chapter 16 commercial mortgage types and decisions mcgraw-hill/irwincopyright © 2010 by the...

TRANSCRIPT

Chapter 16

Commercial Mortgage Types and Decisions

McGraw-Hill/Irwin Copyright © 2010 by The McGraw-Hill Companies, Inc. All rights reserved.

16-2

“Commercial” Loans vs Home Loans Commercial mortgages & notes not as

standardized as home loans Although this was changing with growth in commercial

mortgage-backed securities (CMBS) market Documents are longer & more complex Often no personal liability:

Legal borrower often is a single asset corporation Actual investors are shielded from liability Credit enhancement sometimes is required, especially

by commercial banks

16-3

Commercial Mortgage Loans

Usually a partially amortized “balloon” mortgage 25-30 year amortization of principle 5-10 year loan maturity Balance of loan at maturity must be refinanced or paid

off with a “balloon” payment

16-4

Attractions of Balloon Mortgage to Lender Reduces interest rate risk Reduces default risk

Default risk is generally much greater for commercial mortgage loans than home loans Seldom personal liability No FHA/PMI insurance Borrowers are more “ruthless” about exercising their

default options

16-5

Commercial Mortgage “Spreads” over Treasuries

Mortgage rates highly correlated with 10-Year Treasury Securities

16-6

Restrictions on Prepayment

Lock-out: Prohibition against prepayment for up to 5 years

Prepayment penalties: Percentage of loan: Say, 2-4% of loan balance Yield maintenance penalty: Borrower must pay

lender PV of losses due to prepayment Defeasance penalty: Borrower must replace

mortgage loan with a set of U.S. Treasury securities that produce cash flows equivalent to those on the paid-off mortgage Recently has become most common form of prepayment

penalty

16-7

Other Forms of Commercial Mortgage Financing

Floating (i.e., adjustable) rate mortgage Index rate most commonly is LIBOR

Installment sale financing Buyer makes installment payments to seller Seller only pays capital gain taxes over time in

proportion to the annual payments received

16-8

Other Forms of Commercial Mortgage Financing - continued

Joint Venture Lender likely:

provides a mortgage loan to project provides equity capital receives mortgage interest plus equity cash flows

Borrower likely: provides the project provides expertise & management effort

16-9

Joint Venture - continued

Often between a developer/organizor of a large project and a:

pension fund life Insurance company REIT

Institution provides construction financing and/or long-term mortgage, in addition to some of required equity capital

Institution’s share of operating & sale cash flows are negotiated

16-10

Other Forms of Commercial Mortgage Financing (continued) Sale-leaseback

Owner-user sells property to a long-term investor such as a pension fund limited liability company Tenancy in common

User leases property back from the investor(s) & occupies it under long-term net lease.

16-11

Sale-Leaseback - continued

User benefits: Lease payment is deductible for income taxes Equity capital is freed up to invest in core business of

company

Investor benefits: Can be relatively safe investment (depending on

credit worthiness of tenant). Inflation hedged (especially if lease payments

increase with inflation)

16-12

Other Forms of Commercial Mortgage Financing - continued FHA insured loans for low & moderate income

multifamily housing. Freddie Mac & Fannie Mae multifamily lending

programs Many targeted to low & moderate income housing See Fannie & Freddie websites (www.fanniemae.com

and www.freddiemac.com)

16-13

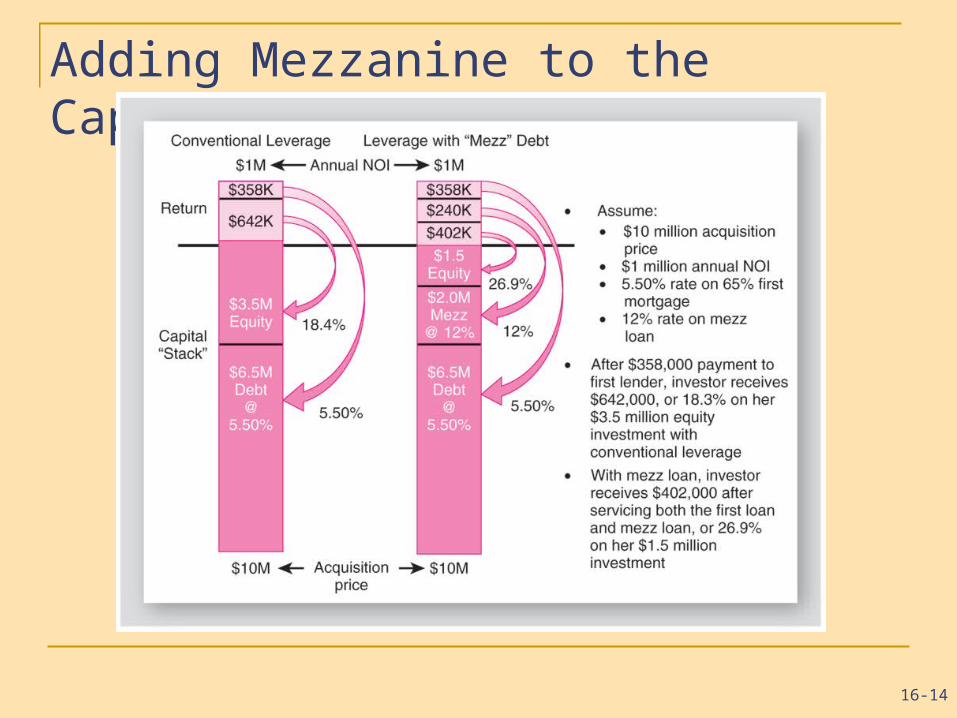

Other Forms of Commercial Mortgage Financing - continued

Mezzanine Debt: Supplements underlying first mortgage debt Sometimes is a second mortgage loan (i.e., secured by

the property) More often is a non-mortgage loan secured by a

pledge of borrower’s ownership interest If borrower defaults, mezz lender takes over borrower’s

ownership position…giving them more control

16-14

Adding Mezzanine to the Capital Stack

16-15

Average Terms on Commercial Mortgages–RealtyRates.com (Exhibit 16-4)

16-16

Important “Underwriting” Ratios

Debt coverage ratio: indicator of “cash flow cushion” from lender’s

perspective

DCR = NOI÷DS

where:NOI is first year NOI

DS is annual debt service (12 monthly payments)

Lender’s want DCR to be as high as possible, but usually > 1.20

16-17

Important “Underwriting” Ratios

Loan-to-value ratio: indicator of equity incentive to maintain the loan

LTV = Loan÷Value

The higher the initial LTV, the greater the probability of subsequent default, all else equal

16-18

The Leveraging Question (How Much Debt?) Reasons for use of debt by investors:

“Magnify” equity returns Diversify the use of one’s equity

Financial risk: Risk of default on mortgage loan. Risk of negative cash flow Increases with greater leverage.

Leverage also increases variability of equity returns (more on this in Chapter 19)

16-19

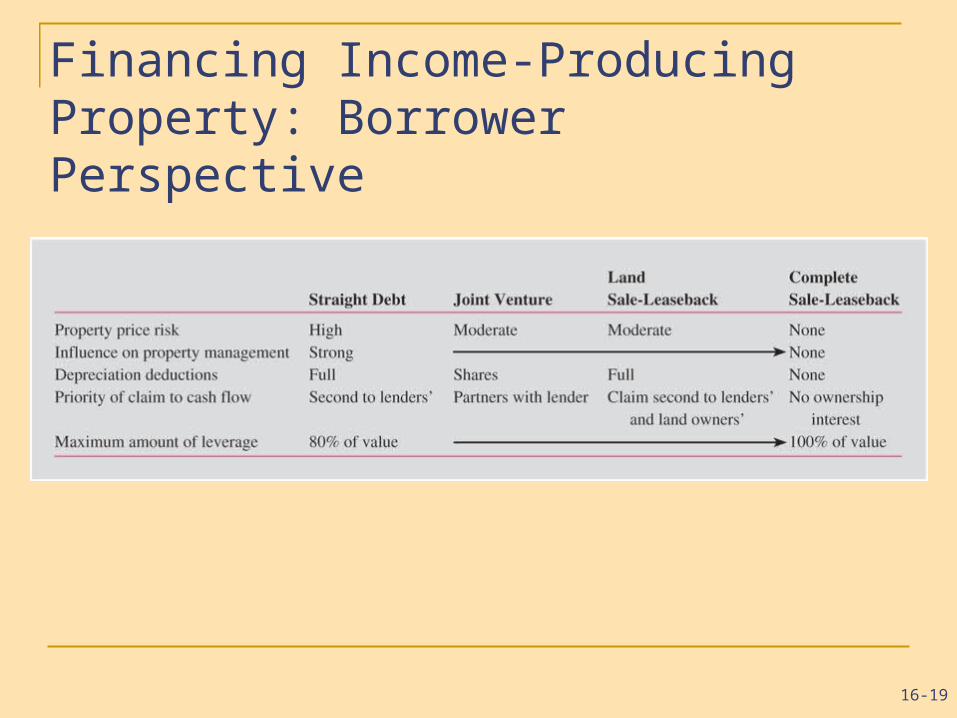

Financing Income-Producing Property: Borrower Perspective

16-20

Refinancing & Default with Commercial Mortgage Loans

Refinancing involves a NPV decision Even more focused on NPV than home mortgage

refinancing Bigger finance issues Fewer non-financial considerations

Often must account for a prepayment penalty NPV = PVOLD – PVNEW – Refi Cost – Prepay Penalty

16-21

Refinancing & Default with Commercial Mortgage Loans

Default is the signature risk of commercial mortgages. Borrower seldom can cover the loan payment for a

crippled commercial property. Borrower often is in a non-recourse position (god

for the borrower, bad for the lender).

16-22

Obtaining a Commercial Mortgage Loan The Loan Submission Package

Loan application from borrower contains Financial statements Credit reports Borrower’s experience resume

16-23

Obtaining a Commercial Mortgage Loan The Loan Submission Package, continued

Property description Legal description Detailed physical description

Photos including aerial shots Survey Site plan Structure drawings & specifications

Market analysis Cash flow pro forma (projections) Market value appraisal

16-24

The Lender’s Decision: Loan Underwriting “Qualitative” considerations

Property type Location Tenant quality Lease terms Property management Building quality Environmental issues Borrower quality

16-25

Loan Underwriting: Crunching the Numbers

16-26

Gatorwood Before-Tax Cash Flow from Operations

16-27

Loan Underwriting: Crunching the Numbers Lender’s focus is usually on projected NOI over

next 12 months Debt coverage ratio:

DCR = NOI÷DS For Gatorwood:

DCR = $1,272,500÷$857,038 = 1.5 Maximum loan:

Maximum debt service = NOI÷ Required DCR For Gatorwood:

Maximum debt service = $1,272,500÷1.25 = $1,018,000

16-28

Loan Underwriting: Determining Maximum Loan Maximum Loan - continued

Assume the lender’s terms would be Term for amortization: 30 years Interest rate: 7.625

PVPV PmtPmtiinn FVFV

360 7.625 $1,018,000 0

$11,878,124.05

16-29

Loan Underwriting: Determining Maximum Loan Maximum loan continued (monthly pmt)

Monthly debt service:MDS = DS÷12 = $1,018,000÷12 = $84,333.33

Assume the lender’s terms would be Term for amortization: 30 years Interest rate: 7.625

PVPV PmtPmtiinn FVFV

360 7.625/12 $84,333.33 0

$11,985,600.86

16-30

Loan Underwriting: Break-Even Ratio Break-even Ratio

BER = (OE + CAPX + DS)÷PGI Indicates required occupancy level (approx.) Gatorwood example:

BER = (400,000 + 37,500 + 857,038)

÷ 1,900,000

= 0.681 or 68%

16-31

Due-diligence: review & verification of the facts and analysis supplied by borrower in loan submission package Analyze rent roll & individual existing leases Analyze history of OE and CAPX Verify other facts (check for credibility and consistency) Check for missing or undisclosed information Verify borrower’s computations and analysis.

Loan Underwriting: Due-Diligence

16-32

45-90 days after receipt of “package” Lender often offers buyer/borrower a “rate lock”

option for a fee Protects borrowers from a rise in interest rates before

the loan is actually closed

Loan Commitment

16-33

Construction and Development Financing Land acquisition financing

Finance purchase of raw land, often on urban fringe

Land development loan Finance installation of improvements to the land

(sewers, utilities, etc.)

Construction loan Finance vertical construction

Mini-perm loan Provide financing for the development phase, plus a

short-term permanent loan upon completion of project

16-34

Construction and Development Financing Land acquisition financing

VERY risky; most traditional lenders will not touch

Land development loan If the land is ready for development, presumably

demand for the finished product is less uncertain

Construction loan Arguably, the collateral securing a construction loan is

more valuable than the collateral securing land acquisition & development loans

End of Chapter 16