cf final ppt

DESCRIPTION

,n,m.TRANSCRIPT

Flow of the presentation

• Indian oil and gas industry • Profile of the concerned organizations• And their dividend policies in brief • Introduction of “event study”• Discussion of the event study results• Discriminant Analysis

Oil and Gas industry

• India has total reserves (proved & indicated) of 1,201 million metric tonnes (MMT) of crude oil and 1,437 billion cubic metres (BCM) of natural gas as on April 1, 2010.

• Growth rate was 2.2% for the 2009-10 financial year.

• Total dividend payout by the industry was Rs 178 Billion.

Industry profilePublic Sector Undertakings (PSU's):ONGC - Oil & Natural Gas Corp (exploration and production)OIL - Oil India Limited (exploration & production)IOC - Indian Oil Corporation (refining & marketing)BPCL - Bharat Petroleum Corporation Ltd (refining and marketing)HPCL - Hindustan Petroleum (refining & marketing)GSPC - Gujarat State Petroleum CorpPrivate Oil & Gas companies in IndiaRIL - Reliance Industries Limited (Indian Oil & gas company)ESSAR (Indian Oil & Gas company)Cairns Energy IndiaBG energyNiko (upstream exploration & production)Shell OilBPTotal (downstream exploration & production, chemicals)

Overview of the Industry

Companies Profile

IOCLMar '10

Sources Of Funds in RS. CrTotal Share Capital 2,427.95

Equity Share Capital 2,427.95Share Application

Money 0Preference Share

Capital 0Reserves 48,124.88

Revaluation Reserves 0.00Equity 50,552.83

Secured Loans 18,292.45Unsecured Loans 26,273.80

Total Debt 44,566.25

47%53%

IOCLTotal Debt Equity

IOCL Share holding Pattern

RIL Capital structure

Mar '10

Sources Of Funds in RS. CrTotal Share Capital 3,270.37

Equity Share Capital 3,270.37Share Application

Money 0Preference Share Capital 0

Reserves 1,25,095.97Revaluation Reserves 8,804.27

Equity 1,37,170.61Secured Loans 11,670.50

Unsecured Loans 50,824.19Total Debt 62,494.69

31%

69%

Reliance

Total Debt Equity

RIL

Capital Structure

16%

84%

ONGCTotal Debt Equity

ONGCMar '10

Sources Of Funds in RS. CrTotal Share Capital 2,138.89

Equity Share Capital 2,138.89Share Application Money 0Preference Share Capital 0

Reserves 85,143.72Revaluation Reserves 0.00

Equity 87,282.61Secured Loans 0.00

Unsecured Loans 16,405.64Total Debt 16,405.64

ONGC Share holding pattern

Dividend History(ONGC)

1st April, 2009 to

31st March, 2010

1st April, 2008 to

31st March, 2009

1st April, 2007 to

31st March, 2008

1st April, 2006

to 31st March, 2007

1st April, 2005 to

31st March, 2006

1st April, 2004 to

31st March 2005

1st April, 2003 to

31st March 2004

1st April, 2002 to

31st March 2003

Face Value of equity shares (Rs. per share)

10 10 10 10 10 10 10 10

Dividend(Rs. in millions)

70,583 68,444 68,444 66,305 64,167 57,037 34,222 42,778

Dividend rate 330% 320% 320% 310% 450% 400% 240% 300%

Dividend Payout Ratio

42.09% 42.44% 40.98% 42.39% 44.47% 43.90% 39.50% 40.60%

Dividend tax(Rs. in millions)

11,616 11,632 11,632 10,125 9,000 7,763 4,385 2,375

HPCL Capital Structure

65%

35%

HPCLTotal Debt Equity

HPCLMar '10

Sources Of Fundsin RS. CrTotal Share Capital 339.01Equity Share Capital 339.01Share Application Money 0Preference Share Capital 0Reserves 11,218.96Revaluation Reserves 0.00Equity 11,557.97

Secured Loans 1,375.88Unsecured Loans 19,926.49

Total Debt 21,302.37

HPCL Share holding pattern

Financial Year

2008-09

2007-08 2006-07 2005-06 2004-05 2003-04 2002-03 2001-02

Interim Dividend

% 0 - 60 - 50 60 20 -

Final Dividend % 52.50 30 120 30 100 160 180 100

Total % 52.50 30 180 30 150 220 200 100

Dividend Amount

Rs. Cr.

177.78

101.59 610.8 101.8 509 746.81 678.66 339.33

Tax on Dividend

Rs. Cr.

30.21 17.27 97.75 14.28 71.15 95.65 78.26 -

Total Rs. Cr207.9

9118.86 708.55 116.08 580.15 842.46 756.92 339.33

Dividend Payout (As % of PAT)

% 36.17 10.47 45.1 28.62 45.42 44.25 49.24 43.06

Related Information

Profit after Tax

Rs.Cr.574.9

81134.88 1571.17 405.63 1277.33 1903.94 1537.36 787.98

EPS Rs.Cr. 16.98 33.51 46.35 11.97 37.69 56.18 45.37 23.26

Book Value/Share

Rs.Cr.316.8

8311.59 283.19 257.74 249.04 228.47 197.12 174.07

Dividend History( HPCL)

NTPC Capital structure

NTPCMar '10

Sources Of Funds in RS. CrTotal Share Capital 8,245.50

Equity Share Capital 8,245.50Share Application

Money 0Preference Share

Capital 0Reserves 55,478.60

Revaluation Reserves 0.00Equity 63,724.10

Secured Loans 9,079.90Unsecured Loans 28,717.10

Total Debt 37,797.00

37%

63%

NTPCTotal Debt Equity

NTPC share holding pattern

Event study

• An Event study is a statistical method to assess the impact of an event on the value of a firm.

• Here we take dividend payout as an event.

Abnormal Return

Constant Return Model

Market Model

Economical model

• Most appropriate model is Capital Asset Pricing Model(CAPM).

Re = Rf + B(Rm – Rf)

Rm = Average market return

Rf = risk free return

B = Sensitivity of the asset returns to the market returns.

CAPM

ModelE(Re) = 7.14 + B(12.59-7.14) +E(Re) = 7.14 + B(5.44)

Normally distribute

Hypothesis

Ho: The dividend payout has no impact on the behavior of returns.

Hypothesis Testing

Estimation and Absorption Period

90 days 15 days

Methodology

Step 1. a) Test market model b) if found significant use Paired T-TestStep 2. a) if market model is not capable in

explaining the behavior of the security, use CAPM model.

b) impact analysis by expected actual(returns)

Step 1. ONGC Regression Model

Model Summaryb

Model R R Square Adjusted R SquareStd. Error of the

Estimate1 .562a .315 .308 .022

a. Predictors: (Constant), Pre event Market return

b. Dependent Variable: Pre event Company return

Coefficientsa

Model

Unstandardized Coefficients

Standardized

Coefficients

t Sig.B Std. Error Beta1 (Constant) .000 .002 -.313 .755

Pre event Market .676 .106 .562 6.405 .000

a. Dependent Variable: Pre event Company return

Step 1.b)

• Regression model says that market returns are significantly influencing the security returns.

• Market model is able to explain the variation in the security returns.

• We decided to go with “Market Model”

Model

E(Re) = -0007+ .562(Rm)

ONGC Dividend Impact

There is no significant impact by the dividend payout.

Paired Samples Test

Paired Differences

t dfSig. (2-tailed)Mean

Std. Deviatio

n

Std. Error Mean

95% Confidence Interval of the

Difference

Lower UpperExpected – Post E .003 .019 .005 -.008 .013 .514 14 .616

RIL Regression model

Model Summaryb

Model R R Square Adjusted R SquareStd. Error of the

Estimate Durbin-Watson1

.175a .031 .020 .025 2.067

a. Predictors: (Constant), preMb. Dependent Variable: preC

Coefficientsa

Model

Unstandardized Coefficients

Standardized

Coefficientst Sig.B Std. Error Beta

1 (Constant) .005 .003 1.987 .050preM -.531 .316 -.175 -1.681 .096

a. Dependent Variable: preC

Step 2

• Regression model is not able to explain behavior of the security returns by market returns.

• So we decided to use CAPM model. ModelE(Re) = 7.14 + 5.44*1.06 ( annual)E(Re) = 12.906 % (annual)

Impact

Impact = Actual return( 15 days)-Expected return( 15 days)

=( -0.03432) -.57 = -.6075 There is negative impact by dividend payout.

HPCLDividend pay out impact using CAPM

Dividend payout year Dividend percent CAR (Cumulative abnormal returns)

interpretation

2010120%

0.0532 positive

200952.5%

-0.229207 negative

200830%

-0.013256 negative

2007120%

-0.002501 negative

200660%

-0.018701 negative

ONGCImpact analysis

Dividend payout year

Dividend percent CAR( cumulative abnormal return)

2010320%

0.00355

2009 180%

-0.037789

2008140%

0.03189

2007180%

-0.01367644

2006140%

-0.038502621

IOCL

Dividend payout year Dividend percent impact

2010 130.00 -0.051887564

2009 75.00 0.0391

2008 55.00 0.06857

2007 130.00 -0.021772

2006 60.00 0.11149384

NTPC

Dividend payout year Dividend percent impact

2010 30%

-0.001326

200928%

-0.000613

200827%

0.00067

200724%

-0.006835

200620%

0.00056

RIL

Dividend payout year Dividend percent impact

201070%

-0.60

2009130%

-0.08275

2008130%

-0.034412

2007100%

0.21406

Discriminant analysis

Objective:- 1. To evaluate the dividend payout decision.

2. To identify the variables, which affect the dividend payout decision.

Sample size = 88 companies from various industries.

Study reliability

Eigenvalues

Function Eigenvalue % of Variance Cumulative %Canonical Correlation

11.365a 100.0 100.0 .760

Wilks' Lambda

Test of Function(s) Wilks' Lambda Chi-square df Sig.1

.423 68.435 13 .000

Decision Criteria

Functions at Group Centroids

Paid or Not Paid

Function

1Not Paid -1.784

Paid .748

Decision Function

-1.784 .784

Influencing factors

Canonical Discriminant Function Coefficients

Function

1

Return On Equity .065Age .011PE Ratio .000Current Ratio -.070Credit Rating -.079Adjusted Cash Margin .011

Adjusted Cash Flow Times .004

Industry -.075ROE/Ke -.434market cap -.133(Constant) -1.740

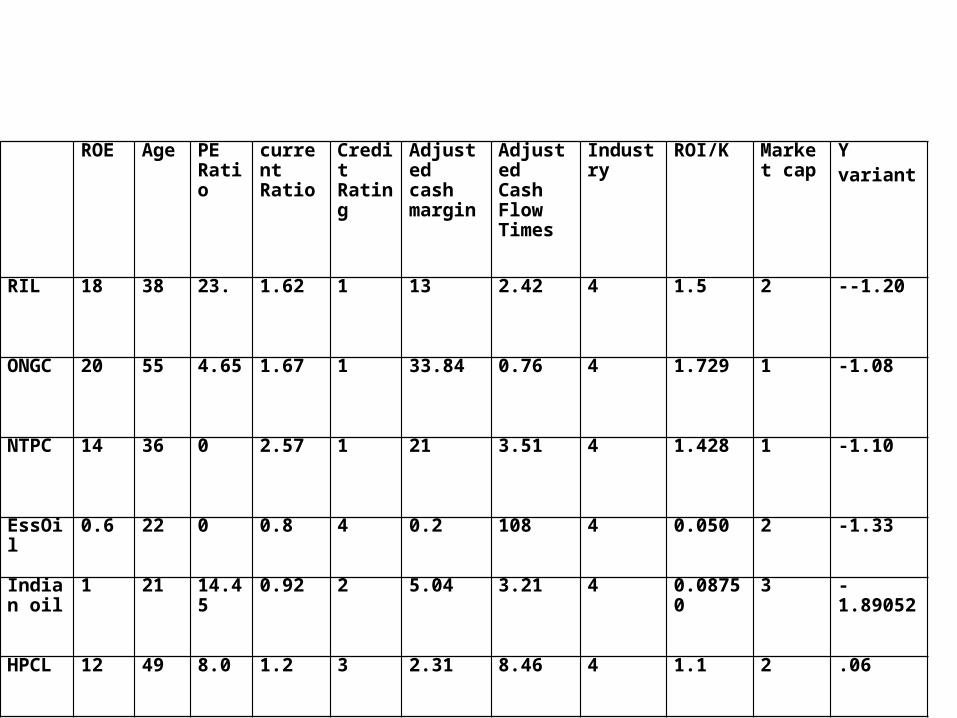

ROE Age PE Ratio

current Ratio

Credit Rating

Adjusted cash margin

Adjusted Cash Flow Times

Industry ROI/K Market cap

Yvariant

RIL

18 38 23. 1.62 1 13 2.42 4 1.5 2 --1.20

ONGC

20 55 4.65 1.67 1 33.84 0.76 4 1.729 1 -1.08

NTPC

14 36 0 2.57 1 21 3.51 4 1.428 1 -1.10

EssOil

0.6 22 0 0.8 4 0.2 108 4 0.050 2 -1.33

Indian oil

1 21 14.45 0.92 2 5.04 3.21 4 0.08750 3 -1.89052

HPCL

12 49 8.0 1.2 3 2.31 8.46 4 1.1 2 .06

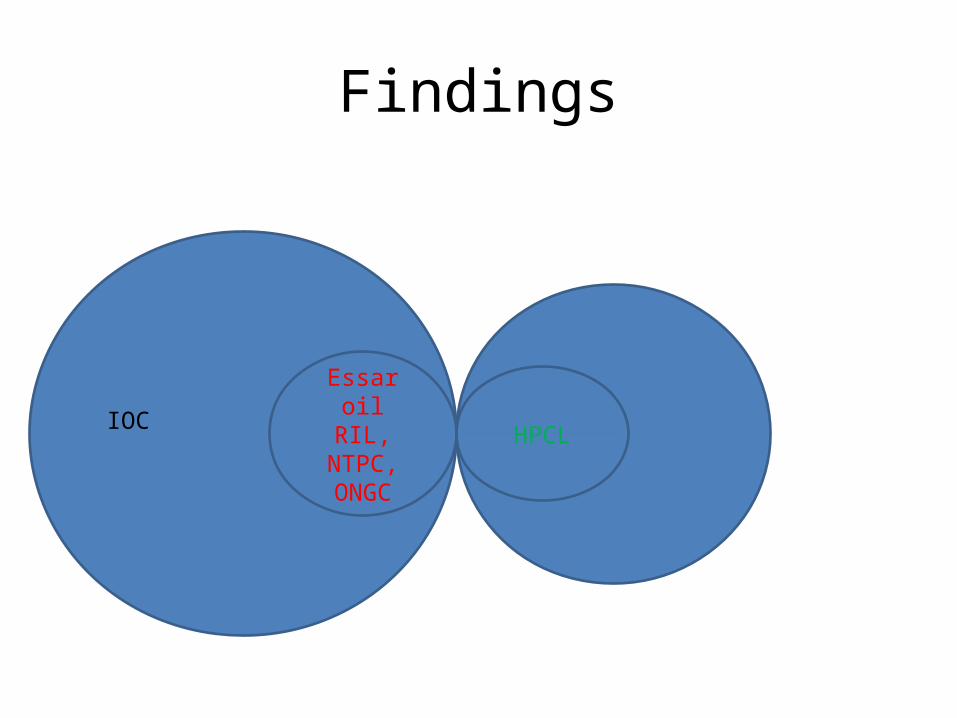

Findings

IOC Essar oil

RIL, NTPC, ONGC

HPCL

Thank You