chapter 10: production and costs - james · pdf filechapter 10: production and costs ......

TRANSCRIPT

Short-run Production DecisionsShort-Run CostsLong-Run Cost

Chapter 10: Production and Costs

Econ 102: Introduction to Microeconomics

Econ 102: Introduction to Microeconomics Chapter 10: Production and Costs

Short-run Production DecisionsShort-Run CostsLong-Run Cost

Goals of this class

Goals of this class 1/ 14

Learn fundamentals of production and costs in order to thinkabout optimal producer behavior.

Learn a framework for understanding production.

Learn a framework for understanding costs.

Econ 102: Introduction to Microeconomics Chapter 10: Production and Costs

Short-run Production DecisionsShort-Run CostsLong-Run Cost

Goals of this class

Goals of this class 1/ 14

Learn fundamentals of production and costs in order to thinkabout optimal producer behavior.

Learn a framework for understanding production.

Learn a framework for understanding costs.

Econ 102: Introduction to Microeconomics Chapter 10: Production and Costs

Short-run Production DecisionsShort-Run CostsLong-Run Cost

Goals of this class

Goals of this class 1/ 14

Learn fundamentals of production and costs in order to thinkabout optimal producer behavior.

Learn a framework for understanding production.

Learn a framework for understanding costs.

Econ 102: Introduction to Microeconomics Chapter 10: Production and Costs

Short-run Production DecisionsShort-Run CostsLong-Run Cost

Measuring ProductionExampleRelationship Between Marginals and AveragesProduct Curves

Short-Run Production 2/ 14

Short-run decisions: we’ll be considering changing only onefactor of production, eg: labor.

Long-run decisions: expand, buy new capital, new buildings,new land, contract, leave industry, new firms enter industry.

Total Product: maximum output that can be produced withgiven quantities of labor.

Marginal Product of Labor (MPL): additional output thatcan be produced when labor is increased by one unit.

Average Product of Labor (APL): average output perworker.

MPL =∆Q

∆LAPL =

Q

L

Econ 102: Introduction to Microeconomics Chapter 10: Production and Costs

Short-run Production DecisionsShort-Run CostsLong-Run Cost

Measuring ProductionExampleRelationship Between Marginals and AveragesProduct Curves

Short-Run Production 2/ 14

Short-run decisions: we’ll be considering changing only onefactor of production, eg: labor.

Long-run decisions: expand, buy new capital, new buildings,new land, contract, leave industry, new firms enter industry.

Total Product: maximum output that can be produced withgiven quantities of labor.

Marginal Product of Labor (MPL): additional output thatcan be produced when labor is increased by one unit.

Average Product of Labor (APL): average output perworker.

MPL =∆Q

∆LAPL =

Q

L

Econ 102: Introduction to Microeconomics Chapter 10: Production and Costs

Short-run Production DecisionsShort-Run CostsLong-Run Cost

Measuring ProductionExampleRelationship Between Marginals and AveragesProduct Curves

Short-Run Production 2/ 14

Short-run decisions: we’ll be considering changing only onefactor of production, eg: labor.

Long-run decisions: expand, buy new capital, new buildings,new land, contract, leave industry, new firms enter industry.

Total Product: maximum output that can be produced withgiven quantities of labor.

Marginal Product of Labor (MPL): additional output thatcan be produced when labor is increased by one unit.

Average Product of Labor (APL): average output perworker.

MPL =∆Q

∆LAPL =

Q

L

Econ 102: Introduction to Microeconomics Chapter 10: Production and Costs

Short-run Production DecisionsShort-Run CostsLong-Run Cost

Measuring ProductionExampleRelationship Between Marginals and AveragesProduct Curves

Short-Run Production 2/ 14

Short-run decisions: we’ll be considering changing only onefactor of production, eg: labor.

Long-run decisions: expand, buy new capital, new buildings,new land, contract, leave industry, new firms enter industry.

Total Product: maximum output that can be produced withgiven quantities of labor.

Marginal Product of Labor (MPL): additional output thatcan be produced when labor is increased by one unit.

Average Product of Labor (APL): average output perworker.

MPL =∆Q

∆LAPL =

Q

L

Econ 102: Introduction to Microeconomics Chapter 10: Production and Costs

Short-run Production DecisionsShort-Run CostsLong-Run Cost

Measuring ProductionExampleRelationship Between Marginals and AveragesProduct Curves

Short-Run Production 2/ 14

Short-run decisions: we’ll be considering changing only onefactor of production, eg: labor.

Long-run decisions: expand, buy new capital, new buildings,new land, contract, leave industry, new firms enter industry.

Total Product: maximum output that can be produced withgiven quantities of labor.

Marginal Product of Labor (MPL): additional output thatcan be produced when labor is increased by one unit.

Average Product of Labor (APL): average output perworker.

MPL =∆Q

∆LAPL =

Q

L

Econ 102: Introduction to Microeconomics Chapter 10: Production and Costs

Short-run Production DecisionsShort-Run CostsLong-Run Cost

Measuring ProductionExampleRelationship Between Marginals and AveragesProduct Curves

Short-Run Production 2/ 14

Short-run decisions: we’ll be considering changing only onefactor of production, eg: labor.

Long-run decisions: expand, buy new capital, new buildings,new land, contract, leave industry, new firms enter industry.

Total Product: maximum output that can be produced withgiven quantities of labor.

Marginal Product of Labor (MPL): additional output thatcan be produced when labor is increased by one unit.

Average Product of Labor (APL): average output perworker.

MPL =∆Q

∆LAPL =

Q

L

Econ 102: Introduction to Microeconomics Chapter 10: Production and Costs

Short-run Production DecisionsShort-Run CostsLong-Run Cost

Measuring ProductionExampleRelationship Between Marginals and AveragesProduct Curves

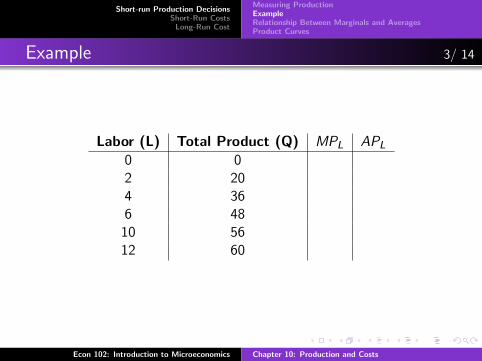

Example 3/ 14

Labor (L) Total Product (Q) MPL APL

0 02 204 366 48

10 5612 60

Econ 102: Introduction to Microeconomics Chapter 10: Production and Costs

Short-run Production DecisionsShort-Run CostsLong-Run Cost

Measuring ProductionExampleRelationship Between Marginals and AveragesProduct Curves

Marginal and Average Product 4/ 14

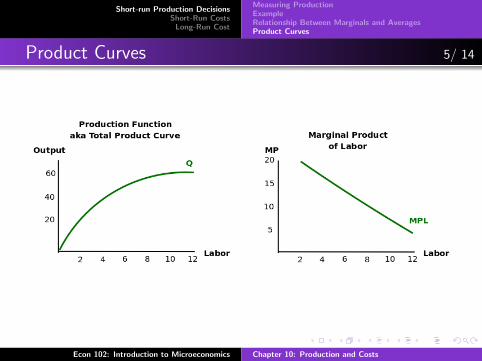

Law of Diminishing Marginal Product: aka law ofdiminishing returns, as the quantity of labor increases, themarginal product of labor decreases.

When graphing the total product curve, diminishing marginalproduct gives it a flattening curve.

Often, at very low levels of production, marginal product isactually increasing.

Relationship between average and marginal:

When the MPL > APL and as labor increases, does theaverage product increase or decrease?When the MPL < APL and as labor increases, does theaverage product increase or decrease?

Econ 102: Introduction to Microeconomics Chapter 10: Production and Costs

Short-run Production DecisionsShort-Run CostsLong-Run Cost

Measuring ProductionExampleRelationship Between Marginals and AveragesProduct Curves

Marginal and Average Product 4/ 14

Law of Diminishing Marginal Product: aka law ofdiminishing returns, as the quantity of labor increases, themarginal product of labor decreases.

When graphing the total product curve, diminishing marginalproduct gives it a flattening curve.

Often, at very low levels of production, marginal product isactually increasing.

Relationship between average and marginal:

When the MPL > APL and as labor increases, does theaverage product increase or decrease?When the MPL < APL and as labor increases, does theaverage product increase or decrease?

Econ 102: Introduction to Microeconomics Chapter 10: Production and Costs

Short-run Production DecisionsShort-Run CostsLong-Run Cost

Measuring ProductionExampleRelationship Between Marginals and AveragesProduct Curves

Marginal and Average Product 4/ 14

Law of Diminishing Marginal Product: aka law ofdiminishing returns, as the quantity of labor increases, themarginal product of labor decreases.

When graphing the total product curve, diminishing marginalproduct gives it a flattening curve.

Often, at very low levels of production, marginal product isactually increasing.

Relationship between average and marginal:

When the MPL > APL and as labor increases, does theaverage product increase or decrease?When the MPL < APL and as labor increases, does theaverage product increase or decrease?

Econ 102: Introduction to Microeconomics Chapter 10: Production and Costs

Short-run Production DecisionsShort-Run CostsLong-Run Cost

Measuring ProductionExampleRelationship Between Marginals and AveragesProduct Curves

Marginal and Average Product 4/ 14

Law of Diminishing Marginal Product: aka law ofdiminishing returns, as the quantity of labor increases, themarginal product of labor decreases.

When graphing the total product curve, diminishing marginalproduct gives it a flattening curve.

Often, at very low levels of production, marginal product isactually increasing.

Relationship between average and marginal:

When the MPL > APL and as labor increases, does theaverage product increase or decrease?When the MPL < APL and as labor increases, does theaverage product increase or decrease?

Econ 102: Introduction to Microeconomics Chapter 10: Production and Costs

Short-run Production DecisionsShort-Run CostsLong-Run Cost

Measuring ProductionExampleRelationship Between Marginals and AveragesProduct Curves

Marginal and Average Product 4/ 14

Law of Diminishing Marginal Product: aka law ofdiminishing returns, as the quantity of labor increases, themarginal product of labor decreases.

When graphing the total product curve, diminishing marginalproduct gives it a flattening curve.

Often, at very low levels of production, marginal product isactually increasing.

Relationship between average and marginal:

When the MPL > APL and as labor increases, does theaverage product increase or decrease?When the MPL < APL and as labor increases, does theaverage product increase or decrease?

Econ 102: Introduction to Microeconomics Chapter 10: Production and Costs

Short-run Production DecisionsShort-Run CostsLong-Run Cost

Measuring ProductionExampleRelationship Between Marginals and AveragesProduct Curves

Marginal and Average Product 4/ 14

Law of Diminishing Marginal Product: aka law ofdiminishing returns, as the quantity of labor increases, themarginal product of labor decreases.

When graphing the total product curve, diminishing marginalproduct gives it a flattening curve.

Often, at very low levels of production, marginal product isactually increasing.

Relationship between average and marginal:

When the MPL > APL and as labor increases, does theaverage product increase or decrease?When the MPL < APL and as labor increases, does theaverage product increase or decrease?

Econ 102: Introduction to Microeconomics Chapter 10: Production and Costs

Short-run Production DecisionsShort-Run CostsLong-Run Cost

Measuring ProductionExampleRelationship Between Marginals and AveragesProduct Curves

Product Curves 5/ 14

Econ 102: Introduction to Microeconomics Chapter 10: Production and Costs

Short-run Production DecisionsShort-Run CostsLong-Run Cost

Measuring ProductionExampleRelationship Between Marginals and AveragesProduct Curves

Product Curves 6/ 14

Econ 102: Introduction to Microeconomics Chapter 10: Production and Costs

Short-run Production DecisionsShort-Run CostsLong-Run Cost

Measures of CostCost Curves

Total Costs 7/ 14

Total Cost (TC): the cost of all the factors of productioncommitted to producing a good.

Total Fixed Cost (TFC): the cost of factors of productionthat are fixed in the short-run.

Examples: cost of owning capital, cost of renting land andbuildings, cost of using buildings.

Total Variable Cost (TVC): the cost of the variable factors,i.e. factors of production that can be changed in the shortrun.

Example: labor

TC = TFC + TVC

Econ 102: Introduction to Microeconomics Chapter 10: Production and Costs

Short-run Production DecisionsShort-Run CostsLong-Run Cost

Measures of CostCost Curves

Total Costs 7/ 14

Total Cost (TC): the cost of all the factors of productioncommitted to producing a good.

Total Fixed Cost (TFC): the cost of factors of productionthat are fixed in the short-run.

Examples: cost of owning capital, cost of renting land andbuildings, cost of using buildings.

Total Variable Cost (TVC): the cost of the variable factors,i.e. factors of production that can be changed in the shortrun.

Example: labor

TC = TFC + TVC

Econ 102: Introduction to Microeconomics Chapter 10: Production and Costs

Short-run Production DecisionsShort-Run CostsLong-Run Cost

Measures of CostCost Curves

Total Costs 7/ 14

Total Cost (TC): the cost of all the factors of productioncommitted to producing a good.

Total Fixed Cost (TFC): the cost of factors of productionthat are fixed in the short-run.

Examples: cost of owning capital, cost of renting land andbuildings, cost of using buildings.

Total Variable Cost (TVC): the cost of the variable factors,i.e. factors of production that can be changed in the shortrun.

Example: labor

TC = TFC + TVC

Econ 102: Introduction to Microeconomics Chapter 10: Production and Costs

Short-run Production DecisionsShort-Run CostsLong-Run Cost

Measures of CostCost Curves

Total Costs 7/ 14

Total Cost (TC): the cost of all the factors of productioncommitted to producing a good.

Total Fixed Cost (TFC): the cost of factors of productionthat are fixed in the short-run.

Examples: cost of owning capital, cost of renting land andbuildings, cost of using buildings.

Total Variable Cost (TVC): the cost of the variable factors,i.e. factors of production that can be changed in the shortrun.

Example: labor

TC = TFC + TVC

Econ 102: Introduction to Microeconomics Chapter 10: Production and Costs

Short-run Production DecisionsShort-Run CostsLong-Run Cost

Measures of CostCost Curves

Total Costs 7/ 14

Total Cost (TC): the cost of all the factors of productioncommitted to producing a good.

Total Fixed Cost (TFC): the cost of factors of productionthat are fixed in the short-run.

Examples: cost of owning capital, cost of renting land andbuildings, cost of using buildings.

Total Variable Cost (TVC): the cost of the variable factors,i.e. factors of production that can be changed in the shortrun.

Example: labor

TC = TFC + TVC

Econ 102: Introduction to Microeconomics Chapter 10: Production and Costs

Short-run Production DecisionsShort-Run CostsLong-Run Cost

Measures of CostCost Curves

Total Costs 7/ 14

Total Cost (TC): the cost of all the factors of productioncommitted to producing a good.

Total Fixed Cost (TFC): the cost of factors of productionthat are fixed in the short-run.

Examples: cost of owning capital, cost of renting land andbuildings, cost of using buildings.

Total Variable Cost (TVC): the cost of the variable factors,i.e. factors of production that can be changed in the shortrun.

Example: labor

TC = TFC + TVC

Econ 102: Introduction to Microeconomics Chapter 10: Production and Costs

Short-run Production DecisionsShort-Run CostsLong-Run Cost

Measures of CostCost Curves

Marginal and Average Cost 8/ 14

Marginal Cost (MC): the additional total cost fromproducing one additional unit of labor.

MC =∆TC

∆Q

Average Total Cost (ATC): the average cost of producingthe good.

ATC =TC

Q

Average Variable Cost (AVC): the average variable cost ofproducing the good.

AVC =TVC

Q

Econ 102: Introduction to Microeconomics Chapter 10: Production and Costs

Short-run Production DecisionsShort-Run CostsLong-Run Cost

Measures of CostCost Curves

Marginal and Average Cost 8/ 14

Marginal Cost (MC): the additional total cost fromproducing one additional unit of labor.

MC =∆TC

∆Q

Average Total Cost (ATC): the average cost of producingthe good.

ATC =TC

Q

Average Variable Cost (AVC): the average variable cost ofproducing the good.

AVC =TVC

Q

Econ 102: Introduction to Microeconomics Chapter 10: Production and Costs

Short-run Production DecisionsShort-Run CostsLong-Run Cost

Measures of CostCost Curves

Marginal and Average Cost 8/ 14

Marginal Cost (MC): the additional total cost fromproducing one additional unit of labor.

MC =∆TC

∆Q

Average Total Cost (ATC): the average cost of producingthe good.

ATC =TC

Q

Average Variable Cost (AVC): the average variable cost ofproducing the good.

AVC =TVC

Q

Econ 102: Introduction to Microeconomics Chapter 10: Production and Costs

Short-run Production DecisionsShort-Run CostsLong-Run Cost

Measures of CostCost Curves

Fixed Costs 9/ 14

Average Fixed Cost (AFC): the average fixed cost ofproducing the good.

AFC =TFC

Q

Since TC = TFC + TVC , it is also true thatATC = AFC + AVC

What happens to the average fixed cost when productionincreases?

What is the difference between marginal total cost andmarginal variable cost?

Econ 102: Introduction to Microeconomics Chapter 10: Production and Costs

Short-run Production DecisionsShort-Run CostsLong-Run Cost

Measures of CostCost Curves

Fixed Costs 9/ 14

Average Fixed Cost (AFC): the average fixed cost ofproducing the good.

AFC =TFC

Q

Since TC = TFC + TVC , it is also true thatATC = AFC + AVC

What happens to the average fixed cost when productionincreases?

What is the difference between marginal total cost andmarginal variable cost?

Econ 102: Introduction to Microeconomics Chapter 10: Production and Costs

Short-run Production DecisionsShort-Run CostsLong-Run Cost

Measures of CostCost Curves

Fixed Costs 9/ 14

Average Fixed Cost (AFC): the average fixed cost ofproducing the good.

AFC =TFC

Q

Since TC = TFC + TVC , it is also true thatATC = AFC + AVC

What happens to the average fixed cost when productionincreases?

What is the difference between marginal total cost andmarginal variable cost?

Econ 102: Introduction to Microeconomics Chapter 10: Production and Costs

Short-run Production DecisionsShort-Run CostsLong-Run Cost

Measures of CostCost Curves

Fixed Costs 9/ 14

Average Fixed Cost (AFC): the average fixed cost ofproducing the good.

AFC =TFC

Q

Since TC = TFC + TVC , it is also true thatATC = AFC + AVC

What happens to the average fixed cost when productionincreases?

What is the difference between marginal total cost andmarginal variable cost?

Econ 102: Introduction to Microeconomics Chapter 10: Production and Costs

Short-run Production DecisionsShort-Run CostsLong-Run Cost

Measures of CostCost Curves

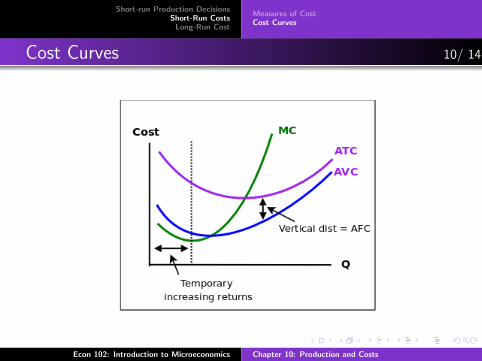

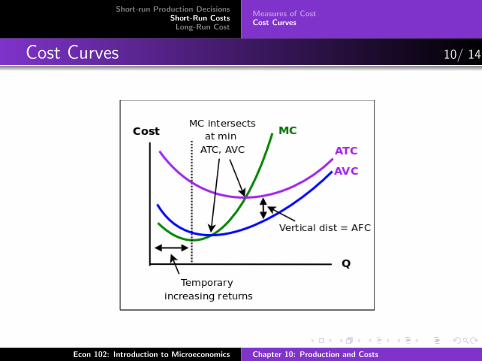

Cost Curves 10/ 14

Econ 102: Introduction to Microeconomics Chapter 10: Production and Costs

Short-run Production DecisionsShort-Run CostsLong-Run Cost

Measures of CostCost Curves

Cost Curves 10/ 14

Econ 102: Introduction to Microeconomics Chapter 10: Production and Costs

Short-run Production DecisionsShort-Run CostsLong-Run Cost

Measures of CostCost Curves

Cost Curves 10/ 14

Econ 102: Introduction to Microeconomics Chapter 10: Production and Costs

Short-run Production DecisionsShort-Run CostsLong-Run Cost

Measures of CostCost Curves

Cost Curves 10/ 14

Econ 102: Introduction to Microeconomics Chapter 10: Production and Costs

Short-run Production DecisionsShort-Run CostsLong-Run Cost

Measures of CostCost Curves

Shifts in Product/Cost Curves 11/ 14

Improvement in technology:

Shifts production function, APL, and MPL upward.Shifts average variable cost downward.Often new technology requires significant fixed costs →increase in TFC, TVC.What do you predict is the impact on ATC?

Increase in cost of factors of production.

Increase in cost of labor: shifts ATC, AVC, MC upward; othersunchanged.Increase in the cost of capital: shifts the AFC, ATC upward;others unchanged.

Econ 102: Introduction to Microeconomics Chapter 10: Production and Costs

Short-run Production DecisionsShort-Run CostsLong-Run Cost

Measures of CostCost Curves

Shifts in Product/Cost Curves 11/ 14

Improvement in technology:

Shifts production function, APL, and MPL upward.Shifts average variable cost downward.Often new technology requires significant fixed costs →increase in TFC, TVC.What do you predict is the impact on ATC?

Increase in cost of factors of production.

Increase in cost of labor: shifts ATC, AVC, MC upward; othersunchanged.Increase in the cost of capital: shifts the AFC, ATC upward;others unchanged.

Econ 102: Introduction to Microeconomics Chapter 10: Production and Costs

Short-run Production DecisionsShort-Run CostsLong-Run Cost

Measures of CostCost Curves

Shifts in Product/Cost Curves 11/ 14

Improvement in technology:

Shifts production function, APL, and MPL upward.Shifts average variable cost downward.Often new technology requires significant fixed costs →increase in TFC, TVC.What do you predict is the impact on ATC?

Increase in cost of factors of production.

Increase in cost of labor: shifts ATC, AVC, MC upward; othersunchanged.Increase in the cost of capital: shifts the AFC, ATC upward;others unchanged.

Econ 102: Introduction to Microeconomics Chapter 10: Production and Costs

Short-run Production DecisionsShort-Run CostsLong-Run Cost

Measures of CostCost Curves

Shifts in Product/Cost Curves 11/ 14

Improvement in technology:

Shifts production function, APL, and MPL upward.Shifts average variable cost downward.Often new technology requires significant fixed costs →increase in TFC, TVC.What do you predict is the impact on ATC?

Increase in cost of factors of production.

Increase in cost of labor: shifts ATC, AVC, MC upward; othersunchanged.Increase in the cost of capital: shifts the AFC, ATC upward;others unchanged.

Econ 102: Introduction to Microeconomics Chapter 10: Production and Costs

Short-run Production DecisionsShort-Run CostsLong-Run Cost

Measures of CostCost Curves

Shifts in Product/Cost Curves 11/ 14

Improvement in technology:

Shifts production function, APL, and MPL upward.Shifts average variable cost downward.Often new technology requires significant fixed costs →increase in TFC, TVC.What do you predict is the impact on ATC?

Increase in cost of factors of production.

Increase in cost of labor: shifts ATC, AVC, MC upward; othersunchanged.Increase in the cost of capital: shifts the AFC, ATC upward;others unchanged.

Econ 102: Introduction to Microeconomics Chapter 10: Production and Costs

Short-run Production DecisionsShort-Run CostsLong-Run Cost

Measures of CostCost Curves

Shifts in Product/Cost Curves 11/ 14

Improvement in technology:

Shifts production function, APL, and MPL upward.Shifts average variable cost downward.Often new technology requires significant fixed costs →increase in TFC, TVC.What do you predict is the impact on ATC?

Increase in cost of factors of production.

Increase in cost of labor: shifts ATC, AVC, MC upward; othersunchanged.Increase in the cost of capital: shifts the AFC, ATC upward;others unchanged.

Econ 102: Introduction to Microeconomics Chapter 10: Production and Costs

Short-run Production DecisionsShort-Run CostsLong-Run Cost

Measures of CostCost Curves

Shifts in Product/Cost Curves 11/ 14

Improvement in technology:

Shifts production function, APL, and MPL upward.Shifts average variable cost downward.Often new technology requires significant fixed costs →increase in TFC, TVC.What do you predict is the impact on ATC?

Increase in cost of factors of production.

Increase in cost of labor: shifts ATC, AVC, MC upward; othersunchanged.Increase in the cost of capital: shifts the AFC, ATC upward;others unchanged.

Econ 102: Introduction to Microeconomics Chapter 10: Production and Costs

Short-run Production DecisionsShort-Run CostsLong-Run Cost

Measures of CostCost Curves

Shifts in Product/Cost Curves 11/ 14

Improvement in technology:

Shifts production function, APL, and MPL upward.Shifts average variable cost downward.Often new technology requires significant fixed costs →increase in TFC, TVC.What do you predict is the impact on ATC?

Increase in cost of factors of production.

Increase in cost of labor: shifts ATC, AVC, MC upward; othersunchanged.Increase in the cost of capital: shifts the AFC, ATC upward;others unchanged.

Econ 102: Introduction to Microeconomics Chapter 10: Production and Costs

Short-run Production DecisionsShort-Run CostsLong-Run Cost

Returns to ScaleLong-Run Costs

Returns to Scale 12/ 14

In the long-run, you can increase all factors of production.

When a firm increases all of its factors of production by thesame proportion and..

output increases by an even larger proportion, then there areeconomies of scale.output increases by the same proportion, then there areconstant returns to scale.output increases by a smaller proportion, then there aredecreasing returns to scale.

Econ 102: Introduction to Microeconomics Chapter 10: Production and Costs

Short-run Production DecisionsShort-Run CostsLong-Run Cost

Returns to ScaleLong-Run Costs

Returns to Scale 12/ 14

In the long-run, you can increase all factors of production.

When a firm increases all of its factors of production by thesame proportion and..

output increases by an even larger proportion, then there areeconomies of scale.output increases by the same proportion, then there areconstant returns to scale.output increases by a smaller proportion, then there aredecreasing returns to scale.

Econ 102: Introduction to Microeconomics Chapter 10: Production and Costs

Short-run Production DecisionsShort-Run CostsLong-Run Cost

Returns to ScaleLong-Run Costs

Returns to Scale 12/ 14

In the long-run, you can increase all factors of production.

When a firm increases all of its factors of production by thesame proportion and..

output increases by an even larger proportion, then there areeconomies of scale.output increases by the same proportion, then there areconstant returns to scale.output increases by a smaller proportion, then there aredecreasing returns to scale.

Econ 102: Introduction to Microeconomics Chapter 10: Production and Costs

Short-run Production DecisionsShort-Run CostsLong-Run Cost

Returns to ScaleLong-Run Costs

Returns to Scale 12/ 14

In the long-run, you can increase all factors of production.

When a firm increases all of its factors of production by thesame proportion and..

output increases by an even larger proportion, then there areeconomies of scale.output increases by the same proportion, then there areconstant returns to scale.output increases by a smaller proportion, then there aredecreasing returns to scale.

Econ 102: Introduction to Microeconomics Chapter 10: Production and Costs

Short-run Production DecisionsShort-Run CostsLong-Run Cost

Returns to ScaleLong-Run Costs

Returns to Scale 12/ 14

In the long-run, you can increase all factors of production.

When a firm increases all of its factors of production by thesame proportion and..

output increases by an even larger proportion, then there areeconomies of scale.output increases by the same proportion, then there areconstant returns to scale.output increases by a smaller proportion, then there aredecreasing returns to scale.

Econ 102: Introduction to Microeconomics Chapter 10: Production and Costs

Short-run Production DecisionsShort-Run CostsLong-Run Cost

Returns to ScaleLong-Run Costs

Long-Run Costs 13/ 14

When a firm expands, the ATC shifts to the right.

The ATC may also shift somewhat downward or upward.

Long-run average total cost (LR-ATC): smallest short-runATC that can be obtained for different scales.

Relationship between LR-ATC and economies of scale:

When increasing scale lowers LR-ATC: economies of scale.When increasing scale does not change LR-ATC: constantreturn to scale.When increasing scale increases LR-ATC: diseconomies ofscale.

Econ 102: Introduction to Microeconomics Chapter 10: Production and Costs

Short-run Production DecisionsShort-Run CostsLong-Run Cost

Returns to ScaleLong-Run Costs

Long-Run Costs 13/ 14

When a firm expands, the ATC shifts to the right.

The ATC may also shift somewhat downward or upward.

Long-run average total cost (LR-ATC): smallest short-runATC that can be obtained for different scales.

Relationship between LR-ATC and economies of scale:

When increasing scale lowers LR-ATC: economies of scale.When increasing scale does not change LR-ATC: constantreturn to scale.When increasing scale increases LR-ATC: diseconomies ofscale.

Econ 102: Introduction to Microeconomics Chapter 10: Production and Costs

Short-run Production DecisionsShort-Run CostsLong-Run Cost

Returns to ScaleLong-Run Costs

Long-Run Costs 13/ 14

When a firm expands, the ATC shifts to the right.

The ATC may also shift somewhat downward or upward.

Long-run average total cost (LR-ATC): smallest short-runATC that can be obtained for different scales.

Relationship between LR-ATC and economies of scale:

When increasing scale lowers LR-ATC: economies of scale.When increasing scale does not change LR-ATC: constantreturn to scale.When increasing scale increases LR-ATC: diseconomies ofscale.

Econ 102: Introduction to Microeconomics Chapter 10: Production and Costs

Short-run Production DecisionsShort-Run CostsLong-Run Cost

Returns to ScaleLong-Run Costs

Long-Run Costs 13/ 14

When a firm expands, the ATC shifts to the right.

The ATC may also shift somewhat downward or upward.

Long-run average total cost (LR-ATC): smallest short-runATC that can be obtained for different scales.

Relationship between LR-ATC and economies of scale:

When increasing scale lowers LR-ATC: economies of scale.When increasing scale does not change LR-ATC: constantreturn to scale.When increasing scale increases LR-ATC: diseconomies ofscale.

Econ 102: Introduction to Microeconomics Chapter 10: Production and Costs

Short-run Production DecisionsShort-Run CostsLong-Run Cost

Returns to ScaleLong-Run Costs

Long-Run Costs 13/ 14

When a firm expands, the ATC shifts to the right.

The ATC may also shift somewhat downward or upward.

Long-run average total cost (LR-ATC): smallest short-runATC that can be obtained for different scales.

Relationship between LR-ATC and economies of scale:

When increasing scale lowers LR-ATC: economies of scale.When increasing scale does not change LR-ATC: constantreturn to scale.When increasing scale increases LR-ATC: diseconomies ofscale.

Econ 102: Introduction to Microeconomics Chapter 10: Production and Costs

Short-run Production DecisionsShort-Run CostsLong-Run Cost

Returns to ScaleLong-Run Costs

Long-Run Costs 13/ 14

When a firm expands, the ATC shifts to the right.

The ATC may also shift somewhat downward or upward.

Long-run average total cost (LR-ATC): smallest short-runATC that can be obtained for different scales.

Relationship between LR-ATC and economies of scale:

When increasing scale lowers LR-ATC: economies of scale.When increasing scale does not change LR-ATC: constantreturn to scale.When increasing scale increases LR-ATC: diseconomies ofscale.

Econ 102: Introduction to Microeconomics Chapter 10: Production and Costs

Short-run Production DecisionsShort-Run CostsLong-Run Cost

Returns to ScaleLong-Run Costs

Long-Run Costs 13/ 14

When a firm expands, the ATC shifts to the right.

The ATC may also shift somewhat downward or upward.

Long-run average total cost (LR-ATC): smallest short-runATC that can be obtained for different scales.

Relationship between LR-ATC and economies of scale:

When increasing scale lowers LR-ATC: economies of scale.When increasing scale does not change LR-ATC: constantreturn to scale.When increasing scale increases LR-ATC: diseconomies ofscale.

Econ 102: Introduction to Microeconomics Chapter 10: Production and Costs

Short-run Production DecisionsShort-Run CostsLong-Run Cost

Returns to ScaleLong-Run Costs

Long-Run Average Total Cost 14/ 14

Econ 102: Introduction to Microeconomics Chapter 10: Production and Costs