chapter 10

DESCRIPTION

Chapter 10. Analysis of Financial Statements. General Accounting Principles. Reliability Understandability Comparability. Primary Financial Statements. The balance sheet enumerates Assets Liabilities Equity. Assets. Current: cash and equivalents, accounts receivable, and inventory - PowerPoint PPT PresentationTRANSCRIPT

Chapter 10

Analysis of Financial Statements

General Accounting Principles

• Reliability

• Understandability

• Comparability

Primary Financial Statements

• The balance sheet enumerates

–Assets

–Liabilities

–Equity

Assets

• Current: cash and equivalents, accounts receivable, and inventory

• Long-term: land, buildings, machinery, and equipment

• Hidden assets

Liabilities

• Current

–.Accounts Payable

–Accruals

–Notes payable

• Long-term

Equity

• Preferred stock

• Common stock

• Additional paid-in capital

• Retained earnings

• Book value

• Book value per share

The Income Statement

• Enumerates–Revenues–Expenses

• To determine–Income (earnings)–Earnings per share

Analysis of Cash Flow: Statement of Cash Flows

• Enumerates–sources of funds–uses of funds

• Determines change in the cash position

• Emphasis on the firm’s ability to generate cash

Cash Inflows

• A decrease in an asset

• An increase in a liability

• An increase in equity

Cash Outflows

• An increase in an asset

• A decrease in a liability

• A decrease in equity

Limitations of Accounting Data

• Nonmeasureable items are excluded

• Aggregations

• Biased estimates of data

• Insufficient challenges by auditors

Depreciation

• Allocation of the cost of plant and equipment over time

• Non-cash expense

• Impact on taxes and cash flow

Depreciation

• Straight-line depreciation

–Equal allocation each year

• Accelerated depreciation

–Larger proportion during the early years

Modified Accelerated Cost Recovery System (MACRS)

• Asset classified by years

3, 5, 7, 10, 15, 20 years

• The half-year convention

Corporate Losses

• Offset earnings from other years

• Carry back 3 years then

• Carry forward

Ratio Analysis

• Builds on a firm's financial statements

• Easy to understand

• Used by both equity investors and creditors

Ratio Analysis

• Facilitates Comparisons– Over time: time-series analysis– Across firms: cross-sectional

analysis

An Application of Ratio Analysis

• The following ratios use Pier I Imports 2002 financial statements

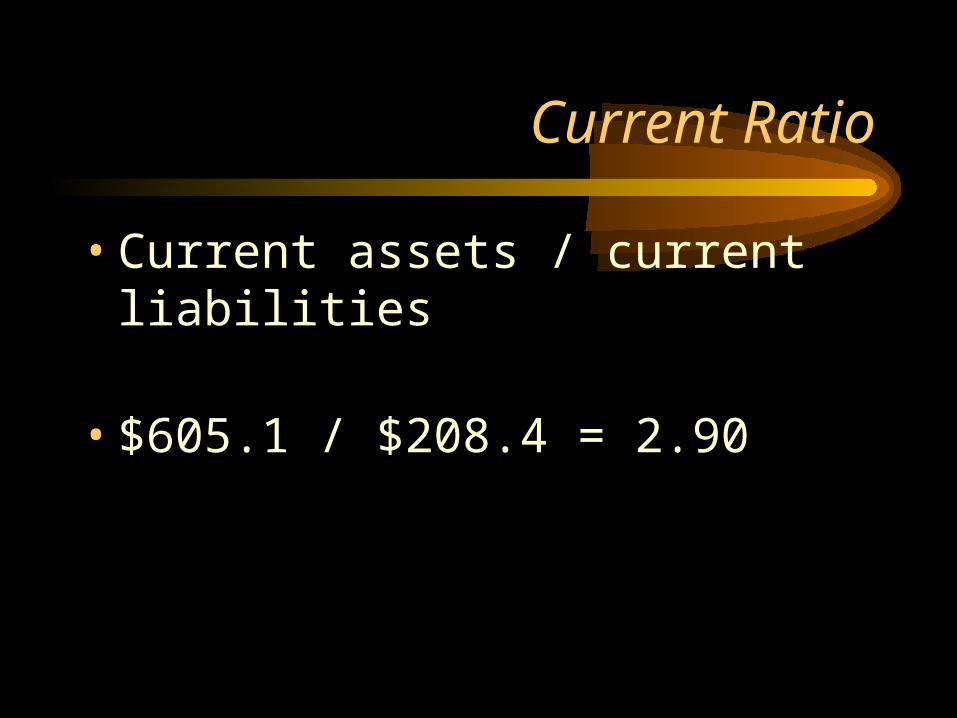

Current Ratio

• Current assets / current liabilities

• $605.1 / $208.4 = 2.90

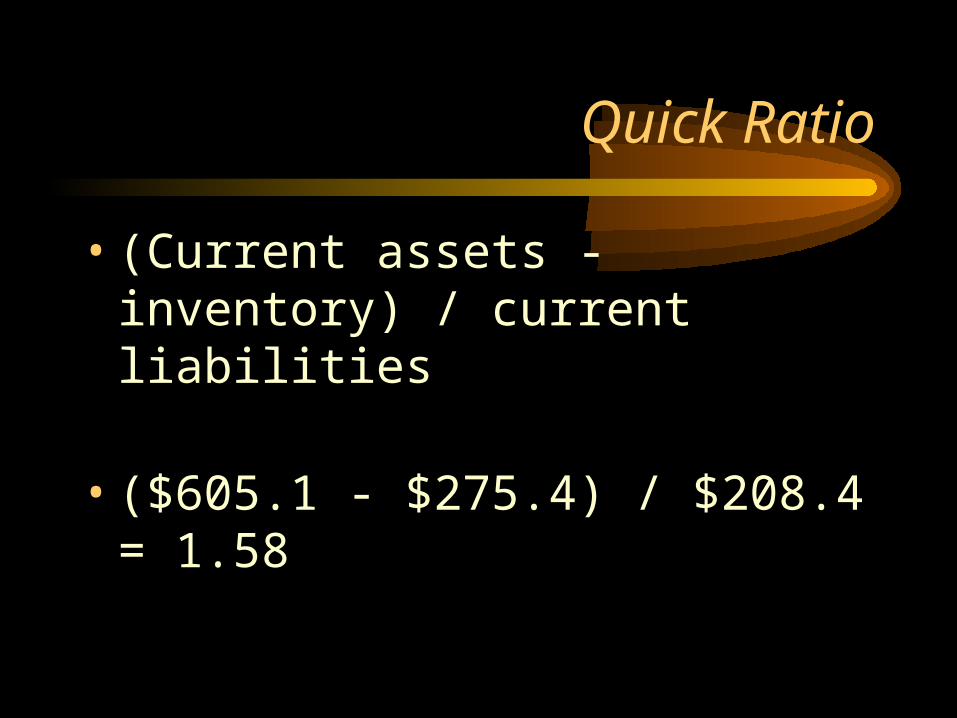

Quick Ratio

• (Current assets - inventory) / current liabilities

• ($605.1 - $275.4) / $208.4 = 1.58

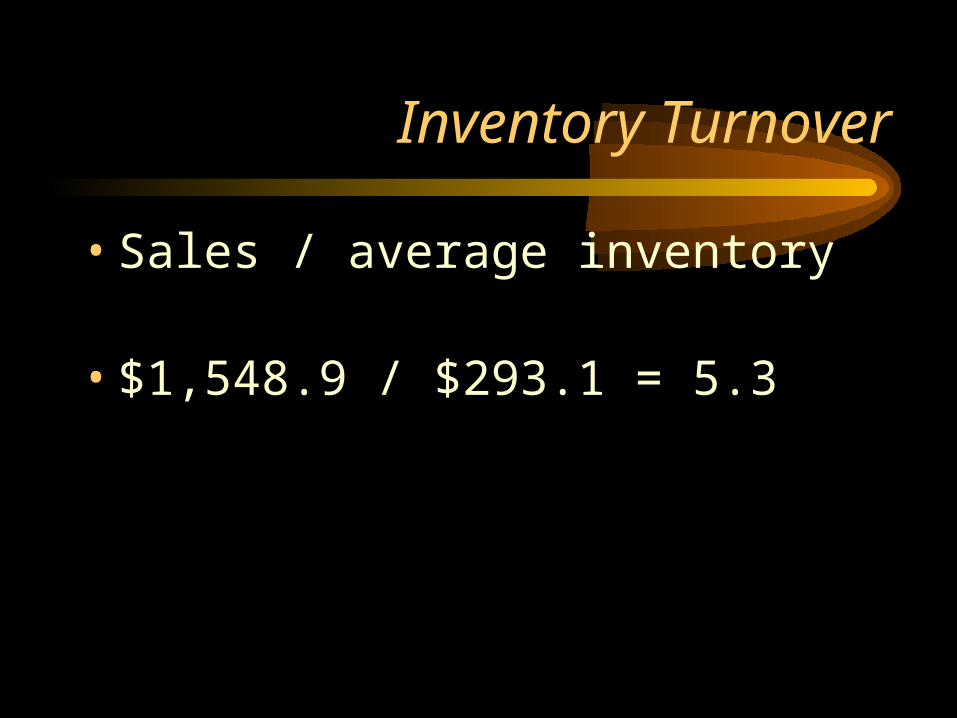

Inventory Turnover

• Sales / average inventory

• $1,548.9 / $293.1 = 5.3

Receivables Turnover

• Sales / accounts receivable

• $1,548.6 / $6,205 = 249.6

• Answer is not meaningful

Receivables Turnover

• For Southern Company

$10,155 / $1,132 = 8.97

• Interpretation: 8.97 is about nine times a year or every six weeks.

Average Collection Period(days sales outstanding)

• For Southern Company

• Accounts receivable / sales per day

• $1,132 / $28,208 = 40 days

Fixed Asset Turnover

• Sales / fixed assets

• $1,159 / $209.9 = 7.38

Total Asset Turnover

• Sales / total assets

• $1,159 / $862.7 = 1.80

Gross Profit Margin

• (revenues - cost of goods sold) / sales

• $649.8 / $1,549 = 41.96%

Operating Profit Margin

• Operating earnings / sales

• $158.8 / $1,549 = 10.26%

Net Profit Margin

• Earnings after taxes / sales

• $100.2 / $1,549 = 6.47%

Return on Assets

• Earnings after taxes / total assets

• $100.2 / $862.7 = 11.6%

Return on Equity

• Earnings after taxes / equity

• $100.2 / $585.6 = 17.1%

Return on Common Equity

• Adjusts for preferred stock

• If no preferred, ratio is same as return on equity

Basic Earning Power

• EBIT / total assets

• $158.8 / $862.7 = 18.47%

Debt Ratio

• Debt / total assets

• $277.0 / $862.7 = 32.1%

Debt to Equity Ratio

• Debt / equity

• $277.0 / $585.7 = 47.3%

DuPont System of Analysis

• Combines

–Net profit margin

–Turnover

–Leverage

• Helps identify source of weakness

DuPont System of Analysis

Times-interest-earned

• Earnings before interest and taxes / interest

• $158,813 / $-184 = -863.1

• Interest earned exceeded interest paid.

Ratio Comparisons

• Ratios of firms within an industry– tend to have similar numerical values

– differences in numerical values are reasons for further analysis

Problems for Interpretation

• Different definitions for the same ratio

• Historical data may be outmoded

• Non-recurring items

• Internet sources differ