATE TOLL REVENUE

GROWTH OVER PREVIOUS FISCAL YEAR

4.99%

2.84%

7.72%

13.34%

6.54%

5.68%

6.97%

10.93%

15.52%

8.62%

0.00%

2.00%

4.00%

6.00%

8.00%

10.00%

12.00%

14.00%

16.00%

18.00%

SR 408 Beachline Eastern Beltway Western Beltway Total System

March 2014

March 2015

5

CENTRAL FLORIDA EXPRESSWAY AUTHORITY

Organizational Background

CENTRAL FLORIDA EXPRESSWAY AUTHORITY

ORGANIZATIONAL HIGHLIGHTS

• Experienced & tenured staff of senior professionals

• Commenced Completion of Orlando Beltway (Wekiva Parkway Project)

– On March 25, 2015, CFX closed a $196.3MM TIFIA loan

• Currently updating five-year work plan & beginning stages of 2040 Master

Plan

• Updates on toll rate increases and traffic

• Conservative risk management in debt portfolio and strategic planning

7

CENTRAL FLORIDA EXPRESSWAY AUTHORITY

CENTRAL FLORIDA EXPRESSWAY AUTHORITY

SYSTEM IS MODERN, MATURE & GROWING

• Established 1963 – over 50 Years Old

• Operates a limited-access highway network

• Comprised of 109 centerline miles of expressways

– 741 Lane Miles

– 14 Mainline Toll Plazas

– 64 Ramp Plazas

– 301 Toll Collection Lanes

8

CENTRAL FLORIDA EXPRESSWAY AUTHORITY

CENTRAL FLORIDA EXPRESSWAY

AUTHORITY ORGANIZATIONAL CHART

Authority Board

Laura Kelley Deputy Executive Director

Administration

Lisa Lumbard Interim Chief Financial

Officer

Claude Miller Director of Procurement

Joann Chizlett Director of Information

Technology

Joseph Berenis, P.E. Deputy Executive Director Engineering

& Operations

Ben Dreiling, P.E. Director of Construction and

Maintenance

Glenn Pressimone, P.E. Director of Engineering

Corey Quinn Director of Expressway

Operations

Joseph Passiatore General Counsel

Joseph Berenis, P.E. Acting Executive Director

Protiviti, Inc. Internal Auditor

Michelle Maikisch Director of Public Affairs

and Communication

Iranetta Dennis Director of Business

Development

David Wynne Director of Toll Operations

9

CENTRAL FLORIDA EXPRESSWAY AUTHORITY

Central Florida Expressway

Authority Service Area

CENTRAL FLORIDA EXPRESSWAY AUTHORITY

CENTRAL FLORIDA EXPRESSWAY AUTHORITY IS

A VITAL COMPONENT OF CENTRAL FLORIDA’S

TRANSPORTATION SYSTEM

11

CENTRAL FLORIDA EXPRESSWAY AUTHORITY

CENTRAL FLORIDA WITHOUT TOLL ROADS

Orlando

Ora

ng

e C

o.

Lake

Co

.

Lake Co.

Polk Co.

Ora

ng

e C

o.

Lake

Co

.

Lake Apopka

East Lake Tohopekaliga

Orange Co.

Orlando Co.

Seminole Co.

Orange Co.

12

CENTRAL FLORIDA EXPRESSWAY AUTHORITY

CENTRAL FLORIDA WITH TOLL ROADS

Orange Co.

Orlando Co.

Ora

ng

e C

o.

Lake

Co

.

Lake Co.

Polk Co.

Ora

ng

e C

o.

Lake

Co

.

Lake Apopka

East Lake Tohopekaliga

408

528

417

429

Western Beltway C

Osceola Parkway

Western Beltway A

417

414

414

429

429

Orlando

Central Florida

Greeneway

East-West Expressway

Beachline Expressway

Wekiva Parkway

John Land Apopka

Expressway

Seminole Co.

Orange Co.

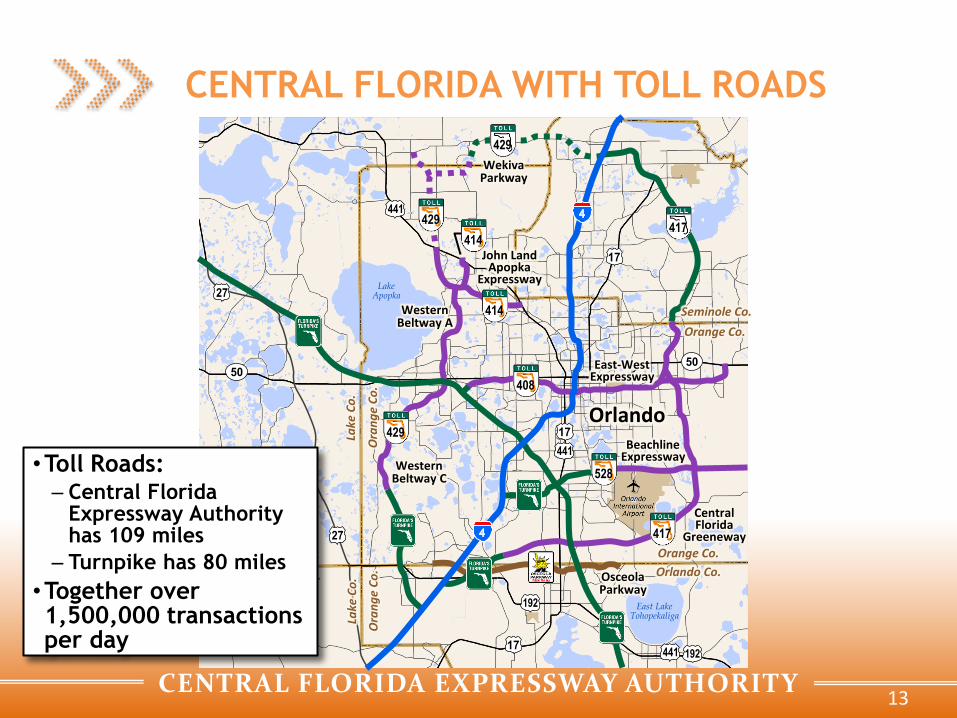

•Toll Roads: – Central Florida

Expressway Authority has 109 miles

– Turnpike has 80 miles

•Together over 1,500,000 transactions per day

13

CENTRAL FLORIDA EXPRESSWAY AUTHORITY

CENTRAL FLORIDA IS VITAL WITH MAJOR

DESTINATIONS CONNECTED BY CFX

• The system provides critical transportation links between the region’s residential

areas, major employment centers and the area’s major tourist attractions

– University of Central Florida – 2nd largest university in the country with Fall 2014

enrollment of 60,810 students1

– Valencia College – Winner of coveted Aspen Prize 2011; 59,958 credit seeking

students in 20132

– Orlando International Airport – nearly 18 million enplanements and 18,000 airport

employees3

– Lake Nona Medical City – Estimated to create up to 30,000 jobs over the next

decade4

– Walt Disney World Resort – 29 hotels5, 30,469 rooms6 and 180,000 Employees7

14

1 https://ikm.ucf.edu/enrollment-graduation/enrollment-statistics/2014-15-enrollment/ 2 http://valenciacollege.edu/aboutus/facts.cfm 3 http://www.orlandoairports.net/statistics/monthly/trfccy2014.pdfAuthority 4 Arduin, Laffer & Moore Econometrics 5 https://disneyworld.disney.go.com/faq/resorts/resort-hotel-list/ 6 http://touringplans.com/walt-disney-world/hotels/number-rooms# 7 http://thewaltdisneycompany.com/sites/default/files/reports/fy14-form-10k.pdf

CENTRAL FLORIDA EXPRESSWAY AUTHORITY

CENTRAL FLORIDA IS HOME TO 7 OF THE

TOP 20 THEME PARKS IN THE WORLD

Theme Park Attendance Statistics

15

Theme Parks 2013

Magic Kingdom 18,588,000

Epcot Center 17,214,000

Disney's Animal Kingdom 10,198,000

Disney's Hollywood Studios 10,110,000

Islands of Adventure at Universal Orlando 8,141,000

Universal Studios at Universal Orlando 7,062,000

SeaWorld Orlando 5,090,000

Busch Gardens Tampa Bay 4,087,000

Water Parks

Typhoon Lagoon 2,142,000

Blizzard Beach 1,968,000

Aquatica 1,553,000

Wet 'n Wild 1,259,000 Source: Themed Entertainment Association (TEA) and AECOM. All figures are estimates.

CENTRAL FLORIDA EXPRESSWAY AUTHORITY

RECENT DEVELOPMENTS AT DISNEY WORLD

WILL PRODUCE ECONOMIC GROWTH

Disney World – Fantasy Land Expansion

– Largest expansion in the history of the

Magic Kingdom park

– 2 new themed areas opened in 2012,

the start of Fantasyland Expansion

– Seven Dwarfs Mine Coaster opened in

2014, completing New Fantasyland

Expansion

– Cost exceeded $600 million

Disney World – Avatar Land

– Construction began 1/10/2014

– Project scheduled to open in early

2017

– Located in the Animal Kingdom

theme park

16

CENTRAL FLORIDA EXPRESSWAY AUTHORITY

5.53 5.93 6.04 6.2 7.06

4.63 5.95

7.67 7.98 8.14

0

2

4

6

8

10

12

14

16

2009 2010 2011 2012 2013

Att

end

ance

(m

illio

ns)

Universal Orlando Attendance

Universal Studios Islands of Adventure

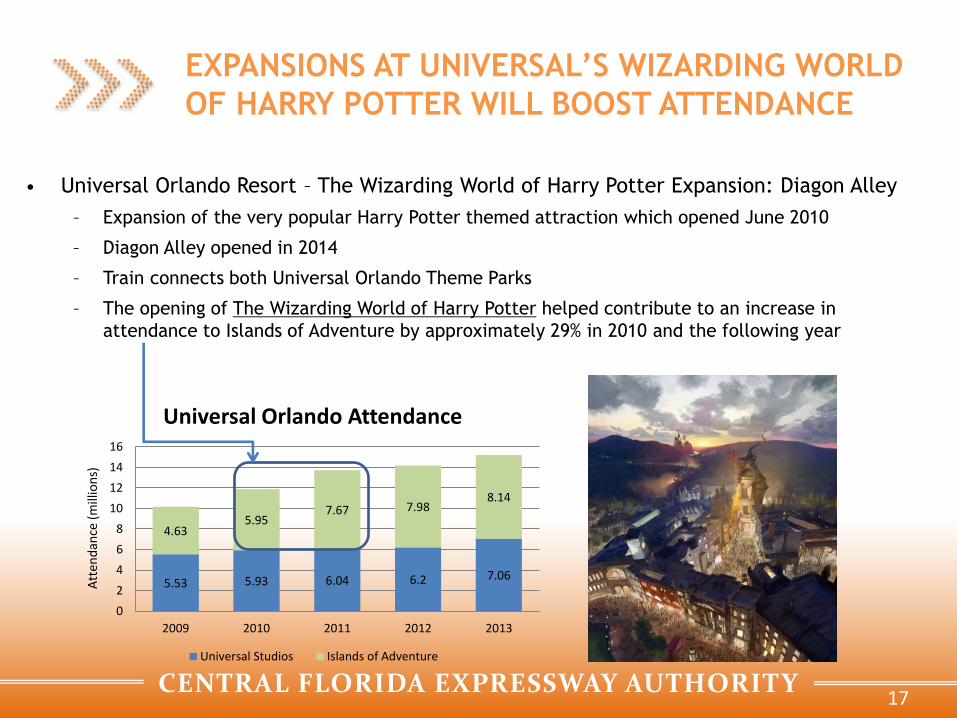

• Universal Orlando Resort – The Wizarding World of Harry Potter Expansion: Diagon Alley

– Expansion of the very popular Harry Potter themed attraction which opened June 2010

– Diagon Alley opened in 2014

– Train connects both Universal Orlando Theme Parks

– The opening of The Wizarding World of Harry Potter helped contribute to an increase in

attendance to Islands of Adventure by approximately 29% in 2010 and the following year

EXPANSIONS AT UNIVERSAL’S WIZARDING WORLD

OF HARRY POTTER WILL BOOST ATTENDANCE

17

CENTRAL FLORIDA EXPRESSWAY AUTHORITY

ECONOMIC DEVELOPMENT – WINTER

GARDEN

2006 2015

18

CENTRAL FLORIDA EXPRESSWAY AUTHORITY

ECONOMIC DEVELOPMENT – MEDICAL

CITY

2006 2015

19

CENTRAL FLORIDA EXPRESSWAY AUTHORITY

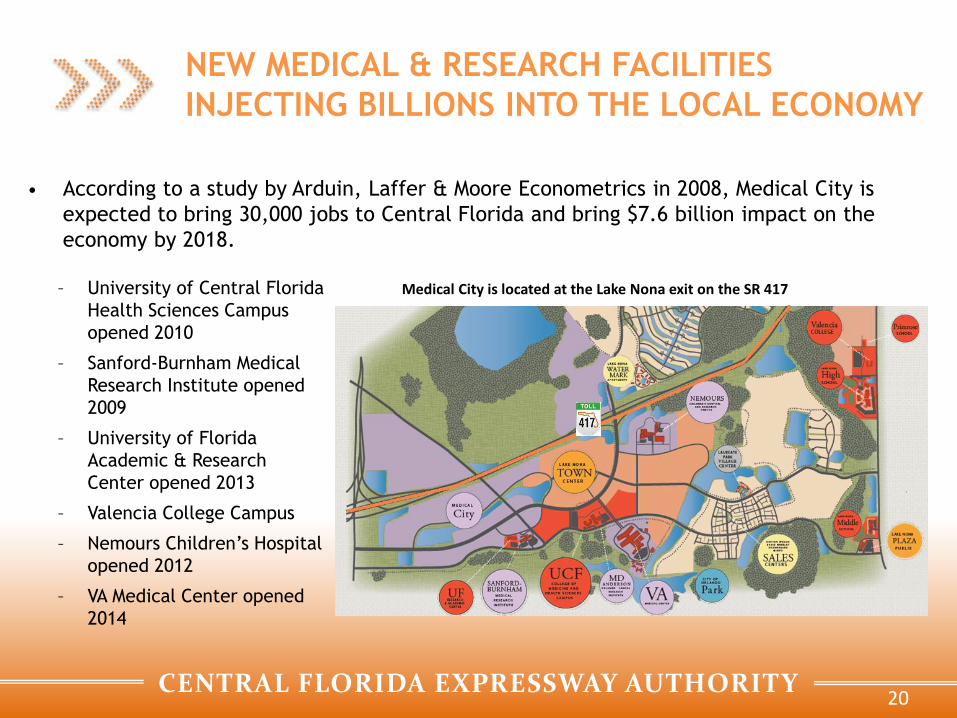

NEW MEDICAL & RESEARCH FACILITIES

INJECTING BILLIONS INTO THE LOCAL ECONOMY

• According to a study by Arduin, Laffer & Moore Econometrics in 2008, Medical City is

expected to bring 30,000 jobs to Central Florida and bring $7.6 billion impact on the

economy by 2018.

– University of Central Florida

Health Sciences Campus

opened 2010

– Sanford-Burnham Medical

Research Institute opened

2009

– University of Florida

Academic & Research

Center opened 2013

– Valencia College Campus

– Nemours Children’s Hospital

opened 2012

– VA Medical Center opened

2014

Medical City is located at the Lake Nona exit on the SR 417

20

CENTRAL FLORIDA EXPRESSWAY AUTHORITY

LAKE NONA SPORTS INNOVATION &

PERFORMANCE DISTRICT

• On April 8th, 2015 the United States Tennis Association (“USTA”) announced its relocation

to Lake Nona; expected to be the largest tennis center in the nation

• $60 million USTA anchor facility on 63 acre site within 11- square-mile sports district

• Expected completion in Fall 2016 with a relocating work force of 150 as well as new

hires from the local area

• The district to eventually include sports-related businesses and associations working in

concert with researchers at Lake Nona's Medical City cluster of health nonprofits and

businesses

21

CENTRAL FLORIDA EXPRESSWAY AUTHORITY

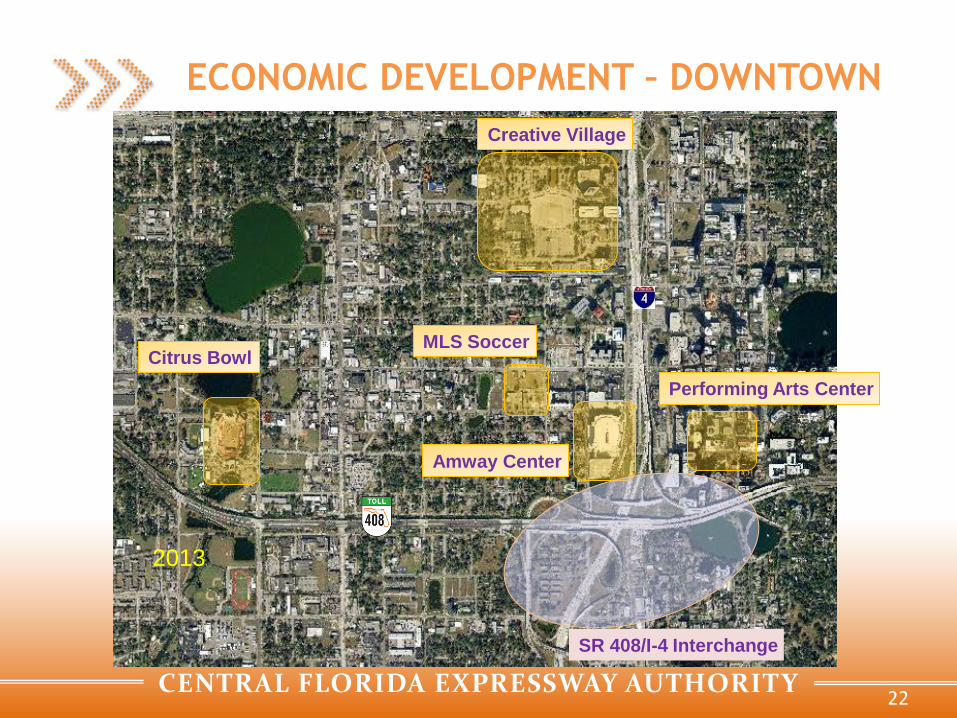

ECONOMIC DEVELOPMENT – DOWNTOWN

2013

2013

Creative Village

Performing Arts Center

Amway Center

Citrus Bowl

SR 408/I-4 Interchange

MLS Soccer

22

CENTRAL FLORIDA EXPRESSWAY AUTHORITY

CENTRAL FLORIDA VENUES

23

Dr. Phillips Center for Performing Arts Amway Center

Citrus Bowl MLS Soccer Stadium

CENTRAL FLORIDA EXPRESSWAY AUTHORITY

CENTRAL FLORIDA CONTINUES TO

IMPROVE AND EXPAND

• SunRail Commuter Rail

– Runs for 31 miles with 12 stations

– Service began in May of 2014

– Extensions for Phase 2 to be completed in

2017

– Carries approximately 3,200 riders per day

• All Aboard Florida

– Private operator for high speed rail from

Orlando to Miami in 3 hours

– Expected to create tens of thousands of

direct, non-recurring jobs and over 500

permanent jobs for the rail operations

24

CENTRAL FLORIDA EXPRESSWAY AUTHORITY

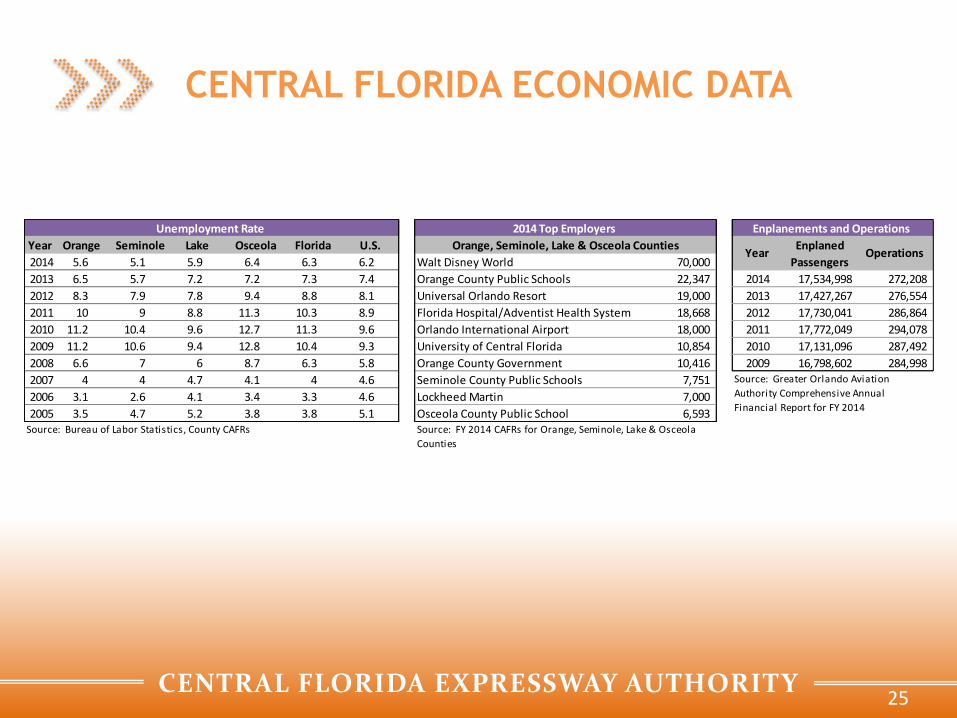

CENTRAL FLORIDA ECONOMIC DATA

25

Year Orange Seminole Lake Osceola Florida U.S. Enplaned

2014 5.6 5.1 5.9 6.4 6.3 6.2 Walt Disney World 70,000 Passengers

2013 6.5 5.7 7.2 7.2 7.3 7.4 Orange County Public Schools 22,347 2014 17,534,998 272,208

2012 8.3 7.9 7.8 9.4 8.8 8.1 Universal Orlando Resort 19,000 2013 17,427,267 276,554

2011 10 9 8.8 11.3 10.3 8.9 Florida Hospital/Adventist Health System 18,668 2012 17,730,041 286,864

2010 11.2 10.4 9.6 12.7 11.3 9.6 Orlando International Airport 18,000 2011 17,772,049 294,078

2009 11.2 10.6 9.4 12.8 10.4 9.3 University of Central Florida 10,854 2010 17,131,096 287,492

2008 6.6 7 6 8.7 6.3 5.8 Orange County Government 10,416 2009 16,798,602 284,998

2007 4 4 4.7 4.1 4 4.6 Seminole County Public Schools 7,751

2006 3.1 2.6 4.1 3.4 3.3 4.6 Lockheed Martin 7,000

2005 3.5 4.7 5.2 3.8 3.8 5.1 Osceola County Public School 6,593 Source: Bureau of Labor Statistics, County CAFRs

Source: Greater Orlando Aviation

Authority Comprehensive Annual

Financial Report for FY 2014

Source: FY 2014 CAFRs for Orange, Seminole, Lake & Osceola

Counties

Unemployment Rate 2014 Top Employers

Orange, Seminole, Lake & Osceola CountiesYear Operations

Enplanements and Operations

CENTRAL FLORIDA EXPRESSWAY AUTHORITY

Operational and Financial

Results

CENTRAL FLORIDA EXPRESSWAY AUTHORITY

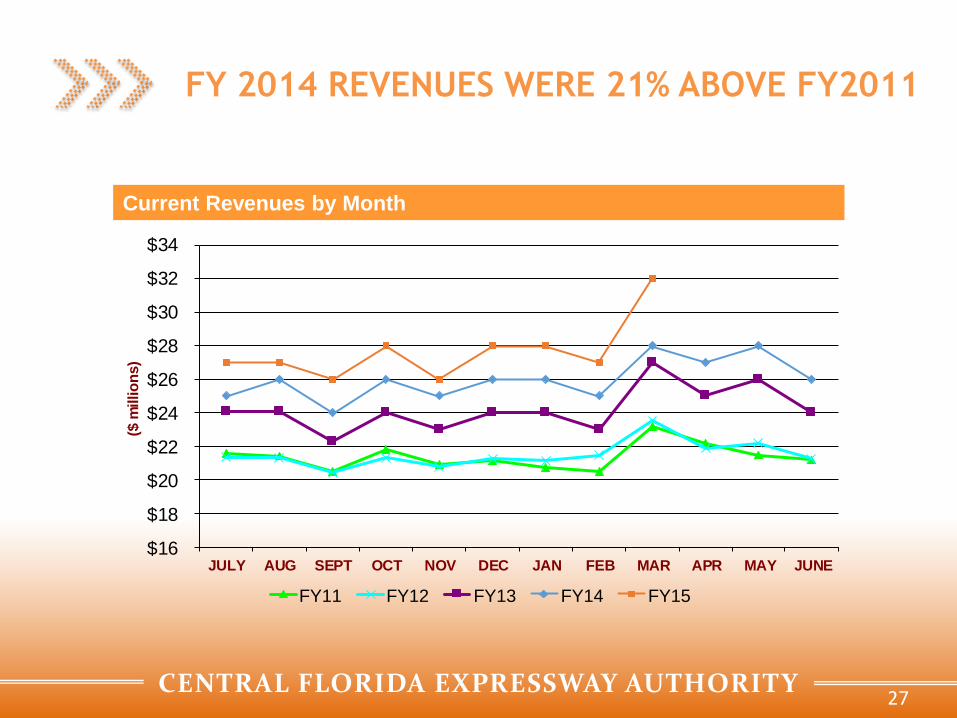

FY 2014 REVENUES WERE 21% ABOVE FY2011

Current Revenues by Month

27

$16

$18

$20

$22

$24

$26

$28

$30

$32

$34

JULY AUG SEPT OCT NOV DEC JAN FEB MAR APR MAY JUNE

($ m

illio

ns)

FY11 FY12 FY13 FY14 FY15

CENTRAL FLORIDA EXPRESSWAY AUTHORITY

20

22

24

26

28

30

32

34

JULY AUG SEPT OCT NOV DEC JAN FEB MAR APR MAY JUNE

($ m

illio

ns)

FY11 FY12 FY13 FY14 FY15

TRANSACTION COUNTS WERE UP 12%

FROM 2011 TO 2014

Current Traffic by Month

28

CENTRAL FLORIDA EXPRESSWAY AUTHORITY

$20

$22

$24

$26

$28

$30

$32

$34

JULY AUG SEPT OCT NOV DEC JAN FEB MAR APR MAY JUNE

($ m

illio

ns)

Actual Projections

REVENUES ARE 6.3% ABOVE PROJECTIONS

THROUGH MARCH FOR THE FISCAL YEAR

Revenue vs. Projections by Month for FY2014

29

CENTRAL FLORIDA EXPRESSWAY AUTHORITY

FY 2014 TOLL REVENUE

SR 408 39%

SR 528 17%

Beltway (417/429

/414) 44%

30

CENTRAL FLORIDA EXPRESSWAY AUTHORITY

% OF ELECTRONIC TRANSACTIONS INCREASED

BY 38% IN PAST 10 YEARS, IMPROVING

EFFICIENCY

Toll Transactions (000s)

31

0

50,000

100,000

150,000

200,000

250,000

300,000

350,000

400,000

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014Fiscal Year

ETC Transactions

Total Transact ions

CENTRAL FLORIDA EXPRESSWAY AUTHORITY

HOW REVENUE IS SPENT (PROJECTED FY 2016)

14%

5%

2%

46%

7%

26%

Operations

Maintenance

Administration

Debt Service

Renewal and Replacement

Available for Projects

32

CENTRAL FLORIDA EXPRESSWAY AUTHORITY

UNPAID TOLL NOTICE (UTN) PROGRAM

CONTINUES TO GROW

33

$1,819,895

$4,216,428

$6,006,815

$8,750,508

$11,150,481

$0.00

$2,000,000.00

$4,000,000.00

$6,000,000.00

$8,000,000.00

$10,000,000.00

$12,000,000.00

UTN Rev FY 2010 UTN Rev FY 2011 UTN Rev FY 2012 UTN Rev FY 2013 UTN Rev FY 2014

* Neither unpaid UTNs nor transactions converted to AVI are included.

CENTRAL FLORIDA EXPRESSWAY AUTHORITY

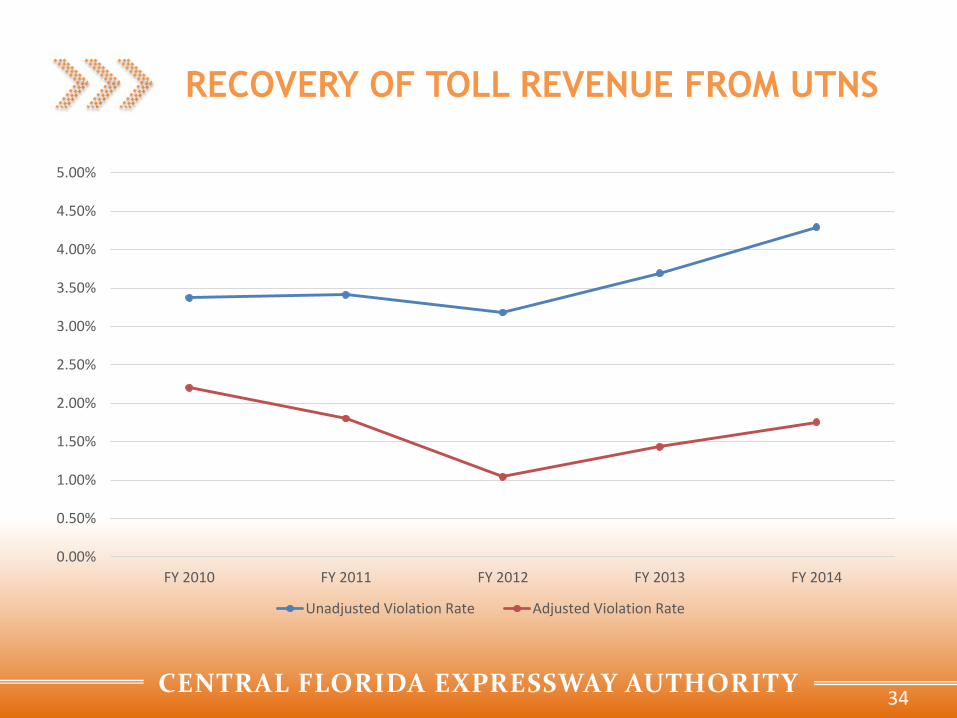

RECOVERY OF TOLL REVENUE FROM UTNS

34

0.00%

0.50%

1.00%

1.50%

2.00%

2.50%

3.00%

3.50%

4.00%

4.50%

5.00%

FY 2010 FY 2011 FY 2012 FY 2013 FY 2014

Unadjusted Violation Rate Adjusted Violation Rate

CENTRAL FLORIDA EXPRESSWAY AUTHORITY

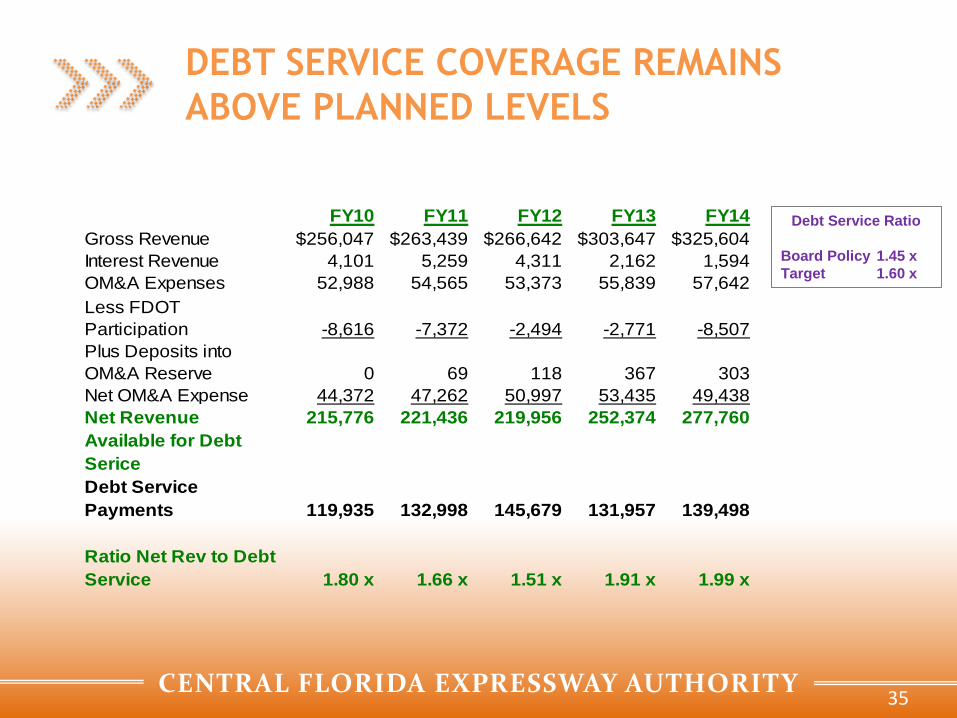

DEBT SERVICE COVERAGE REMAINS

ABOVE PLANNED LEVELS

Debt Service Ratio

Board Policy 1.45 x

Target 1.60 x

35

FY10 FY11 FY12 FY13 FY14

Gross Revenue $256,047 $263,439 $266,642 $303,647 $325,604

Interest Revenue 4,101 5,259 4,311 2,162 1,594

OM&A Expenses 52,988 54,565 53,373 55,839 57,642

Less FDOT

Participation -8,616 -7,372 -2,494 -2,771 -8,507

Plus Deposits into

OM&A Reserve 0 69 118 367 303

Net OM&A Expense 44,372 47,262 50,997 53,435 49,438

Net Revenue

Available for Debt

Serice

215,776 221,436 219,956 252,374 277,760

Debt Service

Payments 119,935 132,998 145,679 131,957 139,498

Ratio Net Rev to Debt

Service

1.80 x

1.66 x

1.51 x 1.91 x 1.99 x

CENTRAL FLORIDA EXPRESSWAY AUTHORITY

CFX HAS A STRONG LIQUIDITY POSITION

• Reserves (as of 3/31/15)

– OM&A $ 7,928,946

– Renewal and Replacement 18,720,183

– Reserve for Swaps 162,545,110

– Unrestricted cash for projects

and operations 295,625,738

$ 484,819,977

36

CENTRAL FLORIDA EXPRESSWAY AUTHORITY

Traffic and Revenue

CENTRAL FLORIDA EXPRESSWAY AUTHORITY

CFX SYSTEM

38

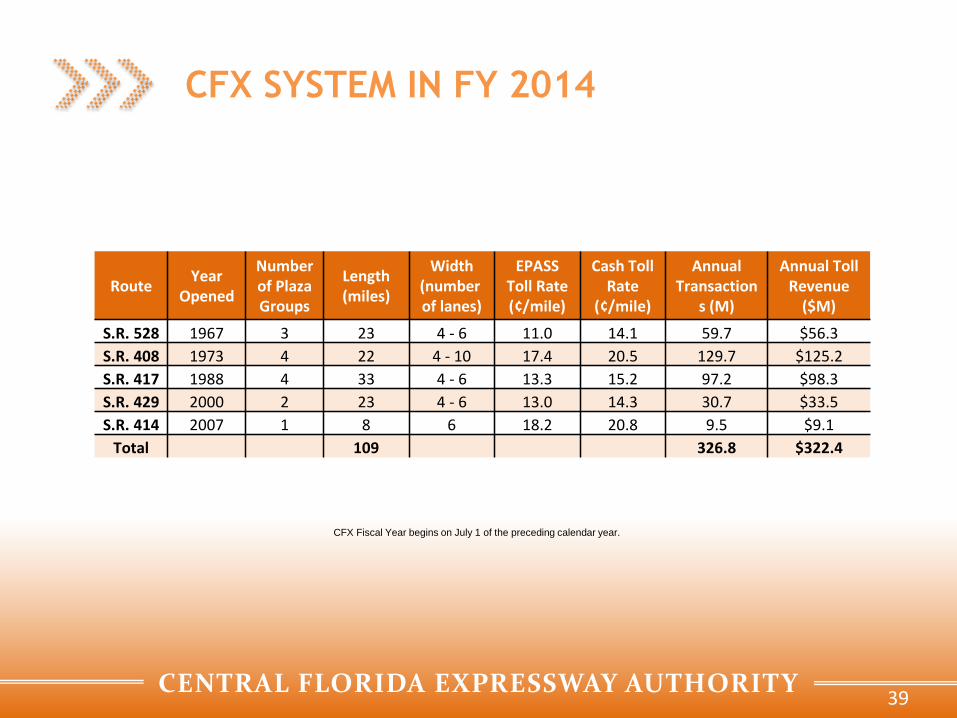

CENTRAL FLORIDA EXPRESSWAY AUTHORITY

CFX Fiscal Year begins on July 1 of the preceding calendar year.

CFX SYSTEM IN FY 2014

39

RouteYear

Opened

Number of Plaza Groups

Length (miles)

Width (numberof lanes)

EPASS Toll Rate (¢/mile)

Cash Toll Rate

(¢/mile)

Annual Transaction

s (M)

Annual Toll Revenue

($M)

S.R. 528 1967 3 23 4 - 6 11.0 14.1 59.7 $56.3

S.R. 408 1973 4 22 4 - 10 17.4 20.5 129.7 $125.2

S.R. 417 1988 4 33 4 - 6 13.3 15.2 97.2 $98.3

S.R. 429 2000 2 23 4 - 6 13.0 14.3 30.7 $33.5

S.R. 414 2007 1 8 6 18.2 20.8 9.5 $9.1

Total 109 326.8 $322.4

CENTRAL FLORIDA EXPRESSWAY AUTHORITY

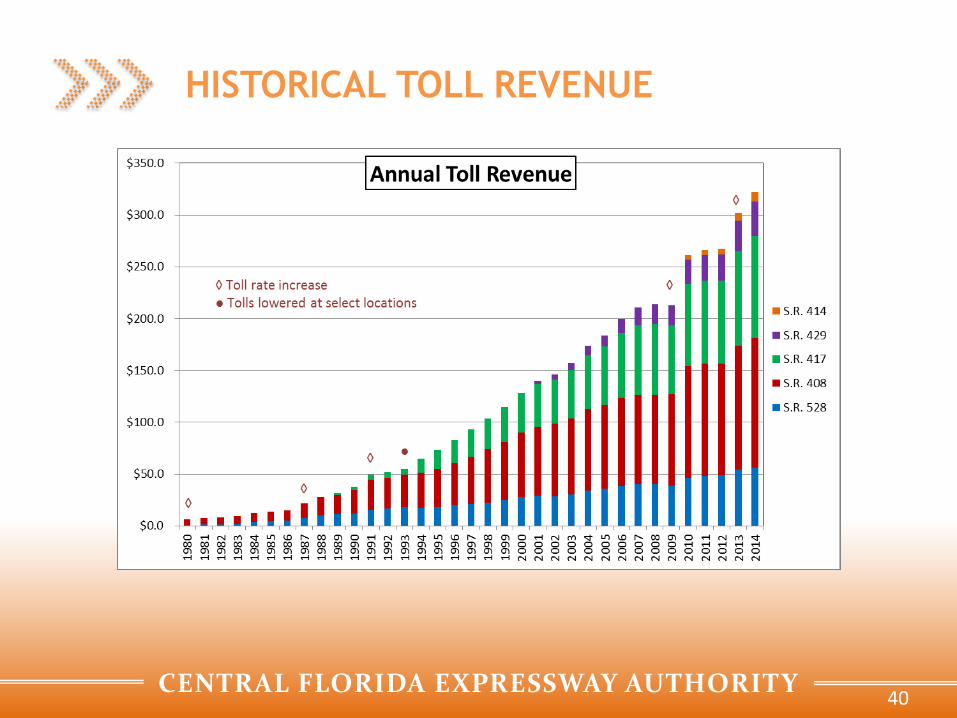

HISTORICAL TOLL REVENUE

40

CENTRAL FLORIDA EXPRESSWAY AUTHORITY

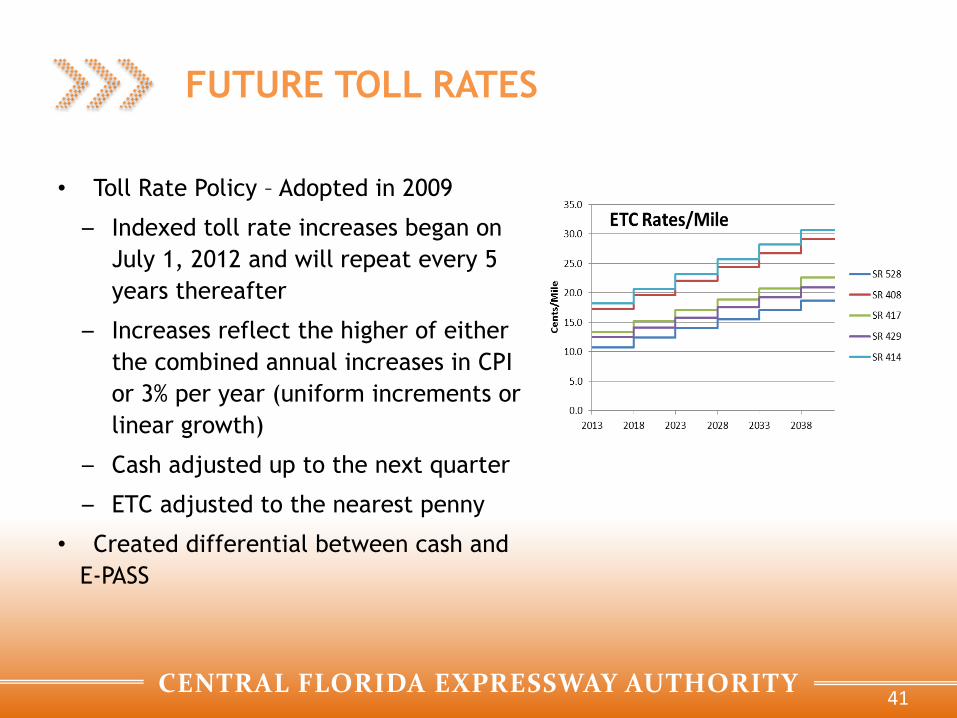

FUTURE TOLL RATES

• Toll Rate Policy – Adopted in 2009

– Indexed toll rate increases began on

July 1, 2012 and will repeat every 5

years thereafter

– Increases reflect the higher of either

the combined annual increases in CPI

or 3% per year (uniform increments or

linear growth)

– Cash adjusted up to the next quarter

– ETC adjusted to the nearest penny

• Created differential between cash and

E-PASS

41

CENTRAL FLORIDA EXPRESSWAY AUTHORITY

DISCOUNT PROGRAMS

• E-PASS transactions receive a volume discount (applied at end of month)

– 5% discount on all transaction is monthly total is between 40 to 80

transactions

– 10% discount on all transactions if the monthly total is more than 80

transactions

– In FY 2014 discount was $11.7 million

• E-PASS transactions on the beltway (SR 417, SR 429 and SR 414) will receive the

I-4 Ultimate Commuter discount

– Additional 5% discount on beltway transactions if the monthly total is 20 or

more transactions

– Limited in duration to six years beginning in FY 2016

– Constrained by overall system performance

– Applies if, and only if, System revenues for the month exceed the forecast

by 2%

42

CENTRAL FLORIDA EXPRESSWAY AUTHORITY

• July 2012 – first indexed toll rate increase – ETC toll rates increased 9% ($0.03 – $0.12)

– Cash toll rates increased $0.25

• Created toll rate differential for E-PASS customers

• E-PASS participation went up 3.4%

• With a 14% increase in toll, S.R. 408 and S.R. 417 had less than 2% reductions in traffic and 12% increases in toll revenue

• S.R. 528 had a change in the toll collection plan, i.e., a new plaza Dallas Main

• S.R. 429 and S.R. 414 had more traffic and revenue (extended to the north)

Toll

Facility Increase Impact Elasticity Impact Elasticity

SR 528 11% 1.3% N/A 12.5% N/A

SR 408 13% -1.8% -0.14 10.8% 0.83

SR 417 14% -1.9% -0.14 12.1% 0.86

SR 429 15% 0.7% N/A 15.3% N/A

SR 414 17% 13.7% N/A 33.6% N/A

Traffic Revenue

2013 TOLL RATE INCREASE

43

CENTRAL FLORIDA EXPRESSWAY AUTHORITY

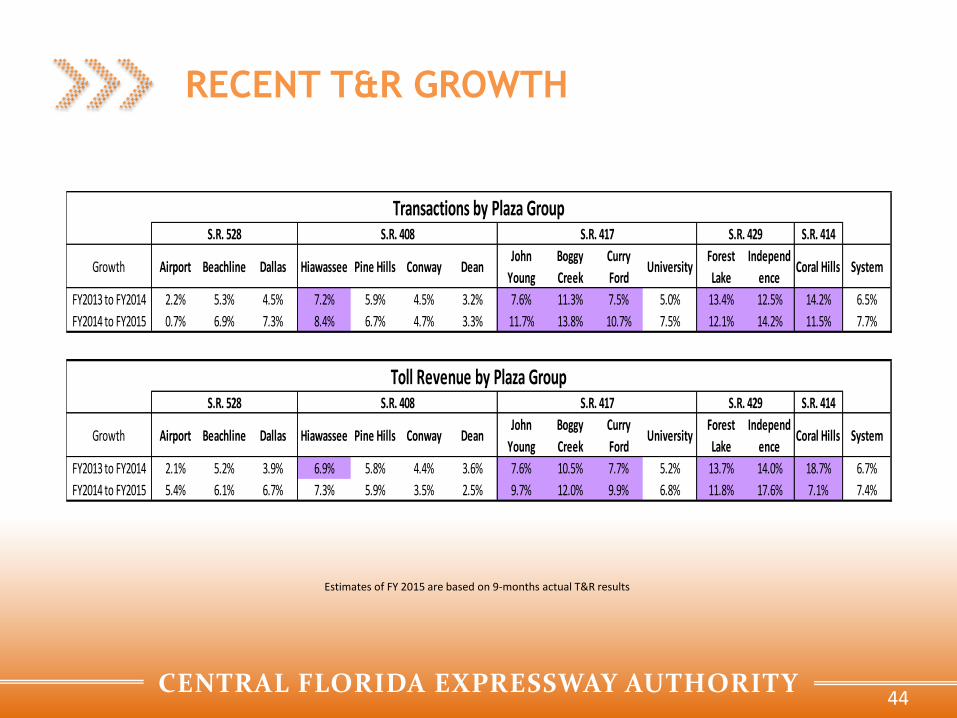

Transactions by Plaza GroupS.R. 528 S.R. 408 S.R. 417 S.R. 429 S.R. 414

Growth Airport Beachline Dallas Hiawassee Pine Hills Conway DeanJohn

Young

Boggy

Creek

Curry

FordUniversity

Forest

Lake

Independ

enceCoral Hills System

FY2013 to FY2014 2.2% 5.3% 4.5% 7.2% 5.9% 4.5% 3.2% 7.6% 11.3% 7.5% 5.0% 13.4% 12.5% 14.2% 6.5%

FY2014 to FY2015 0.7% 6.9% 7.3% 8.4% 6.7% 4.7% 3.3% 11.7% 13.8% 10.7% 7.5% 12.1% 14.2% 11.5% 7.7%

Toll Revenue by Plaza GroupS.R. 528 S.R. 408 S.R. 417 S.R. 429 S.R. 414

Growth Airport Beachline Dallas Hiawassee Pine Hills Conway DeanJohn

Young

Boggy

Creek

Curry

FordUniversity

Forest

Lake

Independ

enceCoral Hills System

FY2013 to FY2014 2.1% 5.2% 3.9% 6.9% 5.8% 4.4% 3.6% 7.6% 10.5% 7.7% 5.2% 13.7% 14.0% 18.7% 6.7%

FY2014 to FY2015 5.4% 6.1% 6.7% 7.3% 5.9% 3.5% 2.5% 9.7% 12.0% 9.9% 6.8% 11.8% 17.6% 7.1% 7.4%

Estimates of FY 2015 are based on 9-months actual T&R results

RECENT T&R GROWTH

44

CENTRAL FLORIDA EXPRESSWAY AUTHORITY

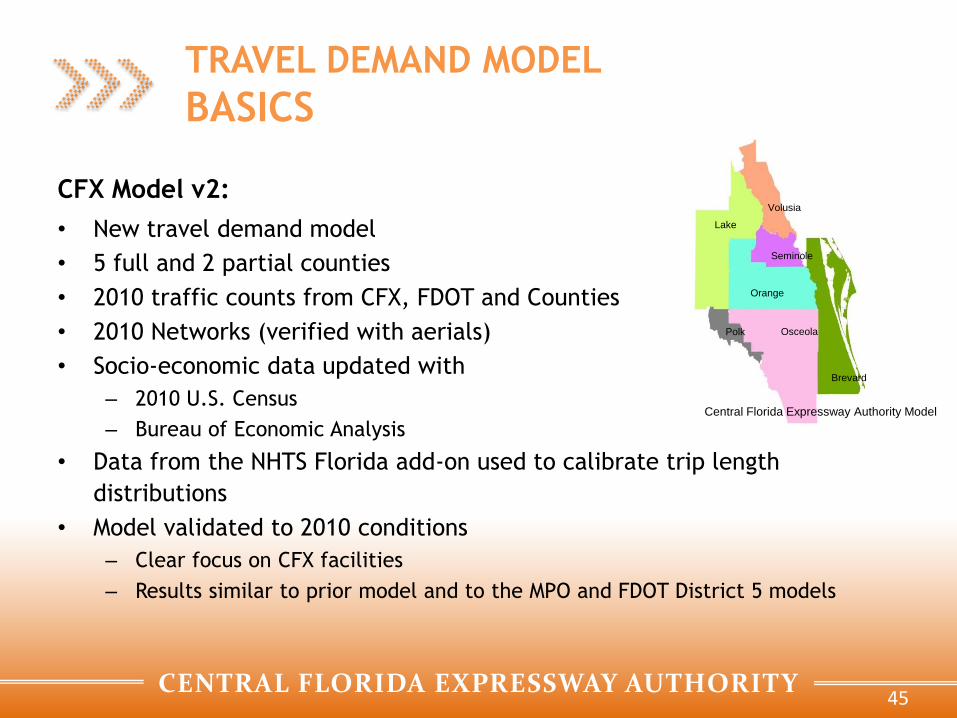

CFX Model v2:

• New travel demand model

• 5 full and 2 partial counties

• 2010 traffic counts from CFX, FDOT and Counties

• 2010 Networks (verified with aerials)

• Socio-economic data updated with

– 2010 U.S. Census

– Bureau of Economic Analysis

• Data from the NHTS Florida add-on used to calibrate trip length

distributions

• Model validated to 2010 conditions

– Clear focus on CFX facilities

– Results similar to prior model and to the MPO and FDOT District 5 models

Orange

Seminole

Brevard

Polk Osceola

Lake

Volusia

Central Florida Expressway Authority Model

TRAVEL DEMAND MODEL

BASICS

45

CENTRAL FLORIDA EXPRESSWAY AUTHORITY

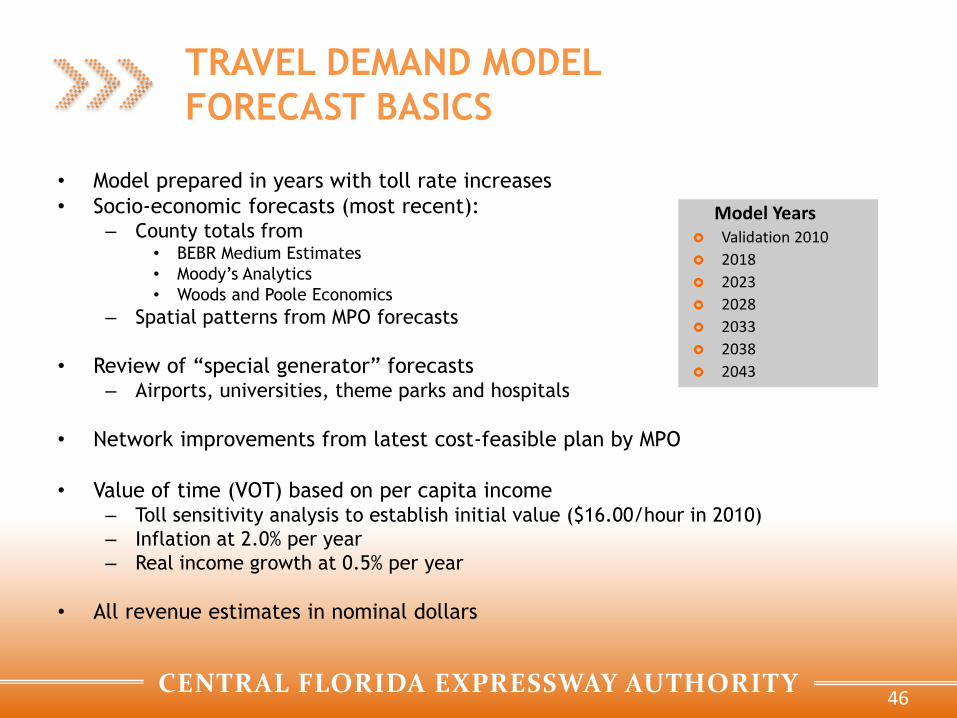

• Model prepared in years with toll rate increases

• Socio-economic forecasts (most recent): – County totals from

• BEBR Medium Estimates

• Moody’s Analytics

• Woods and Poole Economics

– Spatial patterns from MPO forecasts

• Review of “special generator” forecasts – Airports, universities, theme parks and hospitals

• Network improvements from latest cost-feasible plan by MPO

• Value of time (VOT) based on per capita income – Toll sensitivity analysis to establish initial value ($16.00/hour in 2010)

– Inflation at 2.0% per year

– Real income growth at 0.5% per year

• All revenue estimates in nominal dollars

Model Years Validation 2010

2018

2023

2028

2033

2038

2043

TRAVEL DEMAND MODEL

FORECAST BASICS

46

CENTRAL FLORIDA EXPRESSWAY AUTHORITY

REVENUE MODEL FORECAST BASICS

• Revenue model produces annual T&R estimates from

traffic volume estimates out of the travel demand

model

• Revenue model contains a series of adjustment factors

to duplicate transactions by plaza and revenue by

plaza group – Based on 2010 T&R data

– Results are “expected” T&R with violations/leakage excluded

from the start

– Impacts of the revenue recovered from UTNs and the discount

programs are handled separately as a last step in this model

• Taken together: – Travel demand model provides estimates of growth from

changes in the network, land-use and toll rates

– Revenue model ensures the forecast stream is connected to

recent history

47

CENTRAL FLORIDA EXPRESSWAY AUTHORITY

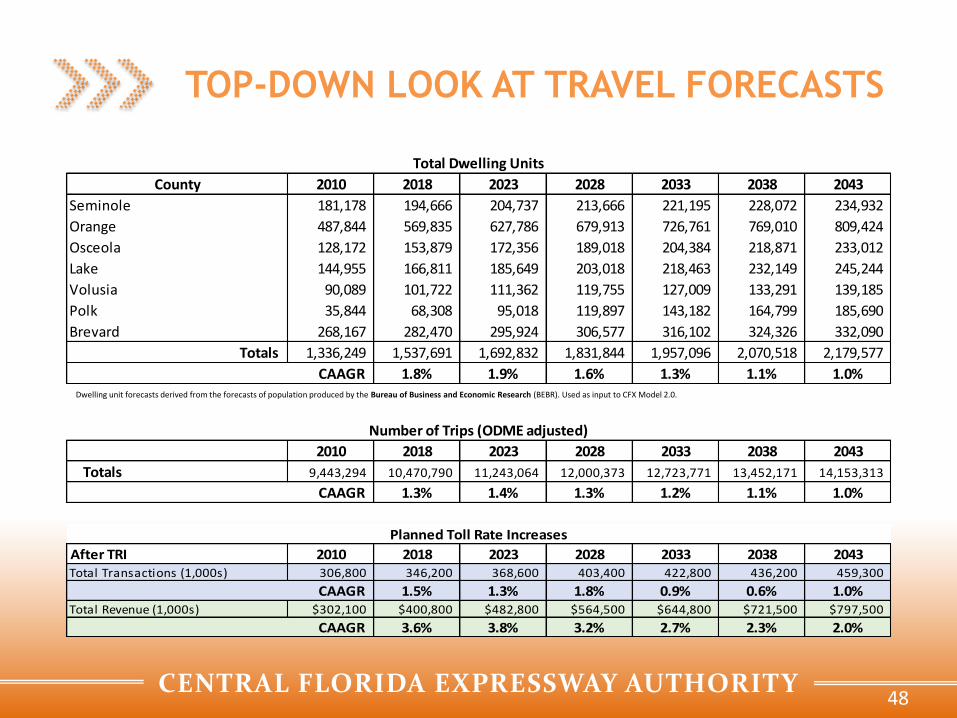

Dwelling unit forecasts derived from the forecasts of population produced by the Bureau of Business and Economic Research (BEBR). Used as input to CFX Model 2.0.

Total Dwelling Units

2010 2018 2023 2028 2033 2038 2043

181,178 194,666 204,737 213,666 221,195 228,072 234,932

487,844 569,835 627,786 679,913 726,761 769,010 809,424

128,172 153,879 172,356 189,018 204,384 218,871 233,012

144,955 166,811 185,649 203,018 218,463 232,149 245,244

90,089 101,722 111,362 119,755 127,009 133,291 139,185

35,844 68,308 95,018 119,897 143,182 164,799 185,690

268,167 282,470 295,924 306,577 316,102 324,326 332,090

1,336,249 1,537,691 1,692,832 1,831,844 1,957,096 2,070,518 2,179,577

1.8% 1.9% 1.6% 1.3% 1.1% 1.0%CAAGR

Volusia

Polk

Brevard

Totals

County

Seminole

Orange

Osceola

Lake

Number of Trips (ODME adjusted)

2010 2018 2023 2028 2033 2038 2043

Totals 9,443,294 10,470,790 11,243,064 12,000,373 12,723,771 13,452,171 14,153,313

1.3% 1.4% 1.3% 1.2% 1.1% 1.0%CAAGR

Planned Toll Rate Increases

After TRI 2010 2018 2023 2028 2033 2038 2043Total Transactions (1,000s) 306,800 346,200 368,600 403,400 422,800 436,200 459,300

CAAGR 1.5% 1.3% 1.8% 0.9% 0.6% 1.0%Total Revenue (1,000s) $302,100 $400,800 $482,800 $564,500 $644,800 $721,500 $797,500

CAAGR 3.6% 3.8% 3.2% 2.7% 2.3% 2.0%

TOP-DOWN LOOK AT TRAVEL FORECASTS

48

CENTRAL FLORIDA EXPRESSWAY AUTHORITY

WEKIVA PARKWAY

49

Development Schedule

Sections 1A and 1BUS 441 through KPROpen 7/1/2017

Sections 2A, 2B and 2CKPR to US 46 and to FDOTOpen 1/1/2018

CENTRAL FLORIDA EXPRESSWAY AUTHORITY

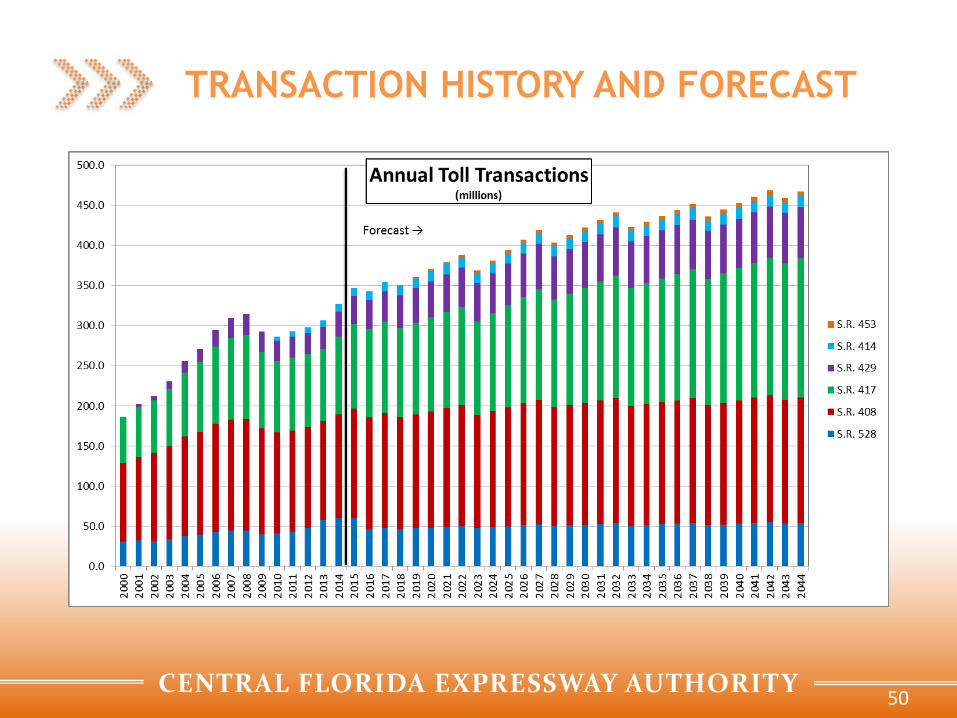

TRANSACTION HISTORY AND FORECAST

50

CENTRAL FLORIDA EXPRESSWAY AUTHORITY

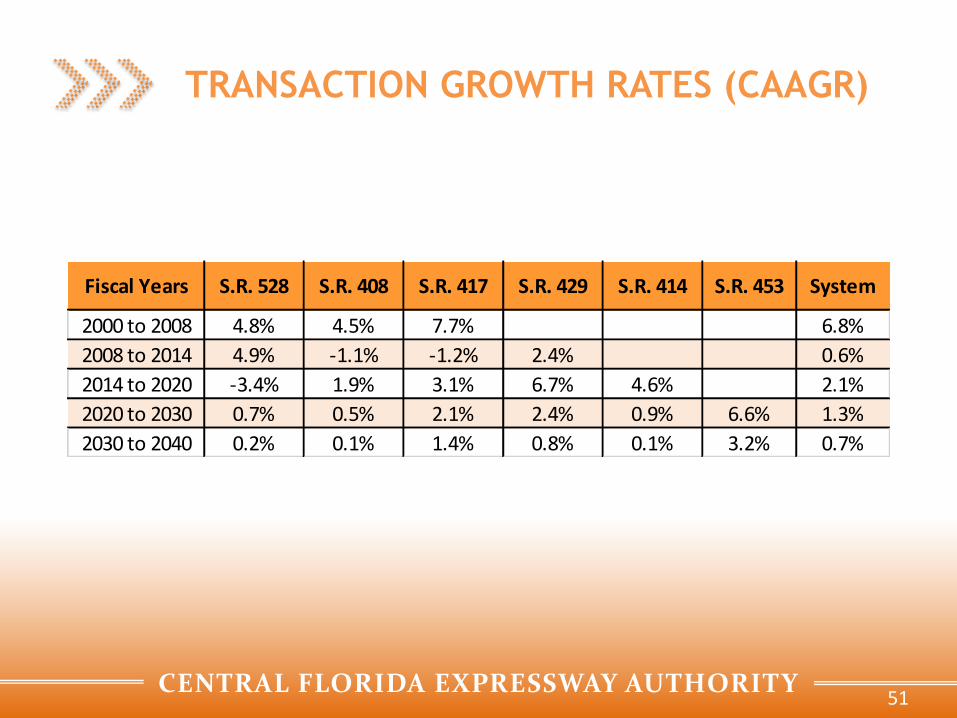

TRANSACTION GROWTH RATES (CAAGR)

51

Fiscal Years S.R. 528 S.R. 408 S.R. 417 S.R. 429 S.R. 414 S.R. 453 System

2000 to 2008 4.8% 4.5% 7.7% 6.8%

2008 to 2014 4.9% -1.1% -1.2% 2.4% 0.6%

2014 to 2020 -3.4% 1.9% 3.1% 6.7% 4.6% 2.1%

2020 to 2030 0.7% 0.5% 2.1% 2.4% 0.9% 6.6% 1.3%

2030 to 2040 0.2% 0.1% 1.4% 0.8% 0.1% 3.2% 0.7%

CENTRAL FLORIDA EXPRESSWAY AUTHORITY

TOLL REVENUE HISTORY AND FORECAST

52

CENTRAL FLORIDA EXPRESSWAY AUTHORITY

TOLL REVENUE GROWTH RATES (CAAGR)

53

Fiscal Years S.R. 528 S.R. 408 S.R. 417 S.R. 429 S.R. 414 S.R. 453 System

2000 to 2008 4.7% 4.1% 7.5% 6.6%

2008 to 2014 5.8% 6.4% 6.2% 9.9% 7.1%

2014 to 2020 5.1% 3.6% 4.6% 8.4% 4.4% 4.8%

2020 to 2030 2.7% 2.6% 3.8% 4.5% 4.1% 9.9% 3.3%

2030 to 2040 2.4% 1.9% 2.8% 2.7% 2.0% 5.4% 2.4%

CENTRAL FLORIDA EXPRESSWAY AUTHORITY

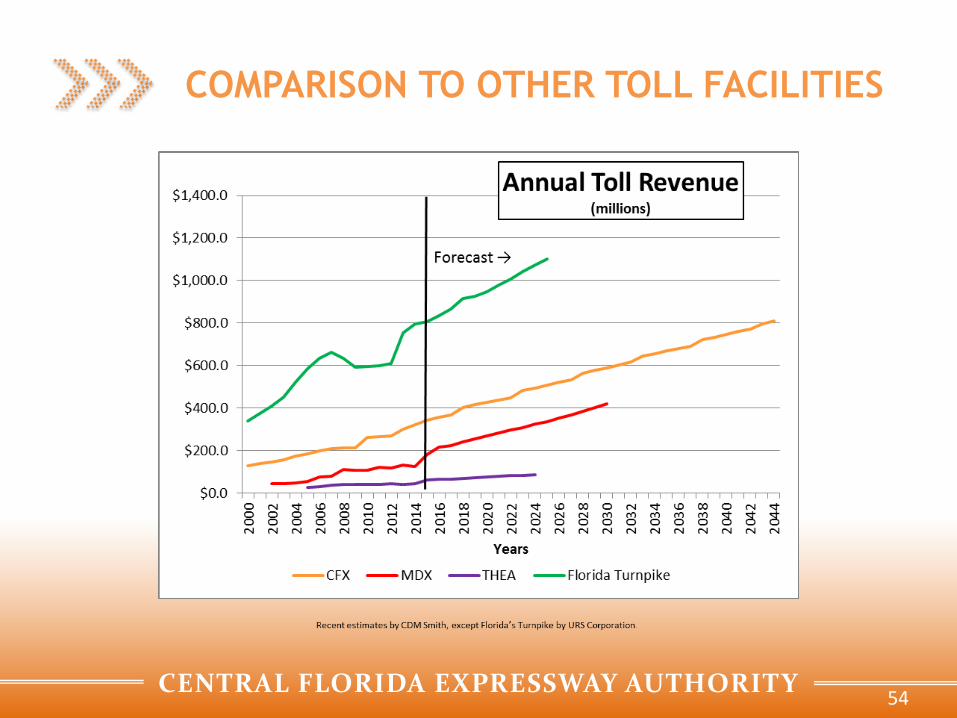

COMPARISON TO OTHER TOLL FACILITIES

54

CENTRAL FLORIDA EXPRESSWAY AUTHORITY

Five-Year Work Plan

CENTRAL FLORIDA EXPRESSWAY AUTHORITY

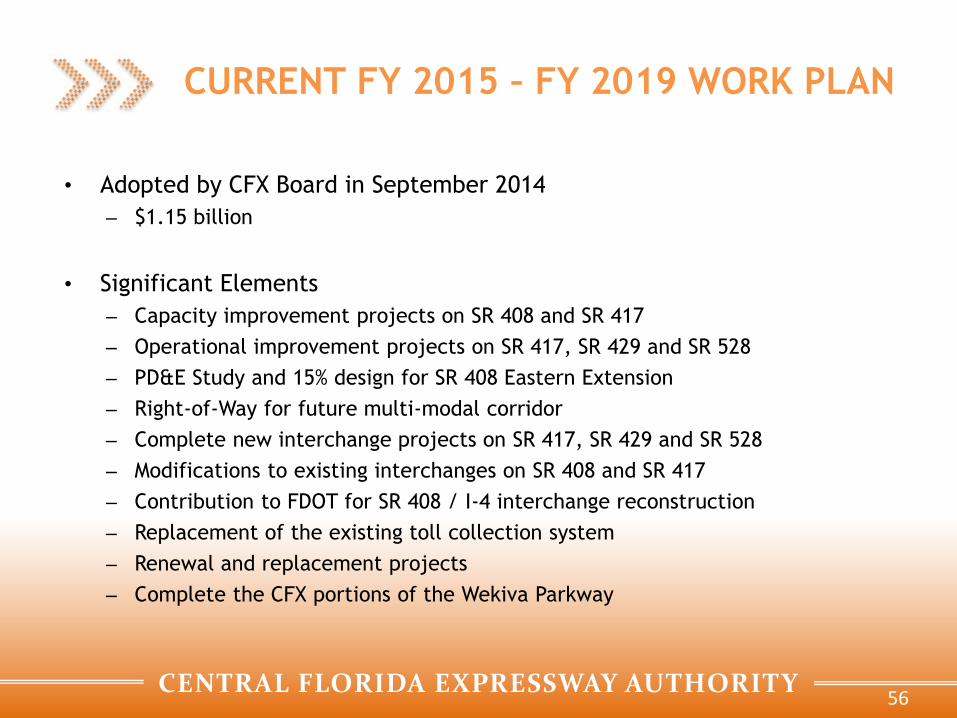

CURRENT FY 2015 – FY 2019 WORK PLAN

• Adopted by CFX Board in September 2014

– $1.15 billion

• Significant Elements

– Capacity improvement projects on SR 408 and SR 417

– Operational improvement projects on SR 417, SR 429 and SR 528

– PD&E Study and 15% design for SR 408 Eastern Extension

– Right-of-Way for future multi-modal corridor

– Complete new interchange projects on SR 417, SR 429 and SR 528

– Modifications to existing interchanges on SR 408 and SR 417

– Contribution to FDOT for SR 408 / I-4 interchange reconstruction

– Replacement of the existing toll collection system

– Renewal and replacement projects

– Complete the CFX portions of the Wekiva Parkway

56

CENTRAL FLORIDA EXPRESSWAY AUTHORITY

CENTRAL FLORIDA EXPRESSWAY

AUTHORITY WORK PLAN PROCESS

Renewal & Replacement Projects

Does Not Meet

Criteria

Intelligent Transportation Systems Projects

Updated Revenue Projections

2030 Master Plan Projects

Draft Five-Year Work Plan

Financial Analysis

Final Five-Year Work Plan

Board Adopts Work Plan

57

CENTRAL FLORIDA EXPRESSWAY AUTHORITY

CURRENT FY 2015 – FY 2019 WORK PLAN

FY 2015 - FY 2019 Work Plan₁

in $ thousands

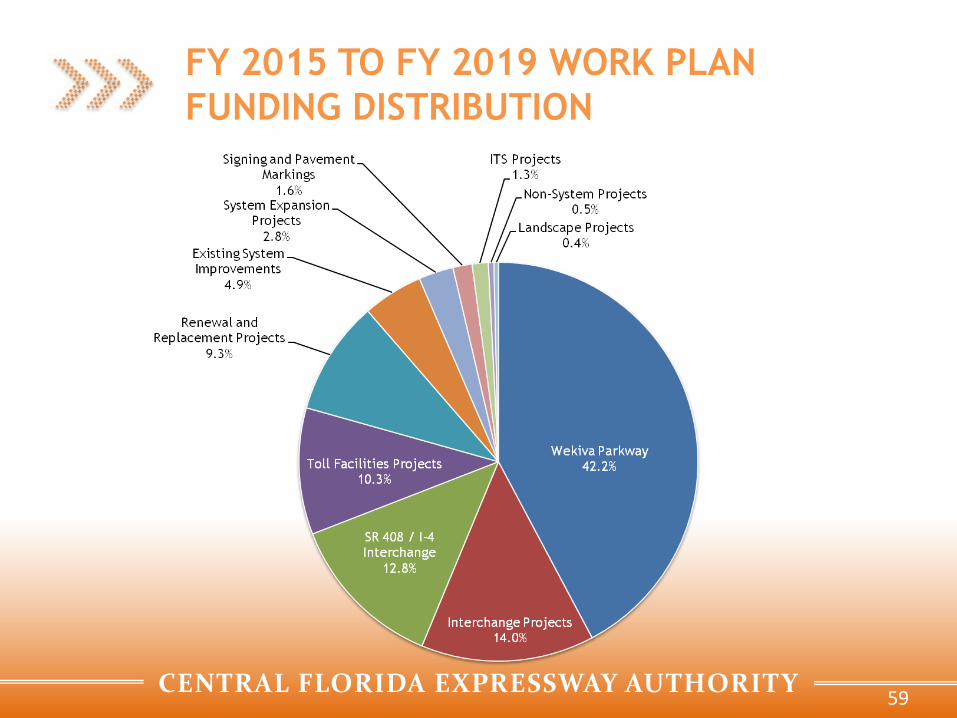

Project FY 2015 FY 2016 FY 2017 FY 2018 FY 2019 Total

Existing System Improvements 12,706 14,061 12,188 811 18,183 57,949

System Expansion Projects 115,323 115,212 42,773 107,593 153,222 534,123

Interchange Projects 84,205 81,575 2,051 75,500 75,500 318,831

Toll Facilities Projects 22,399 32,643 27,930 29,738 8,891 121,601

Intelligent Transportation Systems Projects 6,752 5,458 2,579 171 513 15,473

Renewal and Replacement 26,085 28,438 2,538 3,572 49,310 109,943

Signing and Pavement Marking Projects 7,107 4,749 3,007 1,247 2,289 18,399

Landscaping Projects 1,266 720 750 750 800 4,286

Non-System Project 4,353 - 1,002 - 5,355

Sub - Total 280,196 282,856 93,816 220,384 308,708 1,185,960

Expected Credits2 (30,250) (30,250)

Work Plan Total 249,946 282,856 93,816 220,384 308,708 1,155,710

Notes:

1. Five-Year Work Plan FY 2015 - FY 2019; dated September 11, 2014.

2. Credits for SR 528 / Innovation Way Interchange. Expected credit of $12 million from AAF contribution. Received credits of $11.75 million

from SLR and $6.5 million from Orange County.

58

CENTRAL FLORIDA EXPRESSWAY AUTHORITY

FY 2015 TO FY 2019 WORK PLAN

FUNDING DISTRIBUTION

59

CENTRAL FLORIDA EXPRESSWAY AUTHORITY

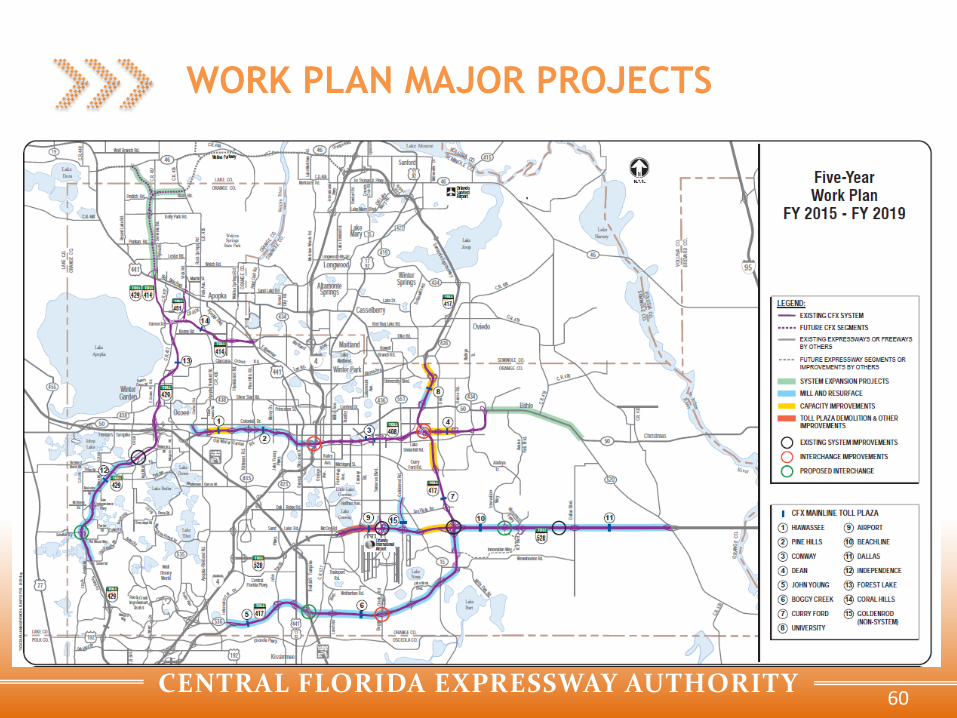

WORK PLAN MAJOR PROJECTS

60

CENTRAL FLORIDA EXPRESSWAY AUTHORITY

PLANNED PROJECTS BEYOND FY 2019

($371 MILLION THRU FY 2024)

• SR 408 / I-4 Interchange

– Critical transportation project

– Central Florida Expressway Authority

contribution for FDOT led project

– $75.5 million in FY 2018

– $75.5 million in FY 2019

– $80.25 million in FY 2020

• SR 408, SR 417 and SR 528 capacity

improvements

• Renewal and Replacement program

61

CENTRAL FLORIDA EXPRESSWAY AUTHORITY

Wekiva Parkway Update

CENTRAL FLORIDA EXPRESSWAY AUTHORITY

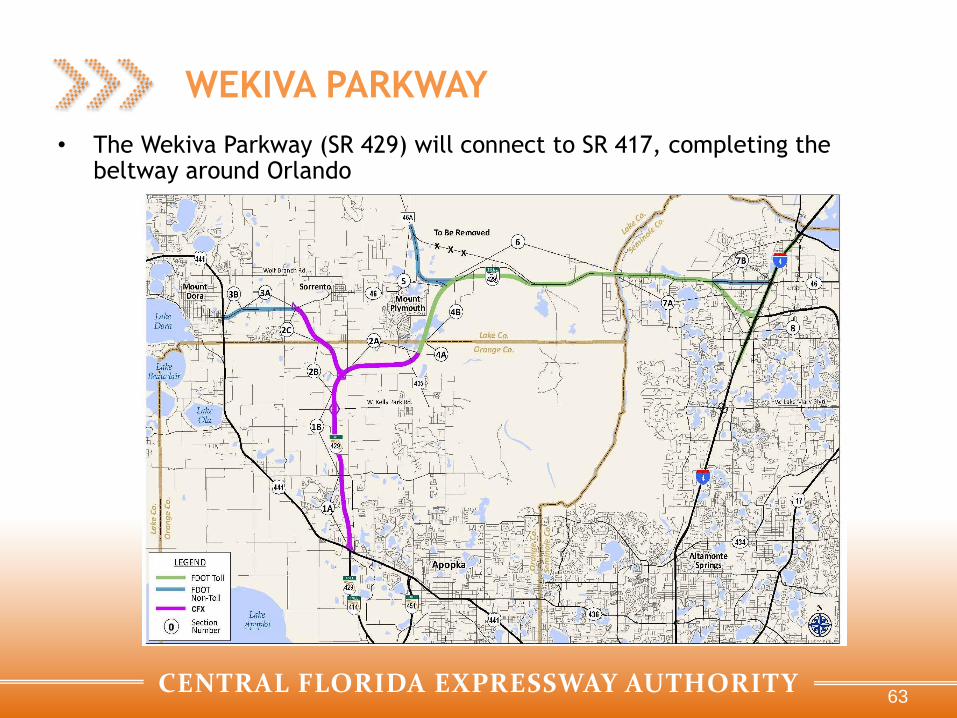

WEKIVA PARKWAY

• The Wekiva Parkway (SR 429) will connect to SR 417, completing the beltway around Orlando

63

CFX

CENTRAL FLORIDA EXPRESSWAY AUTHORITY

WEKIVA PARKWAY PROJECT OVERVIEW

• Estimated $1.6 billion project includes $500 million of non-toll road improvements including:

– Construction of SR 46 as a parallel service road in Lake and Seminole Counties

– Widening four (4) miles of SR 46

– Rebuilding the US 441 / SR 46 interchange in Mount Dora

– Realignment of three (3) miles of CR 46A out of the Seminole State Forest

• Authorized in 2004 by the Wekiva Parkway and Protection Act (Chapter 369, Part III, F.S.), this expressway has been heralded as an example for transportation planning through an environmentally sensitive area – the Wekiva River Basin.

– Development of the Wekiva Parkway has included setting aside more than 3,400 acres of land for conservation.

– The parkway also will include numerous wildlife bridges, and will be largely elevated to reduce accidents between vehicles and wildlife.

64

CENTRAL FLORIDA EXPRESSWAY AUTHORITY

WEKIVA – INTERLOCAL AGREEMENT

• Agreement between FDOT and CFX demonstrating strong project coordination between the parties

• Divides project into sections:

– CFX constructing approximately 10 miles of tolled expressway

– FDOT constructing approximately 17 miles of tolled expressway and non-tolled improvements

– Each agency will own, operate, maintain and collect tolls on their respective sections

– Requires CFX to reimburse FDOT for previous LPA advances in the amount of $20 million per year until final repayment in 2024

– Payments from FDOT of $22 million in 2014 and $6.5 million in both 2016 and 2017 for ROW

– Future bond issues will not enjoy LPA pledge

65

CENTRAL FLORIDA EXPRESSWAY AUTHORITY 66

CENTRAL FLORIDA EXPRESSWAY AUTHORITY

2040 Master Plan Update

CENTRAL FLORIDA EXPRESSWAY AUTHORITY

2040 MASTER PLAN UPDATE

• Establish policies for future decisions:

– Existing system improvements

– Revenue / tolling

– System expansion projects

– Multi-modal transportation role

• Data Collection

– Existing System Traffic

– Pavement Condition Report

– Operations

• Traffic Model Preparation

• Business Leaders, Community Groups and Partner Agency Outreach

68

CENTRAL FLORIDA EXPRESSWAY AUTHORITY

SETTING THE VISION

THEN NOW

Orange County

City of Orlando

Orange County

Lake County

Osceola County

Seminole County

City of Orlando

Limited-access expressway system Limited-access expressway system;

multimodal

109 miles 120 miles (with CFX sections of Wekiva Parkway)

Vision: Defines the optimal desired future state - the mental picture - of

what an organization wants to achieve over time.

69

CENTRAL FLORIDA EXPRESSWAY AUTHORITY

2015 / 2016

SCHEDULE

70

Activity Board Workshops

Documentation Draft Report Final Report

Data Collection / Existing System Needs

Community Outreach and Interviews

Expansion Projects & Multi-Modal Options

Traffic & Revenue and Tolling Analysis

Public Meeting

Identify

April May June July Aug Sept Oct Nov Dec Jan Feb Mar

Evaluate

Draft Plan

CENTRAL FLORIDA EXPRESSWAY AUTHORITY

Debt Management

CENTRAL FLORIDA EXPRESSWAY AUTHORITY

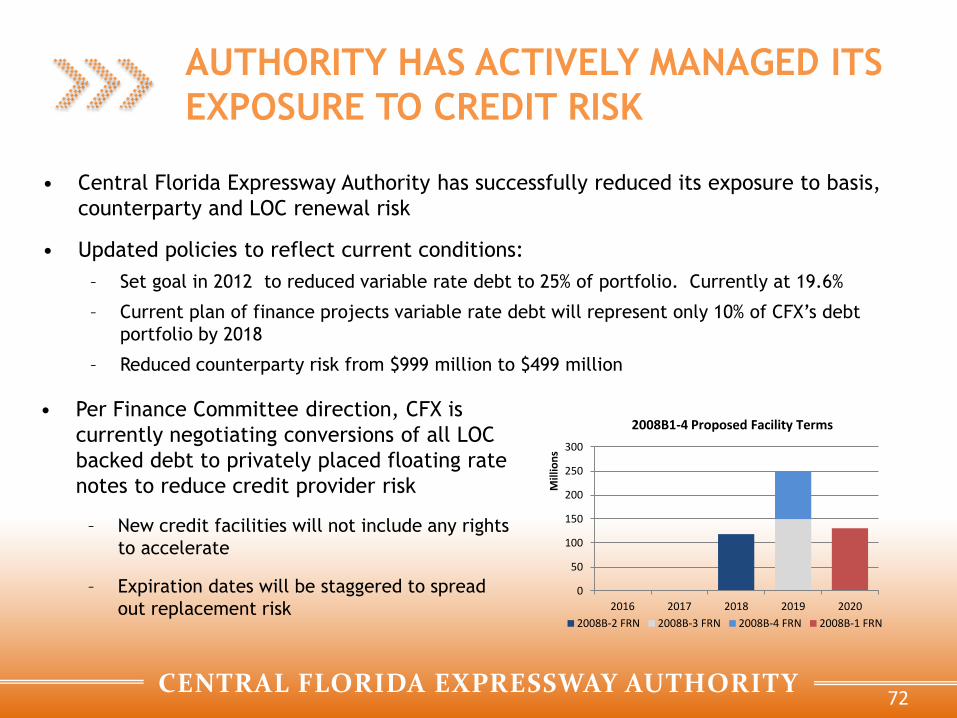

AUTHORITY HAS ACTIVELY MANAGED ITS

EXPOSURE TO CREDIT RISK

• Central Florida Expressway Authority has successfully reduced its exposure to basis,

counterparty and LOC renewal risk

• Updated policies to reflect current conditions:

– Set goal in 2012 to reduced variable rate debt to 25% of portfolio. Currently at 19.6%

– Current plan of finance projects variable rate debt will represent only 10% of CFX’s debt

portfolio by 2018

– Reduced counterparty risk from $999 million to $499 million

72

0

50

100

150

200

250

300

2016 2017 2018 2019 2020

Mill

ion

s

2008B1-4 Proposed Facility Terms

2008B-2 FRN 2008B-3 FRN 2008B-4 FRN 2008B-1 FRN

• Per Finance Committee direction, CFX is

currently negotiating conversions of all LOC

backed debt to privately placed floating rate

notes to reduce credit provider risk

– New credit facilities will not include any rights

to accelerate

– Expiration dates will be staggered to spread

out replacement risk

CENTRAL FLORIDA EXPRESSWAY AUTHORITY

CURRENT SWAP EXPOSURE

73

Snapshot Accrued Interest MTM Value

4/29/2015 ($1,837,288) ($196,985,244)

Bank CounterpartyUBS AG, Stamford

Branch

Citibank, N.A., New

York

Morgan Stanley Capital

Services LLCRoyal Bank of Canada

JPMorgan Chase Bank,

N.A.

Associated

BondsSeries 2008B-1 &

2008B-2

Series 2008B-1 &

2008B-2

Series 2008B-1 &

2008B-2Series 2008B-3 Series 2008B-4

Product Cancellable Swap Swap Swap Swap Swap

Client Pays 4.77530% 4.77530% 4.77530% 4.77530% 4.77530%

Client Receives SIFMA Swap Index SIFMA Swap Index SIFMA Swap Index SIFMA Swap Index SIFMA Swap Index

Trade Date 7/13/2004 7/13/2004 7/13/2004 7/13/2004 7/13/2004

Effective Date 3/1/2005 3/1/2005 3/1/2005 3/1/2005 3/1/2005

Maturity Date 7/1/2040 7/1/2040 7/1/2040 7/1/2040 7/1/2040

MTM Value ($76,392,679) ($60,304,797) ($40,196,816) ($10,045,476) ($10,045,476)

Initial Notional $199,642,000 $149,758,000 $99,821,000 $24,942,000 $24,942,000

Current Notional $199,430,000 $149,598,000 $99,715,000 $24,916,000 $24,916,000

Accrued Interest ($734,915) ($551,280) ($367,458) ($91,817) ($91,817)

Moody's A2 A2 Baa2 Aa3 Aa3

S&P A A A- AA- A+

Fitch A A A AA A+

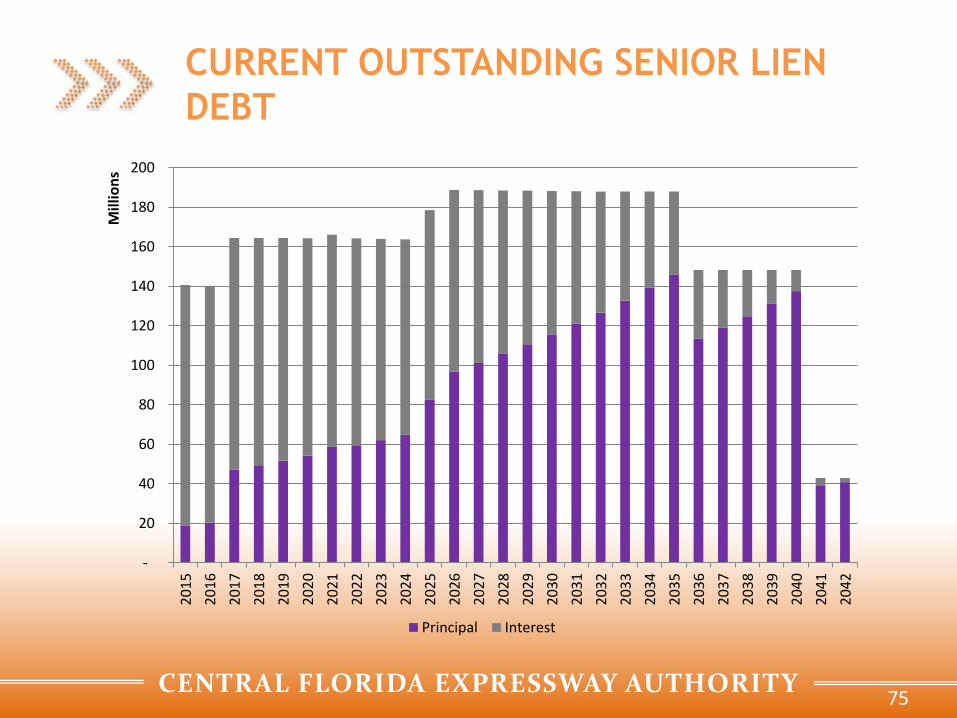

CENTRAL FLORIDA EXPRESSWAY AUTHORITY

CURRENT OUTSTANDING DEBT

74

Outstanding Principal as of March 30, 2015

Outstanding

PrincipalFinal Maturity Type

Remaining

Coupon

Range/Swap

Rate

Remaining

Average

Coupon /

Swap Rate

LC/Liquidity/

FRN Rate

Fee (1)

Remarketing

FeeNet Rate (2)

Net Interest

Cost at

Issuance

Credit

Enhancement

1990 23,655,000 7/1/2016 Natural Fixed 6.00% - 8.25% 6.66% n/a n/a 6.66% 6.67% FGIC

2007A 425,000,000 7/1/2042 Natural Fixed 4.50% - 5.00% 4.90% n/a n/a 4.90% 4.83% FSA

2010A 334,565,000 7/1/2040 Natural Fixed 4.13% - 5.00% 4.98% n/a n/a 4.98% 4.94% uninsured

2010B 180,895,000 7/1/2029 Natural Fixed 3.50% - 5.00% 4.49% n/a n/a 4.53% 4.39% Assured

2010C 283,610,000 7/1/2040 Natural Fixed 4.00% - 5.00% 4.97% n/a n/a 4.97% 4.91% uninsured

2012 201,925,000 7/1/2025 Natural Fixed 3.00% - 5.00% 4.88% n/a n/a 4.88% 2.53% Assured(3)

2012A (sub) 59,060,000 7/1/2025 Natural Fixed 2.37% - 2.37% 2.37% n/a n/a 2.37% 2.37% uninsured

2013A 242,320,000 7/1/2032 Natural Fixed 5.00% - 5.00% 5.00% n/a n/a 5.00% 4.22% uninsured

2013B 173,775,000 7/1/2025 Natural Fixed 3.00% - 5.00% 4.95% n/a n/a 4.95% 2.62% Assured(4)

2013C 107,125,000 7/1/2032 Natural Fixed 3.60% - 3.60% 3.60% n/a n/a 3.60% 3.60% uninsured

SIB Loan (sub) 4,522,714 10/1/2017 Natural Fixed 1.25% 1.25% n/a n/a 1.25% 1.25% uninsured

2,036,452,714 % of Total Debt 80.33%

2008B-1 130,870,000 7/1/2040 Synthetic Fixed 4.78% 4.78% 0.65% 0.07% 5.50% 4.78% uninsured

2008B-2 118,335,000 7/1/2040 Synthetic Fixed 4.78% 4.78% 0.55% 0.07% 5.40% 4.78% uninsured

2008B-3 149,655,000 7/1/2040 Synthetic Fixed 4.78% 4.78% 0.675% 0.00% 5.45% 4.78% uninsured

2008B-4 99,715,000 7/1/2040 Synthetic Fixed 4.78% 4.78% 0.675% 0.00% 5.45% 4.78% uninsured

498,575,000 % of Total Debt 19.67%

TOTAL 2,535,027,714

(1) Does not include additional fee for interest component or day count method.

(2) Net rate is reflective of coupon and on-going fees only. Net rate does not take into account original issue yields.

(3) Assured insured $57,245,000 of the total bonds for maturities in 2024 and 2025.

(4)Assured insured $49,860,000 of the 2022 through 2025 maturities.

(5) CFX also has a contractual obligation through a lease purchase agreement with FDOT to pay $187 million.

Series

SUBTOTAL

SUBTOTAL

CENTRAL FLORIDA EXPRESSWAY AUTHORITY

CURRENT OUTSTANDING SENIOR LIEN

DEBT

75

-

20

40

60

80

100

120

140

160

180

2002

01

5

20

16

20

17

20

18

20

19

20

20

20

21

20

22

20

23

20

24

20

25

20

26

20

27

20

28

20

29

20

30

20

31

20

32

20

33

20

34

20

35

20

36

20

37

20

38

20

39

20

40

20

41

20

42

Mill

ion

s

Principal Interest

CENTRAL FLORIDA EXPRESSWAY AUTHORITY

Plan of Finance

CENTRAL FLORIDA EXPRESSWAY AUTHORITY

PLAN OF FINANCE

• CFX plans to fund its portions of the Wekiva Parkway along with the SR 408/I-4

Ultimate project through the issuance of $216 million senior lien revenue bonds

and a $193.6 million junior (2nd) lien TIFIA loan

– Senior lien BANs expected to be issued in July 2015 to fund $154 MM of project costs which

will be taken out in FY 2019 with the proceeds from a junior lien TIFIA loan

– Additional project costs will be funded by a FY 2017 senior lien bond issuance of $49

million and a FY 2019 senior lien bond issuance of $172 million.

– CFX will fund $307 million of Wekiva project costs from Pay-Go cash

• Senior lien coverage ratio is projected to be at or above 1.60x in all years and

second lien coverage is projected to be at or above 1.55x

• Reserve for Debt Management of $160 million

77

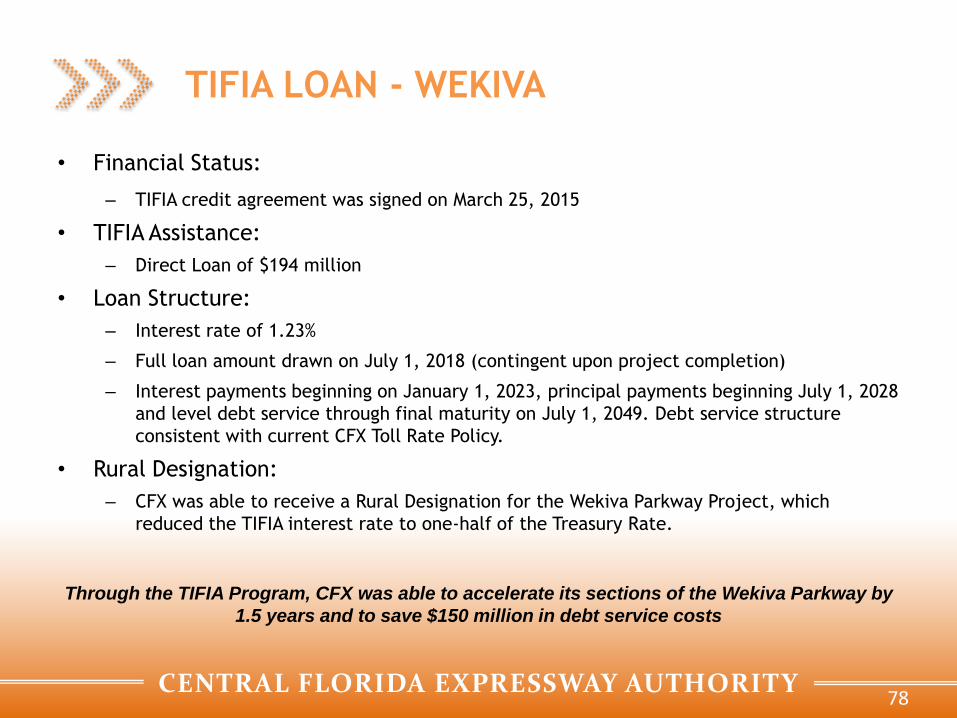

CENTRAL FLORIDA EXPRESSWAY AUTHORITY

TIFIA LOAN - WEKIVA

• Financial Status:

– TIFIA credit agreement was signed on March 25, 2015

• TIFIA Assistance:

– Direct Loan of $194 million

• Loan Structure:

– Interest rate of 1.23%

– Full loan amount drawn on July 1, 2018 (contingent upon project completion)

– Interest payments beginning on January 1, 2023, principal payments beginning July 1, 2028

and level debt service through final maturity on July 1, 2049. Debt service structure

consistent with current CFX Toll Rate Policy.

• Rural Designation:

– CFX was able to receive a Rural Designation for the Wekiva Parkway Project, which

reduced the TIFIA interest rate to one-half of the Treasury Rate.

Through the TIFIA Program, CFX was able to accelerate its sections of the Wekiva Parkway by

1.5 years and to save $150 million in debt service costs

78

CENTRAL FLORIDA EXPRESSWAY AUTHORITY

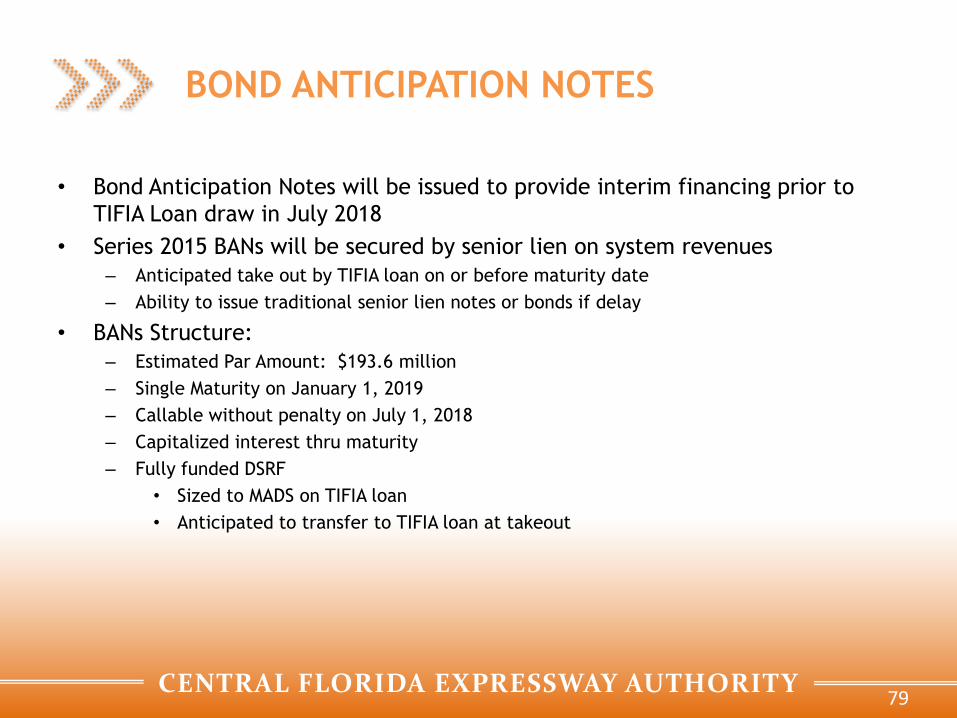

BOND ANTICIPATION NOTES

• Bond Anticipation Notes will be issued to provide interim financing prior to

TIFIA Loan draw in July 2018

• Series 2015 BANs will be secured by senior lien on system revenues

– Anticipated take out by TIFIA loan on or before maturity date

– Ability to issue traditional senior lien notes or bonds if delay

• BANs Structure:

– Estimated Par Amount: $193.6 million

– Single Maturity on January 1, 2019

– Callable without penalty on July 1, 2018

– Capitalized interest thru maturity

– Fully funded DSRF

• Sized to MADS on TIFIA loan

• Anticipated to transfer to TIFIA loan at takeout

79

CENTRAL FLORIDA EXPRESSWAY AUTHORITY

COVERAGE RATIOS REMAIN STRONG

• Senior Lien Planning Coverage Ratio target of 1.60x

• Senior Lien Policy Ratio is 1.45x

• Junior Lien Planning Coverage Ratio target of 1.50x

• CFX bond covenants require coverage of 1.20x

80

Debt Service and Debt Service Coverage Ratio

in $ thousands 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025 2026 2027

Existing System Revenues (CDMSmith FY2014 T&E April 2015) 338,000 345,800 356,000 389,400 400,500 410,600 420,600 439,500 471,700 483,500 495,300 507,100 518,900

Pledged Revenues 283,848 282,350 290,868 316,151 324,709 331,573 338,205 353,615 382,151 390,265 398,321 406,296 414,115

Net Debt Service 142,086 143,308 172,376 172,376 184,774 184,706 186,373 187,218 186,979 186,705 201,426 211,582 210,984

Net Senior Lien Debt Service 140,281 139,797 167,427 167,432 179,838 179,767 181,458 182,316 182,091 181,819 196,569 206,735 206,643

Net Second Lien Debt Service (SIB & TIFIA) 10,188 2,513 1,031 1,075 - - - - 2,501 2,501 11,187 2,501 2,501

General Reserve Fund Obligations 1,400 1,400 6,645 6,890 7,147 7,415 5,703 7,738 8,042 8,350 - - -

LPA Payments 20,000 20,000 20,000 20,000 20,000 20,000 20,000 20,000 20,000 7,000 - - -

Total Aggregate Debt Service 174,047 167,220 200,052 200,341 211,921 212,121 212,076 214,956 217,522 204,555 212,613 214,083 213,485

Resolution Coverage Ratio - Senior 2.02 2.02 1.74 1.89 1.81 1.84 1.86 1.94 2.10 2.15 2.03 1.97 2.00

Junior Lien Coverage Including TIFIA 1.86 1.93 1.67 1.82 1.75 1.79 1.81 1.88 2.01 2.06 1.95 1.89 1.94

Total Debt Service Coverage Ratio (Incl. LPA) 1.63 1.69 1.45 1.58 1.53 1.56 1.59 1.65 1.76 1.91 1.87 1.90 1.94

in $ thousands 2028 2029 2030 2031 2032 2033 2034 2035 2036 2037 2038 2039 2040

Existing System Revenues (CDMSmith FY2014 T&E April 2015) 548,000 559,800 571,400 583,100 594,800 622,400 633,100 643,700 654,400 665,000 692,300 703,700 714,900

Pledged Revenues 439,074 446,586 453,724 460,779 467,642 490,207 495,694 500,861 505,899 510,676 531,903 537,002 541,631

Net Debt Service 210,368 209,639 209,303 208,943 208,582 208,377 208,138 207,879 167,926 167,676 167,379 167,066 166,737

Net Senior Lien Debt Service 206,550 206,413 206,275 206,122 205,973 206,005 206,007 206,002 166,313 166,349 166,348 166,347 166,345

Net Second Lien Debt Service (SIB & TIFIA) 10,605 10,605 10,605 10,605 10,605 10,605 10,605 10,605 10,605 10,605 10,605 10,605 10,605

General Reserve Fund Obligations - - - - - - - - - - - - -

LPA Payments - - - - - - - - - - - - -

Total Aggregate Debt Service 221,491 220,761 220,425 220,064 219,703 219,498 219,258 218,999 179,046 178,756 178,458 178,145 177,816

Resolution Coverage Ratio - Senior 2.13 2.16 2.20 2.24 2.27 2.38 2.41 2.43 3.04 3.07 3.20 3.23 3.26

Junior Lien Coverage Including TIFIA 1.98 2.02 2.06 2.09 2.13 2.23 2.26 2.29 2.83 2.86 2.98 3.01 3.05

Total Debt Service Coverage Ratio (Incl. LPA) 1.98 2.02 2.06 2.09 2.13 2.23 2.26 2.29 2.83 2.86 2.98 3.01 3.05

CENTRAL FLORIDA EXPRESSWAY AUTHORITY

CURRENT WORK PLAN DEBT SERVICE

81

-

100

200

300

400

500

600

700

800

900

20

15

20

16

20

17

20

18

20

19

20

20

20

21

20

22

20

23

20

24

20

25

20

26

20

27

20

28

20

29

20

30

20

31

20

32

20

33

20

34

20

35

20

36

20

37

20

38

20

39

20

40

20

41

20

42

20

43

20

44

20

45

20

46

20

47

20

48

20

49

Mill

ion

s

Senior Lien Debt Service Proposed Series 2016 Proposed Series 2018

Proposed Series 2021 Junior Lien TIFIA Loan Available System RevenuesCDMSmith FY2014 T&E April 2015

CENTRAL FLORIDA EXPRESSWAY AUTHORITY

Summary

CENTRAL FLORIDA EXPRESSWAY AUTHORITY

CENTRAL FLORIDA EXPRESSWAY

AUTHORITY KEY CREDIT DRIVERS • Strong economic base with increased tourism and theme park expansions; service area continues

to diversify with growth in healthcare and education

– Orange County Tourist Development Tax Revenue Bonds rated: AA- / A1 / A+

– Orange County Sales Tax Revenue Bonds rated: AA+ / Aa2 / AA

• Central Florida Expressway Authority’s management of the system and toll rates, together with a

vibrant regional economy, has produced 20 years of revenue growth even through national

recessions

• Excellent condition of the System; Conservative approach towards defining work program;

Competitive toll rates, indexed to inflation, with limited competition; Low cost of toll collections

• Significantly reduced swap exposure & Letter of Credit renewal risk

• Total projected additional senior lien revenue bonds issuance has been reduced due to savings

from the approval of a subordinate TIFIA loan of $193.6 million with no “springing lien”

• Strong debt service coverage and liquidity position provides significant bondholder protections

– As of 7-1-2018, Central Florida Expressway Authority forecasts combined reserve (senior lien DSRF, TIFIA

reserve, debt management reserve and general reserve) balances of $359 million

83