chapter 9 journalizing purchases and cash payments section 9-1

TRANSCRIPT

Chapter 9 – Journalizing Purchases and Cash Payments

Section 9-1

Merchandise –

Merchandising Business –

Retail Merchandising Business –

Wholesale Merchandising Business –

A service business and merchandising business use a similar Chart of Accounts, however, a

merchandising business has additional accounts on the balance sheet and income statement to

account for the _________________ and ________ of merchandise.

Corporation –

Share of Stock –

Capital Stock –

Stockholder –

CONCEPT: Business Entity –

CONCEPT: Going Concern –

A (_________) business with a limited number of daily transactions may record all entries in one

journal (_____________ journal). A (____________) business with many daily transactions

may choose to use a separate journal for each kind of transaction.

Special Journal –

There are five journals to record daily transactions (type and definition):

1.

2.

3.

4.

5.

Cost of Merchandise –

The _________ price must be greater than the cost of merchandise for a business to make a

_________.

Markup –

Revenue earned from the sale of merchandis includes both the

____________________________ and ____________ . Only the ____________ increases

_______________.

Vendor –

______________ account is only used to record the _________ of merchandise purchased.

CONCEPT: Historical Cost –

Purchase on Account –

Purchases Journal –

Special Amount Column –

REMEMBER: All _____________ on account transactions are recorded in the ____________

journal. Nothing dealing with CASH goes in this journal.

Purchase Invoice –

CONCEPT: Objective Evidence –

November 2. Purchased merchandise on account from Crown Distributing, $2,039.00.

Purchase Invoice No. 83.

The purchases journal is _____________ and doubled-rule at the end of each month.

Work Together 9-1

On Your Own 9-1

Section 9-2

Cash Payments Journal –

This journal is used for all transactions were ___________ is being paid for anything. The

__________ amount shown on a purchase invoice is what the customer is expected to pay.

However to encourage _________ payment, a vendor may allow a ______________ from the

invoice amount.

Cash Discount –

Purchases Discount –

When a ______________ discount is taken, the customer pays _____ than the invoice amount

recorded when the ____________________ occurred.

General Amount Column –

REMEMBER: Only cash payment transactions are recorded in the ________ _________

journal.

November 2. Paid cash for advertising, $150.00. Check # 292.

November 5. Paid cash for office supplies, $94.00. Check #293.

List Price –

Trade Discount –

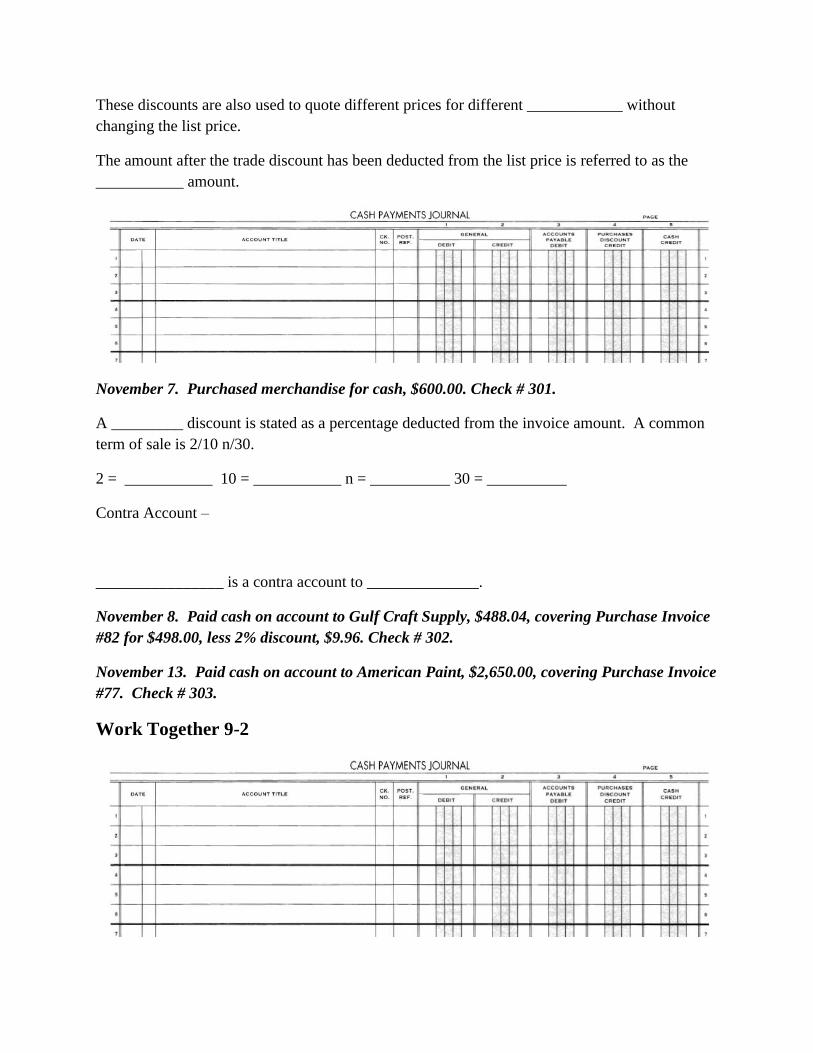

These discounts are also used to quote different prices for different ____________ without

changing the list price.

The amount after the trade discount has been deducted from the list price is referred to as the

___________ amount.

November 7. Purchased merchandise for cash, $600.00. Check # 301.

A _________ discount is stated as a percentage deducted from the invoice amount. A common

term of sale is 2/10 n/30.

2 = ___________ 10 = ___________ n = __________ 30 = __________

Contra Account –

________________ is a contra account to ______________.

November 8. Paid cash on account to Gulf Craft Supply, $488.04, covering Purchase Invoice

#82 for $498.00, less 2% discount, $9.96. Check # 302.

November 13. Paid cash on account to American Paint, $2,650.00, covering Purchase Invoice

#77. Check # 303.

Work Together 9-2

On Your Own 9-2

Section 9-3

Cash Short –

Cash Over –

The account used for either of these is __________________________. The balance can be

either __________ or _________.

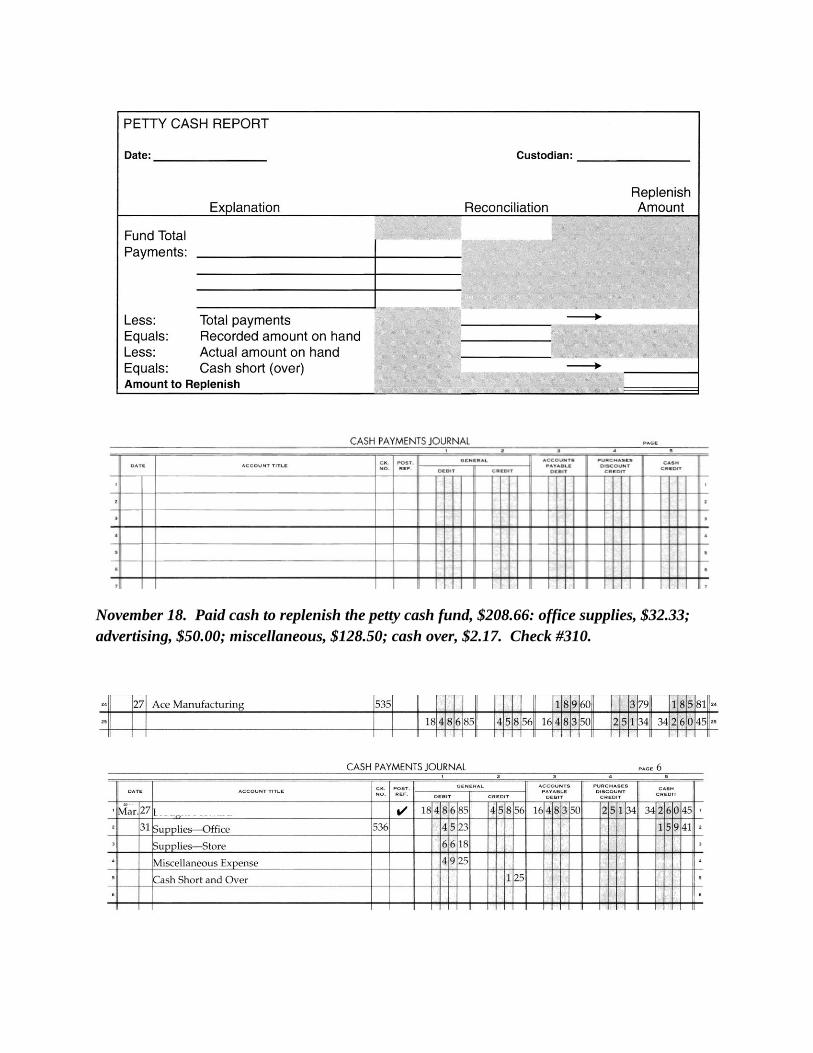

November 18. Paid cash to replenish the petty cash fund, $208.66: office supplies, $32.33;

advertising, $50.00; miscellaneous, $128.50; cash over, $2.17. Check #310.

The Cash Payments journal is ___________ and ______________ at the end of each month.

Verify that __________ equal ____________ when totaling the journal.

Section 9-4

Not all transactions can be recorded in ____________ journals. Transactions that cannot be

recorded in one of the special journals are journalized in the _____________ journal.

November 6. Bought store supplies on account from Gulf Craft Supply, $210.00. Memo #52.

Purchases Return –

Purchases Allowance –

Debit Memorandum –

November 28. Returned merchandise to Crown Distributing, $252.00, covering Purchase

Invoice #80. Debit Memo #78.

Work Together 9-4

On Your Own 9-4