ceo josé sergio gabrielli de azevedo - presentation to the "comitê de cooperação econômica...

TRANSCRIPT

1

XIV Japan Brazil Joint Economic Committee

Meeting

CEO José Sergio Gabrielli de Azevedo

August 9th 2011

2

DISCLAIMER

FORWARD-LOOKING STATEMENTS:

DISCLAIMER

The presentation may contain forward-looking statements about future events within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended, that are not based on historical facts and are not assurances of future results. Such forward-looking statements merely reflect the Company’s current views and estimates of future economic circumstances, industry conditions,company performance and financial results. Such terms as "anticipate", "believe", "expect", "forecast", "intend", "plan", "project", "seek", "should", along with similar or analogous expressions, are used to identify such forward-looking statements. Readers are cautioned that these statements are only projections and may differ materially from actual future results or events. Readers are referred to the documents filed by the Company with the SEC, specifically the Company’s most recent Annual Report on Form 20-F, which identify important risk factors that could cause actual results to differ from those contained in the forward-looking statements, including, among other things, risks relating to general economic and business conditions, including crude oil and other commodity prices, refining margins and prevailing exchange rates, uncertainties inherent inmaking estimates of our oil and gas reserves including recently discovered oil and gas reserves, international and Brazilian political, economic and social developments, receipt of governmental approvals and licenses and our ability to obtain financing.

We undertake no obligation to publicly update or revise any forward-looking statements, whether as a result of new information or future events or for any other reason. Figures for 2011 on are estimates or targets.

All forward-looking statements are expressly qualified in their entirety by this cautionary statement, and you should not place reliance on any forward-looking statement contained in this presentation.

NON-SEC COMPLIANT OIL AND GAS RESERVES:

CAUTIONARY STATEMENT FOR US INVESTORS

We present certain data in this presentation, such as oil and gas resources, that we are not permitted to present in documents filed with the United States Securities and Exchange Commission (SEC) under new Subpart 1200 to Regulation S-K because such terms do not qualify as proved, probable or possible reserves under Rule 4-10(a) of Regulation S-X.

3

THE IMPORTANCE OF NATURAL RESOURCES TO JAPAN

Japanese Imports ‐ Jan‐Jun 2011

0,1% 8,1%

9,5%

2,5%

30,4%

9,4%

20,1%

11,0%

Foodstuff Materials Fuels

Chemical Products Manufactured goods Machines

Transport Equipment Others

Japan imports almost 100% of its natural resources demands, as it does not produce oil, LNG, coal

and iron ore, for instance.

Japan is relatively well positioned in the world’s natural resources supply chain, through joint ventures or development and production project finances

Japan imports almost 100% of its natural resources demands, as it does not produce oil, LNG, coal

and iron ore, for instance.

Japan is relatively well positioned in the world’s natural resources supply chain, through joint ventures or development and production project finances

Japanese Fuel Imports ‐ Jan‐Jun 2011

15,70%

2,90%

3,80%

6,60%

1,20%

Petroleum Petroleum Products LNG LPG Coal

4

49% 51%

Other Discoveries Deep Water

62%38% Brazil

Others

New Discoveries 2005‐2010

(33.989 million bbl) Deep water discoveries

Source: PFC Energy

BRAZIL ON THE LEADERSHIP OF RECENT DISCOVERIESDeep water discoveries in Brazil represent 1/3 of the world’s discoveries in the last 5 years

• Over the last 5 years, more than 50% of the new discoveries (in the world) took place in deep waters

• The development of these new reserves will demand additional capacity in the supply chain

• The expansion of Brazil’s oil and gas supply chain is aligned to this perspective

We expect to double our proven reserves until 2020, keeping finding costs at US$ 2/boeWe expect to double our proven reserves until 2020, keeping finding costs at US$ 2/boe

5

LONG HISTORY OF TECHNOLOGICAL AND OPERATIONAL LEADERSHIP IN DEEPWATERS

Offshore production facilities

100

5

8

8

9

10

12

12

13

15

15

45

0 20 40 60 80 100

Others

ENI/Agip

ConocoPhillips

CNOOC

Total

Anadarko

Chevron

BP

ExxonMobil

StatoilHydro

Shell

Petrobras

FPSO Semi Spar TLP OtherPetrobras operates 20% of deep waters global production

1977Enchova410ft125m

1988Marimbá1,610ft491m

1994Marlim3,370ft1,027m

1997Marlim Sul5,600ft1,707m

2003Roncador6,180ft1,884m

2009Lula

7,125ft2,172m

Source: PFC Energy(1) These 15 operators represented 98% of global deep waters production in 2009. Water depth of 1000 feet

Deep water productionGlobal operations in 2009¹

6

LONG HISTORY OF BILATERAL RELATIONSHIPS

50/60

Participation in the reconstruction efforts of the Japanese naval industry in the Post‐war period, through ships procurement in Japanese shipyardsConstruction of the drilling

ship Petrobras II – NS‐01

70/80

Participation of JGC–Japan Gasoline Corporation in the construction of refineries in BrazilThree‐party model in the

Petrochemical Industry in Camaçari, with the participation of big Japanese companiesConstruction of 4

semisubmersible drilling platforms in Japan (Petrobras IX, X, XI, XII)

90

Platforms lease sale back Bolivia‐Brazil gas pipeline

financingTQC programs in

partnership with JUSEToyo Engineering working

on RELAM’s modernizationParticipation of Japanese

companies in the Albacora Leste and Frade projectsUrucu’s NGPU financingVarious project finances

2000

Various project finances and loansSamurai Bonds issuancePetrobras Japanese Office

begins operationsTechnological cooperation

with Kobe Steel EngineeringPartnerships in international

projectsLPG sales to Idemitsu OilMitsui becomes Petrobras’

partner in gas distributionEmployees interchange

between Petrobras and MitsuiToyo Engineering works on

engineering projectsMOUs with Mitsui, Itochu

Corporation, JOGMECBrazil Japan Ethanol Trading,

in partnership with Japan Alcohol Trading Partnership with Tokyo

UniversityPartnership with Mitsui and

Transocean to build Petrobras 10.000 Drilling Ship

7

Okinawa Refinery acquisition (Nansei Sekiyu Co)JOGMEC’s financing to

NanseiTechnological cooperation

with Tokyo’s UniversityPROMINP’s presentation to

the Japanese marketNT‐ Guanabara’s leaseMOUs with Sumitomo

Corporation and Mitusbishi CorporationTranspetro’s LNG operators

are trained at Tokyo Gas’terminal

MOUs with Marubeni Co. and Mitsui & Co. to Premium I and Premium II’s studiesDBJ financingPartnership with Sapporo

Beer to produce hydrogen from sugar caneMOU with JOGMEC to study

methane hydrates, ERP, CO2 capture, flex pipes, new tubings for the pre‐saltFPSOs contracts (MODEC) FEED of the FLNG with

Saipem‐SBM‐Chiyoda and Technip‐JGC‐MODECLNG Master Agreement with

Japanese companiesPartnership with Mitsubishi

Co and Schain Cury to build the second deep water drilling ship Joint Venture with Mitsui &

Co to ethanol trading based in SingaporePartnership with Toyo

Engineering to micro GTL pilot plant

LNG Master Agreement with Japanese companiesPetrobras 10.000

financing with JBICMitsui & Co. working to

build and operate Comperj’s utilities in partnership with PetrobrasGTL compact on

negotiations with Sumitomo PrecisionSales of E3 gasoline to the

Okinawa marketNANSEI’s financing by DBJ

and ODFCIHI’s cooperation to

rebuild the facilities of the Ishikawajima shipyard in BrazilParticipation of Japanese

companies in two consortiums to study the Floating LNG project

Under negotiations with KEPCO/Kansai Electric Power Company a contract for oil supply in case of emergenciesSecond phase of employees

interchange between Mitsui & Co. and PetrobrasSpecific Agreement with

JOGMEC to develop flexible linesExpansion of E3 sales in

Okinawa (4 gas stations today. Forecast of 20 by year end)Examples of recent projects

with the participation of Japanese companies:₋ FPSO Cidade de São Paulo MV23₋ FPSO Cidade de Angra dos Reis MV22₋ FPSO Cidade de Santos MV20₋ FPSO Cidade de Niterói MV18₋ FSO Cidade de Macaé MV15₋ FPSO Cidade de Rio de Janeiro₋ FPSO Fluminense

2008 2009 2010 2011

LONG HISTORY OF BILATERAL RELATIONSHIPS

8

Perspectives of the Brazilian Market

9

652 718 731 899 1.078

1.097 1.204 1.315

706699 586

231312 320

480

542593 634125136

1.7391.453

2.317

997

436

906

738

401

290

147

141

106

979494

79

38

171717

7.142

4.957

3.8473.7733.464

2009 2010 2011 2015 2020

Ferti l i zers

Electri c energy

Biofuels

Internationa l sa les

Natura l gas

Exports

Other distributors

Sa les to BR

PN 2011‐15 ‐ Volume de VendasTota is do Sis tema Petrobras

Sales volumes (thousand boed) 6,6% p.a.

5,6% p.a.

GROWTH IN SALES VOLUMES

10

87%

7%

3% 2%1%

E&P RTM G&E Distribution Corporate

2011‐2015 INVESTMENTS

International:US$ 11,2 billion

Total:US$ 224,7 billion

57%31%

6%2%1%2%1%

E&P RTM G&EPetrochemicals Distribution BiofuelsCorporate

70,6

3,813,2

3,1

4,12,4

127,5 (*)

(*) US$ 22,8 bi in exploration

11

1.855 1.971 2.004

321 317 334 435

618

1.120

111 132 144141

180

246

2.100

9996 93

96

125

142

2008 2009 2010 2011 2015 2020

Oil Production ‐ Brazil Gas Production ‐ Brazil Oil Production ‐ Intl Gas Production ‐ Intl

2.386 2.516

6.418

3.993

1.148543

Pre-Saltth boe

/day

2.772

845Transfer of Rights

13

+ 10 post‐sal projects

+ 8 pre‐salt projects

+ 1 Transfer of Rights project

+ 35 Systems

Additional capacity

Oil: 2.300 th. bpd

2.575

• Pre‐salt and Transfer of Rights will represent 69% of the additional production until 2020;

• Pre‐salt’s share of Petrobras’ oil production in Brazil will grow from the current 2% in 2011 to 18% in 2015 and 40,5% in 2020.

3.070

4.910

PRODUCTIONWith ample access to new reserves, Petrobras will more than double production on the next decade

12

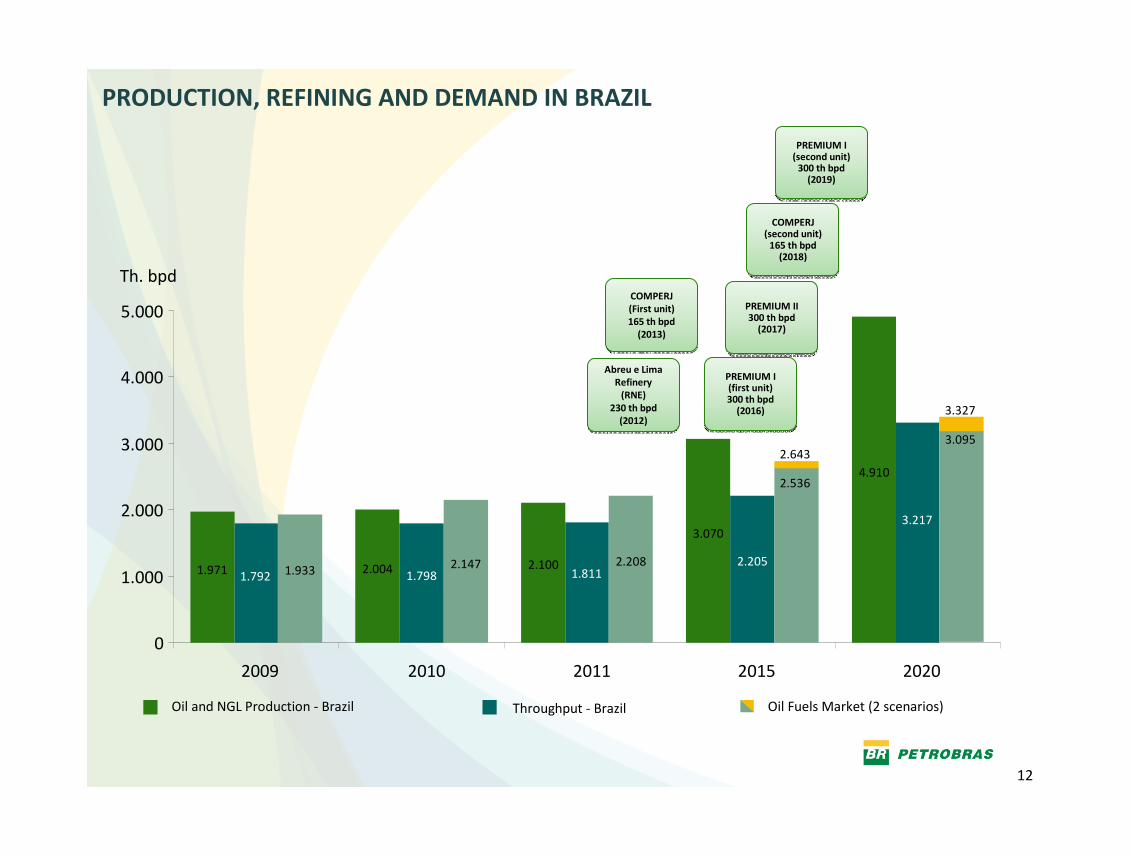

PRODUCTION, REFINING AND DEMAND IN BRAZIL

Abreu e Lima Refinery (RNE)

230 th bpd (2012)

Abreu e Lima Refinery (RNE)

230 th bpd (2012)

COMPERJ(First unit)165 th bpd(2013)

COMPERJ(First unit)165 th bpd(2013)

PREMIUM I(second unit)300 th bpd(2019)

PREMIUM I(second unit)300 th bpd(2019)

PREMIUM II300 th bpd(2017)

PREMIUM II300 th bpd(2017)

COMPERJ(second unit)165 th bpd(2018)

COMPERJ(second unit)165 th bpd(2018)

PREMIUM I(first unit)300 th bpd(2016)

PREMIUM I(first unit)300 th bpd(2016)

1.8112.205

3.217

1.971 2.004 2.100

3.070

4.910

1.792 1.7981.933 2.147 2.208

2.536

3.095

0

1.000

2.000

3.000

4.000

5.000

2009 2010 2011 2015 2020

Oil and NGL Production ‐ Brazil Throughput ‐ Brazil Oil Fuels Market (2 scenarios)

Th. bpd

2.643

3.327

1313

THANK YOU!