chapter 10 market efficiency. explain the concept of efficient markets. describe the three forms of...

TRANSCRIPT

Chapter 10Chapter 10

Market EfficiencyMarket Efficiency

• Explain the concept of efficient markets.• Describe the three forms of market efficiency –

weak, semi-strong, and strong• Discuss the evidence regarding the Efficient

Market Hypothesis.• State the implications of market efficiency for

investors.• Outline major exceptions to the Efficient Market

Hypothesis.

Learning ObjectivesLearning Objectives

• How well markets respond to new information is a very important part of obtaining the equilibrium relationship predicted by the capital market theory

• Should it be possible to decide between a profitable and unprofitable investment given current information?

• Efficient Markets The prices of all securities quickly and fully reflect

all available information

Efficient MarketsEfficient Markets

Efficient MarketsEfficient Markets

Definition of “all available information”• All known information including:

Past information (e.g., last year’s earnings) Current information as well as events that have been

announced but are still forthcoming (e.g., stock splits and dividends)

• Information that can be reasonably inferred For example, if many investors believe that interest rates

will decline soon, prices will reflect this belief before the actual decline occurs

Why the markets can be expected to be efficient?• Large number of rational, profit-maximizing

investors Actively participate in the market Individuals cannot affect market prices (i.e., price-

takers)• Information is costless and widely available to

market participants at approximately the same time• Information is generated in a random fashion (e.g.,

announcements or currency is devalued)• Investors react quickly and fully to new information

causing stock prices to adjust accordingly

Conditions for an Efficient MarketConditions for an Efficient Market

• Quick price adjustment in response to the arrival of random information makes the reward for analysis low

• Prices reflect all available information• Price changes are independent of one another

and move in a random fashion New information is independent of past

Consequences of Efficient MarketConsequences of Efficient Market

• Efficient market hypothesis (EMH) The proposition that securities markets are efficient,

with prices of securities reflecting their true economic value

• Three levels of Market Efficiency Weak form – prices reflect past market data (i.e.,

historical price and volume information for stocks and indexes)

Semi-strong form – prices reflect all public information

Strong form – prices reflect all information, both public and private

Market Efficiency FormsMarket Efficiency Forms

Cumulative Levels of Market Efficiency Cumulative Levels of Market Efficiency and the Information Associated with and the Information Associated with

EachEach

Weak FormMarket Data

Strong Form

All Information

Semi-Strong Form

Public Information

• Prices reflect all past price and volume data• Technical analysis, which relies on the past

history of prices, is of little or no value in assessing future changes in price

• Market adjusts or incorporates this information quickly and fully

Weak FormWeak Form

• Prices reflect all publicly available information• For example: earnings, dividends, stock split

announcements, new product developments, financing difficulties, and accounting changes

• Investors cannot act on new public information after its announcement and expect to earn above-average, risk-adjusted returns

• Encompasses weak form as a subset since market data are part of the larger set of all publicly available information

Semi-Strong FormSemi-Strong Form

• Prices reflect all information, public and private• No group of investors should be able to earn

abnormal rates of return by using publicly and privately available information

• Encompasses weak and semi-strong forms as subsets and represents the highest level of market efficiency

Strong FormStrong Form

• Keys to testing the validity of any of the three forms of market efficiency Consistency of returns in excess of risk Length of time over which returns are earned

• Short-lived inefficiencies appearing on a random basis do not constitute evidence of market inefficiencies, at least in an economic sense

• Economically efficient markets Assets are priced so that investors cannot exploit

any discrepancies and earn unusual returns• Transaction costs matter

Evidence on Market EfficiencyEvidence on Market Efficiency

Ways to test for weak-form efficiency• Test for independence (randomness) of stock price

changes [Random Walk Hypothesis] If stock prices are independent, trends in price

changes do not exist • Knowing and using the past sequence of price

information is of no value to an investor

• Test for profitability of trading rules after brokerage costs Simple buy-and-hold better

• Buying a portfolio of stocks and holding it until a common liquidation date

Weak-Form EvidenceWeak-Form Evidence

Weak-Form EMHWeak-Form EMH

• Stock price changes in an efficient market should be independent

• Statistical tests of price changes are mostly supportive of weak-form EMH

• The sign test involves classifying each price change by its sign, which means whether it was +, 0, or –

• Then the “runs” in the series of signs can be counted and compared to known information about a random series

• Runs tests• looking for patterns in signs of returns• i.e. + + - + - +

Weak-Form EMHWeak-Form EMH

• The signs test supports independence of stock price changes

• Although some runs do occur, they fall within the limits of randomness since a truly random series will exhibit some runs

• Technical trading rules• Technical analysts believe that trends not only exist

but can also be used successfully• Little evidence exists that technical trading, based

solely on past price and volume data, can outperform a simple buy-and-hold strategy

Two Apparent Contradictions to the Two Apparent Contradictions to the Weak-Form EMHWeak-Form EMH

1. Momentum or persistence in stock returns tendency of stocks that have done well over the

past 6 to 12 months to continue to do well over the next 6 to 12 months

2. “Contrarian” Strategies Overreaction Hypothesis [DeBondt & Thaler

(1985)] stocks that have done well over the past 3-5 year

period, will do poorly over the subsequent 3-5 year period

Two Apparent Contradictions to Two Apparent Contradictions to the Weak-Form EMHthe Weak-Form EMH

• Contrarian strategies are trading strategies designed to exploit the overreaction hypothesis

• Since the underlying rationale is to purchase or sell stock in anticipation of achieving future results that are contrary to their past performance record

• DeBondt and Thaler are testing whether the overreaction hypothesis is predictive

• In other words, knowing past stock returns appears to help significantly in predicting future stock returns

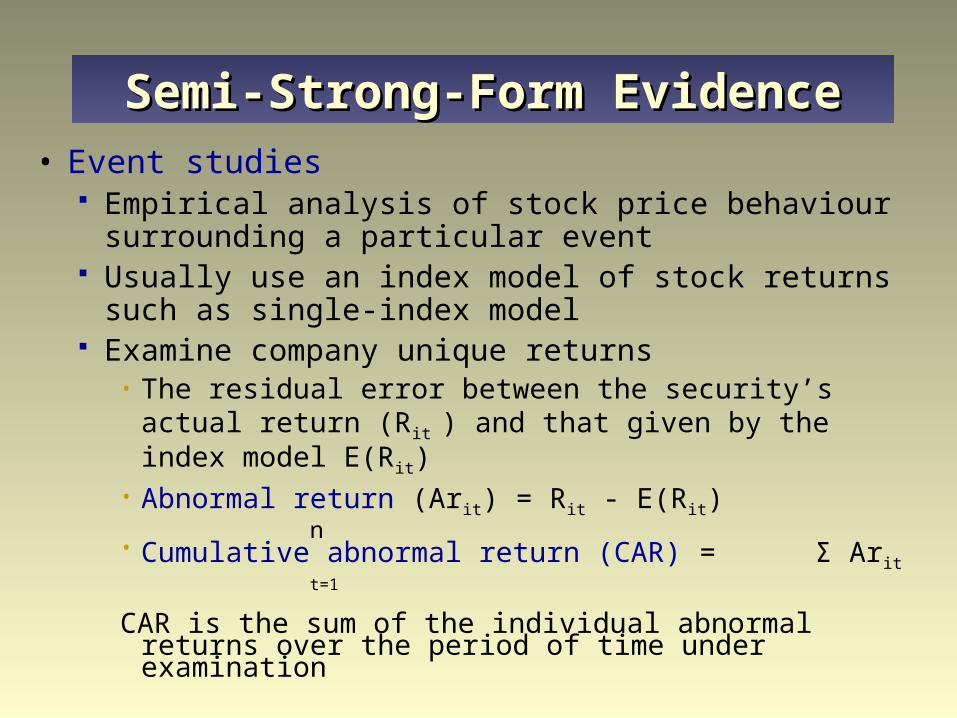

• Event studies Empirical analysis of stock price behaviour

surrounding a particular event Usually use an index model of stock returns such as

single-index model Examine company unique returns

• The residual error between the security’s actual return (Rit ) and that given by the index model E(Rit)

• Abnormal return (Arit) = Rit - E(Rit)n

• Cumulative abnormal return (CAR) = Σ Aritt=1

CAR is the sum of the individual abnormal returns over the period of time under examination

Semi-Strong-Form EvidenceSemi-Strong-Form Evidence

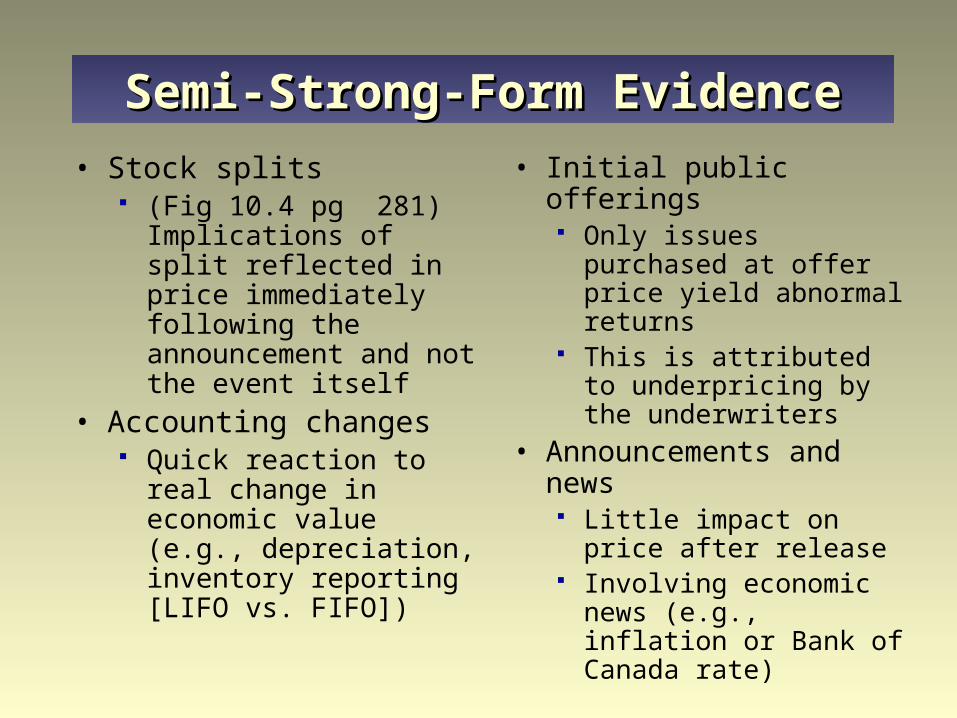

• Stock splits (Fig 10.4 pg 281)

Implications of split reflected in price immediately following the announcement and not the event itself

• Accounting changes Quick reaction to real

change in economic value (e.g., depreciation, inventory reporting [LIFO vs. FIFO])

• Initial public offerings

Only issues purchased at offer price yield abnormal returns

This is attributed to underpricing by the underwriters

• Announcements and news Little impact on price

after release Involving economic news

(e.g., inflation or Bank of Canada rate)

Semi-Strong-Form EvidenceSemi-Strong-Form Evidence

Professional Portfolio Manager Professional Portfolio Manager PerformancePerformance

• There is substantial evidence that portfolio managers do not outperform the market (or earn abnormal risk-adjusted returns) over the long run

• The average active portfolio manager may underperform the market index by 50 to 200 basis points

• Based on fund averages (US-based equity mutual funds & pension funds)

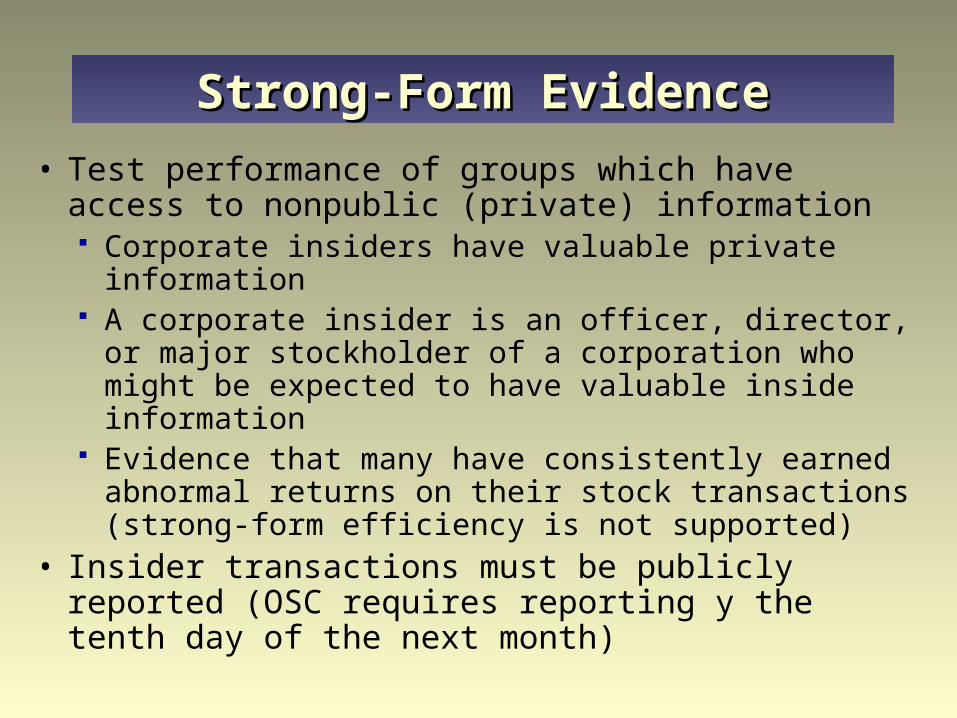

• Test performance of groups which have access to nonpublic (private) information Corporate insiders have valuable private

information A corporate insider is an officer, director, or major

stockholder of a corporation who might be expected to have valuable inside information

Evidence that many have consistently earned abnormal returns on their stock transactions (strong-form efficiency is not supported)

• Insider transactions must be publicly reported (OSC requires reporting y the tenth day of the next month)

Strong-Form EvidenceStrong-Form Evidence

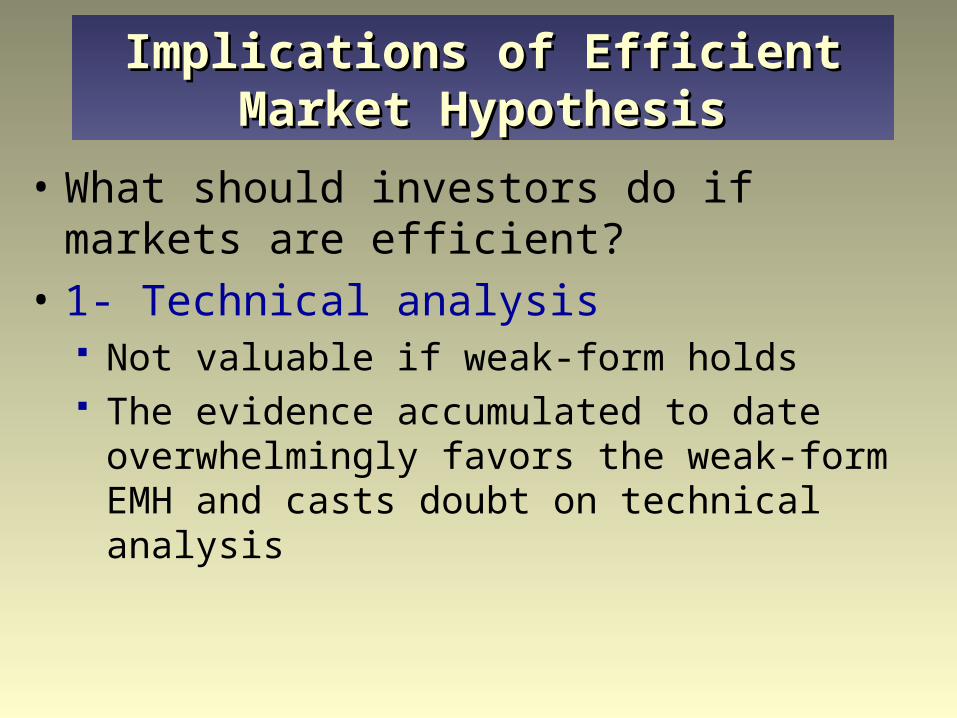

• What should investors do if markets are efficient?

• 1- Technical analysis Not valuable if weak-form holds The evidence accumulated to date

overwhelmingly favors the weak-form EMH and casts doubt on technical analysis

Implications of Efficient Market Implications of Efficient Market HypothesisHypothesis

Implications of Efficient Market Implications of Efficient Market HypothesisHypothesis

• 2- Fundamental analysis Seeks to estimate the intrinsic value of a

security Not valuable if semi-strong-form holds (since

stock prices reflect all relevant publicly available information, gaining access to information others already have is of no value)

EMH suggests that investors who use the same data and make the same interpretations as other investors will experience average results

• 3- Money Management• For professional money managers (assuming that

the market is efficient) Less time spent on assessing individual securities

• Passive investing favored (one passive investment strategy that is becoming increasingly popular is indexing, which involves the construction of portfolios designed to mimic the performance of a chosen market benchmark portfolio, such as S&P/TSX Composite Index)

• Otherwise, must believe in superior insight

Implications of Efficient Market Implications of Efficient Market HypothesisHypothesis

Implications of Efficient Market Implications of Efficient Market HypothesisHypothesis

• 3- Money Management Tasks that portfolio managers have to perform

if markets are informationally efficient• Maintain correct amount of diversification• Achieve and maintain a desired level of

portfolio risk• Manage tax burden• Control transaction costs (can be done through

index funds)

• Exceptions (techniques or strategies) that appear to be contrary to market efficiency

• Regardless of how persuasive the case for market efficiency is, debate of this issue id likely to persist

Market AnomaliesMarket Anomalies

• Size effect Tendency for small firms to have higher risk-

adjusted returns than large firms Market betas could not account for the abnormal

returns Bid-ask spreads, which are higher for smaller

stocks, could not account for the abnormal returns

As a result, when trading on the TSX, the small-firm strategy may be a viable strategy for increasing portfolio returns without an offsetting increase in risk

Market AnomaliesMarket Anomalies

Seasonality in stock returns• January effect

Tendency for small firm stock returns to be higher in January

Of the 30.5% small-size premium, half of the effect occurs in January

Referred to as “the small firm in January effect” because it is most prevalent for the returns of small-cap stocks

More than half of the excess January returns occurred during the first five trading days of that month

Market AnomaliesMarket Anomalies

Market AnomaliesMarket Anomalies

Seasonality in stock returns• Day-of-the-week effect

The average Monday return is negative and significantly different from the average return of the other four days

• Day-of-the-month effect Returns tend to be higher on the last trading day of

each month

• Support for market efficiency is persuasive Much research using different methods Also many anomalies that cannot be

explained satisfactorily

• Markets are quite efficient, but not totally To outperform the market, superior

fundamental analysis (beyond the norm) must be done

The fundamental analysis that is done everyday is already reflected in stock prices

Conclusions about Market Conclusions about Market EfficiencyEfficiency

• If markets are operationally efficient, some investors with the skill to detect a divergence between price and semi-strong value (price based on all available public information) earn profits Excludes the majority of investors Anomalies offer opportunities

• Controversy about the degree of market efficiency still remains

• The evidence to date suggests that investors face an operationally efficient market

Conclusions about Market Conclusions about Market EfficiencyEfficiency