chapter five study of behaviour of equity returns analysis...

TRANSCRIPT

Chapter Five

STUDY OF BEHAVIOUR OF EQUITY RETURNSANALYSIS I

Chapter Five

STUDY OF BEHAVIOUR OF EQUITY RETURNSANALYSIS I

In this chapter, the behavior of all the 20 stocks under study wasexamined in detail. The equity return behavior of the stocks was studied interms of the stocks’ daily returns, average annual returns and Holding PeriodYield. The volatility in returns was given paramount importance in thestudy. The daily returns of the individual stocks for 10 year period from1999 to 2009 were examined to understand their behavior. The statisticaltools like Arithmetic mean, standard deviation, measure of skewness,kurtosis, variances and all were used to study the daily and annual returns.Annual returns were averaged by the number of actual market working daysfor the relevant year. The arithmetic average returns of every year for the tenyears were studied for establishing the behavior. Similarly, Holding PeriodYields of the scrips were worked from the daily returns on yearly basis forall the 10 years to study their behavior. The returns were:

1. Daily Returns (DR)2. Annual Returns (AR)3. Holding Period Yield (HPY)

The returns were calculated as given

1. Daily returns

DR = − 1 100

Here,

P1= New priceP0 = Previous day’s price

2. Annual Returns

=

3. Holding Period Yield (HPY)

HPY =( )-1=( − 1)100

Here,

P1 = Closing Stock price of the yearP0 = Opening stock price of the year

In the analysis, a detailed summary statistics were calculated andgiven as table. The summary statistics includes,

1. Arithmetic mean2. Standard deviation(σ)3. variance(σ2)4. co-variance(Cov)5. skewness6. kurtosis7. correlation(r)8. beta coefficient9. R2 value.

They were all used to analyse the behavior of returns supplementedby tables and graphs.An individual company-wise study of thebehavior of equity returns were carried out on the above backdropas below:

1. ACC

Table No.5.1Summary statistics of ACC from 1999 to 2009

Source: Official website of Bombay Stock Exchange

As per Table 1, the average return of ACC for the period from 1999 to2009 was 0.09%. But the estimated return as represented by the holdingperiod yield (HPY) for the same period was 13.5%. It could be seen that thescrip’s performance was much below the estimated. Similarly ACC’saverage return was lower than the market return of 0.11%. The standarddeviation and variance were slightly significant. During the 10 year periodthe return went up to 15.6% and went down to the extent of -91.84%.

The σ 3.32 and the var.11.04 signify volatility in the return. The rangeof return between the prosperity and adversity 108 was also significant andshows exceptional volatility. The distribution was negatively skewed to theextent of -7.61 which is statistically significant. The value of kurtosis isbigger than 3. The distribution is high leptokurtic.

The correlation between ACC and BSEI were 0.025. It is highlyinsignificant. But both move to the same direction positively. There is only aslight covariance between them to the extent of 0.149. The beta value is lessthan one. The risk of the scrip is considerably lower than the marketportfolio. R2 value is only 0.0006 which says that only an infinitesimal partof the variance is explained by the market and the remaining 99% of thevariance was unexplained by the market.

Average return 0.09% Skewness -7.61σ 3.32 Variance 11.04L 15.6 Cov. 0.15S -91.84 kurtosis 212.01Range 108 cor. 0.025Beta 0.046R2 0.0006 HPY 13.5%

Market return 0.11%

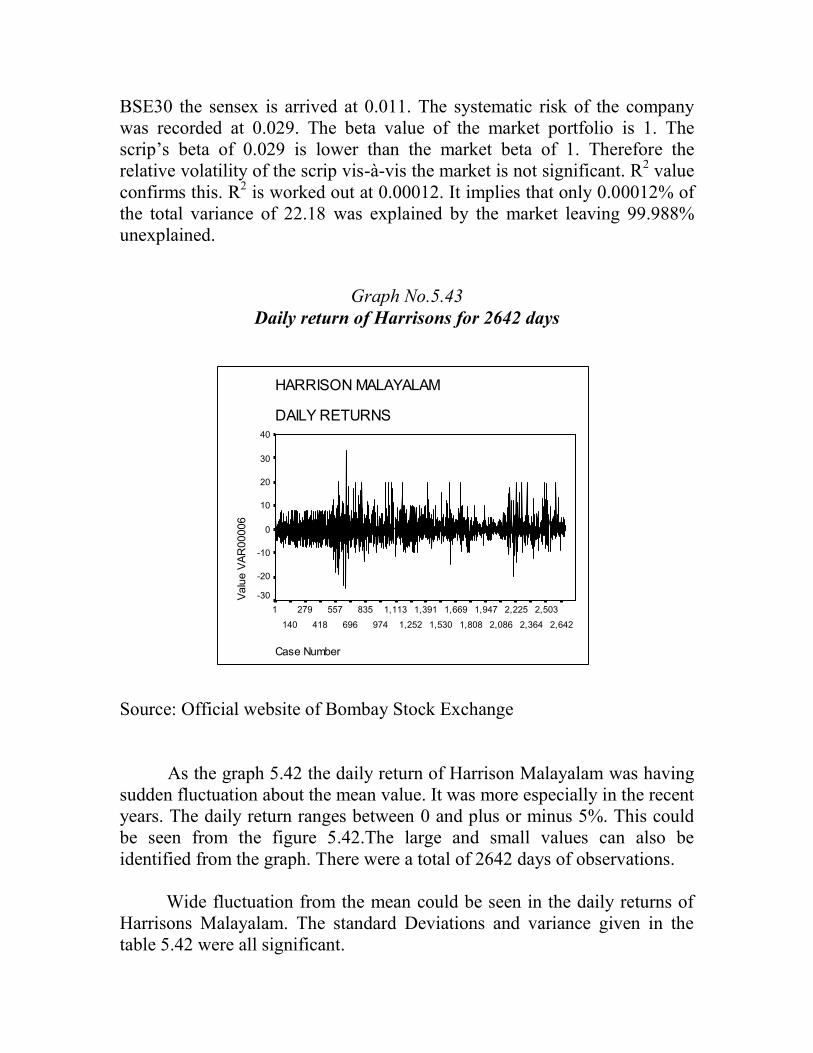

Graph No.5.1Daily returns of the stock for 2642 days.

Daily Return of ACC

No. of observation

Case Number

2,6422,503

2,3642,225

2,0861,947

1,8081,669

1,5301,391

1,2521,113

974835

696557

418279

1401

Value

VAR

0000

1

40

20

0

-20

-40

-60

-80

-100

Source: Official website of Bombay Stock Exchange

It can be seen from the graph 5.1 above that the daily returns of ACCfor 10 years from 1999 to 2009 were closely knitted with an exceptional andabnormal aberration on a particular day where the return fell drastically tothe extent of -91.84%. On all other days the return drawn by the companywas around the expected value 0.09%. The pattern of the return isconspicuously thickly packed about either sides of the abscissa within arange of 0 and 1 per cent. As the standard deviation denotes, the actualvalues tightly fastened to the mean return.

It can be seen from the graph 5.1 above that the daily return of thescrip was moderately volatile. Most of the values lie within a range of -5%and 5%. The X axis is thick and dark because on an average the daily returncoincides with zero. The graph shows that the distribution is less normal.The distribution of daily returns was more leaned towards left due tonegative skewness. High leptokurtic kurtosis can also be viewed from thegraph.

Table No.5.2Holding Period Yield of ACC for the period 1999-2009

Source: Official website of Bombay Stock Exchange

As per table 5.2 above, the largest holding period yield was 105% inthe year 2006. In the first 3 years of the decade the yield was negative. In thefirst year 1999 the yield was -75%. But year after year it was reducing. It canbe viewed from the figure that the yield curve was rising upwards from1999. After the peak performance in the year 2006, the yield abruptly felldown to -6% in 2007, then again fell to a -54% in 2008 before it rose to amagnificent 76% in 2009. The overall performance of the scrip wasprospective with an average of 13% during the decade. Since 1999 the yieldtends to rise upward except in the years 2007 and 2008.The yield curve isnot normal. It is negatively skewed with a high peakedness (Leptokurtic).For five years the scrip was earning negative holding period yield. The otherfive years it was making positive holding period yields. The performancecan be seen from the graph No.5.2 below. The lowest holding period yieldswere earned in 1999. Since 1999 the holding period yield was raising at rateof 200%. The year 1999 had a disastrous effect on the HPY of the company.On the contrary, year 2006 was highly prospective.

YEAR CL OP HPR HPY1999 248.25 1010 0.25 -752000 159 268 0.59 -412001 151.8 160.6 0.95 -52002 165.1 147.4 1.12 122003 245.55 164.25 1.49 492004 338.7 258.65 1.31 312005 534.2 341.5 1.56 562006 1085.55 530.5 2.05 1052007 1024.5 1092.4 0.94 -62008 477.9 1028.1 0.46 -542009 871.5 495.9 1.76 76

AM 13.45

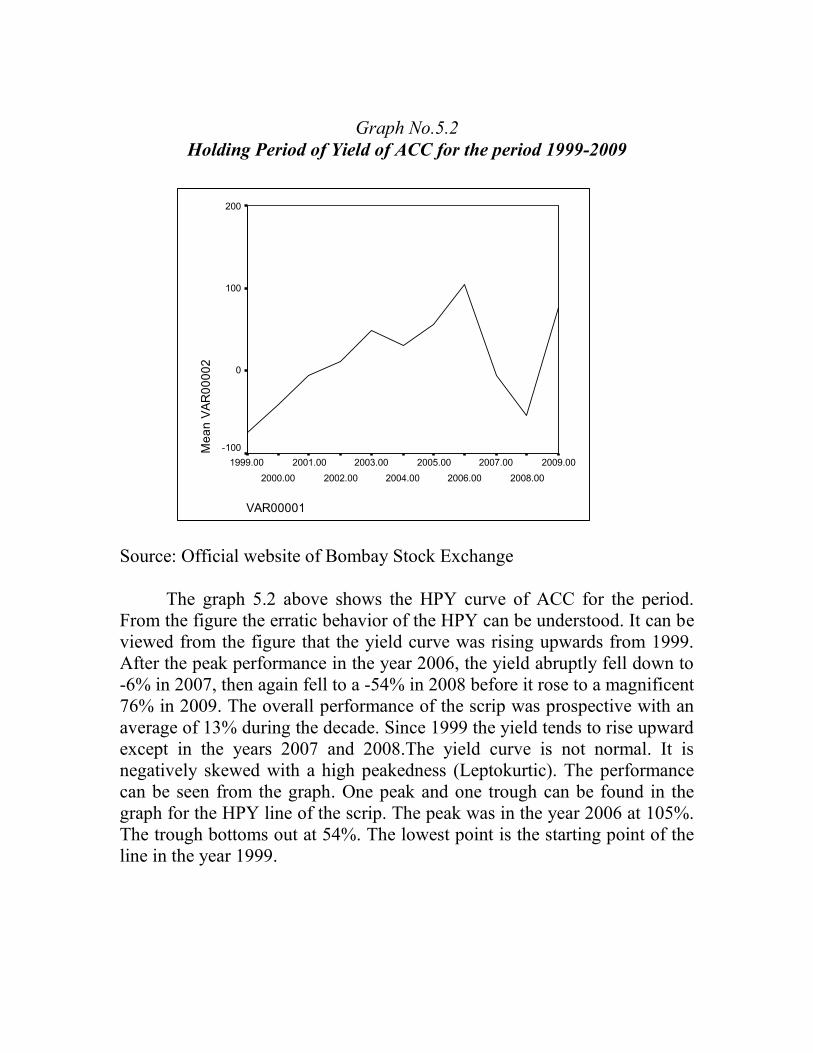

Graph No.5.2Holding Period of Yield of ACC for the period 1999-2009

Source: Official website of Bombay Stock Exchange

The graph 5.2 above shows the HPY curve of ACC for the period.From the figure the erratic behavior of the HPY can be understood. It can beviewed from the figure that the yield curve was rising upwards from 1999.After the peak performance in the year 2006, the yield abruptly fell down to-6% in 2007, then again fell to a -54% in 2008 before it rose to a magnificent76% in 2009. The overall performance of the scrip was prospective with anaverage of 13% during the decade. Since 1999 the yield tends to rise upwardexcept in the years 2007 and 2008.The yield curve is not normal. It isnegatively skewed with a high peakedness (Leptokurtic). The performancecan be seen from the graph. One peak and one trough can be found in thegraph for the HPY line of the scrip. The peak was in the year 2006 at 105%.The trough bottoms out at 54%. The lowest point is the starting point of theline in the year 1999.

VAR00001

2009.002008.00

2007.002006.00

2005.002004.00

2003.002002.00

2001.002000.00

1999.00

Mea

n VA

R00

002

200

100

0

-100

Table No.5.3Annual Return of ACC for the period 1999-2009

Year Annual Return1999 0.182000 -0.132001 0.032002 0.062003 0.212004 0.132005 0.192006 0.322007 0.012008 -0.252009 0.27

AM= 0.09

Source: Official website of Bombay Stock Exchange

Table No.5.3 above, shows the rate of return earned by the scrip from1999 to 2009. On an average the scrip had earned a return of 0.09%. Exceptin 2000 and 2008 it had performed well. In 1999 the annual return of ACCwas 0.18%. In 2009 it rose to 0.27. The rate of growth in the annual rate was1.5 times. In two years ACC had negative annual returns. The annual returnwas registered in 2006 as 0.32% and the lowest 0.25% in 2008.Year 2008was worst for ACC. The graph also elucidates the highly fluctuating natureof the return. From Table No.2 and Table No.3 It can be found that the HPYwas stable and fluctuated moderately while the daily return made violentzigzags. In the case of annual return year 2008 played havoc. It was the mostdisastrous year in the decade for the company as far as annual returnsconcerned.

Graph No.5.3Annual Return of ACC for the period 1999-2009

Source: Official website of Bombay Stock Exchange

The Graph 5.3 above, shows the behavior of the annual return ofACC. The curve was erratic, having lots of ups and downs and formation ofa peak and two troughs. From the graph it can be seen that the negativereturn in 2008 was the major fall in the decade for the stock ACC. Annualreturn line of ACC begun from higher point at Y-axis.Then it sharply fellbelow -1% in year 2000. Then it rose to 0.2% in 2004.After some minorzigzag again it rose to the maximum in 2007. Immediately then the annualreturns line fell sharply to the bottommost point in 2008. In 2009 annualreturns recovered from the depression and went up comfortably. In this waythere were full of ups downs in the movement of the annual return. In 2007the annual return was at the peak. But in the next year 2008 it sharply fell.Again in 2009 the return went up. Annual returns never stay permanent. Itwas moving violently rousing uncertainty and concern to the stake holdersand share holders. The annual returns of ACC were found highly volatileduring the period.

VAR00003

2009.002008.00

2007.002006.00

2005.002004.00

2003.002002.00

2001.002000.00

1999.00

Mea

n V

AR

0000

7

.4

.3

.2

.1

-.0

-.1

-.2

-.3

2. APOLLO TYRES

Table No.5.4Summary statistics of ACC from 1999 to 2009

Source: Official website of Bombay Stock Exchange

Table No.5.4 above shows that the average return of the Apollo Tyreswas 0.10% which was slightly less than the market rate of return. Theestimated return represented by the HPY for the said period was 24.64. TheArithmetic Mean return of the company is considerably lower than thedecade’s holding period yield. The return is highly and negatively skewed ata rate of -4.089. During this period the company had made a maximumreturn of 25.94% and a smallest return of -89.4%. The range of the largestand smallest was 115.34. This shows that the scrip’s return was highlyfluctuating. The company had a high standard deviation of 3.81. Variancealso is high (14.54).The correlation between the company and the market islow as shown by the parameter r = 0.009. The value of kurtosis was 112.858.It signifies a greater amount of peakedness in the distribution. It is that ofLeptokurtic. The scrip’s relative volatility beta is 0.02. It is lower than themarket beta of 1.0. The beta coefficient is insignificant. R2 value of thecompany 0.0004 tells that 99.6% of the return is unexplained and only 0.004% is explained by the market. The scrip is not greatly influenced by themarket.

Average return 0.10% Skewness -4.089σ 3.81 Variance 14.54L 25.94 cov 0.06S -89.4 kurtosis 112.858Range 115.34 cor. 0.009Beta 0.02

R2 0.0004 HPY 24.64

Market return 0.11

Graph No.5.4Daily return of Apollo Tyres for 2642 days

Source: Official website of Bombay Stock Exchange

The Graph 5.4 above shows the fact that the return from the companywas moderately distributed. The substantial portion of the daily return hadoccurred on and around X-axis or zero line. Occasional upheavals were alsofound off the abscissa. But they were only errors. The major chunk of returncould be located in between 0 and 5±. The lowest one day return was shownon the right hand side of the figure. Excessive hump can be seen on the lefthand side indicating negative skewness. As the standard deviation 0f thescrip 3.81 revealed there was high volatility in the daily returns. The graphshows the fact that the daily return has full of events with numerous violentvibrations about and around the mean returns. It shows that the daily returnwas not stable and regular. On the contrary, it was fluctuating and unstable.

Case Number

2,6422,503

2,3642,225

2,0861,947

1,8081,669

1,5301,391

1,2521,113

974835

696557

418279

1401

Val

ue V

AR

0000

2

40

20

0

-20

-40

-60

-80

-100

Table No.5.5Holding period yield of Apollo for the period 1999-2009

YEAR OP CL HPR HPY1999 64.85 159.05 2.45 1452000 171.75 88.55 0.52 -482001 89.2 79.9 0.9 -102002 76.8 134.2 1.75 752003 134.75 258.05 1.92 922004 275.15 235.75 0.86 -142005 239 278.4 1.16 162006 279.45 352.9 1.26 262007 348.35 53.8 0.15 -852008 57.9 19.85 0.34 -662009 20.35 48.8 2.4 140

AM 24.64

Source: Official website of Bombay Stock Exchange

Table No.5.5 above shows, that the HPY of Apollo on an average was24.64%. In 1999 the HPY was 145%. In 2009 it was 140%. The HPY haddecreased by 3.44% during this 10 year period. The HPY was the highest in1999 with 145%. The lowest HPY was registered in 2007 as -85%. The year2007 was worst for the stock Apollo. In 5 years the scrip incurred negativeHPY and the other 5 years it had made positive HPY. Year 1999 was themost prosperous for Apollo. The HPY on an average was declining since1999. The years 2007 and 2008 had disastrous impact on the holding periodyields of the scrip. The performance 2009 was sudden recovery from thepreceding years’ great falls. Therefore the performance of the year 2009cannot be expected to be stable overtime. The history of the HPY for theentire period also did not support such a surmise. The Holding period Yieldof Apollo was full of uncertainties and volatilities during the period. Nothingcould be predicted.

Graph No.5.5Holding Period Yield Apollo for the period 1999-2009

Source: Official website of Bombay Stock Exchange

Graph No.5.5 above, Shows that Apollo’s yield in the year 1999 was145%. In 2000 the HPY sharply fell and went down below the X-axis to theextent of -48%. But from 2001 onwards the HPY tended to go up. In thisway between 1999 and 2009 the HPY widely fluctuated in zigzag manner. In2009 again the holding period yield went up showing a prospective future.On an average in the meantime the company secured an overall HPY of24.64 during the decade. It is to be noted that the overall tendency ofApollo’s HPY is to decline since 1999. In the beginning and end of thedecade only the scrip could make outstanding HPY. They could beconsidered only chance performance. In between these two extreme cases inall other years the scrip’s HPY line was fluctuating and swinging up anddown in an indecisive way creating full of uncertainties. This can be viewedfrom the graph. Four peaks and four troughs could be seen in the movementof the HPY line indicating sporadic volatility in the holding period yield ofthe Apollo.

VAR00003

2009.002008.00

2007.002006.00

2005.002004.00

2003.002002.00

2001.002000.00

1999.00

Mea

n V

AR

0000

4

200

100

0

-100

Table No.5.6Annual return of Apollo for the period 1999-2009

Source: Official website of Bombay Stock Exchange

Table No.5.6 above, shows the annual rate of return earned by thescrip Apollo from 1999 to 2009. On an average the scrip had earned a returnof 0.10%. Except in 2000, 2004, 2007 and 2008 it had performed well. In1999 the annual return of ACC was 0.50%. In 2009 it decreased to 0.43%.The rate of fall in the annual rate was 14 %. In 4 years Apollo had negativeannual returns. The largest annual return was registered in 1999 as 0.50%and the lowest -0.36% in 2008. Year 2008 was worst for Apollo. The annualreturn table of Apollo was very much similar to the HPY table. Years 2007and 2008 yield negative annual returns consecutively. Its impact on theannual returns of the entire period was very high. Even though in 2009 arecovery from previous years’ debacle was made, there was no sign that itwould be repeated in the future. From 1999 to 2009 the annual return of thestock was showing a tendency of declining year after year. Every year therewas only uncertainty about the return whether positive or negative.

Year Annual Return1999 0.502000 -0.182001 0.012002 0.292003 0.322004 -0.022005 0.082006 0.122007 -0.142008 -0.362009 0.43

AM 0.10

Graph No.5.6Annual return of Apollo Tyres for the period 1999-2009

Source: Official website of Bombay Stock Exchange

The Graph 5.6 above shows the behavior of the annual return ofApollo. The curve was erratic, having lots of ups and downs and formationof a peak and two troughs. From the graph it can be seen that the negativereturn in 2008 was the major fall in the decade for the stock ACC. Theannual return line started well from a high point on Y-axis in 1999. Thenimmediately it falls below zero line in deep in 2000. Then it recovers andgoes up in the next years and reaches the maximum in 2003. Then abruptly itswings downwards below zero in 2004 itself. Then it recovers in 2005 andreaches another peak in 2006. There from it again make a somersault andfalls sharply below zero return point and reaches the bottommost showingthe minimum annual return for Apollo. In this way the annual return wasgoing up and down year after year recurring creating chaos and uncertaintyin the occurrence of annual returns for the company. It indicated themagnitude of volatility in the annual return of the stock.

VAR00003

2009.002008.00

2007.002006.00

2005.002004.00

2003.002002.00

2001.002000.00

1999.00

Mea

n V

AR

0000

5.6

.4

.2

-.0

-.2

-.4

-.6

3. ARVIND MILLS

Table No.5.7Summary statistics of Arvind Mills from 1999 to 2009

Source: Official website of Bombay Stock Exchange

Table No.5.7 above shows that Arvind Mill’s average annual returnwas 0.07%. But expected return based on the past 10 years performance asshown by the holding period yield was 14.45%. On an average thecompany’s earnings were lower than the expected. During the same periodthe market return was recorded as 0.11% which was much more than thecompany’s return 0.07%. The standard deviation 3.86 and variance 14.9were significant and signals fluctuation in returns from the average. Duringthis period company earned a maximum of 37.5% return and went as low as-24.12% returns. The return ranged to a total of 61.26. It reveals the tightbond of the returns with the mean. The dispersion of the individual returnwas not wide and scattered from the mean return. The distribution of returnwas not normal. The positive skewness measured as 0.77 shows the fact thatthe distribution was positively skewed. The degree of skewness was veryhigh. The kurtosis worked out was 7.35. It shows the presence of apeakedness of leptokurtic. The correlation coefficient of the company’sreturn with the market was -0.33. It denotes the fact that the correlation isnegative with the market index and significant. The relative volatility of thescrip with the market as denoted by the beta was -0.71. It means thecompany behaved less than proportionately and inversely with the market.The risk of Arvind Mills is not more than the market portfolio. The R2 value

Average return 0.07% Skewness 0.77σ 3.86 Variance 14.9L 37.5 cov -2.28S -24.12 kurtosis 7.35Range 61.26 cor. -.33Beta -0.71 HPY 14.45R2 0.1089

Market return 0.11

0.109 tells the fact that only 11% of the variance 14.9 was explained by themarket and 89 % was unexplained by the market.

Graph No.5.7Daily return of Arvind Mills for 2642 days

Aravind mills

Daily Returns

Case Number

2,6232,485

2,3472,209

2,0711,933

1,7951,657

1,5191,381

1,2431,105

967829

691553

415277

1391

Value

VAR0

0001

50

40

30

20

10

0

-10

-20

-30

Source: Official website of Bombay Stock Exchange

Graph.5.7 shows greater fluctuation in the daily return ofAravind Mills. It can be found that almost all values fall within therange of 0%-5% plus or minus. Largest value and smallest value canalso be noted on some exceptional days from the graph. The valueswere thronging about the average. The distribution is tightly knittedwith some occasional exceptional behavior. The substantial portion ofthe daily return had occurred on and around X-axis or zero line.Occasional upheavals were also found off the abscissa. But they wereonly errors. The major chunk of return could be located in between 0and 5±. The lowest one day return was shown on the right hand sideof the figure. Excessive grouping of returns can be seen on the righthand side indicating positive skewness. As the standard deviation 0fthe scrip 3.9 revealed there was high volatility in the daily returns.The graph shows the fact that the daily return has full of events withnumerous violent vibrations about and around the mean returns. Itshows that the daily return was not stable and regular. On thecontrary, it was fluctuating and unstable.

Table No.5.8Holding period yield of Arvind Mills for the period 1999-2009

Source: Official website of Bombay Stock Exchange

Table No.5.8 above shows, that the HPY of Arvind Mills on anaverage was 14.45%. In 1999 the HPY was -37%. In 2009 it was118%. The HPY had increased by 4.2 times since 1999 during this 10year period. The HPY was the highest in 2002 with 141%. The lowestHPY was registered in 2008 as negative 85%. The year 2008 wasworst for the stock Arvind. In 6 years the scrip incurred negative HPYand the other 4 years positive HPY had been earned. Year 2002 wasthe most prosperous for Arvind. Year 2008 had played havoc to theHPY of the company. The HPY on an average was declining since1999. The years 2005, 2006 and 2008 had disastrous impact on theholding period yields of the scrip. The performance 2009 was suddenrecovery from the preceding years’ great falls. Therefore theperformance of the year 2009 cannot be expected to be stableovertime. The history of the HPY for the entire period also did notsupport such a surmise. Because of most of the years the holdingperiod of Apollo was negative. The Holding period Yield of Apollowas full of uncertainties and volatilities during the period. Nothingcould be predicted.

YEAR OP CL HPR HPY1999 39.7 25.05 0.63 -372000 24.25 13.4 0.55 -452001 13.3 9 0.68 -322002 9.1 21.95 2.41 1412003 21.95 22.55 1.03 32004 68.35 132.3 1.94 942005 134.5 95.6 0.71 -292006 96.8 51.7 0.53 -472007 52.3 90.55 1.73 732008 89.55 17.56 0.2 -802009 17.95 39.1 2.18 118

AM 14.45

Graph No.5.8Holding Period Yield of ArvindMills for the period1999-2009

Source: Official website of Bombay Stock Exchange

The graph 5.8 above shows the HPY curve of Arvind for theperiod from 1999 to 2009.. From the figure the erratic behavior of the HPYcan be understood. It can be viewed from the figure that the yield curve wasrising upwards from 1999. From 1999 to 2009 Arvind’s stock faced 4 peaksand 4 troughs. The HPY curve was highly fluctuating. The overall tendencyof the HPY line was to decline. it could be seen that most of the years theHPY line of the company was going up and down along the x-axis. Despitethis the overall performance of the company was prospective by securing14.5%. The performance of the company in 2009 was impressive while theyear 2008 was worst.

In theend of the decade and occasionally in some years only the scripcould make outstanding HPY. For every rise immediate fall was experiencehy the scrip in the case of HPY. Whenever positive HPY was recorded itwas as if a chance performance. In all years the scrip’s HPY line wasfluctuating and swinging up and down in an indecisive way creating full ofuncertainties. This can be viewed from the graph. Four peaks and fourtroughs could be seen in the movement of the HPY line indicating sporadicvolatility in the holding period yield of the Apollo.

VAR00003

2009.002008.00

2007.002006.00

2005.002004.00

2003.002002.00

2001.002000.00

1999.00

Mea

n V

AR

0000

4

200

100

0

-100

Table No.5.9Annual return of Arvind Mills for the period 1999-2009

Year Annual Return1999 -0.112000 -0.182001 -0.032002 0.442003 0.492004 0.332005 -0.102006 -0.202007 0.272008 -0.522009 0.41

AM 0.07

Source: Official website of Bombay Stock Exchange

Table 5.9 shows the average annual return of Arvind Mills. During the1999-2009 periods in the initial three years the company had made negativereturns. The average annual return was 0.07 per cent. In the year 2002 thecompany gained a return of 0.44%.In 2004 it made the maximum for thedecade 0.49%. In 1999 the annual return of Arvind Mills was -.11%. In 2009it made a return of 0.41%. Since 1999 the annual return of the scip wasincreasing by 4.7 times. In 1999 the annual return was negative. For sixyears the stock was making negative returns. Only four years it was makingpositive annual returns. It all amounts to the prevalence of high uncertaintyin the occurrence of the annual returns of Arvind Mills. There was chaos inthe distribution of annual returns for the stock for the period. Due to thischaos it becomes difficult to predict the future annual returns. Potentialinvestors would be panic as to whether to invest on the stock or not. Such anamount of uncertainty in annual returns of the company was prevailing over.

Graph No.5.9Annual return of Aravind Mills for the period 1999-2009

Source: Official website of Bombay Stock Exchange

It could be seen from the graph No.5.9 that the average annual returnof the company Arvind Mills from 1999 onwards rose from negative returnsto positive and reached the maximum in 2003. Then the annual return linewas falling with lot of minor ups and down. The line had been finally fallento the lowest and worst in 2008. Then again the line recovered and went upin 2009. The annual return line of Arvind stock was highly volatile duringthe period.

The scrip’s annual return curve was starting from low minus point onY-axis. Then it rose to a peak with much hesitation in 2003. There from itfell sharply and abruptly crossing zero line down to a trough in 2006. Thenthe annual return line again rose to a higher point in 2007. Then fell down toanother major trough which was minimum annual returns for the firm in thedecade in 20008. Annual return line in this way had a travail of going up anddown with full of twists and turns of short-living in nature throughout itslength. It all indicates high level of uncertainty prevailing in the occurrenceof annual returns of the company.

VAR00003

2009.002008.00

2007.002006.00

2005.002004.00

2003.002002.00

2001.002000.00

1999.00

Mea

n VA

R00

005

.6

.4

.2

-.0

-.2

-.4

-.6

4. Ashok Leyland

Table No.5.10Summary statistics of Ashok Leyland from 1999 to 2009

Source: Official website of Bombay Stock Exchange

Table 5.10 shows, that the average return earned by Ashok Leylandduring the period was 0.11% which was identical to the market return. TheHPY was 48.27%. The HPY is much higher than the market return of0.11%. As the HPY is a proxy for estimated return the company’s averagereturn was disappointing. During the decade of 1999-2009 the companyearned a largest return of 18.22. The smallest for the same period was -89.2.The return for the period was wavering between these two values giving wayto high level of uncertainty and fluctuations. The range 107.94 is bignumber representing high volatility of the returns. The distribution of thereturn was not normal. It is negatively skewed to the extent of -4.53. Notonly negatively skewed but also had a leptokurtic peakedness. The beta ofthe company reveals the systematic risk of the company. The beta -0.011 isnegative, which only rarely happens, and lower than the market proxy ofB.S.E30. The R2 value given confirms it. The R2 value 0.005 is insignificantin the sense that the only 0.005% of the total variance was explained by themarket, the remaining 99.5% was unexplained by the market. It means thestock’s market-related risk is insignificant.

Average return 0.11% Skewness -4.53σ 3.9 Variance 22.07L 18.22 cov -0.034S -89.2 kurtosis 115.24Range 107.94 cor. -0.005Beta -0.011R2 0.005 HPY 48.27%

Market return 0.11%

Graph No.5.10Daily return of Ashok Leyland for 2642days

Source: Official website of Bombay Stock Exchange

It can be seen from the graph 5.10 above, that most of the valuesrange between 0-5 plus or minus. The maximum return is 18.22% andminimum -89.2% could be observed from the graph. Minor fluctuationaround the x-axis could be traced out. The return was highly fluctuating asshown by the standard deviation and variance. The daily returns were thicklycoated on either sides of the zero-line. It means the actual returns werearound the mean returns. Still enormous minor and major vibrations werefound about the zero line indicating high level of fluctuations in thedistribution of daily return. The standard deviation of Ashok Leyland was3.79. It is well above 3. Standard deviation above 3 is significant. Theimplication of it was that there were intense and violent errors about themean daily returns signaling high degree of price and return volatility. Onthe left side of the distribution undue swarming or humping could be seen inthe picture indicating negative skewness. It was due to the fact that thedistribution was not symmetrical.

ASHOK LEY

DAILY RETURN

Case Number

2,6422,503

2,3642,225

2,0861,947

1,8081,669

1,5301,391

1,2521,113

974835

696557

418279

1401

Valu

e VA

R00

003

40

20

0

-20

-40

-60

-80

-100

TableNo.5.11Holding period yield of Ashok Leyland for the period1999-2009

YEAR OP CL HPR HPY1999 44.8 114.05 2.55 1552000 123.15 43.75 0.36 -642001 44.6 69.65 1.56 562002 68.7 99.15 1.44 442003 98.2 293.7 2.99 1992004 294 24.4 0.08 -922005 24.65 31.85 1.29 292006 31.8 45.45 1.43 432007 46.25 52 1.12 122008 52.15 15.02 0.29 -712009 15.5 49.55 3.2 220

AM 48.27

Source: Official website of Bombay Stock Exchange

Table 5.11 shows that the company was making a holding periodyield of 48.27% for the period 1999-2009. Except 3 years the companymakes good estimated returns during the decade. The maximum HPY 220%was obtained in the year 2009. In the years 2003 and 1999 HPY earned was199 and 155% respectively. In 2009 the company’s performance wasexceptionally good. In 1999 the HPY of Ashok Leyland was 155%. In 2009it was 220%. There was an overall growth of 42% in the HPY since 1999. Inthree years the HPY was negative. For seven years the HPY was positive.The lowest yield -71% was made in the year 2008. The highest HPY wasoccurred in 2009. The year 2008 was disastrous for the HPY of the stock. Atthe same time the year 2009 was prospective for the firm.On average thetrend of the HPY was rise upwards.

Graph No.5.11Holding period yield of Ashok Leyland for the period 1999-2009

Source: Official website of Bombay Stock Exchange

It can be seen from the graph 5.11 that in 1999 the company wassliding from 155% to reach below cutting the x-axis. Then after 2000 it wentup to 199% in 2003. There from it fell sharply down to the all time low in2004. After that it recovered and gathered momentum better its position bygaining the all time best of 220% in 2009. As the graph shows the HPY ofAshok Leyland had full of twists and turns during the period. The yieldnever stayed anywhere more. It was always instable. There was one peak in2003. Immediately after that a deep trough was followed in 2004. Then in2005 the HPY went up and in 2007 tended to fall down and in 2008 the HPYfell to the all time low. In this way the HPY of Ashok Leyland goes up anddown all time without settling for some time anywhere. It all shows thevolatility of the HPY of the stock. The line HPY starts from a high point. Itends also in a high point. Between these points it had endless ups anddowns. This was due to chaos and uncertainty in the distribution of theholding period yield of the company.

VAR00003

2009.002008.00

2007.002006.00

2005.002004.00

2003.002002.00

2001.002000.00

1999.00

Mea

n V

AR

0000

4

300

200

100

0

-100

-200

Table No.5.12Annual return of Ashok Leyland for the period 1999-2009

Year Return1999 0.502000 -0.332001 0.262002 0.192003 0.472004 -0.402005 0.132006 0.192007 0.082008 -0.432009 0.54

AM 0.11

Source: Official website of Bombay Stock Exchange

As per table 5.12, from 1999 to 2009 the company was making anannual rate of 0.11%. Seven years it made positive returns and 3 yearsnegative. In 1999 the annual return was 0.50%. In 2009 it was 0.54%. Theannual return was growing by 8% since 1999. The highest positive returnwas in 2009 that is 0.54% and the lowest return it earned was in 2008 that is-0.43%. The Year 2008 was worst for Ashok Leyland. The year 2008 haddone much harm to the annual returns to the company. In the decade thestock was making steadily positive returns. Only in 3 years it succumbed tonegative results. High volatility was there in the flow of annual return to thestock. High and lows were coming in alternating years. Ups and downs werecoming year after year. There was uncertainty in the occurring of annualreturns. It was not possible to predict the behavior of annual returns due tothe high volatility.

Graph No.5.12Annual return of Ashok Leyland for the period 1999-2009

Source: Official website of Bombay Stock Exchange

The graph 5.12 shows that the return of the stock Ashok Leyland wasin a zigzag manner as in a see-saw. The return went up and down of the zeroline in alternating years. It reveals greater risk. Sudden uprising and declinecan be observed. The highest positive return of the company was earned inthe year 2009 and lowest was in 2004. Between 1999 and 2009 a sporadicvolatility was found with the pattern of return. As the graph had shown therewere three peaks and three troughs occurred in alternating years. It becamecyclical. This volatility in annual returns can be found repeating year afteryear. It shows the high volatility prevailing in the distribution of annualreturns in the decade. It was starting from a high point in 1999. Then, theannual return was suddenly swinging down to below zero line in 2000. Thenagain recovered and went up to a small peak in 2001. In 2002 it further wentup to a major peak in 2003. In 2004 it abruptly had fallen to deep trough. Inthis way the annual returns were never stable throughout the decade

VAR00003

2009.002008.00

2007.002006.00

2005.002004.00

2003.002002.00

2001.002000.00

1999.00

Mea

n V

AR

0000

5

.6

.4

.2

-.0

-.2

-.4

-.6

5. ASIAN PAINTS

Table No.5.13Summary statistics of Asian Paints from 1999 to 2009

Source: Official website of Bombay Stock Exchange

As per table 5.13 above, the average return of the stock AsianPaints for 10 years was 0.09% which was less than the average return of themarket 0.11% for the same period. The HPY was 23.27%. The company wasunder performing. The company’s performance was much below of whatwas expected of it. The large and small value reveals that the return was notwidely scattered. The dispersion from the mean is normal. The standarddeviation 2.09 is not significant. Therefore the company is making a stablereturn for the period. The return varies in between positive 11.61% and anegative 36.19% amounting to range of 47.8. Hence the distribution wastighter. The skewness -2.9 is significant . It says that the return is not onlyasymmetrical but negatively skewed. The kurtosis 57.87 signals leptokurticform of peakedness. The correlation 0.006 between the company and themarket is insignificant. The systematic risk denoted by beta 0.007 is low. R2

says that 1% of the variance is explained by the market. 99% variance isunexplained by the market. The scrip was not much market-related duringthe period.

Average return 0.09% Skewness -2.9σ 2.09 Variance 4.35L 11.61% cov 0.02S -36.19% kurtosis 57.87Range 47.8 cor. 0.006Beta 0.007R2 0.000036 HPY 23.27

Market return 0.11

Graph No.5.13Daily return of Asian Paints for 2642 days

Source: Official website of Bombay Stock Exchange

It can be seen from the above figure that the return is negativelyskewed. The largest return 11.61 and the smallest 36.19% could be locatedfrom the graph. The tightness of the distribution could also be discerned. Lotof minor fluctuations around the zero line can be viewed. The volatility ofstock return about the mean value can be observed. The values were foundlying within a range of 0-5%±. The values were thickly coated along the lineof X. Some values had shown tendency to fall down to the line of abscissaoccasionally can also been located from the figure. Undue humping ofvalues on the left hand side of graph can be seen due to the presence ofnegative skewness of daily returns. From the graph it could be understoodthat the distribution of the daily returns was not symmetrical. Minorvibrations could be located on either side of the mean returns. The lowestand highest daily returns were found in the graph. The volatility in the dailyreturns was not very strong. But small errors were running around the meanof daily returns.

Case Number

2,6422,503

2,3642,225

2,0861,947

1,8081,669

1,5301,391

1,2521,113

974835

696557

418279

1401

Valu

e VA

R00

002

20

10

0

-10

-20

-30

-40

Table No.5.14Holding period yield of Asian paints for the period1999-2009

YEAR OP CL HPR HPY1999 285.5 370 1.3 302000 389.95 276.6 0.71 -292001 272 271.5 1 02002 265.85 324.65 1.22 222003 324.5 336.15 1.04 42004 336.7 320.15 0.95 -52005 320 577.4 1.8 802006 589.75 733.55 1.24 242007 740.85 1102.55 1.49 492008 1136.3 895.1 0.79 -212009 888 1796.25 2.02 102

AM 23.27

Source: Official website of Bombay Stock Exchange

As per table 5.14above, the average holding period yield of AsianPaints was 23.27% which was the expected return of the company. The HPYwas the highest in 2009 with 102%. The lowest was in the year 2000 with -29%. In 2001 the company made no yield at all. In 1999 the HPY of AsianPaints was 30%. In 2009 it was 102%. The HPY had increased 3.4 timessince 1999. In 3 years the HPY was negative. In 7 years the HPY waspositive. The tendency of the HPY was to grow. Even though the companyhad made positive HPY in almost all years in the decade the magnitude ofthis was highly uncertain. Despite the fact that Asian paints made good HPYin the entire period, the HPY was highly erratic. There was no certainty inthe occurrence of the HPY. The pattern and magnitude of the HPY werehighly chaotic. The pattern was uncertain because in a year the HPY was80%, in another year it was 5%. In still another year the HPY was zero. Insome years the HPY was positive and in some other year it was negative. Inthis way the pattern and the magnitude of the HPY of Asian paints had nocertainty. This chaotic behavior entails high level of volatility to the scrip ofAsian paints.

Graph No.5.14Holding Period Yield of Asian Paints for the period 1999-2009

Source: Official website of Bombay Stock Exchange

It could be seen from the graph 5.14 that the HPY of Asian Paintswas highly volatile throughout the decade. As in a see-saw the HPY wasswinging went up and down with constancy throughout the period. But theoverall tendency could be located from the figure that the HPY continuouslygrowing upward. In the year 2009 HPY had been reached a new height in itsperformance. The graph vindicates what was said earlier about the HPY ofAsian Paints. The HPY was driving towards persistently higher and higherpoints of yields. But here and there it confronted resistance and broke down.But the HPY was relentlessly was going towards better results. This thrust ofthe holding period yields of Asian Paints could be learnt from the figure. Inthe travel it faced four minor major troughs and similar peaks also. Thenumber of peaks and troughs tell the intensity of the volatility in thedistribution of the HPY. More ups and downs were found in the case ofAsian paints in varying pattern and magnitude. The more it is, the high thevolatility of the HPY.

VAR00003

2009.002008.00

2007.002006.00

2005.002004.00

2003.002002.00

2001.002000.00

1999.00

Mea

n V

AR

0000

4

120

100

80

60

40

20

0

-20

-40

Table No.5.15Annual return of Asian paints for the period 1999-2009

Source: Official website of Bombay Stock Exchange

As per table 5.15 above, the average annual return of the stock AsianPaints for the period 1999-2009 was 0.09%. In 1999 the annual return was0.15%. In 2009 it was 0.32%. The annual return during the period had beenincreased at the rate of 113% since 1999. In 3 years the annual return wasnegative. In 7 years it was positive. The annual return was the highest in2009 and lowest in 2000. The overall tendency of the annual return was togrow. As shown by the table, the annual returns’ behavior was similar to theholding period yields of Asian paints. While the annual return in 1999 waspositive, it went negative in the next year itself in 2000. Then in the nextyear there was no annual return at all in 2001. Then in 2002 and 2003 thescrip made nominal annual return. After that again 2004, the returns becamenegative. After that there was steady progress in the annual returns till 2008.In 2008 again it earned negative returns. In this way negative positivereturns were earned by the stock in an alternating way. This was due to thehigh price volatility in the market. Therefore high level of uncertainty andchaos found with the annual return of Asian Paints.

Year Annual Return1999 0.152000 -0.082001 0.002002 0.092003 0.052004 -0.012005 0.252006 0.112007 0.192008 -0.072009 0.32

AM 0.09

Graph No.5.15Annual Return of Asian Paints for the period 1999-2009

Source: Official website of Bombay Stock Exchange

As Graph 5.15 showed, in 1999 annual return of Asian paints wasvery high. There after it declined. From 1999 to 2009 the annual return linewas moving across wide fluctuations. Therefore the line of annual returnwas erratic and zigzag. Though the trend was to grow up, the annual returnwas highly volatile in nature. While the annual return in 1999 was positive,in 2000 it went negative. It could be easily found that the fluctuations inannual returns from the graph above. From the beginning of the annualreturn curve to its end in 2009, it went across numerous ups and downs oneafter another. There was no stability to any trend. There was no trend at all.In one year the annual return was positive. In the next year itself it turns tothe opposite. Still the persistent trend that was underlying could be locatedfrom the graph vividly. It was that of going up. But there prevailsuncertainty and chaos as to the accuracy about the occurrence of the returnswhether it would be negative or positive or whether it would be a bigamount or low amount. This form of uncertainty was there in the pattern andmagnitude of the annual returns of Asian Paints.

VAR00003

2009.002008.00

2007.002006.00

2005.002004.00

2003.002002.00

2001.002000.00

1999.00

Mea

n V

AR

0000

5

.4

.3

.2

.1

0.0

-.1

-.2

6. BALLARPUR INDUSTRIES

Table No.5.16Summary statistics of Ballarpur Industries from 1999 to 2009

Source: Official website of Bombay Stock Exchange

As per table 5.16 the average return of Ballarpur was 0.08% whichwas lower than the market average of 0.11%. The expected return based onthe HPY was 16.64%. Company’s average performance for the ten yearperiod was lower than the HPY. The dispersion from the expected value wassignificant as expressed by the standard deviation 3.6. The scrip had made amaximum return of 21.69% and minimum of -79.61% during this period.This amounts to total range of 101.3 which shows a greater amount ofvariance. The values greatly vary in between the large and small. There isgreater amount of uncertainty in the occurrence of return. The skewness -3.49 was significant in the sense that the distribution was negatively skewed.The variance also tells the same tales that there is greater fluctuation in thereturn stream of the company. The variance 13 was significant. The kurtosis90.41 signals peakedness to the character of leptokurtic. The correlation co-efficient 0.023 is not important. The beta 0.0464 does not express anyserious systematic risk. R2 value 0.0005 is insignificant that the variancemainly owing to the own performance of the company.

Average return 0.08% Skewness -3.49σ 3.6 Variance 13L 21.69 cov 0.148S -79.61 kurtosis 90.41Range 101.3 cor. 0.023Beta 0.0464R2 0.0005 HPY 16.64

Market return 0.11%

Graph No.516Daily return of Ballarpur for 2642 days

Source: Official website of Bombay Stock Exchange

Graph 5.16 shows the pattern of the daily return for the company forthe ten year period from 1999 to 2009. The daily return was thickly packedalong the X-axis with few exceptions. Barring some occasional outspreadsthe return in general was permeated along the zero line. The return wasspread within a range of 0-5%. The high and low values can be located fromthe graph easily. The daily returns had lot of minor variations around andabout the line of X axis. Excessive grouping of values can be located on theleft hand side from the center of the zero line due to negative skewness. Thestandard deviation and variance of the daily returns were found significant.The varying trend of the individual returns from the mean could beidentified from the graph. The daily return was shown in the graph as thicklypacked. The density of the values could be grasped from the figure. Thedaily returns of Ballarpur industries were due to excessive price fluctuationsin the market for its stock.

BALLARPUR

DAILY RETURN

Case Number

2,6422,503

2,3642,225

2,0861,947

1,8081,669

1,5301,391

1,2521,113

974835

696557

418279

1401

Valu

e VA

R00

002

40

20

0

-20

-40

-60

-80

-100

Table No.5.17Holding period yield of Ballarpur for the period 1999-2009

YEAR OP CL HPR HPY1999 27.85 58.25 2.09 1092000 62.9 63.05 1 02001 64.4 40.9 0.64 -362002 40.2 43 1.07 72003 43 82.3 1.91 912004 83.2 93.95 1.13 132005 98.15 112.15 1.14 142006 112.95 107.5 0.95 -52007 109.35 173.4 1.59 592008 181.6 20.7 0.11 -892009 20 23.95 1.2 20

AM 16.64

Source: Official website of Bombay Stock Exchange

The Table 5.17 shows the HPY of Ballarpur Industries for the periodfrom 1999 to 2009. The HPY of the stock on an average for the period was16.64%. In 1999 the HPY was 109%. In 2009 it was 20%. The HPY duringthe period had been declined by 82%. In 2000 the HPY was zero. The HPYwas largest in 1999 and smallest in 2008. The year 2008 was very bad forBallarpur Industries. In 3 three years Ballarpur earned negative HPY. In 7Years there was positive HPY. Generally, the tendency of the HPY was todecline. The HPY in the beginning and at the close of the decade showedgreater difference. The HPY from 109% in 1999 had fallen to a mere 20 %in 2009 after 10 years meant greater failure in the performance of the stockin the market. It might be due to the price volatility in the market. The stockearned positive yields in all seven years. Only in three years it was subject tonegative returns. But the impact of three years’ negative performance washighly detrimental. The year 2008 had done much damage to the HPY ofBallarpur.

Graph No.5.17Holding period Yield of Ballarpur for the period 1999-2009

Source: Official website of Bombay Stock Exchange

The graph 5.17 shows that HPY line starts from a peak 109% in 1999 felldown to zero in 2000. It fell further below X-axis to -36 where it bottomedout for a recovery to another peak with 91% in 2003. Again it moveddownward and rose and fell sharply the all time low of -89% before it risesto 20% in 2009. Though HPY was positive in almost all cases except in 3years the overall tendency was to fall down. The HPY was erratic andmostly uncertain. The ups and down showed by the HPY denotes theexistence of high degree of volatility in returns during the period. Theadversity for the scrip Ballarpur Industries with lowest HPY in 2008 can beseen from the figure. The behavior of the HPY of Ballarpur Industries couldbe easily understood from a glance of the graph. It was highly volatile. Thecurve with numerous major and minor swings-downward and upward-hadsettled at relatively a lower point by showing the persistent trend as that ofdeclining over years.

VAR00007

2009.00

2008.00

2007.00

2006.00

2005.00

2004.00

2003.00

2002.00

2001.00

2000.00

1999.00

Mea

n VA

R00

008

200

100

0

-100

Table No.5.18Annual return of Ballarpur for the period 1999-2009

Year Annual Return1999 0.422000 0.112001 -0.132002 0.062003 0.282004 0.092005 0.092006 0.032007 0.222008 -0.532009 0.14

AM 0.07

Source: Official website of Bombay Stock Exchange

The Table 5.18 shows the annual returns of Ballarpur Industries forthe period from 1999 to 2009. The annual returns of the stock on an averagefor the period were 0.07%. In 1999 the annual returns were 0.42%. In 2009it was 0.14%. The annual returns during the period had been declined by67%. The annual return was largest in 1999 and smallest in 2008. The year2008 was very bad for Ballarpur Industries. In 2 years Ballarpur earnednegative returns. In 8 Years there were positive annual returns. Generally,the tendency of the annual returns was to decline. In spite of the stock beingearned positive returns for seven years, the underlying trend was identifiedas that of declining. This was because of the frequent interruption by thedownswing in the annual returns. The downswing was due to nothing but theprice volatility in the market. The continuous earning of the annual returnswas now and then deterred by adverse changes in the stock price in themarket. That was why after making seven years positive returns the stockbecame unable to prosper.

Graph No.5.18Annual returns of Ballarpur for the period 1999-2009

Source: Official website of Bombay Stock Exchange

The graph 5.18 shows, that the behavior of the annual average returnwas very similar to that of the HPY for the period. From 1999 to 2008 theaverage return tends to fall and reaches the all time low of the decade in2008. In 2009 a recovery was achieved and the annual average returnincreased to 0.14%. The curve of annual returns was highly volatile anderratic. The general trend of the annual return of Ballarpur was to decline.The curvature of the annual returns in the graph was shown as highly erratic.It was frequently disrupted and fractured by the downtrend. Frequentinterruptions marred the continuity of the annual returns line could be foundbroken. It was due to the wild uncertainties and fluctuations in the stockprices in the market. The price volatility in the market paved the way for theannual returns volatility since the returns were perceived from the prices ofthe stocks in the market. Therefore lower the price lower will be the returnsalso. As such the volatility was intense in the behavior of the annual returnsof Ballarpur Industries. This could be discerned from the nature of thecurvature of the annual returns curve in the graph. The curve had all thetravails of frequent disruptions and interruptions that was why the annualreturns could not be able to finish impressively in spite of seven yearspositive returns.

VAR00007

2009.002008.00

2007.002006.00

2005.002004.00

2003.002002.00

2001.002000.00

1999.00

Mea

n VA

R00

009

.6

.4

.2

-.0

-.2

-.4

-.6

7. CASTROL

Table No. 5.19Summary statistics of Castrol from 1999 to 2009

Source: Official website of Bombay Stock Exchange

As per table 5.19 above the average return of Castrol was 0.02%which was lower than the market rate of return of 0.11%. Expected returnbased on the performance of the company in the decade was 4.82% whichwas much above the actual. The standard deviation 2.34 was not important.The actual would be almost near the average return. The range of variationbetween the largest and smallest value to the extent of 66.06 wasinsignificant. The variance 5.45 was below the point of significance. Thestandard deviation and the variance did not tell any significant volatility. Thedistribution of return as stated by the skewness -2.49 revealed the presenceof high asymmetry. The distribution was skewed negatively. The kurtosis71.1 is big and significant peakedness of the form of leptokurtic could beobserved. The beta value 0.008 was not significant. The relative volatilitybetween the company and the market was less. R2 value confirmed that lessthan 1% of the variance 5.45 was explained by the market and 99.99% wasunexplained.

Average return 0.02% Skewness -2.49σ 2.34 Variance 5.45L 17.67 Cov 0.025S -48.39 kurtosis 71.1Range 66.06 cor. 0.006Beta 0.008R2 0.000036 HPY 4.82

Market return 0.11%

Graph No. 5.19Daily return of Castrol for2642 days

Source: Official website of Bombay Stock Exchange

The graph 5.19 showed that the daily return of Castrol Ltd coincided mostlywith the zero line and ranged between zero and plus or minus 5% asdepicted by the Graph. Extreme values occurred only occasionally. Thelowest return of -48.39% could be traced from the figure. The highest returnearned during the decade could also be located from the figure. It could beidentified that the return was highly negatively skewed. Lot of minorvolatility around and about the zero line can be seen. The daily returns ofCastrol were highly volatile during the period. The daily returns of the stockwas found in the graph as thickly pasted on either side of the mean returnThe mean return of Castrol was given in the summary statistics tableNo.5.19 as 0.02%. So it could easily be found that the earnings were denselypacked within the immediate range of 0-1%. Some values could also belocated outside this range up to 5%. But majority of values were shown inthe graph lying in between 0-1% range. The standard deviation of the returnswas not significant. The standard Deviation given in the summary StatisticsTable No 5.19 was 2.34. It only confirms the tightness of the distribution.Only minor insignificant fluctuations in earning could be seen from thegraph.

CASTROL

DAILY RETURNS

Case Number

2,6422,503

2,3642,225

2,0861,947

1,8081,669

1,5301,391

1,2521,113

974835

696557

418279

1401

Val

ue V

AR

0000

3

40

20

0

-20

-40

-60

Table No.5.20Holding period yield of Castrol for the period 1999-2009

YEAR OP CL HPR HPY1999 758.25 305.15 0.4 -602000 329.55 273.25 0.83 -172001 276.35 187.6 0.68 -322002 187.8 210 1.12 122003 209.65 237.9 1.13 132004 239.25 217.8 0.91 -92005 217.85 252.3 1.16 162006 254 227.9 0.9 -102007 223 360.65 1.62 622008 350.75 335.5 0.96 -42009 333.7 605.8 1.82 82

AM 4.82

Source: Official website of Bombay Stock Exchange

Table 5.20 showed that The HPY of Castrol on an average for theperiod from 1999 to 2009 was 4.82%. In 1999 the HPY was -60%. In 2009 itwas 82%. The HPY had increase by 136% since 1999. In the initial threeyears of the decade the company made negative holding period yields. In theyear 1999 the return was the lowest to the extent of -60%. Then in 2000 itimproved a little but continued to earn negative HPY of -17%. The highestpositive return was earned in the year 2009 to the tune of 82%. On anaverage holding period yield for the 10 year period from 1999 to 2009 was4.82%. The holding period yield for 2009 was a high 82%. Still the overallholding period yield of the stock for the 10 year period was only 4.82%. Itwas due to frequent downside movement of the price of the stock in themarket. The growth in holding period yields was at times blocked by theoccurrence of negative returns. The traces of the volatility could be foundwith the holding period yields of the stock for the period.

Graph No.5.20Holding Period Yield of Castrol for the period 1999-2009

Source: Official website of Bombay Stock Exchange

The graph 5.20 shows the pattern of the holding period yield Castrol.Since 1999 the yield was rising upwards. The trend of the HPY line is to goup in a stair step manner. From -60% in 1999 the HPY ascended to 82% in2009 gradually and successively year after year. The lowest HPY could belocated in the graph in the year 1999 and the highest in the year 2009. Thecurvature of the holding period yield curve shows that it was confronting alot of strife before it reached the end point. Frequent disruptions,downswings, resistance and all that pull the curve down from going up. Stillthe stock managed to finish positively at the end of the decade in a stair stepmanner. The simile stair-step was meaningful in every respect in the sensethat as in a stair-step for every step upward there will be immediate downstep. But generally the purpose of the stair-step is to go up. In the same waythe overall tendency of the holding period curve was to go up but frequentlyfacing down steps at every up step.

VAR00003

2009.00

2008.00

2007.00

2006.00

2005.00

2004.00

2003.00

2002.00

2001.00

2000.00

1999.00

Mea

n VA

R00

004

100

80

60

40

20

0

-20

-40

-60

-80

Table No.5.21Annual return of Castrol for the period1999-2009

Year Annual Return1999 -0.242000 -0.042001 -0.122002 0.052003 0.072004 -0.022005 0.082006 -0.032007 0.212008 0.022009 0.26

AM 0.02

Source: Official website of Bombay Stock Exchange

Table 5.21 shows that annual return of Castrol in 1999 was -0.24%and in 2009 it was 0.26%. The lowest annual return was recorded in the year2004 as -0.02%. The annual return was highest in 2009 with 0.26%. From1999 onwards the negative return was improving and by 2002 it becamepositive to the tune of 0.05%. The last three years of the decade alsorecorded positive returns. The highest annual return was recorded in 2009.Castrol had made negative returns and positive returns in 5 years each. Theoverall result was that the company made a 0.02% return for the 10 yearperiod. The annual return also behaves in the same way as the HPY. It wasincreasing from -0.24% to 0.26%. The growth in the annual return wastremendous during the period in spite of frequent interruptions by theoccurrence of negative returns. The volatility that caused the negative returncreated lot of chaos and uncertainty in the occurrence of annual returns. Thetable gives details of high levels of volatility.

Graph No.5.21Annual return of Castrol for the period 1999-2009

Source: Official website of Bombay Stock Exchange

From the graph 5.21 the behavior of annual return of Castrol could beunderstood. The annual return moves upward from the deep fall of negative0.24% to the topmost place of 0.26% in 2009 step by step year after year.The shape of the annual return line is like stair-step. The overall trend of theannual return for the decade is that of a steady growth from -0.24 to 26%.There were lots of ups and down throughout the period which were indicatedby the line of annual return. The behavior showed by the table could beunderstood from the graph. The graph represents high level of fluctuations inthe annual returns of the stock. The overall effect of the annual returns wasto go up. But at times the rise of the annual returns curve was checked anddisrupted by the downtrend movements. This caused the volatility in theannual returns. The consequence of it was that no one could predict theoccurrence of annual returns on the stock. The volatility was there in annualreturns of the company in respect of the timing and magnitude of it.

VAR00003

2009.002008.00

2007.002006.00

2005.002004.00

2003.002002.00

2001.002000.00

1999.00

Mea

n VA

R00

005

.3

.2

.1

-.0

-.1

-.2

-.3

8. CENTURY TEXTILES

Table No.5.22Summary Statistics of Century from 1999 to 2009

Source: Official website of Bombay Stock Exchange

The summary statistics of Century Textiles for the period was shownby Table 5.22. On an average the company earns a return of 0.17% contraryto the expected 53%. The performance was better than the market return0.11%.The standard deviation 3.29 was significant. The largest rate of returnearned was 22.84% and the smallest rate was -24%. The breadth between thelarge and small was 46.84. The daily return varied in between this boundary.Therefore the return was tightly and closely bonded within the expectedvalue or mean value that is 0.17%. The chances for the wide variability arerare and remote. Therefore the standard deviation 3.98 does not tell muchvolatility. The distribution of return is positively skewed to the right. Themeasure of skewness 0.18 is not significant. The variance 15.82 issignificant. The kurtosis 2.8 denotes some amount of peakedness near toleptokurtic. The distribution is not symmetric. The co-efficient of correlation0.003 is not significant. The relative volatility of the company in relation tothe BSE represented by the statistic beta 0.01 was not significant. But therisk of the company vis-à-vis the market is lower. R2 only confirmed it.Accordingly 0.000009% of the variance was explained by the market.99.99% was explained by company’s own factors. The HPY which wasconstrued as the expected return over a period of 10 years is 53%. Howeverthe company’s average return was lower than HPY.

Average return 0.17% Skewness 0.18Σ 3.98 Variance 15.8L 22.84 cov 0.021S -24 kurtosis 2.82Range 46.84 cor. 0.003Beta 0.01R2 0.000009 HPY 53%

Market return 0.11%

Graph No.5.22Daily return of Century for 2642 days

Source: Official website of Bombay Stock Exchange

In the Graph.5.22 over a period of 10 years on 2642 observation thedetails of the daily return of Century Textiles are shown. The daily returnwas found thickly packed along the X-axis. Barring occasional rise and fallhither and thither most of the daily return had occurred with range 0-8%±.The largest daily return could be noted at the 557th observation clearly.Similarly the smallest daily return was registered at the same level. Theskewness could also be located slightly to the right side. The daily returnshad high degree of volatility. A thick band of returns was densely formed oneither side of the mean value. The number of values surrounding the meanreturn was immense. The standard deviations variance of returns could beobserved from the graph. They are all significant. The daily returns were allhighly volatile in nature. The volatility could be seen from the graph.

CENTURY

DAILY RETURNS

Case Number

2,6422,503

2,3642,225

2,0861,947

1,8081,669

1,5301,391

1,2521,113

974835

696557

418279

1401

Val

ue V

AR

0000

4

30

20

10

0

-10

-20

-30

Table No.5.23Holding period yield of Century for the period1999-2009

YEAR OP CL HPR HPY1999 42.6 58 1.36 362000 62.6 42 0.67 -332001 43.95 37.65 0.86 -142002 38.2 49.4 1.29 292003 53.9 140.25 2.6 1602004 144.55 176 1.22 222005 186.45 299.65 1.61 612006 301.35 739.8 2.45 1452007 739.8 1170.45 1.58 582008 1207.6 166.65 0.14 -862009 175.1 528.05 3.02 202

AM 52.73

Source: Official website of Bombay Stock Exchange

Table 5.22 above shows the holding period yield of Century Textiles forthe period 1999-2009. The largest HPY for the study period was 202% in theyear 2009. Lowest HPY was registered as -86% in 2008. Century Tex hadmade negative HPY in 3 years and positive returns in 7 years. The overalltendency of the HPY had been to rise upwards. In 1999 the HPY of Centurywas 36%. In 2009 it was 202%. The HPY had increased during this period ata rate of 461%. The tendency of the HPY was to grow. The average of HPYfor the decade was 53%. The year 2008 had detrimental impact on the HPYof the stock. The table showed the presence of high level of volatilitythroughout the decade.

Graph No.5.23Holding Period Yield of Century Textiles for the period 1999-2009

Source: Official website of Bombay Stock Exchange

The graph 5.22 above shows the picturization of the facts analysedabove as to the HPY of Century Textiles. The high and low of HPY can beviewed from the graph clearly. There were 3 peaks and 3 troughs in thepicture. It reveals the thick and thin through which the company crossedduring the period. The high and low HPY happens with an alternatingregularity. The overall trend of the HPY was that of ever increasing. Theincreasing trend of the HPY was at times marred by the upswing anddownswing trends. It was due to major volatility in the market andconsequent volatility in the HPY. The second trough was depicted in thegraph was a major one. The year 2008 inflicted major impact on the HPY ofthe stock.

VAR00001

2009.002008.00

2007.002006.00

2005.002004.00

2003.002002.00

2001.002000.00

1999.00

Mea

n VA

R00

002

300

200

100

0

-100

-200

Table No.5.24Annual return of Century Textiles for the period 1999-2009

Source: Official website of Bombay Stock Exchange

The table 5.23 shows the behavior of average annual rate return ofCentury Textiles during 1999-2009. In 1999 the company had annual returnof 0.27% whereas in 2009 it was 0.53%. The return of 2009 was the highestduring the study period. Lowest annual return was fetched in the year 2000to the tune of -0.06%. The highest positive annual return was 0.53% in 2009and the lowest return was in 2001with an amount of 0.06%. Only in twoyears the company had made negative returns. It made positive annualreturns in 8 years. So the trend was that the scrip regularly makes a positivereturn. The down trend was only limited in the case Century Textiles. Theoverall performance of the company was appreciable. But frequentdowntrends could be observed from the table. There was immense volatilityin the distribution of the holding period yield of the stock Century Enka.

Year Return1999 0.272000 -0.062001 0.062002 0.202003 0.452004 0.152005 0.232006 0.442007 0.242008 -0.662009 0.53

AM 0.17

Graph 5.24Annual return of Century Textiles for the period 1999-2009

Source: Official website of Bombay Stock Exchange

Graph 5.23 Shows, the picturization of the annual return of CenturyTextiles during the study period. The negatively skewed distribution hadmainly 3 troughs and 4 peaks. Peaks and troughs occur regularly in analternating manner. The lowest return registered was notable in the graph. Inspite of a fall in 2008 the annual return fervently jumps up in the year 2009itself. The fall in the year 2008 was the deepest of all. Similarly there weremany peaks in the figure but the one in 2009 was the topmost of all. Theannual return shows wide fluctuations. The peaks troughs and ups anddowns create undue uncertainty over the occurrence of the returns. Thevolatility becomes the reasons for the unpredictability of the annual returns.The magnitude of the volatility and fluctuations could be seen vividly fromthe graph.

Annual Average Return

in %

Year

VAR00004

2009.002008.00

2007.002006.00

2005.002004.00

2003.002002.00

2001.002000.00

1999.00

Mea

n VA

R00

005

.6

.4

.2

0.0

-.2

-.4

-.6

-.8

9. CENTURY ENKA

Table 5.25Summary statistics of CENTURY ENKA from 1999 to 2009

Source: Official website of Bombay Stock Exchange

Table shows the summary statics of the performance of Century Enkafor the period 1999-2009. The annual average rate of the firm during thestudy period was 0.12%. It is more than the average return earned by themarket portfolio. The market average return for the period was 0.11%. Butthe expected return represented by the Holding Period Yield for the sameperiod was 51.82% which was more than the average return and marketreturn. The largest daily return of the company was recorded as 20%. Thesmallest return was -12.52%. The difference between the large and small is32.52. This difference is not statistically a significant. The standarddeviation that measures the dispersion from the average for the companywas worked out at 3.12. It shows that the events are not widely scattered andthe distribution is tightly packed. Therefore the worked standard deviation isnot significant. The systematic risk component beta for the company is only0.116. The firm’s systematic or market related risk is less than the marketportfolio since the beta value for the market is 1. The R2 value of thecompany is 0.004. It confirms the fact that the beta value of the company isnot significant. The implication is that out of the total variance 9.72 only0.004% of it will be explained by the market. The other 99.6 % of the totalvariance is unexplained by the market. The distribution of the return of thecompany is asymmetric. It is positively skewed to the extent of 0.53. Valuesare more leaned towards the right side of the distribution. Therefore, there is

Average return 0.12% Skewness 0.53σ 3.12 Variance 9.72L 20 cov 0.371S -12.52 kurtosis 2.2Range 32.52 cor. 0.066*Beta 0.116R2 0.004 HPY 51.82

Market return 0.11%

peak formation in the distribution to the level of 2.2 to the right of thedistribution. The peakness is almost leptokurtic. The correlation that existsbetween the company and the market is worked out at 0.066 which issignificant at 0.01 level of significance.

Graph No.5.25Daily return of Century Enka for 2642 days

Source: Official website of Bombay Stock Exchange

The graph 5.24 depicts the pattern of daily returns obtained by thestock Century Enka. There were 2718 days of observation over a continuousperiod of 10 years from 1999. The daily returns were highly fluctuatingaround the X-axis. The returns were largely packed along the zero line within a range of 0-10 per cent±. The fluctuations were major and minor. Thelargest daily return is visible from the graph which was located on the 1002nd

observation. The distribution was closely knitted that there is probability forthe occurrence of the expected return. There was no greater uncertainty onthe occurrence of the expected value.

CENTURY ENKA

DAILY AVERAGE RETURN

NO.OF OBSERVATIONS

Case Number

2,718

2,575

2,432

2,289

2,146

2,003

1,860

1,717

1,574

1,431

1,288

1,145

1,002

859

716

573

430

287

144

1

Valu

e VA

R00

001

30

20

10

0

-10

-20

Table No.5.26Holding period yield of Century Enka for the period 1999-2009

YEAR OP CL HPR HPY1999 37.05 67.9 1.83 832000 73.3 44.5 0.61 -392001 44.45 55.5 1.25 252002 57 86.95 1.53 532003 88.35 173.15 1.96 962004 175.75 159.4 0.91 -92005 158.9 229.9 1.45 452006 231.45 139.3 0.6 -402007 141.05 183.5 1.3 302008 187.45 61.5 0.33 -672009 62.25 306.6 4.93 393

AM 51.82

Source: Official website of Bombay Stock Exchange

The table 5.25 depicts the holding period yield of Century Enkafor the period of 1999-2009. The average holding period yield is 51.82% forthe entire study period. In 1999 the HPY was 83%. At the close of thedecade 2009 the HPY was 393%. The growth of HPY for the 10 year periodwas 4.7 times. The highest HPY was earned during 2009. The lowest wasearned in 2008 a yield of -67%. Four years the HPY was negative. 6 yearsthe company earned positive yields. The tendency manifested by the HPY isthat to increase more and more. The year 2009 was prospective for CenturyEnka but 2008 the most adverse. Negative returns caused high volatility inthe holding period yield of the stock. Even though the stock earned positivereturns in six years the magnitude and the time had no consistency. It meansthe prevalence of high degree of volatility in the holding period yield of thestock Century Enka.

Graph No.5.26Holding Period Yield of Century Enka for the period 1999-2009

Source: Official website of Bombay Stock Exchange

As denoted by the table 5.25 the HPY of the century enka was notsteady. It had violent swings and ups and downs. The yield was highlyerratic. In 1999 the HPY had good start from a value well above the zeroline. But in 2000 it went down below the X axis. Then in 2001 HPY went upabove the abscissa. In 2002 it reached a peak point to fall below the zero linein the next year. From 2000 onwards the trend was to fall and touch the axis.But accidentally after 2008 the HPY shot up steeply to reach a handsome alltime high value. The behavior of HPY was highly frivolous and transientforming a see-saw pattern. The volatility was conspicuous from the graph.The holding period was in a cyclical fashion advances to the end of theperiod in a straight line. The path was full of minor and erratic movements.There was large amount of fluctuations which were visible from the graph.

VAR00003

2009.00

2008.00

2007.00

2006.00

2005.00

2004.00

2003.00

2002.00

2001.00

2000.00

1999.00

Mea

n V

AR

0000

4

500

400

300

200

100

0

-100

Table No.5.27Annual return of Century Enka for the period 1999-2009

Year Return1999 0.3742000 -0.1312001 0.1102002 0.2332003 0.3162004 0.0052005 0.1782006 -0.1682007 0.1432008 -0.3972009 0.702

AM 0.124

Source: Official website of Bombay Stock Exchange

The table 5.26 above shows the annual rate of return Century Enka forthe period 1999-2009. In the year 1999 the average annual rate of return was0.37%. At the end of the period 2009 the average return was 0.7%. Thehighest annual rate of returns was 0.7%. The lowest return was -0.397% inthe year 2008. The rate of growth of annual return since 1999 is 89%. Theannual return for entire period was 0.12%. The expected value of annualreturns was 0.12%. The actual annual returns were considerably differentfrom the expected value. There were high fluctuations about the expectedvalue. Moreover, there were negative returns also. These create lot of upsand downs in the annual returns. The magnitude of the volatility was veryhigh in the cases annual returns.

Graph No.5.27Annual returns of Century Enka for the period 1999-2009

Source: Official website of Bombay Stock Exchange

The graph 5.26 above shows the behavior of the annual rate ofreturn of Century Enka. The line which shows the annual return starts from ahigher point in the Y axis and falls below the zero line in the next year2000.Then rises and goes up, then again slides after making a peak. A seriesof peaks and troughs were made during the period. The overall tendency isto go down and touch X axis. The behavior of annual returns in 2009 wasexceptional. The line of annual returns shows greater volatility. There werefull of ups and downs in the annual returns. The frequent interruptions andviolent vibrations were seen in the graph. Therefore, it could be said thatthere existed high degree of volatility in the annual return of the scripCentury Enka.

VAR00003

2009.002008.00

2007.002006.00

2005.002004.00

2003.002002.00

2001.002000.00

1999.00

Mea

n V

AR

0000

5.8

.6

.4

.2

-.0

-.2

-.4

-.6

10.COLGATE PALMOLIVE

Table No.5.28Summary statistics of Colgate Palmolive from 1999 to 2009

Source: Official website of Bombay Stock Exchange

The table 5.27 shows the summary statistics of the performance ofColgate Palmolive for the period 1999-2009. The average return based onthe daily return of the company was 0.07%. The market return for the sameperiod was 0.11%. Colgate’s return was lower than the market returns.Similarly, the expected return based on the Holding Period Yield of thecompany was 12.91%. The firm’s average return was also lower than theHPY. The largest daily return was 20.34%. The smallest daily return was -9.8%. The quantitative difference between the large and small is 30.14.Hence the dispersion of the return is not big. The return was closely andtightly bonded and would be lying about and around the expected value. Thestandard deviation 2.06 is not significant. Distribution of the return is notsymmetrical. The skewness worked out as 0.88 is highly significant andconfirms a high level positive skewness to the right in the distribution. Thecoefficient kurtosis 6.47 is also significant. There is peakedness in thedistribution. As the kurtosis is more than 3 the peakness is clled asleptokurtic. The coefficient of correlation 0.011 is not significant. There isonly slight relation with the market. The comovement denoted by thecovariance is 0.041 is insignificant. The beta tells that the systematic risk ofthe firm is lower than the market portfolio. The R2 value 0.0001 confirmsthat there is no much market dependence in the case of Colgate Palmolive.

Average return 0.07% Skewness 0.88Σ 2.06 Variance 4.25L 20.34% cov 0.041S -9.8% kurtosis 6.47Range 30.14 cor. 0.011Beta 0.013R2 0.0001 HPY 12.91

Market return 0.11%