chapter 6: support department cost allocationhcbus003/acct380solutions/chapter06.doc · web...

TRANSCRIPT

CHAPTER 6SUPPORT DEPARTMENT COST ALLOCATION

QUESTIONS FOR WRITING AND DISCUSSION

1. Stage one assigns service costs to produc-ing departments. Costs are assigned using factors that reflect the consumption of the services by each producing department. Stage two allocates the costs assigned to the producing departments (including ser-vice costs and direct costs) to the products passing through the producing departments.

2. Service costs are part of the cost of produc-ing a product. Knowing the individual prod-uct costs is helpful for developing bids and cost-plus prices.

3. GAAP requires that all manufacturing costs be assigned to products for inventory valua-tion.

4. Allocation of service costs makes users pay attention to the level of service activity being consumed and also provides an incentive for them to monitor the efficiency of the service departments.

5. Without any allocation of service costs, users may view services as a free good and consume more of the service than is opti-mal. Allocating service costs would encour-age managers to use the service until such time as the marginal cost of the service is equal to the marginal benefit.

6. Since the user departments are charged for the services provided, they will monitor the performance of the service department. If the service can be obtained more cheaply externally, then the user departments will be likely to point this out to management. Knowing this, a manager of a service de-partment will exert effort to maintain a com-petitive level of service.

7. The identification and use of causal factors ensures that service costs are accurately assigned to users. This increases the legiti-macy of the control function and enhances product-costing accuracy.

8. Allocating actual costs passes on the effi-ciencies or inefficiencies of the service de-partment, something which the manager of the producing department cannot control. Al-locating budgeted costs avoids this problem.

9. Variable costs should be allocated according to usage, whereas fixed costs should be al-located according to capacity. Variable costs are based on usage because, as a depart-ment’s usage of a service increases, the variable costs of the service department in-crease. A service department’s capacity and the associated fixed costs were originally set by the user departments’ capacities to use the service. Thus, each department should receive its share of fixed costs as originally conceived (to do otherwise allows one de-partment’s performance to affect the amount of cost assigned to another department).

10. Normal or peak capacity measures the origi-nal capacity requirements of each producing department. It is used when one depart-ment’s spike in usage affects the amount of capacity needed.

11. Using variable bases to allocate fixed costs allows one department’s performance to af-fect the costs allocated to other depart-ments. Variable bases also fail to reflect the original consumption levels that essentially caused the level of fixed costs.

12. The dual-rate method separates the fixed and variable costs of providing services and charges them separately. In effect, a single rate treats all service costs as variable. This can give faulty signals regarding the mar-ginal cost of the service. If all costs of the service department were variable, there would be no need for a dual rate. In addi-tion, if original capacity equaled actual us-age, the dual-rate method and the single-rate method would give the same allocation.

13. The direct method allocates the direct costs of each service department directly to the producing departments. No consideration is given to the fact that other service centers may use services. The sequential method allocates service costs sequentially. First, the costs of the center providing the great-est service are allocated to all user depart-ments, including other service departments. Next, the costs of the second greatest

181181

provider of services are allocated to all user departments, excluding any department(s) that have already allocated costs. This con-tinues until all service center costs have been allocated. The principal difference in the two methods is the fact that the sequen-

tial method considers some interactions among service centers, and the direct method ignores interactions.

14. Agree. The reciprocal method is more accu-rate because it fully considers interactions among service centers.

182182

EXERCISES

6–1

a. producingb. supportc. supportd. supporte. support

f. producingg. producing/supporth. producingi. producingj. support

k. supportl. supportm. producingn. producingo. support

6–2

a. supportb. supportc. producingd. producing

e. producingf. supportg. supporth. producing

i. producingj. support

6–3

a. Number of employeesb. Square footagec. Pounds of laundryd. Orders processede. Maintenance hours workedf. Number of employeesg. Number of transactions processedh. Machine hoursi. Square footage

183183

6–4

1. Dr. Poston may want to cost the cleanser for several reasons: to value inven-tory; to determine profitability; and to plan sales and costs for the coming year. As long as he sells relatively few bottles of cleanser, it is not necessary to allocate any indirect costs to the cleanser. The medical assistant is paid the same amount whether she mixes the cleanser or not. The space used to store the cleanser materials is small, and the incremental cost is zero.

2. The situation has changed dramatically. Now, the cleanser should be allo-cated some of the office rent as well as all of the new assistant’s salary. The office rent could be apportioned 75 percent to the three doctors and 25 per-cent to the cleanser bottling operation given that the cleanser operation takes an office and an examining room. It could be argued that this over-states the allocation to the cleanser, since the waiting room area does not serve the cleanser. However, the receptionist probably takes calls and opens mail for this project, so overstating the rent may be an easy way to adjust for this. The cost per bottle would then be:

Materials $0.50Labor ($12,000/40,000) 0.30Office rent* 0.38

Total cost $1.18*Office rent allocation = [($5,000 12)/4]/40,000 bottles

6–5

1. The incremental method of allocating the cost of the trip would result in a cost to LaTisha of $125 ($10 times five nights for the rollaway and $75 for her food).

2. The benefits-received approach could result in the following cost allocation to LaTisha:

Motel ($425/3) $141.67Food 75.00Gas ($50/3) 16.67

Total $233.34The treatment of the motel cost is problematical. This computation adds the rollaway cost for five nights to the cost of the double room for five nights. However, if LaTisha spends the entire time on a (less comfortable) rollaway, she may be less than pleased. Perhaps the vacationers could trade off sleep-ing on the rollaway.

184184

6–6

1. Single charging rate = ($2,500/1,000) + $0.50= $3 per gift

Number Charging Store of Gifts Rate = Total Candles, Etc. 170 $3 $ 510Dream Weaver Gift Shoppe 310 3 930Back-in-the-Saddle Westernwear 240 3 720Cuppa Java Gourmet Coffees 10 3 30Shoe You 50 3 150Dana’s Sportswear 200 3 600Penelope’s Secret 450 3 1,350

Total 1,430 $4,290

2. Number Allocated Store of Gifts Percent Fixed Amount*Candles, Etc. 200 20 $ 500Dream Weaver Gift Shoppe 300 30 750Back-in-the-Saddle Westernwear 100 10 250Cuppa Java Gourmet Coffees 70 7 175Shoe You 50 5 125Dana’s Sportswear 130 13 325Penelope’s Secret 150 15 375

Total 1,000 100 $2,500*Allocated fixed amount = Percent $2,500

Variable rate = $0.50 per gift

Number Variable Fixed Total Store of Gifts Amount + Amount = ChargeCandles, Etc. 170 $ 85 $ 500 $ 585Dream Weaver Gift Shoppe 310 155 750 905Westernwear Back-in-the-Saddle 240 120 250 370Cuppa Java Gourmet Coffees 10 5 175 180Shoe You 50 25 125 150Dana’s Sportswear 200 100 325 425Penelope’s Secret 450 225 375 600

Total 1,430 $715 $2,500 $3,215

185185

6–6 Concluded

3. The shops which actually use the gift-wrapping service less than anticipated would like the single charging rate. The single charging rate assigns less of the fixed cost to the shops using less of the service. Cuppa Java Gourmet Coffees originally anticipated having 70 gifts wrapped per month but actually had only 10 gifts wrapped. Under the single charging rate, Cuppa Java pays only $30; under the dual charging rate, Cuppa Java pays $180.

The dual charging rate method is preferred by shops which use the service as much as or more than anticipated. Penelope’s Secret had a much greater use for the service and would be charged $600 under the dual rate but $1,350 under the single rate.

4. Irrespective of the charging rate method, James may be overcharging by overestimating his fixed costs. The space used by the gift-wrapping service is one of five vacant spaces. The opportunity cost of using it to wrap gifts is zero. Until the eleventh space is rented and there is an occupant for the twelfth, perhaps the fixed cost should include only the salary of the wrapper.

6–7

1. Allocation ratios:Year 1 Year 2

Department A 0.40 0.50Department B 0.60 0.50

Allocation:Department A $48,000 $60,000Department B 72,000 60,000

2. The manager of Department B is not controlling maintenance costs better than the manager of Department A. The only reason that Department A’s allo-cation of maintenance cost increased is because Department B’s usage de-creased.

3. First, variable and fixed costs should be allocated separately. Second, bud-geted (not actual) costs should be allocated. Variable costs should be as-signed to the two user departments by multiplying the budgeted variable cost per hour by the actual hours or budgeted hours used, depending on whether the purpose is performance evaluation or product costing. Fixed costs would be assigned in proportion to the practical or normal activities of each user department.

186186

6–8

1. Product costing (Year 1 and Year 2 are identical):

Department A Department BVariable costs:

($0.25 20,000) $ 5,000($0.25 20,000) $ 5,000

Fixed costs:(0.50 $100,000) 50,000(0.50 $100,000) 50,000

Total cost $ 55,000 $ 55,000

2. Performance evaluation:

Year 1 Department A Department B

Variable costs:($0.25 24,000) $ 6,000($0.25 36,000) $ 9,000

Fixed costs:(0.50 $100,000) 50,000(0.50 $100,000) 50,000

Total cost $ 56,000 $ 59,000

Year 2 Department A Department B

Variable costs:($0.25 25,000) $ 6,250($0.25 25,000) $ 6,250

Fixed costs:(0.50 $100,000) 50,000(0.50 $100,000) 50,000

Total cost $ 56,250 $ 56,250

187187

6–9

1. Allocation ratios:

Traditional Gel Machine hours 0.2500 0.7500Square feet 0.6000 0.4000No. of employees 0.5625 0.4375

Cost assignment:

Power:(0.2500 $90,000) $ 22,500(0.7500 $90,000) $ 67,500

General Factory:(0.6000 $300,000) 180,000(0.4000 $300,000) 120,000

Personnel:(0.5625 $120,000) 67,500(0.4375 $120,000) 52,500

Direct costs 137,500 222,500 Total $407,500 $462,500

2. Departmental overhead rates:

Traditional: $407,500/8,000 = $50.94* per MHrGel: $462,500/24,000 = $19.27* per MHr*Rounded

188188

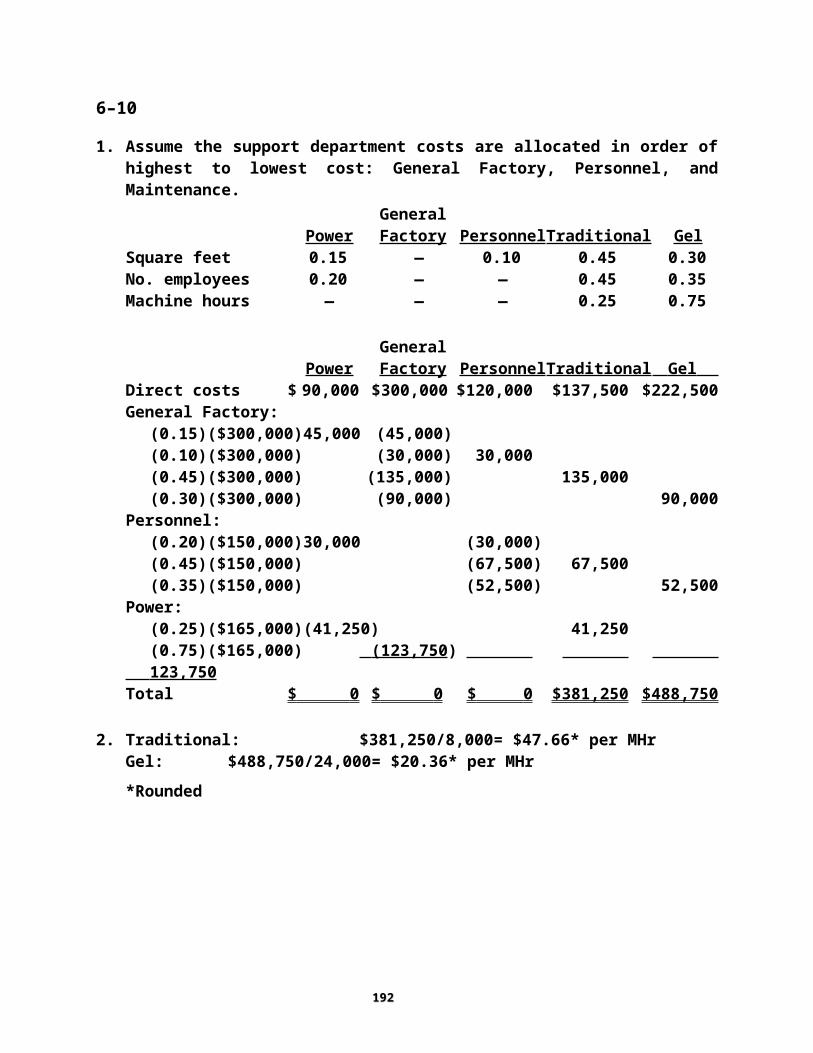

6–10

1. Assume the support department costs are allocated in order of highest to lowest cost: General Factory, Personnel, and Maintenance.

GeneralPower Factory Personnel Traditional Gel

Square feet 0.15 — 0.10 0.45 0.30No. employees 0.20 — — 0.45 0.35Machine hours — — — 0.25 0.75

GeneralPower Factory Personnel Traditional Gel

Direct costs $ 90,000 $ 300,000 $120,000 $137,500 $222,500General Factory:

(0.15)($300,000) 45,000 (45,000)(0.10)($300,000) (30,000) 30,000(0.45)($300,000) (135,000) 135,000(0.30)($300,000) (90,000) 90,000

Personnel:(0.20)($150,000) 30,000 (30,000)(0.45)($150,000) (67,500) 67,500(0.35)($150,000) (52,500) 52,500

Power:(0.25)($165,000) (41,250) 41,250(0.75)($165,000) (123,750 ) 123,750

Total $ 0 $ 0 $ 0 $381,250 $488,750

2. Traditional: $381,250/8,000 = $47.66* per MHrGel: $488,750/24,000 = $20.36* per MHr*Rounded

189189

6–11

1. Allocation:

Maintenance Personnel Assembly PaintingSquare footage — 0.20 0.40 0.40Number of employees 0.10 — 0.24 0.66

P = $60,000 + 0.2M M = $200,000 + 0.1PP = $60,000 + 0.2($200,000 + 0.1P) M = $200,000 + 0.1($102,041)P = $60,000 + $40,000 + 0.02P M = $200,000 + $10,204

0.98P = $100,000 M = $210,204P = $102,041

Allocate Allocate Total AfterDirect Cost Maintenance* Personnel** Allocation

Maintenance $200,000 $(210,204) $ 10,204 $ 0Personnel 60,000 42,041 (102,041) 0Assembly 43,000 84,082 24,489*** 151,571Painting 74,000 84,082 67,347 225,429

$377,000 $377,000*(0.20 $210,204) = $42,041 **(0.10 $102,041) = $10,204(0.40 $210,204) = $84,082 (0.24 $102,041) = $24,489(0.40 $210,204) = $84,082 (0.66 $102,041) = $67,347***Rounded down to balance.

2. Departmental overhead rates:

Assembly: $151,571/25,000 = $6.06*/DLHPainting: $225,429/40,000 = $5.64*/DLH*Rounded

190190

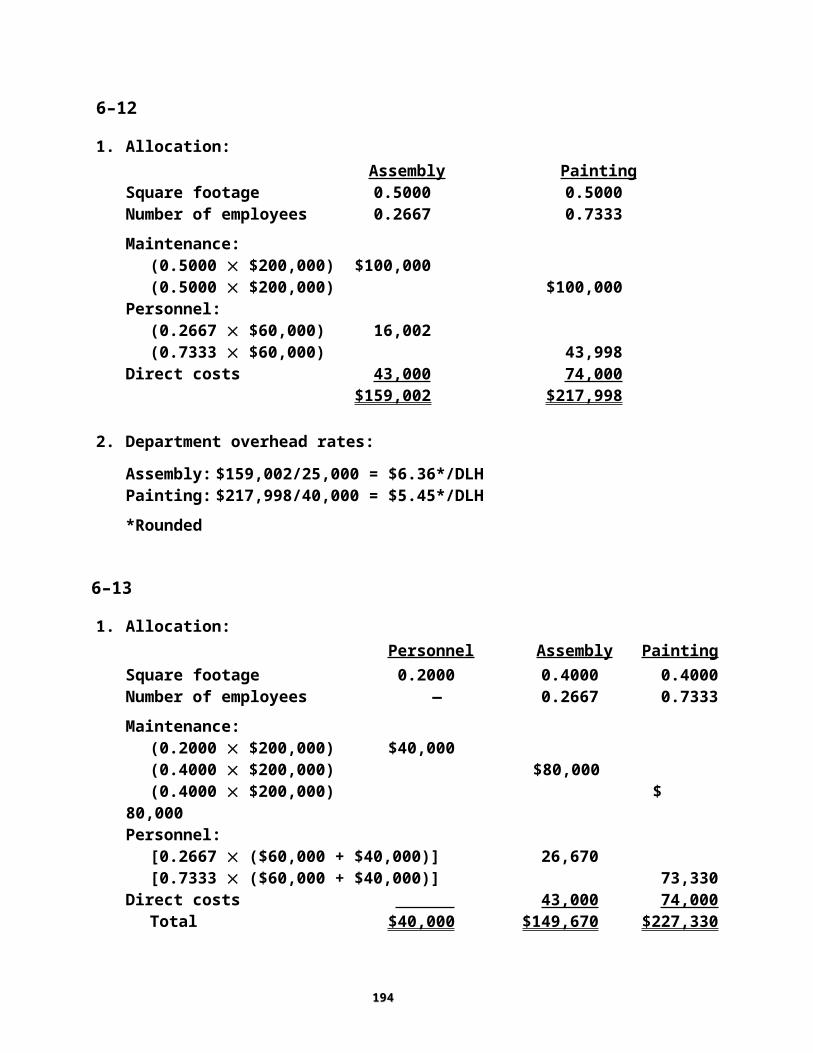

6–12

1. Allocation:Assembly Painting

Square footage 0.5000 0.5000Number of employees 0.2667 0.7333Maintenance:

(0.5000 $200,000) $100,000(0.5000 $200,000) $100,000

Personnel:(0.2667 $60,000) 16,002(0.7333 $60,000) 43,998

Direct costs 43,000 74,000 $159,002 $217,998

2. Department overhead rates:

Assembly: $159,002/25,000 = $6.36*/DLHPainting: $217,998/40,000 = $5.45*/DLH*Rounded

6–13

1. Allocation:Personnel Assembly Painting

Square footage 0.2000 0.4000 0.4000Number of employees — 0.2667 0.7333Maintenance:

(0.2000 $200,000) $40,000(0.4000 $200,000) $ 80,000(0.4000 $200,000) $ 80,000

Personnel:[0.2667 ($60,000 + $40,000)] 26,670[0.7333 ($60,000 + $40,000)] 73,330

Direct costs 43,000 74,000 Total $40,000 $149,670 $227,330

2. Departmental overhead rates:

Assembly: $149,670/25,000 = $5.99* per DLHPainting: $227,330/40,000 = $5.68* per DLH*Rounded

191191

6–14

1. Allocation:Tulsa Ames

Ratio for fixed costs* 0.65 0.35Fixed costs** $ 39,000 $21,000Variable costs*** 65,000 35,000

Total $104,000 $ 56,000 *Tulsa = 1,625/2,500 = 0.65; Ames = 875/2,500 = 0.35

**($60,000 0.65) (60,000 0.35)***$40 1,625 and $40 875

2. Costing out services serves the same purposes as costing out tangible prod-ucts (e.g., pricing, profitability analysis, and performance evaluation). Once the costs are allocated to each revenue-producing center, then the costs must be assigned to individual services through the use of an overhead rate or rates.

6–15

1. a. If the purpose is to cost out individual services, the allocation is identical to that given in Requirement 1 of Exercise 6-14.

b. If the purpose is for performance evaluation, then variable costs equal the predetermined rate multiplied by the actual usage. The fixed costs are al -located the same way as before.

Tulsa Ames Variable costs:

$40 1,200 $48,000$40 1,100 $44,000

Fixed costs 39,000 21,000 $ 87,000 $ 65,000

2. The allocated costs of $152,000 were $1,500 higher than the actual costs of $150,500, because the producing departments are charged an allocation based on budgeted costs rather than actual costs. Budgeted costs are allo-cated so that the efficiencies or inefficiencies of the legal services center are not assigned to the user departments.

192192

6–16

1. 2003 graphics rate $12,000/(2,000 + 2,000) = $3.00/hour2004 graphics rate $14,000/(2,000 + 2,000 + 1,000) = $2.80/hour

2. Total charge to the Nonprofit Organ. Dept. = $2.80 1,000 = $2,800

Mike Adams is no doubt angry. The amount charged was $800 above the in-dicated charge of $2,000.

3. Graphics Department charges did increase by $2,000 ($14,000 – $12,000). However, the charging rate changed as well. Thus, Tangible Goods and Pub-lic Relations saw a decrease in their graphics charges of $400 each. It is this $400 decrease (times 2) which showed up as an $800 increase in Mike’s bill.

193193

PROBLEMS

6–17

1. Allocation ratios for fixed costs (uses normal levels):

SLC Reno PortlandHrs. of flight time 0.2500 0.5000 0.2500No. of passengers 0.3333 0.5000 0.1667Variable rates:

Maintenance: $30,000/8,000 = $3.75 per flight hourBaggage: $64,000/30,000 = $2.1333 per passenger

SLC Reno Portland Maintenance—fixed:

(0.25 $240,000) $ 60,000(0.50 $240,000) $120,000(0.25 $240,000) $ 60,000

Maintenance—variable:($3.75 2,000) 7,500($3.75 4,000) 15,000($3.75 2,000) 7,500

Baggage—fixed:(0.3333 $150,000) 49,995(0.5000 $150,000) 75,000(0.1667 $150,000) 25,005

Baggage—variable:($2.1333 10,000) 21,333($2.1333 15,000) 32,000($2.1333 5,000) 10,667

$138,828 $242,000 $103,172

194194

6–17 Concluded

2. The allocations are the same as in Requirement 1, except variable costs are assigned using actual instead of budgeted activity.

SLC Reno Portland Maintenance—fixed $ 60,000 $120,000 $ 60,000Maintenance—variable:

($3.75 1,800) 6,750($3.75 4,200) 15,750($3.75 2,500) 9,375

Baggage—fixed 49,995 75,000 25,005Baggage—variable:

($2.1333 8,000) 17,066($2.1333 16,000) 34,133($2.1333 6,000) 12,800

$133,811 $244,883 $107,180Yes, maintenance actually cost $315,000, but only $271,875 was allocated. Baggage actually cost $189,000, but $213,999 was allocated (no costs re-main). Actual costs are not allocated so that inefficiencies or efficiencies are not passed on.

6–18

1. Direct method:Proportion of: Pottery Retail

Machine hours 0.375 0.625Number of employees 0.429 0.571

Power:(0.375 $100,000) $ 37,500(0.625 $100,000) $ 62,500

Human Resources:(0.429 $205,000) 87,945(0.571 $205,000) 117,055

Direct costs 80,000 50,000 $205,445 $229,555

195195

6–18 Concluded

2. Sequential method:

Power Human Res. Pottery Retail Machine hours — — 0.375 0.625Employees 0.125 — 0.375 0.500

Direct costs $100,000 $ 205,000 $ 80,000 $ 50,000Human Resources:

(0.125 $205,000) 25,625 (25,625)(0.375 $205,000) (76,875) 76,875(0.500 $205,000) (102,500) 102,500

Power:(0.375 $125,625) (47,109) 47,109(0.625 $125,625) (78,516 ) 78,516

$ 0 $ 0 $203,984 $231,016

3. Reciprocal method:

Power Human Res. Pottery RetailMachine hours — 0.200 0.300 0.500Employees 0.125 — 0.375 0.500

HR = $205,000 + 0.200P P = $100,000 + 0.125HRHR = $205,000 + 0.200($100,000 + 0.125HR) P = $100,000 +

0.125($230,769)HR = $205,000 + $20,000 + 0.025HR P = $128,846

0.975HR = $225,000HR = $230,769

Total Cost Pottery Retail Human Resources: $230,769

(0.375 $230,769) $ 86,538(0.500 $230,769) $115,385

Power: 128,846(0.3 $128,846) 38,654(0.5 $128,846) 64,423

Direct costs 80,000 50,000 $ 205,192 $229,808

196196

6–19

1. Repair Power Molding Assembly Department costs $48,000 $ 250,000 $200,000 $ 320,000Allocation of:

Repair (1/9, 8/9) (48,000) 0 5,333 42,667Power (7/8, 1/8) 0 (250,000 ) 218,750 31,250

Total overhead cost $ 0 $ 0 $424,083 $ 393,917Direct labor hours ÷ 40,000 ÷ 160,000 Overhead rate per DLH $ 10.60 * $ 2.46 **Rounded

2. Algebraic equations for relationship between service departments(R = Repair Department; P = Power Department):R = $48,000 + 0.2PP = $250,000 + 0.1R

R = $48,000 + 0.2($250,000 + 0.1R)= $48,000 + $50,000 + 0.02R

0.98R = $98,000R = $100,000

P = $250,000 + 0.1($100,000)P = $260,000

Repair Power Molding Assembly Department costs $ 48,000 $ 250,000 $200,000 $ 320,000Allocation of:

Repair (0.1, 0.1, 0.8) (100,000) 10,000 10,000 80,000Power (0.2, 0.7, 0.1) 52,000 (260,000 ) 182,000 26,000

Total overhead cost $ 0 $ 0 $392,000 $ 426,000Direct labor hours ÷ 40,000 ÷ 160,000Overhead rate per DLH $ 9.80 $ 2.66 **Rounded

3. The direct allocation method ignores any service rendered by one support department to another. Allocation of each support department’s total cost is made directly to the production departments. The reciprocal allocation method recognizes all support department support to one another through the use of simultaneous equations or linear algebra. This allocation proce-dure is more accurate and should lead to better results which would be of greater value to management. However, the method is infrequently used in actual practice because of the problems associated with developing a more complex or difficult model to recognize the interrelationships between sup-port departments.

197197

6–20

1. $40,000/300,000 = $0.1333/mile (uses normal activity)

2. Variable rate: ($40,000 – $16,000)/300,000 = $0.08/mile

Budget Luxury Truck Fixed cost allocation ratios 0.4000 0.3333 0.2667Allocation of costs:

Fixed portion ($16,000 ratio*) $ 6,400 $ 5,333 $ 4,267Variable portion (act. miles $0.08) 12,000 8,800 8,000

$ 18,400 $ 14,133 $12,267*Budget: 120,000/300,000Luxury: 100,000/300,000Truck: 80,000/300,000

3. Of the actual fixed costs, $1,100 ($17,100 – $16,000) was not allocated. Only budgeted fixed costs were allocated. Variable costs of $1,200 ($30,000 – $28,800) weren’t allocated because the actual variable rate ($0.083 per mile = $30,000/360,000) was greater than the budgeted rate ($0.08 per mile). In both cases, this practice follows the principle of not passing on efficiencies or in-efficiencies of the support department to the producing departments.

6–21

1. Henderson ($431,800/$2,540,000)($182,500)* = $31,025Boulder City ($508,000/$2,540,000)($182,500) = $36,500Kingman ($381,000/$2,540,000)($182,500) = $27,375Flagstaff ($635,000/$2,540,000)($182,500) = $45,625Glendale ($584,200/$2,540,000)($182,500) = $41,975

*($26)(3,750) + $85,000 = $182,500

198198

6–21 Concluded

2. Share of Accounting Department fixed costs based on 2003 sales:

Henderson ($337,500/$2,250,000)($85,000) = $12,750Boulder City ($450,000/$2,250,000)($85,000) = $17,000Kingman ($360,000/$2,250,000)($85,000) = $13,600Flagstaff ($540,000/$2,250,000)($85,000) = $20,400Glendale ($562,500/$2,250,000)($85,000) = $21,250

Variable Cost + Fixed Cost = Total Henderson ($26)(1,475) = $38,350 + $12,750 = $51,100Boulder City ($26)(400) = $10,400 + $17,000 = $27,400Kingman ($26)(938) = $24,388 + $13,600 = $37,988Flagstaff ($26)(562) = $14,612 + $20,400 = $35,012Glendale ($26)(375) = $9,750 + $21,250 = $31,000

3. The method in Requirement 2 ties cost allocated to the driver that causes the cost. Thus, motels would be more likely to use Accounting Department time efficiently. The method in Requirement 1 assigns accounting costs on the basis of a variable which may not be causally related. Also, a motel with sta-ble sales from year to year may still experience wild fluctuations in allocated cost due to changing sales patterns of other motels.

6–22

1. Single rate = [$210,000 + 6,000($14)]/6,000 = $49 per legal hour

Great West Tissue (25 $49) $ 1,225Morton Canned Meats (1,400 $49) 68,600Pettigrew Valve and Tap (3,600 $49) 176,400Bellini Musical Instruments (1,000 $49) 49,000

Total $295,225

199199

6–22 Concluded

2. Dual rate: $14 per legal hour plus share of budgeted fixed costs

Budgeted Share of Division Hours Percent Fixed CostGreat West Tissue 500 8.333 $ 17,499Morton Canned Meats 1,500 25.000 52,500Pettigrew Valve and Tap 3,000 50.000 105,000Bellini Musical Instruments 1,000 16.667 35,001

Total 6,000 100.000 $210,000

Actual Var. Var. Fixed Total Division Hours Rate Amount Amount Cost Great West Tissue 25 $14 $ 350 $ 17,499 $ 17,849Morton Canned Meats 1,400 14 19,600 52,500 72,100Pettigrew Valve & Tap 3,600 14 50,400 105,000 155,400Bellini Musical Instr. 1,000 14 14,000 35,001 49,001

Total $ 84,350 $210,000 $294,350

3. Actual variable costs $ 83,145Actual fixed costs 215,000 $298,145Costs charged 294,350

Difference $ 3,795 The Legal Department spent $3,795 more than was charged to the divisions. Fixed costs were $5,000 over budget. (Actual fixed costs were $215,000, and budgeted fixed costs were $210,000.) However, variable costs came in under budget. The budgeted variable rate was $14, but actual variable cost per hour was $13.80 ($83,145/6,025), resulting in $0.20 savings times the 6,025 actual hours worked.

4. In general, the dual-rate method is preferred. However, some divisions would not be pleased with their charges after the first year. In particular, Great West Tissue is charged far more under the dual-rate method ($17,849) than under the single-rate method ($1,225), because it overestimated its legal needs for the first year. This led to a larger share of fixed costs. This may not be a long-term problem, since Great West may require more legal services in the future (making the first-year experience an anomaly). Note that the estimates made by all four divisions led to the establishment of the size Legal Depart-ment created and that each division must bear responsibility for its estimate.

200200

6–23

1. Clearly, some expenses pertain to women living in the house while others pertain to all members. In-house members use the second floor, most of the food, and most of the variable expenses. All members use the first-floor facil -ities, food for Monday night dinners, and cereal and milk for snacks. HCB must determine a fair method of allocating the costs since the sorority is a nonprofit entity and house bills in total must equal house costs. It is difficult to allocate the costs precisely to the two types of members given the sketchy nature of the data.

2. Using a benefits-received approach, the following charging rates might be applied.

In-house members:Use of second floor ($240,000 – $40,000)/2 $100,000Use of first floor [($240,000 – $40,000)/2]0.6 60,000Food* ($1.01)(60)(20)(32) 38,784Variable expenses 34,800

Total $233,584Charging rate per in-house member per year: $233,584/60 = $3,893

*Cost per meal: $40,000/{[40 + (60 20)] 32} = $1.01

Out-of-house members:Use of first floor [($240,000 – $40,000)/2]0.4 $40,000Food ($1.01)(32)(40) 1,293

Total $41,293Charging rate per out-of-house member per year: $41,293/40 = $1,032

201201

CASE

6–24

1. Allocation, direct method:

Allocation ratios: Laboratory NursingAdministrative (employees) 0.286 0.714Laundry (lbs.) 0.200 0.800Janitorial (sq. ft.) 0.200 0.800

Allocation:Administrative:

0.286 $20,000 $ 5,7200.714 $20,000 $ 14,280

Laundry:0.20 $75,000 15,0000.80 $75,000 60,000

Janitorial:0.20 $50,000 10,0000.80 $50,000 40,000

Direct costs 43,000 150,000 Total costs $ 73,720 $264,280

202202

6–24 Continued

2. Cost-to-charges ratio:

Let X = Number of blood count tests (Test B)

X + 2X + 3X = 22,500 (RVUs)6X = 22,500

X = 3,750 testsRevenues:

B: $5.00 3,750 $ 18,750C: $19.33 3,750 72,488

CB: $22.00 3,750 82,500 Total revenues $173,738

Costs:

Materials:B: $2.00 3,750 $ 7,500C: $5.00 3,750 18,750

CB: $3.00 3,750 11,250 $ 37,500

Labor:B: $2.00 3,750 $ 7,500C: $4.00 3,750 15,000

CB: $6.00 3,750 22,500 45,000

Overhead (from Requirement 1) 73,720 Total costs $156,220

Cost-to-charge ratio = $156,220/$173,738 = 0.90

3. Cost per test using the cost-to-charges ratio:Test B: 0.90 $5.00 = $4.50Test C: 0.90 $19.33 = $17.40

Test CB: 0.90 $22.00 = $19.80

203203

6–24 Concluded

4. Cost per test using RVUs:

Overhead rate: $73,720/22,500 = $3.28 per RVU

Test B:Materials ($2.00 1) $2.00Labor ($2.00 1) 2.00Overhead ($3.28 1) 3.28

Total $7.28Test C:

Materials ($2.50 2) $ 5.00Labor ($2.00 2) 4.00Overhead ($3.28 2) 6.56

Total $15.56Test CB:

Materials ($1.00 3) $ 3.00Labor ($2.00 3) 6.00Overhead ($3.28 3) 9.84

Total $18.84

5. RVU costing is the more accurate approach. This method traces materials and labor to each product and assigns overhead using a factor that corre-lates with its consumption. The cost-to-charges approach makes no effort at all to identify specific consumption of resources by individual products.

6. Test CB, bid using cost-to-charges ratio:Cost (from Requirement 3) $19.80Markup (5%) 0.99 Bid price $20.79

Test CB, bid using RVU costing:Cost (from Requirement 4) $18.84Markup (5%) 0.94 Bid price $19.78

As the problem illustrates, inattention to costing accuracy can cause the hospital to lose bids. If other hospitals, equally efficient, have better cost in -formation, then they will tend to be more successful bidders.

204204

COLLABORATIVE LEARNING EXERCISE

6–25

1. a. Direct methodCooking Packaging and Freezing

Machine hours 0.6667 0.3333Kilowatt-hours 0.5556 0.4444

Maintenance:(0.6667 $340,000) $226,678(0.3333 $340,000) $113,322

Power:(0.5556 $200,000) 111,120(0.4444 $200,000) 88,880

Direct costs 75,000 55,000 $412,798 $257,202

Cooking: $412,798/40,000 = $10.32*/MHrPackaging and freezing: $257,202/30,000 = $8.57*/DLH

Prime costs $16.00Cooking ($10.32 2) 20.64Pack./Freez. ($8.57 0.5) 4 .29 *Total cost $40.93Markup (20%) 8 .19 *Bid price $49 .12 *Rounded

205205

6–25 Continued

b. Sequential method: Maint. Power Cooking Pack./Freez.

Machine hours — 0.4000 0.4000 0.2000Kilowatt-hours — — 0.5556 0.4444Direct costs $ 340,000 $ 200,000 $ 75,000 $ 55,000Maintenance:

(0.4 $340,000) (136,000) 136,000(0.4 $340,000) (136,000) 136,000(0.2 $340,000) (68,000) 68,000

Power:(0.5556 $336,000) (186,682) 186,682(0.4444 $336,000) (149,318 ) 149,318

$ 0 $ 0 $ 397,682 $272,318Cooking: $397,682/40,000 = $9.94*/MHrPack. and Freez.: $272,318/30,000 = $9.08*/DLHPrime costs $16.00Cooking ($9.94 2) 19.88Pack./Freez. ($9.08 0.5) 4.54 Total cost $40.42Markup (20%) 8.08 Bid price $48.50*Rounded

206206

6–25 Continued

c. Reciprocal method:Maint. Power Cooking Pack./Freez.

Machine hours — 0.4 0.4 0.2Kilowatt-hours 0.1 — 0.5 0.4

M = $340,000 + 0.1P P = $200,000 + 0.4MM = $340,000 + 0.1($200,000 + 0.4M) P = $200,000 + 0.4($375,000)M = $340,000 + $20,000 + 0.04M P = $200,000 + $150,000

0.96M = $360,000 P = $350,000M = $375,000

Total Cooking Pack./Freez.From:Maintenance: $375,000

(0.4 $375,000) $150,000(0.2 $375,000) $ 75,000

Power: 350,000(0.5 $350,000) 175,000(0.4 $350,000) 140,000

Direct costs 75,000 55,000 $400,000 $270,000

Cooking: $400,000/40,000 = $10/MHrPack. and Freez.: $270,000/30,000 = $9/DLH

Prime cost $16.00Cooking ($10 2) 20.00Pack./Freez. ($9 0.5) 4.50 Total cost $40.50Markup (20%) 8.10 Bid price $48.60

207207

6–25 Concluded

2. No, the direct method did not produce a winning bid. The direct method fails to consider the interrelationships of the support centers, and, as a conse-quence, assigns too much of the support center costs to the Cooking Depart-ment. Since the job spends more time in the Cooking Department than in the Packaging and Freezing Department, it receives too much overhead and is overpriced. The reciprocal method is the most accurate as it takes into ac-count the use of support departments by other support departments.

CYBER RESEARCH CASE

6–26

Answers will vary.

208208