china’s pan-semiconductor industry s pan-semiconductor industry overview allen lu, ph.d...

TRANSCRIPT

China’s Pan-Semiconductor Industry Overview

Allen Lu, Ph.D

President, SEMI China

GSF Shanghai, March. 9, 2012

Outline

• Semiconductor

• PV

• LED & LCD

• SEMI in China

Americas

27%

Taiwan

12%

China

12%

Europe

14%

India

1%

Japan

23%

Korea

9%

Singapore

2%

CHINA 245

Companies

EUROPE 259

Companies

INDIA 15

Companies

JAPAN 435

Companies

KOREA 167

Companies AMERICAS 521

Companies

SINGAPORE 33 Companies

TAIWAN 216

Companies

1,862 Members As of July 2011

Location of SEMI Member HQs

Total Members by Size

Under $5 M

67%$1B - $2B

1%

$500M - $1B

1%

$100M - $500M

3%

Over $2.5B

>1%

$25M - $100M

6%

$5M - $25M

22%

SEMI: The Global Association

SEMI: The Professional Association

• Established in 1970 to serve the semiconductor supply chain.

• Professional Services

– SEMI Standards

– ITRS

– Industry Research and Statistics

– Trade Shows

– Conferences

– Special interest groups (SIG)

March 20-22, 2012

SEMI Industry Platform Semiconductor Emerging Market PV

Global Pan-Semiconductor Industry Scale

Semiconductor FPD

LED

PV

-0.1

0

0.1

0.2

0.3

0.4

0.5

0.6

1 10 100 1000 10000

CA

GR

Revenue ($ Billion) Source: SEMI, 2011

China’s Semiconductor Industry

Real GDP Growth Rates

Source: IHS Global Insight Jan. 2012

Real GDP Measured in 2005 US$

China Electronic Product Output

Source –CVIA, Ministry of Information Industry of China, SEMI, May 2011

Example of China’s Electronic Product Output in 2010

Output

(Million

units)

Growth

Rate

% of World

Output

Export

(Million

units)

Cell

Phone 998 35% 62% 758

Color TV 114.9 16% 47% 66.3

FPD TV 90.9 25% 48% 52.3

Notebook

PC 193.8 19% 93% 185.9

Digital

Camera 109 14% 75% 91.3

10

China IC Market and Forecast

Source:CCID, SEMI China

RMB

Billion

11

Installed Capacity by Region

2011 Capital Equipment Markets:

Europe

10%

Japan

13%

Korea

20%

North

America

20%

Taiwan

20%

China

9%

ROW

8%

Europe

6% Japan

11%

Korea

21%

North

America

15%

Taiwan

28%

China

9%

ROW

10%

2010 Market Billings = $39.5B 2011 Market Billings = $43.8B

Source: SEMI/SEAJ Feb 2012

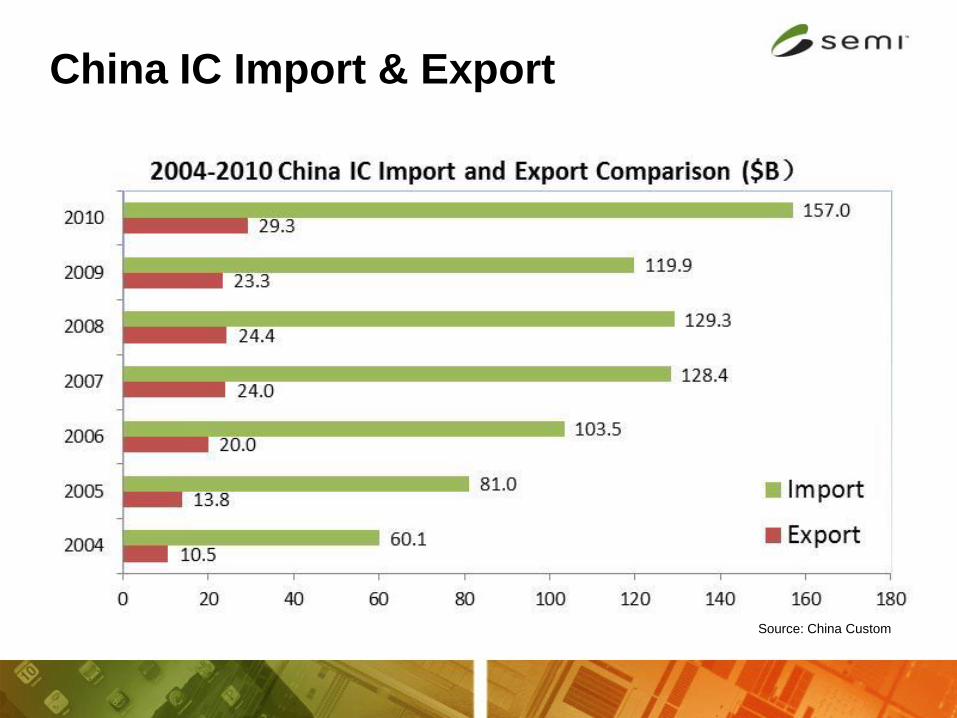

China IC Import & Export

Source: China Custom

2010 Top Importing Goods in

China

14

Source: China Custom

Fig.: 2010 Importing Goods Value of China

单位:10亿美金

China Government Policies

on Semiconductor Industry

• China economy stimulus program on domestic consumption – Home appliance, infrastructure, …

• 12th five year (2011-2015) plan:

– To 2015 target: double annual China IC sales to RMB 330B, CAGR: 18%

• China National Projects (2006-2020): – Project 01: The CORE of electronic devices, HIGH-END general-

purpose chip, software, systems

– Project 02: VLSI Equipment & Material Manufacture and Process Technology R&D (33B RMB funded so far)

• Regional government’s desire and resource to grow Semiconductor industry

Beijing

Xian

Chengdu

Guangzhou

Hong Kong

Leshan

Shanghai

SMIC Fab B1 300 mm

SMIC Fab B2 300 mm

SGNEC Fab 1 150 mm

Legend

Site in production or

ramp Site under construction

* Site equipping

Site in plan

City of population >7M

City of population <7M

Capital

Shenyang

Wuxi

Hynix-Numonyx Fab C1 300 mm

Hynix-Numonyx Fab C2 300 mm

CSMC Fab 1 150 mm

CSMC Fab 2 200 mm

CSMC Fab 5 150 mm Suzhou

Hejian Fab 1 200 mm

Kushan IC Spectrum 200 mm

Anadigics 150 mm

Hangzhou

Silan Fab 2 150 mm

Lion Fab x 150mm

Ningbo BYD Semiconductor

Fab 1 150 mm

Zhuhai ACSMC Fab 1 150 mm

Shenzhen Founder Electronics 150 mm

SMIC Fab 16A/B 300 mm

SMIC Fab 15 200 mm

Xiyue Fab 1 150 mm

ProMOS Fab x 200 mm

CSEC Fab x 150mm

Nantong GMIC Fab 1 200 mm

TI China Fab 200 mm

Dalian

Intel Fab 68 300 mm

Chongqing Wuhan

WXIC Fab 12 300 mm

SMIC Fab 7 200 mm

Tianjin

LPSC Fab 1 150 mm

SMIC Fab 1 200 mm

SMIC Fab 2 200 mm

SMIC Fab 3 Backend

GSMC Fab 1 200 mm

GSMC Fab 2 200 mm

GSMC Fab 3 300 mm

HHNEC Fab 1 200 mm

HHNEC Fab 2 200 mm

HHNEC Fab 1C 200 mm

Huali Fab x 300 mm

ASMC Fab 2 150 mm

ASMC Fab 3 200 mm

ASMC Fab 4 200 mm

BCD Fab 1 150 mm

BCD Fab 2 150 mm

TSMC Fab 10 200 mm

Belling Fab 2 150 mm

SMIC Fab 8 300 mm

SMIC Fab 9 CIS

Leshan

Jiling

Fuzhou

Fushun Microelectronics Fab 2 150 mm

Xiamen Jishun Microelectronics Fab 150mm

JSMC Fab-x 150 mm

Dong Ying Fab X 200 mm

Shangdong

Zheng Zhou Honest Trust

FabX 200 mm

Henan

Henan

Where will be

Samsung’s

12 inch fab?

Semiconductor Wafer Fabs in China

Source: SEMI

12 inch: expansion

ongoing

6~8 inch: Secondary

equipment market

active

Assembly and Testing Plants in China

Intel Chengdu:

one of Intel

biggest P&T

centers

Hitech: P&T for

Hynix DRAM,

start on 2009

Nov.

AMD: announce

to double

Suzhou P&T

house capacity.

CJ-Electronics:

shoot at world

top5 P&T houses

Nantong-Fujitsu:

shoot at world

top 10 P&T

houses

Source: SEMI China Semiconductor Packaging Market Outlook

China IC Industry by Segment

45 82 124 186 226 235 270 364

455

63 181

233

309 398 393 341

447 438

244

283

345

512

628 619 498

629 617

0

200

400

600

800

1000

1200

1400

1600

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011(E)

China IC Industry by Segment (in 100M RMB)

IC design IC Manufacture Packaging & Testing

Source: CISA, SEMI, 2011

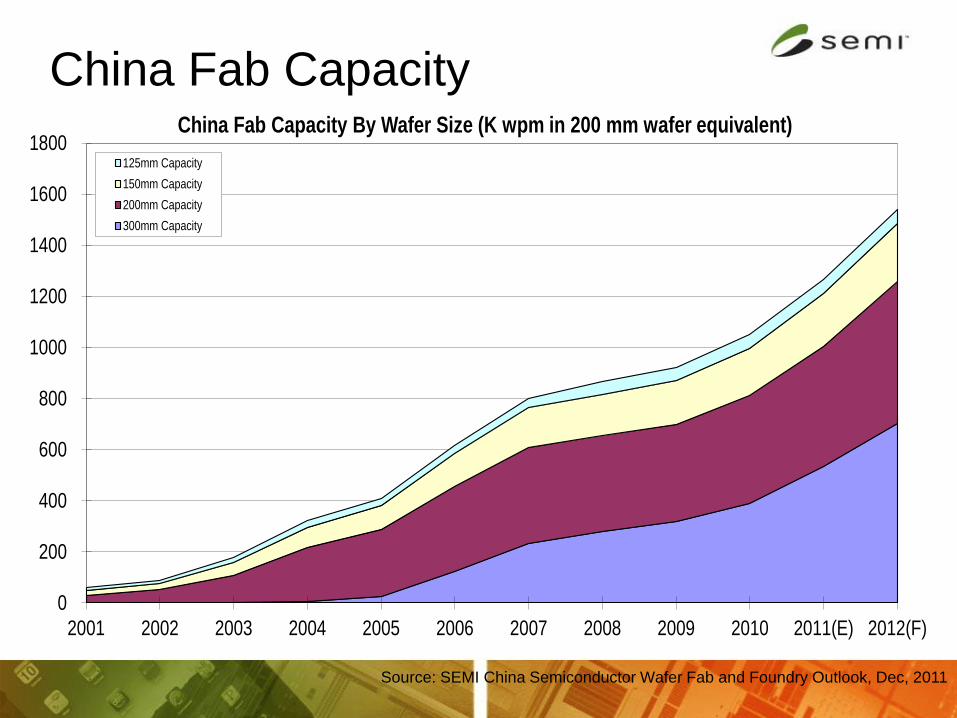

China Fab Capacity

0

200

400

600

800

1000

1200

1400

1600

1800

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011(E) 2012(F)

China Fab Capacity By Wafer Size (K wpm in 200 mm wafer equivalent)

125mm Capacity

150mm Capacity

200mm Capacity

300mm Capacity

Source: SEMI China Semiconductor Wafer Fab and Foundry Outlook, Dec, 2011

Some of Opportunities for China

• China has to narrow the wide gap between IC consumption and producing

– government and industry mandate

• Leading foundries need to be competitive.

• Fully leverage application market:

– Automobile, analog, power, micro-controller, mobile, RFID, …

– “Virtual IDM”?

• Equipment company growth through PV and LED, move up the value

chain (Project 02).

• Common research platform for technology and IP

• Capture IC Manufacturing move to China

• Re-use fab line for consumer electronics IC (non-leading edge)

Fabs Sold /Closed in 2010

8” NXP Böblingen

8” Altis

8” ST Phoenix

8” Atmel Rousset

8”, 12” Qimonda U.S.

8”, 12” Spansion Japan

8” SMIC Chengdu

12” ProMOS Hsinchu

Fabs Sold /Closed in 2010

8” NXP Böblingen

8” Altis

8” ST Phoenix

8” Atmel Rousset

8”, 12” Qimonda U.S.

8”, 12” Spansion Japan

8” SMIC Chengdu

12” ProMOS Hsinchu

Can China capture next wave of

opportunities => IC fab with global product

partnership?

China’s PV Industry

Global PV Market

• 2011 is another remarkable year for global PV industry.

• Effected by government policies, decreasing price, and invest climate,

global PV installation capacity achieved a new height in 2011. 24

Source: EPIA, SEMI

Japan, 3622

NA, 2727

APEC, 593

China, 893

Rest of World, 1854

Belgium, 803

Czech Republic, 1953

France, 1025

Germany, 17193

Italy, 3494

Spain, 3784

Rest of EU, 1000

EU, 29252

Japan

NA

APEC

China

Rest of World

Belgium

Czech Republic

France

Germany

Italy

Spain

Rest of EU

Europe Leads Global PV Market

25

2010 Cumulated Global PV Installation Market Share(MW)

• By the end of 2010, EU takes 74% of global cumulative PV installation

capacity.

• Above all, Germany achieved 17GW cumulative capacity by the end of

2010, which takes 43.5% of global total.

Source: EPIA

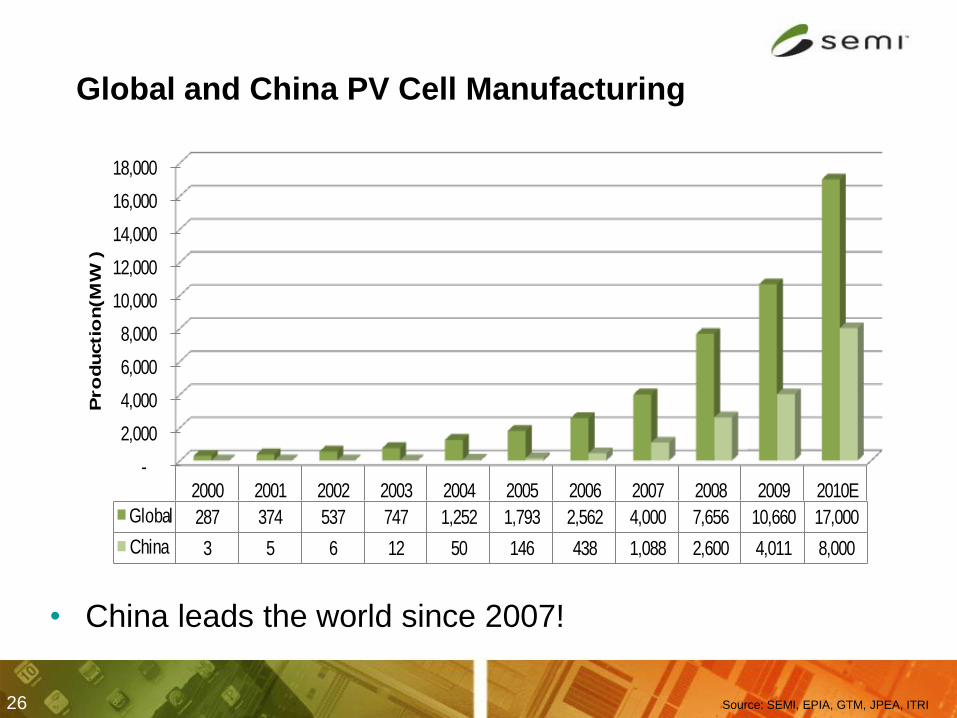

Global and China PV Cell Manufacturing

26

Global and China Cell Production

• China leads the world since 2007!

Source: SEMI, EPIA, GTM, JPEA, ITRI

-

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010E

Global 287 374 537 747 1,252 1,793 2,562 4,000 7,656 10,660 17,000

China 3 5 6 12 50 146 438 1,088 2,600 4,011 8,000

Pro

du

ctio

n(M

W)

550

560

600

650

800

800

800

930

1000

1000

1100

1200

1450

1800

1800

Solarfun

E-Ton Solar

Kyocera

SunPower

Sharp

Canadian Solar

Neo Solar

Gintech

Motech

Yingli

Trina

Q-Cells

First Solar

Suntech

JA Solar

225

260

260

326

360

368

398

399

400

509

525

537

595

704

1011

E-Ton Solar

Snayo

Ningbo Solar

Canadian Solar

Motech

Gintech

SunPower

Trina

Kyocera

JA Solar

Yingli

Q-Cells

Sharp

Suntech

First Solar

Global Leading Cell Manufacturers

2009 Shipment (MW) 2010 Year End Capacity (MW)

Data Source:Photon, GTM Research, SEMI

Polysilicon Plants in China

Data Source: SEMI

Monthly PV Products Price

• In 2011, PV products price experienced startling decline, which surprised

everyone.

• Dropping price actually pushed the industry consolidation.

29

Source: SEMI

China PV company

performance

• China PV companies are facing a tough time.

• Since 2011, Increasing shipment did not equal to increasing revenue any

more. 30

Source: Companies report, SEMI

China PV company

performance

• PV manufacturers must deal with new operation issues, other than general

market demand, since great changes in supply chain and market sentiment.

31

Source: Companies report, SEMI

SEMI PV Book to Bill

• The results of SEMI book to bill program indicated great changes in industry

in 2011.

• Q3’11 worldwide PV equipment Book-to-Bill ratio extended last quarter’s

decline to its lowest level since Q1’10. 32

Source: Bundesnetzagentur, SEMI

• Driven by policy and program, installation capacity in China is starting to grow fast since 2009.

• China PV installation takes 2.1% of global in 2009, and about 3.5% in 2010.

• With high sun irradiation and surge in the electricity demand, China is expected to be

one of the major PV market in the future.

33

China PV Installation (2000-2010)

Source: IEA World Energy Outlook 2010, SEMI

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010E

Annual 3 11 15 10 9 4 12 20 45 160 500

Accumulated 19 30 45 55 64 68 80 100 145 305 805

0

100

200

300

400

500

600

700

800

900

Ch

ina I

nst

allati

on

(MW

)Annual Accumulated

China policy

BIPV Program

Golden Sun Program

China PV FiT Policy

China 12th Five-Years Planning

Inspiring PV Target for 2020

34

SEMI recommendation:

China PV Roadmap for 2020

• China clean energy commitment: by year 2020 – To reduce its carbon intensity(CO2 emission per unit of GDP) by 40-45% from the 2005 level

– To increase the share of non-fossil fuels in the primary energy use to 15%

• Earlier 2011, SEMI PV Group, SEMI China PV Advisory Committee, and

China PV Industry Alliance released new recommendations for China PV

Roadmap. Using the IEA solar PV roadmap as a benchmark, China will

need to have 60GW installed PV capacity by year 2020, and 269 GW by

year 2030.

35

2010(Actual) 2020 2030

Total Electricity Generation(TWh) 4192 6949 8776

% of PV Electricity <0.5% 1.30% 4.60%

Electricity Generation from

PV(TWh)

<2 90 404

Total Installed PV Capacity(GW) 0.7 60 269

China PV installation

• Benefited by series of China PV application policies, PV installation capacity in

China has shown remarkable growth since 2010.

• PV FiT policy effected much than any other policies and programs in China.

36

Source: SEMI, EPIA

China PV installation

• Benefited by series of China PV application policies, PV installation capacity in

China has shown remarkable growth since 2010.

• PV FiT policy effected much than any other policies and programs in China.

37

Source: SEMI, EPIA

China’s LED Industry

LED Industry Supply Chain

39

LED Fab:

epitaxy growth&

Chip

LED package &Module Application

Systems Substrate

Back-End

PCB

Heat sinks

IC Drivers

Cables…

Upstream

MOCVD,

PECVD, Etch, PVD, Laser scribing

MO Chemicals, Sapphire ,SiC Substrate

….

Middle Process

Plasma cleaning, Wire

bonding, coating..

Lead Frame, Resin

phosphor, Gold/copper

wire

…

Big push in frontend manufacturing to China in the last two years

40

$-

$5,000

$10,000

$15,000

$20,000

$25,000

$30,000

$35,000

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

HB LED Manufacturing Industry Revenue by Application General Lighting Personal Lighting

Projectors Signs and displays

Automotive Cell Phones

Other Displays LCD TV and Monitors

Laptops and Netbooks

Source: Yole; SEMI China ;

Inve

stm

ent

LE

D %

In L

CD

TV

LE

D %

In L

igh

ting

Wo

rld E

co

no

my

• 2011, the global LED Manufacturing Industry had a slight growth, much lower than

expectation .

Global LED Manufacturing Industry

14 National LED Lighting Industry Bases In China

41

“National Semiconductor Lighting Project” Sponsored By MOST (Ministry of Science and Technology )

14 LED lighting industry bases have been built in Shenzhen, Shanghai, Dalian, Nanchang, Xiamen, Yangzhou and Shijiazhuang, Tianjin ,Wuhu, etc. where concentrates most of China LED manufacturers.

Shanghai

Yangzhou

Xiamen

Nanchang

Shenzhen

Shijiazhuang

Dalian

Source: SEMI China, 2011

Dongguan

Tianjin

Hangzhou

Weifang

Changzhou

Wuhan

Xi’an

China’s LED Industry

42

Source: CSA; SEMI China ;

• China LED Industry kept growing in 2011.

811 12 14

1924

3136

41

55

69 76

0

10

20

30

40

50

60

70

80

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

China LED Fabs Quantity

Source: SEMI China

LED wafer and Chip Fabs Qty. in China

(2000-2011l)

• By end of 2011,there are 76 LED Fabs in China totally.

• The new LED fab construction in China will slow down after 2011, even some LED Fabs will disappear.

MOCVD Tool Shipment

44

MOCVD Shipment

2010

MOCVD Shipment

2011F

Source: SEMI China ,2011;

Korea 36%

Taiwan 32%

China 23%

Japan 5%

NA&Europe 4%

China , 51%

ROW, 49%

• In 2011, over 50% MOCVD will be shipped to China.

• New MOCVD installation slow down in other regions in 2011 .

45

MOCVD Shipment to

China

• MOCVD shipment in China hit the maximum in 2011, and will slow down in next 2 yrs.

• After 2013, MOCVD installation in China will show a visible growth. Source:; SEMI China ;

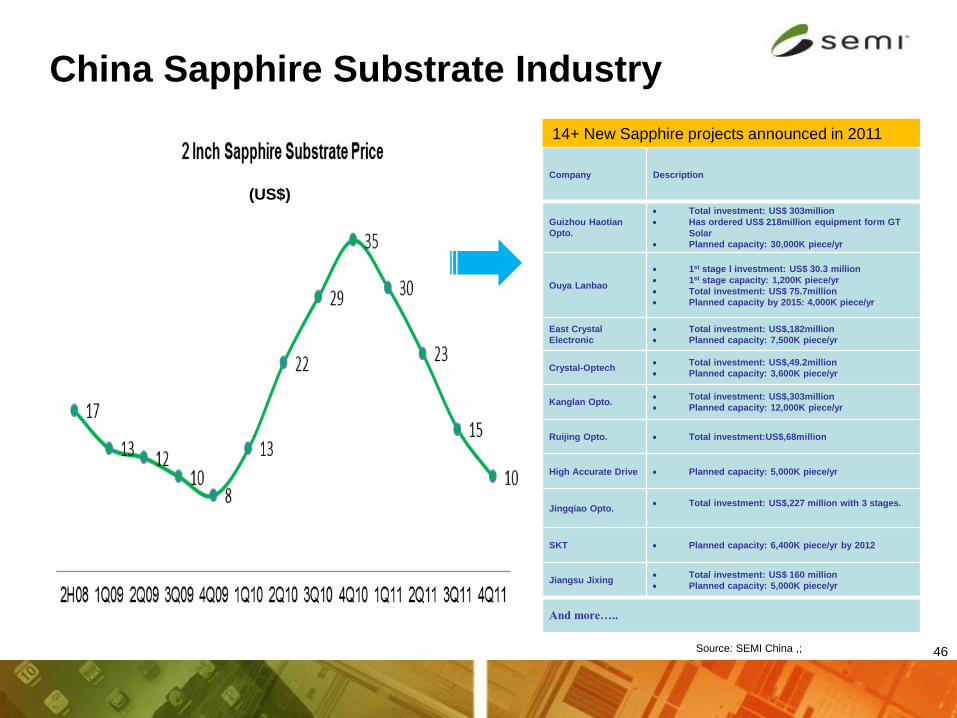

China Sapphire Substrate Industry

46

14+ New Sapphire projects announced in 2011

Company Description

Guizhou Haotian

Opto.

Total investment: US$ 303million

Has ordered US$ 218million equipment form GT

Solar

Planned capacity: 30,000K piece/yr

Ouya Lanbao

1st stage l investment: US$ 30.3 million

1st stage capacity: 1,200K piece/yr

Total investment: US$ 75.7million

Planned capacity by 2015: 4,000K piece/yr

East Crystal

Electronic

Total investment: US$,182million

Planned capacity: 7,500K piece/yr

Crystal-Optech Total investment: US$,49.2million

Planned capacity: 3,600K piece/yr

Kanglan Opto. Total investment: US$,303million

Planned capacity: 12,000K piece/yr

Ruijing Opto. Total investment:US$,68million

High Accurate Drive Planned capacity: 5,000K piece/yr

Jingqiao Opto. Total investment: US$,227 million with 3 stages.

SKT Planned capacity: 6,400K piece/yr by 2012

Jiangsu Jixing Total investment: US$ 160 million

Planned capacity: 5,000K piece/yr

And more…..

Source: SEMI China ,;

(US$)

China’s TFT /LCD Industry

48

China: The Biggest LCD Market

• China is the biggest manufacturing base of LCD TV, PC, monitor, DC, Mobile…huge demands for LCD panels.

• China will be the biggest consumptive market for LCD TV in 2011.

• “Electronics Subsidy Program” activates the demand of LCD TV market in countryside ,which is very big market with high potential.

Source:Displaysearch

Fig.: WW LCD TV Market

• Beijing: BOE-B1 G5; BOE-B4 G8

• Suzhou: Samsung G7.5 (Approved)

• Kunshan:

• IVO G5, AUO (Kunshan) G7.5

• Nanjing:

CEC-Panda G6;CEC-Sharp G8

• Chengdu:

BOE-B2 G4.5;Chengdu Tianma G4.5,

Foxconn G8.5

• Shanghai:

CAOE (pre-SVA-NEC) G5,

Shanghai Tianma G4.5

• Guangzhou: LGD G8.5 (Approved)

• Shanwei: Truly G2.5

• Heyuan: Yazhi G2.5 & G3.5

• Shenzhen:

Century G5, CSOT (TCL) G8.5

• Wuhan: Wuhan Tianma G4.5

• Hefei: BOE-B3 G6; BOE-B5 G8

Note: Red ones have not got the approval of China

central government

China Existing & Announced LCD Fab Plants

Source: SEMI China,2010;

TFT-LCD Fab capacity is moving into China mainland, the TFT-LCD industry is speeding up!

50

China TFT-LCD Capacity Forecast by Generation

0% 0% 1%10% 8%

16% 18% 14% 11% 9%

100% 100% 99%90% 92%

83%

60%

46%

35%28%

0% 0% 0% 0% 0% 1%

15%

19%

15%

12%

0% 0% 0% 0% 0% 0%0%

1%

8%

12%

0% 0% 0% 0% 0% 0%8%

20%30%

39%

0%

20%

40%

60%

80%

100%

120%

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

G4.5 G5 G6 G7.5 G8.5

Source: SEMI, 2011

Fig: China TFT LCD Fab Capacity Share by Gen.

China

The only region in the world, with all “pan-

semiconductor” sectors:

– having large industry base

– continue the dynamic growth.

51

SEMI in China

SEMI China Membership Growth

3/17/2012 Customer Satisfaction Study 53

/ = Statistically significant difference between 2010 and 2011. See “notes” for sample sizes.

0

50

100

150

200

250

300

2007 2008 2009 2010 2011

• 2nd largest SEMICON Show globally

• Largest FPD Show in China with complete supply-chain

• Premium PV Manufacturing and Technology Show

SEMI China Exposition

• The largest SEMICON Show globally - 2012

• Largest FPD Show in China with complete supply-chain

• Premium PV Manufacturing and Technology Show

SEMI China Exposition

• Pan-semiconductor Platform

2012 Scale:

80,000 sqm2

3,000+ Booths

2,000+ Exhibitors

50,000+ Visitors

SEMI China 2012 Exposition

Special theme pavilions serving

the Needs of China Market

– LED Manufacturing Pavilion

– Used IC Fab Line Market and Eco-System Pavilion

– IC Application of China Market Pavilion

– TSV /3D IC

SEMICON China:

China PV Technology International

Conference (CPTIC) - March 21-22, 2012

Conference Chairman

Prof. Martin Green

University of New South Wales, Australia

Zhengrong Shi

Founder,

Suntech

Jifan Gao.

Founder,

Trinasolar

Prof. Eicke R. Weber

Director

Fraunhofer ISE

Bohua Wang.

General Secretory

CPIA

International Advisory Committee

国际顾问委员会

Peng Fang

CEO

JA SOLAR

国际技术委员会 Technical Committee

• The Premium Forum of FPD Market and Technology

Trend

– Co-organized by SEMI and SID

– Focus on the new technology and market development

– Over 700 attendants in 2011 CFC

Advocate for Industry and Promote Global Collaboration

Industry Advocacy, China PV Whitepaper

Promote PV Policy & Legislation

Promote Global PV Industry collaboration

Promote Global Trade

SEMI PV Standard Activity in China

• Form SEMI China PV Standard Committee

– Approve new standard development

– Drive local and global industry consensus

– Top China PV players actively participate

• New Standard Under Development

– Mono-like Wafer Specification

– EVA Test Method

– Specification for PV Module Packaging

Materials

SEMI China Industry Research and

Consulting

大连市泛半导体产业发展规划

天津市太阳能光伏产业战略规划

Honeywell半导体及太阳能光伏产业咨询报告

Comet半导体、太阳能、光电子、

LED产业咨询报告

大连

DaLian

天津

TianJin

Honeywell

《财富》500强

Comet 全球领先

供应商

SEMI China Publication Platform

• Daily News

• Web

• Magazine

SEMI China Magazine & e-Newsletter

-- Help you reach customers

Semiconductor

Manufacturing(bimonthly)

PV Manufacturing(quarterly)

SM e-Magazine

SEMI China Daily News

Show Daily News:

PVM e-Magazine

SEMI PV Daily News

SOLARCON China Daily News

20,000

50,000 10,000

5,000

Print On-line

SEMI China Industry Platform:

Build Better Industry Environment

SEMI China Platform

Professional

Service Publication

Platform

Global

member

base

Exposition/

Conference

Government

Relation

2000 global companies

Global Board of Directors

Regional Advisory Committee Industry sector Committee

Special Interest Groups - Re-use Equipment

- Customs & Logistics

- HR Committee

- Export Control

SEMI Standard

Industry Research

Book to Bill

EHS

China central government

Regional Industry development

Voice of Industry for common issues

US Export Control lobby

Global trade promotion

SEMICON China

FPD China

SOLARCON China

LED Pavilion

ITPC, GFPC, ISS

Web site

Daily News

Magazine

Press release

Together, We Build a “Global

Industry Community” in China!

68

69

Welcome to EMICON /FPD /SOLARCON China:

-- the premium global industry gathering in China

• Largest micro-electronics Show in China

drawing industry and government

participation.

• Exciting Theme Pavilions and Programs.

• Grand Opening Keynote.

• World class technical conferences:

CSTIC, FPD Conference, PV Day, …

• SIG, Committee Luncheon.

• One-on-One Supplier Sourcing Event.

• Industry Gala Dinner.

• China IC Night.

• China PV Night

• Golf Tournament.

• …