ch. 1 managerial accounting in the information age (jiambalvo)

TRANSCRIPT

CHAPTER 1

Managerial Accounting

In the

Information Age

Slide 1-2

Managerial Accounting ( pp. 4-6)

Managerial accounting is designed for

internal users

(Internal Reporting vs. External Reporting)

The goal of Managerial Accounting is to

provide the information managers need for

- Planning

- Control

- Decision making

Slide 1-3 Learning objective 1: State the primary goal of

managerial accounting

Planning ( p. 4)

Slide 1-4 Learning objective 2: Describe how budgets

are used in planning

單位成本 = $0.518 ($2,590,000 / 5,000,000) Special Order $0.51 ?

單位變動成本 = $0.41 (1,500,000+400,000+150,000) / 5,000,000

單位固定成本 = $0.048 (60,000+80,000+100,000) / 5,000,000

Planning and Control Process

Slide 1-5

Learning objective 3: Describe how performance reports are

used in the control process

編制預算

實際成本

預算 vs.實際

績效評量

( p. 5)

Sample Performance Report

績效評量 (實際 vs. 預算)

Slide 1-6 Learning objective 3: Describe how performance reports are

used in the control process

( p. 6)

Managerial vs. Financial Accounting ( p. 7)

Unlike Financial Accounting, Managerial

Accounting:

Is directed at internal users

May deviate from GAAP

Presents more detailed information

May present more nonmonetary

information (顧客滿意度, 不良率, Lead time,…)

Places more emphasis on the future

Slide 1-7 Learning objective 4: Distinguish between financial

and managerial accounting

Cost Terminology ( p. 8)

Variable Costs (直接材料,直接人工,..) - Change in proportion to changes in volume or activity

Slide 1-8 Learning objective 5: Define cost terms used in

planning, control, and decision making

Cost Terminology ( p. 9)

Fixed Costs (折舊,保險費,房地產稅) - Do not change in response to changes in volume or

activity

Slide 1-9 Learning objective 5: Define cost terms used in

planning, control, and decision making

Cost Terminology ( p. 9)

Sunk Costs 沉沒成本

- Costs incurred in the past

- Not relevant to present decisions

Opportunity Costs 機會成本

- Values of benefits foregone when selecting one alternative over another

Slide 1-10 Learning objective 5: Define cost terms used in planning,

control, and decision making

Cost Terminology

Direct and indirect costs直接成本&間接成本

- Direct costs are directly traceable to a

product, activity, or department, indirect

costs are not traceable (Allocation分攤 )

Controllable & noncontrollable costs

- A manager can influence controllable

costs but cannot influence non-

controllable costs可控制成本&不可控制成本

Slide 1-11 Learning objective 5: Define cost terms used in

planning, control, and decision making

Direct and Indirect Cost ( P. 10)

Slide 1-12 Learning objective 5: Define cost terms used in

planning, control, and decision making

Allocation:

水電費 保險費 房地產稅 機器折舊 間接人工

直接材料,直接人工

間接成本 直接成本

保險費

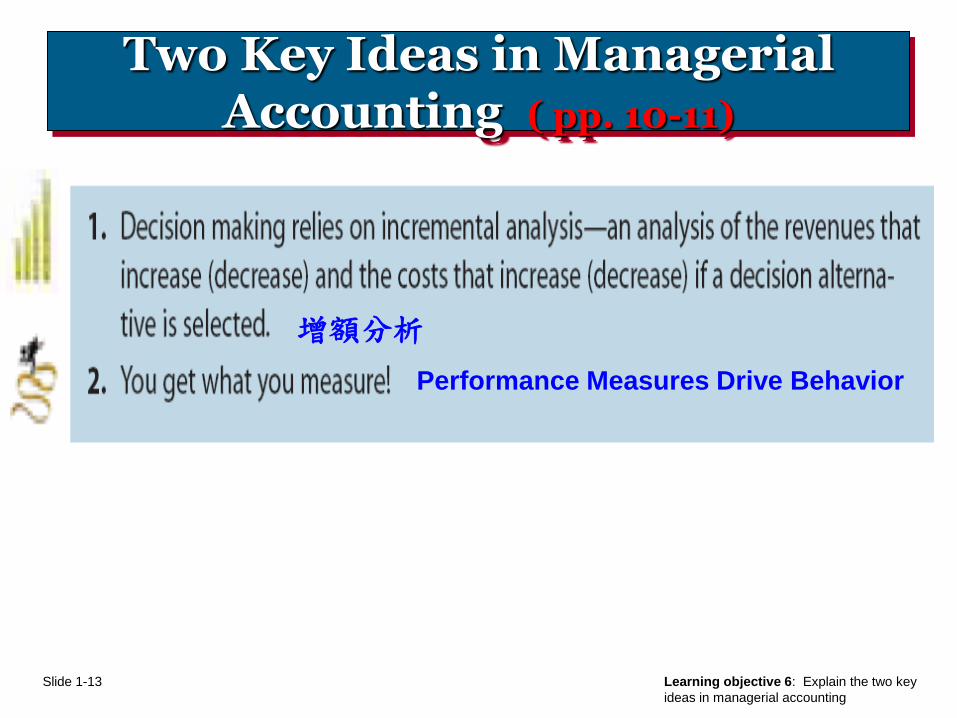

Two Key Ideas in Managerial Accounting ( pp. 10-11)

Slide 1-13 Learning objective 6: Explain the two key

ideas in managerial accounting

增額分析

Performance Measures Drive Behavior

The Value Chain ( p. 14)

Slide 1-14 Learning objective 7: Discuss the impact of information technology on competition, business processes and

the interactions companies have with suppliers and customers

Finished Good Shipping Material Warehouse

基礎建設

採購

(R & D)

(HR or People Team)

Impact of Software Systems on the Value Chain (p. 15)

Enterprise Resource Planning (ERP) - Computerize inventory control and production

planning

Supply Chain Management (SCM) - Organization of activities between a company and

its suppliers

Customer Relationship Management (CRM) - Manages a variety of customer interactions

Slide 1-15 Learning objective 7: Discuss the impact of information technology on competition, business processes and

the interactions companies have with suppliers and customers

Customer Relationship Management (p. 19)

Slide 1-16 Learning objective 7: Discuss the impact of information technology on competition, business processes

and the interactions companies have with suppliers and customers

Ethical and Unethical Behavior

Examples of unethical behavior不道德的行為

Enron managers mislead investors by hiding debt, i.e. Kenneth Lay, CEO, found guilty of fraud

WorldCom overstated profits, i.e. Bernard Ebbers, CEO, received a 25 year prison sentence

Dennis Kozlowski, head of Tyco, was charged with avoiding taxes

Sam Waksal, cofounder of IMClone, was charged with insider trading

Slide 1-17 Learning objective 8: Describe a framework

for ethical decision making

(pp. 16-17)

Sarbanes-Oxley Act (p. 17)

Slide 1-18 Learning objective 8: Describe a framework

for ethical decision making

Enacted by Congress in July 2002 (SOX Act)

Requires CEO and CFO to certify that the financial

statements do not contain any untrue statements or

omissions

Bans certain types of work by the company’s

auditors to ensure their independence

Provides for longer jail sentences and larger fines

for executives (i.e. fines up to $5 million and jail

terms up to 20 years)

Requires companies to report on the existence and

reliability of internal controls

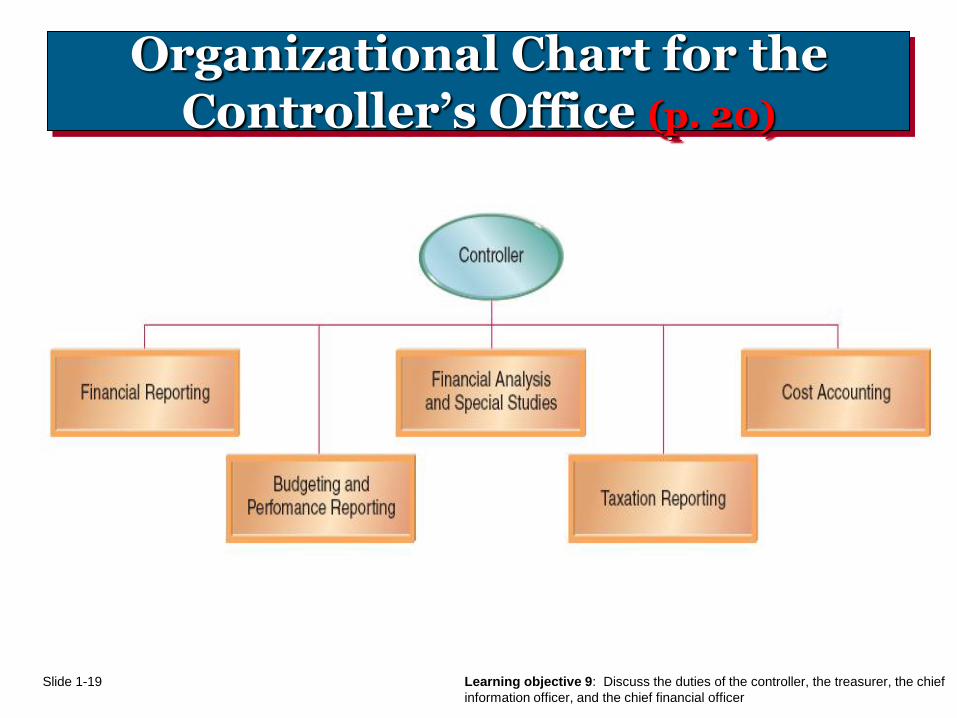

Organizational Chart for the Controller’s Office (p. 20)

Slide 1-19 Learning objective 9: Discuss the duties of the controller, the treasurer, the chief

information officer, and the chief financial officer