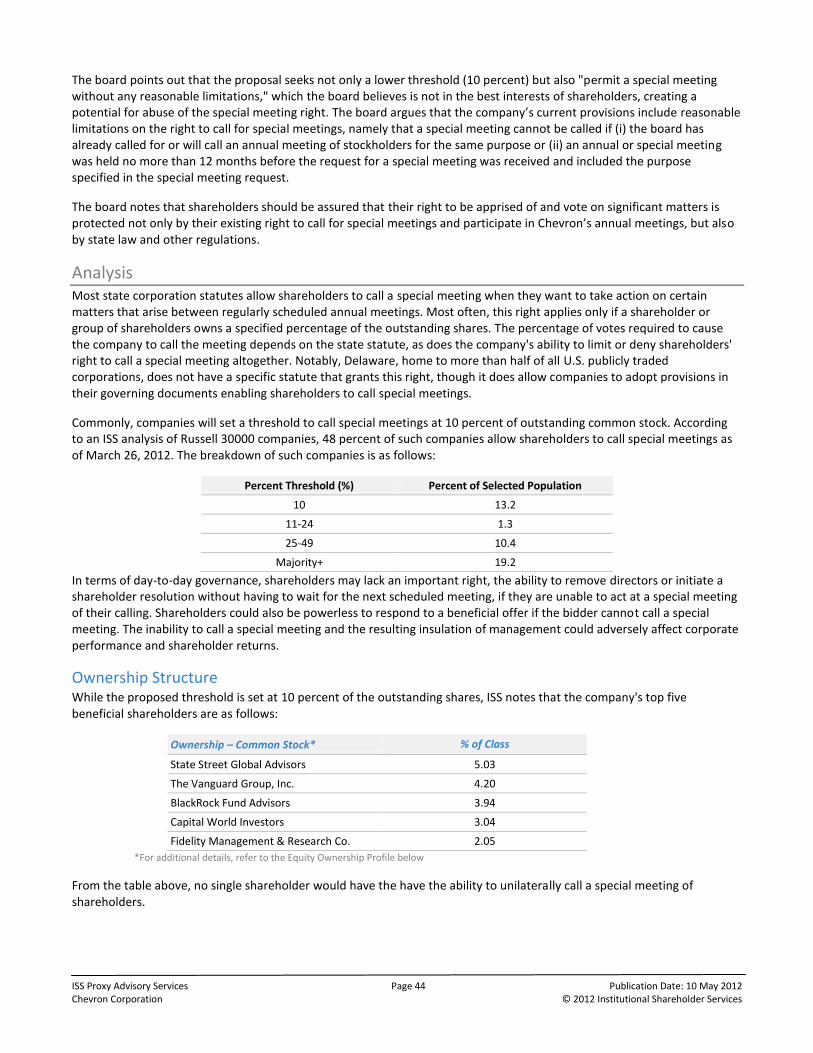

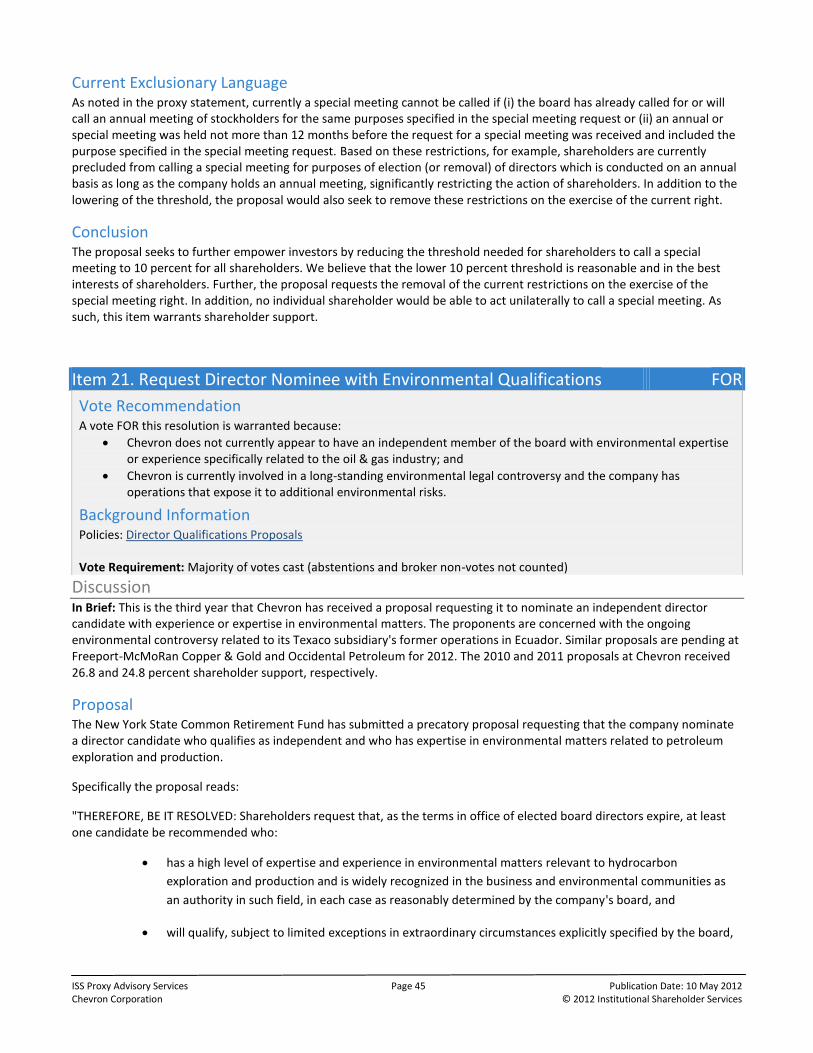

chevron corporation - chevrontoxicochevrontoxico.com/assets/docs/2012-iss-report.pdf · iss proxy...

TRANSCRIPT

ISS Proxy Advisory Services Page 1 Publication Date: 10 May 2012 Chevron Corporation © 2012 Institutional Shareholder Services

ISS Proxy Advisory Services USA

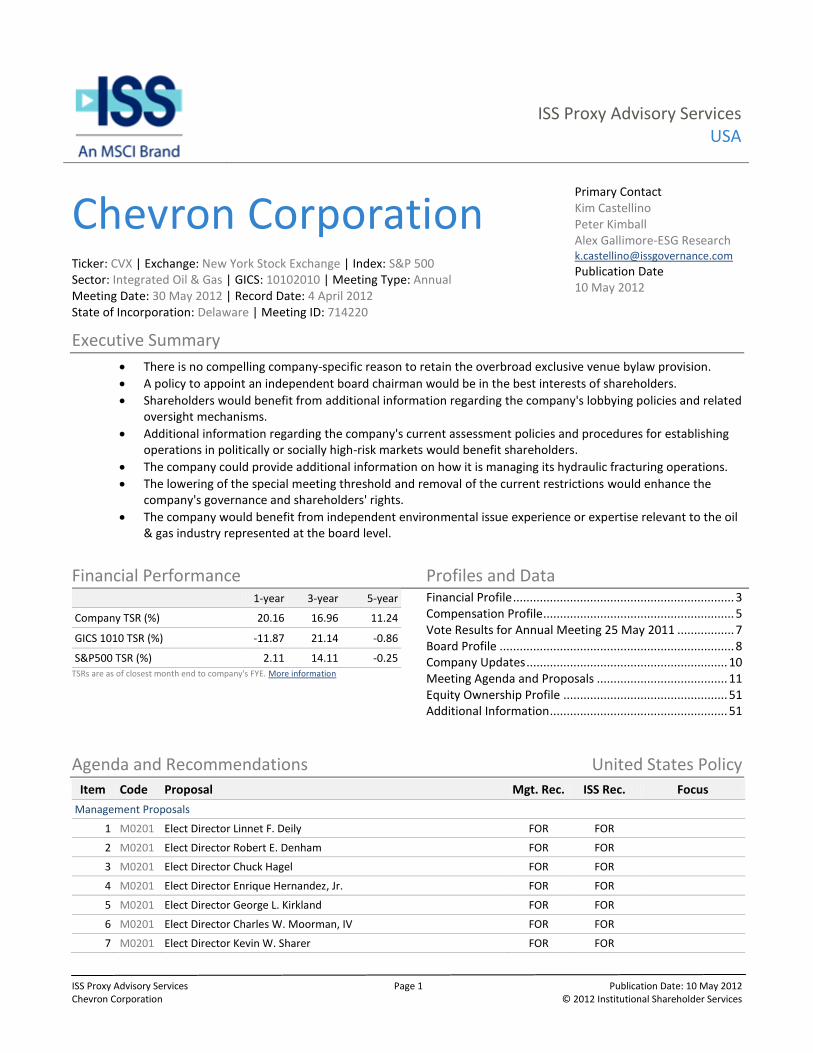

Chevron Corporation Ticker: CVX | Exchange: New York Stock Exchange | Index: S&P 500 Sector: Integrated Oil & Gas | GICS: 10102010 | Meeting Type: Annual Meeting Date: 30 May 2012 | Record Date: 4 April 2012 State of Incorporation: Delaware | Meeting ID: 714220

Primary Contact Kim Castellino Peter Kimball Alex Gallimore-ESG Research [email protected] Publication Date 10 May 2012

Executive Summary

There is no compelling company-specific reason to retain the overbroad exclusive venue bylaw provision.

A policy to appoint an independent board chairman would be in the best interests of shareholders.

Shareholders would benefit from additional information regarding the company's lobbying policies and related oversight mechanisms.

Additional information regarding the company's current assessment policies and procedures for establishing operations in politically or socially high-risk markets would benefit shareholders.

The company could provide additional information on how it is managing its hydraulic fracturing operations.

The lowering of the special meeting threshold and removal of the current restrictions would enhance the company's governance and shareholders' rights.

The company would benefit from independent environmental issue experience or expertise relevant to the oil & gas industry represented at the board level.

Financial Performance 1-year 3-year 5-year

Company TSR (%) 20.16 16.96 11.24

GICS 1010 TSR (%) -11.87 21.14 -0.86

S&P500 TSR (%) 2.11 14.11 -0.25 TSRs are as of closest month end to company's FYE. More information

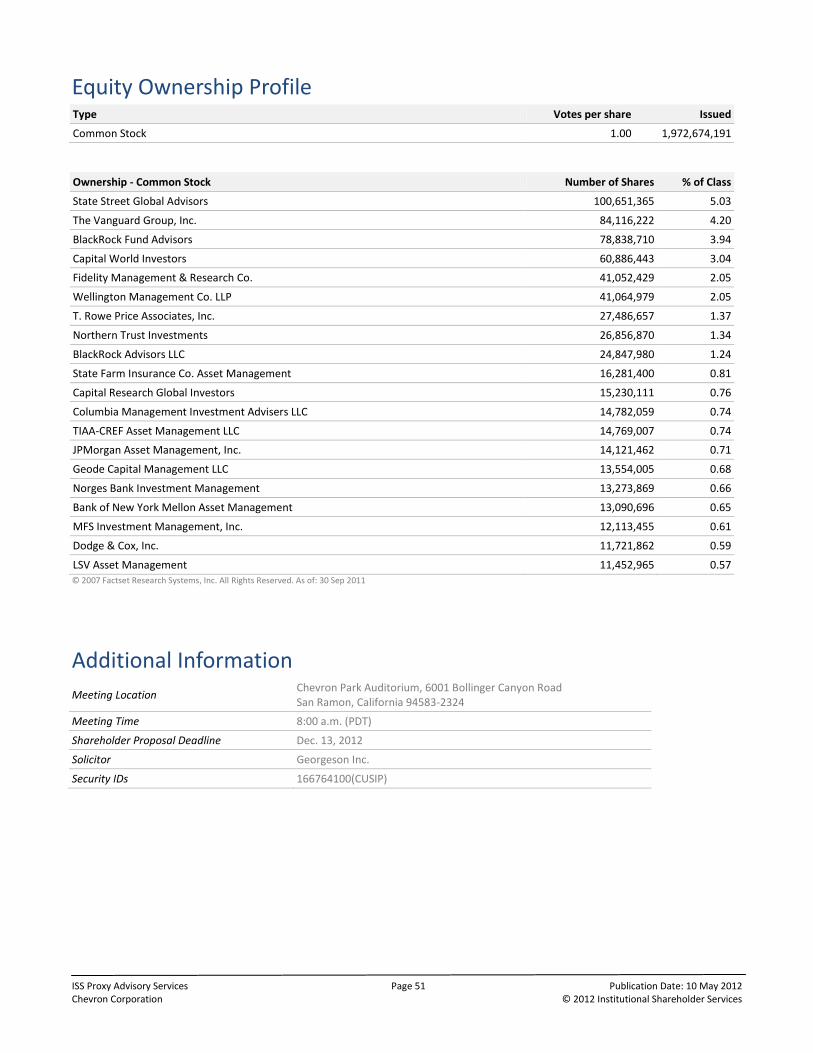

Profiles and Data Financial Profile .................................................................. 3 Compensation Profile ......................................................... 5 Vote Results for Annual Meeting 25 May 2011 ................. 7 Board Profile ...................................................................... 8 Company Updates ............................................................ 10 Meeting Agenda and Proposals ....................................... 11 Equity Ownership Profile ................................................. 51 Additional Information ..................................................... 51

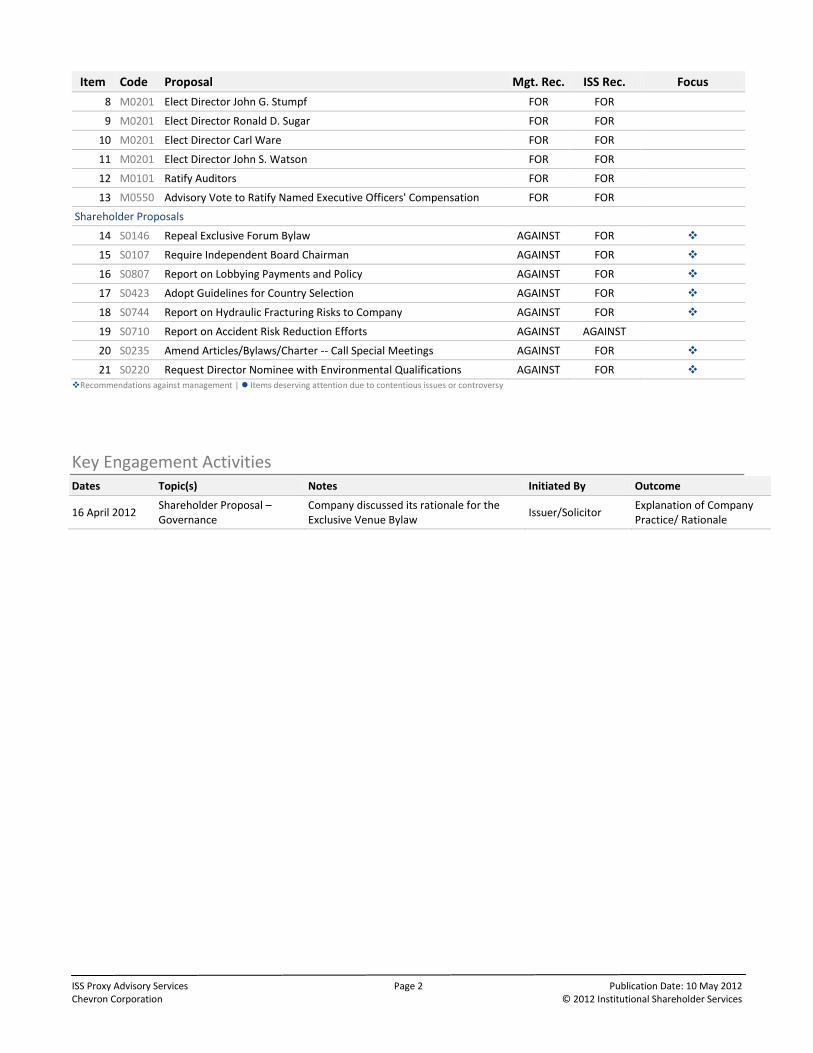

Agenda and Recommendations United States Policy

Item Code Proposal Mgt. Rec. ISS Rec. Focus

Management Proposals

1 M0201 Elect Director Linnet F. Deily FOR FOR

2 M0201 Elect Director Robert E. Denham FOR FOR

3 M0201 Elect Director Chuck Hagel FOR FOR

4 M0201 Elect Director Enrique Hernandez, Jr. FOR FOR

5 M0201 Elect Director George L. Kirkland FOR FOR

6 M0201 Elect Director Charles W. Moorman, IV FOR FOR

7 M0201 Elect Director Kevin W. Sharer FOR FOR

ISS Proxy Advisory Services Page 2 Publication Date: 10 May 2012 Chevron Corporation © 2012 Institutional Shareholder Services

Item Code Proposal Mgt. Rec. ISS Rec. Focus

8 M0201 Elect Director John G. Stumpf FOR FOR

9 M0201 Elect Director Ronald D. Sugar FOR FOR

10 M0201 Elect Director Carl Ware FOR FOR

11 M0201 Elect Director John S. Watson FOR FOR

12 M0101 Ratify Auditors FOR FOR

13 M0550 Advisory Vote to Ratify Named Executive Officers' Compensation FOR FOR

Shareholder Proposals

14 S0146 Repeal Exclusive Forum Bylaw AGAINST FOR

15 S0107 Require Independent Board Chairman AGAINST FOR

16 S0807 Report on Lobbying Payments and Policy AGAINST FOR

17 S0423 Adopt Guidelines for Country Selection AGAINST FOR

18 S0744 Report on Hydraulic Fracturing Risks to Company AGAINST FOR

19 S0710 Report on Accident Risk Reduction Efforts AGAINST AGAINST

20 S0235 Amend Articles/Bylaws/Charter -- Call Special Meetings AGAINST FOR

21 S0220 Request Director Nominee with Environmental Qualifications AGAINST FOR Recommendations against management | Items deserving attention due to contentious issues or controversy

Key Engagement Activities Dates Topic(s) Notes Initiated By Outcome

16 April 2012 Shareholder Proposal – Governance

Company discussed its rationale for the Exclusive Venue Bylaw

Issuer/Solicitor Explanation of Company Practice/ Rationale

ISS Proxy Advisory Services Page 3 Publication Date: 10 May 2012 Chevron Corporation © 2012 Institutional Shareholder Services

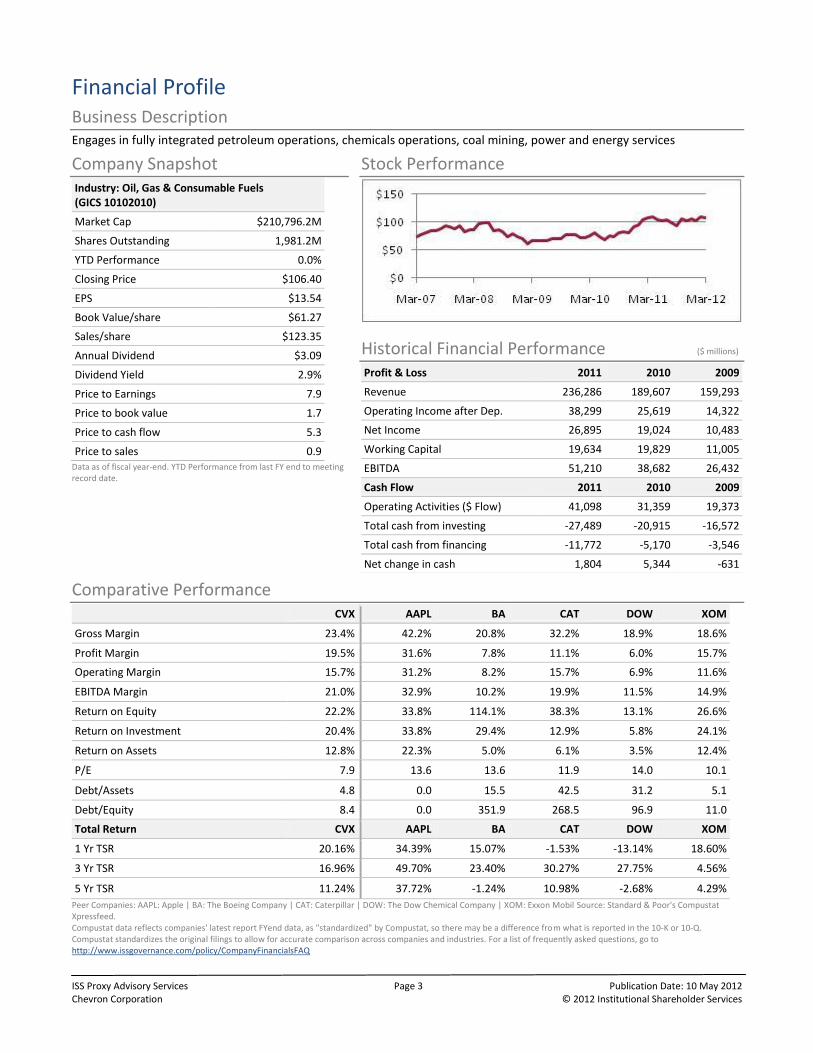

Financial Profile

Business Description Engages in fully integrated petroleum operations, chemicals operations, coal mining, power and energy services

Company Snapshot Industry: Oil, Gas & Consumable Fuels (GICS 10102010)

Market Cap $210,796.2M

Shares Outstanding 1,981.2M

YTD Performance 0.0%

Closing Price $106.40

EPS $13.54

Book Value/share $61.27

Sales/share $123.35

Annual Dividend $3.09

Dividend Yield 2.9%

Price to Earnings 7.9

Price to book value 1.7

Price to cash flow 5.3

Price to sales 0.9 Data as of fiscal year-end. YTD Performance from last FY end to meeting record date.

Stock Performance

Historical Financial Performance ($ millions) Profit & Loss 2011 2010 2009

Revenue 236,286 189,607 159,293

Operating Income after Dep. 38,299 25,619 14,322

Net Income 26,895 19,024 10,483

Working Capital 19,634 19,829 11,005

EBITDA 51,210 38,682 26,432

Cash Flow 2011 2010 2009

Operating Activities ($ Flow) 41,098 31,359 19,373

Total cash from investing -27,489 -20,915 -16,572

Total cash from financing -11,772 -5,170 -3,546

Net change in cash 1,804 5,344 -631

Comparative Performance

CVX AAPL BA CAT DOW XOM

Gross Margin 23.4% 42.2% 20.8% 32.2% 18.9% 18.6%

Profit Margin 19.5% 31.6% 7.8% 11.1% 6.0% 15.7%

Operating Margin 15.7% 31.2% 8.2% 15.7% 6.9% 11.6%

EBITDA Margin 21.0% 32.9% 10.2% 19.9% 11.5% 14.9%

Return on Equity 22.2% 33.8% 114.1% 38.3% 13.1% 26.6%

Return on Investment 20.4% 33.8% 29.4% 12.9% 5.8% 24.1%

Return on Assets 12.8% 22.3% 5.0% 6.1% 3.5% 12.4%

P/E 7.9 13.6 13.6 11.9 14.0 10.1

Debt/Assets 4.8 0.0 15.5 42.5 31.2 5.1

Debt/Equity 8.4 0.0 351.9 268.5 96.9 11.0

Total Return CVX AAPL BA CAT DOW XOM

1 Yr TSR 20.16% 34.39% 15.07% -1.53% -13.14% 18.60%

3 Yr TSR 16.96% 49.70% 23.40% 30.27% 27.75% 4.56%

5 Yr TSR 11.24% 37.72% -1.24% 10.98% -2.68% 4.29%

Peer Companies: AAPL: Apple | BA: The Boeing Company | CAT: Caterpillar | DOW: The Dow Chemical Company | XOM: Exxon Mobil Source: Standard & Poor's Compustat Xpressfeed. Compustat data reflects companies' latest report FYend data, as "standardized" by Compustat, so there may be a difference from what is reported in the 10-K or 10-Q. Compustat standardizes the original filings to allow for accurate comparison across companies and industries. For a list of frequently asked questions, go to http://www.issgovernance.com/policy/CompanyFinancialsFAQ

ISS Proxy Advisory Services Page 4 Publication Date: 10 May 2012 Chevron Corporation © 2012 Institutional Shareholder Services

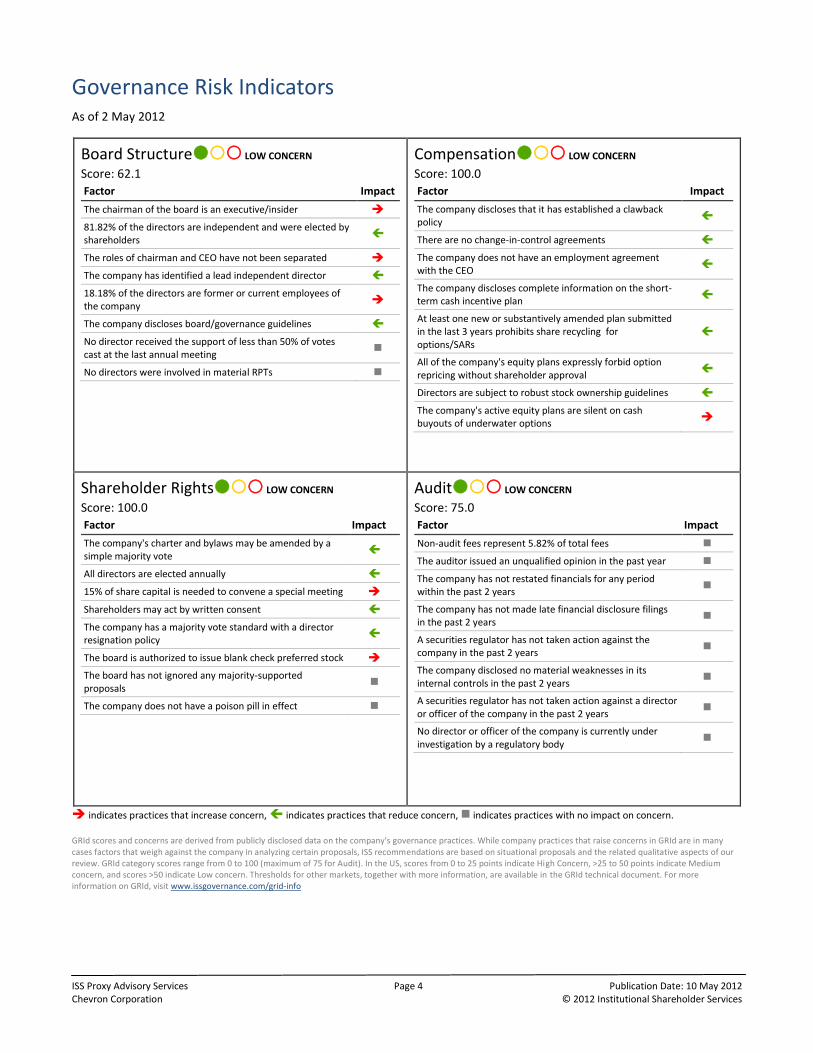

Governance Risk Indicators

As of 2 May 2012

Board Structure LOW CONCERN Score: 62.1

Factor Impact

The chairman of the board is an executive/insider

81.82% of the directors are independent and were elected by shareholders

The roles of chairman and CEO have not been separated

The company has identified a lead independent director

18.18% of the directors are former or current employees of the company

The company discloses board/governance guidelines

No director received the support of less than 50% of votes cast at the last annual meeting

No directors were involved in material RPTs

Compensation LOW CONCERN Score: 100.0

Factor Impact

The company discloses that it has established a clawback policy

There are no change-in-control agreements

The company does not have an employment agreement with the CEO

The company discloses complete information on the short-term cash incentive plan

At least one new or substantively amended plan submitted in the last 3 years prohibits share recycling for options/SARs

All of the company's equity plans expressly forbid option repricing without shareholder approval

Directors are subject to robust stock ownership guidelines

The company's active equity plans are silent on cash buyouts of underwater options

Shareholder Rights LOW CONCERN Score: 100.0

Factor Impact

The company's charter and bylaws may be amended by a simple majority vote

All directors are elected annually

15% of share capital is needed to convene a special meeting

Shareholders may act by written consent

The company has a majority vote standard with a director resignation policy

The board is authorized to issue blank check preferred stock

The board has not ignored any majority-supported proposals

The company does not have a poison pill in effect

Audit LOW CONCERN Score: 75.0

Factor Impact

Non-audit fees represent 5.82% of total fees

The auditor issued an unqualified opinion in the past year

The company has not restated financials for any period within the past 2 years

The company has not made late financial disclosure filings in the past 2 years

A securities regulator has not taken action against the company in the past 2 years

The company disclosed no material weaknesses in its internal controls in the past 2 years

A securities regulator has not taken action against a director or officer of the company in the past 2 years

No director or officer of the company is currently under investigation by a regulatory body

indicates practices that increase concern, indicates practices that reduce concern, indicates practices with no impact on concern.

GRId scores and concerns are derived from publicly disclosed data on the company’s governance practices. While company practices that raise concerns in GRId are in many cases factors that weigh against the company in analyzing certain proposals, ISS recommendations are based on situational proposals and the related qualitative aspects of our review. GRId category scores range from 0 to 100 (maximum of 75 for Audit). In the US, scores from 0 to 25 points indicate High Concern, >25 to 50 points indicate Medium concern, and scores >50 indicate Low concern. Thresholds for other markets, together with more information, are available in the GRId technical document. For more information on GRId, visit www.issgovernance.com/grid-info

ISS Proxy Advisory Services Page 5 Publication Date: 10 May 2012 Chevron Corporation © 2012 Institutional Shareholder Services

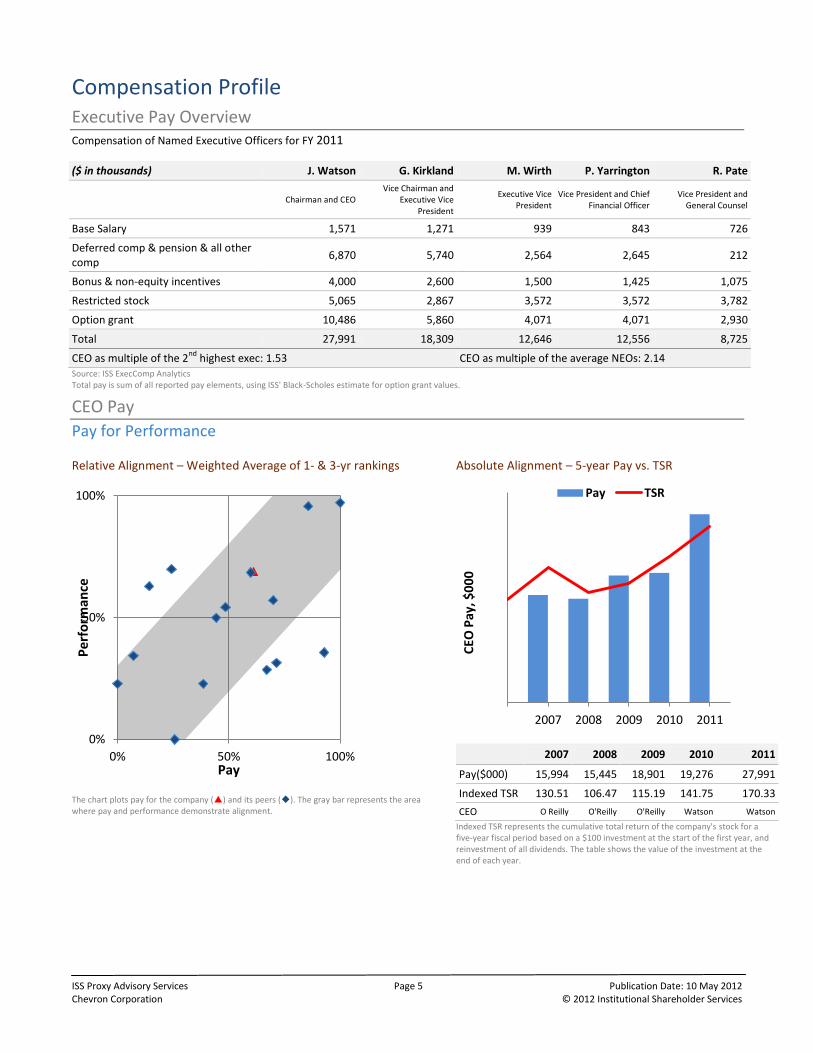

Compensation Profile Executive Pay Overview Compensation of Named Executive Officers for FY 2011

($ in thousands) J. Watson G. Kirkland M. Wirth P. Yarrington R. Pate

Chairman and CEO Vice Chairman and

Executive Vice President

Executive Vice President

Vice President and Chief Financial Officer

Vice President and General Counsel

Base Salary 1,571 1,271 939 843 726

Deferred comp & pension & all other comp

6,870 5,740 2,564 2,645 212

Bonus & non-equity incentives 4,000 2,600 1,500 1,425 1,075

Restricted stock 5,065 2,867 3,572 3,572 3,782

Option grant 10,486 5,860 4,071 4,071 2,930

Total 27,991 18,309 12,646 12,556 8,725

CEO as multiple of the 2nd

highest exec: 1.53 CEO as multiple of the average NEOs: 2.14 Source: ISS ExecComp Analytics Total pay is sum of all reported pay elements, using ISS' Black-Scholes estimate for option grant values.

CEO Pay

Pay for Performance

Relative Alignment – Weighted Average of 1- & 3-yr rankings Absolute Alignment – 5-year Pay vs. TSR

The chart plots pay for the company () and its peers (). The gray bar represents the area where pay and performance demonstrate alignment.

2007 2008 2009 2010 2011

Pay($000) 15,994 15,445 18,901 19,276 27,991

Indexed TSR 130.51 106.47 115.19 141.75 170.33

CEO O Reilly O'Reilly O'Reilly Watson Watson

Indexed TSR represents the cumulative total return of the company's stock for a five-year fiscal period based on a $100 investment at the start of the first year, and reinvestment of all dividends. The table shows the value of the investment at the end of each year.

0%

50%

100%

0% 50% 100%

Pe

rfo

rman

ce

Pay

0

0.2

0.4

0.6

0.8

1

1.2

1.4

1.6

$-

$5,000

$10,000

$15,000

$20,000

$25,000

$30,000

2007 2008 2009 2010 2011

CEO

Pay

, $0

00

Pay TSR

ISS Proxy Advisory Services Page 6 Publication Date: 10 May 2012 Chevron Corporation © 2012 Institutional Shareholder Services

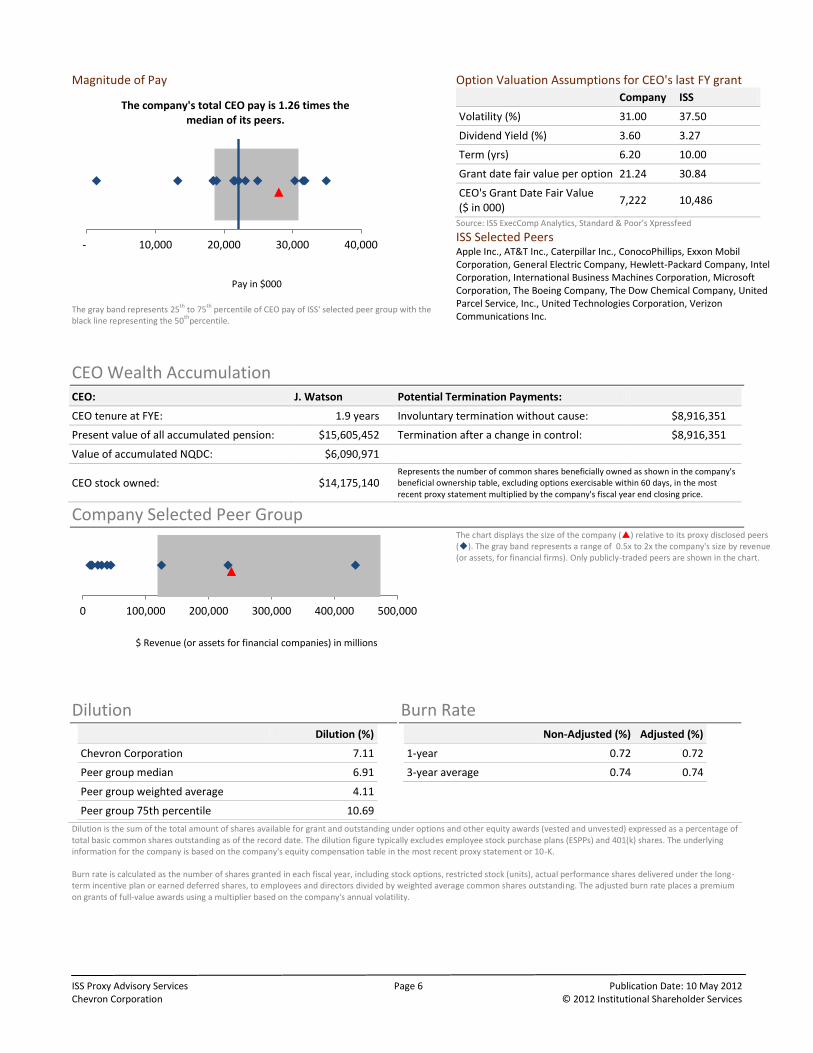

Magnitude of Pay

Pay in $000

The gray band represents 25th to 75th percentile of CEO pay of ISS' selected peer group with the black line representing the 50thpercentile.

Option Valuation Assumptions for CEO's last FY grant

Company ISS

Volatility (%) 31.00 37.50

Dividend Yield (%) 3.60 3.27

Term (yrs) 6.20 10.00

Grant date fair value per option 21.24 30.84

CEO's Grant Date Fair Value ($ in 000)

7,222 10,486

Source: ISS ExecComp Analytics, Standard & Poor's Xpressfeed

ISS Selected Peers Apple Inc., AT&T Inc., Caterpillar Inc., ConocoPhillips, Exxon Mobil Corporation, General Electric Company, Hewlett-Packard Company, Intel Corporation, International Business Machines Corporation, Microsoft Corporation, The Boeing Company, The Dow Chemical Company, United Parcel Service, Inc., United Technologies Corporation, Verizon Communications Inc.

CEO Wealth Accumulation CEO: J. Watson Potential Termination Payments:

CEO tenure at FYE: 1.9 years Involuntary termination without cause: $8,916,351

Present value of all accumulated pension: $15,605,452 Termination after a change in control: $8,916,351

Value of accumulated NQDC: $6,090,971

CEO stock owned: $14,175,140 Represents the number of common shares beneficially owned as shown in the company's beneficial ownership table, excluding options exercisable within 60 days, in the most recent proxy statement multiplied by the company's fiscal year end closing price.

Company Selected Peer Group

$ Revenue (or assets for financial companies) in millions

The chart displays the size of the company () relative to its proxy disclosed peers (). The gray band represents a range of 0.5x to 2x the company's size by revenue (or assets, for financial firms). Only publicly-traded peers are shown in the chart.

Dilution

Dilution (%)

Chevron Corporation 7.11

Peer group median 6.91

Peer group weighted average 4.11

Peer group 75th percentile 10.69

Burn Rate

Non-Adjusted (%) Adjusted (%)

1-year 0.72 0.72

3-year average 0.74 0.74

Dilution is the sum of the total amount of shares available for grant and outstanding under options and other equity awards (vested and unvested) expressed as a percentage of total basic common shares outstanding as of the record date. The dilution figure typically excludes employee stock purchase plans (ESPPs) and 401(k) shares. The underlying information for the company is based on the company's equity compensation table in the most recent proxy statement or 10-K. Burn rate is calculated as the number of shares granted in each fiscal year, including stock options, restricted stock (units), actual performance shares delivered under the long-term incentive plan or earned deferred shares, to employees and directors divided by weighted average common shares outstanding. The adjusted burn rate places a premium on grants of full-value awards using a multiplier based on the company's annual volatility.

- 10,000 20,000 30,000 40,000

The company's total CEO pay is 1.26 times the median of its peers.

0 100,000 200,000 300,000 400,000 500,000

ISS Proxy Advisory Services Page 7 Publication Date: 10 May 2012 Chevron Corporation © 2012 Institutional Shareholder Services

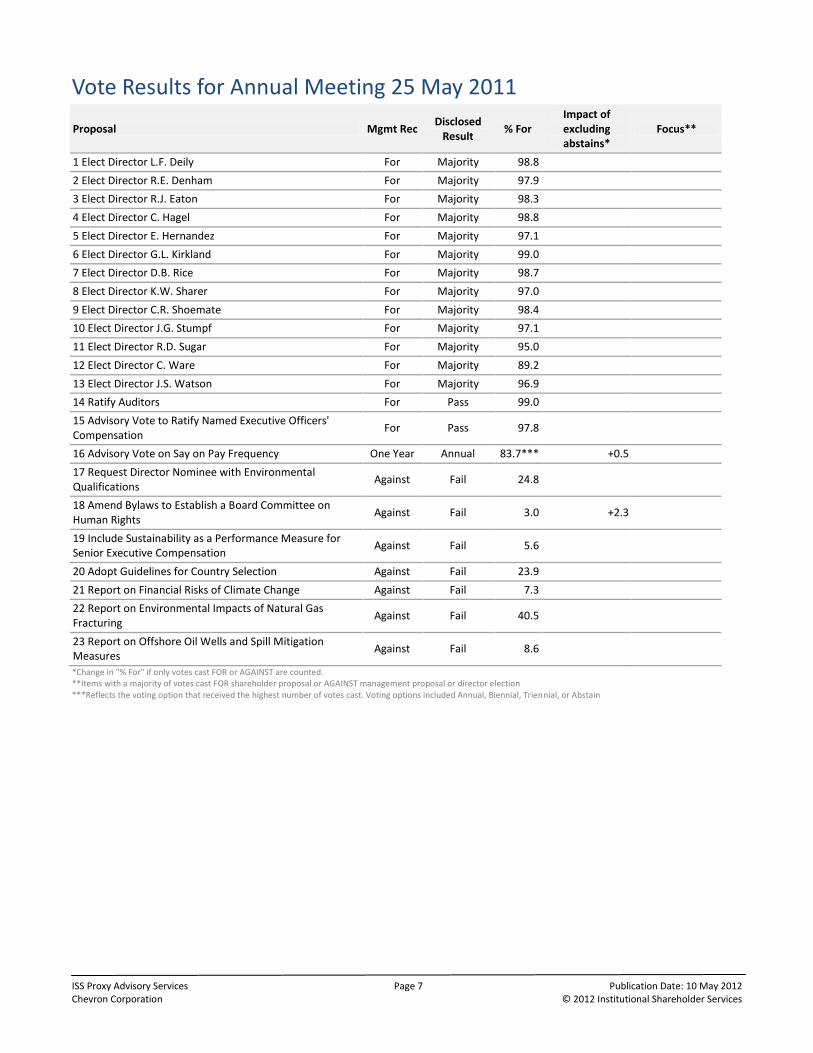

Vote Results for Annual Meeting 25 May 2011

Proposal Mgmt Rec Disclosed

Result % For

Impact of excluding abstains*

Focus**

1 Elect Director L.F. Deily For Majority 98.8

2 Elect Director R.E. Denham For Majority 97.9

3 Elect Director R.J. Eaton For Majority 98.3

4 Elect Director C. Hagel For Majority 98.8

5 Elect Director E. Hernandez For Majority 97.1

6 Elect Director G.L. Kirkland For Majority 99.0

7 Elect Director D.B. Rice For Majority 98.7

8 Elect Director K.W. Sharer For Majority 97.0

9 Elect Director C.R. Shoemate For Majority 98.4

10 Elect Director J.G. Stumpf For Majority 97.1

11 Elect Director R.D. Sugar For Majority 95.0

12 Elect Director C. Ware For Majority 89.2

13 Elect Director J.S. Watson For Majority 96.9

14 Ratify Auditors For Pass 99.0

15 Advisory Vote to Ratify Named Executive Officers' Compensation

For Pass 97.8

16 Advisory Vote on Say on Pay Frequency One Year Annual 83.7*** +0.5

17 Request Director Nominee with Environmental Qualifications

Against Fail 24.8

18 Amend Bylaws to Establish a Board Committee on Human Rights

Against Fail 3.0 +2.3

19 Include Sustainability as a Performance Measure for Senior Executive Compensation

Against Fail 5.6

20 Adopt Guidelines for Country Selection Against Fail 23.9

21 Report on Financial Risks of Climate Change Against Fail 7.3

22 Report on Environmental Impacts of Natural Gas Fracturing

Against Fail 40.5

23 Report on Offshore Oil Wells and Spill Mitigation Measures

Against Fail 8.6

*Change in "% For" if only votes cast FOR or AGAINST are counted. **Items with a majority of votes cast FOR shareholder proposal or AGAINST management proposal or director election ***Reflects the voting option that received the highest number of votes cast. Voting options included Annual, Biennial, Triennial, or Abstain

ISS Proxy Advisory Services Page 8 Publication Date: 10 May 2012 Chevron Corporation © 2012 Institutional Shareholder Services

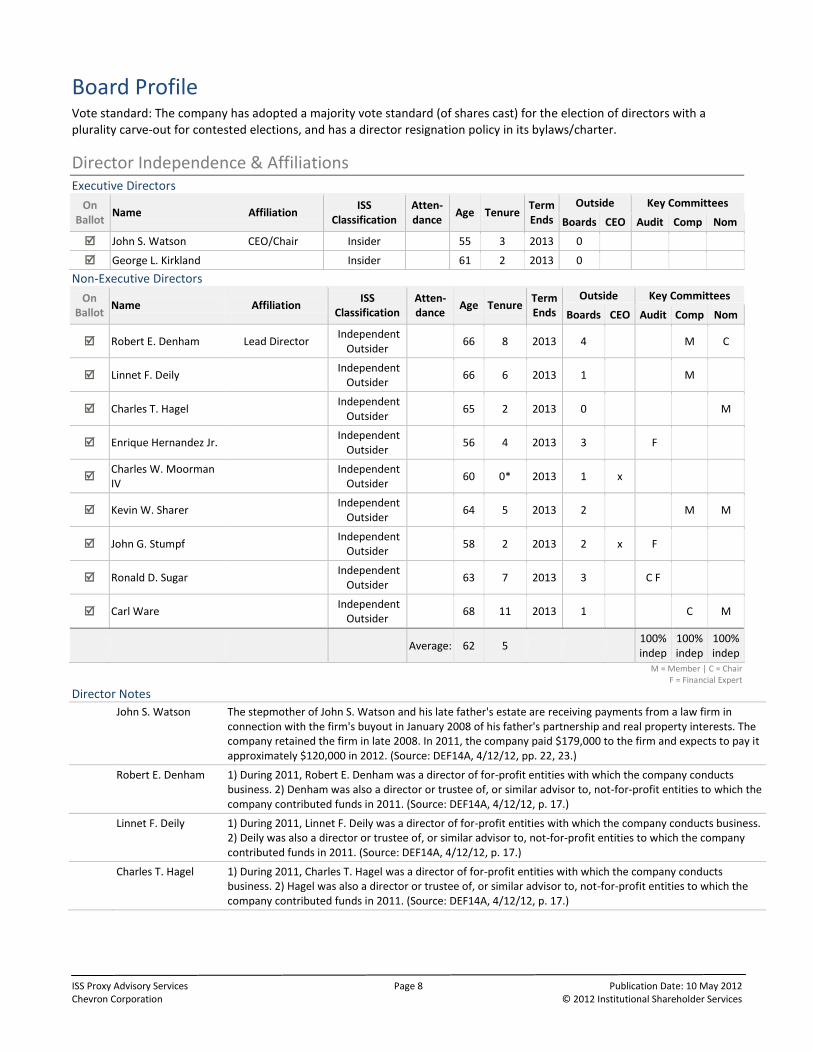

Board Profile Vote standard: The company has adopted a majority vote standard (of shares cast) for the election of directors with a plurality carve-out for contested elections, and has a director resignation policy in its bylaws/charter.

Director Independence & Affiliations Executive Directors

On Ballot

Name Affiliation ISS

Classification Atten-dance

Age Tenure Term Ends

Outside Key Committees

Boards CEO Audit Comp Nom

John S. Watson CEO/Chair Insider 55 3 2013 0

George L. Kirkland Insider 61 2 2013 0

Non-Executive Directors

On Ballot

Name Affiliation ISS

Classification Atten-dance

Age Tenure Term Ends

Outside Key Committees

Boards CEO Audit Comp Nom

Robert E. Denham Lead Director Independent

Outsider 66 8 2013 4 M C

Linnet F. Deily Independent

Outsider 66 6 2013 1 M

Charles T. Hagel Independent

Outsider 65 2 2013 0 M

Enrique Hernandez Jr. Independent

Outsider 56 4 2013 3 F

Charles W. Moorman IV

Independent

Outsider 60 0* 2013 1 x

Kevin W. Sharer Independent

Outsider 64 5 2013 2 M M

John G. Stumpf Independent

Outsider 58 2 2013 2 x F

Ronald D. Sugar Independent

Outsider 63 7 2013 3 C F

Carl Ware Independent

Outsider 68 11 2013 1 C M

Average: 62 5 100% indep

100% indep

100% indep

M = Member | C = Chair F = Financial Expert

Director Notes John S. Watson The stepmother of John S. Watson and his late father's estate are receiving payments from a law firm in

connection with the firm's buyout in January 2008 of his father's partnership and real property interests. The company retained the firm in late 2008. In 2011, the company paid $179,000 to the firm and expects to pay it approximately $120,000 in 2012. (Source: DEF14A, 4/12/12, pp. 22, 23.)

Robert E. Denham 1) During 2011, Robert E. Denham was a director of for-profit entities with which the company conducts business. 2) Denham was also a director or trustee of, or similar advisor to, not-for-profit entities to which the company contributed funds in 2011. (Source: DEF14A, 4/12/12, p. 17.)

Linnet F. Deily 1) During 2011, Linnet F. Deily was a director of for-profit entities with which the company conducts business. 2) Deily was also a director or trustee of, or similar advisor to, not-for-profit entities to which the company contributed funds in 2011. (Source: DEF14A, 4/12/12, p. 17.)

Charles T. Hagel 1) During 2011, Charles T. Hagel was a director of for-profit entities with which the company conducts business. 2) Hagel was also a director or trustee of, or similar advisor to, not-for-profit entities to which the company contributed funds in 2011. (Source: DEF14A, 4/12/12, p. 17.)

ISS Proxy Advisory Services Page 9 Publication Date: 10 May 2012 Chevron Corporation © 2012 Institutional Shareholder Services

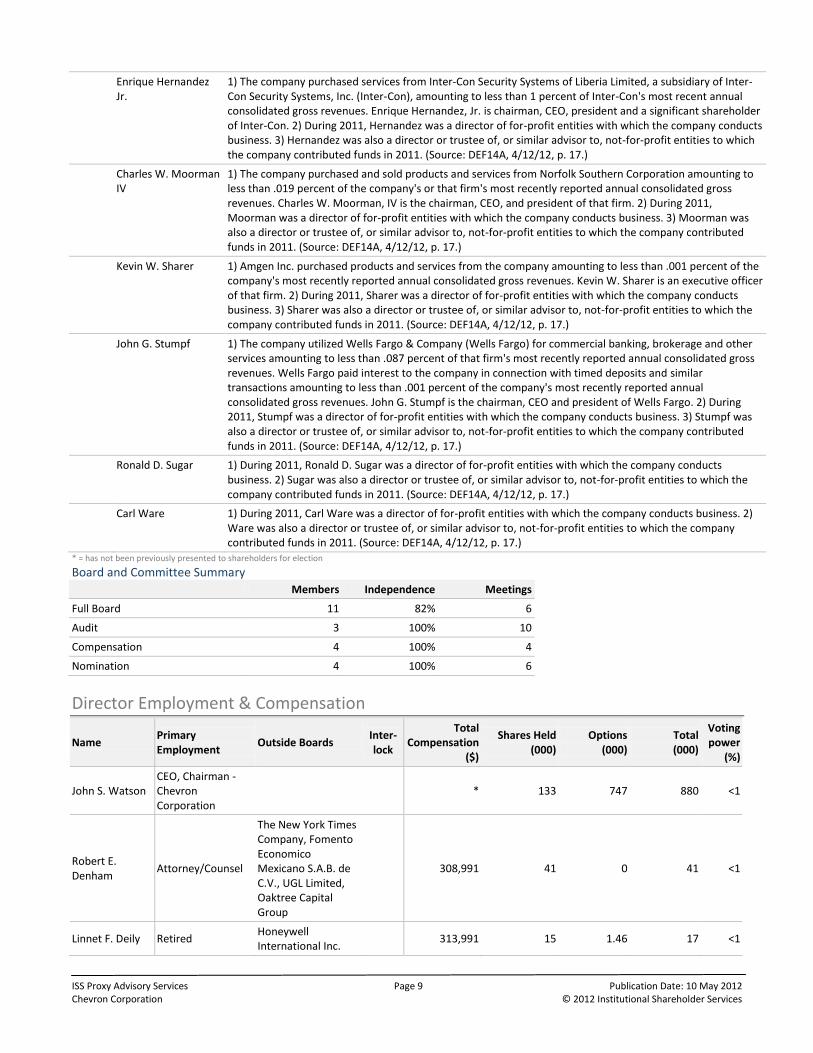

Enrique Hernandez Jr.

1) The company purchased services from Inter-Con Security Systems of Liberia Limited, a subsidiary of Inter-Con Security Systems, Inc. (Inter-Con), amounting to less than 1 percent of Inter-Con's most recent annual consolidated gross revenues. Enrique Hernandez, Jr. is chairman, CEO, president and a significant shareholder of Inter-Con. 2) During 2011, Hernandez was a director of for-profit entities with which the company conducts business. 3) Hernandez was also a director or trustee of, or similar advisor to, not-for-profit entities to which the company contributed funds in 2011. (Source: DEF14A, 4/12/12, p. 17.)

Charles W. Moorman IV

1) The company purchased and sold products and services from Norfolk Southern Corporation amounting to less than .019 percent of the company's or that firm's most recently reported annual consolidated gross revenues. Charles W. Moorman, IV is the chairman, CEO, and president of that firm. 2) During 2011, Moorman was a director of for-profit entities with which the company conducts business. 3) Moorman was also a director or trustee of, or similar advisor to, not-for-profit entities to which the company contributed funds in 2011. (Source: DEF14A, 4/12/12, p. 17.)

Kevin W. Sharer 1) Amgen Inc. purchased products and services from the company amounting to less than .001 percent of the company's most recently reported annual consolidated gross revenues. Kevin W. Sharer is an executive officer of that firm. 2) During 2011, Sharer was a director of for-profit entities with which the company conducts business. 3) Sharer was also a director or trustee of, or similar advisor to, not-for-profit entities to which the company contributed funds in 2011. (Source: DEF14A, 4/12/12, p. 17.)

John G. Stumpf 1) The company utilized Wells Fargo & Company (Wells Fargo) for commercial banking, brokerage and other services amounting to less than .087 percent of that firm's most recently reported annual consolidated gross revenues. Wells Fargo paid interest to the company in connection with timed deposits and similar transactions amounting to less than .001 percent of the company's most recently reported annual consolidated gross revenues. John G. Stumpf is the chairman, CEO and president of Wells Fargo. 2) During 2011, Stumpf was a director of for-profit entities with which the company conducts business. 3) Stumpf was also a director or trustee of, or similar advisor to, not-for-profit entities to which the company contributed funds in 2011. (Source: DEF14A, 4/12/12, p. 17.)

Ronald D. Sugar 1) During 2011, Ronald D. Sugar was a director of for-profit entities with which the company conducts business. 2) Sugar was also a director or trustee of, or similar advisor to, not-for-profit entities to which the company contributed funds in 2011. (Source: DEF14A, 4/12/12, p. 17.)

Carl Ware 1) During 2011, Carl Ware was a director of for-profit entities with which the company conducts business. 2) Ware was also a director or trustee of, or similar advisor to, not-for-profit entities to which the company contributed funds in 2011. (Source: DEF14A, 4/12/12, p. 17.)

* = has not been previously presented to shareholders for election

Board and Committee Summary

Members Independence Meetings

Full Board 11 82% 6

Audit 3 100% 10

Compensation 4 100% 4

Nomination 4 100% 6

Director Employment & Compensation

Name Primary Employment

Outside Boards Inter-lock

Total Compensation

($)

Shares Held (000)

Options (000)

Total (000)

Voting power

(%)

John S. Watson CEO, Chairman - Chevron Corporation

* 133 747 880 <1

Robert E. Denham

Attorney/Counsel

The New York Times Company, Fomento Economico Mexicano S.A.B. de C.V., UGL Limited, Oaktree Capital Group

308,991 41 0 41 <1

Linnet F. Deily Retired Honeywell International Inc.

313,991 15 1.46 17 <1

ISS Proxy Advisory Services Page 10 Publication Date: 10 May 2012 Chevron Corporation © 2012 Institutional Shareholder Services

Name Primary Employment

Outside Boards Inter-lock

Total Compensation

($)

Shares Held (000)

Options (000)

Total (000)

Voting power

(%)

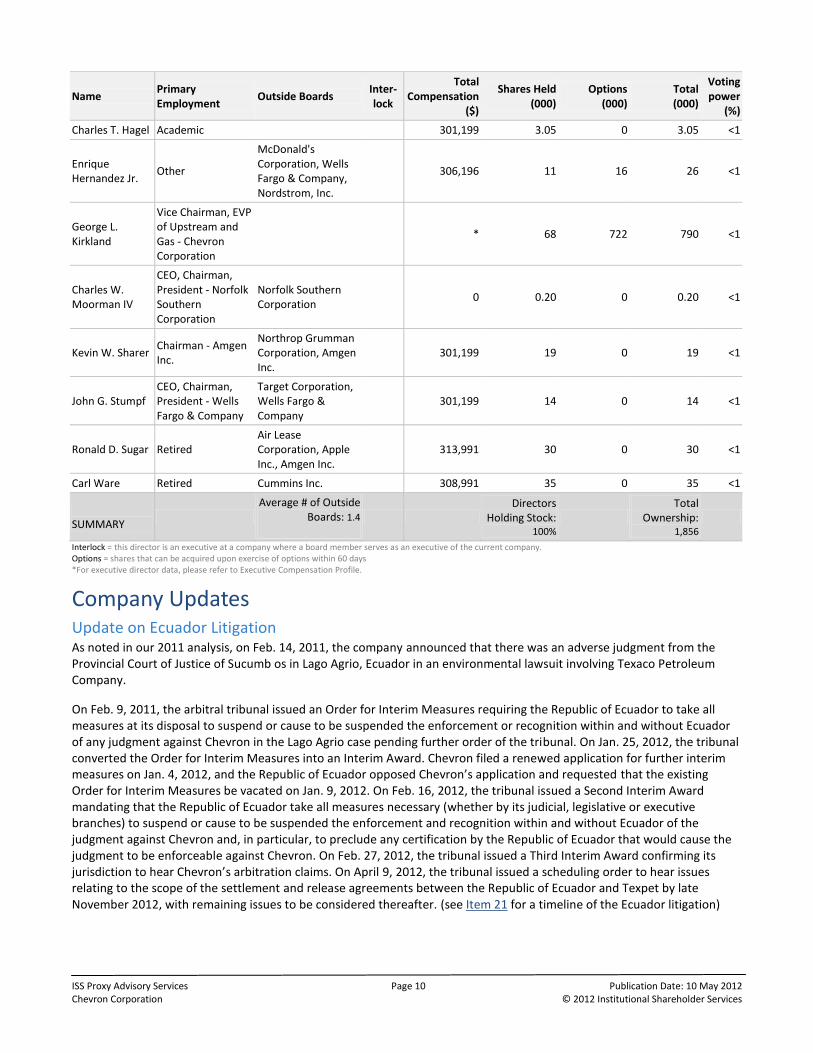

Charles T. Hagel Academic 301,199 3.05 0 3.05 <1

Enrique Hernandez Jr.

Other

McDonald's Corporation, Wells Fargo & Company, Nordstrom, Inc.

306,196 11 16 26 <1

George L. Kirkland

Vice Chairman, EVP of Upstream and Gas - Chevron Corporation

* 68 722 790 <1

Charles W. Moorman IV

CEO, Chairman, President - Norfolk Southern Corporation

Norfolk Southern Corporation

0 0.20 0 0.20 <1

Kevin W. Sharer Chairman - Amgen Inc.

Northrop Grumman Corporation, Amgen Inc.

301,199 19 0 19 <1

John G. Stumpf CEO, Chairman, President - Wells Fargo & Company

Target Corporation, Wells Fargo & Company

301,199 14 0 14 <1

Ronald D. Sugar Retired Air Lease Corporation, Apple Inc., Amgen Inc.

313,991 30 0 30 <1

Carl Ware Retired Cummins Inc. 308,991 35 0 35 <1

SUMMARY

Average # of Outside

Boards: 1.4

Directors

Holding Stock: 100%

Total

Ownership: 1,856

Interlock = this director is an executive at a company where a board member serves as an executive of the current company. Options = shares that can be acquired upon exercise of options within 60 days *For executive director data, please refer to Executive Compensation Profile.

Company Updates Update on Ecuador Litigation As noted in our 2011 analysis, on Feb. 14, 2011, the company announced that there was an adverse judgment from the Provincial Court of Justice of Sucumb os in Lago Agrio, Ecuador in an environmental lawsuit involving Texaco Petroleum Company.

On Feb. 9, 2011, the arbitral tribunal issued an Order for Interim Measures requiring the Republic of Ecuador to take all measures at its disposal to suspend or cause to be suspended the enforcement or recognition within and without Ecuador of any judgment against Chevron in the Lago Agrio case pending further order of the tribunal. On Jan. 25, 2012, the tribunal converted the Order for Interim Measures into an Interim Award. Chevron filed a renewed application for further interim measures on Jan. 4, 2012, and the Republic of Ecuador opposed Chevron’s application and requested that the existing Order for Interim Measures be vacated on Jan. 9, 2012. On Feb. 16, 2012, the tribunal issued a Second Interim Award mandating that the Republic of Ecuador take all measures necessary (whether by its judicial, legislative or executive branches) to suspend or cause to be suspended the enforcement and recognition within and without Ecuador of the judgment against Chevron and, in particular, to preclude any certification by the Republic of Ecuador that would cause the judgment to be enforceable against Chevron. On Feb. 27, 2012, the tribunal issued a Third Interim Award confirming its jurisdiction to hear Chevron’s arbitration claims. On April 9, 2012, the tribunal issued a scheduling order to hear issues relating to the scope of the settlement and release agreements between the Republic of Ecuador and Texpet by late November 2012, with remaining issues to be considered thereafter. (see Item 21 for a timeline of the Ecuador litigation)

ISS Proxy Advisory Services Page 11 Publication Date: 10 May 2012 Chevron Corporation © 2012 Institutional Shareholder Services

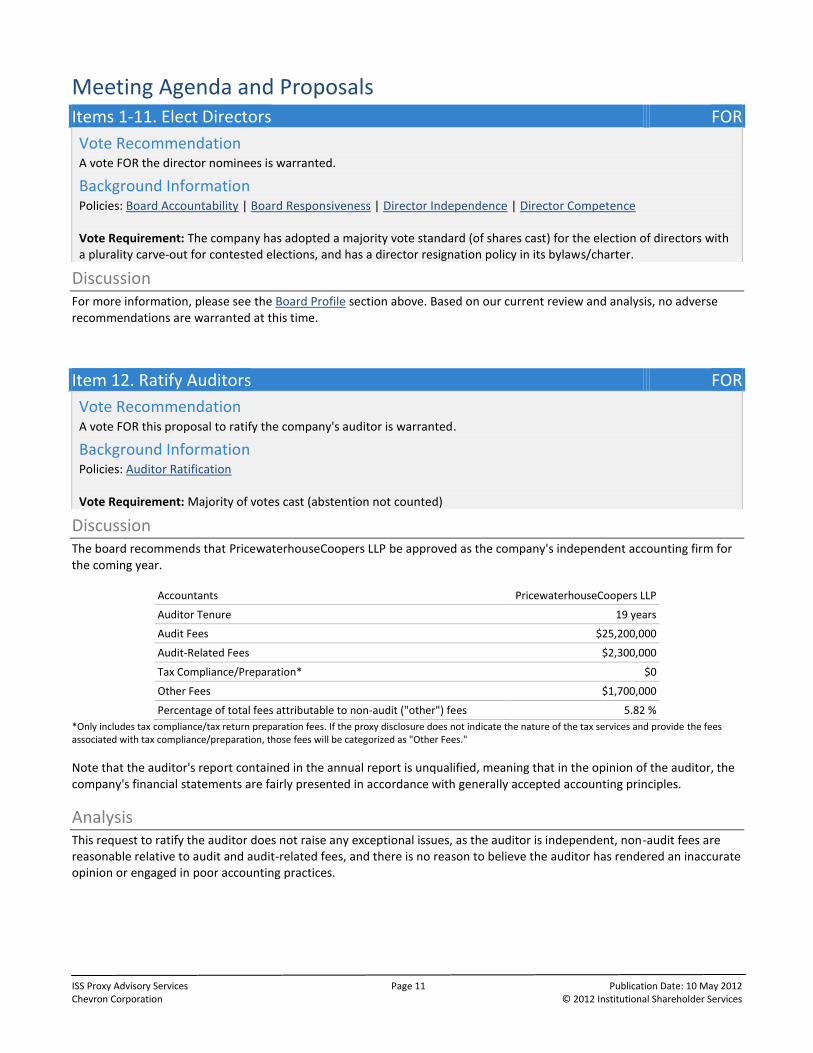

Meeting Agenda and Proposals Items 1-11. Elect Directors FOR

Vote Recommendation A vote FOR the director nominees is warranted.

Background Information Policies: Board Accountability | Board Responsiveness | Director Independence | Director Competence

Vote Requirement: The company has adopted a majority vote standard (of shares cast) for the election of directors with a plurality carve-out for contested elections, and has a director resignation policy in its bylaws/charter.

Discussion For more information, please see the Board Profile section above. Based on our current review and analysis, no adverse recommendations are warranted at this time.

Item 12. Ratify Auditors FOR

Vote Recommendation A vote FOR this proposal to ratify the company's auditor is warranted.

Background Information Policies: Auditor Ratification

Vote Requirement: Majority of votes cast (abstention not counted)

Discussion The board recommends that PricewaterhouseCoopers LLP be approved as the company's independent accounting firm for the coming year.

Accountants PricewaterhouseCoopers LLP

Auditor Tenure 19 years

Audit Fees $25,200,000

Audit-Related Fees $2,300,000

Tax Compliance/Preparation* $0

Other Fees $1,700,000

Percentage of total fees attributable to non-audit ("other") fees 5.82 %

*Only includes tax compliance/tax return preparation fees. If the proxy disclosure does not indicate the nature of the tax services and provide the fees associated with tax compliance/preparation, those fees will be categorized as "Other Fees."

Note that the auditor's report contained in the annual report is unqualified, meaning that in the opinion of the auditor, the company's financial statements are fairly presented in accordance with generally accepted accounting principles.

Analysis This request to ratify the auditor does not raise any exceptional issues, as the auditor is independent, non-audit fees are reasonable relative to audit and audit-related fees, and there is no reason to believe the auditor has rendered an inaccurate opinion or engaged in poor accounting practices.

ISS Proxy Advisory Services Page 12 Publication Date: 10 May 2012 Chevron Corporation © 2012 Institutional Shareholder Services

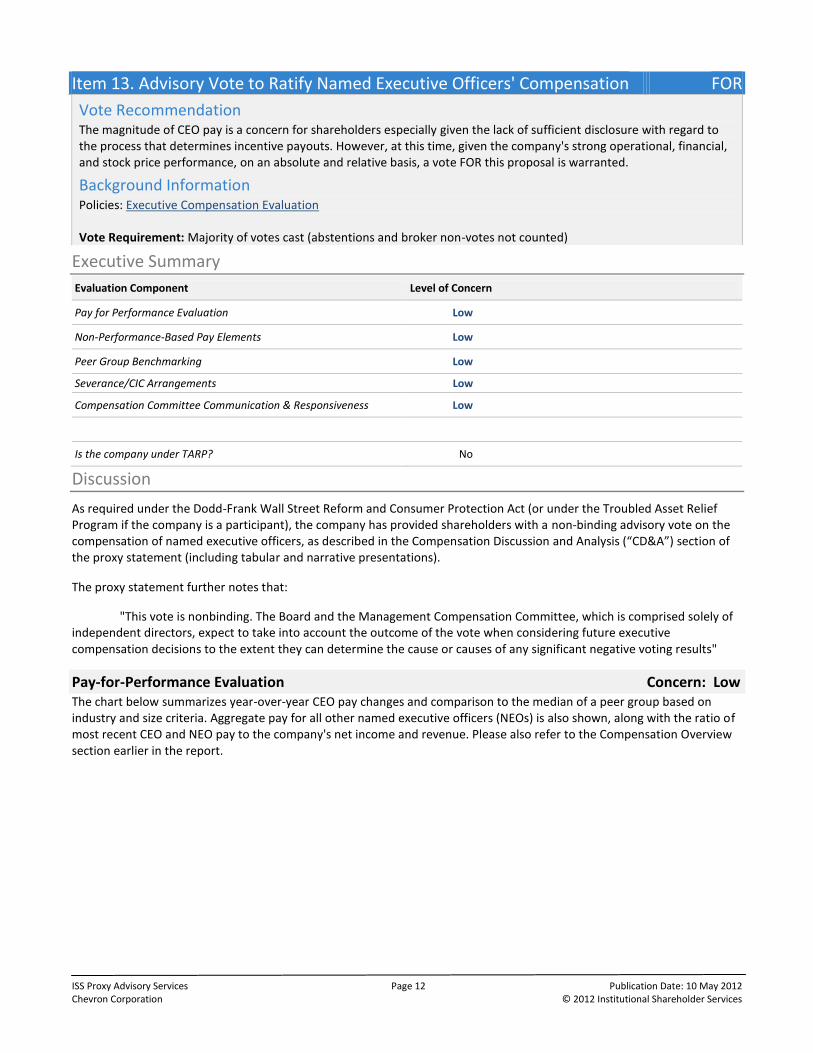

Item 13. Advisory Vote to Ratify Named Executive Officers' Compensation FOR

Vote Recommendation The magnitude of CEO pay is a concern for shareholders especially given the lack of sufficient disclosure with regard to the process that determines incentive payouts. However, at this time, given the company's strong operational, financial, and stock price performance, on an absolute and relative basis, a vote FOR this proposal is warranted.

Background Information Policies: Executive Compensation Evaluation

Vote Requirement: Majority of votes cast (abstentions and broker non-votes not counted)

Executive Summary

Evaluation Component Level of Concern

Pay for Performance Evaluation Low

Non-Performance-Based Pay Elements Low

Peer Group Benchmarking Low

Severance/CIC Arrangements Low

Compensation Committee Communication & Responsiveness Low

Is the company under TARP? No

Discussion

As required under the Dodd-Frank Wall Street Reform and Consumer Protection Act (or under the Troubled Asset Relief Program if the company is a participant), the company has provided shareholders with a non-binding advisory vote on the compensation of named executive officers, as described in the Compensation Discussion and Analysis (“CD&A”) section of the proxy statement (including tabular and narrative presentations).

The proxy statement further notes that:

"This vote is nonbinding. The Board and the Management Compensation Committee, which is comprised solely of independent directors, expect to take into account the outcome of the vote when considering future executive compensation decisions to the extent they can determine the cause or causes of any significant negative voting results"

Pay-for-Performance Evaluation Concern: Low The chart below summarizes year-over-year CEO pay changes and comparison to the median of a peer group based on industry and size criteria. Aggregate pay for all other named executive officers (NEOs) is also shown, along with the ratio of most recent CEO and NEO pay to the company's net income and revenue. Please also refer to the Compensation Overview section earlier in the report.

ISS Proxy Advisory Services Page 13 Publication Date: 10 May 2012 Chevron Corporation © 2012 Institutional Shareholder Services

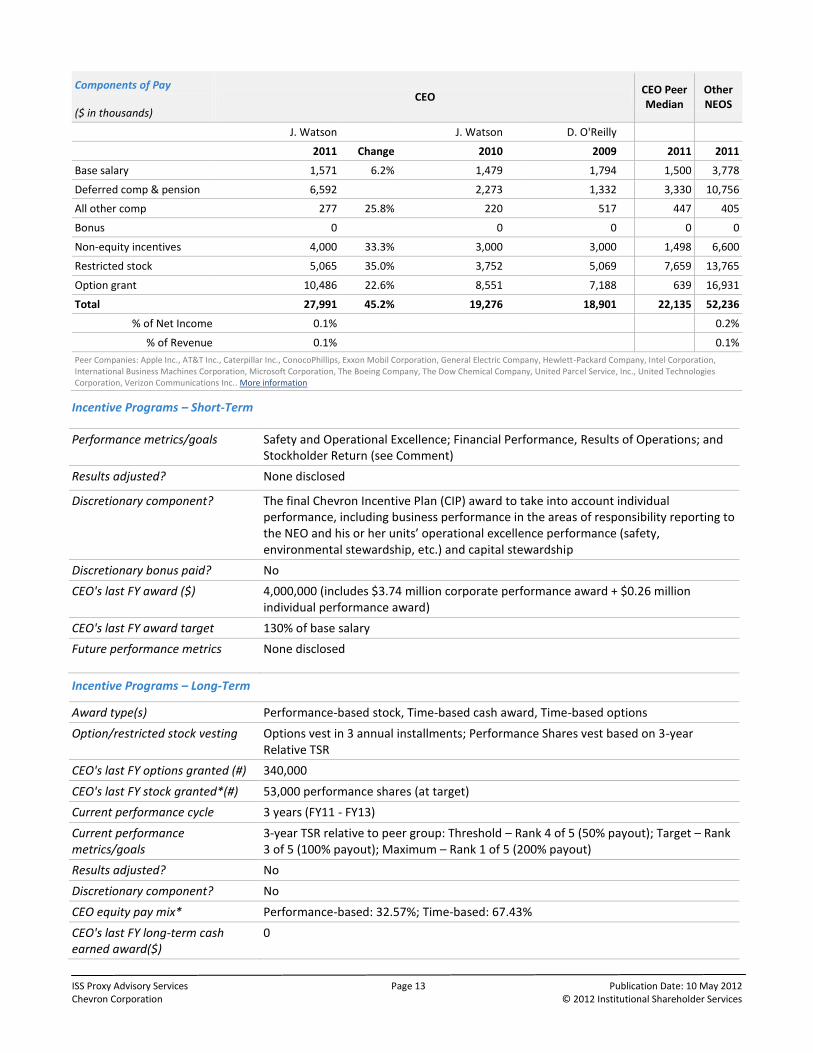

Components of Pay

($ in thousands)

CEO CEO Peer Median

Other NEOS

J. Watson J. Watson D. O'Reilly

2011 Change 2010 2009 2011 2011

Base salary 1,571 6.2% 1,479 1,794 1,500 3,778

Deferred comp & pension 6,592 2,273 1,332 3,330 10,756

All other comp 277 25.8% 220 517 447 405

Bonus 0 0 0 0 0

Non-equity incentives 4,000 33.3% 3,000 3,000 1,498 6,600

Restricted stock 5,065 35.0% 3,752 5,069 7,659 13,765

Option grant 10,486 22.6% 8,551 7,188 639 16,931

Total 27,991 45.2% 19,276 18,901 22,135 52,236

% of Net Income 0.1% 0.2%

% of Revenue 0.1% 0.1%

Peer Companies: Apple Inc., AT&T Inc., Caterpillar Inc., ConocoPhillips, Exxon Mobil Corporation, General Electric Company, Hewlett-Packard Company, Intel Corporation, International Business Machines Corporation, Microsoft Corporation, The Boeing Company, The Dow Chemical Company, United Parcel Service, Inc., United Technologies Corporation, Verizon Communications Inc.. More information

Incentive Programs – Short-Term

Performance metrics/goals Safety and Operational Excellence; Financial Performance, Results of Operations; and Stockholder Return (see Comment)

Results adjusted? None disclosed

Discretionary component? The final Chevron Incentive Plan (CIP) award to take into account individual performance, including business performance in the areas of responsibility reporting to the NEO and his or her units’ operational excellence performance (safety, environmental stewardship, etc.) and capital stewardship

Discretionary bonus paid? No

CEO's last FY award ($) 4,000,000 (includes $3.74 million corporate performance award + $0.26 million individual performance award)

CEO's last FY award target 130% of base salary

Future performance metrics None disclosed

Incentive Programs – Long-Term

Award type(s) Performance-based stock, Time-based cash award, Time-based options

Option/restricted stock vesting Options vest in 3 annual installments; Performance Shares vest based on 3-year Relative TSR

CEO's last FY options granted (#) 340,000

CEO's last FY stock granted*(#) 53,000 performance shares (at target)

Current performance cycle 3 years (FY11 - FY13)

Current performance metrics/goals

3-year TSR relative to peer group: Threshold – Rank 4 of 5 (50% payout); Target – Rank 3 of 5 (100% payout); Maximum – Rank 1 of 5 (200% payout)

Results adjusted? No

Discretionary component? No

CEO equity pay mix* Performance-based: 32.57%; Time-based: 67.43%

CEO's last FY long-term cash earned award($)

0

ISS Proxy Advisory Services Page 14 Publication Date: 10 May 2012 Chevron Corporation © 2012 Institutional Shareholder Services

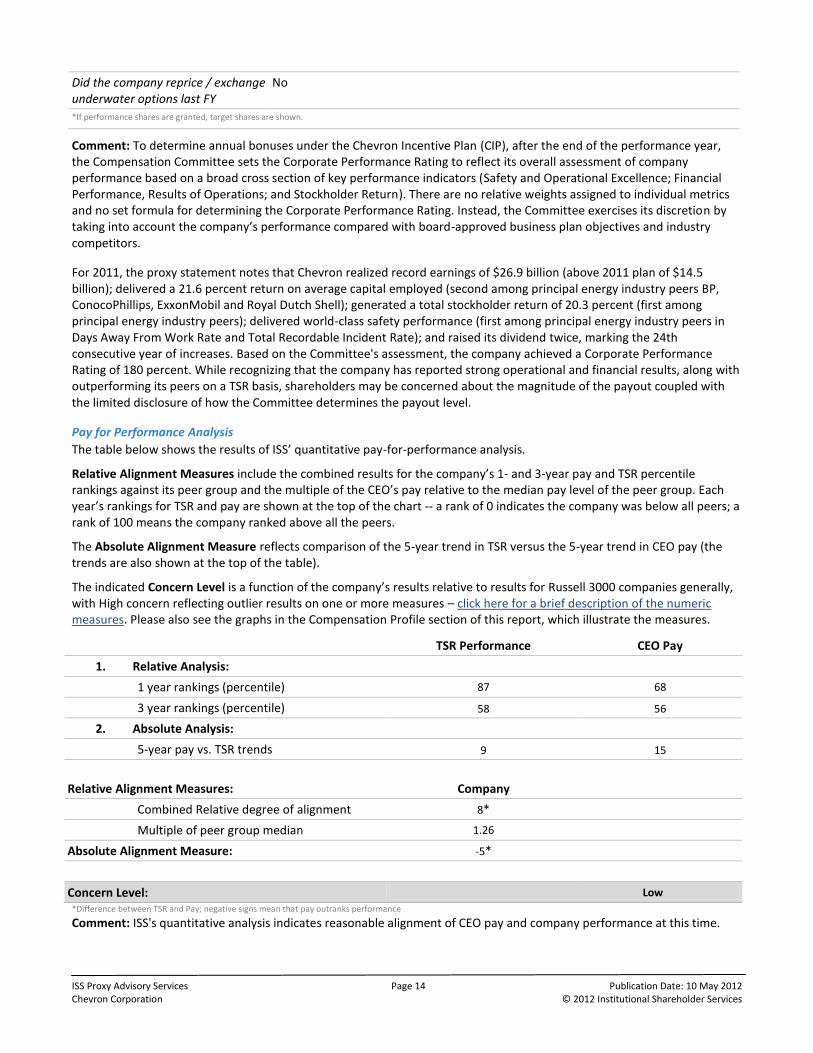

Did the company reprice / exchange underwater options last FY

No

*If performance shares are granted, target shares are shown.

Comment: To determine annual bonuses under the Chevron Incentive Plan (CIP), after the end of the performance year, the Compensation Committee sets the Corporate Performance Rating to reflect its overall assessment of company performance based on a broad cross section of key performance indicators (Safety and Operational Excellence; Financial Performance, Results of Operations; and Stockholder Return). There are no relative weights assigned to individual metrics and no set formula for determining the Corporate Performance Rating. Instead, the Committee exercises its discretion by taking into account the company’s performance compared with board-approved business plan objectives and industry competitors.

For 2011, the proxy statement notes that Chevron realized record earnings of $26.9 billion (above 2011 plan of $14.5 billion); delivered a 21.6 percent return on average capital employed (second among principal energy industry peers BP, ConocoPhillips, ExxonMobil and Royal Dutch Shell); generated a total stockholder return of 20.3 percent (first among principal energy industry peers); delivered world-class safety performance (first among principal energy industry peers in Days Away From Work Rate and Total Recordable Incident Rate); and raised its dividend twice, marking the 24th consecutive year of increases. Based on the Committee's assessment, the company achieved a Corporate Performance Rating of 180 percent. While recognizing that the company has reported strong operational and financial results, along with outperforming its peers on a TSR basis, shareholders may be concerned about the magnitude of the payout coupled with the limited disclosure of how the Committee determines the payout level.

Pay for Performance Analysis

The table below shows the results of ISS’ quantitative pay-for-performance analysis.

Relative Alignment Measures include the combined results for the company’s 1- and 3-year pay and TSR percentile rankings against its peer group and the multiple of the CEO’s pay relative to the median pay level of the peer group. Each year’s rankings for TSR and pay are shown at the top of the chart -- a rank of 0 indicates the company was below all peers; a rank of 100 means the company ranked above all the peers.

The Absolute Alignment Measure reflects comparison of the 5-year trend in TSR versus the 5-year trend in CEO pay (the trends are also shown at the top of the table).

The indicated Concern Level is a function of the company’s results relative to results for Russell 3000 companies generally, with High concern reflecting outlier results on one or more measures – click here for a brief description of the numeric measures. Please also see the graphs in the Compensation Profile section of this report, which illustrate the measures.

TSR Performance CEO Pay

1. Relative Analysis:

1 year rankings (percentile) 87 68

3 year rankings (percentile) 58 56

2. Absolute Analysis:

5-year pay vs. TSR trends 9 15

Relative Alignment Measures: Company Combined Relative degree of alignment 8*

Multiple of peer group median 1.26

Absolute Alignment Measure: -5*

Concern Level: Low *Difference between TSR and Pay; negative signs mean that pay outranks performance

Comment: ISS's quantitative analysis indicates reasonable alignment of CEO pay and company performance at this time.

ISS Proxy Advisory Services Page 15 Publication Date: 10 May 2012 Chevron Corporation © 2012 Institutional Shareholder Services

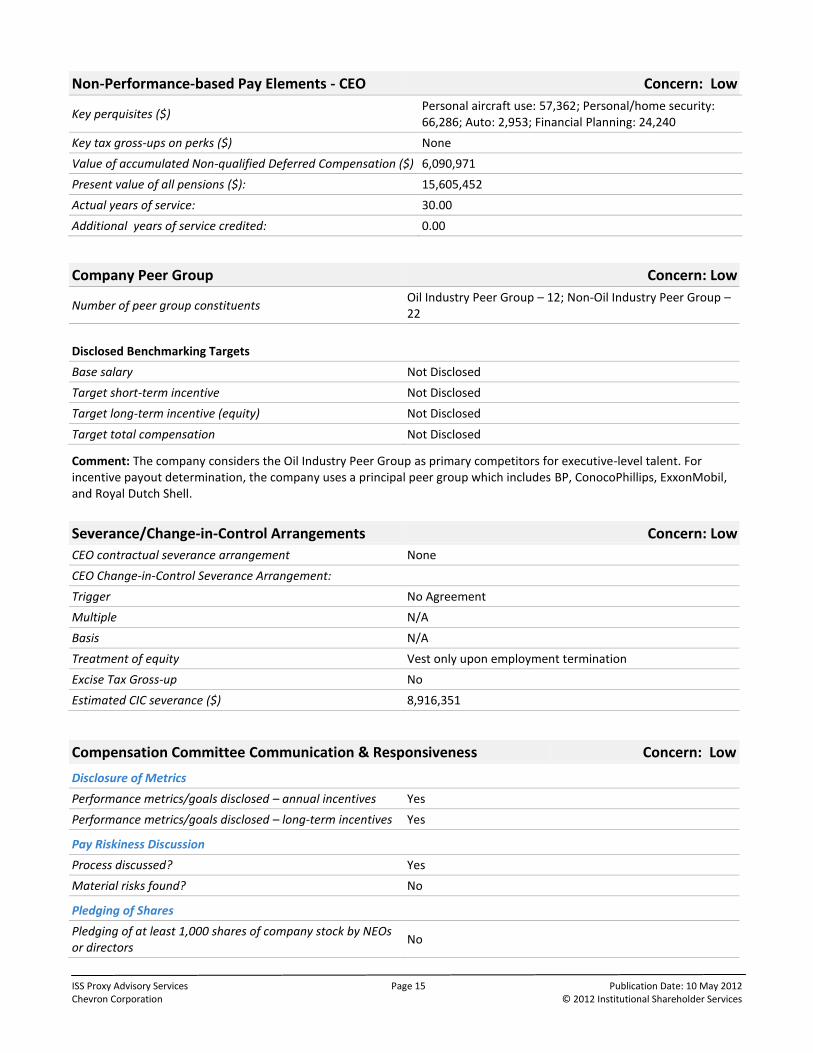

Non-Performance-based Pay Elements - CEO Concern: Low

Key perquisites ($) Personal aircraft use: 57,362; Personal/home security: 66,286; Auto: 2,953; Financial Planning: 24,240

Key tax gross-ups on perks ($) None

Value of accumulated Non-qualified Deferred Compensation ($) 6,090,971

Present value of all pensions ($): 15,605,452

Actual years of service: 30.00

Additional years of service credited: 0.00

Blank

Company Peer Group Concern: Low

Number of peer group constituents Oil Industry Peer Group – 12; Non-Oil Industry Peer Group – 22

*Includes U.S. public company peers

Disclosed Benchmarking Targets

Base salary Not Disclosed

Target short-term incentive Not Disclosed

Target long-term incentive (equity) Not Disclosed

Target total compensation Not Disclosed

Comment: The company considers the Oil Industry Peer Group as primary competitors for executive-level talent. For incentive payout determination, the company uses a principal peer group which includes BP, ConocoPhillips, ExxonMobil, and Royal Dutch Shell.

Severance/Change-in-Control Arrangements Concern: Low

CEO contractual severance arrangement None

CEO Change-in-Control Severance Arrangement:

Trigger No Agreement

Multiple N/A

Basis N/A

Treatment of equity Vest only upon employment termination

Excise Tax Gross-up No

Estimated CIC severance ($) 8,916,351

Blank

Compensation Committee Communication & Responsiveness Concern: Low

Disclosure of Metrics Performance metrics/goals disclosed – annual incentives Yes

Performance metrics/goals disclosed – long-term incentives Yes

Pay Riskiness Discussion Process discussed? Yes

Material risks found? No

Pledging of Shares Pledging of at least 1,000 shares of company stock by NEOs or directors

No

ISS Proxy Advisory Services Page 16 Publication Date: 10 May 2012 Chevron Corporation © 2012 Institutional Shareholder Services

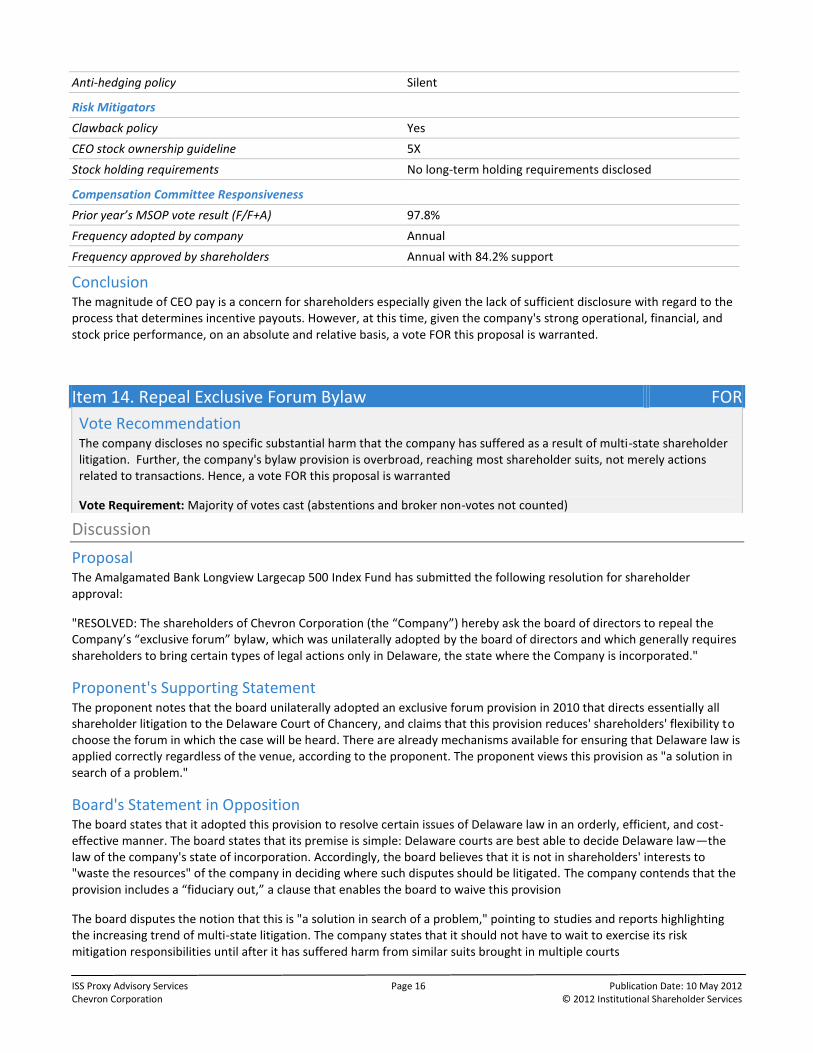

Anti-hedging policy Silent

Risk Mitigators

Clawback policy Yes

CEO stock ownership guideline 5X

Stock holding requirements No long-term holding requirements disclosed

Compensation Committee Responsiveness Prior year’s MSOP vote result (F/F+A) 97.8%

Frequency adopted by company Annual

Frequency approved by shareholders Annual with 84.2% support

Conclusion The magnitude of CEO pay is a concern for shareholders especially given the lack of sufficient disclosure with regard to the process that determines incentive payouts. However, at this time, given the company's strong operational, financial, and stock price performance, on an absolute and relative basis, a vote FOR this proposal is warranted.

Item 14. Repeal Exclusive Forum Bylaw FOR

Vote Recommendation The company discloses no specific substantial harm that the company has suffered as a result of multi-state shareholder litigation. Further, the company's bylaw provision is overbroad, reaching most shareholder suits, not merely actions related to transactions. Hence, a vote FOR this proposal is warranted

Vote Requirement: Majority of votes cast (abstentions and broker non-votes not counted)

Discussion

Proposal The Amalgamated Bank Longview Largecap 500 Index Fund has submitted the following resolution for shareholder approval:

"RESOLVED: The shareholders of Chevron Corporation (the “Company”) hereby ask the board of directors to repeal the Company’s “exclusive forum” bylaw, which was unilaterally adopted by the board of directors and which generally requires shareholders to bring certain types of legal actions only in Delaware, the state where the Company is incorporated."

Proponent's Supporting Statement The proponent notes that the board unilaterally adopted an exclusive forum provision in 2010 that directs essentially all shareholder litigation to the Delaware Court of Chancery, and claims that this provision reduces' shareholders' flexibility to choose the forum in which the case will be heard. There are already mechanisms available for ensuring that Delaware law is applied correctly regardless of the venue, according to the proponent. The proponent views this provision as "a solution in search of a problem."

Board's Statement in Opposition The board states that it adopted this provision to resolve certain issues of Delaware law in an orderly, efficient, and cost-effective manner. The board states that its premise is simple: Delaware courts are best able to decide Delaware law—the law of the company's state of incorporation. Accordingly, the board believes that it is not in shareholders' interests to "waste the resources" of the company in deciding where such disputes should be litigated. The company contends that the provision includes a “fiduciary out,” a clause that enables the board to waive this provision

The board disputes the notion that this is "a solution in search of a problem," pointing to studies and reports highlighting the increasing trend of multi-state litigation. The company states that it should not have to wait to exercise its risk mitigation responsibilities until after it has suffered harm from similar suits brought in multiple courts

ISS Proxy Advisory Services Page 17 Publication Date: 10 May 2012 Chevron Corporation © 2012 Institutional Shareholder Services

In March 2012, the company further amended the bylaw as a result of discussions with the proponents of this resolution. The board describes the March amendments as follows: "The Board amended the by-law to revise the treatment of federal claims and indispensable parties. The amendment allows claims to be brought in state or federal court in Delaware, rather than solely in the Delaware Court of Chancery. This allows federal claims with related Delaware state law claims to be brought in Delaware. The amendment also clarifies that the by-law provision is not applicable if the Delaware court does not have personal jurisdiction over a necessary defendant."

On May 3, 2012, the company filed a supplement to its proxy statement, addressing questions it had received from shareholders on this proposal. The company disclosed in that filing that it is currently litigating two "substantively identical" cases in different courts. It also noted that it has adopted best practices in many areas of corporate governance.

Analysis There is merit to the notion that Delaware judges should be the ones to apply Delaware law to Delaware companies, given their expertise and intimate familiarity with the state's body of corporate law. However, we note that there is often more than one proper forum available to shareholder plaintiffs, and the company's current bylaws curtail the right of shareholders to select any proper forum of their choosing. (We emphasize that the bylaw provision does not necessarily eliminate this right; out-of-state courts may decline to find this provision enforceable.)

Another consideration is that a company generally has two types of shareholders (although not without overlap): those that bring the types of claims targeted by this proposal, and those that do not. The latter group may benefit from an exclusive venue proposal because it is designed in part to reduce the company's litigation costs.

In order to balance these considerations, ISS take a case-by-case approach, evaluating the company's governance features in order to gauge in general terms the board's stewardship of the company on behalf of unaffiliated shareholders, and the company's disclosure relating to specific harm that it has suffered as a result of shareholder litigation brought in courts other than those in the jurisdiction of incorporation.

In this case, directors are elected annually under a majority vote standard, and the company does not have a poison pill in place. However, the company discloses no specific substantial harm that the company has suffered as a result of multi-state shareholder litigation. The March 2012 bylaw amendments do not alter the central component of the exclusive forum bylaw provision—that shareholders cannot select among various proper venues when bringing suit against or on behalf of the company. Most proposed exclusive venue provisions contain a clause enabling the board to waive the provision; the company’s inclusion of this provision is not extraordinary and does not mitigate ISS’ concerns about this provision. The company states that it is currently litigating two similar suits that this provision might address. However, we are unable to conclude that this situation is causing material harm to the company. Moreover, the company cites an academic study for the proposition that nearly half of all transactions in 2011 were the subject of litigation in more than one jurisdiction; however, the company's bylaw provision is overbroad, reaching most shareholder suits, not merely actions related to transactions. For these reasons, we recommend that shareholders support this proposal to eliminate the provision.

ISS Proxy Advisory Services Page 18 Publication Date: 10 May 2012 Chevron Corporation © 2012 Institutional Shareholder Services

Item 15. Require Independent Board Chairman FOR

Vote Recommendation A vote FOR this proposal is warranted given that lead director does not serve as an effective counterbalance to the combined roles of CEO and chairman. Specifically, the lead director does not have explicit authority to approve information that is sent to the board.

Background Information Policies: Independent Chair

Vote Requirement: Majority of votes cast (abstentions and broker non-votes not counted)

Discussion

Proposal A shareholder has submitted a proposal to request that the company adopt a policy that the chair of the board be an independent director. The resolution reads:

RESOLVED: That shareholders of Chevron (“Chevron” or the “Company”) ask the Board of Directors to adopt a policy that the Board’s Chair be an independent director according to the definition set forth in the New York Stock Exchange standards, unless Chevron common stock ceases being listed there and is listed on another exchange, at which point, that exchange’s standards should apply. If the Board determines that a Chair who was independent when he/she was selected is no longer independent, the Board shall promptly select a new Chair who satisfies this independence requirement. Compliance with this requirement may be excused if no director who qualifies as independent is elected or if no independent director is willing to serve as Chair. This independence requirement shall apply prospectively so as not to violate any Company contractual obligation at the time this resolution is adopted.

Proponent's Statement The proponent believes that an independent board chair provides a better balance of power between the CEO and the board and supports strong, independent board leadership and functioning. The primary duty of a board of directors is to oversee the management of a company on behalf of its shareholders. When a CEO also serves as chair, the proponent believes this presents a conflict of interest that can result in excessive management influence on the board and weaken the board’s management oversight.

The proponent cites a 2009 forum that endorsed the voluntary adoption of independent, non-executive chairs of boards, and notes that in 2009 less than 12 percent of incoming CEOs were also made chairs, compared with 48 percent in 2002.

In conclusion, the proponent believes that independent board leadership is key at Chevron, given the questions raised about the oversight by the board of the CEO’s management and disclosure to shareholders of the financial and operational risks to the company from the $18 billion judgment in the Ecuadorian courts in 2011.

Board's Statement The board believes that shareholder interests are best served when the board has the flexibility to determine the best person to serve as chairman, whether that person is an independent director or the CEO. Hence, implementing this proposal would deprive the board of its ability to organize its functions and conduct its business in the most efficient and effective manner. The board states that Chevron’s shareholders have consistently supported combining the chairman and CEO positions, noting that at the company’s 2007 and 2008 annual meetings, similar stockholder proposals were rejected by 64 percent and 85 percent of shares voted, respectively.

At this time, the board believes that the company and its shareholders benefit from the unity of leadership and companywide strategic alignment associated with combining the positions of chairman and CEO, pointing to Chevron’s strong financial performance and competitive returns to investors over the past five years, with TSR exceeding 11 percent for the period—more than 5 percent ahead of its nearest peer competitor and more than 11 percent ahead of the S&P 500.

ISS Proxy Advisory Services Page 19 Publication Date: 10 May 2012 Chevron Corporation © 2012 Institutional Shareholder Services

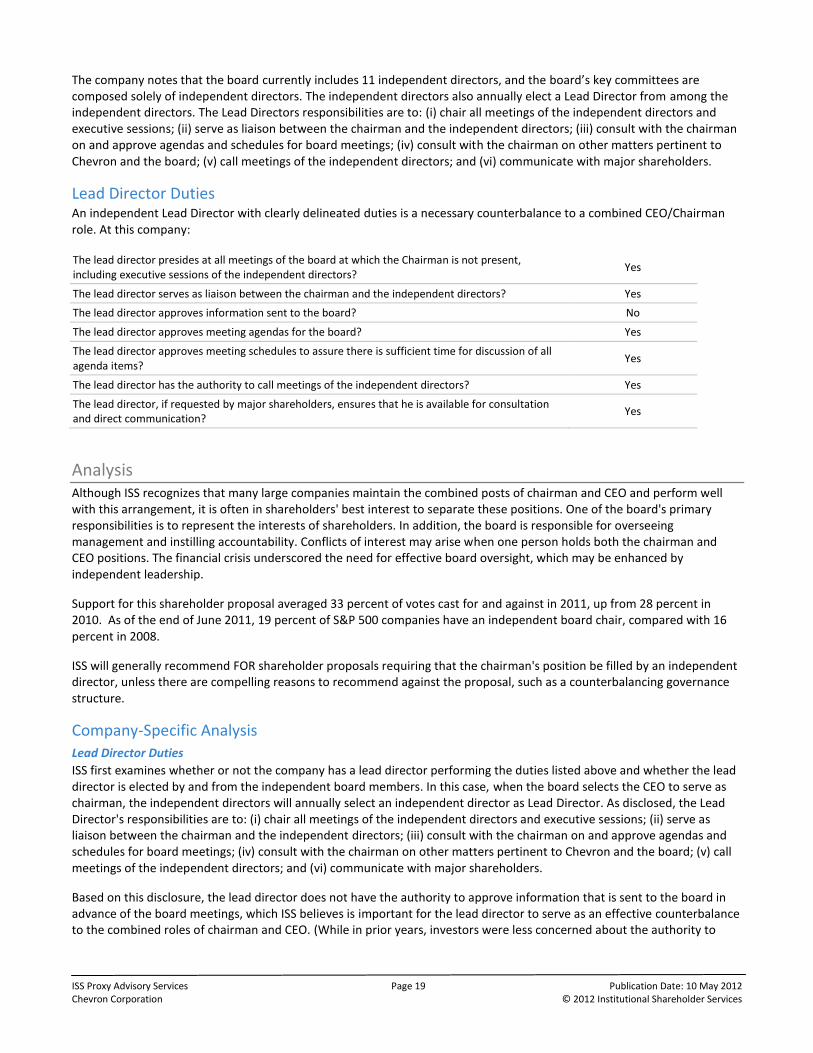

The company notes that the board currently includes 11 independent directors, and the board’s key committees are composed solely of independent directors. The independent directors also annually elect a Lead Director from among the independent directors. The Lead Directors responsibilities are to: (i) chair all meetings of the independent directors and executive sessions; (ii) serve as liaison between the chairman and the independent directors; (iii) consult with the chairman on and approve agendas and schedules for board meetings; (iv) consult with the chairman on other matters pertinent to Chevron and the board; (v) call meetings of the independent directors; and (vi) communicate with major shareholders.

Lead Director Duties An independent Lead Director with clearly delineated duties is a necessary counterbalance to a combined CEO/Chairman role. At this company:

The lead director presides at all meetings of the board at which the Chairman is not present, including executive sessions of the independent directors?

Yes

The lead director serves as liaison between the chairman and the independent directors? Yes

The lead director approves information sent to the board? No

The lead director approves meeting agendas for the board? Yes

The lead director approves meeting schedules to assure there is sufficient time for discussion of all agenda items?

Yes

The lead director has the authority to call meetings of the independent directors? Yes

The lead director, if requested by major shareholders, ensures that he is available for consultation and direct communication?

Yes

Analysis Although ISS recognizes that many large companies maintain the combined posts of chairman and CEO and perform well with this arrangement, it is often in shareholders' best interest to separate these positions. One of the board's primary responsibilities is to represent the interests of shareholders. In addition, the board is responsible for overseeing management and instilling accountability. Conflicts of interest may arise when one person holds both the chairman and CEO positions. The financial crisis underscored the need for effective board oversight, which may be enhanced by independent leadership.

Support for this shareholder proposal averaged 33 percent of votes cast for and against in 2011, up from 28 percent in 2010. As of the end of June 2011, 19 percent of S&P 500 companies have an independent board chair, compared with 16 percent in 2008.

ISS will generally recommend FOR shareholder proposals requiring that the chairman's position be filled by an independent director, unless there are compelling reasons to recommend against the proposal, such as a counterbalancing governance structure.

Company-Specific Analysis Lead Director Duties

ISS first examines whether or not the company has a lead director performing the duties listed above and whether the lead director is elected by and from the independent board members. In this case, when the board selects the CEO to serve as chairman, the independent directors will annually select an independent director as Lead Director. As disclosed, the Lead Director's responsibilities are to: (i) chair all meetings of the independent directors and executive sessions; (ii) serve as liaison between the chairman and the independent directors; (iii) consult with the chairman on and approve agendas and schedules for board meetings; (iv) consult with the chairman on other matters pertinent to Chevron and the board; (v) call meetings of the independent directors; and (vi) communicate with major shareholders.

Based on this disclosure, the lead director does not have the authority to approve information that is sent to the board in advance of the board meetings, which ISS believes is important for the lead director to serve as an effective counterbalance to the combined roles of chairman and CEO. (While in prior years, investors were less concerned about the authority to

ISS Proxy Advisory Services Page 20 Publication Date: 10 May 2012 Chevron Corporation © 2012 Institutional Shareholder Services

approve information sent to the board, ISS policy now focuses on all the functions of the lead director as disclosed in our policy. Hence, we no longer consider the responsibility to "consult" or "review" as equivalent to the authority to approve.)

Governance Features

Next, ISS reviews whether or not the company has a two-thirds independent board, all independent key committees, and established governance guidelines. In this case, the board is 82 percent independent, all key committees are entirely independent, and the company has publicly disclosed governance guidelines.

TSR Performance

ISS also examines the company's TSR performance. ISS also considers whether there has been a change in the chairman/CEO position within the past three years. In this case, the company's one- and three-year TSR are 20.16 percent, and 16.96 percent, respectively, compared to the four-digit GICS industry TSR of -11.87 percent and 21.14 percent, respectively. Hence, the company has outperformed it GICS industry group on a one-year TSR basis, but underperformed its GICS industry group on a three-year basis. Note that John Watson has served as chairman and CEO of the company since Jan. 1, 2010.

Problematic Governance Issues

Finally, ISS considers if the company has any existing problematic governance issues. In this case, ISS notes that the company has no governance issues at this time.

Conclusion After a review of each of the points above, ISS has determined that the board is more than two-thirds independent, all key committees are entirely independent, and the company has publicly disclosed governance guidelines. In addition, the company has outperformed its GICS industry group on a one-year TSR basis. Further, the governance guidelines provide for the election of an independent lead director in the event that the CEO also serves as the chairman. However, the lead director does not have explicit authority to approve information that is sent to the board. Hence, ISS does not believe that the role of lead director serves as an effective counterbalance to the combined roles of chairman and CEO. Thus, a vote FOR this proposal is warranted.

Item 16. Report on Lobbying Payments and Policy FOR

Vote Recommendation A vote FOR this resolution is warranted as the company could provide additional information regarding its lobbying policies and related oversight mechanisms.

Background Information Policies: Political Contributions Proposals

Vote Requirement: Majority of votes cast (abstentions and broker non-votes not counted)

Discussion In Brief: This is the revised resolution for the second year of a now vastly expanded campaign to get companies to report on their direct and indirect grassroots lobbying payments, proposed this year to 40 companies. A press release announcing the 2012 campaign called it a "natural extension" of the continuing effort to get companies to report their political contributions. As in the political contributions campaign, the organizers have said they are particularly concerned about corporate payments to trade associations, and unlike last year's proposal, the 2012 lobbying resolution asks specifically for "membership in and payments to any tax-exempt organization that writes and endorses model legislation." Unlike last year's proposal, it does not ask for the name of the employee who makes the decision on lobbying payments, but rather for a description of the decision-making process and its oversight. This is the first year that Chevron has received a proposal requesting disclosure of the company's lobbying-related policies and activities.

Proposal The American Federation of State, County & Municipal Employees (AFSCME) and the Needmor Fund have submitted a precatory proposal requesting the company report on its lobbying policies and expenditures.

Specifically, the resolution requests:

ISS Proxy Advisory Services Page 21 Publication Date: 10 May 2012 Chevron Corporation © 2012 Institutional Shareholder Services

"Resolved, the shareholders of Chevron Corp. ("Chevron") request the Board authorize the preparation of a report, updated annually, disclosing:

1. Company policy and procedures governing the lobbying of legislators and regulators, including that done on our company's behalf by trade associations. The disclosure should include both direct and indirect lobbying and grassroots lobbying communications.

2. A listing of payments (both direct and indirect, including payments to trade associations) used for direct lobbying as well as grassroots lobbying communications, including the amount of the payment and the recipient.

3. Membership in and payments to any tax-exempt organization that writes and endorses model legislation. 4. Description of the decision making process and oversight by the management and Board for

a. direct and indirect lobbying contribution or expenditure; b. payment for grassroots lobbying expenditure.

For purposes of this proposal, a "grassroots lobbying communication" is a communication directed to the general public that (a) refers to specific legislation, (b) reflects a view on the legislation and (c) encourages the recipient of the communication to take action with respect to the legislation.

Both "direct and indirect lobbying" and "grassroots lobbying communications" include efforts at the local, state and federal levels.

The report shall be presented to the Audit Committee of the Board or other relevant oversight committees of the Board and posted on the company's website."

Shareholders' Supporting Statement In their statement supporting the proposal, the proponents state that they encourage transparency and accountability in the use of staff time and corporate funds to influence legislation and regulation, saying that without a system of accountability, company resources could be used for policy objectives that are not in the company's long-term interests. The filers report that public disclosure shows that Chevron spent approximately $33.7 million in 2009 and 2010 on direct federal lobbying activities, and that in 2010, the company spent $2.4 million on lobbying in three states. The proponents contend these figures are insufficient to give a full picture of its relevant expenditures because they may not include grassroots lobbying and do not include the company's lobbying expenditures in states that do not require disclosure. Finally, the filers state that Chevron does not disclose its contributions to tax-exempt organizations that write or endorse model legislation, noting the company's $50,000 contribution to the American Legislative Exchange Council (ALEC) annual meeting.

Board's Statement In its response opposing the proposal, the board asserts that Chevron is committed to adhering to the highest ethical standards and complying with all laws and regulations regarding the company's political activities. The company states that, in pursuit of the interests of the company and stockholders, it advocates positions on policies that will affect the company's financial and operational performance. The board asserts that its political contributions, lobbying and grassroots programs are governed by policies and internal approval processes, and that all contributions are planned, budgeted, legally reviewed, and approved in advance by senior management. In addition, the company says it discloses an itemized list of the company's annual corporate political contributions, its philosophy for making corporate contributions, and its contributions oversight mechanism. Furthermore, the company notes that it files quarterly reports on its federal lobbying activities. Finally, the board states that Chevron has received recognition by the Center for Political Accountability for its corporate political disclosure practices and as of October 2011, was one of 43 companies in the S&P100 that disclosed any information on its indirect spending through trade associations or other tax exempt organizations.

Background on Political Contributions and Lobbying Since enactment of the 2002 Bipartisan Campaign Act (BCRA) brought renewed attention to campaign funding reform, corporate political spending, including dues used by trade associations, has become a major topic for shareholder consideration. The issue took on new relevance with the January 2010 Supreme Court ruling in Citizens United v. Federal Election Commission that restrictions on independent expenditures by corporations in federal elections violate the First Amendment. One important ramification of the Citizens United decision was its effect on lobbying. The New York Times Jan.

ISS Proxy Advisory Services Page 22 Publication Date: 10 May 2012 Chevron Corporation © 2012 Institutional Shareholder Services

21, 2010, analysis of the ruling began: "The Supreme Court has handed lobbyists a new weapon. A lobbyist can now tell any elected official: if you vote wrong, my company, labor union or interest group will spend unlimited sums explicitly advertising against your re-election." But even before the decision, new attention had been focused on corporate lobbying because of publicity over efforts to fight health care reform, climate change legislation and financial services reform, which were often handled by corporate trade associations.

According to the Center for Responsive Politics, $3.30 billion was spent on lobbying in 2011, and there were 12,633 registered lobbyists. Persons who spend more than 50 hours lobbying or earn more than $6,000 for lobbying services from a single client within a six-month period are required to register with both the U.S. House of Representatives and the U.S. Senate. Under the Federal Lobbying Disclosure Act of 1995, lobbyists are required to file quarterly annual reports on their lobbying expenses with the U.S. Congress.

Activists that have been seeking more transparency in political and lobbying expenditures have criticized the required lobbying registration reports as cryptic, and also have been increasingly concerned about the difficulty of gleaning information on the lobbying link between trade associations and companies. The House of Representatives guide to lobbying disclosure provides the following guidance on trade association lobbying:

"Employee 'A' of a trade association is a 'lobbyist' who spends 25 percent of his time on lobbying activities on behalf of the association. There are $6,000 of expenses related to Employee 'A's' lobbying activities. Employee 'B' is not a 'lobbyist' but engages in lobbying activities in support of lobbying contacts made by Employee 'A.' There are $6,000 of additional expenses related to the lobbying activities of Employee 'B.' The trade association is required to register because it employs a 'lobbyist' and its total expenses in connection with lobbying activities on its own behalf exceed $11,500."

However, trade associations do not have to disclose who their members are or the names of corporations or other entities they get the funds from to lobby on a specific issue. Activists argue that trade association dues may end up supporting trade association lobbying efforts that do not align with a company's stated positions. This has become an important element of the nine-year-old shareholder campaign for political contributions disclosure coordinated by the Center for Political Accountability, and appears central to this companion campaign for lobbying expenditure disclosure.

A November 2011 report that was issued by the IRRC Institute, "Corporate Governance of Political Expenditures: 2011 Benchmark Report on S&P 500 Companies," found that 80 percent of the S&P 500 spend money on lobbying. But it found that only 13 firms provided easily accessible information on lobbying expenditures. The study also found: "Two-thirds of companies in the S&P 500 do not mention lobbying when they talk about political spending, confining their statements to campaign spending issues. Sixty percent of the 100 biggest companies do discuss lobbying (and they are the biggest spenders of lobbying dollars), but there is a striking drop-off among those outside the top revenue tier. Just half of the 25 companies that spent the most on lobbying in 2010 (each more than $8 million) have disclosed policies about this activity. Less than a dozen companies explicitly acknowledge the "grassroots" lobbying efforts they make to mobilize their various stakeholders, including employees and the public, in attempts to influence public policy."

Lobbying Agreements and Corporate Disclosure

While lobbying disclosure, at the level requested by the proponent, is not as established a practice as similar political contributions disclosure, some companies have begun or agreed to begin to increase their lobbying disclosure. Of the 40 proposals filed in the 2012 campaign, 12 proposals, thus far, have been withdrawn after agreements for increased disclosure. These withdrawal agreements were reached at CIGNA, Coca-Cola, Eli Lilly, General Electric, Johnson & Johnson, Northrop Grumman, Occidental Petroleum, PG&E, St. Jude Medical, Target, YUM! Brands, and Zimmer Holdings. Additionally, Prudential Financial serves as an example of a company that has already adopted a practice and included lobbying expenditures in its Political Activity & Contributions Report. In this report Prudential provides a listing of trade associations where it has paid dues and contributions of more than $50,000 and divides out the portion of its dues that have been used for lobbying.

Controversy over Lobbying as an Appropriate Subject for Shareholder Resolutions

Debate about whether shareholder resolutions on lobbying are appropriate has been resolved in favor of the lobbying disclosure campaign — though not other types of lobbying resolutions — and has illuminated some of the issues behind the campaign for both the corporate targets and the activists. In 2011, IBM received a lobbying disclosure proposal from the American Federation of State, County and Municipal Employees, the filer of new lobbying proposals that year. The company was unsuccessful in a challenge that would have allowed it to omit the lobbying proposal under the section of the SEC's

ISS Proxy Advisory Services Page 23 Publication Date: 10 May 2012 Chevron Corporation © 2012 Institutional Shareholder Services

shareholder proposal rule that allows companies to exclude shareholder resolutions that deal with "ordinary business" issues that are for management, not shareholders, to decide. The company contended that it should be able to omit the proposal because the kind of reporting requested "necessarily includes a variety of activities and expenditures incurred by IBM in the ordinary course of business which are made in connection with the sales, support and servicing of IBM's mainline product and service offerings. Given the quantum of data and desired disclosures on ordinary business matters, and the Proponent's desire to impose its own specific detailed methodology for the disclosures, implementation of the Proposal would clearly probe too deeply into matters of a complex nature upon which stockholders, as a group, are not in a position to make an informed."

IBM pointed out that the SEC staff has many precedents for omitting resolutions on lobbying. Historically, most shareholder resolutions that have raised questions about lobbying have dealt with specific issues, such as tobacco, and the SEC staff has allowed companies to exclude such proposals; back in 1989, even while the SEC staff switched its position on smoking and agreed that it was a suitable subject for a shareholder resolution, it nevertheless sanctioned omission of a resolution on tobacco-related lobbying on ordinary business grounds. As recently as 2009, Abbott Labs and Bristol-Myers Squibb were allowed to omit resolutions from the AFL-CIO on lobbying for the Medicare drug benefit on grounds that the resolution involved "lobbying activities concerning its products." But in one of the rare instances of more general shareholder resolutions on the issue, the staff in 2010 required PepsiCo and Wal-Mart to have votes on a resolution from a conservative group, the National Legal and Policy Center, asking for reports on their policy advocacy activities, rejecting ordinary business arguments from both companies. It echoed those decisions in a Jan. 24, 2011, no-action letter requiring IBM to include the AFSCME proposal. In rejecting IBM's argument, it said, "the proposal focuses primarily on IBM's general political activities and does not seek to micromanage the company to such a degree that exclusion of the proposal would be appropriate," but gave no further details on its reasoning.

In successfully arguing that its proposal did not constitute ordinary business, AFSCME contended, among other things, that "Lobbying by trade associations, financed by corporate members whose identities are not disclosed, received a great deal of attention because of concern that it subverts disclosure regulations and allows corporations to avoid accountability for their lobbying activities." The union concluded that "it is indisputable that there is a robust public debate over the role that corporate lobbying, including lobbying done though conduit organizations, plays in the U.S. political process."

The correspondence indicated that the proponents had a particular concern about recent allegations that corporations had been funding simulated grassroots citizen communications, using third-party front groups. It cited allegations that corporate-funded fake grassroots activism was behind the protests over "death panels" that supposedly would have resulted from health care reform legislation, as well as tea party protests against the Obama administration's stimulus proposals. The proponents also cited an Aug. 20, 2009, Newsweek article, "The Browning of Grassroots," which it said "reported on a leaked email from the American Petroleum Institute seeking to orchestrate, through funding and logistical coordination, seemingly independent protests against climate change legislation."

The American Legislative Exchange Council

In addition to expressing concerns with corporate direct, indirect and grassroots lobbying activities, the proponents also reference support for tax-exempt organizations that write and endorse model legislation and specifically cite support for ALEC. ALEC is a non-profit policy organization and according to the organization's Web site, its mission is "…to advance the Jeffersonian principles of free markets, limited government, federalism, and individual liberty, through a nonpartisan public-private partnership of America’s state legislators, members of the private sector, the federal government, and general public…" The private sector is represented at ALEC by the organization's Private Enterprise Board. Since the organizers of the shareholder campaign on lobbying submitted their resolutions, ALEC’s profile has been raised through its association with “stand your ground” model legislation based on the Florida law that has been noted in the February killing of teenager Trayvon Martin by a neighborhood watch volunteer and voter identification legislation. In the past, ALEC has been associated with legislation regarding contentious issues, including model legislation that would repeal state climate-change initiatives and voter identification laws.

Since controversy has broken out over ALEC this spring, a number of corporate members, including Coca-Cola, PepsiCo, Kraft, Wendy's, and McDonald's, have announced decisions not to renew membership in the group. On April 17, 2012, ALEC announced a reorganization plan that will close down its public safety and elections unit, which encouraged passage of stand your ground and same-day voter ID measures. A press release issued by a spokesman for the group said it is

ISS Proxy Advisory Services Page 24 Publication Date: 10 May 2012 Chevron Corporation © 2012 Institutional Shareholder Services

"eliminating the ALEC Public Safety and Elections task force that dealt with non-economic issues and reinvesting these resources in the task forces that focus on the economy."

Related Shareholder Activism

In 2011, AFSCME launched its campaign to get companies to report on their direct and indirect grassroots lobbying payments, submitting a resolution to nine companies. The proposal used the basic format of the resolution in the long-running campaign coordinated by the Center for Political Accountability (CPA) to get companies to report their political contributions, substituting lobbying for political spending. The SEC staff allowed two companies, Citigroup and Occidental Petroleum, to omit the proposal, agreeing that it was "substantially the same" as the CPA political contributions proposal, which they had also received and which had arrived first, and which they were planning to include in their proxies. After further attrition because of two negotiated withdrawals, the resolutions came to votes at five companies. They received an average of 24.2 percent support, with the average drawn down by a vote result of 8 percent at Prudential Financial. The other votes were Bank of America (32.7 percent), ConocoPhillips (24.6), IBM (28.5), and Raytheon (25.6).

In 2012, AFSCME has been joined by a coalition of shareholder activists from many corners of the proponent community, including SRI and church groups, in submitting a revised version of the 2011 lobbying resolution to 40 companies. Timothy Smith, executive vice president of the SRI group Walden Asset Management, joined with John Keenan of AFSCME in organizing the effort. As of April 3, 12 proposals had been withdrawn following agreements.