chapter 07 using accounting information

TRANSCRIPT

© 2012 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Chapter SevenUsing Accounting

Information

7 | 1

PRIDE HUGHES KAPOOR

INTRODUCTION TOBUSINESS

ELEVENTH EDITION

© 2012 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Learning Objectives

1. Explain why accurate accounting information and audited financial statements are important.

2. Identify the people who use accounting information and possible careers in the accounting industry.

3. Discuss the accounting process.

4. Read and interpret a balance sheet.

5. Read and interpret an income statement.

6. Describe business activities that affect a firm’s cash flow.

7. Summarize how managers evaluate the financial health of a business.

7 | 2

© 2012 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Why Accounting Information Is Important

Recent accounting scandals• Pressure on corporate executives to look good to

analysts and investors

Why audited financial statements are important• Bankers, creditors, investors, and government

agencies rely on an auditor’s opinion of the validity of a firm’s financial statements.

7 | 3

© 2012 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Why Accounting Information Is Important (cont’d)

What is an audit?• An examination of a company’s financial statements

and accounting practices• Generally accepted accounting principles (GAAPs)—

an accepted set of guidelines and practices for U.S. companies reporting financial information and the accounting profession

• The FASB is developing a new set of standards combining those of GAAP and the International Financial Reporting Standards

• An audit does not guarantee that a company has not “cooked” the books

7 | 4

© 2012 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

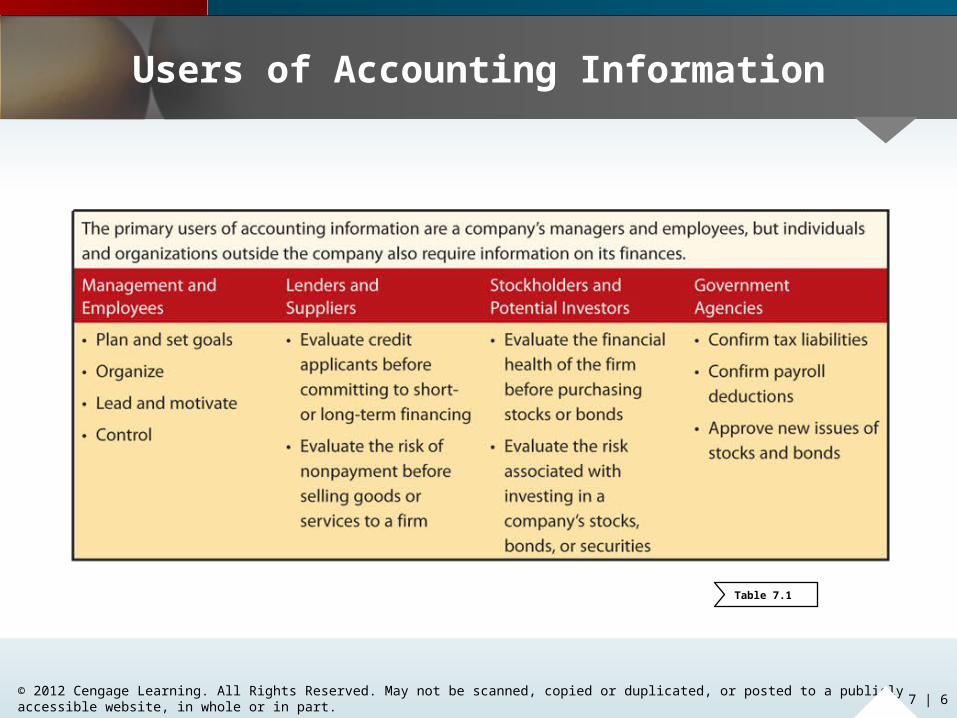

Who Uses Accounting Information

Managers are the primary users• Proprietary: information that is not divulged to

anyone outside the firm

Lenders, suppliers, stockholders, potential investors and government agencies are other users

7 | 5

© 2012 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Users of Accounting Information

7 | 6

Table 7.1

© 2012 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Different Types of Accounting

Managerial accounting provides managers and employees within the organization with information needed to make decisions about a firm’s financing, investing, marketing, and operating activities are the primary users

Financial accounting generates financial statements and reports for interested people outside an organization

7 | 7

© 2012 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Careers in Accounting

Qualities to be successful in accounting• Be responsible, honest, ethical

• Have a strong background in financial management

• Know how to use a computer and accounting software

• Be able to communicate with people who need accounting information

7 | 8

© 2012 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Careers in Accounting (cont’d)

Private Accountant• Employed by a specific organization• Services performed for the employer

- Design its accounting information system- Manage its accounting department- Provide managers with accounting information,

advice and assistance.

Public Accountant• Provides services to clients on a fee basis• Self-employed or employee of an accounting firm

7 | 9

© 2012 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Careers in Accounting (cont’d)

Certified Public Accountant (CPA)• Has met state requirements for accounting education

and experience and has passed a rigorous accounting examination prepared by the AICPA

• Participates in continuing-education programs to maintain certification

Certified Management Accountant (CMA)• Has met requirements for education and experience,

passed a rigorous exam, certified by the Institute of Management Accountants

• Has demonstrated decision-making, financial planning, analysis, and critical-thinking skills

7 | 10

© 2012 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

The Accounting Process

The accounting equation Assets = Liabilities + Owners’ equity

• Assets—the resources that a business owns (e.g., cash, inventory, equipment, and real estate)

• Liabilities—the firm’s debts

• Owners’ equity—the difference between assets and liabilities (what would be left for the owners if the firm’s assets were sold and the money used to pay off its liabilities)

Double-entry bookkeeping system: Each financial transaction is recorded as two separate accounting entries to maintain the balance of the accounting equation

7 | 11

© 2012 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

The Accounting Process (cont’d)

The accounting cycle• Done on a regular basis

- Analyzing source documents- Recording transactions as they occur in the

general journal- Posting transactions to accounts in the

general ledger

Done at the end of the period• Preparing the trial balance of all general ledger

accounts• Preparing financial statements and closing the books

7 | 12

© 2012 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

The Income Statement

A summary of a firm’s revenues and expenses during a specified accounting period• Profit (cash surplus)

• Loss (cash deficit) Revenues

• The dollar amounts earned by a firm from selling goods, providing services, or performing business activities

• Gross sales—the total dollar amount of all goods and services sold during the accounting period

• Net sales—the actual dollar amounts received by a firm for the goods and services it has sold, after adjustment for returns, allowances, discounts

7 | 13

© 2012 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

The Income Statement (cont’d)

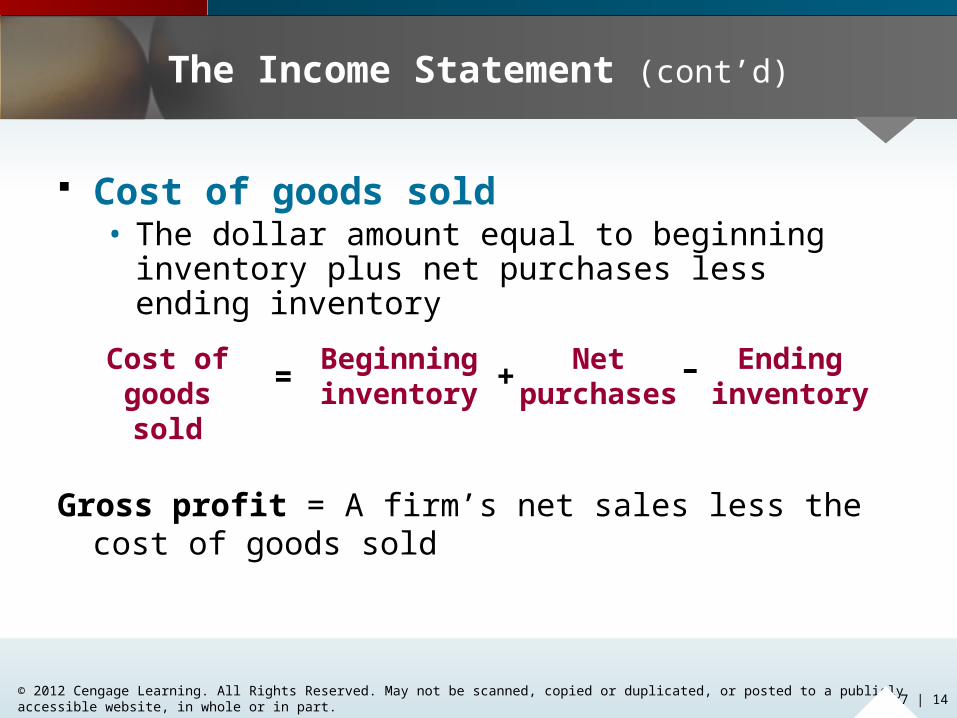

Cost of goods sold• The dollar amount equal to beginning inventory plus

net purchases less ending inventory

Cost of goods sold

Beginning inventory

Net purchases

Ending inventory

= + –

Gross profit = A firm’s net sales less the cost of goods sold

7 | 14

© 2012 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

The Income Statement (cont’d)

Operating expenses• All business costs other than the cost of goods sold

- Selling expenses—costs related to marketing activities- General expenses—costs of managing the business

Net income• Revenues less expenses, when the difference

is positive

Net loss• Revenues less expenses, when the difference

is negative

7 | 15

© 2012 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Personal Income Statement

7 | 16

Figure 7.3

By subtracting expenses from income, anyone can construct a person income statement and determine if they have a surplus or deficit at the end of each month.

© 2012 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

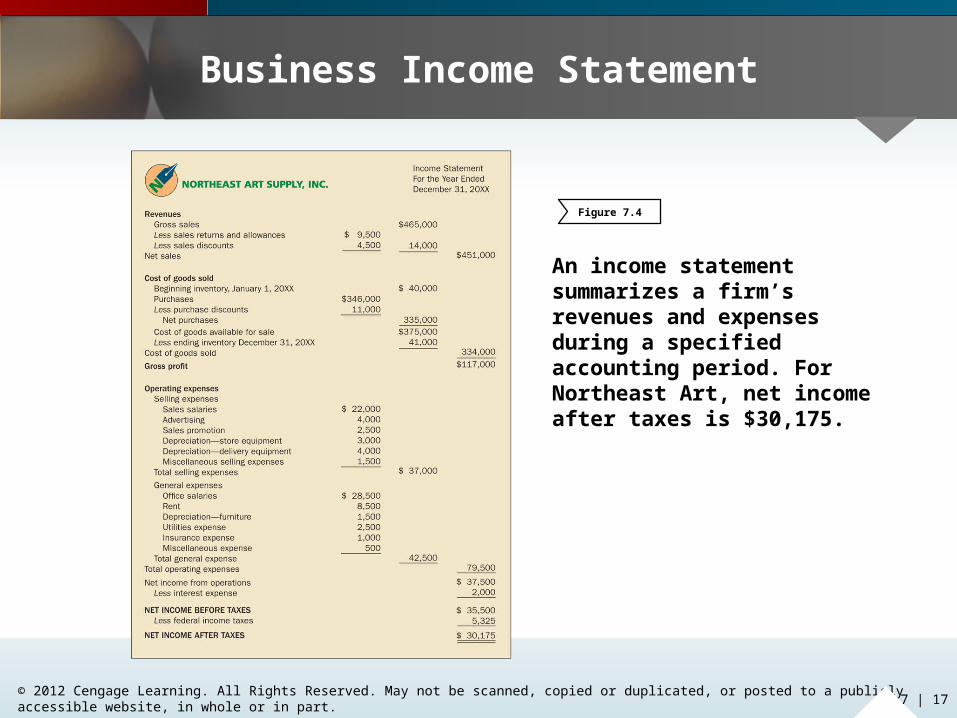

Business Income Statement

7 | 17

Figure 7.4

An income statement summarizes a firm’s revenues and expenses during a specified accounting period. For Northeast Art, net income after taxes is $30,175.

© 2012 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

The Statement of Cash Flows

Illustrates how the operating, investing, and financing activities of a company affect cash during an accounting period

• Cash flows from operating activities (providing goods and services)

• Cash flows from investing activities (purchase and sale of land, equipment, and other assets and investments)

• Cash flows from financing activities (changes in debt obligation and owners’ equity accounts)

7 | 18

© 2012 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

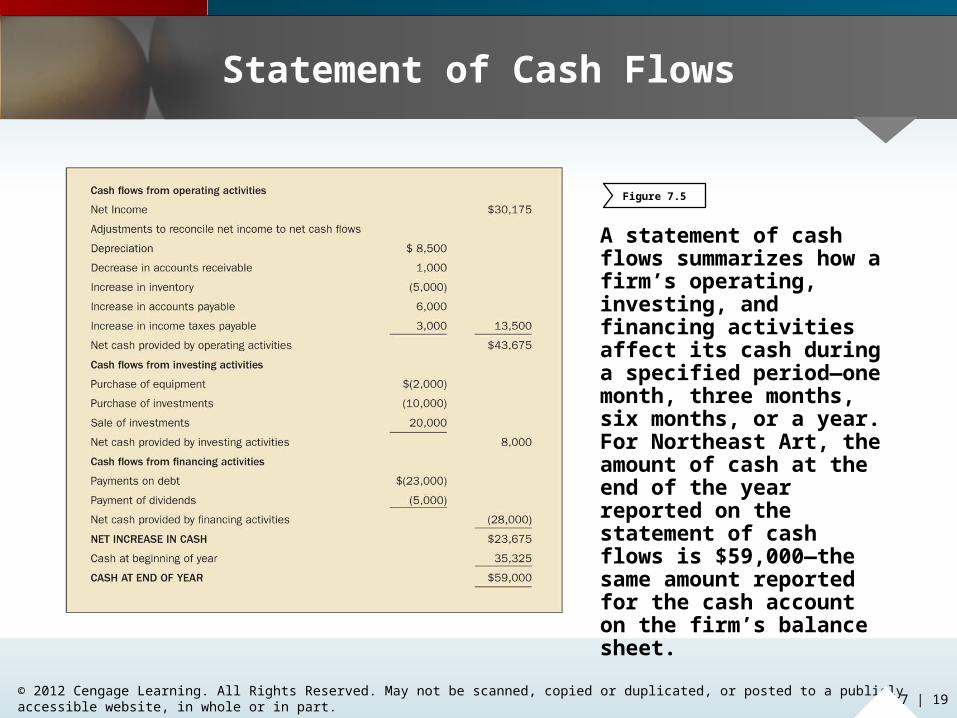

Statement of Cash Flows

7 | 19

A statement of cash flows summarizes how a firm’s operating, investing, and financing activities affect its cash during a specified period—one month, three months, six months, or a year. For Northeast Art, the amount of cash at the end of the year reported on the statement of cash flows is $59,000—the same amount reported for the cash account on the firm’s balance sheet.

Figure 7.5

© 2012 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Evaluating Financial Statements

Using accounting information to evaluate a potential investment• Use common sense to interpret the numbers• Financial statements should be audited by an outside

source and be current• Look for use of new strategies to reduce costs• Determine the firm’s ability to pay its debts and

borrow money in the future• Look at how the numbers relate to each other• Understand the financial ratios

7 | 20

© 2012 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Evaluating Financial Statements (cont’d)

Using accounting information to evaluate a potential investment (cont’d)• Read letters from top executives• Examine the footnotes closely, look for red flags• Examine the comparative data to analyze trends

7 | 21

© 2012 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Comparing Data with Other Firms’ Data

Comparisons are possible because of GAAP

Managers can get a general idea of a firm’s relative effectiveness and its standing within the industry

Data are available from annual reports of public corporations

Industry averages are available from Dun & Bradstreet, Standard & Poor’s, industry trade associations

7 | 22

© 2012 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Financial Ratios

Numbers that show the relationship between two elements of a firm’s financial statements

Can be compared with The firm’s own past ratios Ratios of competitors Industry averages

Information to calculate ratios is found on a firm’s balance sheet, income statement, and statement of cash flows

7 | 23

© 2012 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Financial Ratios (cont’d)

7 | 24

Table 7.2

© 2012 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Financial Ratios (cont’d)

7 | 25

Table 7.2

© 2012 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Financial Ratios (cont’d)

7 | 26

Table 7.2