chapter 2 determination of interest rates © 2003 south-western/thomson learning

TRANSCRIPT

CHAPTER

22Determination of Interest Rates

© 2003 South-Western/Thomson Learning

Chapter ObjectivesChapter Objectives

Explain Loanable Funds Theory of Interest Rate Determination

Identify Major Factors Affecting the Level of Interest Rates

Explain How to Forecast Interest Rates

Relevance of Interest Rate MovementsRelevance of Interest Rate Movements

Changes in interest rates impact the real economy Investment spending Interest sensitive consumer spending such as housing

Interest rate changes affect the values of all securities Security prices vary inversely with interest rates Varying interest rates impact retirement funds and retirement

income Interest rates changes impact the value of financial

institutions Managers of financial institutions closely monitor rates Interest rate risk is a major risk impacting financial

institutions

Loanable Funds Theory of Interest Rate Loanable Funds Theory of Interest Rate DeterminationDetermination

Theory of how the general level of interest rates are determined

Explains how economic and other factors influence interest rate changes

Interest rates determined by demand and supply for loanable funds

Loanable Funds Theory, cont.Loanable Funds Theory, cont.

Demand = borrowers, issuers of securities, deficit spending unit

Supply = lenders, financial investors, buyers of securities, surplus spending unit

Assume economy divided into sectors Slope of demand/supply curves related to

elasticity or sensitivity of interest rates

Sectors of the EconomySectors of the Economy

Household Sector--Usually a net supplier of loanable funds

Business Sector—Usually a net demander in growth periods

Government Sectors States—Borrow for capital projects Federal—Borrow for capital projects and deficit

spending Foreign Sectors—Net supplier since early

1980’s

Demand for Loanable FundsDemand for Loanable Funds

Sum of sector demand (quantity) at varying levels of interest rates

Sector cash receipts in period less than outlays = borrower

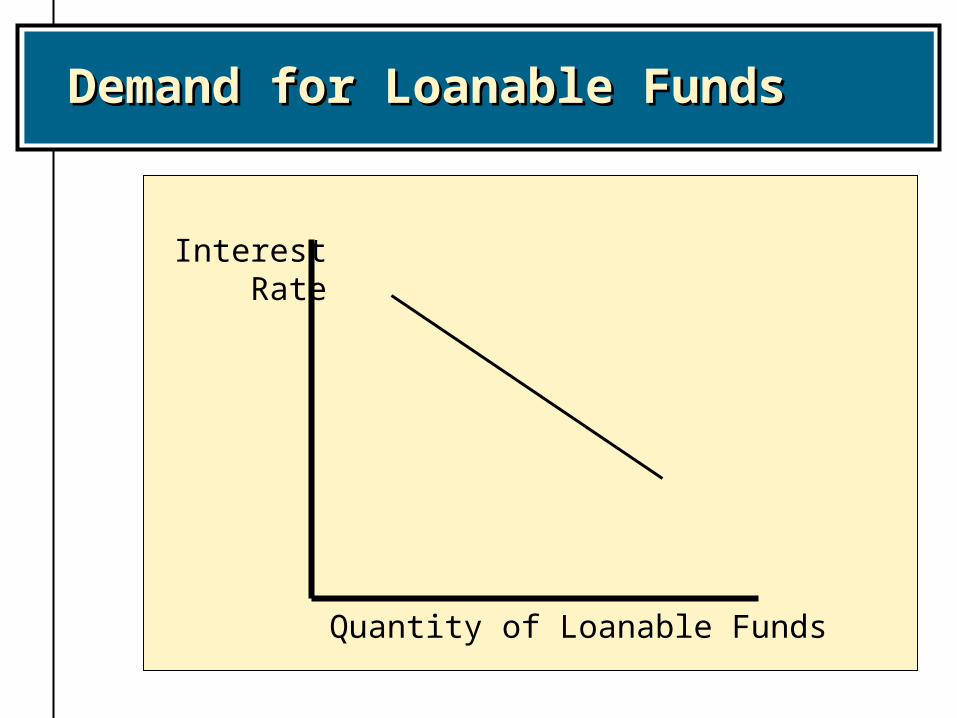

Quantity demanded inversely related to interest rates

Variables other than interest rate changes cause shift in demand curve

Demand for Loanable FundsDemand for Loanable Funds

Interest Rate

Quantity of Loanable Funds

Loanable Funds TheoryLoanable Funds Theory

Households demand loanable funds to finance housing, automobiles, household items

These purchases result in installment debt. Installment debt increases with the level of income

There is an inverse relationship between the interest rate and the quantity of loanable funds demanded

Household Demand for Loanable Funds

Loanable Funds TheoryLoanable Funds Theory

Businesses demand loanable funds to invest in assets

Quantity of funds demanded depends on how many projects to be implemented Businesses choose projects by calculating the project’s

Net Present Value Select all projects with +NPV’s

Business Demand for Loanable Funds

Loanable Funds TheoryLoanable Funds Theory

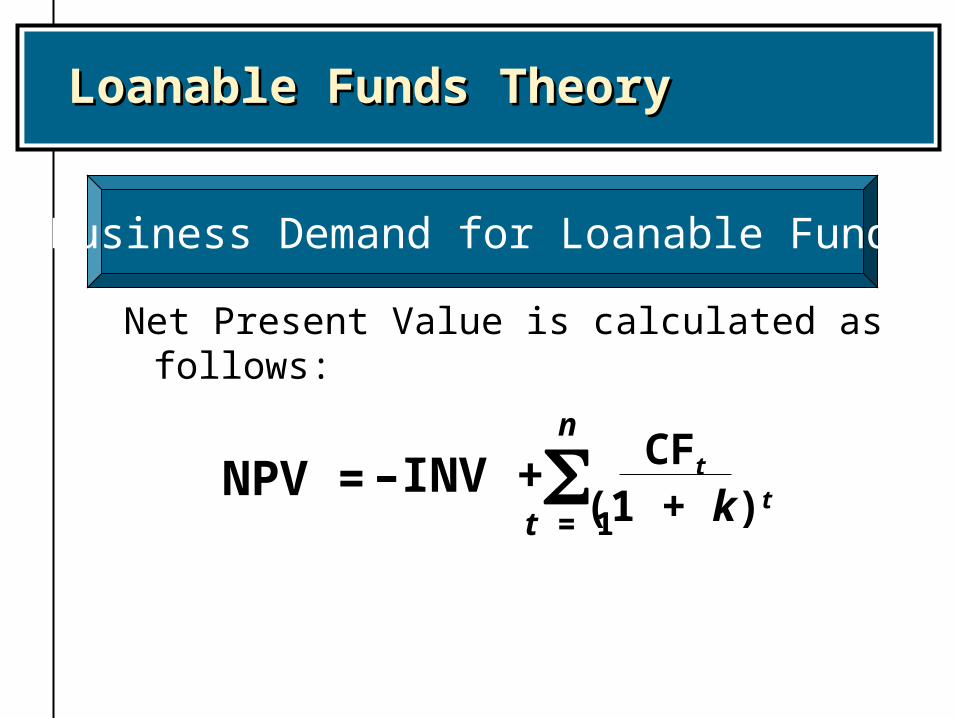

Net Present Value is calculated as follows:

CFt(1 + k)tt = 1

n

–INV +NPV =

Business Demand for Loanable Funds

Loanable Funds TheoryLoanable Funds Theory

Projects with a positive NPV are accepted because the present value of their benefits outweighs their costs

If interest rates decrease, more projects will have a positive NPV

Businesses will need a greater amount of financing Businesses will demand more loanable funds

Business Demand for Loanable Funds

Loanable Funds TheoryLoanable Funds Theory

There is an inverse relationship between interest rates and the quantity of loanable funds demanded

The curve can shift in response to events that affect business borrowing preferences

Example: Economic conditions become more favorable Expected cash flows will increase > more positive NPV

projects > increased demand for loanable funds

Business Demand for Loanable Funds

Loanable Funds TheoryLoanable Funds Theory

When planned expenditures exceed revenues from taxes, the government demands loanable funds

Municipal (state and local) governments issue municipal bonds

Federal government and its agencies issue Treasury securities and federal agency securities.

Government Demand for Loanable Funds

Loanable Funds TheoryLoanable Funds Theory

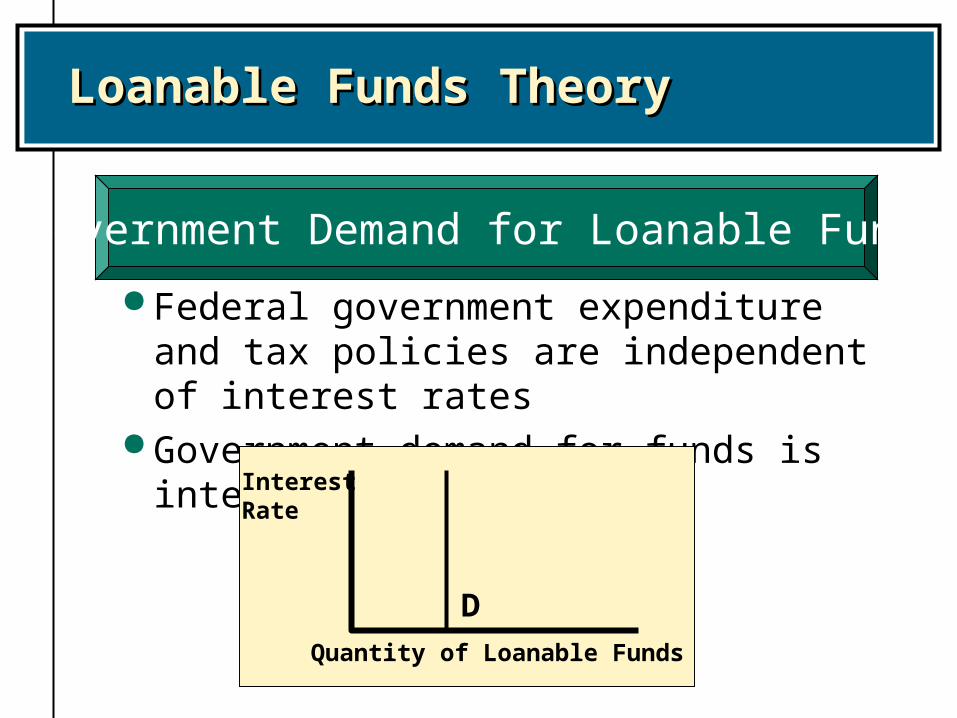

Federal government expenditure and tax policies are independent of interest rates

Government demand for funds is interest-inelastic

D

InterestRate

Quantity of Loanable Funds

Government Demand for Loanable Funds

Loanable Funds TheoryLoanable Funds Theory

A foreign country’s demand for U.S. funds is influenced by the differential between its interest rates and U.S. rates

The quantity of U.S. loanable funds demanded by foreign investors will be inversely related to U.S. interest rates

Foreign Demand for Loanable Funds

Loanable Funds TheoryLoanable Funds Theory

The aggregate demand for loanable funds is the sum of the quantities demanded by the separate sectors

The aggregate demand for loanable funds is inversely related to interest rates

Aggregate Demand for Loanable Funds

Sector Supply of Loanable FundsSector Supply of Loanable Funds

Households are major suppliers of loanable funds

Businesses and governments may invest (loan) funds temporarily

Foreign sector a net supplier of funds in last twenty years

Federal Reserve’s monetary policy impacts supply of loanable funds

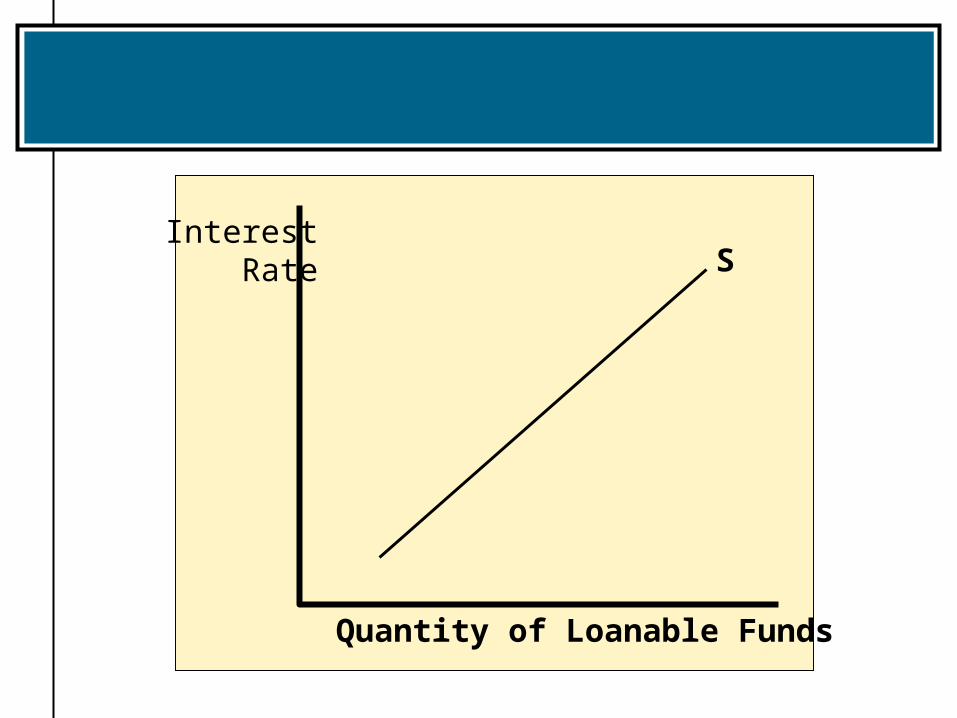

Supply of Loanable FundsSupply of Loanable Funds

Sum of sector supply (quantity) at varying levels of interest rates

Sector cash receipts in period greater than outlays—lender

Quantity supplied directly related to interest rates

Variables other than interest rate changes causes a shift in the supply curve

InterestRate

Quantity of Loanable Funds

S

Loanable Funds TheoryLoanable Funds Theory

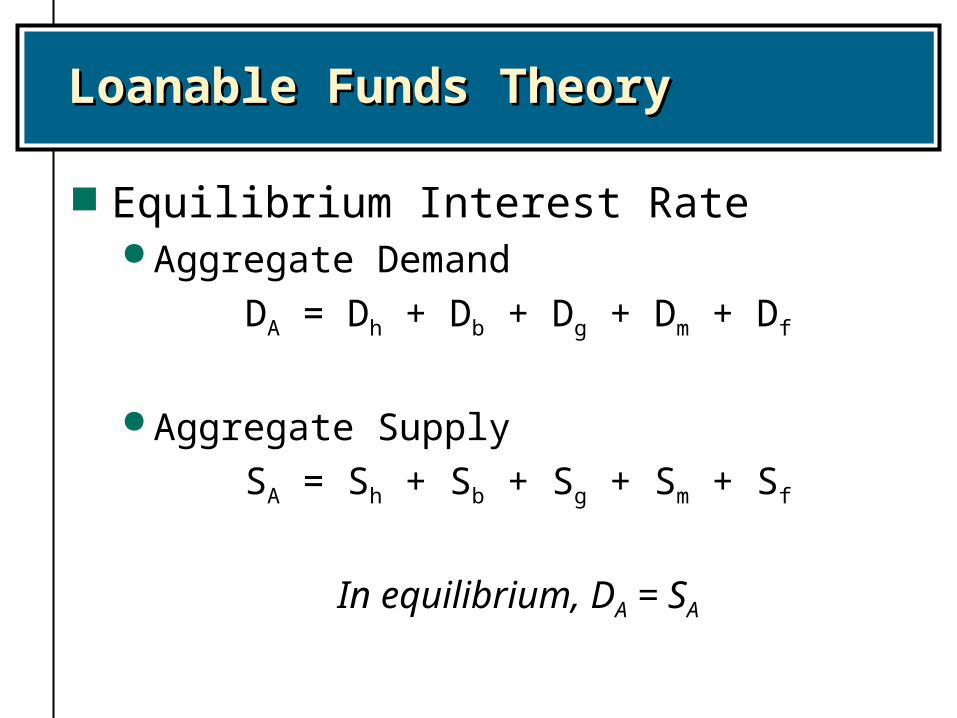

Equilibrium Interest Rate Aggregate Demand

DA = Dh + Db + Dg + Dm + Df

Aggregate Supply

SA = Sh + Sb + Sg + Sm + Sf

In equilibrium, DA = SA

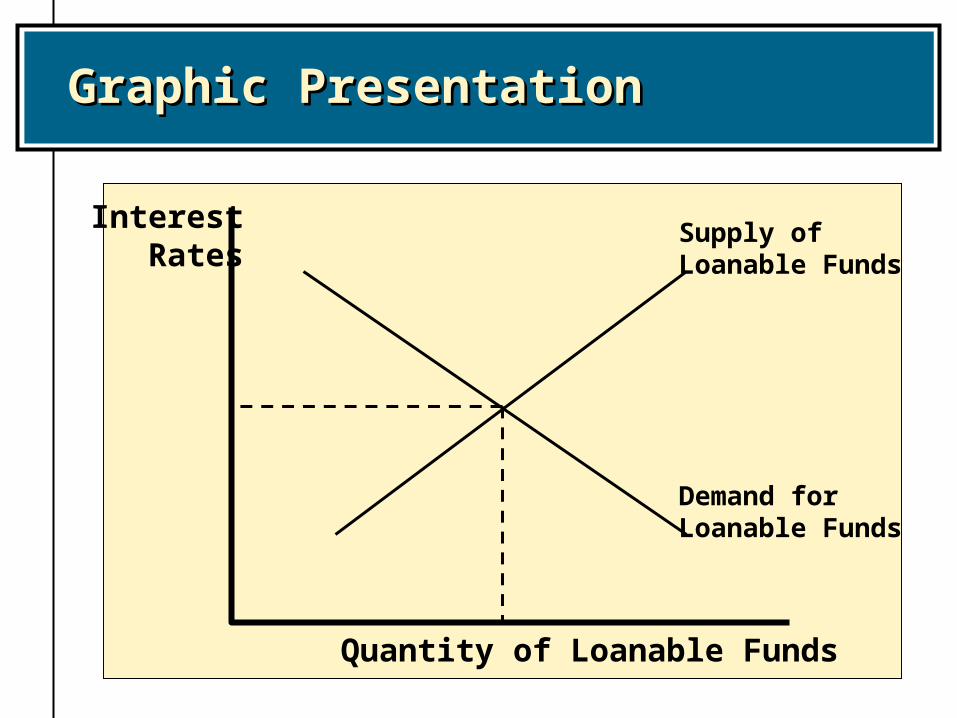

Demand for Loanable Funds

Supply of Loanable Funds

Interest Rates

Quantity of Loanable Funds

Graphic PresentationGraphic Presentation

Loanable Funds TheoryLoanable Funds Theory

Graphic Presentation When a disequilibrium situation exists, market

forces should cause an adjustment in interest rates until equilibrium is achieved

Example: interest rate above equilibrium Surplus of loanable funds Rate falls Quantity supplied reduced, quantity demanded

increases until equilibrium

General Equilibrium Interest RateGeneral Equilibrium Interest Rate

Means of explaining how economic factors affect interest rate levels

Interest rate level where quantity of aggregate loanable funds demanded = supply

Surplus and shortage conditions Surplus- Quantity demanded < quantity supplied

followed by market interest rate decreases ShortageGovernment interest rate ceilings below

market interest rates

Interest Rate ChangesInterest Rate Changes

+ Directly related to level of economic activity or growth rate of economic activity

+ Directly related to expected inflation – Inversely related to rates of money supply

changes

Economic Forces That Affect Interest Economic Forces That Affect Interest RatesRates

Economic Growth Expected impact is an outward shift in the demand

schedule without obvious shift in supply New technological applications with +NPV’s Result is an increase in the equilibrium interest

rate

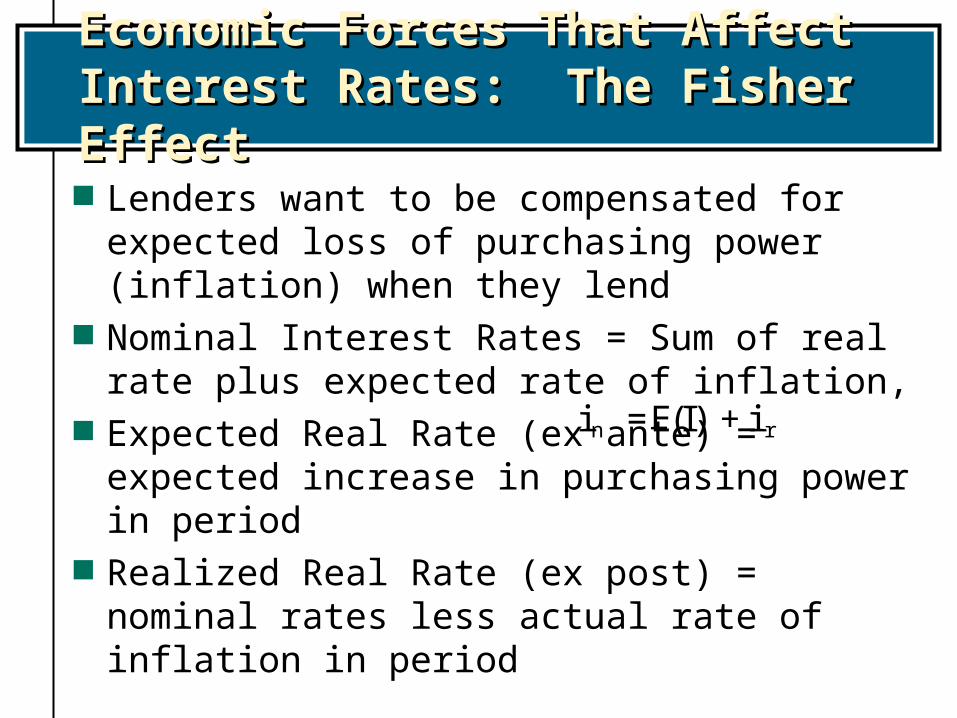

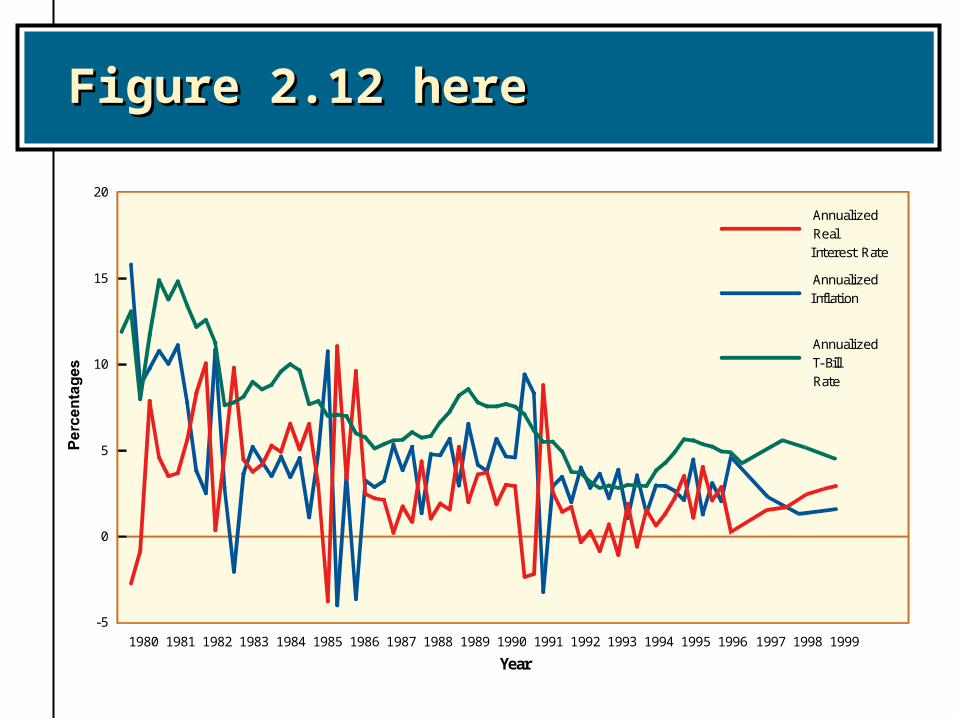

Economic Forces That Affect Interest Economic Forces That Affect Interest Rates: The Fisher EffectRates: The Fisher Effect

Lenders want to be compensated for expected loss of purchasing power (inflation) when they lend

Nominal Interest Rates = Sum of real rate plus expected rate of inflation,

Expected Real Rate (ex ante) = expected increase in purchasing power in period

Realized Real Rate (ex post) = nominal rates less actual rate of inflation in period

i E I in r= +( )

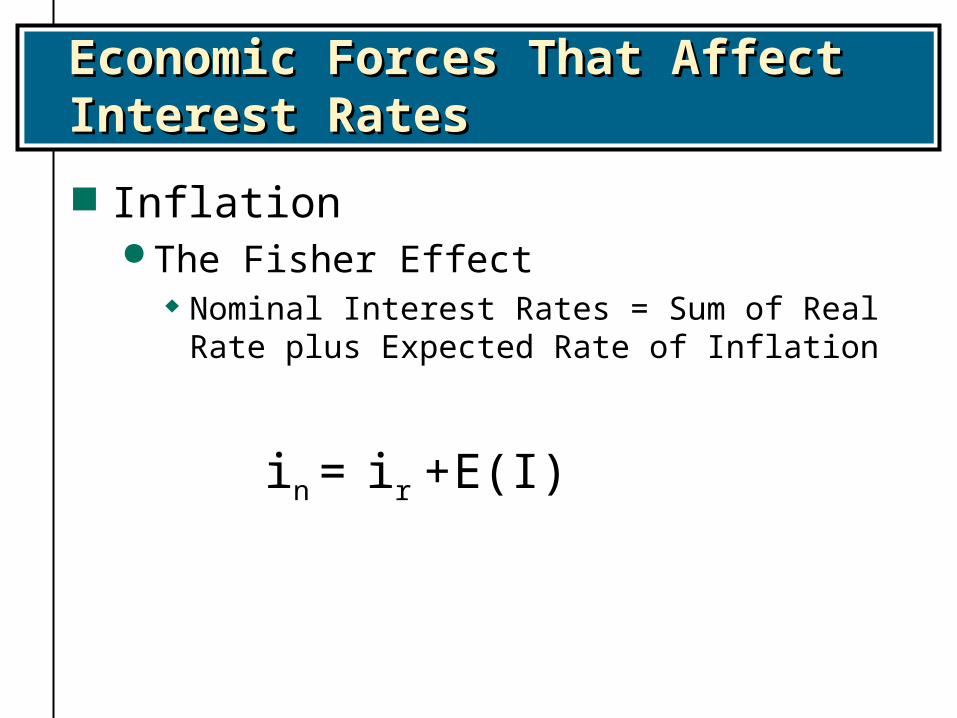

Economic Forces That Affect Interest Economic Forces That Affect Interest RatesRates

Inflation The Fisher Effect

Nominal Interest Rates = Sum of Real Rate plus Expected Rate of Inflation

in ir E(I)+=

Figure 2.12 hereFigure 2.12 here

Year

-5

0

5

10

15

20

Annualized

Real

Interest Rate

Annualized

Inflation

Annualized

T-Bill

Rate

199619951994 19991998199719931992199119901989198819871986198519841983198219811980

Economic Forces That Affect Interest Economic Forces That Affect Interest RatesRates Inflation

If inflation is expected to increase Households may reduce their savings to make purchases

before prices rise Supply shifts to the left, raising the equilibrium rate Also, households and businesses may borrow more to

purchase goods before prices increase Demand shifts outward, raising the equilibrium rate

Economic Forces That Affect Interest Economic Forces That Affect Interest RatesRates

Money Supply When the Fed increases the money supply, it

increases supply of loanable funds Places downward pressure on interest rates

Economic Forces That Affect Interest Economic Forces That Affect Interest RatesRates

Federal Government Budget Deficit Increase in deficit increases the quantity of

loanable funds demanded Demand schedule shifts outward, raising rates Government is willing to pay whatever is

necessary to borrow funds, “crowding out” the private sector

Economic Forces That Affect Interest Economic Forces That Affect Interest RatesRates

Foreign Flows In recent years there has been massive flows

between countries Driven by large institutional investors seeking

high returns They invest where interest rates are high and

currencies are not expected to weaken These flows affect the supply of funds available in

each country Investors seek the highest real after-tax, exchange

rate adjusted rate of return around the world

Forecasting Interest RatesForecasting Interest Rates

Attempts to forecast demand/supply shifts Forecast economic sector activity and impact

upon demand/supply of loanable funds Forecast incremental effects on interest rates Forecasting interest rates has been difficult

Summary: Key Factors Impacting Summary: Key Factors Impacting Interest Rates Over TimeInterest Rates Over Time

Economic Growth—Increased growth; increased demand for funds; interest rates increase

Expected inflation--security prices fall; interest rates increase

Government budgets Deficit—increase borrowing; security prices fall, interest

rates increase Surplus—decreased borrowing; security prices increase;

interest rates decrease

Increased foreign supply of loanable funds—security prices increase; interest rates decrease