chapter 10 the events and behavioural approaches

TRANSCRIPT

Chapter 10

The events and behavioural approaches

New approaches in accounting theory

• Among the new approaches, we may distinguish:– the events approach– the behavioural approach– the human information processing approach – the predictive approach – the positive approach

• Each of these approaches has generated new methodologies and interest, and has employed unique ways of looking at accounting problems

The nature of the events approach

• The events approach was first explicitly stated after a divergence of opinion among the members of the Committee of the American Accounting Association, which issued a Statement of Basic Accounting Theory in 1966

• A majority of the Committee members favoured the value approach to accounting

The value school

The value school, also called the use-need school, considers that needs of users are known sufficiently to allow the deduction of an accounting theory that provides optimal input to the specified decision models

Conventional accounting model weaknesses

The conventional accounting model, based on the value approach, suffers from the following weaknesses:• its dimensions are limited• its classification schemes are not always

appropriate• its aggregation level for information is high• its degree of integration with the other

functional areas of an enterprise is too restricted

The events approach

• The events approach suggests that the purpose of accounting is ‘to provide information about relevant economic events that might be useful in a variety of decision models’

• The characteristics of an event may be directly observed and are of economic significance to the user

• Given the number of characteristics and the number of events susceptible to observation that might be relevant to the decision models of all types of users, the events approach suggests a tremendous expansion of the accounting data presented in financial reports.

Financial statements

• In the value approach:– the income statement is perceived as an

indicator of the financial performance of the firm for a given period

– the statement of cash flows is perceived as an expression of the changes in cash

• In the events approach:– the income statement is perceived as a

direct communication of the operating events that occur during a given period

Financial statements (cont’d)

– the statement of cash flows is better perceived as an expression of financial and investment events

– in other words, an event’s relevance rather than its output on cash flow determines the reporting of an event in the statement of cash flow

The normative events theory of accounting

• The normative events theory of accounting has been tentatively summarised as follows:– ‘In order for interested persons … to better

forecast the future of social organizations, … the most relevant attributes … of the crucial events … which affect the organization are aggregated … for periodic publication free of inferential bias’

• The objective of the normative events theory of accounting is to maximise the forecasting accuracy of accounting reports by focusing on the most relevant attributes of events crucial to the users

The normative events theory of accounting (cont’d)

• The theory calls for:1. an explicit taxonomy of real events,

which the accountant is to report2. more effective classification schemes,

with particular reference to labels that make it possible to associate observations of particular events with other related events

3. the structuring of an events-based accounting information system

Events-based accounting information systems

• One way to meet the objective of the normative events theory is to integrate it with database approaches to information management that assume an enterprise creates a centrally managed database for sharing among a wide range of users with highly diverse needs

• Such accounting systems include:– hierarchical models– network models– relational models– entity-relationship models– REA accounting models

The hierarchical model• The hierarchical model is based on the idea

of an events-accounting information system that allows users to make enquiries of a database

• The components of such a system include:– a mass database that contains a record of

all events in some generalised format– a user-defined structure that provides each

user with his or her own conceptual structure (and aggregation levels) of the events

– user-defined functions, or operations, for manipulating the data

The network model

• The network model is based on the concept of multidimensional accounting presented by Ijiri, and Charnes, Colantoni & Cooper

• The network model uses as input the initially unstructured database and a collection of queries or data requests to develop a hierarchical data structure that will minimise the number of records to be accessed to answer the desired set of queries

The entity-relationship model• The entity-relationship model assumes that

an accounting system is most naturally modelled in a database environment as a collection of real-world entities and relationships among those entities

• This model basically replaced the traditional chart of accounts and double-entry bookkeeping procedures by viewing entity-relationship in the form of entity tables and relationship tables

Evaluation of the events approach

• The events approach offers certain advantages and certain limitations

• The advantages predominantly take the form of efforts to provide information about relevant economic events that might be useful to a variety of decision models

• As a result, more information may be available to users who can then use their own utility function to determine the nature and level of aggregation of the information they need to make their particular decisions

The usefulness of the events approach

The usefulness of the events approach may depend on one or more of the following five factors:

1. the psychological ‘type’ of the decision maker

2. information overload, which may result from the attempt to measure the relevant characteristics of all crucial events affecting the firm

3. an adequate criterion for the choice of the crucial events has not been developed

The usefulness of the events approach (cont’d)

4. measuring all the characteristics of an events approach may prove to be difficult, given the state of the art of accounting

5. more research may be needed to examine the impact of different design approaches to the events approach theory, such as the hierarchical, network, relational, entity-relationship and REA models

The nature of the behavioural approach

• Most traditional approaches accounting theory construction have failed to consider user behaviour in particular and behavioural assumptions in general

• The behavioural approach to accounting theory formulation emphasises the relevance to decision-making of the information being communicated, and of the individual and group behaviour caused by the information being communicated

• The behavioural approach to accounting theory formulation is concerned with human behaviour as it relates to accounting information and problems

Behavioural accounting

• Although relatively new, the behavioural approach has generated enthusiasm and a new impetus in accounting research that focuses on the behavioural structure within which accountants function

• A new multidisciplinary area in the field of accounting has been conveniently labelled ‘behavioural accounting’

• The basic objective of behavioural accounting is to explain and predict behaviour in all possible accounting contexts

Behavioural effects of accounting information

• A more recent and exhaustive attempt by Dyckman, Gibbins and Swieringa illustrates the nature of studies of the behavioural effects of accounting information

• We may divide these studies into five general classes:

1. adequacy of disclosure2. usefulness of financial statement data3. attitudes about corporate reporting practices4. materiality judgements5. decision effects of alternative accounting

procedures

Adequacy of disclosure• Three approaches were used to examine the

adequacy of disclosure:1. the first examined the patterns of use of data

from the viewpoint of resolving controversial issues concerning the inclusion of certain information

2. the second examined the perceptions and attitudes of different interest groups

3. the third examined the extent to which different information items were disclosed in annual reports and the determinants of any significant differences in the adequacy of financial disclosure among companies

Adequacy of disclosure (cont’d)

• The research on disclosure adequacy and use showed:– general acceptance of the adequacy among

financial statements– recognition that the differences in disclosure

adequacy among financial statements are due to such variables as company size, profitability, and size and listing status of the auditing firm

The usefulness of financial statement data

• Two approaches were used to examine the usefulness of financial statement data:1. the first examined the relative importance of

the investment analysis of different information items to both users and preparers of financial information

2. the second examined the relevance of financial statements to decision-making, based on laboratory communication of financial statement data in terms of readability and meaning to users in general

The usefulness of financial statement data (cont’d)

• The overall conclusions of these studies were that:– some consensus exists between users and

preparers regarding the relative importance of the information items disclosed in financial statements

– users do not rely solely on financial statements when making their decisions

Attitudes about corporate reporting practices

• Two approaches were used to examine attitudes about corporate reporting practices:1. the first examined preferences for

alternative accounting techniques2. the second examined attitudes about

general reporting issues, such as how much information should be available, how much information is available, and the importance of certain items

Attitudes about corporate reporting practices (cont’d)

• These research items showed the extent to which some accounting techniques proposed by the authoritative bodies are accepted, and also brought to light some attitudinal differences among professional groups concerning reporting issues

Materiality judgements• Two approaches were used to examine

materiality judgements1. the first examined the main factors

determining the collection, classification and summarisation of accounting data

2. the second focused on what items people consider to be material, and sought to determine the degree of difference in accounting data that is required before the difference is perceived as material

• These studies indicated that several factors appear to affect materiality judgements, and that these judgements differ among individuals

Linguistic effects of accounting data and

techniques• Linguistics and accounting have many

similarities• Belkaoui argues that accounting is a

language and that according to the Sapir-Whorf hypothesis its lexical characteristics and grammatical rules will affect both the linguistic and the non-linguistic behaviour of users

Linguistic effects of accounting data and techniques (cont’d)

• Four propositions derived from the linguistic relativity paradigm to conceptually integrate the research findings of the impact of accounting information on the user’s behaviour, are as follows:

1. users who make certain lexical distinctions in accounting are enabled to talk and/or solve problems that cannot be solved by users who do not

2. users who make certain lexical distinctions in accounting are enabled to perform tasks more rapidly or more completely than those who do not

Linguistic effects of accounting data and techniques (cont’d)

3. users who possess the accounting (grammatical) rules are more predisposed to different managerial styles or emphases than those who do not

4. accounting techniques may tend to facilitate or render more difficult various managerial behaviours on the part of users

• These propositions have been empirically tested and verified in two studies that emphasise the importance of linguistic considerations in the use of accounting information and international standard-setting

Functional and data fixation• Functional fixation originated as a concept

in psychology, arising from an investigation of the impact of past experience on human behaviour

• Dunker introduced the concept of the functional fixation to illustrate the negative role of past experiences

• He investigated the hypothesis that an individual’s prior use of an object in a function dissimilar to that required in a present problem would serve to inhibit the discovery of an appropriate, novel use for the object

Ijiri, Jaedicke and Knight• Ijiri, Jaedicke and Knight viewed the decision

process as being characterised by three factors:– decision inputs– decision outputs– decision rules

• They introduced the conditions under which a decision maker cannot adjust his or her decision process to a change in the accounting process

• They attributed the inability to adjust, if it existed, to the psychological factor of functional fixation

Concepts of functional and data fixation in accounting

Various hypotheses exist for both the functional and data fixation results in accounting studies, namely:– The conditioning hypotheses: It

may be that the subjects of experiments, mostly accounting students, have been conditioned to react to some form of accounting outputs and have failed to adjust their decision processes in response to a ‘well-disclosed’ accounting change

Concepts of functional and data fixation in accounting (cont’d)

– Prospect theory and framing hypothesis: Framing occurs because the wording of a question has the potential to alter a subject’s response

– Primary versus recency ego involvement: In matters of ego involvement with an accounting technique just learned, subjects will give importance to what is perceived as relevant, significant or meaningful

Information inductance• The individual’s behaviour is influenced by

information in two ways:1. through information use when acting as a

recipient2. through information inductance when acting

• As stated by Prakash and Rappaport:‘An individual’s anticipating the consequences of his or her communication might lead him or her – before any information is communicated and, hence, even before any consequences arise – to choose to alter the information, or his or her behaviour, or even his or her objectives. This is the process of information inductance’

Time factors and information inductance

According to Prakash and Rappaport, time factors seem to govern inductance as follows:• ‘First, communication of information that is

either in fact a description of the sender’s behaviour, or is regarded as such by the information sender, or concerning which the information sender has some apprehension that it could be so regarded by the information recipient, will be strongly conducive to information inductance

• ‘Second, consequences that represent possible feedback effects on the information sender will be strongly conducive to information inductance’

The human information processing approach

• Interest in the human information processing approach arose from a desire to improve both the information set presented to financial data users and users’ ability to use such information

• Theories and models from human information processing psychology provide a tool for transforming accounting issues into generic information processing issues

• There are three main components of an information processing model:– input– process– output

Input

• Studies of the information set input (or cues) focus on the variables that are likely to affect the way people process information for decision making

• The variables examined are:1. the scaling characteristics of individual

cues2. the statistical properties of the information

set3. the informational content or predictive

significance4. the method of presentation5. the context

Process

Studies of the process component focus on the variables affecting the decision maker, such as:

1. characteristics of judgement2. characteristics of decision rules

Output

• Studies of the output component focus on variables related to the judgement, prediction or decision that are likely to affect the way the user processes the information

• The variables examined include:1. the qualities of the judgement2. self-insight

Four different approaches

The varying emphasis on any of the three components of an information processing model led to the use of four different approaches:

1. the lens model approach2. probabilistic judgement3. pre-decisional behaviour4. the cognitive-style approach

The lens model• Brunswick’s lens model allows explicit recognition

of the interdependence of environmental and individual-specific variables

• The model is used primarily to assess human judgemental situations in which people make judgements on the basis of a set of explicit cues from the environment

• The model emphasises the similarities between the environment and the subject response

• Most accounting research using the lens model has been motivated by the need to build mathematical models that represent the relative importance of different information cues, and by the need to measure the accuracy of judgement and its consistency, consensus and predictability

The lens model (cont’d)

• Various accounting-decision problems have been examined using the lens model. These include:

1. policy-capturing studies, which examine the relative importance of different cues in the judgement process, and consensus among decision makers

2. accuracy of judgements made on the basis of accounting cues

3. effects of task characteristics on achievement and learning

Probabilistic judgement• The probabilistic judgement approach,

sometimes known as the Bayesian approach, focuses first on a comparison of intuitive probability judgements and the normative model

• The normative model for probability revision, known as Bayes’ Theorem, is used as the descriptive model of human information processing

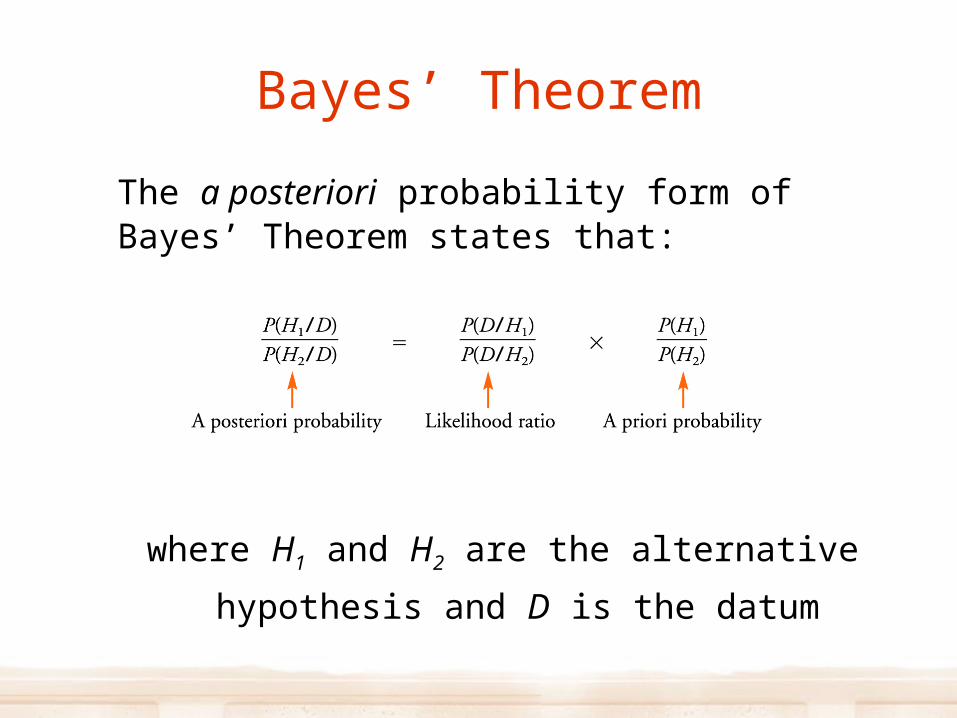

Bayes’ Theorem

The a posteriori probability form of Bayes’ Theorem states that:

where H1 and H2 are the alternative

hypothesis and D is the datum

Probabilistic judgement and Bayes’ Theorem

• The basic question examined in the early research in probabilistic judgement is whether probabilities are revised in the direction indicated by Bayes’ Theorem

• The findings suggest that this occurs to a lesser extent than Bayes’ Theorem suggests

• The phenomenon had been labelled conservatism

Heuristics and probabilistic judgement

• Tversky and Kahneman reported that people rely on a number of heuristics to reduce the complex task of assessing probabilities and predicting values to simpler judgemental operations

• These heuristics include:– representativeness, which refers to the

heuristic people use when they assess the probability of an event on the basis of its degree of similarity, or representativeness, to the category to which it is perceived to belong

Heuristics and probabilistic judgement (cont’d)

– availability, which refers to the heuristic people use when they assess the probability of an event on the basis of the ease with which it comes to mind

– adjustment and anchoring refer to the heuristic people use when they make estimates by starting with an initial value and then adjusting the value to yield the final answer

Pre-decisional behaviour

• Most of the experiments based on the lens model or on probabilistic judgement involve highly repetitive situations in which the task is well-defined, the subject is exposed to the right cues, and the problems are pre-specified, meaning that these experiments fail to explore the stages of pre-decisional behaviour

• Pre-decisional behaviour applies to the dynamics of problem definition, hypothesis formation and information search in less structured environments

Pre-decisional behaviour (cont’d)

• Pre-decisional behaviour is generally examined using process-tracing methods

• Process tracers tend to rely on four methods:1. eye movements2. information search behaviour3. information cue attending or response

time4. verbal ‘think aloud’ introspective

protocols

The cognitive-style approach• ‘Cognitive style’ is a hypothetical construct used to

explain the mediation process between stimuli and responses

• Five approaches to the study of cognitive style in psychology have been reported:– authoritarianism– dogmatism– cognitive complexity– integrative complexity– field dependence

• Accounting studies based on these five approaches have focused on classifying information users by their cognitive style and on designing information systems that are best suited to the decision maker’s cognitive style

Cognitive relativism in accounting

• Cognitive relativism in social psychology has created strong interest in the knowledge structure used in memory, and also in how people learn

• Gibbins describes professional judgement in public accounting as a five-component process:

1. schemas or knowledge structures accumulated through learning or experience

2. triggering event or stimulus3. judgement environment4. judgement process5. decision/action

Cognitive relativism in accounting (cont’d)

• The essence of cognitive relativism in accounting is the presence of a cognitive process that is assumed to guide the judgement/decision process

Cultural relativism in accounting

• Cultural relativism postulates that culture shapes the cognitive functioning of individuals who are faced with an accounting or auditing phenomenon

• This view holds that culture determines the judgement/decision process in accounting

• The definition of the components of culture is provided by Hofstede as four dimensions that reflect a country’s cultural orientations and explain 50 per cent of the differences in value systems among countries, being:

1. individualism versus collectivism2. large versus small power distance

Cultural relativism in accounting (cont’d)

3. strong versus weak uncertainty avoidance

4. masculinity versus femininity• This cultural relativism model assumes that

differences among these four dimensions create different cultural arenas that have the potential to dictate the organisational behaviour that may shape the judgement decision process in accounting

Cross-cultural research in accounting

There are at least five possible basic approaches to cross-cultural research in accounting, which are:

1. parochial studies, being the approach comprising studies of the USA conducted by Americans

2. ethnocentric studies, comprising studies that attempt to replicate American accounting research in foreign countries

3. polycentric studies, which comprise studies that describe accounting phenomena in foreign countries

Cross-cultural research in accounting (cont’d)

4. comparative accounting studies, which focus on identifying the similarities in accounting phenomena and cultures around the world

5. culturally synergistic studies, which focus on creating universality in accounting while maintaining an appropriate level of cultural specificity

Reasons for cross-cultural research

Cross-cultural research is needed in accounting for the following five reasons:1. it would establish the boundary

conditions for accounting models and theories

2. it would enable evaluation of the impact of cultural and ecological factors on behaviour in accounting

Reasons for cross-cultural research (cont’d)

3. although variables are often generally confounded, the confounding is not complete, as a few ‘cultunits’ may present deviant cases

4. cultures act as ‘natural grain-experiments’ by being high or low on variables of particular interest

5. cultures determine aspects of psychological functioning