chapter- 2 manufacturing account - - get a free blog

TRANSCRIPT

1

Manufacturing AccountsManufacturing AccountsClassification of CostsClassification of Costs

2 Ir. Haery Sihombing (IP).Pensyarah Fakulti Kejuruteraan Pembuatan

Universiti Teknologi Malaysia Melaka

MANUFACTURING ACCOUNTSMANUFACTURING ACCOUNTS

The following passage is: The following passage is: a brief introduction to manufacturing a brief introduction to manufacturing accounts and accounts and how manufacturing costs are how manufacturing costs are classified.classified.

Classification of Costs Classification of Costs ((11))

A manufacturing account is prepared to A manufacturing account is prepared to find out: find out: the the cost of goods manufacturedcost of goods manufactured. . Costs of manufacturing include: Costs of manufacturing include: all resources used, directly or indirectly, all resources used, directly or indirectly, in the manufacture of goods. in the manufacture of goods. The manufacturing costs can be The manufacturing costs can be classified into classified into direct costs direct costs and and indirect indirect costscosts

Direct costs can be identified specifically Direct costs can be identified specifically and exclusively with a given costand exclusively with a given costobjective in an economically feasible way.objective in an economically feasible way.

What are direct costs?What are direct costs?

Classification of Costs Classification of Costs ((22))

2

Classification of Costs Classification of Costs ((22))

Direct costsDirect costs are those costs directly are those costs directly involved in the manufacture of goods. involved in the manufacture of goods.

Examples of Examples of direct costs direct costs are: are: direct materials direct materials direct labor direct labor and and direct expensesdirect expenses. . All the direct costs are collectively known All the direct costs are collectively known as as prime costprime cost. .

Indirect costs cannot be identifiedIndirect costs cannot be identifiedspecifically and exclusively with aspecifically and exclusively with agiven cost objective in an economicallygiven cost objective in an economicallyfeasible way.feasible way.

What are indirect costs?What are indirect costs?

Classification of CostsClassification of Costs ((33))

Classification of Costs Classification of Costs ((33))

Indirect costsIndirect costs are not directly are not directly related to production. related to production. They are all the remaining production They are all the remaining production expenses. expenses. Examples of Examples of indirect costs indirect costs include include factory rent, factory power, depreciation factory rent, factory power, depreciation of plant and machinery, etc. of plant and machinery, etc. Indirect costs are also known as Indirect costs are also known as factory factory overheadsoverheads. .

•• A A manufacturing accountmanufacturing account is prepared to find out the is prepared to find out the cost of goods manufactured. Costs of manufacturing cost of goods manufactured. Costs of manufacturing include all resources used, directly or indirectly, in the include all resources used, directly or indirectly, in the manufacture of goods. The manufacturing costs can be manufacture of goods. The manufacturing costs can be classified into direct costs and indirect costs. classified into direct costs and indirect costs.

•• Direct costsDirect costs are those costs directly involved in the are those costs directly involved in the manufacture of goods. Examples of direct costs are direct manufacture of goods. Examples of direct costs are direct materials, direct labor and direct expenses. All the direct materials, direct labor and direct expenses. All the direct costs are collectively known as prime cost. costs are collectively known as prime cost.

•• Indirect costsIndirect costs are not directly related to production. are not directly related to production. They are all the remaining production expenses. Examples They are all the remaining production expenses. Examples of indirect costs include factory rent, factory power, of indirect costs include factory rent, factory power, depreciation of plant and machinery, etc. Indirect costs depreciation of plant and machinery, etc. Indirect costs are also known as factory overheads. are also known as factory overheads.

3

What Distinguishes What Distinguishes Direct and Indirect Costs?Direct and Indirect Costs?

Managers prefer to classify costs as direct rather than indirect whenever it is “economically feasible” or “cost effective.”

Other factors also influence whether a cost is considered direct or indirect.The key is the particular cost objective.

Categories of Categories of Manufacturing CostsManufacturing Costs

Any raw material, labor, or other inputAny raw material, labor, or other inputused by any organization could, in theory, used by any organization could, in theory, be identified as a direct or indirect costbe identified as a direct or indirect costdepending on the cost objective.depending on the cost objective.

Cost Classifications for Cost Classifications for Manufacturing FirmsManufacturing Firms

1.1. Direct MaterialDirect Material2.2. Direct LaborDirect Labor3.3. Manufacturing OverheadManufacturing Overhead/ / indirect indirect

manufacturingmanufacturing

Manufacturing Costs Manufacturing Costs (product costs): all (product costs): all costs associated with the production of costs associated with the production of goods.goods.

Direct Material Costs...Direct Material Costs...

–– include the acquisition costs of all include the acquisition costs of all materials that are physically identified as materials that are physically identified as a part of the manufactured goods and that a part of the manufactured goods and that may be traced to the manufactured goods may be traced to the manufactured goods in an economically feasible way.in an economically feasible way.

4

Direct Labor Costs...Direct Labor Costs...

–– include the wages of all labor that can be include the wages of all labor that can be traced specifically and exclusively to the traced specifically and exclusively to the manufactured goods in an economically manufactured goods in an economically feasible way.feasible way.

Indirect Manufacturing Costs...Indirect Manufacturing Costs...

–– or or factoryfactory overheadoverhead,, include all costs include all costs associated with the manufacturing process associated with the manufacturing process that cannot be traced to the manufactured that cannot be traced to the manufactured goods in an economically feasible way.goods in an economically feasible way.

Cost Classifications for Cost Classifications for Manufacturing FirmsManufacturing Firms NonNon--Manufacturing CostsManufacturing Costs

1.1. Selling CostsSelling Costs2.2. General and Administrative CostsGeneral and Administrative Costs

NonNon--manufacturing Costsmanufacturing Costs (period costs): all (period costs): all costs not associated with the production of costs not associated with the production of goods.goods.

5

Product Costs...Product Costs...

–– are costs identified with goods produced are costs identified with goods produced or purchased for resale.or purchased for resale.Product costs are initially identified as Product costs are initially identified as part of the inventory on hand.part of the inventory on hand.These costs, inventoriable costs, become These costs, inventoriable costs, become expenses (in the form of cost of goods sold) expenses (in the form of cost of goods sold) only when the inventory is sold.only when the inventory is sold.

Period Costs...Period Costs...

–– are costs that are deducted as expenses are costs that are deducted as expenses during the current period without going during the current period without going through an inventory stage.through an inventory stage.

1 2 3

4 5 6 7 8 9 10

11 12 13 14 15 16 17

18 19 20 21 22 23 24

25 26 28 29 30 3127

Period or Product Costs Period or Product Costs

In In merchandising accountingmerchandising accounting, insurance, , insurance, depreciation, and wages are period costs depreciation, and wages are period costs (expenses of the current period).(expenses of the current period).In In manufacturing accountingmanufacturing accounting, many of these , many of these items are related to production activities and items are related to production activities and thus, as indirect manufacturing, are product thus, as indirect manufacturing, are product costs.costs.

Period Costs Period Costs ––Merchandising and ManufacturingMerchandising and Manufacturing

In both merchandising In both merchandising andand manufacturing manufacturing accounting, selling and general accounting, selling and general administrative costs are period costs.administrative costs are period costs.

6

Product and Period CostsProduct and Period Costs

Product Costs Product Costs and and Period Costs Period Costs are are Synonymous with Manufacturing and Synonymous with Manufacturing and

Nonmanufacturing costs, respectively.Nonmanufacturing costs, respectively.

Product Cost Information in Financial Product Cost Information in Financial Reporting and Decision MakingReporting and Decision Making

GAAP (Generally Accepted Accounting GAAP (Generally Accepted Accounting Principles) requires that inventory on Principles) requires that inventory on balance sheets and cost of goods sold on balance sheets and cost of goods sold on income statements be disclosed (reported) income statements be disclosed (reported) using using Full Cost Full Cost information.information.

Balance Sheet Presentation of Balance Sheet Presentation of Product CostsProduct Costs

1.1. Raw Materials InventoryRaw Materials Inventory..2.2. Work in Process InventoryWork in Process Inventory..3.3. Finished Goods Inventory.Finished Goods Inventory.

Flow of Product Costs in AccountsFlow of Product Costs in Accounts

Product costs flow from the Product costs flow from the Direct Direct MaterialsMaterials, , Direct LaborDirect Labor and and MManufacturinganufacturingOverheadOverhead through through Work in ProcessWork in Process to to Finished Goods InventoryFinished Goods Inventory and finally to and finally to Cost of Goods SoldCost of Goods Sold. .

7

Flow of Product Costs in AccountsFlow of Product Costs in Accounts Income Statement Presentation Income Statement Presentation of Product Costsof Product Costs

When finished goods are sold they are When finished goods are sold they are moved from moved from Finished GoodsFinished Goods to to CCost of ost of Goods SoldGoods Sold..

Cost of Goods ManufacturedCost of Goods Manufactured

Cost of Goods Manufactured Cost of Goods Manufactured includes all includes all costs of goods completed during the period.costs of goods completed during the period.

Cost of Goods SoldCost of Goods Sold

Cost of Goods Sold.Cost of Goods Sold.

8

Types of Costing SystemsTypes of Costing Systems

Companies use product costing systems Companies use product costing systems to measure and record the cost of to measure and record the cost of manufactured products. Two types:manufactured products. Two types:

1.1. JobJob--Order Costing SystemOrder Costing System..2.2. Process Costing System.Process Costing System.

Overview of Job Costs and Overview of Job Costs and Financial Statement AccountsFinancial Statement Accounts

In a In a JobJob--Order Costing SystemOrder Costing System, the three , the three product costs (materials, labor and product costs (materials, labor and overhead) are related to specific jobs.overhead) are related to specific jobs.

Relating Product Costs to JobsRelating Product Costs to Jobs Job Costs and Financial Job Costs and Financial Statement AccountsStatement Accounts

9

Flow of Costs in a JobFlow of Costs in a Job--Order Order Costing SystemCosting System JobJob--Order Costing SystemOrder Costing System

In In JobJob--Order Costing Systems Order Costing Systems the primary the primary document (likely electronic) is called a document (likely electronic) is called a JobJob--Cost Sheet. Cost Sheet. It is used to accumulate It is used to accumulate or capture the following costs:or capture the following costs:

1.1. Direct Material Cost.Direct Material Cost.2.2. Direct Labor Cost.Direct Labor Cost.3.3. Manufacturing OverheadManufacturing Overhead..

Direct MaterialsDirect Materials

A A Materials Requisition Form Materials Requisition Form is used is used to request the release of materials to request the release of materials from stores inventory into production.from stores inventory into production.

Direct MaterialsDirect Materials

10

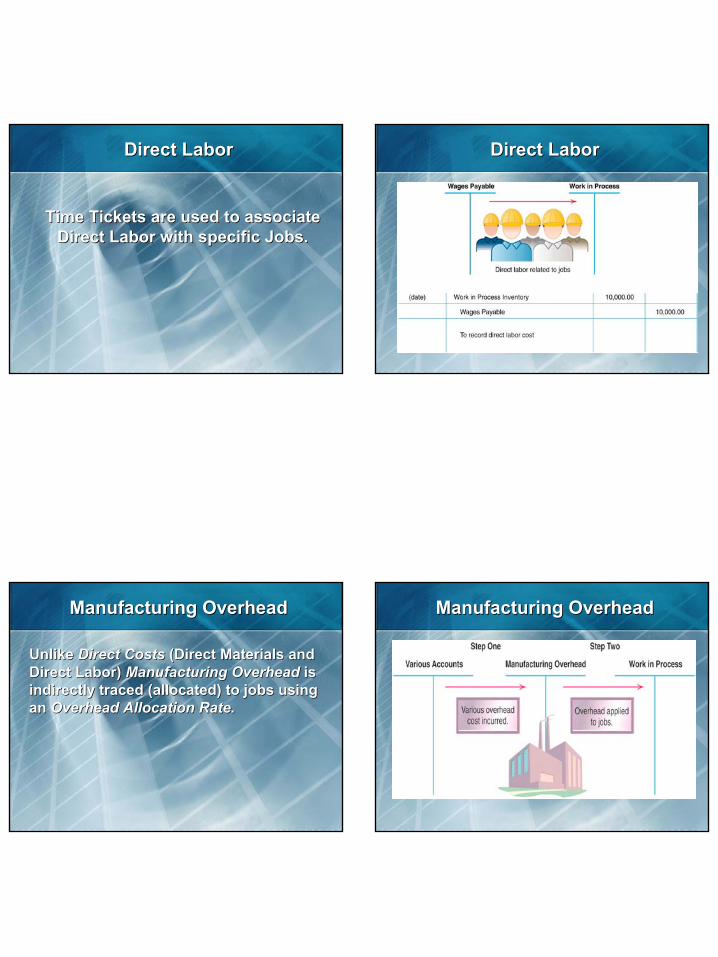

Direct LaborDirect Labor

Time Tickets Time Tickets are used to associate are used to associate Direct Labor Direct Labor with specific with specific Jobs. Jobs.

Direct LaborDirect Labor

Manufacturing OverheadManufacturing Overhead

Unlike Unlike Direct Costs Direct Costs (Direct Materials and (Direct Materials and Direct Labor) Direct Labor) Manufacturing OverheadManufacturing Overhead is is indirectly traced (allocated) to jobs using indirectly traced (allocated) to jobs using an an Overhead Allocation RateOverhead Allocation Rate..

Manufacturing OverheadManufacturing Overhead

11

Assigning Costs to Jobs: A SummaryAssigning Costs to Jobs: A Summary Relation Between the Costs of Relation Between the Costs of Jobs and the Flow of CostsJobs and the Flow of Costs

Allocating Overhead to Jobs: A Allocating Overhead to Jobs: A Closer LookCloser Look

1.1. Overhead Allocation RatesOverhead Allocation Rates2.2. Overhead Allocation BaseOverhead Allocation Base3.3. Activity Based Costing Activity Based Costing (ABC) and (ABC) and

Multiple Overhead RatesMultiple Overhead Rates

Overhead Allocation RateOverhead Allocation Rate

Overhead Allocation Rate = Overhead Allocation Rate =

Overhead CostOverhead Cost

Allocation BaseAllocation Base

12

Overhead Allocation BaseOverhead Allocation Base

Alternative bases include:Alternative bases include:

1.1. Direct labor hoursDirect labor hours2.2. Direct labor costDirect labor cost3.3. Machine hoursMachine hours4.4. Direct material cost. Direct material cost.

ActivityActivity--Based Costing (ABC) Based Costing (ABC) and Multiple Overhead Ratesand Multiple Overhead Rates

ABC is a method of assigning overhead ABC is a method of assigning overhead based on a number of different allocation based on a number of different allocation bases (rather than just one). ABC groups bases (rather than just one). ABC groups overhead costs into overhead costs into Cost Pools.Cost Pools.

Predetermined Overhead RatesPredetermined Overhead Rates

Predetermined Overhead Rate =Predetermined Overhead Rate =

Estimate Total Overhead CostEstimate Total Overhead Cost

Estimated Level of Allocation BaseEstimated Level of Allocation Base

Eliminating Overapplied or Eliminating Overapplied or Underapplied OverheadUnderapplied Overhead

1.1. Actual costs (Materials, Labor and Actual costs (Materials, Labor and Overhead) are accumulated in the Overhead) are accumulated in the Manufacturing Overhead Manufacturing Overhead Account andAccount and

2.2. Overhead is applied to production Overhead is applied to production based on the based on the Predetermined Predetermined Overhead RateOverhead Rate. .

13

Eliminating Overapplied or Eliminating Overapplied or Underapplied Overhead Underapplied Overhead (continued)(continued)

1.1. Unless estimates are perfect, there Unless estimates are perfect, there will be either a debit or credit balance will be either a debit or credit balance in the in the Manufacturing Overhead Manufacturing Overhead account.account.

2.2. If actual > applied, a debit balance, If actual > applied, a debit balance, results, thus results, thus underappliedunderapplied overhead.overhead.

3.3. If actual < applied a credit balance, If actual < applied a credit balance, results, thus results, thus overappliedoverapplied overhead.overhead.

Eliminating Overapplied or Eliminating Overapplied or Underapplied Overhead Underapplied Overhead (continued)(continued)

1.1. Manufacturing Overhead should Manufacturing Overhead should have a zero balance at yearhave a zero balance at year--endend

2.2. Often closed it out to Cost of Goods Often closed it out to Cost of Goods Sold.Sold.

3.3. Theoretically it should be allocated Theoretically it should be allocated between Work in Process, Finished between Work in Process, Finished Goods and Cost of Goods Sold.Goods and Cost of Goods Sold.

JobJob--Order Costing for Service Order Costing for Service CompaniesCompanies

1.1. JobJob--Order Costing is also used by Order Costing is also used by service companies.service companies.

2.2. Examples include hospitals (patients) Examples include hospitals (patients) and automobile repair firms.and automobile repair firms.

Modern Manufacturing Practices and Modern Manufacturing Practices and Product Costing SystemsProduct Costing Systems

1.1. JustJust--inin--Time (JIT) Production.Time (JIT) Production.2.2. ComputerComputer--Controlled ManufacturingControlled Manufacturing..3.3. Total Quality Management (TQM).Total Quality Management (TQM).

14

Quick Review Quick Review Question #1Question #1

1.1. Which of the following is a period cost?Which of the following is a period cost?a.a. Raw materials costs.Raw materials costs.b.b. Manufacturing plant maintenance.Manufacturing plant maintenance.c.c. Wages for production line workers.Wages for production line workers.d.d. Salary for the vice president of Salary for the vice president of

finance.finance.

Quick Review Quick Review Question #2Question #2

2.2. Which of the following is a direct Which of the following is a direct materials cost?materials cost?a.a. Steel for a ship builder.Steel for a ship builder.b.b. Production supervisor salary for an Production supervisor salary for an

auto manufacturer.auto manufacturer.c.c. Factory rent.Factory rent.d.d. Pocket protector for company Pocket protector for company

accountant.accountant.

Quick Review Quick Review Question #3Question #3

3.3. Beginning workBeginning work--inin--process plus total process plus total manufacturing costs minus ending manufacturing costs minus ending workwork--inin--process equalsprocess equalsa.a. Cost of materials used.Cost of materials used.b.b. Finished goods inventory.Finished goods inventory.c.c. Cost of goods sold.Cost of goods sold.d.d. Cost of goods manufactured.Cost of goods manufactured.

Quick Review Quick Review Question #4Question #4

4.4. Cost of Goods Sold is $200,000, Cost of Goods Sold is $200,000, beginning Finished Goods is $50,000, beginning Finished Goods is $50,000, ending Finished Goods is $100,000 ending Finished Goods is $100,000 and ending Work in Process is and ending Work in Process is $10,000. What is the Cost of Goods $10,000. What is the Cost of Goods Manufactured?Manufactured?a.a. $100,000$100,000b.b. $250,000$250,000c.c. $50,000$50,000d.d. $150,000$150,000

15

THE ENDTHE END