cfo india - august 2011

DESCRIPTION

Volume 2 Issue 8TRANSCRIPT

CF

O I

ND

IA

ISSUE

VO

LUM

E ST

RA

TEG

Y W

HA

T W

OU

LD P

ETER

DR

UC

KER

DO

? 26 | CFO

PR

OFILE: N

ISHA

NT

FAD

IA 22 | A

UD

I A6 U

LTIM

AT

E IN LU

XU

RY

50

08

02

A 9.9 MEDIA PUBLICATION

NISHANT FADIACFO PROFILE p. 22

AUDI A6 ULTIMATE IN LUXURY p. 50

STRATEGYWHAT WOULD PETER DRUCKER DO? p. 26

VOLUME 02ISSUE 08Rs.50AUGUST 2011

CFOs are increasingly facing an avalanche of added responsibilities thanks to strictcorporate governance, tougher compliancelaws and increased stakeholder demand. How are they tackling these challenges? Pg 12

withCopingCompliance

CF

O I

ND

IA

ISSUE

VO

LUM

E

STR

AT

EGY

WH

AT

WO

ULD

PET

ER D

RU

CK

ER D

O? 26 | C

FO P

RO

FILE: NISH

AN

T FA

DIA

22 | AU

DI A

6 ULT

IMA

TE IN

LUX

UR

Y 50

08

02

A 9.9 MEDIA PUBLICATION

NISHANT FADIACFO PROFILE p. 22 AUDI A6 ULTIMATE IN LUXURY p. 50

STRATEGYWHAT WOULD PETER DRUCKER DO? p. 26

VOLUME 02ISSUE 08Rs.50AUGUST 2011

CFOs are increasingly facing an avalanche ofadded responsibilities thanks to strict

corporate governance, tougher compliancelaws and increased stakeholderdemand. How are they tacklingthese challenges? Pg 12

WITH COPInG

COMPLIAnCe

governance

18 LESSONS FROM EAST AND WESTA CIMA report argues in favour of a corporate governance model that takes into account the best practices from Asia and the West

insight

42 ORGANISATIONAL HEALTH: THE ULTIMATE COMPETITIVE ADVANTAGE To sustain high performance, organisations must build their capacity to learn and keep changing over timeTo sustain high performance, organisations must build their capacity to learn and keep changing over time

ILLUSTRATION & COVER DESIGN SHIGIL N

AD INDEX Financial Executive 02 | Airtel 35,36 | Sodexo Back Cover

CFO InsIdeA U G U S T | 2 0 1 1

COPING WITH COMPLIANCE! CFOs today face an avalanche of new responsibilities, thanks to stricter corporate governance and compliance laws. How are they tackling these challenges?

cover story12

cfo profileFocussed: 3D Vision in FinanceNishant Fadia, the CFO of Prime Focus, one of the world’s leading visual entertainment firms talks of the joys and pains of his job

in practice26 WHAT WOULD DRUCKER DO?Two US-based chief financial officers discuss how they apply Peter Drucker’s techniques to their current business challenges

i thinK10 S MAHALINGAM The CFO and ED of TCS says currency volatility, uncertainty in the global economy and issues like retaining talent, keep him awake at night

10

case stUDy

32 COMMUNICATING FOR PROFITSushil Agarwal, CFO of Aditya Birla Nuvo, recalls how a debt burden was reduced and a business unit made profitable

cfo loUnge

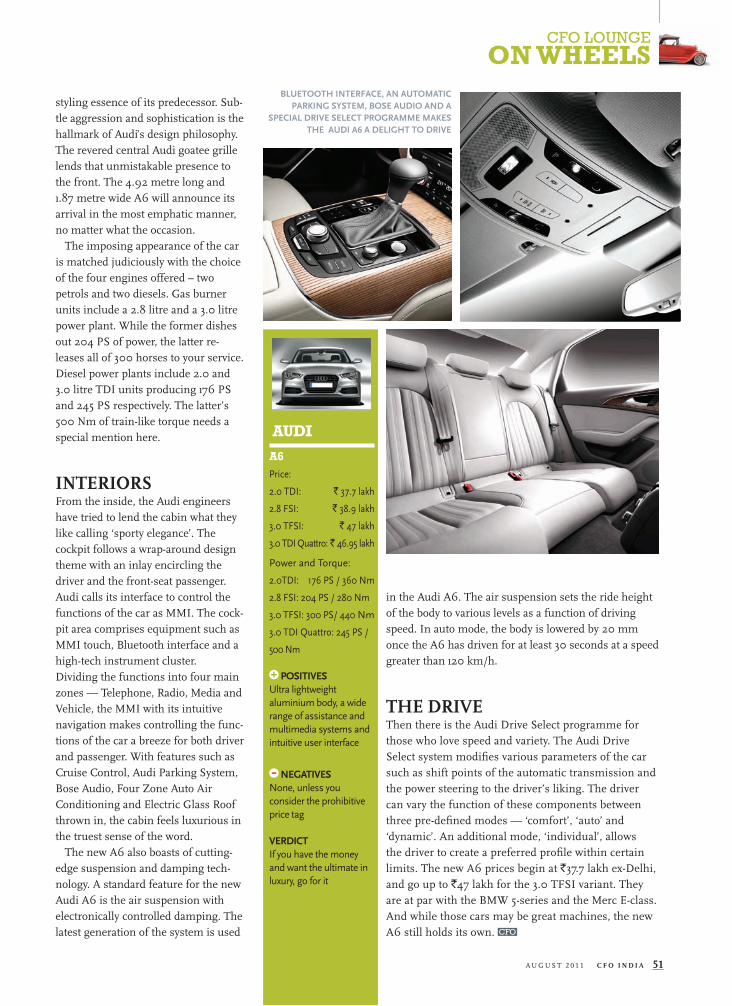

50 ON WHEELS | AUDI A6

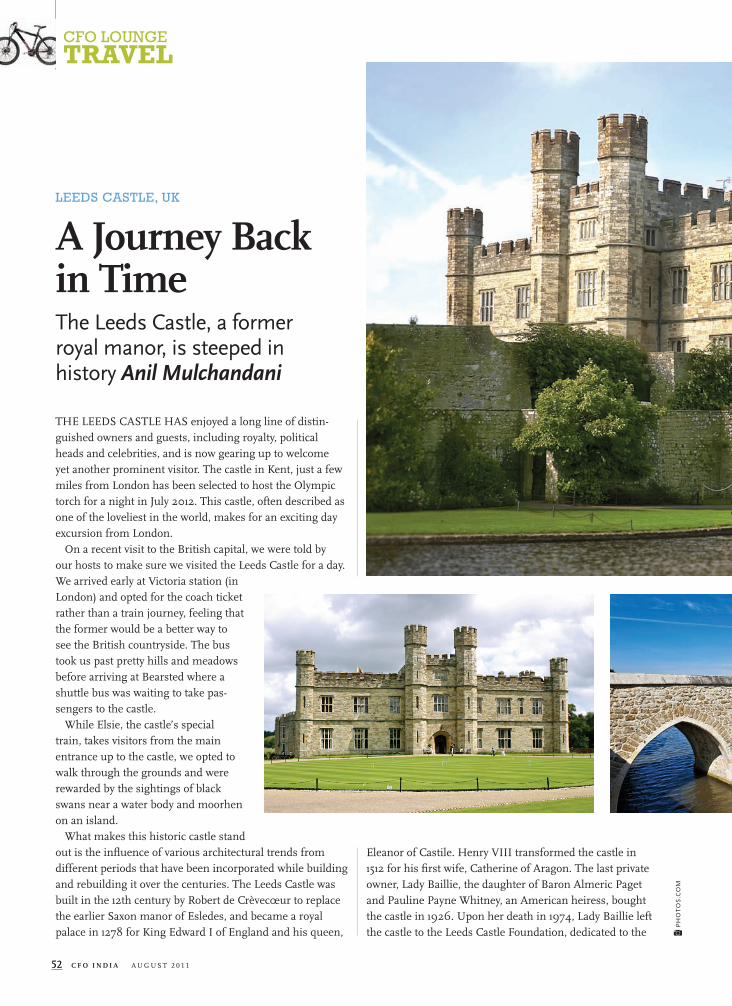

52 TRAVEL | LEEDS CASTLE

54 GIZMOS | DENON HOME THEATRE regUlars

4 LETTERS TO THE EDITOR

06 O-ZONE

56 NOT JUST THE LAST

WORD

52

22

More than 15,000 Members | 85 Chapters Worldwide | 79 Year History

"Member relationships with !nancial thought leaders from large, highly-diversi!ed global corporations and conglomerates to smaller private companies and non-pro!ts.”

Mary Jo GreenSenior Vice President & TreasurerSONY CORPORATION OF AMERICA

"Leading-edge content and objective research for the competitive advantage I need to meet the demands of a multinational computer technology corporation.”

Taylor HawesCFO Intellectual Property & LicensingMICROSOFT CORPORATION

FINANCIALEXECUTIVES.ORG | MEMBER SERVICES 877.359.1070

A newly-established category of FEI membership that empowers talented, motivated !nancial professionals with ongoing opportunities for personal and professional growth as their careers advance

Choose FEI to support your advancing career as a !nancial professional.

membership Interested in learning more about the Financial Executives

International India Chapter? Contact Tom Thompson at

tthompson@!nancialexecutives.org

THE VALUE OF FEI MEMBERSHIP Financial Executives International (FEI) is the professional association of choice for senior-level finance executives.

3AU G U S T 2 0 1 1 C F O I N D I A

from the managing editor

dhiman [email protected]

Complying withCompliance

LATE LAST YEAR when I met S Durgashankar, the CFO of Mahin-dra-Satyam (he has since moved back to Mahindra & Mahindra as Head of M&A), for a cover feature on the remarkable turnaround story of the beleaguered software giant, he spent half-a-day explain-ing why every CFO in India must ensure that their companies fol-lowed all compliance norms. Or else, he said, sooner or later, many of them would meet the fate that befell Satyam.

As we went about writing this issue’s cover package, my colleague Bennett Voyles, spoke to a number of C-suite executives as well as experts on governance, about the level of compliance in India Inc and the challenges CFOs faced. Some of what we learnt was indeed worrying. For instance, how do CFOs manage to cope with the over 200 filings companies are supposed to make every year? Apparently, many fail the test. One of the experts we spoke to, Nitin Deshmukh, Chief Executive Officer of Kotak Private Equity Group, said his team seldom completes a due diligence exercise on a company without finding compliance related problems. “Without exception, there are almost always issues in all mid-sized companies,” he said.

The good news is that a majority of companies and their CFOs have understood the correlation between compliance and success in the market and are gearing up to meet this challenge. Read our cover story (Coping with Compliance, Pg12) to find out how CFOs across India are facing up to this challenge.

Of course, there is a lot more in this issue. Read about the exciting journey of Nishant Fadia, the 34-year-old CFO of Prime Focus, the company that started in 1997 from a garage in Mumbai. Today it is the world’s largest special effects and post-production firm with its wings spread across three continents. The festive season is upon us and in the Lounge section, we have featured some of the best things you can bring home this month – the new Audi A6, a new Denon home theatre or tickets to a holiday in UK. Enjoy the issue.

SUBSCRIBER SERVICES:

Call +91-120-4010999

VISIT CFO INDIA’S WEBSITE

www.cfo-india.in

MANAGING DIRECTOR: Dr. Pramath Raj Sinha

EDITORIALEDITOR: Anuradha Das MathurMANAGING EDITOR: Dhiman ChattopadhyayCONTRIBUTING EDITOR: Bennett Voyles

DESIGNSENIOR CREATIVE DIRECTOR: Jayan K NarayananART DIRECTORS: Binesh Sreedharan & Anil VKASSOCIATE ART DIRECTOR: PC Anoop VISUALISERS: Prasanth TR, Anil TSENIOR DESIGNERS: Joffy Jose, NV Baiju, Chander Dange & Sristi MauryaDESIGNER: Suneesh K, Shigil N & Charu DwivediCHIEF PHOTOGRAPHER: Subhojit Paul PHOTOGRAPHER: Jiten Gandhi

THE CFO INSTITUTEEXECUTIVE DIRECTOR: Deepak GargNATIONAL HEAD: Bindu KrishnaASSISTANT BRAND MANAGER: Nisha AnandSENIOR MANAGER: Shreya PilaniASSOCIATE: Deepika Sharma

SALES & MARKETINGASSISTANT REGIONAL MANAGER (SALES): Rajesh Kandari (+91-9811140424)NATIONAL MANAGER (EVENTS & SPECIAL PROJECTS): Mahan-tesh Godi (+91-9680436623) ASSISTANT BRAND MANAGER: Arpita GanguliCO-ORDINATOR (AD SALES, MIS, SCHEDULING): Aatish MohiteSOUTH: Vinodh Kaliappan (+91-9740714817)WEST: Sachin N Mhashilkar (+91-9920348755)For any customer queries and assistance please contact [email protected]

PRODUCTION & LOGISTICSSENIOR GENERAL MANAGER (OPERATIONS): Shivshankar M HiremathASSISTANT PRODUCTION MANAGER: Vilas MhatreLOGISTICS: MP Singh, Mohamed Ansari, Shashi Shekhar Singh

OFFICE ADDRESSNine Dot Nine Interactive Pvt Ltd Kakson House, A & B Wing, 2nd Floor80 Sion Trombay Road, Chembur, Mumbai- 400071 INDIA.

Published, Printed and Owned by Nine Dot Nine Interactive Pvt Ltd. Published and printed on their behalf by Kanak Ghosh. Published at Bungalow No. 725, Sector - 1, Shirvane, Nerul, Navi Mumbai - 400706 Printed at Nutech Photolithographers,B-240, Okhla Industrial Area Phase-1,New Delhi-110020

All rights reserved: Reproduction in whole or in part without written

permission from Nine Dot Nine Interactive Pvt Ltd is prohibited.

44 C F O I N D I A AU G U S T 2 0 1 1

Letters

Most articles in CFO India are informative and cover a wide variety of subjects. I quite enjoyed reading the last issue. — Vardhan Dharkar,CFO, KEC International, Mumbai

Informative and enjoyable

CFO INDIAAugust 2011

AT PAR WITH THE BESTI am regular reader of CFO India magazine. The content of the magazine is amazing and can any day match that of cfo.com, the American magazine. My work as a consultant is around CFO services. The insights you provide are really helpful in increasing my understanding and knowledge about the ‘CFO’ subject. Can you put up some webcasts of key interviews on your website? — Rahul Palwe, Consultant, Deloitte, Mumbai IRREGULAR DELIVERYI have been receiving my copy of CFO India late for the past few months. Will you kindly look into the matter? — Sunil Nayak, CFO ACC Ltd, Mumbai

EXCITING COVER FEATUREI really liked the July issue (The Dream Mer-chants). It was interesting to find out about the nature of challenges faced by CFOs of football clubs or of companies that sell yachts, holidays and ice creams. — Alpesh Gandhi, CA, Gurgaon

THANK YOU!I enjoyed reading the July issue. On a personal

note, thank you for covering Marine Solutions and writ-ing about the challenges before CFOs like us.— Indranil Deb, CFO, Marine Solutions, Mumbai

FACTUAL ERRORS: MARRIOTT HOTELSThe article “The Dream Merchants” (July 2011) has some factual errors regarding our Area Director of Finance, Ms Ulrike Stark and about the hotel. The fol-lowing points need immediate correction: Ms Ulrike Stark is Area Director of Finance (India, Ma-laysia, Maldives, Australia) and not Director of Finance, South Asia as mentioned. The article also mentions that in the hotel business CFOs have to be prepared to foot the bills of some politicians or stars who may dine at the hotel but do not pay the tab. We deny this. Since we are the only hotel mentioned, this has a negative connotation to our company. Finally, a statement made by another CFO about their company’s IPO has been wrongly attributed to her, since the statement ends with the words “she says” instead of “he says”. A cor-rigendum would be appreciated.— Khushnooma Kapadia

Managing Editor’s note: We sincerely regret the errors.

08.11 Your voice can make a change: Share your viewpoint on what’s happening in the community and your feedback on the magazine at [email protected]

SH

IGIL

N

66 C F O I N D I A AU G U S T 2 0 1 1

Indian CIOs Better Prepared than Global Peers

BUZZ

08.11

CEOS AND CFOS will be relieved to hear this piece of news. A recent global study by IBM has confirmed that technology officers (CIOs) in India and South Asia (ISA region) are more confident of addressing changes and complexity in business environment than their counterparts in mature markets.

According to IBM 2011 Global CIO study, about 58 per cent chief informa-tion officers in the ISA region said they were prepared to address changes in environment on the back of learnings from past experience and support from other functions of the organisation.

Only 49 per cent respondents from mature markets agreed with them. “CIOs are now moving from being the leaders of a support function to one that is more closely aligned with the CEO’s agenda and the larger organisational business objectives,” IBM India/South Asia Partner and Strategy and Transformation Leader ( Global Business Services) Clifford Patrao said.

IBM conducted the study with 3,018 CIOs globally across 71 countries and 18 industries, including 178 CIOs in five sectors across India and South Asia. The study was conducted to understand how technology officers are helping their firms adapt to the accelerating change and complexity in today’s competitive and economic landscape, he said.

About 83 per cent of the respondents in ISA region said they were focusing on business intelligence and analytics solutions, while 57 per cent said they are focusing on risk management and compliance. About 74 per cent said they were looking at mobility solutions to help increase competitiveness of their organisation.

IF FACEBOOK IS RAKING in the dollars, it is also inspiring oth-ers in far away lands to come up with business plans using the social networking website’s popularity. The Rajasthan Government has come up with a plan that will help all the young Facebook addicts study harder! It is launching a social network-ing site that will also help brush up a youngster’s aca-demic knowledge.

“The idea is to utilise the popularity of social network-ing sites among students. Most of them spend a lot of time on such websites every day,” a senior official of the state’s Information Technol-ogy Department, which is developing the portal, told the media.

The government portal will give tips to students on subjects like physics, chemistry and math-ematics. Experts will be roped in to answer the academic queries students post on it. “We thought why not make it a bit educational so that students can not only enjoy the fun that these sites offer but also get to learn something,” the official said. Students will be able to open up their individual accounts, add friends and and interact among themselves just like they do on Facebook. “We will store e-books, objective questions and coaching material related to each subject,” the officer added. The development of the portal is in the final phase, he said.

EDUCATION

A Facebook-like Education Website

PH

OT

OS.

CO

M

77AU G U S T 2 0 1 1 C F O I N D I A

THE CFO POLL

Is succession planning an accepted practice in your workplace?

Will the US debt crisis have a cascading effect on India Inc?

WHAT’S AROUND ZONECloud on Smartphones ....................................... Pg 08Jargon Decoded: Ducks in a row......................... Pg 08Cyberstalking & Stress........................................Pg 09Good Fat Found ....................................................Pg 09

Vote now at www.cfoinstitute.com/poll

70%Yes

13%N.A

RESULT

CURRENT POLL QUESTION

No17%

DOMESTIC PASSENGER CAR sales have fallen for the first time after 30 months of continuous growth, registering a 15.8 per cent decline in July this year, mainly due to hikes in lending rates and lower produc-tion by market leader Maruti Suzuki during the month. Car sales in the country stood at 1,33,747 units in July, 2011, as against 1,58,767 units in the same month last year, according to figures released by the Society of Indian Automobile Manufacturers (SIAM) recently. “This is the first time since January 2009, that car sales have fallen. Interest rates and fuel prices were going up in recent months and that led to an overall negative sentiment in the market,” SIAM Director General Vishnu Mathur told reporters here. The car market last witnessed a fall in January 2009, when sales shrunk by 3.2 per cent year-on-year. Last month’s decline is the steepest since November 2008, when car segment sales fell 19.3 per cent.

AUTO

No Buyers for Cars?

March 2010 to Present – CFO,

Netambit.

Dec 2008 – Feb 2010 – CFO

Bothli Chemicals & Mining

2006-2008 – National

Commercial Manager, Spencer's

Retail

1999 – 2006 – Sr Manager,

Seagram

AN

IL T

O-ZONE

88 C F O I N D I A AU G U S T 2 0 1 1

IMAGINE LIFE FOR the CFO if he could download and store unlimited data on his smartphones, simply because the phone was ‘cloud-friendly’! The world’s second largest network equipment maker, Huawei Technologies of China, will soon unveil its cloud computing smartphones. Huawei is plunging its cloud computing smartphones as a medium to seize market shares from the likes of Apple and Samsung. Cloud computing smartphones will allow its customers to download applications without demanding inad-equate storage space on their handsets as cloud computing relates to data and software stored on computer servers rather than indi-vidual PCs and can be accessed over the internet.

CLOUD

Cloud Computing Smartphones

JARGON DECODEDThe phrase: Ducks in a row

THE MEANING:The phrase refers to a situation when someone has to organise things properly or have business plans in order.

THE USAGEDon’t peek into your colleague’s cubicle to see if he is hiding his pet ducks there, if you hear someone say-ing: “Ravi always has his ducks in a row.” It simply means Ravi is well organised.

cfobook

hemedra paliwalWall Info Boxes +

What’s on your mind?

Hemendra Paliwal believes Anna Hazare’s fight against corrpution is a worthy cause August 19 at 10.30 pm · Comment · Like

Hemendra Paliwal supports the nationwide campaign to save the girl childAugust 17 at 9.05 pm· 2 people Commented · 1 person likes this

Hemendra Paliwal loves solving complex mathematical puzzlesAugust 12 at 11.00 pm · 5 people commented · Like

I Read...All sorts of good fiction writingAugust 16 at 6.26pm · Comment · 4 people Like this

Hemendra Paliwal likes Zicom, CFO India and 2 others

Zicom, CFO India, Moneycontrol.com August 17, 8.55 pm · 2 Comments · 7 people Like this

RECENT ACTIVITY

Attach Share

I Listen...To light classical music and old Hindi film songs August 14 at 7:14pm · Comment · 1 person likes this

PERsONAL

Zodiac: Capricorn Political Views: Liberal

WORK

November 1997 to Present –COO & CFO, Zicom Electronic Security Systems 1993-1997 – Damania Group of Industries as Manager Accounts

EDUCATION

Institute of Chartered Accountants of India BSc – Mohanlal Sukhadia

University, Udaipur, 1991 Kanwar Pada Senior Secondary School, 1987

PH

OT

OS.

CO

M

O-ZONE

99AU G U S T 2 0 1 1 C F O I N D I A

AFTER A FEW YEARS of lull when Indian students showed a sudden change in their preferences as far as destinations for education went, the US is back on top again.

More Indian students have applied for visas to study in US in 2011 than in the previous five years. According to a data released by US embassy, the applications exceeded over 20 per cent over last year. Last year 24,500 students were granted visas to join American universities. Most of them applied for Masters and 14.5 per cent joined a grad school. Pratibha Jain, a Mumbai-based counsellor, who helps such

students told agencies, “This year has seen a phenomenal rise in number of undergraduate student applications.”

That applications were significantly higher than last year, were confirmed by officials at the American embassy in New Delhi. An official said, “The US has greatly expanded its counsel-lor staffing and educational outreach initiatives to ensure that prospective students can get visa appointments and information they need.” He also added, “This effort includes signifi-cantly increased funding for the Edu-cation USA advising centres.”

OVERsEAs

WESTWARD HO!

HEALTH

Cyberstalking Causes Intense StressCYBERSTALKING HAS been proved to cause more intense stress than being harassed or stalked in person, according to a new study in the US.

“It’s a new method for an old problem,” says Dr Elizabeth Carll, a clinical psychologist in Long Island, NY. “Obviously the ones that everyone is aware of is putting false and humiliating information on the internet, such as discussion boards, blogs, message boards, Facebook, as well as sending harassing emails and text messages,” she said. But the psychological fallout from such electronic bully tactics can be even more devastating for those targetted than face-to-face exchanges, said Carll, who presented a talk on the issue on Saturday at the annual meeting of the American Psychological Association in Washington. Twenty per cent of online stalkers use social networking to keep tabs on their vic-tims. A number of American states are looking at legislation to counter cyberstalk-ing, while some already have laws in place.

Good Fat Found!Researchers at Joslin Diabetes Centre and Children’s Hospital Boston have shown that a type of ‘good’ fat known as brown fat occurs in varying amounts in children — increasing until puberty and then declining — and is most active in leaner children. The study used PET imaging data to document chil-dren’s amounts and activity of brown fat, which, unlike white fat, burns energy instead of stor-ing it. Results were published in The Journal of Pediatrics.

“Increasing the amount of brown fat in children may be an effective approach at combat-ing the ever-increasing rate of obesity and diabetes in children,” said Aaron Cypess, MD, PhD, an assistant investigator and staff physician at Joslin and senior author of the paper.

Bigger Brains?The farther that human popula-tions live from the equator, the big-ger their brains, according to a new study by Oxford University. But it turns out that this is not because they are smarter, but because they need bigger vision areas in the brain to cope with the low light lev-els experienced at high latitudes.

Scientists have found that people living in countries with dull, grey, cloudy skies and long winters have evolved bigger eyes and brains so they can visually process what they see, reports the journal Biology Letters.

The study takes into account a number of potentially confound-ing effects, including the effect of phylogeny (the evolutionary links between different lineages of modern humans).

snippeTs

1010 C F O I N D I A AU G U S T 2 0 1 1

cfo i think

Facts & TriviaQUALIFICATION: CA from the Institute

of Chartered Accountants of India

FIRST JOB: IT consultant at TCS

PREVIOUS JOB: Has worked in marketing, operations and HR at TCS. CFO since

2003, ED since 2007

OVER THE LAST FOUR decades with Tata Consultancy Services (TCS), I have managed just about every busi-ness function – project management, sales, human resources and now, finance. Therefore, my worries tend to be very business-oriented, with finance, my current area of responsi-bility, getting greater focus.

The worsening global economic situation is the latest source of worry, particularly because of our high expo-sure to the US and Europe. When economic uncertainty becomes the new normal, we have to be very agile and ever-more responsive to clients’ needs. The client-centric, verticalised organisation structure we unveiled in 2008 is helping us achieve this. We have built a cadre of business finance managers, equipped with superior MIS, who provide business unit heads with the insights and analyses needed to quickly respond to events on the

The CFO and ED of Tata Consultancy Services says currency volatility, uncertainty in the global markets, operational challenges and internal issues such as retaining key talent are matters that keep him awake at night

“Hedging is a short-term fix that helps buy time. On a long term basis, we need to align our costs to an appreciating rupee”

S MAHALINGAM

ground and engage more effectively with clients.

The other worry is the heightened currency volatility. Until recently, it was sufficient to track movement of the INR against the USD alone, since other currencies moved with the USD.

That is no longer so and therefore, I also have to track the GBP, the euro and the Australian dollar. We watch various economic parameters and hedge for the next two to three quar-ters. But hedging is only a short-term fix that helps buy time. On a long term basis, we need to structurally align our costs to an appreciating rupee.

Then, there are organisational challenges. We operate in 42 coun-tries. Coordinating the compilation, consolidation and audit of accounts within days of the quarter-end, across various subsidiaries at all these loca-tions is immensely complex. For it to run smoothly, processes have to be standardised and importantly, we have to foster collaboration and openness within the team.

Our scale and complexity calls for a broad range of expertise within the finance team, not just at the corporate level but also at each key location.

1111AU G U S T 2 0 1 1 C F O I N D I A

Finding the right individuals with the necessary competencies is never easy, but to do that in large numbers, across the globe, makes it a true challenge. Equally important is the need to instil our values in individuals from varying backgrounds and cultures.

Lastly, there is the challenge of retention and motivation. Building

a team takes time, but you can lose key members in an instant. We pride ourselves on our industry-leading retention rates but still, when some-one does leave, all that business knowledge is lost forever. So it’s criti-cal to keep employees engaged and to give them opportunities to grow. A lot of my time and effort goes into

interacting with employees at all lev-els, across the globe, to understand ground-level issues. I don’t begrudge that time. It’s really an investment. After all, when I put in place a self-sustaining institution composed of competent, ethical and highly moti-vated individuals, I’ve earned my right to a good night’s sleep.

very year, there’s more paper-work. Every year, there are greater chances that one missed signature or one missed disclosure could earn your company a fine or even hurt its chances of an impor-tant investment down the line.

How can CFOs keep up with the 200+ filings that companies must make in any given year? In many cases, they simply don’t. Nitin Deshmukh, Chief Executive Officer of Kotak Private Equity Group, a major private equity investor, says that his team seldom conducts due diligence on a company with-

out finding compliance problems. “Without excep-tion, there are almost always issues in mid-sized companies,” says the Mumbai-based investment manager. Most violations are not serious, he says, but a few end up being deal-breakers.

But, as regulations are expected to keep on growing, regulatory experts say it’s important not just to dig out of your current drift, but also to look up and see where the next batch of rules may come crashing down. CFOs and compliance experts agree that an organised approach to filing and a more strategic view of rule-making can go a long way toward better protecting your company – and yourself.

As regulations and compliance pressures grow with stricter corporate governance laws, CFOs across India Inc are gearing up for the challenge so that they don’t get buried under a pile of paper

BENNETT VOYLES SHIGIL N

cover story

13AU G U S T 2 0 1 1 C F O I N D I A 13

Not the worst, but closeWhen it comes to regulation, Indian companies don’t have it easy. One global regulatory benchmark, the World Bank’s Ease of Doing Business in India report, ranks India only 134th in the list of best places in the world to do business. This was based on a composite score that included a ranking of 177th for dealing with construction permits; 164th for ease of paying taxes, payment frequency, and tax rate; and 94th for registering property. China, by comparison, ranks 79th, a bit worse in dealing with construction permits (181), a lot better at registering property (38), and much better on taxes (114). It’s also worse than most of the big developing markets – Mexico, Indonesia, the Russian Federation and Brazil.

Worryingly, things are not always moving in the right direction. Although India keeps creeping up in the rank-ings, the simplification of the general regulations seems to be more than offset by complications in the rules governing specific industries.

One sign that there is more paper in the future of most finance departments: the demand for legal and accounting services is forecast to rise faster than the GDP. RSG Consult-

ing, a UK legal strategy firm, forecast in 2010 that demand for legal services in India will continue to rise by 11 per cent a year over the next five years. Demand for accountants is growing too: in 2010, Ritwik Mukherjee, president of the Institute of Chartered Accountants of India, forecast that the need for fresh graduates would continue to exceed supply any time GDP exceeded six per cent.

It might be tempting to ascribe this growth in red tape to the reputed Indian genius for bureaucracy. After all, wasn’t the reform of Licence Raj supposed to be about less regu-lation? But Vikramaditya Khanna, a professor of law at the University of Michigan Law School, argues that de-regulation has led to economic growth, and that economic growth itself tends to lead to more rules.

“As you go from the particular kind of economic system that India had prior to 1991 and you go toward a more de-regulated system, that doesn’t mean you have no regulation, it means you regulate for the new environment,” Mr Khanna says.

This new environment often brings on more complexity. For example, the rules on foreign direct investment used to be simple, Khanna says. The rule was that no foreigner could buy more than 40 per cent of an Indian business. Now the regulators have changed that – somewhat. Today, the percentage of investment allowed depends on the sec-tor. “Every six months they update the regulations to reflect either new sectors that they’re opening up or additional restrictions or rules that they’re putting into place,” Mr Khanna says.

In addition, the fact that so many Indian companies are going global multiplies the possibility of compliance head-aches as well. For instance, the tough new 2010 British Brib-ery Act applies not just to British companies but to any com-pany with UK links. Penalties are serious, including a stint of

“Without exception, there are almost always

issues in mid-sized companies” —NITIN DESHMUKH,

CEO, KOTAK PRIVATE EQUITY GROUP

cover story

up to 10 years in one of Her Majesty’s Prison Service facilities, an unlimited fine and confiscation of property.

Compliance pressures aren’t only being applied by gov-ernment agencies. Company directors are also much more focussed on the issue than they once were. “They’re actually pushing through a lot of these processes and making sure this mechanism can give them comfort,” says Kaushik Dutta, director of New Delhi’s Thought Arbitrage Research Institute and corporate governance expert.

Why the sudden interest? Recent scandals have made directors more aware of the executive and director’s potential liability if things inside the company turn out to be seriously amiss. “The chance that a director will get convicted may not actually be all that high, but they could get arrested, they could have to wait awhile for the trial,” Mr Khanna says. And he means a while: two-and-a-half years after their arrest, for example, the Satyam defendants are still in jail, waiting for their day in court.

Even if their problems go that far, just a little something amiss could be unpleasant. “If you wake up one morning and one of the 6000 cheques your company issued last week bounced and there’s a cop at your door, that could be stress-ful,” he says.

Facing the challengeHow should CFOs respond to the paper avalanche? Sand-eep Batra, CFO of adhesives and chemicals company, Pidilite Industries, says his office maintains a list of everything that requires some certification; finds the executive who should be responsible for that process; and then follows up to make sure that all filings are made.

Mindtree, the Bangalore-based software firm has actu-ally automated its to-do list, with a database that tracks compliance issues across the 14 countries in which it does business. The tool took around two years to build and still requires constant updating, according to Rostow Ravanan, the company’s long-time CFO. A dashboard attached to the tool signals the status of particular filing issues as red, amber or green, making it easier for them to track issues across the entire organisation.

Mr Batra also encourages communication. Finding out about potential issues as early as possible is one of his priori-ties. “The objective is to capture everything at inception and therefore prevent non-compliance or contravention,” Batra says. “There is no point in trying to be smarter after the event. The thing is to prevent it through whatever ways you can, and do it in an efficient manner.”

In particular, it pays to look at your company’s transactions closely. The biggest issues tend to arise most frequently in land deals and licences, according to Richard Dailly, Manag-ing Director of the Mumbai office of Kroll, the global private investigation service. “Sectors such as infrastructure, mining, power generation and oil are particularly high risk for inves-tors because they require both land and licences,” he says.

CFOs of family-owned companies should be especially careful. “In smaller, family-owned companies, there is very often the view that ‘this is the way business is done’,” Mr Dailly says.

At first, these shortcuts may not be an issue, but later on, they can turn serious. “The problems become apparent when the small companies start to expand and are expected to behave in a more compliant manner, or when a serious investor takes an interest,” he explains. Once a company reaches a certain

“sectors such as infrastructure, mining, power generation and

oil are particularly high risk for investors because they require

both land and licences” —RICHARD DAILLY

MD, MUMBAI OFFICE,

KROLL PRIVATE INVESTIGATORS

15AU G U S T 2 0 1 1 C F O I N D I A 15

size, not complying is no longer an option: “The penalties for non-compliance are so severe it pays to be preventive,” Mr Batra adds.

There have been claims that Indian companies are invest-ing abroad simply to get away from the paper, but regulatory experts say they haven’t really seen it. In any case, he doesn’t

think there’s really any escape. “Most countries have their own specific area of complication. For example, in Brazil, the tax laws are very complicated,” he says.

Getting it rightBesides watching what’s going on inside the company, it’s also a good idea to keep an eye on what the regulators are doing. Most agencies propose regulations first, before issuing final guidelines, and it can be a good opportunity to advise the government about how to make the regulation more bearable for the company, according to Mr Khanna.

Sometimes, a successful lobbying effort can be even more valuable than that. As License Raj veterans know, regula-tion can be a source of competitive advantage: companies are sometimes able to steer law-makers in ways that favour their company over potential competitors. Early last cen-tury in the US, for instance, AT&T president Theodore Vail actually courted government regulation of the fast-growing telephone industry, guessing – correctly as it turned out – that regulation could make them the de facto telephone monopoly for decades.

It pays to keep an eye on what’s going on abroad as well, Khanna says. Even if a company doesn’t have overseas busi-ness, the approach the laws take toward an issue may be a preview of how the rules will eventually evolve. A chemical company, for instance, might want to follow what’s going on in the European Union or the US for an idea of what the requirements and the approach may be down the line.

“If, for example, you’re a biofuels company in India, it may not be a bad idea to see how the markets for that kind of thing developed in Europe or in the US,” Mr Khanna says. “That may not reflect what the rules will be in India – because that’ll be the result of the political process and the regulatory pro-cess – but it may give you some indication of what the likely areas are that … people would want to think about regulating.”

But, however it’s done, it will probably be done. Mr Khan-na believes that, sooner or later, regulators are likely to keep on piling on the forms. “I think it’s safe to assume that the amount of internal compliance work and risk management is likely to increase,” he says. He anticipates growth in a number of areas, all of which are large legal sectors in the US: mass tort claims (suits alleging harm by large groups of people), financial regulation, securities regulation and envi-ronmental regulation. The Companies Bill too, when and if it’s passed, will also lead to some huge changes.

Sometimes timely operational adjustments are also an important part of a compliance programme. For example, MindTree decided a few years ago that compliance issues, particularly around visas, would become tougher in the US because of high unemployment. To better position itself, the company began hiring more locals - a move that raised labour costs in the short term but sidestepped some expensive wran-gling later - and Mr Ravanan says it is now paying off.

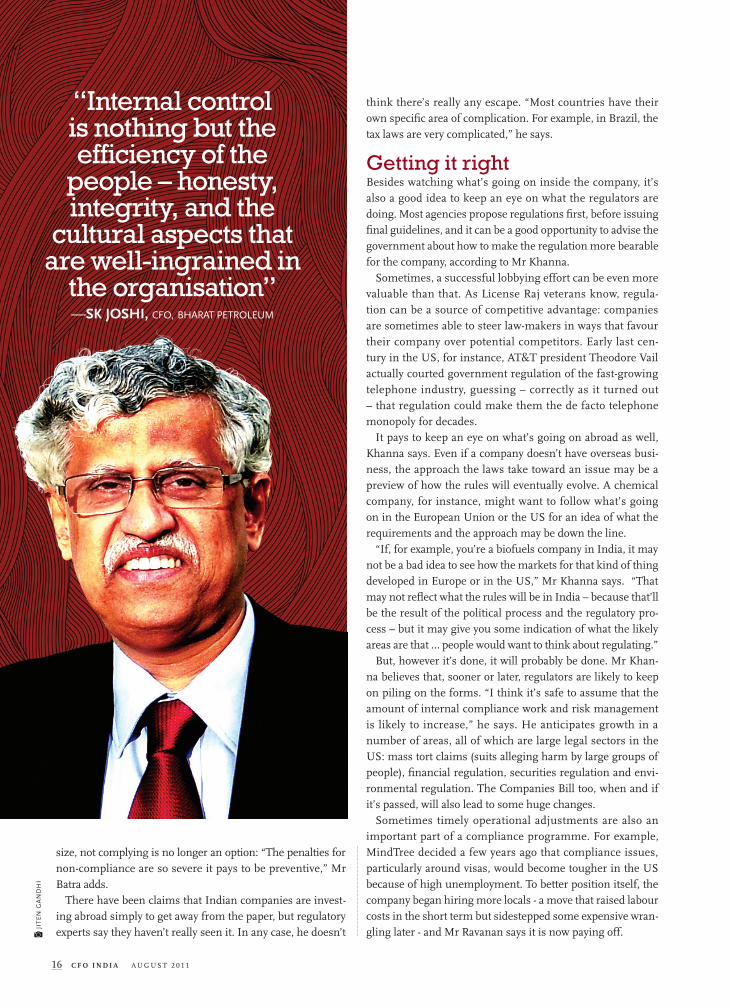

—SK JOSHI, CFO, BHARAT PETROLEUM

“Internal control is nothing but the efficiency of the

people – honesty, integrity, and the

cultural aspects that are well-ingrained in

the organisation”

16 C F O I N D I A AU G U S T 2 0 1 1

JIT

EN

GA

ND

HI

—SANDEEP BATRA, CFO, PIDILITE INDUSTRIES

“the objective is to capture everything

at inception and therefore prevent non-compliance or contravention.

there is no point in trying to be smarter

after the event”

How do you know if you are getting compliance right? One sign is that it is not causing too much angst.

“If there is too much process there will be a feeling of bureaucracy, there will be a feeling of inefficiency, which cre-ates tension,” says Hiren Israni, CFO of Microsoft India. “If there are not enough processes and controls however, then you are spending a lot more time with one-offs and non-com-pliances and things that have fallen off the table. If you have got the right balance and the right culture of doing it the right way...it is more efficient.”

Of course, keeping track of changes in the rules is only one part of compliance. Character matters too. SK Joshi, CFO of Bharat Petroleum, the largely state-owned up-stream oil company, takes a broad view of control issues. “Internal control is nothing but the efficiency of the people – honesty, integrity, and the cultural aspects that are well-ingrained in the organisation,” says Mr Joshi. It’s important to have a good team in place, echoes Israni. Seriousness about com-pliance is a value that tends to filter down from the top, he says, adding that it is essential for the senior management to walk the talk.

Just do itUltimately, even in instances where it seems possible to skirt around a compliance issue, it may pay to go ahead and file. And not just for the government’s sake: investors tend to pay

more for companies where they can see what’s going on. “In general, opaque and complex firms trade at a discount to their break-up value, in part because of the inability of investors to see through their operations,” says Vikas Mehrotra, chair of the department of finance and statistical analysis at the Uni-versity of Alberta School of Business in Edmonton, Canada.

It can reduce some awkward explanations later too. Mr Deshmukh often runs into companies that say they under-stated their profits to avoid taxes and now face the difficult issue of trying to prove to their teams that they are actually more profitable than they look on paper.

Mr Israni sees a positive attitude towards compliance as a factor that builds credibility and eventually adds value to the company’s reputation. “I think it is part and parcel of the fabric that ultimately builds the brand of the organisation,” he says.

More importantly – at least from the CFO’s point of view – is the fact that the CFO is likely to be among the first called on the carpet in the event of a serious compliance problem. Just ask Vadlamani Srinivas, former CFO of Satyam, who spends his days now awaiting trial in Chanchalguda Central Prison along with his fellow accused Satyam executives. If you really, really like to play badminton – Srinivas and the other former Satyam executives reportedly get two hours’ court time a day – it might be an attractive option. Otherwise, you are probably better off filing early and often.

17AU G U S T 2 0 1 1 C F O I N D I A

JIT

EN

GA

ND

HI

orporate governance can be defined as the way in which organisations are directed and controlled. Although practices may vary, the core underlying principles of governance are the same throughout the world. They strive to protect the rights of

shareholders, to create an environment of transparency and appropriate disclosure, and to define the roles and responsi-

While the core principles of governance are the same across the world, the Asian model places emphasis on trust and relationships. A Chartered Institute of Management Accountants study discusses the

differences between the western and Asian approaches.

bilities of stakeholders in running a company. These prin-ciples are necessary to establish a stable and competitive business and, in the case of publicly quoted companies, an attractive destination for investment. National economies also benefit from good governance as a critical component for safeguarding wealth, employment and GDP growth.

Broadly speaking, transparency and agreed rules of engagement are paramount in the west. The focus is on rules (including principles based accounting standards and codes of practice as well as legislation) and transparency,

1818 C F O I N D I A AU G U S T 2 0 1 1

cover story

creating a level playing field for compet-itors. This western model has led glo-balisation, produced most of the stron-gest multinationals and is the bedrock of the world’s developed economies.

Understandably, it is widely viewed as best practice. But, in light of the dispropor-tionate impact of the global financial crisis on western institutions, there is now widespread recognition that there are limits to what such measures can achieve. There is now much more emphasis on behavioural issues.

In Asia, Africa and most emerging markets the approach to business is somewhat different: relationships sometimes take precedence over transparency. This has its roots in systems in which regulations are not always strongly enforced and legal redress can take years or even decades. In this environment business is based on trust and loyalty.

Business leaders in the east and west who understand the differences and can extract the best from both styles may stand to benefit. On the other hand, underestimating the challenge can cause problems. Some western companies stumbled as they expanded into Asia when their rules-based processes clashed with the local culture, for example. At the same time, eastern companies aspiring to become powerful multinationals found that their personal networks became strained and ineffective when stretched across vast distances and different cultures.

the significance of individual relationships in AsiaIndividual relationships have been an integral part of busi-ness for centuries throughout Asia. Entertaining and get-ting the measure of your prospective business partner were often the first steps in making a deal, well before benefits and money were even mentioned. Relationships in companies could trump performance and leaders were greatly respected – their word was law and their decisions indisputable.

John Hooker, Professor of Business Ethics and Social Responsibility at the Tepper School of Business, discussing various shades of nepotism and cronyism, recently wrote: many such cultural differences arise from the fact that western cultures are built on rules and transparency, while most of the world’s other cultures are relationship-based. Westerners trust rule-based institutions; others trust their friends and family far more and are therefore especially keen to cultivate strong relationships.

When doing business with Asian part-ners, western companies are often hin-dered as they grope through an unfamil-

ne of Asia’s most prevalent problems is a reluctance

to question decisions made by

a superior. obedience to father figures is easily transferred to obedience to anyone in authority

iar landscape. Companies and business units in Asia are often run by the founders and their relatives. Knowing the right person in the right place could mean a difference of months, if not longer, in securing a licence or a key meeting.

The reasons that relationships can still mean more than legal contracts are rooted in cultures that value family ties and, by extension, the bonds of friendship highly. Also, until recently in some Asian countries, a political and legal climate in which governments and bureaucracies were seen as unfair reinforced these bonds by making trust a valuable commod-ity. By placing so much emphasis on individual relationships, Asian firms find it harder to implement procedures that are considered best practice in the West, particularly those that increase transparency – e.g., performance-based evaluations. Their employees can view even basic control tools as a lack of trust in them.

One of Asia’s most prevalent problems is a reluctance to question decisions made by a superior. Obedience to father figures is easily transferred to obedience to anyone in author-ity. This is exacerbated in some companies where the chair-man is the founding patriarch. In his 2008 book Outliers, Mal-

colm Gladwell cited an example in which such deference to authority had fatal consequences. In the 1980s and 1990s, national flag carrier Korean Air had one of the world’s worst safety records and its aircraft suffered a series of fatal crashes. Gladwell attributes the problem, in part, to the inability of junior flight officers to challenge a captain’s actions, even when disaster was imminent.

Asian society’s lack of transparency cre-ates a fertile ground for corruption, too.

The shortfall Satyam chairman Ramalinga Raju

admitted to having hidden

cover story

1919AU G U S T 2 0 1 1 C F O I N D I A 19

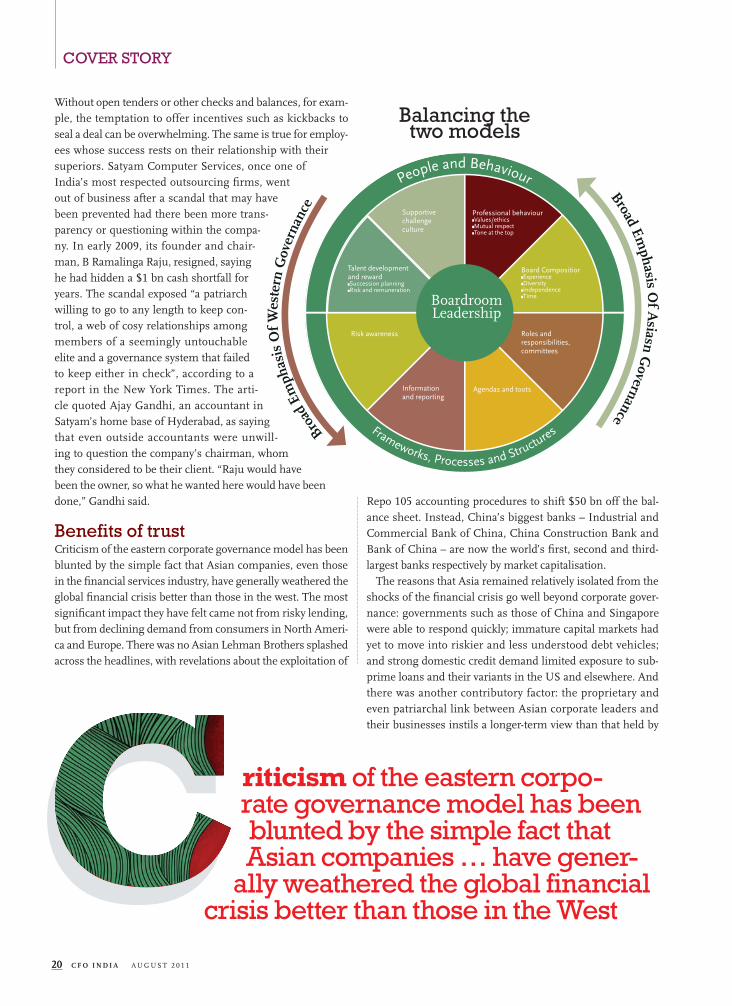

BoardroomLeadership

Professional behaviourValues/ethicsMutual respectTone at the top

Board CompositiorExperienceDiversityIndependenceTime

Talent developmentand rewardSuccession planningRisk and remuneration

Roles andresponsibilities,committees

Supportivechallengeculture

Agendas and tootsInformationand reporting

Risk awareness

People and Behaviour

Frameworks, Processes and StructuresBroad

Em

phas

is O

f Wes

tern

Gov

erna

nce

Broad Emphasis O

f Asiasn G

overnanceWithout open tenders or other checks and balances, for exam-ple, the temptation to offer incentives such as kickbacks to seal a deal can be overwhelming. The same is true for employ-ees whose success rests on their relationship with their superiors. Satyam Computer Services, once one of India’s most respected outsourcing firms, went out of business after a scandal that may have been prevented had there been more trans-parency or questioning within the compa-ny. In early 2009, its founder and chair-man, B Ramalinga Raju, resigned, saying he had hidden a $1 bn cash shortfall for years. The scandal exposed “a patriarch willing to go to any length to keep con-trol, a web of cosy relationships among members of a seemingly untouchable elite and a governance system that failed to keep either in check”, according to a report in the New York Times. The arti-cle quoted Ajay Gandhi, an accountant in Satyam’s home base of Hyderabad, as saying that even outside accountants were unwill-ing to question the company’s chairman, whom they considered to be their client. “Raju would have been the owner, so what he wanted here would have been done,” Gandhi said.

Benefits of trustCriticism of the eastern corporate governance model has been blunted by the simple fact that Asian companies, even those in the financial services industry, have generally weathered the global financial crisis better than those in the west. The most significant impact they have felt came not from risky lending, but from declining demand from consumers in North Ameri-ca and Europe. There was no Asian Lehman Brothers splashed across the headlines, with revelations about the exploitation of

riticism of the eastern corpo-rate governance model has been blunted by the simple fact that Asian companies … have gener-

ally weathered the global financial crisis better than those in the West

Repo 105 accounting procedures to shift $50 bn off the bal-ance sheet. Instead, China’s biggest banks – Industrial and Commercial Bank of China, China Construction Bank and Bank of China – are now the world’s first, second and third-largest banks respectively by market capitalisation.

The reasons that Asia remained relatively isolated from the shocks of the financial crisis go well beyond corporate gover-nance: governments such as those of China and Singapore were able to respond quickly; immature capital markets had yet to move into riskier and less understood debt vehicles; and strong domestic credit demand limited exposure to sub-prime loans and their variants in the US and elsewhere. And there was another contributory factor: the proprietary and even patriarchal link between Asian corporate leaders and their businesses instils a longer-term view than that held by

Balancing the two models

2020 C F O I N D I A AU G U S T 2 0 1 1

cover story

many western executives of a company’s success. Asian business leaders tend to see themselves as custodians of valuable property that will be passed on to future generations. This view inspires a more cautious approach to risk, a deeper under-standing of the business itself and a will-ingness to sacrifice short-term gains for long-term health. “There’s no doubt in my mind that this approach creates a focus on the long-term,” says Charles Tilley, Chief Executive of Chartered Institute of Man-agement Accountants (CIMA).

Balancing thetwo modelsGiving relationships pre-eminence can expose fault-lines in governance: failures and fraud can go undetected, systems that lack transparency become more susceptible to corrup-tion and the rights of minority shareholders are jeopardised, for instance. But, as the global crisis has shown, the west-ern model also carries its share of risk, including an intense focus on short-term shareholder value that can overshadow the prospects of long-term sustainability. The weaknesses of both models must be addressed as the global economy enters a new era, and their advantages preserved. Shareholder value and trusted relationships are not exclusive. They can (and possibly should) co-exist in a governance model that balances the two approaches. CIMA’s boardroom leadership frame-work provides a useful basis for understanding the relative merits of the two models.

the cIMA boardroom leadership frameworkThis was designed to illustrate how a number of critical fac-tors are necessary to achieve board effectiveness – and, by implication, good governance. It can be applied to under-stand the Asian and western corporate governance models.

The diagram is divided into two halves: people and behaviour frameworks, processes and structures

Broadly speaking, the Asian model has placed relatively more weight on the people and behavioural aspects of gover-nance, while the western model has tended to address struc-tural and process issues.

But, as we have seen, the financial crisis is leading to a reap-praisal of western approach: more attention is being paid to behavioural issues. And, while the Asian model emphasises relationships, it is important to recognise the need for sup-porting tools and frameworks to ensure that decisions are made for sound reasons – i.e., whether work will be done properly – and not purely to maintain a relationship.

Western-style rules and transparency have been shown to aid corporate gover-nance, although corporate governance by itself cannot ensure success, of course. In Asia, where so many businesses are controlled by majority shareholders, com-panies’ fortunes are more directly inter-twined with the interests of their ‘owner-shareholders’. Minority shareholders, on the other hand, can be classed as ‘investor-shareholders’, who have shorter attention spans and may simply be looking for quick returns.

These two groups have divergent interests. Investor-shareholders have only one stakeholder role – that of shareholder – and they are generally seeking only personal benefits. Owner-shareholders are possibly more accepting of multiple

stakeholder roles, as they may feel a more direct responsibility towards business associates, employees and the community, at which level personal relationships play an important role.

But beyond the relationship level there may be a dimin-ished acceptance of stakeholder responsibility, such as towards the environment, which is where the western gover-nance model may be more effective through stricter regula-tion and enforcement.

Yet, while the relationship-based model promotes longer-term thinking, rules and transparency are essential in help-ing to prevent the excesses of individuals, especially those at the top of the corporate ladder. ‘Old-boy networks’, as they are known in the west, can often hide dealings that are illegally detrimental to competition, customers and community alike. Many western standards and laws have been set in place spe-cifically to break these opaque networks.

In practice, many multinationals from the east and west have approached finding a balance by mixing employees from the home office with local staff, particularly in senior roles. Managed badly, this structure can create damaging conflicts between expatriate and local views. Managed well, it can create a healthy tension that brings out the best of both views. Sophisticated recruitment policies are crucial to craft-ing a functional team, as are performance metrics that are customised for local contexts.

In helping companies in both the east and the west find this balance, management accountants must be careful not to impose haphazardly western models that have their own intrinsic faults. Instead, they would be wise to understand the benefits that relationship-based models offer and help to create a system that mitigates the disadvantages and keeps the advantages through appropriate financial plans, incentive structures and information systems. Those who are success-ful will build tremendous shareholder value.

There were no banks collapsing in Asia, like Lehman Brothers. Instead the world’s top 3 banks by market

cap are now Asian banks

2121AU G U S T 2 0 1 1 C F O I N D I A

cover story

21

2222 C F O I N D I A AU G U S T 2 0 1 1

CFOProfile NiSHANT fADiA

GLOBAL CFO, PRIME FOCUS

In the 11 years he has spent as CFO of Prime Focus, one of the world’s leading visual entertainment firms, Nishant Fadia has led M&A deals in three continents, raised funds, launched an IPO and seen the company grow from a `3 crore baby to a `500 crore MNC

ONE OF HIS EARLY dreams died young: Nis-hant Fadia was never quite good enough to make it to the Indian cricket team. Of course, the 34-year-old sometimes dreams of receiving an SOS from MS Dhoni to turn his arm over for the men in blue. But Fadia is not complaining. Why would anyone, if he happens to be head-ing the global finance team of a company that is responsible for those stunning special effects in Harry Potter & the Deathly Hallows, Star Wars and the soon-to-be-released Ra-One?

As CFO of Prime Focus, one of the world’s largest visual entertainment services companies, Fadia is in the hot seat. Over the last 11 years he has seen the company rise, as it achieved a `1000 crore market cap and generated over `500 crore revenue. In that time, he closed M&A deals across three continents, raised capital and played a key role in making Prime Focus a world leader in its field.

What makes this self-confessed cricket fanat-ic’s story different is that till late into his college days, being a chartered accountant didn’t fig-

DHIMAN CHATTOPADHYAY

JI

TE

N G

AN

DH

I

3DVisionFocussed:

Finance in

CFO PROFILE

2323AU G U S T 2 0 1 1 C F O I N D I A

FIRST JOB Deloitte Haskins

A HA! MOMENT When we did the

IPO in 2006

TOUGHEST CHALLENGE:

Managing the finances during the economic crisis

LESSER KNOWN SIDE: I am miserly when it comes to spending on myself

DREAM To bowl to

members of the Indian cricket team one day

MileSToNeS

CFO PROFILE

2424 C F O I N D I A AU G U S T 2 0 1 124 C F O I N D I A AU G U S T 2 0 1 1

CFOProfile

ure in his list of priorities. “If not a cricketer, I wanted to be a lawyer. My uncle is a lawyer and seeing the way he dressed and the aura around the profession, I wanted to study law,” says Fadia as we sit in his plush office on top of a hill, just a stone’s throw from Mumbai’s Film City.

Born into a business family (his father and uncles own and run a textile business), enter-prise, he says, was in his blood from an early age. Only, he didn’t want to run the family busi-ness. “My grandfather convinced me to sit for my CA exams, since he believed that even if I didn’t join the business, I needed a good ground-ing to understand how businesses work,” recalls Fadia. He became a CA in 1999 and soon after, completed a CPA from USA and joined Deloitte the following year.

Perhaps he would have stayed on at the famous auditing firm. But at this point (in 2000), his childhood friend Namit Malhotra made him an offer that he couldn’t refuse. “Namit (the founder and CEO of Prime Focus) and I have been friends since we were children. From the day he started Prime Focus in his garage-cum-office, I would have informal discussions with him about the finances of the company. So I knew a lot about the firm even before I joined,” says Fadia. At the time, the company was tiny, with annual revenues of less than `3 crore. “We had just moved out of the garage to a small office and the total staff strength was 25,” he smiles. Today the multinational firm has opera-tions in India, UK and USA and employs over 4,000 people.

It is interesting to note that Fadia never real-ly worked his way to the top like most other CFOs. The reason is simple: he began his career in Prime Focus as the head of finance. “To be fair, operations were very small, so there wasn’t much of a team. I was the man handling finance, so obviously I was heading it,” he laughs. But as operations grew with acquisitions across conti-nents, the company became a global player.

At 34, Fadia’s experience is rich and varied. Over the years he has led M&A deals in India, UK and USA, successfully bringing on board private equity (from Adlabs), strategic investors (Reliance Capital) and financial investors (Rakesh Jhunjhunwala). His biggest moment however, was the IPO in 2006. “We had been planning it since 2001, but we were too small back then and

experts advised us against an IPO. By 2006, how-ever, we were aiming big and needed to take the next step,” says Fadia. The experience was nerve wracking but one that he cherishes. “It was a ter-rible time for an IPO in hindsight. In June 2006, the day our roadshows began, the stock markets shut down. Bankers and investors were worried and people didn’t give us a chance. Nonethe-less, we launched the IPO and got a mere 2X

FADIA IS A WORKAHOLIC WHO IS IN OFFICE SIX DAYS A WEEK BUT AT HOME HE LOVES TEAMING UP WITH

HIS TWINS TO PLAY CRICKET. HE ALSO ENJOYS READING

fAvouriTe PickS

NEWSPAPERS

TOI/ET

MAGAZINES

FILM TRADE

MAGAZINES

BOOK

ALL JOHN

GRISHAM

BOOKS

DESTINATION

LAKE DISTRICT

& SCOTLAND

MOVIE

AGNEEPATH &

ANDAAZ APNA APNA

2525AU G U S T 2 0 1 1 C F O I N D I A 25AU G U S T 2 0 1 1 C F O I N D I A

CFOProfile

subscription. In retrospect we know we could have done things differently, but it was a great experience,” he says.

The year 2006, was a landmark one for the company in other ways too. In April, it acquired British postproduction firm VTR plc for GBP 4.7 mn. Three more companies were also acquired and consolidated in the UK. A year later, PF crossed the Atlantic to North America with the purchase of Post Logic Studios and Frantic Films for $43 mn. These acquisitions allowed Prime Focus to offer cutting-edge services and technol-ogy in Los Angeles, New York, Vancou-ver and Winnipeg.

His big sleepless moment, though, came in 2009 during the economic cri-

sis. “The toughest challenge was deal-ing with negative perceptions. Our scrip fell from 1,300 to 52 between October 2008 and September 2009. Banks were losing confidence and investors were getting jittery. It was a character defining moment for all of us,” he says.

The last 12 months in contrast have been brilliant for PF. “We have been one of the first to hitch a ride on the 3D band-wagon. In March, we worked on Clash of the Titans, the world’s first 3D conversion of a film,” Fadia says. The financial results also bear testimony to this success. Profits after tax in 2010-11 is a healthy `76 crore, up from `33 crore in the previous year, a 120 per cent jump.

Looking ahead, Fadia sees the company double its size in the next few years. “We will have to retain our leadership position in the 3D market. Our VFX is also set to grow manifold,” he reveals.

As we head for the photo shoot, I ask him if he gets any time to spend with his twins and his wife, given his hectic schedule. “At home my seven-year-old sons and I make up a team of naughty boys. Sundays are spent playing crick-et,” he says with a smile.

He still has one other dream: that one day he will spend Monday and Tuesday mornings playing cricket with his sons. And, maybe even bowl a few at MS Dhoni. Who knows!

“The toughest challenge was dealing with negative perceptions. Our scrip fell from 1,300 to 52 between October 2008 and September 2009”

in practice BEST PRACTICES

2626 C F O I N D I A AU G U S T 2 0 1 1

PATRICK SWEENEY

WHAT WOULDPETER DRUCKER DO?Peter Drucker, arguably the most influential management thinker of the last century — was known for teaching that the best leaders ask the right questions. Two chief financial officers discuss how they apply Drucker’s techniques to their current business issues

Peter Drucker, the manage-ment consultant and author widely credited with inventing the discipline of management, had an insatiable curiosity and an uncanny ability to ask questions that got to the heart of the matter. His messages focussed on self-discovery, which he viewed as an intro-spective and creative journey required of every leader.

As Drucker frequently noted in his books, articles and lectures, the best leaders ask the right questions. And the right questions don’t change as often as the answers do. Leaders — from author Jim Collins to legendary General Elec-tric Corp. Chief Executive Jack Welch — have each said that a day they spent with Drucker was the most memorable day they’d ever had.

Welch recalled Drucker questioning him: “If you weren’t in this business today, would you invest the resources to enter it?” Delving into that with Drucker, led Welch to issue his famous

edict that each of GE’s businesses had to be No. 1 or No. 2 in its market or the manager would have to sell it or close it.

Winston Churchill described Drucker as a guiding light who makes us think. When asked at the right time, a ques-tion as deceptively simple as, “Who is your customer?” can cause an executive to re-evaluate his or her strategy.

Born at the beginning of the last century, Drucker trained as a journal-ist and received his doctorate in public and international law. From 1971 to his death in 2005, he was the Clarke Profes-sor of Social Science and Management

at Claremont Graduate University. In 1987, in his honour, the university’s management school was named the Peter F. Drucker Graduate School of Management (later known as the Peter F. Drucker and Masatoshi I to Graduate School of Management). He taught his last class at the school in 2002 at age 92.

Drucker became a highly sought-after consultant when his book Concept of the Corporation became an international bestseller. He subsequently authored 39 books.

Drucker emphasised two things: asking and listening. And his lessons and questions still resonate with corporate executives.

Michael McLamb, Executive Vice President and Chief Financial Officer of boating and yachting retailer MarineMax Inc., in Clearwater, Fla., says that in his experience chief financial officers tend to lead by asking questions. He empha-sises, however, that while questioning is important, “You want to make sure

The age till which Peter Drucker

continued to take classes

92

2727AU G U S T 2 0 1 1 C F O I N D I A

in practice

your questions are asked in a way that is open, curious and provokes exploration and keeps the ideas flowing.”

He says that questioning “should foster creativity, not shoot it down.” McLamb says he often finds that “what may sound like a crazy idea can be tweaked so that a slight derivation of it can be a really good thing for the company. When people say ‘no’ to an idea too quickly, the entire room gets shut down. And the next time you are in a meeting, ideas are less likely to be offered and considered.”

McLamb also believes that CFOs, in general, ask more questions “to make

Drucker became a highly sought-after consultant when his book Concept of the Corporation became an international bestseller. He subsequently authored 39 books

sure that we understand something completely and to make sure that the individual making the suggestion understands the ramifications and has thoroughly thought through what they are proposing.”

McLamb says he is a fan of Drucker and his teachings. “We all still ben-efit today from his approaches and les-sons,” he adds.

Bill Anderson, CFO of Boston-based diamond company, Hearts On Fire, says that, “to be an effective CFO, you’ve got to listen at least 50 per cent of the time. It is important to understand everyone’s point of view.”

The rest of the time, he says, the CFO should be asking questions. “To thrive in the business world requires the per-spective of every key voice. Any business run strictly by finance would be stifled.” So, he adds, CFOs need to understand the different alternative lenses that oth-ers peer through, and try to help every-one arrive at the best solution — not the compromise solution, because the compromise is rarely the best solution.

Questions that should be asked, says Anderson, include: “Which solution best meets the needs of the business opportunity?” “Are we still maintain-ing the integrity of the brand?” “Are we

2828 C F O I N D I A AU G U S T 2 0 1 1

In PRACTICE

28 C F O I N D I A AU G U S T 2 0 1 128

being financially responsible?” “Have we minimised the risks, and maxi-mised the opportunity?”

CFOS AS DECISION-MAKERSHow do CFOs help other decision-mak-ers at the executive table to consider the right questions? How can they promote debate about an idea, or an idea that might be derived from that idea? How can they question a half-baked idea while still encouraging innovation?

McLamb says his questioning “usual-ly stems from an in-depth understand-ing of our company, as well as of our brand, our culture, our capabilities, our competition, the marketplace and our clients’ needs.”

Then, he says, in weighing the pros and cons of an idea, his questions will focus on “understanding the implica-tions of the idea for myself, as well as clarifying for others whether this is an idea that we want to put on the fast track or one that needs further refine-ment.” Through questions, CFOs try to provide a solid understanding for themselves and everyone else of the core issues that need to be considered.

McLamb, who has been with Marine-Max for 13 years, attributes his ques-tioning approach to his background in public accounting, having been with Arthur Anderson nearly 10 years. “It

was a great education to be involved with so many different types of clients and experiences. I learnt an enormous amount from senior executives with differing philosophies, styles and cul-tures, who were making decisions that sometimes helped their companies grow and sometimes made mistakes that had to be quickly corrected.”

Beyond his education and experi-ence, McLamb believes his questions are also keenly influenced by his pre-dominantly thorough nature. The tra-jectory of his questions is the result of a need to understand the nuances, hid-den concerns and possible potential of a new idea.

Through his questions, McLamb says, he is also seeking to understand how a new idea could integrate with the company’s current offerings. “Some-times literally just walking through a procedure can shed some light on how to improve or enhance an idea,” he adds. “In our business, we carry premium brands of boats, and we have to be very disciplined about any new brands we bring on. One of our core philosophies is not to take on directly competitive products,” he says. So, he adds, “there is always questioning around making sure that a new brand would not, in any way, eat away at our

market share for the other premium brands we carry.”

Especially during the economic downturn, he says, his company has had many manufacturers knocking on its doors. The process for a poten-tial new brand is to “run the decision through our brand funnel to make sure it reflects the quality for which we’ve become known. Is it well supported by the manufacturer? Does it compete with one of our current brands? If it is in a gray area, how do we weigh our decision?” McLamb asks. He adds, “At such junctures, it is important that the right questions are asked.”

Hearts on Fire’s Anderson says the last thing he wants to do is throw water on an idea that may have some merit. At the same time, “I have to ask some important questions to make sure that if we are going to run with a new idea and seize the moment that we have a clear understanding of what is needed to incorporate the idea into our game plan,” he adds. “Have we thoroughly considered and weighed the risks? Are we set up to deliver?”

While he encourages input from oth-ers and is open to new ideas, Anderson also has a structured side, so he needs to know that all bases have been covered and all the details have been thought through before he agrees to move for-ward on new ideas.

One of the most important decisions Hearts On Fire has been weighing is entering the China market. As a fast- growing luxury market company, it has been preparing for the past seven years and is poised to start doing business in

to thrive in business requires the perspective of every key voice. any business run strictly by finance would be stifled”

– BILL ANDERSON, CFO, Hearts On Fire

Asking questions leads to better results,

9 out of 10 times

90%

2929AU G U S T 2 0 1 1 C F O I N D I A

In PRACTICE

29AU G U S T 2 0 1 1 C F O I N D I A

China this year, Anderson says. Seizing that opportunity took getting the right answers to many questions. It was clear, he says, “that we needed to be in China. It was just a matter of how and when.”

In its nearly seven years in existence, the company opened six Hearts On Fire stores in Taiwan, during which time, Anderson says, “we learnt as much as we could about how to succeed in that region of the world.” The firm also opened a regional headquarters in Hong Kong.

By doing so, Anderson says senior management “has been able to answer many of the questions that were holding us back, so there are fewer unknowns.” Diamonds are becoming even more precious than gold in China as a display and celebration of wealth,” he says. “Now is the right time for us to seize this opportunity.”

He concedes going forward there will still be many questions, but “we are ready for them — because we have carefully prepared for and answered the fundamental questions.”

ASKING THE RIGHT QUESTIONS Anderson also encouraged Hearts On Fire’s Founder and CEO, Glenn Roth-man, and President, Mark Israel, to consider other questions before the firm enters China.

Among those: “What will the busi-ness structure be?” “Do we have the resources to support that business structure?” “Will this focus take away from our other ventures?” “What are the border issues?” “Where will signifi-cant financial transactions take place?” “Do we sell into China or invest in our Chinese operations?” “How do we pro-tect the integrity of our brand?”

Generally, CFOs question ideas to probe further, to make sure that every- thing comes together so that they, and others in senior management roles, are assured of when is the right time to seize a new opportunity.

McLamb underscores that in addi-tion to being thorough and curious, one of the most important character-istics a CFO needs is the ability and desire to collaborate — something, he says, that he’s learnt over the years. “The initial response of someone with a financial background is to be conser-vative and to respond with a dozen rea-sons not to pursue an opportunity. But as I grew into the position, I began to understand that there are many ideas that come along — and you’ve got to work those ideas and understand what’s being proposed and look for a solution rather than looking for a way to stop something.”

In addition, he ponders: “When there is a proposition on the table that can have a significant impact on the company, or certainly has a significant price tag, it is the CFO’s role to really

get comfortable with that idea. Should the idea be pursued or dropped?” Nearly 90 per cent of the time, he says, by asking questions, a group comes to a better conclusion.

Drucker encouraged his followers to ask questions, though to not look for answers the way you were taught in school. “Schools are organised on the assumption that there is only one right way to learn and that it is the same for everybody,” he wrote in Managing One-self. But, there is not one right answer. Life is not a multiple-choice test. It’s more about filling in the blanks. And, Drucker writes, what is really most important is to ask the right questions at the right time. The right answers will follow. The best CFOs have come to know this intuitively.

A final thought from Drucker: “Don’t believe assumptions. Keep asking ques-tions. And don’t settle for anything less than the best possible answers.” Any questions now?

PATRICK SWEENEY (PATRICK@CALI-PERCORP .COM) IS PRESIDENT OF CAL-IPER, A TALENT MANAGEMENT CON-SULTING FIRM ENTERING ITS 50TH YEAR OF HELPING COMPANIES HIRE AND DEVELOP TOP PERFORMERS

FINANCIAL EXECUTIVE | JULY 2011 | (C) 2011 FINANCIAL EXECUTIVES INTER-NATIONAL | WWW.FINANCIALEXECU-TIVES.ORG

When people say ‘no’ to an idea too quickly, the entire room gets shut down. and the next time you are in a meeting,

ideas are less likely to be offered”– MICHAEL MCLAMB, Executive Vice President and CFO,

MarineMax Inc

32 C F O I N D I A AU G U S T 2 0 1 1

Case Study

The financial position of Aditya Birla Nuvo has gone from strength to strength since Sushil Agarwal’s appointment as CFO in 2009. The debt burden has been reduced, cash-strapped subsidiaries given a lifeline and the lifestyle division made profitable

DHIMAN CHATTOPADHYAY

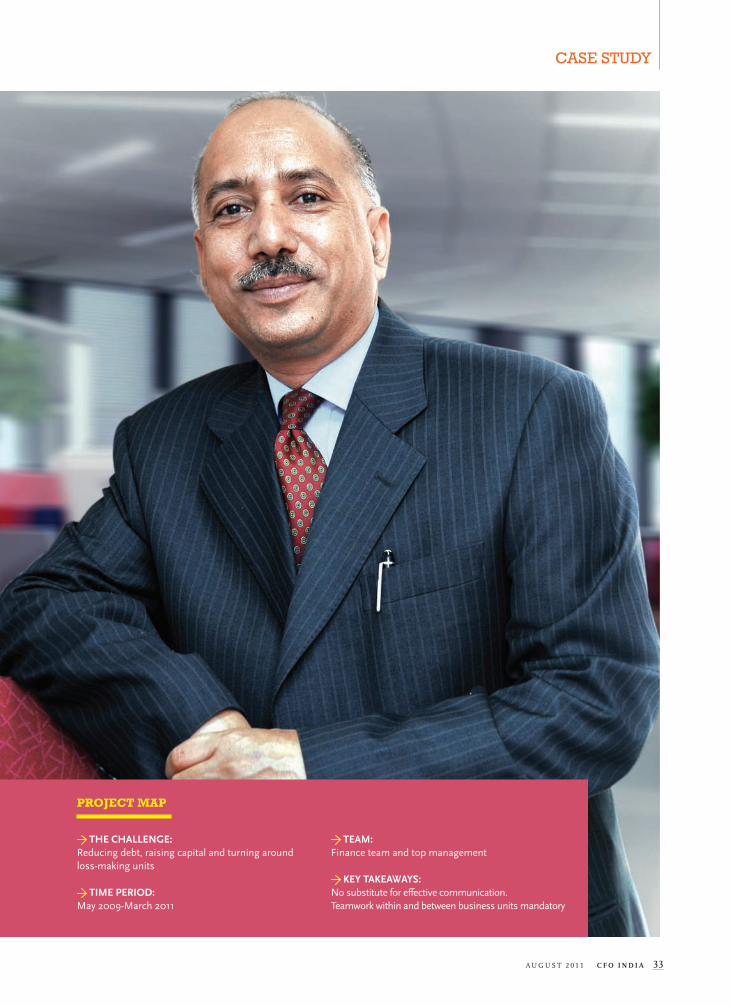

When Sushil Agarw-al became CFO of Aditya Birla Nuvo (AVNL) two years ago, the diversi-

fied conglomerate was grappling with serious challenges, each threatening the growth prospects of the $4 bn firm.

Having spent the past two decades in various business units of the AV Birla Group, Agarwal knew if the challenges were to be dealt with successfully, he had to convince his colleagues to rally around

quickly. “The biggest headache at this stage was the high debt and the resul-tant stress on the balance sheet. Con-servation of cash was another challenge and we also had to turn around a loss making unit,” he recalls as we sit in his office at Nuvo’s Mumbai headquarters.

TACKLING THE CHALLENGESAgarwal, who has recently been elevat-ed to the Board at ABNL, remembers that back in 2008-09, the company had

a gross debt of ` 4500 crore, and a fur-ther ` 5300 crore of strategic invest-ments in subsidiaries. “We had to raise additional borrowings in 2009 to fund part of the investment requirement and maintain liquidity. Unfortunately, this coincided with the global financial cri-sis,” he recalls. While the amount was sufficient to meet the funds require-ment for investments and loan repay-ments in the 2009-10 financial year, it weakened ABNL’s leveraging position.

“I faced a Catch-22 situation that

Using Communication

weaveto

magicfinancial

33AU G U S T 2 0 1 1 C F O I N D I A

Case stUdy

THE CHALLENGE:Reducing debt, raising capital and turning around loss-making units

TIME PERIOD:May 2009-March 2011

TEAM: Finance team and top management

KEY TAKEAWAYS:No substitute for effective communication. Teamwork within and between business units mandatory

Project MaP

34 C F O I N D I A AU G U S T 2 0 1 1

Case stUdy

“the biggest headache for the organisation at this stage was its high debt and the resultant stress on the balance sheet. Conservation of cash was another big challenge”

required urgent action,” Agarwal explains. Convinced that they needed to focus on growth at this stage, Agar-wal and his team evaluated all possible fundraising options based on the long-term need of funds, timelines and vola-tility in the stock markets. “Finally, fund infusion through preferential allotment to the promoters, emerged as the quick-est and most appropriate option. Meet-ing deadlines was essential. I was lucky to have a a great team,” he admits. The entire team played their defined roles to complete this equity infusion of `1,000 crore in ABNL.