chicagobta allied member hotel industry update john hach senior vice president travelclick august 2...

TRANSCRIPT

ChicagoBTAAllied Member Hotel Industry Update

John Hach Senior Vice President TravelClick August 2nd, 2012

1

Agenda:

Global hotel performance Global hotel performance

Regional analysis of key North American markets Regional analysis of key North American markets

Local Chicago market perspectiveLocal Chicago market perspective

2012 / 2013 Outlook2012 / 2013 Outlook

Corporate, consortia, BAR research findingsCorporate, consortia, BAR research findings

2

At-A-Glance | Global Trends

Source: Smith Travel Research Note: Europe based on Euro, all other regions in USD. Q1 2012.

3

At-A-Glance | Global Trends: Americas

ADR are in local currency. Source: Smith Travel Research. Q1 2012.

4

The Brand Website revenue contributed 22.5% of the $7.6 billion total revenue booked

Highlights | First Quarter 2012

Revenue by Channel2012 Q1

5

Source: MarketVision Demand Position. Top 50 markets worldwide from participating brands

Shifting Reservations First Quarter Comparison

6

2012 Q12012 Q1 2011 Q12011 Q1

Source: MarketVision Demand Position. Top 50 markets worldwide from participating brands

Third Party Internet Reservations

7

Source: MarketVision Demand Position. Top 50 markets worldwide from participating brands

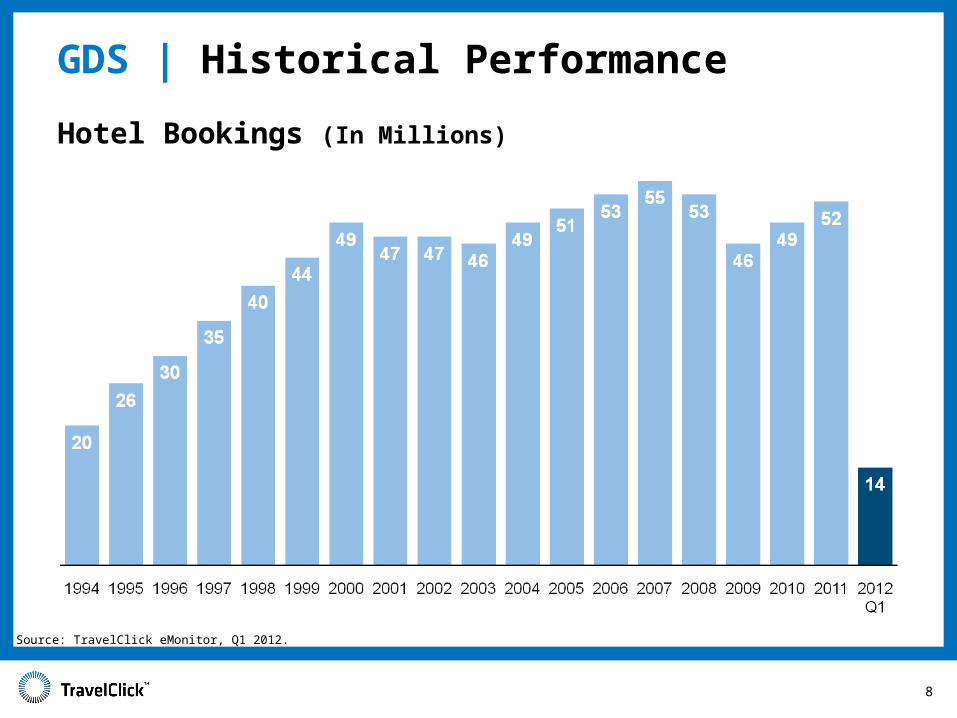

Hotel Bookings (In Millions)

GDS | Historical Performance

Source: TravelClick eMonitor, Q1 2012.

8

ADR by Channel

9

Source: MarketVision Demand Position. Top 50 markets worldwide from participating brands

• For the third quarter of 2012, overall committed occupancy is up 6.8% year-over-year for the top 25 markets.

• Committed occupancy for the group segment is up 5.6% and the transient segment is up 9.9% compared to a year ago.

• ADR for the second quarter is 7.0% ahead compared to the same time last year.

• The group segment ADR is up 6.0% and the transient segment ADR is up 7.5% compared to a year ago.

Emerging Trends / Third Quarter 2012

10

2012 Occupancy OutlookCommitted Occupancy

11

Legend

Total

Variance – All Markets

Scope:Committed Occupancy (Group Block + Transient Reserved)

Q2, 2012 – Q1, 20131.7%

2.2%21.1%7.4%3.2%

-0.5%4.3%

-2.6%7.4%

-1.5%6.6%

12.3%-6.5%5.3%4.7%4.0%

-1.4%7.9%5.5%6.3%

-3.2%3.7%

13.1%1.1%1.7%

Source: MarketVision Demand Position.

3.4%9.4%7.7%8.9%5.3%4.8%8.3%

10.8%5.2%3.2%6.1%4.1%7.4%6.7%5.9%9.9%5.3%6.2%7.3%9.3%7.1%5.3%9.6%

-0.1%1.2%

2012 Average Daily Rate Outlook

12

Note: CAD has depreciated versus the USD by 4% year over year

Legend Total

Variance – All Markets

Scope:ADR (Group Reserved, Transient Reserved)

Q2, 2012 – Q1, 2013

Source: MarketVision Demand Position+6.1%

2012 RevPAR Outlook

13

Note: CAD has depreciated versus the USD by 4% year over year

Scope:RevPAR (Group Reserved, Transient Reserved)

4.4%7.7%

12.3%14.0%8.3%

11.3%9.1%

28.6%10.9%3.3%9.9%5.9%3.2%

11.4%8.0%5.2%2.1%

14.2%10.6%15.9%6.1%8.2%

14.0%0.4%4.7%

Legend

Total

Variance – All Markets

Q2, 2012 – Q1, 2013

Source: MarketVision Demand Position

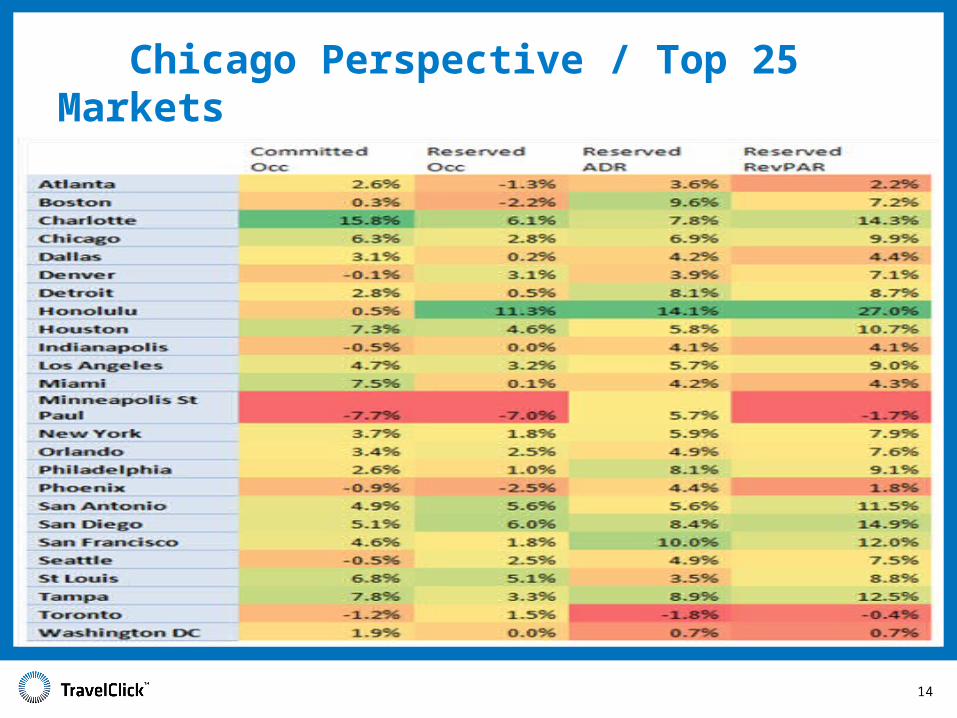

Chicago Perspective / Top 25 Markets June 2012 Through May 2013

14

Corporate / Consortia / BAR

Research Project

15

Corporate Negotiated Rate Disbursement

16

Consortia / BAR Rate Disbursement

17

• Bookings Per Unique Agency

Corporate: 1 booking per 31.5 agencies

BAR: 1 booking per 1.8 agencies

Consortia: 1 booking per 2.3 agencies

Corporate / Consortia / BAR: Research Project

Survey Period: May 2012

Sample Size: 1,200,00 Bookings

18