choice for the future - cabinet office...the past records between 1990 and 2013 are compiled from...

TRANSCRIPT

Choice for the Future <Reference Charts>

May 2014 Committee for Japan’s Future

[Table of Contents] ○ Population ..................................................... 1-3 ○ Growrh and Development ............................ 4-12 ○ Human Resources .......................................13-22 ○ Prospects of the Regions ........................... 23-27 ○ Meeting Record ............................................. 28

Provisional translation by Cabinet Office

2,000

4,000

6,000

8,000

10,000

12,000

14,000

1990 2000 2010 2020 2030 2040 2050 2060 2070 2080 2090 2100 2110

(万人)

(年)

2013年12,730万人

(高齢化率:25.1%)

社人研(国立社会保障・人口問題研究所)

中位推計

出生率回復(2.07)ケース

2060年 10,545万人(人口減少率(対2013年比)17.2%)

(高齢化率:33.0%)

4,286万人

(高齢化率:41.3%)

総人口

8,674万人

(人口減少率(対2013年比)31.9%)

(高齢化率:39.9%)

出生率回復(2.07)ケース

2110年 9,661万人(高齢化率:26.6%)

Long-term population changes (total population) and projections

1. Projection of Population

1

If the current trend continues, the population in 2060 is expected to decrease by two thirds of the current pupolation, that is, approximately 87 million.

However, if the total fertility rate goes up to 2.07 by 2030, it is estimated that the population in 50 years will be 100 million, and another generation later, the population will take an upward turn, even if only a slight increase.

Population decline will stop (mid

2090s)

(Million people) 2013

127.3 mil. people (Population aging

rate: 25.1%)

Case where the birthrate recovers (2.07)

2110: 96.61 million people (Population aging rate: 26.6%)

Total population

(Year)

Population decline stops

(Mid 2090s) Population decline rate

(comparison with 2013) 31.9%) (Population aging rate: 39.9%)

86.74 mil. people

42.86 mil. people (Population aging

rate: 41.3%) (National Institute of Population and Social Security Research)

Medium variant projections

IPSS

(Remark) 1. The past records between 1990 and 2013 are compiled from “Population Census Report” and “Annual Report of Population Estimates" by the Ministry of Internal Affairs and Communications (MIC) and "Vital Statistics" by the Ministry of Health, Labour and Welfare (MHLW). 2. The medium variant projections by the National Institute of Population and Social Security Research in Japan (IPSS) are based on "Population Projections for Japan (January 2012)" by the IPSS. Until 2014, the total fertility rate shifted around 1.39, and afterwards, it is expected to drop to 1.33 by 2024 and hover at around 1.35. 3. The estimates for recovered birthrate were calculated with the population by gender and age in 2013 as a baseline assuming that the total fertility rate recovers to 2.07 in 2030 and the rate hovers at that level while the survival rate was the assumed value after 2013 for the medium variant projections by the IPSS (i.e., life expectancy goes up to 84.19 for males and 90.93 for females by 2060).

Case where the birthrate recovers (2.07) 2060: 105.45 million people

(Population decline rate (comparison with 2013) 17.2%) (Population aging rate: 33.0%)

Long-term population changes ("new productive age population"/"productive population") and projections

(Remark ) 1. The past records between 1990 and 2013 are compiled from “Population Census Report” and “Annual Report of Population Estimates” by the Ministry of Internal Affairs and Communications (MIC) and "Vital Statistics" by the Ministry of Health, Labour and Welfare (MHLW).

2. The medium variant projections by the IPSS are based on "Population Projections for Japan (January 2012)" by the IPSS. Until 2014, the total fertility rate shifted around 1.39, and afterwards, it is expected to drop to 1.33 by 2024 and hover at around 1.35.

3. The estimates for recovered birthrate were calculated with the population by gender and age in 2013 as a baseline assuming that the total fertility rate recovers to 2.07 in 2030 and the rate hovers at that level while the survival rate was the assumed value after 2013 for the medium variant projection by the IPSS (i.e., life expectancy goes up to 84.19 for males and 90.93 for females by 2060).

2. Projected Population of 20 to 70-Year-Olds

2

If the current situation continues, the productive population will drop to 44 million by 2060 and continue to decrease at the same pace.

If the total fertility rate recovers to 2.07 by 2030 and when 20 to 70 years old is a "new productive age population”, the “new productive age population” will reach around 56 million in 2060 and afterwards shift around that size.

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

10,000

1990 2000 2010 2020 2030 2040 2050 2060 2070 2080 2090 2100 2110

(万人)

(年)

生産年齢人口

(15~64歳)

2,333万人

2,126万人

(万人)

2013年7,901万人

出生率回復(2.07)ケース

2110年 5,461万人

(万人)

(年)

20~70歳人口

(「新生産年齢人口」)

社人研

中位推計 4,418万人

(万人)

2013年7,901万人

2013年8,329万人

4,777万人

出生率回復(2.07)ケース

2060年 5,555万人

2013 83.29 mil. people

2013 79.01 mil. people

IPSS Medium variant

projections

Productive population

(15-64 years)

(10,000 people)

(Year)

44.18 mil. people

47.77 mil. people

Population aged 20-70 ("new productive age

population")

Case where the birthrate recovers (2.07)

2060: 55.55 mil. people

Case where the birthrate recovers (2.07)

2110: 54.61 mil. people

23.33 mil. people

21.26 mil. people

0 500 1000 1500 2000 25000

10

20

30

40

50

60

70

80

90

100

2060年

~19歳

1,104 12.7%

20~64歳

4,105 47.3%

65~74歳

1,128 13.0%

75歳~

2,336 26.9%

(Remark) Created from "Population Projections for Japan (January 2012)" by the IPSS. The estimates for recovered birthrate were calculated with the population by gender and age in 2013 as a baseline assuming that the total fertility rate recovers to 2.07 in 2030 and the rate hovers at that level while the survival rate was the assumed value after 2013 for the medium variant projections by the IPSS (i.e., life expectancy goes up to 84.19 for males and 90.93 for females by 2060).

0 500 1000 1500 2000 25000

10

20

30

40

50

60

70

80

90

100

2010年

~19歳

2,293 17.9%

20~64歳

7,564 59.1%

65~74歳

1,529 11.9%

75歳~

1,419 11.1% Case where the birthrate recovers

Case where the current situation

continues

0 500 1000 1500 2000 25000

10

20

30

40

50

60

70

80

90

100

2030年

~19歳

1,698 14.6%

20~64歳

6,278 53.8%

65~74歳

1,407 12.1%

75歳~

2278 19.5%

0 500 1000 1500 2000 25000

10

20

30

40

50

60

70

80

90

100

2030年

~19歳

2,176 18.0%

20~64歳

6,245 51.6%

65~74歳

1,413 11.7%

75歳~

2269 18.7%

(10,000)

(10,000) 0 500 1000 1500 2000 2500

0

10

20

30

40

50

60

70

80

90

100

2060年

~19歳

2,181 20.7%

20~64歳

4,881 46.3%

65~74歳

1,132 10.7%

75歳~

2,351 22.3%

(10,000)

3

3. Changes in Demographic Structure until 2060 In the current Japan‘s demographic structure, the working-age population accounts for 59.1% while the elderly population

makes up 23.0%. If the current trend continues, the imbalance in the demographic structure will remain in 2060. If the birthrate recovers (i.e., in the case where the total fertility rate increases to 2.07 by 2030) the demographic structure will

consists of 20.7% for the population under 20 years, 46.3% for the age group of 20-64 years, and 33.0% for the population over 65 years, which means the imbalance will almost be resolved.

2010

2030 2060

75+ years

65-74 years

65-74 years

65-74 years 65-74 years

65-74 years

Ratio by age group and the number of age groups almost match and the

imbalance disappears

75+ years

75+ years

75+ years

0-19 years

0-19 years 0-19 years

0-19 years 0-19 years

75+ years

(10,000 people)

(10,000 people)

(10,000 people) (10,000 people)

(10,000 people)

20-64 years

20-64 years

20-64 years

20-64 years

20-64 years

* Future images when no action is taken to change the current situation

Productivity

Decline of labor force population

Decline of saving rate

Capital

Labor

Growth of labor force participation rates

Stagnation in technology

advancement

Decrease in productivity

Increase in

productivity

* Future image when choosing another way

Labor

Capital

Productivity

Aging population

Population decline

Capital accumulation

- Innovation - Branding, marketing - Knowledge capital

- Labor participation of young people, females, elderly people according to ability and motivation

- Investment in growing industries - Strengthening financial functions - Promotion of investment in Japan

Open

Dynamism

4

4. Future Image of Growth and Development If the current trend continues, Japan's economic growth and development will inevitably lose its dynamism

due to decrease of pupulation, savings rate, and technology advancement. From the macro aspect, the following are desired: (1) increase in productivity, (2) growth of labor force

participation rates, and (3) flow from savings to investment as well as increase of inward investment. In particular, the increase level of productivity is a focal point.

⇒ Increase in value-added productivity at the micro level through innovation ⇒ Dynamic industry structure through bold systematic reforms ⇒ Efforts to increase the growth of the global economy by building an open nation

6,577

5,683

3,795 4,453

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

2013 2030 2060

(万人)

(年)

6,5776,285

4,792

5,522

現状継続

ケース

経済成長・労働参加ケース

出生率回復ケース

年平均減少率:▲0.3%減少数:▲17万人

年平均減少率:▲0.9%減少数:▲53万人

年平均減少率:▲0.4%減少数:▲25万人

年平均減少率:▲1.3%減少数:▲63万人

社人研中位推計ケース

(Remark) Created from "Labour Force Survey" by the MIC, "Estimate for Demand and Supply of Labor (2014)" by the Employment Policy Research Group of the MHLW, "Population Projections for Japan (January 2012) " by the IPSS, and "Labour Force Survey" by Statistics Sweden.

(Note) 1. Labor force population is the total number of employees and completely unemployed people aged 15 and over. 2. The case where the current situation continues is estimated by fixing the labor force participation by gender and age in 2012 (the Employment Policy Research Group of the MHLW).

The case where economic growth and labor force participation improve is estimated assuming that participation of women and elderly and young people into the labor market progresses (the Employment Policy Research Group of the MHLW). For example, the labor force participation of women aged 30-49 years is assumed to increase from 71% in 2012 to 85% in 2030 with the M-shaped curve eliminated.

3. The case of medium variant projections by the IPSS is calculated by multiplying the population by gender and age in 2060 which the IPSS estimated by the labor force participation. The estimates for recovered birthrate were calculated first by assuming that the total fertility rate recovers to 2.07 in 2030 and the rate hovers at that level afterwards while the survival rate was the assumed value after 2013 for the medium variant projections by the IPSS (i.e., life expectancy goes up to 84.19 for males and 90.93 for females by 2060) and second by multiplying the values by labor force population rate.

4. Labor force population in 2060 took into consideration the above Note 1., i.e., estimate by the Employment Policy Research Group of the MHLW and is based on the assumptions that labor force participation of women and elderly progresses, and labor force participation of women aged between 30 and 49 years goes up to Sweden‘s level (85% in 2030 → 90% in 2060), using labor force participation of people over 60 years raised by five years respectively.

Estimate of labor force population

Raise the labor force participation of females of 30-49 years to Sweden's level (90%)

Raise the labor force participation of males and females over 60 years by five years respectively

2060 2030 2013

5

5. Estimate of Labor Force Population The labor force population will decline to around 55 million in 2060 even if the birthrate recovers (the total

fertility rate recovers to 2.07 in 2030) women work as much as those in Sweden, and elderly people work five years longer than now.

Annual average Decline rate: -0.3%

Number of phenomena: - 0.17 mil. Annual average

Decline rate: -0.4% Number of phenomena:

- 0.25 mil.

Annual average Decline rate: -0.9%

Number of phenomena: - 0.53 mil.

The case where the current situation

continues

Case where the

birthrate recovers

Case of economic growth and labor participation

Case of IPSS's medium variant

projections

(10,000 people)

(Year)

Annual average Decline rate: -1.3%

Number of phenomena: - 0.63 mil.

(Remark) Created based mainly on "System of National Accounts" and "Private Corporate Capital Stock" by the Cabinet Office, "Labour Force Survey" by MPHPT, "Indices of Industrial Production" and "Indices of Tertiary Industry Activity" by METI, "Monthly Labour Survey" by the MHLW, "Estimate for Demand and Supply of Labor (2014)" by the Employment Policy Research Group of the MHLW, and "Population Projections for Japan (January 2012) " by the IPSS.

(Note) 1. Regarding labor force population in the case where the current situation continues, labor force participation and working hours are assumed to remain the same as the ones in 2012. 2. In the case where economic growth and labor force participation improve, labor force population in 2020 and 2030 is adopted from the estimate by the Employment Policy Research Group of the MHLW. Working hours are assumed to remain at

the same level as in 2012. 3. Regarding the labor force population in 2060 in the case where the labor force participation of women and elderly progresses and working hours of elderly people become longer, it is assumed that the labor force participation of women and

elderly people improves more than in 2030 (women aged 30-49 work as much as those in Sweden, labor force participation rate for elderly people over 60 years becomes five years longer), and working time of male and females over 60 is used for 64 years.

4. Like the case of Note 3 above, labor force participation in 2060 in the case where the birthrate recovers is estimated assuming that the total fertility rate recovers to 2.07 in 2030 and the rate hovers at that level afterwards, while the survival rate was the assumed value after 2013 for the medium variant projections by the IPSS (i.e., life expectancy goes up to 84.19 for males and 90.93 for females by 2060).

6

6. Changes in Potential Growth: Degree of Contribution of Labor Input and Capital Investment

The degree of contribution of labor input is expected to remain on the declining trend even if the birthrate recovers, the labor force participation of women and elderly progresses and working hours of elderly people become longer.

The controbution level of capital investment will be smaller than before. The increase of total factor productivity (TFP) is required for the improvement of the potential growth rate.

0.6

-0.3 -0.3

2.0

0.5 0.6

1.8

1.4

0.5

4.4

1.6

0.8

-2.0

-1.0

0.0

1.0

2.0

3.0

4.0

5.0

1981-1990 1991-2000 2001-2010

(年平均成長率、%)

資本投入寄与度

TFP寄与度

潜在GDP成長率

(年)

労働投入寄与度

-0.5 -0.6

-0.9

-0.1 -0.3

-0.6

-0.3

-2.0

-1.0

0.0

1.0

2.0

3.0

2011-2020 2021-2030 2031-2060

(年平均成長率、%)

現状継続ケース

(年)

女性・高齢者の労働参加が図られ、高齢者の労働時間が伸びるケース

出生率が回復し、女性・高齢者の労働参加が図られ、高齢者の労働時間が伸びるケース

経済成長・労働参加ケース

労 働 投 入 寄 与 度

Changes in Japan's potential growth rate

0.4 0.5

0.6

0.3 0.3 0.3 0.4 0.4

0.5

-2.0

-1.0

0.0

1.0

2.0

3.0

2011-2020 2021-2030 2031-2060

(年平均成長率、%)

実質GDPと設備投資が、いずれも2%成長するケース

(年)

実質GDPが1%成長、設備投資が1.5%成長するケース

実質GDPと設備投資が、いずれも1%成長するケース

資 本 投 入 寄 与 度

(Average annual growth rate, %)

(Year)

(Year)

(Year)

(Average annual growth rate, %)

(Average annual growth rate, %)

Contribution degree of labor input

Contribution degree of capital investment

Contribution degree of capital investment

Contribution degree of TFP

Potential GDP growth rate

Contribution degree of labor input

Case where the birthrate recovers, the labor force participation of women and elderly progresses and working hours of elderly people becomes longer

Case where the labor force participation of women and elderly progresses and working hours of elderly people becomes longer

Case of economic growth and labor participation

Case where real GDP grows by 1% and facility investment goes up by 1.5%.

Case where real GDP and facility investment both increase by 2%

Case where real GDP and facility investment both increase by 1%

Case where the current situation continues

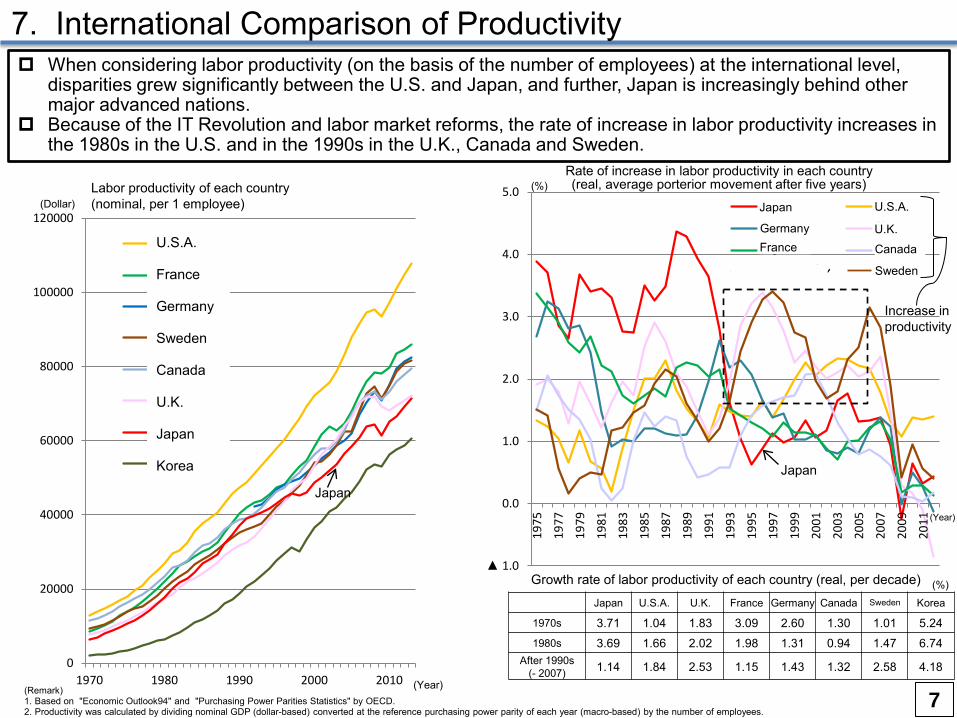

Growth rate of labor productivity of each country (real, per decade)

(Remark) 1. Based on "Economic Outlook94" and "Purchasing Power Parities Statistics" by OECD. 2. Productivity was calculated by dividing nominal GDP (dollar-based) converted at the reference purchasing power parity of each year (macro-based) by the number of employees.

(Year)

▲ 1.0

0.0

1.0

2.0

3.0

4.0

5.0

1975

1977

1979

1981

1983

1985

1987

1989

1991

1993

1995

1997

1999

2001

2003

2005

2007

2009

2011

日本 米国

ドイツ 英国

フランス カナダ

スウェーデン

Japan

(Year)

(%) Labor productivity of each country (nominal, per 1 employee)

Rate of increase in labor productivity in each country (real, average porterior movement after five years)

Japan U.S.A. U.K. France Germany Canada Sweden Korea

1970s 3.71 1.04 1.83 3.09 2.60 1.30 1.01 5.24 1980s 3.69 1.66 2.02 1.98 1.31 0.94 1.47 6.74

After 1990s (- 2007) 1.14 1.84 2.53 1.15 1.43 1.32 2.58 4.18

(%)

Sweden

Increase in productivity

(Dollar)

0

20000

40000

60000

80000

100000

120000

1970 1980 1990 2000 2010

米国

フランス

ドイツ

スウェーデン

カナダ

英国

日本

韓国

Japan

7

7. International Comparison of Productivity When considering labor productivity (on the basis of the number of employees) at the international level,

disparities grew significantly between the U.S. and Japan, and further, Japan is increasingly behind other major advanced nations.

Because of the IT Revolution and labor market reforms, the rate of increase in labor productivity increases in the 1980s in the U.S. and in the 1990s in the U.K., Canada and Sweden.

U.S.A. France Germany Sweden Canada U.K. Japan Korea

Canada

U.K.

U.S.A. Japan

Germany France

Japan Germany Total population

Peak 2008 (128.08 million people)

2003 (82.53 million people)

Decrease rate - 0.1% - 0.1%

Total fertility rate* 1.41 1.36*

Population aging rate*

24.1% 21.1%

Productive population

Peak 1998 (67.93 million people)

1999 (55.96 million people)

Decrease rate - 0.5% - 0.3%

Main data

* 2012. The total fertility rate of Germany is the one in 2011.

8

8. Productivity Comparison between Japan and Germany In Japan and Germany, total population and productive population are both in decline. The contribution of labor input to the

potential growth rate is also negative. On the other hand, in Germany, the contribution of TFP and capital investment to the economic growth is larger than in Japan.

Behind the economic growth of Germany, there are promoted participation in the labor market as a result of the labor market reform policy under the Schroeder regime, proactive ICT capital investment in the service industry, and the creation of additional value in business services among others.

(Remark) Created from EU KLEMS and statistics of each country.

0.7 0.4

-0.3 -0.2 -0.2

1.7 2.0

1.7 1.0

0.5

1.7 2.3

0.9

0.1 0.7

4.1 4.6

2.3

0.9 0.9

-1.0

0.0

1.0

2.0

3.0

4.0

5.0

1981-1985 1986-1990 1991-1995 1996-2000 2001-2007

Japan

TFP contribution

Capital investment contribution

Labor input contribution

(Change in contributions from previous year, %)

-0.7

0.5

-0.4 0.0

-0.2

0.9

1.2 1.3 1.3

0.8

1.0

1.5

1.0 0.7 1.2

1.3

3.2

1.9 2.0 1.7

-1.0

0.0

1.0

2.0

3.0

4.0

5.0

1981-1985 1986-1990 1991-1995 1996-2000 2001-2007

Germany (前年比寄与度、%) (Change in contributions from previous year, %)

TFP contribution

Capital investment contribution

Labor input contribution

(Year) (Year)

Potential growth rate

0

5

10

15

20

25

Japan and Germany's exports by industry ($ 100 mil.)

Japan

Germany

Share of business services (Note) is 6% Country A

Country B

Country C Created based on data from OECD (2013).

Image of export amount of added value*

Export amount (100)

Export amount (110)

Added value (10)

Added value (100)

* With the intermediary goods trade expanded because of Global Value Chain (GVC), added values are double counted in the calculation of total amount of world trade. To deal with this issue and to measure wolrd trade in value added calculated by each country, OECD and WTO jointly constructed a database for the world trade in value added.

9

9. Added Value of Japan and Germany by Industry With the value chain becoming more complicated and an international division of labor developing including

services, is possible to identify in which domestic industirial secotrs addded values are created in terms of export by paying attention to export amount of added value (calculated from added value created within a country), instead of export amount including values of imported intermediate goods.

According to the export amount of added value calculated by OECD, the business service industry is creating the most added value in Germany. On the other hand, in Japan, the highest added value is created at the distribution stage.

05

10152025

Japan and Germany's added value exports by industry (億ドル)

Japan

Germany

Share of business services (Note) is 23%

Japan and Germany are reversed

For Japan's wholesale and transportation, added value exports are larger than exports

($ 100 mil.)

Source: Created by the Cabinet Office based on OECD-WTO-TiVA. Note: Business services concludes marketing, consulting, IT-related, advertising, legal, accounting, R&D-related and other services.

0%

2%

4%

6%

8%

10%

12%

80 85 90 95 2000 05 07

無形資産投資(GDP比、実質)

(年)

情報化資産

革新的資産

経済的競争能力

0%

20%

40%

60%

80%

100%

日本

EU1

5

北欧諸国

英国等

大陸欧州

地中海諸

国

アメリカ

オースト

ラリア

無形資産投資の構成比(2005年)

Innovative property

経済的競争能力

情報化資産

(Remark) Based on analyses in Annual Report on the Japanese Economy and Public Finance 2011 Computerized information, innovative property and economic competitive capabilities are estimated using the following methods: (1) Computerized information ... Software order is estimated based on investment in software, package software on sales of the

software service industry, and internally developed software on the ratio of internaly developed software calculated using the Economic Census and database on sales of the information providing service industry.

(2) Innovative property ... R&D in the field of natural science is estimated based on science technology research and survey, rights of resource exploitation on cost of mineral exploitation and amount invested in exploration, copyright and license on nominal output values of publishing and printing services and other creative services for video/sound/character information purchased in each industry, design on sales of the design industry, display on sales of the display industry, machine design on sales of the machine design industry, architectural design on nominal output value of engineering services, and product development in the financial services industry on 20% of nominal intermediate input in the financial services industry and insurance business respectively.

(3) Economic competitive capabilities ... Brand assests is estimated based on advertising cost and marketing survey (advertising cost is 60% of nominal output value purchased from the advertising industry by other industries and market survey is the figure calculated by multiplying nominal output volume in the information services industry by the ratio of the information providing services industry obtained using Economic Census), human capital particular to individual companies on average training costs for regular employees from General Survey on Working Conditions, organizational strucuture on the figure calculated by multiplying nominal output volume in the professional and business services industry by the ratio of the managing and consulting services industry obtained using Economic Census respectively.

経済的競争能力

・ブランド資産、マーケティング力

・企業固有の人的資本

・組織構造

情報化資産

革新的資産

・自然科学分野の研究開発

・資源開発権

・著作権及びライセンス

・他の製品開発、デザイン、自然科学分野以外の研究開発

・データベース

(デザイン、ディスプレイ、機械設計、 建築設計、金融業における製品開発)

・受注ソフトウェア

・パッケージ・ソフトウェア

・自社開発ソフトウェア

10

10. Current Status and International Comparison of Knowledge Capital Investment (Intangible Assets Investment)

According to the breakdown of knowledge investment, a low proportion was classified under "economic competitive capabilities“, such as brand power and marketing capacity, while a high proportion was under the "innovative property“, such as research and development investment. Investment in intangible assets (to GDP, real) Composition ratio of investment in intangible assets (2005)

Economic competitive capabilities

Economic competitive capabilities

Innovative property

Innovative property

Computerized information

Computerized information

Economic

competitive capabilities

Computer-ized

information

Japa

n E

U15

N

orth

Eur

ope

U.K

., et

c.

Con

tinen

tal

Eur

ope

Med

iterra

nean

co

untri

es

U.S

.A

Aus

tralia

(Year)

• R&D in the field of natural science • Rights of resource exploitation • Copyright and license • Other product development, design, R&D in

other fields than natural science (design, display, machine design, architectural design, product development in the financial services industry)

• Brand property, marketing capacity • Human capital in corporate enterprises • Organizational structure

• Software order • Package software • Internally developed software • Database

2% 0%

24%

8%

3% 15%

5%

12% 5% 6%

20%

3% 0%

28%

11% 3%

14% 7%

10%

7% 17%

1980 1970 1990 2000 2010

6% 1%

38%

8% 2%

15% 5% 8%

7% 10% 4% 0%

30%

10% 3%

16% 6%

9%

7% 15% 1% 0%

22%

6%

3% 16%

6%

13%

6% 6%

21%

(Remark) Japan: created based on “System of National Accounts” by the Cabinet Office. Before 1990, the information and communication industries were combined to make up category of transportation and communication industry.

Other countries: Created based on "National Accounts Main Aggregates Database" by the U.N.

GDP by economic activity Agriculture, forestry and fisheries

Mining

Manufacturing

Construction

Electricity/gas/water

Wholsaling and retailing

Financial and insurance

Real estate

Transportation

Services Information and Communications

Services industry total 47%

Services industry total 56%

Services industry total 58%

Services industry total 66%

Services industry total 71%

GDP breakdown by category of economic activity for Japan remains almost unchanged for the past 10 years. In other countries, some industries such as the financial services industry, the medical and welfare services industry, and the education industry, significantly grew.

11. International Comparison of GDP Classified by Economic Activities

11

3%

28%

5% 7% 15%

9%

16%

10%

7%

1%

12% 4%

4%

15%

6% 33%

17%

8% 1% 16%

3% 5%

16%

6%

31%

15%

7% 2% 19%

5% 4%

18% 6%

25%

13% 8%

3%

21%

7% 5%

18% 7%

20%

8% 11% 3%

25%

4% 5%

19% 7%

17%

8% 12%

2%

22%

11%

6% 14% 8%

17%

13%

7% 2%

19%

5% 7%

15% 9%

22%

14%

7% 1%

15% 5%

6%

17% 9%

27%

16%

4% 1%

10% 5% 6%

17%

8%

53%

7%

26%

3% 7% 12% 10%

14%

4% 17%

5%

21%

4% 6%

12% 10% 15%

3%

24%

4%

19% 4%

7% 12% 9%

19%

4%

22%

2%

21% 3% 4%

11% 11%

25%

18%

5% 2%

17% 5% 5%

13% 10%

48%

U.S.A.

U.K.

Sweden

Manufacturing

Mining and electricity/ gas/water

Construction

Wholsaling, retailing etc.

Transportation, communication etc.

Financial and real estate, etc.

Education, medical servieces, etc.

Education, administrative services (including national defense)

Agriculture, etc. Manufacturing

Mining and electricity/ gas/water, etc.

Construction

Wholsaling, retailing, etc.

Transportation, communication etc.

Others

Agriculture, etc.

Services industry total 63%

Services industry total

57%

Services industry total

57%

Services industry total 64%

Services total

59%

Services industry total

64%

Services industry total

70%

Services industry total

67%

Services industry total

66%

Services industry total 75%

Services industry

total 79%

Services industry

total 73%

Services industry total

70%

Services industry

total 78%

Services industry

total 71%

Japan

-10

-8

-6

-4

-2

0

2

4

6

8

10

2000 02 04 06 08 10 12

(名目GDP比、%)

(備考)内閣府「国民経済計算年報」をもとに作成。

(年度)

企業

一般政府

家計

経常収支

Changes in balance between savings and investment by sector (I-S balance)

Case of neglecting the present situation

Gross Domestic Product (GDP) = Consumption + Investment + Government expenditures + Balance of trade (Export - Import)

(GDP - Tax + Income from abroad - Consumption - Investment) + (Tax - Government expenditure) = (Trade balance + Income from abroad) Net savings of the domestic private economy Treasury budget Current account

12

12. Effects on Macro-Economy (prospects of balance between savings and investment by sector)

As population aging advances, excess savings in household budgets are in decline. Assuming that the budget deficit increases, financial flow from other countries is necessary to compensate for domestic capital

shortfall.

(To nominal GDP, %)

Company

Household budget

Current account

General government

(Fiscal year)

(Remark) Created from "Annual Report on National Accounts for 2012" by the Cabinet Office.

13. Map of Current Situation of "Human Resources" (Concept Illustration) Human resource development and labor market optimized for the economic and social model developed through the post-war period of high growth

• Emphasis on maintaining and improving standards at the national level

• Education emphasizing uniformity • Lack of a long-term perspective such as the

advancement of science technologies

• Educational costs oppressing household finances

• Discontinuity between education and career (Contents learned are not considered in the labor market)

• Trainings after graduation rely on OJT provided by companies

• Re-learning is not common among working people

• Bulk hiring of new graduates (hiring for potential) • Policy of nurturing human resources in-house • Emphasis on team power • Work style without clarifying duties • Treatment emphasizing seniority • Wage based on stable employment, long time labor and

livelihood > Trainings focusing on OJT

• Non-regular employees: low wages, unstable employment, few

chances of OJT • Low unemployment rate among young people at the international level • External labor markets (special professions, mid-career) are

undeveloped • Criteria for ability evaluations in external labor markets are not clear

Regular employees (non-limited employment) Inside company

• Financial condition is relatively stable • People tend to work long hours and striking a

balance between work and life is difficult • Only one of partners (woman in particular) is liable

to be charged with housework and child-rearing

• Career formation initiated by company • Difficult for middle-aged and elderly

people who experienced divorce to be re-employed

• Few places to utilize their abilities and skills • <--> Many non-regular employees • Quite a few number of women leaving their jobs

during childbirth and child-rearing

• Difficult to get promoted to managing posts without working long hours

• Career formation is difficult • Re-employment after childbirth and child-

rearing is difficult • Few opportunities to be a regular employee

• Unstable life due to unstable employment and low wages

• Trainings after graduation are not considered

Regular

employees

Wom

en N

on-regular em

ployees

• Setting retiring age and subsequent drastic changes in working environment

• Shortage of places for elderly people to utilize their capabilities

• Shortage of successors of know-how and skills

• Increase in the ratio of elderly people

• Lifestyle-related disease became central to disease structure

• Rapid growth of demand for nursing as the result of aging baby boomers

• Accessibility to medical services under the universal healthcare system

• Issues related to "place to belong" and "purpose of life" for elderly people

Work style of elderly people Life of elderly people

Working environment

• Extension of average life span and life expectancy

• Improvement of physical strength and increase of willingness to work among elderly people

• Lack of knowledge about medical cost • Differences in awareness of disease

prevention and health maintenance

• Work style in younger age significantly

affects livelihood in old age • Significance of human relationships

• Few places for NEETs and job hoppers to learn professional skills

• Few opportunities to receive education linked with working such as training to develop global human resources

• Few places for lifelong learning

• Living conditions make it difficult to feel fulfillment

Work style Human resource

development

• Poor utilization of vocational abilities in the advanced age period

Widening disparities

Decline in Birthrate/Population Stable economic growth Globalization

Educational environment

Education before employment

Education after employment

- Social changes including the declining birthrate - Changes in desired human resources and work style amid population decline and aging

• Average academic achievement is one of the highest in the world

• Not enough training for acquiring the strength to live a life

• Educational environment where "non-straghter" that is, those with negative background such as repeating school year and dropout cannot succeed

• Educational gaps due to differences in parents' income

• Difficult to challenge global players • Difficult to acquire abilities to form

career on one's own initiative and expertise necessary for professions

Increase of social security costs

Social system

Work style and life in the advanced age period

Current status of people

Human life

Social issues

• NEETs (Not in Education, Employment or Training) remaining at high levels, aging • Lack of social resources to support employment

Survival of local communities

13

14. Labor Force Participation of Women in Major countries (M-shaped curve)

0.0

10.0

20.0

30.0

40.0

50.0

60.0

70.0

80.0

90.0

100.0

15-19 25-29 35-39 45-49 55-59 65-69

日本 アメリカ イギリス

ドイツ フランス スウェーデン

Japan

Germany

(%)

(Age)

Source: Japan: "Labour Force Survey" by the MIC, Other countries: OECD Database

Japan U.S.A.

Germany

France

U.K.

Sweden

42.3%

47.5% 47.4% 47.2% 47.2% 46.5% 46.1% 45.3% 43.6%

41.6% 39.2%

36.1%

11.1%

38.7%

34.4% 31.2%

43.0%

35.7%

29.9%

36.7% 34.3%

9.4%

52.7%

25.0%

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

日本

フランス

ノルウェー

スウェーデン

アメリカ

イギリス

ドイツ

オーストラリア

シンガポール

韓国

フィリピン

マレーシア

就業者 管理的職業従事者

International comparison of the labor force participation rates for women

International comparison of the ratios of female managerial employees

Source: "Labour Force Survey" (2012) by the MIC ILO LABORSTA (2012) Eurostat: Eurostat Database (2012) Note 1) Data for Japan are from 2012, for Australia from 2008, and for other

countries from 2010. Note 2) In "Labour Force Survey" by the MIC, "managerial employee" means

workers with section chief status or higher position of companies such as managerial public officer. The definitions of "managerial employee" vary country by country.

Female employees All employees

14

In Japan, the labor force participation of women in and around their 30s and early 40s still illustrates an "M-shaped curve". In major European countries, such an M-shaped curve cannot be seen. When compared with other countries, the ratio of female managerial employees is low in Japan.

Ja

pan

Fran

ce

Nor

way

S

wed

en

U.S

.A

U.K

. G

erm

any

Aus

tralia

S

inga

pore

K

orea

P

hilip

pine

M

alay

sia

U.S.A.

France

U.K.

Sweden

Female managerial employees All managerial employees

(Remark) Created from OECD Annual Labour Force Statistics and OECD Factbook 2013.

Changes in total fertility rate and labor force participation of women in major countries (15 to 64 years old)

1.0

1.2

1.4

1.6

1.8

2.0

2.2

2.4

2.6

45.0 50.0 55.0 60.0 65.0 70.0 75.0 80.0 85.0

(合計特殊出生率)

(15~64歳の女性労働力率、%)

● 始点(1970年) ■ 終点(2010年)

アメリカ フランス

日本 スウェーデン

1990

2005

1980

1980

2000

2001

イギリス

ドイツ

15

15. Relation between Birthrate and Labor Force Participation of Women

In France and Sweden, simultaneous recovery of high labor force participation and increased birthrate was achieved. Recently, in Sweden in particular, a birthrate higher than 1970 was attained.

The birthrate tends to be higher when the labor force participation of women is high in recent years.

(Total fertility rate)

(Labor force participation of women aged 15-64, %)

Starting point (1970) End point (2010) U.K.

France

Germany

Japan Sweden

U.S.A.

16. Changes in Average Ideal/Planned Numbers of Children

13.6%

22.3%

45.6%

15.7%

1.7% 0.3% 0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

40.0%

45.0%

50.0%

0人 1人 2人 3人 4人 5人以上

Source: Created from "The Fourteenth Japanese National Fertility Survey in 2010" by the IPSS.

Distribution of married couples by the number of children (2010)

Changes in average ideal/planned numbers of children

1.85 1.88 1.93 1.86 1.84 1.78 1.77 1.71

2.61

0.32

2.62

0.32

2.67

0.3

2.64

0.32

2.53

0.32

2.56

0.35

2.48

0.34

2.42

0.36

0

0.5

1

1.5

2

2.5

3

第7回調査 (1977年)

第8回調査 (1982年)

第9回調査 (1987年)

第10回調査 (1992年)

第11回調査 (1997年)

第12回調査 (2002年)

第13回調査 (2005年)

第14回調査 (2010年)

2.17 2.20 2.23 2.18 2.16 2.13 2.11 2.07

Source: Created from "Japanese National Fertility Survey, Married Couples" by the IPSS.

Note) The subjects for the survey were married couples (first marriage for both partners) whose wives were under 50 years old. The planned number of children was calculated by adding the number of children in existence to the planned additional number of children. The total number includes the cases where marriage duration was not clear. The years of surveys are the ones when the surveys were conducted.

(people)

Ideal number of children

Planned additional number of children

Number of children in existence

Planned num

ber of children

16

Although the average ideal and actual numbers of children are both on a downward trend in the long term, the ideal and planned numbers of children remain 2 or higher.

On the other hand, the average number of children in existence is actually under 2, there exists a gap between desires and reality.

(People)

0 people 1 people 2 people 3 people 4 people 5+ people

7th survey 8th survey 9th survey 10th survey 11th survey 12th survey 13th survey 14th survey (1977) (1982) (1987) (1992) (1997) (2002) (2005) (2010)

17. Ratio of Non-Regular Employment of Men and Women and Wage Disparities

0.0%10.0%20.0%30.0%40.0%50.0%60.0%70.0%80.0%

男性の非正規比率

0.0%10.0%20.0%30.0%40.0%50.0%60.0%70.0%80.0%

女性の非正規比率

0

100

200

300

400

500

600

700

800

男女別 雇用形態別賃金カーブ 正規 男性 正規 女性 非正規 男性 非正規 女性

Source: "Labour Force Survey (Detailed Tabulation)" (2013) by the MIC

Source: "Basic Survey on Wage Structure" (2013) by the MHLW Note) Data above are for general workers and do not consider part-

time workers. Wages are based on annual income.

(10,000 yen)

0.0

50.0

100.0

150.0

200.0

250.0

20歳以下 30〜39歳 40〜49歳 50〜59歳 60歳以上

男性

ドイツ フランス 英国

0.0

50.0

100.0

150.0

200.0

250.0

20歳以下 30〜39歳 40〜49歳 50〜59歳 60歳以上

女性

ドイツ フランス 英国 Germany

Source: "Structure of Earnings Statistics 2010" by the EU (Note) Data above are monthly earnings, and the index

number was "20 years old or younger" of each country as a base of 100.

Wage curves for men and women (EU)

17

In the case of males, the percentage of non-regular employees is high among young and elderly people, while it is high in all ages in the case of females.

Wages of non-regular male and female employees are significantly low in comparison to those of regular male and female employees.

Ratio of non-regular male employees

Ratio of non-regular female employees

Wage curves by gender and by form of employment

Regular, male Non-regular, male

Regular, female Non-regular, female

Germany France

France

U.K.

U.K.

-19

year

s ol

d

20-2

4 ye

ars

old

25-2

9 ye

ars

old

30-3

4 ye

ars

old

35-3

9 ye

ars

old

40-4

4 ye

ars

old

45-4

9 ye

ars

old

50-5

4 ye

ars

old

55-5

9 ye

ars

old

60-6

4 ye

ars

old

65-6

9 ye

ars

old

70- y

ears

old

20 years old and under

20 years old and under

30-39 years old

30-39 years old

50-59 years old

50-59 years old

40-49 years old

40-49 years old

60 years and over

60 years and over

Female

Male

15-2

4

25-3

4

35-4

4

45-5

4

55-6

4

65-

15-2

4

25-3

4

35-4

4

45-5

4

55-6

4

65-

(Age)

(Age)

2.4%

9.6%

33.4%

60.1%

40.1%

1.3% 3.7%

14.5%

27.1%

11.6%

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

15~19歳 20~24歳 25~29歳 30~34歳 15~34歳計

正規の職員・従業員 非正規の職員・従業員

Source: "Employment Status Survey" (2012) by the Statistics Bureau, MIC (Note) 1. The term "non-regular worker"means a person such as a part-time/temporary worker, dispatched worker, a contract worker, and a shokutaku

(short-term contract) worker. 2. The term "males with spouse" here means the total number of males excluding single men.

18. Comparison of Ratio of Males with Spouses by Age and Form of Employment

Regular workers

Non-regular workers

(%)

18

When comparing the ratio of males with spouses by form of employment, the percentage of non-regular male employees with spouses is notably low in all ages.

This suggests that economic conditions, such as income and form of employment, have a major impact on the decision to marry.

15-19 years old 20-24 years old 25-29 years old 30-34 years old Total: 15-34 years old

Regular employees Non-regular employees

19. International Comparison of Birthrate Decline Related Index

Japan France U.K. Sweden Germany U.S.A.

Average age of first marriage of women

29.2 (2012)

30.8 (2011) ― 33.0

(2011) 30.2

(2011) 25.8 (Note 1)

Average age of women when giving birth to their first children

30.3 (2012)

28.6 (2006)

30.6 (2010)

29.0 (2011)

29.0 (2011)

25.1 (2005)

Ratios of children born out of marriage (2008) 2.1% 52.6% 43.7% 54.7% 32.7% 40.6%

Ratio of long-hours workers (49 or more per week) (2012)

Total 22.7% Males 31.6%

Females 10.6%

Total 11.6% Males 16.1%

Females 6.5%

Total 12.0% Males 17.3%

Females 5.8%

Total 7.6% Males 10.7%

Females 4.2%

Total 11.2% Males 16.4%

Females 5.0%

Total 16.4% Males 21.8%

Females 10.2%

Hours consumed for housework and childcare by husbands (2006) 1:00 2:30 2:46 3:21 3:00 3:13

Ratio of family related government expenditures against GDP (2009)

(Note 2)

* Including child allowance and childcare services

0.96% (1.35% in FY2011)

3.20% 3.83% 3.76% 2.11% 0.70%

Source: Average age of first marriage of women: “Vital Statistics” by the MHLW for Japan, and data from “Eurostat Database” for France, Sweden, and Germany. Average age of women when giving birth to their first children: “Vital Statistics” by the MHLW for Japan, data from “Eurostat Database” for European

countries, and “National Health Statistics Report” by the Centers for Disease Control and Prevention, National Center for Health Statistics for U.S.A. (March 22, 2012).

Ratio of long-hours workers: "ILO database". Hours consumed for housework and childcare by husbands: "How Europeans Spend Their Time: Everyday Life of Women and Men" (2004) by Eurostat,

"American Time-Use Survey Summary" (2006) by the Bureau of Labor Statistics of the U.S., and "Survey on Time Use and Leisure Activities" (2006) by the MIC.

Ratio family related government expenditures against GDP: "Social Expenditure Database" by OECD. Note 1) Data for U.S.A. are the average figures for the period between 2006 and 2010. Note 2) The ratio of family related expenditures against GDP is the figure only for expenditure and excludes tax deduction.

19

10.4 12.3

6.7

10.2 9.1 6.1 7.3

1.4

1.8

0.1

0.5 2.2

0.8 1.0

1.0

2.0

2.9

5.0 2.3

1.5

2.4

7.2

9.0

8.1

7.3 8.6

8.3 6.6

1.0

3.2

3.8

3.7

2.1

0.7 2.3

1.2

3.7

2.5

3.0

3.5

1.8

3.1

22.2

32.1

24.1

29.8

27.8

19.2

22.1

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

日本 フランス イギリス スウェーデン ドイツ アメリカ OECD平均

20. International Comparison of Social Security Related Government Expenditure

Social security related government expenditures against GDP in Japan are at the almost the same level as the average of OECD member countries and relatively lower than European countries. The ratio of family related government expenditure is low.

Source: "Social Expenditure" by OECD (2009)

(Contrasted with GDP, %)

年金・介護 遺族(遺族年金等) 障害者施策・労災等 医療 家族 その他 計

20

Japan France U.K. Sweden Germany U.S.A. OECD average

Pension/ Nursing care

Survivor (ex. survivor pension)

Measures for Persons with Disabilities/workmen's compensation

Medical Family Others Total

25.00

27.00

29.00

31.00

33.00

35.00

37.00

39.00

41.00

43.00

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

65~69歳 男子 65~69歳 女子 70~74歳 男子

70~74歳 女子 75~79歳 男子 75~79歳 女子

(Remark) Created from “Physical Fitness Survey (Japan Fitness Test)” by the Ministry of Education, Culture, Sports, Science and Technology (MEXT).

Note) Data above is the average of the total scores for the following items: grip strength, sit-ups, sit and reach, standing test on one leg with eyes open, 10 meter obstacle walk, 6 minutes walk

21. Changes in Physical Fitness of Elderly People

21

Most of the scores for physical fitness of elderly people show trends of improvement. Comparing the total scores of 1998 and 2012, the score of 2012 improved and became close

to the score for people five years younger.

Trends in physical fitness of elderly people

65-69 years old, Male 65-69 years old, Female 70-74 years old, Male 70-74 years old, Female 75-79 years old, Female 75-79 years old, Male

2010年

1,419万人

(11.1%)

2020年

1,879万人

(15.1%) 2030年

2,278万人

(19.5%)

2040年

2,223万人

(20.7%)

2050年

2,385万人

(24.6%)

2060年

2,336万人

(26.9%)

0

500

1,000

1,500

2,000

2,500

-

20

40

60

80

100

120

140

160

2000 2005 2010 2015 2020 2025 2030 2035 2040 2045 2050 2055 2060

(万人)(兆円)

(Source) 1. Regarding the social welfare benefits, actual values up to FY2011 are based on “The Financial Statistics of Social Security in Japan FY2011" by the IPSS, estimates for FY2012 and onward are based on "Revised Future Estimation of Social Security Cost (March 2012)" by the MHLW.

* Preconditions for the economic situation used in the above estimates: Conditions up to 2022 are based on Conservative Scenario in “Economic and Fiscal Projections for Medium to Long Term Analysis (January 24, 2012)" by the Cabinet Office, and conditions in 2023 and onward are based on nominal economic growth rate (1.8%), wage growth rate (2.4%) and price increase rate (1.2%).

2. The ratio of the population aged 75 and over is based on medium variant projections for birth and death in "Population Projections for Japan (January 2012)" by the IPSS.

Changes in social welfare benefit by sector

Medical care

Pension

Nursing care, etc.

Estimate

FY2025 Medical care: 54.0 trillion yen Pension: 60.4 trillion yen Nursing care, etc.: 34.4 trillion yen Total: 148.9 trillion yen

Population aged 75 and over (Percentage of total population)

Uneven distribution of medical and nursing care services (as of 2040)

(Source) The 9th National Council on Social Security System Reform (April 19, 2013). Extracted from the material document submitted by Professor Tai Takahashi (Graduate School, International University of Health and Welfare)

FY2011 Medical care: 34.1 trillion yen Pension: 53.1 trillion yen Nursing care, etc.: 20.4 trillion yen Total: 107.5 trillion yen

22. Future of Social Security

It is expected that social welfare benefit increases especially in the fields of medical care and nursing care. Uneven regional distribution of medical and nursing care services is anticipated, and especially in the Tokyo

metropolitan area, there will be a major shortage of those services as the population ages.

22

(Trillion yen) (10,000 people)

2010 14.19 mil.

people

2020 18.79 mil.

people 2030

22.78 mil. people

2040 22.23 mil.

people

2050 23.85 mil.

people

2060 23.36 mil.

people

Regions that can afford: For both medical and nursing care. (slight increase or decline of elderly population) For medical care. Slightly for nursing care. For medical care. Average for nursing care

Regions that cannot afford:

For both medical and nursing care. Especially for nursing care. Especially for medical care.

3割以上5割未満減少,

619自治体(34.4%)

3割未満減少,

269自治体

(15.0%)

維持・増加, 15自治体(0.8%)

1万人未満

523自治体

(全体の29.1%) 1万人以上5万人未満

316自治体

(全体の17.6%)

5万人以上10万人未満

40自治体

(全体の2.2%)

10万人以上

17自治体

(全体の0.9%)

5割以上減少, 896自治体

(49.8%)

23. "Possibility of Disappearance" of Local Cities

Estimates of the number of communities whose "female population aged 20-39" will decline by more than 50% for local cities whose population outflows do not stop

1799

1276

1556

0

500

1000

1500

2000

Total number of

local governments

Cases w

here population outflow

s do not stop C

ases where population

outflows stop

The number of local governments as of 2040

Possibility of disappearance

of 523 local governments

Possibility of disappearance

of 243 local governments

Breakdown by population size for municipalities whose female population aged 20-39 will decline more than 50%

The number of municipalities from the aspect of changes in female population aged 20-39

(Remark) Created from the material document for the first “Committee for Japan’s Future” submitted by Mr. Masuda (committee member) (January 30, 2014).

(Note) 1. "Local governments with high possibility of disappearance" is defined as a community whose population will be less than 10,000 by 2040 among local governments whose "female population aged 20-39" will decline by 50% during the period between 2010 and 2040.

2. Created from “Regional Population Projection for Japan: 2010-2040 (March 2010)” and associated data by the IPSS. 3. Estimates for the cases where population outflows do not stop are calculated by multiplying the net migration rates by year, sex,

and age (for population aged under 85) by a certain adjustment coefficient according to positive and negative migration rates so that the net social increase (total of items with positive net migration rate) and the net social decrease (total of items with negative net migration rate) of population during the period from 2010 to 2015 hover at almost the same level afterwards.

4. For the figures above, a ward is considered to be one municipality regarding 12 designated cities. In addition, municipalities in Fukushima prefecture are not included. 23

For the local cities whose population outflow to large metropolitan area (especially Tokyo) does not stop, there is a deep concern that 523 out of 1,800 local governments have the "possibility of disappearance" in 2040. Even for local cities whose population outflows stop, 243 local governments still will suffer from the "possibility of disappearance".

same, increase, 15 local governments (0.8%)

Decrease by 50% or more,

896 municipalities (49.8%)

Decrease by 30% or more/less than 50%,

619 municipalities (34.4%)

Decrease by less than 30%,

269 municipalities

(15.0%) Less than

10,000 people, 523 municipalities

(29.1%) 10,000 people or more and

less than 50,000 people,

316 municipalities

(17.6%)

100,000 people or more,

17 municipalities (0.9% of the total)

50,000 people or more and less than 100,000

40 municipalities (2.2% of the total)

24. Population Concentration in Urban Areas in the World

Status of population concentration in urban areas in the world (2013)

Fortune Global 500 The number of main offices of

global businesses by city

Note 1: Source is Demographia: World Urban Areas & Population Projections (Wendell Cox) Note 2: "Urban area" is basically defined as an area with a population density of 400 people /km2 or more and lined with buildings. Note 3: Total population of each country is based on estimates for 2013 regarding medium fertility from "World Population Prospects: The 2010 Revision" by the U.N. Note 4: The Tokyo metropolitan area here means the area consists of Tokyo, Kanagawa, Chiba and Saitama prefectures, and some urbanized areas in Gunma, Tochigi and Ibaraki prefectures.

The population of the Tokyo metropolitan area is 30 million or more, accounting for nearly 30% of the total population in Japan. Also, 70% of main offices of global businesses are located in the area.

Such a high concentration of domestic population and functions is remarkable except in Korea.

(Source) Fortune Global 500 (2013)

Fortune Global 500 lists global businesses of top ranking up to 500th in terms of sales value.Share means the percentage of global businesses listed in Fortune Global 500 whose main offices are located in the above cities in the total number of such businesses in each country.

Ranking City of main office

No. of businesses Share

1 Beijing 48 53.9% 2 Tokyo 45 72.6% 3 Paris 19 61.3%

4 New York 18 13.6%

5 London 17 63.0% 6 Seoul 12 85.7% 7 Osaka 8 12.9% 7 Shanghai 8 9.0%

3,724

2,675

2,287 2,330 2,283 2,177 2,124 2,067 2,057 2,003

1,579 1,507

1,087 958 731

29.29%

10.70%

46.42%

1.86% 1.65%

22.12%

11.66%

6.46%

10.27%

16.38%

11.05%

18.37% 16.91%

15.17%

8.84%

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

30.00%

35.00%

40.00%

45.00%

50.00%

0

500

1000

1500

2000

2500

3000

3500

4000

都市

圏の人

口(万

人)

総人

口に占めるシェア

(%)

都市的地域の人口(万人)

その都市的地域の存する国の総人

口に占めるシェア

24

Population in urban areas (10,000 people) Percentage in the total population of the country where the urban area is located

Pop

ulat

ion

in u

rban

are

as (1

0,00

0 pe

ople

)

Per

cent

age

in th

e to

tal p

opul

atio

n (%

)

Toky

o m

etro

polit

an

area

(Not

e 4)

Jaka

rta

Seo

ul -

Inch

on

Del

hi

Sha

ngha

i

Man

ila

Kar

achi

New

Yor

k

Sao

Pau

lo

Mex

ico

city

Mos

cow

Cai

ro

Par

is

Lond

on

Ess

en -

Dus

seld

orf

73.9

30.9

-35.0 -55.0 -56.0

-44.9 -100

-50

0

50

100

150

200

農業、林業

建設業

製造業

情報通信業

運輸業、郵便業

卸売業、小売業

金融業、保険業

不動産業、物品賃貸業

学術研究、専門・技術サービス業

宿泊業、飲食サービス業

生活関連サービス業、娯楽業

教育、学習支援業

医療・福祉

東京圏 三大都市圏 その他の地域

(万人)

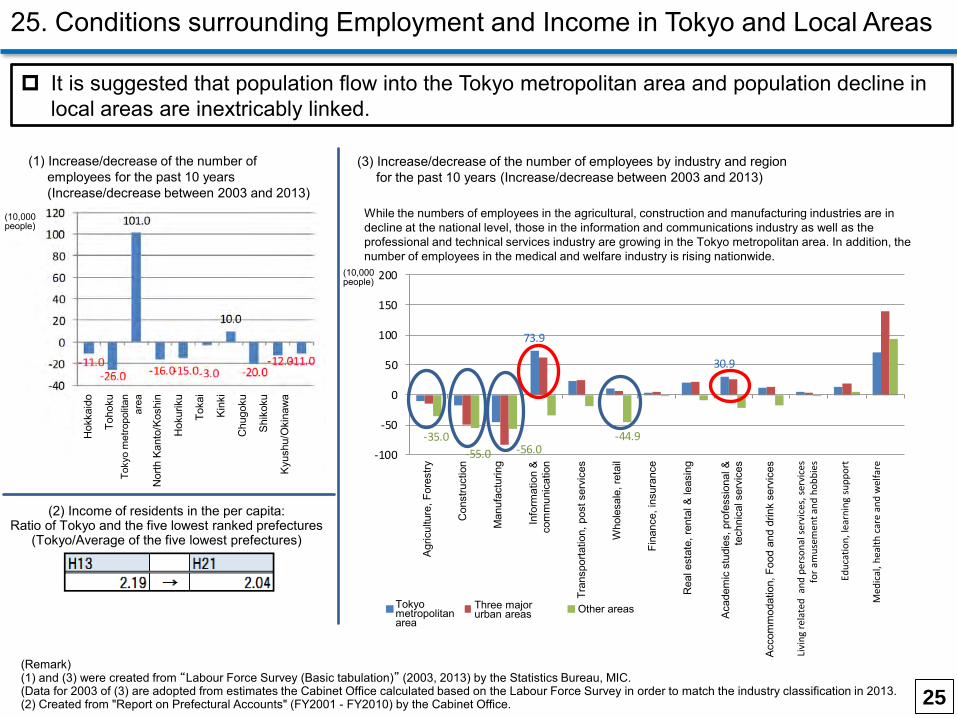

25. Conditions surrounding Employment and Income in Tokyo and Local Areas

It is suggested that population flow into the Tokyo metropolitan area and population decline in local areas are inextricably linked.

(2) Income of residents in the per capita: Ratio of Tokyo and the five lowest ranked prefectures

(Tokyo/Average of the five lowest prefectures)

(1) Increase/decrease of the number of employees for the past 10 years (Increase/decrease between 2003 and 2013)

(Remark) (1) and (3) were created from “Labour Force Survey (Basic tabulation)” (2003, 2013) by the Statistics Bureau, MIC. (Data for 2003 of (3) are adopted from estimates the Cabinet Office calculated based on the Labour Force Survey in order to match the industry classification in 2013. (2) Created from "Report on Prefectural Accounts" (FY2001 - FY2010) by the Cabinet Office.

(3) Increase/decrease of the number of employees by industry and region for the past 10 years (Increase/decrease between 2003 and 2013)

While the numbers of employees in the agricultural, construction and manufacturing industries are in decline at the national level, those in the information and communications industry as well as the professional and technical services industry are growing in the Tokyo metropolitan area. In addition, the number of employees in the medical and welfare industry is rising nationwide.

25

(10,000 people)

(10,000 people)

Tokyo metropolitan area

Three major urban areas Other areas

Hok

kaid

o

Toho

ku

Toky

o m

etro

polit

an

area

Nor

th K

anto

/Kos

hin

Hok

urik

u

Toka

i

Kin

ki

Chu

goku

Shi

koku

Kyu

shu/

Oki

naw

a

Agr

icul

ture

, For

estry

Con

stru

ctio

n

Man

ufac

turin

g

Info

rmat

ion

&

com

mun

icat

ion

Tran

spor

tatio

n, p

ost s

ervi

ces

Who

lesa

le, r

etai

l

Fina

nce,

insu

ranc

e

Rea

l est

ate,

rent

al &

leas

ing

Aca

dem

ic s

tudi

es, p

rofe

ssio

nal &

te

chni

cal s

ervi

ces

Acc

omm

odat

ion,

Foo

d an

d dr

ink

serv

ices

Liv

ing

rela

ted

and

per

sona

l ser

vice

s, se

rvic

es

for a

mus

emen

t and

hob

bies

Educ

atio

n, le

arni

ng s

uppo

rt

Med

ical

, hea

lth c

are

and

wel

fare

(Remark) Created based on "Annual report on the internal migration in Japan derived from the basic resident registers" by the Statistics Bureau, MIC.

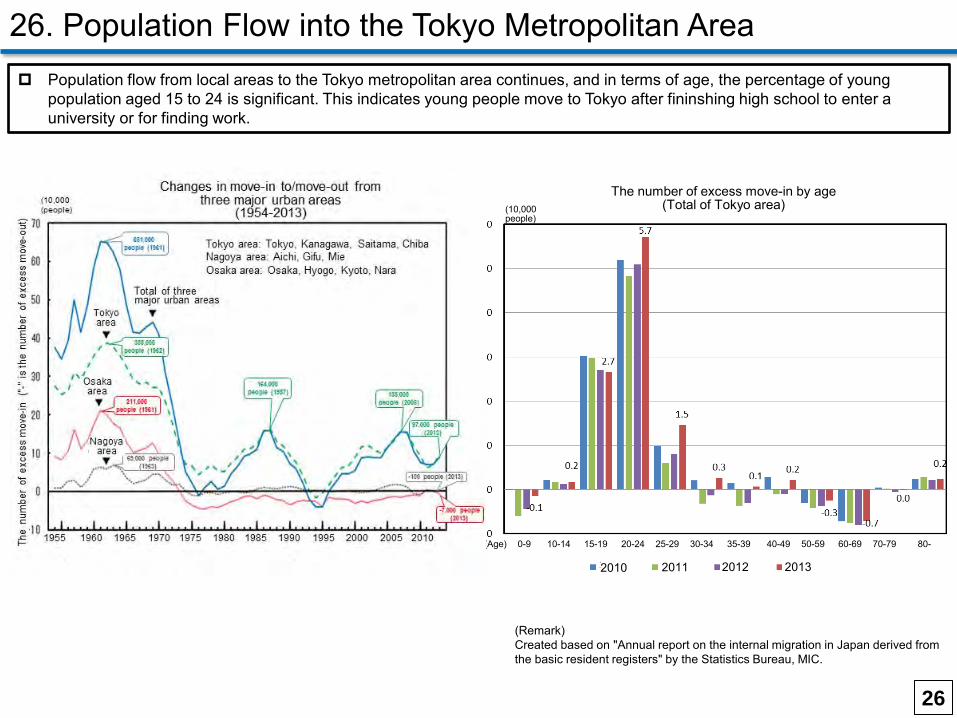

26. Population Flow into the Tokyo Metropolitan Area Population flow from local areas to the Tokyo metropolitan area continues, and in terms of age, the percentage of young

population aged 15 to 24 is significant. This indicates young people move to Tokyo after fininshing high school to enter a university or for finding work.

26

(10,000 people)

(Age) 0-9 10-14 15-19 20-24 25-29 30-34 35-39 40-49 50-59 60-69 70-79 80-

2010 2011 2012 2013

The number of excess move-in by age (Total of Tokyo area)

27. Map of Current Situation of Population Concentration in Tokyo (Concept Illustration)

Concentration of industries and

population

[High-growth period]

Tokyo metropolitan

area

Local areas

Structure of population outflow

Information dissemination abilities centralized in Tokyo Extensive authority of administration

Good transportation network Advanced culture and interactive functions

Head office functions remaining in the Tokyo metropolitan area Concentration of international

operations and financial functions

Strong yen Increased competition from

Asian countries

Improvement of logistical efficiency by developing domestic transportation network

Improvement of communication functions

Overseas transfer and closure of plants

Decline of employment in local areas

Young people move to the Tokyo metropolitan area after finishing high School

to enter a university or for finding work

Relative gaps in income, etc. compared to local areas

Population concentration in the Tokyo metropolitan

area

Accumulation of human capital

High productivity

Depressed economic and social activities in local areas

Population decline in local areas

Initially, large-scale flow of population to three major city areas

Distribution of functions of plants, etc. lowers population decline with income gap

Normalization of outflow of population (esp. young people) from local areas Fixing of income disparity

Spiral in which a population outflow causes further economic disparities and population outflows

Spiral of Concentra-

tion

Spiral of Outflow

Decentralization of plants, etc.

Infrastructure development

Decline of branch functions

[Issues]

Enhancement of global

competitive-ness

Vitalization of industries supporting local areas

Control of outflow of

population, especially for young people

[Stable growth period] Around 1973 - 1975

27

• January 20: First Council on Fiscal and Economic

Policy (CEFP) meeting - Set up the "Future of Choices" committee

• January 30: First committee meeting - Agenda of the committee

• February 14: Second committee meeting - Items to be considered at the committee - Potential growth rate, people's feeling of well-being

and income, demographic movement

• February 24: Third committee meeting - Future to be aimed at - Economic growth and development, issue of declining birthrate

• March 12: Fourth committee meeting

- Prospects of the regions

• April 7: Fifth committee meeting - Human resources

• April 21: Sixth committee meeting

- Discussions considering reports from chiefs of working groups

- Interim draft summarizing points

• May 13: Seventh committee meeting - Reports from working groups - Interim summarization

Chairperson

Akio Mimura: Senior Advisor, Honorary Chairman at Nippon Steel and Sumitomo Metal Corporation

19th Chairman of the Japan Chamber of Commerce and Industry

Acting chairperson Kazumasa Iwata: President at the Japan Center for Economic

Research Former deputy governor at the Bank of Japan

Fujiyo Ishiguro: President & CEO of Netyear Group Corporation

Yuriko Kato: President, M2 Labo Co., Ltd.

Sawako Shirahase: Professor at the University of Tokyo, Graduate School of Humanities and Sociology

Tomotaka Takahashi: CEO of ROBO GARAGE Co., Ltd.

Masataka Fukao: Associate Professor at Ryukoku University, Faculty of Policy Science

President of the Kyoto Foundation for Positive Social Change

Hiroya Masuda: Visiting Professor at the University of Tokyo, Graduate School of Public Policy Former governor of Iwate Prefecture

Hiroshi Yoshikawa: Professor at the University of Tokyo, Graduate School of Economics

28. Meeting Record of “Committee for Japan’s Future” Meeting record List of committee members

28