chapter 28: monetary policy and the debate about macro policy · web view4.there are few regional...

TRANSCRIPT

CHAPTER 11: MONETARY POLICY

Questions and Exercises

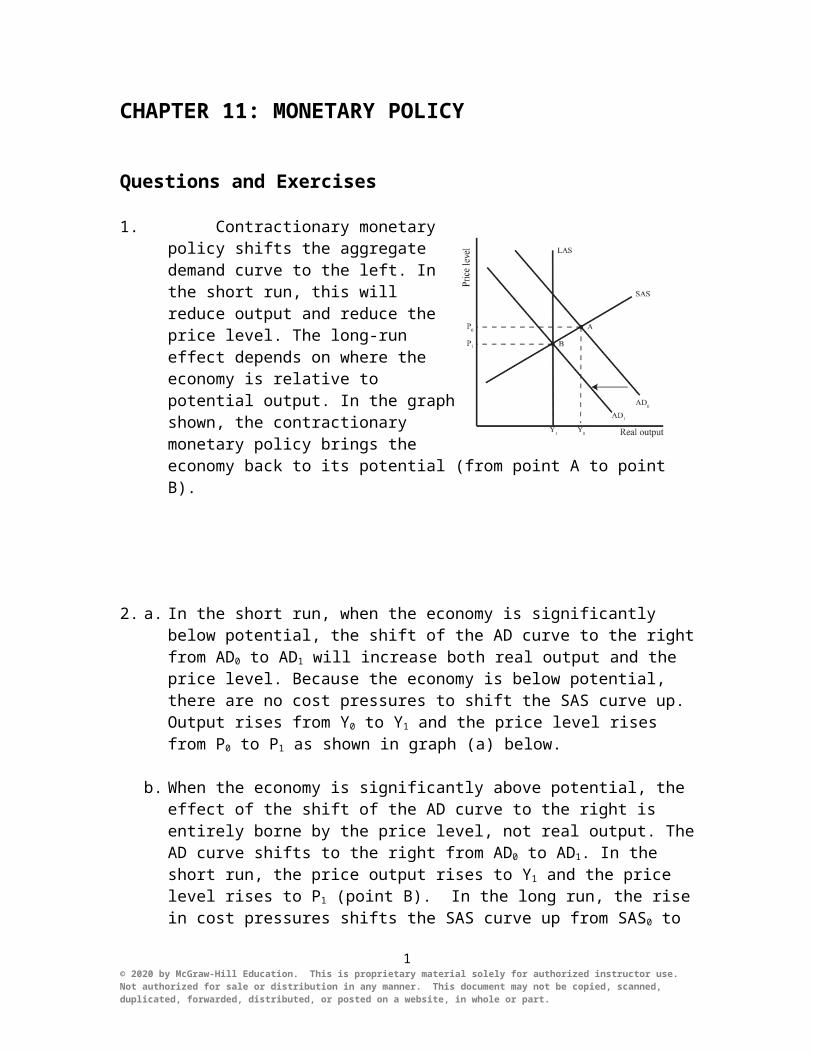

1. Contractionary monetary policy shifts the aggregate demand curve to the left. In the short run, this will reduce output and reduce the price level. The long-run effect depends on where the economy is relative to potential output. In the graph shown, the contractionary monetary policy brings the economy back to its potential (from point A to point B).

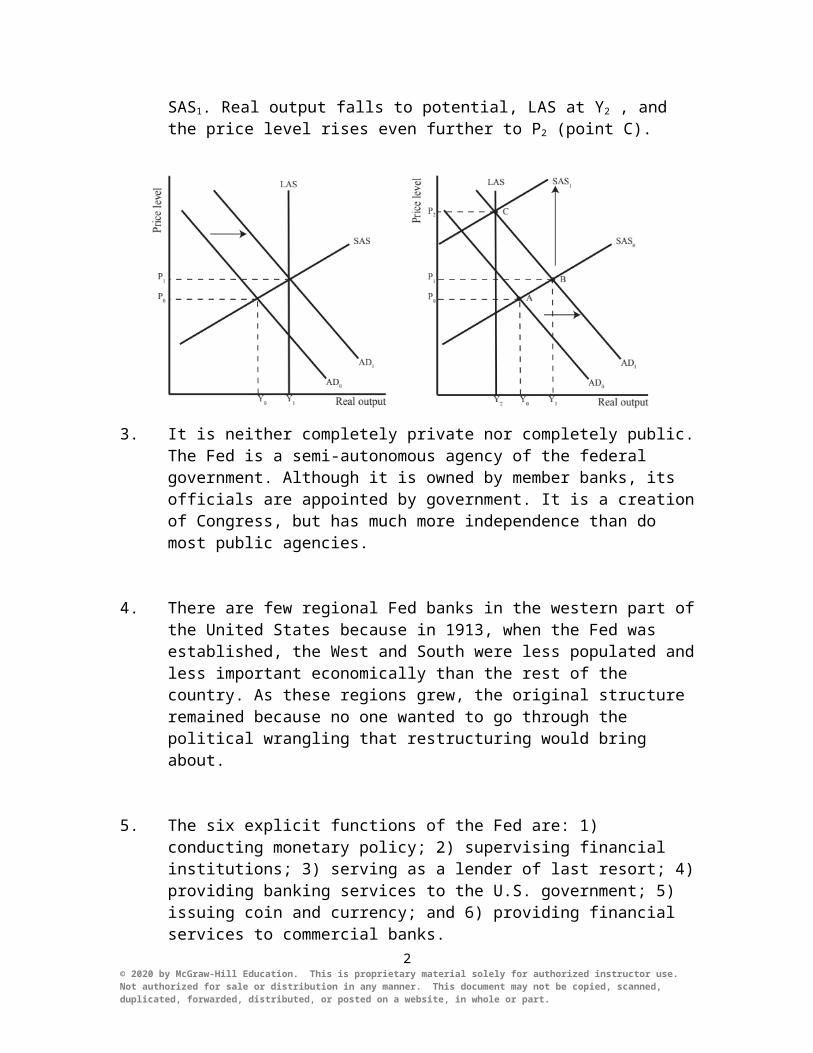

2. a. In the short run, when the economy is significantly below potential, the shift of the AD curve to the right from AD0 to AD1 will increase both real output and the price level. Because the economy is below potential, there are no cost pressures to shift the SAS curve up. Output rises from Y0 to Y1 and the price level rises from P0 to P1 as shown in graph (a) below.

b. When the economy is significantly above potential, the effect of the shift of the AD curve to the right is entirely borne by the price level, not real output. The AD curve shifts to the right from AD0 to AD1. In the short run, the price output rises to Y1 and the price level rises to P1 (point B). In the long run, the rise in cost pressures shifts the SAS curve up from SAS0 to SAS1. Real output falls to potential, LAS at Y2 , and the price level rises even further to P2 (point C).

1© 2020 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole or part.

3. It is neither completely private nor completely public. The Fed is a semi-autonomous agency of the federal government. Although it is owned by member banks, its officials are appointed by government. It is a creation of Congress, but has much more independence than do most public agencies.

4. There are few regional Fed banks in the western part of the United States because in 1913, when the Fed was established, the West and South were less populated and less important economically than the rest of the country. As these regions grew, the original structure remained because no one wanted to go through the political wrangling that restructuring would bring about.

5. The six explicit functions of the Fed are: 1) conducting monetary policy; 2) supervising financial institutions; 3) serving as a lender of last resort; 4) providing banking services to the U.S. government; 5) issuing coin and currency; and 6) providing financial services to commercial banks.

6. The Fed buys and sells bonds to increase and decrease the amount of reserves banks have on hand. When the Fed buys bonds, banks have more reserves and then are able to lend more. As they lend more, the money supply increases.

7. The money multiplier is 1/r. If the Fed eliminated the reserve requirement, the money multiplier would increase and, without other Fed action, the supply of money would also increase.

8. If the Fed raises the interest rate paid on reserves, banks will hold more reserves, leading to a decline in the money supply. If the Fed lowers the interest paid on reserves, banks will hold less reserves, leading to an increase in the money supply.

9. An economy is in a liquidity trap when banks do not lend increases in reserves added by the Fed, instead choosing to keep them as excess.

10. Banks can also borrow reserves from the Fed at the discount window. The rate banks pay to borrow reserves from the Fed is called the discount rate.

11. The Federal funds rate is the interest rate that banks charge one another for Fed funds or reserves.

2© 2020 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole or part.

12. You would expect it to fall since the Fed’s actions of buying bonds would increase the money supply by making more reserves available to banks and the greater economy.

13. Defensive policies are simply changes to offset fluctuations in the demand for money. Therefore, a change in the direction of monetary policy would be an offensive action.

14. Because the current money multiplier is 10 (1/0.1), the Fed would buy $300,000 ($3,000,000/10) worth of bonds, increasing the monetary base, and in turn, increasing the money supply by $3 million.

15. a. The money multiplier would be 1.

b. The money supply would decrease enormously.

c. This could be offset by the Federal government buying up Treasury bills, directlyincreasing the money supply, or by the Federal government making loans toindividuals and businesses.

16. a. The money multiplier is 1/r. If this is equal to 4, then the current reserve requirement is 25 percent. Given that the money supply is currently $5,000, banks have $1,250 in reserves. For this amount of reserves to support a money supply of $5,350, the money multiplier has to be 4.28 ($5,350/$1,250), which means the reserve requirement must be lowered to .23 percent (1/4.28 = 0.234).

b. Lowering the discount rate will encourage banks to borrow. This will increase the amount of reserves in the system so that the money supply increases. If the Fedwishes to increase the money supply by $350, and the multiplier is 4, reservesmust be increased by $87.50. If banks will borrow an additional $10 for everypoint the discount rate is lowered, the Fed should lower the rate by 8.75percentage points.

c. To increase the money supply by using open market operations, the Fed shouldbuy bonds, thus increasing the level of reserves in the banking system. To achievean increase of $350 (if the multiplier is 4) the Fed should buy $87.50 ($350/4) worth of bonds.

17. To increase income by $240, investment should increase by $80 (the income multiplier is 3). Increasing investment by $80 requires decreasing the interest rate by 4 percentage points (investment increases by $20 for every 1 percentage point

3© 2020 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole or part.

drop in interest). To change the interest rate by 4 percentage points requires a change of $20 in the money supply (each change of $5 in the money supply changes the interest rate by 1 percent). Since the money multiplier is 4, the monetary base should increase by $5. Thus, the recommended policy is an open market purchase that would increase the monetary base by $5.

18. a. Since the money multiplier is 5 (1/.2), the Fed must increase reserves. You would tell the Fed open market desk to buy $10 (50/5) worth of bonds.

b. We could have also reduced the discount rate and lowered the reserverequirement, although by how much cannot be determined with the informationgiven.

c. Using the AS/AD model, the effect of increasing the money supply in the short run would be to increase real output and the price level. In the long run, the effectdepends on where the economy is relative to potential. If the policy brought theeconomy to its potential, real output and the price level would not change anyfurther. If the policy brought the economy to a level above potential, real outputwould return to its original level before the policy was implemented and the pricelevel would rise even further.

19. The tools of monetary policy are those things over which the Fed has direct controlsuch as the open market operations. These tools have a direct effect on operatingtargets such as the Fed funds rate. These operating targets, in turn will affectintermediate targets such as consumer confidence. It is these intermediate targetsthat then impact the Fed’s ultimate targets—prices, growth and employment.Because the Fed cannot directly control its ultimate targets, the Fed must rely onadjusting its tools to try to achieve its ultimate targets.

20. Fed tools include open market operations, the discount rate, and the reserve requirement. (Note: the Fed now pays interest on reserves, which the Fed has yet to utilize. Therefore the answer need not include this tool.) The operating target is the Fed funds rate. The ultimate targets are stable prices, sustainable growth, acceptable employment, and moderate long-term interest rates.

21. In Year 2, the Fed engaged in slightly contractionary policy, but for the remaining years, it engaged in expansionary policy as the Fed funds target rate dropped.

22. The Taylor rule [2 percent + Current inflation + 1/2(Current inflation – Inflation target) + 1/2(percent output deviates from potential output)] suggests that the Fed will target a Fed funds rate of 5.5 percent [2 + 3 + .5(1) + .5(0)].

4© 2020 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole or part.

23. The Taylor rule is that the Fed funds target is 2 percent + Current inflation + 1/2(Current inflation – inflation target) + 1/2(percent output deviates from potential output).

a. Fed funds rate target will be 2.5 percent [2 + 2 + .5 (-1) + .5(-2)].

b. Fed funds rate target will be 8.5 percent [2 + 4 + .5 (2) + .5 (3)].

c. Fed funds rate target will be 5.5 percent [2 + 4 + .5(1) + .5 (-2)].

24. An inverted yield curve occurs when long-term bonds pay a lower interest rate than short-term bonds.

25. You are more likely to see an inverted yield curve when the Fed is contracting the money supply. The inverted yield curve indicates that the Fed's conventional monetary policy will not have any significant effect on investment or the economy.

26. Policy makers pay attention to the shape of the yield curve because it will tell them whether their policies are likely to be effective. Specifically, an inverted yield curve means that policies to lower the interest rate will not result in increased investment.

27. Expectations definitely matter to policy makers, because expectations will alter people’s responses to policy actions. If the Fed follows expansionary monetary policy to spur the economy, and the result is raised expectations of inflation, the Fed might end up with higher, not lower, long-term interest rates.

28. Real interest rate Nominal interest rate Expected inflationa. 5 7 2b. -1 3 4c. 3 6 3d. 4 5 1

Real interest rate = Nominal interest rate – Expected inflation

29. A monetary regime is a predetermined statement about what policies will be followed in various situations. It ties the hands of policy makers and is meant to change the way people form their expectations. A policy is a one-time action that does not require a particular course of future actions.

5© 2020 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole or part.

30. An inflation target policy might make the Fed pursue a contractionary monetary policy when only temporary factors raise inflation, whereas it might have been better to wait until the temporary factors disappeared instead of slowing the economy.

31. With transparency, the Fed tells the people what it is doing and then the people see that in fact, the Fed does what it says it will. This adds credibility to Fed policy.

Questions from Alternative Perspectives

1. AustrianHis argument was that financial institutions can create an almost infinite number of effective substitutes for money, which undermines the ability of the Fed to control the economy with monetary policy.

2. Feminista. Some feminists would argue that an almost exclusive focus on men in prominent

quotations perpetuates male bias in the economics profession. It ignores the contributions of women economists and political economists such as Mary Wollstonecraft, Charlotte Perkins Gilman, Joan Robinson, Marianne Ferber, Barbara Bergmann, and Heidi Hartmann among many more.

b. This is a judgment question and judgments differ. Most feminists believe that we

should be concerned.

3. Institutionalista. When interest rates are very low, it is unlikely that they will go any lower, which

makes people worried about holding long-term bonds, since the value of a fixed interest rate bond falls when interest rates rise, and they want to avoid that capital loss. Thus, they prefer to hold money even though it pays no interest.

b. One possibility is to change the nature of money, making it lose value. There were such proposals put forward during the Great Depression. Another possibility would be for monetary policy to be directed to foreign exchange, and not on local bonds. By lowering the price of the country’s currency, such a policy could stimulate the economy.

4. Post-KeynesianIf it were accepted that money were non-neutral, then there would be less focus on using monetary policy only to fight inflation and more consideration of using monetary policy to expand the economy.

6© 2020 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole or part.

5. Radicala. This is a judgment question and judgments differ. Radical economists believe that

the Fed’s conduct of monetary policy helps the rich bondholders more than it helps the poor.

b. This is a judgment question and judgments differ. Radical economists believe that the Fed should serve the interests of the entire society, with special focus on low-income individuals.

Issues to Ponder

1. If we consider the example of an open market sale by the Fed, the initial transaction or "splash" would be the Fed sells a bond, and in exchange a person writes a check to the Fed, which the Fed presents to the person's bank for payment. The bank now must adjust to this change, and the "ripples" will show up on its balance sheet. Paying cash to the Fed means that the bank's reserves are too low, and the bank must figure out a way to meet its reserve requirement. It may call in loans to do so, but that in turn could mean that someone paid the loan from a checking account, which has further balance sheet implications. Now that the bank wants to make fewer loans, it will increase its interest rates, which will discourage investment and have further ripple effects on the economy.

2. When the Fed takes money out of the economy, banks are in violation of Fed regulations and have no choice but to contract their loans in order to meet their reserve requirements. When the Fed puts money into the economy, banks have excess reserves, but there is no regulation that they are violating because they are covering required reserves. Although they may have a financial incentive to make loans, they are not required to do so. Similarly, consumers are not required to borrow. Since banks are not required to make loans, and thus will not necessarily reduce interest rates, the saying “You can lead a horse to water, but you can’t make it drink” is relevant.

3. a. This would increase excess reserves enormously.

b. Banks would most likely favor this proposal, because they would now earn interest on their assets held at the Fed.

c. Central banks would likely oppose this because it would reduce their superiority to other political institutions and may require that they ask Congress for appropriations to pay the interest, reducing their political independence.

d. This would be expected to increase the interest rate paid by banks because the additional interest would increase their profit margin. The initial increased profit margin would shift the demand for depositors out as new banks entered the

7© 2020 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole or part.

market and as existing banks competed for more deposits. This would increase the interest paid to depositors until the normal profits are once again earned.

4. Treasury bills pay interest; cash does not.

5. a. This Act will reduce float because money will be transferred almost immediately from bank to bank.

b. Because checks will be less likely to be transferred by truck or air, weather will be less likely to affect the level of float, so its variability will decline, unless computer glitches arise.

c. If the variability of float declines, so will the level of defensive Fed actions designed to offset this variability.

8© 2020 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole or part.