chapter 2 the balance sheet copyright © 2013 pearson education, inc. publishing as prentice hall...

TRANSCRIPT

Chapter 2The Balance Sheet

Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall

2-1

Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall

The Balance Sheet

• Also called the statement of condition or the statement of financial position

• Shows the financial condition of a company on a particular date

• Summarizes what the firms owns and what the firm owes to outsiders and to internal owners

2-2

Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall

Financial Condition

• Assets are what the firm owns.

• Liabilities are what the firm owes to outsiders.

• Stockholders’ equity is what the firm owes to internal owners.

equity rs'Stockholde sLiabilitie Assets

2-3

Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall

Financial Condition

Consolidation

• Parent company owns more than 50% of voting stock.

• Financial statements are combined.

2-4

Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall

Financial Condition

Balance Sheet Date

• The date the balance sheet is prepared

• Could be the end of the calendar year, fiscal year, quarter, etc.

2-5

Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall

Financial Condition

Comparative Data

• SEC requires two-year audited balance sheets.

• Provides a reference point for determining changes in financial position

2-6

Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall

Financial Condition

Common-Size Balance Sheet• Expresses each item on the balance

sheet as a percentage of total assets

• Reveals the composition of assets

• Form of vertical ratio analysis

• Useful for evaluating trends within a firm

• Allows for making industry comparisons

2-7

Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall

Financial Condition

2-8

Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall

Assets

Segregated according to how they are utilized

• Current Assets

• Property, Plant, and Equipment

• Other Assets

2-9

Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall

Assets

Current Assets

• Expected to be converted to cash within one year or one operating cycle

• Continually used up and replenished

2-10

Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall

Assets

Current Assets

• Operating cycle

Time required to purchase or manufacture inventory, sell the product, and collect the cash

• Working capital

Also called net working capital

Current assets less current liabilities

2-11

Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall

Assets

Current Assets

• Cash and cash equivalents

• Marketable securities

• Accounts receivable

• Inventories

• Prepaid expenses

2-12

Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall

Assets

2-13

Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall

Assets

Current Assets – Cash and Cash Equivalents

• Cash awaiting deposit

• Cash in a bank account

• Short-term investments that can be converted to cash within three months

2-14

Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall

Assets

Current Assets – Marketable Securities

• Short-term investments that can be converted to cash within a year

• Three categories Held to maturity

Trading securities

Securities available for sale

2-15

Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall

Assets

Current Assets – Accounts Receivable

• Customer balances outstanding on credit sales

• Net realizable value – actual amount of account less an allowance for doubtful accounts

2-16

Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall

Assets

Current Assets – Accounts Receivable

• Allowance for doubtful accounts Affects balance sheet valuation

Important in assessing earnings quality

Should reflect volume of credit sales, past experiences with customers, customer base, credit policies, collections practices, and economic conditions

2-17

Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall

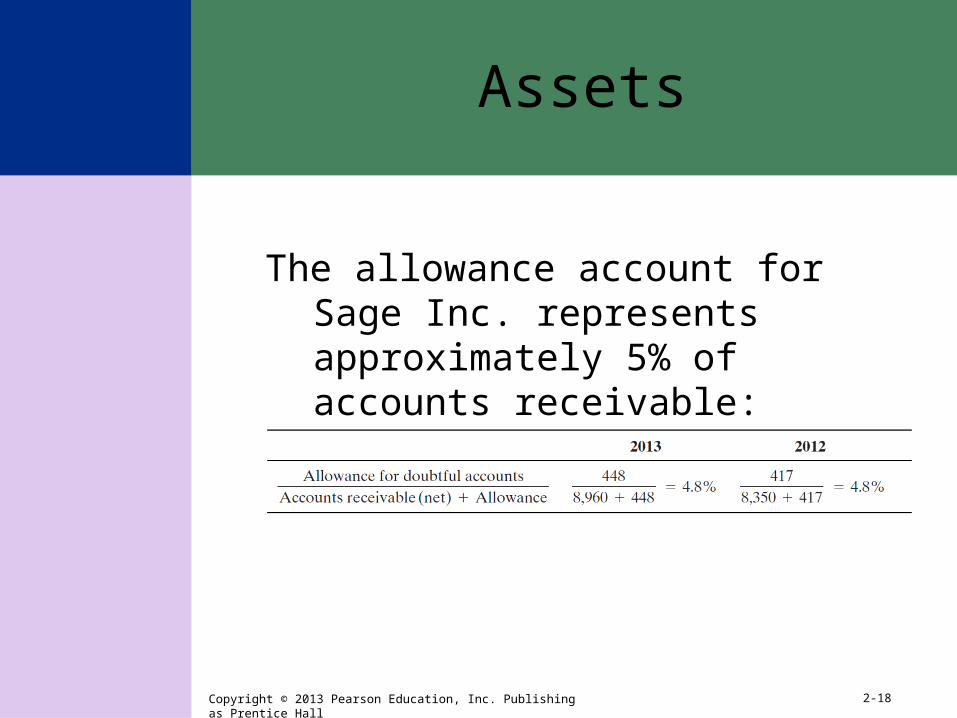

Assets

The allowance account for Sage Inc. represents approximately 5% of accounts receivable:

2-18

Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall

Assets

Current Assets – Accounts Receivable

• There should be a consistent relationship between the rate of change in sales, accounts receivable, and the allowance for doubtful accounts.

2-19

Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall

Assets

Sage Inc.

2-20

Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall

Assets

To analyze the preceding information, consider the following:

• Are all three accounts changing in the same directions and at consistent rates of change?

• If the direction and rates of change are not consistent, what are possible explanations for these differences?

• If there is not a normal relationship between the growth rates, what are possible reasons for the abnormal pattern?

2-21

Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall

Assets

For Sage Inc.,

• Sales, accounts receivable, and the allowance for doubtful accounts have all increased.

• Allowance account has increased appropriately in relation to accounts receivable.

• Sales have grown at a much greater rate. More sales in cash have probably been

collected.

Sage will probably experience fewer defaults.

2-22

Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall

Assets

Current Assets – Accounts Receivable

• Additional information helpful to the analysis of accounts receivable and the allowance account is provided in the schedule of “Valuation and Qualifying Accounts.” Additions Charged to Costs and

Expenses

Deductions

2-23

Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall

Assets

2-24

Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall

Assets

• “Additions Charged to Costs and Expenses” is the amount estimated and recorded as bad debt expense each year on the income statement.

• “Deductions” is the actual amount the firm has written off as accounts receivable they no longer expect to recover.

• Analyst should use this schedule to assess the probability that the firm is intentionally over- or underestimating the allowance account.

• Sage Inc. appears to estimate an expense fairly close to the actual amount written of each year.

2-25

Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall

Assets

Current Assets – Inventories

• Items held for sale

• Items used in the manufacture of products that will be sold

• Major revenue producer for most companies

2-26

Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall

Assets

Current Assets – Inventories

• Retail companies Finished goods

• Manufacturing companies Raw materials

Work-in-process

Finished goods

• Service –oriented companies Little to no inventory

2-27

Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall

Assets

2-28

Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall

Assets

Current Assets – Inventories

• Inventory Accounting Methods Method used has considerable impact on

financial position and operating results.

Valuation is based on an assumption regarding the flow of goods, not the actual order in which products are sold.

Cost flow assumption is made in order to match the cost of products sold to the revenue generated.

Disclosure of inventory cost flow assumption is found in the notes.

2-29

Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall

Assets

Current Assets – Inventories

• Inventory Accounting Methods First in, first out (FIFO)

Last in, first out (LIFO)

Average cost

2-30

Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall

Assets

2-31

Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall

Assets

Example – A new company in its first year of operations purchases five products for sale in the order and at the prices shown. The company sells three of these items at the end of the year.

Item Purchase Price

#1 $5

#2 $7

#3 $8

#4 $9

#5 $11

2-32

Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall

Assets

Cost flow assumptions

Resulting effect on the income statement and balance sheet

2-33

Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall

Assets

Current Assets – Inventories

• Inventory Accounting Methods During a period of inflation, the LIFO

method typically produces

• the highest cost of goods sold expense

• the lowest ending valuation of inventory

• undervalued inventories on the balance sheet

• cost of goods sold values at current cost of inventory items

2-34

Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall

Assets

Current Assets – Inventories

• Inventory Accounting Methods During a period of inflation, the FIFO

method typically produces

• the lowest cost of goods sold expense

• the highest ending valuation of inventory

• inventory values on the balance sheet that are at current cost

• cost of goods sold values below the current cost of inventory items

2-35

Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall

Assets

Current Assets – Inventories

• Inventory Accounting Methods During a period of deflation, the FIFO

method typically produces

• the highest cost of goods sold expense

• the lowest ending valuation of inventory

• undervalued inventories on the balance sheet

• cost of goods sold values at current cost of inventory items

2-36

Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall

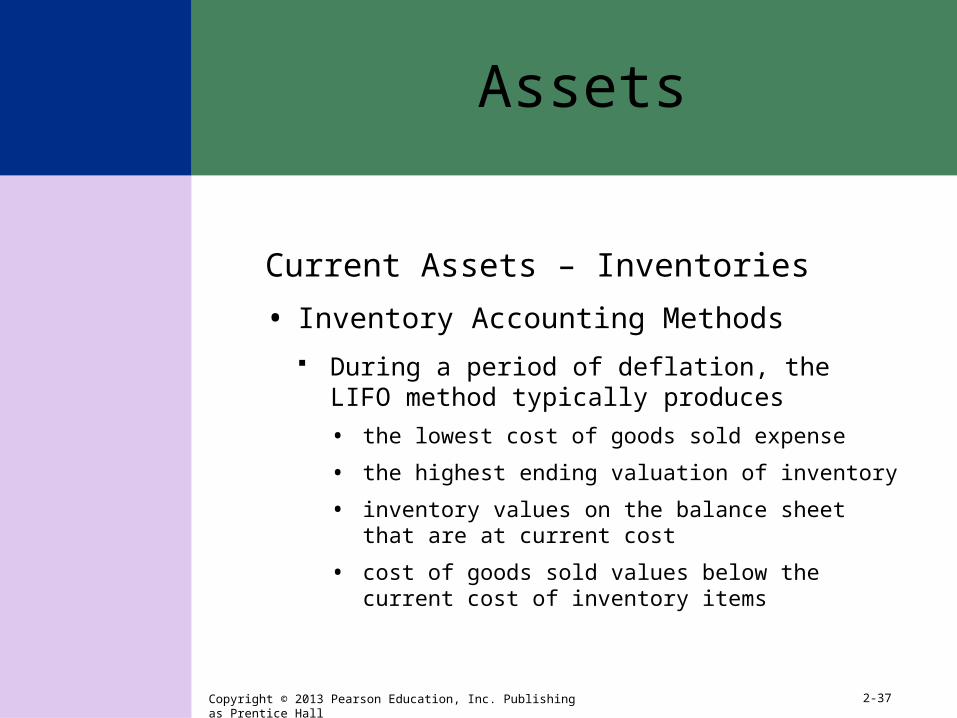

Assets

Current Assets – Inventories

• Inventory Accounting Methods During a period of deflation, the LIFO

method typically produces

• the lowest cost of goods sold expense

• the highest ending valuation of inventory

• inventory values on the balance sheet that are at current cost

• cost of goods sold values below the current cost of inventory items

2-37

Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall

Assets

Current Assets – Prepaid Expenses

• Expenses paid in advance Insurance

Rent

Property taxes

Utilities

• Included in current assets if they expire within one year or one operating cycle

• Generally not material to the balance sheet

2-38

Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall

Assets

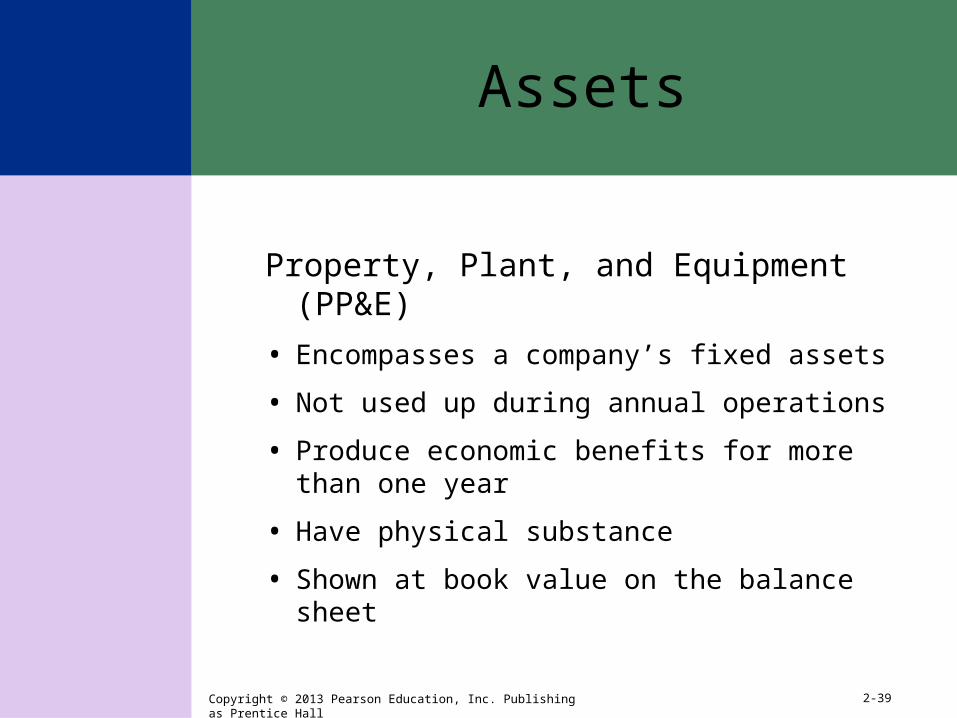

Property, Plant, and Equipment (PP&E)

• Encompasses a company’s fixed assets

• Not used up during annual operations

• Produce economic benefits for more than one year

• Have physical substance

• Shown at book value on the balance sheet

2-39

Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall

Assets

Property, Plant, and Equipment (PP&E)

• The relative proportion of fixed assets in a company’s asset structure will largely be determined by the nature of the business.

• Manufacturing firms typically have higher percentages of fixed assets than retailers or wholesalers.

• Firms with newly purchased assets will have higher percentages of fixed assets than firms with older fixed assets.

2-40

Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall

Assets

2-41

Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall

Assets

Property, Plant, and Equipment

• Land

• Buildings

• Leasehold improvements

• Construction in progress

• Equipment

2-42

Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall

Assets

PP&E – Land

• Property used in business

• Not investment property

2-43

Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall

Assets

PP&E – Buildings

• Buildings owned by the company Stores

Corporate offices

2-44

Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall

Assets

PP&E – Leasehold Investments

• Additions made to leased structures

• Improvements made to leased structures

• Revert to the property owner when the lease expires

• Amortized by the lessee over the economic life of the improvement (or the life of the lease)

2-45

Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall

Assets

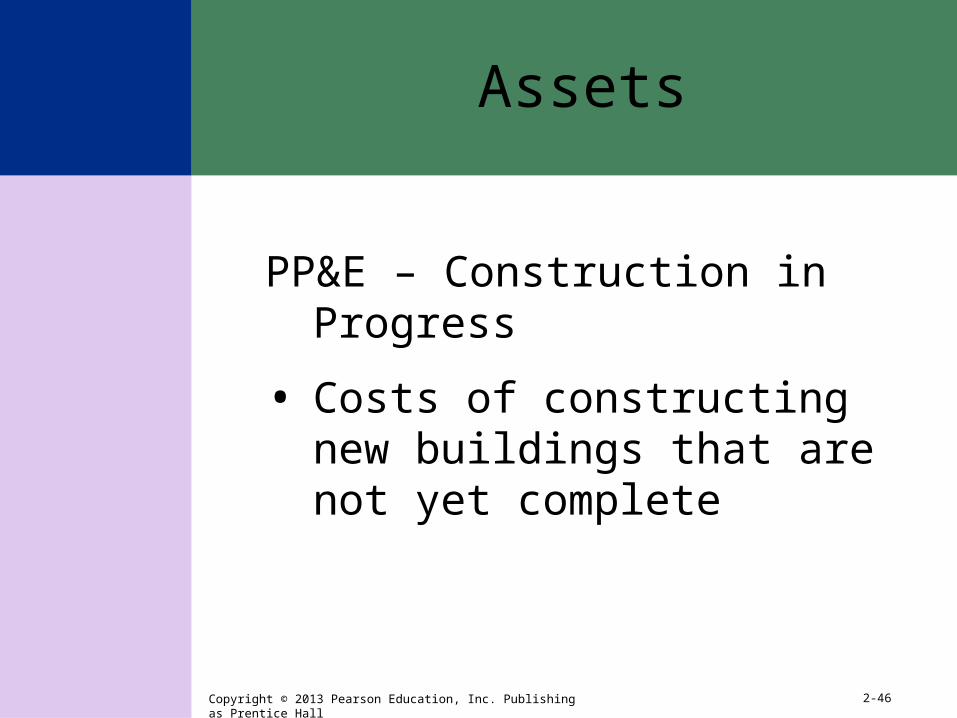

PP&E – Construction in Progress

• Costs of constructing new buildings that are not yet complete

2-46

Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall

Assets

PP&E – Equipment

• Original cost of machinery and equipment used in business operations

2-47

Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall

Assets

PP&E – Depreciation

• Fixed assets (with the exception of land) are depreciated over the period of time they benefit the firm.

• Method of allocating the cost of long-lived assets

• Original cost less estimated residual value is spread over the asset’s expected life.

2-48

Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall

Assets

PP&E – Depreciation Methods

• Straight-line method allocated an equal amount of expense to each year of the depreciation period.

• Accelerated methods apportions larger amounts of expense to earlier years of the asset’s depreciable life.

• Units-of-production method bases depreciation expense on actual use.

2-49

Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall

Assets

Example – Assume that Sage Inc. purchases an artificial ski mountain for its Phoenix flagship store in order to demonstrate skis and allow prospective customers to test-run skis on a simulated course. The cost of the mountain is $50,000 and is expected to have a five-year useful life and $0 salvage value at the end of that period.

2-50

Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall

Assets

2-51

Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall

Assets

2-52

Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall

Assets

Goodwill

• Arises when one company acquires another company for a price in excess of the fair market value of the net identifiable assets acquired

• Evaluated annually If no loss of value has occurred, goodwill

remains on the balance sheet.

If the book value exceeds the fair value, the excess must be written off as an impairment expense

2-53

Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall

Assets

Other Assets

• Can include a multitude of other noncurrent items Property held for sale

Start-up costs associated with a new business

Cash surrender value of life insurance policies

Long-term advance payments

Intangible assets (other than goodwill)

2-54

Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall

Liabilities

• Represent claims against assets

• Current liabilities Must be satisfied in one year or

one operating cycle

• Noncurrent liabilities Obligations with maturities

beyond one year

2-55

Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall

Liabilities

2-56

Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall

Liabilities

Current Liabilities

• Accounts payable

• Notes payable

• Current portion of long-term debt

• Accrued liabilities

• Unearned revenue

2-57

Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall

Liabilities

Current Liabilities – Accounts Payable

• Short-term obligations that arise from credit extended by suppliers for the purchase of goods and services

• Eliminated when the bill is satisfied

• Increase and decrease depending on credit policies, economic conditions, and cyclical nature of operations

2-58

Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall

Liabilities

Current Liabilities – Notes Payable

• Also referred to as short-term debt

• Short-term obligations in the form of promissory notes

• Lines of credit to suppliers or financial institutions

2-59

Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall

Liabilities

Current Liabilities – Current Maturities of Long-term Debt

• Portion of the principal of long-term debt that will be repaid during the upcoming year

2-60

Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall

Liabilities

Current Liabilities – Accrued Liabilities

• Result from recognition of an expense prior to actual payment of cash

• Reserve accounts Set up for the purpose of estimating

obligations for items such as warranty costs, sales returns, or restructuring charges

Identified in the notes to the financial statements

2-61

Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall

Liabilities

Current Liabilities – Accrued Liabilities

Example – Assume that a company has a $100,000 note outstanding with 12% interest due in semiannual installments on March 31 and September 30. For a balance sheet prepared on December 31, interest will be accrued for three months (October, November, and December). The December 31 balance sheet would include an accrued liability of $3,000:

$10,000 x 0.12 = $12,000 annual interest$12,000/12 = $1,000 monthly interest$1,000 x 3 = $3,000 accrued interest for three months

2-62

Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall

Liabilities

Current Liabilities – Unearned Revenue

• Also called deferred credits

• Result from payments received in advance for services and products

• Transferred to a revenue account when the service is performed or the product is delivered

2-63

Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall

Liabilities

Deferred Taxes

• Result of temporary differences in the recognition of revenue and expense for taxable income relative to reported income

• Depreciation methods are the most common source for temporary differences.

2-64

Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall

Liabilities

Deferred Taxes

• Other temporary differences arise from methods used to account for Installment sales

Long-term contracts and leases

Warranties and service contracts

Pensions and other employee benefits

Subsidiary investment earnings

2-65

Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall

Liabilities

Deferred Taxes

• Permanent differences in income tax accounting do not affect deferred taxes. Municipal bond revenue

Life insurance premiums

2-66

Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall

Liabilities

Deferred Taxes

• Valuation allowance Used to reduce deferred tax

assets to expected realizable amounts

Used when it is more likely than not that some of the deferred tax assets will not be realized

2-67

Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall

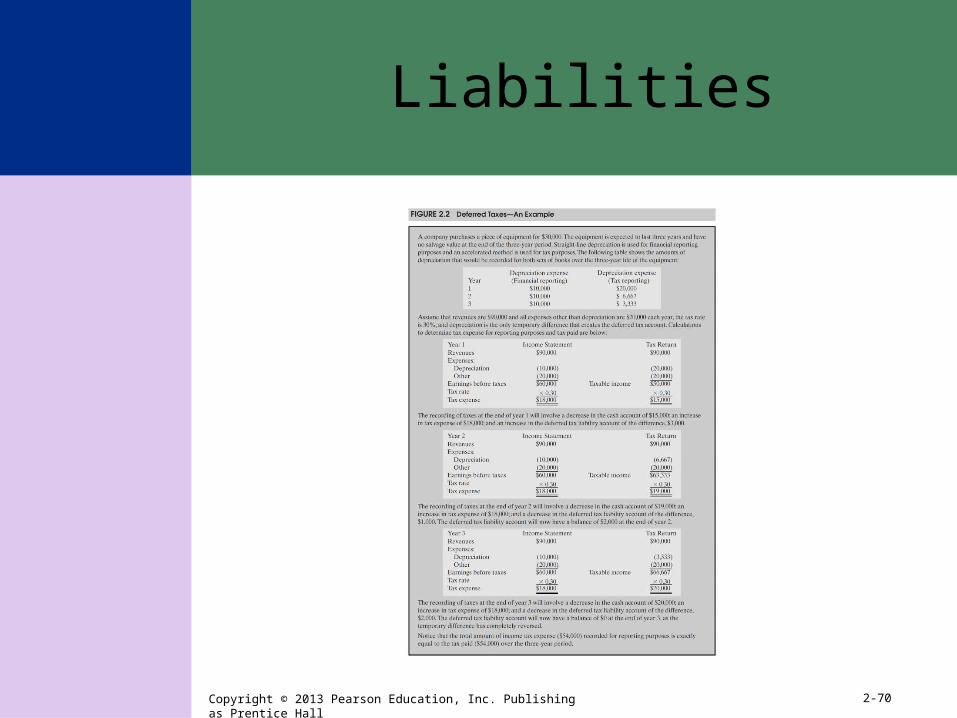

Liabilities

Example – Assume that a company has a total annual revenue of $500,000, expenses other than depreciation of $250,000, and a depreciation expense of $100,000 for tax accounting and $50,000 for financial reporting. The income for tax reporting purposes would be computed two ways, assuming a 34% tax rate:

2-68

Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall

Liabilities

Taxes actually paid ($51,000) are less than the tax expense ($68,000) reported in the financial statements. To reconcile the $17,000 difference between the expense recorded and the cash outflow, there is a deferred tax liability of $17,000:

2-69

Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall

Liabilities

2-70

Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall

Liabilities

Deferred Taxes

• Deferred taxes are not always classified as current liabilities.

• They may also appear on the balance sheet as a current asset

noncurrent asset

noncurrent liability

2-71

Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall

Liabilities

Noncurrent Liabilities

• Long-term debt

• Capital lease obligations

• Postretirement benefits other than pensions

• Commitments and contingencies

• Hybrid securities

2-72

Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall

Liabilities

Noncurrent Liabilities – Long-term Debt

• Bonds

• Long-term notes payable

• Mortgages

• Obligations under leases

• Pension liabilities

• Long-term warranties

2-73

Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall

Liabilities

Noncurrent Liabilities – Capital Lease Obligations

• Are, in substance, a “purchase” rather than a “lease”

• Affect both balance sheet and income statement

• Disclosures found in the notes, often under both the PP&E note and the commitments and contingencies note

2-74

Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall

Liabilities

Noncurrent Liabilities – Pensions and Postretirement Benefits

• Pensions are cash compensation paid to retired employees.

• Postretirement benefits are benefits other than pensions that employers promise to pay for retired employees.

• Can appear under the liability section of the balance sheet

2-75

Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall

Liabilities

Noncurrent Liabilities – Commitments and Contingencies

• Commitments refer to contractual agreements that will have a significant financial impact in the future.

• Contingencies refer to potential liabilities (such as possible damage awards assessed in lawsuits).

• Intended to draw attention to the fact that required disclosures can be found in the notes to the financial statements.

2-76

Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall

Liabilities

Noncurrent Liabilities – Hybrid Securities

• Have the characteristics of both debt and equity

• Also called mandatorily redeemable preferred stock

• Financial instrument is preferred stock, but the issuing company must retire the shares at a future date.

2-77

Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall

Stockholders’ Equity

• Also called shareholders’ equity

• Residual interest in assets that remains after deducting liabilities

• Owners bear greatest risk and benefit from greatest rewards.

2-78

Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall

Stockholders’ Equity

Common Stock

• Shareholders do not ordinarily receive a fixed return

have voting privileges in proportion to ownership interest

can benefit through price appreciation

can suffer through price depreciation

2-79

Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall

Stockholders’ Equity

Common Stock

• Dividends are declared at the discretion of a company’s board of directors

• Amount listed on the balance sheet is based on the par or stated value of the shares issued (which bears no relationship to actual market price).

2-80

Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall

Stockholders’ Equity

Additional Paid-In Capital

• Reflects the amount by which the original sales price of the stock shares exceeded par value

2-81

Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall

Stockholders’ Equity

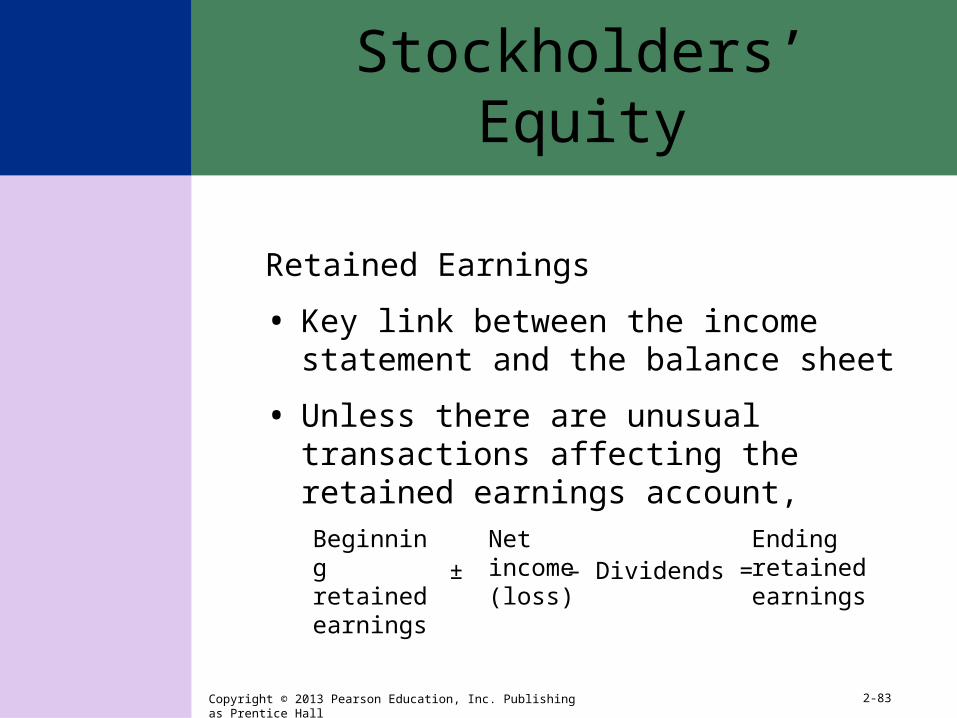

Retained Earnings

• Sum of every dollar a company has earned since inception less any payments made to shareholders

• Funds a company has elected to reinvest in the operations of the business rather than pay out in stock

• Measurement of all undistributed earnings

2-82

Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall

Stockholders’ Equity

Retained Earnings

• Key link between the income statement and the balance sheet

• Unless there are unusual transactions affecting the retained earnings account,Beginning retained earnings

Net income (loss)

Ending retained earnings

– Dividends =±

2-83

Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall

Stockholders’ Equity

Other Equity Accounts

• Preferred stock

• Accumulated other comprehensive income (expense)

• Treasury Stock

• Employee benefit trusts

• Equity attributable to noncontrolling interests

2-84

Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall

Stockholders’ Equity

2-85

Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall

Stockholders’ Equity

Other Equity Accounts – Preferred Stock

• Carries a fixed annual dividend payment

• Carries no voting rights

2-86

Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall

Stockholders’ Equity

Other Equity Accounts – Accumulated Other Comprehensive Income (Expense)

• Unrealized gains or losses in the market value of investments in available-for-sale securities

• Any change in the excess of additional pension liability over unrecognized prior service cost

• Certain gains and losses on derivative financial instruments

• Foreign currency translation adjustments resulting from converting financial statements from a foreign currency into U.S. dollars

2-87

Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall

Stockholders’ Equity

Other Equity Accounts – Treasury Stock

• Repurchased shares of stock that are not retired

• Shown as an offsetting account

2-88

Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall

Stockholders’ Equity

Other Equity Accounts – Equity Attributable to Noncontrolling Interests

• Represents the equity interest a firm has in companies whose financial statement have been consolidated with the firm’s statements but that are not 100% owned by the firm

2-89

Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall

Quality of Financial Reporting

• Economic recession of 2008 and many market gyrations since can be traced directly to overvaluation of balance sheet assets.

• When financial reporting does not reflect economic reality quality and usefulness are significantly impaired.

• Type of debt used to finance assets, commitments and contingencies, and the classification of leases relate directly to quality of financial reporting.

2-90

Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall

Quality of Financial Reporting

• “Commitments and Contingencies” disclosure in the notes to financial statements provide important information about off-balance sheet financing and other complex financing arrangements.

• Enron is a prime example of a company with enormous activity reported in the “Commitments and Contingencies” disclosure.

2-91

Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall

Other Balance Sheet Items

• Corporate balance sheets are not limited to the accounts described in this chapter.

• The reader of annual reports will encounter additional accounts and will find many of the same accounts listed under different titles.

2-92

Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall

Copyright Notice

All rights reserved. No part of this publication may be reproduced, stored in a retrieval system, or transmitted, in any form or by any means, electronic, mechanical, photocopying, recording, or otherwise, without the prior written permission of the publisher. Printed in the United States of America.

2-93