chapter 15 corporations: dividends, retained earnings, and ... · 15-1 chapter 15 corporations:...

TRANSCRIPT

15-1

CHAPTER 15 Corporations: Dividends, Retained Earnings,

and Income Reporting

ASSIGNMENT CLASSIFICATION TABLE

Study Objectives

Questions

Brief Exercises

Exercises

Problems Set A

Problems Set B

1. Prepare the entries for cash dividends,

stock dividends, and stock splits, and compare their financial impact.

1, 2, 3, 4, 5, 6, 7

1, 2, 3, 4, 12

1, 2, 3, 4, 5, 7, 8

1, 2, 3, 4, 5

1, 2, 3, 4, 5

2. Prepare a statement of retained earnings.

8, 9, 10, 11, 12, 13

5, 6 5, 6, 7 2, 3, 5, 7 1,3, 5, 6

3. Prepare the shareholders’ equity section of a balance sheet.

14, 15 7 7, 8, 9 3, 4, 5 1, 2, 3, 4, 5

4. Illustrate the proper form and content of corporation income statements.

16, 17 8 10, 11 6, 7 6, 7

5. Explain the concept of intraperiod tax allocation and illustrate its impact on the financial statements.

18 8, 9 10, 11 6, 7 6, 7

6. Illustrate the statement presentation of material items not typical of regular operations.

19, 20 9 10, 11 6 6, 7

7. Calculate earnings and dividend ratios. 21, 22 10, 11, 12, 13

12, 13 6, 8 5, 6, 7, 8

15-2

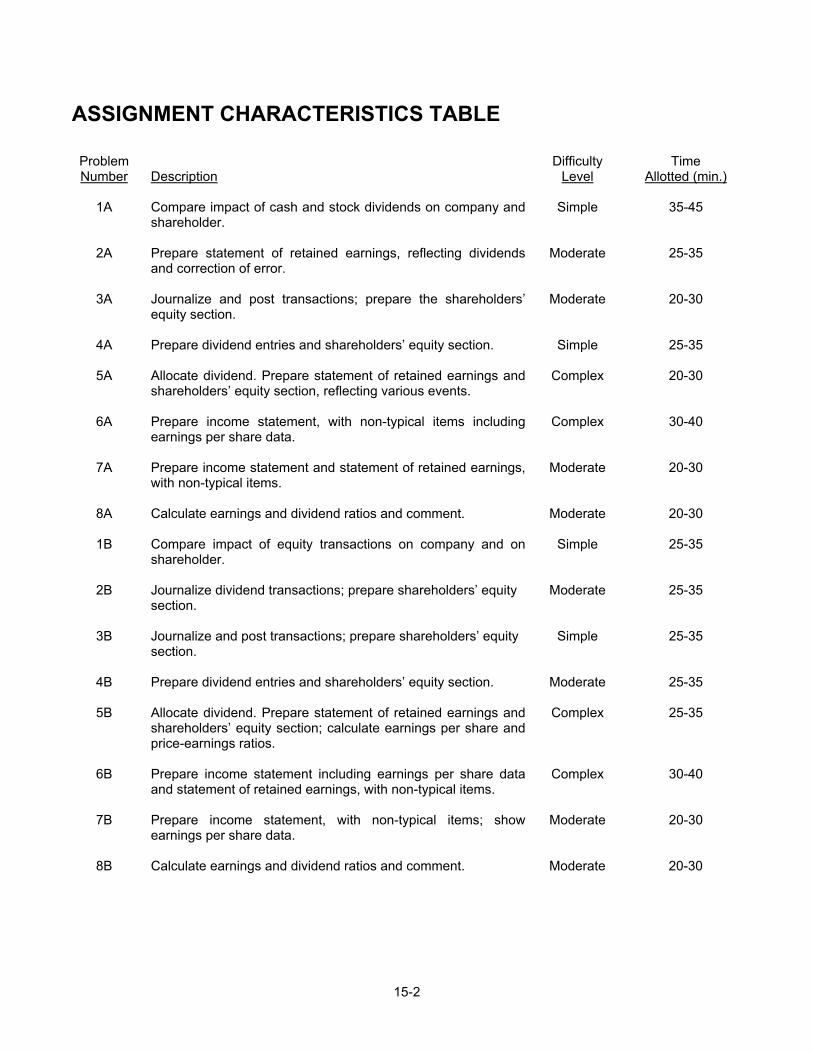

ASSIGNMENT CHARACTERISTICS TABLE

Problem Number

Description

Difficulty Level

Time Allotted (min.)

1A Compare impact of cash and stock dividends on company and

shareholder.

Simple 35-45

2A Prepare statement of retained earnings, reflecting dividends and correction of error.

Moderate 25-35

3A Journalize and post transactions; prepare the shareholders’ equity section.

Moderate 20-30

4A Prepare dividend entries and shareholders’ equity section.

Simple 25-35

5A Allocate dividend. Prepare statement of retained earnings and shareholders’ equity section, reflecting various events.

Complex 20-30

6A Prepare income statement, with non-typical items including earnings per share data.

Complex 30-40

7A Prepare income statement and statement of retained earnings, with non-typical items.

Moderate 20-30

8A Calculate earnings and dividend ratios and comment.

Moderate 20-30

1B Compare impact of equity transactions on company and on shareholder.

Simple 25-35

2B Journalize dividend transactions; prepare shareholders’ equity section.

Moderate 25-35

3B Journalize and post transactions; prepare shareholders’ equity section.

Simple 25-35

4B Prepare dividend entries and shareholders’ equity section.

Moderate 25-35

5B Allocate dividend. Prepare statement of retained earnings and shareholders’ equity section; calculate earnings per share and price-earnings ratios.

Complex 25-35

6B Prepare income statement including earnings per share data and statement of retained earnings, with non-typical items.

Complex 30-40

7B Prepare income statement, with non-typical items; show earnings per share data.

Moderate 20-30

8B Calculate earnings and dividend ratios and comment. Moderate 20-30

15-3

BLOOM’S TAXONOMY TABLE Correlation Chart between Bloom’s Taxonomy, Study Objectives and End-of-Chapter Material

Study Objectives Knowledge Comprehension Application Analysis Synthesis Evaluation 1. Prepare the entries

for cash dividends, stock dividends, and stock splits, and compare their financial impact.

Q15-1 Q15-2 Q15-3 Q15-4 Q15-5 Q15-7

Q15-6 BE15-1 BE15-2 BE15-3 BE15-4 BE15-12 E15-1 E15-2 E15-3 E15-4

E15-5 E15-7 E15-8 P15-2A P15-3A P15-4A P15-5A P15-2B P15-3B P15-4B P15-5B

P15-1A P15-1B

2. Prepare a statement of retained earnings

Q15-11

Q15-8 Q15-10 Q15-12 Q15-13

Q15-9 BE15-5 BE15-6 E15-5 E15-6 E15-7 P15-2A

P15-3A P15-5A P15-7A P15-3B P15-5B P15-6B

P15-1B

3. Prepare the shareholders’ equity section of a balance sheet.

Q15-14 Q15-15 BE15-7 E15-7 E15-8 E15-9 P15-3A

P15-4A P15-5A P15-2B P15-3B P15-4B P15-5B

P15-1B

4. Illustrate the proper form and content of corporation income statements.

Q15-16 Q15-17 E15-11 P15-6A P15-7A P15-6B P15-7B

BE15-8

E15-10

5. Explain the concept of intraperiod tax allocation and illustrate its impact on the financial statements.

Q15-18 BE15-9 E15-11 P15-6A P15-7A P15-6B P15-7B

BE15-8

E15-10

6. Illustrate the statement presentation of material items not typical of regular operations.

Q15-19 Q15-20

BE15-9 E15-11 P15-6A P15-6B P15-7B

E15-10

7. Calculate earnings and dividend ratios.

Q15-21 Q15-22

BE15-10 BE15-11 BE15-12 BE15-13 E15-12 E15-13

P15-6A P15-8A P15-5B P15-6B P15-7B P15-8B

Broadening Your Perspective

BYP15-1 BYP15-2 BYP15-3 BYP15-4 BYP15-5

BYP15-6 BYP15-7

15-4

15-5

ANSWERS TO QUESTIONS 01. (a) A dividend is a distribution by a corporation to its shareholders on

a pro rata (equal) basis, per share. (b) Disagree. Dividends may take four forms: cash, property, scrip

(promissory note to pay cash), or shares. 02. Robin is not correct. Adequate cash is only one of the conditions. In

order for a cash dividend to occur, a corporation must also have sufficient retained earnings and the dividend must be declared by the board of directors.

03. (a) The three dates are:

• Declaration date is the date when the board of directors formally declares the cash dividend and announces it to shareholders. The declaration commits the corporation to a binding legal obligation that cannot be rescinded.

• Record date is the date that marks the time when ownership

of the shares is determined from the shareholder records maintained by the corporation. The purpose of this date is to identify the persons or entities that will receive the dividend.

• Payment date is the date on which the dividend cheques are

mailed to the shareholders.

(b) The accounting entries and their dates are:

• Declaration date—Debit Cash Dividends and Credit Dividends Payable.

• No entry is made on the record date.

• Payment date—Debit Dividends Payable and Credit Cash.

15-6

Questions Chapter 15 (Continued) 0 4. From the perspective of the corporation, cash dividends decrease

assets, retained earnings, and total shareholders' equity. A stock dividend decreases retained earnings, increases share capital (contributed capital if the shares have a stated or par value), and has no effect on total assets and total shareholders' equity. If a cash dividend is paid, an individual shareholder’s personal financial position will increase by the amount of cash received. If a stock dividend is received, the shareholder’s personal financial position will increase by the market value of the share multiplied by the number of shares received.

5. A corporation generally issues stock dividends for one of the following

reasons:

1. To satisfy shareholders' dividend expectations without spending cash.

2. To increase the marketability of its share by increasing the number of shares and thereby decreasing the market price per share. Decreasing the market price of the share makes the shares easier to purchase for smaller investors.

3. To emphasize that a portion of shareholders' equity that had been reported as retained earnings has been permanently reinvested in the business and therefore is unavailable for cash dividends.

6. In the Pella Corporation the number of shares will increase to 20,000

(10,000 X 2). The effect of a split on market value is generally inversely proportional to the size of the split. In this case, the market price would fall to approximately $70 per share ($140 ÷ 2).

7. The different effects of a stock split versus a stock dividend are:

Item

Stock Split

Stock Dividend

Total contributed capital Total retained earnings Total value recorded for common shares Legal capital per share

No Change No Change No Change Decrease

Increase Decrease Increase No Change

15-7

Questions Chapter 15 (Continued) 8. A prior period adjustment is a correction of a material error in

reporting income of a prior period. The correction is reported in the current year's statement of retained earnings as an adjustment of the beginning balance of retained earnings.

9. The understatement of amortization in a prior year overstates the

beginning retained earnings balance. The statement of retained earnings presentation is:

Balance, January 1, as previously reported................ $240,000

Less: Correction for understatement of prior prior year's amortization (net of $22,500 income tax saving)............................. 67,500* Balance, January 1, as adjusted................................... $172,500

*$90,000 – ($90,000 X 25% tax savings) = $67,500 10. The purpose of a retained earnings restriction is to indicate that a

portion of retained earnings is currently unavailable for dividends. Restrictions may be either contractual or voluntary.

11. Retained earnings restrictions are generally reported in the notes to

the financial statements. (Occasionally, separate accounts are created, within the shareholders’ equity section of the balance sheet, for the restricted or appropriated amounts.)

12. The debits and credits to retained earnings are:

Debits

Credits

1. Net loss 2. Prior period adjustments

for overstatements of net income

3. Cash and stock dividends 4. Cumulative effect of a

change in accounting principle that decreased net income

1. Net income 2. Prior period adjustments for

understatements of net income

3. Cumulative effect of a change in accounting principle that increased net income

15-8

Questions Chapter 15 (Continued) 13. The cumulative effect of a change in accounting principle on net

income is reported, net of applicable income tax, as an adjustment to the opening balance of retained earnings. Thus, your friend is correct.

14. Omar is incorrect. Only the ending balance of retained earnings is

reported in the shareholders' equity section of the balance sheet. (The beginning balance appears in the statement of retained earnings, however. It would also appear as the ending balance of retained earnings for the preceding period, in a set of comparative financial statements.)

15. (a) Contributed Capital—Share Capital

(b) Contributed Capital—Share Capital (c) Contributed Capital—Share Capital (d) Contributed Capital—Additional Contributed Capital (e) Retained Earnings

16. Nels should be told that although many factors affect the market price

of a share at a given time, the reported net income is one of the most significant factors. When companies announce increases or decreases in net income, the market price of its share usually increases or decreases immediately. Net income also provides an indication of the amount of dividends that a company can distribute. In addition, net income leads to a growth in retained earnings, which is often reflected in a share's market price. Because net income is found on the income statement not the balance sheet, it is important to analyze all the financial statements when making investment decisions.

17. The unique feature of a corporation income statement is a separate

section that shows income tax expense. The presentation is as follows:

Income before income tax...........................................$500,000

Income tax expense* ...................................................0150,000 Net income ...................................................................$350,000

* This is usually subdivided, to show the portion which is currently due

and the portion which is due in future periods.

15-9

Questions Chapter 15 (Continued) *18. Intraperiod tax allocation refers to assigning income tax within the

financial statements (income statement and statement of retained earnings) to each item that directly affects the income tax for the period. As a result, income tax expense is allocated to income before income tax and to each nontypical item (discontinued operations, extraordinary items, and changes in accounting principles). Intraperiod tax allocation is important because it reflects the true effective tax rate in the income statement, and matches the income tax expense to the items which affect the tax.

*19. Discontinued operations refer to the disposal of a significant segment

of the business, such as the cessation of an entire activity or the elimination of a major class of customers. It is important to report discontinued operations separately from income from continuing operations because the discontinued segment will not affect future income statements. Thus, the predictive value of the income statement is enhanced.

20. Items (a), (d), and (g) are extraordinary items.

*21. Earnings per share (EPS) on income before extraordinary items

usually is more relevant to an investment decision than EPS on net income. Income before extraordinary items represents the results of continuing and ordinary business activity. It is therefore a better basis for predicting future operating results than an EPS figure which includes the effect of extraordinary items that are not expected to recur again in the foreseeable future.

22. (a) Favourable (b) Unfavourable

(c) Favourable (d) Unfavourable

15-10

SOLUTIONS TO BRIEF EXERCISES BRIEF EXERCISE 15-1 Nov. 1 Cash Dividends .................................................. 100,000

Dividends Payable...................................... 100,000 Dec. 1 No entry required on record date. Dec. 31 Dividends Payable.............................................. 100,000

Cash............................................................. 100,000 BRIEF EXERCISE 15-2 Dec. 1 Stock Dividends (8,000 X $15)........................... 120,000

Stock Dividends Distributable................... 120,000

31 Stock Dividends Distributable .......................... 120,000 Common Shares ......................................... 120,000

BRIEF EXERCISE 15-3

Before Stock

Dividend

After Stock

Dividend (a) Shareholders' equity

Common shares Retained earnings

Total shareholders' equity (b) Shares issued (c) Book value per share

$1,000,000 300,000 $1,300,000

100,000

$13.00

$ 1,160,000 140,000 $ 1,300,000

110,000

$11.82

15-11

BRIEF EXERCISE 15-4 I would anticipate the market price after the split would be $8 ($12 x 2/3 = $8). The reason for a stock split is usually to increase the marketability of the shares by reducing its price. BRIEF EXERCISE 15-5 CADIEN INC. Statement of Retained Earnings For the Year Ended December 31, 2003 Balance, January 1 ............................................................................. $220,000 Add: Net income ............................................................................... 0150,000 370,000 Less: Dividends ................................................................................. 0085,000 Balance, December 31........................................................................ $285,000 BRIEF EXERCISE 15-6 The cumulative prior income effect of a change in accounting principle is reported as an adjustment to the opening balance of retained earnings. In this case, the adjustment would be a deduction of $49,000, as follows: Cumulative effect of change in accounting principle

Effect on prior years' income of change in amortization method, net of $21,000 ($70,000 X 30%) income tax saving................................................................................... $49,000

Changes for the current year are reported in the current year’s income statement. The $8,000 would be included in the current year’s amortization expense.

15-12

BRIEF EXERCISE 15-7

MÉNARD CORPORATION Partial Balance Sheet

December 31, 2003

Shareholders' equity Share capital

Common shares, no par value, unlimited shares authorized, 5,000 shares issued..... $50,000 Common stock dividend distributable........... 15,000

Total share capital.................................... 65,000 Retained earnings (see Note 3) .............................. 29,000

Total shareholders' equity .............................. $94,000

Note 3: Retained earnings of $20,000 has been restricted for loan agreements

BRIEF EXERCISE 15-8 TEC.COM CORPORATION Partial Income Statement For the Year Ended November 30, 2003 Income before income tax ................................................................. $300,000 Income tax expense ($300,000 X 25%).............................................. 0 75,000 Income before extraordinary item..................................................... 225,000 Extraordinary loss from flood, net of $20,000 ($80,000 X 25%) income tax saving................................................ 0 60,000 Net income .......................................................................................... $165,000

15-13

BRIEF EXERCISE 15-9 OSBERN CORPORATION Partial Income Statement For the Year Ended December 31, 2003 Discontinued operations

Loss from operations of Mexico facility, net of $105,000 ($300,000 X 35%) income tax savings ............................... $195,000 Loss on disposal of Mexico facility, net of

$56,000 ($160,000 X 35%) income tax savings.................. 104,000 $299,000 BRIEF EXERCISE 15-10 Net income ($580,000 – $200,000 – $90,000) .................................... $290,000 Earnings per share: Income from continuing operations ................................................. $5.80 Loss from discontinued operations.................................................. (2.00) Income before extraordinary item..................................................... 3.80 Extraordinary loss .............................................................................. (0.90) Net income .......................................................................................... $2.90 BRIEF EXERCISE 15-11 (a) Earnings per share = $1.85 ($370,000 ÷ 200,000) (b) Earnings per share = $1.75 [($370,000 – $20,000) ÷ 200,000] (c) There would be no difference. Since the preferred shares are

cumulative, they need to be paid before any of the earnings become available to the common shareholders. Therefore, cumulative preferred dividends must be deducted from net income in calculating earnings per share, whether they are declared and paid or not.

15-14

BRIEF EXERCISE 15-12

Share Price Earnings per Share

Price-Earnings

Current

$52.50

$5.00

10.5

After 2% stock dividend

$51.451

$4.903

10.5

After 2-for-1 stock split

$26.252

$2.504

10.5

1 $52.50 x 98% = $51.45 2 $52.50 ÷ 2 = $26.25 3 $5.00 x 98% = $4.90 4 $5.00 ÷ 2 = $2.50 Both the stock dividend and the stock split will increase the number of shares, without changing the overall value of the company. Therefore, both will (theoretically) decrease the market price per share proportionately. Both will also decrease the earnings per share proportionately. Consequently, the price-earnings ratio should not be affected by either of these events. However, the stock markets may react favourably to the stock dividend and/or the stock split, with the result that the share price does not decrease proportionately, and hence the price-earnings ratio increases. BRIEF EXERCISE 15-13 Payout ratio = Cash dividends per share ÷ Earnings per share = $1.00 ÷ $ 3.75 = 26% Dividend yield = Cash dividends per share ÷ Share price = $1.00 ÷ $25.00 = 4%

15-15

SOLUTIONS TO EXERCISES EXERCISE 15-1 (a)

2002

2003

2004 Total dividend declaration Allocation to preferred shares Remainder to common shares

$6,000 06,000 $ 0

$12,000 008,000 $ 4,000

$28,000 008,000 $20,000

(b)

2002

2003

2004 Total dividend declaration Allocation to preferred shares Remainder to common shares

$6,000 06,000 $ 0

$12,000 12,0001 $ 0

$28,000 012,0002 $16,000

1 Cumulative dividend for 2002, $4,000, plus $8,000 for 2003 2 Cumulative dividend for 2003, $2,000, plus $10,000 for 2004

(c) Dec. 31 Cash Dividends—Preferred................................. 8,000 Cash Dividends—Common ................................. 20,000 Dividends Payable ................................ 28,000 Dec. 31 Cash Dividends—Preferred................................. 12,000 Cash Dividends—Common ................................. 16,000

Dividends Payable ................................ 28,000

15-16

EXERCISE 15-2

Before Action

After Stock

Dividend

After Stock

Split Shareholders' equity

Common shares Retained earnings

Total shareholders' equity Shares issued Book value per share

$ 800,000 400,000$ 1,200,000 80,000

$15.00

$ 856,000* 344,000 $1,200,000

84,000

$14.29

$ 800,000 400,000 $ 1,200,000

160,000

$7.50

* $800,000 + (80,000 shares X 5% X $14) = $856,000 Note that the total shareholders’ equity is the same in each case. EXERCISE 15-3 (a) (1) Book value before the stock dividend was $20.00 ($400,000 ÷ 20,000 = $20.00)

(2) Book value after the stock dividend is $18.18 ($400,000 ÷ 22,000 = $18.18)

(b) Share capital

Balance before dividend..................................................... $225,000 Stock dividend (2,000 x $18) .............................................. 00336,000

New balance................................................................. $261,000

Retained earnings Balance before dividend..................................................... $175,000 Stock dividend (2,000 X $18) .............................................. 0036,000

New balance................................................................. $139,000

15-17

EXERCISE 15-4 1. Dec. 31 Cash Dividends......................................... 30,000

Dividend Expense............................. 30,000 2. Dec. 31 Stock Dividends* ...................................... 10,000

Dividends Payable.................................... 10,000 Common Stock Dividends Distributable 10,000 Retained Earnings* ........................... 10,000

3. Dec. 31 Preferred Shares ...................................... 2,000,000

Retained Earnings ............................ 2,000,000 No entry is required for a stock split * Note: This portion of the correcting entry could be omitted since the

Stock Dividend account is closed into the Retained Earnings account at year end.

EXERCISE 15-5 (a) April 1 Cash............................................................... 85,000 Common Shares ................................... 85,000 June 15 Cash Dividends (80,000 X $1)...................... 80,000

Dividends Payable ................................ 80,000

July 10 Dividends Payable........................................ 80,000 Cash ....................................................... 80,000

Dec. 15 Cash............................................................... 38,000

Common Shares ................................... 38,000 Cash Dividends (82,000 X $1.30)................. 106,600

Dividends Payable ................................ 106,600 (b) In the statement of retained earnings, cash dividends of $186,600 will

be deducted. In the balance sheet, dividends payable of $106,600 will be reported as a current liability.

15-18

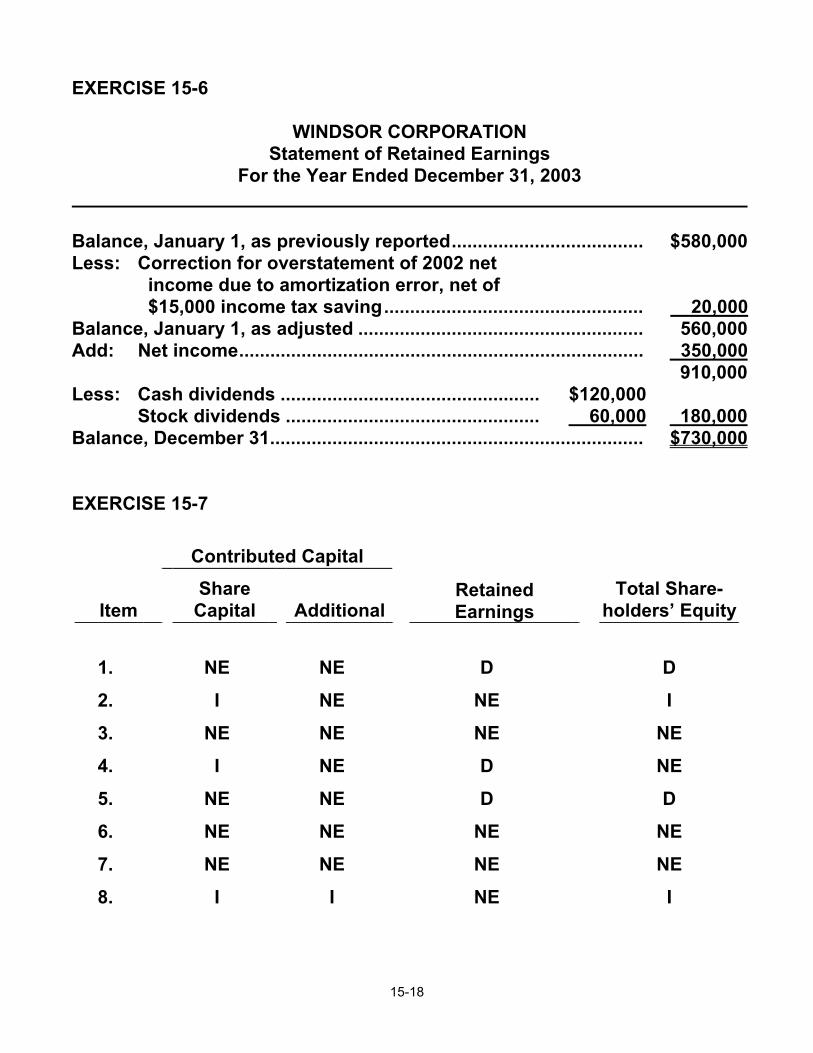

EXERCISE 15-6 WINDSOR CORPORATION Statement of Retained Earnings For the Year Ended December 31, 2003 Balance, January 1, as previously reported..................................... $580,000 Less: Correction for overstatement of 2002 net income due to amortization error, net of $15,000 income tax saving.................................................. 20,000 Balance, January 1, as adjusted ....................................................... 560,000 Add: Net income.............................................................................. 350,000 910,000 Less: Cash dividends .................................................. $120,000

Stock dividends ................................................. 0060,000 180,000 Balance, December 31........................................................................ $730,000 EXERCISE 15-7

Contributed Capital

Item

Share Capital

Additional

Retained Earnings

Total Share-

holders’ Equity

1. 2. 3. 4. 5. 6. 7. 8.

NE I

NE I

NE NE NE I

NE NE NE NE NE NE NE I

D

NE NE D D

NE NE NE

D I

NE NE D

NE NE I

15-19

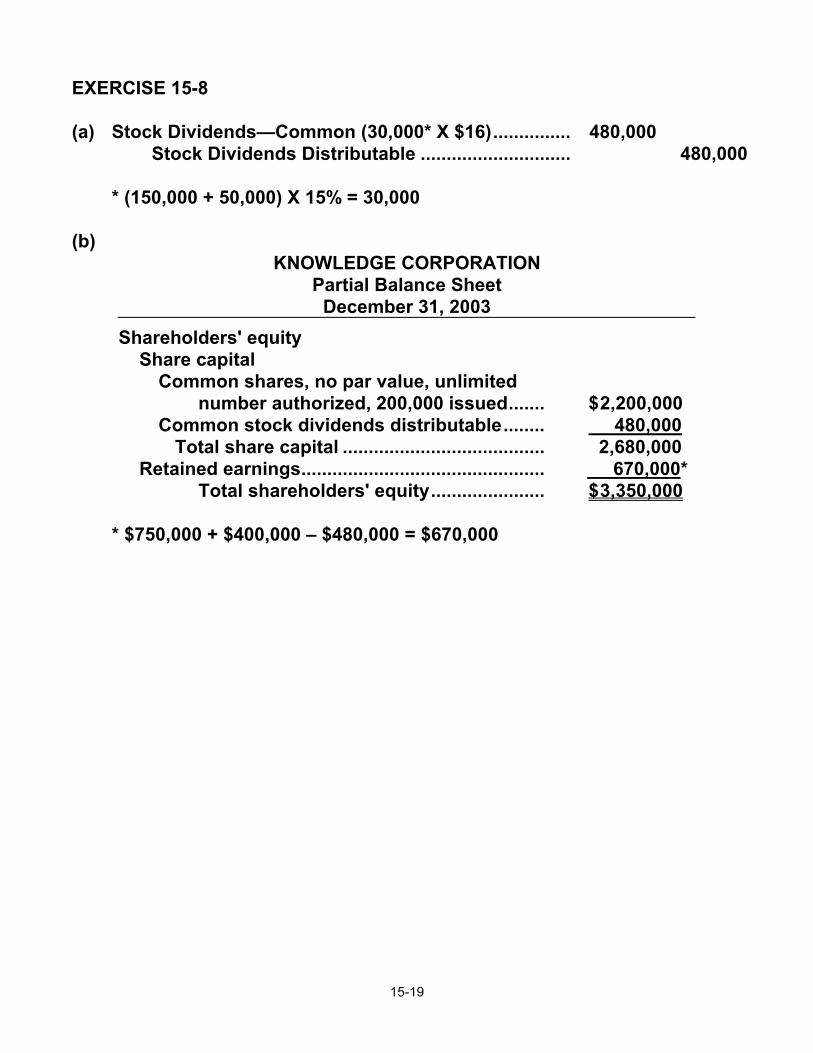

EXERCISE 15-8 (a) Stock Dividends—Common (30,000* X $16)............... 480,000

Stock Dividends Distributable ............................. 480,000

* (150,000 + 50,000) X 15% = 30,000 (b)

KNOWLEDGE CORPORATION Partial Balance Sheet

December 31, 2003 Shareholders' equity Share capital Common shares, no par value, unlimited number authorized, 200,000 issued.......

Common stock dividends distributable........ Total share capital ....................................... Retained earnings............................................... Total shareholders' equity......................

$ 2,200,000 480,000

2,680,000 670,000* $ 3,350,000

* $750,000 + $400,000 – $480,000 = $670,000

15-20

EXERCISE 15-9 BYUNG–KEE INC.

Partial Balance Sheet December 31, 2003

Shareholders' equity Contributed capital Share capital 8% preferred shares, $5 stated value, cumulative, 40,000 shares authorized, 30,000 shares issued $0,150,000 Common shares, no par value, 400,000 shares authorized, 300,000 shares issued ................... 866,000 Common stock dividends distributable ................... 75,000

Total share capital ...................................... 1,091,000 Additional contributed capital

Contributed capital in excess of stated value —preferred shares.............................................. 244,000

Total contributed capital ............................ 1,335,000 Retained earnings (See Note R)........................................... 900,000

Total shareholders' equity ......................... $2,235,000 Note R: Retained earnings restricted for plant expansion, $100,000.

15-21

EXERCISE 15-10 (a)

GROMETER CORPORATION Partial Income Statement For the Year Ended October 31, 2003

Income before income tax................................................. $640,000

Income tax expense ($640,000 X 30%) ............................. 0 192,000 Income before extraordinary item .................................... 448,000 Extraordinary loss from fire, net of $30,000 ($100,000 X 30%) income tax saving ............................. 00 70,000 Net income.......................................................................... $378,000

(b) To: Dave Grometer Corporation

From: Independent Auditor After reviewing your income statement for the year ended October 31,

2003, we believe it is misleading for the following reasons:

The amount reported for income before extraordinary items is overstated by $30,000. The income tax expense should be 30% of $640,000, or $192,000, not $162,000. The after-tax income from operations was only $448,000, not $478,000.

Also, the effect of the extraordinary loss on net income is only $70,000, not $100,000. An income tax savings of $30,000 should be netted against the extraordinary loss. Taking these tax savings into consideration, the real cost of the fire damage was only $70,000, not $100,000.

15-22

EXERCISE 15-11 (a) DASOLA CORPORATION

Partial Income Statement For the Year Ended December 31, 2003

Income from continuing operations................................. $240,000

Discontinued operations Gain on discontinued division, net of $15,000 income tax expense ....................... 35,000

Income before extraordinary item .................................... 275,000 Extraordinary loss, net of $24,000 income tax saving ... 56,000

Net income ......................................................................... $219,000 (b) The correction of an error in last year's financial statements is a prior

period adjustment. The correction is reported in the 2003 statement of retained earnings as an adjustment that increases the reported beginning balance of retained earnings by $14,000, after income tax expense [$20,000 – ($20,000 X 30%)].

The effect on prior years of the change in accounting principle

(amortization method) should also be treated as an adjustment to the reported beginning balance of retained earnings. It would reduce the retained earnings by $24,500, after income tax expense. [$35,000 – ($35,000 x 30%)]

EXERCISE 15-12 (a) $ 547,000 – $16,000 = $531,000 ÷ 100,000 = $5.31 (b) $ 547,000 – $16,000 = $531,000 ÷ 100,000 = $5.31 Note that, since the preferred dividends are cumulative, there is no difference between parts (a) and (b)

15-23

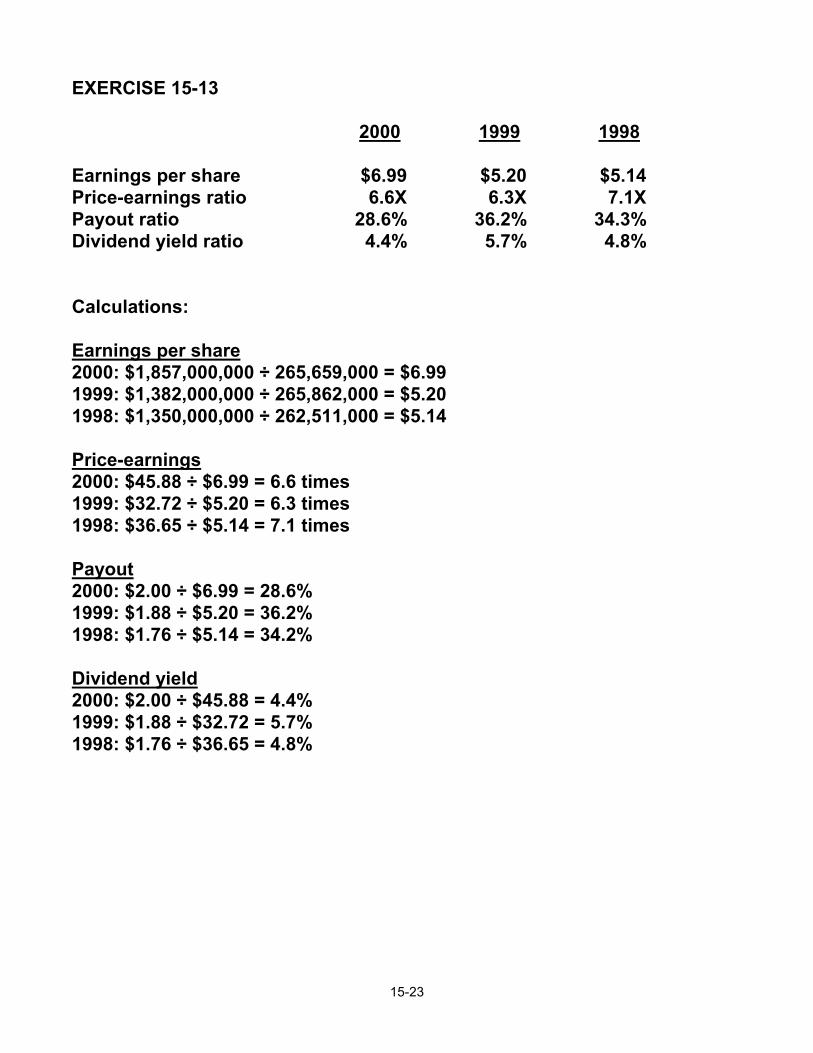

EXERCISE 15-13 2000 1999 1998 Earnings per share $6.99 $5.20 $5.14 Price-earnings ratio 6.6X 6.3X 7.1X Payout ratio 28.6% 36.2% 34.3% Dividend yield ratio 4.4% 5.7% 4.8% Calculations: Earnings per share 2000: $1,857,000,000 ÷ 265,659,000 = $6.99 1999: $1,382,000,000 ÷ 265,862,000 = $5.20 1998: $1,350,000,000 ÷ 262,511,000 = $5.14 Price-earnings 2000: $45.88 ÷ $6.99 = 6.6 times 1999: $32.72 ÷ $5.20 = 6.3 times 1998: $36.65 ÷ $5.14 = 7.1 times Payout 2000: $2.00 ÷ $6.99 = 28.6% 1999: $1.88 ÷ $5.20 = 36.2% 1998: $1.76 ÷ $5.14 = 34.2% Dividend yield 2000: $2.00 ÷ $45.88 = 4.4% 1999: $1.88 ÷ $32.72 = 5.7% 1998: $1.76 ÷ $36.65 = 4.8%

15-24

EXERCISE 15-13 (Continued) Earnings per share have improved over the past year, moving from $5.14 to $6.69. This indicates that the company is earning more income for each of its common shareholders. This increase occurred partially because net income is higher and partially because the number of common shares issued has decreased. The PE ratio declined in 1999, then rebounded slightly in 2000. This number should be compared to other companies in the industry to see if a multiple of around seven (6.6 in 2000) is good for this type of business. Even though the dividend is increasing, the dividend yield and the payout ratios have generally decreased. The company is earning more income but is not increasing its dividend proportionally. Although some investors who like receiving dividends may be concerned, the company may simply be retaining the remaining income to finance further growth.

15-25

SOLUTIONS TO PROBLEMS

PROBLEM 15-1A

(a)

Cash Dividend Stock Dividend Assets

$13,500,000 - $80,000a = $13,420,000

No effect = $13,500,000

Liabilities

No effect = $1,500,000

No effect = $1,500,000

Share capital

No effect = $2,000,000

$2,000,000 + $80,000b = $2,080,000

Retained earnings

$10,000,000 - $80,000 = $9,920,000

$10,000,000 - $80,000 $ 9,920,000

Total shareholders’ equity

$12,000,000 - $80,000 = $11,920,000

No effect ($12,000,000 + $80,000 - $80,000 = $12,000,000)

Number of shares

No effect = 40,000

2,000 increase (2,000 + 40,000 = 42,000)

a 40,000 X $2 = $80,000 b 40,000 X 5% = 2,000 x $40 = $80,000 (b) 1. Cash dividend Cash dividend 1,000 X $2 = $2,000 Market value of shares 1,000 X $40 = $40,000 Stock Dividend Stock dividend 1,000 x 5% = 50 x $40 = $2,000 Market value of shares 1,050 X $40 = $42,000

15-26

PROBLEM 15-1A (Continued) (b) 1. (Continued) In terms of final value the shareholder would be in the same

position having received either a cash or a stock dividend. However, a stock dividend would allow the shareholder to control the receipt of the cash and the related tax payment. Since the shareholder can control when the shares are sold, they can control when the income tax would have to be paid on any gains. Alternatively, some shareholders may prefer to receive a cash dividend since they do not have to sell the shares to obtain the cash. As well, there are often brokerage fees associated with selling shares.

The decision as to whether a cash or stock dividend would be more

beneficial really depends on the preferences of the shareholder and their tax situation.

(b) 2. The shareholder would record the cash dividend as a debit to Cash

and a credit to Dividend Revenue. The stock dividend would be recorded only as an increase in the number of shares held.

15-27

PROBLEM 15-2A

Journal entries–not required July 1 Cash Dividends–Common ............................. 45,000

(180,000 X $0.25) Dividends Payable–Common ................. 45,000

Aug . 1 Accumulated Amortization ............................ 72,000 Income Tax Payable................................ 22,000

Retained Earnings................................... 50,000 Sept. 1 Dividends Payable–Common......................... 45,000

Cash.......................................................... 45,000 Dec. 01 Stock Dividends–Common (18,000 X $15).... 270,000

Common Stock Dividends Distributable 270,000 15 Cash Dividends–Preferred (4,000 X $10) ...... 40,000

Dividends Payable–Preferred................. 40,000

15-28

PROBLEM 15-2A (Continued) TMAO INC. Statement of Retained Earnings For the Year Ended December 31, 2003

Balance, January 1, as previously reported ......................... $500,000

Add: Correction for overstatement of amortization in 2002, net of income tax expense of $22,000 ..... 0050,000 Balance, January 1, as adjusted............................................ 550,000 Add: Net income................................................................... 0350,000

900,000 Less: Cash dividends—preferred .................... $040,000

Cash dividends—common ..................... 45,000 Stock dividends—common .................... 270,000 355,000

Balance, December 31............................................................ $545,000

15-29

PROBLEM 15-3A

GENERAL JOURNAL J1

Date Account Titles and Explanation

Debit

Credit

Jan. 20 Stock Dividend Distributable ................. 200,000 Common Shares.............................. 200,000 Feb. 12 Cash.......................................................... 150,000 Common Shares.............................. 150,000

Mar. 31 Income Tax Payable ................................ 20,000 Retained Earnings................................... 50,000

Inventory .......................................... 70,000

Dec. 31 Cash Dividends ....................................... 100,000 Cash ................................................. 100,000

31 Revenues ................................................. 900,000

Retained Earnings........................... 900,000 31 Retained Earnings................................... 600,000

Expenses ......................................... 600,000 31 Retained Earnings................................... 100,000

Cash Dividends ............................... 100,000

15-30

PROBLEM 15-3A (Continued) (b) Common Shares Date

Explanation

Ref.

Debit

Credit

Balance

Jan. 1 20 Feb. 12

J1 J1

200,000 150,000

1,500,000 1,700,000 1,850,000

Common Stock Dividends Distributable Date

Explanation

Ref.

Debit

Credit

Balance

Jan. 1 20

J1 J1

0200,000

200,000

0200,000

000,000 Cash Dividends Date

Explanation

Ref.

Debit

Credit

Balance

Jan. 1 Dec. 31

Closing entry

J1 J1

100,000

100,000

100,000

0 Retained Earnings Date

Explanation

Ref.

Debit

Credit

Balance

Jan. 1 Mar. 31 Dec. 31 31 31

Closing entry Closing entry Closing entry

J1 J1 J1 J1

50,000

600,000 100,000

900,000

600,000 550,000

1,450,000 850,000 750,000

15-31

PROBLEM 15-3A (Continued) (c) CEDENO INC. Partial Balance Sheet December 31, 2003

Shareholders' equity

Share capital Common shares, no par value, unlimited number of shares authorized, 580,000 shares issued ......................................... $1,850,000

Retained earnings ........................................................... 00,750,000 Total shareholders' equity ....................................... $2,600,000

15-32

PROBLEM 15-4A

(a)

GENERAL JOURNAL J1

Date Account Titles and Explanation

Debit

Credit

Jan. 15 Cash Dividends (70,000 X $1) ................ 70,000

Dividends Payable........................... 70,000

Feb. 15 Dividends Payable .................................. 70,000 Cash ................................................. 70,000

Apr. 15 Stock Dividends (7,000 X $13) ............... 91,000

Common Stock Dividends Distributable 91,000

May 15 Common Stock Dividends Distributable 91,000 Common Shares ............................. 91,000

July 01 Memo: two-for-one stock split increases the number of shares to 154,000 (77,000 X 2)

Dec. 01 Cash Dividends (154,000 X $0.50) ......... 77,000

Dividends Payable........................... 77,000 31 Revenues ................................................. 1,000,000

Retained Earnings........................... 1,000,000 31 Retained Earnings................................... 750,000

Expenses ......................................... 750,000 31 Retained Earnings .................................. 238,000

Cash Dividends ............................... 147,000 Stock Dividends .............................. 91,000

15-33

PROBLEM 15-4A (Continued) (b) Common Shares Date

Explanation

Ref.

Debit

Credit

Balance

Jan. 1 May 15

J1

91,000

900,000 991,000

Common Stock Dividends Distributable Date

Explanation

Ref.

Debit

Credit

Balance

Apr. 15 May 15

J1 J1

091,000

0191,000

091,000 000,000

Cash Dividends Date

Explanation

Ref.

Debit

Credit

Balance

Jan. 15 Dec. 1 31

Closing entry

J1 J1 J1

70,000 77,000

147,000

70,000

147,000 0

Stock Dividends Date

Explanation

Ref.

Debit

Credit

Balance

Apr. 15 Dec. 31

J1 J1

091,000

01

91,000

091,000 000,000

Retained Earnings Date

Explanation

Ref.

Debit

Credit

Balance

Jan. 1 Dec. 31 31 31

Closing entry Closing entry Closing entry

J1 J1 J1

750,000 238,000

1,000,000

540,000

1,540,000 790,000 552,000

15-34

PROBLEM 15-4A (Continued) (c)

LEBLANC CORPORATION Partial Balance Sheet

December 31, 2003 Shareholders' equity

Share capital Common shares, no par value, unlimited number of shares authorized, 154,000 shares issued......... $ 991,000

Retained earnings ............................................................ 00,552,000 Total shareholders' equity..................................... $1,543,000

15-35

PROBLEM 15-5A

(a) Total dividend $600,000 Allocated to preferred shares— current year only (10,000 X $10) 0100,000 Remainder to common shares $500,000

Note: the preferred shares are noncumulative and therefore no dividends in arrears have to be paid

(b)

JAJOO CORPORATION Statement of Retained Earnings

For the Year Ended December 31, 2003

Balance, January 1 ............................................... $ 2,450,000

Add: Net income................................................. 880,000 3,330,000 Less: Cash dividends—Preferred ...................... $100,000 Cash dividends—Common ...................... 500,000

Stock dividends......................................... 00140,000* 740,000 Balance, December 31 ......................................... $2,590,000

* 400,000 x 5% = 20,000 x $7 = $140,000

15-36

PROBLEM 15-5A (Continued) (c)

JAJOO CORPORATION Partial Balance Sheet

December 31, 2003 Shareholders' equity

Contributed capital Share capital

$10 preferred shares, no par value, noncumulative, 20,000 shares

authorized, 10,000 shares issued .............. $1,200,000 Common shares, $5 stated value, 600,000 shares authorized, 400,000 shares issued 2,000,000

Common stock dividends distributable, 20,000 shares............................................ 140,000

Total share capital.................................... 3,340,000 Additional contributed capital

Contributed capital in excess of stated value—common shares.............................. 1,100,000

Total contributed capital.......................... 4,440,000 Retained earnings (See Note 3) ..................................... 2,590,000

Total shareholders' equity....................... $7,030,000 Note 3: Retained earnings restricted for plant expansion, $100,000.

15-37

PROBLEM 15-6A

(a) HYPERCHIP CORPORATION Income Statement For the Year Ended November 30, 2003

Net sales .............................................................. $1,400,000

Cost of goods sold.............................................. 0 ,800,000 Gross profit ......................................................... 600,000 Selling expenses................................................. $110,000 Administrative expenses.................................... ,140,000 250,000 Income from operations ..................................... 350,000 Other revenues and gains.................................. $40,000 Other expenses and losses ............................... 0030,000 0, 010,000 Income before income tax.................................. 360,000 Income tax expense ($360,000 X 30%) .............. 0 ,108,000 Income from continuing operations.................. 252,000 Discontinued operations

Loss from operations of ceramics division, net of $45,000 income tax saving .......... $105,000 Gain on sale of ceramics division, net of $18,000 income tax expense ....... 0042,000 00, 063,000

Income before extraordinary item ..................... 189,000 Extraordinary loss from truck accident, net of $27,000 income tax saving .......... 63,000 Net income........................................................... $ 126,000

Note that the effect of the change in accounting principle (amortization method) on prior years’ income would be shown on the statement of retained earnings, not the income statement.

15-38

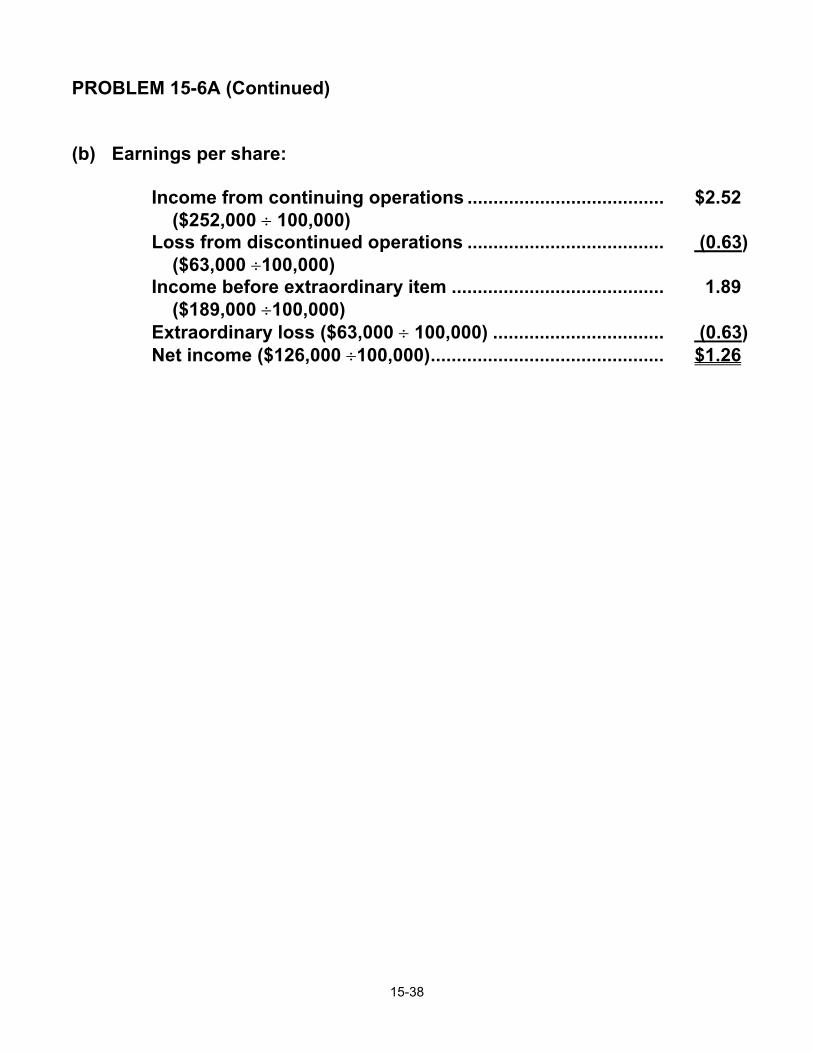

PROBLEM 15-6A (Continued) (b) Earnings per share:

Income from continuing operations ...................................... $2.52 ($252,000 ÷ 100,000) Loss from discontinued operations ...................................... (0.63) ($63,000 ÷100,000) Income before extraordinary item ......................................... 1.89 ($189,000 ÷100,000) Extraordinary loss ($63,000 ÷ 100,000) ................................. (0.63) Net income ($126,000 ÷100,000)............................................. $1.26

15-39

PROBLEM 15-7A

(a) BLUE BAY LIMITED

Income Statement For the Year Ended December 31, 2003

Sales.................................................................................... $9,214,000

Cost of goods sold............................................................. ,7,220,000 Gross profit ........................................................................ 1,994,000 Operating expenses........................................................... 1,219,000 Amortization expense........................................................ 363,000 Income before income tax................................................. 412,000 Income tax expense........................................................... 0, 115,000 Income from continuing operations................................. 297,000 Discontinued operations

Loss from discontinued operations net of $63,000 income tax saving ......................... 182,000

Income before extraordinary item .................................... 115,000 Extraordinary gain, net of $25,000 income tax expense................................................................. 77,000 Net income.......................................................................... $ 192,000

(b) BLUE BAY LIMITED

Statement of Retained Earnings For the Year Ended December 31, 2003

Balance, January 1, as previously reported .................... $ 979,000 Less: Effect on prior years' net income of

change in accounting policy, net of $40,000 income tax saving ................................ 126,000

Balance, January 1, as adjusted....................................... 853,000 Add: Net income.............................................................. 0 ,192,000 1,045,000 Less: Cash dividends....................................................... (30,000)

Balance, December 31....................................................... $1,015,000

15-40

PROBLEM 15-8A

2000 1999 Earnings per share $3.85 $2.98 Price-earnings ratio 11.5X 12.8X Payout ratio 17.6% 19.6% Dividend yield 1.6% 1.5% Calculations ($ in millions): Earnings per share 2000: ($772 - $11) ÷ 197.9 = $3.85 1999: ($602 - $9) ÷ 199.3 = $2.98 Price-earnings 2000: $44.35 ÷ $3.85 = 11.5 times 1999: $38.20 ÷ $2.98 = 12.8 times Payout 2000: $136 ÷ $772 = 17.6% 1999: $118 ÷ $602 = 19.6% Dividend yield 2000: $136 ÷ 197.9 = $0.69 ÷ $44.35 = 1.6% 1999: $118 ÷ 199.3 = $0.59 ÷ $38.20 = 1.5%

15-41

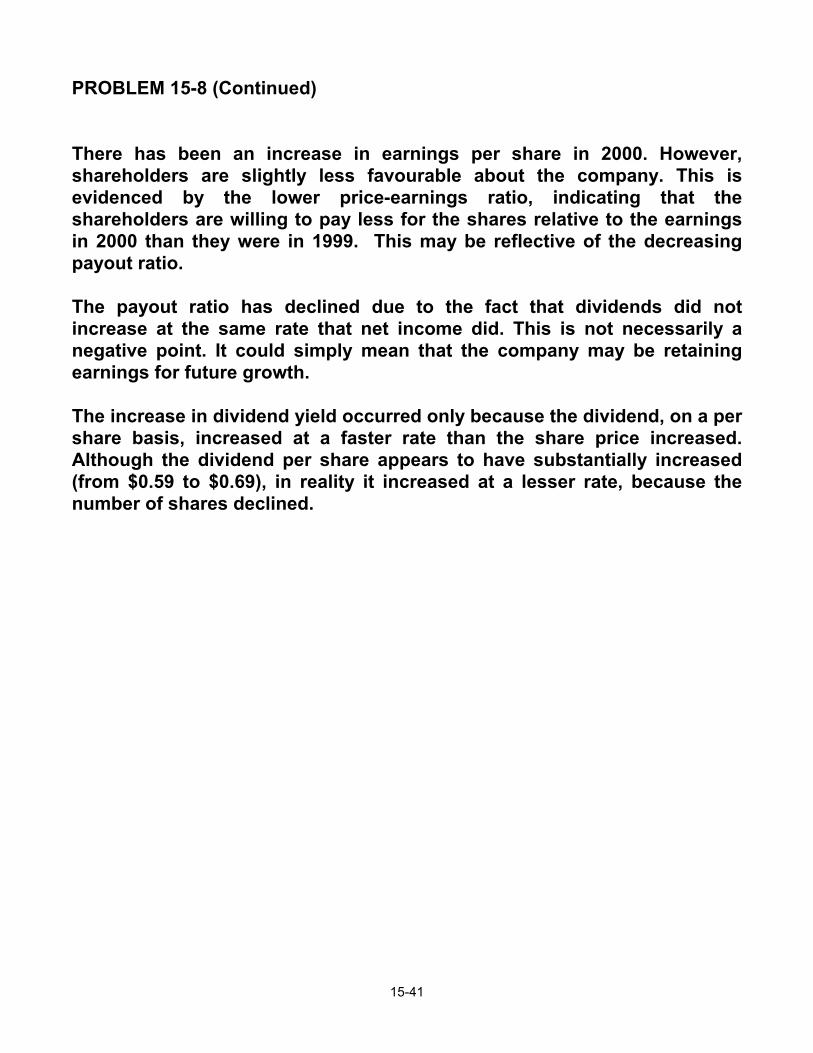

PROBLEM 15-8 (Continued) There has been an increase in earnings per share in 2000. However, shareholders are slightly less favourable about the company. This is evidenced by the lower price-earnings ratio, indicating that the shareholders are willing to pay less for the shares relative to the earnings in 2000 than they were in 1999. This may be reflective of the decreasing payout ratio. The payout ratio has declined due to the fact that dividends did not increase at the same rate that net income did. This is not necessarily a negative point. It could simply mean that the company may be retaining earnings for future growth. The increase in dividend yield occurred only because the dividend, on a per share basis, increased at a faster rate than the share price increased. Although the dividend per share appears to have substantially increased (from $0.59 to $0.69), in reality it increased at a lesser rate, because the number of shares declined.

15-42

PROBLEM 15-1B

(a)

Date

Share Price

Retained Earnings

Total Shares

Issued

Mark's Shares

Value of Mark's Shares

July 1 $25.00 $120,000 100,000 18,000 $450,000

Aug. 1

$26.50 $120,000 100,000 18,000 $477,000

Aug. 31 $28.00 $120,000 - $112,000 = $ 8,000

100,000 X 1.04 = 104,000

18,000 X 1.04 = 18,720

$524,160

Nov. 1

$32.00 $8,000 104,000 18,720 $599,040

Dec. 1 $30.00 $8,000 104,000 + 20,000 = 124,000

18,720 + 3,600 = 22,320

$669,600

Mar. 31 pre-split

$26.00 $8,000 124,000 22,320 $580,320

Mar. 31 post-split

$13.00 $8,000 248,000 44,640 $580,320

June 30 $10.50 ($34,000) 248,000 44,640 $468,720 (b) During the year, the company’s retained earnings dropped by

$154,000 from $120,000 to a deficit of $34,000. During the same period of time, the value of Mark’s shareholdings grew from $450,000 to $468,720, an $18,720 increase. The number of shares owned by Mark increased due to the additional purchase of shares and the stock split. However, the value of his portfolio has not increased proportionally because of the decrease in share price from a high of $32 in November to a low of $10.50 at the end of the year.

15-43

PROBLEM 15-2B

(a) Sept. 020 Cash Dividends–Common...................... 100,000

(50,000 X $2.00) Dividends Payable–Common ......... 100,000

Stock Dividends–Common (10,000 X $8) 80,000 Common Stock Dividends Distributable 80,000 (b)

CASH AND KIND CORPORATION Partial Balance Sheet

October 15, 2003

Shareholders' equity

Share capital Common shares, no par value, 60,000 shares issued .............................................. $545,000

Retained earnings .............................................................. 0,65,000 Total shareholders' equity .......................................... $610,000

15-44

PROBLEM 15-3B

(a)

GENERAL JOURNAL J1

Date Account Titles and Explanation

Debit

Credit

July 07 Cash Dividends—Common .................... 125,000

(250,000 X $0.50) Dividends Payable—Common........ 125,000

Aug. 01 Accumulated Amortization .................... 45,000 Income Tax Payable ........................ 15,000

Retained Earnings........................... 30,000

Sept. 01 Dividends Payable—Common ............... 125,000 Cash ................................................. 125,000

Dec. 01 Stock Dividends—Common (25,000 X $18) ....................................... 450,000

Common Stock Dividends Distributable 450,000

15 Cash Dividends— Preferred (12,000 X $4.50) ................... 54,000

Dividends Payable—Preferred ....... 54,000 31 Revenues ................................................. 900,000

Retained Earnings........................... 900,000 31 Retained Earnings................................... 515,000

Expenses ......................................... 515,000

31 Retained Earnings .................................. 629,000 Cash Dividends—Common ............ 125,000 Cash Dividends—Preferred............ 54,000 Stock Dividends—Common ........... 450,000

15-45

PROBLEM 15-3B (Continued) (b) Preferred Shares Date

Explanation

Ref.

Debit

Credit

Balance

Jan. 1

Balance

800,000 Common Shares Date

Explanation

Ref.

Debit

Credit

Balance

Jan. 1

Balance

500,000 Common Stock Dividends Distributable Date

Explanation

Ref.

Debit

Credit

Balance

Dec. 1

J1

0450,000

0450,000

Cash Dividends – Common Date

Explanation

Ref.

Debit

Credit

Balance

July 7 Dec. 31

Closing entry

J1 J1

125,000

125,000

125,000

0 Stock Dividends – Common Date

Explanation

Ref.

Debit

Credit

Balance

Dec. 1 31

Closing entry

J1 J1

450,000

450,000

450,000

0

15-46

PROBLEM 15-3B (Continued) (b) (Continued) Cash Dividends–Preferred Date

Explanation

Ref.

Debit

Credit

Balance

Dec. 15 31

Closing entry

J1 J1

54,000

54,000

54,000

0

Retained Earnings Date

Explanation

Ref.

Debit

Credit

Balance

Jan. 1 Aug. 1 Dec. 31 31 31

Balance Closing entry Closing entry Closing entry

J1 J1 J1 J1

515,000 629,000

030,000 900,000

900,000 930,000

1,830,000 1,315,000

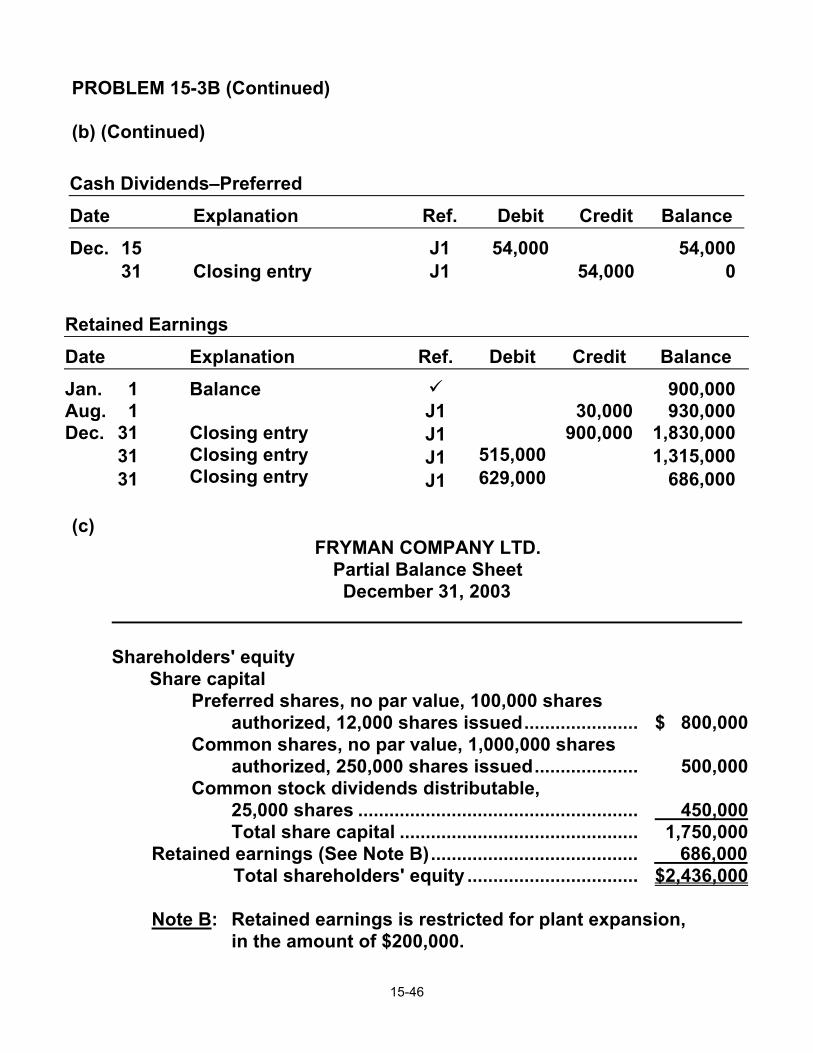

686,000 (c)

FRYMAN COMPANY LTD. Partial Balance Sheet

December 31, 2003

Shareholders' equity

Share capital Preferred shares, no par value, 100,000 shares authorized, 12,000 shares issued...................... $ 800,000 Common shares, no par value, 1,000,000 shares authorized, 250,000 shares issued.................... 500,000

Common stock dividends distributable, 25,000 shares ...................................................... 450,000

Total share capital .............................................. 1,750,000 Retained earnings (See Note B)........................................ 0 ,686,000

Total shareholders' equity ................................. $2,436,000

Note B: Retained earnings is restricted for plant expansion, in the amount of $200,000.

15-47

PROBLEM 15-4B

(a)

GENERAL JOURNAL

J1

Date Account Titles and Explanation

Debit

Credit

Feb. 1 Cash Dividends—Common (65,000 X $1) ......................................... 65,000

Dividends Payable—Common........ 65,000

March 1 Dividends Payable—Common ............... 65,000 Cash ................................................. 65,000

April 1 No entry required—Memo only to increase the number of common shares to 260,000 (65,000 X 4)

July 01 Stock Dividends—Common (13,000 X $13) ........................................ 169,000

Common Stock Dividends Distributable ................................. 169,000

July 31 Stock Dividends Distributable ............... 169,000 Common Shares.............................. 169,000

Dec. 1 Cash Dividends—Common [(260,000 + 13,000) X $0.50] ................ 136,500 Dividends Payable—Common........ 136,500

31 Revenues ................................................. 900,000

Retained Earnings........................... 900,000 31 Retained Earnings................................... 550,000

Expenses ......................................... 550,000 31 Retained Earnings .................................. 370,500

Cash Dividends—Common ............ 201,500 Stock Dividends—Common ........... 169,000

15-48

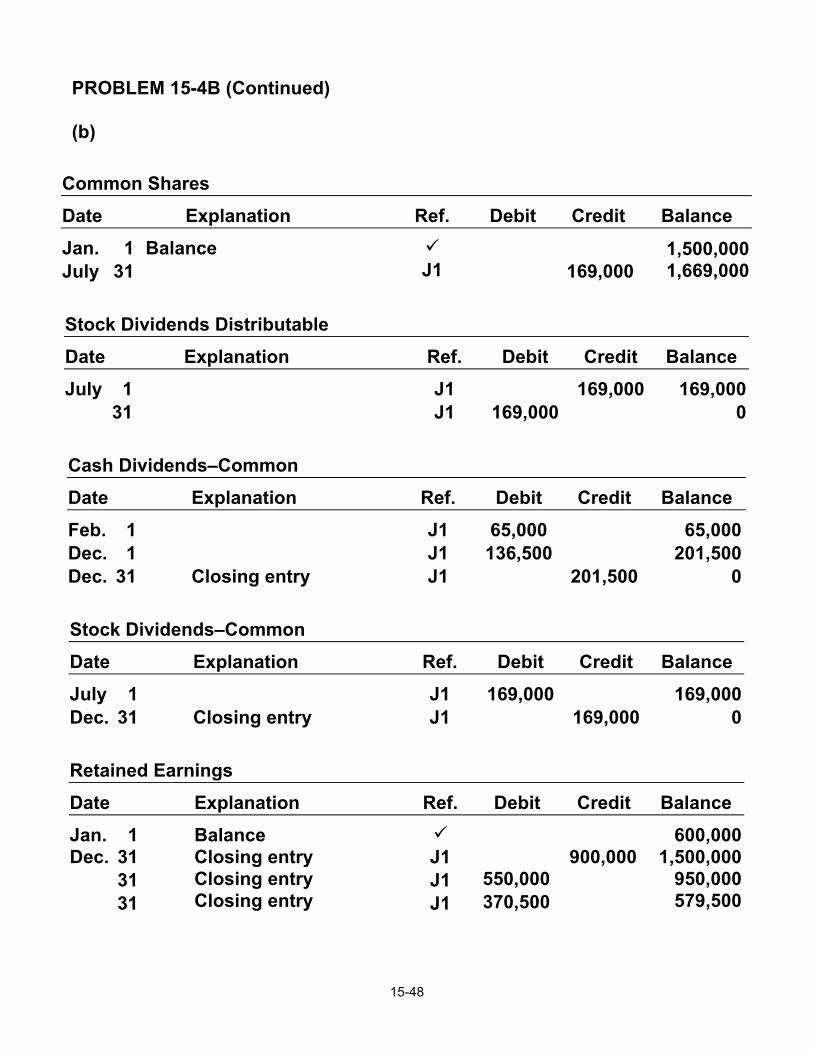

PROBLEM 15-4B (Continued) (b)

Common Shares Date

Explanation

Ref.

Debit

Credit

Balance

Jan. 1 July 31

Balance

J1

169,000

1,500,000 1,669,000

Stock Dividends Distributable Date

Explanation

Ref.

Debit

Credit

Balance

July 1 31

J1 J1

169,000

169,000

169,000

0 Cash Dividends–Common Date

Explanation

Ref.

Debit

Credit

Balance

Feb. 1 Dec. 1 Dec. 31

Closing entry

J1 J1 J1

65,000

136,500

201,500

65,000

201,500 0

Stock Dividends–Common Date

Explanation

Ref.

Debit

Credit

Balance

July 1 Dec. 31

Closing entry

J1 J1

169,000

169,000

169,000

0 Retained Earnings Date

Explanation

Ref.

Debit

Credit

Balance

Jan. 1 Dec. 31 31 31

Balance Closing entry Closing entry Closing entry

J1 J1 J1

0 550,000 370,500

900,000

600,000

1,500,000 950,000 579,500

15-49

PROBLEM 15-4B (Continued) (c)

ASAAD CORPORATION Partial Balance Sheet

December 31, 2003

Shareholders' equity

Share capital Common shares, no par value, unlimited number of shares authorized, 273,000 shares issued................................................... $1,669,000

Retained earnings ......................................................... 00,579,500 Total shareholders' equity .................................... $2,248,500

15-50

PROBLEM 15-5B

(a) Total cash dividend $250,000

Allocated to preferred shares: 2002 dividend in arrears (15,000 X $5) $75,000 2003 dividend 75,000 0150,000

Remainder to common shares $100,000 (b)

MICHAUD CORPORATION Statement of Retained Earnings For the Year Ended December 31, 2003

Balance, January 1, as previously reported ......................... $1,170,000

Less: Correction of overstatement of 2002 net income due to amortization error, net of $18,000 income tax saving........................... 42,000

Balance, January 1, as adjusted............................................ 1,128,000 Add: Net income................................................................... 00,495,000

1,623,000 Less: Cash dividends—preferred .................... $150,000 Cash dividends—common ..................... 100,000

Stock dividends....................................... 0320,000 0 ,570,000 Balance, December 31............................................................ $1,053,000

15-51

PROBLEM 15-5B (Continued) (c)

MICHAUD CORPORATION Partial Balance Sheet

December 31, 2003

Shareholders' equity

Share capital Preferred shares, no par value, unlimited number of shares authorized, 15,000 shares issued........................................... $1,000,000 Common shares, no par value, 500,000 shares

authorized, 250,000 shares issued ................... 2,900,000 Common stock dividends distributable,

20,000 shares...................................................... 320,000 Total share capital.................................... 4,220,000

Retained earnings (See Note X) .................................. 1,053,000

Total shareholders' equity ......................... $5,273,000

Note X: Retained earnings is restricted for plant expansion, in the amount of $200,000.

(d)

$495,000 $75,000 * $1.68250,000

−=

* 15,000 X $5 = $75,000

(e)

$16.00 (from item 7) 9.5 times$1.68 from part (d)

=

15-52

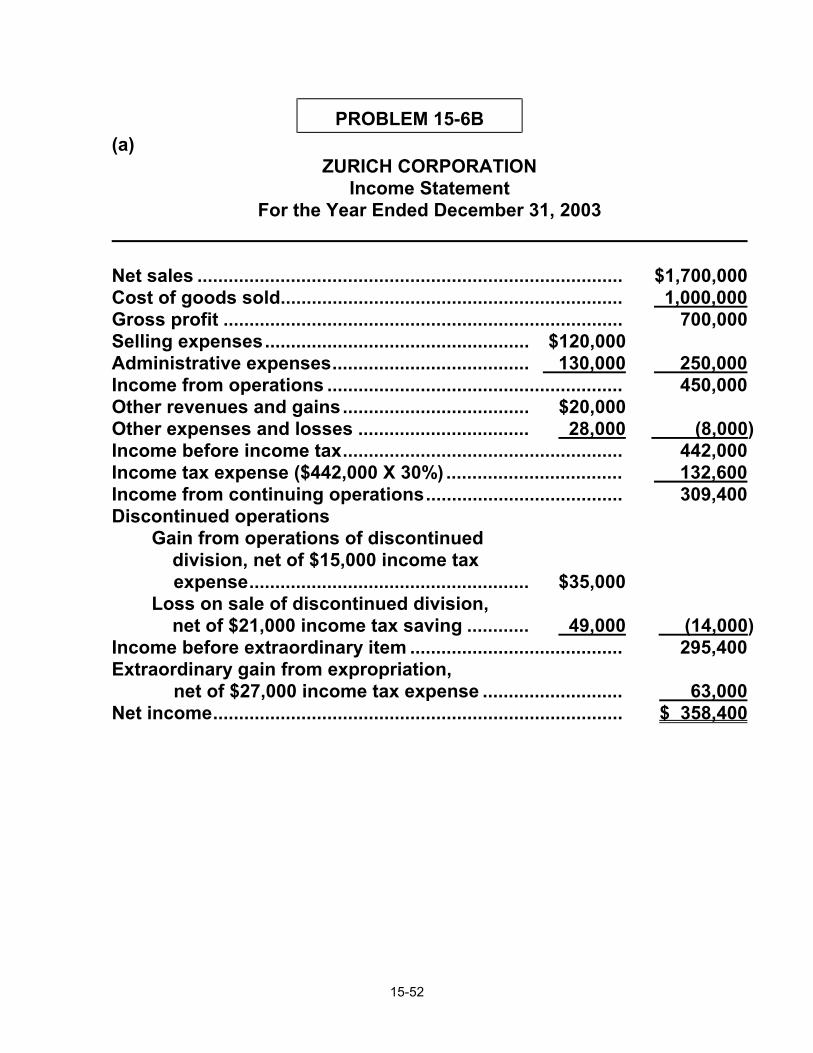

PROBLEM 15-6B

(a) ZURICH CORPORATION Income Statement For the Year Ended December 31, 2003

Net sales .................................................................................. $1,700,000

Cost of goods sold.................................................................. 01,000,000 Gross profit ............................................................................. 700,000 Selling expenses................................................... $120,000 Administrative expenses...................................... 0,130,000 250,000 Income from operations ......................................................... 450,000 Other revenues and gains.................................... $20,000 Other expenses and losses ................................. 028,000 0 0 (((8,000) Income before income tax...................................................... 442,000 Income tax expense ($442,000 X 30%) .................................. 0 ,132,600 Income from continuing operations...................................... 309,400 Discontinued operations

Gain from operations of discontinued division, net of $15,000 income tax expense...................................................... $35,000 Loss on sale of discontinued division, net of $21,000 income tax saving ............ 049,000 00 (14,000)

Income before extraordinary item ......................................... 295,400 Extraordinary gain from expropriation, net of $27,000 income tax expense ........................... 63,000 Net income............................................................................... $ 358,400

15-53

PROBLEM 15-6B (Continued) (a) (Continued) Earnings per share:

Income from continuing operations ($309,400 ÷ 100,000)........................................................... $3.09 Loss from discontinued operations ($14,000 ÷100,000).............................................................. (0.14) Income before extraordinary item ($295,400 ÷100,000)............................................................ 2.95 Extraordinary gain ($63,000 ÷ 100,000) ................................. 0.63 Net income ($358,400 ÷ 100,000)............................................ $3.58

(b) ZURICH CORPORATION

Statement of Retained Earnings For the Year Ended December 31, 2003

Balance, January 1, as previously reported ............................. $340,000 Add: Effect on prior years' net income of

change to straight-line amortization, net of $18,000 income tax expense ............................... 00,0 42,000

Balance, January 1, as adjusted................................................ 382,000 Add: Net income ........................................................................ 0, 358,400 740,400 Less: Cash dividends ................................................................. 0025,000

Balance, December 31................................................................ $715,400

15-54

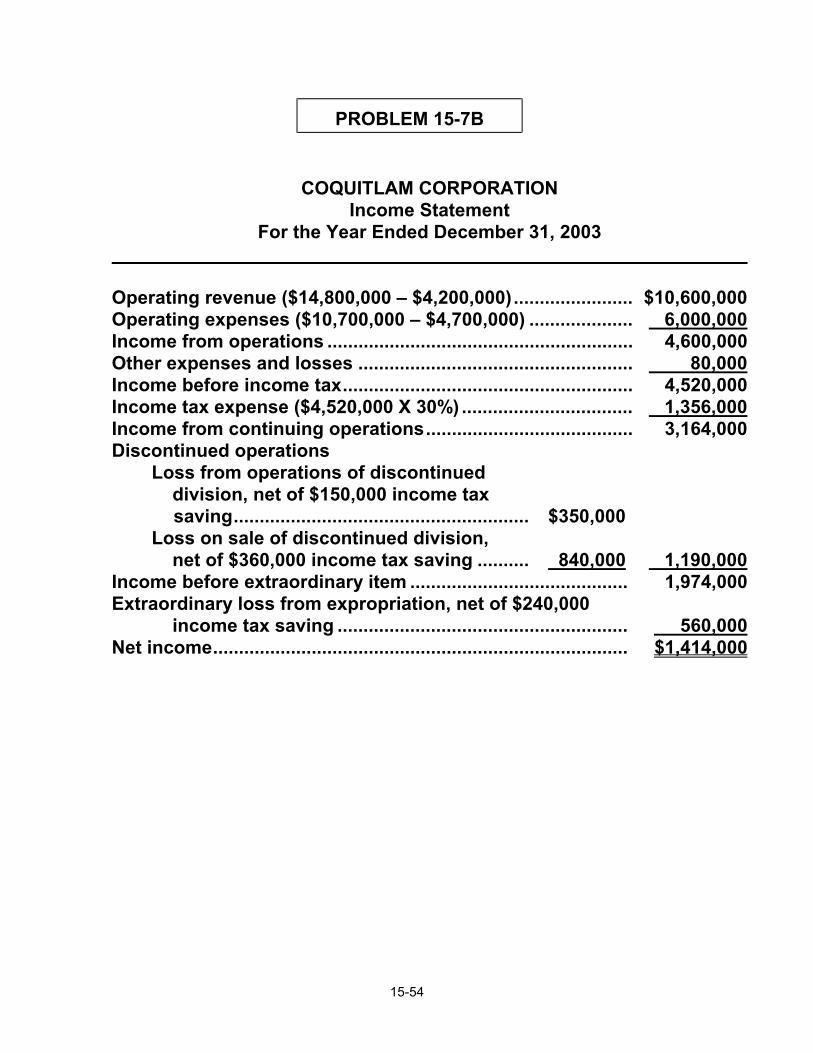

PROBLEM 15-7B

COQUITLAM CORPORATION Income Statement For the Year Ended December 31, 2003

Operating revenue ($14,800,000 – $4,200,000)....................... $10,600,000

Operating expenses ($10,700,000 – $4,700,000) .................... 6,000,000 Income from operations ........................................................... 4,600,000 Other expenses and losses ..................................................... 0 0080,000 Income before income tax........................................................ 4,520,000 Income tax expense ($4,520,000 X 30%) ................................. 0,1,356,000 Income from continuing operations........................................ 3,164,000 Discontinued operations

Loss from operations of discontinued division, net of $150,000 income tax saving......................................................... $350,000 Loss on sale of discontinued division, net of $360,000 income tax saving .......... 0840,000 0 1,190,000

Income before extraordinary item .......................................... 1,974,000 Extraordinary loss from expropriation, net of $240,000

income tax saving ........................................................ 560,000 Net income................................................................................ $1,414,000

15-55

PROBLEM 15-7B (Continued) Earnings per share:

Income from continuing operations ...................................... $7.91 ($3,164,000 ÷ 400,000) Loss from discontinued operations ...................................... (2.98) ($1,190,000 ÷ 400,000) Income before extraordinary item ......................................... 4.93 ($1,974,000 ÷ 400,000) Extraordinary loss ($560,000 ÷ 400,000) ............................... (1.40) Net income ($1,414,000 ÷ 400,000)......................................... $3.53

15-56

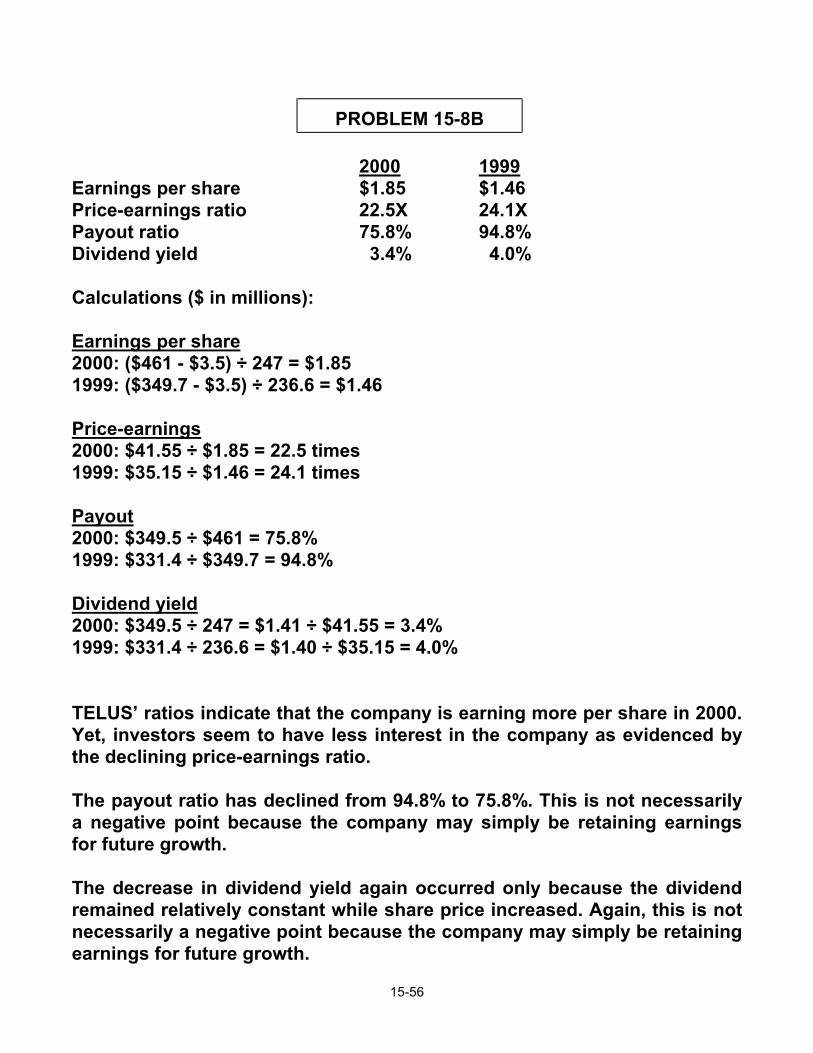

PROBLEM 15-8B

2000 1999 Earnings per share $1.85 $1.46 Price-earnings ratio 22.5X 24.1X Payout ratio 75.8% 94.8% Dividend yield 3.4% 4.0% Calculations ($ in millions): Earnings per share 2000: ($461 - $3.5) ÷ 247 = $1.85 1999: ($349.7 - $3.5) ÷ 236.6 = $1.46 Price-earnings 2000: $41.55 ÷ $1.85 = 22.5 times 1999: $35.15 ÷ $1.46 = 24.1 times Payout 2000: $349.5 ÷ $461 = 75.8% 1999: $331.4 ÷ $349.7 = 94.8% Dividend yield 2000: $349.5 ÷ 247 = $1.41 ÷ $41.55 = 3.4% 1999: $331.4 ÷ 236.6 = $1.40 ÷ $35.15 = 4.0% TELUS’ ratios indicate that the company is earning more per share in 2000. Yet, investors seem to have less interest in the company as evidenced by the declining price-earnings ratio. The payout ratio has declined from 94.8% to 75.8%. This is not necessarily a negative point because the company may simply be retaining earnings for future growth. The decrease in dividend yield again occurred only because the dividend remained relatively constant while share price increased. Again, this is not necessarily a negative point because the company may simply be retaining earnings for future growth.

15-57

BYP 15-1 FINANCIAL REPORTING PROBLEM

(a) Per Note 8 to the financial statements there were 49,170 shares issued

for cash to employees and directors for the year ended June 24, 2000. (b) As at June 24, 2000, 9.1% ($1,698,000 ÷ $18,565,000) of the company

assets were financed by shareholders’ equity. (c) Per the consolidated statement of operations and deficit, there were no

discontinued operations or extraordinary items in the years 2000 or 1999.

(d) 2000: Earnings per share = $0.10

1999: Loss per share = ($0.72)

Per the Consolidated Statements of Operations and Deficit. (e) There was a special dividend of $18,719,000, declared on April 26,

2000. The dividend was paid on May 31, 2000. See details in Note 8 to the financial statements.

15-58

BYP 15-2 INTERPRETING FINANCIAL STATEMENTS

(a) Both the stock dividend and the stock split will increase the number of

shares, without changing the overall value of the company. A stock dividend will increase the share capital and decrease retained earnings by the same amount. A stock split will simply increase the number of shares issued.

(b) Nortel probably split its shares to reduce its share price thereby

making its shares more affordable to the average investor. This should increase the marketability of the shares.

(c) Investors purchase shares based on how they expect the company to

perform in the future. Obviously investors felt that Nortel had strong earnings potential and were willing to buy the shares based on this expectation.

15-59

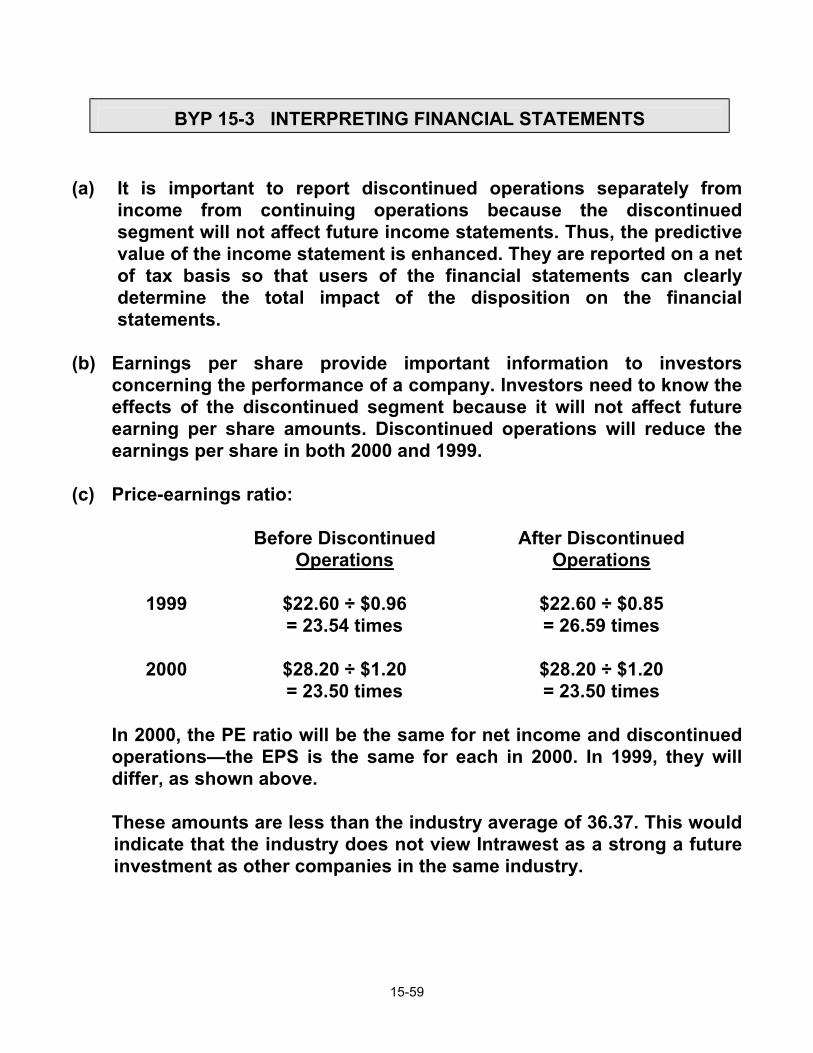

BYP 15-3 INTERPRETING FINANCIAL STATEMENTS

(a) It is important to report discontinued operations separately from

income from continuing operations because the discontinued segment will not affect future income statements. Thus, the predictive value of the income statement is enhanced. They are reported on a net of tax basis so that users of the financial statements can clearly determine the total impact of the disposition on the financial statements.

(b) Earnings per share provide important information to investors

concerning the performance of a company. Investors need to know the effects of the discontinued segment because it will not affect future earning per share amounts. Discontinued operations will reduce the earnings per share in both 2000 and 1999.

(c) Price-earnings ratio:

Before Discontinued Operations

After Discontinued Operations

1999

$22.60 ÷ $0.96 = 23.54 times

$22.60 ÷ $0.85 = 26.59 times

2000

$28.20 ÷ $1.20 = 23.50 times

$28.20 ÷ $1.20 = 23.50 times

In 2000, the PE ratio will be the same for net income and discontinued

operations—the EPS is the same for each in 2000. In 1999, they will differ, as shown above.

These amounts are less than the industry average of 36.37. This would

indicate that the industry does not view Intrawest as a strong a future investment as other companies in the same industry.

15-60

BYP 15-3 (Continued) (d) Adjustments for changes in accounting principles are reflected in the

statement of retained earnings rather than the income statement because they reflect changes to prior years’ income that has been closed into the retained earnings. As well, because the changes are retroactive, presenting such information in the income statement would be inappropriate as the income statement presents the results of the current years operations only. If the 1999 data is presented the financial statements will be restated to reflect the retroactive change.

15-61

BYP 15-4 ACCOUNTING ON THE WEB

Due to the frequency of change with regard to information available on the world wide web, the Accounting on the Web cases are updated as required. Their suggested solutions are also updated whenever necessary, and can be found on-line in the Instructor Resources section of our home page [www.wiley.com/canada/weygandt2].

15-62

BYP 15-5 COLLABORATIVE LEARNING ACTIVITY

(a) Total operating income refers to the income from the company’s

continuing regular business operations, before any “other revenues and gains” or “other expenses and losses”. Once these are included, and income tax expense is deducted, you arrive at income from continuing operations (or income before discontinued operations and extraordinary items).

(b)

Earnings per Share

Current Year

Prior Year

Continuing operations* Discontinued operations Extraordinary items Net income**

$7.99 (0.67) 0 0 $7.32

$3.12 (0.19) 1.09 $4.02

* Calculation is income from continuing operations less preferred

dividends divided by the number of common shares issued. ** Calculation is net income (income from continuing operations, less

loss from discontinued operations, plus extraordinary gain) less preferred dividends, divided by the number of common shares issued.

(c) The effects of material non-typical items were very significant in the prior year but much less significant in the current year. In the prior year, these items had a positive effect of $21.4 ($25.8 – $4.4), which was 26% of income from continuing operations ($21.4 ÷ $83.6) and 20% of net income ($21.4 ÷ $105.0). In the current year, these items had a negative effect of $16.9, which was 8% of income from continuing operations ($16.9 ÷ $209.9) and 9% of net income ($16.9 ÷ $193.0).

15-63

BYP 15-5 (Continued) (d)

THE TRACK CORPORATION Statement of Retained Earnings For the Current Year (In millions of dollars)

Balance, January 1, as previously reported ............................... $405.3

Add: Cumulative effect on prior years’ income of change in method of accounting for tax ......................... 0 2.7

Balance, January 1, as adjusted.................................................. 408.0 Add: Net income ......................................................................... 193.0

601.0 Less: Dividends—Preferred.......................................... $08.8

Dividends—Common.......................................... 043.3 0 52.1 Balance, December 31.................................................................. $548.9

15-64

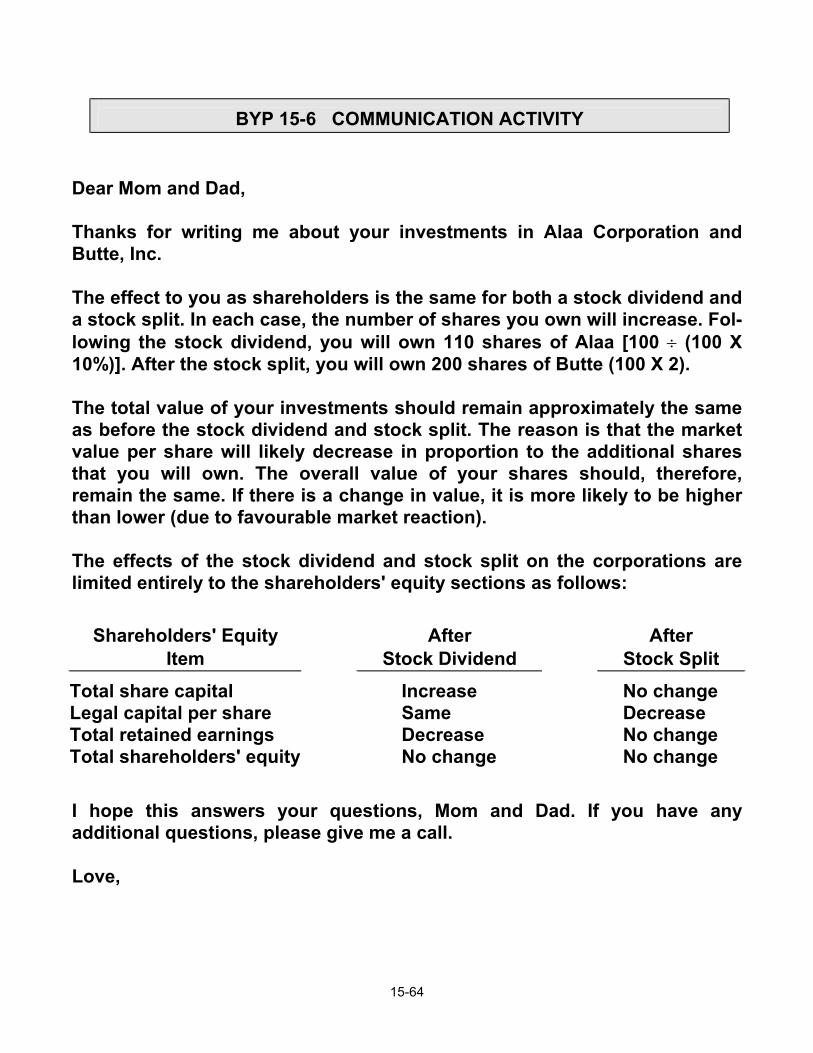

BYP 15-6 COMMUNICATION ACTIVITY

Dear Mom and Dad, Thanks for writing me about your investments in Alaa Corporation and Butte, Inc. The effect to you as shareholders is the same for both a stock dividend and a stock split. In each case, the number of shares you own will increase. Fol-lowing the stock dividend, you will own 110 shares of Alaa [100 ÷ (100 X 10%)]. After the stock split, you will own 200 shares of Butte (100 X 2). The total value of your investments should remain approximately the same as before the stock dividend and stock split. The reason is that the market value per share will likely decrease in proportion to the additional shares that you will own. The overall value of your shares should, therefore, remain the same. If there is a change in value, it is more likely to be higher than lower (due to favourable market reaction). The effects of the stock dividend and stock split on the corporations are limited entirely to the shareholders' equity sections as follows:

Shareholders' Equity Item

After

Stock Dividend

After

Stock Split Total share capital Legal capital per share Total retained earnings Total shareholders' equity

Increase Same Decrease No change

No change Decrease No change No change

I hope this answers your questions, Mom and Dad. If you have any additional questions, please give me a call. Love,

15-65

BYP 15-7 ETHICS CASE

(a) The stakeholders in this situation are:

Vince Ramsey, president of Flambeau Corporation Janice Rahn, financial vice-president The shareholders of Flambeau Corporation

(b) There is nothing unethical in issuing a stock dividend. But the presi-

dent's order to write a press release convincing the shareholders that the stock dividend is just as good as a cash dividend is unethical. A stock dividend is not a cash dividend and does not necessarily place the shareholder in the same position. A stock dividend is not paid in cash, it is “paid” in shares. This does provide a future potential opportunity to receive cash if the additional shares can be profitably sold.

(c) As a shareholder, preference for a cash dividend versus stock

dividend is dependent upon one's investment objective—income (cash flow) or growth (reinvestment). By not paying out the cash, the stock dividend leaves it in the company, where it is reinvested and contributes to the growth of the company and an increase in the value of its shares. Some shareholders prefer stock dividends for income tax reasons—deferring the payment of the tax on the dividend. As well, more shares provide an opportunity for future profitable resale of these shares, especially if the share price climbs.