ch12 all macro__lecture_ppt

TRANSCRIPT

© 2015 Pearson Education, Inc

Chapter 12

Short-Run Fluctuations

12 Short-Run Fluctuations

Chapter Outline

12.1 Economic Fluctuations and Business Cycles

12.2 Macroeconomic Equilibrium and Economic

Fluctuations

12.3 Modeling Expansions

EBE What caused the recession of 2007‒2009?

© 2015 Pearson Education, Inc

12 Short-Run Fluctuations

Key Ideas

1. Recessions are periods (lasting at least two

quarters) in which real GDP falls.

2. Economic fluctuations have three key features:

co-movement, limited predictability, and

persistence.

© 2015 Pearson Education, Inc

12 Short-Run Fluctuations

Key Ideas

3. Economic fluctuations occur because of

technology shocks, changing sentiments, and

monetary/financial factors.

4. Economic shocks are amplified by downward

wage rigidity and multipliers.

© 2015 Pearson Education, Inc

12 Short-Run Fluctuations

Key Ideas

5. Economic booms are periods of expansion of

GDP, associated with increasing employment

and declining unemployment.

6. Three key factors contributed to the

2007‒2009 recession: a collapsing housing

bubble, a fall in household wealth, and a

financial crisis.

© 2015 Pearson Education, Inc

12.1 Economic Fluctuations and Business Cycles

Economic fluctuations or business cycles:

Short-run changes in the growth of GDP.

We can examine the business cycle by comparing

the path of real GDP to a trend line.

© 2015 Pearson Education, Inc

© 2015 Pearson Education, Inc

12.1 Economic Fluctuations and Business Cycles

Exhibit 12.1 Real U.S. GDP and a Trend Line (1929‒2013;

billions of 2009 constant dollars)

We can also examine the business cycle by

plotting the percent deviation of real GDP from

the trend line.

Question: What historical episodes can you

identify in the data?

© 2015 Pearson Education, Inc

12.1 Economic Fluctuations and Business Cycles

© 2015 Pearson Education, Inc

12.1 Economic Fluctuations and Business Cycles

Exhibit 12.2 Percent Deviation Between U.S. Real GDP and

Its Trend Line (1929–2013)

Answer:

• Great Depression from 1929 to 1940

• World War II from 1941 to 1945

• Great Recession from 2007 to 2009

© 2015 Pearson Education, Inc

12.1 Economic Fluctuations and Business Cycles

A recession is defined as episodes of negative

economic growth.

An expansion is defined as a period of positive

growth. Expansions are periods between

recessions.

Since 1929, a recession has occurred about once

every six years, and recessions have lasted on

average about one year.© 2015 Pearson Education, Inc

12.1 Economic Fluctuations and Business Cycles

© 2015 Pearson Education, Inc

12.1 Economic Fluctuations and Business Cycles

Exhibit 12.3 U.S. Recessions from 1929 to 2013

Economic fluctuations have three key properties:

1. Co-movement of many macroeconomic

variables

2. Limited predictability of fluctuations

3. Persistence in the rate of economic growth

© 2015 Pearson Education, Inc

12.1 Economic Fluctuations and Business Cycles

Many aggregate macroeconomic variables grow or

contract together during booms and busts, exhibiting

a pattern of positive or negative co-movement.

Variables such as real consumption, real investment,

and employment move positively (or together) with

real GDP.

Variables such as unemployment move negatively (or

opposite) real GDP.

© 2015 Pearson Education, Inc

12.1 Economic Fluctuations and Business Cycles

© 2015 Pearson Education, Inc

12.1 Economic Fluctuations and Business Cycles

Exhibit 12.4 Real Consumption Growth Versus Real Investment

Growth (1929–2013)

Recessions and expansion do not follow a

repetitive, easily predictable pattern.

As a result, it is impossible to forecast during an

expansion when the expansion will end.

Similarly, it is impossible to forecast during a

recession when the recession will end.

© 2015 Pearson Education, Inc

12.1 Economic Fluctuations and Business Cycles

Even though the beginnings and ends of

recessions are somewhat unpredictable, economic

growth is not random but persistent.

When the economy is growing, it will probably

keep growing the following quarter.

Likewise, when the economy is contracting, the

economy will probably keep contracting the

following quarter.

© 2015 Pearson Education, Inc

12.1 Economic Fluctuations and Business Cycles

The Great Depression of 1929‒1933 illustrates

the three key properties of economic fluctuations:

1. Co-movement in economic aggregates

2. Limited predictability

3. Persistence in the rate of growth

© 2015 Pearson Education, Inc

12.1 Economic Fluctuations and Business Cycles

© 2015 Pearson Education, Inc

Exhibit 12.5, Panel (a) The Great Depression

12.1 Economic Fluctuations and Business Cycles

© 2015 Pearson Education, Inc

Exhibit 12.5, Panel (b) The Great Depression

12.1 Economic Fluctuations and Business Cycles

© 2015 Pearson Education, Inc

Exhibit 12.5, Panel (c) The Great Depression

12.1 Economic Fluctuations and Business Cycles

Question: Why are there economic fluctuations?

Answer: It depends on who you ask.

Caveat: There is a significant body of shared

knowledge that unexpected shifts to labor

demand, called shocks, are important.

© 2015 Pearson Education, Inc

12.2 Macroeconomic Equilibrium and Economic Fluctuations

At the beginning of a recession, the labor demand

curve shifts to the left due to:

1. A fall in output prices

2. A decrease in output demand

3. A decrease in labor productivity

4. A rise in input prices

© 2015 Pearson Education, Inc

12.2 Macroeconomic Equilibrium and Economic Fluctuations

In the case of a recession, if wages are flexible,

the leftward shift in the labor demand curve will

lead to a fall in wages and a decrease in the

quantity of labor.

As a result, real GDP

will decrease.

© 2015 Pearson Education, Inc

12.2 Macroeconomic Equilibrium and Economic Fluctuations

© 2015 Pearson Education, Inc

12.2 Macroeconomic Equilibrium and Economic Fluctuations

Exhibit 12.6, Panel (a) Leftward Shift in

the Labor Demand Curve with Flexible

Wages

Exhibit 12.6, Panel (b) The Relationship

Between Employment and Real GDP

If wages are downward rigid, the leftward shift in

the labor demand curve will lead to no change in

the wage rate and a larger decrease in the

quantity of labor.

As a result, output will decrease more under

downward rigid wages than under flexible wages.

© 2015 Pearson Education, Inc

12.2 Macroeconomic Equilibrium and Economic Fluctuations

© 2015 Pearson Education, Inc

12.2 Macroeconomic Equilibrium and Economic Fluctuations

Exhibit 12.6, Panel (c) Leftward shift in

the labor demand curve with downward

rigid wages

Exhibit 12.6, Panel (b) The relationship

between employment and real GDP

There are three different schools of thought on the

sources of economic fluctuations:

1. Real business cycle theory emphasizes

changes in productivity and technology

2. Keynesian theory focuses on business and

consumer expectations of the future.

3. Financial and monetary theory looks at

changes in prices and interest rates.

© 2015 Pearson Education, Inc

12.2 Macroeconomic Equilibrium and Economic Fluctuations

Real business cycle theory emphasizes changes

in productivity and technology:

• Technological advances and other

productivity-enhancing innovation cause

expansions.

• An increase in input prices like oil causes

recessions.

© 2015 Pearson Education, Inc

12.2 Macroeconomic Equilibrium and Economic Fluctuations

Keynesian theory focuses on changes in

expectations of the future:

• Animal spirits are the psychological factors

that lead to changes in business and consumer

mood or sentiment. Animal spirits can lead to

decreases in spending (recessions) or

increases in spending (expansions).

© 2015 Pearson Education, Inc

12.2 Macroeconomic Equilibrium and Economic Fluctuations

Keynesian theory (cont’d):

• A negative shock can hit the economy and

generate pessimism. Willingness to spend

decreases and is not offset by increased

spending in other parts of the economy.

© 2015 Pearson Education, Inc

12.2 Macroeconomic Equilibrium and Economic Fluctuations

Keynesian theory (cont’d):

• The initial decrease in spending is amplified

by further decreases in other persons’ spending

due to multipliers.

© 2015 Pearson Education, Inc

12.2 Macroeconomic Equilibrium and Economic Fluctuations

Financial and monetary theory—whose main

proponent is Milton Friedman—looks at changes

in prices and interest rates:

• A decrease in the money supply (M2) will

cause the price level to fall.

• A fall in the price level will reduce

employment because of downward wage

rigidity.© 2015 Pearson Education, Inc

12.2 Macroeconomic Equilibrium and Economic Fluctuations

Financial and monetary theory (cont’d):

• A decrease in the money supply (M2) will also

cause an increase in the real interest rate.

• Higher real interest rates will reduce

investment spending by firms.

© 2015 Pearson Education, Inc

12.2 Macroeconomic Equilibrium and Economic Fluctuations

Multipliers can amplify

the effects of any

economic shock,

regardless of its source.

Consider a negative

consumption shock.

© 2015 Pearson Education, Inc

12.2 Macroeconomic Equilibrium and Economic Fluctuations

© 2015 Pearson Education, Inc

12.2 Macroeconomic Equilibrium and Economic Fluctuations

Exhibit 12.8 Multipliers in a Contracting Economy

By lowering household income, multipliers will

shift the labor demand curve further to the left.

As a result, wages and employment will decrease

further, to the trough of the business cycle.

© 2015 Pearson Education, Inc

12.2 Macroeconomic Equilibrium and Economic Fluctuations

© 2015 Pearson Education, Inc

12.2 Macroeconomic Equilibrium and Economic Fluctuations

Exhibit 12.9 Multipliers in an Economy with Flexible Wages

In addition, multipliers can reduce labor demand

further by:

© 2015 Pearson Education, Inc

12.2 Macroeconomic Equilibrium and Economic Fluctuations

• A fall in asset prices

• A rise in mortgage

defaults

• A rise in household and

firm bankruptcies

Here is how a shock plays out in the short run:

1. An initial shock shifts the labor demand curve

to the left.

2. Downward wage rigidity leads to greater

reductions.

3. Multipliers cause the labor demand curve to

shift leftward even more.

© 2015 Pearson Education, Inc

12.2 Macroeconomic Equilibrium and Economic Fluctuations

© 2015 Pearson Education, Inc

12.2 Macroeconomic Equilibrium and Economic Fluctuations

Exhibit 12.11 Multipliers in an Economy with Rigid Wages

Economic recovery in the medium run:

1. Market forces from (a) inventory rebuilding,

(b) technological advances, and (c) financial

intermediation shift the labor demand curve to

the right for a partial recovery.

© 2015 Pearson Education, Inc

12.2 Macroeconomic Equilibrium and Economic Fluctuations

© 2015 Pearson Education, Inc

12.2 Macroeconomic Equilibrium and Economic Fluctuations

Exhibit 12.12 Partial Recovery Due to a Partial Rightward Shift in

the Labor Demand Curve

Economic recovery in the medium run:

2. Expansionary monetary policy will lower

interest rates and raise inflation.

Lower interest rates will raise spending, which

shifts the labor demand curve to the right.

Higher inflation will lower real wages, which

shifts the labor supply curve to the left.

© 2015 Pearson Education, Inc

12.2 Macroeconomic Equilibrium and Economic Fluctuations

© 2015 Pearson Education, Inc

12.2 Macroeconomic Equilibrium and Economic Fluctuations

Exhibit 12.13, Panel (a) The Effect of Inflation on the Labor

Market Equilibrium

Note that the leftward shift in labor supply has an

impact only if the new market-clearing wage is

above the original wage rate.

© 2015 Pearson Education, Inc

12.2 Macroeconomic Equilibrium and Economic Fluctuations

© 2015 Pearson Education, Inc

12.2 Macroeconomic Equilibrium and Economic Fluctuations

Exhibit 12.13, Panel (b) The Effect of Inflation on the Labor

Market Equilibrium

The following diagram puts all these effects

together:

1. Pre-recession starting at point 1 to…

2. Recessionary trough at point 2 to…

3. Partial recovery at point 3 to…

4. Full recovery at point 4

© 2015 Pearson Education, Inc

12.2 Macroeconomic Equilibrium and Economic Fluctuations

© 2015 Pearson Education, Inc

12.2 Macroeconomic Equilibrium and Economic Fluctuations

Exhibit 12.14 Full Recovery

12.3 Modeling Expansions

The focus so far has centered on recessions. We

now shift to economic expansions.

Suppose that Apple and other technology firms

become optimistic about the future demand for

their products.

Question: What happens to its demand for labor?

© 2015 Pearson Education, Inc

12.3 Modeling Expansions

© 2015 Pearson Education, Inc

Exhibit 12.15 Rightward Shift in the Labor Demand Curve, Shift from 1 to 2

Only

12.3 Modeling Expansions

In response, firms that supply the technology get

higher sales, and consumers start to spend more.

Question: What happens in the labor market?

© 2015 Pearson Education, Inc

12.3 Modeling Expansions

© 2015 Pearson Education, Inc

Exhibit 12.15 Rightward Shift in the Labor Demand Curve

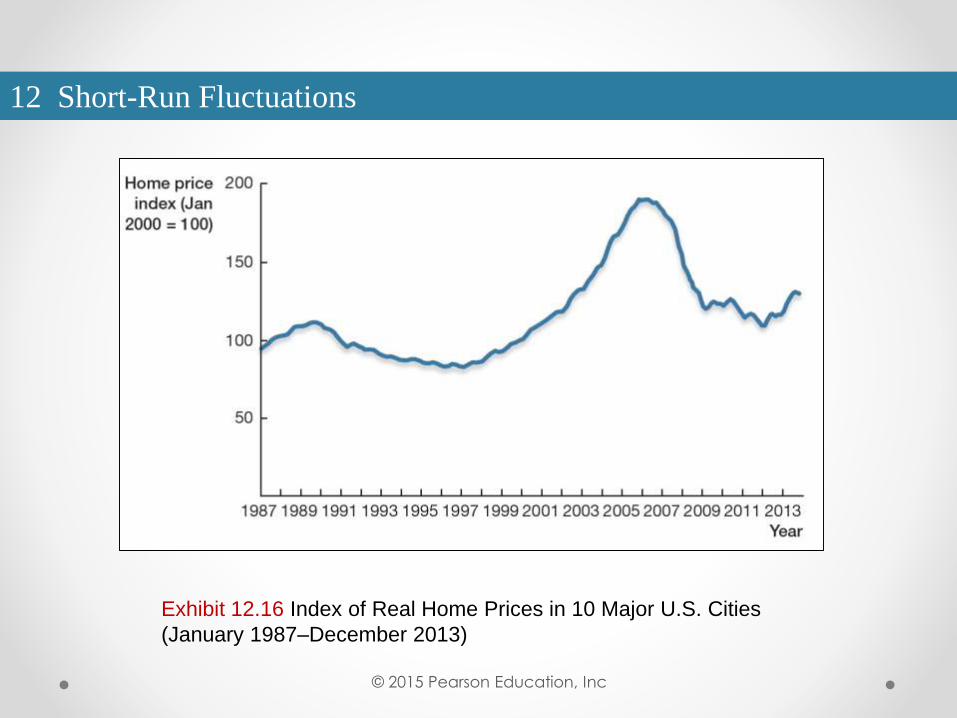

Evidence-Based Economics Example:

Question: What caused the recession of 2007–

2009?

Data: Historical data on housing prices (Case-

Shiller home price index), residential

investment (NIPA), foreclosure rates (Mortgage

Bankers’ Association), and bank balance sheets

(FDIC and Lehman Brothers).© 2015 Pearson Education, Inc

12 Short-Run Fluctuations

Answer: Three key factors appear to have played

central roles in the crisis:

1. A fall in housing prices, which caused a

collapse in new construction

© 2015 Pearson Education, Inc

12 Short-Run Fluctuations

© 2015 Pearson Education, Inc

Exhibit 12.16 Index of Real Home Prices in 10 Major U.S. Cities

(January 1987–December 2013)

12 Short-Run Fluctuations

© 2015 Pearson Education, Inc

Exhibit 12.17 Real Investment in Residential Construction

(1987:Q1–2013:Q4; Normalized to 100 in 2009)

12 Short-Run Fluctuations

2. A sharp drop in consumption

© 2015 Pearson Education, Inc

12 Short-Run Fluctuations

© 2015 Pearson Education, Inc

12 Short-Run Fluctuations

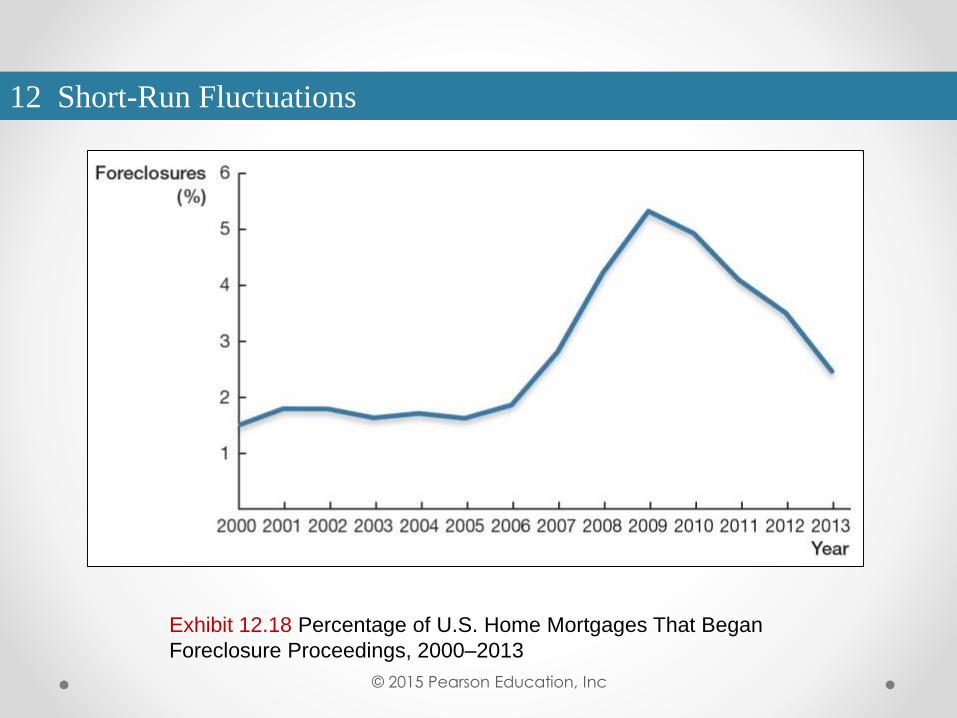

3. Spiraling mortgage defaults that caused many

bank failures, leading the entire financial

system to freeze up

© 2015 Pearson Education, Inc

12 Short-Run Fluctuations

© 2015 Pearson Education, Inc

12 Short-Run Fluctuations

Exhibit 12.18 Percentage of U.S. Home Mortgages That Began

Foreclosure Proceedings, 2000–2013