cenvat credit some issues

TRANSCRIPT

V S Datey

Cenvat Credit – Some Issues

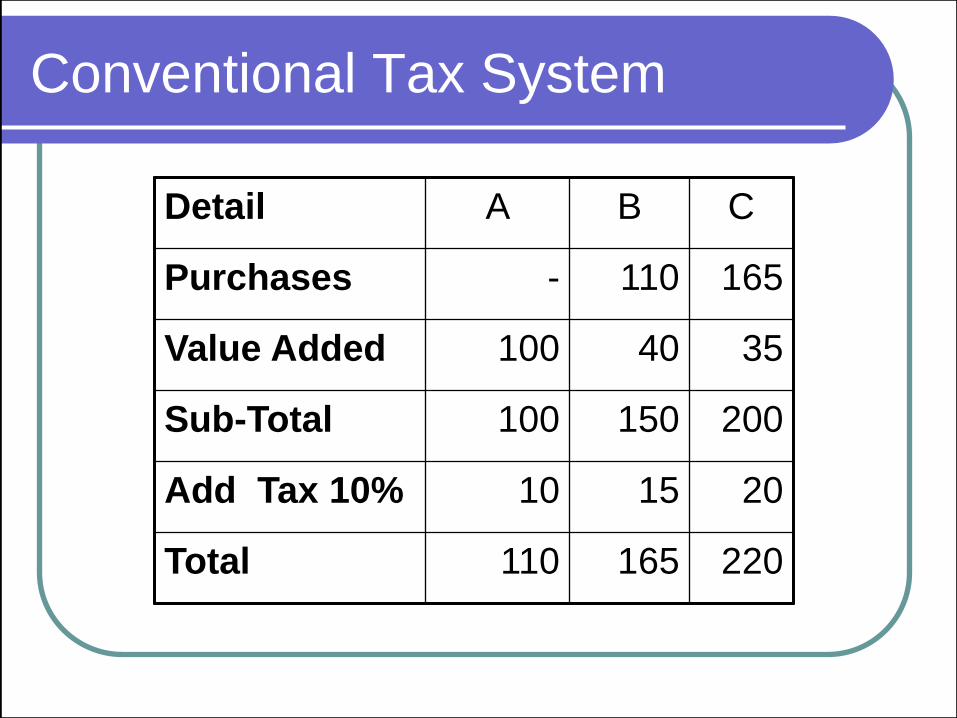

Conventional Tax System

Detail A B C

Purchases - 110 165

Value Added 100 40 35

Sub-Total 100 150 200

Add Tax 10% 10 15 20

Total 110 165 220

Tax credit System under Vat

Transaction without VAT Transaction With VAT

Details A B A B

Purchases - 110 - 100

Value

Added 100 40 100 40

Subtotal 100 150 100 140

Add Tax 10 15 10 14

Total 110 165 110 154

Highlights

Instant Credit

One to one co-relation not required in

Vat/Cenvat

Credit of excise duty on inputs and capital

goods and service tax on input services.

The credit is inter-changeable, except that

credit of education cess and SAHE cess for

education cess and SAHE cess only

Utilisation of Cenvat Credit

All taxes and duties specified in rule 3(1)

of Cenvat Credit Rules form a „pool‟. This

credit can be utilised by manufacturer of

excisable goods or provider of taxable

service, for payment of any tax or duty

as specified in rule 3(4) of Cenvat Credit

Rules

One to one relation not required

Eligible duty paying documents

Original or Duplicate Invoice, Dealer‟s

Invoice, Bill of Entry, Supplementary

Invoice, Railway certificate

Xerox not permitted. Endorsed

Invoice/Bill of Entry permissible

Defect in document – Permission of

AC/DC required to avail Cenvat Credit

Duty paying document valid for 6

months

Duty paying document valid only for 6

months w.e.f. 1-9-2014

Provision applies to earlier invoices also

Problems – (a) Goods returned for re-

work (b) Invoices not passed due to

disputes (c) Demands for past periods

Provision can be challenged

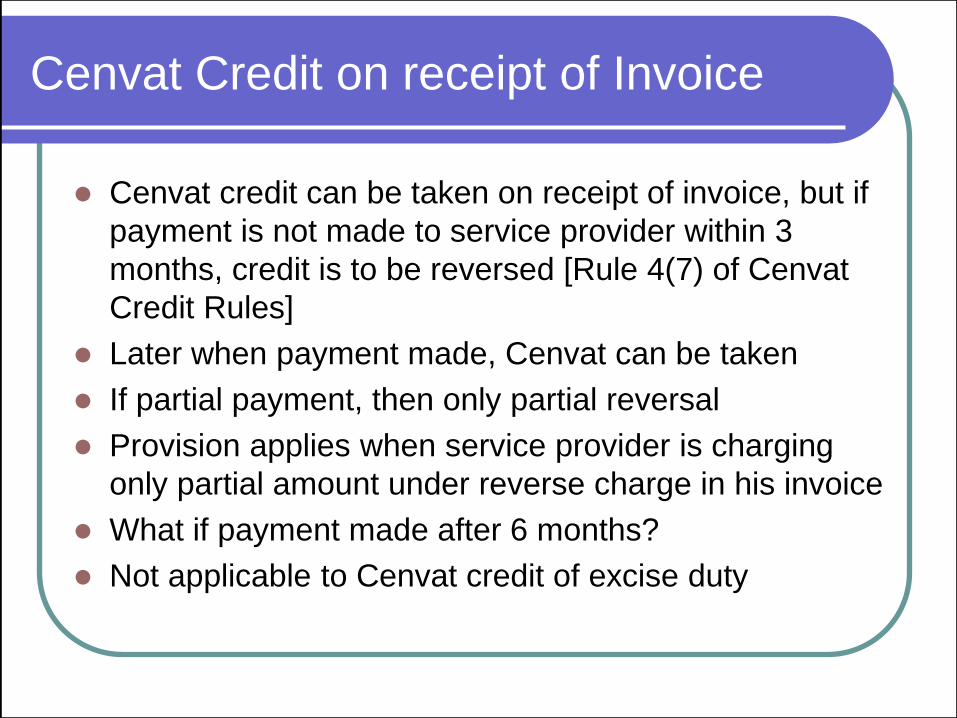

Cenvat Credit on receipt of Invoice

Cenvat credit can be taken on receipt of invoice, but if

payment is not made to service provider within 3

months, credit is to be reversed [Rule 4(7) of Cenvat

Credit Rules]

Later when payment made, Cenvat can be taken

If partial payment, then only partial reversal

Provision applies when service provider is charging

only partial amount under reverse charge in his invoice

What if payment made after 6 months?

Not applicable to Cenvat credit of excise duty

Cenvat Credit in case of reverse charge

When 100% tax payable by service receiver, Cenvat

Credit can be taken after payment of service tax to

government, even if no payment made to service

provider

When partial reverse charge applies, service receiver

liable to pay his portion of service tax to Government,

even if no payment is made to service provider within

three months – even then he can take Cenvat credit

only after making payment to service provider - unfair

What if payment made to service provider after 6

months as GAR-7 challan will be more than 6 months

old

Inputs for manufacturer

All goods used in factory by

manufacturer having some relation with

manufacture are eligible

Accessories and warranty spares

supplied along with main final product

Power generation for captive

consumption

Inputs for service provider

Definition restricted

Only inputs used for providing taxable

services eligible

Consumable eligible

If property in inputs transferred to buyer

– not eligible for Cenvat

Ineligible Inputs

Goods on which 1%/2% excise duty is paid [proviso to

rule 3(i) nt eligilbe

Goods (and services) used for civil construction not

eligible except when used for construction itself

Canteen food (and services), goods for personal use

not eligible

Goods having no relation with manufacture not eligible

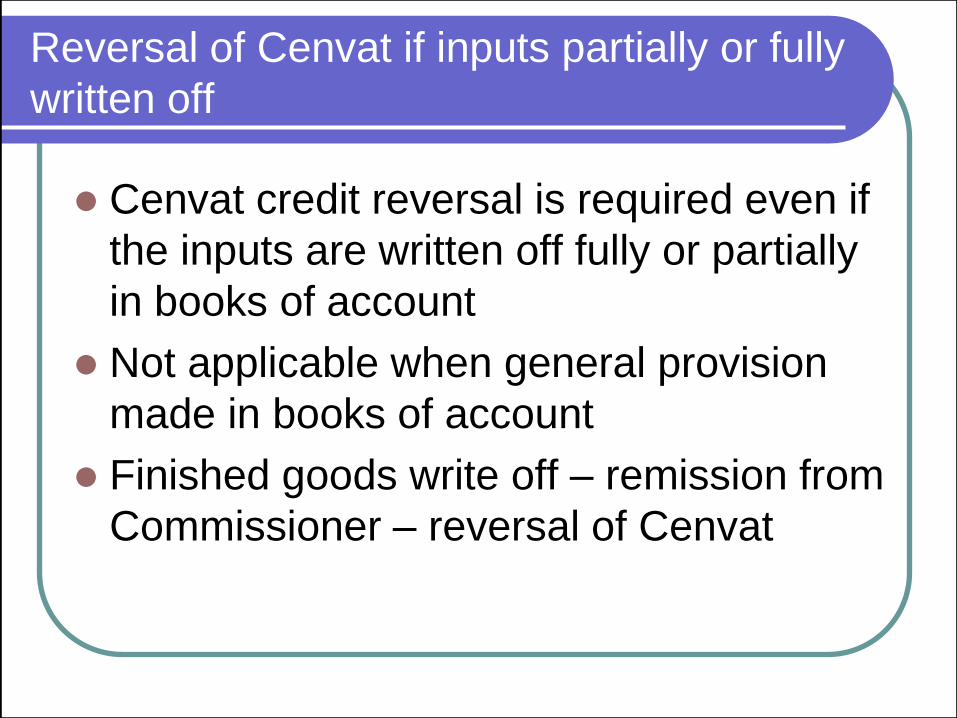

Reversal of Cenvat if inputs partially or fully

written off

Cenvat credit reversal is required even if

the inputs are written off fully or partially

in books of account

Not applicable when general provision

made in books of account

Finished goods write off – remission from

Commissioner – reversal of Cenvat

Capital Goods

Capital goods (machinery, plant, spare parts of

machinery, tools, dies, etc. ) as defined in rule 2(a),

used for manufacture of final product and/or used for

providing output taxable service will be available.

Capital goods should be used in the factory. Capital

goods used outside the factory for generation of

electricity for captive use within the factory eligible

50% credit is available in current year and balance in

subsequent financial year or years, except in case of

SSI

Assessee should not claim depreciation on duty

portion on which he has availed Cenvat credit

Capital Goods

Only those defined as capital goods eligible –

check chapter heads

Steel, cement for construction not eligible

Spare parts, components, tools covered under

the definition though normally not capitalised in

books of account

If not covered under capital goods, may be

eligible as input if has some relation with

manufacture

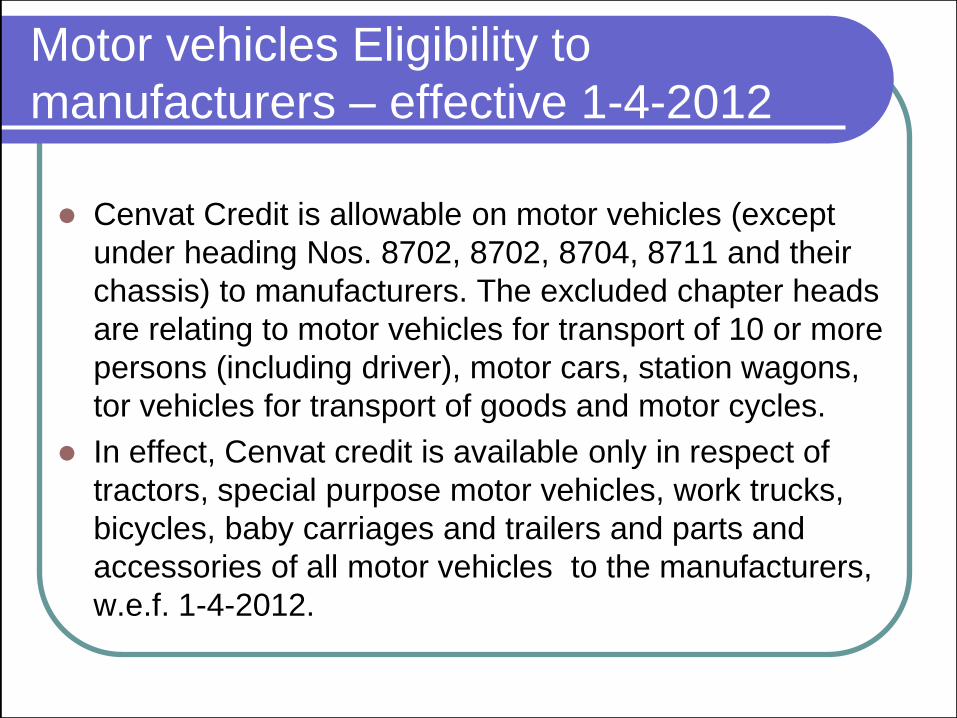

Motor vehicles Eligibility to

manufacturers – effective 1-4-2012

Cenvat Credit is allowable on motor vehicles (except

under heading Nos. 8702, 8702, 8704, 8711 and their

chassis) to manufacturers. The excluded chapter heads

are relating to motor vehicles for transport of 10 or more

persons (including driver), motor cars, station wagons,

tor vehicles for transport of goods and motor cycles.

In effect, Cenvat credit is available only in respect of

tractors, special purpose motor vehicles, work trucks,

bicycles, baby carriages and trailers and parts and

accessories of all motor vehicles to the manufacturers,

w.e.f. 1-4-2012.

Cenvat Credit of Motor Vehicles

to Service Providers

Cenvat credit of motor vehicles covered

under headings 8702, 8703, 8704 and

8711 and their chassis is available only

to specified service providers like

courier, renting or hire of motor vehicles,

transportation of passengers, motor

driving training schools, transportation of

inputs and capital goods used for

providing an output service

Removal of capital goods after

use

If capital goods are cleared after use as scrap

or second hand goods, an „amount‟ payable by

reducing the original Cenvat credit @ 2.5% per

quarter ( [rule 4(5A)] (Higher reduction in case

of computers)

If excise duty calculated on basis of

transaction value of the old capital goods is

higher, then „amount‟ equal to that duty

payable.

Ineligible Input Services

Rent-a-cab services, insurance of motor vehicles,

repair of motor vehicles not eligible, except where

motor vehicle is eligible as „capital goods‟

Architect and Construction services for building, civil

structure, laying of foundation or structures for capital

goods – except when used for construction itself

Canteen, club membership of employees, insurance of

employees, LTA of employees – not eligible

Services in inclusive part of definition

These relate to procurement, marketing,

administration, accounting, raising of

finance, human resources

All five „resources i.e. M‟ s – Men,

Material, Machines, Money and Minutes

covered

Except services specifically excluded, all

other services should get covered

Wasteful Expenditure as per department

for non-eligibility of Cenvat credit

Open society - Building for office or

factory is a waste

Employees, staff, should travel by public

bus or airplane. Motor vehicle, taxi is

luxury

Employee benefit is a luxury – employ

only casual labour

Zero rated and exempt transactions

Basic principle is that Cenvat credit

available only when tax payable on final

product or output services

In zero rated transaction, tax not payable

on final product, but Credit of input taxes

is available (e.g. exports)

In „exempted transaction‟, tax is not

payable on final product and input credit

is not available

Rule 6 of Cenvat Credit Rules

Rule 6 applies where both exempted

goods and taxable goods are

manufactured or exempted and taxable

services provided

Four Options are available to assessee

Four Options

(1) Maintain separate inventory and accounts

of receipt and use of inputs and input services

used for exempted goods/exempted output

services – Rule 6(2) of Cenvat Credit Rules

(2) Pay amount equal to 6% of value of

exempted goods (if he is „manufacturer‟) and

of value of exempted services (if he is service

provider) – Rule 6(3)(i) as amended w.e.f. 1-4-

2012 (Continued)

Four Options (Continued)

(3) Pay an „amount‟ equal to proportionate

Cenvat credit attributable to exempted final

product/ exempted output services, as

provided in rule 6(3A) – Rule 6(3)(ii) of Cenvat

Credit Rules

(4) Maintain separate accounts for inputs and

pay „amount‟ as determined under rule 6(3A)

in respect of input services - Rule 6(3)(iii) of

Cenvat Credit Rules as inserted w.e.f. 1-4-

2011.

Intimation to department in case of

proportional reversal

If assessee intends to opt for

proportionate reversal, he is required to

intimate department

What if intimation not given? Really only

a procedural lapse

Tribunal has held that reversal means

Cenvat credit was not taken

Rule 6(2) and 6(3)(ii) complementary or mutually

exclusive

Rule 6(2) – separate records – rule

6(3)(ii) – proportionate reversal

Can assessee follow rule 6(2) where

direct relation between input service and

output service available and follow rule

6(3)(ii) in other cases?

In my view - yes

Exempted Services

“Exempted service” means a - (1) taxable service

which is exempt from the whole of the service tax

leviable thereon; or (2) service, on which no service

tax is leviable under section 66B of the Finance Act; or

(3) taxable service whose part of value is exempted on

the condition that no credit of inputs and input

services, used for providing such taxable service, shall

be taken; - - but shall not include a service which is

exported in terms of rule 6A of the Service Tax Rules,

1994 [Rule 2(e) of Cenvat Credit Rules as inserted

w.e.f. 1-7-2012].

Exempted goods

As per Rule 2(d) of Cenvat Credit Rules,

'exempted goods' means goods which are

exempt from whole of duty of excise leviable

thereon and includes goods which are

chargeable to 'Nil' rate of duty and the goods

in respect of which the benefit of an exemption

under Notification No. 1/2011-CE dated 1st

March 2011 or entries at Sr Nos 67 and 128 of

Notification No. 12/2012-CE dated 17-3-2012

is availed

Provision in case of traded

goods

Difference between sale price and cost

of goods sold (gross margin) is to be

treated as value of exempted service

Good and sensible provision – should

apply to past also

Provision can apply to works contract

service also

Exemptions subject to condition of non-

availment of Cenvat Credit

Rule 6(3D) states that payment of

„amount‟ under rule 6(3) means Cenvat

credit not taken for purpose of an

exemption notification where exemption

is granted on condition that no Cenvat on

input and input services is availed

Good provision – even Tribunal had held

so earlier

Value for Services under abatement

scheme

Entire Value will be treated as value of

„exempted service‟ for rule 6

However, if 6% „amount‟ is payable, it

will be on amount on which service tax

not paid (e.g. if service tax paid on 40%,

„amount‟ of 6% will be on balance 60%)

Value of service for services under composition

Schemes for rule 6

In case of services covered under composition

scheme, „value‟ for applying rule 6 will be tax

amount divided by rate of service tax

applicable under general exemption. Present

rate is 12%

If gross amount Rs. 1,000, service tax paid Rs.

48. Then value of taxable service for rule 6

would be Rs. 400.

If service tax rate 10% then service tax would

be Rs 400 and value will be Rs 400.

Overriding Provisions

In respect of banking service, the Bank or

NBFC is required to pay „amount‟ equal to

50% of Cenvat Credit availed on inputs and

input services [Rule 6(3B) of Cenvat Credit

Rules as inserted w.e.f. 1-4-2011].

No reversal in case of zero rated

transactions

Export of goods and export of services

Supplies to SEZ, EOU

Goods supplied against international

competitive bidding, goods supplied to

UN organisations, foreign diplomats

Provision of services to SEZ (where

exemption is available)

Principle Behind Calculations

Take entire Cenvat credit of inputs and input

services used in exempted as well as taxable final

products and exempted as well as taxable services.

At the end of month, assessee should

calculate and reverse Cenvat credit

attributable to exempted final products and

exempted services on provisional basis

Rule

6(3A)(b)(i) Inputs used for exempted final products

Rule

6(3A)(b)(ii) Inputs used for exempted services (On

proportionate basis, based on ratio of

previous year)

Rule

6(3A)(b)(iii) Input services used for exempted final

products and exempted services (On

proportionate basis based on ratio of

previous year).

Total 1+2+3 = amount to be reversed every

month on provisional basis

Calculations at the end of the year

Assessee should calculate the ratios on

actual basis and make fresh calculations

and pay difference, if any, before 30th

June.

If it is found that he had paid excess

amount based on provisional ratio, he

can adjust the difference himself by

taking credit.

Rule 6 in composition scheme

Restaurant service – only 40% Cenvat

credit available

Works contract service – 25%, 40% and

70% schemes – difference between sale

price of goods and purchase price to be

treated as value of „exempted service‟

and then apply rule 6

Input Service Distributor – Rule 7

HO or Branch or Depot can pass on

credit to factories.

They have to register, file returns etc.

Monthly Invoice

No credit where input service exclusively

for exempted goods or exempted service

Distribution on turnover basis of previous

month

Refund of Cenvat Credit – Rule 5

Refund of Cenvat credit on proportionate

basis of exports of goods and services

General Experience is bad – some

excuse is found to reject the refund claim

Removal for job work

Own challan

Return within 180 days.

Dutiability of scrap at job worker‟s place