chapter 1v housing finance schemes in india...

TRANSCRIPT

CHAPTER - 1V

HOUSING FINANCE SCHEMES IN INDIA - AN ANALYSIS

House is a basic necessity. Everyone, rich or poor, whether in rural

areas or urban areas, needs a house to protect his life and property and also to

promote his well-being. Houses do a great deal more than housing the people.

They channel human relationship and are an integral part of the society. A house

is not an isolated structure but forms part of the neighbourhood and the total

community.

Housing does not mean the construction of a shelter only, a shelter

to protect way from the inclemencies of weather. Housing in its wide sense a

comprehends a shelter designed to fit in with his social and cultural wants and

located in proper environment supported by physical and social infrastructure.

The physical characteristic of the present day houses in the country

also reflects various phases of the evolutionary process in the socio-cultural

growth of the country. There is a growing demand for recognition of housing as

basic human right. Providing adequate housing is the responsibility of the State.

In a large country like lndia, natural diversities, geographical and climatic

extremes and socio- economic disparities have enhanced the magnitude of the

problem of housing. The rural urban divide is a glaring example of the disparity.

Estimates show that lndia will have 41 million people without a proper roof over

their head by the year 2000 A.D. Of this, 32 million people would be in rural

areas. Although there has been a sharp increase in the construction of houses in

the past two decades, escalating land prices, paucity of land in urban centres

and high interest rate have dampened the pace in recent years.

HOUSING SHORTAGE IN INDIA

Housing shortage is the gap between total demand and total stock

of houses. A shortage arises due to many forces among which the most

important are the slze and growth in population, the marriage age and the

prosperity of the economy

The housing shortage is estimated to have increased from 9 million

dwelling units in 1951 to 21.1 million in 1981 to 39.1 million in the year 2001.

Table No. 4.1

Source: NBO and Seventh Five Year Plan.

As is seen in Table No. 4.1, housing shortage has grown faster in

rural areas as compared to the urban sector. Rural and urban housing conditions

in the country are unsatisfactory. The migration from rural areas, growth of cities

and towns, growth of population, limited land, steep rise in construction materials

have all contributed to the problem.

In spite of the tremendous boost provided to the housing sector in

recent times, the hous~ng shortage in the country continues to be alarming. State

Govt. has encouraged specific programmes and policies in the public and private

sectors in construction activities. The housing policy aims at all-round

development in housing and environmental situation and eradicating the

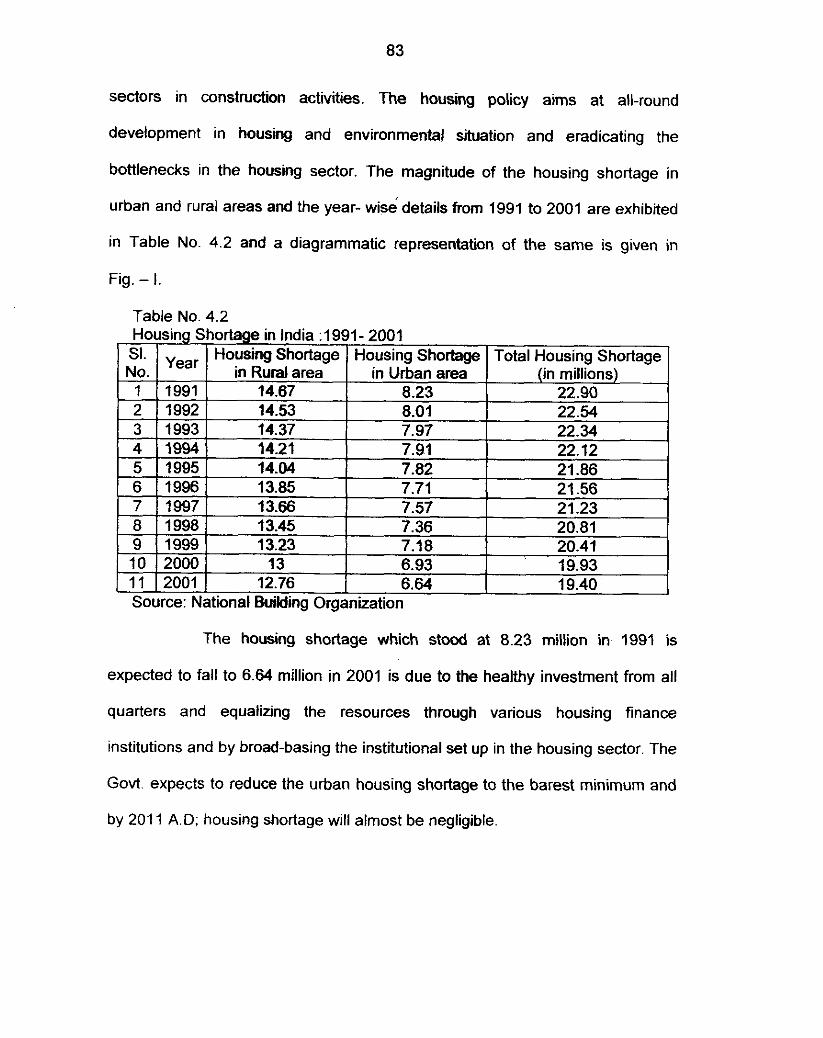

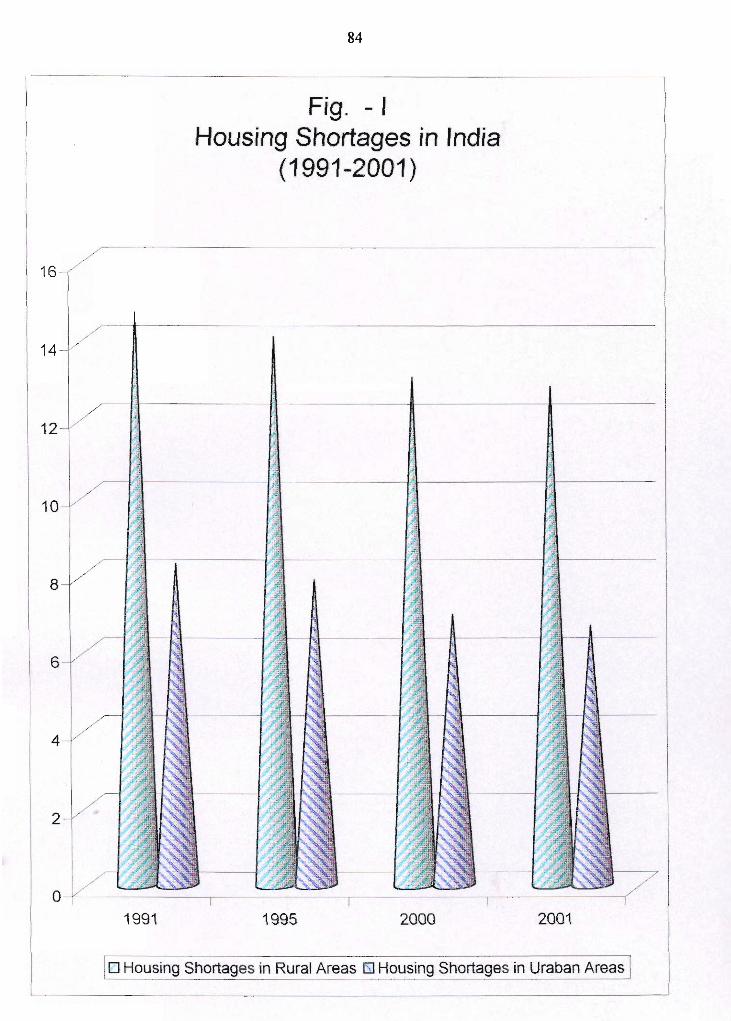

bottlenecks In the housing sector. The magnitude of the housing shortage in

urban and rural areas and the year- wise details from 1991 to 2001 are exhibited

in Table No. 4.2 and a diagrammatic representatiin of the same is given in

Fig. - 1.

Table No. 4.2

Source: National milding Organization

The housing shortage which stood at 8.23 million i n 1991 is

expected to fall to 6.64 million in 2001 is due to the healthy investment from all

quarters and equalizing the resources through various housing finance

institutions and by broad-basing the institutional set up in the housing sector. The

Govt. expects to reduce the urban housing shortage to the barest minimum and

by 201 1 A.D; housing shortage will almost be negligible.

Fig. - I Housing Shortages in India

(7991-2007)

HOUSING AND THE FIVE YEAR PLANS:

The Housing Programmes and Policies of the Govt. date back to

the First Five Year Plan when the emphasis was laid on encouraging the housing

to people from various sectors. Both the central and the state Governments have

been implementing a number of housing schemes right from the first five year

plan for eliminating the housing shortage in the country. It is therefore not

surprising that houslng is regarded as an important index of overall economic

activtty. It would appear that housing has not enjoyed a high priority under our

Plans.

Though emphasis was laid on housing during the Five Year Plans,

the investment in housing was not adequate enough to meet the ever increasing

demand, owing to further growth of population and the new household

formations. In the initial stages adequate priority was not accorded to the housing

sector thus resulting in low investment in this particular area.

The allocat~on made for housing in successive Five Year Plans

reveals that though there has been a cumulative increase as compared to the

total outlay, the percentage of provision made for housing has been declining.

Total Financial Outlay and Outlay for Housing in Five Year Plans are presented

In Table 4.3

Table No. 4.3 Total Financial Outlay and Outlay for Housing in Five Year Plans

, Fl, F~eFcenGg; 1 outlay

for Housin 1150 34

:

F;i ;year Total Outlay Plans (Rs. in crore)

1 First 3360 2 Second 6750 1300 19 3 Third 10400 1550 15 4 Fourth 22635 5 Fifth 47561

172210 7 Sek 8 Ei hth

Source: Ministry

80 3 1458 10 610000 77976

Jrban Affairs and Employment.

In the First Five Year Plan, provision made for housing was 34

percent of the total plan outlay. It was 19, 15 and 12 per cent respectively in the

Second, Third and Fourth Plan periods. It was 10 per cent in the Seventh Plan

period and it was kept to the extent of 12 per cent of the total outlay during the

Eighth Five Year Plan.

HOUSING FINANCE

Housing Finance is an important element of housing policies

persuaded by'the Governments of developed and developing countries of the

world. In India the flow of credit into the housing sector comes from two sources

that is formal and informal sectors. According to Dr. Rangarajan Committee

Report in the year 1987, the formal sector comprises of :

b Central and State Governments' budgetary allocation

'i General financial institution, namely LIC, GIC, and its subsidiaries,

scheduled commercial banks and Provident Funds

P Specialized housing finance instiiutiins like National Housing Bank (NHB)

the HUDCO.

Apex and Cooperative finance institutions are in the public sector

while HDFC and other housing finance companies are in the private sector. The

informal sector consists of the households themselves, public and private

employers extending house loans to their employees and project financing by

HUDCO and other agencies outside the budgetary processes.

In lndia 1941, we had 5.72 lakhs surpluses houses, but in 1951, we

had a shortage of 2.57 lakhs houses and the shortage is co:ntinuously increasing

with the growth in population. The Government has been able to solve the

problem of food, but not shelter. For 1988 itself we needed 250 lakhs houses in

India. which required a finance of Rs. 88,000 crore. This shortage is increasing

by 3.5 per cent per annum and by 2000 A.D. lndia will require 320 lakhs houses

more. The finance of which requires Rs. 1,80,000 crore. Table No. 4.4 shows the

housing requirements in the Ninth Plan.

Table No. 4.4

As per the Ninth Plan, a total sum of Rs.150.370 crore is need for

construction of 330.1 lakhs units leaving a margin of 98.370 crore to be mobilized

Housing Requirements during Ninth Plan

No.

1 2

Segment

Urban Rural

Total

Number of Units (in Lakhs)

167.6 162.5

Source: Industrial Economist, 30'~ 0ctober - 1 4 ' ~ o v e m ~ ~ e r 1998, p. 48

Fund's Requirement From Formal

121.370 29.000

330.1 150.370

by the expansion of formal sector and also encouraging informal sector flows.

Supply demand ratio for urban housing comes to 1:3.

In such circumstances, it is not possible for the Government alone

to tackle the problem. Hence it was decided to sponsor the private sector in

housing finance through the National Housing Bank, which is a subsidiary of RBI.

They will help all private wrporations to work as per their norms. They expect the

private sector not to depend on them totally but will sponsor wrporations, which

generate funds from the public itself by. way of deposits and from the loan

seekers by way of House Loan Account Scheme.

For housing finance no recognized instiiutions were existed till

1971. When Government of lndia constituted the Housing and Urban

Development Corporation (HUDCO), individual demands for housing loans were

fulfilled by the setting up of Housing Development Finance Corporation (HDFC)

in 1977. The establishment of National Housing Bank (NHB), an apex body

owned by the RBI in 1988, has a new direction to the decentralized finance

system by promoting housing finance institutions.

The major institutions meeting the housing finance in lndia are:

1. NATIONAL HOUSING BANK OF INDIA (NHB)

NHB was set up in July 1988 under the National Housing Bank Act

1987 with the following objectives:

i. To mobilize resources for the housing sector,

ii. To promote financial institutions, both in the urban and rural areas.

iii. To provide financial, technical and administrative assistance to such

institutions.

iv. To regulate the working of housing finance institutions at all levels.

v To provide advisory services in operating the policies relating to savings

mobilization, credit appraisal, disbursement and recovery.

vi. To identrfy, legal, fiscal, institutional and other constraints to the

development of the housing finance system and to recommend measures

to remove them.

vii. Establishing House Loan Account Scheme, extending the refinancing

schemes for housing finance by commercial banks and other financial

institutions; and

viii. Co-operative land development and shelter programme of public and

private agencies through HUDCO and other financial institutions and

scheduled banks.

It must be stated that housing finance companies across the

country are confronted with a stark problem : a cash crunch of unprecedented

proportions. Refinancing is inadequate and institutional credit is limited. Many

squarely blame the NHB for the present state of affairs as the apex institution

NHB is expected to refinance approved HFCs. Currently there are about 370

Housing finance companies in the country and only 26 of them have been

approved by NHB for refinance facilities. There are a large number of HFCs,

which are depending on it for more than 65 per cent of their loan funds. The

problem is that the NHB itself neck deep in trouble due to the stock scam.

The RBI has suspended the long-term operational assistance of

Rs.50 crore to NHB. The 13 per cent bonds floated by the NHB in December 92

yielded only Rs 45 crore when compared to Rs 88 crore mobilized in 1991. The

Capital Gains Bond Scheme under which NHB mobilized Rs. 156 crore till

September 1992 has been terminated. NHB's problem has naturally had a

deleterious effect on the refinance it is able to offer to the HFCs. The

Government has been dithering over the implementation of the Working Group

Report on Finance for the Housing Sector as the RBI, the Ministry of Finance and

Ministry of Rural Development have objected to some of the important proposals

put forward by the Group. For instance, the report argued that the Government

must do away with the discrimination, which the HFCs face, compared to other

financial institutions.

There are three main factors which have a direct bearing of housing

finance, viz., I) The availability of serviced land, which is a natural resource and

cannot be changed; 2) Providing land for housing implies, cutting of other

sections like agriculture and forestry as the industrialization and urbanization

have appropriated a large chunk of land, the environment is affected by this

encroachment; and 3) the availability of building materials at a reasonable price.

Since 70 per cent of the Indians are poor, the housing components

must therefore be manageable. With this housing situations ,claiming immediate

national attention, housing finance institutions have mushroomed in the last few

years. However, despite them and their disbursement, much needs to be done

especially in areas of policy, law and taxation.

These aspects have been analyzed and reported by the Working

Grwp on Finance for the Housing Sector. It is considered as the most

comprehensive document on the subject. But many of the suggestions have

been demolished. Rejection and lethargy have also disillusioned and

d~scouraged the housing finance authorities.

2. HOUSING AND URBAN DEVELOPMENT CORPORATION (HUDCO)

Over the decades the housing scenario presents a dismal picture.

The living conditions of the people, especially those from the economically

weaker strata, are abysmally low. Shelter, even though a roof over one's head,

continues to be one of the burning issues of the day.

It is in this environment that it was decided in 1970 to establish

HUDCO as a fully owned Government of lndia enterprise with the following

conditional objectives:

i. To provide long term finance for construction of houses for residential

purposes or finance or undertake housing and urban development

programmes in the country.

ii. To finance or undertake, wholly or partially, the setting up of new satellite

towns.

iii. To finance or undertake the setting up of building material industries.

iv. To administer the money received from time to time from the Government

of lndia and other sources as grants or otherwise for the purposes of

financing or undertaking housing and urban development programmes in

the country.

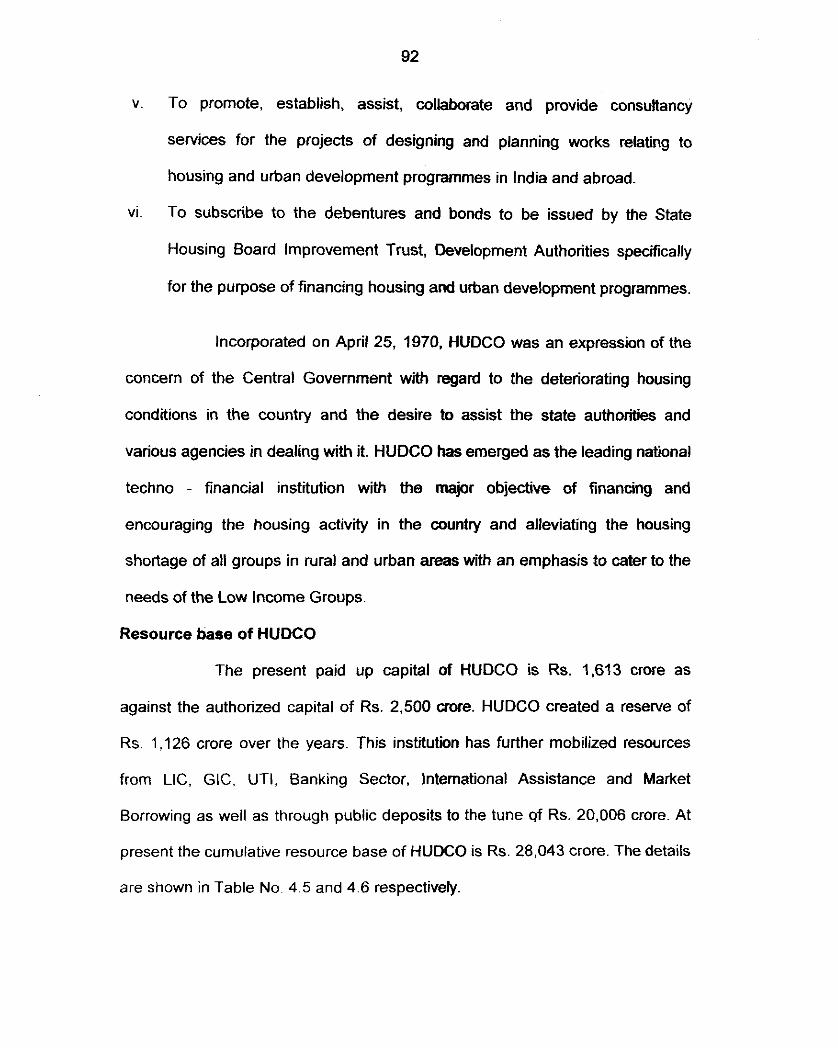

v. To promote, establish, assist, collaborate and provide consultancy

services for the projects of designing and planning works relating to

housing and urban development programmes in India and abroad.

vi To subscribe to the debentures and bonds to be issued by the State

Housing Board Improvement Trust, Development Authorities specifically

for the purpose of financing housing and urban development programmes.

Incorporated on April 25, 1970, HUDCO was an expression of the

concern of the Central Government with regard to the deteriorating housing

conditions in the country and the desire to assist the state authorities and

various agencies in dealing with it. HUDCO has emerged as the leading national

techno - financial institution with the major objective of financing and

encouraging the housing activrty in the country and alleviating the housing

shortage of all groups in rural and urban areas with an emphasis to cater to the

needs of the Low Income Groups.

Resource base of HUDCO

The present paid up capital of HUDCO is Rs. 1,613 crore as

against the authorized capital of Rs. 2,500 crore. HUDCO created a reserve of

Rs. 1,126 crore over the years. This institution has further mobilized resources

from LIC, GIG, UTI, Banking Sector, International Assistance and Market

Borrowing as well as through public deposits to the tune ~f Rs. 20,006 crore. At

present the cumulative resource base of HUDCO is Rs. 28,043 crore. The details

are shown in Table No. 4.5 and 4.6 respectively.

Table No. 4.5 Resource Base of HUDCO (as on 31.03.2003)

B. INTERNATIONAL RESOURCES

Table No. 4.6

A. INTERNAL RESOURCES

Foreign Aided Projects Sanctioned

SI. No.

1

2

W, Germany DM 135M 8670 MJY (Million Japanese Yen) availed for 26 Projects

BIC, Japan for Water Supply & Sewerage Projects Rs. 345.57 Cr (LOC) ($73M) $30M (Rs. 135.60) Cr. raised from US Capital Market

ian Development $100M for Housing (Rs

Source : Website of HUDCO

Programmes of HUDCO:

-

Provisional

Capital Base (Authorized) Equ~ty (Paid-up) Share Application Money Reserves Net Worth

Borrowings (SLR Debentures, Taxablemax-free Bonds, Loans from LIC, GIC, UTI, NHB, International Borrowings, Public Deposits etc.)

In order to realize the objectives for which it was established,

Amounts (Rs. in crore) 2500 1613

50 1126 2748

20006

L Total

HUDCO has implemented a variety of schemes for providing shelter and there by

28043

improving the living conditions of the people. HUDCO extends assistance of

benefiting the masses in urban and rural areas under the broad spectrum of

programmes as described below:

Housing: Urban Housing, Rural Housing, Staff Rental Housing, Co-

operative Housing, Repairs and Renewals, Urban employment through Housing

and Shelter upgradation, Night Shelter for Pavement Dwellers, Working Women

Ownership Condominium Housing, Housing schemes through Private Builders.

In addition to Housing, HUDCO also extends assistance to

infrastructural facilities (like land acquisition, urban infrastructure, basic

sanitation, etc.), consultancy se~ices, building technology and training in human

settlements.

HUDCO's financial assistance for their projects are made available

to agencies which include State Housing Board, Rural Housing Boards, Slum

Clearance Boards, Development Authorities, Primary Co-operatives, Apex Co-

operative Housing Federation, NGOs and Professional Private Developers.

Though HUDCO started its assistance for Rural Housing only from

1977-78, its contribution to rural housing for weaker section has been significant

since its inception.

Financing by HUDCO is invariably project oriented and the

objective is to ensure that projects are affordable to the target groups and at the

same time technically sounds, financially viable and legally acceptable. HUDCO

ensures that the houses built for Economically Weaker Section (EWS) and Low

Income Group (LIG) families remain within their repaying capacity.

People who have been classified by HUDCO in different economic

categories include:

I. Economically Weaker Section Economically Weaker Section (EWS) with

household income of Rs. 1,250 per month or less.

ii. Low Income Group (LIG) - household income not more than Rs. 2,650 per

month. This group should be above EWS

iii. Middle Income Group (MIG) with household income above the LIG but not

more than Rs. 4,450 per month and

iv. High Income Group (HIG) above MIG -but not more than Rs. 4450 per

month.

The details of annual allocation of resources by HUDCO are shown

in Table No. 4.7.

Table 4.7 indicates that 30per cent of the annual allocation of

resources by HUDCO is for EWS, while the annual allocation of resources to LIG

and MIG represent 25 per cent each. The annual allocation of resources by

HUDCO to HIG and Other categories constitutes 20per cent only.

A differential interest rate policy operates for various categories of

household with over ridding emphasis on concessional rate of lending for EWS

and LIG .The lower the household income, the lower the interest rate and vice -

versa. Similarly, the lower the cost of shelter unit, the higher the HUDCO's loan

Table No. 4.7 Annual Allocation of Resources by HUDCO - 'I. No. I 2 3 4

Category Financed

EWS LIG -- MIG HIG 8 Others

- Total 100

Percentage Allocated

Source: Corporate Protile: HUDCO

30 25 25 20

55

45

component as part of the project cost. In the case of EWS where the unit cost is

Rs. 7500 or below, HUDCO finances the entire project cost.

From the following it can be seen that with the increase in unit cost,

project cost goes of declining. Details of the Extent of Financing of the Cost of

Houses to loanees coming under various categories of Income are given in Table

No. 4.8

Table No. 4.8 Details of the Extent of Financina of the Cost of Houses to Loanees corning under various iategories of lncome

Other major fields where HUDCO operates are:

I. Urban infrastructure

II. Training and Research input into Shelter Programmes

Ill. Action Plan Schemes such as:

a. Integrated low cost sanitation scheme

b. Urban employment generation schemes through shelter

upgradation and training.

c. Night shelters

d. Building centres

IV. HUDCO's asststance to rehabilitation housing for national calamities

V. Land Bank for shelterless category

VI. Layout design and analysis models developed by HUDCO

SI. No. I

- I .-..- I . - 4 1 HIG

Income Category

FWS

60

Extent of Financing of the Cost of House (in percentage)

RO

Source: Corporate Profile: HUDCO

VII. Support to building material industry

VIII. Design development and consultancy support

Trends in Sanctioning and Releasing of Funds by HUDCO:

HUDCO's programmes during the 8th plan period, i.e., from 1992 to

1997, had envisaged to support housing and infrastructure projects with a

substantial loan commitment. The sanctions were of the order of Rs. 7323 crore

and the releases were to the tune of about Rs. 5,286 crore.

The increased sanctions and release size, reflects the

Government's thrust for a larger housing effort for the poor and the urban basic

services. This prop3 indeed had helped to provide shelter and amenities to a

large number of economically weaker and socially downtrodden sections of the

society in rural and urban areas.

Table No. 4.9 Details regarding the Operations of HUDCO during the Eighth plan period

Source: Corporate Profile: HUDCO

The Eighth Plan operations of HUDCO had surpassed its financial

and operational efforts during the last twenty two years (i.e., 1972 to 1992) as is

evident from Table 4.9.

HUDCO - Vision 2002

The vision statement for HUDCO 2002 envisages the role of market

leader in supporting housing and urban development needs of the emerging 21''

century into the right choices of options, for policies, progammes and projects

and diversified mode of delivery options through public, private, cooperative,

corporate, NGO and individual sectors.

The HUDCO vision 2002, projects its activity levels of financial

sanction and releases of the order of Rs.12, 717 crore and Rs.11, 058 crore as

given in Table No. 4.70 and a diagrammatic representation of the same is given

in Fig. - II.

Table No. 4.10 HUDCO: Vision 2002 -- (Rs. in crore)

St. No. 1 2 3

Operations

. Up to Eighth Plan (70-92) Eighth Plan (92-97) Vision 2002 Ninth Plan (97-2002)

Total

Sanctions

6,801 7,323 12,717

Source: Corporate Profile HUDCO 26,841

Releases

4,358 5,286 11,058

Grand Total 11,159 12,609 23,775

20,702 47,543

Fig. - I I Funds Sanctioned and Released by HUDCO

(1 970-92,92-97 & 97-2002)

As a market leader in this area of techno - financial assistance,

HUDCO would emerge as the only organization of its kind for dealing with the

needs of shelter and infrastructuie development of human settlements. In short it

would be the overwhelming endeavor to serve as an organization for housing

and urban development sector and also for meeting the goals of social objectivity

and profitability.

As HUDCO completes three decades in the service of the nation, it

has contributed its mite towards poverty alleviation with successful performance

in provision of housing and basic services. Today HUDCO's assistance covers

the housing needs of all income categories of the society with a significant

emphasis on the needs of the deprived. It covers assistance for construction of

new housing stocks as well as for upgradation of the existing housing stock with

an exclusive allocation of its annual resources for the needs of the weaker

section and low income groups. HUDCO extends funds to this section at a

cheaper and affordable rate of interest with a higher amount of funding towards

the total cost of house and a longer repayment period. HUDCO during its three

decades of existence, has extended assistance for taking up over one crore

dwelling units in total, in urban and rural areas. HUDCO's assistance for housing

in last three decades has helped in providing shelter to 101.4 lakhs families in

urban and rural areas and significantly 94 per cent has beneficiaries are the poor

and low income groups. In recent years its annual contribution has been over 1.5

million housing units. In 1999 to 2000, its contribution as part of 2 Million Housing

Programme is particularly significant as HUDCO is contributing to support more

than 4 lakhs units as a + thep!%gramme tq&yf seven hkhs in urban areas t .- 7.; y,.;;; r- \ and more than six lakhs'.@?qainst the prograhuqe target of 13 lakhs in rural

, . ,i ~

areas. Under the 2 Millin Hou- ~ % i j ~ ~ & ~ against the target of 10 lakhs

housing units, HUDCO extended support to build 10.65 lakh units in 1998 to

1999 and 11.09 lakh housing units in 1999 to 2000.

In the fiekl of provision of basic infrastructure in urban areas

HUDCO's contribution has been significant. HUDCO has assisted in the

implementation of 1811 projects with a total project cost of Rs.20,613 crore and

its loan assistance came to the tune of Rs. 12,242 crore. This covers

infrastructural facilities such as water supply, sewage, drainage, sdid water

management, transportation, including airports.

Human Settlement Management Institute (HSMI), the research and

training wing of HUDCO, is the model institute on behalf of the Ministry of Urban

Affairs and Employment to co-ordinate various training and documentation

activities under the Information, Education and Communication (IEC) component

of Swarna Jayanti Shahari Rozgar Yogana (SJSRY), the major poverty

alleviation prograri-*lie in urban area. Seventy training programmes have been

conducted under IEC during January 1999-March 2000.

HUDCO had achieved a land mark performance during 1999-2000.

HUDCO achieved an all time high sanction of Rs 8.899. 89 crore, about 33.5 per

cent growth over last year's achievement of Rs 6666.67 crore by providing

assistance for construction of 16.34 lakh dwelling units and over 1.8 lakh

sanitation units. It had also given support by taking up 86 urban infrastructural

projects through out the country. The loan amount released during 1999-2000

amounted to Rs 4,317.50 crore, which shows an increase of 35 per cent over the

period 1998-1999 (Table No.4..11). HUDCO had also received awards for its

outstanding performance as evaluated against the MOU's entered into with the

respective ministries. The award, for being the top ten Public Sector

Undertakings, was received by HUDCO from the Prime Minister on 1st April

Details regarding HUDCO's Operational Performance as on 3oth

Table No 4 11 HUDCO's Landmark Performance at a glance during 1999-2000.

- - - - --- (Rs. in crore)

June 2003 are presented in Table No.4.12

No 1 2 Source. Shelter - HUDCO publication, Vol. Ill No: 2,

April 2000, p. 6.

Operations

sanctions - -Releases

1998-'99

6,666.67 3,200.68

1999-2000

8,899.89 4,317.50

Growth (in percentage)

33.50 35.00

Table No.4. 12

From Table No.4.12, it is discernible that HUDCO has so far given

assistance for the construction of more than1.35 crore Residential Dwellings,

1.10 crore Dwellings for Economically Weaker Section, 13.84 lakh Residential

Dwellings for Lower Income Group, 4.3 lakh Dwellings and for Middle Incpme

Group and 2.67 lakh Residential Dwellings for Higher lncome Croup besides

providing financial assistance for the construction of 4.15 lakh HUDCO Niwas

Deta~ls regarding the Scheme-wise assistance given by HUDCO

upto 3oth June 2003 are given in .Table No.4.13

Table No.4.13 Details regarding the Scheme-wise assistance given by HUDCO upto 30" June 2003

Table No.4.13 indicates that a major part of HUDCO's financial

assistance constitutes assistance for Urban Housing (68.93 per cent),while the

assistance for Rural Housing; Co-operative Housing and Staff Rental Housing

represent 2.9 per cent, 1.18 per cent and 2.09 per ceni respectively.

Details regarding the Urban Infrastructure Operations of HUDCO

upto 30Ih June 2003 are exhibited in Table No.4.14

Table No. 4.14

Details regarding the Urban lnfrastructure Operations of HUDCO upto 3oth June, 2003

Source: Website of HUDCO

It can be observed from Table N0.4.14 that HUDCO's Urban

lnfrastructure Operations encompasses Utility Infrastructure, Social lnfrastructure

and Commercial Infrastructure. Among the Urban lnfrastructure Operations,

Utility lnfrastructure represents the single major component accounting for about

71.5 per cent of the total, while Sociallnfrastwcture and Commercial

lnfrastructure constitutes 7.08 per cent and 21.42 per cent respectively.

3. HOUSING DEVELOPMENT FINANCE CORPORATION (HDFC)

Incorporated 1n1977 with a share capital of Rs. 100 million, HDFC

has since emerged as the largest mortgage finance institution in the country,

promoted by lClCl and with initial investments from the International Finance

Corporation and the Aga Khan, the corporation had a series of share issue

raising its capital to Rs. 1 19 billion.

Objectives:

The prlmary objective of HDFC is to enhance residential housing

stock and to promote house ownership. Another objective is to increase the flow

of resources for housing through the integration of housing finance institutions

with the domestic capital market.

Operations:

HDFC commenced operations as a mortgage bank. It raised large

resources, both domestic and international ,and lends primarily to individual

households. In 1991, it entered the retail deposit market by offering savings and

~nvestment opportunities to households by competing with other instruments in

the financial market As a result, the number of depositors have risen from 56

thousand in 1991 to over 9, 58000 in 1998 with an outstanding amount of Rs.

44.24 billion, HDFC has a mix of individual and corporate clients ,both on the

funding and lending side.

HDFC's lease finance facilities are being offered to companies and

devebpment authorities for the development of infrastructural facilities and other

assets. Cumulative approvals and disbursements of HDFC as on 31'' March

1998 were Rs.4.33 b~llion and Rs.3.01 billion respectively.

Table NO. 4.15 shows the total resources raised by HDFC during

the years 1996 -1998, including international borrowings.

Table No. 4.15 Details regarding the Resources of HDFC from 1996 -1998

(Rs. in Billion). SI. - IF-. 1 Institutional Loans

Years 1997 1998 7.70 7.52 8.19

2 Domestic loansand Bonds 17.82 22.58 29.06 3 Deposits -- - . , - 25.13 35.02 44.24

Total .- -- -- 50.65 65.12 81.49 Source: HDFC, Corporate Profile.

The total resources of HDFC which stood at Rs.50.65 billion during

1996 has increased to Rs.81.49 billion during the year 1998,registering a growth

rate of 60.88 per cent when compared to the period 1996 as is evident from

Table No.4.15

Lending :

HDFC's loan approvals in the year 1991 aggregated to Rs. 8.14

billion, which increased to Rs. 32.51 billion by 1998. Disbursements for 1998

were Rs.27.54 billion. At the end of March 1998 the cumulative loan approvals

amounted to Rs. 148.38 billion and disbursement amounted to Rs.122.33 billion.

Financial Performance:

HDFC has a track record of high growth and profitability and has

consistently maintained a sound financial position. As at 31st March 2000

HDFC's capital and reserves were Rs.119.11 crore and Rs.1976.86 crore (Table

No.4.16).

The div~dend declared for financial year 1998 was Rs.75 per share.

The capital adequacy of the corporation as at 31st March 1998 was 17.6 per cent

as against a minimum of 8 per cent. Non-performing loans of HDFC were 0 .69

per cent of the loans outstanding.

Houslng finance companies accepting deposits are required to

obtain credit rating for their deposit instruments from a recognized agency and

HDFC was awarded "AAA rating for deposits and bonds both from CRlSlL and

The financial results for the year ended, 31st March 1999 and 31st

March 2000 is presented in Table No. 4.16

Table No. 4.16 The financial results of HDFC for the year ended, 31st March 1999 and

L - h a ? --

Source HDFC - mancia1 results dated. 3rd ME!~ 2000. 1

2 3 (2-1)

4 5 (54)

6 . - 7 - -

I I t,

Getails regarding the pattern of Shareholding of HDFC are shown

In Table No. 4.17

and Taxation) Depreciation Profit before ax Provision for Tax Net Profit Equlty Capital (Paid Up) Reserves --- Earnings Per Share (Shares of Rs.10 each during the

49.77 388.90 55.00

333.90 119.11

1,852.73

28.03

43.58 460.81 59.00

401.81 119.11

1,976.86

33.73

Table No. 4.17

Source: HDFC financial results dated, 3rd May 2000

Foreign Institutional Investors represent the major part (53.68 per

cent) of the shareholding of HDFC, while Foreign Direct.lnvestment, contribution . account for 20.89 per cent of the total. The share of Members (in the Depositoty)

works out to be a miniscule share (0.09 per cent) of the total.

Loan Portfolio

At present HDFC has 3,14.000 loan accounts with an excellent

record of loan recovery with a most sophisticated Management Information

System and loan recoveries. Non-perfonin~.i::..;?ns cover only 0.69 per cent of its

outstanding portfolio.

Other major services rendered by HDFC include the following:

I Property related services - Property identification, sales and service,

property valuat~on~

-. Training - Centre for housing finance, is an effective managerial training

~nstltut~on for houstng finance institutions and for housing finance

\i International Union for housing finance

P Major Consultancy Services - Investment appraisal for housing finance,

Development of mortgage servicing manual, Workshop on housing

finance

Housing finance companies promoted by HDFC include:

P SBI Home Finance Ltd - SBI Capital Market of HDFC

P Can Fin Homes Ltd - Canara Bank and HDFC and ADB

P GIC Housing finance Ltd. - GIC and HDFC

i HDFC Bank - The Bank was promoted by HDFC and commenced

operations in Feb.1995 with a capital of Rs.2 billion of which 25.78 per

cent is held by HDFC and 20 per cent Nat West Group. HDFC Bank has

37 branches (31st March 1998).

In order to face the cut throat competition from the banks that are

entering this sector. HDFC plans to further increase it to reach by adding

branches and opening service centres in smaller cities. As it is mainly focused on

individual customer it has been able to control -it NPA at 0.52 per cent of its loan

portfolio at present. HDFC has a very strong capital adequacy ratio of 20.8 per

cent of risk weighted assets. It has been a consistent performer. Its total income

from operations has grown to Rs.2012.86 crore on 31st March 2000 as against

Rs 1.746.87 in the financial year ended 31st March 1999.

The fall in the interest rate did not affect HDFC, as it was able to

raise deposits before ~nterest rate started coming down.

Different Home Loan Schemes of HDFC:

Home loans for Individuals I Housing Loan I Extension loans I

Home Land Purchase Loans. Under these schemes HDFC offers loans for

houses for buying or constructing home or even to extend or to improve existing

home. Purchase of land, apartments, and multi family bungalow are also allowed

in the scheme.

The maximum loan amount, which can be availed under the

scheme, is Rs.50 lakhs to an individual. HDFC will allow 85 per cent of the cost

of the property, including the cost of land.

The current rate of interest applicable in respect of total loan

sanctioned is ilj.75 per cent. Rate of interest includes interest taxes. The

effective rate of interest varies depending on the term of loan. HDFC reserve the

rate to vary the rate of Interest prospectively at any time in response to changes

In money market condltron or of a levy, tax on interest or any other charge or

burden is imposed or levled by any authority or Government.

Table No. 4.18 The current rate of interest applicable in respect of total loan sanctioned by HDFC

Loan Sanctioned Rate of Interest (%) Per annum'

12.50 13.50 14.50 14.50 15.00

Source: HDFC Corporate Profile

Home Loans for N.R.l's:

Under this scheme an NRI person can avail a maximum amount of

Rs. -50 lakhs or 85 O/o of the cost of the property including cost of the land which

ever is less.

Home Improvement Loans:

Home improvement loans are being sanctioned for:

9 Internal and external repairs

9 Water proofing and roofing

9 Internal and external painting

> Plumbing and electrical works

The loan amount will not exceed Rs. 10 lakhs or 90 per cent of the

cost of the improvement, which ever is lower.

Adjustable Rate Home Loans (ARHL):

Housing finance market has witnessed periodic fluctuations in

interest rate - both downward and upward. That is the loanee stands to gain

interest rates drop and vice versa. Adjustable rates are linked to retail Prime

Lending Rate (PLR). Kate adjustment takes place evey six months from the date

of the first disbursement, if there is change in RPLR .The Current Applicable

Rate of lnterest in respect of ARHL is presented in Table No. 4.19

Table No. 4.19 I The ~ r r e n ~ i i g " e ~ R z + o f lnterest of lRHL Current rate (%)

No. Loan Amount Bas~s ~- ~~~ ~- ~p

Per annum - - I Uq to R S -~ 1 Crore ~- RPLR 12.5 *

Wllh effect hwn May 8, 2WO (Tern 20 years -- Repayment by way of EM1 on annual rest basis)

Source: HDFC Corporate Profile

The effective interest rate of HDFC with effect from May 8,2000 on

different loan schemes were listed in Table No. 4.20 and Table No. 4.21.

Table No. 4.20 lnterest Rates of HDFC

Name of Loans No:

- - - extension loans1 land

urchase loan loans/ land

Table No. 4.21

Single Rate Irrespective of loan amount

ARHZ % I Fixed Rate %

!purfse loan for :.: Terms of Repayment

-- U to W r s

6 years - 10 years

- U to 5 m r s 6 ears-loyeam -

p.a.

12.50

Future Trends

p.a.

13.00

Source: HDFC Brochure.

-

applicable to Home Loans by HDFC

HDFC has developed a network of institution to serve its customers

-

Rate Of

- -

Interest %) P.a.

- --- - 12.50 13.50

- - 14.50

15.50 - -

with specialized finarlclal services through partnership with the best institutions in

thew particular fields of activity

Fixed Rate Home loans

source HDFC Brochure P

Processing of Admission fee

1.00 1 .OO 1 00

1 00

ROI % p.a.

1 1.50

12.50

EM1 for a loan of Rs. 10,000

350 284 246 224

(6 years)

EM1 for Rs. 1, 00,000

2,284 1,856

(for 7 years) Current ratio per annum

11.00 12.00

The Government of lndia had constituted a Committee to review

the entry of private sector in the insurance scenario and the Committee

submitted its report in January 1994, recommending major reforms in the filed of

insurance. In the light of the recommendations by the Committee, the

Government had taken a decision to deregulate the present nationalized

insurance sector and as a result of this the new lnsurance Regulatory Bill was

passed in the Parliament permitting the entfy of private sector into the field of

insurance.

HDFC's next endeavor is to enter into insurance business.

lnsurance has direct links with the competitive advantages that HDFC has

developed over the years. HDFC has a large customer base of shareholders,

depositors and borrowers. Insurance has very close links with housing finance.

HDFC has also submitted a proposal to the SEBI to launch Real

Estate Mutual Fund Guidelines are formulated by SEBI, thus expanding the

areas of which it understands best in serving customers professionally and

effectively.

4. DEWAN HOUSING FINANCE LIMITED (DHFL):

The Premier Housing Finance Corporation in private sector was

incorporated in 1984 under the Companies Act 1956. The Board of Directors

consists of eminent personalities having wide exposure and expertise in the field

of Banking and Finance. Union Bank of lndia has acquired an equity participation

In DHFLS capital structure

DHFL lends at the current rate of interest to individuals, corporate

bodies, co - operatives and associations of persons for residential houses other

than resort houses in lndia.

DHFL is classified as a " Housing Fmance Corporation by the NHB

and recognized by the Government of lndia through its Ministry of Finance.

HOUSING LOAN SCHEMES OF DHFL

Double Protection Plan

Free accident risk cover plus property insurance is offered to the

extent of loan liability to safeguard the interest of the borrower or his family.

Regressive Payments Scheme

The scheme is meant for applicants who are due for retirements

with in five to ten years and have applied joinUy with the eligible younger co-

applicants.

Special Rural Housing Scheme (SRHS)

The objective of Special Rural Housing Scheme (SRHS) is to

address the problems of rural housing through improved access to housing

credit, which would enable an individual to build a modest new house or to

improve or to add to his dwelling in 'rural area'. Rural area for the purpose of the

scheme is the area i r l any town, the population ofwhich does not exceed 50,000

as per 1991 Census

Loan w~ll be given for construction, purchase, improvement

upgradation, major repairs of houses in free hold !and in rural areas.

The interest rates applicable on home loans of DHFL during 2003 is

presented in Table No. 4.22

Table No. 4.22 Details regarding the interest rates applicable on home loans of DHFL during 2003

Annual rates of interests (fixed rates) applicable to the loan amount

ranging from Rs. 10,000 to Rs. 100,00,000 for 1 - 5 years works out to 9.25 per

cent per annum, while the same for 6 - 10 years and 11 to 20 years represent

9.75 per cent per annum and 10.25 per cent per annum respectively (Table No.

4.22). But the annual rates of interest (variable rate) for the periods mentioned

above come to 10 per cent per annum only.

House Loans Account Scheme:

DHFL is authorized to accept HLA deposits by the NHB. The

scheme is deslgned to help an aspiring house maker in more ways than one. It

inculcates the habit of saving in a planned manner by providing a person

considerable incentive by way of concessional interest rate on the housing loans.

The scheme matures at the end of five years from opening the account. A person

1s entitled to a housing loan according to his aggregate savings in the HLA

account, ranging from four times to fifteen times of the savings. The scheme

allows great flexibility in terms of the amount of deposits, frequency of deposits;

etc

Rented Housing Scheme

This scheme has devised for the benef& of employees and workers

in the corporate world. Under this scheme proposals for rental housing projects

will be considered, provided the proposal is exclusively for the employees or

workers

Land Development, Shelter Project Scheme:

This is a scheme for professional developers, applicable to project

of land development of either for plot development or for group housing or a mix

DHFL, slnce its incorporation in 1984, has taken a quantum leap in

all facets of its operations to become a front runner among housing finance

companies in India. The company has a paid up equity base of Rs. 9.03 crore,

having the following share holding pattern. Details regarding the pattern of Share

Holding of DHFL are given in Table No. 4.23

Table No. 4 23 Detail-ardtn-epattern of Share Holding of DHFL - - -- I :A I Name of the Shareholder / % Of Shares held /

. -. --

Total ~ -- 100.00 -- Source: DHFL Brochure.

LIC and Housing Finance

With a view to solve the problem of housing shortage in the country

LIC has taken massive efforts by providing financial assistance to individuals,

Co-operative housing societies and State Governments. LIC has established a

new subsidiary called LIC Housing Finance Ltd in 1989. The main objective of

this organization is to provide long t e n financial assistance to realize the

objective of National Housing society.

LIC Housing Finance Ltd (LICHF) with its network of 67 area offices

and 6 regional offices has a cumulative housing loan disbursement of over

Rs.4536 crore. It has a market share of 25 per cent of the organized housing

finance. It ranks second only to HDFC which has 54 per cent of the market share

.of the organized housing finance.

CANFIN Homes Ltd

CANFIN Homes Ltd is a housing finance company supported by

NHB on a regional level under the Indian Companies Act in the International Year

of Shelter for home less (1987) in association with UTI, HDFC, IClCl and Canara

bank Financial Services Ltd. The main objective is to lend money to individuals,

co-operatives and corporate bodies for acquisition or construction of residential

units only.

Housing Finance in Co-operative Sector:

The principles of mutual aid, self help, practice of thrift which one

the basic principles of co operative organizations, generate a sturdy feeling of

self reliance which is of basic importance in a democratic way of life. By pooling

their experience and knowledge and by helping one another, members of co-

operative societies not only find solutions of individual problems but also become

better citizens.

The Co-Operabve Societies Act of 1904, the legislation in india with

regard to Cooperatives, amended in1912 to permit the formation of solutions for

purposes other than credit. The first co operative housing society was set up in

lndia in 1909 known as Bangalore Cooperative Society in Mysore state

(Karnataka) and Bombay Co-operative housing Association in 1913 in Bombay

state (Maharashtra)

In lndia in the field of housing there is a three tier co-operative

structure with the National Co-operafive Housing Federation at the apex level

and the State Housing Federation with middle and the Primary Societies in the

lower level. There are different kinds of Housing Cooperatives in lndia, which

range from building societies to Co-operatives, Township societies and housing

cooperatives, higher purchase companies, etc.

The housing structure of co-operative housing societieq in Kerala

consists of two levels, i.e, primary and state level societies. In the state level the

Kerala State Housing Federation (House Fed) established in 1970 provide loans

and advances to primary c:ooperatives. The federation provided financial

assistances amounting Rs.1, 00,283 houses up to 1998.

At present the housing society apex co-operatives are getting

finance from LIC. NHH & HUDCO. The apex federation raises more of its funds

from LIC, NHB & HUDCO as their effective role of refinance in co-operative

sector. So the central Government must ensure the regular flow of funds to the

housing co-operatives for the execution of their housing projects because the

central Government can play an effective. role for the u p l i e n t of this institution.

The following chart depicts the channel of f iand to cooperative sector.

CHANNEL OF FINANCE

HUDCO

i -+ State Co-operqtive Housing Federation

+ Members

Role of Banks in Housing Finance:

There is a vast scope for housing promotion in India and banks can

play a vital role in the promotion of housing. To enable larger flow of resources to

the housing sector banks have been allowed to change interest at different rates,

provided they are below the prime lending rate in respect of housing finance

intermediary agencies.

Currently banks advances up to Rs. 3 lakh for housing in rural and

semi-urban areas. rhese areas are treated as priority sector advances by banks.

It has been decided to increase the limit up to Rs. 5 lakh for the purpose of

compensation of priority sector advances. The RBI has approved the advances

made by commercial banks for construction and repairs as priority sector

advances. Indirect lending through Government housing finance agencies such

as HDFC for construction of homes, slum clearances, etc will also be considered

as priority sector advancement subject to a ceiling of Rs.3 lakh per housing units.

The RBI has removed the margin restricfions on housing finance by

banks and has brought about many changes. For instance, the Syndicate Bank

provides Housing finance up to 70 per cent of the value of the property, subject

to a ceiling of Rs.25 lakh per housing unit. The banking sector received an edge

over the housing finance companies because of the lower prime lending rate.

Banks also do not levy commitment charges, administrative fees, unlike housing

f iand companies, which increase the lending cost by 1 to 1.5 per cent.

Taking advantage of the cost factor, number of banks has revised

their lending rates. ANZ Grindlays Bank have made their home loans easily

affordable through scheme like "Home Loans Umbrella, Home loans Banner" for

buying, construction, extension and renovation of houses. Syndicate disbursed

loans amounting to Rs 80.64 crore in 1997-98 and corporation bank has a target

of Rs 150 crore. in the total disbursement of Rs 126 crore in 1997-98.

Rate of Interest in Housing Finance:

Housing finance up to Rs 5 lakhs is being considered as priority

sector advance as per the RBI regulations 1997. Bank offers the most

competitive rate of riter rest ranging from 12 per cent to 15 per cent. Housing

Finance Corporation Banks offers the best rate of interest compared to other

housing finance companies ranging from 12 per cent -25 per cent to 14 per cent.

The rates of interest have been steeply decreasing from year to year due to the

acute competition among various institutions in the field of housing finance.

The Interest rates of Commercial banks and other Housing Finance

Corporations are presented in Table No. 4.24.

Table No. 4.24 Details regarding the Interest rates of Commercial Banks and other Housing

CANFIN Homes Construction

8-1 5 years

lClCl

Source: The Mathrubhumi Daily 2001, October 30. p.10.

The Repayment Method :

Considering repayment of loans in comparison with the interest

rates, different housing finance companies work out different repayment

equations. Some companies calculate interest as a monthly reducing balance

compared to HDFC the calculation is in a year reducing basic which is costlier

than monthly reducing balance method. Bank of lndia calculates interest on daily

balance system. State Bank of lndia uses a quarterly balance system while all

other banks uses monthly reducing balancing system. The other requirements for

lending housing loans slightly varies from one institution to other such as the

repayment period, monthly repayment period (EMI) maximum loan amount,

processing charges, administrative fees, penalty for premature closing and

number of documents required. Table No. 4.25 clearly shows the comparative

procedures for obtaining a housing loan from different housing finance

companies.

Table No. 4.25 Comparative procedures for obtaining a housing loan from different Housing Finance Companies and Banks

I !

I

I Maximum loan I

i 9 ' Rs.

amount [ 25,00,000

i I

- ~ 4 - -~

I Penalty for I repayment of

36 times of

monthly income or 80

%of total cost

'3 loan ahead NIL

scheduled period ~~~

I -~

Rs . 25,00,000

NIL

85 % of total cost up to Rs. 50,00,000

2 O h

11 Insurance p-

-~ - , Required Required

Rs. 10,00,000

NIL

Source: Brochure of~espective Institutions. Required Required

redemption charges

NIL

The demand for housing finance can be attributed to a fall in the

rates of interest . Other factors responsible indude the stabilization of real estate

in the country is increasing the disposable income of Government employees on

account of pay revision and acute shortage of dwelling units in the country.

Presently 150 households manage with hundred houses. As per the estimate of

Planning commission, the shortage in urban and rural housing will be 93 million

units and 29.8 million units respectively by the year 2001; thus taking the total

shortage to all most forty million units which requires an investment of Rs. 52,000

crore in the Ninth F i e year Plan period.

Housing finance companies on their part are restricting their

strategies by opening single window clearance for a number of products and

opening new service centers in various cities of the countries to tap the growing

demand.

It is important for consumer that not only he should feel pleased in

the availability of multiple sources of housing finance but also other aspects like

the interest rate, pay back facility flexibility in repayment of monthly installment

and other legal and economic conditions .

The problem of housing still past due to multi dimensional problems

encounter by HFC's themselves such as: Availability of Funds: The average

lending rate of HFC's varies between 12 to 15 per cent but the cost of raising

funds is around 16 per cent in many cases.

Entering into an Era of Rate War

Players in the field have entered to an era of rate war due to high

competitive market.

Risk of Default

Since the HFC's are running short of funds, any default by the

customers will have a direct impact on the lending capaclty of the companies.

When compared to commercial banks HFC's NPA level is only 49 per cent where

as the banks NPA comes to 8.20 per cent.

The other two major problems faced by the HFC have legal

aspects (default by borrower and time to take its settlement) and high stamp

duties.

Towards improving the quality and quantny of housing stock,

housing calls for vast capital resource but adequate incentives are not provided

to individuals for investing in instrument of housing finance. Fiscal concessions

will go a long way in mobilizing the much needed resources. The law makes

compulsory by HFC's to deduct taxes at the source on interest more than Rs.

2,500 a financial year . This is a gross discrimination as mutual funds do not

come under its purview and consequently appear attractive.

The tax sop in the union budget coupled with falling interest rate

have made housing frnance more attractive proposal for the individual today.

Most HFC's decide the quantum of loan on the basis of his income and the

assessed repayment capac~ty.

Housing finance does not enjoy the status of a priority sector. The

role played by everyone operating in this field is not very laudable. Many of the

conditions governing their operations are conducive. It is high time that the

strategic importance of housing finance is recognized and encouraged.

The economy witnessed continuation of reform and the general

policy of liberalization especially in the banking sector. This development had

important bearing on mobilization and deployment of saving potentials with

further deregulation of interest rates. For a significant development the concept

of 'Affordable Housing' is being increasingly seen in terms of cost reduction and

income up gradation rather than in the form of subsidies. This will evolve a

sustainable housing solution in the housing market.

In the changing economic scenario, it is equally important to

integrate the housing financing system with the other sectors of the economy so

that surplus funds could be channelised for housing.

A large volume of funds is to be injected to the housing sector to

improve the lending capacity.

Banks and housing finance institution should be empowered to

create equitable mortgage by taking the deposits of title deeds and given power

of sale in that court intervention. Settling a secondary mortgage market could be

a viable alternative for mobilizing additional resources.

A unlforrn and reasonable stamp duty is to introduce through out

the country to mlttgate the magnitude of the problems.

Amendment of Transfer of Property Act has been called for to

recognize the right of flat owners in a co-operative society for the creation of

mortgage.

Prov~ding housing facilities is a social responsibility of the

Government. There fore profa should be secondary, particularly the Government

sponsored housing finance company.

Removal of Urban Land Ceiling Act, grant of infracture status to

housing reduction of interest rate, for housing loan, simplified procedures in the

sanctioning of loans, more income tax concessions to individuals will give a boost

to construction.

With the rapid transformation taking place in financial system, as a

result of liberalization and globalization of capital movements, the very structure

of existing institutions are passing through the process of rigorous

transformation. Housing finance companies are also not exception to it and have

made great strides in past few years. Restructuring of these institutions and

developing appropriate marketing orientations is a major challenges faced by

them.

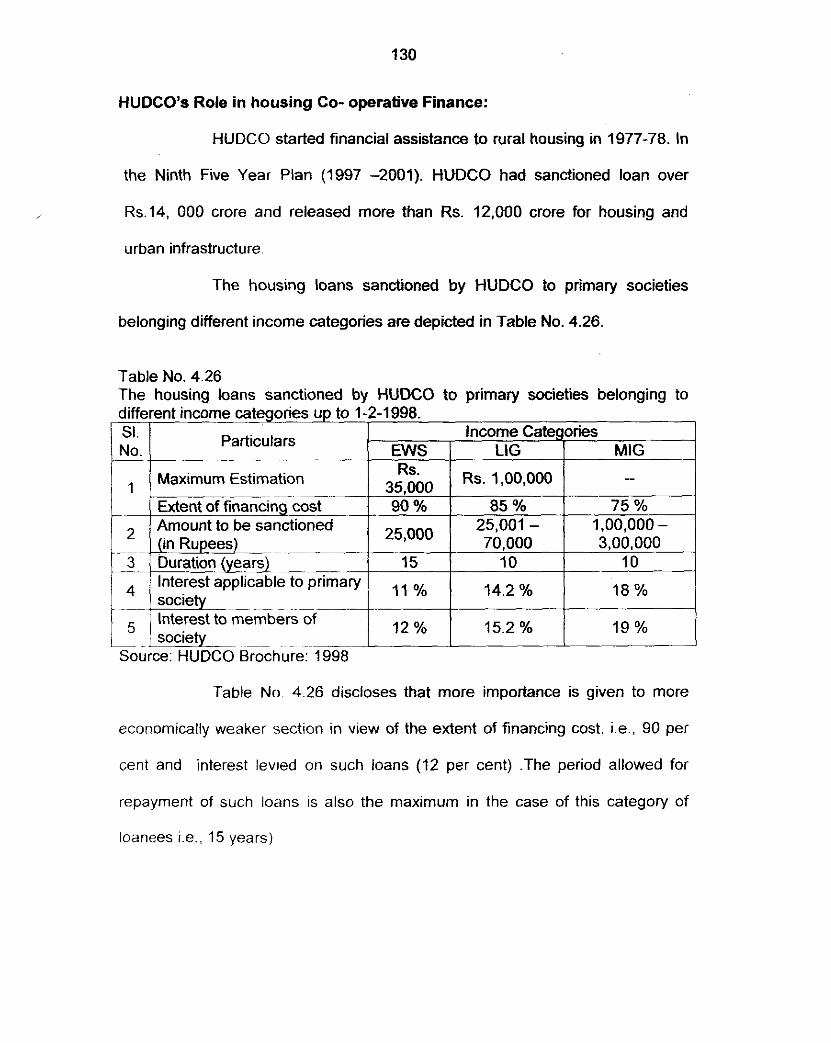

HUDCO's Role in housing Co- operative Finance:

HUDCO started financial assistance to rural housing in 1977-78. In

the Ninth Five Year Plan (1997 -2001). HUDCO had sanctioned loan over

Rs.14, 000 crore and released more than Rs. 12,000 crore for housing and

urban infrastructure

The housing loans sanctioned by HUDCO to primary societies

belonging different income categories are depicted in Table No. 4.26

Table No. 4.26 The housing loans sanctioned by HUDCO to primary societies belonging to different income categories up to 1-2-1998.

,a,icu,ars Income Categories

- - - - EWS I LIG MIG I . 1 Maximum Estimation 1 ,.- RS. A,.- I

1 1 (in Rupe;) .- ) ~

3 Duration ears 15 10 10 lnterest applicable to primary

- -. ~~

socie 15.2 % 19 %

-~ ~ -

Source: HUDCO Brochure: 1998

Table No. 4.26 discloses that more importance is given to more

economically weaker section in view of the extent of financing cost, iie., 90 per

cent and interest levled on such loans (12 per cent) .The period allowed for

repayment of such loans is also the maximum in the case of this category of

loanees i.e.. 15 years)